a study on customer perception in banking industry using gap analysis

TRANSCRIPT

A STUDY ON CUSTOMER PERCEPTION IN BANKING INDUSTRY USING

GAP ANALYSIS

- Dr. Hema Bhalakrishnan

Background

Our perception is an approximation of reality. Our brain attempts to make sense

out of the stimuli to which we are exposed. This works well when we are about to

perceive familiar facts. However, our perception is sometimes “off” when we are not

clear about concepts. Perception is a process by which an individual select, organize &

Interpret stimuli in a meaningful picture of the world Also, we can describe as “how we

see the world around us” Perception is the process of selecting, organizing, & Interpreting

or attaching meaning to events happening in environment

The Concept of Perception

Perception is one of the objects studied by the science of consumer behaviour.

Analyzing the works of scientists studying consumer behaviour, it is possible to make a

conclusion that perception is presented as one of personal factors, determining consumer

behaviour. Personal factors mean the closest environment of a human, including

everything what is inside the person, his head and soul, characterizing him as a

personality. Using his sensory receptors and being influenced by external factors, the

person receives information, accepts and adapts it, forms his personal attitude, opinion,

and motive, which can be defined as factors that will influence his further activity and

behaviour. Perception within this context is considered as one of the principal personal

factors, conditioning the nature and direction of remaining variables.

Authors J. C. Mowen (1987), D. L. Loudon and A. J. Della Bitta (1993) determine

perception as a phase of information processing, while C. G. Walters and B. J. Bergiel

(1989), F. G. Crane and T. K Klarke (1994), G. D. Harrell, G. L. Frazier (1998), M. R.

Solomon (1999), B. Dubois (2000) define perception as a separate variable of consumer

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 1

behaviour having features of the process and including separate phases of the process. C.

G. Walters and B. J. Bergiel (1989) characterize perception as a solid process during

which an individual acquires knowledge about the environment and interprets the

information according to his/her needs, requirements and attitudes. The works of F. G.

Crane and T. K Klarke (1994), G. D. Harrell, G. L. Frazier (1998), M. R. Solomon

(1999), B. Dubois (2000) present perception as a more complicated process, during

which sensory receptors of a consumer capture a message sent by external signals and the

information received is interpreted, organized and saved, providing a meaning for it and

using it in a decision making process.

Customer Perception

Customer perception is an important component of our relationship with our

customers. Customer satisfaction is a mental state which results from the customer’s

comparison of expectations prior to a purchase with performance perceptions after a

purchase. A customer may make such comparisons for each part of an offer called

‘‘domain-specific satisfaction’’ or for the offer in total called ‘‘global satisfaction’’.

Moreover, this mental state, which we view as a cognitive judgment, is conceived of as

falling somewhere on a bipolar continuum bounded at the lower end by a low level of

satisfaction where expectations exceed performance perceptions and at the higher end

by a high level of satisfaction where performance perceptions exceed expectations.

Customer Perception on Service

These characteristics of service also make service unique and different from goods as

described below

1. Intangibility. Unlike manufactured goods that are tangible, a service is intangible. The

products from service are purely a performance. The consumer cannot see, taste,

smell, hear, feel or touch the product before it purchased

2. Heterogeneity. A service is difficult to produce consistently and exactly over time.

Service performance varies from producer to producer, from customer to customer,

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 2

and from time to time. This characteristic of service makes it difficult to standardize

the quality of the service

3. Inseparability. In service industries, usually the producer performs the service at the

time the consumption of the service takes place. Therefore, it is difficult for the

producer to hide mistakes or quality shortfalls of the service. In comparison the goods

producers, have a buffer between production and customers’ consumption

4. Perishability. Unlike manufactured goods, services cannot be stored for later

consumption. This makes it impossible to have a quality check before the producers

send it to the customers. The service providers then only have one path, to provide

service right the first time and every time.

5. Non-returnable. A service is not returnable, unlike products. On the other hand, in

many services, customers maybe fully refunded if the service is not satisfactory.

6. Needs-match uncertainty. Service attributes are more uncertain than the product. This

yield to higher variance of making a match between perceived needs and service is

greater than perceived need and product match.

7. Interpersonal. Service tends to be more interpersonal than products. For example,

compare buying a vacuum cleaner to contracting for the cleaning of a carpet. While

customers will judge the quality of the vacuum cleaner by how clean the carpet is,

customers will tend to judge the quality of the carpet cleaning service on both the

appearance of the carpet and the attitude of the technician.

8. Personal. Customers often view services to be more personal than products. For

example, a customer may perceive the service of her car (balancing the tires) as more

personal than purchasing new tires. If the same customer has problems later with the

tires, the defect in the tires would be less personal than if the tires were never

balanced.

9. Psychic. Even though the food at a restaurant might not be as delicious as other famous

restaurants., the customers will recognize the restaurant and tend to be satisfactions if

the service of the restaurant is excellent. Another example is when a flight is delayed,

and people tend to be upset with this poor service . However, if the gate agent is very

helpful and friendly, people tend to still be pleased with the service (Groth, & Dye,

1999).

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 3

Like other industries, banking and financial services companies have reached the

conclusion that the relationship with the customer should not (metaphorically and

literally) end at the bank door. Customer access after the transaction adds value to the

transaction.

Definition of Banking

Banking means accepting for the purpose of lending or investment, of deposits of

money from the Public, repayable on demand or otherwise and withdraw able by

cheques, draft, order or otherwise.

Features of Banking:

1. Dealing in Money:

The banks accept deposits from the public and advancing them as loans to the

needy people. The deposits may be of different types- Current, Fixed, Savings, etc.

accounts. The deposits are accepted on various terms and conditions.

2. Deposits must be withdrawable:

The deposits (other than fixed deposits) made by the public can be withdrawable

by cheques, draft or otherwise, i.e., the bank issue and pay cheque. The deposits are

usually withdrawable on demand.

3. Dealing with Credit:

The banks are the institutions that can create Credit i.e., creation of additional

money for lending. Thus, ‘Creation of Credit’ is the unique feature of banking.

4. Commercial in Nature:

Since all the banking functions are carried on with the aim of making profit, it is

regarded as a commercial institution.

