mirror.unhabitat.orgmirror.unhabitat.org/downloads/docs/3662_46163_hs-311.pdfjakarta a. scope and...

TRANSCRIPT

Page 1

National Trends in Housing-Production PracticesVolume 2: Indonesia

Table of Contents

Foreword

I. A changing shelter policy

A. Scope and scale of the shelter problem

o 1. Identifying the poor

o 2. Housing stock

o 3. Housing need

o 4. Housing demand

o 5. Housing supply

B. Reorganization of the housing sector

II. Housing supply at the national level

A. Actors in the shelter-delivery process

o 1. Government and public-sector agencies

a. Perum-Perumnas

b. BTN

c. Other public-sector actors

o 2. Actors in the private formal sector

a. Private contractors

b. Financial institutions

o 3. Informal-sector actors

a. NGOs

b. CBOs

c. Cooperatives

d. Individuals/households

B. Housing finance

o 1. Household savings for housing

a. BTN savings

o 2. Housing-credit systems

a. BTN credit schemes

Page 2

b. P. T. Papan Sejahtera credit schemes

o 3. Incentives for investment in housing

o 4. Subsidies in the housing sector

o 5. Affordability

III. Jakarta

A. Scope and scale of the shelter problem

o 1. Housing stock

o 2. Housing needs

B. Actors and housing supply

o 1. Public-sector actors

a. Perum-Perumnas

b. Jakarta housing enterprises

c. Bappem KIP-MHT

d. Central-government agencies

o 2. Private-sector actors

o 3. Other actors

C. Summary and recommendations

IV. Bandung

A. Scope and scale of the shelter problem

o 1. Housing stock

o 2. Housing needs

B. Actors and housing supply

o 1. Public-sector actors

a. Perum-Perumnas

b. Bandung Municipality

i. Bandung Urban Development Project (BUDP)

ii. INDAL Pilot Renewal Project

c. Government agencies

o 2. Private-sector actors

o 3. NGOs

Page 3

a. The Environmental Research Centre (PPLH)

b. The Institute of Community Self-help (LPSM)

o 4. CBOs and cooperatives

a. Tamansari Rental Housing

b. Palasari arisan Housing

c. St. Borromeus Hospital Employee Credit Cooperative

d.. Bina Karya

C. Summary and recommendations

V. Alleviating the housing problem in Indonesia: Conclusions and recommendations

A. Access to credit and affordability

B. Access to land

C. Building regulations

D. "Positive" regulations on housing developments

E. Transport

F. Building materials

G. Decentralization and community participation

Bibliography

Page 4

National Trends in Housing-Production PracticesVolume 2: Indonesia

List of figures

1. Main actors in housing finance in Indonesia, by income group

Page 5

Figure 1. Main actors in housing finance in Indonesia, by income group

Page 6

National Trends in Housing-Production PracticesVolume 2: Indonesia

List of tables

1. Planned Perum-Perumnas and REI housing production (1974-1994)

2. Actual Perum-Perumnas and REI housing production (1974-1991)

3. Population, Indonesia (1961-2000)

4. Population growth, 1961-2000 (average percentage/year)

5. Land area, population, and population density, Indonesia

6. Urban household incomes (1976)

7. Official poverty lines in Indonesia (1976-1990)

8. Urban household incomes, Indonesia (1992)

9. Housing stock, Indonesia (1989)

10. Housing tenure, Indonesia (1989)

11. Size of houses (1989)

12. Housing preferences (1991), by desired type and monthly expenditure class

13. Urban formal-sector housing production, by actors (to 1990)

14. Rural formal-sector housing production, by programme (to 1990)

15. Volume of urban formal-housing production, by actors (to 1991)

16. Settlement-upgrading programmes (1969-1994)

17. Settlement improvement projects (to 1991)

18. Housing production by Perum-Perumnas (1974-1991)

19. REI housing production, by income group (to 1991)

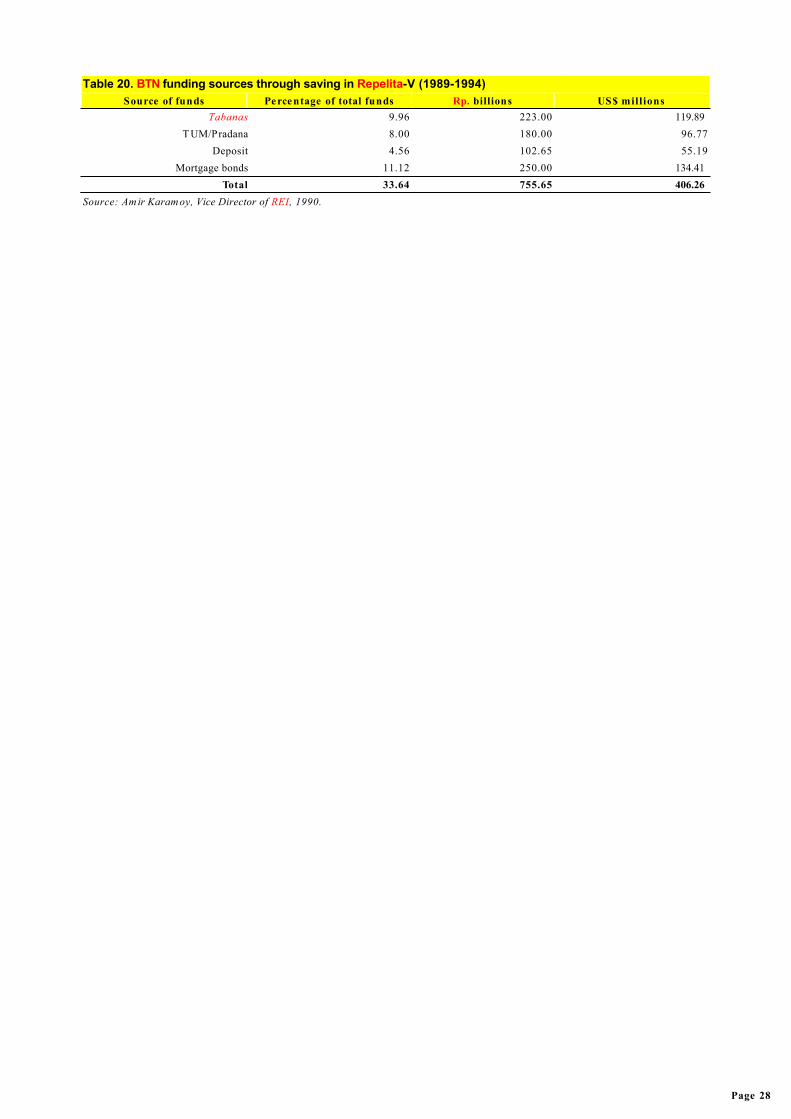

20. BTN funding sources through saving in Repelita-V (1989-1994)

21. Inflation and exchange rates (1976-1992)

22. BTN interest rates (1976-1992)

23. Ownership credit/loan systems of BTN (1992)

24. Papan Sejahtera's interest rates (1992)

25. Average house prices (1992)

26. Population of Jakarta (l990)

27. Housing ownership, Jakarta (1990)

28. Housing needs, Jakarta (l990)

Page 7

29. Housing production, Jakarta (to 1992)

30. Housing production, Botabek (to 1992)

31. Expected housing demand, Jakarta (1990-1995)

32. Perum-Perumnas housing production, Jakarta (to 1992)

33. Rental flats owned by DKI Jakarta (1990)

34. REI housing developments in Jabotabek, by source of finance (to 1992)

35. Housing stock, Bandung (1992)

36. Perum-Perumnas housing production, Bandung (to 1992)

Page 8

Table 1. Planned Perum-Perumnas and REI housing production (1974-1994)Repelita Perum-Perumnas Private and REI Total

II 73,000 - 73,000III 100,000 70,000 170,000IV 140,000 160,000 300,000V 122,500 327,500 450,000

Total 435,500 557,500 993,000Source: CBS, 1989a; 1992a; 1992c; and Sardjono (1986).

Page 9

Table 2. Actual Perum-Perumnas and REI housing production (1974-1991)Repelita Perum-Perumnas Private and REI Total

II-IV 198,594 698,911 897,505Va 17,962 243,441 261,403

Total 216,556 942,352 1,158,908a: Up to 1991Source: CBS, 1989a; 1992a; 1992c; Sardjono, 1986.

Page 10

Table 3. Population, Indonesia (1961-2000)

YearUrban

Rural

Total MillionMillion Percentage Million Percentage1961 14 14.4 83 85.6 971971 21 17.6 98 82.4 1191980 33 22.3 115 77.7 1481990 55 30.6 125 69.4 1802000 a 85 38.6 135 61.4 220

a: Projected.Source: CBS, 1992c; 1992d.

Page 11

Table 4. Population growth, 1961-2000 (average percentage/year)Period Urban Rural Total

1961-1971 4.14 1.68 2.071971-1980 5.15 1.79 2.451980-1990 5.24 0.84 1.981990-2000a 4.45 0.77 2.03

a: Projected.Source: Based on CBS, 1992d.

Page 12

Table 5. Land area, population, and population density, Indonesia

IslandArea

(percentage)Population

(percentage)Population density

(persons/km²)Java 7 60 814

Nusa T enggara 5 6 115Sumatera 25 20 77Sulawesi 10 7 66

Kalimantan 28 5 17Irian Jaya 22 1 7

Other islands 3 1 n.a.Totals 100 100 89

Source: CBS, 1992d:39-40.

Page 13

Table 6. Urban household incomes (1976)

Income groupPercentage of

total populationMonthly income

Rp.'000 US $Highest 2 > 90 > 214Middle 8 50-90 119-214

Moderate 20 30-50 71-119Low 30 10-30 24-71

Lowest 40 < 10 < 24Source: Modified from Prisma Magazine, 1986b:12-23.

Page 14

Table 7. Official poverty lines in Indonesia (1976-1990)

Year

Per capita poverty line

Percentage of population living be lowthe poverty lineUrban area

Rural area

Rp. $ Rp. $ Urban areas Rural areas Total1976 4,522 11 2,849 8 39 40 401978 4,969 12 2,981 8 31 33 331980 6,831 12 4,449 8 29 28 291981 9,777 15 5,887 9 28 26 271984 13,731 13 7,746 7 23 21 221987 17,381 11 10,294 6 20 16 171990 20,614 11 13,925 7 17 14 15

Source: CBS, 1989a; 1992d; Swasembada magazine, 1988a.

Page 15

Table 8. Urban household incomes, Indonesia (1992)

Income groupPercentage of urban

populationMonthly incomes

Equivalent to:Rp.'000 US $High 5 > 3,500 > 1,748 Business persons

Middle 15 1,250-3,500 619-1,748 ProfessionalsModerate 20 750-1,250 371-619 3rd and 4th group of civil servants

Low 40 (Upper) 450-750 228-371 2nd group of civil servants (Lower) 100-450 50-228 1st group of civil servants

Lowest 20 < 100 < 50 Informal sector below poverty lineSource: BTN, 1992a; CBS, 1992d; Herlianto, 1993; REI, 1990.

Page 16

Table 9. Housing stock, Indonesia(1989)Area Number of housing units Percentage

Urban 10,826,352 27.8Rural 28,094,808 72.2Total 38,921,160 100.0

Source: CBS, 1990:14.

Page 17

Table 10. Housing tenure, Indonesia (1989)Type of tenure Urban areas Rural areas Total

Own 65.7 92.4 85.0Lease 12.0 0.4 3.6

Rented 8.0 0.9 2.9Instalment plan 1.0 0.1 0.3

Official 3.8 1.5 2.1Rent free 5.3 2.5 3.3

Other 4.1 2.2 2.8Total 99.9 100.0 100.0

Source: CBS, 1990:58-63.

Page 18

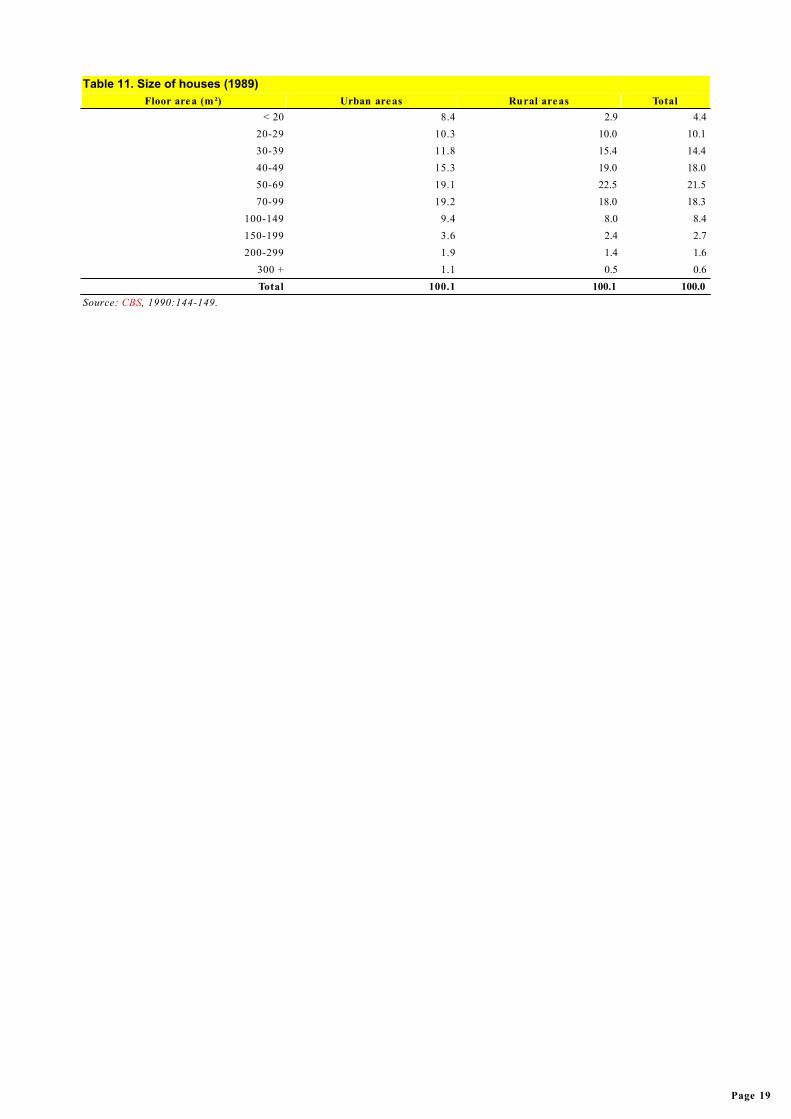

Table 11. Size of houses (1989)Floor area (m²) Urban areas Rural areas Total

< 20 8.4 2.9 4.420-29 10.3 10.0 10.130-39 11.8 15.4 14.440-49 15.3 19.0 18.050-69 19.1 22.5 21.570-99 19.2 18.0 18.3

100-149 9.4 8.0 8.4150-199 3.6 2.4 2.7200-299 1.9 1.4 1.6

300 + 1.1 0.5 0.6Total 100.1 100.1 100.0

Source: CBS, 1990:144-149.

