abbott, grace 75 abstracters board of examiners, nebraska 601

TRANSCRIPT

9/17/2015

1

Presentation by Janet M. Bonnefin

Aldrich & Bonnefin, PLC

Washington Bankers Association2015 Northwest Compliance Conference

TRID – We’re Down to the Wire!

• Creditor’s duty to give Loan Estimate• Restrictions on charging fees at time of

application• Good faith determination of borrower’s costs

(tolerances)• Avoiding tolerance violations• Creditor’s duty to provide Closing Disclosure• Issuing corrected Closing Disclosure• Post-consummation changes• Correcting tolerance violations

Agenda

9/17/2015

2

• This presentation is intended solely for educational purposes to provide you general information about laws and regulations and not to provide legal advice. There is no attorney-client relationship intended or formed between you and the presenter. Consult your institution’s legal counsel for advice about how this information impactsyour institution.

Disclaimer

Important Definitions

9/17/2015

3

• General definition – Day on which creditor is open for carrying on substantially all of its business functions– May include Saturdays and Sundays if you’re

open, depending on the extent of the services you offer on weekends

• Precise definition – All calendar days excluding Sundays and 10 defined legal holidays (same as rescission definition)

Business Day –Two Definitions

• Consummation is when the consumer becomes contractually obligated on a credit transaction

• State law governs

• Generally it is when the consumer signs the debt instrument (promissory note, loan agreement, etc.)

Consummation

9/17/2015

4

Duty to Give Loan Estimate

• Creditor is responsible for providing Loan Estimate

• Within 3 business days of receipt of application

• “General” business day definition– A day your institution is open to the

public for carrying on substantially all of its business functions

Creditor’s Responsibility

9/17/2015

5

• Mortgage broker may give LE but creditor is still responsible for it

• Creditor may not issue a revised LE to correct broker’s errors

• But may issue a revised LE if an event occurs which permits creditor to issue one (more on this later)

Mortgage Brokers

• Application consists of 6 items of information – ALIENSA = Address of propertyL = Loan amountI = Income of consumerE = Estimated value of propertyN = Name of consumerS = Social security number

Application Defined

9/17/2015

6

• Creditor is allowed to request more information than just ALIENS– E.g., general application form, FNMA 1003, etc.

• Creditor may also request documentation to verify consumer’s information– Pay stubs

– Tax returns

– Signed verification forms

• But . . . creditor must provide LE once it has ALIENS, even if it hasn’t received the additional information or documentation it requested

May Request AdditionalInfo & Documentation

• When consumer is shopping for a new home, usually he has not identified a property or have an estimated value of the property (the purchase price)

• When consumer applies for a preapproval, you don’t have the “A” or “E” in ALIENS

• Thus the request for preapproval is not considered an “application” under TRID, so you don’t have to provide an LE yet

• When you get the “A” and “E,” giveLoan Estimate within 3 business days

Preapprovals Are Not Dead

9/17/2015

7

• In person• By regular mail• Overnight delivery (USPS, UPS, FedEx,

etc.)• Creditor may deliver Loan Estimate

electronically, but must comply with E-Sign Act first– E-Sign disclosure– Consumer’s consent given electronically

Manner of Delivery

• There must be 7 business days between when Loan Estimate is mailed or delivered and consummation– 7-business-day waiting period starts when

LE is mailed or delivered

• Consummation can occur on 7th business day

• Precise business day definition applies– All calendar days except Sundays and 10

legal holidays

7-Business-Day Waiting Period

9/17/2015

8

• Hand delivered: same day• By mail:

– 3-business-day mailbox rule– You may instead rely on evidence

(documentation) of earlier receipt

• By email:– Must comply with E-SIGN Act– 3-business-day mailbox rule– You may instead rely on evidence

(documentation) of earlier receipt

When Consumer is Deemed to Receive LE

• Two Reasons• Reason #1: Creditor/broker may not

impose a fee (except for credit report fee) until consumer –– Receives LE; and– Indicates an intent to proceed with the loan

• Reason #2: If creditor issues a revised LE, consumer must receive it at least 4 business days prior to consummation

