about prasac 2 · about prasac 2 vision and mission ... about prasac 3 4 6 7 8 11 vision and...

TRANSCRIPT

ABOUT PRASAC 2Vision and Mission ______________________________________________3

Background ____________________________________________________4

Our Challenges _________________________________________________6

Business Objectives ______________________________________________7

Clients and Client Highlights ______________________________________8

Financial Products and Eligible Criteria ___________________________ 11

OWNERSHIP AND GOVERNANCE 12Organizational Structure _______________________________________ 13

Shareholders _________________________________________________ 14

Board Committee _____________________________________________ 15

Board of Directors ____________________________________________ 16

Management _________________________________________________ 18

OPERATIONAl HIGHlIGHTS 22Remark From Chairman _______________________________________ 23

Remark From General Manager _________________________________ 25

Financial Performance Highlights ________________________________ 28

Operational Highlights _________________________________________ 30

Staffing and Capacity Building __________________________________ 32

Internal Control and Risk Management ___________________________ 34

Marketing and Social Activities _________________________________ 36

AUDITED FINANCIAl STATEmENTS 40Report of the Board of Directors ________________________________ 41

Report of the Independent Auditors ______________________________ 46

Balance Sheet ________________________________________________ 47

Income Statement ____________________________________________ 48

Statement of Changes In Equity _________________________________ 48

Statement of Cash Flows _______________________________________ 49

CONTACT US 50Office Network with Contact Address _____________________________ 51

Outreach Highlights with Operational Map _________________________ 62

1

2

ABOUT PRASAC

3

4

6

7

8

11

VISION

AND

MISSION

BACKGROUND

OUR

CHALLENGES

BUSINESS

OBJECTIVES

CLIENTS

AND

CLIENT HIGHLIGHTS

FINANCIAL

PRODUCTS

AND

ELIGIBLE CRITERIA

3

To improve the living standards of the rural people contributing to sustainable economic development by being a financially viable microfinance institution.

To provide sustainable access to financial services for rural communities and micro-enterprises.

VISION

mISSION

4

BACKGROUND

PRASAC was a former credit component of

PRASAC’s project funded by the European Union

and implemented by three ministries of the Royal

Government of Cambodia.

The project started in 1995 to rehabilitate and

support agricultural sector in six provinces around

Phnom Penh i.e. Kompong Cham, Kompong Chhnang,

Kompong Speu, Takeo, Prey Veng, and Svay Rieng.

PRASAC’s project phased out in December 2003.

To ensure the access to financial services to rural

communities and micro-enterprises,PRASAC’s

Project Steering Committee made a strategic

decision to transform its credit component into a

licensed MFI. In March 2002, the transformation

was started by creating PRASAC Credit Association

as credit operator registered with the National Bank

of Cambodia (NBC).

In 2003, a trust fund called Cambodia Rural

Development Foundation (CRDF) and PRASAC

Staff Company were established to facilitate

the transformation. With two initial shareholders,

PRASAC was established by registering with the

Ministry of Commerce as a private limited liability

company in August 2004 and got its license from the

NBC in November 2004 to legally provision financial

services to rural communities and micro-enterprises.

To finalize its transformation, PRASAC started to

identify and negotiate with investors since 2005

in order to replace the temporary shareholders

i.e. CRDF. In 2007, PRASAC completed its

transformation by replacing CRDF with new five

shareholders such as BIO (Belgian Investment

Company for Developing Countries), DGC (Dragon

Capital Group Limited), FMO (The Netherlands

Development Finance Company), LOLC (Lanka

ORIX LEASING Company Ltd), and Oikocredit.

Particularly, PRASAC received a permanent license

from NBC in December 2007.

5

mIlESTONE

1995 - 1999: PRASAC I, three EU funded rural

development projects in six provinces, with three

different credit components.

2000 - 2003: Extension as PRASAC II, combined to

one project, one credit component.

2000: First strategic decision to create a sustainable

institution beyond the closure of PRASAC II

project.

2001: HO and branch offices separated from

PRASAC II, with separate management but still as a

part of the project.

2002: Creation of PCA (PRASAC Credit Association),

registered with the NBC in March 2002 as Rural

Credit Operator.

2003: Two initial shareholders were created, a Trust

Fund called CRDF created by PRASAC II and

PRASAC Staff Company created by staff members.

2004: Registered as PRASAC MFI Ltd with

Ministry of Commerce as a private limited liability

company and received license from NBC.

2005: The credit fund was transferred from EC to

the government and finally to PRASAC MFI Ltd as

Subordinated Debt.

2006: The commercialization process was to seek for

equity investment participation from commercial and

social investors.

2007: PRASAC completed its transformation by

replacing CRDF with new five shareholders, BIO,

DGC, FMO, LOLC, and Oikocredit. And, PRASAC

received a permanent license from NBC in December

2007.

2008: PRASAC increased its capital to 15 billion

riels from six shareholders. PRASAC was extending

its financial services throughout the country.

2009: PRASAC selected Oracle FLEXCUBE

Universal Banking to modernize its MIS to build

competitive advantages, offer more diversified ranges

of products and prepare for the next level.

6

OUR CHAllENGES

1. To continue serving the rural poor under high

professional and moral standards implementing

transparency and good governance on all

operational levels

2. To enforce credit discipline among staffs

and clients by strengthening internal control

system

3. To diversify loan portfolio and review financial

products and services to be competitive and suit

clients’ demands, and to look for external

funding to safeguard funds and plan expansion

7

The business objectives of the Company are to carry out

activities of microfinance by providing financial

services to rural households and small and medium

enterprises, such as:

Credit services in the form of group and 1.

individual loans

Savings and money transfer services2.

To raise funds or borrow money in such manner 3.

as the company shall think fit and to secure the

repayment of any money borrowed, raised or

owed to creditors

Do all such other things as incidental or which 4.

the Company may think fit and conducive to the

attainment of the above objectives.

The objectives shall be achieved by strict adherence of

high professional and moral standards, transparency,

and good governance.

BUSINESS OBJECTIVES

8

a. PRASAC’s Client:

Rural Community

Clients are the rural village households that have

repayment capacity residing in rural areas

outside the urban areas of all provincial towns.

Microenterprise

Clients are microenterprises that have number of

employees less than 11 and or assets less than

USD50,000.

ClIENTS AND ClIENT HIGHlIGHTS

9

b. Client Highlight:

MRS. DAM TOCH, 35, Raising Pig, Kampong

Speu

MRS. DAM TOCH, 35 years old, is PRASAC’s

client who is successfulin her business with

PRASAC’s loan. Presently, she is living in Sdok

Slart village, Phnom Touch commune,Udong

district, Kampong Speu province. She spends

most of her daily time on raising pigs

and doing housework. She and her husband,

MR. SENG THAN, a wine producer, wanted

to raise more pigs to extend their business.

After getting advice from their sister, they

decided to request for USD 2,000 loan for 21

months from PRASAC to support their limited

capital. After selling some pigs, Mrs. Dam Toch

had got better living standards and was able

to repair her house and buy more furniture.

MRS. DAM TOUCH becomes our potential

client; she repays regularly and will pay-off soon.

She said with smiling face and hope that, “I’m

really thankful to PRASAC that always provides

me both financial supports and motivation and

advice to do business so that I can get more

incomes.”

SORN SOKHA, 38, Cake Baker, Pursat

MRS. SOKHA, 38 years old, a cake baker

living in Bambekleach village, Roleab commune,

Sampov Meas district, Pursat province,

described her business story that she’s been

baking egg-powder cake for four years. Previously,

her business was not running well due to the

shortage of capital. Later , after discussing with

her husband, in 2008 she decided to request for

USD 5,000 loan for 24 months from PRASAC

to buy more equipment and materials for

baking the cake. After seeing that her business

getting better with PRASAC’s loan, recently, she

was able to pay-off and request for USD 4,800

loan from PRASAC for the second time to buy

an electronic oven so that she can increase her

productivities to respond to her clients’ needs.

MRS. SOKHA said that, “I am very happy

that my business goes well. I also would like to

thank to PRASAC that provided me financial

resource to extend my business. Moreover, what

I like the most is that PRASAC staffs are friendly

and polite, and the loan assessment is also easy

and fast; that is the reason why I can trust in

PRASAC.”

