academies accounts and audit workshop - buzzacott & co · academies accounts and audit workshop...

TRANSCRIPT

Academies Accounts and Audit Workshop

Catherine Biscoe and Hugh Swainson

Agenda

Legal requirements and reporting framework

Financial statements

– Narrative reports

– Primary statements

– Notes to the accounts

Audit requirements and common issues

Reporting framework

Academies are exempt charities and companies limited by guarantee

Accounts comply with Charity, Company and DfE requirements

– Charity Statement of Recommended Practice - SORP 2005

– Companies Act 2006

– EFA Accounts Direction (‘Coketown Academy’ model accounts)

2 Accounts Directions 2014/15

– Implementation based on when the Academy incorporated

– 2005 SORP v 2015 SORP

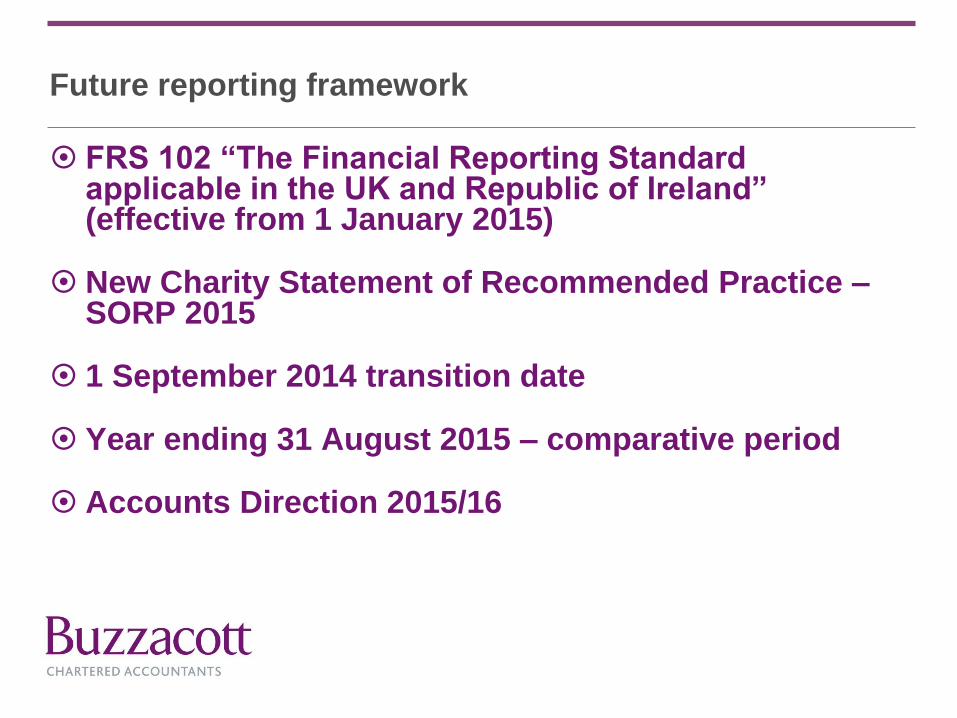

Future reporting framework

FRS 102 “The Financial Reporting Standard applicable in the UK and Republic of Ireland” (effective from 1 January 2015)

New Charity Statement of Recommended Practice – SORP 2015

1 September 2014 transition date

Year ending 31 August 2015 – comparative period

Accounts Direction 2015/16

Narrative statements

Reference and administrative details

Trustees’ report (incorporating a Strategic Report)

Governance statement

Statement on regularity, propriety and compliance

Statement of Trustees’ responsibilities

Independent Auditor’s report on the financial

statements

Independent Reporting Accountant’s report on

regularity

Statement of financial activities

Incoming resources

Resources expended

Transfers

Other gains and losses

Funds reconciliation

Restricted versus unrestricted - Restricted general & restricted fixed assets

Statement of financial activities - Income

Incoming resources from generated funds

Voluntary income includes:

– Private sponsorship

– Donated fixed assets

– Other donations

– Transfer of net assets from the Local Authority on conversion to Academy status

Statement of financial activities - Income

Incoming resources from generated funds

Activities for generating funds includes:

– Fundraising events such as jumble sales, fireworks displays and concerts

– Hire of facilities

– Catering income (per Coketown Academy)

Investment income includes:

– Incoming resources from investments assets, including dividends, interest and rents

– Where an academy has subsidiaries, all payments to the charity by its subsidiary

