a study on mutual funds program with reference to banks

TRANSCRIPT

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 356

A Study on Mutual Funds program with Reference to

Banks

Bellaji Vishnu Vardhan Reddy, Ch. Shivapriya

Department of Business Management

Anurag University

Abstract: Mutual funds mobilize the savings of the people and channelize it to the money and capital market. One of the main

advantages of mutual funds over any other investment to small investor is that they give small investors access to

professionally managed, diversified portfolio of equities, bonds and other securities, which is rather impossible for a small

investor to create with a small amount of capital he/ she owns. Mutual funds constitute a very important component of the

capital market in developed countries and are now becoming vibrant in emerging markets like India. The origin of mutual

funds industry in India can be traced in the enactment of the Unit Trust of India (UTI) Act in 1963. Due to historic reasons,

the UTI enjoyed the total monopoly in the initial years and until now continues to maintain the largest market share. The

industry has now moved from complete monopoly to that of a monopolistic competition. Presently, the share of Net Assets of

mutual funds is more than 7 percent of India’s gross domestic product (GDP). Also, the monies accredited to mutual funds

form an adequate part of gross domestic savings (GDS) in the country. This indicates the important place of mutual funds as

an investment vehicle in the country. Majority of the money parked in mutual funds come from the institutional segment

including corporates, banks and foreign institutional investors (FIIs).

Keywords: Capital market, Investment patterns, Market share, Mutual Funds.

Introduction: Mutual Fund is a trust that pools the savings of a number of investors who share a common financial goal. This pool

of money is invested in accordance with a state objective. The joint ownership of the fund is thus “Mutual”, i.e. the fund belongs to

all investors.

The money thus collected is then invested in capital market instrument such as shares, debentures, and other securities. The income

earned through these investments and the capital appreciations realized are shared by its unit holders in proportions the number of

units owned by them. Thus a Mutual Fund is the most suitable investment for the common man as it offers an opportunity to invest

in a diversified, professionally managed basket of securities at a relatively low cost.

A Mutual Fund is an investment tool that allows small investors access to a well-diversified portfolio of equities, bonds and other

securities. Each shareholder participates in the gain or loss of the fund.

Objectives: To know the extent of Mutual Funds in earing returns over fixed deposits or savings account, to analyze the way of

investment pattern in Mutual Funds by customers and to know the banking operations carried on with respect to Mutual Funds.

Research Methodology: Detailed information which is relevant to the project is gathered by visiting the different banks.

Secondary data is used only for the reference and it has been collected through various journals and websites.

Company Profile:

SBI: The State Bank of India (SBI) is an Indian multinational, public sector banking and financial services statutory body. It is

a government corporation statutory body headquartered in Mumbai, Maharashtra. SBI is ranked as 236th in the Fortune Global 500

list of the world's biggest corporations of 2019. It is the largest bank in India with a 23% market share in assets, besides a share of

one-fourth of the total loan and deposits market.

SBI is an Indian multinational, Public Sector banking and financial services company. SBI is one of India’s major banks and is an

industry leader in terms of size, business sector promotion and initiatives for the progress and economic enhancement of the Indian

economy. SBI is entering into many new businesses with strategic tie ups – Pension Funds, General Insurance, Custodial Services,

Private Equity, Mobile Banking, Point of Sale Merchant Acquisition, Advisory Services, organized items and so on – every one of

these activities having a massive potential for development.

Housing Development Finance Corporation Limited

HDFC Bank Limited is an Indian financial services company based in Mumbai, Maharashtra that was incorporated in August 1994.

HDFC Bank is the fifth or sixth largest bank in India by assets and the first largest bank by market capitalization as of November 1,

2012. The bank was promoted by the Housing Development Finance Corporation, a premier housing finance company (set up in

1977) of India.

BANK OF BARODA: Bank of Baroda (BOB) was founded by Maharaja Sayajirao Gaekwad in July 1908. It started with a paid-

up capital of Rs 10 lakh. Bank of Baroda is a pioneer in various customer centric initiatives in the Indian banking sector. Bank is

amongst first in the industry to complete an all–inclusive rebranding exercise wherein various novel customer centric initiatives

were undertaken along with the change of logo. The initiatives include setting up of specialized NRI Branches, Gen–Next Branches

and Retail Loan Factories/ SME Loan Factories with an assembly line approach of processing loans for speedy disbursal of loans.

