a study to determine the significance of market

TRANSCRIPT

A STUDY TO D E T E R M I N E T H E S I G N I F I C A N C E O F

M A R K E T P E N E T R A T I O N IN T H E CONSUMER

E L E C T R O N I C P R O D U C T S INDUSTRY

A P P R O V E D :

G r a d u a t e C o m m i t t e e :

^ a j o r P r o f e s s o r t c Vj

C o m m i t t e e M e m b e r

Memjyg

Corn

vwf R u s i n e s s v A d m i n i D e a n of t h ^ C o l l e g e of Bus in.es s^Admini s t r a t i on

Dean of trie G r a d u a t e School

ABSTRACT

Thornton , Nelson JL,, J r . , _A Study to D e t e r m i n e the Signi f icance

of Ma.rket P e n e t r a t i o n in the Consumer E lec t ron i c P r o d u c t s Indus t ry .

Doctor of Phi losophy (Marketing), May, 1973, 291 p p . , 45 t a b l e s ,

b ib l iography , 252 t i t l e s .

The p u r p o s e s of th is s tudy, in addi t ion to t e s t ing the h y p o t h e s e s ,

w e r e to p r e p a r e an a n a l y s i s of the s i ze , growth, s t r u c t u r e , and p r o b -

l e m s of the indus t ry ; d e t e r m i n e the inf luence of i m p o r t s on the gen -

e r a l s t r u c t u r e of the indus t ry ; d e t e r m i n e the s ign i f i cance of m a r k e t

p e n e t r a t i o n to d o m e s t i c m a n i u a c t u r e r s , w h o l e s a l e r s , r e t a i l e r s , and

f o r e i g n m a n u f a c t u r e r s and i m p o r t e r s ; and e x a m i n e the m a r k e t p e n e -

t r a t i o n r e p o r t i n g m e c h a n i s m , i ts a c c u r a c y , u s e f u l n e s s , p r o m p t n e s s

in feedback of da ta , and the advan tages and d i s advan tages of m a i n -

ta in ing s e c r e c y of da ta . The hypo theses w e r e t h e s e : t he m e c h a n i s m

f o r r e c o r d i n g and r epo r t ing indus t ry s a l e s is i n a c c u r a t e ; and t he d e -

s i r e of United States m a n u f a c t u r e r s to m a i n t a i n or i n c r e a s e m a r k e t

p e n e t r a t i o n r e s u l t s in g r e a t e r e m p h a s i s on s a l e s of uni ts than on

do l l a r s a l e s or p ro f i t p e r p roduc t group, comple t e con t ro l o r d o m i -

nance by the m a n u f a c t u r e r of the m a r k e t i n g channe l s , the power of

the m a n u f a c t u r e r to e s t a b l i s h and cont ro l p r i c e s at the w h o l e s a l e and

r e t a i l l eve l , t he power of the m a n u f a c t u r e r to f o r c e fu l l l ine se l l ing ,

* I \

t

the power of the m a m i f a c t u r e r to con t ro l m a r k e t i n g a c t i v i t i e s of i t s

who lesa l ing and r e t a i l i ng organizat ion, s t r u c t u r e , and r educed p r o f i t s

f o r the w h o l e s a l e r and r e t a i l e r f r o m what they o t h e r w i s e would b e .

P r i m a r y data w e r e obtained f r o m p e r s o n a l i n t e rv i ews wi th

r e t a i l e r s and w h o l e s a l e r s , and f r o m q u e s t i o n n a i r e s comple t ed by

m a n u f a c t u r e r s and i m p o r t e r s , w h o l e s a l e r s , r e t a i l e r s , l a r g e s c a l e

r e t a i l e r s , and spec i a l u s e r s cf the p roduc t . Unpublished da ta w e r e

f u r n i s h e d by g o v e r n m e n t agenc ie s , t r a d e a s s o c i a t i o n s , and o t h e r s

a s s o c i a t e d with the i ndus t ry . Secondary data w e r e d r a w n f r o m

c u r r e n t books and p e r i o d i c a l s .

P r e l i m i n a r y in t e rv i ews with m e m b e r s of the i ndus t ry r e v e a l e d

m a r k e t pene t r a t i on to be of s ign i f i can t i m p o r t a n c e to t he i ndus t ry .

A need to ana lyze the p r o b l e m s of the i n d u s t r y in a l l a r e a s which

r e l a t e to m a r k e t p e n e t r a t i o n was d e t e r m i n e d . These p r o b l e m s

w e r e : an ana ly s i s of the indus t ry and its r e p o r t i n g m e c h a n i s m f o r

r e c o r d i n g data , the i m p o r t a n c e of i m p o r t s , m a r k e t p e n e t r a t i o n ,

m a r k e t and sa l e s potent ia l , d i s t r ibu t ion , p roduc t , p r i c i n g , p r o -

mot ion , a t t i tudes of the m a r k e t , c o n s u m e r i s m , channel conf l ic t ,

and the l ega l env i ronmen t .

The study inc ludes s ix c h a p t e r s . Chapter I is the in t roduc t ion .

Chapte r II p r e s e n t s an a n a l y s i s of t he growth of the i ndus t ry , in-

cluding i m p o r t s . Chap te r s III and IV d i s c u s s the p r o b l e m s of the

i ndus t ry in the areas which r e l a t e t e m a r k e t p e n e t r a t i o n . Chap te r

V is a n a n a l y s i s of the data compi led f r o m comple t ed q u e s t i o n n a i r e s .

Chapter VI inc ludes the summary , conc lus ions , and r e c o m m e n d a -

t i o n s .

The f indings of the s tudy r e v e a l the i n d u s t r y to be of con-

s i d e r a b l e s i ae , highly c o n c e n t r a t e d a t the m a n u f a c t u r i n g l eve l ,

e x t r e m e l y compet i t ive , and unde r i n c r e a s e d p r e s s u r e s f r o m f o r e i g n

goods . It is concluded t h a t m a r k e t p e n e t r a t i o n is u s e d both a s a

m e a s u r e m e n t tool and a s a company goal . F u r t h e r m o r e , it i s

concluded tha t the d e s i r e f o r main ta in ing o r i n c r e a s i n g m a r k e t

p e n e t r a t i o n r e s u l t s in the power of the m a n u f a c t u r e r and o t h e r

s u p p l i e r s to e s t a b l i s h and con t ro l p r i c e s , to f o r c e fu l l l ine se l l ing

even of unpro f i t ab l e p r o d u c t s , and to con t ro l the m a r k e t i n g a c -

t i v i t i e s of o t h e r s . The d e s i r e f o r m a r k e t p e n e t r a t i o n c a u s e s e m -

p h a s i s to be p laced on unit s a l e s r a t h e r than do l l a r s a l e s o r p r o f i t ,

and t he r e s u l t is l ower p r o f i t s f o r w h o l e s a l e r s and r e t a i l e r s than

would o t h e r w i s e have b e e n r e a l i z e d .

Since the d e s i r e f o r ma in t a in ing or i n c r e a s i n g m a r k e t p e n e -

t r a t i o n r e s u l t s in m a n y p o s s i b l y i l legal p r a c t i c e s and d e e m p h a s i z e s

p r o f i t , it is r e c o m m e n d e d tha t m a r k e t p e n e t r a t i o n not be u s e d a s a

company goal . It should be used a s a m e a s u r e m e n t too l only when

the da ta is known to b e a c c u r a t e .

A STUDY TO D E T E R M I N E T H E SIGNIFICANCE O F

IViARKET P E N E T R A T I O N IN THE CONSUMER

E L E C T R O N I C P R O D U C T S INDUSTRY

DISSERTATION

P r e s e n t e d to t he G r a d u a t e Counci l of t h e

N o r t h T e x a s Sta te U n i v e r s i t y in P a r t i a l

F u l f i l l m e n t of t h e R e q u i r e m e n t s

F o r the D e g r e e of

DOCTOR O F PHILOSOPHY

By

N e l s o n L. Thorn ton , J r . , B. B. A. , M, B. A,

Denton, T e x a s

May, 1973

Copyright by-

Nelson L. Thornton, J r .

1973

TABLE O F CONTENTS

"Pa. a 0

J. < 0 w

LIST OF TABLES . . v i

Chap te r

L INTRODUCTION . . . • • • 1

i Background of the Consumer E l e c t r o n i c

P r o d u c t s Indus t ry Pu r p o s e of th i s Inves t iga t ion Hypotheses of Study Sources of Data Methods of Study Definition of T e r m s Del im ita t ions O r d e r of P r e s e n t a t i o n

JL AN ANALYSIS O F THE CONSUMER ELECTRONIC PRODUCTS INDUSTRY 13

E a r l y F o r m a t i o n of the E l ec t ron i c Indus t ry Genera l Growth of the E l e c t r o n i c s Indus t ry Individual P roduc t Sales Growth Census C o m p a r i s o n of Growth Individual Product. Development S t r u c t u r e of the Indust ry Compet i t ion Signi f icance of Impor t s to Indus t ry

III. MARKET PENETRATION. MARKET POTENTIAL, AND THE REPORTING MECHANISM FOR RECORDING INDUSTRY DATA . 73

P r o b l e m s of the Indus t ry Ma rket Penetration Marke t and Sales Po ten t i a l The Report ing M e c h a n i s m fo r Record ing

Indus t ry Data

Chapte r Pa g®

IV. THE MARKETING MIX AND OTHER INDUSTRY PROBLEMS 1 IT

Other P r o b l e m s of the Indus t ry Dis t r ibu t ion P r o b l e m s P roduc t P r o b l e m s P r i c i n g P r o b l e m s P r o m o t i o n P r o b l e m s At t i tudes of the Marke t C o n s u m e r i s m Channel Confl ic t Channel Cont ro l Legal Env i ronmen t

V. PRESENTATION AND ANALYSIS O F PRIMARY DATA . . . 16?

Sample Size and Response Quality and Coverage of Response Value of Study The Signi f icance of Marke t P e n e t r a t i o n The Repor t ing Sys tem f o r Record ing

Marke t P e n e t r a t i o n Data Signif icance of Dol la r and Unit Sales Control o r Dominance of the Marke t ing Channel The Power to Control P r i c e s The Power to Control Market ing Ac t iv i t i e s The Power of the Supplier to F o r c e

Ful l Line Selling P r o f i t Re la t ionsh ips Other P r o b l e m s of the Indus t ry Ways to I n c r e a s e Marke t P e n e t r a t i o n

VI. SUMMARY, CONCLUSIONS, AND RECOMMENDATIONS 221

S u m m a r y Conclus ions R e c o m m e n d a t i o n s

A P P E N D I C E S 241

BIBLIOGRAPHY 273

v

LIST O F TABLES

Tab le P a g e

I. Indus t ry S u m m a r y of F a c t o r y Sales by Selected Y e a r s , 1925 -1970 16

II. Total U. S. Sales of Te lev i s ion R e c e i v e r s , Rad ios , Phonographs and R e c o r d s 1960-1970 . . . . » . « . 19

III. Quantity and Value of Shipments of a l l

P r o d u c e r s : 1967 and 1963; F o r Home Use 20

IV. F a c t o r y Sales of C o n s u m e r P r o d u c t s 23

V. Tota l U. S. Sales of Audio Home Magnet ic Tape

R e c o r d e r s and R e p r o d u c e r s , 1960-1970 . . . . . . 25

VI. Tota l U. S. Sales of Phonographs , 1946-1970 28

VII. U. S. Radio Set Sales 1922-1949 31

VIII. Total U. S. Sales of Radios , 1950-1970 32

IX. Tota l U. S. Sales of Te lev i s ion R e c e i v e r s , 1946-1970 36

X. R e t a i l e r s and Publ ic Level P u r v e y o r s in Some p h a s e of A p p l i a n c e - R a d i o - T V Merchand i s ing . . . . 45

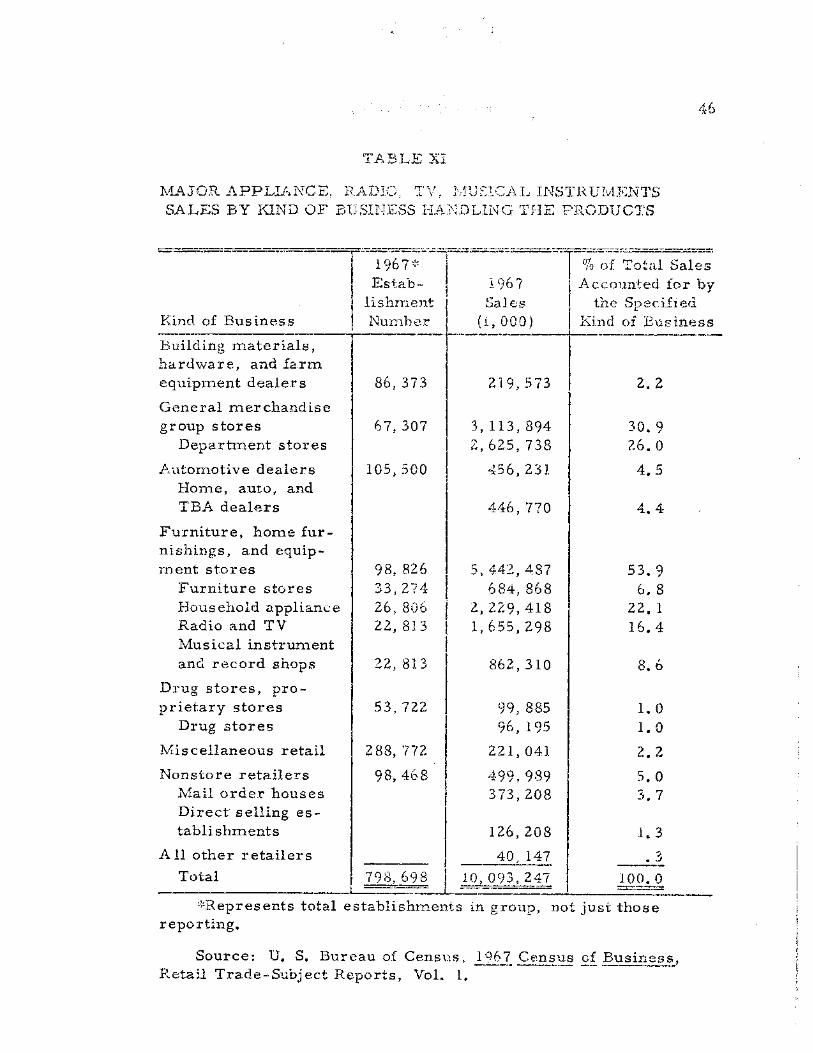

XI. Ma jo r Appl iance , Radio, TV, Musica l I n s t r u m e n t s Sales by kind of B u s i n e s s Handling the P r o d u c t s . . 46

XII. Repor ted Sales of Home E n t e r t a i n m e n t Lines by Type of Outlet , 1967, 1963 49

XIII. Te lev i s ion R e c e i v e r s (Monochrome and Color ) and Combina t ions , U. S. Shipments , I m p o r t s f o r Consumption, Expor t s of Domes t i c M e r c h a n d i s e , and Apparen t Consumpt ion , 1966-71 . 59

vi

Table Page

XIV, Radio R e c e i v e r s - -U. S. Shipments , I m p o r t s f o r Consumption, Expor t s of Domes t i c Merchand i se , and Appa ren t Consumpt ion , 1966-71 . 61

XV. Phonographs and Record P l a y e r s - -U . S. Sh ipments , I m p o r t s f o r Consumpt ion , Expor t s of Domes t i c M e r c h a n d i s e , and Apparen t Consumption, 1966-71 . 62

XVI. Radio - P h o n o g r a p h Combinat ions - - U . S. Sh ipments , Impor t s f o r Consumpt ion, Expor t s of D o m e s t i c M e r c h a n d i s e , and Apparen t Consumpt ion , 1966 -71 . 64

XVII. Tape P l a y e r s and R e c o r d e r s - -U. S. Sh ipments , I m p o r t s f o r Consumpt ion and Appa ren t Con-sumpt ion , 1966-71 . . . . . . . 66

XVIII. Sample Size and Response by Segment of Indus t ry . . 169

XXIV.