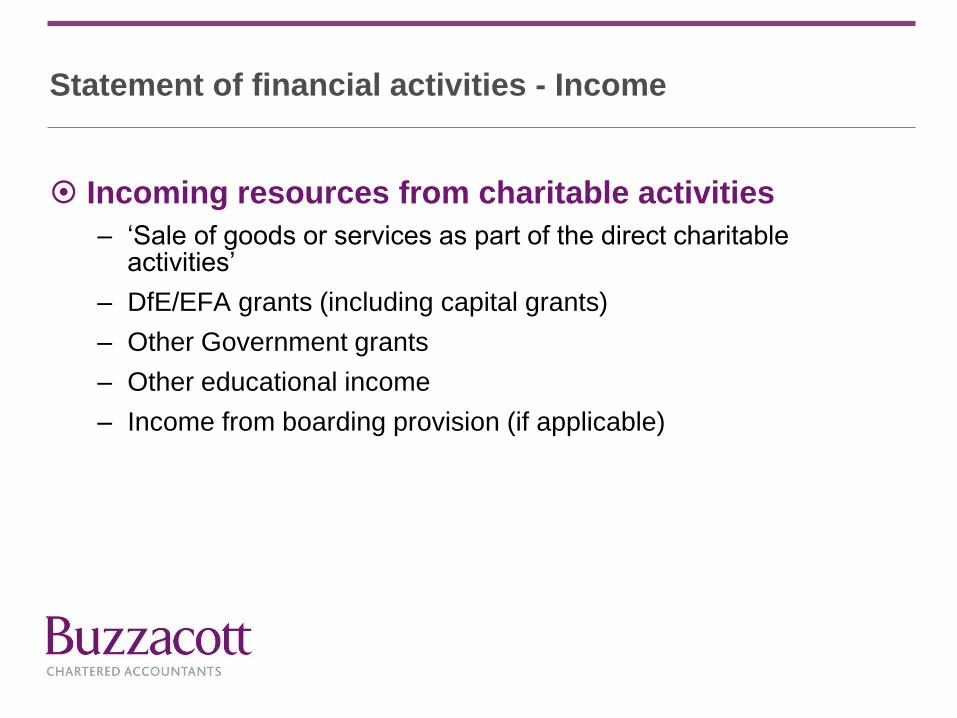

Statement of financial activities - Income

Incoming resources from charitable activities

– ‘Sale of goods or services as part of the direct charitable activities’

– DfE/EFA grants (including capital grants)

– Other Government grants

– Other educational income

– Income from boarding provision (if applicable)

Statement of financial activities - Expenditure

Cost of generating funds

– Costs of generating voluntary income

– Fundraising trading

– Costs of managing investments

– Any other costs of generating income

Statement of financial activities - Expenditure

Cost of charitable activities

– Should provide an understanding of the nature of the activities undertaken

– For most academies charitable activities are normally just totalled as one heading - “Academy trust’s educational operations”

– Also boarding provision costs, if applicable

– The notes should identify the breakdown of these costs between direct costs and support costs

Statement of financial activities - Expenditure

Governance costs

– Costs associated with the governance arrangements of the academy trust

– Relating to the general running of the academy as opposed to those costs associated with fundraising or educational activity

– Normally includes internal and external audit, legal advice for trustees and costs associated with constitutional and statutory requirements e.g. the cost of trustee meetings and preparing statutory accounts

– Included within this category are any costs associated with the strategic as opposed to day to day management of the academy's activities

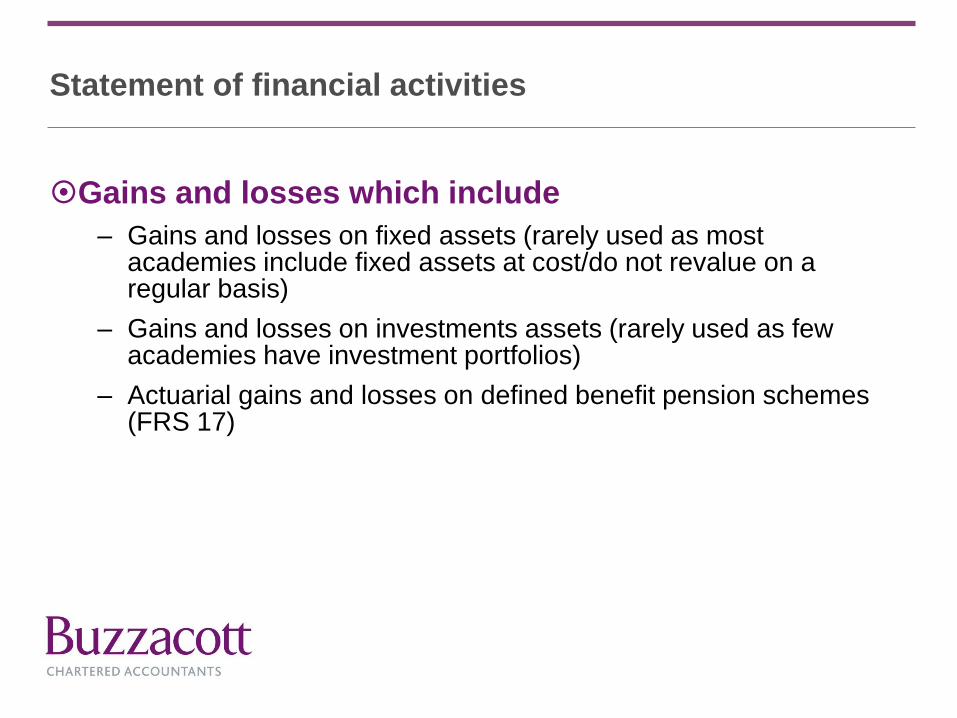

Statement of financial activities

Gains and losses which include

– Gains and losses on fixed assets (rarely used as most academies include fixed assets at cost/do not revalue on a regular basis)

– Gains and losses on investments assets (rarely used as few academies have investment portfolios)

– Actuarial gains and losses on defined benefit pension schemes (FRS 17)

Fund Accounting

Restricted

– General

– Fixed assets (capital)

Unrestricted

– Designated

– General

– ‘Free reserves’

