abstract - centre for economic performancecep.lse.ac.uk/pubs/download/dp0528.pdf · abstract this...

TRANSCRIPT

Abstract

This paper studies the effect of managerial ownership on performance and the determinants of managerial ownership for small and medium-sized private companies. We use a panel of around 1300 firms in the German business-related service sector for the years 1997-2000. Managerial ownership up to around 80 per cent has a positive impact on firm performance (incentive effect); for higher shares the effect becomes negative (entrenchment effect). Moreover, risk-aversion of managers and signalling of firm quality leads to a non- linear relationship between managerial ownership and the risk exposure of a firm. The determinants of performance and ownership are estimated simultaneously. JEL Classification: G32; C23 Keywords: corporate governance, managerial ownership, firm performance, small and medium-sized enterprises.

This paper was produced as part of the Centre’s Labour Markets Programme

Acknowledgements

We thank Bernd Fitzenberger, Steve Nickell and Marcia Schafgans for helpful discussions and Irene Bertschek, Dirk Czarnitzki, Ulrich Kaiser and Joachim Winter for useful comments. All remaining errors are our own.

Elisabeth Mueller is a member of the Centre for Economic Performance, London School of Economics. Contact: [email protected]. Alexandra Spitz is a member of the Centre for European Economic Research (ZEW), Research Group Information and Communication Technologies, PO Box 103443, 68034 Mannheim, Germany. Contact: [email protected] Published by Centre for Economic Performance London School of Economics and Political Science Houghton Street London WC2A 2AE Elisabeth Mueller and Alexandra Spitz, submitted December 2001 ISBN 0 7530 1549 8 Individual copy price: £5

Managerial Ownership and Firm Performance

in German Small and Medium-Sized Enterprises

Elisabeth Mueller and Alexandra Spitz

April 2002

1. Introduction 1

2. Theoretical Underpinnings and Previous Empirical Results 4

2.1 Theoretical Considerations on Managerial Ownership 4

2.1.1 Managerial Ownership Share and Firm Performance 4

2.1.2 Managerial Ownership Share and Risk 6

2.2 Previous Empirical Results 7

3. Data Description 9

3.1 Data Set 9

3.2 Definition of Key Variables 11

4. Estimation Results 13

4.1 Determinants of Company Performance 13

4.2 Determinants of Managerial Ownership 18

4.3 Simultaneous Determination of Managerial Ownership and Performance 21

5. Conclusion 24

6. Appendix 25

References 29

The Centre for Economic Performance is financed by the Economic and Social Research Council

Non–technical Summary

This paper studies the incentive effect and entrenchment effect of managerial ownership

in a sample of small and medium–sized firms in the German business–related service

sector. Moreover, the determinants of managerial ownership share are investigated.

Up to now, questions concerning corporate governance issues were mostly studied in

samples of large firms that are listed on the stock market. We address these questions in

a sample of private limited liability firms (GmbHs). GmbHs are the most important legal

form in Germany. They are characterized by the fact that the liability of the owners is

restricted to the amount of equity capital they invested in the firm. Typically, GmbHs

are small and medium–sized firms. We aim to analyse whether the distortions caused

by the separation of firm ownership and control are also present in GmbHs. Looking at

their overall importance, neglecting these distortions might result in negative aggregate

economic effects.

The analysis shows that managerial ownership is associated with incentive effects as

well as entrenchment effects. Increasing managerial ownership up to around 80 per cent

has a positive impact on firm performance, then the effect becomes negative. The positive

effect reflects better incentives whereas the negative effect is due to an entrenchment effect.

We also find that firms perform better when fewer managers with ownership stakes

are involved. With respect to outside owners, we find that companies with more outside

owners perform better. Monitoring by banks has a positive effect, as the more bank

relationships a firm has, the worse is its performance.

Moreover, we find a non–linear relationship between managerial ownership and the risk

exposure of a firm. For low and high levels of risk the relationship is positive, for medium

levels it is negative. The positive relationship between risk and managerial ownership in-

dicates signalling of firm quality by management whereas the negative relationship points

to the risk aversion of managers.

These results are robust to the use of different specifications and several estimation

methods. The simultaneous determination of performance and ownership is also consid-

ered.

1 Introduction

The economics profession has been interested in contract theory since the 1930s (see e.g.

Williamson, 1985). One important insight of this theory is that the firm is seen as a

governance structure, whereas approaches within the neoclassical framework characterize

the firm by a production function. The view of the firm as a governance structure changed

the whole analysis of economic organizations. Especially, the incentive literature and the

transaction cost approach emphasize that ownership matters. This paper is concerned

with one branch of the incentive literature, the agency literature and, more precisely,

with the principal-agent problem.

The main subject in the principal-agent literature is the separation of the ownership of

a firm from the control rights. This separation is supposed to create agency costs because

owners (principals) and managers (agents) have different objective functions. Berle and

Means (1932) provide a seminal work in this context. They state that with the large

size of modern firms and the diffuse ownership which often resulted, management took

over effective control. As a consequence, it seems very likely that management operates

the firm in its own interest. Then, the main focus of the literature is how managerial

discretion could be brought under more effective control.

This paper studies the effect of a firm’s ownership structure on its performance. Specif-

ically, we concentrate on the effect of managerial ownership on performance. We expect

to find two opposing effects – the incentive and the entrenchment effect. Managerial

ownership is one way to align the objective functions of the owners and the managers. It

is one way of ex ante incentive alignment that puts constraints on the managerial discre-

tion to reduce the ex post misallocation of resources (e.g. Holmstrom, 1979). From this

incentive effect we expect a positive relationship between managerial ownership and firm

performance. The entrenchment effect is especially important for high shares of manage-

rial ownership. If managers hold large shares of the equity, it becomes more difficult for

outside owners to exercise control. In this case managers will probably not maximize firm

value and a negative relationship between managerial ownership and firm performance

is possible. We also investigate the relationship between managerial ownership and the

risk exposure of a firm. In risky environments the management is reluctant to hold high

ownership shares in order to diversify their assets. But the size of managerial ownership

also has signalling effects, indicating firm quality.

We address these questions empirically for a sample of small and medium–sized pri-

1

vate companies with limited liability (GmbHs) in the German business–related service

sector.1 There are only a few empirical studies so far that examine issues of corporate

governance for small and medium–sized companies, in particular for private companies.2

Most empirical studies of corporate governance look at large firms that are listed on the

stock market (see e.g. Jensen and Murphy, 1990; Kaplan, 1994a, 1994b). However, the

distortions caused by the separation of ownership from control are also present in pri-

vate companies with limited liability. Moreover, although listed firms play a large role

in the United States, their overall importance in Europe is much smaller. In Europe,

incorporated firms not listed on stock markets are much more important. In Germany,

for example, GmbHs accounted for 32 per cent of total turnover in 1998 and their overall

importance has increased steadily in the last thirty years.3

GmbHs are characterized by limited liability of the owners, which means that owners

can lose at most the amount they contributed to the firm’s equity capital. They are not

liable for the company’s debt with their personal assets. In general, they share profits

according to the proportion of the firm’s equity capital they own. The GmbH is run by

managers who can hold a stake in the firm as well. The managers have plenary power

of representation to do business on behalf of the firm. Although it is not possible to

limit this power of representation with respect to third parties, other arrangements can

be made within the firm. The legal form of the GmbH is quite flexible. The respective

rights of managers and owners are agreed upon in the company contract, for which the

law stipulates only minimum requirements. For example, an owner always has the right

to see the accounts of the firm and a change in the company contract always requires a

minimum of three quarters of the vote. The distribution of profits is also regulated in

the company contract. Usually it occurs according to ownership share, but the company

contract can specify any other rule.

Due to management’s unrestrictable power of representation, the agency problem as-

sociated with the separation of ownership and control can be a serious phenomenon for

firms in the legal form of a GmbH. This issue may be reinforced by the relatively low

audit and public announcement requirements. Disclosure rules have been intensified since

1The counterpart of German GmbHs are limited companies (Ltds) in the UK and close corporations

in the USA.2One example is Bennedsen et al. (2000) which analyses ownership dilution for Danish closely held

corporations.3See table A1 in the appendix. Also see Harhoff and Stahl (1995) for a detailed description of the

increasing importance of GmbHs in Germany in the seventies and eighties.

2

1987, but de facto they are still quite weak (see e.g. Harhoff and Stahl, 1995).

Compared to existing empirical work on ownership structure and company performance

our work has the advantage that we cover a panel of nearly 1400 companies of the business–

related service sector from 1997–2000, that were drawn from a stratified random sample

according to their distribution in the population.4 Usually, empirical studies cover cross–

sections of the biggest companies in an economy, which are in general around 500 firms.