• We’ll discuss issuing revised Loan Estimates later

Why Do We Care When Consumer Receives LE

9/17/2015

9

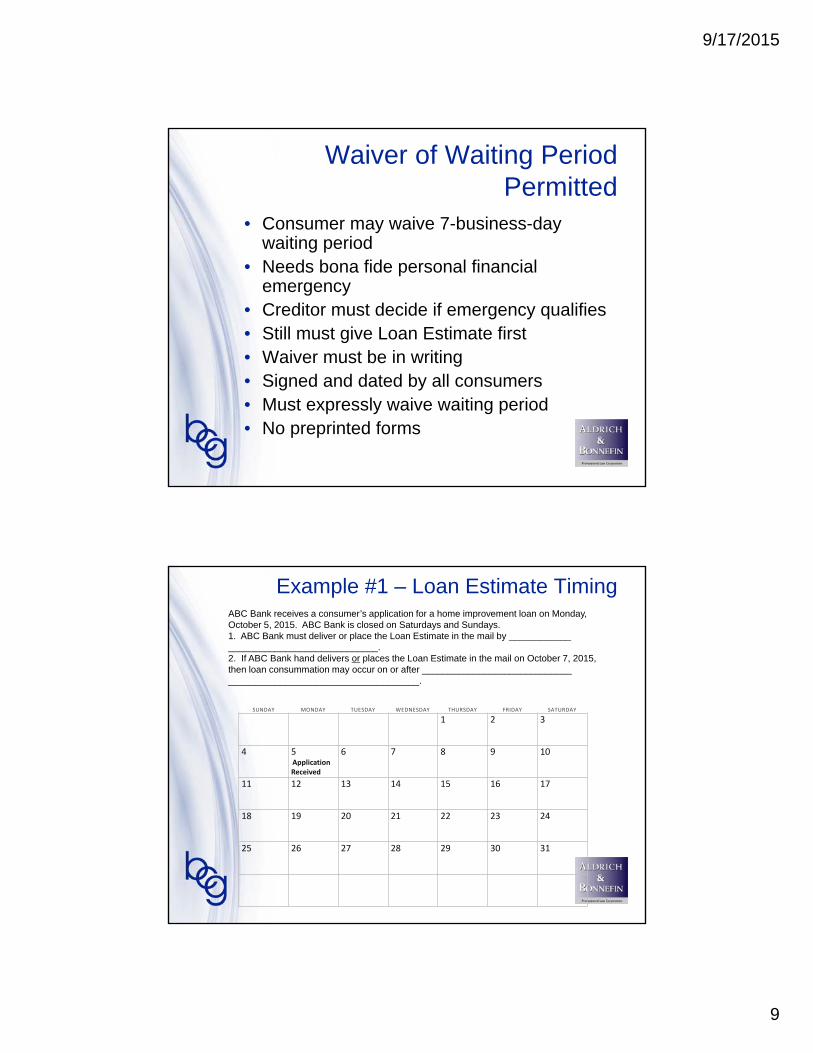

• Consumer may waive 7-business-day waiting period

• Needs bona fide personal financial emergency

• Creditor must decide if emergency qualifies• Still must give Loan Estimate first• Waiver must be in writing• Signed and dated by all consumers• Must expressly waive waiting period• No preprinted forms

Waiver of Waiting Period Permitted

Example #1 – Loan Estimate Timing

SUNDAY MONDAY TUESDAY WEDNESDAY THURSDAY FRIDAY SATURDAY

1 2 3

4 5 6 7 8 9 10Application Received

11 12 13 14 15 16 17

18 19 20 21 22 23 24

25 26 27 28 29 30 31

ABC Bank receives a consumer’s application for a home improvement loan on Monday, October 5, 2015. ABC Bank is closed on Saturdays and Sundays.1. ABC Bank must deliver or place the Loan Estimate in the mail by ____________ _____________________________. 2. If ABC Bank hand delivers or places the Loan Estimate in the mail on October 7, 2015, then loan consummation may occur on or after _____________________________ _____________________________________.

9/17/2015

10

• No one can collect any fees until– Loan Estimate is delivered AND

– Consumer expresses intent to proceed

• Only exception– Bona fide and reasonable credit report

fee

Restrictions on Charging Fees

Good Faith Determination(aka Tolerances)

9/17/2015

11

• Closing costs deemed to be made in good faith if charge consumer pays at closing doesn’t exceed the amount disclosed on the Loan Estimate

• So consumer must be charged the same as what was stated on Loan Estimate, unless the increase is within the applicable tolerance

Good Faith Determination of Charges

• Zero tolerance items– Origination charges– Fees charge by service providers the creditor

controls

• 10% aggregate tolerance items– Fees charge by service providers consumer

selects from provider list or doesn’t select at all

• Items not subject to limit at all– Unlimited variations permitted for certain fees

Three Categories of Tolerances

9/17/2015

12

• These fees are always subject to a zero tolerance

• Fees paid to creditor or mortgage broker

• Fees paid to affiliate of creditor or broker

• Transfer taxes

• Fees paid to unaffiliated third party if the creditor did not permit the consumer to shop for the third-party service provider

