aberdeen/fieldaware building a culture of service excellence

TRANSCRIPT

BUILDING A CULTURE OF SERVICE EXCELLENCEJuly 2015

Aly Pinder, Senior Research Analyst,Service Management

2 2

Aly PinderSr. Research Analyst

Aberdeen Group

As a senior research analyst in the service management practice, Aly Pinder Jr. researches and explores how service and manufacturing executives utilize technology and implement best practices to improve post-sales service and support processes. Through practitioner benchmarking and analysis of

Aberdeen’s research database, he examines how Best-in-Class service organizations are reengineering their

service chains for improved performance and increased profitability

Nik ParraCTO

Resource POS

As Chief Technical Officer at Resource POS, Nik is responsible for propelling his company forward utilizing best in class technology. Nik headed the

implementation of FieldAware's field service management software in 2014.

3

TODAY’S AGENDA:

1. Aberdeen Research Methodology

2. New Generation of Service

3. Transform the Service Business

4. Benefits of Service Excellence

5. Steps to Optimize the Service Chain

6. Q&A

ABERDEEN RESEARCH METHODOLOGY

5

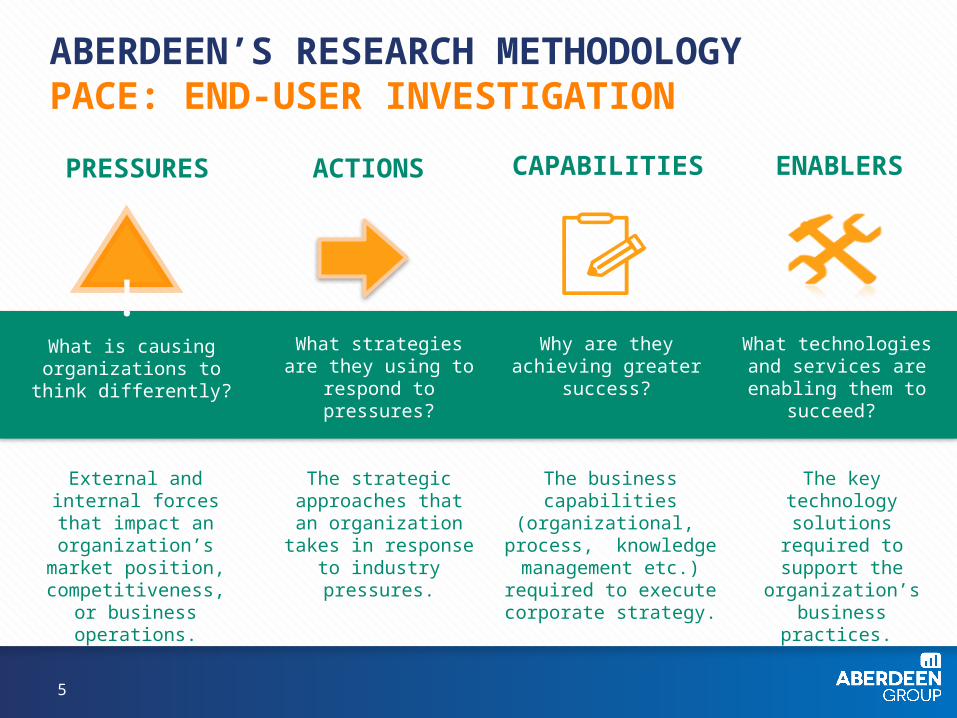

ABERDEEN’S RESEARCH METHODOLOGYPACE: END-USER INVESTIGATION

PRESSURES ACTIONS CAPABILITIES ENABLERS

External and internal forces that impact an organization’s market

position, competitiveness, or business operations.

The strategic approaches that an organization takes in response to industry pressures.

The business capabilities (organizational, process, knowledge management etc.) required to execute

corporate strategy.

The key technology solutions required to

support the organization’s business

practices.

What is causing organizations to think

differently?

What strategies are they using to respond to

pressures?

Why are they achieving greater success?

What technologies and services are enabling

them to succeed?

!

