a worldwide perspective on precision agriculture adoption

TRANSCRIPT

A Worldwide Perspective on Precision Agriculture Adoption

Source: Waldner et al., Remote Sensing, 2015

Is Precision Agriculture

Adoption Linked to

Farm Field Size?

Just in case you are

wondering about Harper

Adams University:

• Harper Adams is a British

public agricultural

research and teaching

university established in

1901

• 200 km northwest of

London in Shropshire

• 5000 students in Agri-

business, Ag Engineering,

Food Science, Animal

Science and Veterinary

Science.

• Campus within a 550

hectare working farm

James Lowenberg-DeBoer, Elizabeth Creak Professor

of Agri-Tech Applied Economics,

Harper Adams University, Newport, Shropshire, UK

Objectives:1) Summarize worldwide

Precision Agriculture

adoption.

2) Develop hypotheses to

understand PA adoption

patterns.

3) Discuss key adoption

challenges in the next

decadeSource: Lowenberg-DeBoer, SAE, 1998

Sparse Data Warning:

• No country systematically collects official data on use of

precision ag technology.

• Only a few governments (i.e. USA, Australia, UK) sporadically

do surveys of PA adoption. Alternative sampling methods may

not provide representative data.

• Manufacturers and PA dealers usually do not reveal sales data –

proprietary information!

• Our knowledge of PA adoption comes from piecing together

data from sporadic and geographically dispersed surveys.

• It is essential to look at adoption by specific practice or

technology. PA is a toolbox. Farmers choose what is useful.

Retailers Adopted GPS Guidance Rapidly for Internal Business Use (% of Retailers)

• Lightbars rapidly adopted starting in late 1990s.

• Autosteer rapidly adopted starting in about 2004.

• Both are easy to use and have short run benefits

24%

42% 44%

56%61%

64%67% 68%

73%

79%

66% 65% 63%

55%

5% 6%

20%27%

37%

53% 63% 61%

83%78%

4% 2% 3% 5%4%

4%

6% 5%8%

11%16%

20%

37%34%

2% 3%1%

3% 3%7%

15%20%

9%

39%

53%

74% 73%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

GPS guidance

GPS guidance with manual control/lightbar

GPS guidance with auto control/ autosteer

GPS for logistics

Telemetry - field-home office

GPS-enabled sprayer boom/nozzle control

Retailers Slower to Adopt Sensing Technologies

• Return for sensing technologies more complicated—no return until data is turned into a decision

• Percent of retailers -Note % scale compared to previous slide

6

12%

19% 20%

24% 18% 20%

20% 19%

27%

35%

32%

41%43%

16%18%

22%20%

28%

30%

30%

39%

51% 52%

6%8%

11%

6%

9%

13%

13%12%

14%

22%16%

24%

4%7%

6%

9%

3% 3%

7%

0%

10%

20%

30%

40%

50%

60%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Field mapping (GIS) for legal/ billing/insur.

Satellite/aerial imagery for internal use

Soil electrical conductivity mapping

UAVs

Chlorophyll/greenness sensors

Other vehicle-mounted soil sensors for mapping

Ag Retailers Slower to Offer Data Gathering Technologies to Customers (% of Retailers)

• Data collection technologies are foundation of data-driven farming

• Intensive soil sampling services have become almost standard practice.

• After many years over 50% offer satellite imagery

• 2020 numbers are their projections

7

33%

45%

38%36%

44%

52%

47%45%45%

40%

53%52% 52%

57%

67%

82%85%

29%

38%37%

34%

41%

50%42%

33%

39%

35%

47% 44%47%

49%

57%

78%83%

24%

29% 23%18%

24%

30%28%29%

27%26%

34% 39%36%

42%

51% 57%

67%

15%20%

15%11%

16%23% 22%

24%23%

19% 24%

29%

29%

27%

41%

48%

12% 13%15%

19%15%

26%

23%

25%

33%

48%

59%

71%

24% 23%

28%

36%39%

14% 13%

19%

34%

45%

32%

59%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Grid or zone soil sampling

Field mapping (with GIS)

Yield monitor and other data analysis

Yield monitor sales/support

Satellite/aerial imagery

Guidance/autosteer sales & support

Soil EC mapping

UAV or drone imagery

Dealer Offerings of Variable Rate Technologies

• % of Retailers

• VRT is the action side of data technologies for data-driven farming

• Most dealers offer VRT services.

