acce e ol -...

TRANSCRIPT

ACCESS THE WORLD

Inside this issue . . .

ISSUE 36 | Spring 2017

Contact MAP at:16000 Christensen Road, Ste 200Tukwila, Washington 98188

Phone: 1.866.598.0698Fax: 206.439.0045Email: [email protected]

www.mapacific.com See “MAP’s Annual Conference” on page 2

— uConference17

— Loyalty Insights

P.2

P.5

P.8

P.6

— OCCU is “Best in Class”

— ATM fraud skyrocketsP.4

— Tackling EMV at Waterfront FCU

P.11

Disruption was the order of the day for 2016 in the payments industry. 2017 is looking to be just as exciting. New regula-tion, improved support for non-bank play-ers and increased collaboration are all set to further shake up the status quo. Based on feedback from clients that want see more action-based activities at our conference, MAP worked with the Center for Financial Service Innovation (CFSI) to develop the FinX workshop to help our clients respond to this new environment and build products that meet their members’ changing needs.

The FinX workshop is a different way to learn how hardworking, everyday people

— The Fed reports fraud rises

— Visa News

make financial decisions. In partnership with MAP, CFSI has built an action-based exercise to shed light on what it feels like to manage finances with a small cushion of cash in a world of unpredictable events. Today, as many as 66 million Americans have zero dollars saved for an emergency. That’s roughly a quarter of U.S. adults who are ill-prepared for an unplanned expense, according to Bankrate.com. Building payment products and other financial solutions requires understanding current market forces influencing the tools member are using.

During the workshop, participants will be ran-domly assigned in groups and given a household

— Letter from the CEO

— Costco switch to Visa

— Industry News

P.3

MAP’s uConference17 to feature CFSI’s FinX Workshop

P.7

— A.I. impacts payments industry

2

ACCESS THE WORLD

Optimization enables issuers to proactively and effectively communicate relevant messaging with their cardholders in a timely fashion.

MAP is pleased to welcome back Michael Marx, Visa’s Vice President of Research Services. As an intelligence consultant and liaison with card issuers, Michael shares market research, competitive intelligence and consumer trends data with financial institutions issuing Visa-branded cards focusing on consumer and payments trends for both macro-based and key market segments.

MAP hosts this small conference each year for credit unions where we bring together industry experts to meet in a relaxed setting for learning and exploring what is happening in the payments industry and how it will impact our members. As an intimate event for select participants, space is limited.

MAP’s 2017 Annual Conference will be held August 24 and 25 at Alderbrook Resort in Union, Wash. is about 45 minutes north of Olympia and 90 minutes from SeaTac. Surrounded by the Olympic Mountains, the Resort & Spa rests on the shores of the Hood Canal, a glacier-carved fjord home to eagles and osprey, salmon and seals. To register, go to uconference17com. For more information, please contact your Client Services Manager or Karl Kaluza at 866-598-0698 x1618 or [email protected].

persona from the U.S. Financial Diaries. Each group begins with known assets and liabilities. Depending on the persona assigned, groups will earn income in vari-ous amounts and intervals. They will also incur fixed and once-off expenses. The group must then make decisions on how to deploy their available cash — mak-ing tradeoffs between which bills are most critical and must be paid now, how much to stash away for the future, and how to manage unexpected life-events. The FinX workshop will be the primary focus of Thursday’s uConfrence17 on August 24.

On Friday, August 25, the second day of the conference will feature payment industry experts with a focus on Leadership and Card Program Management. MAP’s keynote speaker is Don Schmincke, famed lecturer and anthropologist from Johns Hopkins University, offers the most provocative and sensational view of business of all other speakers today. An author of “The Code of the Executive” and “High Altitude Leadership,” Don’s irreverent humor and unconventional methods provide audiences such a refreshing change to other status-quo topics that he’s been called the world’s “management renegade.” His patent-pending offerings transcend typical programs via refreshing alternatives to trendy theories, unproven methods, and phony “experts.”

Joining Dr. Schmincke on Friday morning is John Best, a thought leader and “outside the box” innovator, recognized throughout the FinTech arena, with a particular affinity for credit unions. John is the founder and CEO of the financial technology firm Best Innovation Group (BIG), which focuses on industry-wide code sharing and API prototype development. He speaks regularly at industry events, hosts a weekly FinTech podcast and facilitates a highly interactive financial technology forum. Prior to going BIG, John spent over a decade at Wescom Credit Union and Wescom Resources Group, serving as Chief Technology Officer and Senior Vice President.

Guest presenter Gina Pask, Visa’s Product Director of Portfolio Optimization, will review the the card network’s innovative offering dubbed the cardholder relationship management tool.