5. Nature of Agent:

Besides the basic functions of accepting deposit and lending money as loans,

banks possess the character of an agent because of its various agency services.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 4

Measuring Customer Perception in the Banking Industry

Banking operations are becoming increasingly customer dictated. The demand for

'banking super malls' offering one-stop integrated financial services is well on the rise.

The ability of banks to offer clients access to several markets for different classes of

financial instruments has become a valuable competitive edge. Convergence in the

industry to cater to the changing demographic expectations is now more than evident.

Bancassurance and other forms of cross selling and strategic alliances will soon alter the

business dynamics of banks and fuel the process of consolidation for increased scope of

business and revenue. The thrust on farm sector, health sector and services offers several

investment linkages. In short, the domestic economy is an increasing pie which offers

extensive economies of scale that only large banks will be in a position to tap. With the

phenomenal increase in the country's population and the increased demand for banking

services; speed, service quality and customer satisfaction are going to be key

differentiators for each bank's future success. Thus it is imperative for banks to get useful

feedback on their actual response time and customer service quality aspects of retail

banking, which in turn will help them take positive steps to maintain a competitive edge.

The working of the customer's mind is a mystery which is difficult to solve and

understanding the nuances of what perception the customer has to attain satisfaction is, a

challenging task. This exercise in the context of the banking industry will give us an

insight into the parameters of customer satisfaction and their measurement. This vital

information will help us to build satisfaction amongst the customers and customer loyalty

in the long run which is an integral part of any business. The customer's requirements

must be translated and quantified into measurable targets. This provides an easy way to

monitor improvements, and deciding upon the attributes that need to be concentrated on

in order to improve customer satisfaction. We can recognize where we need to make

changes to create improvements and determine if these changes, after implemented, have

led to increased customer satisfaction.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 5

The Need to Measure Customer Perception:

Satisfied customers are central to optimal performance and financial returns. In

many places in the world, business organizations have been elevating the role of the

customer to that of a key stakeholder over the past twenty years. Customers are viewed as

a group whose satisfaction with the enterprise must be incorporated in strategic planning

efforts. Forward-looking companies are finding value in directly measuring and tracking

customer satisfaction as an important strategic success indicator. Evidence is mounting

that placing a high priority on customer satisfaction is critical to improved organizational

performance in a global marketplace.

With better understanding of customers' perceptions, companies can determine the

actions required to meet the customers' needs. They can identify their own strengths and

weaknesses, where they stand in comparison to their competitors, chart out path future

progress and improvement. Customer satisfaction measurement helps to promote an

increased focus on customer outcomes and stimulate improvements in the work practices

and processes used within the company.

When buyers are powerful, the health and strength of the company's relationship

with its customers – its most critical economic asset – is its best predictor of the future.

Assets on the balance sheet – basically assets of production – are good predictors only

when buyers are weak. So it is no wonder that the relationship between those assets and

future income is becoming more and more tenuous. As buyers become empowered,

sellers have no choice but to adapt. Focusing on competition has its place, but with buyer

power on the rise, it is more important to pay attention to the customer.

Customer satisfaction is quite a complex issue and there is a lot of debate and

confusion about what exactly is required and how to go about it. This article is an attempt

to review the necessary requirements, and discuss the steps that need to be taken in order

to measure and track customer satisfaction.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 6

Need and Importance of the Study

One of the most important developments in banking sector has been the growth of

the financial industry over the past two decades. The benefits of financial industry can be

seen in the form of large scale industrial development, increased employment

opportunities, higher turnover as well as revenue generation to the government and also

increase in export of goods and services.

Banking industry in India has undergone a process of evolution with the package

of time. To count or to depend on a bank merely by the function it is supposed to perform

would be insufficient in the world that we live today.

Investments play a vital role on the part of the customers. A real investor does not

simply throw his or her money random investment; he or she performs through analysis

and commits capital only when there is a reasonable expectation of profit. Hence they

both are interdependent i.e., it all depends upon the customer. “Customer knows what to

expect”. Today banks have a relationship management approach with their clients.

Banks are offering more customized solutions to their clients. The need of the

hour is not only to introduce more value added products for which the customers are

willing to pay here but also to innovate & enter new segments like small business &

periodical finance.

Everything resolves around the customer and banks via with their innovative and

quality products to suit their clients. Today the bottom line for any customer is

convenience understanding and evaluating the customers perception on the service &

products of a bank has without doubt become a need, which propels the body to structure

itself for better performance and service.

Thus delivering high quality service to clients is just as important as delivering

performance that meets or exceeds their expectations. It is in this context that a study is

necessary to know about awareness levels on the services provided by the public and

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 7

private sector banks namely, Public Sector Banks : State Bank of India, Indian Bank and

Indian Overseas Bank and Private Sector Banks : ICICI, HDFC and IndusInd Bank and

the customer perception towards the banks.

Objectives

The objectives of the study are:

♦ To evaluate the different factors considered by the investors while making

investments.

♦ To study the services provided by Private Sector and Public Sector banks and the

performance of it.

♦ To analyze the service facilities those are being effectively utilized by the

customers.

♦ To ascertain suggestions from the investors for further improvement of the

institutions.

Methodology

The data required for this study has been collected from the primary sources.

Initially a ‘Pilot Study’ will be conducted for testing the questionnaires. The pilot survey

will help in making certain improvement in the final questionnaire. A structured

questionnaire shall then be prepared for the respondents in order to collect primary data.

The questionnaire is designed based on the objectives.

Source of Data

The researcher proposed to gather the required data through primary data and

secondary data. Primary data are those which are collected afresh and for the first time,

and thus happen to be original in character. It will be collected through questionnaires

method. Secondary data is collected from the possible records like books, magazines,

periodicals and websites.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 8

Universe

The proposed study is to find out the services rendered by the Public and Private

Sector Banks to their Customers. The population is uncountable and is considered as

infinite. However, the proposed sample for the study from Private Sector Banks and

Public Sector Banks are 300 respectively.

Sampling Method

The universe of the study is the account holders of Public and Private Sector

banks and the sampling technique adopted will be convenient sampling method.