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 357

Data analysis and interpretation:

2. What is the preferred way of communication to your customers about Mutual Funds?

Table 1: Table showing preferred way of communication to their customers about Mutual Funds

Mode No. of respondents Percentage

Directly to the

customers 25 41.6

media 10 16.6

Internet 24 40

Telephone 1 1.6

TOTAL 60 100%

Fig.1. Graph showing the percentage of mode of communication

Interpretation: By seeing the graph, we can understand that out of 60 respondents, most of the banks prefer to communicate

directly with their customers about Mutual Funds and also use internet to communicate with their customers

3. While investing in Mutual Funds, which factors customers prefer most?

Table 2: Table showing factors that customers prefer the most

Factors No. of respondents percentage

Liquidity 13 21.6

low risk 37 61.6

high returns 10 16.6

company reputation 0 0

Total 60 100

Modes

Directly to the customers Media Internet Telephone

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 358

Fig 2: Graph showing the percentage of factors that customers prefer the most

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, most of customers of banks prefer Mutual Funds for low risk

and also invest by seeing opportunity of liquidity. Some people invest in mutual funds by expecting high returns.

4. Which type of Mutual Funds scheme do you suggest to your customers?

Table 3: Table showing the type of Mutual Fund schemes that bankers suggest to their customers

Type of scheme No. of respondents Percentage

Growth 8 13.33

Income 24 40

Balanced 28 46.66

Total 60 100

Factors

Liquidity Low risk High returns Company reputation

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 359

Fig 3: Graph showing the percentage of type of schemes that bankers suggest to their customers

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, most of the bankers suggest their customers to invest in balanced

schemes because of the low risk or diversification of the risk.

5. Which mode of investment does your customers prefer?

Table 4: Table showing mode of investment preferred by customers

Mode of investment No. of respondents Percentage

SIP 44 73.33

One-time investment plan 16 26.66

Total 60 100

Fig 4: Graph showing the percentage of mode of investment preferred by customers

Type of schemes

Growth Income Balanced

Mode of investment

SIP One time investment plan

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 360

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, most of the investors prefer investing in the Mutual Funds

through SIP.

6. Which kind of investors do you regularly see?

Table 5: Table showing kind of investors that bankers regularly see

Kind of investors No. of respondents percentage

Risk averse 39 65

Moderate risk taker 21 35

High risk taker 0 0

Total 60 100

Fig 5: Graph showing the percentage of kind of investors

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, most of the customers of the banks who invest their savings in

Mutual Funds are risk averse.

7. Most of your Mutual Fund customers in your bank are from

Table 6: Table showing the customers from the sector they belong to

Type of

customers No. of respondents Percentage

Government 5 8.33

Private Sector 26 43.33

Business 23 38.33

Agriculture 3 5

Others 3 5

Total 60 100

Kind of investors

Risk averse Moderate risk taker High risk taker

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 361

Fig 6: Graph showing the percentage of customers from the sector they belong to

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, most of the customers who invest in Mutual Funds are business

persons and also from private sector.

8. Through which channel your customers invest in Mutual Funds?

Table 7: Table showing channels through which the customers invest in Mutual Funds

Channel No. of respondents percentage

Directly from AMC 36 60

Brokers 12 20

Sub Brokers 12 20

Other sources 0 0

Total 60 100

Type of customers

Government Private sector Business Agriculture Others

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 362

Fig 7: Graph showing the percentage of channels through which the customers invest in Mutual Funds

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, most of the investors invest in Mutual Funds through AMC’s

and very less people are through Brokers and Sub Brokers.

9. How much percentage of your customers are continuously following up about their investments?

Table 8: Table showing the percentage of customers who continuously follow up their investments

Percentage of customers No. of respondents Percentage

10-20% 5 8.33

20-30% 32 53.33

30-40% 21 35

40-50% 2 3.33

Above 50% 0 0.00

Total 60 100

Channels

Directly from AMC Brokers Sub Brokers Other Sources

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 363

Fig 8: Graph showing the percentage of customers who continuously follow up their investments

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, 20-30% of customers are following up their investments.