Zero Tolerance

• Examples of services consumers typically cannot shop for:– Appraisals

– Credit reports

– Flood determinations

• Therefore these fees are subject to a zero tolerance

Zero Tolerance Examples

9/17/2015

13

• Recording fees

• Third-party fees where consumer:– Can shop for service provider and– Chose one from creditor’s provider list or

made no selection at all

• This tolerance doesn’t apply to fees paid to creditor or broker, or their affiliates– These would be zero tolerance fees

10% Aggregate Tolerance

• Examples of service providers consumers usually can shop for:– Settlement agents

– Title companies

• Therefore, these fees are eligible for 10% tolerance

10% Aggregate Tolerance (cont’d)

9/17/2015

14

10% Aggregate Tolerance Example

• Total fees disclosed on LE subject to 10% aggregate tolerance = $750– So the tolerance is $75

• If one or more fees increase by a total of $70, creditor made a good faith determination

• But if one or more fees increase by a total of $80, there would be a tolerance violation– Unless creditor takes corrective measure– That is, issue a revised Loan Estimate if permitted– Or refund the difference

• Prepaid interest

• Property insurance premiums

• Amounts placed in escrow account

• Charges paid to third-party service providers selected by consumer not on creditor’s list

– E.g., consumer purchases title insurance from a company not on creditor’s written provider list

• Charges paid for third-party services not required by the creditor

– These can be paid to creditor’s affiliates

– Property survey fee

– Real estate agent’s commission

• These aren’t really subject to an “unlimited” tolerance– The original estimate still must have been based on the “best

information reasonably available”

– You can’t just guess or wildly over inflate the figures

Certain Variations PermittedWithout Limit

9/17/2015

15

• ABC Bank discloses a $400 escrow (settlement agent) fee on the Loan Estimate

• Assume the consumer is allowed to shop for the escrow agent and ends up choosing an escrow agent (not affiliated with ABC Lender) from ABC’s Written Provider List

• Is the $400 escrow fee subject to a□ Zero tolerance (no deviation allowed)?

□ 10% aggregate tolerance?

□ An unlimited variation?

Exercise #2

• Same facts as above but the consumer instead chooses an escrow agent that is not listed on ABC’s Written Provider List

• Is the $400 escrow fee subject to a

□ Zero tolerance (no deviation allowed)?

□ 10% aggregate tolerance?

□ An unlimited variation?

Exercise #3

9/17/2015

16

• Tolerance violations can be avoided in certain circumstances by issuing a revised Loan Estimate

• Issuing revised Loan Estimate is optional in all cases except . . .

• Creditor must issue a revised LE when the creditor and consumer agree to lock the interest rate or the rate is relocked

Avoiding Tolerance Violations –Issue Revised LE

• Creditor is to issue revised LE within 3 business days (general definition) of receiving info that allows the creditor to issue a revised LE

• Consumer must receive the revised LE at least 4 business days (precise definition) prior to consummation

Timing for Revised LEs

9/17/2015

17

• Changed circumstances• Consumer’s eligibility is affected• Consumer requests a change• Interest rate is locked (or relocked)• Loan estimate expires after 10

business days• Delayed settlement date in

connection with initial construction loan

When Creditor May IssueRevised LE

• If interest rate is locked (or relocked), creditor is required to issue a revised LE

• Timing – within 3 business days following the date the interest rate is locked

• Revised Loan Estimate to include –– Revised interest rate– Points disclosed– Lender credits– Any other interest rate dependent

charges and terms

Interest Rate Lock

9/17/2015

18

• If consumer indicates intent to proceed more than 10 business days (general definition) after original Loan Estimate was issued, creditor is not bound by the original LE

• Creditor may –– Continue to use original Loan Estimate or– Issue a completely new Loan Estimate or– Issue a revised Loan Estimate

• No justification other than the passage of time is needed to issue a new or revised Loan Estimate

Loan Estimate Expires in 10 Business Days

• Rule applies to new (initial) construction loans

• If creditor reasonably expects consummation to occur more than 60 days after providing Loan Estimate

• Then creditor may provide revised Loan Estimate at any time up to 60 days before consummation

Delayed Consummation Date on New Construction Loans

9/17/2015

19

• Creditor must include required statement on page 3 of the original Loan Estimate in “Other Considerations” section –

Delayed Consummation Date on New Construction Loans (cont’d)

“You may receive a revised Loan Estimate at any time prior to 60 days before consummation”

