about calicut - beyond squarefeet study: focus mall ... 6 kadavu resort pradeep a.r. asst. manager...

TRANSCRIPT

www.beyondsquarefeet.com 1

2

About Calicut

www.beyondsquarefeet.com

www.beyondsquarefeet.com 3www.beyondsquarefeet.com

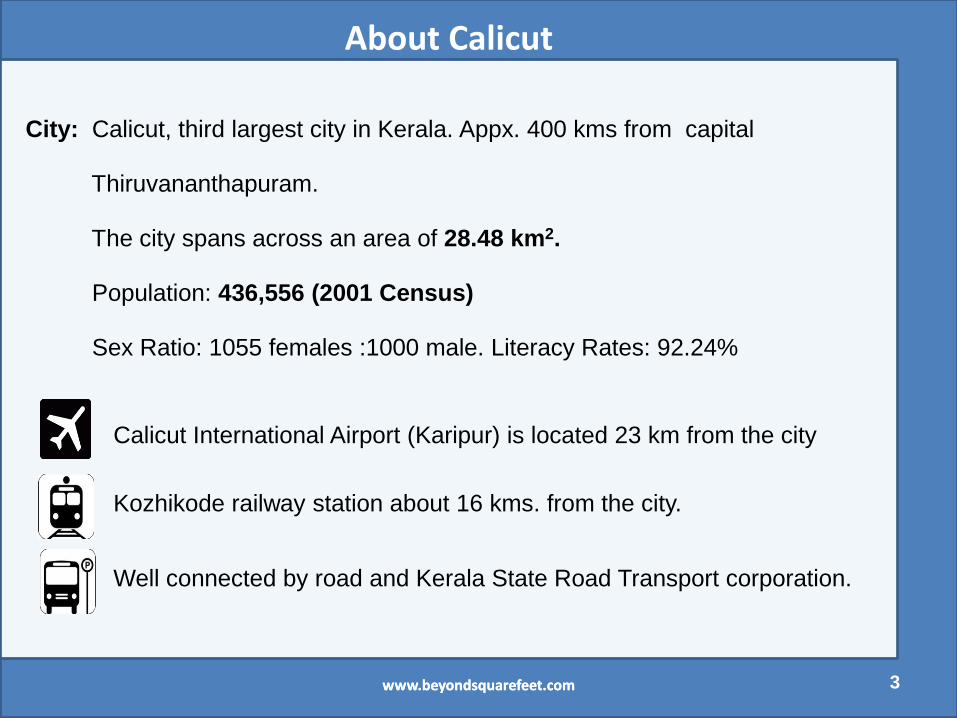

Calicut International Airport (Karipur) is located 23 km from the city

Kozhikode railway station about 16 kms. from the city.

Well connected by road and Kerala State Road Transport corporation.

City: Calicut, third largest city in Kerala. Appx. 400 kms from capital

Thiruvananthapuram.

The city spans across an area of 28.48 km2.

Population: 436,556 (2001 Census)

Sex Ratio: 1055 females :1000 male. Literacy Rates: 92.24%

About Calicut

Location in Calicut for proposed concept

www.beyondsquarefeet.com 4

Focus MallBig Bazaar

Most shopping options are situated on

Mavoor Road.

