a4 finland

TRANSCRIPT

Taxation in Finland

Basic information about taxation in Finland

● In Finland almost all income is taxed, as are goods and services

● The State, the Municipalities, the Evangelic Lutheran Church

and the Orthodox Church all have the power to levy taxes.

● Direct taxes include state income tax, capital tax, inheritance

and gift tax, and asset transfer tax, all payable to the State

● Municipal tax payable to the appropriate Municipality, and

● Church tax payable to the church.

● Indirect taxes include VAT added to the price of products, and

excise and customs duties.

What is VAT?

● VAT is a consumption tax that the seller of goods or services will add to the price.

● The seller thus collects this tax from customers to remit it to the state.

● Liability to pay VAT concerns anyone who sells goods and services, rents out goods, or is engaged in similar commercial operations on an ongoing basis.

VAT Rates of 2015

● General rate of VAT, effective for most goods

and services

24 %

● Food, animal feed, restaurant services, meal

catering services

14 %

● Books, medicine, services relating to physical

exercise and sports, movies, entrance to

cultural events and to entertainment events,

transport of passengers, accommodation

10 %

Environmental protection tax

● Payed from products which are harmful for health or environment● From the consumer price of gas, over 64% are taxes, 24% of them are VAT● Mild alcohol drinks: +15% ● Strong alcohol drinks +10%

Earned income

● Earned income are wages or salary, and pensions. Similarly, fixed income such as social benefits, compensation, and unemployment relief are regarded as earned income.

● Earned income is a progressive tax. That means the more person earns, the more he/she pays taxes

● In addition, there are two flat rates of tax applicable to earned income, namely municipal tax and church tax (1% to 2%).

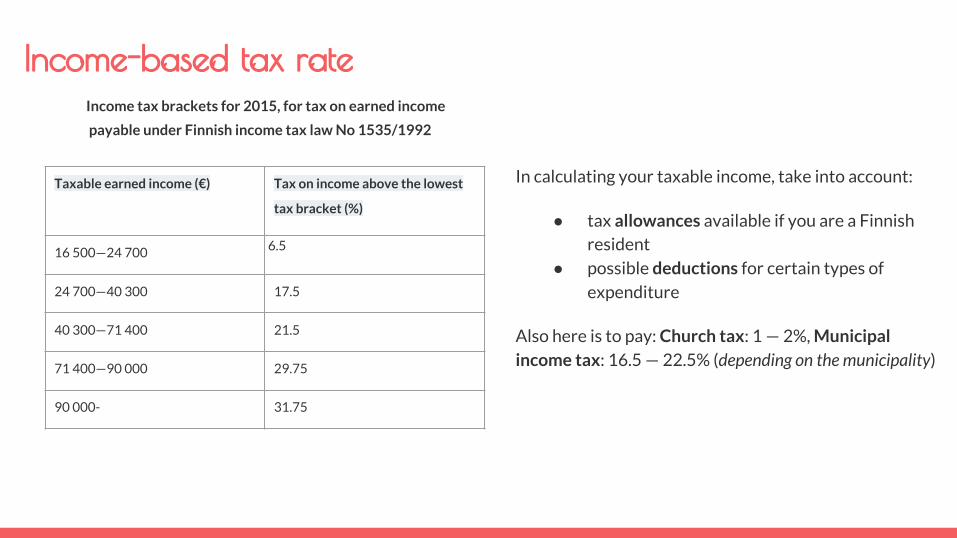

Income tax brackets for 2015, for tax on earned income

payable under Finnish income tax law No 1535/1992

In calculating your taxable income, take into account:

● tax allowances available if you are a Finnish resident

● possible deductions for certain types of

expenditure

Also here is to pay: Church tax: 1 — 2%, Municipal income tax: 16.5 — 22.5% (depending on the municipality)

Taxable earned income (€) Tax on income above the lowest

tax bracket (%)