6

ABERDEEN MATURITY CLASS FRAMEWORKDEFINING THE BEST-IN-CLASS

Selected Performance Criteria (KPI)

Worker Productivity

Customer Satisfaction

Service Revenue

Total Respondents

- Top 20%

- Middle 50%

- Bottom 30%Respondents are scored individually across KPI

Best-in-Class

Industry Average

Laggard

NEW GENERATION OF SERVICE

8

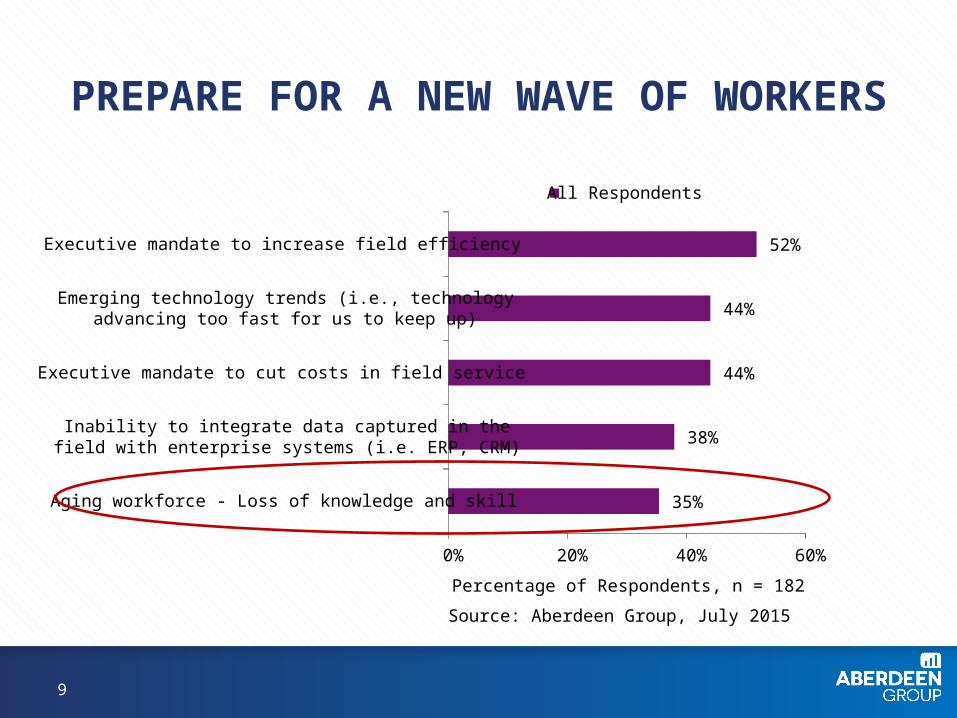

TOP CHALLENGES FACING SERVICE

35%

38%

44%

44%

52%

0% 20% 40% 60%

Aging workforce - Loss of knowledge and skill

Inability to integrate data captured in thefield with enterprise systems (i.e. ERP, CRM)

Executive mandate to cut costs in field service

Emerging technology trends (i.e., technologyadvancing too fast for us to keep up)

Executive mandate to increase field efficiency

Percentage of Respondents, n = 182

All Respondents

Source: Aberdeen Group, July 2015

9

PREPARE FOR A NEW WAVE OF WORKERS

35%

38%

44%

44%

52%

0% 20% 40% 60%

Aging workforce - Loss of knowledge and skill

Inability to integrate data captured in thefield with enterprise systems (i.e. ERP, CRM)

Executive mandate to cut costs in field service

Emerging technology trends (i.e., technologyadvancing too fast for us to keep up)

Executive mandate to increase field efficiency

Percentage of Respondents, n = 182

All Respondents

Source: Aberdeen Group, July 2015

10

THE GOOD ‘OLE DAYS

11

NOWADAYS

33%

36%

37%

43%

52%

0% 10% 20% 30% 40% 50% 60%

Improve service-relatedprofitability

Drive service revenues

Improve customer retention /loyalty

Drive service resourceproductivity / utilization

Improve customersatisfaction

Percentage of Respondents, n = 219

All Respondents

Source: Aberdeen Group, July 2015

TRANSFORM THE SERVICE BUSINESS

14

INVEST IN KNOWLEDGE FOR THE SERVICE WORKER

Strategic Actions Best-in-Class Respondents

Invest in mobile tools to provide technicians with better access to information in the field

44%

Improve forecasting of and planning for future service demand

41%

Increase availability of service knowledge in order to diagnose and resolve service issues more quickly

41%

Source: Aberdeen Group, July 2015

15

INCENT AND DEVELOP THE SERVICE WORKFORCE

48%

27%

17%

0%

10%

20%

30%

40%

50%

60%

Field technicians incented to identify cross-sell and up-sellopportunities (i.e. either direct sell or lead generation for

sales team)

