a scenario-based approach to asset allocation · 2019-02-21 · a scenario-based approach to asset...

TRANSCRIPT

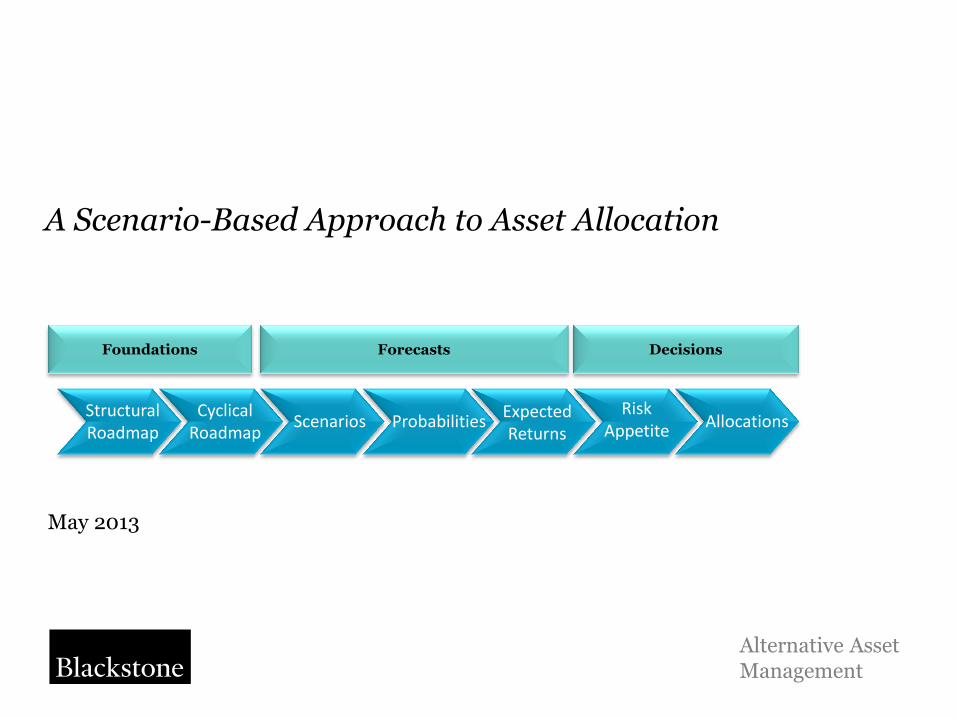

A Scenario-Based Approach to Asset Allocation

May 2013

Alternative Asset Management

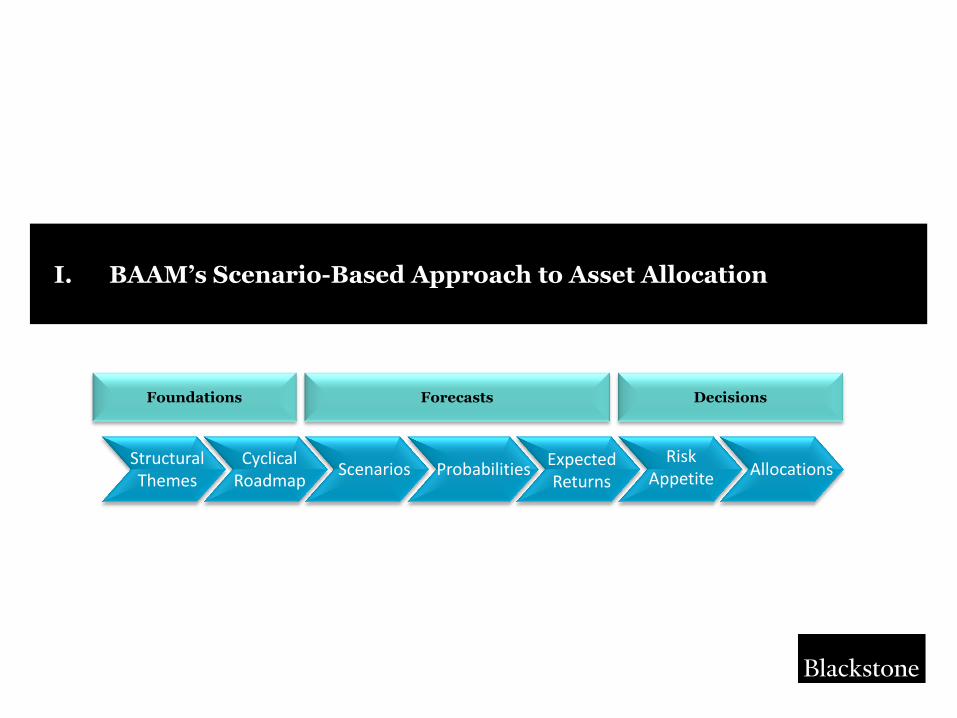

Allocations Risk

Appetite

Foundations Forecasts Decisions

Expected Returns

Probabilities Scenarios Cyclical

Roadmap Structural Roadmap

Confidential

Blackstone 1

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Disclosure

Important Disclosure Information:

The materials contained herein are for informational purposes only and do not constitute an offer to sell or a solicitation of an offer to purchase any interest in any investment vehicles (the “Blackstone Funds”) managed by Blackstone Alternative Asset Management L.P. or any of its investment advisory affiliates (together, “Blackstone”). Any such offer or solicitation shall be made only pursuant to the confidential private placement memorandum for a Blackstone Fund (“PPM”), which qualifies in its entirety the information set forth herein and contains a description of the risks of investing. These materials are also qualified by reference to the governing documents and the subscription agreement relating to the relevant Blackstone Fund (collectively, the “Agreements”). The PPM and Agreements relating to a Blackstone Fund should be reviewed carefully prior to an investment in that Fund. The Blackstone Funds are speculative and involve a high degree of risk.

In connection with your consideration of an investment in any Blackstone Funds, you should be aware of the following risks:

The Blackstone Funds may be leveraged and their portfolios may lack diversification, thereby increasing the risk of loss. The Blackstone Funds may invest in instruments that are highly illiquid and extremely difficult to value, which may limit an investor's ability to redeem or transfer its investment or delay receipt of redemption proceeds. The Blackstone Funds’ are speculative, involve a high degree of risk and their performance may be volatile. An investor may lose some or all of its investment. Blackstone has total investment authority over the Blackstone Funds, which could result in a lack of diversification and, consequently, higher risk. There is no secondary market for investors’ interests in the Blackstone Funds. There are restrictions on withdrawal and transfer of interests in the Blackstone Funds. The Blackstone Funds’ fees and expenses, and those of underlying portfolio funds, are substantial and will negatively impact performance.

Investments in the Blackstone Funds are not subject to the same regulatory requirements or governmental oversight as mutual funds. Blackstone Funds and their underlying managers may purchase instruments that are traded on exchanges located outside the United States that are “principal markets” and are subject to the risk that the counterparty will not perform with respect to contracts. Furthermore, since there is generally less government supervision and regulation of foreign exchanges, Blackstone Funds and their underlying managers are also subject to the risk of the failure of the exchanges and there may be a higher risk of financial irregularities and/or lack of appropriate risk monitoring and controls.

Investment managers and general partners of Blackstone Funds are not required to provide their Investors with periodic pricing or valuation information and any information provided is generally unaudited. Investors in Blackstone Funds generally will have limited rights with respect to their investment interest, including limited voting rights and limited participation in the management of the Funds. Blackstone Funds may involve complex tax and legal structures.

Investment in any of the Blackstone Funds is only suitable for sophisticated investors for which such an investment does not constitute a complete investment program and which fully understand and are willing to assume the risks involved in such Funds. We strongly encourage Investors to obtain independent advice from their own tax, accounting and legal advisers regarding any investment in any Blackstone Fund. Investors are also urged to take appropriate advice regarding any applicable legal requirements and any applicable taxation and exchange control regulations in the country of their citizenship, residence or domicile which may be relevant to the subscription, purchase, holding, exchange, redemption or disposal of any Blackstone Funds.

This communication is exempt from the restriction on the promotion of unregulated schemes (in section 238 of the Financial Services and Markets Act 2000 and the UK Financial Conduct Authority's Conduct of Business Sourcebook 4.12) on the grounds that the communication is only made to or directed at either (1) persons having professional experience of participating in unregulated schemes and the units to which the communication relates are available only to such persons; persons who do not have professional experience in participating in unregulated schemes should not rely on it, or (2) eligible counterparties and/or professional clients as those terms are defined in the rules of the UK Financial Conduct Authority. The units to which the communication relates are available only to such persons. Any person who is not an investment professional, an eligible counterparty or a professional client must not act or rely upon the contents of this communication. Blackstone is registered as an investment adviser with the SEC. This material has been approved for distribution by The Blackstone Group International Partners LLP which is authorised and regulated by the UK Financial Conduct Authority. The Blackstone Group International Partners LLP performs marketing and investor services activities outside the United States for Blackstone, which is located in the United States.

This document contains highly confidential information regarding Blackstone's investments, strategy and organization. Your acceptance of this document from Blackstone constitutes your agreement to (i) keep confidential all the information contained in this document, as well as any information derived by you from the information contained in this document (collectively, "Confidential Information") and not disclose any such Confidential Information to any other person, (ii) not use any of the Confidential Information for any purpose other than to consider investing in, or monitor investments in, Blackstone Funds, (iii) not use the Confidential Information for purposes of trading any security, including, without limitation, securities of Blackstone or its portfolio companies, (iv) not copy this document without the prior consent of Blackstone, and (v) promptly return this document and any copies hereof to Blackstone upon Blackstone's request. The use of the Confidential Information also is subject to the confidentiality provisions set forth in the Agreements and in any other written agreement between the recipient and Blackstone.