Don Schmincke

uConference17ALDERBROOK RESORT

Union, WA

MAP’s Annual ConferenceContinued from page 1

Portfolio Optimization’s breadth of capabilities goes well beyond marketing, supporting all kinds of contextual cardholder communication simply and effectively, without requiring extra time and resources. With rules-based campaigns, Portfolio

John Best

Michael Marx

3

ISSUE 36 | Spring 2017

As the EMV liability shift deadline loomed in 2015, financial institutions across the country scrambled to determine how best to handle the change.

The transition wouldn’t be easy: Every consumer credit and debit card needed to be replaced with a chip-enabled card. That in itself would be a challenge. But often, institutions discovered they had to find a new plastics vendor just to get those new cards made. Plus, many credit unions and banks needed to update or replace some of the systems they had been using in-house for years.

Waterfront Credit Union’s situation was no different when it came to the tasks that needed to be completed. But this institution had one resource that would help the entire process go smoothly and get completed quickly. That resource was a long-standing relationship with Member Access Pacific.

Teaming up with the right peopleMAP, a card processing company that specifically focuses on credit unions, has been working with Waterfront for more than a decade. In that time, the two organizations have gotten to understand each other very well.

MAP knows that Waterfront is a small credit union that works extremely hard to help its members realize their financial goals. MAP also knows that Waterfront’s members count on the credit union for personalized advice for their finances. Since being founded in 1964, Waterfront has catered its services to a select group of people: employees of specific unionized industries, mostly in the maritime sector.

Waterfront knows that MAP is dedicated to its partners, able to take on enormous

have the PIN keys it needed to complete the change. Obstacles like this can easily make an already-extensive project timeline even longer.

“The project takes at least nine months if there are no issues,” Schmidt said. “It’s time intensive. MAP is a significant help throughout the project.”

MAP’s immense helpfulness didn’t come as a surprise to the people at Waterfront.

“MAP always provides excellent service,” Schmidt explained. “They have great department leads and will work on an issue until satisfactorily resolved.”

Today, Waterfront’s member base of more than 5,500 are pleased with the advancements their credit union made. They’re particularly fond of the new card designs Waterfront created for the EMV project, Schmidt noted.

But they’re also grateful that their credit union took the right steps to ensure every member’s finances were safe, secure and handled by an institution that’s up to date on the latest industry standards - a distinction that MAP helped Waterfront achieve.

Tackling EMV at Waterfront FCU

projects like converting to EMV, and will go the extra mile to make sure the transition goes smoothly. And that’s exactly what Waterfront experienced when it turned to MAP for help with its conversion.

Like many financial institutions, Waterfront needed to find and coordinate with a new card producer. Plus, it needed to change some of its Visa DPS programming. These are large tasks to take on, and can become incredibly complicated for a credit union trying to go it alone. Luckily, MAP’s team is knowledgeable on everything that needs to get done.

“MAP led the project and held weekly meetings,” recalled Waterfront President and CEO Rebecca Schmidt. “[The project leader] Mike did a fantastic job keeping everyone on track and solving issues when they arose.”

Overcoming obstacles with MAPThe switch to EMV usually uncovers additional challenges that a financial institution needs to address. Waterfront, for instance, didn’t