Page 19

Table 12. Housing preferences (1991), by desired type and monthly expenditure class

Expenditure classSize of unit (m²)

Maisonette Total18 21 27 36 45 51 70 90 120 150 250 300< 30 15 53 5 - 16 3 8 - - - - - - 100

30-39 24 13 12 17 20 5 6 - - - - - 3 10040-49 20 17 13 24 14 3 6 2 - - - 1 - 10050-74 19 18 10 25 17 6 5 1 - 1 - - - 10275-99 14 20 10 22 15 6 7 2 1 1 1 1 - 100

100-149 12 24 11 23 14 5 8 1 1 1 1 1 - 102150-199 6 14 10 25 19 5 12 3 1 1 1 2 - 99200-299 3 12 9 28 16 8 14 4 3 1 2 1 1 102300-399 2 4 5 22 17 6 27 3 5 7 - 3 - 101400-499 - 7 4 19 21 5 20 2 11 4 - 7 - 100

500 + - 6 1 14 23 6 23 8 3 9 - 9 1 103Total 11 17 10 24 16 6 10 2 1 1 1 1 1 101

Source: CBS, 1992a:356-359.

Page 20

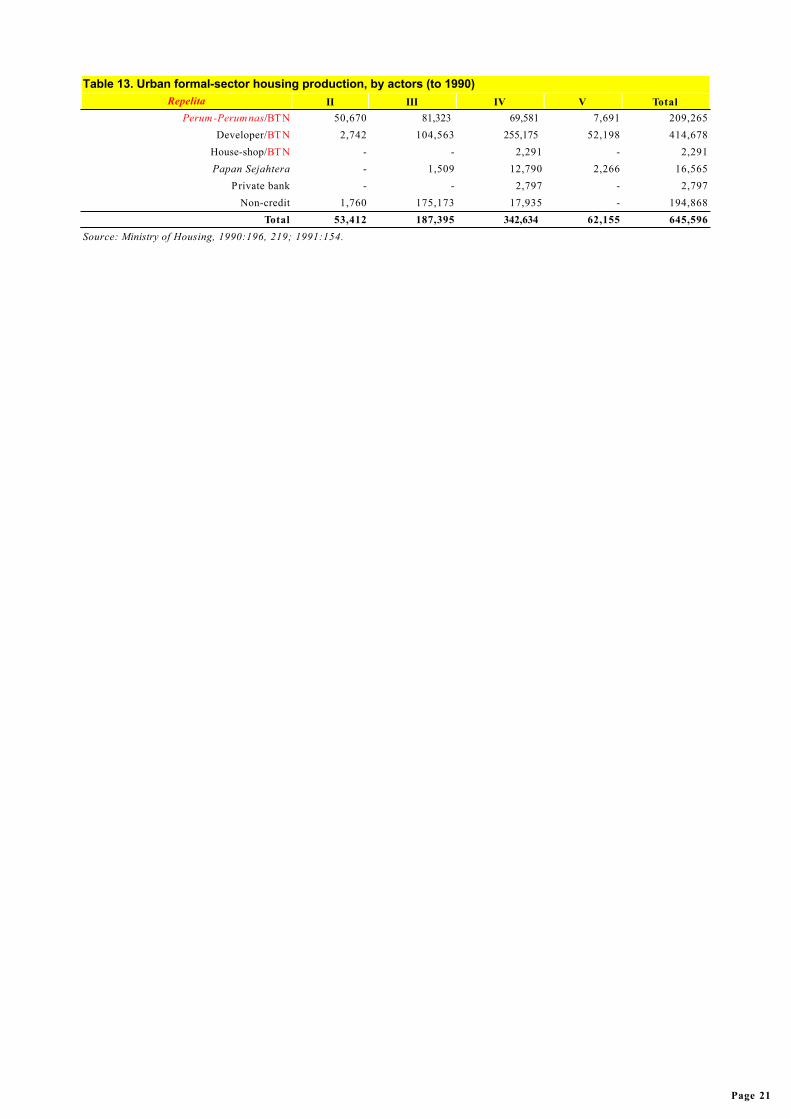

Table 13. Urban formal-sector housing production, by actors (to 1990)Repelita II III IV V Total

Perum-Perumnas/BT N 50,670 81,323 69,581 7,691 209,265Developer/BT N 2,742 104,563 255,175 52,198 414,678

House-shop/BT N - - 2,291 - 2,291Papan Sejahtera - 1,509 12,790 2,266 16,565

Private bank - - 2,797 - 2,797Non-credit 1,760 175,173 17,935 - 194,868

Total 53,412 187,395 342,634 62,155 645,596Source: Ministry of Housing, 1990:196, 219; 1991:154.

Page 21

Table 14. Rural formal-sector housing production, by programme (to 1990)Repelita II-III IV V

P2LDT (units) - 190,395 -P2LDT (villages) - 7,946 -

T ransmigration - 597,502 -Social housing - 12,190 -

Source: Ministry of Housing, 1990:196, 219; 1991:154.

Page 22

Table 15. Volume of urban formal-housing production, by actors (to 1991)Built by Number of units Percentage

Perum-Perumnas 216,556 18.7Private developers with BT N credit facilities (including members of REI) 725,966 62.6

REI for the middle- and high-income groups with assistance of private banks such asPapanSejahtera 216,386 18.7

Total 1,158,908 100.0Source: CBS, 1992a.

Page 23

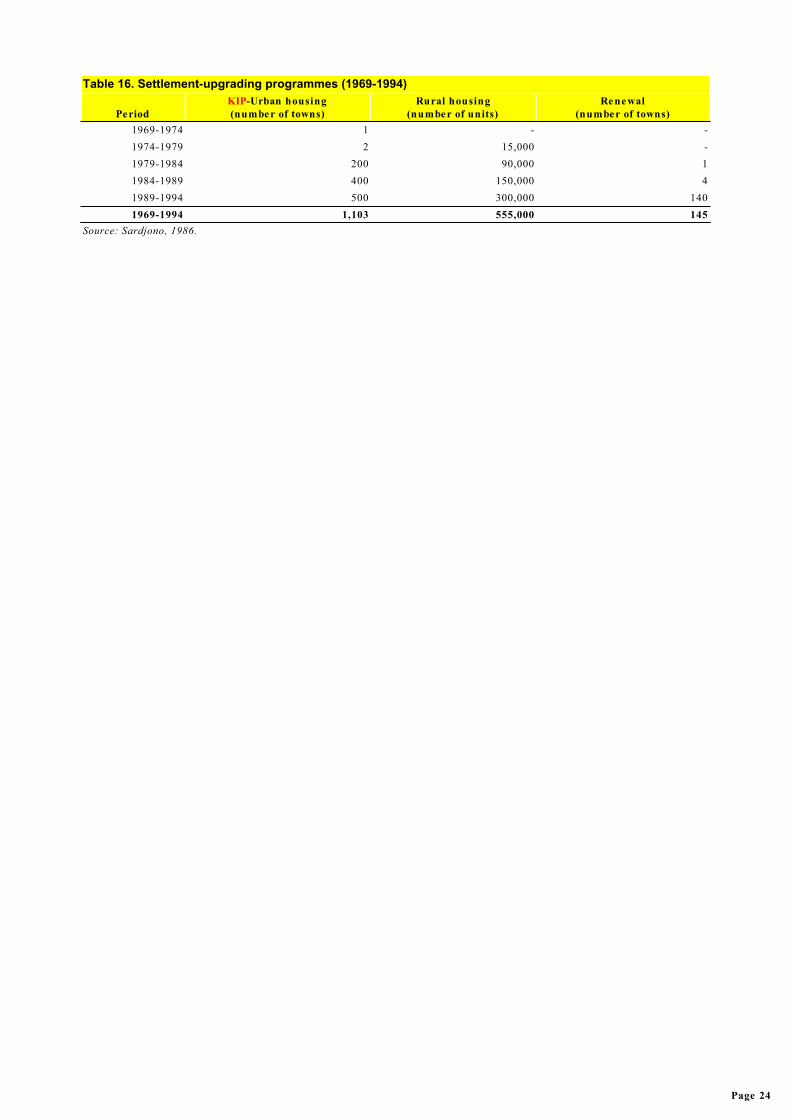

Table 16. Settlement-upgrading programmes (1969-1994)

PeriodKIP-Urban housing(number of towns)

Rural housing(number of units)

Renewal(number of towns)

1969-1974 1 - -1974-1979 2 15,000 -1979-1984 200 90,000 11984-1989 400 150,000 41989-1994 500 300,000 1401969-1994 1,103 555,000 145

Source: Sardjono, 1986.

Page 24

Table 17. Settlement improvement projects (to 1991)Programme Number of citie s/villages Hectares Households

KIP 212 981 n.a.P2LPK 981 12,250 n.a.P2LDT 441 21,194 56,226

Source: Ministry of Housing, 1990.

Page 25

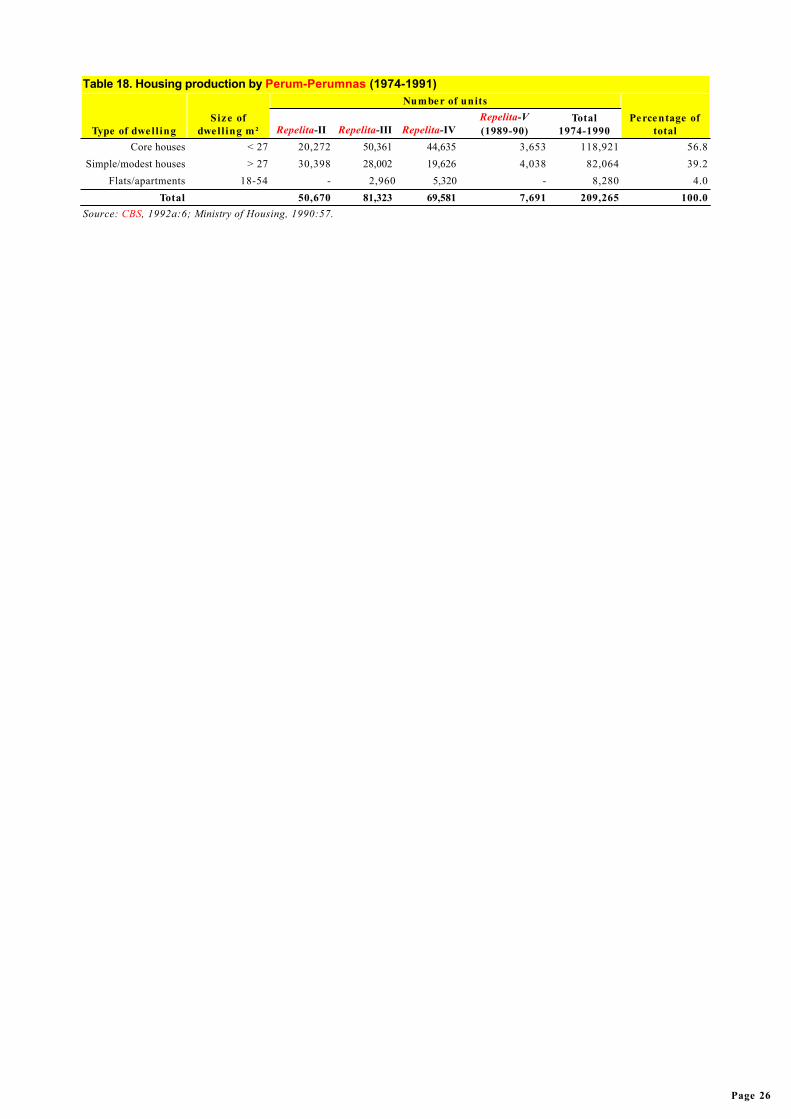

Table 18. Housing production by Perum-Perumnas (1974-1991)

Type of dwell ingSize of

dwell ing m²

Number of unitsPercentage of

totalRepelita-II Repelita-III Repelita-IVRepelita-V(1989-90)

Total1974-1990

Core houses < 27 20,272 50,361 44,635 3,653 118,921 56.8Simple/modest houses > 27 30,398 28,002 19,626 4,038 82,064 39.2

Flats/apartments 18-54 - 2,960 5,320 - 8,280 4.0Total 50,670 81,323 69,581 7,691 209,265 100.0

Source: CBS, 1992a:6; Ministry of Housing, 1990:57.