In our sample, the average firm has only 39 employees.

Our performance measure is obtained from a quarterly business survey in the business–

related service sector conducted by the Centre for European Economic Research in Mannheim,

Germany, since 1994. The companies are asked on a quarterly basis whether their profits

have increased, stayed the same or decreased in the last three months. On the basis of

these quarterly answers, we construct a performance measure that takes seasonal and

sectoral effects into account.

We use this performance measure since there is no balance sheet information and no

stock market price available for small private limited liability firms in Germany. It might

be criticized for giving only the direction of change but not the size of the change. But this

measure also has advantages, for example, we avoid the reliance on accounting data that

is often generated with tax considerations in mind. Also, the companies have no incentive

to misrepresent results since the questionnaire answers have no effect on, for example,

credit decisions by banks or on their reputation. We also avoid the use of Tobin’s Q.5

This measure relies on the efficiency of financial markets. In practise, stock valuations are

sometimes very volatile, and in this case, Tobin’s Q can be a poor measure of company

performance.

Since we use panel data, we are able to control for unobserved firm heterogeneity, e.g.

manager ability.

Our main finding is that a managerial ownership share up to around 80 per cent has a

positive effect on firm performance and a negative effect thereafter. We conclude that the

first effect is due to better incentives and that the second effect is due to entrenchment.

We also find that companies that are totally owned by managers do especially well.

In the context of our analysis it is very likely that firm performance influences the size

of managerial ownership. We address the question of reverse causality and of endogeneity

4For details on the data set and on the stratification design see section 3.1 below.5Tobin’s Q is equal to the ratio of the firm’s market value to the replacement cost of its physical assets.

It is a proxy for the firm’s valuable intangible assets like, for example, management performance.

3

by estimating lagged specifications as well as providing estimations using instrumental

variables. These estimations confirm our previous result of an inverse U–shaped form of

the influence of managerial ownership share on firm performance. Moreover, we apply the

Arellano–Bond dynamic panel estimation technique in order to take effects of past firm

performance into account. We find that firms that were more successful in the past tend

to perform better in the future. Furthermore, this specification also confirms the inverted

U–form relationship between managerial ownership share and firm performance.

Since the ownership structure of companies is a crucial question in the corporate gov-

ernance literature, we also investigate the relationship between managerial ownership and

the risk exposure of firms. Here we find a non-linear relationship between risk and man-

agerial ownership share. The negative effect might reflect risk–averse managers whereas

the positive effect might be due to signalling or commitment requirements.

In a last step, we take into account the fact that managerial ownership and firm per-

formance influence each other by estimating a system of simultaneous equations. This

analysis confirms qualitatively the results from the single equation estimates.

This paper is structured as follows: In section 2 we describe the theoretical underpin-

nings and previous empirical results. Section 3 gives a data description, section 4 presents

the estimation results, and section 5 concludes.

2 Theoretical Underpinnings and Previous Empirical

Results

2.1 Theoretical Considerations on Managerial Ownership

2.1.1 Managerial Ownership Share and Firm Performance

One of the major topics in corporate governance deals with the difficulties suppliers of

finance to firms may have in getting returns on their investment. Of particular interest

are the agency conflicts resulting from the separation of ownership and control. This sep-

aration is said to create agency costs to the extent that owners (principals) and managers

(agents) have different objectives. For example, managers may invest funds in low-value

projects to expand their empire instead of distributing these funds to the owners, who

might have better investment opportunities. The main focus of the literature is how

managerial discretion could be brought under more effective control, with special atten-

4

tion to difficulties caused by asymmetric information. The manager is generally better

informed than the owner about the potential of a company. Incentive contracts are a way

to mitigate the problems of asymmetric information. Since effort is not observable, it is

not possible to contractually define how much effort the manager should expend. In this

context, managerial ownership is one way of ex ante incentive alignment.

Jensen and Meckling (1976) distinguish between inside and outside suppliers of finance.

The insiders manage the firm, and are able to augment their stream of cash–flow by con-

suming additional amenities of office. As noted above, managers have an incentive to

adopt investment strategies that benefit them but reduce the payment to outside suppli-

ers of funds. Thus, the performance of the firm depends on the fraction of managerial

ownership. The greater this fraction, the greater the value of the firm.

According to Demsetz (1983) it is not clear whether owner managers or employed

managers consume more on the job. The compensation scheme of managers who are

at the same time owners has three components: pecuniary wage, profit of owners and

amenities of office. Employed managers compensation scheme consists only of pecuniary

wage and amenities of office. Since the managers objective is to maximize utility and

not to maximize profits, the amenities of office may have a great importance, especially

if one takes into account that managers typically spend most of their day at work. In a

competitive environment the managers have to pay for their on–the–job consumption by

a reduction in their pecuniary managerial compensation. That is, in a competitive world

with zero monitoring costs, there is an inverse correlation between take–home wages and

on–the–job consumption. As a consequence, the managers will not consume while on

the job unless the cost of doing so is less than if they consumed at home. Positive

monitoring costs weaken this relationship. The ownership structure of an organization

is an endogenous outcome that is an optimal response to company specific advantages

and disadvantages of different ownership structures. Therefore, no relationship between

ownership structure and profitability is to be expected.

The entrenchment hypothesis, on the contrary, states that there is a negative rela-

tionship between managerial ownership and profitabiltiy, especially at very high levels of

managerial ownership. The higher the ownership stake of the manager, the more difficult

it is for outside owners to control the management.

Taking the incentive hypothesis and the entrenchment hypothesis into account, we

expect a non–linear relationship between management’s ownership share and firm perfor-

mance. At low levels of ownership we expect the incentive effect to be dominant, that is,

5

we expect a positive effect. However, at very high levels of ownership the entrenchment

effect might be more important and the effect of ownership could be negative.

The literature also affords special interest to the role of banks in raising funds with

emphasis on the control rights attached to this. For Germany (and Japan), the financial

system is often classified as bank–based. This is due to the observation that banks have

close links with and a strong influence on firms they finance. Moreover, German firms

are said to maintain only a few bank relationships with a great degree of reliance on one

bank, the so–called “Hausbank”.6 One role of banks is to monitor the firms they finance.

In the case of debt, banks (or creditors in general) have to pay more attention to the risks

that managers take, whereas the effort level is not negatively influenced by debt. These

issues are related to the question of the optimal financial structure of the firm. Every

capital–structure is linked to a certain kind of governance structure.7

2.1.2 Managerial Ownership Share and Risk

Theoretical considerations about the relationship of managerial ownership and risk show

two opposing effects. On the one hand, since managers are risk averse, one would expect a

negative relationship between company risk and managerial ownership. The utility loss of

concentrating money in one investment is higher if the investment is riskier. On the other

hand, Leland and Pyle (1977) showed that managerial ownership can also serve as a signal

for company quality. A manager will only be willing to invest large amounts of his wealth

into the company if he is convinced that the company will be successful. This is taken into

account by banks when deciding on loan applications. Since banks are especially reluctant

to lend to risky companies, we expect that managers of risky companies need to make

more use of this signal. Therefore there can be a positive relationship between company

risk and managerial ownership. This paper attempts to analyse empirically which of the

opposing effects dominates for which risk levels.

6Some studies question these distinctive features of the German and Japanese financial systems in

comparison to the market–based Anglo–American system. Mayer (1990) observes, that in Germany bank

finance accounted only for 20 per cent of total sources, which is the same fraction as in the United States

and the United Kingdom, whereas in France, Japan and Italy bank finance accounted for 40 per cent of

total sources.7Unfortunately, we do not have information about the capital structure of the firms in our sample.

For this reason, we do not look at these arguments in more detail. For more information on this issue

see e.g. Aghion and Bolton (1989, 1992), Williamson (1988) and Harris and Raviv (1991).

6

2.2 Previous Empirical Results

As explained in the previous subsection, economic theory reveals many counteracting

mechanisms concerning the relationship between managerial ownership and firm perfor-

mance, without any hint as to which effects might be dominant. As a consequence,

empirical work is needed to identify the main effects. But, as will be shown in this study,

the empirical evidence is also contradictory.

First of all, to the best of our knowledge there are no studies that investigate the impact

of managerial ownership on firm performance for small and medium–sized German firms.8

However, there are some interesting empirical results for firms in the United States and

the UK.

Morck et al. (1988) investigate the relationship between management ownership of the

firm’s equity and Tobin’s Q in a cross–section of 371 Fortune 500 firms in 1980. They

find that Tobin’s Q rises as managerial ownership increases from 0 per cent to 5 per cent,

as ownership share increases further up to 25 per cent it falls, and then continues to rise

again as ownership share exceeds 25 per cent. The increasing Tobin’s Q supports the

incentive effect, whereas the decreasing Tobin’s Q supports the entrenchment hypothesis.