P® XIX. Job Con'

s i t ion Held by P e r s o n s plet ing Ques t i onna i r e s „ 173

XX. Types Man

of F r o d u c t s Marke ted by u f a c t u r e r s and I m p o r t e r s

XXI. Marke t Eva and

P e n e t r a t i o n a s a Signif icant Means of luat ing M a n u f a c t u r e r s , W h o l e s a l e r s , R e t a i l e r s

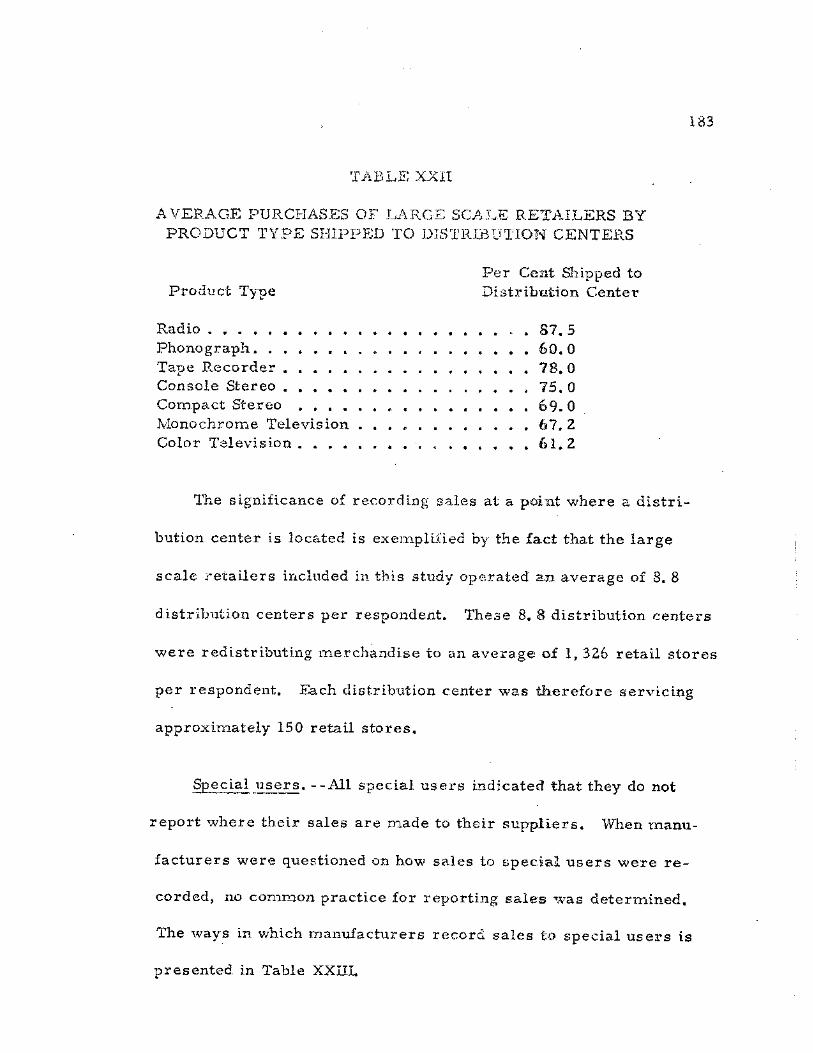

XXIL A ve ra ge P u r c h a s e s of L a r g e Scale R e t a i l e r s by P r o d u c t Type Shipped to Dis t r ibu t ion C e n t e r s

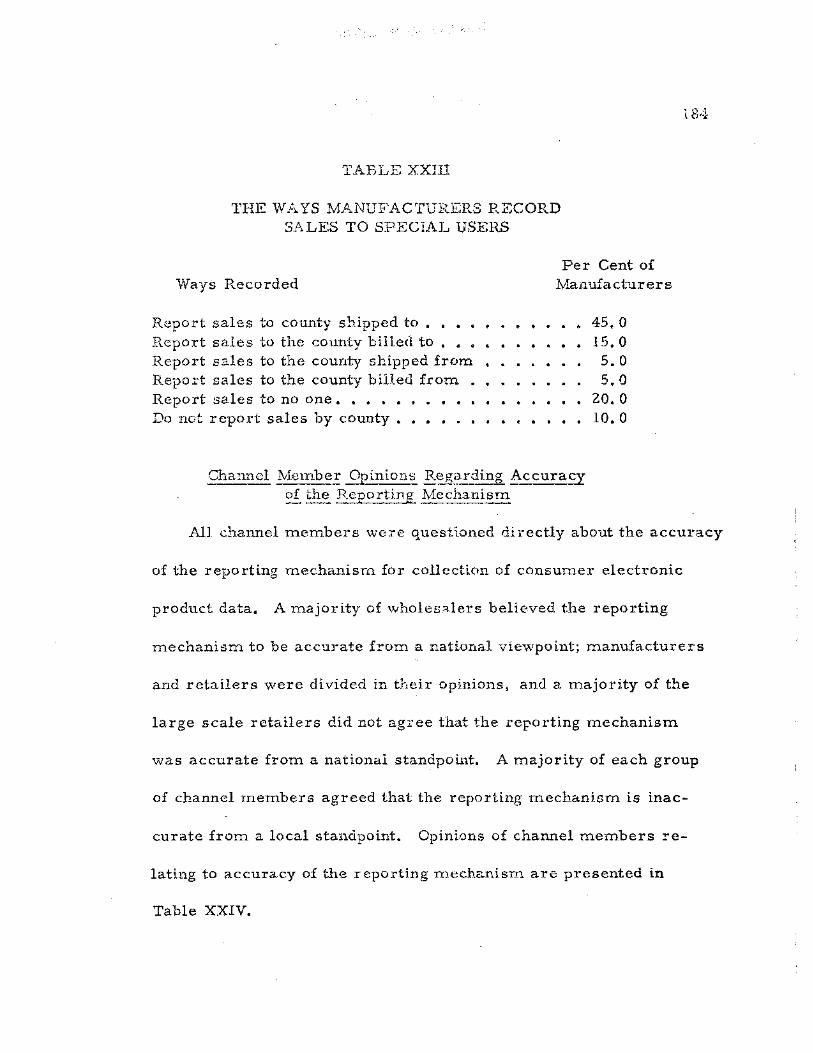

XXIII. The Ways M a n u f a c t u r e r s Record Sales to Special U s e r s

Opinions of Channel M e m b e r s Relat ing to A c c u r a c y of the Repor t ing Mechan i sm f r o m a Najtional and Local Viewpoint . . . . . . .

XXV. Channel M e m b e r s Agree ing Marke t P e n e t r a t i o n Data is Re tu rned Soon Enough to be of Value .

174

179

183

184

185

185

v u

Table

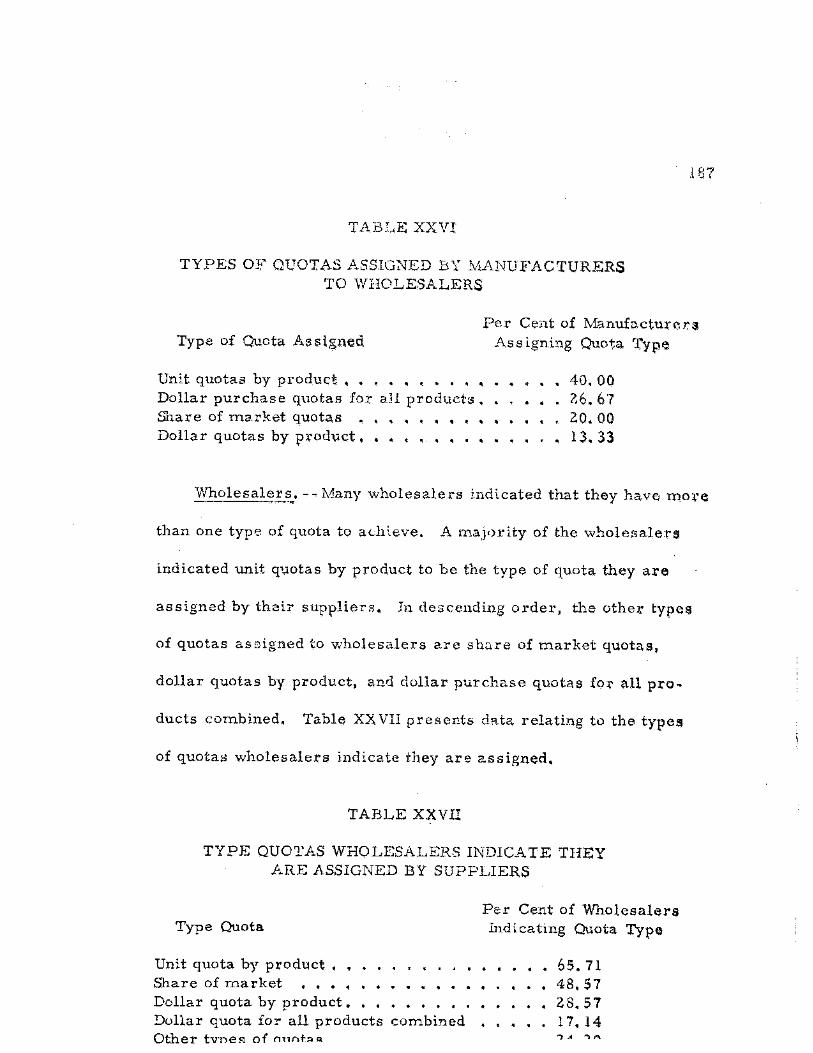

XXVI. Types of Quotas Ass igned by M a n u f a c t u r e r s to Who le sa l e r s . .

Page

IS?

XXVII, Type Quotas 'Wholesalers Indica te They a r e Ass igned by Suppl ie rs . . . . . .

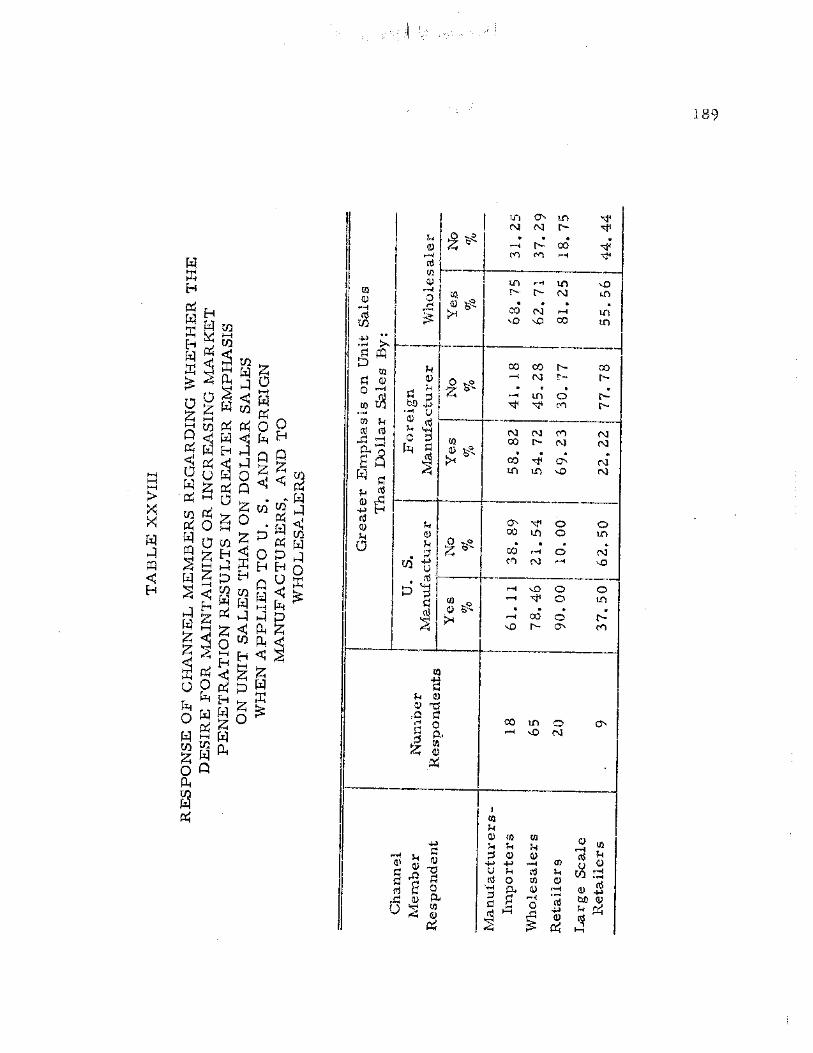

XXVIII. Response of Channel M e m b e r s Regard ing "Whether the D e s i r e f o r Maintaining o r I nc r ea s ing M a r k e t P e n e t r a t i o n Resu l t s in G r e a t e r E m p h a s i s on Unit Sales than on Dol lar Sales when Applied to U. 3. and F o r e i g n Manuf a c t u r e r s , and to W h o l e s a l e r s