10

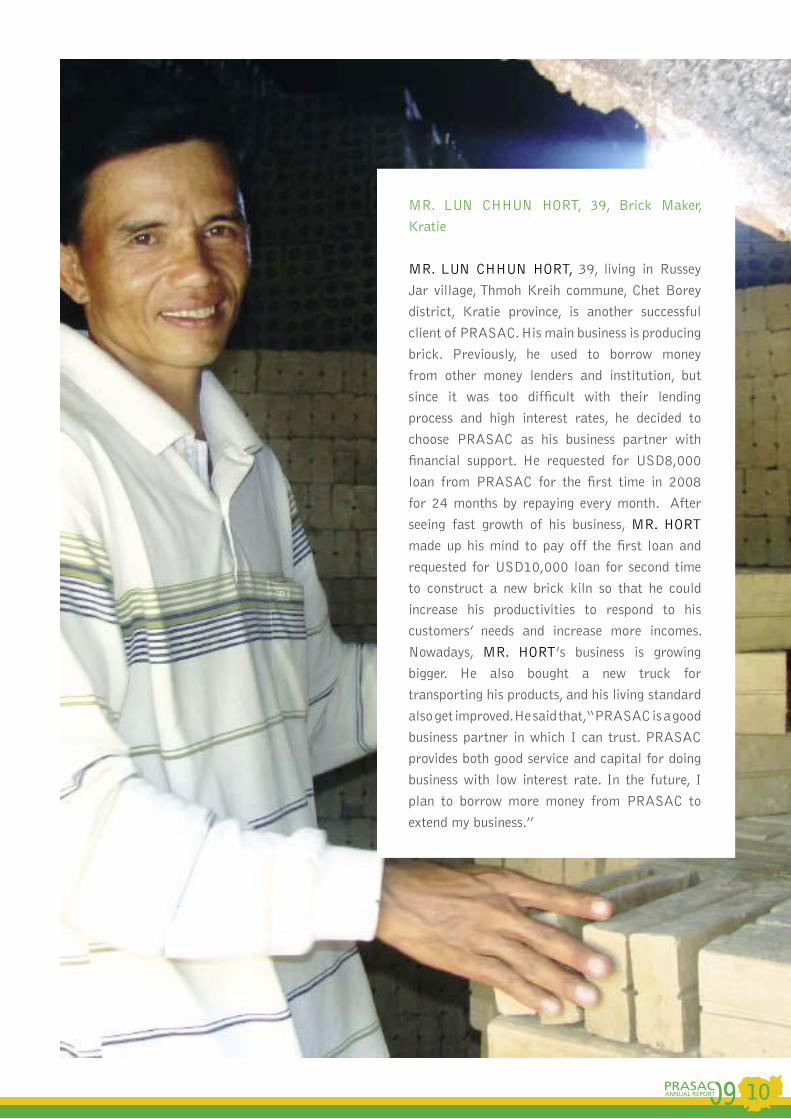

MR. LUN CHHUN HORT, 39, Brick Maker,

Kratie

MR. LUN CHHUN HORT, 39, living in Russey

Jar village, Thmoh Kreih commune, Chet Borey

district, Kratie province, is another successful

client of PRASAC. His main business is producing

brick. Previously, he used to borrow money

from other money lenders and institution, but

since it was too difficult with their lending

process and high interest rates, he decided to

choose PRASAC as his business partner with

financial support. He requested for USD8,000

loan from PRASAC for the first time in 2008

for 24 months by repaying every month. After

seeing fast growth of his business, MR. HORT

made up his mind to pay off the first loan and

requested for USD10,000 loan for second time

to construct a new brick kiln so that he could

increase his productivities to respond to his

customers’ needs and increase more incomes.

Nowadays, MR. HORT’s business is growing

bigger. He also bought a new truck for

transporting his products, and his living standard

also get improved. He said that, “PRASAC is a good

business partner in which I can trust. PRASAC

provides both good service and capital for doing

business with low interest rate. In the future, I

plan to borrow more money from PRASAC to

extend my business.”

11

FINANCIAl PRODUCTS AND ElIGIBlE CRITERIA

a. Financial Products

Group Loan: Group loan is used in which the group members

are self-selected between 2 to 5 members with

one group leader. Each member can borrow

amount of money ranging from

KHR 50,000 to KHR 1,000,000

or

USD 15 to USD 250

within 12 months loan period.

Individual Loan: The target clienteles are micro and small

enterprises. The clients can borrow either in

Riel or Dollar with the amount ranging from

KHR 300,000 to KHR 100,000,000

or

USD 75 to USD 25,000

with the period up to 26 months. The monthly

interest rate is 2.7% to 1.6%.

b. Eligible Criteria

Group Loan: - Group member: 2-5 members, and one is

selected as a group leader

- One member from each

household

- Permanent residents in the

village

- Similar loan purposes

(not homogeneous)

- Age between 18 – 65 years

Individual Loan: - Permanent resident

in the village

- Aged between 18 – 65 years

- Have/show profitable business

- Contribute 20% of their own capital into

the business activity

- Have physical collateral and

personal guarantee

12

13

14

1516

18

OWNERSHIP AND GOVERNANCE

ORGANIZATIONAL

STRUCTURE

SHAREHOLDERS

BOARD

COMMITTEE

BOARD OF

DIRECTORS

MANAGEMENT

13

ORGANIZATIONAl STRUCTURE

BIO is a member of EDFI, the Association of European Development Finance Institutions. BIO participates in

European Financing Partners / EFP, a co-financing facility established by ten of the EDFI-members. Its purpose

is to facilitate the financing of private sector projects in the ACP states in collaboration with the European

Investment Bank.

Dragon Capital Group (DCG) is a diversified investment banking institution offering traditional financial

products and services with an exclusive focus on Vietnamese capital markets. The firm is known both within

Vietnam and international financial circles as one of the premier Vietnam focused financial institutions. Dragon

Capital Group serves the investment banking needs of international and domestic businesses to enable them to

realize their investment goals in Vietnam.

The Netherlands Development Finance Company (FMO) supports the private sector in developing countries

and emerging markets in Asia, Africa, Latin America and Central and Eastern Europe. We do this with loans,

participations, guarantees and other investment promotion activities. Lanka Orix Leasing Company strives to

deliver financial services to its customers with both corporate and rural grass roots level, in every region where it

operates in Sri Lanka. Since its inception in 1980, it has been working with small and medium size entrepreneurs,

which represents over 80% of its client portfolio. The Company innovates continuously in providing adapted

financial solutions such as leasing products, factoring services, savings and deposit products, small loans and

insurance broking services.

Lanka Orix Leasing Company strives to deliver financial services to its customers with both corporate and rural

grass roots level, in every region where it operates in Sri Lanka. Since its inception in 1980, it has been working

with small and medium size entrepreneurs, which represents over 80% of its client portfolio. The Company

innovates continuously in providing adapted financial solutions such as leasing products, factoring services,

savings and deposit products, small loans and insurance broking services.

Oikocredit started as a pioneer in the field of development financing. Today, it is one of the largest financiers

of the microfinance sector worldwide. Oikocredit is one of the few ethical investment funds, which finances

development projects in the South benefiting disadvantaged and marginalized people. Privately owned, Oikocredit

is a unique cooperative society, which encourages investors to invest their funds in a socially responsible manner.

PRASAC Staff Company (PSCo.) was established under the law and general provisions of Kingdom of Cambodia

and has the following objectives: To make equity investments in PRASAC MFI Ltd and to manage the

investments in accordance to high moral and professional standards, with transparency and good governance.

The company might be engaged in any other capital and asset management, investment and trading and other

financial or other activities and services which relate directly or indirectly to the above objectives or similar

purposes, and are characteristic of the development of the company’s operations.14

SHAREHOlDERS

The share capital of the Company as at December

2009 was KHR 15 Billion (Fifteen billion Khmer

Riel) distributed among the five shareholders 18%

each BIO, Dragon Capital Group (DCG), The

Netherlands Development Finance Company (FMO),

Lanka Orix Leasing Company (LOLC), Oikocredit,

and 10% for PRASAC Staff Company (PS Co.).

SHAREHOLDERS % SHAREHOLDING

BIO 18%

DCG 18%

FMO 18%

LOLC 18%

Oikocredit 18%

PSCo 10%

15

BOARD COmmITTEE

Board of Director Committee:

With full capacity of the Board of Directors, the two initial committees were created in order to support the

management in operations.