McConnell and Servaes (1990) confirm the non–linear relationship but with a different

form. They find a positive relationship up to a managerial ownership share of 40 to 50

per cent, and a negative relationship for higher shares.

Mehran (1995) tests the relationship between executive compensation structure, owner-

ship and firm performance. Using 153 randomly–selected manufacturing firms in 1979–

1980, he finds that managerial ownership has a positive impact on firm performance mea-

sured both by Tobin’s Q and by return on assets (ROA). He also estimates regressions

with various dummy variables for different levels of managerial ownership, like Morck et

al. (1988). However, the results favour a linear relationship over non–linearity.9

Demsetz and Lehn (1985) find no significant linear relationship between managerial

ownership and firm performance as measured as accounting profit rate.

8There are some studies dealing with corporate governance in Germany, see e.g. Kaplan (1994a),

Januszewski et al. (1999) or Koke (2000), but their main focus is different.9They also find a positive relationship between Tobin’s Q/ROA and equity–based management com-

pensation. But the relation between equity–based compensation and managerial ownership turned out

to be negative. This last result coincides with a study by Ofek and Yermack (2000), who find that

high–ownership managers tend to sell more of the shares they get from equity compensation to diversify

away the idiosyncratic risk associated with ownership concentrated in a single asset.

7

The empirical studies surveyed up to now show contradictory empirical evidence. One

explanation could be that there are differences in managerial ownership data. This issue

was investigated by Kole (1995), who examines three commonly used data sets in the

United States and focuses especially on the results of Morck et al. and McConnell and

Servaes. His study concludes that the different results on the relationship of managerial

ownership and firm performance are not due to differences in ownership data. There are

other variables that have to be controlled for, in particular the firm size.

Himmelberg et al. (1999) investigate the determinants of managerial ownership and the

relation between managerial ownership and firm performance in a panel regression. They

address the endogeneity problem associated with simple regressions of firm performance

on managerial ownership share. Their result is that managerial ownership depends on

the contracting environment a firm acts in, especially on the riskiness of the firm, which

determines the managers’ scope for moral hazard. In a risky environment, where moni-

toring activities by the owners are relatively expensive and the scope for moral hazard for

the managers is big, managers must have greater ownership stakes to align the respective

objective functions.

Harhoff and Stahl (1995) investigate the impact of managerial ownership on firm sur-

vival and on firm employment growth in German SMEs. They find that an increasing

share of managerial ownership has a positive impact on firm survival whereas there is no

significant effect of managerial ownership share on employment growth.

The effect of outside shareholders is studied by Nickell et al. (1997). They investigate

the impact of product market competition, financial market pressure and shareholder

control on firm productivity. Using panel data from 580 UK manufacturing firms they

find that dominant external shareholders have in general no positive effect on company

performance. However, if the dominant shareholder is a financial institution, then a

positive effect of monitoring is found.

Harhoff and Korting (1998) study the interaction between borrowers and lenders in

small and medium–sized German firms. They found that firms with more concentrated

borrowing and long–lasting bank relationships are able to negotiate better contract con-

ditions in terms of collateral requirements, interest rates, and credit availability.

Ang et al. (2000) study the relationship between a firm’s ownership structure and

its agency costs for a sample of small US companies. Two efficiency measures proxy for

agency costs: the ratio of operating expense to annual sales and the ratio of annual sales

to total assets. They find that companies with an owner manager have lower agency

8

costs, that agency costs decrease with the managerial ownership share, and that agency

costs increase with the number of outside shareholders. The results with respect to the

monitoring role of banks were less clear cut.

Our paper improves on the existing literature by looking at the influence of managerial

ownership on the profitability of private companies. So far only company growth and

efficiency measures have been considered. This is due to limitations on data availability.

Since balance sheets and profit and loss accounts are not available for German private

companies, we resort to the use of survey data. The availability of panel information is

also novel to the study of private companies. This allows us to control for firm specific

effects. We are the first to study the determinants of ownership for private companies.

Furthermore, we are the first to study the simultaneous determination of performance

and managerial ownership.

3 Data Description

3.1 Data Set

The data basis for the estimation is derived from a business survey in the German

business–related service sector carried out since 1994 by ZEW and Creditreform, Ger-

many’s largest credit rating agency. Since there is no exact definition of “business–related

services” in the literature, this industry is defined by enumerating certain sectors as done,

for example, by Hass (1995). The sectors as well as their industrial classification codes

are displayed in table A2 in the appendix.

The survey is carried out quarterly. A single page questionnaire is sent to about 4000

firms and the response rate is approximately 25 per cent. In 1994, when the survey

was launched, a stratified sample covering all companies included in the Creditreform

database was taken. The stratification was done according to company size, region and

sector affiliation. A sample refreshment takes place annually.

The questionnaire is divided into two parts. The first part contains questions on the

business development of the firms in the current quarter with respect to the previous

quarter and on their expectations for the next quarter. The second part is devoted to

questions of current economic or political interest. The survey is conducted as a panel.10

More precisely, in the first part, firms are asked about the development of their returns,

10For more details on the sample design and the data set see Kaiser et al. (2000).

9

sales, prices, demand, and number of employees. They indicate on a three point Likert

scale whether these variables have decreased, stayed the same, or increased in the current

quarter compared to the previous quarter. For the purpose of the current research the

variable of most interest is the assessment of the firm’s returns.11

The data derived from the survey is merged with company information from the Cred-

itreform database. This database contains detailed information on the ownership struc-

ture of firms. It also contains the size of the stakes that managers hold in a firm and

we know the identity of outside owners. Furthermore, the number of bank relationships

a firm holds is displayed. Other information is the number of employees, the age of a

company, and the number of business fields a company is active in. These variables have

been gathered on a yearly basis since 1997.

The main estimations are based on 2797 observations referring to 1351 firms. The

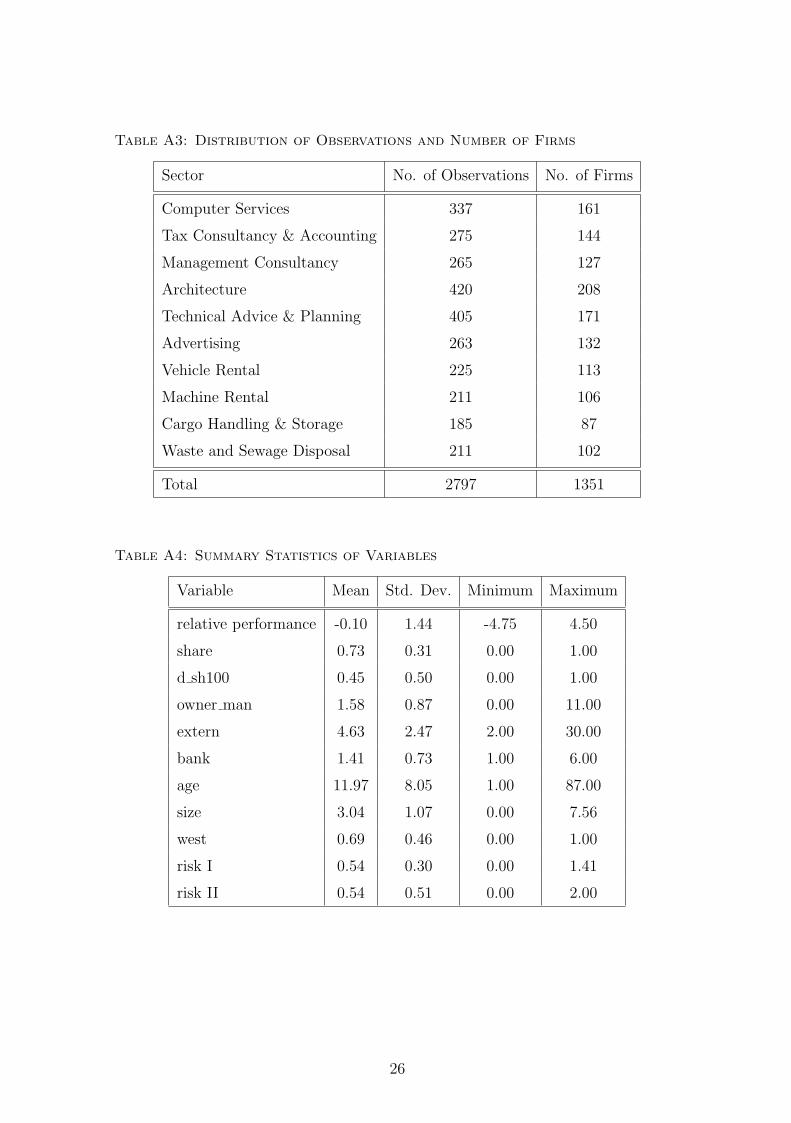

number of observations and firms per sector is displayed in table A3 of the appendix.