187

189

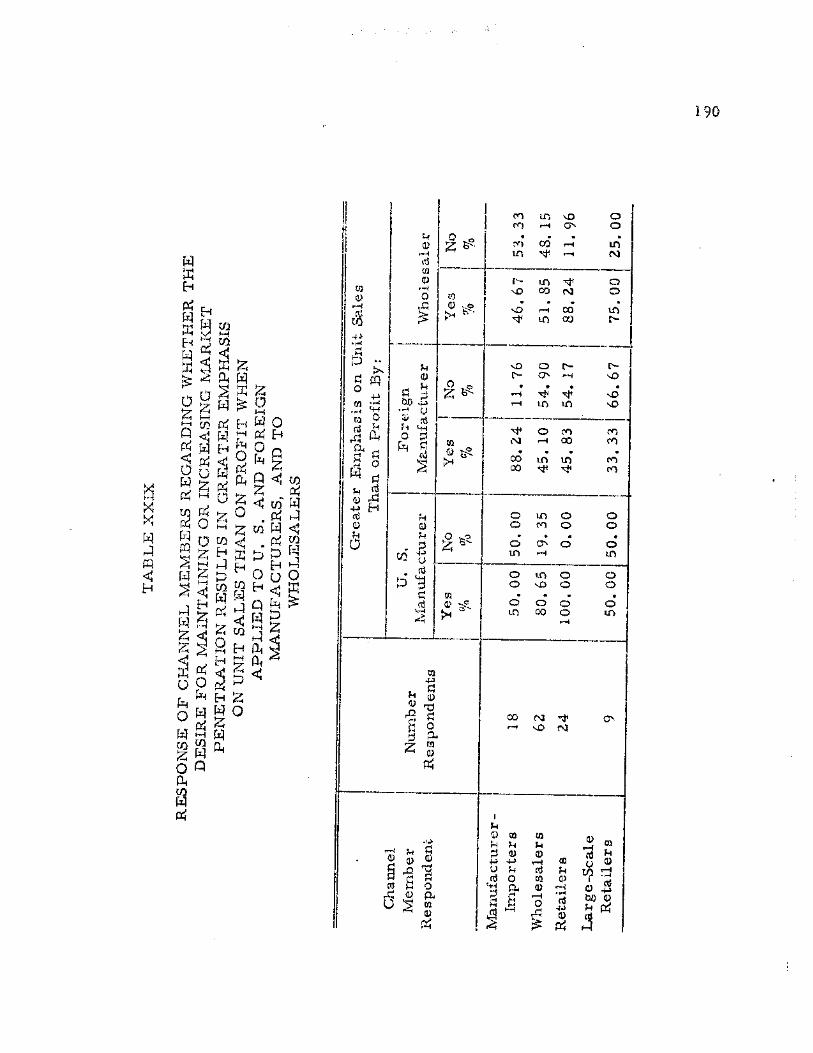

XXIX. Response of Channel M e m b e r s Regard ing Whether the D e s i r e f o r Maintaining or I n c r e a s i n g M a r k e t P e n e t r a t i o n Resu l t s in G r e a t e r E m p h a s i s on Unit Sales than on P r o f i t when Applied to U. S. and F o r e i g n M a n u f a c t u r e r s , and to W h o l e s a l e r s . . 190

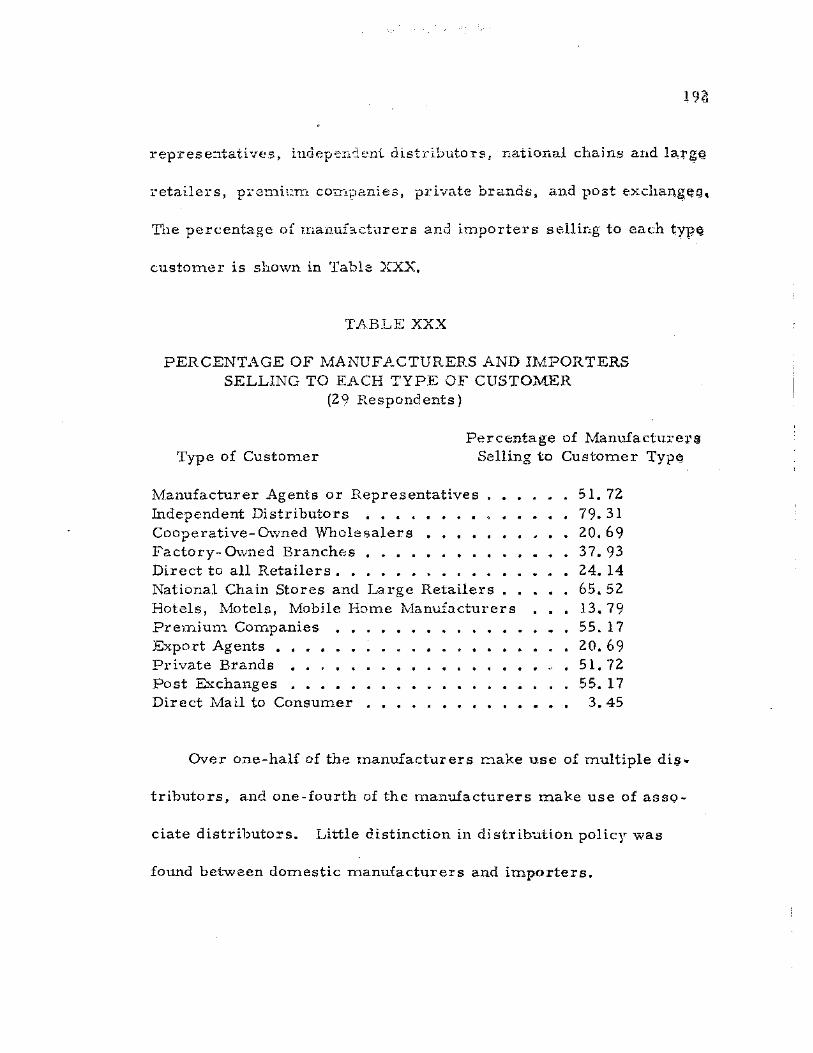

XXX. P e r c e n t a g e of M a n u f a c t u r e r s and I m p o r t e r s Selling to Each Type of C u s t o m e r 192

XXXI. P r i c e Bes t Desc r ib ing P u r c h a s e P r i c e of Special U s e r s 195

XXXII. P u r c h a s i n g P r a c t i c e s of Special U s e r s by P e r c e n t a g e Fol lowing P r a c t i c e 196

XXXIII. Response of Channel M e m b e r s Regard ing Whether the D e s i r e f o r Mainta ining o r I n c r e a s i n g Marke t P e n e t r a t i o n r e s u l t s i.n Dominance of the Market ing Channel when Applied to U. S. M a n u f a c t u r e r s , F o r e i g n M a n u f a c t u r e r s , and to Who le sa l e r s 199

XXXIV. Response of Channel M e m b e r s Regard ing Whether the D e s i r e f o r Maintaining or I n c r e a s i n g Marke t Pene t r a t i on Resu l t s in the Power of the M a n u f a c t u r e r to Es t ab l i sh and Cont ro l P r i c e s at the Wholesa le and Reta i l Leve l . . . . 202

v i u

Tabl« Fag?

XXXV. Response of Channel Members Regarding Whether the Des i re for Maintaining o r Increasing Market Penet ra t ion Resul ts in the Power of the Wholesaler to Es tab l i sh and Control P r i c e s at the Retai l Level , * , 203

XXXVI. Response of Channel Members Regarding Whether the Des i re for Maintaining o r Increasing Market Pene t ra t ion Resul t s in the Power of the Manufacturer to Control Marketing Activit ies of its Wholesaling and Retailing Organization St ructure 205

XXXVII. Response of Channel Members Regarding Whether the Desire for Maintaining o r Increasing Market Penet ra t ion Resul ts in the Power of the Wholesaler to Control Marketing Activit ies of its Retai l Organi -zation St ruc ture 206

XXXVIII. Response of Channel Members Regarding Whether the Desire fo r Maintaining or Increasing Market Penet ra t ion Resul ts in the Power of the Supplier to F o r c e Foil Line Selling, Even on Products which a r e Unprofitable, when Applied to U. S. Manu-f a c t u r e r s , Fore ign Manufac ture rs , and to Wholesalers 208

XXXIX. Prof i t Rating by Product as Applied by Channel Member Group 209

XL. Reasons Indicated by Channel Members f o r Continuing to Car ry Marginal P ro f i t and Unprofitable Produc ts 212

XLI. Response of Channel Members Regarding Whether the Desi re of Manufac turers to Maintain or Increase Market Pene t ra t ion Results in Reduced Prof i t s for the Whole-sa le r and Reta i ler F r o m What They Otherwise Would Be 214

IX

Table P a g e

XL.JL Response of Channel M e m b e r s Rega rd ing Whether the D e s i r e of W h o l e s a l e r s to Maintain or .Increase Marke t P e n e t r a t i o n Resu l t s in Reduced P r o f i t s f o r t h e R e t a i l e r F r o m What They O t h e r w i s e Would Be . <. 2.15

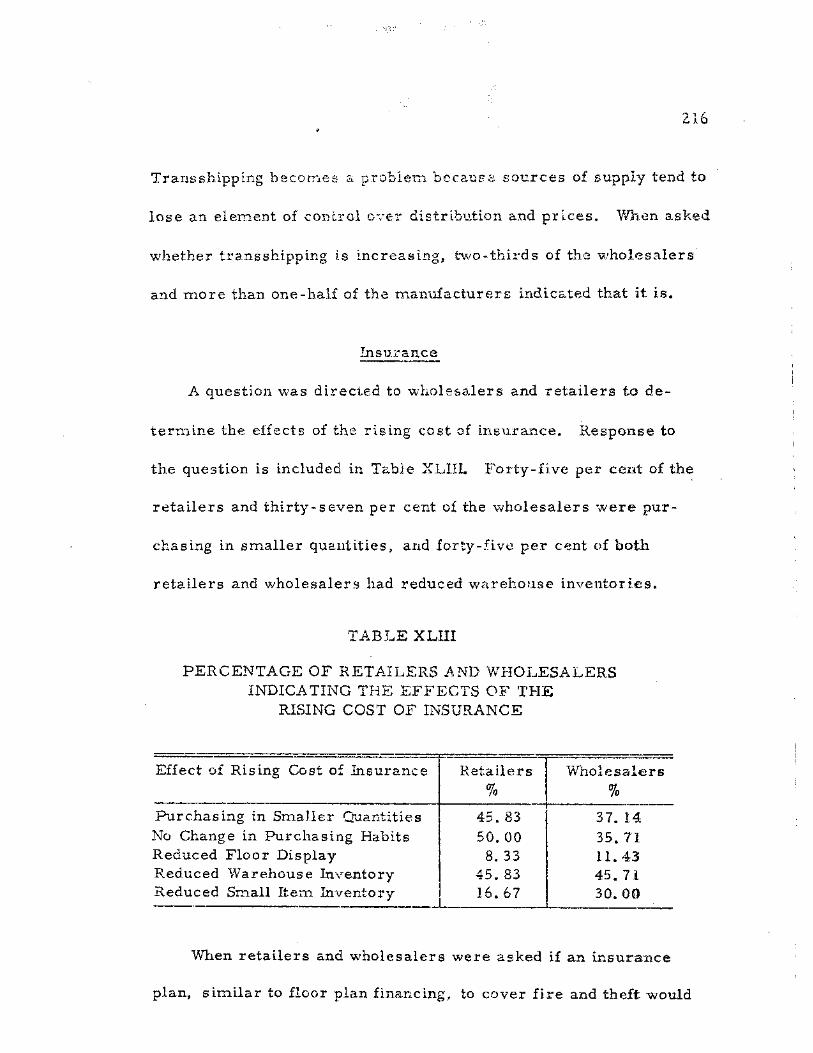

XLIIL Percentage of R e t a i l e r s and W h o l e s a l e r s Indicating tb.e E f f e c t s cf the Ris ing Cost of Insurance 216

XLIV. Percentage of Channel M e m b e r s Rat ing the Effects of Publ i shed R e p o r t s of Private Test ing Organ iza t ions 217

XLV. Response of Channel M e m b e r s Agree ing That C o n s u m e r Tes t ing Organ iza t ions P rov ide a F a i r Tes t of a P r o d u c t 218

CHAPTER I

INTRODUCTION

Background of the C o n s u m e r E l e c t r o n i c P r o d u c t s Indus t ry

The dynamic n a t u r e of the indus t ry , the? l a r g e po ten t ia l vo lume

of b u s i n e s s ava i lab le , and the in tense compet i t ion which e x i s t s h a s

tended to cause the c o n s u m e r e l e c t r o n i c p r o d u c t s i n d u s t r y to

eva lua t e i tself on the b a s i s of i ts s h a r e of m a r k e t in each p roduc t

c a t e g o r y . Share of m a r k e t is g e n e r a l l y d i s c u s s e d in t e r m s of

" m a r k e t pene t r a t i on . " Since a s ingle p e r c e n t a g e point change in

m a r k e t s h a r e in any p r o d u c t c l a s s amoun t s to s e v e r a l mi l l ion

d o l l a r s o r t ens of t housands of un i t s in s a l e s , the s i gn i f i c ance of

m a r k e t p e n e t r a t i o n to the m a n u f a c t u r e r b e c o m e s m o r e a p p a r e n t .

