abac malaysia -sme finance forum workshop on … kristine ng wei miem, credit... · workshop on...

TRANSCRIPT

ABAC Malaysia - SME Finance Forum Workshop on Innovative Financing for SMMEs

InterContinental Hotel Kuala Lumpur 21st May 2015

9:30 am – 11.30 am

Ms. Kristine Ng Wei Miem(EVP, Business Development)

This proposal is the sole property of Credit Guarantee Corporation Malaysia Berhad. (12441-M) This intellectual property should not be

disseminated or otherwise conveyed to any third party without the prior written permission of the Corporation.

Session 1: Moving Into the Mainstream – Showcase of Alternative Funding Mechanisms for SMMEs

Introduction on CGC

Corporate Information

PoweringMalaysian SMEs

• Authorised Capital: RM3.0 bil

• Paid Up Capital (Ordinary & Preference Shares: RM1,785. 6 mil

• Shareholders

ØNegara Malaysia – 78.65%

ØFinancial Institutions – 21.35%

To be an effective financial institution dedicated to

promoting the growth and development of competitive

and dynamic SMEs.

Vision

Mission

To enhance the viability of SMEs through the provision of products and services at

competitive terms and, with the highest degree of professionalism, efficiency

and effectiveness

3

CGC’s Mandated Role

To assist SMEs avail financing from financial institutions

"The Credit Guarantee Corporation is a key institutional arrangement in facilitating greater access to financing forthe SMEs. By providing guarantee to loans obtained by SMEs, CGC addresses one of the main constraints of SMEs thatis, the lack of collateral.“

- Tan Sri Dr. Zeti Akhtar Aziz, Governor of Central Bank of Malaysia (BNM)

SMEs with

§ No collateral§ Insufficient collateral§ Do not have any track record

How?