• Farmer up take of VRT has been slower

• 2020 are projections

8

81% 84%

20%

32%32%29%

50%

45%

41%43%

47%

43%

56%56%

54% 54%

69%

9%

15% 14%16%

20%

26%23%22%

25%25%

33% 39%42% 42%

64%

33%37%

34% 33%36%

33%

44%44% 45% 45%

59%

67%70%

10%12%12%14%

16%13%

23%23%

22% 22%

27%

17%

42%

3%3% 4% 3% 2%

6% 5% 6%9% 6%

15%

18%

23% 24%

50%

56%

66%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

VRT fertilizer application

VRT Fertilizer, single nutrient

VRT Fertilizer, multiple nutrient

VRT lime application

VRT pesticide application

VRT seeding prescriptions

Farmer Adoption of GNSS Guidance in the USA

• USDA ARMS data has an irregular survey cycle with different crops each year, but it is probably the best data available.

• Easy to imagine that the cloud of data points forms a classic “S” shaped adoption curve for GNSS guidance

• Other data suggests that sprayer boom control, seederrow shut offs and other GNSS guidance related technology has been adopted rapidly by farmers as well as dealers.

Source: Based on data from USDA ARMS - https://data.ers.usda.gov/reports.aspx?ID=17883

5%

15%

45%

5%

20%

45%

10%

35%

11%

23%

26%

53%

4%

49%

0%

10%

20%

30%

40%

50%

60%

2000 2002 2004 2006 2008 2010 2012 2014

Percent of Planted Area on which GPS Guidance Used, USA 2000

to 2013

Corn Soy Winter Wheat Cotton Rice Peanuts

Farmer Adoption of Variable Rate Technology (VRT)

• Farmer use of VRT on cereals and oilseeds rarely exceeds 20% anywhere.

• In spite of widespread availability of VRT services, intense publicity, and subsidies in some counties and states, VRT use by US farmers shows only a slight upward trend.

• The >20% adoption of VRT in the 2010-12 period was during a period of high grain prices. Evidence suggests that farmers have cut back on VRT since to reduce costs. Source: Based on data from USDA ARMS - https://data.ers.usda.gov/reports.aspx?ID=17883