4

ACCESS THE WORLD

ATMs are driving skyrocketing debit fraud

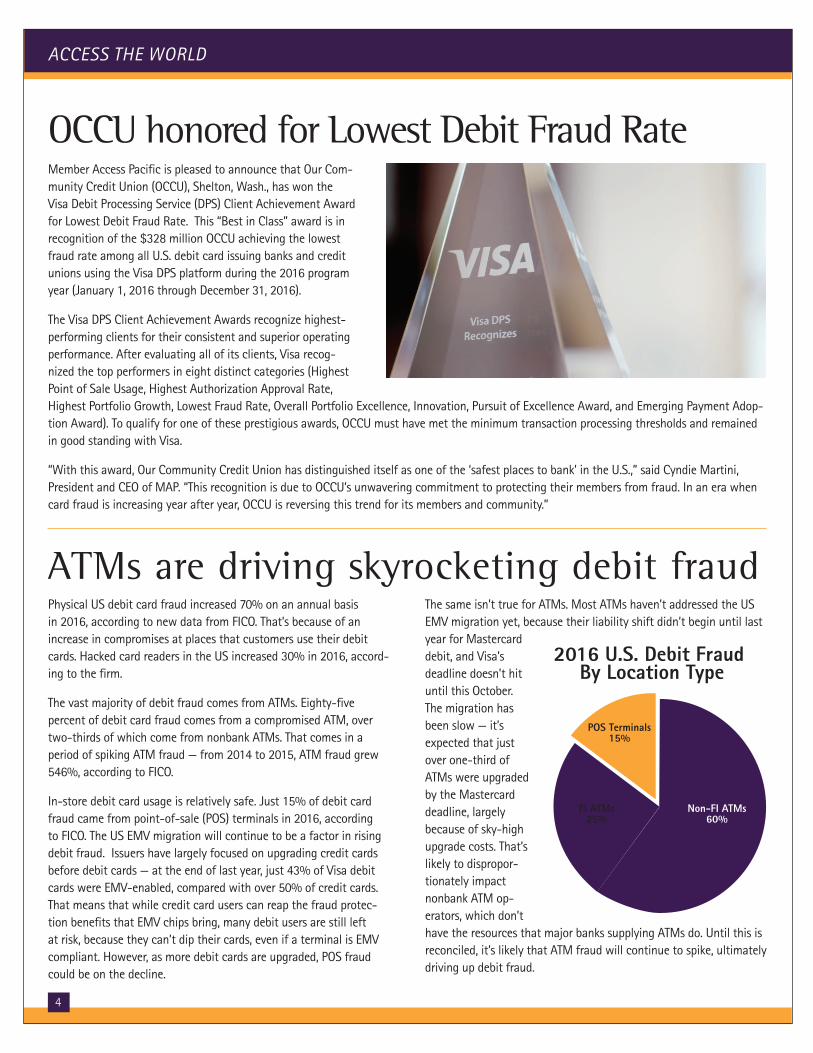

Member Access Pacific is pleased to announce that Our Com-munity Credit Union (OCCU), Shelton, Wash., has won the Visa Debit Processing Service (DPS) Client Achievement Award for Lowest Debit Fraud Rate. This “Best in Class” award is in recognition of the $328 million OCCU achieving the lowest fraud rate among all U.S. debit card issuing banks and credit unions using the Visa DPS platform during the 2016 program year (January 1, 2016 through December 31, 2016).

The Visa DPS Client Achievement Awards recognize highest-performing clients for their consistent and superior operating performance. After evaluating all of its clients, Visa recog-nized the top performers in eight distinct categories (Highest Point of Sale Usage, Highest Authorization Approval Rate, Highest Portfolio Growth, Lowest Fraud Rate, Overall Portfolio Excellence, Innovation, Pursuit of Excellence Award, and Emerging Payment Adop-tion Award). To qualify for one of these prestigious awards, OCCU must have met the minimum transaction processing thresholds and remained in good standing with Visa.

“With this award, Our Community Credit Union has distinguished itself as one of the ‘safest places to bank’ in the U.S.,” said Cyndie Martini, President and CEO of MAP. “This recognition is due to OCCU’s unwavering commitment to protecting their members from fraud. In an era when card fraud is increasing year after year, OCCU is reversing this trend for its members and community.”

OCCU honored for Lowest Debit Fraud Rate

Physical US debit card fraud increased 70% on an annual basis in 2016, according to new data from FICO. That’s because of an increase in compromises at places that customers use their debit cards. Hacked card readers in the US increased 30% in 2016, accord-ing to the firm.

The vast majority of debit fraud comes from ATMs. Eighty-five percent of debit card fraud comes from a compromised ATM, over two-thirds of which come from nonbank ATMs. That comes in a period of spiking ATM fraud — from 2014 to 2015, ATM fraud grew 546%, according to FICO.

In-store debit card usage is relatively safe. Just 15% of debit card fraud came from point-of-sale (POS) terminals in 2016, according to FICO. The US EMV migration will continue to be a factor in rising debit fraud. Issuers have largely focused on upgrading credit cards before debit cards — at the end of last year, just 43% of Visa debit cards were EMV-enabled, compared with over 50% of credit cards. That means that while credit card users can reap the fraud protec-tion benefits that EMV chips bring, many debit users are still left at risk, because they can’t dip their cards, even if a terminal is EMV compliant. However, as more debit cards are upgraded, POS fraud could be on the decline.

The same isn’t true for ATMs. Most ATMs haven’t addressed the US EMV migration yet, because their liability shift didn’t begin until last year for Mastercard debit, and Visa’s deadline doesn’t hit until this October. The migration has been slow — it’s expected that just over one-third of ATMs were upgraded by the Mastercard deadline, largely because of sky-high upgrade costs. That’s likely to dispropor-tionately impact nonbank ATM op-erators, which don’t have the resources that major banks supplying ATMs do. Until this is reconciled, it’s likely that ATM fraud will continue to spike, ultimately driving up debit fraud.

POS Terminals 15%

FI ATMs 25%

Non-FI ATMs 60%

2016 U.S. Debit Fraud By Location Type

5

ISSUE 36 | Spring 2017

Visa News

5

Continued on page 9

Visa wants you to pay with your sunglasses. In an effort to prove that it is at the forefront of innovation in the payments game, Visa has announced it will be launching its new NFC sunglasses. Users will be able to pay for their purchases by taking the sunglasses off and taping them on the card process-ing reader. The sunglasses will be embedded with a tiny chip on the side. According to Visa: “It ties back to our tag-line of everywhere you want to be. Without it it’s hard for us to fulfil our tagline. Our view is we take form factors that you don’t expect to be payment-enabled like sunglasses or maybe like a ring and expose to the market that maybe it can be.”