Statistical Tools and Techniques

The collected data have been analyzed with the help of tools like Gap Analysis

and Factor Analysis

Limitations of the Study

The time spent for canvassing the bankers and customers to get the questionnaire

filled was considerable. Further, there was reluctance on the part of customers to respond

the questionnaire. The cost and time factors are the other limitations. However adequate

care was taken to collect unbiased data.

Gap Analysis

The gap analysis is carried out between the expected level and derived level of

satisfaction on the various aspects such as

Loan Flexibility;

Easy Access;

Security;

Customer friendly

Latest Facilities (Phone banking, Net banking, etc);

Reasonable Interest rate for Credit card transaction.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 9

This analysis is carried out using t-test based on the average score of the values

obtained for each factors. The significance is assessed using 5% level. The results are

presented in the following tables with suitable interpretations.

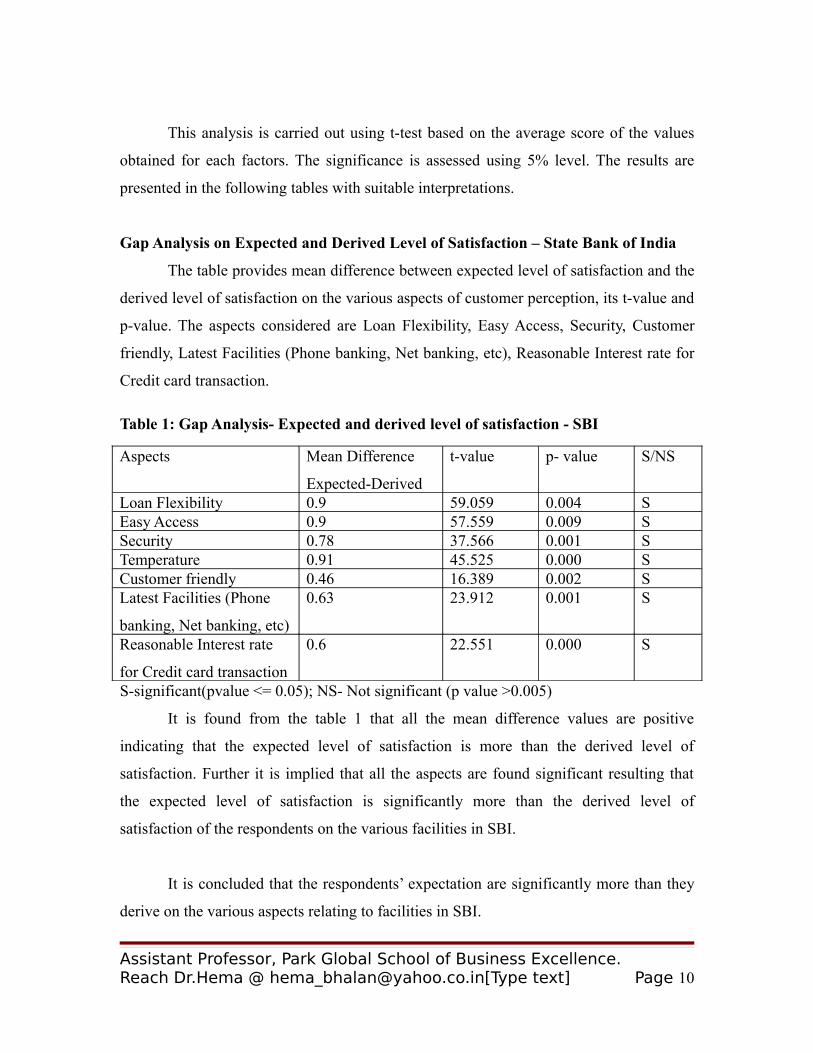

Gap Analysis on Expected and Derived Level of Satisfaction – State Bank of India

The table provides mean difference between expected level of satisfaction and the

derived level of satisfaction on the various aspects of customer perception, its t-value and

p-value. The aspects considered are Loan Flexibility, Easy Access, Security, Customer

friendly, Latest Facilities (Phone banking, Net banking, etc), Reasonable Interest rate for

Credit card transaction.

Table 1: Gap Analysis- Expected and derived level of satisfaction - SBI

Aspects Mean Difference

Expected-Derived

t-value p- value S/NS

Loan Flexibility 0.9 59.059 0.004 SEasy Access 0.9 57.559 0.009 SSecurity 0.78 37.566 0.001 STemperature 0.91 45.525 0.000 SCustomer friendly 0.46 16.389 0.002 SLatest Facilities (Phone

banking, Net banking, etc)

0.63 23.912 0.001 S

Reasonable Interest rate

for Credit card transaction

0.6 22.551 0.000 S

S-significant(pvalue <= 0.05); NS- Not significant (p value >0.005)

It is found from the table 1 that all the mean difference values are positive

indicating that the expected level of satisfaction is more than the derived level of

satisfaction. Further it is implied that all the aspects are found significant resulting that

the expected level of satisfaction is significantly more than the derived level of

satisfaction of the respondents on the various facilities in SBI.

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects relating to facilities in SBI.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 10

Gap Analysis: Expected and derived level of Satisfaction - SBI

0

1

2

3

4Loan Flexibility

Easy Access

Security

Customer Friendly

Latest Facilities

Reasonable Interest Rates

Expected

Derived

Gap Analysis on Expected and Derived Level of Satisfaction – IOB

The table provides mean difference of IOB between expected level of satisfaction

and the derived level of satisfaction on the various aspects of customer perception, its t-

value and p-value. The aspects considered are loan Flexibility, easy access, security,

customer friendly, latest Facilities (Phone banking, Net banking, etc), reasonable interest

rate for credit card transaction.