Banana Chips

Cherootty Road

Infrastructure & Facilities in Calicut

5

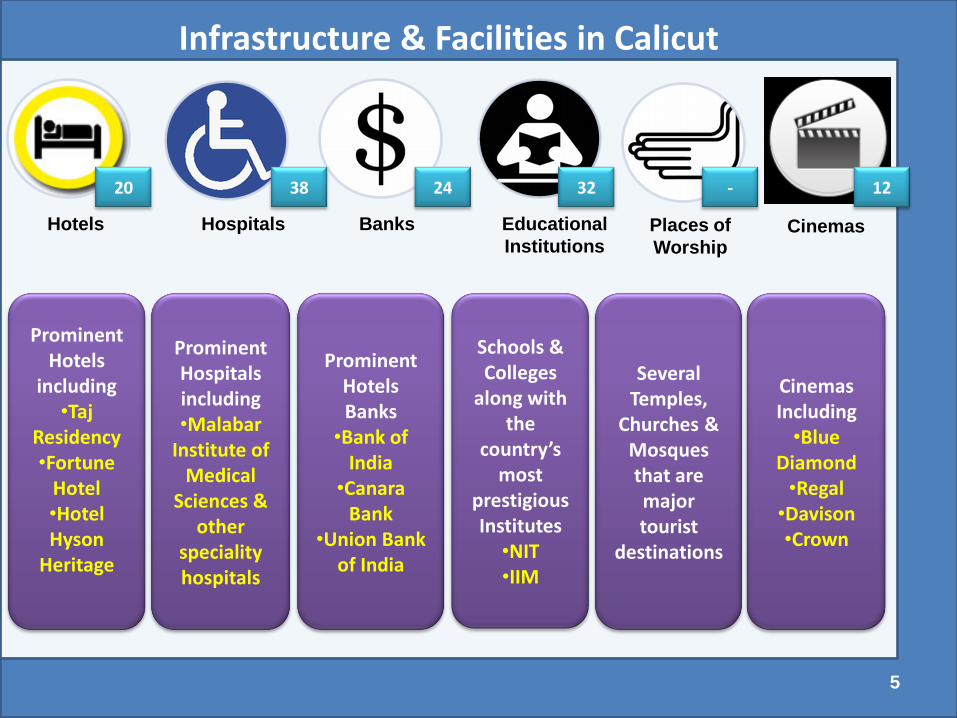

Hotels Hospitals Banks Educational

InstitutionsPlaces of

Worship

Prominent Hotels

including•Taj

Residency•Fortune

Hotel•Hotel Hyson

Heritage

Prominent Hospitals including•Malabar

Institute of Medical

Sciences & other

speciality hospitals

Prominent Hotels Banks

•Bank of India

•CanaraBank

•Union Bank of India

Schools & Colleges

along with the

country’s most

prestigious Institutes

•NIT•IIM

Several Temples,

Churches & Mosques that are major tourist

destinations

Cinemas

CinemasIncluding

•Blue Diamond

•Regal•Davison•Crown

20 38 24 32 - 12

Key Tourist Attractions

6

Kappad Beach Pazhassi Raja Museum Thusharagiri Waterfalls

Tali Temple Kadalundi Bird Sanctuary Beypore Port

www.beyondsquarefeet.com

Competition Intelligence*

Existing Malls in Calicut

Focus Mall - 1.65 lakh sq. ft. GLA

Marina Mall

Space Mall (commercial + retail) – 1.3 lakh sq. ft.

Blue Diamond Mega Mall – 1.25 lakh sq. ft.

Dreams, The Mall/ Satra galleria – 1 lakh sq. ft.

The grand high street Mall – 75,000 sq. ft.

Leader Mall

Coupon Mall

www.beyondsquarefeet.com 7

* Source: Popular Blogs

Competition Intelligence*

Case Study: Focus Mall

Area: 1.65 Lakh sq. ft. GLA across 6 floors

Parking: 300 car parks (2 floors)

Footfalls: Over 10,000 nos. /day

Avg. Rentals: Rs. 45/- (On GLA)

CAM: Rs. 17/-

Prominent Brands

Anchors: Max, Focus Hypermarket.

Vanilla:

F & B: Pizza Corner, Wimpey’s, Baskin Robins etc.

www.beyondsquarefeet.com

* Source: Focus Website

8

Research Report

www.beyondsquarefeet.com 9

The Research Team

Susil S. DUNGARWAL

Mr. Sundara Rajan Ms. Shaheen Baig

www.beyondsquarefeet.com 10

15 member ground Research Team

Approach

Research Findings (15/12/10)

Analysis (13/12/10)

Data Collation (08/12/10)

Data Collection (22/11/10)

Approval from GG (10/10/10)

Questionnaire development (05/10/10)

GG Appoints BSAPL (17/11/10)

www.beyondsquarefeet.com 11

Background of the Study

Gokulam group intends to build a mixed-use complex in Calicut.

The location of the project is ideal for setting up a multi usecommercial/retail building. The client is open on the concept & would deriveat the format/mix, based on this research.

Gokulam group wished to understand the market potential of the propertygiven the rapid changes taking place in Calicut.

This report outlines the findings of the Study.

www.beyondsquarefeet.com 12

Objectives of the Study

To find out the feasibility/ acceptability of such a Mall

To assess the potential for such a property in terms of the felt need of thetarget audience / market.

To map the potential competition in the target area.

To determine the different price points at which the respondents are willingto shift.

To understand the ideal mix of shopping, offices, banquets and hotel.

www.beyondsquarefeet.com 13

Research Methodology

Overall Approach:

Face-to-face interviews with the customers using a structured questionnaire.

Face-to-face interviews with the retailers using a structured questionnaire.

Face-to-face interviews with the corporate using a structured questionnaire.

Mystery buyer approach with Real Estate Agents

Mapping of all major commercial office spaces in 1 km radius of the location in

Calicut

Target Respondents:

Consumers Corporate Retail Hotel Agent

Those who belong to SEC A1, A2, B1, B2

Covering IT, financial services, Banking, Insurance etc

Covering apparel, shoes, food, jewellery categories

Banquet in charge/ Decision Maker

Agents who deal in commercial properties

www.beyondsquarefeet.com 14

Sample Size Distribution

Type of Respondents Achieved Sample Size

Consumers 250

Retailers 25

Corporate 11

Real Estate Agents 5

Hotels 8

Total 299

www.beyondsquarefeet.com 15

Respondent List - Retailers

SrNo.

Retailer Name

Respondent Name Designation

13G Mobile World Aneesh Manager

2PM Sales & Service Valsalam Manager

3 Wrangler Arun Manager

4 KG Mart Babu Owner

5Nokia Priority Sunil Kumar Owner

6 White Salt Saleemka Manager

7 Live-in Safeed Manager

8 Levi Manoj Manager

9 Bata India Sumesh Manager

10 Hi Lite Akhilesh Manager

11K. D. Hardware Smith Manager

12 Basics Manoj Manager

SrNo.