Page 26

Table 19. REI housing production, by income group (to 1991)Type of housing by RepelitaII-IV

(actual)RepelitaIV(planned)Income group Floor area m²

High > 200 - -Middle 70-200 11,337 3,903

Moderate 36-70 92,957 21,498Low 12-36 358,178 134,777

Source: BKPN, 1991:22-23; Ministry of Housing, 1991:154.

Page 27

Table 20. BTN funding sources through saving in Repelita-V (1989-1994)Source of funds Percentage of total funds Rp. billions US$ mill ions

Tabanas 9.96 223.00 119.89T UM/Pradana 8.00 180.00 96.77

Deposit 4.56 102.65 55.19Mortgage bonds 11.12 250.00 134.41

Total 33.64 755.65 406.26Source: Amir Karamoy, Vice Director of REI, 1990.

Page 28

Table 21. Inflation and exchange rates (1976-1992)

Date of decisionInterest rate by size of unit, m²

< 21 27-36 45 70+1976 5 5 5

1979 April 5 9 91986 April 9 12 151987 Sept. 9 12 151989 April 12 16 181990 April 12 16 17.51990 Sept. 12 16 17.5 18.51990 Oct. 12 19 19-21 22

1991 March 12 21-23 24-26 27-281992 July 12/10a market market market

a: "Simple houses" and RSS respectively.Source: BTN, 1992c.

Page 29

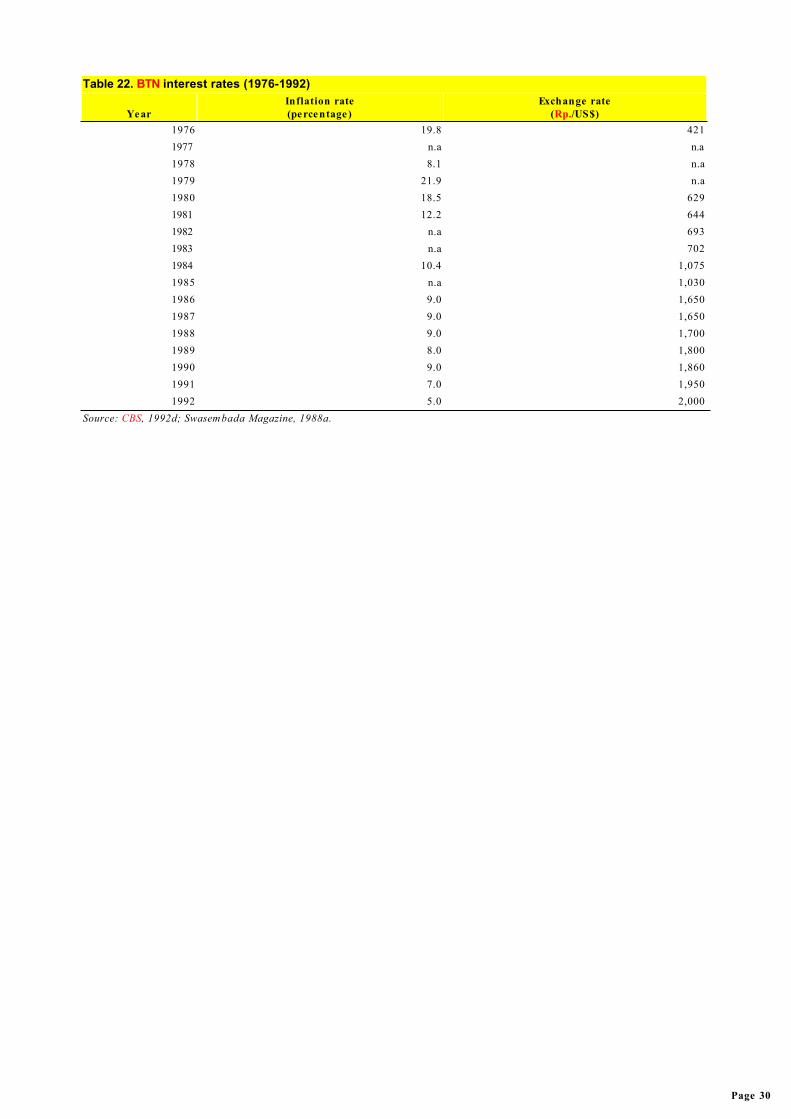

Table 22. BTN interest rates (1976-1992)

YearInflation rate(percentage)

Exchange rate(Rp./US$)

1976 19.8 4211977 n.a n.a1978 8.1 n.a1979 21.9 n.a1980 18.5 6291981 12.2 6441982 n.a 6931983 n.a 7021984 10.4 1,0751985 n.a 1,0301986 9.0 1,6501987 9.0 1,6501988 9.0 1,7001989 8.0 1,8001990 9.0 1,8601991 7.0 1,9501992 5.0 2,000

Source: CBS, 1992d; Swasembada Magazine, 1988a.

Page 30

Table 23. Ownership credit/loan systems of BTN (1992)

PackageIncomegroup

Monthly income (Rp.'000)

House size(m²)

Repaymentperiod(years)

Interest(percentage per

annum)Very simple house ownership credit (KPRSS) lowest < 150 21 10

lower-low < 200 36 10House-ownership credit (

KPR-Griya) (for modest-qualityhouses)

corelower-low < 450 1 12upper-low < 750 21 15

mediumupper-low < 750 27 21moderate < 1,250 36 21

large middle > 1,250

45 & 70 23< 5 23

5-10 23.510-20 24

Serviced-plots ownership credit (KP-KSB)(self-help construction) lowest 150 12

House-shop ownership credit (KP-Ruko) (for individual use)

small < 5 23medium 5-10 23.5

10-20 24Improvement credit (KUPARA) (for existing

houses)< 5 23

5-10 23.5Housing development credit (KSG) (for people

with a plot of land)< 5 23

5-10 23.510-20 24

Rental house credit (KGS) (building of flats orhouses to be rented)

< 5 235-10 23.5

10-20 24Construction credit (KYG) (for developers) 25Company housing (KPP) (for companies to

build houses for they employees) credit interest +1Emergency credit (K. Swadana) (for

emergencies regardless of deposit status) deposit interest +2Source: Based on BTN, 1992d:1-3.

Page 31

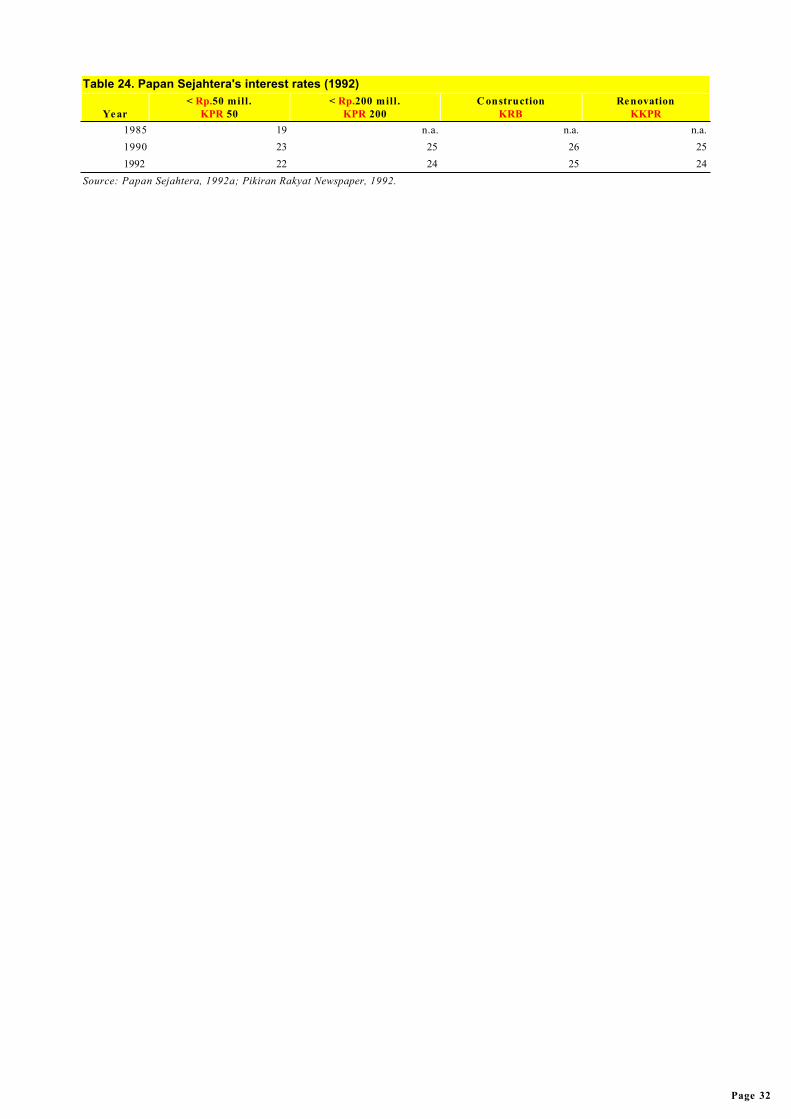

Table 24. Papan Sejahtera's interest rates (1992)

Year< Rp.50 mill.

KPR 50< Rp.200 mill.

KPR 200Construction

KRBRenovation

KKPR1985 19 n.a. n.a. n.a.1990 23 25 26 251992 22 24 25 24

Source: Papan Sejahtera, 1992a; Pikiran Rakyat Newspaper, 1992.

Page 32

Table 25. Average house prices (1992)

House type Unit size (m²) Plot size (m²) Eligible income groupsPrice (Rp. mill ion)

Perum-Perumnas Private deve lopersVery simple 21 54 lower-low 3.5 -Core house 15 60 lower-low 5-6 -

Simple 21 72 lower-low 6-7 8-10 27 90 upper-low 7-9 10-15

Medium 36 100 upper-low 9-12 15-20 45 120 moderate 12-15 20-40 54 150 middle 15-20 40-50 60 160 middle 20-25 50-60

Large 70 200 middle 25-30 60-80 90 250 high - 80-100 110 300 high - > 100

Source: Herlianto, 1993.

Page 33

Table 26. Population of Jakarta (l990)

RegionArea(km²) Population

Population density(persons/km²)

Number ofhouseholds

Household size(persons)

South 145.4 1,905,004 13,102 392,474 4.85East 187.7 2,064,495 10,999 444,975 4.64

Central 47.9 1,074,752 22,437 224,594 4.79West 126.1 1,815,316 14,396 383,880 4.73

North 154.1 1,362,948 8,845 294,293 4.63Total 661.2 8,222,515 12,434 1,740,216 4.72

Source: DKI (1991a, 1991b).

Page 34

Table 27. Housing ownership, Jakarta (1990)O wnership Number Percentage

Privately owned 1,052,399 79.8Rented 94,202 7.1

Contracted/leased 152,180 11.5Boarding house 19,847 1.5

Total 1,318,628 99.9Source: DKI, 1991a.

Page 35

Table 28. Housing needs, Jakarta (l990)

RegionHousing stock

(units)Households

per unitHousing need

(units)Housing shortage

(units)South 346,449 1.13 372,061 25,612

East 339,347 1.13 370,812 31,465Central 163,318 1.38 187,161 23,843

West 291,483 1.32 319,900 28,417North 223,031 1.32 245,244 22,213Total 1,318,628 1.32 1,450,178 131,550

Source: DKI, 1991a; 1991b.

Page 36

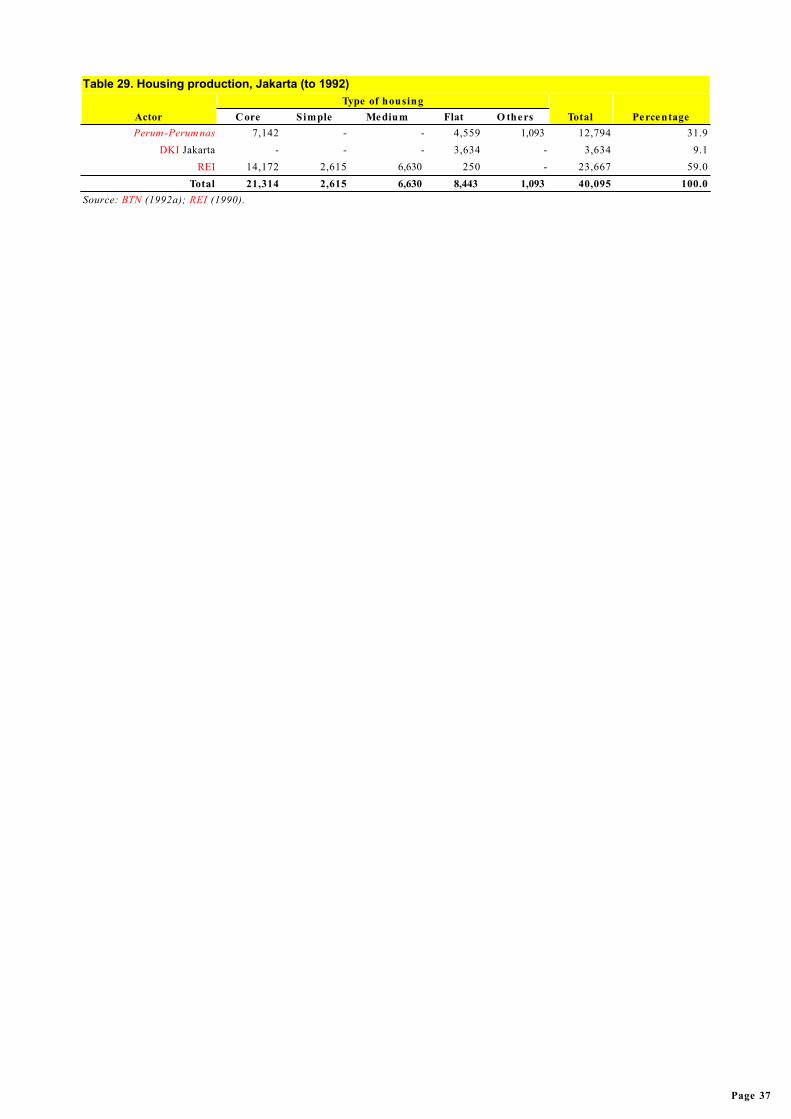

Table 29. Housing production, Jakarta (to 1992)

ActorType of housing

Total PercentageCore Simple Medium Flat O thersPerum-Perumnas 7,142 - - 4,559 1,093 12,794 31.9

DKI Jakarta - - - 3,634 - 3,634 9.1REI 14,172 2,615 6,630 250 - 23,667 59.0

Total 21,314 2,615 6,630 8,443 1,093 40,095 100.0Source: BTN (1992a); REI (1990).