Endowment

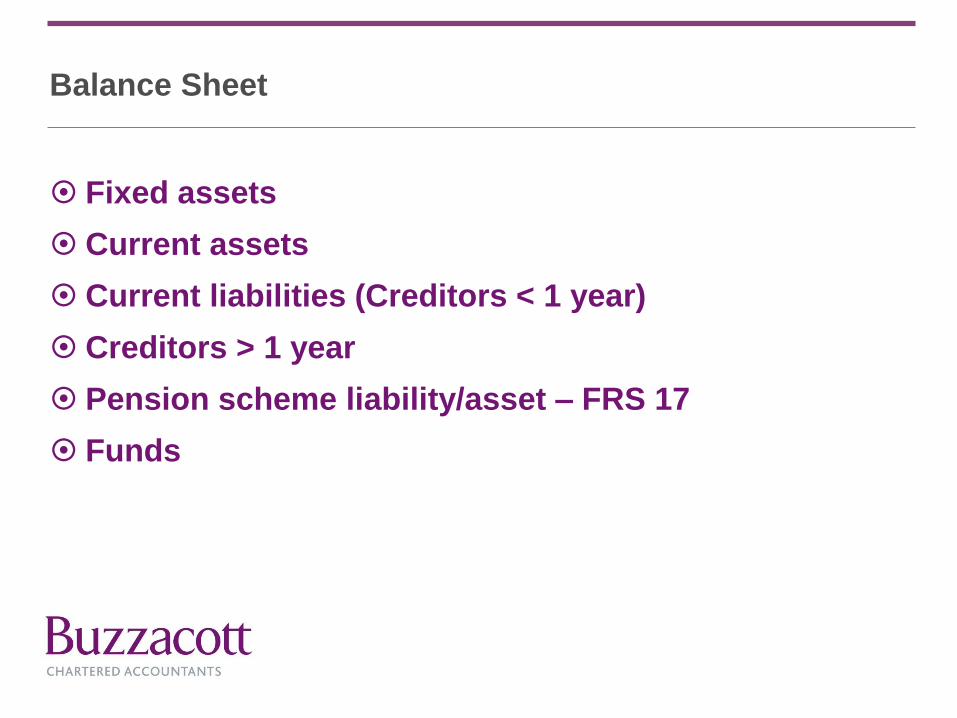

Balance Sheet

Fixed assets

Current assets

Current liabilities (Creditors < 1 year)