Visa and Mastercard expand availability of QR pay-ments. Both Visa and Mastercard announced the expanded availability of their QR-code-based payments systems. mVisa, a QR code-base new mobile-payment service that is intended to accelerate digital commerce, expects to be available in seven new countries, including Egypt, Ghana, and Indonesia, after already launching in India, Rwanda, and Kenya. Masterpass QR is now live in seven African and Asian countries, including Kenya, Nigeria, and Pakistan. As smartphone penetration continues to increase globally, it will become easier to access financial services, which could drive up adoption of financial mobile offerings.

Visa and Mastercard ink a tokenization deal. Visa and Mastercard announced a tokenization agreement associated with Visa Checkout and Masterpass. The agreement will allow each company to provision the other’s tokens into its wallet, essentially making the two products interoperable. Visa and Mastercard expect to launch the cross-provisioning in the second half of 2017 in the US, with a global launch to follow.

Visa and IBM partner for Internet of Things deal: A new partnership between Visa and IBM Watson will give the firm’s Big

The Federal Reserve Board of Governors isn’t rushing to reduce its caps on debit interchange after its latest report on debit transactions found that issuers’ debit card processing costs went down in 2015. In the biennial report released Nov. 30, the Fed also found that fraud losses increased dramatically industry-wide. Typical of previous years, issuers’ costs of authorizing, clearing and settling (ACS) debit card transactions, excluding issuer fraud losses, varied by issuer in 2015, according to the Fed. Issuers with the highest debit card transaction volume generally had the lowest ACS costs per transaction. Industry-wide, the overall average ACS cost per transaction was 4.2 cents per transaction in 2015, a decrease from 4.6 cents per transaction in 2013. The Fed’s report includes surveys of all 14 payment networks that process debit card transactions, and 129 issuers.

Overall, payments networks processed 60.6 billion debit and general-use prepaid card transactions valued at $2.31 trillion in the U.S. last year, compared with 53.7 billion transactions valued at $2.07 trillion in 2013. Total transaction volume grew 6.8 percent from 2014 to 2015, similar to the average annual growth over the previous three years, according to the report.

Interchange fees across all debit cards in 2015 totaled $18.41 billion, compared with $16.33 billion two years ago. The average interchange fee per covered transaction was 23 cents in 2015 “and has not changed materially since Regulation II took effect Oct. 1, 2011,” the report noted. The average network fee per transaction was $0.102 in 2015, marking negligible change from 2013. Network fees totaled $6.16 billion in 2015.

Industry-wide debit card fraud losses totaled approximately $2.41 billion in 2015, a 44 percent increase compared with 2013’s estimate. “The estimated increase in total fraud losses is driven by two factors: a 28 percent increase in average fraud losses as a share of transaction value and a 12 percent increase in the value of total transactions from 2013 to 2015,” according to the report.

The Federal Reserve reports that debit transaction costs decrease, but fraud rises

6

ACCESS THE WORLDACCESS THE WORLD

Loyalty Insight: Are cash rewards king?New reports on the growing appeal of cash-back rewards from the Wall Street Journal and Nielsen serves as a catalyst to examine the pros and cons of cash back rewards.

The Wall Street Journal article highlights the growing arms race among U.S. credit card issuers in which cards offer increasingly rich cash-back rewards: up to 10 percent in some cases. American Express, which is leading the pack in lucrative cash-back offers in spite of its investment in the points-based Membership Rewards program, is offering promotional rates of 10 percent on Amazon.com purchases and 6 percent on grocery purchases. Top U.S .issuers such as Capital One, Chase, and Citi are also offering lucrative rewards.

Recently, USAA started beta-testing offers of cash rewards for basic retail banking transactions such as maintaining a checking account balance, using a debit card, or transfering money into a savings account. All of this cash flowing from reward cards has seen some cardholders earn $1,000 or more annually through careful gamesmanship of their cash-back cards.

The Journal highlights a recent Creditcards.com survey in which nearly 75 percent of consumers surveyed prefer cash rewards to other loyalty rewards - just 16 percent prefer airline miles. Does this trend toward cash rewards mean that points-based reward programs are no longer worth the expense incurred by brands to operate them or the time consumers spend navigating them?

The recent Nielsen Global Retail Loyalty Sentiment Survey, a poll of 30,000 online consumers in 63 countries, likewise reveals that discounts and cash are king when it comes to global reward preferences. “When it comes to the most-valued loyalty-program benefits, monetary incen-tives top the list in every region, by a wide margin. More than half of global loyalty-program participants (51%) say product discounts are among the three most valued benefits, and discounts are particularly popular in Europe (62%). Fewer global program participants (45%) say rebates or cash back are among the most-valued benefits, but cash back is slightly more popular than discounts in North America (49% vs. 46%) and Latin America (48% vs. 47%).”