10. Is there a need for creating awareness among the public about the benefits of investing the Mutual Funds?

Table 9: Response given by bankers for creating awareness about benefits of investing in Mutual Funds

Response No. of respondents percentage

Yes 58 96.66

No 2 3.33

Total 60 100

Fig 9: Graph showing the percentage of response given by bankers about creating awareness

Percentage of customers

10-20% 20-30% 30-40% 40-50% Above 50%

Response

Yes No

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 364

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, most of the bankers opinion is that there is a need for creating

awareness among the public about the benefits of investing in the Mutual Funds.

11. Does your bank arranges campaigns to create awareness on Mutual Funds?

Table 10: Response given by bankers about campaigns to create awareness on Mutual Funds

Response No. of respondents Percentage

Yes 53 88.33

No 7 11.66

Total 60 100

Fig 10: Graph showing the percentage of response given by bankers about campaigns

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, most of the banks are conducting awareness campaigns for the

Mutual Funds.

12. Average age of customers taking Mutual Funds in your banks?

Table 11: Table showing the average age of customers taking Mutual Funds

Age No. of respondents Percentage

20-25

years 4 6.66

25-30 38 63.33

30-35 18 30

Above 35 0 0

Total 60 100

Response

Yes No

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 365

Fig 11: Graph showing the percentage of age of customers taking Mutual Funds

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, average age of customers who invest in Mutual Funds is 25-30

years and also mostly by the people age between 30-35 years and very less people from age 20-25 years.

13. Do customers have the option of buying Mutual Funds online?

Table 12: Table showing whether the customers have the option of buying Mutual Funds online

Response No. of respondents percentage

Yes 60 100

No 0 0

Total 60 100

Age of customers

20-25 years 25-30 30-35 Above 35

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 366

Fig 12: Graph showing the percentage of response given by bankers about option of buying online

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, most of the banks are maintaining the Mutual Funds through

online.