Creditors > 1 year

Pension scheme liability/asset – FRS 17

Funds

Balance Sheet

Fixed assets

– Tangible fixed assets

• Land and buildings – freehold & leasehold

• Furniture and equipment

• Computer equipment

• Motor vehicles

– Investments

• Held for long term financial return

• Investments in subsidiaries

Balance Sheet

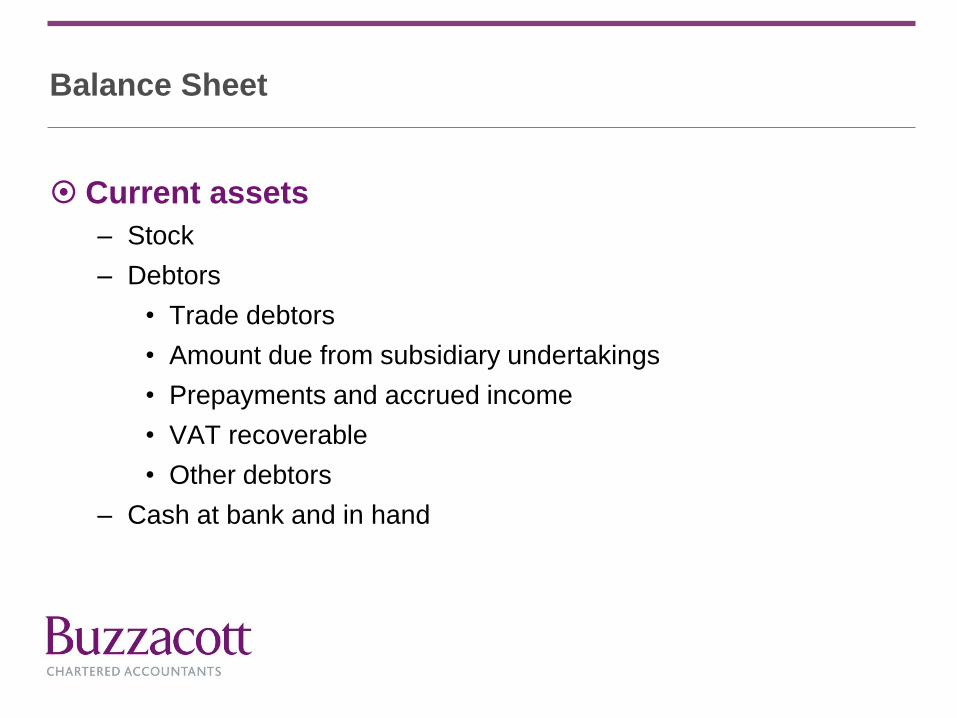

Current assets

– Stock

– Debtors

• Trade debtors

• Amount due from subsidiary undertakings

• Prepayments and accrued income

• VAT recoverable

• Other debtors

– Cash at bank and in hand

Balance Sheet

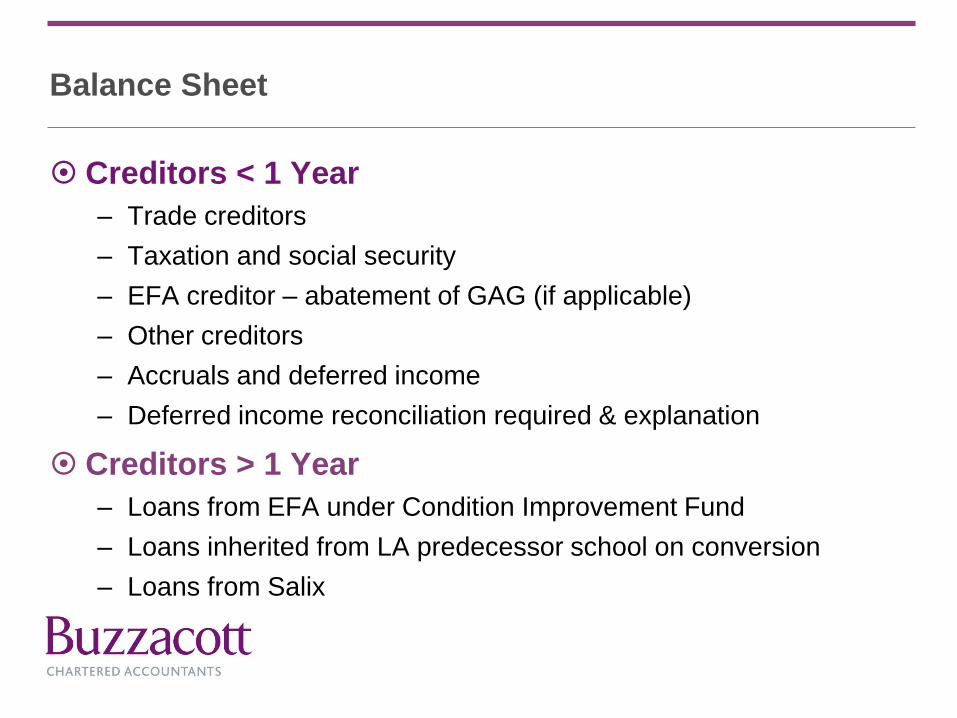

Creditors < 1 Year

– Trade creditors

– Taxation and social security

– EFA creditor – abatement of GAG (if applicable)

– Other creditors

– Accruals and deferred income

– Deferred income reconciliation required & explanation

Creditors > 1 Year

– Loans from EFA under Condition Improvement Fund

– Loans inherited from LA predecessor school on conversion

– Loans from Salix

Balance Sheet

Pension liability

– Local Government Pension Scheme

– Assessed each year by the actuaries (FRS 17 report)

