ac303 summer 2015 prof. g. thomas white. revenues are inflows or other enhancements of assets of an...

TRANSCRIPT

Operating Activities & Earnings Quality

AC303Summer 2015

Prof. G. Thomas White

Operating Activities

Revenues are inflows or other enhancements of assets of an entity or settlements of its liabilities (or a combination of both) from delivering or producing goods, rendering services, or other activities that constitute the entity’s ongoing major or central operations.

Expenses are outflows or other using up of

assets or incurrences of liabilities (or a combination of both) from delivering or producing goods,42 rendering services, or carrying out other activities that constitute the entity’s ongoing major or central operations.

Operating Activities

Gains are increases in equity (net assets) from peripheral or incidental transactions of an entity and from all other transactions and other events and circumstances affecting the entity except those that result from revenues or investments by owners.

Losses are decreases in equity (net assets)

from peripheral or incidental transactions of an entity and from all other transactions and other events and circumstances affecting the entity except those that result from expenses or distributions to owners.

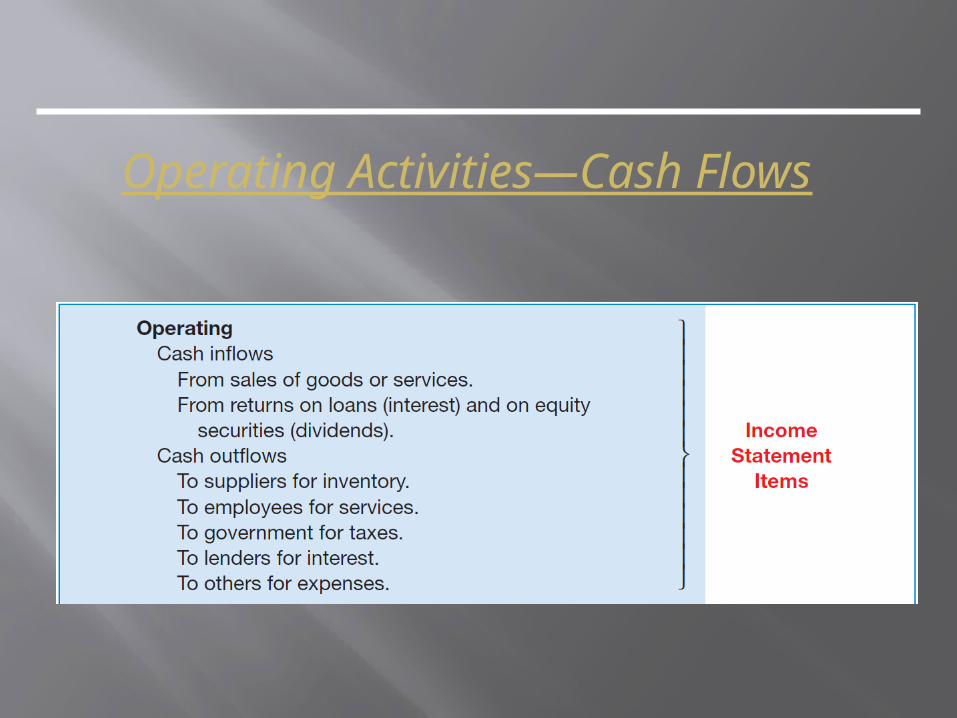

Operating Activities—Cash Flows

Company Product Life Cycle

Operating Activities—Cash Flows All Types

Operating Activities—Income Statement Structure

Operating Section Sales or Revenue Section Cost of Expenses General or Administrative Expenses

Non-operating Section Other Revenues and Gains Other Expenses and Losses

Income Tax Discontinued Operations Non-controlling Interest Net Income Earnings per Share