Consumers like cash-back rewards, which is why cash-back reward cards are proliferating. Program operators like cash-back rewards be-cause they’re easy to implement, incur no liability, and require minimal reward program infrastructure to deliver. If you’re considering cash-back

options in your own reward program, however, consider the following limitations:

1. Cash-back has limited emotional appeal. Again, customers who say they prefer cash-back rewards do not often attach emotional memories to the earning or spending of cash rewards.

2. Cash-back makes your funding rate transparent. Part of the reason cash-back rewards have grown so rich is that, absent the more opaque funding rate in currency-based programs, there’s no hiding the obvious benefit in a cash-back program. With no other cards to play, upping the ante by raising the percentage offered is an issuer’s only available option to increase program value.

3. Cash-back offers no perceived value stretch. The reason why points-based programs offer more elasticity is that you can build in perceived value in your rewards. For example, the incremental cost of delivering a reward flight to a frequent-flyer program member is far less than the perceived value of that free flight to the member. If you’re offering 5 percent cash back, on the other hand, then every $100 your cardholder spends earns them $5 back - no more and no less.

Even after weighing all the limitations to cash-back rewards, it can still be an effective value proposition - card issuers wouldn’t be doling out all of that cash if it wasn’t moving the needle. That said, there are important considerations to take into account when choosing a loyalty value proposition. Understanding the key differences between cash-back and currency-based programs, and how members respond to them, will ensure that you offer your members the right rewards to achieve the behavioral outcomes you desire.

7

ISSUE 36 | Spring 2017

7

Industry News

7

Continued on page 10

Costco still gaining from switch to Visa brand

Amazon accounts for 43% of U.S. online retail sales. An analysis by Slice Intelligence released this week found that 43% of all online retail sales in the US went through Amazon in 2016, as the e-commerce gi-ant’s market share continues to grow. According to the study, which analyzed more than 4 million online purchases, Amazon accounted for the majority (53%) of the growth in US e-commerce sales for the year. Slice said that Amazon’s growth in 2016 was driven by sales in the electronics, home, and apparel categories. Electronics contrib-uted to an estimated 18% of the company’s sales growth in 2016, as the number of US households that own an Amazon Echo device more than doubled from 2015.

Apple Pay expands acceptance. Thirty-five percent of US retailers, or 4 million locations, now support Apple Pay and acceptance is expected to nearly double, to two in three retailers, in 2017, according to Apple Insider. However, Apple Pay adoption in the US stagnated just below a quarter of eligible users, according to data from PYMNTS and InfoScout. And even among users that have adopted the wallet, it’s not very sticky, largely because users aren’t sure whether or not a given store will accept the transaction. Adding retail locations, which requires retailers to upgrade to newer, NFC-capable terminals, could help solve that problem because they give the wallet greater ubiquity.

LG Pay set to debut in South Korea. LG Pay is set to make its debut in June, but the new mobile payment system will only be available to consum-ers in South Korea, according to multiple media reports. An early version of the company’s technology will be featured on the LG G6 in certain

Costco’s decision to shift its business to Visa from Amex in June of last year is still having a “very positive” impact, according to Richard Galanti, the company’s CFO. As part of the move, the retailer trans-ferred its store card portfolio to Visa, launched a new product called the Citi Visa Anywhere card, and began accepting all Visa cards in its stores.

Costco estimates 85% of the 11.4 million Amex cards transferred for conversion have been activated as Citigroup Visa cards. In addition, over 1 million customers have signed up and been approved for a new card. Those customers are helping lift Costco in a few ways. • Out-of-store spend on these cards remains high. In the first

three-and-a-half weeks of the new card, 66% of sales on the new card occurred outside of Costco stores.

• That could be because it’s easier to spend out-of-store on these cards. Visa has a wider acceptance network than Amex — in 2014, Visa’s 9.5 million US merchants paled in comparison to Amex’s 6.9 million — which means that it’s easier for users to pay with these cards in more places and could encourage usage.

That benefits Costco in the long run. Galanti noted that the new card had an impact of 38 basis points on the firm’s overall perfor-mance in the quarter. Those totals are higher than the firm expected, and they were driven partly by that out-of-store spending. That’s because Costco has a revenue sharing agreement from Visa and Citi-group for purchases made outside of Costco, and that’s been “a little more” than the firm anticipated. If Costco can continue to capture massive out-of-store spend, the firm, as well as Citigroup, could be poised to continue to see gains from a major way as a result of the shift.

8

ACCESS THE WORLD

Whether t’s Facebook Messenger, Twitter’s Direct Messaging chat-bot, Apple’s Siri, Amazon’s Alexa, Google’s Allo, or WhatsApp, there’s no shortage of services that offer integrated bots that can handle everything from customer service, booking airline tickets or hotel rooms, and shopping online. Bots aren’t just limited to eCommerce apps or sites. The Fintech industry is also exploring the endless op-portunities that bots may present. For example, banks like Santander and Bank of America are planning on using bots to create one-to-one conversations, while others believe that bots will be used to onboard customers and aid them with important financial decisions.