– Balance sheet shows net position

– Notes to the accounts show the movements in year

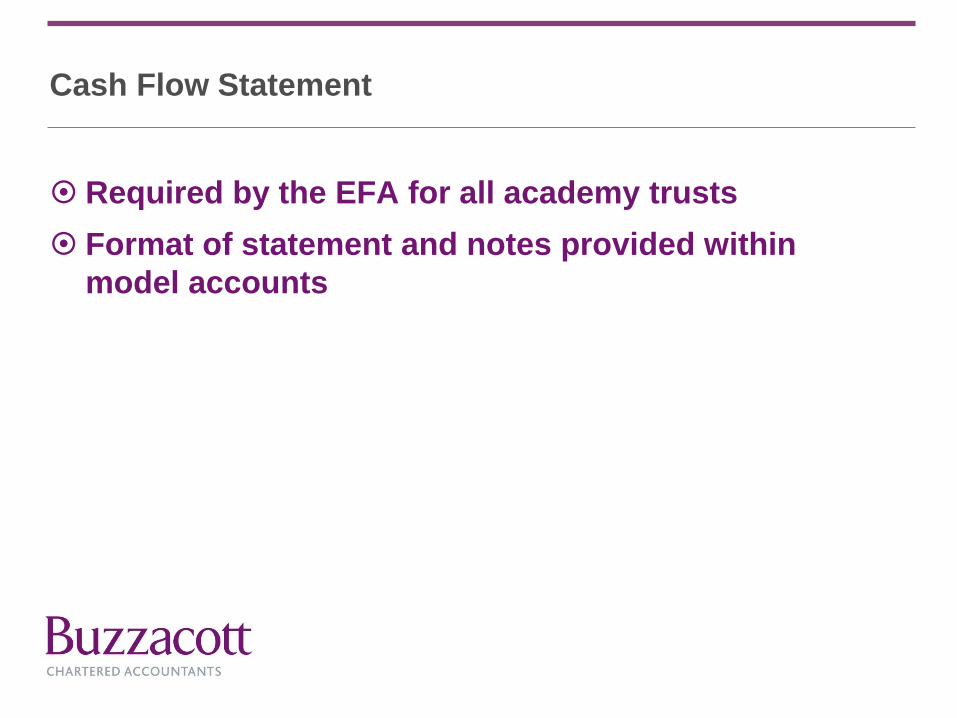

Cash Flow Statement

Required by the EFA for all academy trusts

Format of statement and notes provided within

model accounts

Accounting policies and notes to the accounts

Accounting policies

– Use Coketown Academy as a model

– Must be a policy included for all material items

– Guidance on capitalisation limits

Notes to the accounts

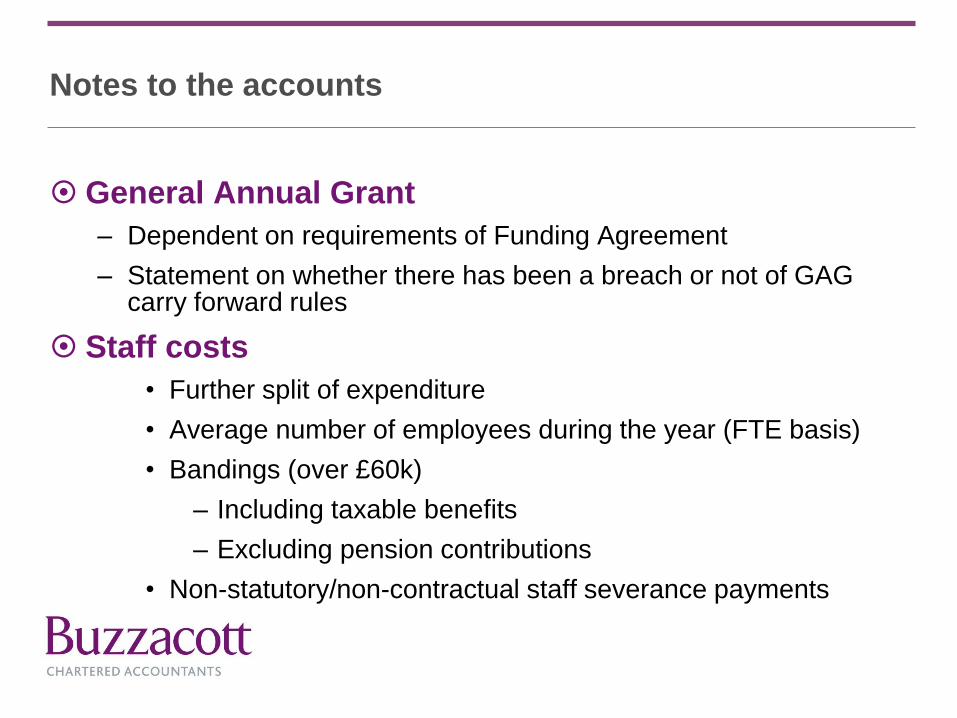

General Annual Grant

– Dependent on requirements of Funding Agreement

– Statement on whether there has been a breach or not of GAG carry forward rules

Staff costs

• Further split of expenditure

• Average number of employees during the year (FTE basis)

• Bandings (over £60k)

– Including taxable benefits

– Excluding pension contributions

• Non-statutory/non-contractual staff severance payments

Notes to the accounts

The following items should be disclosed in

aggregate, any transactions over £5,000 should also

be disclosed individually

– Ex-gratia compensation payments

– Gifts made by the academy trust

– Losses on fixed assets, stock or bad debts

– Guarantees, letters of comfort and indemnities

– Acquisition or disposal of freehold or leasehold land and buildings

Notes to the accounts

Governors’ remuneration and expenses

– Disclosure of the salaries in £5,000 bands of the Principal and Staff Governors (if they are also Trustees/Directors of the academy trust)

Related party transactions

Restricted funds

– Detail supporting each column in the SOFA and descriptions

Boarding trading account

Pensions

– TPS and LGPS

AD update 2014-2015 (SORP 2005 version)

Governance statement

– Governance review

– Value for Money statement

Buildings occupied by Church academies

Staff costs

– Staff severance payments

– Pension contributions

Financial reporting

– Donations

– Loans and long term creditors

Risk Protection Arrangements

SORP 2015

“Plain English” on the SoFA

Comparatives for all funds

Governance costs now a support cost

Uncertainties in going concern assessment

Key estimates and judgements

Key management personnel disclosures

Capital grants – moved to “donations and capital grants”

Computer software – within “intangible assets”

Audit - introduction

Overview of audit requirements

Key areas of accounts and audit preparation

Common issues

Multi-academy trusts

Audit requirements

Financial statements audit opinion

– True and fair view

– Prepared in accordance with UKGAAP

– Compliance with EFA Accounts Direction

– Consistency with governors’ report

Conclusion on regularity

AAR conclusion

True and fair view

Risk of error

– In preparation of financial statements;

– In underlying records (see audit assertions);

– Presentation and disclosure

Risk of fraud

Audit assertions

• Accuracy

• Classification

• Completeness

• Existence

• Ownership

• Cut off

• Valuation

The big 3

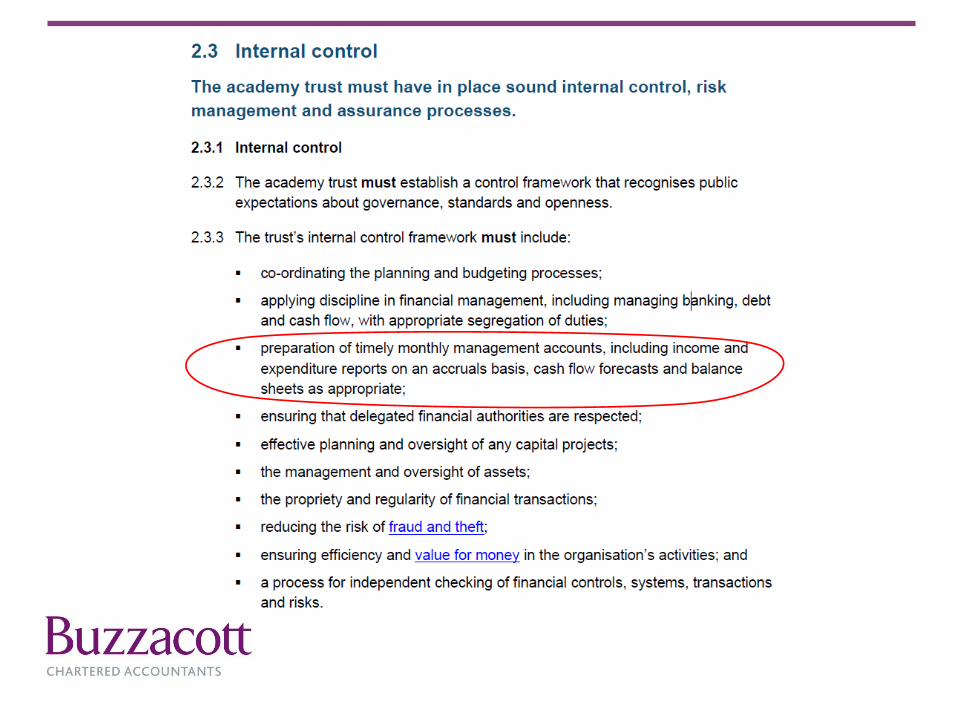

Internal control environment

Financial reporting environment

Audit preparation

Internal control environment

Culture – set from the top

Risks actively managed

Established systems and processes

Clear delegated authority and ownership

– including payroll and budgeting

Financial Reporting environment

Clear chart of accounts

Reconciliations and processes

(Semi) automated financial reporting

Clear and transparent financial analysis

Internal scrutiny

Audit preparation

Schedules and spreadsheets

Cross checking and review

Disclosures and analysis

(NB: What if Buzzacott assist with accounts prep?)