It is an unbalanced panel data set that includes observations from 1997 to 2000. The

participation pattern of the firms is as follows: 5 per cent of the firms participated in

all 4 years, 25 per cent participated in at least 3 years, and 50 per cent of the firms are

observed twice or less.

Is our dataset representative for companies in the German business-related service

sector? There are several possibilities how biases could be introduced. As mentioned,

the population for the questionnaire is all companies covered by Creditreform. Since

Creditreform aims to include all registered companies in their database, this should not

pose a problem. A second source of bias is the response pattern of the companies to

the questionnaire. If the no–responses are related to the topic we want to investigate –

the effect of ownership structure on performance – then our results will be biased. This

seems, however, unlikely. The survivor bias is present in our sample since we can only

observe profitability for companies that are still alive. In an annual sample refreshment

all companies are deleted that haven’t answered in the six preceding waves. The last

source of bias is the frequency with which Creditreform updates company information.

Companies for which there are more inquiries are updated more often. Again, if the

updating frequency is not related to our analysis, we face no problem.

11The exact question is: in comparison to the last three months, have your profits increased, stayed

the same or decreased?

10

3.2 Definition of Key Variables

Our first regression explains the links between ownership characteristics and company

performance. Since it is not possible to obtain balance sheet information for German

private companies we construct a performance measure on the basis of survey answers.

Every quarter, participating firms indicate whether their returns decreased, stayed the

same or increased in the current quarter in comparison to the previous quarter. The per-

formance variable (Relative Performance) is measured as the difference of the number

of times a company has answered that its returns have increased and the number of times

a company has reported that its returns have decreased in comparison with the average

“increased” and “decreased” responses from its industry. The performance measure is

calculated annually. The exact formula is:12

Relative Performance:

# of ‘increases’ per company per year−# of ‘decreases’ per company per year

−# of ‘increases’ per sector per year−# of ‘decreases’ per sector per year

# of companies in the sector

Compared to the direct use of the quarterly categorical answers of the firms this rel-

ative performance measure has several advantages. First, it avoids the estimation of

fixed–effects in panel ordered probit or logit models. Second, transforming the quarterly

data into annual data eliminates seasonal effects and sector effects are eliminated by the

normalization.

The relative performance measure is a continuous variable and the estimation of linear

panel models is feasible. Concerning the choice of our estimation method, the question

whether we want to estimate probabilities for specific outcomes or whether we are inter-

ested in average developments is important. Since our aim is to identify the latter we use

linear panel models.

12We also work with a second performance measure constructed on the basis of the survey answers

that took only the number of “increased” answers into account. We decided to concentrate on the

reported measure since the second measure may be subject to seasonality and does not take all the

available information into account. Nevertheless, we estimated the specifications reported below with

both performance measures with very similar results. This suggests that the results are robust to different

specifications of the performance measure.

11

The definitions of the variables determining performance are as follows (summary

statistics are displayed in table A4 in the appendix):

Ownership share of managers (share) is the sum of ownership stakes held by the

management of the firm. It is measured between 0 and 1. We expect a non–linear effect

on performance due to the incentive and entrenchment effect.

We construct a dummy variable that takes the value 1 if the stake that the manage-

ment holds is 100 per cent (d sh100). The share of companies that are totally owned

by managers varies with sectors between 31 per cent and 59 per cent. The average in

the whole sample is 45 per cent. Excluding companies that are totally owned by man-

agers the distribution of ownership share is approximately normal, centred around 55 per

cent and with relatively more observations above the mean. This distribution does not

vary substantially across sectors. We expect a positive sign since companies that do not

experience a separation of ownership and control should perform better.

The number of managers who hold ownership shares (owner man). We expect a

negative sign since for more managers it is more difficult to come to an agreement. Fur-

thermore, the incentive for a single manager is diminished, if the ownership is divided

between several managers.

The number of a firm’s external equity holders (extern). Larger external equity hold-

ers have a bigger incentive to monitor. Therefore we expect a negative sign.

The number of a firm’s bank relationships (bank). We expect a positive sign. If there

are fewer banks, they will have a bigger loan volume to the company and therefore more

incentives to monitor.

The natural log of number of employees (size). Regarding the number of employees,

the firms are relatively small. 78 per cent of the firms have less than 50 employees, 14

per cent have between 50 and 100 employees and only 9 per cent have more than 100

employees. It is not clear in which direction the relationship between profitability and

size goes.

In a second regression we explain the ownership share of managers (share). The

regression includes the following variables:

The standard deviation of the responses to the profitability question by company (risk

I). The profitability variable takes the value two if profitability has gone up, the value

one if profitability has stayed the same, and the value zero if profitability has decreased.

The forecasting error for returns by company (risk II). The absolute value of the

deviation of coding of forecasted return from coding of realized return for one period,

12

divided by the number of periods for which we have this information. We expect a non–

linear relationship between risk and managerial ownerhip due to risk–aversion of managers

and signalling of company quality.

A dummy variable that takes the value 1 for West German firms (west). This is a

control variable. We are not having a certain expectation with respect to its sign.

The natural log of number of employees (size). Because of wealth constraints we

expect that there is a negative relationship between managerial ownership and the size of

a company.

4 Estimation Results

4.1 Determinants of Company Performance

Our first specification estimates the relationship between relative firm performance and

the ownership share of managers, a dummy for ownership exclusively by managers, the

number of managers who hold ownership stakes, the number of outside owners, the number

of bank relationships, and the size of the company. We also include the quadratic term for

the ownership share of managers to allow for non–linearities. Due to the panel structure

of the data set, we are able to control for unobserved firm–specific effects, e.g. managerial

ability, by estimating fixed effect models.

The results of the first specification are displayed in table 1, column 1.13

The effect of the ownership share on performance has the form of an inverted “U”. We

find that managerial ownership has a positive effect up to an ownership share of around

50 per cent, then the effect becomes negative. The positive effect might reflect higher

incentives for managers. The negative effect of high ownership shares might be due to an

entrenchment effect. If managerial ownership exceeds a certain share then outside owners

find it more difficult to make managers accountable for their activities. These effects on

firm performance are statistically significant.

We find that companies with exclusive managerial ownership perform better than com-

panies that include outside owners. It seems to be the case that managers do better if

there is no interference from outside. Moreover, firms perform better when fewer managers

13We also estimated random effect models. The random effect method is rejected by the Hausman test.

This rejection of the random effect model indicates that the firm specific effects are correlated with the

regressors.

13

with ownership stakes are involved.14

The positive effect of exclusive managerial ownership is somewhat striking since the

difference in incentives for ownership between 90 per cent and 99 per cent of a company

compared to 100 per cent are not big enough to explain the difference in performance.

The difference cannot solely be due to incentives. There might be other effects at work.

One effect could be of a psychological nature. A manager who is the sole owner might feel

more involved with his company and might therefore work harder. Another explanation

might be that this result is driven by reverse causality. Managers might only elect to take

100 per cent ownership of the very best companies. If companies do not perform very well

they might prefer shared responsibility. In the latter case, they could shift the blame for

bad performance onto the influence of the other owners.