Moreover, bots have the ability to also impact the payments industry by creating innovative systems and platforms. There are two kinds of chatbots: scripted bots and A.I. bots. A scripted chatbot doesn’t carry even a glimpse of A.I., whereas A.I. bots are built on Natural Lan-guage Processing (NLP) and Machine Learning (ML) and are based on the human capability of learning and absorbing information, but imbued with more efficiency.

Unlike the minimal A.I. interface, chatbots are capable of processing 1,000 times faster than humans. Chatbots are also more convenient since “an interface just presents options,” while A.I. chatbots allow you to type in your own answer. In other words, A.I. chatbots present many more possibilities.

By harnessing the power of A.I. software to process language from interactions with people in chat programs, messaging apps, and virtual assistants, the payments industry will be able to use A.I. bots to take on a variety of tasks:

Make quick and painless peer-to-peer payments through integra-tions. The PayPal bot is an example of this since it integrates with Facebook Messenger, Siri, and Slack. This allows users to make direct p2p payments without leaving your preferred app or platform.

Streamline the payment process by making direct payments within Messenger. Since more than 800 million use Facebook Mes-senger each month, which is about 11% of the world’s population, it’s safe to say that Messenger is a big deal.

Facilitate P2P payments via text messaging. Outside of integra-tions through Messenger or Slack, chatbots could be used to pay other people, check mobile wallet balances, review the status of group payments, and remind others that they owe you money.

Create personalized customer experiences. A.I. bots are being used primarily to improve the customer experience by developing a per-sonalized journey. Bots could extend services like making financial decisions, reviewing purchases, learning more about cardholder benefits, and monitoring spending.

Set-up recurring payments through verbal commands. Let’s say that you just received a new credit card that you use for a subscrip-tion or to make recurring payments. In the past, you would have to manually enter the new card information.

Reduce costs. Where members are calling to make a payment or ask a question, the cost is estimated to be about $6 per call. Chatbots can replace those calls, which in turn will save your business money. In fact, T-Mobile was able to save “48 percent in customer care costs by shifting customers away from customer-hostile voice calls to messaging and bots.”

A.I. bots have the power to impact the payments industry by al-lowing users to initiate and review payments directly from their smartphones. Furthermore, bots could streamline the entire payment process from viewing a catalog to making a purchase to tracking the order. Most importantly, bots are an affordable and effective way to improve the members’ payment experience, allowing people to send and receive payments more quickly and conveniently than they ever have before.

How will A.I. (Artificial Intelligence) Bots will impact the payments industry?

9

ISSUE 36 | Spring 2017

99

Visa NewsContinued from page 5

The inventory of EMV cards is gathering dust in its warehouses, up by “double digits” according to Reuters. This is due to a slower-than-expected uptick in demand for EMV cards, as small and mid-size issuers have put off upgrading due to the higher price of the cards and the infrastructure that supports them. The problem for slow EMV adoption among issuers is that it could hurt industry stakehold-ers and cardholders alike.

Fraud rates will increase for non-EMV compliant issuers’ custom-ers. With the deadline for issuers to have rolled out EMV-compliant cards to their customers having come and gone, those financial institutions are now on the hook for fraudulent transactions at ATMs and the point of sale.

While the rollout meanders to the long tail of adoption, criminals will follow the path of least resistance – targeting ATMs, merchants, and consumers who haven’t upgraded to secure EMV technology. This phenomenon, along with a similarly motivated rise in online fraud, explains why the number of consumers experiencing identity fraud rose by 18% year-over-year to 15.4 million in 2016, according to a 2017 Javelin Strategy & Research report.

Looking ahead, reduced costs should give customer-centric issuers of any size enough reason to adopt the secure card technology. EMV-holdouts are making a bet that the cost of upgrading will outweigh expected fraud costs, but that leaves fraud-victimized customers spending their time to resolve fraud that banks can and should prevent – and potentially switching banks as a result.

Blue Watson IoT platform clients access to Visa payment services through the card network’s tokeni-zation offerings. The partnership, which reflects a wider trend of payments moving into the Internet of Things (IoT), could give Visa access to as many as 6,000 IoT client companies by allowing them to provision Visa tokenization into their devices, effectively turning those into point-of-sale (POS) terminals that allow users to pay on-the-go.

Visa enjoys robust growth. Visa plans to stick with the ap-proach that delivered exceptionally strong growth in Q4 2016. CEO Alfred Kelly noted that the firm doesn’t foresee making massive changes to its strategy, but will instead remain ready to adapt to industry-wide changes and focus on key areas for growth: Payment volume: In Q4, Visa payment volume hit $1.8 trillion, with $803 billion coming from the US and $998 billion internationally. That’s up 39% year-over-year (YoY) on a constant currency basis. Though gross volume is down slightly sequentially, when accounting for the loss of Visa Europe co-badge volume, which was no longer counted beginning in Q4, it marks a slight acceleration. The acquisition of Visa Europe will help grow the company by adding new markets, but its performance was not the main improvement factor. Transaction growth: Visa processed 40.8 million transactions in Q4, up 41% on a year-over-year basis. Of those, 65% were debit, and 35% credit, in-dicating the strength of Visa’s massive debit network. That indicates that, though users are spending more on credit than on debit, both in the US and abroad, debit cards are used more often.