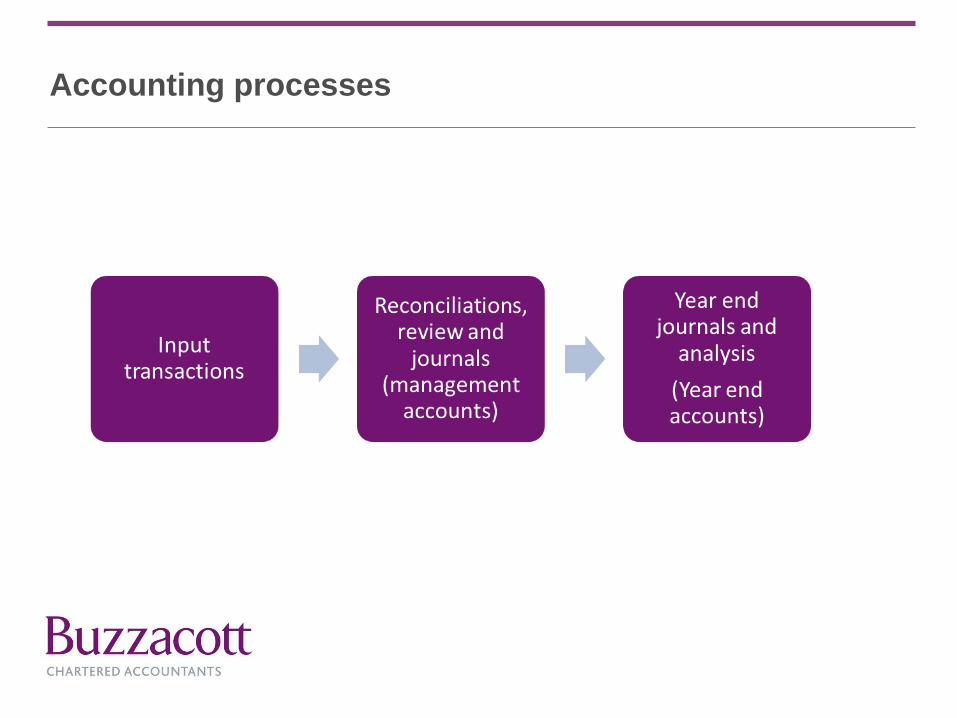

Accounting processes

Year end preparation

Financial reporting processes

– Bank, VAT, trade debtors and creditors, PAYE, other control accounts

– Accruals and prepayments

– Fixed assets

– FRS 17 journal (annual)

Additional year end information

– Fund analysis

– Additional disclosures: Remuneration, ex-gratia/gifts, losses etc

– AAR disclosures (counter party etc)

Preparing the accounts

Completeness of year end audit journals

Mapping the trial balance to the accounts

Additional schedules for accounts and audit

Income

GAG income

– SBS, minimum funding guarantee, education services grant, allocation protection, pre-16 high need funding, post-16 high needs funding

– NOT pupil premium and start up grants

Income recognition: Classification and cut-off

– Grants paid for year to 31 August included

– Grants paid for year to 31 March apportioned (e.g. pupil premium)

– Capital grant when receivable

Income reconciliation

TB Coding Classification

School Budget Share GAG

Minimum funding guarantee GAG

Education services grant GAG

Allocation protection GAG

Pre-16 high need funding GAG

Post-16 high needs funding GAG

Start-up grants Start-up

Pupil Premium EFA Other

Capacity building grant EFA Other

Schools Direct Other Gov

SEN Other Gov

Devolved formula capital Other Gov

ACMF Capital Grant EFA Capital

EFA reconciliation £

TOTAL EFA remittances X

Deferred from 13/14 (pupil premium?) X

Opening accrual (X)

Deferred to 15/16 (pupil premium) (X)

Accrued income X

TOTAL EFA funding Y

Split between:

GAG X

Start up grants X

Capital grants X

Other X

Y

EXPENDITURE ANALYSIS

Accounts Direction headings

TB

codes

Accounts Direction headings

TB

codes

EXPENDITURE ANALYSIS

Other year end analysis schedules

Both financial statements and AAR

Expenditure analysis

Staff costs analysis

Staff costs reconciliation to payroll

Pension analysis

Fixed asset register (reconciliation)

Debtors and creditors analysis (inc accruals/prepay)