Audit Committee:

The audit committee comprises of two Board of Directors, i.e. Mr. Michael Temple and Mr. Ranjit Fernando

and Internal Audit Department Manager. The duties of the audit committee are to review the report of the

internal and external audit reports, monitor the integrity of the financial statements, compliance of the

policies and procedures, review the internal control system and risk management of PRASAC, and provide

recommendations for implementation. In addition, the non-executive members will meet the external

auditors twice a year i.e. in September before the external audit starts and in March after the completion of

the external audit assignment. The committee will meet at every three months.

HR and Remuneration Committee:

The key role of this committee is to evaluate the performance of the top management and determine

remuneration for the top management. The committee is composed of Mr. Stefan Harpe and Ms. Anne

Demeuse.

16

MR. MICHAEL TEMPLE,

Director, Chairman of the Board, Representative of DCG

MICHAEL was educated in both Hong Kong and Scotland and joined the HSBC

Group as an International Manager in 1977. He worked for HSBC in a number of

areas primarily in the corporate banking and risk management in Germany,

Brunei, Hong Kong, India, Indonesia, Bahrain and Vietnam. His last role in the

HSBC Group was Chief Operating Officer in Vietnam where he worked for 6 years.

He was also the project leader in evaluating the potential of Vietnam as a site for

an HSBC Data Processing and Call Center site. He’s retired from the HSBC Group

in 2005 and became a Director of Dragon Capital, a UK based Investment Bank

and Fund Management Company whose main focus of business is in Vietnam. He

is the Group COO and is part of the committee that evaluates the Groups private

investments. PRASAC is the Dragon Capital Groups’ first investment in Cambodia.

BOARD OF DIRECTORS

MR. STEFAN HARPE,

DIRECTOR, Member of the Board, Representative of Oikocredit

STEFAN is Manager Equity Investments, Oikocredit, Amersfoort, Netherlands;

working with Oikocredit’s local managers in 28 country offices in Africa, Latin

America, Asia and Eastern Europe to manage the private equity investment

portfolio__i) financial (mostly microfinance);__ii) non-financial (businesses with

high development impact);__iii) specialized equity funds. Oikocredit is a global

development finance institution with about € 340 million total assets, funded by

individuals (26,000 shareholders), churches, and institutional investors. While not

profit-maximizing, and balancing dual objectives of development impact and

investment return, Oikocredit is sustainable and generates a healthy surplus on the

total portfolio (loans and equity). Previously, Stefan was Fund Manager, AfriCap

Microfinance Fund, based in, Senegal, and prior to that Director International

Operations, Calmeadow, Toronto, Canada. His formal education includes - MBA,

University of Western Ontario, Canada, and B.Sc (Econ), LSE, England.

MR. ISHARA C. NANAYAKKARA,

Director, Member of the Board, Representative of LOLC

ISHARA is the Deputy Chairman of Lanka ORIX LEASING Company Ltd. He is

the Managing Director of Ishara Traders, the pioneering importer of reconditioned

motor vehicles in Sri Lanka. Having obtained a diploma in Business Accounting

from Australia, he worked in Japan for two years with the largest exporter of

reconditioned motor vehicles Yamagin Corporation, Tokyo. ISHARA is a Director

of Ishara Plantations (Pvt) Ltd, and Ishara Property Development (Pvt) Ltd. Mr. I

C Nanayakkara also serves as a director on the boards of all LOLC subsidiaries.

17

MR. OUM SAM OEUN, DIRECTOR,

Member of the Board, Representative of PSCo.

SAM OEUN used to work as chief accounting officer in Takeo Province commerce

department. Since 1995, he has worked with PRASAC credit program, and he has

attended several training courses related to microfinance operations. He was elected

as Chairman of Board of Director of PRASAC Staff Company (PSCo., Ltd) since

2003, and he was re-elected as the chairman PS Co., Ltd until now. He holds Master

Degree of Business Administration, Bachelor degree in Business Management and

obtained a Diploma in Accounting and Commerce in 1988.

MR. RANJIT MICHAEL SAMUEL FERNANDO,

Director, Member of the Board, Representative of FMO

RANJIT is Team Leader ICT Capacity Building Program, implemented by the

Government of Sri Lanka and funded by the World Bank. He is also a team leader

in consultancy assignment funded by the World Bank for the setting up of the

Housing FinanceCorporation in the Maldives.

He is an expert in Project / SME / Microfinance Financing Specialist, Development

Banking, Legal Aspects relating to credit and Banking, Institutional Development

and Strategic Planning, and Corporate Governance. He holds Attorney at Law

(1st Class Honours), Ceylon Law College, Sri Lanka; Bachelor of Laws (Hons),

University of Sri Lanka; Fellow of the Chartered Institute of Bankers, United Kingdom;

Fellow of the Chartered Institute of Management Accountants, United Kingdom.

MS. ANNE DEMEUSE,

Director, Member of the Board, Representative of BIO

ANNE has been active within BIO nearly since its inception in July 2002. She

initiated BIO’s first investments, mainly in the microfinance sector and SME funds,

and held the position of Senior Investment Officer Asia until the end of 2005. Later

in 2006, she changed to the position of Portfolio Controler, responsible for the

monitoring of BIO’s investments. Before joining BIO, Ms. Demeuse worked in the

banking sector, and more specifically in commercial banking and corporate finance

where she advised for IPOs and trade sale transactions. She also gained audit

experience within Ernst and Young after her graduation. Ms DEMEUSE holds a

degree of Management Engineer from the Solvay Business School.

18

mANAGEmENT

MR. SIM SENACHEERT,

General Manager

SENACHEERT holds Master and Bachelor Degrees in Business Administration

and obtained Diploma in Accounting and Finance in 1994. Since 1995, he has

attended several training courses related to microfinance operations and

management. He is also an accredited Microfinance Training of Trainer certified by

ADBI, TDLC of the WB, and UNCDF. He used to work in banking sector, and he

started working with PRASAC since 1995 as Credit Officer and was promoted to

various positions such as accountant, Branch Manager, MB Trainer and Supervisor,

Finance Manager. From mid 2002, he used to hold positions of Branch Manager,

Operation Manager, and Deputy CEO with another MFI before joining PRASAC as

General Manager in late 2003.

MR. OUM SAM OEUN,

Deputy General Manager, Chief Operations Officer

SAM OEUN accredited Micro Finance Training of Trainer certified by ADBI,

TLDC of the WB, and UNCDF, holding MBA of Banking and FinanceHe obtained

a Diploma in Accounting and Commerce in 1988 and holds a Bachelor degree

in Business Management. He used to work as chief accounting office in Takeo

Province commerce department. Since 1995, he has worked with PRASAC credit

program, and he has attended several training courses related to microfinance

operations. He was promoted as Deputy General Manager of PRASAC MFI in

early 2007.

MR. OUM SOPHAN,

Deputy General Manager, Chief Finance Officer

SOPHAN obtained his Bachelor’s Degree in economics, specializing in banking

and finance from the Royal University of Laws and Economics and holds a Master

Degree in Business Administration from Norton University in 2003.

Before joining PRASAC’s team, Sophan had many years of experience in the field

of accounting, banking, and finance. For instance, he used to hold CFO position at

TPC Microfinance Institution from 2003 to 2008. He worked for the National

Bank of Cambodia in various supervisory positions, including credit, planning, and

accounting from 1981 to 1992. He joined Thai Farmers Bank where he served as

Finance and Accounting Supervisor from 1992 to 2001. He also used to work as

Accounting Manager of various private companies. He is currently holding the

position of deputy general manager, chief finance officer.

19

MR. YANG KIMSRENG,

Finance Manager

KIMSRENG holds MBA in Finance and Banking, BA in the field of Accounting in 2003

and obtained Associates degree Specialized in Banking in 1998 at the Center for

Banking Study. Also,he has more than ten-year experiences with Micro-banker system

as well as finance and banking. Since 1998, he participated in several training courses

related to microfinance. He joined PRASAC in 1998, and he was promoted to be senior

staff in 2001 and to be Deputy Finance Manager in October 2007 and Finance

Manager in April 2008.

MR. NEANG SOKHIM,

Credit Manager

SOKHIM is an accredited Micro Finance Training of Trainer certified by ADBI,

TLDC of the WB, and UNCDF. He holds Master Degree in Business Administration

and obtained bachelor degree of science in Agronomy in 1997, and he studied two

years of BBA. He has attended many courses related to micro finance operations

and other courses.