• Bridge FIs and SMEs via guarantee mechanism

5

Prai 25/06/2001

Main Branch 3/07/2000

Ipoh 9/10/2000

Kuala Lumpur 3/11/2003

Seremban 23/07/2001

Melaka 21/04/2001

Johor Bahru 6/11/2000

Batu Pahat 3/11/2003

Kuantan 28/05/2001

Kuala Terengganu 26/11/2001

Kota Bharu 18/06/2001

Kuching 21/01/2002

Miri 24/02/2004

Kota Kinabalu 21/01/2002 Sandakan

19/01/2004

16 Branches across MalaysiaAlor Setar 8/04/2002

Branch Network

7

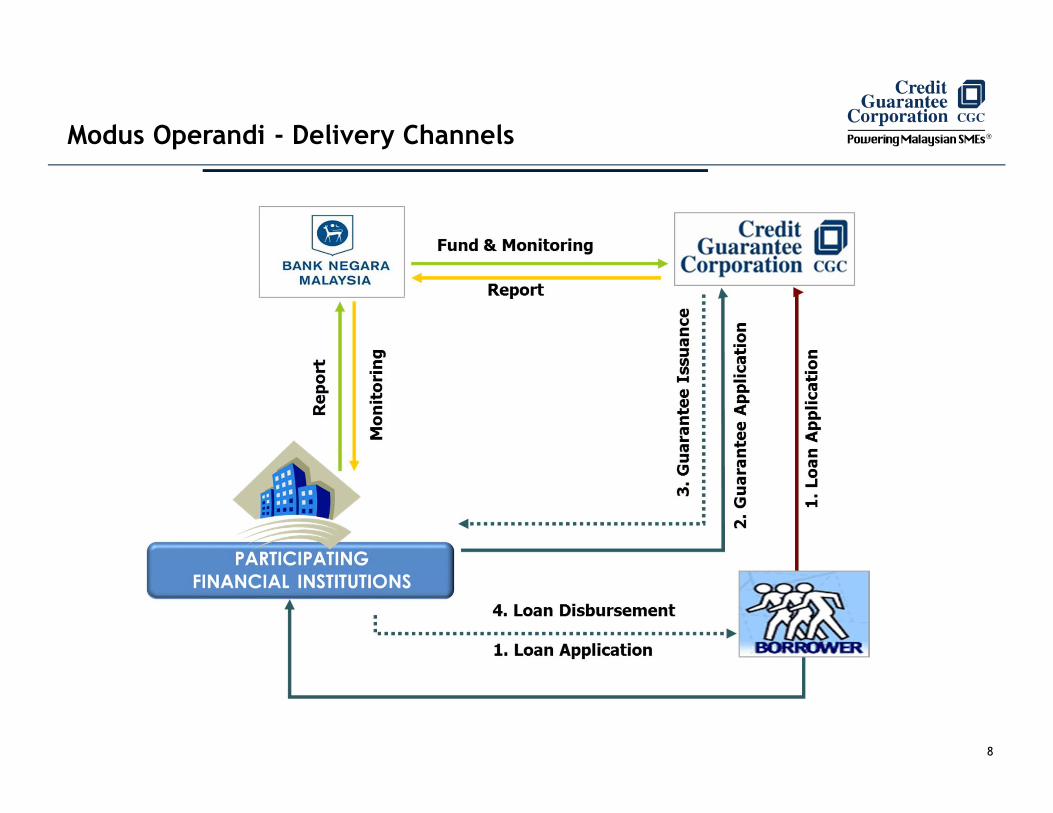

Modus Operandi - Delivery Channels

8

SME Outreach

9

SME Outreach (cont’)

As at 2014, 46.2% or 142,832 SMEs have successfully graduated from CGC schemes

#Graduates : SMEs that no longer have CGC guarantee since 2 years from date of reporting* Starting Jan’14 the Graduated SMEs are inclusive of other cancellation status e.g. expiry of cover, fully recovered (after claim approved), fully settled after claims rejected/returned & fully settled after wound down. Prior to January 2014, the Graduated SMEs are only those Cancellation with Fully Paid status only.**Based on the same base for Dec’13 of 138,189 for like for like comparison. 10

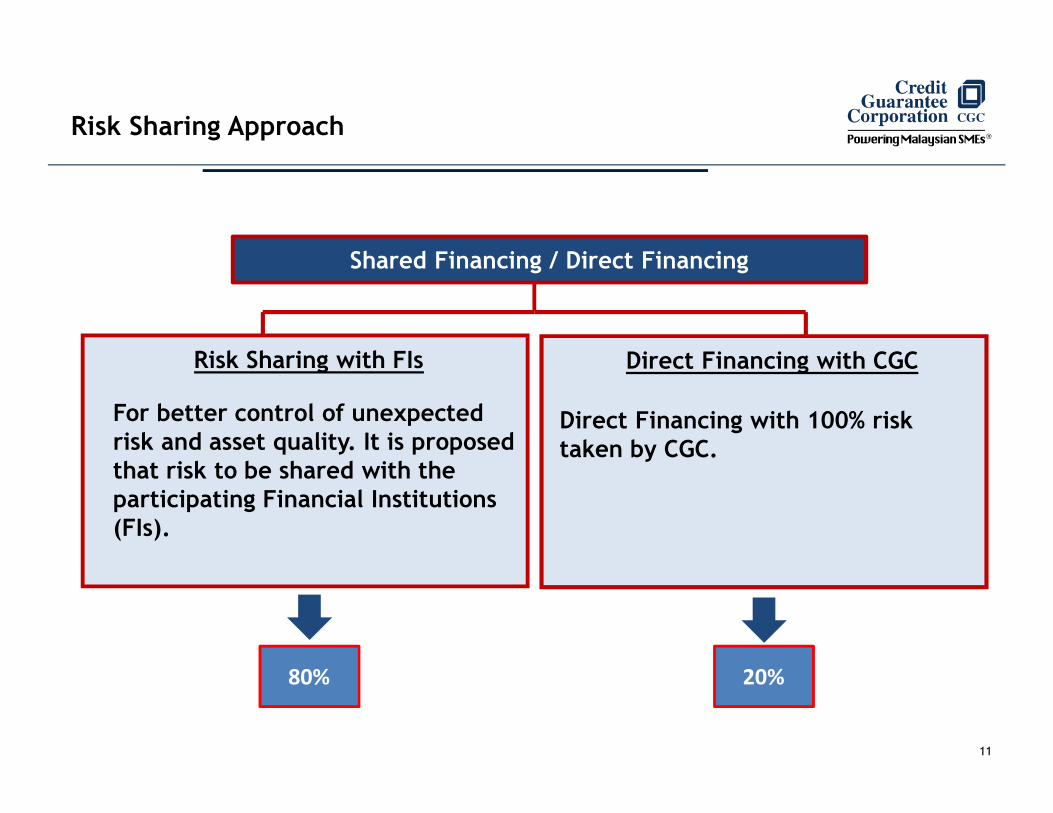

Risk Sharing Approach

Shared Financing / Direct Financing

Direct Financing with CGC

Direct Financing with 100% risk taken by CGC.