Perc

enta

ge o

f Res

pond

ents

Best-in-Class Industry Average Laggards

Source: Aberdeen Group, July 2015n = 182

16

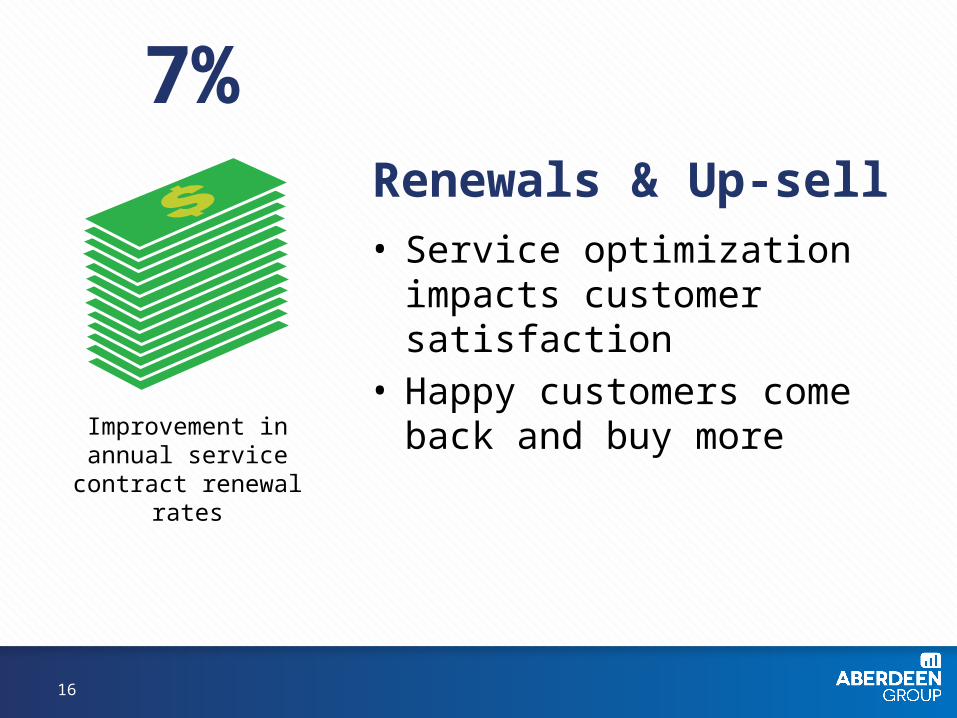

Renewals & Up-sell• Service optimization impacts

customer satisfaction• Happy customers come back

and buy more

7%

Improvement in annual service contract renewal

rates

17

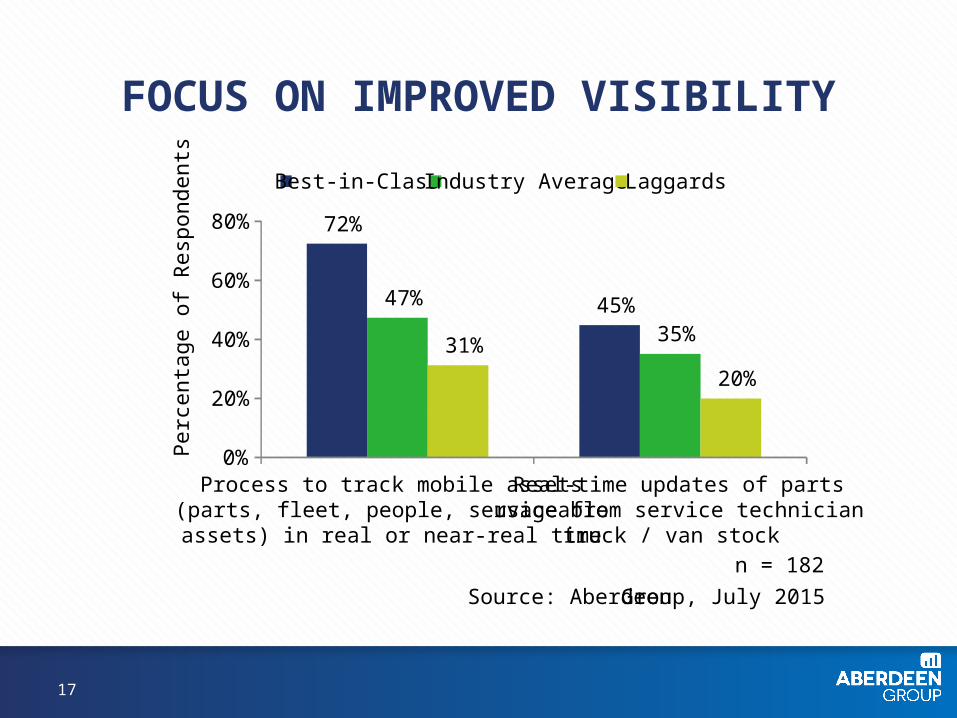

FOCUS ON IMPROVED VISIBILITY

72%

45%47%

35%31%

20%

0%

20%

40%

60%

80%

Process to track mobile assets(parts, fleet, people, serviceableassets) in real or near-real time