Table 2: Gap Analysis- Expected and derived level of satisfaction - IOB

Aspects Mean Difference (E-D) t-value p- value S/NS

Loan Flexibility 0.9 62.95 0.002 SEasy Access 0.9 46.123 0.000 SSecurity 0.9 55.687 0.003 SCustomer friendly 0.93 46.165 0.000 SLatest Facilities (Phone

banking, Net banking, etc)

0.96 54.311 0.000 S

Reasonable Interest rate

for Credit card transaction

0.2 9.703 0.005 S

S-significant(pvalue <= 0.05); NS- Not significant (p value >0.005)

It is found from the table 2 that all the mean difference values are positive

indicating that the expected level of satisfaction is more than the derived level of

satisfaction. Further it is implied that all the aspects are found significant resulting that

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 11

the expected level of satisfaction is significantly more than the derived level of

satisfaction of the respondents on the various aspects of Indian Overseas bank.

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects of Indian Overseas bank.

Gap Analysis: Expected and Derived level of Satisfaction - IOB

0

1

2

3

4Loan Flexibility

Easy Access

Security

Customer Friendly

Latest Facilities

Reasonable Interest Rates

Expected

Derived

Gap Analysis on Expected and Derived Level of Satisfaction – Indian Bank

The table provides mean difference of Indian Bank between expected level of

satisfaction and the derived level of satisfaction on the various aspects of customer

perception, its t-value and p-value. The aspects considered are loan Flexibility, easy

access, security, customer friendly, latest Facilities (Phone banking, Net banking, etc),

reasonable interest rate for credit card transaction.

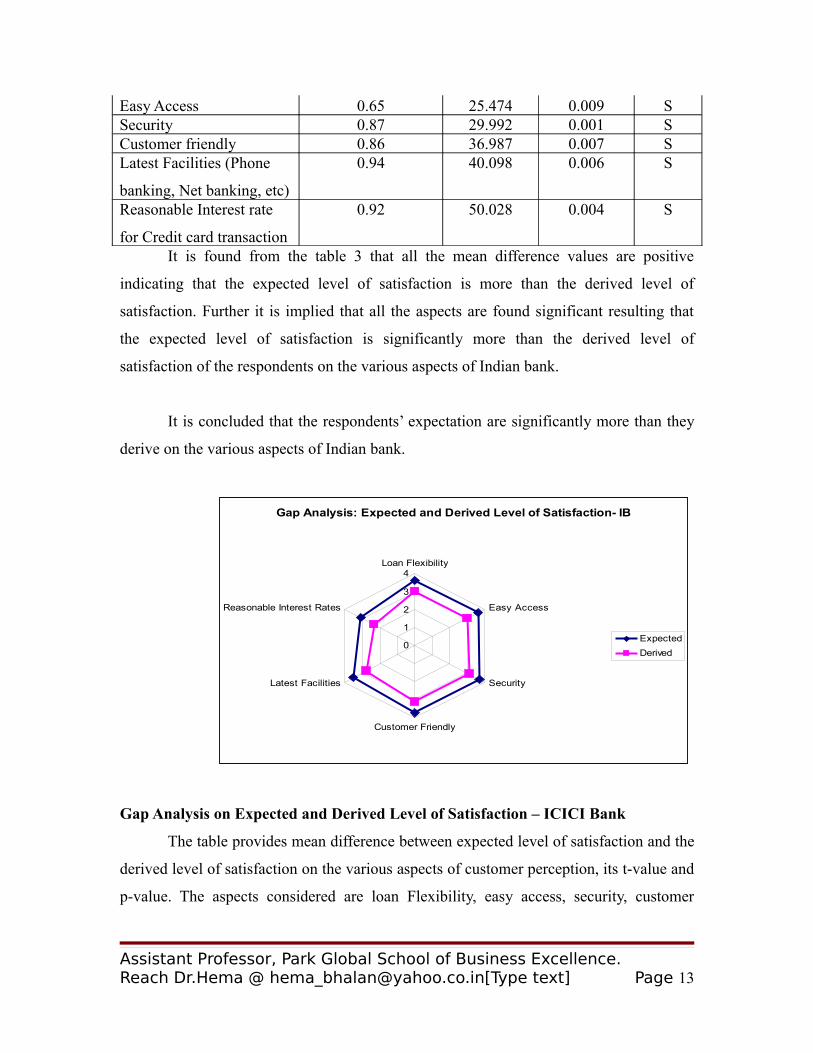

Table 3: Gap Analysis- Expected and derived level of satisfaction - IB

Aspects Mean Difference

Expected-Derived

t-value p- value S/NS

Loan Flexibility 0.62 24.097 0.003 S

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 12

Easy Access 0.65 25.474 0.009 SSecurity 0.87 29.992 0.001 SCustomer friendly 0.86 36.987 0.007 SLatest Facilities (Phone

banking, Net banking, etc)

0.94 40.098 0.006 S

Reasonable Interest rate

for Credit card transaction

0.92 50.028 0.004 S

It is found from the table 3 that all the mean difference values are positive

indicating that the expected level of satisfaction is more than the derived level of

satisfaction. Further it is implied that all the aspects are found significant resulting that

the expected level of satisfaction is significantly more than the derived level of

satisfaction of the respondents on the various aspects of Indian bank.

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects of Indian bank.

Gap Analysis: Expected and Derived Level of Satisfaction- IB

0

1

2

3

4Loan Flexibility

Easy Access

Security

Customer Friendly

Latest Facilities

Reasonable Interest Rates

Expected

Derived

Gap Analysis on Expected and Derived Level of Satisfaction – ICICI Bank

The table provides mean difference between expected level of satisfaction and the

derived level of satisfaction on the various aspects of customer perception, its t-value and

p-value. The aspects considered are loan Flexibility, easy access, security, customer

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 13

friendly, latest Facilities (Phone banking, Net banking, etc), reasonable interest rate for

credit card transaction.

Table 4: Gap Analysis- Expected and derived level of satisfaction - ICICI

Aspects Mean Difference

Expected-Derived

t-value p- value S/NS

Loan Flexibility 0.61 24.637 0.005 SEasy Access 0.61 25.066 0.001 SSecurity 0.61 23.922 0.001 SCustomer friendly 0.61 21.494 0.000 SLatest Facilities (Phone

banking, Net banking, etc)

0.72 28.127 0.004 S

Reasonable Interest rate

for Credit card transaction

0.75 29.045 0.001 S

S-significant(pvalue <= 0.05); NS- Not significant (p value >0.005)

It is found from the table 4 that all the mean difference values are positive

indicating that the expected level of satisfaction is more than the derived level of

satisfaction. Further it is implied that all the aspects are found significant resulting that

the expected level of satisfaction is significantly more than the derived level of

satisfaction of the respondents on the various facilities in ICICI bank.