Until r e c e n t y e a r s , United States m a n u f a c t u r e r s have been ab le

to domina t e the d o m e s t i c m a r k e t fo r c o n s u m e r e l e c t r o n i c p r o d u c t s .

Recen t ly , however , i m p o r t p roduc t s have p e n e t r a t e d the m a r k e t

wi th s o m e d e g r e e of s u c c e s s in each p roduc t a r e a . In s o m e in-

s t a n c e s United States m a n u f a c t u r e r s have coun te r ed the f o r e i g n

b r a n d compet i t ion by m a n u f a c t u r i n g p r o d u c t s in o the r na t ions .

Other m a n u f a c t u r e r s have i n c r e a s e d t h e i r p r o m o t i o n a l a c t i v i t i e s ,

appl ied p r e s s u r e to t h e i r d i s t r ibu t ing o r g a n i z a t i o n s , sold d i r e c t l y to

l a r g e b u y e r s , o r accep ted a decl in ing m a r k e t s h a r e . Some m a n u -

f a c t u r e r s have d iscont inued m a r k e t i n g c e r t a i n p r o d u c t s .

The p r o b l e m of ma in ta in ing or i n c r e a s i n g s h a r e of m a r k e t is

v i t a l to the m a n u f a c t u r e r , yet each m a n u f a c t u r e r g u a r d s i ts m a r k e t

p e n e t r a t i o n data in a m o s t s e c r e t i v e m a n n e r . Data a r e co l l ec ted

by and known only to the E lec t ron i c I n d u s t r i e s A s s o c i a t i o n .

P u r p o s e of t h i s Invest igat ion

'This s tudy was e x p l o r a t o r y in n a t u r e . Its p u r p o s e s w e r e to

1. P r e p a r e an a n a l y s i s of the s i ze , g rowth , s t r u c t u r e , and

problems; of the c o n s u m e r e l e c t r o n i c p r o d u c t s i ndus t ry .

2. Deter m i r e the s ign i f i cance of m a r k e t p e n e t r a t i o n to m a n u -

f a c t u r e r s , w h o l e s a l e r s , and r e t a i l e r s .

3. Examine the m a r k e t p e n e t r a t i o n r e p o r t i n g m e c h a n i s m , i ts

a c c u r a c y , u s e f u l n e s s , p r o m p t n e s s in f e e d b a c k of da ta , and

the advan tages and d i sadvan tages of m a i n t a i n i n g s e c r e c y

of da ta .

4. D e t e r m i n e if the d e s i r e f o r ma in t a in ing or i n c r e a s i n g m a r -

ke t pene t r a t i on by United States m a n u f a c t u r e r s r e s u l t s in

a . G r e a t e r e m p h a s i s on gales of un i t s t h a n on do l l a r s a l e s

or p r o f i t p e r p roduc t g roup .

b . Complete con t ro l or dominance by the m a n u f a c t u r e r of

t h e m a r k e t i n g channe l s .

c . The power of the m a n u f a c t u r e r to e s t a b l i s h and con t ro l

p r i c e s at the who le sa l e and r e t a i l l e v e l .

d. The power of the m a n u f a c t u r e r to f o r c e fu l l l ine se l l ing .

e . The power of the m a n u f a c t u r e r to con t ro l m a r k e t i n g

ac t iv i t i e s of i ts wholesa l ing and r e t a i l i n g o r g a n i z a t i o n

s t r u c t u r e .

f. Redticed p r o f i t s f o r the w h o l e s a l e r and r e t a i l e r f r o m

what p r o f i t s o t h e r w i s e would be .

5. D e t e r m i n e t he s ign i f i cance of m a r k e t p e n e t r a t i o n to f o r e i g n

m a n u f a c t u r e r s and i m p o r t e r s .

6. D e t e r m i n e the inf luence of i m p o r t s upon the g e n e r a l

s t r u c t u r e of the i n d u s t r y .

Hypo t h e s e s of Study

The hypo theses of th i s s tudy a r e

1, T h e d e s i r e f o r main ta in ing or i n c r e a s i n g m a r k e t p e n e -

t r a t i o n by United States m a n u f a c t u r e r s r e s u l t s in

a . G r e a t e r e m p h a s i s on s a l e s of un i t s than on d o l l a r s a l e s

o r p r o f i t p e r p roduc t g roup .

b. Comple te con t ro l o r dominance by the m a n u f a c t u r e r of

the m a r k e t i n g channe l s .

c . The power of the m a n u f a c t u r e r to e s t a b l i s h and c o n t r o l

p r i c e s a t the who le sa l e and r e t a i l l eve l .

d. H ie power of the m a n u f a c t u r e r to f o r c e fu l l l ine se l l i ng .

e . The power of the m a n u f a c t u r e r to con t ro l m a r k e t i n g

ac t iv i t i e s of its -wholesaling and r e t a i l i ng o r g a n i s a t i o n

s t r u c t u r e .

f. Reduced p r o f i t s f o r the -wholesaler and r e t a i l e r f r o m

what they o t h e r w i s e would be.

2. The m e c h a n i s m f o r r e c o r d i n g and r e p o r t i n g i ndus t ry s a l e s

is i n a c c u r a t e .

Sources of Data

P r i m a r y data w e r e obtained f r o m

1. A p r e l i m i n a r y s e r i e s of p e r s o n a l i n t e r v i e w s wi th two m a n u -

f a c t u r e r s , f o u r t e e n w h o l e s a l e r s , and t en r e t a i l e r s to de-

t e r m i n e if m a r k e t p e n e t r a t i o n was a s ign i f i can t a r e a of

s tudy within the c o n s u m e r e l ec t ron i c p r o d u c t s i ndus t ry .

2. R e s p o n s e f r o m a l e t t e r r e q u e s t i n g i n d u s t r y data f o r w a r d e d

to the fol lowing

a . One hundred seventy m a n u f a c t u r e r s and i m p o r t e r s ,

r e p r e s e n t i n g to ta l c o v e r a g e of t he Merchand i s ing Week

l i s t ing of m a n u f a c t u r e r s and i m p o r t e r s .

b. S ix ty-f ive m a r k e t and aud ience r e s e a r c h o r g a n i z a t i o n s

r e l a t e d to the c o n s u m e r e l e c t r o n i c p r o d u c t s i n d u s t r y

as compi led by Te lev i s ion Fac tbook .

c. I V o hundred n ine teen a d v e r t i s i n g , p r o m o t i o n , and

public r e l a t i o n s compan ie s a s s o c i a t e d with the con-

s u m e r e l e c t r o n i c p r o d u c t s i n d u s t r y .

d. F o r t y - n i n e b u s i n e s s and t r a d e j o u r n a l s r e l a t ed to t he

indus t ry .

e. Twenty-one indus t ry t r a d e a s s o c i a t i o n s .

f. Twelve gove rnmen t d e p a r t m e n t s , a g e n c i e s , c o m -

m i s s i o n s , and c o m m i t t e e s r e l a t e d to the i ndus t ry a s

compi led by Te lev is ion Fac tbook .

g. Twelve b r o a d c a s t e r s , banks , f i n a n c i a l and r e l a t e d in-

d u s t r y s o u r c e s .

3. A second s e r i e s of p e r s o n a l i n t e rv i ews with t h i r t e e n whole -

s a l e s and s ix r e t a i l e r s who w e r e ava i l ab le in Da l l as , T e x a s ,

f o r comple t ing q u e s t i o n n a i r e s .

4. Specia l ly p r e p a r e d q u e s t i o n n a i r e s f o r w a r d e d to the fo l lowing;

a . All m a n u f a c t u r e r a and i m p o r t e r s l i s t ed in Me rch smd.ising

Week ' s " F i r s t Annual Di s t r ibu to r D i r e c t o r y " and in

Te lev i s ion Fac tbook . The ini t ia l ma i l i ng of 195 q u e s -

t i o n n a i r e s w a s fol lowed by a ma i l i ng of 15 q u e s t i o n -

n a i r e s to d o m e s t i c m a n u f a c t u r e r s who fa i led to r e p l y to

the f i r s t q u e s t i o n n a i r e . In addi t ion, one q u e s t i o n n a i r e

was m a i l e d to a f o r m e r p r e s i d e n t of a m a j o r f i r m .

b. Two hundred s e v e n t y - f o u r of t he 1 ,631 w h o l e s a l e r s

l i s t e d in Merchand i s ing Week's " F i r s t Annual D i s t r i -

bu to r D i r e c t o r y . " The s a m p l e cons i s t ed of e v e r y

d i s t r i b u t o r in Texas . In addi t ion, 182 w h o l e s a l e r s

loca ted in 13 m a r k e t s %vhere 5 o r m o r e d o m e s t i c

b r a n d s w e r e being d i s t r ibu ted w e r e s e l e c t e d by s t r a t i -

f ied r a n d o m sampl ing . Six w h o l e s a l e r c o o p e r a t i v e s

and 11 w h o l e s a l e r s a l e s m e n w e r e s u r v e y e d . They

w e r e s e l e c t e d f r o m n a m e s a p p e a r i n g in t r a d e publ i -

ca t ions .

c . F o r t y - n i n e r e t a i l e r s of c o n s u m e r e l e c t r o n i c p roduc t s

se lec ted a t r a n d o m f r o m the 127 l i s t e d in the October

1971 Sou thwes te rn Bell Telephone Company G r e a t e r

Dal las Yellow Page D i r e c t o r y .

d. F i f t y - f i v e large scale retailers. Of these, 19 w e r e

selected from. Texas wholesaler responses a s having

s ign i f i can t influence on the Texas market. The b a l a n c e

of 36 la.rge scale retailers were selected from depart-

ment store, discount, mail order, j e w e l r y , and mass

merchandising chains in the United States listed in Dun

and Brad street Million Dollar Directory a s having s a l e s

of over $100, 000, 000 in 1970.

e . S ixty-one s p e c i a l type u s e r s of c o n s u m e r e l e c t r o n i c

p r o d u c t s who w e r e c o n s i d e r e d to b e po ten t i a l d i r e c t

p u r c h a s e r s f r o m the m a n u f a c t u r e r . The s a m p l e was

s e l ec t ed at random f r o m t r a d e j o u r n a l and t r a d e a s s o -

c ia t ion l i s t i n g s of mob i l e h o m e m a n u f a c t u r e r s , e l e c -

t r o n i c s e r v i c e compan ie s , rental f i r m s , p r e m i u m and

incent ive m e r c h a n d i s i n g f i r m s , large p r e m i u m b u y e r s ,

c r e d i t c a r d compan ie s , and t r a d i n g s t a m p c o m p a n i e s .

5. Government a g e n c i e s , pub l i ca t ions , and. r e p o r t s .

Secondary da ta w e r e d r a w n f r o m

l t C u r r e n t p e r i o d i c a l s in, and r e l a t e d to , t h e c o n s u m e r

e l e c t r o n i c p r o d u c t s i ndus t ry .

2. C u r r e n t books , pub l i ca t ions , and o t h e r l i b r a r y s o u r c e s .

Methods of Study

By means-of a s e r i e s of p r e l i m i n a r y p e r s o n a l i n t e rv i ews wi th

m a n u f a c t u r e r s , w h o l e s a l e r s , and r e t a i l e r s , and th rough a t ho rough

s tudy of indus t ry t r a d e publ ica t ions , it w a s d e t e r m i n e d tha t m a r k e t

penetra t ion, was a s u b j e c t of s ign i f i can t i m p o r t a n c e to each m e m b e r

of the. indus t ry , but of s p e c i a l i m p o r t a n c e to the m a n u f a c t u r e r and

w h o l e s a l e r . The r e t a i l e r a p p e a r e d to be l e s s i n t e r e s t e d in m a r k e t

p e n e t r a t i o n , but is a f fec ted by t h o s e ac t ions of h i s s u p p l i e r s d i r e c t e d

t oward a t t a inment of t h e i r m a r k e t p e n e t r a t i o n g o a l s .

P r e l i m i n a r y in t e rv i ews and a s e a r c h of s e c o n d a r y s o u r c e s of

da ta a l s o p e r m i t t e d the iden t i f i ca t ion of i ndus t ry p r o b l e m s having a

r e l a t i o n s h i p to m a r k e t p e n e t r a t i o n . These p r o b l e m s p e r t a i n e d to

the i m p o r t a n c e of i m p o r t s to the i ndus t ry , and to d e t e r m i n a t i o n of

t he a c c u r a c y of the r e p o r t i n g s y s t e m f o r r e c o r d i n g i n d u s t r y da ta ,

m a r k e t and s a l e s po ten t i a l s , compet i t ion , p h y s i c a l d i s t r i b u t i o n ,

p r o d u c t s , p r ic ing , p romot ion , a t t i t udes of t he m a r k e t , con-

s u m e r i s m , channel conf l ic t , and the l ega l e n v i r o n m e n t .

L e t t e r s r eques t ing da ta r e l a t i n g to the fo rego ing indus t ry p r o b -

l e m s w e r e m a i l e d to 548 po ten t i a l i ndus t ry s o u r c e s a s d e s c r i b e d

u n d e r " s o u r c e s of da ta . " The r e s p o n s e f r o m t h e s e l e t t e r s c o m -

bined wi th s econda ry s o u r c e s of da ta m a d e it p o s s i b l e to ana lyze

e a c h p r o b l e m .

A s e r i e s of f ive q u e s t i o n n a i r e s (see Append ices ) w e r e deve loped

to d e t e r m i n e the opinions of i ndus t ry p a r t i c i p a n t s r e g a r d i n g indus t ry

p r a c t i c e s r e l a t i ng to the p u r p o s e s and h y p o t h e s e s of the study and to

o the r indus t ry p r o b l e m s . Sepa ra t e q u e s t i o n n a i r e s w e r e des igned

f o r and m a i l e d to m a n u f a c t u r e r s and i m p o r t e r s , w h o l e s a l e r s , r e -

t a i l e r s , l a r g e s c a l e r e t a i l e r s , and potent ia l s p e c i a l u s e r s of t he

p r o d u c t . A n u m b e r of the w h o l e s a l e r and r e t a i l e r q u e s t i o n n a i r e s

w e r e comple ted by p e r s o n a l i n t e rv i ews b e c a u s e p e r s o n s w e r e ava i l -

ab le , Completed q u e s t i o n n a i r e s m a d e it p o s s i b l e to va l ida t e t he

h y p o t h e s e s of the s tudy.