Real-time updates of partsusage from service technician

truck / van stock

Perc

enta

ge o

f Res

pond

ents

Best-in-Class Industry Average Laggards

Source: Aberdeen Group, July 2015n = 182

18

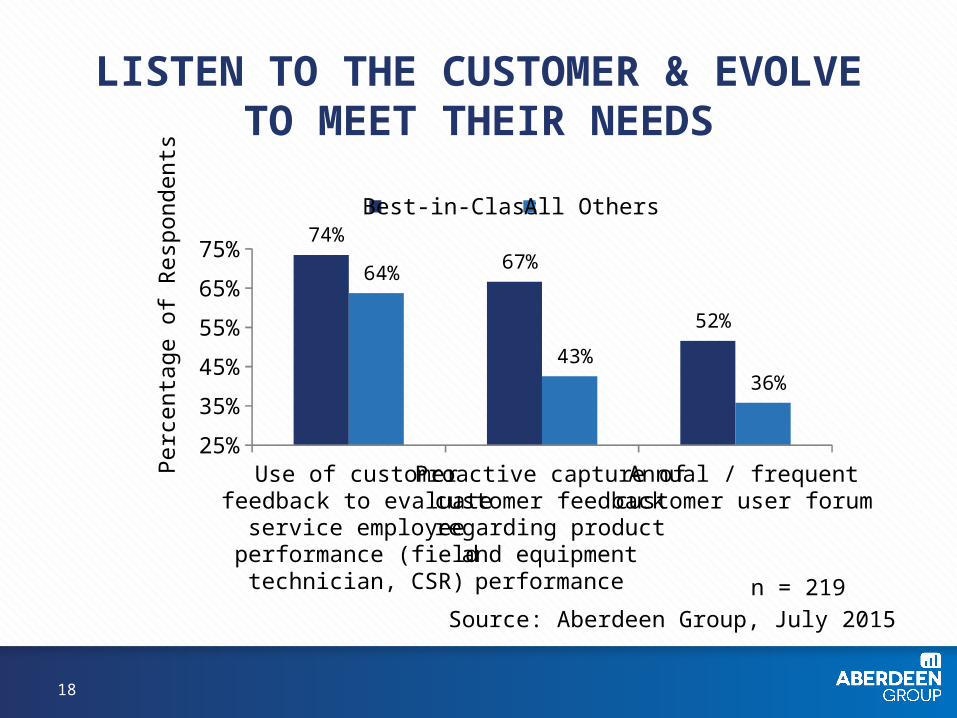

LISTEN TO THE CUSTOMER & EVOLVE TO MEET THEIR NEEDS

74%67%

52%

64%

43%36%

25%

35%

45%

55%

65%

75%

Use of customerfeedback to evaluate

service employeeperformance (field

technician, CSR)