Risk Sharing with FIs

For better control of unexpected risk and asset quality. It is proposed that risk to be shared with the participating Financial Institutions (FIs).

80% 20%

11

Business Model

Pricing

Risk Management

SME Outreach

Advisory Services

Building Capacity to Guarantee

Business Model

• Pricing based on risk•“Blended rate” concept.

•Robust Internal Risk Rating Model •Pricing Model.•Risk sharing with FIs•Utilize CBM services (PD & CMS)•Early Care (ECM)• Smaller loan amount•Policy on high risk sectors.•Group exposure limits

•Focus on number of SMEs.•Customer exposure limit.•Branches playing greater role.•Products that meet FI needs

•Advisory services limited to financial only

• Investment viewed as an integral component of business model.

• Investment to subsidize development12

Product Segmentation

GUARANTEE PRODUCTS / DIRECT LENDINGGUARANTEE PRODUCTS / DIRECT LENDING

Commercial

• Attractive & flexible features

• Generate returns

• Credit Enhancer Scheme

• Enhancer Express Scheme

• Enhancer Excel

• Enhancer Bumi Scheme

• SmallBiz Express

• Flexi Guarantee Scheme

• Portfolio Guarantee (PG)

• BizMula-i

Government-backed Schemes

• High developmental content

(Programme Lending)

• Backed by Government via

Funding

• Risk sharing

• Green Technology Financing Scheme

• IP Financing Scheme

• Franchise Financing Scheme

• Bumiputera Entrepreneur Project Fund – i / Tabung Project Usahawan Bumiputera-i

General Product Features

� Loan amount: - Between RM20,000

to RM10 mil

� Guarantee cover:- Between 30% to 100%

� Guarantee fee : - Between 0.5% - 5.75%

(based on risk adjusted pricing)

� Interest / profit rate:- Depending on the scheme

or FIs may determine <= 50% guarantee

13

Alternative Funding Mechanisms for SMMEs

20

Improving Access to Financing

CGC has embarked on the following intitiatives to Alternative Funding Mechanisms for SMMEs:

Funding the start ups with minimal

financial information required. Leverage more on the Know

Your Customer (KYC) approach.

1 Direct Financing

Overcoming high fee via by reward GOOD

customers with as high as 30% discount by

lowering SMEs guarantee cost.

4Rebates

Mechanism

Supporting Government initiatives for SMEs to

access funding via Government backed-Schemes. (i.e. Green Technology Financing

Scheme (GTFS), Intellectual Property

and Special Relief Fund.

3Government-

backed Schemes

Enhance relationship with the FIs –

introduced innovative products such as

Portfolio Guarantee where the approvals from CGC is within 3

days.

2Portfolio

Guarantee (PG)

Ancillary Services Provided CGC

Information on Associate / Subsidiary Companies

Bank Negara Malaysia

Financial Institutions

78.65% 21.35%

Governance Structure

Credit Bureau Malaysia Sdn. Bhd.

55%

Subsidiary

15

Credit Bureau Malaysia Sdn. Bhd. [ formerly SME Credit Bureau (M) Sdn. Bhd.]

Objectives

Ø Promotes greater transparency, professionalismand sound credit culture among SMEs.

Ø Acts as a systemic risk management tool.

Ø Develop SME rating database to guide businessand make credit decisions.

Ø Broadens the role of CGC in SME sectordevelopment.

16

Credit Bureau Malaysia Sdn. Bhd.

Bridging the Credibility Gap

LACK OF COLLATERAL INADEQUATE INFORMATION

SMEs & Micro- businesses need to build a Credit TRACK RECORD

Credit Reports

Financial Institutions can improve TIMELINESS & ACCESS TO FINANCING

17

How to contact us?