Note: Can be combined with a Statement of Comprehensive Income

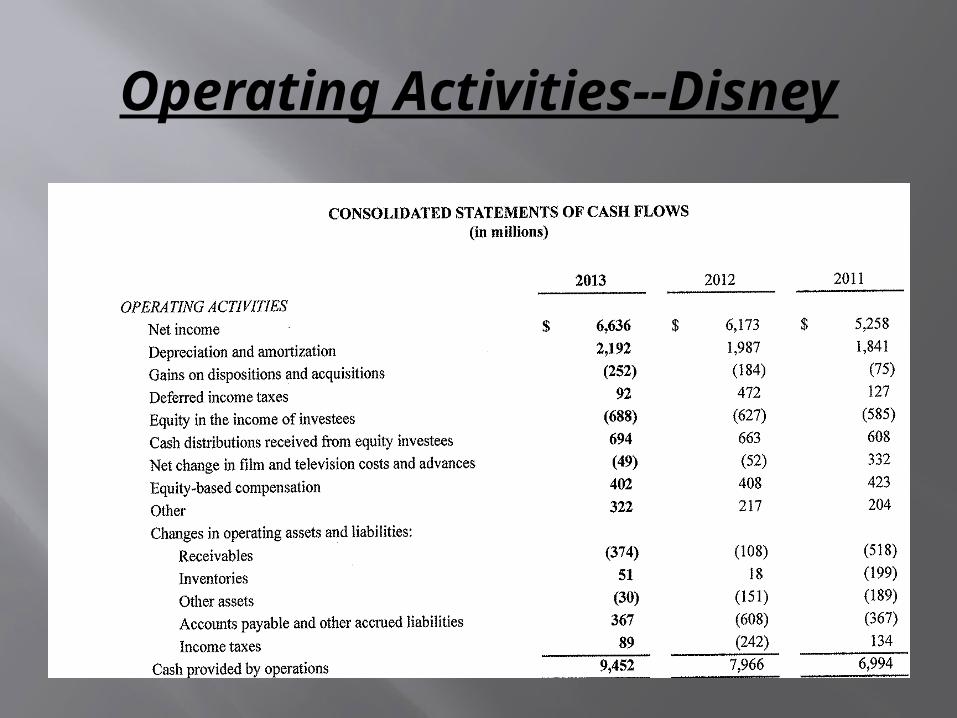

Operating Activities--Disney

Operating Activities--Disney

Use of Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and

assumptions that affect the amounts reported in the financial statements and footnotes thereto. Actual

results may differ from those estimates.

Revenue Recognition

Television advertising revenues are recognized when commercials are aired. Revenues from television subscription services related to the Company’s

primary cable programming services are recognized as services are provided. Certain of the Company’s contracts with cable and satellite operators include annual programming commitments. In these cases, recognition of revenues subject to the

commitments is deferred until the annual commitments are satisfied, which generally results in higher revenue recognition in the second half of the year.

Revenues from advance theme park ticket sales are recognized when the tickets are used. For non-expiring, multi-day tickets, revenues are recognized over a five-year time period based on estimated usage, which is derived from historical usage

patterns.

Operating Activities--Disney

Revenue Recognition--continued

Revenues from the theatrical distribution of motion pictures are recognized when motion pictures are exhibited. Revenues from home entertainment and video game sales, net of anticipated returns and customer incentives, are recognized on the date that video units are made available for sale by retailers. Revenues from the licensing of feature films and television programming are recorded when the content is available for telecast by the licensee and when certain other conditions are met. Revenues from the sale of electronic formats of feature films and television programming are recognized when the product is received by the consumer.

Merchandise licensing advances and guarantee royalty payments are recognized based on the contractual royalty rate when the licensed product is sold by the licensee. Non-refundable advances and minimum guarantee royalty payments in excess of royalties earned are generally recognized as revenue at the end of the contract term.

Revenues from our branded online and mobile operations are recognized as services are rendered. Advertising revenues at our internet operations are recognized when advertisements are viewed online.

Taxes collected from customers and remitted to governmental authorities are presented in the Consolidated Statements of Income on a net basis.

Operating Activities—In Class Exercise on Revenue RecognitionOn October 15, 1990, United Airlines (UAL Corporation) placed the largest wide-body air-craft order in commercial aviation history—60 Boeing 747-400s and 68 Boeing 777s—withan estimated value of $22 billion. With this order, United became the launch customer forthe B777. This order was equally split between firm orders and options.

a. Comment on when United Airlines should record the purchase of these planes.

b. Comment on when Boeing should record the revenue from selling these planes.

c. Speculate on how firm the commitment was on the part of United Airlines to accept delivery of these planes. d. 1. Speculate on the disclosure for this order in the 1990 financial statements and notes

of United Airlines.

2. Speculate on the disclosure for this order in the 1990 annual report of UnitedAirlines. (Exclude the financial statements and notes.)

e. 1. Speculate on the disclosure for this order in the 1990 financial statements and notesof Boeing.