Page 37

Table 30. Housing production, Botabek (to 1992)Region Perum-Perumnas REI Total

Bogor 22,500 8,726 31,226T angerang 16,685 13,213 29,898

Bekasi 17,044 16,635 33,679Total 56,229 38,574 94,803

Source: BTN, 1992a; REI, 1990.

Page 38

Table 31. Expected housing demand, Jakarta (1990-199S)

Type ofunits

Sizem²

Targetincome

group (Rp.'000)

Housing deve lopments (thousand units)

PD-SJ Perum-Perumnas REIHouseholds/communitie s Total

Core 18 < 100 8 5 2 5 20Small 21 100-150 12 10 8 10 40

36 150-200 10 10 9 16 45Medium 45 200-250 8 9 10.5 32.5 60

54 250-300 3 3 8 28 42 70 300-500 3.5 2.5 6 33 45

Large >70 > 500 2 1 4.5 27.5 35Total Number 46.5 40.5 48 152 287

Total Percentage 16.2 14.1 16.7 53.0 100.0Source: DKI (1991a).

Page 39

Table 32. Perum-Perumnas housing production, Jakarta (to 1992)

LocationSub-core

15m²Core21m²

Flat housing (unit size )

Duplex

Maisonette70m² Total18m² 21m² 36m² 54m² 45m² 54m²

Klender 190 6,952 - - 1,216 64 524 202 367 9,515Kebon Kacang - - - 240 230 66 - - - 536T anah Abang - - - - 1,271 - - - - 1,271

Kemayoran - - 704 480 288 - - - - 1,472

Total 190 6,952 704 720 3,005 130 524 202 36712,79

4Source: Perum-Perumnas and DKI, 1991a.

Page 40

Table 33. Rental flats owned by DKI Jakarta (1990)Location Agency Stories Type (m²) Units

Pondok Kelapa PD-SJ 2 14 & 16 140Cipinang Besar PD-SJ 2 14 & 16 144Pondok Bambu PD-SJ 2 14, 16 & 28 132

Cengkareng PD-SJ 2 14 & 16 114Karang Anyar PD-SJ 4 18 & 27 350

Jati Rawasari PD-SJ n.a. n.a. 146Pondok Sarana Karya PD-SJ 4 14 & 16 152

T ambora PD-SJ 4 18 463Penjaringan PD-SJ 4 18, 36 & 54 933

Bermis-Industri PD-SJ 4 48 64Penjaringan BPL Pluit 4 36 400

Pulo Mas YPM 4 45 & 54 596Total 3,634

Source: DKI, 1991a.

Page 41

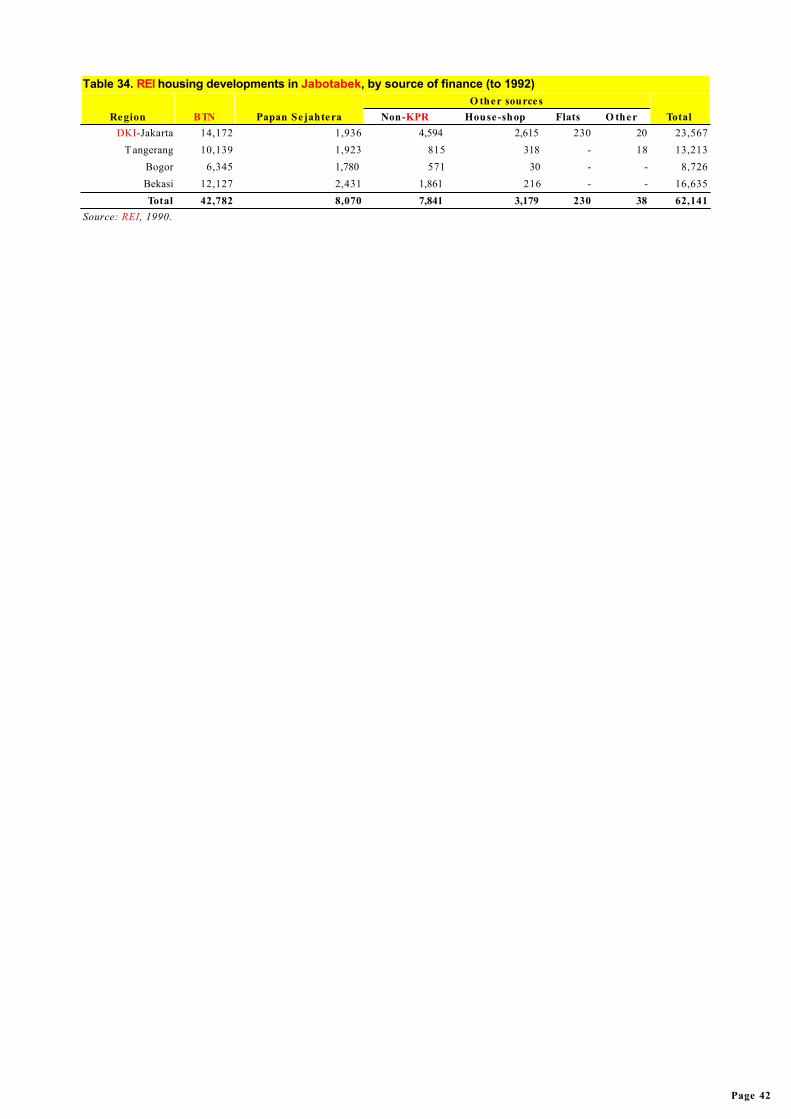

Table 34. REI housing developments in Jabotabek, by source of finance (to 1992)

Region BTN Papan SejahteraO ther sources

TotalNon-KPR House-shop Flats O therDKI-Jakarta 14,172 1,936 4,594 2,615 230 20 23,567

T angerang 10,139 1,923 815 318 - 18 13,213Bogor 6,345 1,780 571 30 - - 8,726Bekasi 12,127 2,431 1,861 216 - - 16,635Total 42,782 8,070 7,841 3,179 230 38 62,141

Source: REI, 1990.

Page 42

Table 35. Housing stock, Bandung(1992)Condition of units Number Percentage

Permanent 218,561 64.7Semi-permanent 82,596 24.4

T emporary 36,840 10.9Total 337,997 100.0

Source: Unknown, 1992a:16.

Page 43

Table 36. Perum-Perumnas housing production, Bandung (to 1992)

Location

Type of units

TotalRSS21m²

Core house21m²

Simple house27-70m²

Sukaluyu - - 150 150Sadang Serang - 504 360 864

Cijerah - - 460 460Sarijadi non-flat - 1,950 1,151 3,101

Sarijadi flat - - 864 864Kopo - - 354 354

Cibuntu - - 339 339Antapani - 4,949 754 5,703

Rancaekek 209 2,298 455 2,962Total 209 9,701 4,887 14,797

Source: Herlianto, 1993 (citing Perum-Perumnas, Bandung branch).

Page 44

National Trends in Housing-Production PracticesVolume 2: Indonesia

List of acronyms and special termsADB Asian Development BankArisan Collective lotteryBappeda Municipal Planning and Development Agency (Badan Perencanaan dan Pembangunan Daerah)Bappem Development Execution Board (Badan Pelaksana Pembangunan) Bappenas National Planning and Development Agency (Badan Perencanaan dan Pembangunan Nasional) BAWS Bandung Area Water SupplyBKPM Capital Investment Coordinating Body (Badan Koordinasi Penanaman Modal)BKPN National Housing Policy Board (Badan Kebijaksanaan Perumahan Nasional)Botabek Bogor-Tangerang-Bekasi regionBPD Local Development Bank (Bank Pembanguan Daerah)BPN National Land Agency (Badan Pertanahan Nasional)BTN State Saving Bank (Bank Tabungan Negara)BUDP Bandung Urban Development ProjectBUTP Bandung Urban Transportation ProjectCBLCH Community-based low-cost housing CBO Community-based organization CBS Central Bureau of Statistics Desa VillageDKI Capital Special Area, Municipality of Jakarta (Daerah Khusus Ibukota)ESCAP United Nations Economic and Social Commission for Asia and the PacificGBHN State National Development Goal (Garis Besar Haluan Negara) gotong royong Mutual self-helpGSS Global Strategy for Shelter to the Year 2000IBRD International Bank for Reconstruction and Development, the World BankINDAL Industri Dalam streetIYSH International Year of Shelter for the HomelessJabotabek Jakarta-Bogor-Tangerang-Bekasi urban agglomeration JPR Public Housing Agency (Jawatan Perumahan Rakyat) Kabupaten Rural municipalityKampung Village in urban area Kecamatan DistrictKelurahan Sub-district/villageK. Swadana Emergency credit (BTN)KGS Rental house credit (BTN)KIP Kampung Improvement ProgrammeKK Construction and improvement credit (Kredit Konstruksi)KKPR Credit for housing construction and improvement (Kredit Konstruksi dan Perbaikan Rumah)

(Papan Sejahtera)Kotamadya Urban municipality (city status)KP-Ruko House-shop ownership credit (BTN)KPKSB Empty/serviced plots ownership credit (Kredit Pemilikan Kapling Siap Bangun)KPP Company housing credit (BTN)KPR House ownership credit (Kredit Pemilikan Rumah) KPR-Griya House ownership credit (BTN)KPRSS Very simple house ownership credit (BTN)KRB New home construction credit (Kredit Rumah Baru) (Papan Sejahtera)KSG Housing development credit (BTN)KUD Rural unit cooperative (Koperasi Unit Desa)KUK Small economic activity credit (Kredit Usaha Kecil)KUPARA Improvement credit (BTN) KYG Construction credit (BTN)LPMB Regional Housing Centre (Lembaga Penyelidikan Masalah Bangunan)LPSM Institute of Community Self-help (Lembaga Pengembangan Swadaya Masyarakat)NGO Non-governmental organizationP2LDT Rural Housing Improvement Programme

Page 45

P2LPK Urban Housing Pioneering Project (Proyek Perintis Perbaikan Lingkungan Perumahan Kota)P3KT Integrated Urban Infrastructure Development Programme (Proyek Pembangunan Prasarana Kota

Terpadu)PD-SJ The housing company of DKI (Perusahaan Daerah Saran Jaya) Perum-Perumnas National Urban Housing Development Corporation (Perusahaan Umum Perumahan Nasional)PITB Building Information Centre (Pusat Informasi Tehnik Bangunan) PPLH Environmental Research Centre (Pusat Penelitian Lingkungan Hidup)REI Indonesian Association of Real Estate Developers (Real Estate Indonesia)Repelita Five Year Development PlanRp. RupiahsRSS Very simple house (Rumah Sangat Sederhana) SP3L Location Principle Approval Tabanas National SavingUNDP United Nations Development ProgrammeYKP Housing Bank Foundation (Yayasan Kas Pembangunan)YSS Sugyapranata Social Foundation

Page 46

National Trends in Housing-Production PracticesVolume 2: Indonesia

Bibliography

Bandung Municipality. 1991. Master Plan of Bandung, Bandung.

Bappenas. 1988. The State National Development Goal (GBHN), Jakarta.

Bappenas. 1989. Fifth Five Year National Development Plan (Repelita-V), Jakarta.

BKPN. n.d. Conference Materials for Fiscal Year: 1989-1992, Jakarta.

BKPN. 1991. National Housing Policy and Strategy, Jakarta.

BTN. 1990. Regulation of the House Ownership Credit.

BTN. 1991a. 1990 Annual Report, Jakarta.

BTN. 1991b. Brief Information on Home Ownership Loan.

BTN. 1992a. Realization of BTN Credit as of June 1992, Jakarta.

BTN. 1992b. Recapitulation of Housing Credit Debtor in Bandung, Bandung.

BTN. 1992c. Circulation of BTN Bureau of Credit, September 1, Jakarta.

BTN. 1992d. Housing Credit of the State Savings Bank (BTN), Jakarta.

CBS. 1989. Poverty. Income Distribution And Basic Needs, Jakarta.

CBS. 1989a. Housing Construction Statistics in Indonesia 1988, Jakarta.

CBS. 1990. Housing and Environmental Statistics 1989, Jakarta.

CBS. 1992a. Housing Construction Statistics in Indonesia 1991, Jakarta.

CBS. 1992b. People's Welfare Indicator 199/, Jakarta.

CBS. 1992c. Population of Indonesia, Results of the 1990 Population Census, Jakarta.

CBS. 1992d. Statistical Yearbook of Indonesia 1991, Jakarta.

Cipta. 1988. "Housing for The Poor, 1987." Cipta, No.69.

DHV Consultants and Associates. 1991. Jabotabek Metropolitan Development Plan - Review, June.