He started working in micro finance sector in 1998 as Credit officer, and then he

was promoted to be a Junior Internal Auditor, Senior Internal Auditor, Deputy

Operation Manager, Deputy Credit Manager. Currently, he is holding the position

of Credit Manager.

MR. SAY SONY,

Marketing Manager

SONY is an accredited Microfinance Training of Trainer certified by ADBI, TDLC

of the WB, and UNCDF. He holds master of business administration and bachelor

degree in Marketing Management.

Since 2005, he has attended numerous local and international training courses

in Asia and Europe related to micro finance operations, products development,

research and marketing.

He has more than seven-year experiences in project management as well as

marketing coordination in both social and private sector. He joining PRASAC MFI

in early 2005 as chief marketing, he was promoted to be a Marketing Manager of

PRASAC MFI in 2007.

20

MR. OUK SAROEUNG,

Internal Audit Manager

SAROEUNG holds Master degree of Business Administration and obtained a Bachelor

degree in Banking in 1989. Since 1995, he participated in several training courses

both in local and international including in Asia, Africa and Europe related to

Audit, Finance, Management, and Microfinance. He used to work in banking sector.

Also,he worked for the National Bank of Cambodia at Branch Svay Rieng in various

supervisory positions, including credit and planning from 1983 to 1995. He has more

than ten-year experiences in microfinance. He joined PRASAC in 1995; he was

promoted to be Audit Manager in 2003.

MR. LY SOPHEAKTRA,

IT Manager

SOPHEAKTRA holds M.Sc. IT and MBA of Finance & Banking; He obtained

B.Sc. of IT in 2002 and BA of Accounting & Finance in 2001.

Since 2002, he has attended numerous local and international training courses in

Asia and Europe related to IT/MIS technology, Management, and Microfinance.

He has more than eight-year experience in IT/MIS Management, Database Design

& Report Writing, Financial Accounting, and Microfinance operations. Prior to

joining PRASAC, He used to work for a private construction company. He joined

PRASAC in 2002 as MIS Officer, moving on to be senior staff in 2003 as MIS Unit

Manager, and he was promoted to be IT Department Manager in early 2007.

MR. SUM SINATH,

Branch Support Manager

SINATH accredited Microfinance Training of Trainer certified by ADBI, TDLC

of the WB, and UNCDF, obtained associate degree in Accounting and Finance,

bachelor degree in Business Administration and holds Master degree of Business

Administration.

Moreover, he participated in several training course in career development of

Microfinance skills both in local and oversea courses.

He has more than seven-year experiences in Microfinance sector. He joined PRASAC

in 2002 as credit officer; he was promoted to be branch manager, Regional

Manager and was promoted to be Branch Support Manager in early 2007.

21

MR. SOU VANTHAN

Human Resourse Manager

VANTHAN with more than twenty-year experiences in Microfinance and banking

sectors since 1982 from various positions with PRASAC, NBC, and another MFI

such as credit officer, accountant, micro banker and teller, internal auditor and

field supervisor, district bank manager, provincial credit coordinator, vice-credit

department manager, branch manager, area manager, and regional manager.

Vanthan also participated in many training courses such as TOT Principles of MFIs

and Delinquency Management certified by CGAP & EDA Rural Systems Pvt Ltd,

staff supervision and motivation, Goal Oriented Project planning and other training

courses. Vanthan is a rare resource with deep root of experiences in human

resource management and aspects especially for microfinance institution. Based on

his commitment and management skill, he was promoted from a low level status

to a highly-recognized and appreciative position, and he is currently holding the

position of Human Resourse Manager of PRASAC, standing as a good model for

other staffs.

22

23

25

28

30

32

34

36

OPERATIONAl HIGHlIGHTS

REMARK

FROM

GENERAL

MANAGER

REMARK

FROM

CHAIRMAN

FINANCIAL

PERFORMANCE

HIGHLIGHTS

OPERATIONAL

HIGHLIGHTS

STAFFING

AND

CAPACITY

BUILDING

INTERNAL

CONTROL

AND RISK

MANAGEMENT

MARKETING

AND

SOCIAL

ACTIVITIES

23

REmARK FROm CHAIRmAN

2009 was a challenging year for Cambodia, as it was for all economies around the world. The country

encountered economic slowdown and GDP growth was estimated to be stagnant at 0%. The slowdown impacted

all the main sectors of the economy including agriculture, garments and tourism. However, in late 2009 positive

signs emerged with agribusiness export more than doubling, year-on-year air tourist arrival stop declining, and

domestic credit and inflow of foreign direct investment began to bounce back. The government also started to

diversify the export market. Economic growth in 2010 is forecast to reach around 4%.

By anticipating the impact of the global economic downturn early, more stringent measures were put in place

to screen out unqualified clients as much as possible to ensure that we provided credit only to existing and

established clients so that we were able to manage the risks for ourselves and our clients. Portfolio quality took

priority over portfolio growth. As a result, in spite of turbulent economic environment, PRASAC’s Portfolio at

Risk was the lowest among major microfinance institutions in Cambodia, even though the number of clients

decreased. Though there has been some improvement in the economic environment, the current issues in the

international market place means that we will have to continue in our vigilance and though we anticipate

PRASAC increasing its loan portfolio this year it will not be as rapid growth as previously.

One of the major issues that came out of the economic environment in 2009 was over indebtedness. This has

caused a general rise in the MFI sectors PAR figures and is a concern. PRASAC together with the Cambodian

Microfinance Association is discussing ways that this can be managed with the National Bank Of Cambodia until

such a time the proposed Credit Bureau is up and running.

24

To serve more clients and reduce costs for the clients, we have expanded into new areas by opening new offices.

To be a more responsible lender, to improve client satisfaction and loyalty, reputation and brand value, PRASAC

also established “Client Protection Policy”, which educates our staff on ethical behavior in dealing with clients.

In addition to the office network expansion and the strict measures to maintain good quality of loan

portfolio, efficiency and productivity remain a major challenge. In 2009, the implementation of the new

Flexcube Core Banking system started and it proved to be a challenging task. Our staffs have worked hard in

setting up the new system, and a lot of training courses were conducted on the new software. We believe that this

new technology base will allow the company to further grow and enhance its products and service, and enhance

customer satisfaction. We anticipate switching over to this new system by the end of 2010.

Founded in 1995 as a small rural project, and transformed into a financially viable commercial company

offering microfinance services, PRASAC currently operates through 134 offices and growth in offices will

continue as we move into new provinces and areas. PRASAC has a long history of investing in our

communities through charitable contributions, sponsorships, and workplace giving. PRASAC has sponsored

public events or organizations relating to improving microfinance practice in Cambodia. PRASAC aimed

to be a sustainable company that conducts its business in ways that benefits extend naturally to all

stakeholders, including employees, customers, business partners, the communities in which it operates, and, of

course, shareholders. We believe that our business operation is not only profitable, but also sustainable. We are

currently looking at various options to give back to the communities where we operate and the focus of this will be

finalized with the Board by the middle of 2010.

Our past is defined by adherence to our core values. Our future will be determined by the same commitment to

these values and the solid execution of our strategies.

On behalf of the Board of Directors of PRASAC MFI, I wish to thank PRASAC’s management and staffs for

their hard work and dedication to our customers. I also wish to thank Board of Directors, shareholders,

customers, suppliers, the Royal Government of Cambodia, and especially the National Bank of Cambodia for their

continued support and advice.

MICHAEL A. TEMPLE,

Chairman

25

From financial year 2004 to 2008 were considered as good period which allowed PRASAC to expand its

operations and grow portfolio rapidly from USD6.6 Million to USD60.0 Million by end of 2003 and 2008

respectively. But, due to the global financial crisis and the economic downturn, the operations of PRASAC during

2009 were also affected and it was considered as a difficult period which we had never faced this kind of difficult

external environment during the past five years. Although, we could not escape from the impacts of the global

financial crisis and economic downturn, but we still could manage our operations with remarkable achievements.

And the followings are the highlights of our achievements.