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects relating to facilities in ICICI bank.

Gap Analysis; Expected and Derived Level of Satisfaction - ICICI

0

1

2

3

4Loan Flexibility

Easy Access

Security

Customer Friendly

Latest Facilities

Reasonable Interest Rates

Expected

Derived

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 14

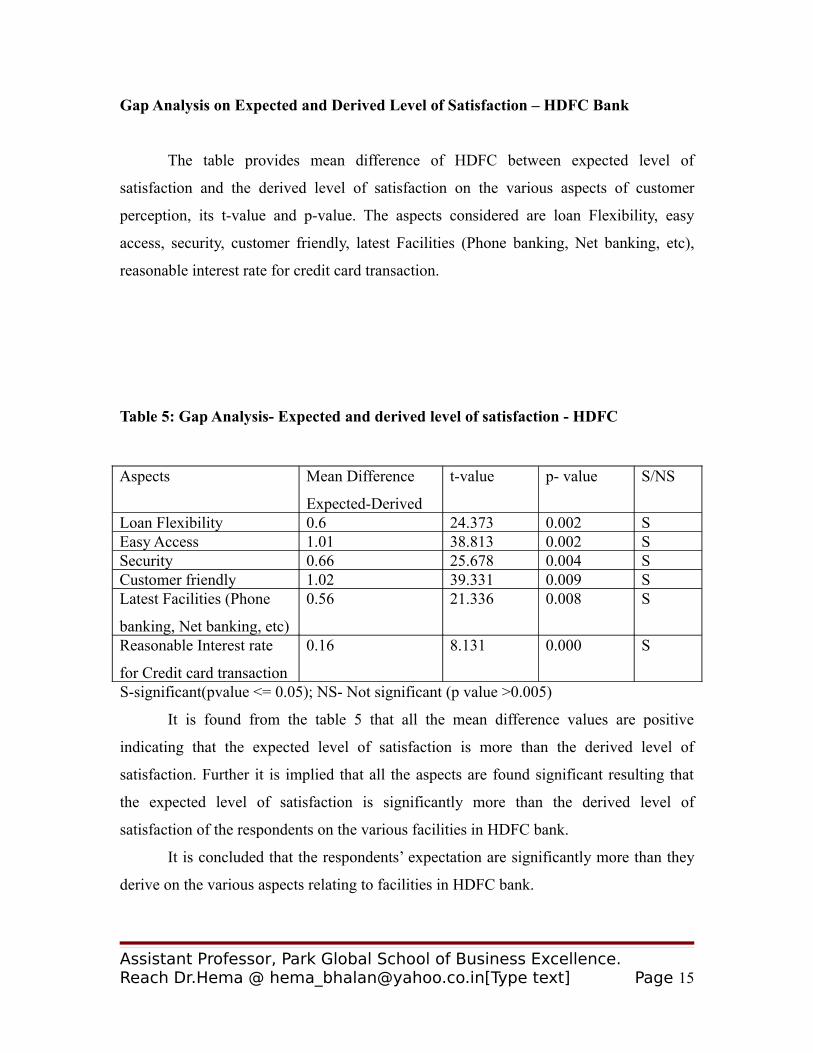

Gap Analysis on Expected and Derived Level of Satisfaction – HDFC Bank

The table provides mean difference of HDFC between expected level of

satisfaction and the derived level of satisfaction on the various aspects of customer

perception, its t-value and p-value. The aspects considered are loan Flexibility, easy

access, security, customer friendly, latest Facilities (Phone banking, Net banking, etc),

reasonable interest rate for credit card transaction.

Table 5: Gap Analysis- Expected and derived level of satisfaction - HDFC

Aspects Mean Difference

Expected-Derived

t-value p- value S/NS

Loan Flexibility 0.6 24.373 0.002 SEasy Access 1.01 38.813 0.002 SSecurity 0.66 25.678 0.004 SCustomer friendly 1.02 39.331 0.009 SLatest Facilities (Phone

banking, Net banking, etc)

0.56 21.336 0.008 S

Reasonable Interest rate

for Credit card transaction

0.16 8.131 0.000 S

S-significant(pvalue <= 0.05); NS- Not significant (p value >0.005)

It is found from the table 5 that all the mean difference values are positive

indicating that the expected level of satisfaction is more than the derived level of

satisfaction. Further it is implied that all the aspects are found significant resulting that

the expected level of satisfaction is significantly more than the derived level of

satisfaction of the respondents on the various facilities in HDFC bank.

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects relating to facilities in HDFC bank.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 15