Retailer Name

Respondent Name Designation

13 Thomas Cook Dhanesh Manager

14 Galaxy Alavi In charge

15 Lifestyle Irshad Manager

16 CADD CentreLeethuPrabhakar Manager

17 UAE Exchange Riju

Asst. Branch Head

18 Park Avenue Sumith Manager

19 Reebok Denny Manager

20 Silky Boutique Fahad Manager

21 Woodland Biju Manager

22 CollorPlus Shiju Manager

23 Reebok Shop Denny Manager

24 Titan Eye Mahesh Manager

25Woodland Footwear Biju Manager

www.beyondsquarefeet.com 16

Respondent List - Hotel

Sr No Hotel Name Respondent Name Designation

1 Kovilakom Residense Rajesh Admin Manager

2 Gateway Hotel Rajiv Banquet In charge

3 Malabar Palace Suji Radhakrishnan Manager-Operations

4 Hyson Heritage Rajesh

5 Westway P. Bijoy Manager

6 Kadavu Resort Pradeep A.R. Asst. Manager

7 Hotel Maharani Sukumaran N. Manager

8 Malabar Gate Hotel Prakash Nair Manager

www.beyondsquarefeet.com 17

Detailed Analysis – Consumers

Consumers

www.beyondsquarefeet.com 18

Shopping Places Generally visited

S.M. Street is the most visited shopping place….More than half the respondents

generally visit S. M. Street

ConsumersBase: 250, Values in %

55

2422 21

129 8 8

0

10

20

30

40

50

60

S.M.Street Big Bazar Focus Mall Cherootty Road

More Koyencco Palayam Nadakkavu

www.beyondsquarefeet.com 19

9278

12 3 6 1 5 1 12

50

31

64 1 4 1 1

1

45

56

19

1026

721

6

24

1

8

4

30

6

26

15

19

Focus Mall Big Bazar Grand Highstreet

Dreams The Mall

Marina mall Blue Diamond mall

Orbit Mall Space Mall Leader Mall

Aided Spontaneous TOM Visited

Awareness about the Shopping Malls

Consumers in Calicut display higher awareness for Focus Mall and Big Bazaar as

compared to other malls. Awareness about Marina mall, Orbit mall and Leader mall is

good, but they are not visited much.

ConsumersBase: 250, Values in %

www.beyondsquarefeet.com 20

8578

12 126 5

0

10

20

30

40

50

60

70

80

90

Focus Mall Big Bazaar Grand High Street

Leader Mall Marina Mall

Orbit Mall

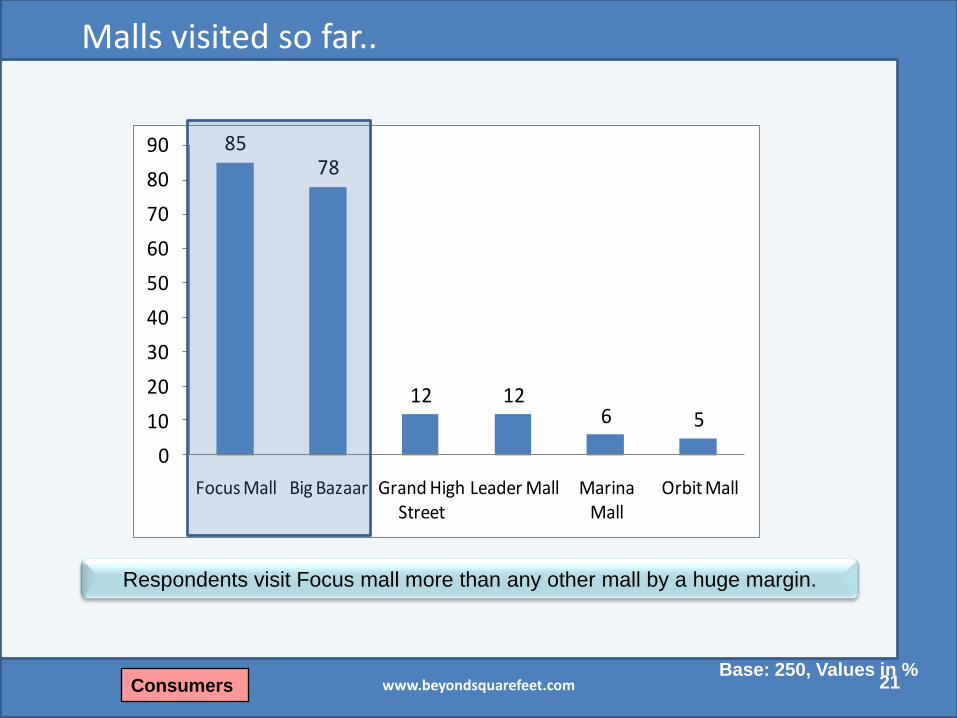

Malls visited so far..

Respondents visit Focus mall more than any other mall by a huge margin.

ConsumersBase: 250, Values in %

www.beyondsquarefeet.com 21

Frequency of Visit to the Malls

Respondents in Calicut regularly visit malls with half of them visiting once a

month and 20% visiting once a fortnight.

Consumers

Once a week11%

Once a fortnight

21%

Once a month51%

Once in 2-3 months

15%

Once in 6 months

2%

Base: 250, Values in %www.beyondsquarefeet.com 22

83% consumers visit Malls at least once a

month.