16 500—24 700 6.5

24 700—40 300 17.5

40 300—71 400 21.5

71 400—90 000 29.75

90 000- 31.75

Income-based tax rate

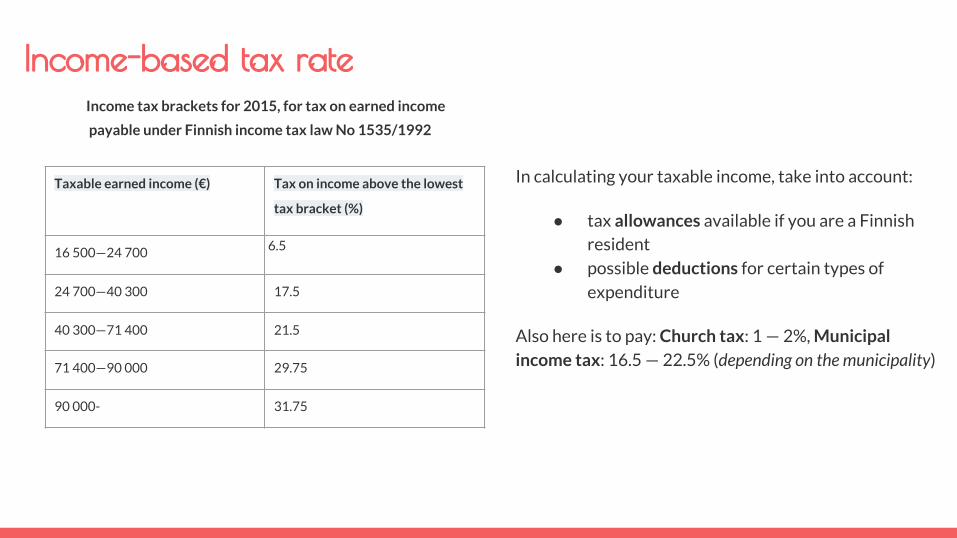

Income tax brackets for 2015, for tax on earned income

payable under Finnish income tax law No 1535/1992

In calculating your taxable income, take into account:

● tax allowances available if you are a Finnish resident

● possible deductions for certain types of

expenditure

Also here is to pay: Church tax: 1 — 2%, Municipal income tax: 16.5 — 22.5% (depending on the municipality)

Taxable earned income (€) Tax on income above the lowest

tax bracket (%)

16 500—24 700 6.5

24 700—40 300 17.5

40 300—71 400 21.5

71 400—90 000 29.75

90 000- 31.75

Income-based tax rate

Capital income

Profits, returns, earnings etc. derived from investments that the taxpayer has made are regarded as capital income. Also regarded as capital income are: Gains from selling an asset, any other income that can be attributed to the fact that the taxpayer has owned assets, dividend income, rental income, capital gains, interest income, proceeds from a life insurance contract, the share of profits of an investment fund.

In 2015 the capital income tax rate is 30% for income up to €30,000 and 33% for

capital income exceeding that amount.

Community charge

● Local income tax paid by residents, real estate tax

and a share of corporate tax account for almost half

of all municipal revenues.

● Community sets their own per cent of community

charge, it could be for example 20% In Kemi

community charge is 21,25% and in Kauniainen

community charge is 16,5.

● And that is it because people who live in Kauniainen

are rich and healthy.

Community charge

Fees and charges account for about a quarter of municipal revenues. Most of the customer charges are

collected for services such as water supply, waste disposal, power supply and public transport. Just under

one tenth of social welfare and health expenditure is covered through customer and patient charges. Basic

education is free.

Central government grants local authorities financial assistance in exchange for a wide range of statutory

services. The central government transfer system evens out financial inequalities between local authorities

and ensures equal access to services throughout the country. Central government transfers account for less

than one-fifth of all municipal revenues.

Tax exemptions= exemption from taxes

In Finland, the general rule of individual taxation is that

you are obligated to pay tax on all your income to the state

and the municipality. On individual taxation incomes are

divided into earned income, investment income and tax-

exempt income.

Tax-exempt incomes are, for instance, income from

self-collected berries and mushrooms, strike pay and

alimony. Besides, some social benefits are also tax-free,

for example child benefit.

Tax exemptions and value added tax

On value added taxation, among other things health and medical care services are tax-free. In addition, if the turnover of the company is less than 10000€ in a year, the company is not obligated to register for VAT, at which time it is able to sell their products exclusive of value added tax.