• Coverage limited to – Loan for the purchase of a home that

has yet to be built, or– Loan to purchase a home currently

under construction

• Does not apply to – Home improvement or remodeling loans– Loan if use and occupancy permit

issued before Loan Estimate issued

Scope of Special Construction Loan Rule

9/17/2015

20

• Note that construction lenders are not required to use this exception in order to issue a revised Loan Estimate because there is a downside to using this exception

• If creditor provides a Loan Estimate that would not otherwise be permitted by the other five exceptions, the creditor must wait at least 60 days after issuing the revised Loan Estimate before it can consummate the loan

• Creditors instead may choose to issue a revised Loan Estimate only if permitted by the other five exceptions in which case the creditor is not required to wait 60 days before consummatingthe loan

Consider Whether You Should Use This Exception

• Consumer must receive revised LE at least 4 business days prior to consummation

• Precise definition of “business day” applies• If LE not delivered in person, consumer

deemed to receive revised LE 3 business days after it is mailed

• So 3 + 4 = 7 business days• At least 7 business days must elapse

between when Loan Estimate is mailed and when consummation can occur

Timing After Issuing Revised Loan Estimate

9/17/2015

21

Closing Disclosure

• Creditor has the responsibility to provide Closing Disclosure

• Creditor may divide up responsibility with settlement agent

• Creditor must provide Closing Disclosure at least 3 business days before consummation– Precise business day definition

Duty to Provide Closing Disclosure

9/17/2015

22

• Consumer may waive the 3-day waiting period, according to the same rules as the Loan Estimate waiver

• You cannot issue a revised Loan Estimate once you issue the Closing Disclosure

Duty to Provide Closing Disclosure

• Same as Loan Estimate receipt rules

• Hand delivered: same day

• By mail:– 3-business-day mailbox rule– You may rely on evidence (documentation) of

earlier receipt

• By email:– Must first comply with E-SIGN Act– 3-business-day mailbox rule– You may rely on evidence (documentation) of

earlier receipt

When Consumer is Deemed to Receive CD

9/17/2015

23

SUNDAY MONDAY TUESDAY WEDNESDAY THURSDAY FRIDAY SATURDAY

1 2 3

4 5 6 7 8 9 10Application Received

Loan Estimate mailed or delivered in person

11 12 13 14 15 16 17Columbus Day Consummation

can occur

18 19 20 21 22 23 24Consummation scheduled

25 26 27 28 29 30 31

Example #4

October2015

ABC Bank receives a consumer’s application for a home improvement loan on Monday, October 5, 2015. ABC Bank is closed on Saturdays and Sundays. The lender must deliver or place the Loan Estimate in the mail by Thursday, October 8, 2015, in which case consummation can occur on or after Saturday, October 17.

1. If consummation is scheduled for Monday, October 19, 2015, and ABC Bank will be delivering the Closing Disclosure in person, ABC must hand deliver the Closing Disclosure by October __________.

2. If consummation is scheduled for Monday, October 19, 2015, and ABC Bank will be mailing the Closing Disclosure, ABC must place the Closing Disclosure in the mail by ____________.

3. On Thursday, October 15, the consumer requests a change to the loan, going from an adjustable-rate mortgage to a fixed-rate loan, which increases several charges beyond the applicable tolerances. a. In order to avoid tolerance violations, ABC would have to issue a

revised Loan Estimate by October ______________.b. If ABC issues a revised Loan Estimate on that date, the earliest

consummation may occur is October _________________.c. In that case, ABC must issue the Closing Disclosure by

October ________________.

Example #4 (cont’d)