DKI Provincial Government. 1987. Jakarta 2005, Jakarta's City Master Plan of 1985-2005, Jakarta.

DKI Provincial Government. 1991a. Housing in Jakarta, Jakarta, Housing Office.

DKI Provincial Government. 1991b. Jakarta in Figures, Jakarta.

Government of Indonesia. 1991. Declaration On The Establishment of National Secretariat of Planning and Housing.

Hendropranoto Suselo. 1986. "Some problems on low-cost housing", paper prepared by the Director of Programmingof the Directorate General of Human Settlements, Ministry of Public Works, Jakarta.

Herlianto. 1982. "Integrated Kampung Improvement Programme in Indonesia", paper presented to the InternationalCongress of the Association of Sociologists at Mexico City, August 1982. (This paper is published as a chapterin the book Housing Needs and Policy Approaches(pp.236-248), Durham, N.C., Duke University Press, 1985).

Page 47

Herlianto. 1984. "Rural Development in Indonesia" , paper presented at the Seminar on Rural Development in Asia andPacific (NHA-UNESCO-AIT), Khon Kaen, Thailand.

Herlianto. 1986a. "Kampung Improvement as a Means To Urban Development", paper presented at the WorldCongress of Housing and Planning, Adelaide, October 1986, published in a book by EAROPH (1988).

Herlianto. 1986b. Urbanization and Urban Development, Bandung, Alumni Press.

Herlianto. 1987. "Kampung Improvement Project", paper presented at the National KIP- Course, Directorate ofHousing, Ministry of Public Works, Jakarta.

Herlianto. 1990a. "Experience with the project approach to shelter delivery for the poor in Indonesia", case studyprepared for UNCHS, Nairobi.

Herlianto. 1990b. "The emerging role of non-governmental organizations " , paper presented at the InternationalCongress of the Association of the Major Metropolises, Melbourne, October.

Herlianto. 1993. "National trends in housing production practices in Indonesia". Case study prepared for UNCHS(Habitat), Nairobi.

Jakarta Capital City Government. 1976. Jakarta's Kampung Improvement Programme , in the Context of City SettlementProblem, Jakarta.

Llewelyn-Davies, Kinhill, Sycip, Gorres, Velayo & Co. 1979. Bandung Urban Development and Sanitation Project, Finalreport.

LP3ES. 1982. Studies on the impact of Kampung Improvement on Low Income People in Jakarta, Jakarta.

Ministry of Cooperatives. n.d. Ideas Regarding Housing Provision by Cooperatives, Jakarta.

Ministry of Housing. 1989. Decree on Housing Development Task Force, Jakarta, Office of the State Minister. Ministryof Housing. 1990. Housing Development 1990, Jakarta, Office of the State Minister .

Ministry of Housing. 1991. Housing for All People, book prepared by staff of the State Minister of Housing, Jakarta.

Ministry of Housing. 1992. Reports ~n Housing for Cabinet Meetings, Jakarta, Office of the State Minister .

Ministry of Housing. n.d. "Information Book" Jakarta, Office of the State Minister of Housing.

Ministry of Public Works. 1982. Kampung Improvement Programme (KIP), Jakarta, Directorate General of HumanSettlements.

Ministry of Public Works. 1984. Development Programme of the Directorate General of Human Settlements in Repelita-IV, Jakarta.

Ministry of Public Works. 1985. Definition of Low Cost Housing , Jakarta.

Ministry of Public Works. 1986. Second Bandung Urban Development Project, Feasibility Study, Jakarta

Ministry of Public Works. 1989. Development Programme of The Directorate General of Human Settlements in Repelita-V, Jakarta.

Ministry of Public Works. Annual Reports of the Directorate General of Human Settlements, Jakarta.

P.T. Margahayu Raya. 1990. Margahayu Raya Housing Development Report, Bandung.

P.T .Papan Sejahtera. 1992a. Leaflets.

P.T. Papan Sejahtera. 1992b. Prospectus, June 6.

Perum-Perumnas. 1985. Klender Flat Housing Project, Jakarta.

Page 48

Perum-Perumnas. 1985. Klender Site and Services Project.

Perum-Perumnas. 1987. Environmental Impact Study of the Klender Housing Project, Jakarta, Perum-PerumnasEvaluation Team.

Perum-Perumnas. 1989a. Annual Report 1987-1989, Jakarta.

Perum-Perumnas. 1989b. Corporate Plan 1989-1994, Jakarta.

Perum-Perumnas. 1989c. Kemayoran Ex-Airport Flat Housing.

Perum-Perumnas. 1989d. National Urban Housing Development Program in Pelita-V, Jakarta.

Perum-Perumnas. 1992. Perum-Perumnas,17 years.

Perum-Perumnas. n.d. Brochure of Bandar Kemayoran, Jakarta.

Pikiran Rakyat. 1987. Housing and Its Problem, supplemental publication to welcome the International Year of Shelter,Bandung, August.

Pikiran Rakyat. 1988. Housing and Its Problem, supplemental publication to welcome the opening of Papan SejahteraOffice in Bandung, Bandung, September .

Pikiran Rakyat. 1992. "Papan Sejahtera decreased its interests " , Bandung, 31 October.

Prisma. 1986a. "Housing for people: not a dream?", Prisma, No.5, May.

Prisma. 1986b. "Towards the take off of national development", Prisma, VI 6th edition.

Prisma. 1988. Non-governmental organization, Prisma, No.4.

Prospek. 1991. "Ten most expensive cities", April 13.PTL. 1991. "Community based low cost housing", unpublishedinception report of Project INS/89/006.

REI. 1989. Decree of the National Congress of the Association of Real Estate in Indonesia, Jakarta.

REI. 1990. Statistics on 1990 Housing Development by Real Estate Indonesia.

Sardjono. 1986. "Towards the take off of national housing development", Prisma 5, May.

Struyk, Raymond J., and others 1990. The Market for Shelter in Indonesia Cities, Jakarta, Hasfarm Dian Consultant, andWashington, D.C., The Urban Institute.

Sugyapranata Social Foundation. 1986. Schedule of Profile Data, Semarang.

Swasembada. 1988a. "Years without devaluation?" Swasembada, No.3/IV , June.

Swasembada. 1988b. "Uncovering the real estate business", Swasembada No.3/IV , June.

University of Indonesia. 1990a. Executive Summary of Klender Evaluation Study , Jakarta, Faculty of Economics.

University of Indonesia. 1990b. Report on the Aspiration of Flat Housing Dwellers at Klender Housing Project, Jakarta,Faculty of Economics.

University of Indonesia. 1991. Projection of Indonesian Population: 1990-2020, Jakarta, Demographic Institute, Facultyof Economics.

Unknown. 1992a. "Infrastructure development planning of Bandung City", paper presented at the Public WorksTraining, Bandung, 2 October .

Unknown. 1992b. "Urban infrastructure development plan for Bandung City", paper presented by the head of the

Page 49

Planning Board at the Housing Seminar in Bandung, 3 October 1992.

Ustianto, M. 1990. The Social Problem Gap in Jakarta Qty and Social and Humanitarian Services, Jakarta.

Warta Perumnas. 1983a. "The impact of high rise housing", Warta Perumnas 6 April.

Warta Perumnas. 1983b. "Urban Renewal Project", Warta Perumnas No.3, Jakarta.

Warta Perumnas. 1989. "Market orientation of Perum-Perumnas in Pelita-V", Warta Perumnas No.2, July-August.Yanuati, Nunun. 1990. Housing Case Study: West Margahayu Raya Project, Bandung.

Yanuati, Nunum. 1990. Housing Case Study: West Margahayu Raya Project, Bandung.

Page 50

National Trends in Housing-Production PracticesVolume 2: Indonesia

Notes

1. The Regional Housing Centre, UN-RHC/LPMB, has since been renamed the Institute of Human Settlements(Puslitbang Pemukiman).

2. About 200 YKPs have so far been established, and they were responsible for the construction of a total of13,138 housing units during the 1951-1981 period. For various reasons, in particular financial ones but also dueto the expansion of Perum-Perumnas, only two YKPs operate successfully today, i.e., in the cities of Surabaya(in east Java) and Klaten (in central Java).

3. Administratively Indonesia is subdivided into 27 provinces. These are subdivided into 241 rural municipalities(kubupaten) and 55 urban municipalities (kotamadya). The 296 municipalities are subdivided in a total of 3601districts (kecamatan), which in turn are subdivided into 66,979 villages in rural areas (kelurahan).

4. Approximately 60 per cent of the total urban population live in kampung areas.

5. The National Land Agency (BPN) was established in 1990 to pursue these objectives.

6. This compares well with the size of Bandung city before the extension in 1987 (when its area was doubled from8000 to 17,000 hectares).

7. This equals approximately $US 263 million (based on current exchange rates, see table 22).

8. See section II.B.2.a for more details on the various credit schemes offered by BTN .

9. This may seem overtly optimistic if compared with past experience.

10. For details on the CBLCH scheme, see section II.A.3.b.

11. Average household size fell from 5.36 in 1976 (Llewelyn-Davies and others, 1979).

12. So far, the Housing Section of the Municipality has registered 74 housing project locations in Bandung city.Only seven of these were Perum-Perumnas projects.

13. The Antapani development was discussed in section IV.B.I.a above.

14. The minimum monthly income required to qualify was adjusted upward in 1990 - to about Rp.300,000 - implyingthat parts of the lower-low-income group could qualify. Yet, the additional requirement of minimum monthlyinstalments of Rp.100,000 implies that, in practice, only upper-low- and moderate-income groups would qualify.

15. For a brief discussion of the arisan system, see section II.A.3.b.

Page 51

ABOUTNational Trends in Housing-Production

PracticesVolume 4: Indonesia

HS/311/93 EISBNE 92-1-131502-6 (electronic version)

Text source: UNCHS (Habitat) printed publication: ISBN 92-1-131236-1 (published in 1993).This electronic publication was designed/created by Inge Jensen.

This version was compiled on 2 January 2006.Copyright© 2001 UNCHS (Habitat); 2002-2006 UN-HABITAT.

All rights reserved. This electronic publication has been scanned from the original text, without formal editing by the United Nations.The designations employed and the presentation of the material in this publication do not imply the expression of anyopinion whatsoever on the part of the United Nations Secretariat concerning the legal status of any country, territory,city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries.Reference to names of firms and commercial products and processes does not imply their endorsement by the UnitedNations, and a failure to mention a particular firm, commercial product or process is not a sign of disapproval.Excerpts from the text may be reproduced without authorisation, on condition that the source is indicated.

UN-HABITAT publications can be obtained from UN-HABITAT's Regional Offices or directly from:

UN-HABITAT,Information Services Section,

G.P.O. Box 30030,Nairobi 00100, KENYA

Fax: (254) 20-7623477 or (7624266/7)E-mail: [email protected]

Web-site: http://www.unhabitat.org/

Page 52

National Trends in Housing-Production PracticesVolume 2: Indonesia

Foreword

In most developing countries today, the provision of shelter is grossly inadequate. This is so despite severaldecades of direct government intervention in the shelter sector. The adoption by the United Nations GeneralAssembly of the Global Strategy for Shelter to the Year 2000 (GSS) in 1988 implied a global recognition of the severityof the housing problem. Since the public sector has shown itself unable to meet the increasing housing demand, theGSS calls for the adoption of new roles and responsibilities of the various actors in the shelter-deli very process. Itdoes not, however, propose that governments should withdraw from housing. On the contrary, the GSS placessignificant responsibilities on the public-sector agencies for creating an enabling environment and ensuring theavailability of shelter for all. By emphasizing the need for flexibility and local initiative in designing the new housingpolicy, it recognizes that the response of government in various countries may differ, depending on their respectivehousing conditions and the state of administrative and regulative system.

That is the point of departure for this publication, which is a series of four volumes on national trends inhousing-production practices in India, Indonesia, Mexico and Nigeria, respectively. All four countries have recentlyadopted new national housing policies that incorporate the enabling approach advocated in the GSS. Thesepublications identify problems encountered and lessons learned during the process of initiating enabling shelterstrategies. Yet, because the experiences in different countries in many ways are unique, it is necessary to discuss theexperiences gathered against the background of a more comprehensive discussion of the shelter-delivery process inthe individual countries. None of the four publications in this series thus attempts to compare the experiences ofdifferent countries. That has been done - with a particular focus on the lowest income groups - in a separatepublication entitled National Experiences with Shelter Delivery for the Poorest Groups.

The four volumes take a close look at the implementation of the GSS at the national level. They also reviewlessons at the sub-national level, by presenting the experience of the cities of Bombay, Calcutta and Delhi in India;Jakarta and Bandung in Indonesia; Mexico City, Ciudad Obregon and Jalapa in Mexico; and Lagos in Nigeria. Aparticular emphasis of all four publications is the presentation of data documenting the performance of the sheltersector at large and of the various actors involved therein.

Each of the four volumes consists of four main parts. The first part takes a close look at the development ofnational shelter policies and strategies in the light of the introduction of enabling shelter strategies. It also describesthe scope and scale of the shelter problem in each of the four countries. The second part analyses the changing rolesand responsibilities of the various actors in the shelter-delivery process, including relevant financial institutions andinstruments. It also provides figures on actual housing production at the national level. The third part takes a closerlook at the above issues at the city level. The fourth and concluding part, is just that, a conclusion to the abovediscussion. The chapter highlights obstacles to an effective housing supply, as well as particular innovativeapproaches towards alleviating the housing problem in the country.