8%

12% 12%

9%

12%

22%

7%

8%

7%

5%

8%

22%

2%

3%

8%

14%

3%4%

5%6%

5%

6%

21%

1%

3%

18%

0%

5%

10%

15%

20%

25%

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

VRT for Any Purpose by Crop 1998-2013

% of planted area

Corn Soy Winter Wheat Cotton Rice Peanuts

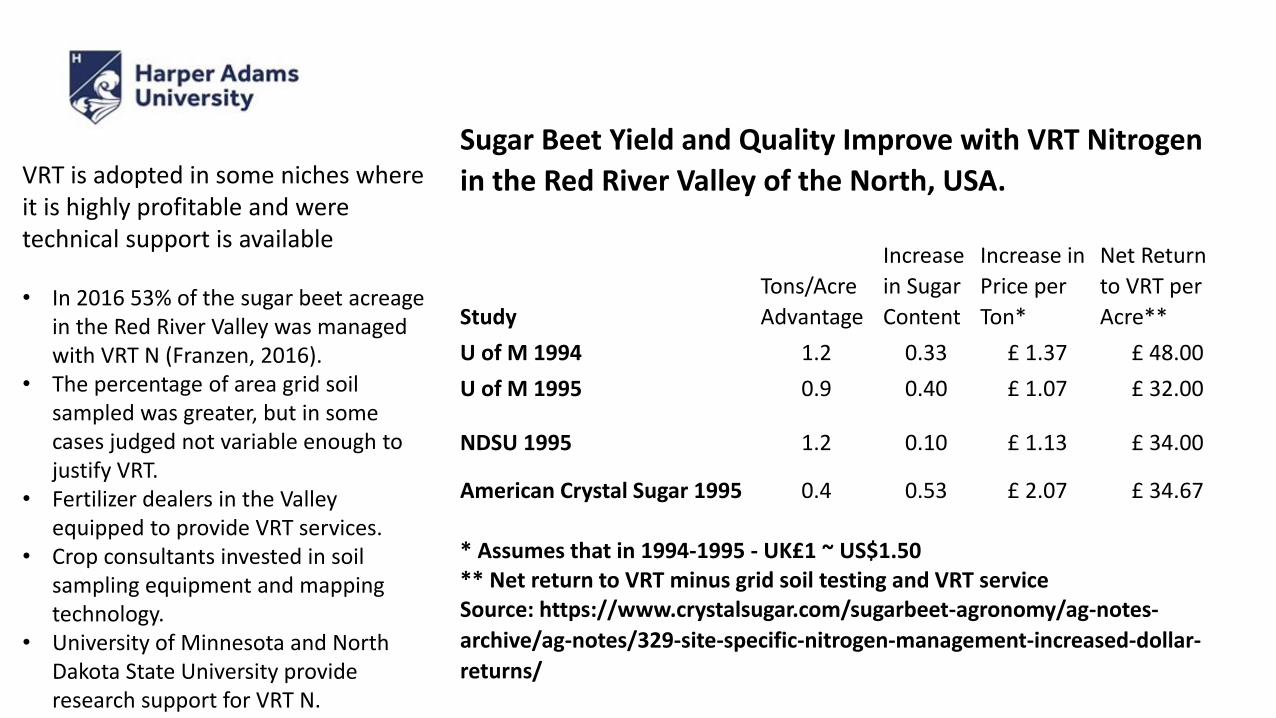

VRT is adopted in some niches where it is highly profitable and were technical support is available

• In 2016 53% of the sugar beet acreage in the Red River Valley was managed with VRT N (Franzen, 2016).

• The percentage of area grid soil sampled was greater, but in some cases judged not variable enough to justify VRT.

• Fertilizer dealers in the Valley equipped to provide VRT services.

• Crop consultants invested in soil sampling equipment and mapping technology.

• University of Minnesota and North Dakota State University provide research support for VRT N.

Sugar Beet Yield and Quality Improve with VRT Nitrogen

in the Red River Valley of the North, USA.

Study

Tons/Acre

Advantage

Increase

in Sugar

Content

Increase in

Price per

Ton*

Net Return

to VRT per

Acre**

U of M 1994 1.2 0.33 £ 1.37 £ 48.00

U of M 1995 0.9 0.40 £ 1.07 £ 32.00

NDSU 1995 1.2 0.10 £ 1.13 £ 34.00

American Crystal Sugar 1995 0.4 0.53 £ 2.07 £ 34.67

* Assumes that in 1994-1995 - UK£1 ~ US$1.50** Net return to VRT minus grid soil testing and VRT serviceSource: https://www.crystalsugar.com/sugarbeet-agronomy/ag-notes-

archive/ag-notes/329-site-specific-nitrogen-management-increased-dollar-

returns/

Farmer Adoption Estimated by Retailers in their Market

• % acres in the retailer’s market area, not % farmers

• GPS guidance becoming standard

• For yield monitor data always a question of use

• 2020 are projections

12

14% 16%20%

22%26%

32%33%

43%

3% 4% 6%

7%9% 9%

13%15%

18% 19%

33%

6%

22%

12% 13%15%

19% 21%17% 18%

22%

27%30%

34%37%

41%

45%

62%

3% 4%

2%

9%17%

3%

4%

3%10%

4% 6%

11%15%

21%

30%

34%

52%

60%

72%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Yield monitor w/ GPS

Satellite or aerial imagery

UAV or drone imagery

Grid or zone soil sampling

Soil EC mapping

Chlorophyll/greenness sensors for N management

Guidance/autosteer

Farmer VRT Adoption Estimated by Retailers

• % acres, not % farmers, in the retailer’s market area

• Substantially higher estimates than USDA and other sources

• Farmer interest in VRT seeding remarkable

• 2020 are projections

13

38%

54%

8%

7%

9% 11%13%15%15%

19% 22%

27% 26% 27% 31%

5%

6% 7% 8%10%10%

13%16% 18%

22%24%

32%

8% 9%11%

15%16%

18% 16%

22%24%

33% 33%31%

41% 40%

51%

2% 3%

4%5% 6%8% 7%

10%9%

10%13% 13% 14%

3%

13%

2% 2% 4%3% 3% 4% 5%

7%9% 10%

13%

30%

0%

10%

20%

30%

40%

50%

60%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

VRT nutrient application

VRT single nutrient application

VRT multiple nutrient application

VRT lime application

VRT pesticide application

VRT seeding prescription

Nutrient Management and Hybrid/Variety Selection Dominate Decisions Based on Farm Data

• 58% of retailers manage and/or archive yield, soil test and other data for farmers.