From January to September of 2009, loan portfolio was lower than 2008 portfolio and the disbursement

was slowdown impacted by several factors such as global financial crisis, economic downturn, the multiple

loans / overlapping loans with other MFIs, decrease of portfolio quality, and so on. But the portfolio started

picking up again during the last quarter of 2009 and as a result portfolio growth by 11% to KHR267 Billion

from KHR240 Billion by end of 2009 and 2008 respectively. Portfolio in agricultural decreased from 37% in

2008 to 29% in 2009 while portfolio in trading increased from 33% to 36% and personal loans increased from

12% to 14% at end of 2008 and 2009. The portfolio in agriculture sector was decreased due to the decrease

of group loans. During 2009, in order to avoid overlapping loans, group loan disbursements were reduced. As

part of our social objectives by cooperation with the National Biodigester Project (NBP), we also provided 1213

loans (about USD700,260) to the farmers for renewable energy in 2009 in accumulated there were 2,559 loans

provided to this purpose since November 2007 to December 2009 and PRASAC also contract with ECOSORN

in order to contribute to poverty reduction through the improvement of physical access to financial services such

as credit and savings. PRASAC reaching 13,962 beneficiaries, in which 4,577 borrows, 3,248 savers with

KHR2,780,975,500 of disbursement from November 2007 to December 2009 and PRASAC have established

19 offices in these three provinces ( Siem Reap, Battambang, and Banteay Meanchey ) and operating in 14

districts 40 communes and 91 villages.

REmARK FROm GENERAl mANAGER

26

It was observed that 2009 the portfolio quality of the whole sector was deteriorated due to the

financial crisis, economic downturn, and over indebtedness caused by the overlapping or multiple loans from

different MFIs and banks. Thank to our professional and discipline staffs and our proactive measures we could

maintain our portfolio at-risk ratio below the sector rate. However, our nonperformance loans increased from

0.23% (end of 2008) to 1.66% (end of 2009).

The number of active clients decreased by 12% from 100,116 to 87,945 at the end of 2008 and 2009. The

decrease of number of clients due to the decrease of group loans in order to avoid overlapping loans with other

MFIs during the crisis period. As a result, the group loans decreased by 50% from 19,179 to 9,634 as end of

2008 and 2009. In addition, the individual loans also decreased by 3% in 2009.

Total revenue for 2009 was 12% lower than projections due to the decrease of portfolio and decrease

of interest rate to attract good clients. It increased by 19% compared with 2008. Yield on gross

portfolio decreased from 30.2% to 27% due the increase of larger loans with lower interest rate. The

financial expenses increased by 70% compared with 2008 from 2.6MUSD to 4.5MUSD due to the increase

of borrowing rate during late 2008. The operating increased by 14% and 5.7% higher than projections.

The actual higher than projections caused by the set-up new offices in new area. However, the operating costs

decreased to 13.4% from 15.5% and to 12.5% from 14.8% compared with gross portfolio and total assets

respectively. Net profit was 6% lower than last year. Similar to revenue, the net profit decrease due to slowdown

disbursements and lowering interest rate. Risk coverage ratio decreased from 717% to 128% due to the increase

of non-performing loans during 2009. But, it still could cover this risk. The equity increased by 29% and the

capital was still adequate (CAR was 23.6%).

By taking the opportunity of the slowdown period, we spent our resources to strengthen our

institutional capacity such as increase number of offices from 90 (2008) to 116 (2009) in order to increase

clients’ convenience and cut costs to the clients, increased number of staff from 1,024 to 1,246 by end of 2008

and 2009, selection and implementing new core banking system and as a result there were four offices running

new system parallel with the legacy system.

During 2009, the second credit rating was undertook by Microfinanza rating agency (First rating

undertook by the agency) with the rate of BBB+ and stable outlook. At the same time the first social

rating was also undertook by Microfinanza with rate of BB. Although, the rating was not good, but there were

some strengths and opportunities explored by Microfinanza during the rating.

STRENGTHS OPPORTUNITIES

- Ownership structure defined

- Good geographic coverage in the whole country

- Rather good standardization of processes

- Strong and successful relationship with many

stakeholders (donors, investors, technical

assistance providers, etc.)

- Good capitalization

- Expansion into untapped markets of the country

- Transformation into a deposit-taking institution

- Adoption of the new MIS

- Focus on capacity building given the significant

market share

- New financial products such as social loans

(educational, housing products)

27

By adopting the prudential strategy for 2010, PRASAC will not prioritize on portfolio growth, but will

focus on improving portfolio quality, strengthen management and staff capacity, strengthening

management control, rolling out core banking system to all offices, and introducing new services.

Finally, on behalf of management and staff, I would like to express my sincere thanks to all stakeholders that

always support us and hoping that all stakeholders will continue supporting and help developing PRASAC to

become an institution that will continue provide more benefits to all stakeholders.

Sincerely yours,

SIM SENACHEERT,

General manager

28

FINANCIAl PERFORmANCE HIGHlIGHTS

Portfolio per credit officer increased from 91,127USD in 2007 to 111,353USD in 2008 and increase to •

116,384 USD per credit officer in 2009.

Number of active client per credit officer decreased from 189 clients in 2008 to 163 clients in 2009.•

Portfolio at Risk (30days) increased from 0.23% in 2008 to 1.66% in 2009.

The yield on portfolio decreased from 30.2% in 2008

to 27.0% in 2009 .

2007 2008 2009

Exchange rate 4,003 4,081 4,169

Currency USD USD USD

Total loan outstanding 32,988,091 57,950,559 62,730,902

Total Number of CO 362 529 539

Outstanding per CO 91,127 111,353 116,384

Active client 94,555 100,116 87,945

Active client per CO 261 189 163

Portfolio at Risk 0.22% 0.23% 1.66%

Funding costs increased from 5.5% in 2008 to 6.9%

in 2009.

PRODUCTIVITIES AND EFFICIENCy

PROFITABIlITy

140,000

120,000

100,000

80,000

60,000

40,000

20,000

91,127

Outstanding per CO Portfolio at Risk

111,353 116,384

2007 2008 2009

1.80%1.60%1.40%1.20%1.00%0.80%0.60%0.40%0.20%0.00%

300

250

200

150

100

50

Active client per CO

2007 2008 2009

261189 163

30%

31%32%

29%28%27%26%

24%25%

Yield on portfolio

2007 2008 2009

32%30%

27%

6.0%

7.0%

5.0%

4.0%

3.0%

2.0%

0.0%1.0%

Financial Expense Ratio

2007 2008 2009

5.5%

4.4%

6.9%

29

Operating expenses deceased from 14.8% in 2008

to 12.5 in 2009 compared with average total assets.

In order to improve the efficiency, the plan is to

increase the productivity of credit officers (revised

incentive) and offices through the increasing of loan

officers who will work with the clients.

Return on Assets decreased from 5.8% in 2008 to

4.1% in 2009.

Admin Expenses decreased from 5.5% in 2008 to

3.7% in 2009.

12.0%14.0%16.0%

10.0%8.0%6.0%4.0%

0.0%2.0%

Operating Expense Ratio

2007 2008 2009

15.8%14.8%

12.5%

6.0%

5.0%

4.0%

3.0%

2.0%

0.0%

1.0%

Return On Assets (ROA)

2007 2008 2009

6.0% 5.8%

4.1%

6.0%

5.0%

4.0%

3.0%

2.0%

0.0%

1.0%

Administrative Expense Ratio

2007 2008 2009

5.5%

3.7%

5.5%

30

OperatiOnal HigHligHtS

By the end of 2009, the PRASAC’s loan portfolio reached KHR 267,183 million, increased 11.14 percent

over the previous year.

Loan has been classified as group loan and individual loan that can be disbursed in KHR and USD

currency. The group loan represented 2.45 % where as individual loan represented 97.55% of total

portfolio outstanding. The group loan portfolio outstanding decreased by 5.48% with amount of KHR6,816

million and individual loan increased by 11.66 percent with amount of KHR 260,367 million compared to

previous year.

Loan portfolio in KHR currency grew by 1.87 percent with amount of KHR107,569 million and loan

portfolio in USD currency grew by 18.41 percent with amount of KHR159,614 million.

Loan Portfolio (Figures are in KHR Millions)

By the end of 2009, the number of active borrowers was 87,945 a decrease of 12.16 percent compared to

previous year. In term of product types, group loan borrowers decreased by 49.77%, and individual loan

borrowers decreased by 3.24%. In term of gender. Female borrowers increased by 0.56% while male

borrowers decreased by 22.99% compare to previous year.