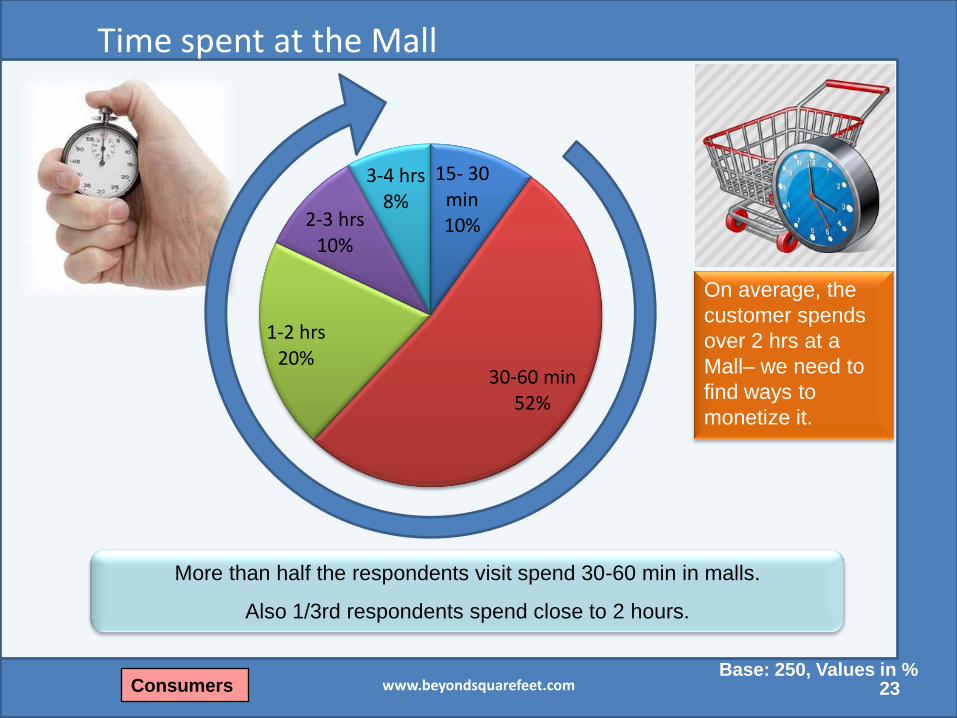

Time spent at the Mall

More than half the respondents visit spend 30-60 min in malls.

Also 1/3rd respondents spend close to 2 hours.

Consumers

15- 30 min10%

30-60 min52%

1-2 hrs20%

2-3 hrs10%

3-4 hrs8%

Base: 250, Values in %www.beyondsquarefeet.com 23

On average, the

customer spends

over 2 hrs at a

Mall– we need to

find ways to

monetize it.

Most Preferred Shopping Mall

Focus mall is clearly the most preferred mall in Calicut

ConsumersBase: 250, Values in %

www.beyondsquarefeet.com 24

Reasons for Preferring a Shopping Mall

ConsumersBase: 126, Values in %

BIG BAZAAR FOCUS MALL

www.beyondsquarefeet.com 25

Respondents want

quality products

available at one place.

The main focus is on

the layout of the Mall

and the range of

products available.

Product Categories visited in most preferred Mall

Focus Mall Big Bazaar

Base 118 126

Apparel 75 48

Shoes/Foot wear 20 14

Fancy Items/ Impulse 14 11

Jewellery /Ornaments 9 10

Bag & Luggage 7 8

Grocery items 5 14

Food items/Eatables 5 14

Consumers

Product

category

Name of

Mall

Clothes (Apparel) is the most visited category. Clearly shows

that more focus should be on apparel category.

Values in %www.beyondsquarefeet.com 26

Product Categories preferred to buy

Consumers

Focus Mall Big Bazaar

Base 118 126

Apparel 57 37

Shoes/Foot wear 14 8

Fancy Items/Impulse 12 6

Jewellery /Ornaments 7 9

Food items/Eatables 6 14

Grocery items 3 10

Bag & Luggage 3 5

Perfume 3 5

Kitchen items/Crockery 2 6

Product

category

Name of

Mall

A wide range of apparel should be made available to people

who’ll visit the mall as respondents spend mostly on

Clothes.

Values in %www.beyondsquarefeet.com 27

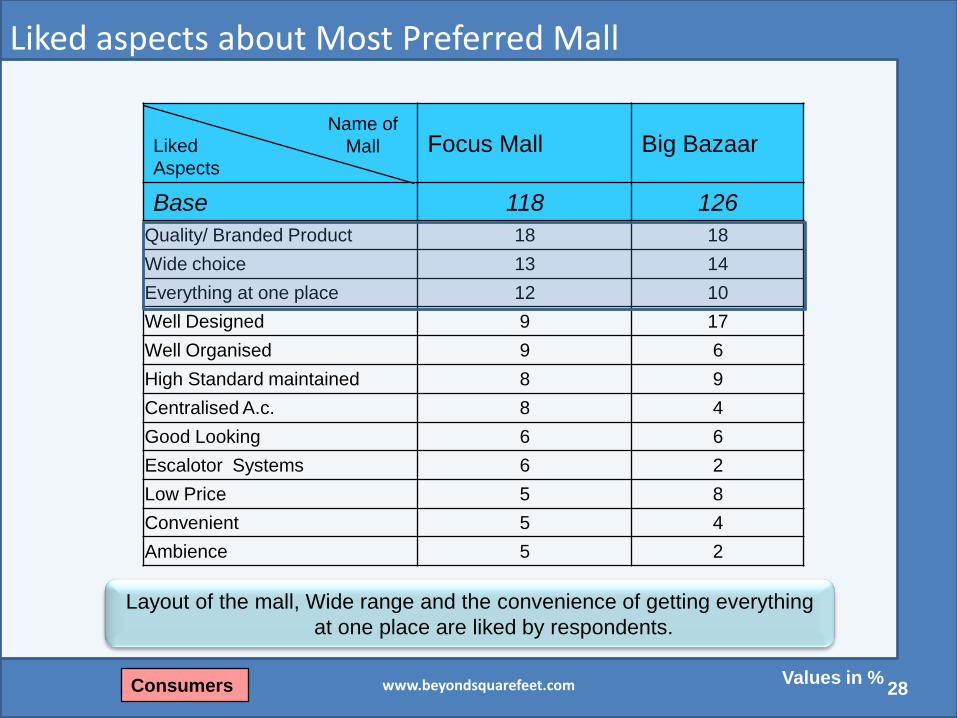

Liked aspects about Most Preferred Mall

Layout of the mall, Wide range and the convenience of getting everything

at one place are liked by respondents.