Client Service CentreLevel 2, Bangunan CGC, Kelana Business Centre, 97, Jalan SS 7/2, 47301, Petaling Jaya, Selangor Darul Ehsan

Tel : 03-788 000 88Fax : 03-7803 0077

Email : [email protected] Hours

8.30am -5.30pm (Monday- Friday)

For more info, please visit our websitewww.cgc.com.my

Thank You

GUARANTEE SCHEME’S

Introducing

BizMula-iA NEW scheme

launched in May 2014

BizMula-i

Eligibility Criteria

q Malaysian-controlled & Malaysia-owned businesses

q Comply as SME by BNM’s definition

q Good credit record

q Business in operations for less than 3 years

q Business is at least licensed by a local authority

Financing Limit RM50,000 – RM300,000

Financing Rate From BFR + 0.3% to BFR + 1.65% only

Facilities Term Loan

Tenure Max 7 years

Eligible age 21 to 58 (at point of application)

BizMula-i

BizMula-iKey benefits

• Help businesses with less than 3 years operation andlack of track record to access financing.

• It is collateral free. No security to be pledged.• Competitive financing rate and financing tenure up to 7

years.• Direct funding from CGC.

§ A project most recently with OCBC Bank valued at MYR 500 million in 2011. This product was alsopreviously available to RHB Bank and Standard Chartered Bank, with such great success that new trancheshave been added.

§ The objective of this PG arrangement will be to assist Malaysian SMEs who have viable businesses withstrong potential for growth, but lack sufficient collateral to obtain the required financing. The PortfolioGuarantee in essence provides a guarantee through a risk partnership basis.

§ Under the portfolio guarantee scheme, CGC guarantees 70% of the approved total principal amountundertaken by SMEs and assists to verify the credibility of the SME applicants in consultation with OCBCBank. The applicants are assessed on a special programme scorecard jointly agreed upon with CGC usingsimplified fulfillment criteria for loan eligibility. With this, banks can enjoy greater confidence whengranting loans to SMEs. Accordingly, a portfolio guarantee enables SMEs to enjoy quicker access tofinancing. CGC can advise on the status of the loan application within three business days as opposed totwo weeks under other schemes.

§ The minimum loan quantum under the guarantee scheme is RM100, 000 and the maximum RM1 million foreach tranche per SME customer at a fixed loan tenor of five years. The loans are fully unsecured and theguarantee fee and lending rate pre-determined by OCBC Bank in consultation with CGC.

§ This particular PG with OCBC has benefited 187 SMEs since launch on the 10 of March 2011. As at Dec2011, CGC’s PG has availed uncollateralized financing to 1,668 SMEs and NPL amount is at an impressivelevel of 2.4% with only 49 SMEs turning NPL within a year.

Portfolio Credit Guarantee (PG)

Green Technology is the development and application of products, equipment and systems, used to conserve the natural environment and resources and to minimise the negative impact of human activities.

What is Green Technology?

The awareness to protect the environment has opened the door for SMEs thatsupply and utilize Green Technology, which is envisaged to be one of theemerging drivers of economic growth for Malaysia. GTFS was established bythe Government through Ministry of Finance to promote and supportinvestments in Green Technology.

Green Technology Financing Scheme (GTFS)

Green Technology Financing Scheme (GTFS)

To promote investments in Green Technology which refers to products, equipments or system which satisfy the following criteria :

Minimizes the degradation of the environment

Has a zero or low green house gas (GHG) emission

Safe for use and promotes healthy and improved environment for

all forms of life

Promotes the use of renewable resources

Conserves the use of energy and natural resources

Objectives of the scheme

Green Technology Financing Scheme (GTFS)

Key FeaturesProducer User

Purpose To finance investment for the production of green products

To finance investment in the utilization of green technology

Financing Size Maximum: RM50 million per company

Maximum: RM10 million per company

Financing Tenure Up to 15 years Up to 10 yearsEligibility Company approved by the Malaysia Green Technology

CorporationLegally registered Malaysian companies that have at least 51% Malaysian shareholding

Legally registered Malaysian companies that have at least 70% Malaysian shareholding

Participating Financial Institutions (PFIs)

All commercial and Islamic banks, and DFIs (Bank Pembangunan, SME Bank, Agrobank, Bank Rakyat, EXIM Bank and Bank Simpanan Nasional)

Government Incentives Rebate of 2% per annum of interest/profit rate

Application DateThe Scheme will open until 31 December 2015 or upon approval of financing up to RM3.5 billion, whichever is earlier

Green Technology Financing Scheme (GTFS)

Green Technology USER ?The person/company who used or operates the business using the green technology produced items/components. i.e;

Green LaundryGT Component including:-• Water & energy efficiency washer (resulting in 50% of water

saving)• High capacity tumble dryer with energy recycling system• Energy efficiency flatwork ironer• Energy efficiency sheet folder

Green BuildingGT Component including:-• Climate Responsive Building Envelope

(e.g. eco-glass window, sun-shading and heat reflective paint)

• Energy Efficient Air-Conditioning System• Energy Efficient Lighting• Rain water harvesting

Green Technology Financing Scheme (GTFS)

Green Technology Producer ?