The main conclusion that can be drawn from these studies is that the shelter problem today in most developingcountries is worse than it was before massive public-sector interventions were initiated two to three decades ago. Theexample of Indonesia can serve as a good illustration of the rather limited success of two decades of direct shelterprovision by the public sector. Total public-sector housing supply during the entire 1974-1991 period is less than theannual housing need created by population growth alone. Furthermore, there are signs in all four countries thatpublic-sector involvement in housing is being reduced, i.e., while the volume of units produced is increasing,public-sector investments in housing are decreasing. This indicates a trend where the focus of formal-sector housingproduction is turning away from the production of ready-to-move-in units and towards the provision of a wide menuof actions that lead to the construction of a dwelling unit. This results in a situation in which more units (althoughqualitatively different) can be produced with the same amount of funds. Yet, if the total formal-sector investment isreduced, this may indicate the beginning of a trend where the importance of shelter is being reduced rather thanstrengthened.

However, the picture is not altogether bleak. The four publications also show examples of how the shelterproblems can be effectively addressed. We should, nevertheless, keep in mind that in any market, choice is a positivefunction of income. The consequence is that in a situation of housing shortage, the poor have no choice in housing atall. Any strategy to alleviate the shelter problem should keep this in mind. Unless housing supply is fully able to meetthe need, direct interventions are required if the needs of the poorest groups are to be addressed.

We gratefully acknowledge the contribution of Ir. Herlianto for the preparation of the case study on which thispublication is based.

Page 53

Dr. Wally N'DowAssistant-Secretary-General,

United Nations Centre for Human Settlements (Habitat)

Page 54

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter I. A changing shelter policy

The first major involvement of the Government of Indonesia in the housing - delivery process was theconvening of a Public Housing Congress in 1950. One major result of the Congress, besides receiving the support ofthe President, was that efforts were made to establish housing corporations in every province in Indonesia. A PublicHousing Agency (JPR) was founded two years later to initiate housing research, policy development and technicalguidance, and to develop a housing-finance system. A Regional Housing Centre (1) was established in 1955 inBandung, in cooperation With ESCAP, to do housing research. Furthermore, a Housing Board was founded by thethen Minister for Public Works and Energy, to develop a housing-finance system. The Housing Board encouraged theestablishment of Housing Bank Foundations (YKPs) (2) in every big city (kotamadya) in the country to build a nationalhousing mortgage loan system. (3)

In the State National Development Goal (GBHN) of 1960, housing was regarded as an important factor, and itwas developed as a part of the Community Welfare Programme under the Ministry of Social Affairs. In 1961, a HousingBank was developed to serve the public housing sector, and in 1963 a Presidential Decree established a HousingPlanning Board (Badan Perancang Perumahan) chaired by the Minister of Public Works. The first Housing PrincipalLaw (Undang-Undang Pokok Perumahan) was formulated in 1964. It states that

"... housing is one of the basic ingredients of people's welfare; (and, further more, that) every citizen has the right toreceive and to enjoy appropriate housing, in accordance with social, technical, security, healthy, and ethicalnorms. "

The treatment of housing issues in the first five-year development plan (Repelita-I: 1969-1974) wasconcentrated on research on housing technology, guidance, institution building and finance. In addition, some 2000prototype houses were built during this period, under special instruction of the Minister of Public Works, as apreparation for the formal housing programme which was to be initiated in Repelita-II. A National Housing Policy andDevelopment Financing Workshop convened in 1972, became a milestone for the extensive housing programmes in thefollowing years.

The first formal housing development started in Repelita-II (1974-1979). In the first year of Repelita-II, five newhousing bodies were established: the National Housing Policy Board (BKPN), the National Urban HousingDevelopment Corporation (Perum-Perumnas), the State Savings Bank (BTN), the Indonesian Association of RealEstate Developers (REI) and the Building Information Centre (PITB).

In Repelita-III (1979-1984), two important events should be noted. These were the establishment of a privatesector financial institution, P.T. Papan Sejahtera, to cater to the needs of the middle- and higher-income groups, andthe appointment of a Junior Minister for Housing, under the Minister of Public Works.

Repelita-IV (1984-1989) can be seen as the first official recognition of the private sector's role in housingproduction. This is the first development plan where the planned production of the private sector exceeds that ofPerum-Perumnas. The real production of the private sector had then exceeded that of Perum-Perumnas for severalyears (see tables 1 and 2 ). Another important occurrence during Repelita-IV (in 1984) was the transformation of theJunior Minister for Housing into an independent State Minister of Housing outside the structure of the Ministry ofPublic Works.

Despite these interventions in the housing market, the gap between housing supply and housing demand inIndonesia is still widening. The International Year of Shelter for the Homeless (IYSH), promoted by the United Nationsin 1987, and the adoption of the Global Strategy for Shelter to the Year 2000 (GSS) by the General Assembly of theUnited Nations in 1988 inspired Indonesian housing authorities to develop new insights into how to address thehousing problem. The promotion of the IYSH and the adoption of the GSS occurred during the Indonesian effort toformulate its fifth five-year development plan, known as Repelita-V (1989-1994). A new housing policy was developedand - in line with the recommendations of the GSS - a central theme of the new policy was the changed role of theGovernment, from being a "provider" to becoming an "enabler. "

This change of policy is discussed at length in section I.B . The remainder of this introductory chapter reviewsthe scope and scale of the shelter problem in Indonesia. Chapter II discusses the shelter-delivery process in Indonesiaat large, while chapters III and IV take a closer look at the shelter-delivery process in two of the three largest cities inIndonesia, Jakarta and Bandung. The last chapter summarizes the findings.

Page 55

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter I. A changing shelter policyA. Scope and scale of the shelter problem

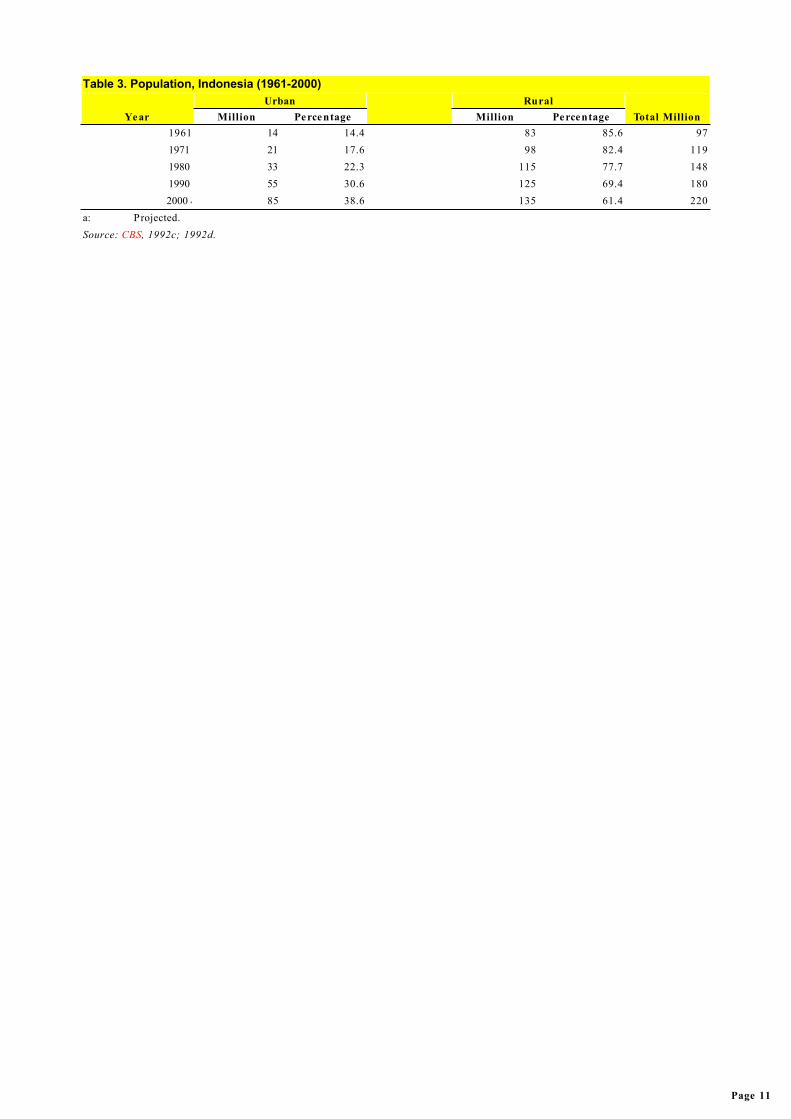

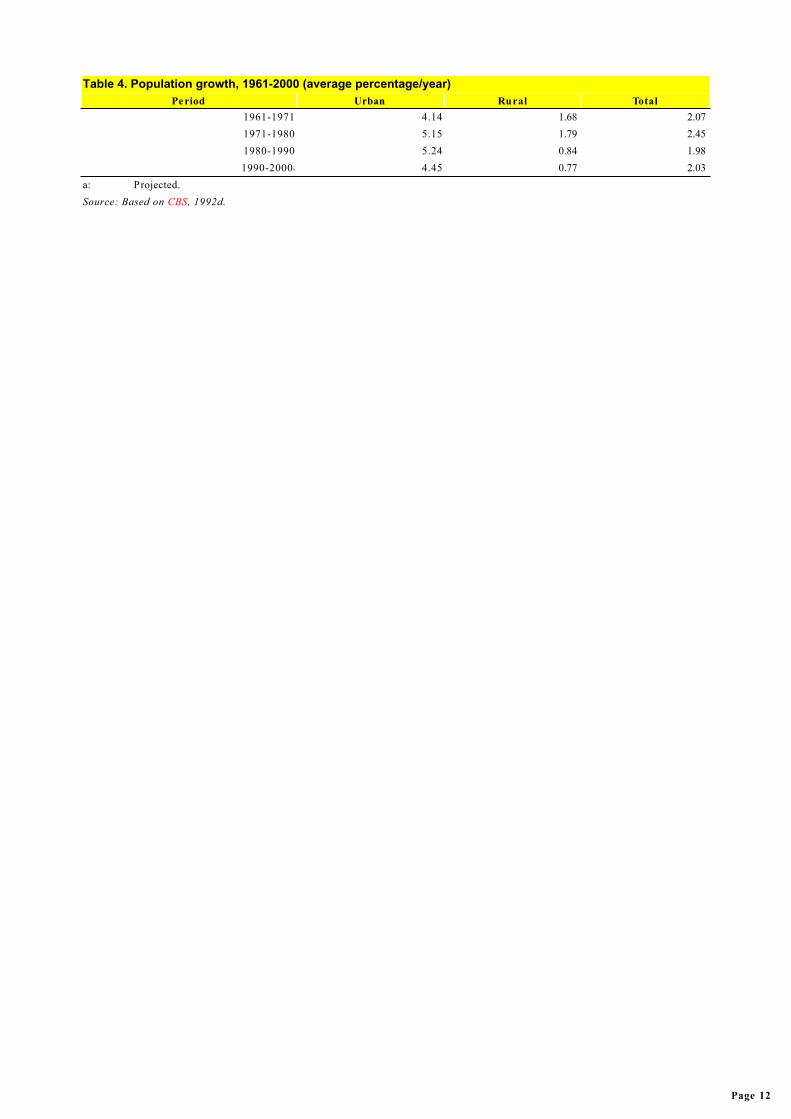

The root of the demand side of the housing problem in Indonesia is four-fold, and can be summarized as beingone of population size, population growth, spatial distribution of population and the rate of urbanization (see tables 3,4 and 5 for details):

Indonesia's population numbered 180 million in 1990, making Indonesia the fourth most populated country inthe world. The population in the year 2000 is estimated to 220 million.

The population increased by an annual rate of 1.98 per cent during the 1980-1990 period, down from 2.32 percent during the 1970-1980 period.

60 per cent of all Indonesians live on the island of Java (which makes up only 7 per cent of the total landarea). The population density on Java in 1990 was 814 persons per km2, while it was only 7 and 17,respectively, in Irian Jaya and Kalimantan, which between them account for 50 per cent of the total land area.The population in urban areas increased by about 6 per cent per year during the 1980-1990 period. In thesame period the annual population growth in rural areas was only 0.8 per cent. Since the national populationgrowth is about 2 per cent, and since fertility rates in rural areas are higher than those in urban areas, it cansafely be assumed that more than two thirds of the urban population growth is caused by people migratingfrom rural to urban areas. This translates into a population movement of 2-2.5 million people per year.

During the years from 1961 to 1990 the absolute population growth was nearly identical in urban and rural areas- from 14 to 55 million in rural areas (300 per cent increase) and from 83 to 125 million in rural areas (50 per centincrease). Yet, this implied that the relative size of the urban population increased from 15 per cent to 31 per cent. Infact, the absolute population growth in urban areas in 1990 was estimated to be more than three times that in the ruralareas (3.3 and 1 million each year, respectively). This contrasts sharply with the 1960s when the absolute populationgrowth in urban areas was only half of that in the rural areas. With current growth rates, nearly 40 per cent of allIndonesians will be living in urban areas by the year 2000.

The urban housing problem is further aggravated by the fact that the largest population increase occurs in thelargest cities, i.e., those with a population of more than 500,000. By 1990, the three most populous cities were thecapital Jakarta (with more than 8 million inhabitants), Surabaya (2.5 million) and Bandung (2 million). The housingsituation in Jakarta and Bandung is discussed in detail in chapters III and IV.