Consumers

Focus Mall Big Bazaar

Base 118 126

Quality/ Branded Product 18 18

Wide choice 13 14

Everything at one place 12 10

Well Designed 9 17

Well Organised 9 6

High Standard maintained 8 9

Centralised A.c. 8 4

Good Looking 6 6

Escalotor Systems 6 2

Low Price 5 8

Convenient 5 4

Ambience 5 2

Liked

Aspects

Name of

Mall

Values in %www.beyondsquarefeet.com 28

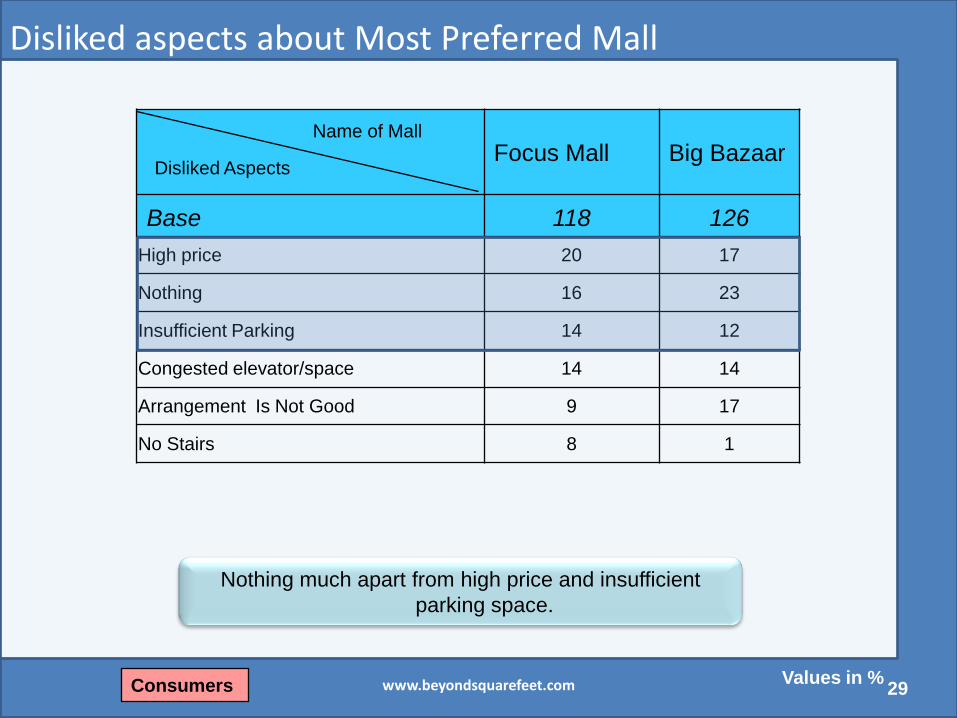

Disliked aspects about Most Preferred Mall

Nothing much apart from high price and insufficient

parking space.

Consumers

Focus Mall Big Bazaar

Base 118 126

High price 20 17

Nothing 16 23

Insufficient Parking 14 12

Congested elevator/space 14 14

Arrangement Is Not Good 9 17

No Stairs 8 1

Disliked Aspects

Name of Mall

Values in %www.beyondsquarefeet.com 29

Mode of Travel to the Malls

Respondents use personal transport to travel to the Malls….

ConsumersBase: 250, Values in %

www.beyondsquarefeet.com 30

Product Purchases Vs. Places of Visits

Respondents visit Calicut for Eating out, Grocery purchase, Footwear and home

furnishing purchase.

Consumers

Eating out

Apparel purchase

Grocery purchase

Home furnishing

purchase

Accessories purchase

Footwear purchase

Durables purchase

Top 3 places of Visit (values in %)