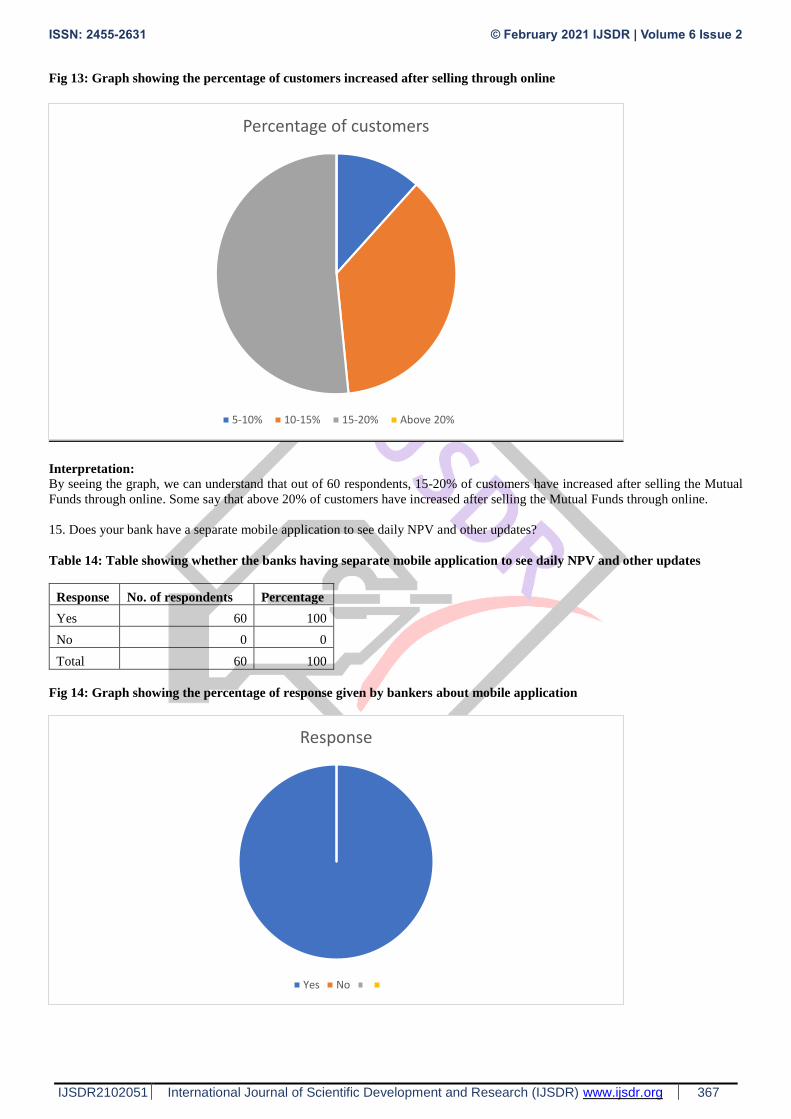

14. What is the percentage of customers increased after selling through online?

Table 13: Table showing the percentage of customers increased after selling through online

Response No. of respondents percentage

5-10% 7 11.66

10-15% 22 36.66

15-20% 31 51.66

Above 20% 0 0.00

Total 60 100

Response

Yes No

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 367

Fig 13: Graph showing the percentage of customers increased after selling through online

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, 15-20% of customers have increased after selling the Mutual

Funds through online. Some say that above 20% of customers have increased after selling the Mutual Funds through online.

15. Does your bank have a separate mobile application to see daily NPV and other updates?

Table 14: Table showing whether the banks having separate mobile application to see daily NPV and other updates

Response No. of respondents Percentage

Yes 60 100

No 0 0

Total 60 100

Fig 14: Graph showing the percentage of response given by bankers about mobile application

Percentage of customers

5-10% 10-15% 15-20% Above 20%

Response

Yes No

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 368

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, now-a-days every bank is maintaining their own mobile

application for the convenience of their customers.

16. Do you have a separate customer support for Mutual Funds?

Table 15: Table showing the percentage of banks having separate customer support for Mutual Funds

Response No. of respondents percentage

Yes 60 100

No 0 0

Total 60 100

Fig 15: Graph showing the percentage of banks having separate customer support for Mutual Funds

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, Now-a-days every bank is treating their customers very carefully

and supporting for in every situation.

17. Does your customers are pushed to buy Mutual Funds while opening a savings account with your bank?

Table 16: Response given by bankers regarding the purchase of Mutual Funds by their customers

Response No. of respondents Percentage

Yes 19 31.66

No 41 68.33

Total 60 100

Response

Yes No

ISSN: 2455-2631 © February 2021 IJSDR | Volume 6 Issue 2

IJSDR2102051 www.ijsdr.orgInternational Journal of Scientific Development and Research (IJSDR) 369

Fig 16: Graph showing the percentage of response given by bankers regarding the purchase of Mutual Funds by their

customers

Interpretation:

By seeing the graph, we can understand that out of 60 respondents, most of the bankers say that no customer is pushed to buy the

Mutual Funds in any banks.

Findings:

Most of the banks are selling Mutual Funds from last 25 years.

Most of the bankers feel that public need more awareness towards Mutual Funds.

By conducting awareness campaigns and by advertisements the public can be more aware of Mutual Funds.

Most of the customers invest their savings in Mutual Funds for the diversification of the risk and for the liquidity purpose

even though they are getting less returns.

Most of the bankers prefer balanced Mutual fund schemes to invest.

Most Government banks or nationalized banks don’t really bother about the mutual funds in their banks.

Now-a-days, almost every bank is using mobile applications for the ease of customers services.

Customers who invest their savings in Mutual Funds do follow up their investments regularly through online applications.

There is a scope for earning higher returns in mutual funds when compared to fixed deposits because the rate of interest in

fixed deposits is fixed and the rate in mutual funds varies according to the market fluctuations. Portfolio diversification is

always helpful.

Conclusion:

The survey is conducted among 60 respondents and I observed few things where customer relationship should improve. Investing

in a Mutual Fund is best option for the investors irrespective of their knowledge upon the stock markets and the Mutual Funds

because the funds of the investor are effectively managed by the professional fund managers by investing in the various business

of various sectors rather than confiding to single corporate entity nor the single industry sector.

There are several aspects need to considered before choosing either Asset Management Company or Scheme.

“Mutual Fund is like appointing an driver to drive a vehicle rather than Self-Driving

References:

www.timesofindia.com

Sales

Yes No