2. Speculate on the disclosure for this order in the 1990 annual report of Boeing.(Exclude the financial statements and notes.)

Operating Activities--Disney

Expense Recognition: Allowance for doubtful accounts

“The Company maintains an allowance for doubtful accounts to reserve for potentially uncollectible receivables. The allowance for doubtful accounts is estimated based on our analysis of trends in overall receivables aging, specific identification of certain receivables that are at risk of not being paid, past collection experience and current economic trends. In times of domestic or global economic turmoil, the Company’s estimates and judgments with respect to the collectability of its receivables are subject to greater uncertainty than in more stable periods.” (Source: FY2013 Annual Report, emphasis added.)

Operating Activities--Disney

Expense Recognition: Various Items Film and television production, participation and

residual costs are expensed over the applicable product life cycle based upon the ratio of the current period’s revenues to estimated remaining total revenues (Ultimate Revenues) for each production

The costs of television broadcast rights for acquired movies, series and other programs are expensed based on the number of times the program is expected to be aired or on a straight-line basis over the useful life, as appropriate. Rights costs for multi-year sports programming arrangements are amortized during the applicable seasons based on the estimated relative value of each year in the arrangement.

Operating Activities--Disney

Expense Recognition: Various Items Software product development costs incurred prior to

reaching technological feasibility are expensed. We have determined that technological feasibility of our video game software is generally not established until substantially all product development is complete.

Parks, resorts and other property are carried at historical cost. Depreciation is computed on the straight-line method over estimated useful lives as follows:

Attractions 25 – 40 yearsBuildings and improvements 20 – 40 yearsLeasehold improvements Life of lease or asset life if

lessLand improvements 20 – 40 yearsFurniture, fixtures and equipment 3 – 25 years

Operating Activities--Disney

In-Class Exercise:Big Car Company did substantial advertising in late December. The company’s year-end date was December 31. The president of the firm was concerned that this advertising campaign would reduce profits.

a. Define an asset

b. Would the advertising payments represent an asset? Comment.

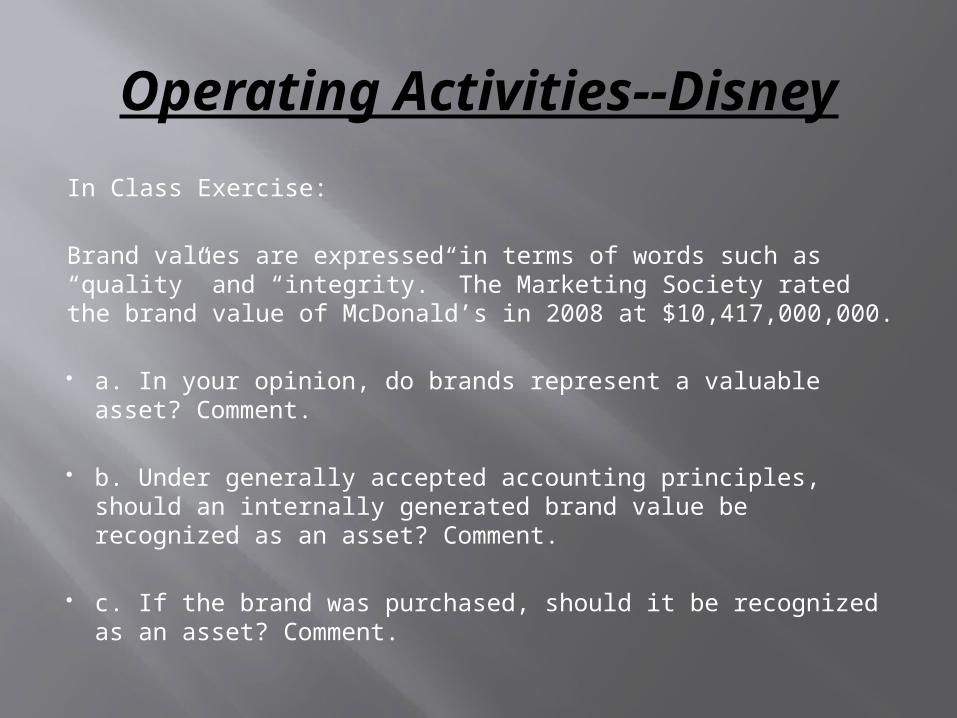

Operating Activities--Disney

In Class Exercise:

Brand values are expressed in terms of words such as “quality” and “integrity.” The Marketing Society rated the brand value of McDonald’s in 2008 at $10,417,000,000.

a. In your opinion, do brands represent a valuable asset? Comment.

b. Under generally accepted accounting principles, should an internally generated brand value be recognized as an asset? Comment.

c. If the brand was purchased, should it be recognized as an asset? Comment.