Key indicatorsDecember December December Changed Changed

2007 2008 2009 Amount %

Total loan portfolio 134,295 240,394 267,183 26,789 11.14%

Portfolio in group loan 5,491 7,267 6,816 (451) -6.21%

Portfolio in individual loan 128,804 233,128 260,367 27,239 11.68%

Portfolio loan in KHR 68,705 105,598 107,569 1,971 1.87%

Portfolio loan in USD(000) 65,590 134,797 159,614 24,817 18.41%

Key indicatorsDecember December December Changed Changed

2007 2008 2009 Amount %

Total Number of Borrower 94,555 100,116 87,945 (12,171) -12.16%

Group Loan Borrowers 27,237 19,179 9,634 (9,545) -49.77%

Individual Loan Borrowers 67,318 80,937 78,311 (2,626) -3.24%

Female 43,555 46,053 46,311 258 0.56%

Male 51,000 54,064 41,634 (12,430) -22.99%

BORROWERS

lOAN PORTFOlIO

31

At the end of 2009, Portfolio at risk ratio was 1.66% and repayment ratio 97.45%. The good loan

portfolio comes from good portfolio monitoring from all staff level, well trained staff, especially, credit

officers, well established credit policy, and procedures and clear loan work out policy. Staff motivation,

such as incentive that link with loan quality is also a tool for maintaining good portfolio quality. Besides

these, the current MIS system can provide data and information that make availability for staffs to monitor

and follow up and analyze portfolio well.

(PAR amount and principal past due is in Millions)

Key indicatorsDecember December December Changed Changed

2007 2008 2009 Amount %

PAR Amount (30days) 296 543 4,437 3,894 717.13%

Principal Past Due 294 413 3,004 2,591 627.36%

PAR Ratio (30days) 0.22% 0.23% 1.66% 1.43% 621.74%

PAR Ratio (30 days) Group Loan 0.90% 0.01% 3.54% 3.53% 35300.00%

PAR Ratio (30 days) individual Loan 0.19% 0.23% 1.66% 1.43% 621.74%

Repayment Ratio 99.30% 99.30% 97.45% -1.85% -1.86%

lOAN PORTFOlIO QUAlITy

By the end of 2009, PRASAC operated in 21 provinces, 131districts, 1,256 communes, and 8,098 villages,

an increase of 4 provinces, 5 districts, 76 communes, 623 villages compared to previous year. In term of office

net work, there were an increase of 3 branches, 13 sub branches, and 12 service offices compared to previous

year.

In 2009, PRASAC disbursed loan with total amount of KHR 346,313 million an increase of 5.69 percent

over previous year. The total number of loans disbursed in 2009 was 88,735 a decrease of 5.69 percent

compared to previous year. The average disbursed loan size was KHR 3.90 million.

Loan Disbursed (Amounts are in KHR Millions)

Key indicatorsDecember December December Changed Changed

2007 2008 2009 Amount %

Total Number of province 14 17 21 4 23.53%

Total Number of District 100 126 131 5 3.97%

Total Number of Commune 941 1,180 1,256 76 6.44%

Total Number of Village 6,210 7,475 8,098 623 8.33%

Key indicatorsDecember December December Changed Changed

2007 2008 2009 Amount %

Total Disbursed Amount 200,602 327,665 346,313 18,648 5.69%

Total Number of Loans Disbursed 89,010 95,732 88,735 (6,997) -7.31%

Avg Loan Amount Disbursed 2.25 3.42 3.90 0.48 14.02%

OPERATION AREA AND BRANCH NETWORK

lOAN DISBURSEmENT

32

- Currently, PRASAC has employed 1,246 staffs

comprised of 967 males and 279 females.

- In 2009, through this figure, we could also say

that PRASAC’s turnover rate was improved since

it was lower than the past years.

PRASAC needs skillful and knowledgeable staffs

that can carry out their tasks and understand

about micro-finance or banking environment.

With this intention, PRASAC has 24 staffs who

hold Associate Degree, 424 Bachelor Degree, and

18 Master Degree. Moreover, most of them are

improving their education background by

pursuing another degree including 14 in Associate

Degree, 417 in Bachelor Degree, 93 in Master

Degree, 4 in CPA and 3 PhD Degree.

To assure the quality of services, PRASAC pays

more attention to staff development and training

since they started their careers with PRASAC.

The in-house trainings are regularly organized

and provided. PRASAC occasionally provides

the chances to many staffs to participate in the

in-country and oversea courses to gain knowledge

of microfinance development in Cambodia

as well as in global contexts, microfinance

management skills, related technical skills and

regulation of National Bank of Cambodia.

STAFFING AND CAPACITy BUIlDING

STAFFING AND EmPlOymENT TREND

STAFF TRAINING AND DEVElOPmENT

1200

1400

1000

800

600

400

0

200

2007 2008 2009

40152 111

413

1024

1246

311

89

722

Turn Over Total StaffRecruitment

As a result, in the year 2009:

- PRASAC trained 332 new staff

- There were 2,461 participants in refreshment

training in which some of them attended more

than one course during this year.

- For oversea courses, participated by 10

professional staff.

33

PRASAC welcomes people who are interested

in joining a diverse, talented, professional, and

extremely committed team. Every position

at PRASAC, from the bottom to the top,

contributes to understanding of vision and

mission. PRASAC gives opportunity for those

who are interested in a career dedicated to the

poverty alleviation and an institute promoting the

transparency, challenging working condition and

working environment; providing fairness and

accuracy benefit package; and fully following or

extra the Labor Law of Cambodia.

PRASAC offers a competitive benefit pacages as

following:

- Competitive Salary and annually increased

- Working days: 5 days or 40 hours / week

- Education support and facilitation

- Bonus during traditional events (Khmer NewYear,

Pchum Ben)

- 18 days of Annual Leave

- Public holiday as determined by AKNUKRET of

the government

- Maternity Leave and allowance

- Variable salary depending on performance

- Severance Pay

- Annual Incentive at year end up to three months

of current salary

- Insurance on Accident & Health Care program

and indemnity payment for all staff

- Non-financial recognition

- And more…

JOB OPPORTUNITy BENEFITS HIGHlIGHT

34

INTERNAl CONTROl AND RISK mANAGEmENT

To minimize the risk factor, PRASAC’s management

has linked Internal Control to risk management. Risk

management is the process of assessment of relative

risk and ensuring that controls are present and

effective. It covers prevention of potential problems

and the early detection of actual problems when they

occur.

Internal Control is a set of integrated methods and

procedures translated into regular and periodic

activities that preserves safety of asset, improves client

service, ensure reliability of financial information

and staff adherence to management policies and

guidelines. PRASAC’s management uses Internal

Control to ensure a system of accountability along

with prevention of errors and irregularities, Internal

Audit department is an independent appraisal

function under the control of the board of the

directors of PRASAC, the audit committee. Internal

auditing is essential for ensuring the operations,

appropriateness of control and ensuring the

reliability and integrity of financial management

system of keeping record and reporting.

Internal Audit department was started in 2001

with a clear roles and responsibilities to improve

the internal control and analysie risk related to the

operations as well as the compliance by producing

accurate reports on time to branch management and

executive management to take actions.

The internal audit reports are issued monthly based

on each branch with recommendations to respond to

the real cases and findings. Additionally, the summary

of significant findings are issued monthly bases to

Audit Committee as well as the management to

understand the current business situation and trends.

At the beginning of the internal audit role, the

internal control policy and procedures have been

developed and updated accordingly and particularly

with professional staff. As at December 2009 the

total staff of internal audit department consist of

one internal Audit manager, one Deputy Internal

Audit manager, three Audit Unit managers one

Senior Auditor and 13 Audit Assistants working in

three main units such as Operations Internal Audit

Unit, Finance and Admin Internal Audit Unit and IT/

MIS Internal Audit Unit.

As at December 2009, there were 16,098 loan

accounts audited, 20 reports related to Finance,

Human Resource and Admin Department, and 174

reports related to operations.

Through the findings of internal audit assignment

in the full year of 2009, we noticed that the trend

of errors and frauds decreased, and most field staff

shown stronger commitments to comply with

institutional policies and procedures. Moreover, most

of clients are not only satisfied with PRASAC’s

services but also appreciated with our professional

staff with customer care minded.