Proactive capture ofcustomer feedbackregarding product

and equipmentperformance

Annual / frequentcustomer user forum

Perc

enta

ge o

f Res

pond

ents

Best-in-Class All Others

Source: Aberdeen Group, July 2015n = 219

19

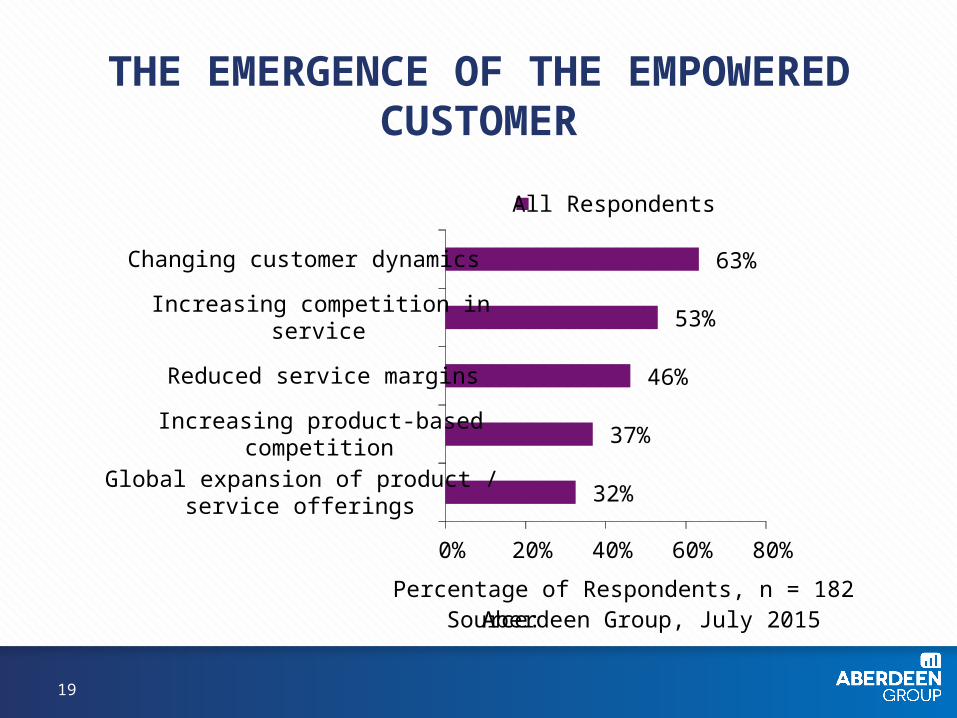

THE EMERGENCE OF THE EMPOWERED CUSTOMER

32%

37%

46%

53%

63%

0% 20% 40% 60% 80%

Global expansion of product /service offerings

Increasing product-basedcompetition

Reduced service margins

Increasing competition inservice

Changing customer dynamics

Percentage of Respondents, n = 182

All Respondents

Source:Aberdeen Group, July 2015

20

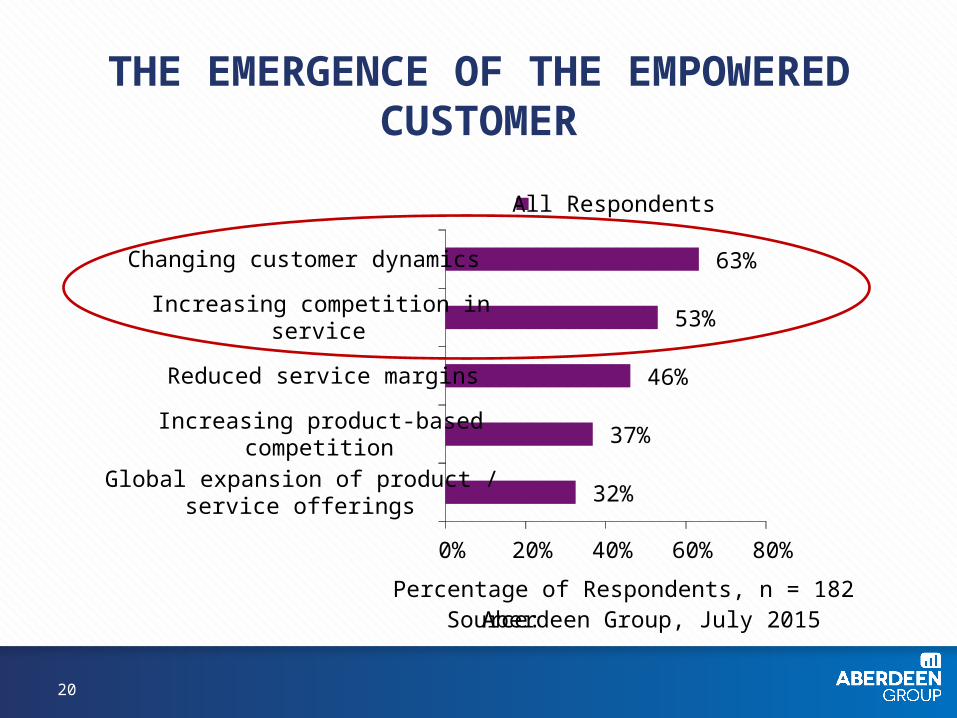

THE EMERGENCE OF THE EMPOWERED CUSTOMER

32%

37%

46%

53%

63%

0% 20% 40% 60% 80%

Global expansion of product /service offerings

Increasing product-basedcompetition

Reduced service margins

Increasing competition inservice

Changing customer dynamics

Percentage of Respondents, n = 182

All Respondents

Source:Aberdeen Group, July 2015

22

TOP 5 MOST CRITICAL METRICS THAT DEFINE SERVICE SUCCESS

68%

41%38%

34%29% 28% 26% 25%

20%

30%

40%

50%

60%

70%

80%

CustomerSatisfaction

ServiceProfitability

First-TimeFix Rate orFirst-Call

Resolution

ServiceRevenue

SLA /contract

compliancerate

ServiceCosts

(overall)