FRS 17 pension working

Other fund accounts

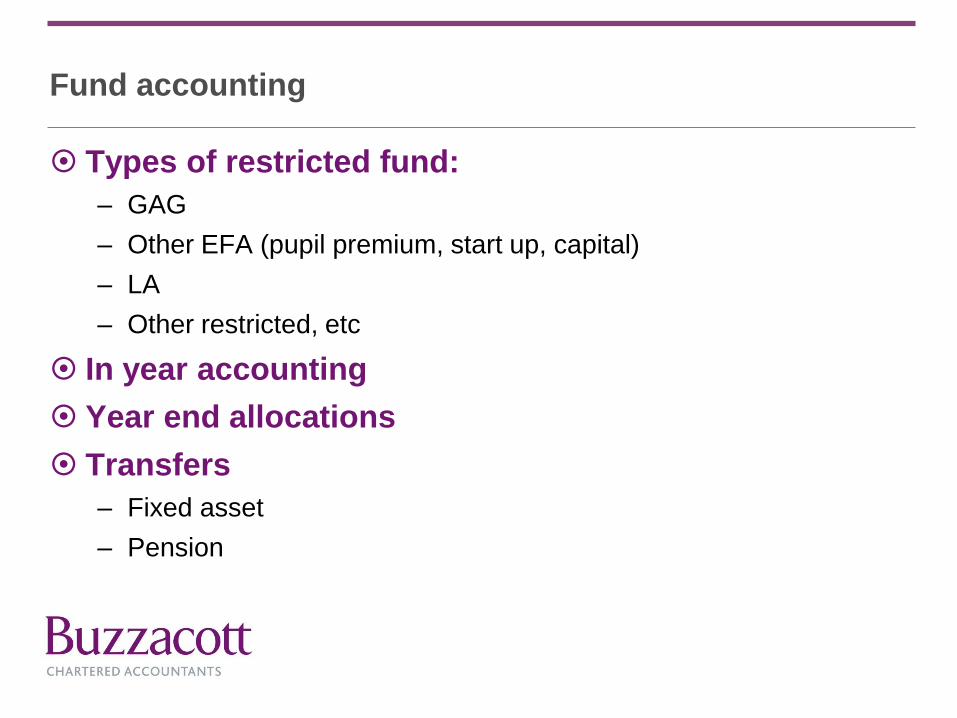

Fund accounting

Types of restricted fund:

– GAG

– Other EFA (pupil premium, start up, capital)

– LA

– Other restricted, etc

In year accounting

Year end allocations

Transfers

– Fixed asset

– Pension

Consolidation

Single trial balance or separate

Aggregation (single legal entity)

Consolidation (separate legal entities)

Aggregation / consolidation approaches

– Software

– Columnar based Excel approach

Consolidation

Academy 1

Trial

Balance

Academy 2

Trial

Balance

Academy 3

Trial

Balance

Central

Office

TB

Other

Trial

Balance

Aggregation

Adjustments

Academy

Trust

Total

Subsidiary

Company

TB

Consolidation

Adjustments

Consolidated

Total

(x) (x) (x) (x) (x) x (x) (x) x (x)

(x) (x) (x) (x) (x) - (x) (x) - (x)

(x) (x) (x) (x) (x) - (x) (x) - (x)

(x) (x) (x) (x) (x) - (x) (x) x (x)

(x) (x) (x) (x) (x) - (x) (x) - (x)

(x) (x) (x) (x) (x) - (x) (x) - (x)

(x) (x) (x) (x) (x) x (x) (x) - (x)

(x) (x) (x) (x) (x) - (x) (x) - (x)

(x) (x) (x) (x) (x) x (x) (x) x (x)

x x x x x - x x (x) x

x x x x x - x x - x

x x x x x (x) x x - x

x x x x x - x x - x

x x x x x (x) x x (x) x

x x x x x - x x - x

x x x x x - x x (x) x

x x x x x - x x - x

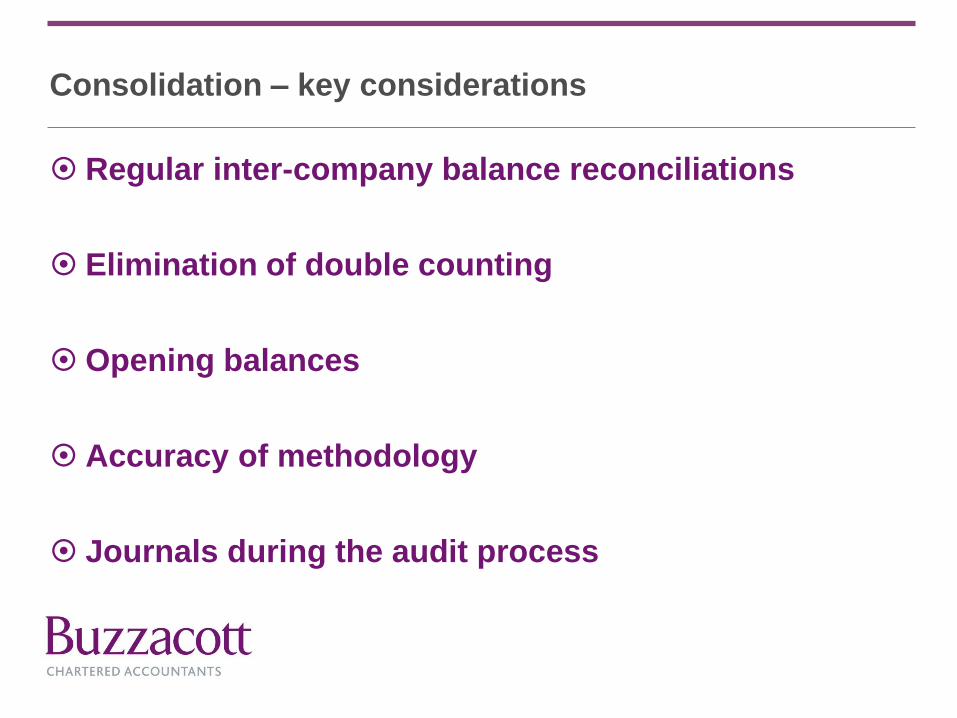

Consolidation – key considerations

Regular inter-company balance reconciliations

Elimination of double counting

Opening balances

Accuracy of methodology

Journals during the audit process

FRS 8: Related party transactions

Accounting standards

– Definitions: Control or “significant influence”

– Key management, governors, close family members, organisations that the above control/influence

Charity SORP

Academies Financial Handbook

– “At cost” requirement

Academy Accounts Direction

– Additional information (arms length)

Going concern and reserves policy

Reserves policy and disclosures

Forecasts

– Factoring in know changes (capital, income changes, expenditure changes)

Financial KPIs

– Staff costs ratio

– Other?