Samsung Pay partners with Visa. Samsung announced a partnership with Visa that will inte-grate Samsung Pay with Visa Checkout, according to Finextra. As a result of the partnership, Samsung Pay custom-ers will be able to tap a co-branded Samsung Pay/Visa Checkout button at any merchant that offers Visa Checkout and authenticate their purchase using a fingerprint. Visa Checkout has improved completion rates by up to 86%, accord-ing to a ComScore study. Now, Samsung Pay will have access to that at scale: The service counts over 300,000 partner merchants representing $173 billion in addressable volume, which Samsung Pay will now be exposed to.

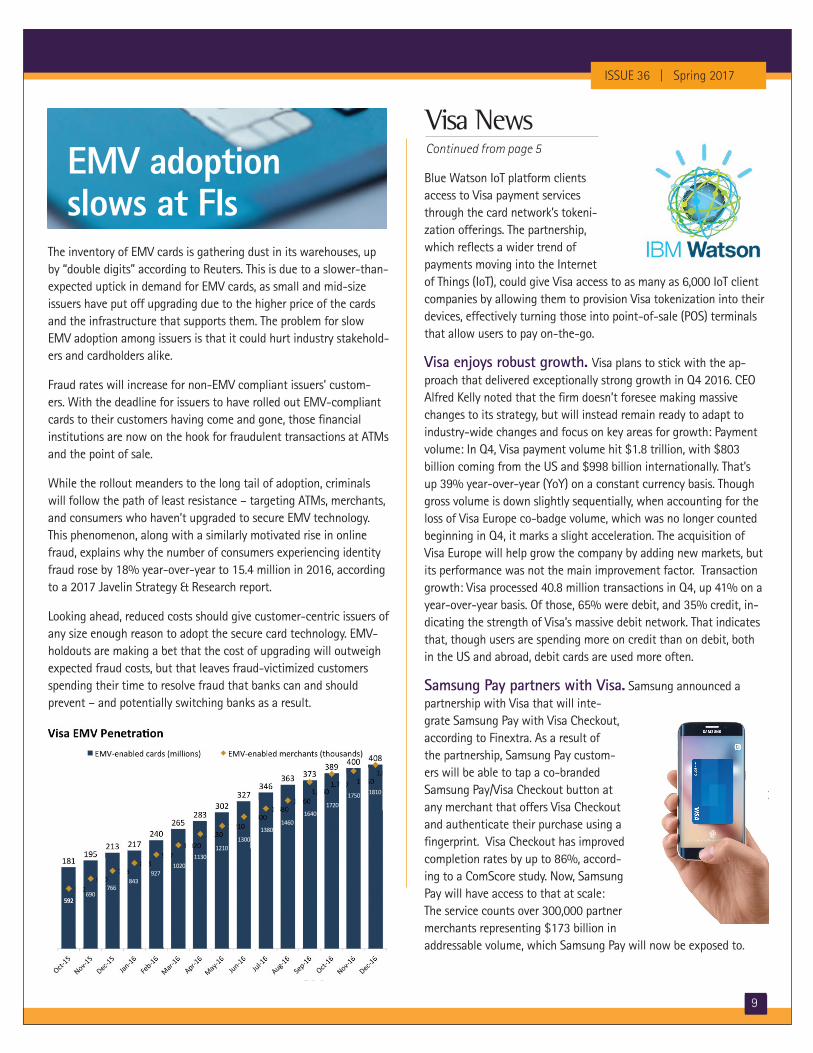

EMV adoption slows at FIs

592592690

766843

9271020

11301210

13001380

14601640

17201750 1810

10

ACCESS THE WORLD

Industry NewsContinued from page 7

It turns out Americans don’t know as much about cybersecurity as they probably should. Despite the increasingly connected digital world many people operate in today, new data from the Pew Research Center showed that many Americans are still in the dark when it comes to key cybersecurity topics. In fact, the majority of internet users were able to answer fewer than half of the questions correctly on Pew’s cybersecurity knowledge quiz, which covered a variety of issues and concerns.

“Cybersecurity is a complicated and diverse subject, but these questions cover many of the general concepts and basic building blocks that cybersecurity experts stress are important for users to protect themselves online,” Pew explained in its report.

The median number of questions answered correctly on the 13-question quiz was only five. Just 20 percent of 1,055 adult internet users who responded were able to answer more than eight questions correctly and only 1 percent were able to achieve a perfect score.

The two questions that the majority of respondents were able to get right involved identifying the strongest password from a list of four options and understanding that just because a public Wi-Fi network is password protected doesn’t mean it’s safe to use for online banking.