Gap Analysis: Expected and Derived Level of Satisfaction- HDFC

0

1

2

3

4Loan Flexibility

Easy Access

Security

Customer Friendly

Latest Facilities

Reasonable Interest Rates

Expected

Derived

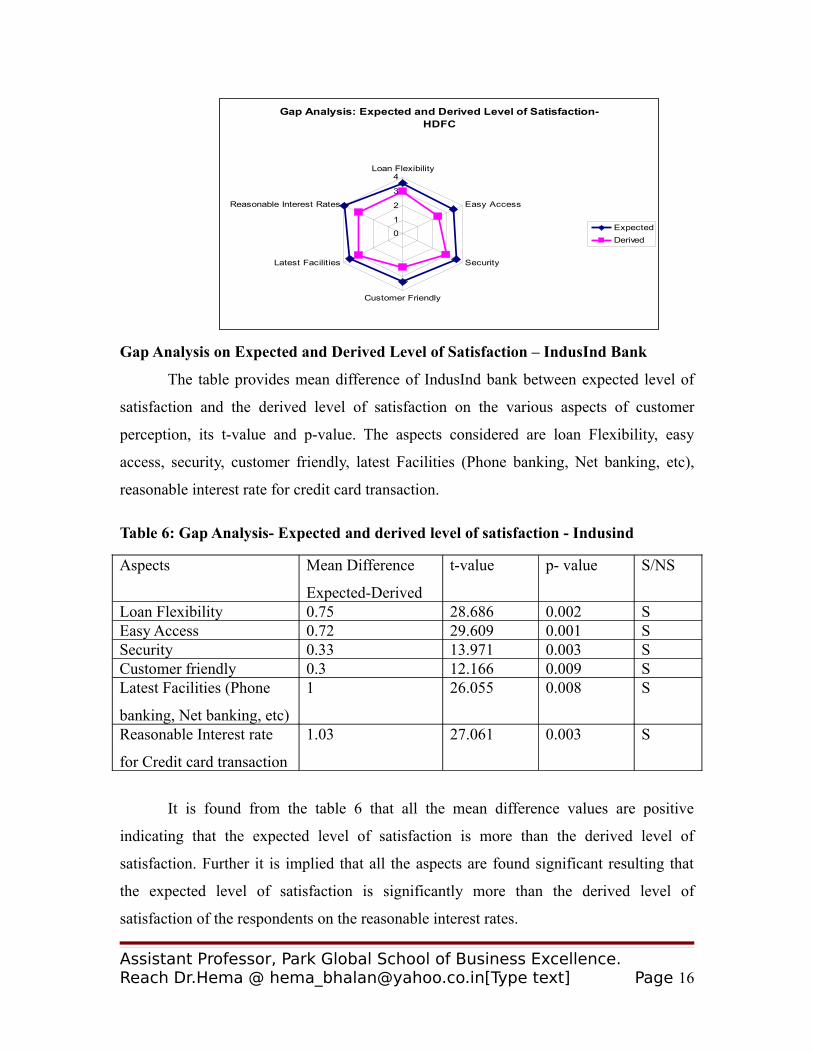

Gap Analysis on Expected and Derived Level of Satisfaction – IndusInd Bank

The table provides mean difference of IndusInd bank between expected level of

satisfaction and the derived level of satisfaction on the various aspects of customer

perception, its t-value and p-value. The aspects considered are loan Flexibility, easy

access, security, customer friendly, latest Facilities (Phone banking, Net banking, etc),

reasonable interest rate for credit card transaction.

Table 6: Gap Analysis- Expected and derived level of satisfaction - Indusind

Aspects Mean Difference

Expected-Derived

t-value p- value S/NS

Loan Flexibility 0.75 28.686 0.002 SEasy Access 0.72 29.609 0.001 SSecurity 0.33 13.971 0.003 SCustomer friendly 0.3 12.166 0.009 SLatest Facilities (Phone

banking, Net banking, etc)

1 26.055 0.008 S

Reasonable Interest rate

for Credit card transaction

1.03 27.061 0.003 S

It is found from the table 6 that all the mean difference values are positive

indicating that the expected level of satisfaction is more than the derived level of

satisfaction. Further it is implied that all the aspects are found significant resulting that

the expected level of satisfaction is significantly more than the derived level of

satisfaction of the respondents on the reasonable interest rates.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 16

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects relating to various facilities in Indusind bank.

Gap Analysis: Expected and Derived level of Satisfaction - Indusind

0

1

2

3

4Loan Flexibility

Easy Access

Security

Customer Friendly

Latest Facilities

Reasonable Interest Rates

Expected

Derived

Factor Analysis

The factor analysis is mainly employed for 2 purposes

1. For data reduction

2. For identifying the factor which influences most.

In this section the factor analysis under extraction method of principal component

analysis is employed to identify the important aspects relating to customer perception on

public sector and private sector banks.

Important factors are identified with extraction value more than 0.7. The results

are presented in table 7. Table 7 describes the extraction values for each aspect relating to

customer perception on public sector and private sector banks.

through principal component analysis.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 17

Table 7: Extraction Values- Aspects relating to customer perception on service of

banks

Aspects Extraction values

Customer Friendly 0.888

Easy Access 0.910

Can Relax 0.795

Stress Reduction 0.771

Security 0.836

Safe 0.720

Go to bank with a trobled mind and ther sort it out for you 0.816

Sleep in night without worrying whats going on 0.640

Facilities are too good 0.657

Come away with a aproportion of what you want 0.764

Got what you went down for 0.743

Everything went according to plan 0.762

Met expectations 0.767

To be unsatisfied when you come and you are still in the same level

as you went before

0.409

Happy with results 0.551

Content with whats been done for you 0.574

Awareness about net banking 0.534

Not frustrated 0.462

Everything goes smooth 0.710

No hassle 0.787

Straight forward 0.409

It is found from the table 7 that among the 21 aspects relating to customer

perception towards public and private sector banks 14 aspects are considered as more

important than other aspects because of their expectation value more than 0.7. Further it

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 18

can be deduced that “ easy access” is considered as very important because of its high

extraction value 0.910 followed by “customer friendly” (0.888); “security” (0.836); “Go

to bank with a troubled mind and there sort it out for you” (0.816); “can relax” (0.795)

and so on.

It is concluded that among the various aspects relating to perception of customers

“easy access” is considered as more important than the other factors.

Factors Influencing Customer Perception

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Wal

ked

out

Can

Rel

ax

Sec

ure

Go

to b

ank

Ach

ievi

ng

Got

wha

t yo

u

Met

Hap

py w

ith

Hap

py w

ith

Eve

ryth

ing

Str

aigh

t

Series1

Findings based on GAP Analysis

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects relating to facilities in SBI.

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects of Indian Overseas bank.

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects of Indian bank.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 19

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects relating to facilities in ICICI bank.

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects relating to facilities in HDFC bank.

It is concluded that the respondents’ expectation are significantly more than they

derive on the various aspects relating to various facilities in Indusind bank.

Findings from Factor Analysis

It is concluded that among the various aspects relating to perception of customers

“easy access” is considered as more important than the other factors.

SUGGESTIONS, DISCUSSIONS AND CONCLUSIONS

Suggestions

The following suggestions are the outcome of the research and applications of these

Every bank should take precautions to keep customers experience safe. It should

take continued efforts to safeguard online banking transactions.

All internet banks should provide close interaction between bank service and web

based e-commerce and even service through direct electronic payments.