Big Bazaar, 24 Focus Mall, 18 SM Street, 11

Base: 250, Values in %www.beyondsquarefeet.com 31

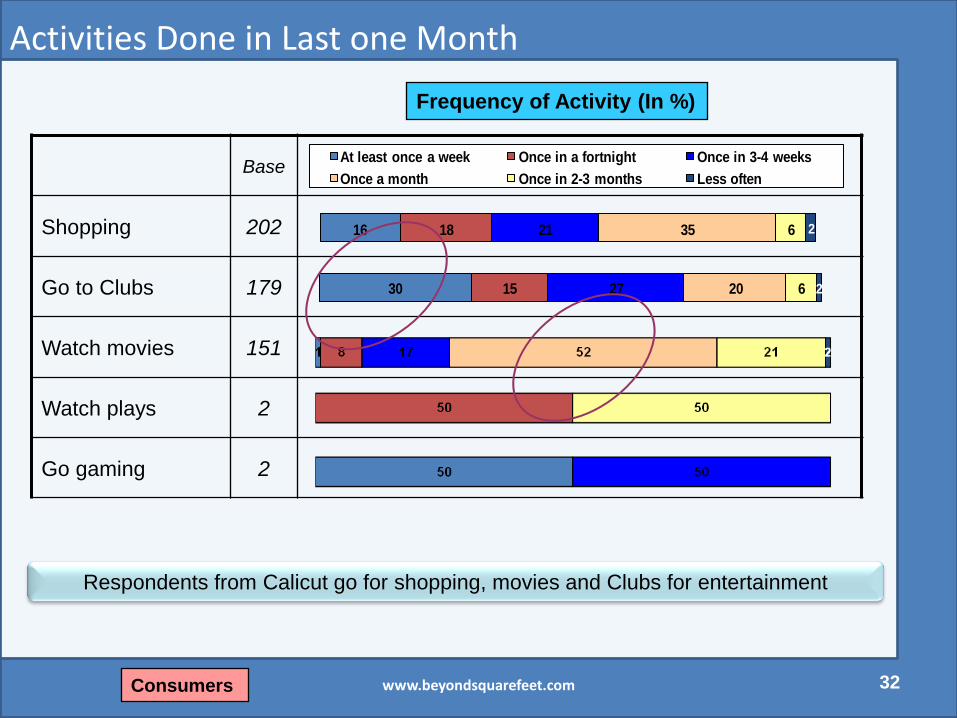

Base

Shopping 202

Go to Clubs 179

Watch movies 151

Watch plays 2

Go gaming 2

16 18 21 35 6 2

At least once a week Once in a fortnight Once in 3-4 weeks

Once a month Once in 2-3 months Less often

Activities Done in Last one Month

Respondents from Calicut go for shopping, movies and Clubs for entertainment

Consumers

30 15 27 20 6 2

Frequency of Activity (In %)

www.beyondsquarefeet.com 32

Watching a Movie

Respondents tend to watch movies both in Multiplex as well as Local

theatre.

ConsumersBase: 250, Values in %

www.beyondsquarefeet.com 33

Respondent Profile who go for Shopping once a month/once in 3-4 weeks

Almost half of the respondents (who go for shopping once a month or

once in 3-4 weeks) belong to the age group 36 – 50 years.

These respondents belong to both SEC A and SEC B.

Base: 114

Age wise Break up

Gender wise Break up

Base – 114, all fig in %, Base represents no. of respondents who go for shopping once a month or once in 3-4 weeks

Consumers34

www.beyondsquarefeet.com

Respondent Profile who go for a Movie once a month/once in 2-3 months

Almost half of the respondents (who go for shopping once a month or

once in 3-4 weeks) belong to the age group 36 – 50 years.

These respondents belong to SEC A1 /A2.

Base: 110

Age wise Break up

Gender wise Break up

Base – 110, all fig in %, Base represents no. of respondents who go for movies once a month or once in 2-3 months Consumers 35

www.beyondsquarefeet.com

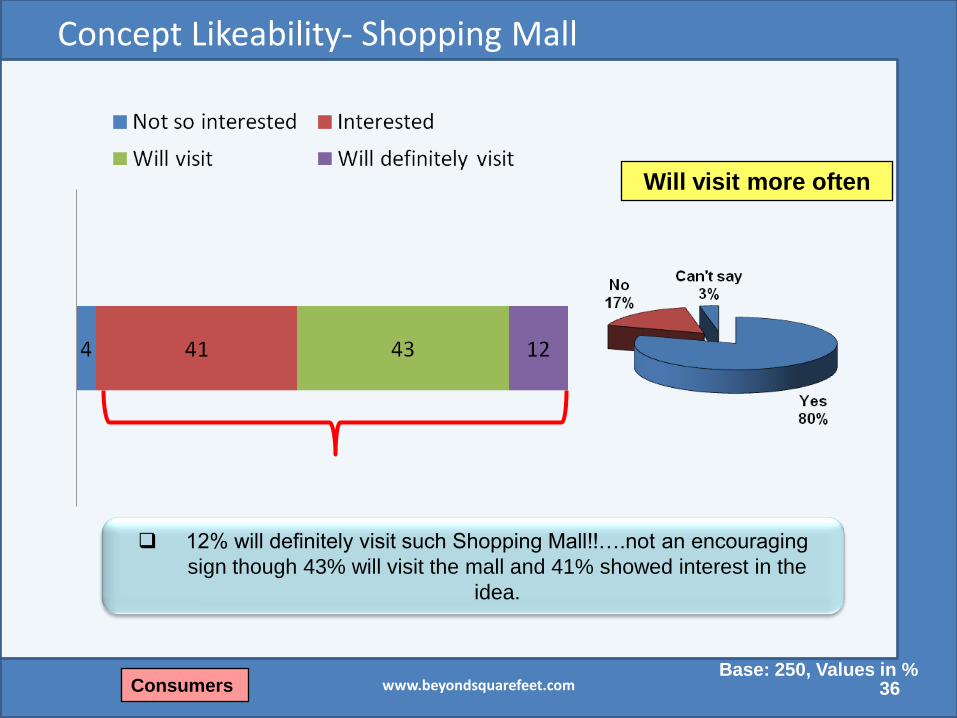

Concept Likeability- Shopping Mall

Will visit more often

12% will definitely visit such Shopping Mall!!….not an encouraging

sign though 43% will visit the mall and 41% showed interest in the

idea.

ConsumersBase: 250, Values in %

www.beyondsquarefeet.com 36

Products /Items/ Entertainment options would like to Buy/ Experience

71

20

15

13

9

7

7

6

6

5

4

4

4

Apparels

Shoes/Footwear

Theatre

Jewellery /Diamond

accesories

Fancy Items

Kitchenware

grocery items

Swimming Pool

Electronic Gadgets

Furniture

Food court

Baggage

Apparel is the most wanted item the respondents would like to buy/ purchase.