“Although the share of online adults who can correctly answer questions about cybersecurity issues varies from topic to topic, in most cases the share providing an actual incorrect answer is relatively small. Rather, many users indicate that they simply are not sure of the correct answer to a large number of the questions in this survey,” Pew researchers pointed out.

This uncertainty in cybersecurity topics may leave the door open for a big opportunity as hackers continue to get both smarter and more sophisticated.

markets with a more advanced version of the system to appear more widely next year.

Cash Still King for P2P, Even Among Millennials. A recent study from VocaLink polled more than 5,000 U.S. consum-ers ages 18 to 35 on their payments behavior and preferences. And while the survey found that cash has lost ground to cards for most types of payments, it’s stubbornly clinging to the No. 1 spot when it comes to P2P. Survey respondents cited cash as the most popular way of lending money to friends, with 53 percent saying they use cash for that purpose. Cash was the most popular method of sharing a bill and paying someone for work they’ve done, at 47 percent and 49 percent, respectively. Cash also ranked highly for tipping (58 percent), coming in just behind payment cards (61 percent).

Consumer Credit Card Debt Inches Toward $1 Tril-lion. According to Wallethub, consumers will end the year about $80 billion more in credit card debt than they began the year with. They say that brings us dangerously close to 2008’s all-time record of just under $1 trillion in credit card debt - bringing the average owed by each indebted household to just over $8,000. If that doesn’t sound bad enough - maybe this will: we now owe roughly the same amount we did - right before the Great Recession officially began in 2008. So wake up and smell the coffee - just don’t buy it. Especially if you can’t afford it. Because the last thing we all need right now is another recession.

Fuel Pump EMV Delayed. Mastercard and Visa recently an-nounced a 3 year delay in the EMV transition for Automated Fuel Dispens-ers (AFDs). In fairness, gas stations do tend to need more time for POS changes, given the nature of their card swipes and the physical changes needed. Gas station operators face a lot of construction and technol-ogy work. AFD conversion costs can easily run $10,000 per pump. So the question becomes whether the EMV delay will significantly increase transaction fraud losses.

Pew Study reveals how little Americans know about cybersecurity

11

Letter from the CEO

ISSUE 36 | Spring 2017

Cyndie MartiniPresident/CEO

Winds of change are blowing in Washington, D.C. The election of Donald J. Trump as president, combined with a Republican-controlled U.S. House and Senate has the potential to usher in widespread change, and much of it could affect the payments industry. While Congress is moving forward on a number of fronts, there’s some uncertainty around how fast and how far all of the president’s reforms will go. 2017 and beyond could be a good time for the payments industry, especially if it leads to regulatory relief.

Here are some of the biggest regulatory and legislative issues to watch in 2017. Rolling back the Dodd-Frank Act and its numerous regulatory tentacles is a priority. Since the law was signed following the 2008 financial crisis, Republicans have been quite vocal about their disdain for the legislation, which many say imposes too many rules and costs on financial services companies, and results in reduced and/or more expensive services for consumers.

Some of the biggest potential changes could be for the Consumer Financial Protection Bureau (CFPB) — in structure, leadership, funding, reach or all of the above. Some lawmakers are looking to overhaul the bureau’s leadership structure and budget oversight, including legislation that would eliminate Director Richard Cordray’s position, replacing it with a bipartisan, five-member commission charged with promoting consumer protections as well as competitive markets. The agency would also be subject to congressional oversight and appropriations. Currently, the CFPB is funded primarily from the Fed’s operating budget, with certain caps, and its budget is not subject to congressional approval.

Critically, many wonder if the roll back of Dodd-Frank will include the Durbin Amendment, and the debit interchange caps and network routing rules that were put in place by the Fed as a result. It’s widely rumored that former Rep. Randy Neuge-bauer (R-Texas) is the likely candidate to replace Cordray at the helm of the CFPB. He has been a strong opponent of the Durbin Amendment. including interchange caps, arguing that financial institutions reduced their free checking account offer-ings, increased account fees and instituted higher minimum balance requirements because of the regulations.

It’s clear the atmosphere is right for a plethora of possible changes coming out of Washington in 2017 and beyond, with many affecting the payments industry. Whether it’s the Dodd-Frank Act, the CFPB and its rulemaking, the battle over in-terchange or the Affordable Care Act, there’s a lot to watch. At MAP, we strive to make our clients more competitive by providing payments solutions that best serve their members. Our success comes from providing cost-effective, best-in-class solutions for our clients. For more information about how MAP can best serve you and your institution, feel free to call me, 1-866-598-0698, ext 1610 or email me at [email protected].

16000 Christensen Road, Ste 200Seattle, Washington 98188

Phone: 1.866.598.0698Fax: 206.439.0045

Email: [email protected]

PRSRT STDUS POSTAGE

PAIDSEATTLE, WA

PERMIT #1445