The bank should provide more convenient international transactions which means

internet along with general trends.

Elimination of geographical boundaries will help free access of internet banking.

The bank should provide more customer awareness and need of transparency in

their dealings.

All banks should provide digital certification procedure as it helps the customers

data that they receive from the correct system.

The banks should come up with innovative ways of service at their door steps this

may be a costly affair but will surely give positive results in the long run.

The banks should take the initiative of training the advisors about the new

schemes from time to time which also makes the advisors connected to the bank.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 20

The banks should also emphasis on the monitoring of EMI which directly relates

to the returns of a loan amount.

The company should come up with proper fixed deposit plans at this point of time

where the market is highly volatile and the investors become very cautious at this

level.

The banks should use brand ambassadors for example the CEO’s of major

companies where the company allocate the funds. This will probably ensure

proper results.

The banks should focus on the advertising strategy and also the marketing of the

bank product.

The bank doesn’t have enough tax saving plans or appropriate plans for tax so

which they should come up with.

Managerial Implications and Discussions

Good Performance, Questionable Health

Indian banks have compared favourably on growth, asset quality and profitability

with other regional banks over the last few years. The banking index has grown at a

compounded annual rate of over 51 per cent since April 2001 as compared to a 27 per

cent growth in the market index for the same period. Policy makers have made some

notable changes in policy and regulation to help strengthen the sector. These changes

include strengthening prudential norms, enhancing the payments system and integrating

regulations between commercial and co-operative banks. However, the cost of

intermediation remains high and bank penetration is limited to only a few customer

segments and geographies. While bank lending has been a significant driver of GDP

growth and employment, periodic instances of the “failure” of some weak banks have

often threatened the stability of the system. Structural weaknesses such as a fragmented

industry structure, restrictions on capital availability and deployment, lack of institutional

support infrastructure, restrictive labour laws, weak corporate governance and ineffective

regulations beyond Scheduled Commercial Banks (SCBs), unless addressed, could

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 21

seriously weaken the health of the sector. Further, the inability of bank managements

(with some notable exceptions) to improve capital allocation, increase the productivity of

their service platforms and improve the performance ethic in their organisations could

seriously affect future performance.

Opportunities and Challenges for Players

The bar for what it means to be a successful player in the sector has been raised.

Four challenges must be addressed before success can be achieved. First, the market is

seeing discontinuous growth driven by new products and services that include

opportunities in credit cards, consumer finance and wealth management on the retail side,

and in fee-based income and investment banking on the wholesale banking side. These

require new skills in sales & marketing, credit and operations. Second, banks will no

longer enjoy windfall treasury gains that the decade-long secular decline in interest rates

provided. This will expose the weaker banks. Third, with increased interest in India,

competition from foreign banks will only intensify. Fourth, given the demographic shifts

resulting from changes in age profile and household income, consumers will increasingly

demand enhanced institutional capabilities and service levels from banks.

Need to Create a Market-Driven Banking Sector with Adequate Focus on Social

Development

The term “policy makers” used in this thesis, refers to the Ministry of Finance and

the RBI and includes the other relevant government and regulatory entities for the

banking sector. We believe a co-ordinated effort between the various entities is required

to enable positive action. This will spur on the performance of the sector. The policy

makers need to make co-ordinated efforts on six fronts: Help shape a superior industry

structure in a phased manner through “managed consolidation” and by enabling capital

availability.

Focus on Social Development

Focus strongly on “social development” by moving away from universal directed

norms to an explicit incentive-driven framework by introducing credit guarantees and

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 22

market subsidies to encourage leading public sector, private and foreign players to

leverage technology to innovate and profitably provide banking services to lower income

and rural markets. Create a unified regulator, distinct from the central bank of the

country, in a phased manner to overcome supervisory difficulties and reduce compliance

costs. Improve corporate governance primarily by increasing board independence and

accountability. Accelerate the creation of world class supporting infrastructure (e.g.,

payments, asset reconstruction companies (ARCs), credit bureaus, back-office utilities) to

help the banking sector focus on core activities. Enable labour reforms, focusing on

enriching human capital, to help public sector and old private banks become competitive.

Need For Decisive Action by Bank Managements

Management imperatives will differ by bank. However, there will be common

themes across classes of banks: PSBs need to fundamentally strengthen institutional skill

levels especially in sales and marketing, service operations, risk management and the

overall organisational performance ethic. The last, i.e., strengthening human capital will

be the single biggest challenge. Old private sector banks also have the need to

fundamentally strengthen skill levels. However, even more imperative is their need to

examine their participation in the Indian banking sector and their ability to remain

independent in the light of the discontinuities in the sector. New private banks could

reach the next level of their growth in the Indian banking sector by continuing to innovate

and develop differentiated business models to profitably serve segments like the rural/low

income segments; actively adopting acquisitions as a means to grow and reaching the

next level of performance in their service platforms.

Attracting, developing and retaining more leadership capacity would be key to

achieving this and would pose the biggest challenge. Foreign banks committed to making

a play in India will need to adopt alternative approaches to win the “race for the

customer” and build a value-creating customer franchise in advance of regulations

potentially. At the same time, they should stay in the game for potential acquisition

opportunities as and when they appear in the near term. Maintaining a fundamentally

long-term value-creation mindset will be their greatest challenge. The extent to which

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 23

Indian policy makers and bank managements develop and execute such a clear and

complementary agenda to tackle emerging discontinuities will lay the foundations for a

high-performing sector in the near future

Scope for Future Research

There is a wide scope to extend this study in the future. Future researchers may

continue the same study or they can study by taking all the private sector banks or public

sector banks. The study may be done as a world wide study to bring about the potential of

the bank industry.

Conclusion

The last decade has seen many positive developments in the Indian banking

sector. The policy makers, which comprise the Reserve Bank of India (RBI), Ministry of

Finance and related government and financial sector regulatory entities, have made

several notable efforts to improve regulation in the sector. The sector now compares

favourably with banking sectors in the region on metrics like growth, profitability and

non-performing assets (NPAs). A few banks have established an outstanding track record

of innovation, growth and value creation. This is reflected in their market valuation.