Defini t ion of T e r m s

The fol lowing def in i t ions a r e p rov ided a s an explana t ion of the

m e a n i n g of each t e r m a s it is u s e d in the c o n s u m e r e l e c t r o n i c p r o -

duc ts i n d u s t r y :

Marke t p e n e t r a t i o n is the r a t i o of a c o m p a n y ' s s a l e s to the

t o t a l i n d u s t r y s a l e s in a given geog raph ic a r e a and t i m e p e r i o d .

Brand s h a r e is the r a t i o of a s ing le b r a n d ' s s a l e s to t he to t a l

i ndus t ry s a l e s of a l l b r a n d s of a given c o m m o d i t y in a g iven geo-

g r a p h i c a r e a and t i m e p e r i o d .

Share of m a r k e t is c o n s i d e r e d to be the s a m e a s m a r k e t p e n e -

t r a t i o n and b r and s h a r e ; h o w e v e r , r e f e r e n c e is g e n e r a l l y d i r e c t e d

• 1 0

t oward e i the r the c o m p a n y ' s s a l e s o r the "brand's s a l e s . Sales can

be c o n s i d e r e d in t e r m s of e i the r uni ts or d o l l a r s of a g iven p roduc t

c a t e g o r y .

Marke t p e r f o r m a n c e is a b r o a d e r t e r m than, s h a r e of m a r k e t

and inc ludes such evalua t ion f a c t o r s as deve lopmen t of a f i r m and

b rand image , a d v e r t i s i n g e f f e c t i v e n e s s , p e r c e n t a g e of o r d e r s f i l l ed ,

p r o m p t n e s s in de l i ve ry , d e a l e r deve lopment , p r o d u c t s e r v i c i n g , and

o t h e r s , a s well a s s h a r e of m a r k e t .

Marke t potent ia l is "a ca lcu la t ion of m a x i m u m p o s s i b l e s a l e s

oppor tun i t i e s fo r a l l s e l l e r s of a good or s e r v i c e dur ing a s t a t ed

p e r i o d ,

Consumer e l e c t r o n i c p r o d u c t s in th is s tudy a r e c o n s i d e r e d to

be r a d i o s , phonographs , s t e r e o s , t ape r e c o r d e r s , and t e l e v i s i o n

s e t s .

Del imi ta t ions

This study includes only t h o s e p roduc t s men t ioned in the de f i -

n i t ion of c o n s u m e r e l e c t r o n i c p r o d u c t s . Such i t e m s a s e l e c t r o n i c

o r g a n s , p ianos , g u i t a r s , and o ther m u s i c a l i n s t r u m e n t s , as wel l a s

1 A m e r i c a n Marke t ing Assoc ia t ion , C o m m i t t e e on Def in i t ions , Marke t ing Definit ions (Chicago, I960), p. 15.

I i

phonograph r e c o r d s , pho tograph ic e q u i p m s m , and au tomobi le r a d i o s

a r e not included. F requen t ly c o n s u m e r e l e c t r o n i c p r o d u c t s a r e r e -

f e r r e d to a s "home e n t e r t a i n m e n t " o r "home e l e c t r o n i c " p r o d u c t s .

O r d e r of P r e s e n t a t i o n

Chapte r II p r e s e n t s an a n a l y s i s of the deve lopmen t of t he con-

s u m e r e l ec t ron i c p r o d u c t s indus t ry , i ts f o r m a t i o n , s i ze , g rowth ,

and deve lopmen t of individual p r o d u c t s . The s ign i f i cance of i m -

p o r t s to t he indus t ry is t r e a t e d a s wel l as the n a t u r e of compe t i t i on

wi th in the indus t ry .

C h a p t e r s III and IV examine the p r o b l e m s of t he i n d u s t r y a s

d e t e r m i n e d f r o m p r e l i m i n a r y in t e rv i ews and s e c o n d a r y data.. Data

f r o m a l l s o u r c e s o the r than mul t ip l e q u e s t i o n n a i r e s and i n t e r v i e w s

f o r comple t ing q u e s t i o n n a i r e s a r e t r e a t e d in t h e s e c h a p t e r s . The

s u b j e c t s of m a r k e t pene t r a t i on , m a r k e t and s a l e s po ten t ia l , and

the r e p o r t i n g s y s t e m f o r r e c o r d i n g indus t ry da ta a r e d i s c u s s e d in

Chap te r III.

Chapte r IV includes a d i s c u s s i o n of the i ndus t ry p r o b l e m s r e -

l a t ed to d i s t r ibu t ion , p r o d u c t s , p r i c i n g , p r o m o t i o n , a t t i t udes of the

m a r k e t , c o n s u m e r i s m , channel conf l ic t and con t ro l , and t he l ega l

e n v i r o n m e n t .

Chapter V p r e s e n t s and a n a l y s e s the da ta compi led f r o m

m u l t i p l e q u e s t i o n n a i r e s . Response f r o m t h e s e q u e s t i o n n a i r e s

e x p r e s s e d the opinions of the f ive groups of x cspondcnts r e g a r d i n g

i n d u s t r y p r a c t i c e s r e l a t i ng to the purposes and h y p o t h e s e s of t he

s tudy and r e l a t e d indus t ry p r o b l e m s .

Chapter VI inc ludes the s u m m a r y , conc lus ions , and r e c o m -

m e n d a t i o n s .

CHAPTER II

AN ANALYSIS OF THE CONSUMER ELECTRONIC

PRODUCTS INDUSTRY

E a r l y F o r m a t i o n of the E l ec t ron i c Indus t ry

The h i s t o r y and f o r m a t i o n of the c o n s u m e r e l e c t r o n i c p r o d u c t s

i n d u s t r y can be t r a c e d to the deve lopment of the r e c o r d i n g m a c h i n e

in the l a t e n ine teenth cen tu ry . F r o m the r e c o r d i n g m a c h i n e c a m e

the beginning of the phonograph and the r e c o r d i n d u s t r y . Radio,

h o w e v e r , w a s the f i r s t e l e c t r o n i c p roduc t of the i n d u s t r y .

The c o m m e r c i a l p o s s i b i l i t i e s of rad io w e r e r e c o g n i z e d immed i -

a te ly fol lowing World War I when t he United States Navy f o r e s a w

the need f o r a United States o rgan iza t ion to con t ro l r a d i o c o m m u n i -

ca t ion in the United S ta tes , Until th i s t i m e , the B r i t i s h Marcon i

Company, with i ts s u b s i d i a r y , the Marcon i W i r e l e s s T e l e g r a p h

Company of A m e r i c a , held the dominant pos i t i on of l e a d e r s h i p and

t h r e a t e n e d wor ld con t ro l of r ad io communica t i on . To p r e v e n t such

con t ro l , t he Navy Depa r tmen t sugges ted to the Gene ra l E l e c t r i c

Company tha t it not s e l l c e r t a i n equipment to Marcon i , but t ha t

Gene ra l E l e c t r i c a t t e m p t to get Marconi to d ives t i tself of the

13

. • 14

A m e r i c a n Marconi Company, including p a t e n t s . F r o m t h e s e nego-

t i a t ions and gove rnmen t p r e s s u r e s , the Radio C o r p o r a t i o n of

A m e r i c a w a s f o r m e d in 1919 by combining the pa t en t r i gh t s and

i n t e r e s t s of the Marconi W i r e l e s s T e l e g r a p h Company of A m e r i c a

and t h e Genera l E l e c t r i c Company,

The founding of the Radio Corpora t ion of A m e r i c a s e e m e d to

c l ea r the pa ten t deadlock that ex i s ted at the t i m e be tween the

West inghouse E l e c t r i c and Manufac tur ing Company, A m e r i c a n

Telephone and Te leg raph Company, and the In te rna t iona l Radio

Te l eg raph Company. C r o s s - l i c e n s e a r r a n g e m e n t s m a d e it p o s s i b l e

f o r i m p r o v e m e n t s to be m a d e in t r a n s m i s s i o n and r ece iv ing equip-

m e n t . Publ ic b r o a d c a s t i n g began with a s ing le s t a t ion in N o v e m b e r ,

19^0. Instant s u c c e s s a c c e l e r a t e d the ins t a l l a t ion of o ther new

s t a t i o n s .

Nea r ly t h r e e hundred s ta t ions w e r e in o p e r a t i o n by the end of

1922, be tween f ive hundred and s ix hundred by mid -1926 , and

n e a r l y s e v e n hundred in mid -1927 . * This b rough t about t he i m -

m e d i a t e a c c e p t a n c e of r ad io a s is indicated by the fo l lowing:

P r i o r to 1921, the s a l e of r ad io a p p a r a t u s o the r than tha t u s e d f o r public r a d i o - t e l e g r a p h communica t ion p u r p o s e s was confined chief ly to the s a l e of r ad io p a r t s and vacuum

* John George Glover and Wil l iam B. Cornel l , The Develop-m e n t of A m e r i c a n Indus t r i es , r ev . ed. (Englewood Cl i f f s , N. J . , 1941), p7 836. ~ ~

15

t ubes to a m a t e u r s and e x p e r i m e n t e r s f o r t h e i r p e r s o n a l 'use: but when lav i n t e r e s t was a r o u s e d by t he e a r l y b r o a d c a s t i n g ac t i v i t i e s , the demand f o r s impl i f i ed r a d i o r e c e i v e r s f o r h o m e e n t e r t a i n m e n t g rew to such v o l u m e du r ing 1922 to 1923 tha t , a t t i m e s , m a n u f a c t u r i n g f a c i l i t i e s w e r e b a r e l y able to cope wi th the demand . Thus, the s a l e of r ad io r e c e i v e r s g rew f r o m a b u s i n e s s of a few thousand d o l l a r s p e r annum in 1922 to h u n d r e d s of m i l l i ons of d o l l a r s p e r annum s u b s e -

2 quent to 1922.

Genera l Growth of the E l e c t r o n i c s Indus t ry

Table I p r e s e n t s an indus t ry s u m m a r y of f a c t o r y s a l e s by

s e l e c t e d y e a r s s ince 1925. Tota l i ndus t ry s a l e s g rew f rom. $180

m i l l i o n in 1925 to ove r $24 b i l l ion in 1970. Today, a s in i ts in-

cubat ion pe r iod , the indus t ry is inf luenced, a s we l l a s suppor t ed ,

to a l a r g e d e g r e e by t he g o v e r n m e n t , e s p e c i a l l y the m i l i t a r y . The

g o v e r n m e n t s e c t o r h a s accounted f o r a p p r o x i m a t e l y f o r t y - s e v e n to

f i f t y - s e v e n p e r cent of i ndus t ry s a l e s f o r the l a s t f i f t e e n y e a r s .

The second l a r g e s t s e g m e n t of the i n d u s t r y is the i n d u s t r i a l

s e g m e n t . This s e g m e n t is expe r i enc ing the m o s t r a p i d g rowth and

now r e p r e s e n t s a p p r o x i m a t e l y o n e - t h i r d of i n d u s t r y s a l e s . If r e -

p l a c e m e n t components a r e included with the i n d u s t r i a l s e c t o r , to ta l

i n d u s t r i a l s a l e s exceeded $8.6 b i l l ion in 1970.

C o n s u m e r e l e c t r o n i c p r o d u c t s a l e s have cont inued to g row, but

not a t t he r a t e of g rowth of t he e l e c t r o n i c s i n d u s t r y . P r i o r to 1951,

^Ibid. , p . 844.

x b

W

<

H

o r~ o •—i i m 04 o

CO rt <4 H

Q H H U H J

H CO

r—1 m o CO H W «w J "

<5 CO

b 3 Ph d

O §

h

o H

fl ® 2 n b 2 ® S O O rt & CL >-"

S 6 o5

a)

i b

>

0

Q

O u ft.

d (3 .2 S

a s o U

u ^ CQ 0 d w u O 0 Q

** A a* J5 ft* u ^

CO d o U ft*

<3 0) Jx

o o i n o i n o o i n c o o m m O O O ^ O N f O r } ' i f i O - « H ^ so . H M N H CO C"~ CO 04 CO « sD sD

£**- m fvj r-«i o t*~ o ^ ^ vo csj m ^ o

^ h in h- N

•eK

H ^ f o i ^ t ^ o o o u n o o c<-» to ^ H H M (sj <\j ea

o o o o m m o o o m o o r -

(M 04 CO sO in m vq o "vD r- vO •m-

r - o i n m o o m ^ ^ o ^ o c o r - c ^ P O O O ^ O ^ O r O M N ^ v O ( M \ O Q O O O

oo o r*- m 04 vd sO vD H !> »—«

h on ^ vo oo oo •-< M ra h

o o o o m o o oa co co vo in la o o o oo «~-i o4 o f-n o <o m co vD N co \0 o

^ ^ nH to v.o o r-*Pr

m in m co o o o o un o oo rH oo o o o O ^ o r - C v a r - O o ^ o o o o v o ' - H o ^ r ^ ' - H r s j ^

04 »—i h oo m CO CO -vO O vO sO co so oo o

rt H H >H H (\J f\J CO ^ ^ fO 4&

m f> o iH CO 0s- tsw o r— r- 00 O CO m r- 00 o o esi (S3 (M CO CO CO in m in UO m <vO s£> sO sO *4D NO r-

O O cr- O o o 0N 0s" o 0s G'v o o 0X o <T-rH r«i r-«i H ,r—4 f-H rH i—4 i—i rH H r*l 1—! rH rH r»*n rH rH

m -p

o a s <D rQ flj i—! d &0 • |m£ 0) *-«

O

05 O -d

d o 4*» c3 •h o o ?&

<u m o>

0 rd A O • r<< d o u

U 0>

a

i> O rH 4 0 Q W ctS 4~> ca Q

•m 0 r-*4

1

d o 4~ u

t4l u

"Q CO n a) d u o

a I

* 3 W (3

17

c o n s u m e r e l ec t ron i c p roduc t s domina ted the e l e c t r o n i c s i n d u s t r y

with ove r f i f ty p e r cent of i ts annual s a l e s . By 195 8 th i s had d e -

cl ined to about twenty p e r cent . In 1970, c o n s u m e r e l e c t r o n i c s

accounted f o r only s ix t een p e r cen t of the to ta l s a l e s of the e l e c -

t r o n i c s indus t ry . In d o l l a r s , c o n s u m e r e l e c t r o n i c p roduc t s a l e s

g r ew f r o m $92 mi l l ion in 1925 to $1. 5 b i l l ion in 1950, $1. 6 b i l l ion

in 1953, $2. 0 b i l l ion in I960, and n e a r l y $4, 0 b i l l ion in 1970,

Dol lar s a l e s have i n c r e a s e d subs tan t i a l ly ; howeve r , when the

g rowth y e a r s of co lor TV, 1964-1967, a r e excluded "you s e e

some th ing s t a r t l i ng and even unique: c o n s u m e r e l e c t r o n i c s g rows

today at a r a t e SLOWER than Gross National Produc t !"* '

It should be noted t h a t the data in Table I a r e d o m e s t i c l abe l

s a l e s which include p roduc t s e i t he r p roduced in the United States

or impor t ed by United States m a n u f a c t u r e r s f o r s a l e with t h e i r

b r a n d n a m e . T h e r e f o r e , f o r e i g n l abe l i m p o r t s a l e s a r e excluded,

and the s ign i f i cance of c o n s u m e r e l e c t r o n i c p r o d u c t s a l e s is under-

s ta ted b e c a u s e of i m p o r t s . Domes t i c p roduc t ion is o v e r s t a t e d

b e c a u s e s o m e d o m e s t i c b r a n d s a r e p roduced in f o r e i g n na t ions .