• 17% pool that data within their customer base.

• 10% pool that data beyond their customers

• Only 13% of retailers do not help customers with farm data

14

17%

18%

29%

20%

31%

25%

33%

23%

37%

55%

85%

44%

39%

34%

40%

39%

45%

38%

42%

37%

30%

10%

29%

32%

28%

32%

22%

27%

27%

30%

25%

11%

3%

10%

11%

9%

7%

8%

3%

3%

4%

2%

5%

1%

0% 20% 40% 60% 80% 100%

Nitrogen decisions

P and K decisions

Liming decisions

Overall hybrid or variety selection

Variable hybrid or variety placement in field

Overall crop planting rates

Variable seeding rate prescriptions

Pesticide selection (herbicides, insecticides, or…

Cropping sequence/rotation decisions

Irrigation decisions

Other

% of respondents

No answer No influence Some influence Major influence on decision

Profitability of Precision Service Offerings

• % of Retailers

• VRT fertilizer related services usually profitable

• Sensing services (e.g. UAV, satellite/aerial imagery, soil EC, chlorophyll sensors) less profitable

11%

6%

5%

7%

27%

19%

19%

17%

26%

30%

23%

5%

22%

31%

23%

29%

26%

13%

5%

4%

4%

6%

9%

9%

14%

16%

29%

12%

5%

8%

0%

6%

20%

10%

45%

21%

11%

20%

25%

32%

37%

39%

36%

27%

27%

28%

33%

42%

27%

27%

44%

31%

68%

80%

69%

42%

39%

35%

31%

22%

14%

38%

61%

38%

27%

44%

24%

20%

0% 20% 40% 60% 80% 100%

Field mapping (with GIS)

VRT fertilizer or lime presc

VRT fertilizer appl

VRT lime appl

VRT pesticide appl

VRT seeding presc

Yield monitor sales/support

Yield monitor and other data analysis

Satellite/aerial imagery

UAV

Guidance/autosteer sales and support

Grid or zone soil sampling

Soil EC mapping

Chlorophyll/greenness sensors

Precision planter equip sales

Telematics equip sales

Profit/cost mapping

% of respondents who offer the service

Don't know Not breaking even Breaking even Making a profit

PA Adoption by Medium and Small Scale Farmers in the USA

• The initial wave of PA technology was designed mainly for large scale, mechanized grain producers.

• Not surprisingly, PA adoption has been concentrated among those large scale producers.

• As PA technology prices decline with mass production and the technology becomes easier to use, the expectation is that it will be used by all mechanized farms.

8

16

2428

8

16

24

3230

51

61

81

0

10

20

30

40

50

60

70

80

90

Smallest Small Med-Small Medium

Maximum Area by Crop for Each Farm Size, hectares

Maize, 2016 Soy, 2012 Rice, 2013

USDA ARMS data is collected by crop.

Analysis focused on the smallest 15% of farms

by crop. What is considered small differs by

crop.

Source: Schimmelpfennig, IaDB, 2017

Like larger farms, small and medium farms in the US are adopting guidance

0%

10%

20%

30%

40%

50%

60%

70%

80%

Maize AutoSteer Maize SoilMapping

Maize VRT fert Maize YieldMapping

Rice AutoSteer Rice Soil mapping Rice VRT fert Rice Yield Mapping Soy AutoSteer Soy Soil Mapping Soy VRT fert Soy Yield Mapping

PA Adoption by Crop & Technology

for Small and Medium Farms, %

Smallest Small Med-Small Medium

The smallest US rice

farms are bigger than

the smallest corn and

soybean farms and

consequently are

adopting guidance

Precision Agriculture In the UK

• Overall, UK adoption of PA is modest, % of farms in 2012:• GPS - 22%• Soil Mapping – 20%• VRT – 16%• Yield Mapping – 11%

• As almost everywhere PA adoption is greater on larger farms and on those specialized in cereals and oilseeds.

• UK pattern similar to rest of the world, but UK has more smaller livestock and mixed farms, and fewer large arable farms which lead PA adoption everywhere

0%

5%

10%

15%

20%

25%

30%

35%

GPS (a) Soil mapping Variable rateapplication

Yield mapping

17% 17%

12%

9%

24%

21%19%

12%

32%

24%

22%

14%

Proportion of UK Holdings Using PA Techniques

Small Medium Large

Source: DEFRA 2012 Farming Practices Survey

In UK data farm size defined by number of workers:

• Small <2 workers

• Medium - 2 or 3 workers

• Large – over 3 workers

• Strong interest in PA for sugar cane

driven by economics & environmental

concerns.