Page 56

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter I. A changing shelter policyA. Scope and scale of the shelter problem

1. Identifying the poor

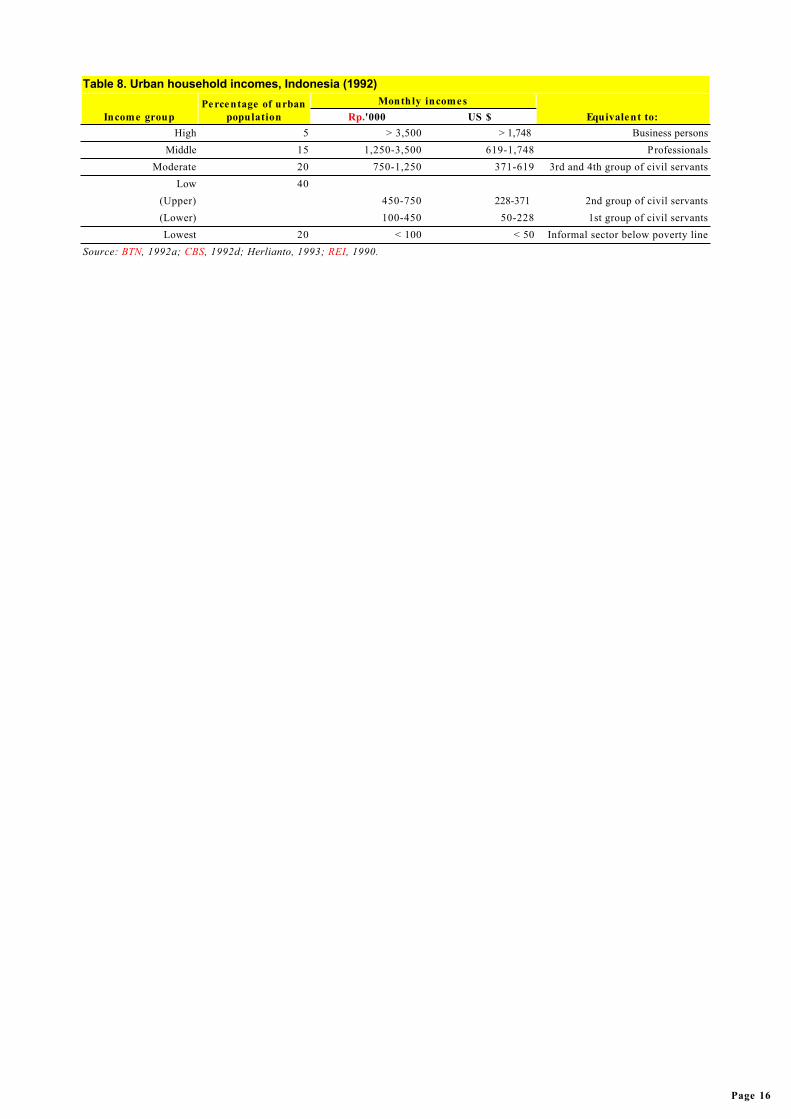

After the completion of Repelita-I, poverty was still rampant in Indonesia. By 1976, 40 per cent of all urbanhouseholds were classified as belonging to the lowest income group, defined as those with a monthly income of lessthan US$ 24, while a further 30 per cent of urban households were classified as low-income, i.e., with incomes in therange US$ 24-71 (see table 6 ). During the following 15 years, economic growth reduced the number of poorsignificantly. This general improvement can be exemplified by the fact that the percentage of the total population withincomes below the official poverty line was reduced from 40 to l5 in the period from 1976 to 1990 (see table 7 ). Sincethe average household consists of about five people, the household poverty line is about Rp. l00,000 in urban areasand Rp. 70,000 in rural areas.

A major reason for the considerable economic improvement since 1976 was the increased participation of theprivate sector. Yet, 60 per cent of all Indonesians were still classified as belonging to the lower low- or lowest-incomegroups in 1992, i.e., they were members of households that had monthly incomes of less than US$ 228 (see table 8 ).

Page 57

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter I. A changing shelter policyA. Scope and scale of the shelter problem

2. Housing stock

One of the main consequences of the low incomes is that a vast number of households are unable to securedecent housing. Housing conditions - in particular in rural areas and in kampungs (villages in urban areas) - do notcomply with acceptable technical or health standards.

The 1990 Census estimated that the total number of households in Indonesia was 39.7 million, of which 11.7million (29.5 per cent) lived in urban areas and 28.0 million (70.5 per cent) lived in rural areas (CBS, 1992c: 212). Yet,according to a national survey conducted in 1989, there were only 38.9 million housing units, of which 10.8 million (27.8per cent) were located in urban areas, and 28.1 million (72.2 per cent) were located in rural areas (see table 9 ). Themajority of houses in urban, as well as in rural areas, were owner-occupied, as is illustrated in table 10.

According to the same survey, the majority of households (21 million) lived in house units with floor areas inthe range 30-70 m2. Only about 15 per cent of the households lived in homes with floor areas of less than 30 m2, i.e.,those considered to be too small for the average household (see table 11 ).

Page 58

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter I. A changing shelter policyA. Scope and scale of the shelter problem

3. Housing need

Based on the above figures, the housing shortage in 1990, defined as the difference between the number ofhouseholds and the number of dwellings, is estimated at about 770,000 units. If this shortage is to be eliminated withinthe next 20 years, 38,500 units have to be constructed annually. Furthermore, in order to supply the new entrants in thehousing market with a place to live, an additional 700,000 houses have to be built every year (to cater for a 1.98 percent annual population growth). Finally, if the housing stock is to be kept at an acceptable standard - i.e., if anestimated 3 per cent of the housing stock is rehabilitated/upgraded or replaced each year - an additional 1,050,000 unitsshould be provided annually. The total annual housing need in Indonesia in 1990 is thus estimated to about 1.8 millionunits.

Page 59

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter I. A changing shelter policyA. Scope and scale of the shelter problem

4. Housing demand

An urban survey carried out by the Central Bureau of Statistic (CBS)revealed that about 45 per cent of therespondents were interested in obtaining Perum-Perumnas housing (CBS, 1990: 352-353). Yet, the economic situationof most of these respondents disqualified them from obtaining such housing. Table 12 provides details of housingpreferences according to expenditure class as revealed by the above mentioned survey. Sixty-one per cent of thehouse seekers are looking for a house of 36 m2 or smaller, only 7 per cent are looking for a house larger than 70 m2. Themost popular house types are the 36 m2 type (24 per cent), the 21 m2 type (17 per cent), and the 45 m2 type (16 per cent).

Yet, housing demand is not a function of income alone. People tend to choose housing units with access toproper infrastructure, and that are also near their place of work. Kampung rental houses are thus still the most popularhousing for the majority of the low- and lowest-incomes people. Furthermore, the majority of housing demand comesfrom the poorest groups. These groups cannot afford the houses supplied by the formal housing market. The newgovernment policy of building ..very simple houses" (RSS) and rental houses may alleviate some of the problems facedby the poorest groups.

Page 60

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter I. A changing shelter policyA. Scope and scale of the shelter problem

5. Housing supply

Table 13 provides an outline of formal-sector housing production in urban areas since 1974. If these figures arecompared with the housing need, outlined above, it becomes clear that the role of the formal sector in housing supplyis rather insignificant. During Repelita-IV the formal sector produced only 13 per cent of the number of dwelling unitsneeded annually. The table further shows that the importance of Perum-Perumnas is decreasing. WhilePerum-Perumnas were responsible for 92 per cent of formal-sector housing production during Repelita-II, this sharehad dropped to only 6 per cent during Repelita-IV.

In rural areas, the public sector has been responsible for all formal-sector housing, through the rural housingimprovement programme (P2LDT) and the transmigration programme (see table 14 ). The sheer volume of dwellingunits produced under the transmigration programme during Repelita-IV, more than eight times that of BTN and twicethat of all private developers, is a good indicator of what can be done in the field of shelter delivery, if sufficientpolitical importance is given to it.

BKPN has estimated that the formal sector supplies only 15 per cent of all urban housing units in Indonesia. Inrural areas the figure is estimated to be only 1 per cent. With current figures for urban/rural distribution of the housingstock, this would indicate that the formal sector has been responsible for 4.9 per cent of total housing production inIndonesia. Yet, this estimate may be a bit on the high side. If the total number of houses constructed by formal-sectoractors up to 1989 (see table 2 ) is compared with the housing stock in 1989 (see table 8 ), the formal sector's share oftotal housing production adds up to only 2.3 per cent of the total housing stock. Herlianto (1993) has thus estimatedthe formal sector's share of urban housing production to be 11 per cent.

Table 15 outlines the contribution of various actors to housing supply in Indonesia in the period 1974-1991.Section II.A discusses the actors in the housing production process in more detail.

Traditional urban housing schemes and empty plots have proved to be unaffordable for the lowest-incomegroup. To reach this group, who mostly live in kampung areas, (4) the Government has initiated the KampungImprovement Programme (KIP). This was initiated (with loans from IBRD) in Jakarta in 1969, and was later extended toinclude 10 other big cities. A government decision to use a national fund (APBN) for kampung improvement resultedin the covering of hundreds of towns during Repelita-III and more than thousands of medium and small towns duringRepelita-V. Although KIP was not aimed at eradicating the housing shortage, but rather at improving the condition ofinfrastructure - i.e., roads, drainage, sewerage, and the provision of potable water and public toilets - the programmehas proved that infrastructural improvement of kampung areas encourages the people living there to develop theirhouses.

For people resident in a kampung, an official improvement programme that has the support of the Governmentimplies that the status of the kampung is legalized and thus eligible for government subsidies. The subsidies are US$25 per capita for IBRD-funded KIP and about US$ 15 per capita for the government-funded improvement programme,Urban Housing Pioneering Project (P2LPK), which was started during Repelita-III.

The main housing problem in rural areas is one of quality rather than quantity, i.e., the quality of availableinfrastructure - such as the provision of water - as well poor building materials and construction technologies. Themain government activity in rural areas, besides the transmigration programme, has thus been P2LDT. Tables 16 and 17outline the volume of units improved under the urban and rural development programmes. A comparison of the effectsof various public-sector programmes in Indonesia reveals that the urban as well as the rural improvement programmesare the ones that most efficiently have addressed the needs of the poorest groups.

The most significant human settlements programme in Indonesia today is the huge Integrated UrbanInfrastructure Development Programme (P3KT) which is supported with loans from IBRD, the Asian DevelopmentBank (ADB), and the United Nations Development Programme (UNDP), as well as other funding agencies. Thefoundation of this programme was laid during Repelita-IV, and it was widely implemented during Repelita-V. Theprogramme attempts to integrate all urban development programmes. Its main objective is that local governments,rather than the Central Government - with or without foreign loans - shall be responsible for the development of urbaninfrastructure. Through this decentralization of the provision of infrastructure more people may get access to improvedinfrastructure, thus enabling them to improve their living environment.

Page 61

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter I. A changing shelter policyB. Reorganization of the housing sector

In its early years the objective of the national housing strategy was to address the shortage of housing and toprovide housing for low-income people. Yet, it soon became obvious that the Government was unable to meet theincreasing demand (let alone the target groups) through this strategy of public housing provision. The massivesubsidies that went into the essentially provider-based housing programmes of Repelita-II, Repelita-III and Repelita-IV far exceeded the capability of the BTN - which had been given the task of channelling subsidies to the housingsector - and thus the Government. During Repelita-IV and even more during Repelita-V, the emphasis wasincreasingly placed on private investments in the housing sector. The overall objectives of the housing sectorprogrammes, as stated in the latest GBHN - to be reached by the Year 2000 through the implementation of Repelita-VI(1994-1999) - can be summarized as follows (Bappenas, 1988):

The majority of the people in urban as well as rural areas shall be living in a healthy housing environment;

Housing and human settlement developments in urban areas shall keep pace with the urban populationincrease;

Housing and environment improvement support shall reach out to all rural villages;

Legal, institutional and financial systems - as well as the construction industry - shall be supportive of thehousing development programmes.

To realize these objectives the Government adopted an enabling shelter strategy, in line with therecommendations of the GSS. The philosophy of the new housing strategy in Repelita-V can be outlined as (Bappenas, 1989):

Housing provision is, in principle, the responsibility of people themselves. The role of the Government ismainly to create business and building opportunities and to push, mobilize and stimulate communityparticipation to enable the communities themselves to meet their housing needs.

The implementation of housing development is based on the principles of justice, equity, affordability,environmental awareness, and the ample consideration of the socio-cultural condition of the people.

Housing development is a multi-sectoral activity which should be supported by policies on spatial planning,land tenure, infrastructure, building technology, building-materials and construction industries, finance,institutional arrangements, human-resources development, legal regulations, and research and development.

Based on this broad philosophy a number of more specific interventions were identified:

Coordination of the activities of related agencies.

Involvement of all actors in the housing-delivery process, in the planning process as well as inimplementation.

Enhancing the role and capacity of local governments, cooperatives and non-governmental organizations(NGOs).

Support the participation of the private sector by enabling, mobilizing and developing its capabilities.

Establishment of coordinating agencies for rural housing development in central, provincial and municipalgovernments.

Develop communities' potential for mobilization of funds among themselves.

Control land price and land use (to attract investments in housing), introduce limitations on land ownership(to make more land available for public use), ensure the optimum use of empty lands (in particular toaccommodate large-scale housing development schemes on unused government land), support landacquisition for public use (to assist large-scale housing developments, rather than commercial andrecreational use), and simplify land registration and administration (to reduce building expenses). (5)

Page 62

Develop a simplified house design, simplify the housing construction process and the procedure to obtainbuilding permits.

Support research on appropriate technologies and local building materials (to reduce the price of buildingmaterials and to ease the pressure on distribution and marketing networks - as well as to reduce the importleakages from the housing sector).

Establish regional building information centres to guide and disseminate information on appropriateconstruction technologies and building materials.

Establish a Youth Education Agency, to increase the awareness of better and healthier housing among theyouth.