CustomerRetention(Customer

Churn)

ServiceableAsset

Uptime /Availability

Perc

enta

ge o

f Res

pond

ents

All Respondents

n = 219

Source: Aberdeen Group, July 2015

BENEFITS OF SERVICE EXCELLENCE

24

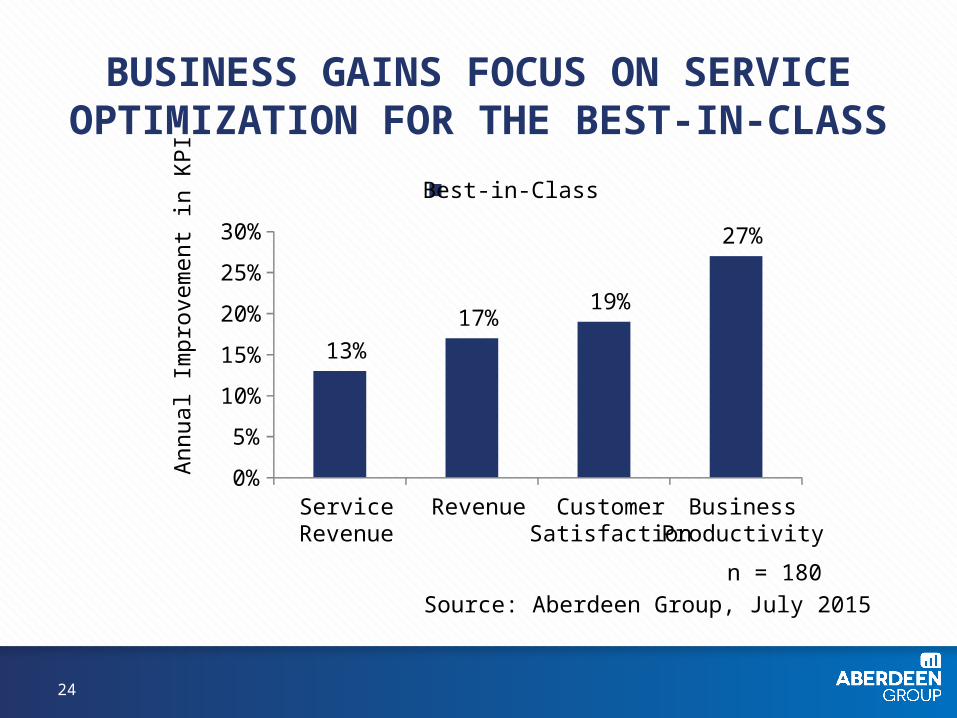

BUSINESS GAINS FOCUS ON SERVICE OPTIMIZATION FOR THE BEST-IN-CLASS

13%17%

19%

27%

0%

5%

10%

15%

20%

25%

30%

ServiceRevenue

Revenue CustomerSatisfaction

BusinessProductivity

Annu

al Im

prov

emen

t in

KPI

Best-in-Class

n = 180Source: Aberdeen Group, July 2015

STEPS TO OPTIMIZE SERVICE CHAIN

26

TAKEAWAYS• Implement / Invest in technology

– Top challenge facing service — insufficient technology infrastructure– Top strategy for Best-in-Class is to invest in mobile tools to provide techs

service workers with better access to information (44% of Best-in-Class)• Create a team of service worker partners

– Top 3 goals for service• Improve customer sat / loyalty• Drive service resource productivity• Drive service revenue

– Service workers incented to identify cross- or up-sell opps • Build value in the customer partnership / relationship• Become a trusted partner

• Improve visibility into the service chain– Real-time updates of service resources– Process to track mobile assets in real- or near-real time

27

28

THANK YOU

For more information about FieldAware and how they help customers automate their service chain visit

www.fieldaware.com

THANK YOU

For more information on this and other topics, please visit aberdeen.com

@pinderjr

https://www.linkedin.com/pub/aly-pinder-jr/2/8a9/2a4