• Public sector research in PA for

viticulture and some adoption of

selective harvest.

• Australia led development of GPS

guidance in part motivated by soil

compaction and profitability of

controlled traffic.

• CSIRO adoptions studies show:

o As in USA, GPS guidance widely

used.

o Many have yield monitors, but do

not use data.

o Note – “Vary Fertilizer Rates”

includes manual variation.

o Lack of technical support identified

as key constraint.Source: Llewellyn & Ouzman, CSIRO, 2014

Precision Agriculture in Australia

• Larger farms in

Latin America have

been part of PA from

the early 1990s.

• Argentine data

collected in terms of

number of machines

• Rapid growth in

GPS guidance

• Variable rate

fertilizer is less than

20% of crop areaSources: Ricardo Melchiori, INTA, Parana, Argentina

Precision Agriculture in Argentina

Precision Agriculture in Brazil

• Strong interest in Precision Ag for sugar – both guidance and

VRT

• Growth in use of GPS guidance

• Interest in VRT fertilizer, but often very coarse resolution (e.g. 5

ha grids).

• Adoption slowed by:

o High cost of technology – in part due to taxes and import

tarifs

o “No Frills” preference because of high capital costs and

composition of the labor force

o Has been more profitable to bring new land into farm

production than to intensify on existing land

Source: J. P. Molin, INFO AG , 2015

79

58

30

28 Variable rate seed

application

Variable rate chemicals

application

Variable rate fertilizer

application

Soil fertility

mapping

5545

Do you use some PA technique?N = 992

No

Yes

N = 443

All indications in %. Based on number of interviews.

Forty Five% of Brazilian grain farmers in 2013

used something from the PA toolbox

Based on Kleffmann Group telephone interviews with 992 large scale farmers in 2013.

and

• Largely because of high soil

testing costs Brazilian

farmers use very large soil

test grid sizes.

• In the 2013 survey 14 %

used larger than 9 ha.

• Almost 50% used larger than

4 ha.

• The grid size used in by

these Brazilian farmers is

larger than the average field

size on many European

farms.

Rethinking Precision Agriculture in Africa

• Use of GNSS guidance and classic PA

technology on farms in South Africa and on

some large scale estates elsewhere.

• Traditional African agriculture is very site-

specific, but manual, so PA technology from

the Americas and Australia does not solve

their problems.

• Rethinking PA for African smallholder

farmers to identify uses that solve African

problems. Some ideas:

➢ Handheld soil nutrient sensors.

➢ Using cell phones to communicate

remote sensing and other sensor based

weather & pest management

information.

• In most areas little or no ag inputs supply

infrastructure, so no PA services or support.

Precision Agriculture in Europe

• PA technology developed in the Americas or Australia often not a good fit, in part because of

smaller farm size.

• European PA adoption estimates are “soft” because only the UK government collects random

sample data. In other countries number are based on on-line survey and other methods

• Interest in GNSS guidance growing especially in areas with relatively large farm size such as

eastern Germany

• Use of on-the-go sensing for fertilizer application probably highest in the world because:

o Relatively higher N prices

o Higher grain prices

o Environmental regulation limits N use in some countries

o Government support for N sensor use

• Growing interest in PA technologies that fit European farming, including:

o Controlled traffic

o Precision livestock, especially robotic milking

o Precision horticulture and viticulture

8%

4%3%

32%

9%

4%3%

8% 8%

0%

5%

10%

15%

20%

25%

30%

35%

Germany Denmark Finland

PA in N. Europe, 2011

Variable Rate Fertilizer GPS Autoguidance Robotic Milking

“The most successful example of PA on

arable land is the use of Controlled Traffic

Farming (CTF), which has been able to

reduce machinery and input costs up to 75%

in some cases, whilst also increasing crop

yield.” (EU Directorate-General for Internal

Policies – Agriculture & Rural Dev., 2014)

Source: Lartey et al. (Computers & Electronics

in Agriculture, 2011) – Survey of farmers in

four European countries

European Farmers Taking Time to find PA

Technology that Fits Their Needs

PA Adoption Summary –GNSS Guidance Success Story

• GNSS guidance being widely adopted on mechanized farms almost everywhere.