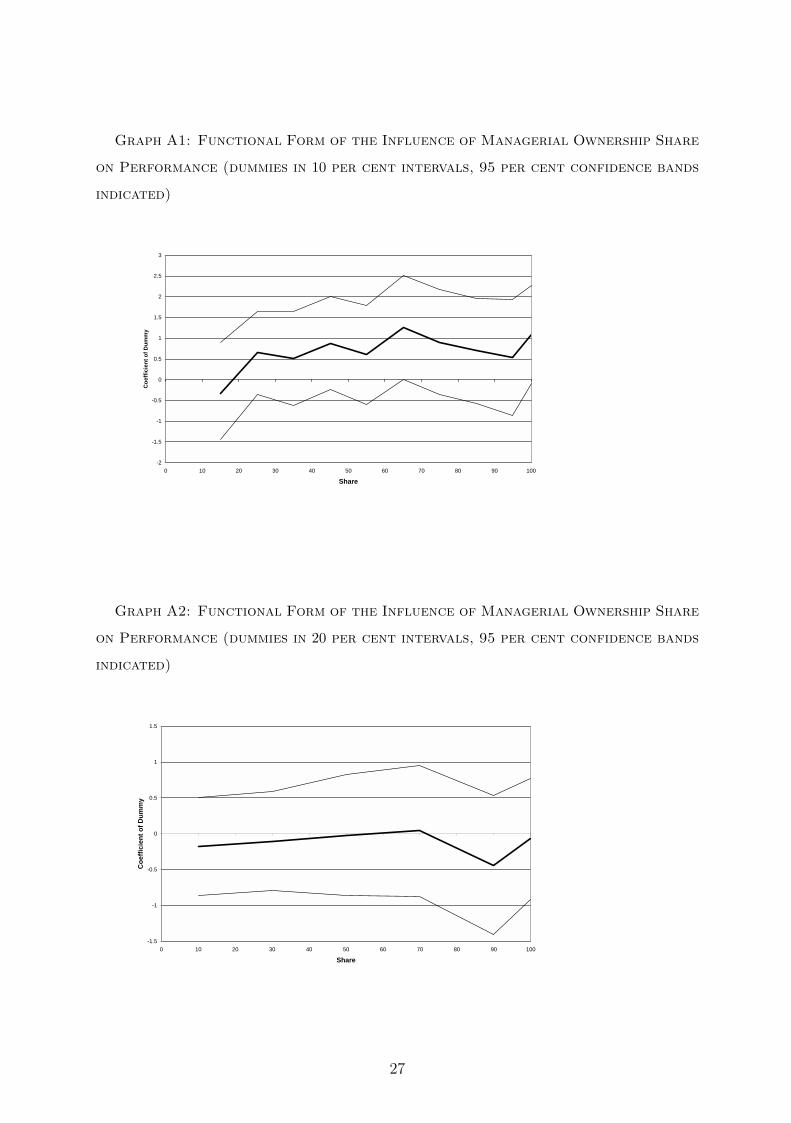

We test the appropriateness of the quadratic specification with regressions where we

include dummies for every 10 per cent interval (and 20 per cent interval) of share owner-

ship. This regression confirms the inverted U–shape of the influence of ownership share.

It also confirms the extraordinarily good performance of companies with 100 per cent

managerial ownership. Graph A1 in the appendix illustrates these results, graph A2 dis-

plays the results of a regression with dummies for every 20 per cent managerial ownership

share. The graphs also contain 95 per cent confidence bands.

The number of managers with ownership stakes has a negative influence on performance

as expected, although the effect is not significant in the regression. If there are several

managers it becomes more difficult to agree on the company strategy and, furthermore,

the incentive due to the ownership stake is smaller for each single manager.

With regard to the effect of outside owners we find that the more outside owners,

the better the performance. This finding is in contrast to corporate governance literature,

which pronounces the importance of monitoring activities, best performed by concentrated

ownership. In contrast, widespread ownership leads to the free rider problem since there

are only weak incentives for individual investors to seek information about the managers’

work. We, in turn, do not find that owners with a big share would be more effective

in monitoring. In this context, this estimation result confirms the previously mentioned

14We regress the change in profits on the level of managerial ownership share. Our results do not imply

that better companies will grow faster than the worse for ever. Nickell et al. (1997) find that competitive

pressure has a positive influence on productivity growth. Companies that grow faster build up market

share over time, but then they face less competitive pressure to innovate and hence their productivity

declines.

14

notion that it is better to leave the manager alone. Ownership changes through inheritance

can be used to illustrate this point. For example, after the death of the founder it is often

the case that family members who are not involved in the management of the company

become owners. It can be harmful if these new owners try to influence important decisions.

This result might also be driven by reverse causality. It might be necessary for badly

performing companies to find several owners because no one is willing to take on sole

responsibility.

We find that monitoring by banks has a positive effect. The more bank relationships

a company has, the worse its performance. This is compatible with the argument that

banks with a high loan volume to one company will spend more resources on monitoring

than banks with a small loan volume. But it also confirms the view that companies with

a poor performance need to seek loans from several banks because no bank wants to make

a big commitment. It is not possible to differentiate between these two arguments.

We also include measures of market concentration and import competition in the re-

gression to control for the effects of competitors on performance. For market concentration

we calculate the Herfindahl index on a sectoral level with (partly estimated) turnover fig-

ures of the companies in our sample. For import competition we use a question from

the survey on whether the company faces competition from foreign companies. However,

both measures turn out to have little explanatory power. The results are not shown in

the tables.

As already noted above, the regression potentially suffers from a problem of reverse

causality. It is possible that the performance of a company has an influence on the size

of the ownership stake a manager is willing to take. Managers tend to be very well

informed about the potential of a company before they decide on the stake. This could

lead to higher ownership stakes in well performing companies and lower ownership stakes

in badly performing companies. But it is also necessary to take the price that managers

need to pay for the stake into account. If a company is known to be good, the former

owners will charge a high price and the stake the new manager is going to buy will be

consequently lower. Nevertheless, if managers are better informed about the potential of

a company than the owners, our results might represent an overestimate of the effect of

ownership on performance.

It is also necessary to consider the managerial owners’ dilemma regarding the optimal

date of selling the stakes. Managers might sell when the company is doing very well

because they then get a high price for the stake, but managers might also sell when the

15

company is doing badly because they need to raise additional capital. In both cases, the

share of managerial ownership will fall but the relationship to the performance of the

company is undetermined.

To study the dynamic effects of managerial ownership share on performance and to

address the endogeneity problem, we estimated lagged specifications. The use of fixed

effect estimation helps to control for endogeneity as long as the effect is time–invariant,

because in this case it will be captured by the fixed effect. The lagged specification

additionally controls for endogeneity due to a correlation of the time–invariant error term

with regressors of the same time period. Table 1, column 2, reports the estimation results

of the regression including lagged specifications of the share variables.

The specification with lagged explanatory variables confirms the inverted U–form. The

maximum point increases to around 80 per cent, i.e. we find a positive effect of managerial

ownership share up to 80 per cent, then the effect becomes negative. Taking lags increases

the level of significance of the share and share-squared coefficients, moreover, the values

of the coefficients increase.

Graph A3 in the appendix illustrates how (ceteris paribus) performance changes as

managerial ownership share changes from zero to 100 per cent. Firm performance in-

creases steadily up to around 80 per cent managerial ownership share. Afterwards, the

performance measure decreases slightly. Nevertheless, due to the way the performance

measure is constructed, it is not possible to relate these index values to growth rates.

The estimated influence of our further regressors remains unchanged. Firms with fewer

managers perform better, in the lag specification this effect turns out to be significant on

the 5 per cent level. Widespread outside ownership has a positive effect. We also still find

that firms with fewer bank relationships have a better performance. In this specification

we did not include the dummy for exclusive managerial ownership because it was not

significant.

Thus, the results of our first specification reported in table 1, column 1, seem not to be

driven by reverse causality. The general effects are confirmed by the lagged specification.

We can also show that the effect of managerial ownership on performance needs time to

take full effect. Changes in incentives and entrenchment need some time to be reflected

in the performance of the company.

16

Table 1: Estimation Results of Fixed–Effect and Arellano–Bond Regressions

Dep. Variable: Relative Performance

(1) Fixed Effect (2) Fixed Effect (3) Arellano–Bond

share 3.54* 5.52*

(2.16) (2.90)

share (lag) 7.34***

(2.88)

share squared -3.17* -5.86**

(1.78) (2.41)

share squared (lag) -4.32**

(2.16)

owner man -0.13 -0.01

(0.11) (0.14)

owner man (lag) -0.50**

(0.21)

d sh100 0.79** 1.24**

(0.40) (0.57)

extern 0.19** 0.15* 0.12

(0.08) (0.09) (0.12)

bank -0.11* -0.18** -0.14

(0.15) (0.08) (0.11)

size -0.21 -0.23 -0.43*

(0.15) (0.26) (0.26)

relative performance 0.13***

(lag) (0.05)

Number of observations: 2797 1434 1143

Number of firms: 1351 777 612

F-Test: 2.06 3.10

(degrees of freedom) (7, 1439) (6, 651)

Wald chi2(8)–Test: 22.06***

Arellano–Bond test for first–order autocorrelation in the first differenced residuals: -10.17***

Arellano–Bond test for second–order autocorrelation in the first differenced residuals: 0.55

***,**,*=significant on the 1, 5 and 10 per cent level, standard errors are in parentheses

17

Due to the panel structure of our data set we are able to investigate the impact of

past firm performance on current firm performance. It is very likely that firms that were

successful in the past continue to perform better.

We study the persistence of firm performance by applying a General Method of Mo-

ment (GMM) estimator that, in the context of dynamic panel estimation, is proposed by

Arellano and Bond (1991). Further lags of the level and the difference of the dependent

variable are used to instrument the lagged dependent variable included in a dynamic panel

model. Lags of the performance measure going back to 1994, the year when the survey

started, were used. Estimation results are displayed in table 1, column 3.