9/17/2015

24

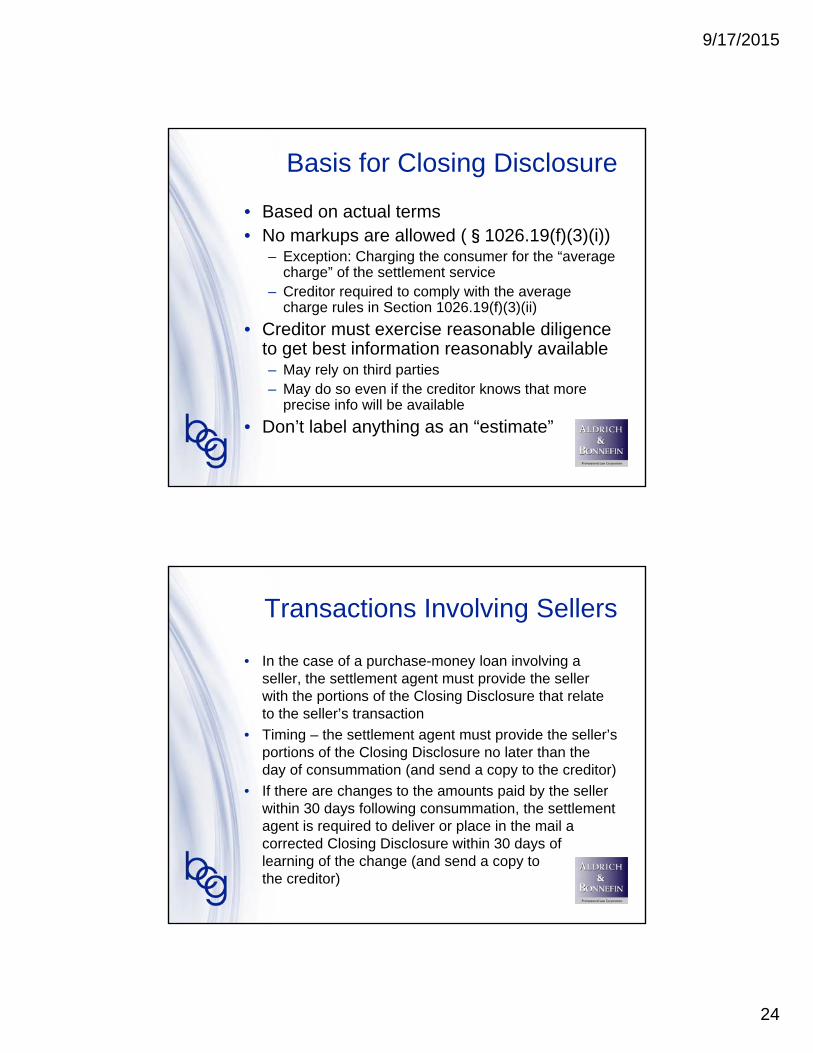

• Based on actual terms• No markups are allowed (§1026.19(f)(3)(i))

– Exception: Charging the consumer for the “average charge” of the settlement service

– Creditor required to comply with the average charge rules in Section 1026.19(f)(3)(ii)

• Creditor must exercise reasonable diligence to get best information reasonably available– May rely on third parties– May do so even if the creditor knows that more

precise info will be available

• Don’t label anything as an “estimate”

Basis for Closing Disclosure

• In the case of a purchase-money loan involving a seller, the settlement agent must provide the seller with the portions of the Closing Disclosure that relate to the seller’s transaction

• Timing – the settlement agent must provide the seller’s portions of the Closing Disclosure no later than the day of consummation (and send a copy to the creditor)

• If there are changes to the amounts paid by the seller within 30 days following consummation, the settlement agent is required to deliver or place in the mail a corrected Closing Disclosure within 30 days of learning of the change (and send a copy tothe creditor)

Transactions Involving Sellers

9/17/2015

25

Corrected Closing Disclosures

• Creditor is required to issue a corrected Closing Disclosure if CD doesn’t reflect– Actual terms of the transaction or

– Actual costs associated with settlement

• Two categories– Pre-consummation corrected CDs

– Post-consummation corrected CDs

Issuing Corrected Closing Disclosures

9/17/2015

26

• Some changes trigger corrected CD and new 3-business-day waiting period

1. APR out of tolerance• Regular transactions: 0.125%

• Irregular transactions: 0.250%

• Also other APR tolerances in Section 1026.22

2. Change to loan “product”

3. Creditor adds a prepayment penalty

Issuing Corrected Closing Disclosure Pre-Consummation

• Other types of changes don’t trigger new 3-day period– For example, seller credit increases by

$500 the day before loan signing

• But creditor must still provide corrected CD at or before consummation

• And creditor must make corrected CD available for consumer’s inspection one business day (general definition) before consummation

Other Changes to Closing Disclosure Pre-Consummation

9/17/2015

27

• If an event occurs within 30 days following consummation that changes the amount the consumer actually paid– For example, recording fee

• Creditor is required to issue a corrected Closing Disclosure

• Provide corrected CD within 30 days of learning of event

Post-Consummation Changes

• A creditor does not violate the Closing Disclosure requirements if it corrects non-numeric clerical errors within 60 days after consummation by sending a corrected Closing Disclosure

• For example, typo in name of settlement service provider or mortgage broker

Non-numeric Clerical Errors

9/17/2015

28

• If actual costs paid by the consumer exceed Loan Estimate amounts (beyond tolerance), refund overcharge within 60 days

• Deliver corrected CD (reflecting refund) too

Correcting Tolerance Violations

Contact Information

Janet M. Bonnefin

PrincipalAldrich & Bonnefin, PLC18500 Von Karman Ave., Suite 300Irvine, CA [email protected]

Questions?