3 A l b e r t o Socolovsky, The Decade of E l e c t r o n i c s (New York, 1970), p . 6.

' "• •- 13

Individual P roduc t Sales Growth

E lec t ron ic Indus t r i e s Associa t ion da ta , co l lec ted on an annual

b a s i s , indicate the size arid growth of individual p r o d u c t s . The

da ta p r e s e n t e d in Table II a r e to ta l U. S. s a l e s by product in uni ts

and d o l l a r s f r o m I960 to 1970. All f i g u r e s a r e in thousands and

include impor t s a l e s , a s well a s domes t i c m a n u f a c t u r e r s 1 s a l e s .

Impor t do l la r f i g u r e s a r e basad on the a v e r a g e va lue of to ta l im-

p o r t s as e s tab l i shed by the Depar tment of C o m m e r c e .

Combined sa l e s of rad io , t e lev is ion , phonograph, and r e c o r d e r

p roduc t s grew f r o m $1. 3 bi l l ion in i960 to $3.2 b i l l ion in 1970.

Unit s a l e s fo r t h e s e p roduc t s i n c r e a s e d f r o m 28. 6 mi l l ion to 60. 3

mi l l i on during the s a m e per iod of t i m e . All p r o d u c t s had phe -

nomena l growth dur ing the 1960's with the excep t ion of phono-

g r a p h s . While unit s a l e s of phonographs i n c r e a s e d f r o m 4. 5

mi l l i on in I960 to 5 .6 mi l l ion in 1970, do l la r s a l e s i n c r e a s e d only

$17 mi l l ion , f r o m $359 mi l l ion to $376 mi l l ion .

R e c o r d e r s a l e s i n c r e a s e d f r o m fewer than 300 thousand uni ts

in I960 to m o r e than 8 . 4 mi l l ion uni ts in 1970. Dol lar s a l e s of

r e c o r d e r s i n c r e a s e d f r o m $14. 6 mi l l ion to $243. 8 mi l l ion f o r the

s a m e y e a r s . Unit s a l e s of r ad ios n e a r l y doubled f r o m 18 million,

uni ts in I960 to 34 mi l l ion uni ts in 1970. Dol lar s a l e s of r a d i o s

did double f r o m $190 mi l l ion to $380 mil l ion. Unit s a l e s of

M J

< 5 H

m

m u 0)

U Q V <D

O

> o r—!

H

cs »«*

r~* O Q

CO 4^

%.~4

8

rd ft. CIS

m o 3 D

fi CO 4~* j3 &

CO U <§ r—j o Q

m -y

d &

m u ctf

f-H *~4 o Q

m

$

it> 0) !x

^ ^ 00 «"*« i f i lf»

O f\3 O <»

O ?>- (M o

m

co

00 CO

o Cx!

If) \Q iCl rM r~4 tft iO CO O \C l> NsO l> o N ^ sO CO in ^ sT> i n

o tn

c i i> i n

CO

o <M

co

ir>

<-H »—i (S3 CO CO CO ^ !Ti ^0 OD

o o »-•« o m od o co o so m o co cm o cm oo o o i> co o co ^ ^ *r> •£) ^ i n ^ oo

c o o ^ c m o o c o v j d m o o cm oo m ^ m co o cm o cm cm lO O r-H, r—1 r-H CO vO CO xO

^ co ^ i n i n mo vD -4^ *rT un

o o r -O On o r~< r-«l fsj

o r - oo so r - o CM '• H tM CO CO

CO CO CO

r-l CM O h N CO CO ^ CO

H ^ H |V3 00 0 s Ov- rt* CO IT) 00 o i n 00 !> 00 O v o r ^ s o i n ^ o r - ^ D

O O c O N H c O c O f — i ^ H N N M N f l c O c O

r -o

00

IT) O o

o O 00 xO o co co

0s- r -

vO

o

i n

r^ r -N0

m oo U1

o CM

CM CM CM <M (S3

o m ^ co M H ff) CO o oo co i—i o

i> !>

i n so s>-

r-H vQ r - i d

nT -T

00 o CO

r<H ca

•» * «

CO cf) CM

o <MI CM

O ^ C M C O ^ i D v D r ^ o o o ^ o v O x D x O - s D v O v O v J D v O v D s D C ^ < > 0 0 0 0 0 0 0 O Qs O vm\ t m m , 1 * 4 ^ r**

0 o - r-a 4»>

O o C?i

m CL>

03 0

d

CM ^ O f\3 ^ 00 ^ O

•* n «K CO O ^ CM CO CO

1 9

20

t e l e v i s i o n s e t s i n c r e a s e d f r o m 5, 8 miliioxi in I960 to 12.2 m i l l i o n

in 1970 whi le do l l a r s a l e s n e a r l y t r i p l e d f i o m $797 m i l l i o n to $2, 2

b i l l ion . Te lev i s ion accounted f o r ove r t w o - t h i r d s of d o l l a r s a l e s

f o r a l l p r o d u c t s in 1970.

Census C o m p a r i s o n of Growth

In o r d e r to c o m p a r e data , Table III p r e s e n t s an a b s t r a c t i o n

showing quant i ty and va lue of s h i p m e n t s and do l l a r t o t a l s f o r e a c h

T A B L E III

QUANTITY AND VALUE O F SHIPMENTS O F A L L PRODUCERS: 1967 AND 1963 FOR HOME USE

1967 1963

Unit Quantity (Million)

Dol la r Value

(Million)

Unit Quant i ty (Million)

Dol lar Value

(Million)

Tota l Radio 11. 1 4 7 5 . 4 10.5 3 4 3 . 4

Tota l Te lev i s ion 9. 7 2, 191. 5 7. 7 1, 067. 1

Tota l Phonograph 3. 7 138.5 3. 6 127. 6

Tota l R e c o r d e r _0._8 4 9 . 6 0 . 4 43. 5

Tota l f o r Home Use 25. 3 2, 855 .0 22. 2 1, 581 .6

S t a t i s t i c s , Jan . 1971, U. ,S. D e p a r t m e n t of C o m m e r c e Publ ica t ion-

p r o d u c t with which th i s s tudy is c o n c e r n e d . The Census of Manu-

f a c t u r e r s 1 da ta in Table III a r e c o n s i d e r a b l y l e s s in un i t s in e v e r y

p r o d u c t c a t e g o r y than the E l ec t ron i c I n d u s t r i e s A s s o c i a t i o n da ta

• . • ' ' "> I r , 5 \ , - . * " * » • »ek

p r e s e n t e d in Table II f o r c o m p a r a b l e y e a r s . D i f f e r e n c e s a r e s u b -

s t an t i a l in s o m e in s t ances , such a s the twenty mi l l ion unit d i f f e r -

ence in r a d i o s a l e s in 1967. One r e a s o n f o r p a r t of t h e s e m a j o r

d i f f e r e n c e s is the inc lus ion of i m p o r t s a l e s in Table IX,

Although the unit s a l e s a r e l e s s for r ad io and phonograph p r o -

duc t s , the to ta l do l la r s a l e s a r e g r e a t e r . F o r 1967, t he Census of

M a n u f a c t u r e r s r e p o r t e d rad io s a l e s to be 11. 1 mi l l i on un i t s and

$475 mi l l i on . Te lev i s ion s a l e s w e r e 9 .7 mi l l i on uni ts and $2, 1

b i l l ion . Phonograph s a l e s w o r e 3. 7 mi l l ion un i t s and $138 m i l l i o n

whi le r e c o r d e r s a l e s w e r e 800 thousand uni t s and $49. 6 mi l l i on .

Combined s a l e s f o r a l l p roduc t s in 1967 w e r e 25. 3 mi l l i on un i t s

and $2. 8 bi l l ion.

Average Growth

Accord ing to the U. S. Indus t r i a l Outlook 1971, the a v e r a g e

growth of the c o n s u m e r e l e c t r o n i c p roduc t s i n d u s t r y sh ipmen t s b e -

tween 1963 and 1970 has been about 5 , 5 p e r cen t p e r y e a r . The y e a r

1970 was a d e p r e s s e d one fo r the indus t ry and growth r a t e dec l ined

f rom, p r e v i o u s y e a r s . Export va lues dur ing th i s pe r iod i n c r e a s e d

a t an annual r a t e of t h i r t e e n p e r cent while i m p o r t s i n c r e a s e d a t an

annual r a t e of t h i r t y - t w o p e r cen t . Expor ts r e p r e s e n t e d fou r p e r

cent of p r o d u c t s h i p m e n t s dur ing 1970. ^

4 U . S. Domest ic and In terna t iona l Bus ines s A d m i n i s t r a t i o n , U. S. Indus t r i a l Outlook, 1971 (Washington, 1971), pp. 296-297.

Average Unit Selling P r i c e

The a v e r a g e . m a n u f a c t u r e r ' s se l l ing p r i c e o£ each -p roduc t f o r

t he y e a r 1971 th rough Sep tember was $87. 08 f o r m o n o c h r o m e t e l e -

v i s ion s e t s , $340.41 f o r color t e l ev i s i on s e t s , $15.95 f o r r a d i o s ,

$40.50 f o r tab le and p o r t a b l e phonographs , and $196.53 f o r conso le

phonographs . These da ta a r e included in Table IV.

Individual P roduc t Deve lopment

R e c o r d e r

The r e c o r d e r was developed dur ing the l a t e n ine teen th c e n t u r y .

Most of t he e a r l y p r o d u c t s w e r e c o m m e r c i a l t ypes used in the p r o -

c e s s f o r p roduc ing phonograph r e c o r d s . P r o d u c t i o n of r e c o r d e r s

f o r h o m e u s e was ins ign i f i can t unt i l a f t e r World War II, a l though

c o n s i d e r a b l e deve lopment o c c u r r e d dur ing the l a t e 1930's t h rough

World War II, p a r t i c u l a r l y in Ge rmany . ®

E a r l y p roduc t ion of r e c o r d e r s w a s of the d i s c and w i r e t y p e s .

By 1 954, a l l s a l e s w e r e of the magne t i c t a p e type of r e c o r d e r .

Until the deve lopment of the t r a n s i s t o r , t he m a j o r i t y of r e c o r d e r s

r e t a i l e d f o r m o r e than $200.

^ Paul Kagon, "No Blank Ca r t r i dge , " B a r o n ' s Weekly, X.LIX (September 8, 1969), 11.

2 3

> KH

W J

ca < H

W H Q t> Q

O

Ph cq , ffj rt

w 3 5 1 °

B q

W T3

o 1,5

U ,2 h c O D

w W <

to ><

ffi O H U < fx.|

O o o *d <

o t> er-

as 0 o

u flj

CD

s 0) 4a PM a>

co

<o ? <»

* .3 © •£ > t>

< 1 ^

r~ o

0) 4-i

P

0 +»

f-i aS

I* ?H

B CD 01 a)' m

m u di

rH "HI a

O.

<» 4~S • r i d

ID

<D fl) m ci H

s -

03 14 (tf

O Q

03 44 • H d

*4- u 0 O

a .

f*®4 » o? o >o o u0 o l o | CO u*j f O o a CO tn 1>I CO f '•• i * « • * m • * * # «n

CM Ci o in | o t> r\j LO CO NO IT) r<n CM CO CO OC/ m 1 o (Ns "«-4 p-*4 CO o l CO CO ft-4 I 00 fH | c I <M i»H

NO H 0,- vX> CT- CO vO CO o %o IT) i»H r- ins C"^ cn sO O •O r»H «—4 vD C\] 1 00 r- O i*H t-0 co| ; ^ 00 ?> c>0 CO 0 o CM CM VO xO CO H vDj 1 co' •vO CO cT o' CN m oi fC un CO I ' 00 Is- f«M( CO CO UO m f—HI m (M I (Si o f *"* rH »«H

H r-

CO O 00 Cv3 o NO ID oo rH CO o vO !>v r-»i r< CO CO !> vD Is- vO CQ CM in o !vi cO <M IT) 1^ I> H CO vO sO Cs3 l>

.. f. * ev *< «•

CO rn cn rH CO m

fM ca' I co r—< cn f-4 in CO r- vO LH ; o

iH CO; o NO un o r- o LO o o to O 00 * 9 1 * #' • o » * V • * * » «

CN3 o h>< o 00 00 CO *n co o CM CO CM 00 00 s>3 "•H r*«4 rH rH cn a - cn CO O vO

H cn (M 5

00 r- LTf O; co in CO CO NO LO vO rH •H ; CO O rH o o 00 00 r- m CO

00 LTl m o 0V rH i-H CO NO rH NO sO •* «\ «« •> 4K •> •N o CM CM rH m O rH NO r- CM r m

SO r~4 in vO ,-H CO o NO C- <M CO ca CO xf r*4

r-H j ,-H

c*

fM

oO >o

NO CO | 0 CO CM CM 00 o m m 00 CO O f CO NO uo xO r- O CO rH Xp <0 ?*o NO o CM co m CM 00 00 rH o o o o CO NO o

! * •s 4>k *

CO J 00 i> CM %o CM CM rH

> rH <D

B

0}

a o u

43 u o c o

0> f-H

rO rt 4-> JL, o &

08 0)

0)

JD

a o

U

<D —j 4* «5

O fS

o o 03 sS § ^ o

o H

fi o

r»I o

O

d o IG >

<D r-4 0)

H

<3 -4~> o

H

oa o • H T* <3

pi

a> ^ n" °

,JQ Q flj r-i

H U

o> *—?