ConsumersBase: 250, Values in %

www.beyondsquarefeet.com 37

Expectations from such Shopping Mall

35

19

15

14

10

8

7

6

6

5

5

4

4

3

2

2

Should have everything under one roof

Should have good quality products

Should have reasonable prices of the products

Should have products with lot of variety

Should have a theatre

Should have plenty of shops

Nothing specific

Should have attractive showrooms

Should have provision of bar in the restaurant

Should be easily accessible

Should have gym, library & a hospital

It can have a retail mix & hospital

Should have good food variety

Should have good parking area

Should be spacious

Area should be neat & clean

Respondents feel that they

should get everything under

one roof….along with good

quality & reasonable rates…

ConsumersBase: 250, Values in %

www.beyondsquarefeet.com 38

Things missing in Calicut

ConsumersBase: 250, Values in %

0 50 100 150 200

Nothing

Entertainment

Department Store

Hypermarket

Beauty parlour

Theatre Should be There

Beverage's Availability

Fish Market

Book Store

www.beyondsquarefeet.com 39

Detailed Analysis – Retailers

Retailers

www.beyondsquarefeet.com 40

Amenities provided by Developer & Arranged by Self

Amenities / FacilitiesBase: 25

Provided by Developer(in %)

Arranged by self(in %)

24*7 Security / Help Desk 64 0

Intercom 32 0

Garden 60 8

Space outside Façade 40 0

Lifts 72 0

Cargo Lifts 52 4

Escalators / Elevators 56 4

Cellar & Surface Parking for staff 56 4

Parking for guest 68 4

Restaurant / Canteen / Cafeteria 60 0

Centralized A/c 60 12

24 Hrs water facility 84 8

Power back up 56 20

Fire extinguisher 64 16

Emergency exit 52 8

Base: 25, Values in %www.beyondsquarefeet.com 41Retailers

Satisfaction with Current Location & Premises

4

4

88

92

8

4

Location

Premises

Not at all Satisfactory Dissatisfaction

Neither satisfied nor dissatisfied Satisfied

Very Satisfied

Base: 25, Values in %www.beyondsquarefeet.com 42Retailers

Concept Acceptability

Attractive location

Yes (64%)

No (36%)

Beneficial for

business

Yes (33%)

No (67%)

Planning to open another outlet

Yes (8%)

No (88%)

Yes12%

No88%

Interested in getting space in the prosed

property

Though retailers find the location attractive they are

reluctant to open their outlet at the proposed location.

Base: 25, Values in %www.beyondsquarefeet.com 43Retailers

Expected rent for retail outlet in the proposed property

Expected rent (In Rs per sq ft per month)

In nos.

Average price expected as rent

Rs 62 sq ft per month

30 4.00%

40 8.00%

45 4.00%

50 36.00%

60 16.00%

70 4.00%

75 4.00%

80 12.00%

100 8.00%

125 4.00%

More than half of the corporate expect the rent in the proposed property to be Rs 60 per sq ft per month.

Base: 25, Values in %www.beyondsquarefeet.com

44Retailers

CORPORATE SEGMENTDetailed Analysis

www.beyondsquarefeet.com 45

Current scenario: built up area of office

Built-up area of current office (in sq ft) In nos.

Average built-up area of office 2027 sq ft

500 2

800 1

1000 1

2000 3

2500 1

3000 2

5000 1

www.beyondsquarefeet.com 46corporate

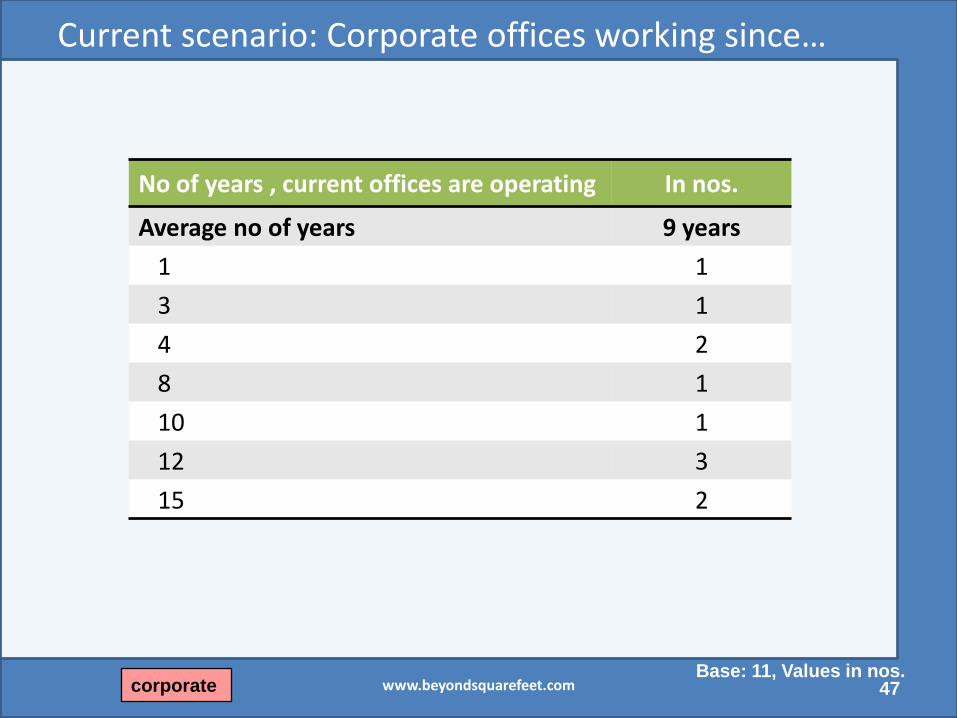

Current scenario: Corporate offices working since…

No of years , current offices are operating In nos.