PRASAC has designed Risk Management tools and

approaches that respond to their specific clients,

lending methodologies, operating environments,

financial and social performance objectives. Each

Department has identified risks by themselves with

mitigation measures in place, but we are in process

of doing.

35

The effective approaches to managing credit risks in PRASAC are included as the following:

• Well-designed screening form for borrowers, careful loan assessment, close monitoring, clear collection

procedures, and active oversight by senior management. Delinquency is understood and addressed promptly

to avoid its rapid spread and potential for significant loss.

• Good portfolio reporting that accurately reflects the status andmonthly trends in delinquency, including

a portfolio-at-risk aging schedule and separate reports by loan product.

36

mARKETING AND SOCIAl ACTIVITIES

PRASAC is the largest MFI in Cambodia in terms

of number of staffs, loan portfolio, office networks,

and coverage areas. By end of 2009, PRASAC had

1,246 staff, 114 offices in 17 provinces/towns, 131

districts, 1,256 communes, 8,098 villages, 87,945

borrowers, total assets 295 billion KHR, and 267

billion KHR loan outstanding about 22% of total

microfinance market shares.

Our clients are village households with repayment

capacity that constitutes up to 90% of all

households located in rural areas where bad roads

and absence of facilities and utilities prevail. Apart

from rural people who generate income from rice

production as well as from farming, PRASAC also

targets micro-enterprises that produce or/and offer

services predominantly to the market.

As mentioned, PRASAC is serving about 11% of total

microfinance clients which 49.5% of those clients

used loans for agricultural livelihoods; particularly,

rice production and other multi-cultivations

including buying seeds, animals, biogas and other

agricultural equipments while 50.5% of loans

utilized for services and trade activities.

PRASAC is continuously building up its corporate

brand image as well as its products via effective

communication strategy and approach. It has

developed a clear communication strategy with

division of internal and external audiences by different

communication tools such as website, annual reports,

newsletters, brochures, calendars, leaflets, posters,

T-shirts, banners, and other mass media

communication via Radio and TV.

As a result, PRASAC had defined its current

positioning in good client perception as a well

managed and reliable MFI as a neighborhood MFI

with deep roots in which communities it operates.

PRASAC MFI goes out of its way to serve its

customers with respect and friendly service.

BRANDING AND COmmUNICATIONSmARKET AND ClIENTS

37

As a deep rooted MFI in community, PRASAC is

intending to stand as a combined social and

commercial oriented company which is to continue

focusing on poverty reduction in Cambodia with

sustainable financial returns.

Environment:

PRASAC’s credit policy does not allow any

involvements with environmental pollutions such as

toxic gas, polluted water, chemical residue, etc. and it

also limits itself not to provide its services to any

activity that may negatively effect to the environment.

However, PRASAC has been joining a national

biodigester program to take part in forest

protection as well as community sanitation. In this

regard, PRASAC provided loans to 1,346

households out of 2,200 plants; it’s about 61% of

total plants constructed by the program as at

December 31, 2008.

Social Ethics:

Apart from commercial and environmental

protection, Social Ethics is another concerning issue.

PRASAC enforces ethical practice not only to field

staffs but also to management levels by creating an

internal rule together with a revised personnel

policy, customer care and service policy to ensure

that all staffs are treated fairly, and to enforce a

common relationship among staffs as well as towards

clients and community as a whole. Particularly a

simple client protection principle was also set to keep

client’s satisfaction and sharing our social ethics to

Cambodian people.

PRASAC provides loans to beneficiaries of

ECOSORN project

PRASAC contracted with ECOSORN project in

order to contribute to poverty reduction through the

improvement of physical access to financial services

such as credit and savings. At the same time, the

project helps increasing the household income;

particularly, through increasing agricultural

productivity and local community empowerment in

selected rural areas of Cambodia.

PRASAC reaches the expected results of the contract

with remarkable achievements, by established 19

offices in 14 districts 40 communes and 91 villages in

three provinces, Siem Reap, Battambang and Banteay

Meanchey. As a result of the cooperation, PRASAC

targeted 13,962 beneficiaries in which 4,577

borrowers, 3,248 savers with KHR2,780,975,500

of disbursement amount from November 2007 to

December31, 2009 in ECOSORN target communes.

SOCIAl ACTIVITIESENVIRONmENTAl AND SOCIAl ETHICS

38

At the same time, PRASAC also provides financial

literacy to the poor

Besides credit operations, under the support of

ECOSORN project, PRASAC also provides financial

literacy training to the households in three provinces.

Particularly, this training focused on two modules

such as “Savings” and “Budgeting” for the

purpose of increasing the household’s understanding

on households’ savings and savings disciplines on how

to set savings goal and make savings plan, and how to

analyze their family’s financial situation.

As a result, in 2009, we organized 74 courses

conducted in three provinces, Battambang, Banteay

Meanchey and Siem Reap with total of 3,467

participants in which 74% are women. From this

social commitment, we hope that the household

living standards will get more improvement, the rate of

migration from remote areas will be reduced and

there will be more saving increment and alleviation

of high risk from emergency expense.

PRASAC’s provide loan for Biodigester Production

Relation to the Millennium Development Goals,

PRASAC has been collaborating with the National

Biodigester Programme (NBP) since 30th November

2007. In terms of social responsibility, the

collaboration is not only for poverty reduction but

also environment protection since it can save on

traditional energy sources, fossil energy sources and

improving soil fertility.

To comply with the partnership goal, PRASAC has

formed the new biogas loan product to serve the

people who plan to buy the biogas production in 8

biodigester programme provinces, Prevey Veng, Svay

Rieng, Kadal, Takeo, Kampong Speu, Kampot,

Kampong Cham, and Kampong Chhnanng.

As a result, by December 2009, PRASAC served

2,559 clients with convenience services, low

interest rate with total of USD1,450,670 loan

disbursement. Moreover, besides getting easier with

renewal energy resource especially the use of biogas

cooker instead of firewood, the biogas also help

protect human health as well as reduce indoor

environmental pollution with the improvement of

hygienic circumstances and dung management.

39

PRASAC Sponsors Buy Cambodian Products

Campaign

The Phnom Penh Small and Medium Industry

Association (PSMIA) organized a trade fair “Buy

Cambodian Products” on the occasion of Water

Festival in 2009. As the main sponsor of this event,

PRASAC objectively expects to take part in promoting

the campaign in order to improve the quality of local

products to be more standardized and competitive if

compared to the imported products. This is expected

that Cambodian people will change their habits for

consuming or buying our local products instead.

Concerning with this, PRASAC is willing to promote

Small and Medium Enterprise (SME) for better

competitive position in the market.

PRASAC contributes to build youth capacity and

career development

As always being part of building quality of education

as well as growing human roots of Cambodia,

PRASAC has actively joined as co-sponsor for

various educational events such as Career Guidance

for the Future, Outstanding Student Talk Program,

and Student Best Speakers Program prepared by

The Cambodian Mekong University for improving

the quality of education in Cambodian and developing

their critical thinking and understanding through

multiple perspectives. PRASAC also joined as

co-sponsor for Life Preparation for Success seminar

which was organized by Help Our Homeland

Association for building youth capacity and

competency especially leading them to be ready for

decision making and preparation for their life and

growth for the future.

All Cambodian students are the significant human

capital for fueling the economic growth and moving

the country out of the poverty trap. Consequently,

PRASAC is always willing to provide support in such

meaningful events to produce more challenging

output and increase more economic growth and

poverty reduction through PRASAC social

contribution.

PRASAC’s Presence at Banking and Microfinance

Events

As an active microfinance practitioner, PRASAC

joins in many microfinance and banking events as

a contribution sponsor as well as to expose itself

to the government, all banking and microfinance

sectors and other private companies and NGOs.

PRASAC joined in a Baking Exhibition 2009

organized by NiDA and IDG, Modernization of the

Banking and Microfinance Industry in Cambodia

hosted by the NBC, the Cambodia Microfinance

Conference by MoEF and IDG and PRASAC was also

present at the Cambodia’s Microfinance amid the

Global Crisis by focusing on how microfinance

institution could boost the country’s economy,

promote financial inclusion and enhance customer

protection. Within the hard time of economic crisis,

PRASAC is not only a key financial service provider

but also a good protector for its clients in terms of

interest rate reduction and careful client assessment

preventing from over indebtedness.