The results confirm the persistence of firm performance. Firms that were more suc-

cessful in the past tend to perform better in the future. This effect is significant on the

1 per cent level. Moreover, the inverted U–form specification of the influence of man-

agerial ownership share and firm performance is still appropriate, with a maximum point

of around 50 per cent of managerial ownership share. The signs of the other regressors

remain unchanged compared to the fixed–effect results, although the level of significance

drops considerably for some of them.

Arellano–Bond tests for first and second–order autocorrelation in the first differenced

residuals are also reported. The null hypotheses of no first–order autocorrelation in the

differenced residuals is rejected, but it is not possible to reject the null hypotheses of no

second–order autocorrelation. Given first differences, the presence of first–order autocor-

relation in the differenced residuals does not imply that the estimates are inconsistent,

whereas the presence of second–order autocorrelation would imply that the estimates are

inconsistent.15

4.2 Determinants of Managerial Ownership

Managerial ownership is determined by several firm characteristics of which risk exposure

of a firm is especially important. Because managers are risk averse, we expect a negative

relationship between risk exposure and managerial ownership. However, managers also

use their ownership stake to signal firm quality to banks. Since banks are especially

reluctant to lend money to risky firms, there can also be a positive relationship between

risk exposure and managerial ownership. The results will show which effect dominates for

which risk levels.

15See Arellano–Bond (1991: 281f.) for a discussion on this point.

18

We use the tobit regression model to find the determinants of managerial ownership

because our endogenous variable – the managerial ownership share – is censored to lie

between zero and one hundred per cent. We do not use a fixed–effect estimator because

most of our regressors do not vary much over time. Managerial ownership is explained by

company risk, firm size, sector, and region. The results of the share regression are given

in table 2 below. Column 1 shows the result of the first risk measure (risk I), in column

2, the result of the second risk measure (risk II) is reported.

Both risk measures indicate a polynomial functional form of the influence of risk on

the managerial ownership share. We find that ownership share first decreases with risk

and then increases, finally, it decreases again. The negative relationship between risk

and managerial ownership share indicates that managers are risk-averse. They prefer

to diversify risk by investing their financial assets elsewhere, especially as they already

have their human capital in the firm. After a certain point, banks could be reluctant to

lend to risky companies because they are afraid of losing their money. The only way a

manager can convince the bank that even though the company is risky it is of high quality

is by holding a big personal stake. This finding is in contrast to the theory of optimal

risk sharing, which predicts that risk–averse managers will hold smaller stakes in riskier

companies because the advantage of aligned incentives is outweighed at a lower level of

ownership by the higher cost of risk bearing. For that reason, it is not surprising that

our estimation results suggest that, after a certain level of risk, the cost of risk bearing

exceeds the advantage of aligned incentives, i.e. in high risk companies the relationship

between risk and managerial ownership share tends to be negative again.

This functional form was also confirmed by a dummy variable regression (see graph A4

in the appendix).

As expected, the size of a company has a negative influence on managerial share hold-

ings. Big companies need more outside owners because of the limited wealth of the

managers.

Although not reported, there is considerable sectoral variation of managerial ownership

across sectors. Five out of ten sectoral dummies are significant. The difference between

East and West Germany is also significant. In West Germany ownership stakes are 5 per

cent higher.

In order to investigate possible reasons for the positive relationship between risk and

managerial ownership, we exploit information from the survey through the question:

“Have your business activities been hindered by financial restrictions?”. This question

19

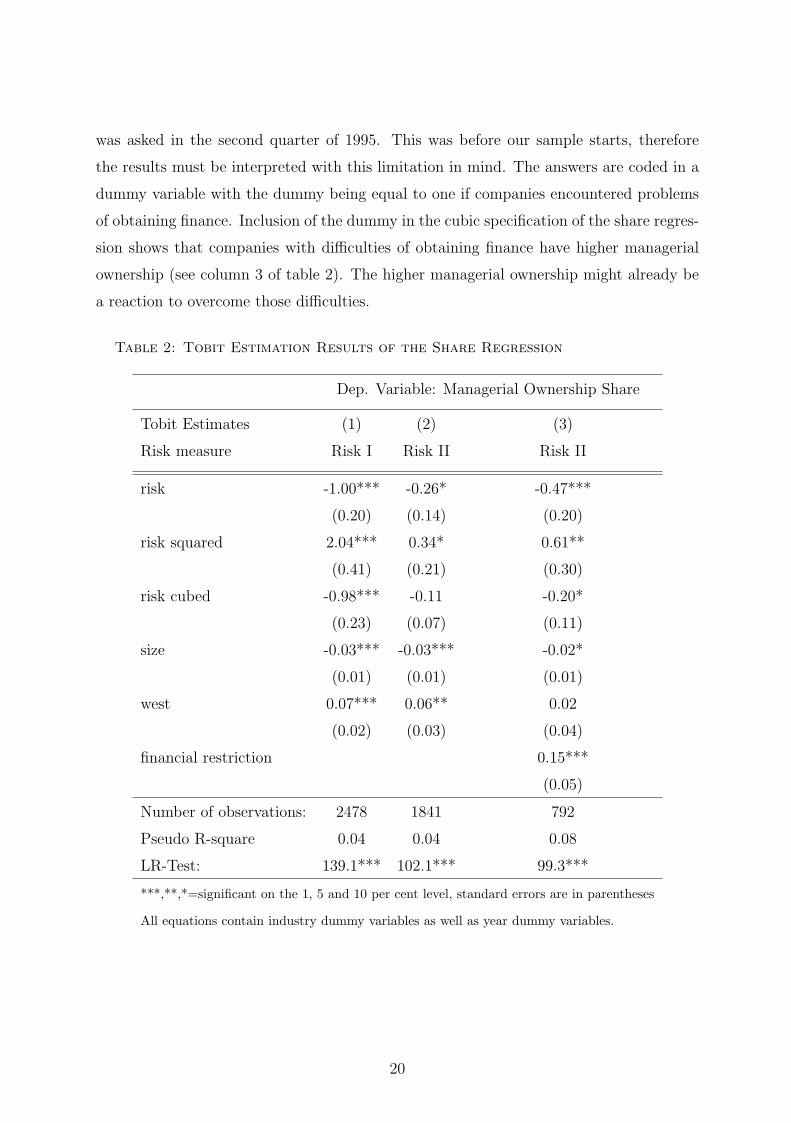

was asked in the second quarter of 1995. This was before our sample starts, therefore

the results must be interpreted with this limitation in mind. The answers are coded in a

dummy variable with the dummy being equal to one if companies encountered problems

of obtaining finance. Inclusion of the dummy in the cubic specification of the share regres-

sion shows that companies with difficulties of obtaining finance have higher managerial

ownership (see column 3 of table 2). The higher managerial ownership might already be

a reaction to overcome those difficulties.

Table 2: Tobit Estimation Results of the Share Regression

Dep. Variable: Managerial Ownership Share

Tobit Estimates (1) (2) (3)

Risk measure Risk I Risk II Risk II

risk -1.00*** -0.26* -0.47***

(0.20) (0.14) (0.20)

risk squared 2.04*** 0.34* 0.61**

(0.41) (0.21) (0.30)

risk cubed -0.98*** -0.11 -0.20*

(0.23) (0.07) (0.11)

size -0.03*** -0.03*** -0.02*

(0.01) (0.01) (0.01)

west 0.07*** 0.06** 0.02

(0.02) (0.03) (0.04)

financial restriction 0.15***

(0.05)

Number of observations: 2478 1841 792

Pseudo R-square 0.04 0.04 0.08

LR-Test: 139.1*** 102.1*** 99.3***

***,**,*=significant on the 1, 5 and 10 per cent level, standard errors are in parentheses

All equations contain industry dummy variables as well as year dummy variables.

20

4.3 Simultaneous Determination of Managerial Ownership and

Performance

In the last two subsections we analysed the determinants of firm performance and man-

agerial ownership share in single equation specifications. Concerning firm performance

we addressed the problem of reverse causality and of dynamic effects. Moreover, by es-

timating fixed-effect regressions, potential time–invariant correlation between regressors

and the disturbance term have been eliminated.

In this subsection, we estimate the performance equation and the managerial ownership

equation in a system of equations using a three–stage least squares regression method.

This method is an instrumental variable approach and takes potential endogeneity of

managerial ownership as well as of firm performance into account. This endogeneity is

due to unobserved firm–specific forces, e.g. managerial ability or managerial motiva-

tion that influence the endogenous explanatory variable as well as the outcome variable.

Compared to our fixed–effects regression in section 4.1, which eliminates endogeneity

by controlling for unobserved firm characteristics via the fixed–effects, this instrumental

variable approach also controls for endogeneity due to the time–varying component of the

error term. Moreover, the three–stage least squares regression method allows for correla-

tion of the disturbances of the two equations, which increases efficiency compared to the

two–stage least squares regression method.