& ($ 4J

0 01

a3 4»» o

H

05 o •

73 CO ^

42 re.

Co H b o

6 o -

o •A

<D *-H 4a rt 4^ *« o $4

o ^ a) ^

d o

43 04

o CQ £

o Q

ct5 Pi

43

O ®

d

CJ

JS o

H

i 4

«*0

0)

a • i~4

0

O

1

i

> t-H

H J

m

< 1

H

o

o

0

Pi a>

* §

o +•>

p -

a>

C O

o

c3

0)

S><

U 0 r Q

a 0> 4->

o .

a>

c o

&> m cd

a $ u 4

0 $

GO

U a H

a

<n

d

0 m Q Cw jS

U A 0) c$

> > <

m u

»—(

O

Q

CO

4->

d

S

U 0 * 0

O u d *

fTS fT, o c. ra

49 * •

O C D

0 1 O O D

fsl

•sO m r - I I r—4 o

M l v & O UT^

#t «\ ^ f

^ v O r-»4 o '

r - m 0 0

r a v O

r-« i

o o o

r - IX) M

0 0 r -

r—i rsT

O c o l >

UD m r -

• • •

O \ 0 v D

crv

r-H

Is-

0) US

, d , Q

Cu CO

c« t !

M £ b O P

o H-i

d o

£

cs 4~>

o

B

® - §

Xi ca

•iS H U

o

c$

O (G

d o

ctf

o

C O r\J o

m CS3 s D o

?r% !-"« C D

IK •4 w<i

m o i n i n

cr* ^ m Q N

r H rvj o

c < n

^ CO r ~

m ^ s O

c n o

m (N3 m

CO 4 J

U

2

T *

O

H i

U 0 %

m d o

U

o

H

& o

<-«4

• m4

4 J

0)

r *

1-4

I

ci .<-4

u

a

G*

03 <

® 0 .*4

u AJ~ m 0

U A

d o

4-»

U

0

< | u

^ d

' p !

a

O -<h> W )

d **••4

Xi w aJ

u ^

© u

d

t B

d ©

m

cd

c u

© Q

Cfi

& U

m

o

? 0

d

d

a

ju, *4-i

a) & as

o

o

d .,-4

?-f

0 T 3

k

O

u

<D

h

05

O ,

eg

o

50

a) H

cS

Cft

03 a) 4-*

it

tn

*o 0 4 ^ .<*>»

P

r«J

ftJ 4->

o 4->

4 ^

6

w a> 4-> &

u

d

© J Q

CEl

E h

0)

C O

•rf

a

D

o

r -

f-H

d

d

o

C O

( M

• W -

d <4 m 4->

» r1^

d 3

d o

co

o 4~> o

•".£i

0 %

d

o

s s D

•Sfijr

d ctf

CO 4->

" d

d ca

O

r d

o

M D

C' s

G3

0)

*>«4

Gi yj

O

MA c

d a)

o

3L,

0) &

Q) d

d

4J>

> N

H

1-4

0)

d fH

o

Q

d

o

Q

O

rt

to

a?

i d

o

u

0)

0>

u

3

o

a

CO

. 0)

F*

c S

o

cc 4 ^

?»4

0

1

© r—I

aS

to

*wrl

csS + A

O

4 ^

s4-{ o

4-»

d 0)

u

. 0 ) c u

m

o

4-> 'id 0) d »r-(

u

<D

- o

n d

0$

X !

d o *1*4

Q d

O

u a i

03

a> • p

S 5

t ?

<D 4-> »*mI

d &

o

r -

o

f-H

tti

u 0

1 *»Wi

Rl

d

feO • r4

<P & w

r«S

d

CO + *

*«*4

d

4-»

o

' H

o

t 0 Q

U o p .

C\J

u O

r d

<D $ o

u

u

o

! >

0 ^

03

1 3

a

«s

^ 2

CD

0)

o

o

r -

o

m 0

r^f aS m r~l

O

M-4

o

" S

0)

u

u 0 a

s -4^

A * fm$ 0

d

c«

a)

tM

O

s

s-»

o

0 O d r~4

<tf

0)

rC|

o V 4

T J

0)

O

a

a &

25

> W

CQ

<!

H

w

J

<3

H

O

H

in . -i-1

f-, ®

f—4 fmj c6 r$

1 o S E-f

i-H 0) rO

CQ 4 H-1 ?-{ 0 d a. bC d **-4 C3 0

hH

O

<D rJQ rt

ca J

Jj o O .M a » I 8

a o

Q

® 0 0 u

c3 ^ W "g

>S U u o 4 u <tt

a CO

^ m rO fO ^ CO ^ CO ^ %D vD o h co o r- m o —< *o co

sJD H o (Nj O (M Ol CO CO ^ 00

^ od a* r- co co o co on

rHi r*"*? i~*l t~*-{ r»—i CM

m xo m r-t H ur> ix> on on o o 0s- N£> r- ^ so r- so r- co m

*-« so co m «£* n£s it. m cj"

r-T h co co to oo ^ m vD od

m co co ^ o o on n m h c o o « — ' o o o o c r ^ v O t n » — « o no r-4 o co o r- c- co »-* m on

if) m m c- ^ n n h <> id r H H r s j f O c o ^ i n o o o r o

m r - a ^ o o o c o c a o o o o o o O Is- O if) ^ C T ^ N ^ ^ O rthNcOOMDlfi^N^h-

h N1 (^ N M ^ IT vO*1

^ fsJ CO \D on ^ r- oo o ^ ^ co co ia

>• CO o o o o H ^ M H (\J LO on o co h co a-

^ ^ o 0 s on \D ca CM ^ so

m on m 0* m o in ^ in oo H N N N r O O v O J f l ^ N O O

r—< co m vO oo co

o h o o ^ ^ o h o ^ ( m en in s o m N H ^ ^ N H i n N o o to in \0 \D ^ vO vjO h m o- *r>

oo oo ^ rH q\ o m vo 0 s m «—i on *44 m in co %o m ^ ?n ^

N ttl o>

5>i

in no r H O v D m o D o o G ^ v O p-h 00 sO ^ iT) OD rn s£5 oo lO h oo

CO ^ ^ \0 oo J> V0 xO CO

o ^ N r n ^ i n o h o o ( > o vO ^0 •>£) sD vO \C n0 <vO vO !>-0s" 0% 0s- O O 0 s 0 s 0 s 0 s 0 s 0 s

d o

a> 03 <3

,n

so & 4-> $

g • r«i 4J S3

W

I >s Q i2 ^

0) Ct >0X)

a

04

-d rt 0$

c-vO cr*

?-i o • r«S

0,

0) Ps

*—» CtJ >

u ($ r~4 o

'V 4-i

O Pu X 0)

d

a

ci

m a -

o

o u 2 ^

-H 0) nS U

P ^ H o

u 0a a> ?-i

o

0)

I

o u

02 nd

U a$ d)

•° 2 a) Q m Cu'd

U +» o

^ u a « t j w

SL ^

JS ^ u ° ^ «5

2 o 05 4-> tQ

<D

? f r j h M U a <D o ^4 t-0 -+-> 4-i ? o H

^ d

w d 0 (3 CO

s a> 4 to N 02

U «#«Hi m 0

CD

s>d d d o

c«

d d

i3

<1>

!5

d 0)

a

01

^ >N <y

U Q O <D a * d d *T3

, a £

o a

e H > .s

S 2 V~«4 4«»

4> fl m

v t3 » 0) Q y 43 3 +»

1 «

S . " • *>

s a rCS <« a «

® -O +» c fl d CD ?h

a * cu ^

• p«4 •«*! d o) ,g

cp -*•*

« 'S 0) ^

d *w«i u d

m 0)

0) H

CQ

<a>

o

N 0) U d

n3 o

Pu ^ *d pu

0 L4 0) M

44 <U

O <D Vt5 rd

r Q CO

o H

u T ' S h

$ CO ^ u <$

rn ^ u *r3

• ri P 5

o3

s

'H o

03 k O

d .. s « . ^

3 m ? g S B

J2 x>

d o .r-t 4-> rd

• *>4

U o m m <

m 0

m d

d o

4 u ©•

u

r-0N

rM 0 o PQ

o5 Q

4 -0)

?H cti

s

d o m 4 u Q

*•«<

w

Q

Q

W r* ® S u a U bG d d o -pi

w *5 5Q c$

p

i*»0

-The.Ampex-Corpora t ion r e p o r t e d indus t ry s a l e s f o r 1969 to b e

8. 8 m i l l i o n uni ts , which is cons ide rab ly h ighe r than the 6. 9 m i l l i on

uni ts r e p o r t e d by E l ec t ron i c i ndus t r i e s A s s o c i a t i o n as p r e s e n t e d is.

Table IV. Ampex a l so h a s p r o j e c t e d r e t a i l s a l e s of t ape r e c o r d e r s

to exceed one bi l l ion d o l l a r s in 1975. Only o n e - t h i r d of United

States househo lds owned t ape r e c o r d e r s m 1969. Thus , the po-

t en t i a l f o r continued growth is g r e a t when c o m p a r e d to t he m o r e

t h a n n ine ty pe r cent s a t u r a t i o n l eve l s of o the r c o n s u m e r e l e c t r o n i c

p r o d u c t s . ^

Phonograph

Development of the phonograph o c c u r r e d p r i o r to the i n t r o -

duc t ion of e l e c t r o n i c s . The invention is a t t r i bu t ed to Thomas A.

Edison in 1877. The phonograph was one of the e a r l i e s t h o m e en-

t e r t a i n m e n t p roduc t s , and tended to condit ion A m e r i c a n s to e n t e r -

t a i n m e n t in the l iving r o o m . People look to t e l e v i s i o n , r ad io , and

phonograph p roduc t s f o r e n t e r t a i n m e n t . F o r th i s r e a s o n , the

c o n s u m e r e l e c t r o n i c s i ndus t ry is freqxiently r e f e r r e d to a s the h o m e

e n t e r t a i n m e n t p roduc t s i ndus t ry .

L

Ampex Corpora t ion , Consumer Equipment Divis ion, The Sound Idea Manual (Elks Grove Village, HI . , 1970), p . II, A / 1 .

7 "The Publ ic Impact of Science in the Mass Media, " B u s i n e s s

Topics , VI (Fall , 1958), 12.

Total d o m e s t i c s a l e s of phonographs f r o m 1946 to 1970 a r e

shown in Table VI. Unit s a l e s decl ined f r o m 3,. 9- m i l l i o n un i t s in

.1946 to 1. 35 mi l l ion in 1952, Dol lar s a l e s f o r the s a m e y e a r s de -

cl ined f r o m $216 mi l l i on to $51 mi l l i on d o l l a r s . Although s a l e s

have i n c r e a s e d s ince 1952, t h e r e h a s been c o n s i d e r a b l e v a r i a t i o n

f r o m one y e a r to the next f o r r e a s o n s to be expla ined . Unit s a l e s

in 1970 w e r e 5 . 6 mi l l i on . Dollar s a l e s f o r the s a m e y e a r w e r e

$376 mi l l i on .

It was not unt i l the beginning of the e l e c t r o n i c s age in the

1920's tha t the sound box was r e p l a c e d by e l e c t r o n i c a m p l i f i c a t i o n .

With the deve lopment of r ad io , many p e r s o n s p r e d i c t e d the dea th

of the phonograph . Sales did dec l ine and t he phonograph p layed a

s e c o n d a r y r o l e to r ad io dur ing the d e p r e s s i o n y e a r s of the 1930 's

and War y e a r s of the 1940 's . The pent up c o n s u m e r demand and

the cumula t ion of individual sav ings r e su l t ing f r o m World War II

p rov ided the n e c e s s a r y s t i m u l u s f o r i n c r e a s i n g s a l e s fol lowing t he

War f o r a p e r i o d of t h r e e y e a r s .