40

41

REPORT OF

THE BOARD

OF DIRECTORS

46

REPORT OF

THE INDEPENDENT

AUDITORS

AUDITED FINANCIAl STATEmENTS

47

BALANCE

SHEET

48

INCOME

STATEMENT

48

STATEMENT OF

CHANGES IN

EqUITY

49

STATEMENT OF

CASH FLOWS

The Board of Directors have pleasure in submitting

their report together with the audited financial

statements of PRASAC Microfinance Institution

Limited (“the Company” or “PRASAC”) for the year

ended 31 December 2009.

PRINCIPAl ACTIVITy

RESERVES AND PROVISIONS

BAD AND DOUBTFUl lOANS

PRASAC is engaged primarily in the provision of

micro-finance services to the rural population of

Cambodia through its headquarters in Phnom Penh

and various provincial offices in the Kingdom of

Cambodia.

There were no material movements to or from

reserves and provisions during the financial year

other than as disclosed in the financial statements.

Before the income statement and balance sheet of

the Company were prepared, the Board of Directors

took reasonable steps to ascertain that actions had

been taken in relation to the writing off of bad loans

and the making of allowance for doubtful loans, and

satisfied themselves that all known bad loans had

been written off and adequate allowance had been

made for bad and doubtful loans.

At the date of this report, the Board of Directors is

not aware of any circumstances, which would render

the amount written off for bad loans, or the amount

of allowance for doubtful loans in the financial

statements of the Company, inadequate to any

substantial extent.The financial results of the Company for the year

ended 31 December 2009 were as follows:

KHR’000

Profit before income tax 14,708,981

Income tax expense (3,551,075)

Profit for the year 11,157,906

FINANCIAl RESUlTS

REPORT OF THE BOARD OF DIRECTORS

41

CURRENT ASSETS

Before the income statement and balance sheet of

the Company were prepared, the Board of

Directors took reasonable steps to ensure that any

current assets, other than debts, which were unlikely

to be realised in the ordinary course of business at

their value as shown in the accounting records of the

Company had been written down to an amount which

they might be expected to realise.

At the date of this report, the Board of Directors is

not aware of any circumstances,which would render

the values attributed to the current assets in the

financial statements of the Company misleading.

VAlUATION mETHODS

CHANGE OF CIRCUmSTANCES

At the date of this report, the Board of Directors is not

aware of any circumstances which have arisen which

render adherence to the existing method of valuation

of assets and liabilities in the financial statements of

the Company as misleading or inappropriate.

At the date of this report, the Board of Directors is

not aware of any circumstances, not otherwise dealt

with in this report or the financial statements of the

Company, which would render any amount stated in

the financial statements misleading.

The results of the operations of the Company for the

financial year were not, in the opinion of the Board

of Directors, substantially affected by any item,

transaction or event of a material and unusual

nature.

There has not arisen in the interval between the end

of the financial year and the date of this report any

item, transaction or event of a material and unusual

nature likely, in the opinion of the Board of Directors,

to affect substantially the results of the operations of

the Company for the current financial year in which

this report is made.

ITEmS OF UNUSUAl NATURE

42

At the date of this report, there does not exist:

(a) any charge on the assets of the Company

which has arisen since the end of the

financial year which secures the

liabilities of any other person;

(b) any contingent liability in

respect of the Company that has

arisen since the end of the financial year

other than in the ordinary course of its

business operations.

No contingent or other liability of the Company has

become enforceable, or is likely to become

enforceable within the period of twelve months after

the end of the financial year which, in the opinion

of the Directors, will or may substantially affect the

ability of the Company to meet its obligations as and

when they fall due.

CONTINGENT AND OTHER lIABIlITIES

EVENTS SINCE THE BAlANCE SHEET DATE

No significant events occurred after the balance sheet

date that requires disclosure or adjustment other than

those already disclosed in the accompanying notes to

the financial statements.

The members of the Board of Directors during the

year and at the date of this report are:

MR. MICHAEL A. TEMPLE,•

representing Dragon Capital Group Limited,

(Chairman)

MRS. ANNE DEMEUSE,•

representing Belgian Investment Company

for Developing Countries SA, (Director)

MR. RANJIT FERNANDO, •

representing the Nederlandse

Financierings-Maatschappij voor

Ontwikkelingslanden N.V., (Director)

MR. ISHARA C. NANAYAKKARA,•

representing Lanka ORIX LEASING

Company Ltd, (Director)

MR. STEFAN A.V. HARPE, •

representing Oikocredit, Ecumenical

DevelopmentCooperative Society,

U.A., (Director)

MR. OUM SAM OEUN,•

representing PRASAC Staff Company Ltd.,

(Director)

All members are non-executive board members,

except MR. OUM SAM OEUN, who holds the position

of Deputy General Manager.

THE BOARD OF DIRECTORS

43

DIRECTORS’ INTERESTS

The Directors are representing the interests of shareholders of PRASAC during the year and at the date of this

report are as follows:

SHAREHOLDER REPRESENTED BY HOLDING

%

NUMBER OF SHARES

KHR 20,000 EACH

Dragon Capital Group Limited MR. MICHAEL A.

TEMPLE

18% 138,626

Belgian Investment Company for

Developing Countries SA (BIO)

MRS. ANNE

DEMEUSE

18% 138,626

The Nederlandse

Financierings Maatschappij voor

Ontwikkelingslanden N.V.(FMO)

MR. RANJIT

FERNANDO

18% 138,626

Lanka ORIX LEASING Company Ltd

(LOLC)

MR. ISHARA C.

NANAYAKKARA

18% 138,626

Oikocredit, Ecumenical Development

Cooperative Society, U.A.

MR. STEFAN A. V.

HARPE

18% 138,626

PRASAC Staff Company Ltd. MR. OUM SAM OEUN 10% 77,020

100% 770,150

DIRECTORS’ BENEFITS

During and at the end of the financial year, no arrangements existed to which the Company is a party with

the object of enabling Directors of the Company to acquire benefits by means of the acquisition of shares in or

debentures of the Company or any other body corporate.

Since the end of the previous financial year, no Director of the Company has received or become entitled to

receive any benefit (other than a benefit included in the aggregate amount of emoluments received or due and

receivable by the Directors as disclosed in the financial statements) by reason of a contract made by the

Company or a related corporation with a firm of which the Director is a member, or with a company in which

the Director has a substantial financial interest other than as disclosed in the financial statements.

44

The Board of Directors is responsible for ascertaining that the financial statements are properly drawn up so as

to give a true and fair view of the financial position of the Company as at 31 December 2009, and of the results

of its operations and its cash flows for the year then ended. In preparing these financial statements, the Board

of Directors is required to:

(i) adopt appropriate accounting policies which are supported by reasonable and prudent judgments

and estimates and then apply them consistently;

(ii) comply with Cambodian Accounting Standards and the guidelines issued by the National Bank of

Cambodia or, if there have been any departures in the interest of true and fair presentation, ensure

that these have been appropriately disclosed, explained and quantified in the financial statements;

(iii) maintain adequate accounting records and an effective system of internal controls;

(iv) prepare the financial statements on a going concern basis unless it is inappropriate to assume that

the Company will continue operations in the foreseeable future; and

(v) control and direct effectively the Company in all material decisions affecting the operations and

performance and ascertain that such have been properly reflected in the financial statements.

The Board of Directors confirms that the PRASAC has complied with the above requirements in preparing the

financial statements.

On behalf of the Board of Directors

MICHAEL A. TEMPLE,

Chairman

17 March 2010

RESPONSIBIlITIES OF THE BOARD OF DIRECTORS IN RESPECT OF THE FINANCIAl STATEmENTS

45

REPORTOF THE INDEPENDENT AUDITORSTO THE SHAREHOlDERS

46

KPMG Cambodia LtdNo 2 Street 208sangkat Beoung ProlitKhan 7 Makara Phnom PenhKingdom of Cambodia

REPORT OF THE INDEPENDENT AUDITORSTo the shareholdersPRASAC Microfinance Institution Limited

Telephone +855 (23) 216 899Fax +855 (23) 217 279internet www.kpmg.com

We have audited the accompanying financial statements of PRASAC Microfinance Institution Limited (“the Company” or “PRASAC”), which comprise the balance sheet as at 31 December 2009, and the income statement, statement of changes in equity and statement of cash flows for the year then ended, and a summary of significant accounting policies and other explanatory notes as set out on pages 8 to 65.

Management’s Responsibility for the Financial Statements