Table 3 displays the regression results. The first structural equation explains firm

performance. In this equation managerial ownership is instrumented by its lag, the lag of

relative performance, the number of managers holding ownership stakes, the number of

external owners, the number of bank relationships, the riskiness of the firm, the size and

various year dummies. We also included quadratic terms for the lagged share variable and

the relative performance variable. Risk is included in a polynomial form of third order.

The same holds for the instrumentation of the quadratic term of managerial ownership.

The second equation explains managerial ownership. We use the same set of instru-

ments as in the first structural equation to instrument relative performance and its square.

For the performance equation the panel structure of the data set is taken into account

by using fixed–effects (see Baltagi, 1995: 113ff.).16

16As is described by Baltagi (1995), one has to eliminate the fixed effects by generating deviations from

firm–specific means for all variables. In the first step one regresses the mean deviation of the endogenous

regressors on the mean deviation of the instruments. The second step is a regression of the mean deviation

21

These estimations with instrumental variables (IV) confirm our previously derived

results although the coefficients of some regressors increase considerably.

The effect of managerial ownership on firm performance still has the form of an inverted

“U”, with the maximum point lying at around 80 per cent managerial ownership share.

The signs of the other regressors remain unchanged.

The single equation results of the share equation are also confirmed. Relative per-

formance in the first as well as in the second order has a positive effect on managerial

ownership. This means that managers hold higher stakes in better performing companies.

The effect of firm risk on managerial ownership share has a polynomial functional form,

with share first decreasing with risk, then increasing and finally decreasing again. The

signs of the other regressors also remain unchanged compared to the results in table 2.

Although IV estimates are usually seen as the main method of dealing with endoge-

nous explanatory variables, their application should be carried out cautiously because

weak correlation of the instruments with the endogenous explanatory variables leads to

inconsistency in IV estimates, even if the sample size is relatively large (Bound et al.,

1995). The authors emphasize the importance of examining the “first stage” estimates

which generated the instruments and propose the partial R2 and the F statistic of the

regressions of the first stage as useful indicators of the quality of the IV estimates.

In table 3, we report the partial R2 and the F statistics of the regressions for the instru-

ments of the first stage. Although comparable results are lacking, a partial R2 of around

25 per cent for the share instruments seems to be quite good. The reported F statis-

tics for the share instruments are highly significant. The statistics for the performance

instruments are weaker, however.

It is hard to say which of the employed estimation techniques is best suited to deal

with the problem of reverse causality. However, since all methods come to the same

conclusion with respect to signs and point of maximum effect, we are confident that these

are correctly identified.

of the dependent variable on the mean deviation of the exogenous and predicted endogenous regressors.

22

Table 3: System Estimation of Managerial Ownership and Performance

Dep. Variable: Relative Performance

share 60.05***

(22.45)

share squared -36.33***

(13.71)

owner man -0.71**

(0.30)

extern 1.23***

(0.45)

bank -0.29***

(0.10)

size -0.91**

(0.37)

Partial R2 for instruments in the first stage 0.25 (share)/ 0.22 (share squared)

F-test for instruments in the first stage, F(8, 1087) 44.13 (share)/ 33.75 (share squared)

Dep. Variable: Managerial Ownership Share

relative performance 0.10***

(0.03)

relative performance squared 0.20***

(0.02)

risk -0.88***

(0.17)

risk squared 1.04***

(0.25)

risk cubed -0.29***

(0.09)

size -0.01

(0.01)

west 0.03

(0.03)

Partial R2 for instruments in the first stage 0.13 (rel. perf.)/ 0.04 (rel. perf. squared)

F-test for instruments in the first stage, F(8, 1087) 21.11 (rel. perf.)/ 5.90 (rel. perf. squared)

Number of observations per equation: 1102

Wald chi2–Test: 47.96 to 6 dof (performance equ.)/ 7859.44 to 20 dof (share equ.)

The performance equation accounts for the panel structure of the data set.

The managerial ownership share equation contains industry dummy variables as well as year dummy variables.

***,**,*=significant on the 1, 5 and 10 per cent level, standard errors are in parentheses

23

5 Conclusion

In this paper, we investigate the relationship between managerial ownership and firm

performance.

We use an unbalanced panel data set of private limited liability firms in the German

business–related service sector. This is the most important legal form in Germany. Up to

now, most studies on corporate governance have concentrated on companies that are listed

on the stock market. However, the distortions caused by the separation of ownership and

control are also present in private limited liability firms.

The main conclusion from our analysis is that ownership does influence company per-

formance. We find a positive effect of managerial ownership share up to around 80 per

cent on firm performance, then the effect becomes negative. Companies that are totally

owned by managers do especially well. Further results show that there is no gain from

monitoring by outside owners. We also find that companies with many bank relationships

do worse, which may be due to the monitoring effect.

We address the question of reverse causality and of endogeneity by estimating lagged

specifications as well as instrumental variable methods. Furthermore, we investigate the

dynamic structure of the panel using the Arellano–Bond GMM estimation technique. The

results of these specifications confirm the previous findings.

With respect to the determinants of managerial ownership, we find that the influence

of the risk of the firm’s business on managerial ownership share is non–linear. Managers

in risky companies can use the ownership stake to signal the quality of their company

to the market. Without this signal it would be more difficult to attract outside funding.

However, the relationship is also partly negative, indicating that risk-averse managers

prefer to diversify their assets.

Since company performance and managerial ownership influence each other, we also

estimate a simultaneous equation system with lagged endogenous variables as instruments.

The results from the single equation specifications are qualitatively confirmed.

24

6 Appendix

Table A1: Turnover Accounted for by Different Legal Forms of Enterprise (in

per cent of overall turnover)

Type of legal form 1972 1986 1990 1998

AG 19.1 21.2 20.2 21.5

GmbH 17.1 25.5 29.1 32.0

OHG 6.8 6.8 6.1

KG 24.0 23.9 22.4

Sole proprietor 23.8 15.4 14.9 13.3

Other a 7.9 7.2 5.1 4.7

Notes: a Includes publicly-owned enterprises and cooperatives.AG’s are companies that are allowed to issue shares. They may or may not be listed on a stock market.The OHG is a private company that has several owners with unlimited liability. The KG has at least oneowner with unlimited liability and at least one owner with limited liability. A sole proprietor is a singleowner with unlimited liability.

Source: Statistisches Bundesamt, 1972 to 1998.

Table A2: The Business–Related Service Sector

Sector WZ 93

Computer Services 72100, 72201–02, 72301–04, 72601–02, 72400

Tax Consultancy & Accounting 74123, 74127, 74121–22

Management Consultancy 74131–32, 74141–42

Architecture 74201–04

Technical Advice & Planning 74205–09, 74301–04

Advertising 74844, 74401–02

Vehicle Rental 71100, 71210

Machine Rental 45500, 71320, 71330

Cargo Handling & Storage 63121, 63403, 63401

Waste and Sewage Disposal 90001–07

Note: The WZ93 industrial classification code is a classification system developed by the German FederalStatistical Office in accordance with the European NACE Rev. 1 standard that classifies economic unitsaccording to their sector of concentration.

25

Table A3: Distribution of Observations and Number of Firms

Sector No. of Observations No. of Firms

Computer Services 337 161

Tax Consultancy & Accounting 275 144

Management Consultancy 265 127

Architecture 420 208

Technical Advice & Planning 405 171

Advertising 263 132

Vehicle Rental 225 113

Machine Rental 211 106

Cargo Handling & Storage 185 87

Waste and Sewage Disposal 211 102

Total 2797 1351

Table A4: Summary Statistics of Variables

Variable Mean Std. Dev. Minimum Maximum

relative performance -0.10 1.44 -4.75 4.50

share 0.73 0.31 0.00 1.00

d sh100 0.45 0.50 0.00 1.00

owner man 1.58 0.87 0.00 11.00

extern 4.63 2.47 2.00 30.00

bank 1.41 0.73 1.00 6.00

age 11.97 8.05 1.00 87.00

size 3.04 1.07 0.00 7.56

west 0.69 0.46 0.00 1.00

risk I 0.54 0.30 0.00 1.41

risk II 0.54 0.51 0.00 2.00

26

Graph A1: Functional Form of the Influence of Managerial Ownership Share

on Performance (dummies in 10 per cent intervals, 95 per cent confidence bands

indicated)

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

0 10 20 30 40 50 60 70 80 90 100

Share

Coe

ffici

ent o

f Dum

my

Graph A2: Functional Form of the Influence of Managerial Ownership Share

on Performance (dummies in 20 per cent intervals, 95 per cent confidence bands

indicated)

-1.5

-1

-0.5

0

0.5

1

1.5

0 10 20 30 40 50 60 70 80 90 100

Share

Coe

ffici

ent o

f Dum

my

27

Graph A3: Impact of Changes in Managerial Ownership Share on Firm Per-

formance (lag specification)

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

0 10 20 30 40 50 60 70 80 90 100

Share

Perfo

rman

ce

Graph A4: Functional Form of the Influence of Risk I on Managerial Owner-

ship Share (95 per cent confidence bands indicated)

0.4

0.6

0.8

1

1.2

1.4

1.6

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1 1.1 1.2 1.3 1.4

Risk Value

Coe

ffici

ent o

f Dum

my

28

References

Aghion, P. and P. Bolton (1989), The Financial Structure of the Firm and the Problem

of Control, European Economic Review 33, 286–293.