However, improved regulations, innovation, growth and value creation in the sector

remain limited to a small part of it. The cost of banking intermediation in India is higher

and bank penetration is far lower than in other markets. India’s banking industry must

strengthen itself significantly if it has to support the modern and vibrant economy which

India aspires to be. While the onus for this change lies mainly with bank managements,

an enabling policy and regulatory framework will also be critical to their success. The

failure to respond to changing market realities has stunted the development of the

financial sector in many developing countries. A weak banking structure has been unable

to fuel continued growth, which has harmed the long-term health of their economies. In

this “white paper”, we emphasise the need to act both decisively and quickly to build an

enabling, rather than a limiting, banking sector in India.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 24

References

1. C.Ashokan, Hariharan.G, “Profile and Perception of Retail Consumers – An Empirical study in Palakkad District”, Indian Journal of Marketing, Vol: XXXVIII, Number: 2, February 2008, PP – 44.

2. Dr.N.Panchanathan, S.Senthilkumar, Dr.R.Mathivannan, K.S.Selvavinayagam, “A study on Consumer Preference and Satisfaction in Uzhavar Sandai at Namakkal District”, Indian Journal of Marketing, Vol: XXXVIII, No: 2, February 2008, PP – 30.

3. Dr.Shrimant F.Tangade, Dr.Basavarj C.S, “Perceptions about Consumers Protection Laws and the Consumer Forum – An Empirical study of Complainant – Consumers of Aulbarga District”, Indian Journal of Marketing, Vol: XXXVI, No: 6, June 2006, PP – 30.

4. Dr.B.V.R.Naidu, “Buyers Perception towards Prawn Feed – A study in West Godavari District, Andhra Pradesh”, Indian Journal of Marketing, Vol: XXXVII, No: 10, October 2007, PP – 19.

5. M.Bhaskar Roa, “Tourists’ Perceptions Towards Package Tours”, Indian Journal of Marketing, Vol: XXXVII, No: 5, May 2007, PP – 28.

6. Dr.R.Ganapathi and Dr.T.Ramasamy, “A study on Consumers’ Expectation Towards Share Brokers”, Indian Journal of Marketing, Vol: XXXVII, No: 9, September 2007, PP – 38.

7. Dr.Sasmita Mishra, Swapna Menon and Sree Kumar, “Consumers Attitude towards Network Marketing with special reference to the city of Rourkela”, Indian Journal of Marketing, Vol: XXXVIII, No: 3, March 2008, PP – 42.

8. Vigg Silky, Mathur Garima, Holani Umesh,“Customer satisfaction in retail services: A comparative study of public and private sector banks”, The Journal of Indian Management & Strategy 8M, Volume: 12, Issue: 2, Year: 2007.

9. R.A. Ravi , “User Perception of Retail Banking Services: A Comparative Study of Public and Private Sector Banks”, The ICFAI Journal of Bank Management, Vol. 12, No. 2, May 2008 , pp. 32-46

10. Ivana Adamson, Kok- Mun Chan, Donna Handford, “Relationship Marketing: Customer Commitment and Trust as a strategy for Smaller Hong Kong Corporate Banking Sector”, International Journal of Bank Marketing,Vol.21, No. 6/7, 2003, pp. 347-358.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 25

11. Arturo Molina, David Martin- Consuegra, Agueda Esteban, “Relational Benefis and Customer Satisfaction in Retail banking”, International journal of Bank Marketing, Vol.25, No.4, 2007, 253-271.

12. Raechel Johns, Bruce Perott, “The Impact of Internet Banking on Business- Customer relationships (Are You Being Self-Served)”, International journal of Bank Marketing, Vol 26, No.7, 2008, pp.465-482.

13. Anita Lifen Zhao, Stuart Hanmer- Lioyd, Philippa Ward, Mark M.H. Goode, “Perceived Risk and Chinese Consumers’ Internet Banking Services Adoption”, Vol 26, No.7, 2008, pp.505-525.

14. Aruna Dhade and Manish Mittal, “Preferences, Satisfaction Level and Chances of Shifting: A Study of the Customers of Public Sector and New Private Sector Banks”, The Icfai University Journal of Bank Management, May, 2008

15. G.S. Suresh Chander, Chandrasekharan Rajendran, R.N. Anantharaman, “Customer Perceptions of Service quality in the Banking Sector of a Developing Economy: A Critical Analysis”, International Journal of Bank Marketing, Vol 21, No5, 2003, pp.233-242.

16. R.A.Ravi, “User Perception of Retail Banking Services: A Comparitive Study of Public and Private Sector Banks”, ICFAI University Journal of Bank Management, May 2008.

17. Dimitrios K. Koutouvalas and George J. Siomkos, “An examination of the relationship between service quality perceptions and customer loyalty in public versus private Greek banks” International Journal of Financial Services Management, Vol 1, No. 2-3 , 2006, pp. 190 – 204.

18. Peter Kangis, Vassilis Voukelatos, “Private and Public Banks: A Comparision of Customer Expectations and Perceptions”, International Journal of bank Marketing, Vol.15, No.7, 1997, pp. 279-287

19. Chowdari Prasad, K.S.Srinivasa Rao, “Private Sector Banks in India—A SWOT Analysis”, The ICFAI University Journal of bank Management, Vol.4, Issue.1, Feb 2005, pp.31-63.

20. Shrimal Perera, Michael Skully, J. Wickramanayake, “Cost Efficiency in South Asian Banking: The Impact of Bank Size, State Ownership and Stock Exchange Listings”, International review of Finance, Vol. 7, No.1-2., pp.35-60.

21. Mishra, Garima, Goyal, Rashi, “The World and the Indian Banking Industry”, University Library of Munich, MPRA Paper with Number 1266, Aug 26, 2006.

22. Global Banking Industry, Report, April 2006

23. Technology Spend Outlook for Asian Banks during the Crisis Period (2009-2010), www.thebankingacademy.com, Publication Date: 3 March, 2009, Category: Regional Surveys.

Assistant Professor, Park Global School of Business Excellence.Reach Dr.Hema @ [email protected][Type text] Page 26