• Sprayer boom control, seed row shut offs and other technology linked to GNSS guidance being widely adopted.

• Hypothesis #1 - Investment in GPS guidance and related technologies cashflowed by reduction in overlap and more efficient field operations. Other benefits (e.g. reduced fatigue, flexibility in hiring) are unquantified side effects.

• Hypothesis #2 – GPS guidance technology is not disruptive and consequently is easily sold through existing agribusiness channels

Variable Rate Technology Adoption has Lagged

• Variable Rate Technology (VRT) being adopted in niches where it is highly profitable. For example, sugar beet growers in the USA, in the Red River Valley of the North, Minnesota and North Dakota.

• VRT adoption for all broad acre crops only rarely exceeds 20% of area or farms.

• Hypothesis #3 - Constraints to VRT adoption include:• High cost of site specific information (e.g. grid or zone soil sampling)

• Cost of developing individualized prescription maps

• Lack of demonstrated value – impact on yields and profits often hard to see

• Cost of being wrong (and over applying) is often small because environmental impacts not measured

• VRT is disruptive technology that would require substantial changes in agronomic practices and in business models.

Challenge #1 - On-the-go sensors & fertilizer application

29

Source: Fritzmeirer-umwelttechnik.com

• The hypothesis is that VRT fertilizer adoption has lagged

for bulk commodities because of current technology is

knowledge intensive, requires human intervention at

several points and yields only modest benefits.

• The most likely technical solution is on-the-go fertilizer

sensor and applicator combinations that embody current

knowledge and reduce need for direct human

intervention.

• Combining on-the-go sensors measurements with some

estimate of crop response capacity (e.g. soil depth, yield

maps) can fine tune the fertilizer application.

• Currently most advanced for nitrogen application, but

could be developed for P, K, lime and micronutrients.

Challenge #2 – Pest management at the individual plant level

https://www.harper-adams.ac.uk/news/203084/field-robot-event-comes-to-uk-for-the-first-time

https://www.deere.co.uk/en/our-company/news-and-media/press-releases/2017/sep/deere-and-company-to-acquire-blue-river-technology.html

John Deere Blue River “see and spray” tech.

Field robot competition at Harper Adams University in June 2017

• The future of crop pest management may use

conventional pesticides, but in much smaller

quantities, because they are applied only to specific

weeds, insects or diseased plants.

• That plant or insect specific application might be

by large scale equipment or small robots.

• Robotic pesticide application could be adapted to

small farms.

Challenge #3 - Proof of Concept for Big Data and Artificial Intelligence in Agriculture

• In theory “Big Data” gives us the opportunity to systematically learn from cropping experience, but lack objective data on distribution of benefits.

• In practice, the use of big data in agriculture are limited by the lack of a good business model for farmer data pooling. Some options:• Paying farmers for data in cash or discounts on inputs

• Benchmarking relativeto other farmers in their area and other analysis

• Cooperative models that commit to sharing benefits of data pooling with farmers

• Given the transactions costs of pooling farm data, the Big Data proof of concept may come very large farms in places like the Ukraine, Kazakhstan, or Brazil, rather than pooling data from medium and small. The transactions costs would be lower.

31

Challenge #4 – The biggest PA market opportunity is low cost technology for small and medium farms

For example, soil or optical fertilizer sensors:

• In the developing world soil tests are expensive and not easily available.

• Smallholder farmers lack information about the type and amount of fertilizer that their crops need.

• Research has show the potential of handheld nitrogen senors on medium and small farms, But the cost of the sensors is still too high.

• To achieve widespread use an N sensor should cost < US$10.

• To attain the required price threshold the sensor will probably be a cell phone app or accessory

32

Research in the Yaqui Valley of Mexico shows that use of sensor based nitrogen management can improve farm profits and benefit the environment

Source: CIMMYT

James Lowenberg-DeBoer

Elizabeth Creak Professor of Agri-Tech Applied Economics

Take home message:• GPS guidance and related technology is being adopted worldwide by

mechanized agriculture because it is easy to use, benefits are seen quickly, and it does not disrupt agribusiness structure.

• VRT adoption for bulk commodity crops has lagged worldwide because it is more complicated, technology is not mature, and it is more disruptive.

• Precision agriculture adoption challenges in the next decade include:

• On-the-go sensors and application for fertilizer

• Plant level pest management

• Proof of concept for value of Big Data and artificial intelligence in agriculture

• Precision agriculture technology for small and medium farms