Aghion, P. and P. Bolton (1992), An Incomplete Contract Approach to Financial Con-

tracting, Review of Economic Studies 59, 473–494.

Ang, J.S., R.A. Cole, and J.W. Lin (2000), Agency Costs and Ownership Structure,

Journal of Finance 55, 81–106.

Arellano, M. and S. Bond (1991), Some Tests of Specification for Panel Data: Monte

Carlo Evidence and an Application to Employment Equations, Review of Economic

Studies 58, 277–297.

Baltagi, B.H. (1995), Econometric Analysis of Panel Data, Chichester.

Bennedsen, M., M. Fosgerau, and D. Wolfenzon (2000), Control Dilution and Distribution

of Ownership, Copenhagen Business School Working Paper 16-2000, Copenhagen

Berle, A.A. and G.C. Means (1932), The Modern Corporation and Private Property, New

York.

Bound, J., D.A. Jaeger, and R.M. Baker (1995), Problems with Instrumental Variables

Estimation when the Correlation Between the Instruments and the Endogenous

Explanatory Variable is Weak, Journal of the American Statistical Association 90,

443–450.

Demsetz, H. (1983), The Structure of Ownership and the Theory of the Firm, Journal

of Law and Economics 26, 375–391.

Demsetz, H. and K. Lehn (1985), The Structure of Corporate Ownership: Causes and

Consequences, Journal of Political Economy 93, 1155–1177.

Harris, M. and A. Raviv (1991), The Theory of Capital Structure, The Journal of Fi-

nance 46, 297–355.

Harhoff, D. and K. Stahl (1995), Unternehmens- und Beschaftigungsdynamik in West-

deutschland: Zum Einfluß von Haftungsregeln und Eigentumerstruktur, ifo Studien,

17–50.

29

Harhoff, D. and T. Korting (1998), Lending Relationship in Germany–Empirical Evi-

dence from Survey Data, Journal of Banking and Finance 22, 1317–1353.

Hass, H.-J. (1995), Industrienahe Dienstleistungen: Okonomische Bedeutung und poli-

tische Herausforderung, Beitrage zur Wirtschafts- und Sozialpolitik 223, 3–39.

Himmelberg, C.P., R.G. Hubbard, and D. Palia (1999), Understanding the Determi-

nants of Managerial Ownership and the Link Between Ownership and Performance,

Journal of Financial Economics 53, 353–384.

Holmstrom, B. (1979), Moral Hazard and Observability, The Bell Journal of Economics

10, 74–91.

Januszewski, S., F.J. Koke and J.K. Winter (1999), Product Market Competition, Cor-

porate Governance and Firm Performance: An Empirical Analysis for Germany,

ZEW Discussion Paper No. 99-63, Mannheim.

Jensen, M. and W.H. Meckling (1976), Theory of the Firm: Managerial Behavior, Agency

Costs, and Ownership Structure, Journal of Financial Economics 3, 305–360.

Jensen, M. and K.J. Murphy (1990), Performance Pay and Top-Management Incentives,

Journal of Political Economy 98, 225–264.

Kaiser, U., M. Kreuter, and H. Niggemann (2000), The ZEW/Creditreform Business

Survey in the Business–Related Services Sector: Sampling Frame, Stratification,

Expansion and Results, ZEW Discussion Paper No. 00-22, Mannheim.

Kaplan, S.N. (1994a), Top Executives, Turnover, and Firm Performance in Germany,

Journal of Law, Economics, and Organization 10, 142–159.

Kaplan, S.N. (1994b), Top Executive Rewards and Firm Performance: A Comparison of

Japan and the United States, Journal of Political Economy 102, 510–546.

Koke, J. (2000), Control Transfer in Corporate Germany: Their Frequency, Causes and

Consequences, ZEW Discussion Paper No. 00-67, Mannheim.

Kole, S.R. (1995), Measuring Managerial Equity Ownership: A Comparison of Sources

of Ownership Data, Journal of Corporate Finance 1, 413–435.

30

Leland, H.E. and D.H. Pyle (1977), Informational Asymmetries, Financial Structure,

and Financial Intermediation, Journal of Finance 32, 371–387.

Mayer, C.P. (1990), Financial Systems, Corporate Finance, and Economic Development,

in: Hubbard, R.G. (ed.), Asymmetric Information, Corporate Finance, and Invest-

ment, Chicago, 307–332.

McConnell, J.J. and H. Servaes (1990), Additional Evidence on Equity Ownership and

Corporate Value, Journal of Financial Economics 27, 595–612.

Mehran, H. (1995), Executive Compensation Structure, Ownership, and Firm Perfor-

mance, Journal of Financial Economics 38, 163–184.

Morck, R., A. Shleifer and R.W. Vishny (1988), Management Ownership and Market

Valuation: An Empirical Analysis, Journal of Financial Economics 20, 293–315.

Nickell, S., D. Nicolitsas and N. Dryden (1997), What makes Firms perform well?, Eu-

ropean Economic Review 41, 783–796.

Ofek, E. and D. Yermack (2000), Taking Stock: Equity-Based Compensation and the

Evolution of Managerial Ownership, The Journal of Finance 55, 1367–1384.

Statistisches Bundesamt (1998), Finanzen und Steuern, Fachserie 14, Reihe 8.

Williamson, O.E. (1985), The Economic Institutions of Capitalism, New York.

Williamson, O.E. (1988), Corporate Finance and Corporate Governance, The Journal

of Finance 43, 567–591.

31

CENTRE FOR ECONOMIC PERFORMANCE Recent Discussion Papers

527 D. Acemoglu J-S. Pischke

Minimum Wages and On-the-Job Training

526 J. Schmitt J. Wadsworth

Give PC’s a Chance: Personal Computer Ownership and the Digital Divide in the United States and Great Britain

525 S. Fernie H. Gray

It’s a Family Affair: the Effect of Union Recognition and Human Resource Management on the Provision of Equal Opportunities in the UK

524 N. Crafts A. J. Venables

Globalization in History: a Geographical Perspective

523 E. E. Meade D. Nathan Sheets

Regional Influences on US Monetary Policy: Some Implications for Europe

522 D. Quah Technology Dissemination and Economic Growth: Some Lessons for the New Economy

521 D. Quah Spatial Agglomeration Dynamics

520 C. A. Pissarides Company Start-Up Costs and Employment

519 D. T. Mortensen C. A. Pissarides

Taxes, Subsidies and Equilibrium Labor Market Outcomes

518 D. Clark R. Fahr

The Promise of Workplace Training for Non-College Bound Youth: Theory and Evidence from Germany

517 J. Blanden A. Goodman P. Gregg S. Machin

Change in Intergenerational Mobility in Britain

516 A. Chevalier T. K. Viitanen

The Long-Run Labour Market Consequences of Teenage Motherhood in Britain

515 A. Bryson R. Gomez M. Gunderson N. Meltz

Youth Adult Differences in the Demand for Unionisation: Are American, British and Canadian Workers That Different?

514 A. Manning Monopsony and the Efficiency of Labor Market Interventions

513 H. Steedman Benchmarking Apprenticeship: UK and Continental Europe Compared

512 R. Gomez M. Gunderson N. Meltz

From ‘Playstations’ to ‘Workstations’: Youth Preferences for Unionisation

511 G. Duranton D. Puga

From Sectoral to Functional Urban Specialisation

510 P.-P. Combes G. Duranton

Labor Pooling, Labour Poaching, and Spatial Clustering

509 R. Griffith S. Redding J. Van Reenen

Measuring the Cost Effectiveness of an R&D Tax Credit for the UK

508 H. G. Overman S. Redding A. J. Venables

The Economic Geography of Trade, Production and Income: A Survey of Empirics

507 A. J. Venables Geography and International Inequalities: the Impact of New Technologies

506 R. Dickens D. T. Ellwood

Whither Poverty in Great Britain and the United States? The Determinants of Changing Poverty and Whethe r Work Will Work

505 M. Ghell Fixed-Term Contracts and the Duration Distribution of Unemployment