The company who involved in production of the green products /components i.e;

Solar energy producer

Energy saver lighting bulb producer

Energy Efficient Air-Conditioning System producer

Eco-glass window producer

Green Technology Financing Scheme (GTFS)

§ Financing will be provided by all commercial & Islamic banks andDevelopment Financial Institutions (DFIs)

§ 0.5% p.a. guarantee fee to the government§ Projects are to be located in Malaysia§ Refinancing is not allowed

PROJECT COMPANY Producer: Max RM50 mil for 15 years max User: Max. RM10 mil for 10 years max

PROJECT COMPANY Producer: Max RM50 mil for 15 years max User: Max. RM10 mil for 10 years max

GREENTECH MALAYSIA(Promotions, Green

Certification, Monitoring)

FINANCIAL INSTITUTIONS(Credit assessment,

financing)

FINANCIAL INSTITUTIONS(Credit assessment,

financing)CREDIT GUARANTEE CORPORATION

(Administer guarantee & rebate)

(1) Green Certificate

(2) Loan(3) 2% rebate & 60% guarantee

Coordinator, Regulator

How to apply?

Rebate Mechanism

Who Qualifies?Good conduct of accounts /credit behavior

No adverse record on the existing loan facility

Aged more than 1½ years with CGC

Rebate upon next LG issuance

Eligible schemes – BizMula-i, Enhancer/Enhancer-I, Enhancer Direct & Enhancer Excel.

Rebate Mechanism

Ø Reduce cost of borrowing – as part of the National Agenda toassist SMEs

• Ease cash flow of SMEs in early stages of growth• Good customers indirectly enjoy “discount” in total guarantee

fees charged.

Ø Encourage and motivate customers to consistently maintaintheir good conduct of account / credit behavior.

Benefits of Rebates

Rebate Mechanism

As at March 2015

REBATE has been granted to 1,027 customers valued

of RM569,926.50

Special Relief Facility 2015

No. Features SRF

1. Source of Funds

BNM

2. Scheme Type Islamic & Conventional

3. Total Facility RM500 million allocation

4. Financing Tenure

Up to 5 years including 6 months of moratorium period on both principal and interest/profit payment.

5. Purpose of Financing

• Repairs and purchases of assets for commercial use to replace those damaged during the flood and working capital only.

• The Facility shall not be used to refinance the existing credit facility.

6. Type of Financing

Term Financing only

7. Eligibility Business

• SMEs affected by the floods located in the districts defined by Majlis Keselamatan Negara, Jabatan Perdana Menteri as flood disaster areas.

• Businesses must be a Malaysian-owned company and institutions registered under the Companies Act 1965, Societies Act 1966 or the Cooperative Societies Act 1993 with at least 51% Malaysian members, and entrepreneurs registered under the Registration of Businesses Act 1956.

• For self-employed individuals or micro enterprises, a valid business registration and/ or business license is sufficient.

Special Relief Facility 2015 (cont’)

No. Features SRF

8. Guarantee Cover

• BNM via CGC will provide 60% guarantee cover on the principal and normal interest, while the remaining 40% credit risk will be borne by the PFIs.

• No guarantee fee will be charged to customers.• PFIs should not require any collateral.

9. Funding Rate to PFIs

Fund to be provided by BNM to PFIs at concessionary rate of 0% p.a.

10. Financing rate • Up to 2.25% effective rate per annum (p.a.).• For Islamic financing, the profit rate for the Islamic contract is also up to 2.25% p.a.

11. Maximum financing amount

An aggregate of RM500,000 per group of companies.

12. Stamp duty Waived for all financing agreements under the Facility.

13. Application deadline

• Facility is open for applications received by the PFIs not later than 30 June 2015 or uponexhaustion of allocation, whichever is earlier.

14. Participating financial institutions

• All commercial banks• All Islamic banks• Small Medium Enterprise Development Bank Malaysia Berhad (SMEBank)• Bank Kerjasama Rakyat MalaysiaBerhad (Bank Rakyat)• Bank Pertanian Malaysia Berhad (Agrobank)• Bank Simpanan Nasional (BSN)