Multi-academy trusts

– Organisational changes

– Pooling of reserves

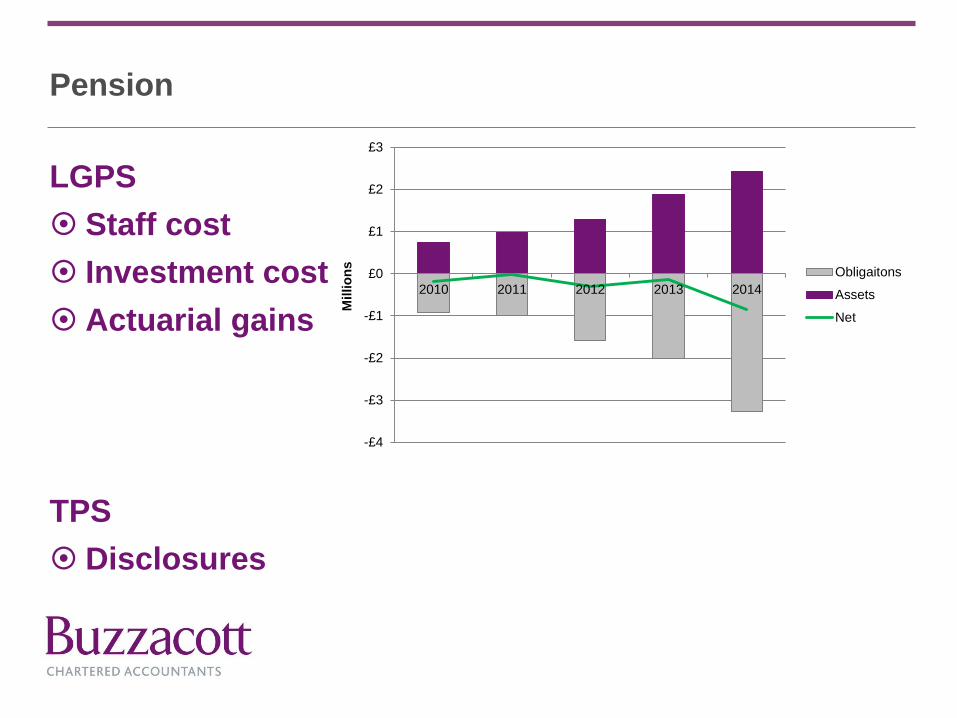

Pension

LGPS

Staff cost

Investment cost

Actuarial gains

TPS

Disclosures

-£4

-£3

-£2

-£1

£0

£1

£2

£3

2010 2011 2012 2013 2014

Millio

ns

Obligaitons

Assets

Net

FRS 15: Tangible fixed assets

Capital vs. revenue

Capitalisation of tangible fixed asset

– Risks and rewards of ownership

– Cost or valuation

Depreciation rates

– Useful economic lives

Fixed asset register

– Include all fixed assets in financial statements

– Additions and disposals (including AFH requirements)

– Check over the existence of assets

VAT, taxation and PAYE

Employment tax exposure on using freelancers

Costly Employer’s NIC changes with “contracted-

out” status going from April 2016

Care when hiring out facilities if not within the

Academy’s objects – could be taxable trading

Running nurseries are not deemed to be primary

purpose trading where children < 3 years old

Property works – may have an unintended VAT cost

depending on plans and future usage

Regularity, propriety and compliance

Regularity: For the purposes intended by Parliament

Propriety: Standards of conduct, behaviour and corporate

governance maintained when applying funds

Compliance: With the terms of the funding agreement (including

Academies Financial Handbook)

Regularity – common audit issues

119 regularity qualifications 2013/14 or 4.6% (2012/13, 83 or 3.7%)

Internal controls

Related party transactions not “at cost”

Severance payments not sought prior approval

Finance leases

Fraud or theft

Financial procedures out of date or not in line with actual practice

Lack of approval of relevant transactions (section 2.4 of handbook)

Regularity

2014 Academies Financial Handbook

– Compliance with the handbook

– Documented procedures

Accounting officer’s statement

Audit obligation

– Understanding of academy’s controls (and checks)

– Review of relevant transactions

– Review of supporting evidence

Self assessment checklist

Multi-academy trusts

New MATs

Growing MATs

Established MATs

Multi-academy trusts

New MATs

– Governance including audit committee

– Central services

– Regularity: Policies and procedures

– Financial reporting:

• Accounting system

• Aggregation

• Fund accounting

• Budgeting

– AAD financial statements disclosures for MATs

Multi-academy trusts

Growing MATs

– Development of central office

– Infrastructure investment (e.g. management structure)

– Inter-company

– Tax and VAT

– Risk management

– Internal monitoring and assurance

Internal control – 3 lines of defence

Multi-academy trusts

Established MATs

– Change management

– Financial strategy

– Aggregation - methods

– Control environment and internal monitoring

– Central office audit

– Fund accounting

– Buildings arrangements

Questions