Financial Reporting & Earnings Quality

LO 1

Increase in Reporting Requirements

Reasons:

Complexity of business

environment.

Necessity for timely information.

Accounting as a control and

monitoring device.

Full Disclosure Principle

Differential Disclosure

“Big GAAP versus Little GAAP”.

FASB has traditionally taken the position that there

should be one set of GAAP.

FASB is working with an advisory committee to explore

ways that its standards can be more cost-effective for

all companies, regardless of size.

Full Disclosure Principle

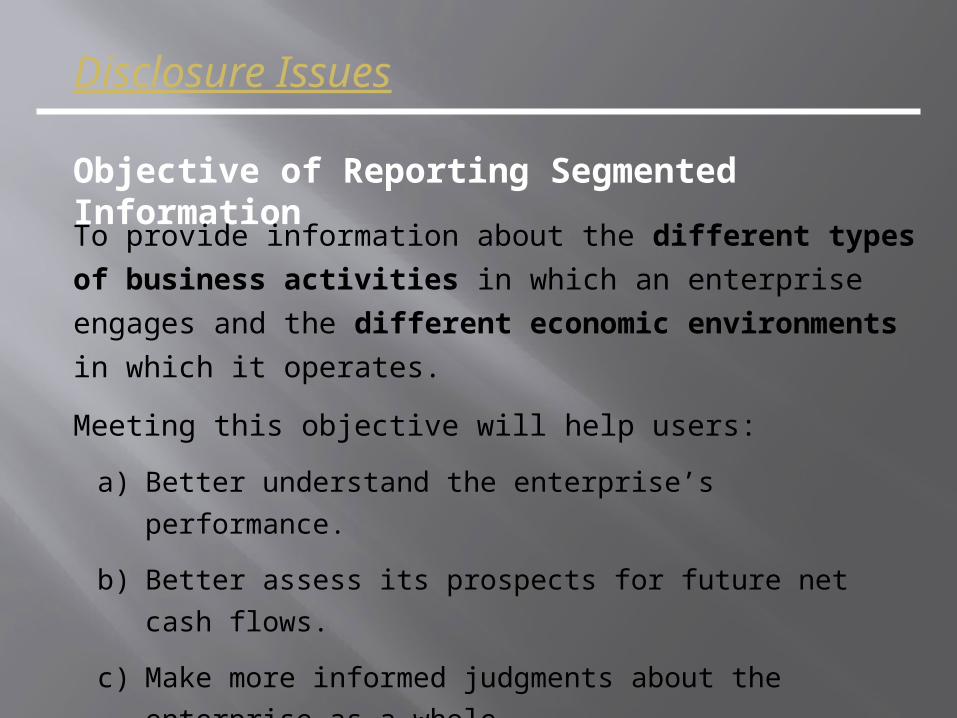

Objective of Reporting Segmented Information

To provide information about the different types of business

activities in which an enterprise engages and the different

economic environments in which it operates.

Meeting this objective will help users:

a) Better understand the enterprise’s performance.

b) Better assess its prospects for future net cash flows.

c) Make more informed judgments about the enterprise as a

whole.