The in t roduct ion of 45 R P M and 33 1 /3 R P M long-p lay ing pho-

n o g r a p h s y s t e m s o c c u r r e d in 1948 and 1949. The compe t i t i ve

ba t t l e be tween s y s t e m s and the l a ck of i ndus t ry s t a n d a r d s tended

to confuse b u y e r s and cont r ibuted to a d e p r e s s e d m a r k e t , Hi - f ide l i ty

e n t h u s i a s t s ' i n t e r e s t in b e t t e r qual i ty sound s y s t e m s dur ing the e a r l y

28

I—i >

W J FQ <

H

o c-Cf> r-H I

>£> O

0} 5

C Ptf a o z o ffi A fo

O m

W J < t/D

uy

6

a <

H o H

o o o

•"d

C

$ O

H *n

o

N O P-I jH G n

«) rO flj 1 - 3 ,

rt ,1 w> o « H

o

o H

u

o i*

o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o o

o V If) N if) H 00 N O O !> (> C> (> h o u{ H O O H N ^ i f i L n c o o ^ ^ i n c o m o o o ^ ^ o

• —* h rg n co co ro f in M CO N H H

N ^ v O N O ^ O i n r O ^ O O O O c n ^ c O ^ ^ N ^ O CO O lO O ^ ^ 'JO O 00 N 00 ifi l> O N CO if} ^ if) CO c> n o o m co vo o r- vo o co m 0s »—i r-i

00 CO <\3 rH » — « < — i H N N r O ^ C O ^ ^ C O ^ i ^ ^ v O

sD r- 00. o o r-H N2 CO I f ) vD r~ CO o ra 00 1*1 m m m m *n m in m m m vO vO vD vD %o

O o <T- o 0x o o o o o o o o o O o O o O o r~H rH H r-H i-H r-H r-H r-H r—1 r-H r*H r*H rH t~4 r**"< r~5 »—i »«4 i*H r-H

2 9

x t

0) r* d

0 O

1

i f-H :>

M J

« H

Ctf +> O

H

d cxS

O

<D

10

s ^

| S» o

I f-i O

01 u

H *.~i o n

$q

<3 i—t rH

a

(3 4^ o

H

o o o o o o o o o o o o

o 0*1 o 00 o cr- r -^4 in CO

no m o o (M O {N3 CNJ sO ^ CO \£>

•V **. »* »* no VO \O m

o o o o o o o o o o o o

00 o fs3

m oo m o r<j l o cm

n o m vo

jm $ 0)

{H

o o o o o o o o o o o o o o o

** «* ** *.» »\

oo o m i—* 04 in 00 vO 00 in i1 ^ ^ co

CO f—f {>" UO f-H O O xO O CO ^ O c>

<* *» ** «v * vo m m ^ co

SO r - O) o o xO vO MO vO f -o a - Gv o

»—•t p-«4 -—1

Q

<8 -2

+ Z

d

&o &

, n

d &jq $

<D <~i «J

d o>

a &:

«r*4

u*

o 0) a .

dJO d

• •>*•»•

Q

0

13 0

0 , 5Q

<D 0

4*s> u «s

tH 3

1

8

13 <D

4->

CQ a>

o m o

f *n

•T3I 6 r* o OS

u

rQ 0 , o <p

u H>-{ 0

d o

t ? o *«

4"> d «,»i

CD rCj 4-* s

rO

Tf 0 4> C§

*3

?•*» &

rQ 4~> J-f 3

0) u

0)

£

a

cO m o

d • w4

r&

S

00 m o r-l

d • w

05

S <D

bO 3 o

rC{

cd

€<J

0)

a o 02

0) a

•t**i

o

o

a 0)

rCj 4<»

d as

vD sO O

« r«

a> q«

o 4«>

13

13 d a> 4^

<D H

03

ri r—| r-4 0

(»

-d

a>

0) £

CQ «> »~4

m

u

0$ rH H D

Tl bjo S

a f»«i u 0

13

0

02 d o CQ d

a> u

m

m

Q

fti

a? CO $ <D

Q tf

13 0)

.3 m o u

0) >

CO 0)

r.{ 0$ (0

02 r-4

u &

<

d o

Wtsw4 02 t> ©

a

o a

13 d $

t? © 4»* U* S oa

O

C$

rQ,

>, a$ j*~? a -

0) 13

U

o u o

05 U

<D 13 JL| o o

0) k

o 4* 0

4 }

CO 4^ <p ri4

u

v$

• • 30

s h i f t f r o m co-Moles to p o r t a b l e , m o d u l a r { and c6tS.j3a.et m u J i c §y®»

t e m s a l so occur red* Unit s a l e s have coutiiitied to i i i c f e a s e beCEtiga

of the lower cos t of impor ted phor.Ograph§«

x .ad i§

C o m m e r c i a l r ad io s e t rcianvifaeturing had i ts beginning ill f h s

1926'Si The c o n s u m e r e l e c t r o n i c p roduc t s indus t ry t ends to Us§

1920 as i t s b i r t h y e a r r a t h e r than the e a r l i e r b i r t h da te of thg pho*

nographi Approx ima te ly 100 thousand uni ts with a r e t a i l valu£ of

$5 mi l l ion w e r e p roduced in 1922 j Table VII ind ica tes tha t by

1925 p roduc t ion to ta led 2 mi l l i on r ad ios with a r e t a i l va lue of $200

mi l l ion . Data in Table Vill r e v e a l that unit s a l e s iri 1970 to ta led

34 mi l l i on uni t s with a m a n u f a c t u r e r s ' value: Of $380 miliiori, A

d e s c r i p t i o n of t he growth p a t t e r n follows*

Growth of r ad io was continuous th rough the 1930's arid 1940'g,

bu t t ended to be a f fec ted by the in t roduc t ion of t e l e v i s i o n fol lowing

World War i l A leve l ing of r ad io s a l e s o c c u r r e d be tween 1948

and 1958 and many be l ieved rad io to be a dying i n d u s t r y j Be-

ginning in 1958* s e v e r a l f a c t o r s cont r ibuted to a r e s u r g e n c e of

r ad io s a l e s : f i r s t* a s t rong t eenage of yOuth m a r k e t with afi. ifl*

t e r e s t iri r a d i o developed; second, b r o a d c a s t i n g s t a t ions changed

t h e i r p r o g r a m f o r m a t to m a t c h the wan t s of th is younger tiia.rket;

t h i r d , the t r a n s i s t o r was developed and appl ied to r ad io cons t ruc t ion ;

T A B L E VII

U, S,.. RADIO SET SALES 1922-1949

31

Y e a r

Tota l Rad io Se t s Manufa c t u r ed

Y e a r Numb e r R e t a i l Value

1922 100 ,000 $ 5 , 0 0 0 , 0 0 0 1923 5 5 0 , 0 0 0 30, 000, 000 1924 1, 500, 000 1 0 0 , 0 0 0 , 0 0 0 1925 2 , 0 0 0 , 0 0 0 165 0 0 0 , 0 0 0 1926 1 , 7 5 0 , 0 0 0 2 0 0 , 0 0 0 , 0 0 0 1927 1 , 3 5 0 , 0 0 0 168, 000, 000 1928 . 3 , 2 8 1 , 0 0 0 4 0 0 , 0 0 0 , 0 0 0 1929 4, 428, 000 6 0 0 , 0 0 0 , 0 0 0 1930 3 , 8 2 7 , 0 0 0 300 0 0 0 , 0 0 0 1931 3 ,420 , 000 225, 000, 000 1932 3 , 0 0 0 , 0 0 0 140, 000, 000 1933 3 , 8 0 6 , 0 0 0 180, 500, 000 1934 4, 084, 000 214, 500, 000 1935 6 , 0 2 6 , 8 0 0 3 3 0 , 1 9 2 , 4 8 0 1936 8, 248, 000 450, 000, 000 1937 8, 064, 780 4 5 0 , 0 0 0 , 0 0 0 1938 6,.000, 000 210, 000, 000 1939 10, 500 ; 000 354, 000, 000 1940 1 1 , 8 0 0 , 0 0 0 4 5 0 , 0 0 0 , 0 0 0 1941 1 3 , 0 0 0 , 0 0 0 4 6 0 , 0 0 0 , 0 0 0 1942 4, 400, 000 154, 000, 000 1943 1944

* « * * • • •

1945 5 0 0 , 0 0 0 2 0 , 0 0 0 , 0 0 0 1946 1 4 , 0 0 0 , 0 0 0 7 0 0 , 0 0 0 , 0 0 0 1947 17, 000, 000 8 0 0 , 0 0 0 , 0 0 0 1948 1 4 , 0 0 0 , 0 0 0 6 0 0 , 0 0 0 , 0 0 0 1949 1 0 , 0 0 0 , 0 0 0 500, 000, 000

S o u r c e : B r o a d c a s t i n g 1971 Yea rbook , Compi led by-M a r k e t i n g World , Ltd. , New York .

3 2

>

J

PQ <

H

o r -o r-H

I o m o

CO

0 HH

Q <

C*J

p q

0

1 0

W

J <

1 0

CO

J < H

O

H

o o o

XS <

c3

0

H

0) & co <§

4-» H-l f-J o a a . &*> f* .r~! a a>

o |£|

(D

r Q

M

ts a)

a o

Q

o o o o o o 0 o o

I > CO s O vO NS ^ 001 CO t o

o d i n n r o 0 s r - ^ n I s * ^ h ( s i o o o>- o <-* ^ c o c o r~4 cm id i f ) r - c o l o o o o i n c o <*> M CM fN3 h CO O I s - l > O x D r - v O UO v O f -

h V " s o h o o cr^ o i n c o r o ^ m r o h ^ H H H ( % 3 N ( \ J f \ J f O C O

o o o

00 00

o o o o o o

o m

u C$ nj

! *

<M m CM m i n O O O O u n 0 0 O CO CM H M i n f O O I > M H nO h - \ D N

r-H o m oo m o 0 s »-h r*-

H N UT) h * N (S3 m N h -H r~*i r—f r H r H

h * H r - r—4 0 0 CO

o 0 4

o o o o o o o o o o o o o o o o o o o o o o o o o o o

O <M O O C"*- <7X f s j r-H m 0s (?• o o r - h- h ro r—I r—t «—H I-H ( M f—< r—i ( M ( M

n,0 O O 0 0 ^ »--< ( M S> CO O v O <M 0 0 r - i ^ n i n s o c o , m i n n ^ h o h o o r o h v o N ^ N N O H f O C ^ N C M n i n O O ^ O O O O ^

o r - !>- s o r ~ o o c o c o c r - ~ i h c > c c o ^

O h n o") ^ t n s O h o o o O h r g r-o ^ u i s p m m m m i n m i n i f ) m m v O s O ^ v D ^ v D s o o ^ o o o N c r ^ a ^ o ^ o o ^ o o o o o o o o

33

T3 Q) 3

d o

U

> w

J ffl

H

03

o H

0) rQ

m 4 t-J

u O fS a &B

S *3

o

0)

u

i. *-4 4-> CO CP o

Q

o o o

CO ~~t CO l > CO CO

o o o o o o

*\3 O fsj 00

CO

^ ca oo c-a O 0 )

r-H ^ CO 0 0

r—4 •<# o

CO CO

o o o o o o

nT O CO 00 r-H

o o o o o o

\C vO i n l o csj N*

nO CNI i—4 sO r"~4 v,,£i

CsT H

O SO CM Cs3

o o o o o o

o o CM f~4

O O o o o o

vD ^ vO OO!

u & Q >*

oo o vD nO un vo •*

fsj *—«

o CO o

o r - "

r - 00 ON O sO N0 MD J> 0 0 ' O O f»-4 rHI 5f—4 ^-t

Q

4-*

o g -

,. £ « £ — u

• s . w 0

» . 3

• £ 2 as •-<

e> "0 a ^ g

-Q M y j "0 ® . <U 4» H-. r l s_ '

o CJ

0 m

& r i f w o *+»* TH

&*)

PQ cj to

| .2 f-l -u» ^ 0 0 * * 0

£*?

o

CO

o

rs 4^ <u m

€>

O - 4

05 O

s * 3 ^ • s * *> 2 ^ o &* M +* W " P >N (S 'O In

» s §

O ffi

. £ o <u £-i

£ 2 »

0 ^ ^

§ 3 6 r - l T Q ^ * £ > <+-i

0) 0" m h£ O 0) v3 *•* &G U Q U <D d rt > 2 ^ at g o

d 0

o O £ h0

rrf -H ! § 0 0)

a> -

<z? &

s §

•g a

£ ^ k 0 ^ (S

k % 4)

-• e j >

I ) ^ " t J fc -a

I -®" a

0)

Q r-4 on ©

u

o

.Q m m

i « fi 4 m a) u ^ ^

.a ® i

* 1

:§ 10

O

CD ?-i

3 2 p

rO . 4 «U OS

g w

aS

o D 5

4) -O U 4^ 0) 0) 0 4 - 5 + ^

* o o Pu CU s g

•H .w O o m m <

to «>

• r-»

02

5

[ u

& « o o ?HI p «

a* eft

4^ © Q 5 o

"O

o 6

0 d

(12 R 0) ?«<

a u 0$

1 cl

S

a * ***4 0> u o

H-4 «,H o i>* u

4)

J3 wlS

ca " §

ca

m c$

o v *

St cS

o X u

6

3 4

Table VIII ind ica tes tlie i f cpor t ance of i m p o r t r ad io s a l e s .

Cu r r en t l y , i m p o r t r a d i o s cons t i tu te about 91. 5 p e r cent of t h e to t a l

d o m e s t i c m a r k e t , but nea r ly 20 p e r cent of the impor t ed r a d i o s a r e

sold u n d e r a d o m e s t i c m a n u f a c t u r e r ' s b r a n d .

The Radio Adver t i s ing Bureau e s t ima ted tha t 62 mi l l i on

United Sta tes h o m e s , o r m o r e than 98 per cent , w e r e r a d i o equipped

8

in 1970. In addition,, p o r t a b l e r ad ios , au tomobi l e r a d i o s , and

mu l t i p l e s e t ownersh ip expanded the m a r k e t f u r t h e r . Domes t i c

s a l e s of r a d i o s be tween 1965 and 1970 exceeded the popula t ion of [ i

the United S ta tes . ; I

Te lev is ion ? }

"Apr i l 30, 1939 m a r k e d the r e a l beginning of m o d e r n t e l e v i s i o n ;

when P r e s i d e n t Rooseve l t f o r m a l l y opened the New York W o r l d ' s j

F a i r . Only a few hund red r e c e i v e r s , m o s t of t h e m h o m e m a d e , j 9 F-w e r e in e x i s t e n c e to tune in to th i s c e r e m o n y . " 5

Although l i t t l e growth in t e l ev i s i on s a l e s o c c u r r e d unt i l a f t e r

1946, p r inc ipa l l y b e c a u s e of the War and g o v e r n m e n t p roh ib i t ion

on new cons t ruc t i on of f a c i l i t i e s , the g rowth r a t e of few i n d u s t r i e s

I

: "~™~ ! ' " ! ~~ ' ! ' ~ ' ~ ~ | .

^Broadcas t i ng , 1971 Yearbook (Washington, 1971), p . 64. .

^Albe r t W. F r e y , Adver t i s ing (New York, 1961), p . 251.

can c o m p a r e to that of the t e l e v i s i o n indus t ry . F a c t o r y s a l e s ,

shown in Table IX, moved f r o m an e s t i m a t e d 6, 000 uni t s va lued a t