Average no of years 9 years

1 1

3 1

4 2

8 1

10 1

12 3

15 2

Base: 11, Values in nos.www.beyondsquarefeet.com 47corporate

Current scenario: Level of satisfaction

Level of satisfactionSatisfaction with current office location

Satisfaction with current premises

Very much satisfied 0 0

Satisfied 9 7

Neither satisfied nor dissatisfied 2 2

Dissatisfied 0 2

Not at all satisfied 0 0

Corporate are satisfied with their current office location and premise.

Base: 11, Values in nos.www.beyondsquarefeet.com 48corporate

Expected rent for office in the proposed property

Expected rent (In Rs per sq ft per month) In nos.

Average price expected as rent Rs 64 sq ft per month

60 6

62 1

70 3

75 1

More than half of the corporate expect the rent in the proposed property to be Rs 60

per sq ft per month.

Base: 11, Values in nos.www.beyondsquarefeet.com 49corporate

Proposed property: Advantages Vs. Apprehensions

Advantages of the proposed property Apprehensions in the proposed property

It is a town area (7)

Attractive location (3)

Good area for corporate (3)

Central location (1)

Good views from the road (1)

Parking (6)

No issues (5)

Base: 11, Values in nos.www.beyondsquarefeet.com 50corporate

Proposed property: Expected facilities

Expected facilities in the proposed property In nos.

Proper parking facility 9

Good layout 1

Office setup 1

Uninterrupted water supply 1

Proper parking facility is the single most important expectation of corporate from the

proposed property.

Base: 11, Values in nos.www.beyondsquarefeet.com 51corporate

Summary of Findings:

Consumers

Corporate

Retailers

Hotels

Agents

52www.beyondsquarefeet.com

CONSUMER SEGMENT

Key findings

53www.beyondsquarefeet.com

Key findings: Consumer

S M street, Focus Mall and Big Bazaar are the most visited places for shopping.

83% of Calicut shoppers visit a Mall at least once in a month.

Consumers tend to spend leisure time of over 2 hours (avg.) on a visit to a Mall.

Respondents want quality products available at one place. The main focus is on

the layout of the mall and the range of products available.

Clothes (Apparel) is the most visited category.

High price followed by insufficient parking space are major concerns of

consumers.

Majority of the respondents use personal transport to travel to the malls.

55% of the respondents intend to visit the shopping mall in the proposed location.

www.beyondsquarefeet.com 54

CORPORATE SEGMENT

Key findings

55www.beyondsquarefeet.com

Key findings: Corporate – Current scenario

On an average, corporate respondents are operating in current offices since 10 years having average built-up area of– 2027 sq ft

50% of the corporate own their office whereas rest 50% have it on rent.

Corporate are satisfied with their current office location, having only one major concern of parking facilities.

Corporate expect the rent to in the range between Rs 60 – 75 sq ft per month. Average rent expected is Rs 65 per sq ft per month.

Corporate appreciate the location of the proposed project and expect builders office, restaurant and hotels to come primarily in the proposed mall.

www.beyondsquarefeet.com 56

RETAIL SEGMENT

Key findings

57www.beyondsquarefeet.com

Key findings: Retail segment – Current scenario

80% of retail outlets are on rental basis with sizes varying from 200 –

2500 sq ft. (average size of outlet - 945 sq ft.)

Most of the retail outlets have opened within a span of 1 – 4 years having

an average footfall of 315 /day per retail outlet.

Average rent expected by the retailers in the proposed premises - Rs 62

per sq ft per month.

64% of the retailers found the proposed location attractive for shopping

as it is location in the town area.

Retailers expect apparel and footwear outlets to come primarily in the

proposed mall.

Proper parking facility is the single most important expectation by

retailers.

www.beyondsquarefeet.com 58

HOTEL SEGMENT

Key findings

59www.beyondsquarefeet.com

Key findings: Hotel segment

The current area of banquet halls in Calicut vary from 500 to 3500 sq ft. with an average size of 1850 sq ft.

Hotels charge from Rs 250 to 500 per person for banquet halls. (Avg. rate charged Rs 372/person)

Hoteliers expect the rent to in the range between Rs 60 – 125 sq ft per month. Average rent expected is Rs 95 per sq ft per month.

Hoteliers (7 out of 8) find the proposed location attractive because of its central location.

The most prominent expectation by most hoteliers are proper parking facilities.

www.beyondsquarefeet.com 60

AGENTS

Key findings

61www.beyondsquarefeet.com

Key findings: Agents

Agents in Calicut deal majorly (4 out of 5) in shop space and office space.

4 out of 5 agents found the proposed location attractive for commercial complex and showed interested in dealing in this property as they found it beneficial for their business.

Agents expect the rent to be in the range between Rs 50 – 100 sq ft per month. Average rent expected is Rs 75 per sq ft per month.

Agents expect mobile phone, apparel and footwear retail outlets to come primarily in the proposed mall.

Proper parking facility is the single most important expectation by agents.

www.beyondsquarefeet.com 62

Way Forward

To conceptualize a Mall/mix-use complex keeping in mind the key findings

of the research.

The Mall has to connect to the age segment of the consumers.

To have a tenant mix which will compete with the existing preferred Malls.

Infrastructure and services of the Mall to exceed customer expectations.

Create a one-stop-shop.

Challenge: The well travelled customer.

www.beyondsquarefeet.com 63

Action Plan

Hotels and corporate do not see any business opportunity in the banquet

hall concept.

Extensive promotions required for the success of the mall.

Shopping mall with multiplex will be preferred by the consumers as Calicut

presently does not have a shopping mall with multiplex.

www.beyondsquarefeet.com 64

www.beyondsquarefeet.com 65