Disclosure Issues

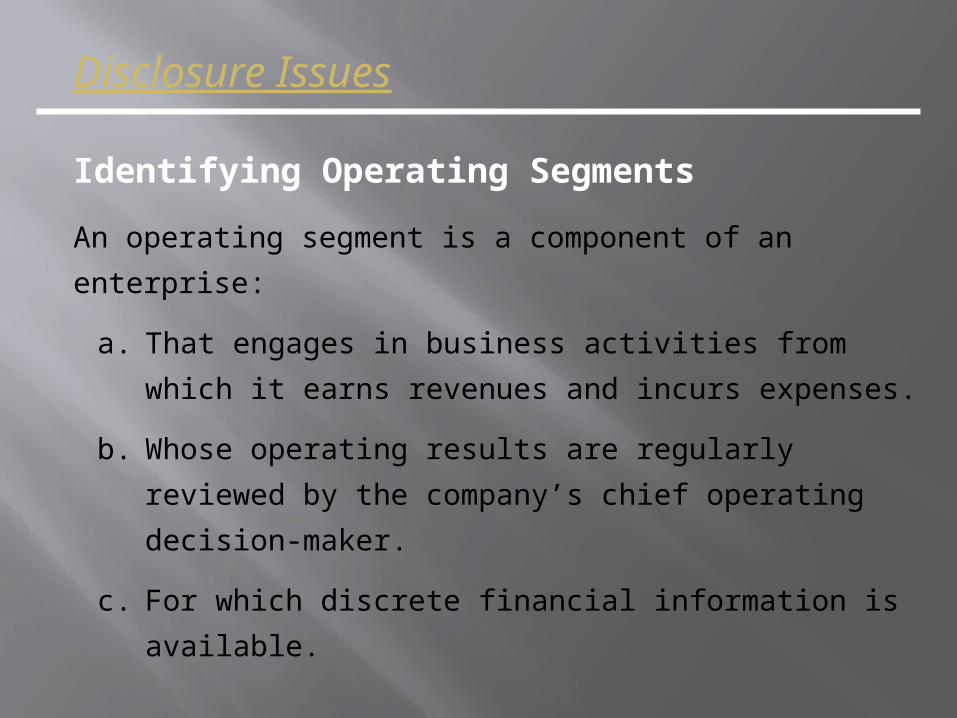

Identifying Operating Segments

An operating segment is a component of an enterprise:

a. That engages in business activities from which it earns

revenues and incurs expenses.

b. Whose operating results are regularly reviewed by the

company’s chief operating decision-maker.

c. For which discrete financial information is available.

Disclosure Issues

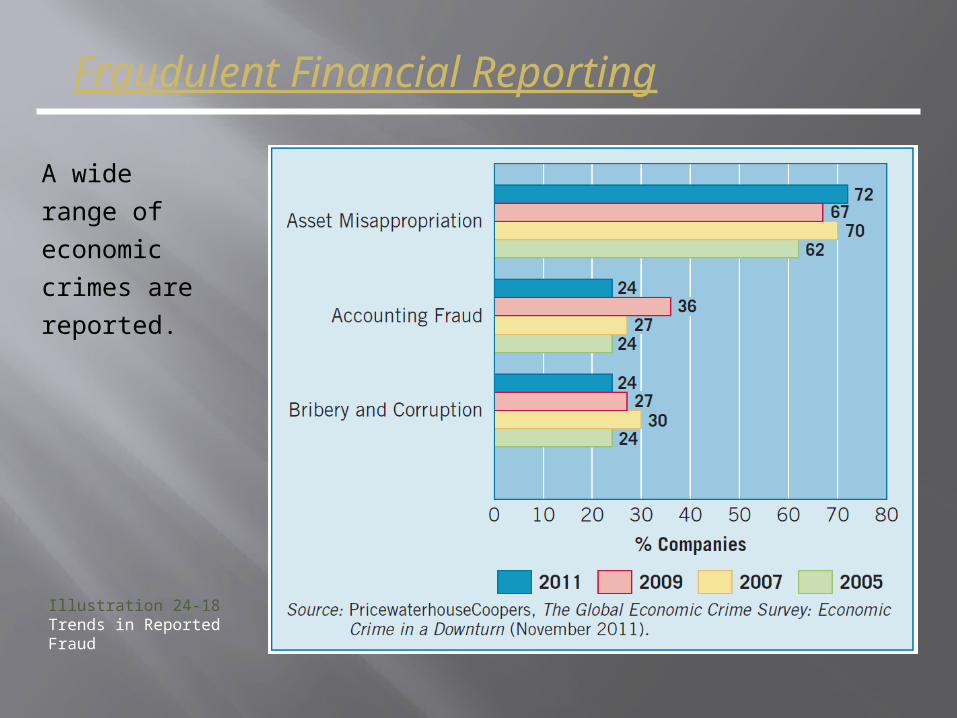

Fraudulent Financial Reporting

Source: Recent

global survey of

over 3,000

executives from

54 countries

documented

the types of

economic

crimes.

Illustration 24-17Types of Economic Crime

Fraudulent Financial Reporting

A wide range of

economic

crimes are

reported.

Illustration 24-18Trends in Reported Fraud