Since the adoption of the GSS by the General Assembly of the United Nations, the Government of Indonesiahas taken a number of steps to facilitate housing supply. The most important changes to the legal and regulatoryframework may be summarized as follows:

The State Minister of Housing's decree No.0l/KPTS/1989 of 2 January 1989 on home-ownership credit fromBTN, to support broader housing and settlement programmes.

The State Minister of Housing's decree No.04/KPTS/1989 of 19 January 1989 on the use of home-ownershipcredit for empty plots, to enable people to build their houses according to their own taste and affordability.

The State Minister of Housing's decree No.07/KPTS/1989 of 27 July 1989, on the reorganization of the StateMinistry of Housing, in anticipation of increased urban housing and settlement development.

The President's Instruction No.5/1990 on rehabilitation of slum areas on government land-

The Head of the National Land Agency's decree No.4/1991 on "Land Consolidation" in order to facilitate thetransfer of land from private ownership for the public good.

The State Minister of Housing's decree No.54/PRT/1991 on RSSs. The RSS is defined as being simpler andcheaper than the "simple house" as it is built with lower-quality materials. It is built as a ready-to-move-inunit, but requires the dweller to complete some final work. The units are intended to be within the reach ofthe lowest-income people.

The National Housing Policy and Strategy, which was released in 1991 by the Office of the State Minister ofHousing, is one of the most important efforts by the Government in support of the enabling approach. In its firstchapter it states that housing is an important part of the macro-economics of the country. Besides a higher housingproduction target, this Strategy supports housing schemes that include private and community participation throughthe provision of "empty plots," "rental housing" and through urban and rural improvement programmes.

The Government Law on Housing and Settlements, No.4/1992 of 10 March 1992, released by the Office of theState Minister of Housing, is the main document on housing development in Indonesia. It confirms the aboveministerial decrees and states that housing is one of the main national priorities.

Page 63

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter II. Housing supply at the national level

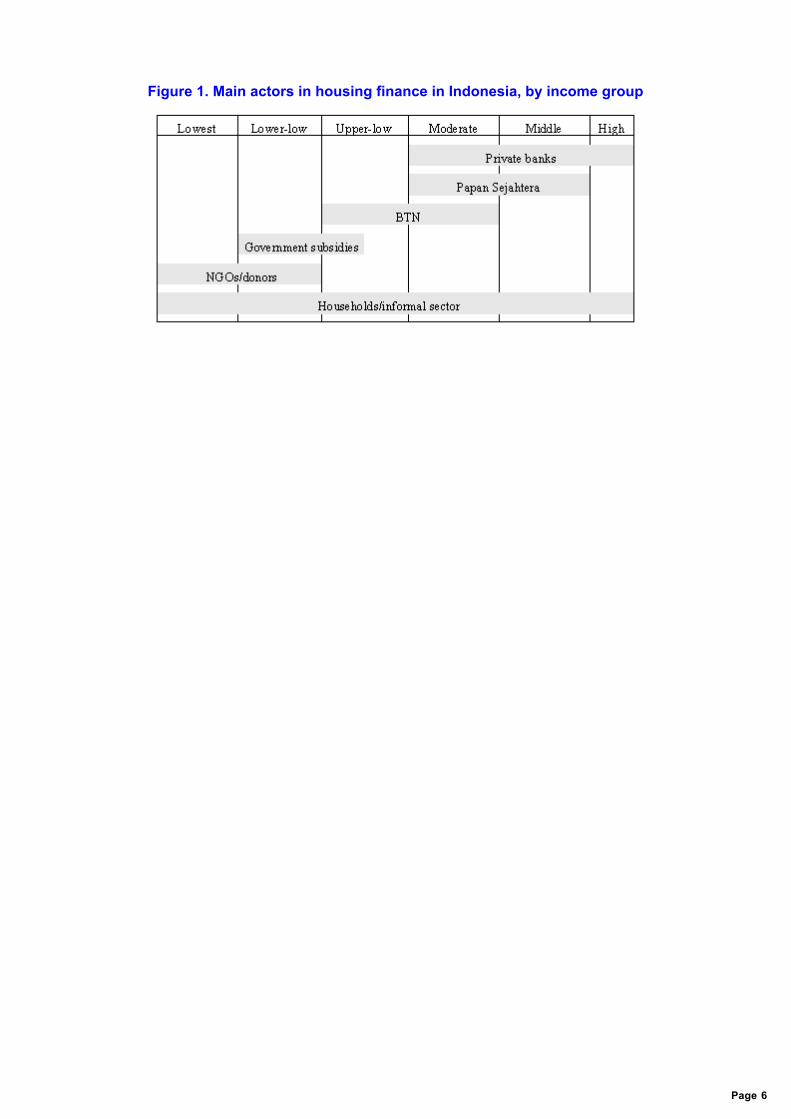

Following the recent changes in national shelter policies in Indonesia, the role of the public sector has beenredefined, from being the provider of housing for all (in theory, that is) to being a facilitator or enabler. As outlinedabove, Repelita-V clearly places the responsibility for housing provision on the people themselves. This chapter willtake a closer look at the actors operating in the shelter sector in Indonesia today. It will also briefly discuss thefinancial mechanisms operating in the housing sector in Indonesia. Figure 1 gives a brief overview of the main actorsfinancing housing.

Page 64

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter II. Housing supply at the national levelA. Actors in the shelter-delivery process

The most important actors in the shelter-delivery process in Indonesia are the households themselves. Morethan 90 per cent of all housing units constructed in Indonesia each year are built without support fromPerum-Perumnas, BIN, or from private banks. The vast majority of low- and lowest-income group households receivevery little assistance, if any, from formal-sector housing institutions. This section takes a closer look at the roles andresponsibilities of the various actors in the shelter-delivery process in Indonesia, in the public as well the privateformal and informal sectors.

Page 65

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter II. Housing supply at the national levelA. Actors in the shelter-delivery process1. Government and public-sector agencies

Following the past 20 years of government provision of housing in Indonesia, many different public bodies andagencies are currently in operation. Due to the recent policy changes, the roles and responsibilities of these agenciesare undergoing significant changes. The responsibility of the public-sector actors has primarily been to providehousing for households in the low-income category, and in particular to government employees or army staff who areunable to build houses on their own, due to their lack of savings. During Repelita-II, about 80 per cent of all unitsproduced by the public sector benefited households of the lower low-income group. This percentage, however, hassince declined, due to an increased demand for housing from the higher low- or moderate-income groups. Theincreased demand inflated the price of land, and in a situation with insufficient government subsidies, the lower low-and lowest-income groups found the publicly produced housing to be far too expensive.

Although in recent years some strategic plots (wide and near main streets) have been sold to individuals fromthe middle- or high-income groups as empty plots, most public-sector housing developments have targeted the low-and moderate-income groups. The middle- and high-income group have mainly been left to private-sector actors, whilethe lowest-income group is not reached at all through formal-sector housing supply. The only public sectordevelopments that can claim to have had a positive impact on the lowest-income group is the KIP and more recently,during Repelita-V, the building of RSSs and rental housing schemes.

The main government body in the human settlements sector is the State Ministry of Housing. The Ministry isresponsible for the coordination of housing development activities in Indonesia. The State Minister for Housing isalso the head of the BKPN, which was established to develop housing policies that enable the Government and theprivate sector to provide housing for low-income people. The main public-sector actors in the shelter-delivery process,however, are Perum-Perumnas and BTN. The following sections outlines the roles of each of these agencies in moredetail.

Page 66

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter II. Housing supply at the national levelA. Actors in the shelter-delivery process1. Government and public-sector agencies

a. Perum-Perumnas

Perum-Perumnas was established as the operational agency responsible for undertaking housingdevelopments for the low-income groups. Following the recent housing policy changes the role of Perum-Perumnashas declined. From bearing the main responsibility for formal-sector housing provision during Repelita-II, theimportance of the formal private sector has outgrown the public sector. Table 2 shows that Perum-Perumnas built lessthan 18,000 dwelling units during the first two years of Repelita-V, thirteen times less than the number of units built bythe formal private sector.

The total number of dwelling units built by Perum-Perumnas, up to the end of 1991, is 216,556. Among these,57 per cent were core houses (of less than 27 m2), 39 per cent "simple/modest houses" and 4 per cent apartments orflats (see table 18 ). Most flats (56 per cent) were of 36 m2, 33 per cent were smaller than 36 m2 (18 or 21 m2) while only IIper cent were larger (42, 51 or 54 m2).

Page 67

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter II. Housing supply at the national levelA. Actors in the shelter-delivery process1. Government and public-sector agencies

b. BTN

BTN was established to offer home-ownership loans to the low-income groups. Up to 1991, BTN had releasedsuch credits to 210,348 families through Perum-Perumnas and 515,618 families through other developers (CBS, 1992a).Following the recent housing policy changes, the role of BTN has changed dramatically. To alleviate the financialsqueeze on BTN, caused by a demand for loans that far exceeded BTN's financial resources, the Government decidedto diversify and privatize the housing finance system. The public and IBRD funds that had enabled BIN to offersubstantial subsidies on housing-loans dried up in the late 1980s. By July 1992 all housing subsidies had beenremoved, apart from those going to units of less than 21 m2 or to RSSs. These subsidies were, however, no longer themonopoly of BIN, but were channeled through a variety of private and regional development banks. Because of thisdevelopment, BIN was privatized in early 1991.

In 1990, BIN had a total of 6.5 million customers throughout the country, through its 25 branches and 17 cashoffices. It also deployed 30 mobile cash units, and posted assets totalling Rp. 2,935 billion (US$ 1,467 million) andprofits amounting to Rp. 24.6 billion (US$ 12.3 million).

Page 68

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter II. Housing supply at the national levelA. Actors in the shelter-delivery process1. Government and public-sector agencies

c. Other public-sector actors

Besides the actors outlined above with direct responsibilities for housing provision, several other agencies andministries are involved in the multi-sectoral process of human settlements development. The most significant of theseare briefly outlined below.

The Ministry of Finance is responsible for the mobilization of funds for housing development and to channelthese through various financial institutions. It also has a role to encourage popular participation in thefunding of housing, and to increase the role of local governments in housing development.

The State Bank (Bank Indonesia) plays an important role in providing liquidity credit for banks and otherfinancial institutions engaged in shelter development.

The Ministry of Cooperatives is responsible for encouraging people to develop community cooperatives,i.e., cooperatives for housing development, building materials and building components, water treatment,waste disposal and potable water.

The Ministry of Home Affairs is responsible for encouraging local governments to create the atmosphere foran integrated development that includes housing. One of the most important development programmesstarted under the auspices of this Ministry during Repelita-IV was the huge P3KT programme, in whichhousing is a main component. The P3KT programme is supported with loans from IBRD, ADB, UNDP andother funding agencies. The objective of the programme is to enable local governments to develop the urbaninfrastructure, with or without foreign loans.

The National Land Agency (BPN) was established in 1990 to pursue the objectives on land policies outlinedin section I.B . Its main objective is to regulate landownership and land prices to make land for housingaccessible for the majority. BPN is also given the responsibility of acquiring large areas of land for housingdevelopments.

The Ministry of Industry is responsible for guidance and support to the building-materials and constructionindustries, to encourage them to use locally-available materials, in line with the broader aim to widenemployment opportunities.

The National Planning and Development Agency (Bappenas) is responsible for setting national goals andhousing development policies and objectives. It also sets programme priorities for housing developments inthe framework of the general national development policy and priorities.

The Ministry of Social Affairs is responsible for encouraging community participation in housingdevelopment. One of the more visible activities of the Ministry was initiated during Repelita-II, i.e., theNational Social Solidarity Day (HKSN), which encouraged many parties to take part in the development andimprovement of urban slums. The Ministry is also responsible for the construction of houses forgeographically isolated populations.

The State Ministry of Population and Living Environment is responsible for directing housing andsettlement developments to balance physical developments with demographic, economic, social and culturalaspects of development.

The Ministry of Transmigration is responsible for developing new rural communities and attracting peoplefrom the more densely populated regions (especially the Java and Bali). This is primarily done by acquiringand allocating ready-to-move-in houses and productive lands for cultivation. The transmigration programmewas intensified during Repelita-IV, when nearly 600,000 transmigration dwellings were constructed (seetable 14 ).

The Ministry of Women's Affairs is responsible for enhancing the role of women in housing development, todevelop housing that encourages a healthy family development.

The Ministry of Health is responsible for providing guidance on the public and environmental health

Page 69

aspects of housing development programmes.

Page 70

National Trends in Housing-Production PracticesVolume 2: Indonesia

Chapter II. Housing supply at the national levelA. Actors in the shelter-delivery process

2. Actors in the private formal sector

Since Repelita-III, the Government has encouraged the private sector to take a more active part in housingdevelopments by offering the assistance of BTN and Papan Sejahtera. The importance of the private sector in shelterdelivery is best illustrated by the fact that the actual production of the formal private sector during Repelitas-II to IVwas more than three and a half times that of the public sector (see table 2 ).

The privatization of housing production has increased formal-sector housing production quite substantially.More people than ever before have thus gained access to formal-sector land and housing. Yet, one major problemarises out of these policies, the beneficiaries of these private formal-sector developments are mainly from theupper-low, moderate- and middle-income groups. The new land policies have led to substantial increases in the priceof land, and concentration of landownership, and have strengthened the lowest-income groups' dependence on theinformal housing sector. An increasing number of people build their homes individually or communally, withassistance from community-based organizations (CBOs), cooperatives and/ or NGOs. To alleviate some of the housingdeficit for the lowest-income groups, Repelita-V includes the planned development of 20,000 units of rental housing.

Page 71

National Trends in Housing-Production PracticesVolume 2: Indonesia