Confidential

Blackstone 2

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Additional Disclosure

The provision of this document to any person does not constitute, and may not be used for the purposes of, an offer of, or invitation to subscribe for, securities or financial products of any kind to that person. Any such offer or invitation will only be extended to a person in Australia under the terms of a separate document (such as a Confidential Memorandum), containing the full terms and conditions of any such offer or invitation. This document is not a disclosure document for the purposes of the Corporations Act 2001 (Cth) (“Act”) and has not been lodged with the Australian Securities and Investments Commission.

This document is provided only for the use of persons who are wholesale clients as defined in the Act (“wholesale client”). Any securities or financial products described in, or services that may be referred to or provided in connection with, this document are not made available to any person who is a retail client as defined in the Act. By accepting this document, you expressly acknowledge and represent that you are a wholesale client. This document is not intended to be distributed or passed on, directly or indirectly, to any class of persons in Australia other than wholesale clients.

The information in this document has been prepared without taking into account any recipient’s investment objectives, financial situation, taxation position or other particular needs or requirements and should not be relied on for the purposes of making any investment decision. If a recipient is considering making any decision in connection with the information in this document, that recipient should obtain their own independent advice.

To the extent that this document contains financial product advice, that advice is provided by The Blackstone Group (Australia) Pty Limited ACN 149 142 058 AFSL 408376 (“BGA”). BGA holds an Australian financial services licence authorising it to provide the financial services it provides in Australia. To the extent that advice is provided solely by Blackstone Alternative Asset Management LP (“BAAM”), BAAM is exempt from the requirement to hold an Australian financial services licence under the Corporations Act 2001 (Cth) in respect of the financial services it provides in Australia. BAAM is regulated by the Securities and Exchange Commission under the laws of the United States of America, which differ from Australian laws

Confidential

Blackstone 3

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Table of Contents

I. BAAM’s Scenario-Based Approach to Asset Allocation 4 Structural and Cyclical Themes 6 Scenario-Based Approach 7 Probability-Weighted Scenarios 9 Returns Matrix 11 Portfolio Construction 14 II. Insights from Our Views and Framework for Australian Portfolios 15

Portfolio Set 1: No Benchmark 17 Portfolio Set 2: Additional Shocks 19 Portfolio Set 3: Benchmark & Additional Shocks 23 Portfolio Set 4: Post-FX Returns 25

III. Appendix 1 28 Optimization Sensitivity 30 Correlations 31 Asset Class Returns 32

IV. Appendix 2 37 Top Down View Formation 38 Long-Term Scenarios 39

I. BAAM’s Scenario-Based Approach to Asset Allocation

Allocations Risk

Appetite

Foundations Forecasts Decisions

Expected Returns

Probabilities Scenarios Cyclical

Roadmap Structural Themes

Confidential

Blackstone 5

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

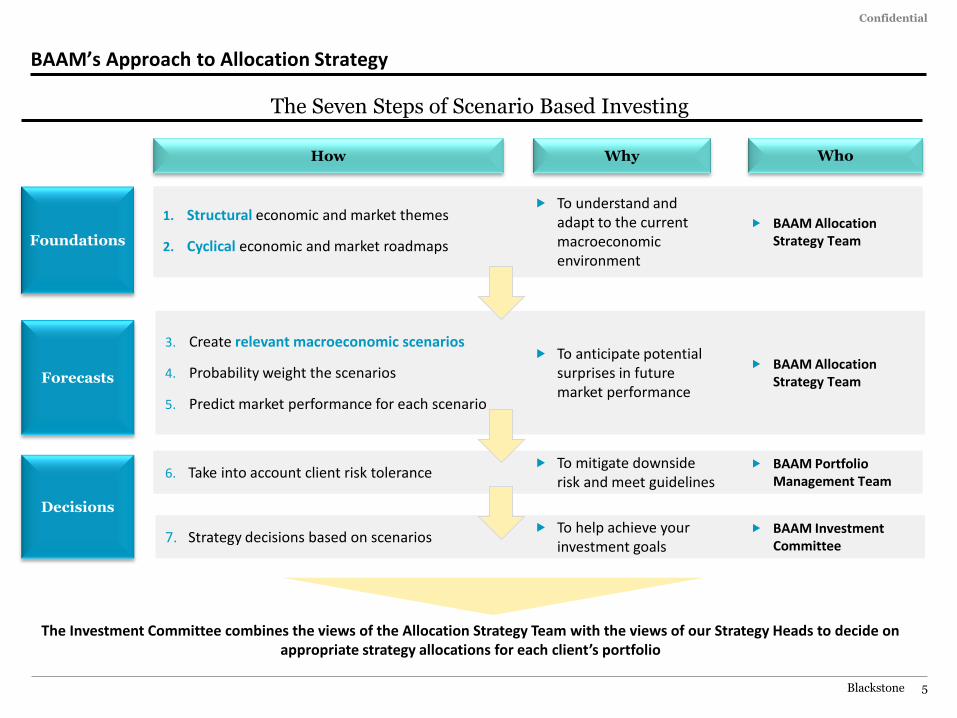

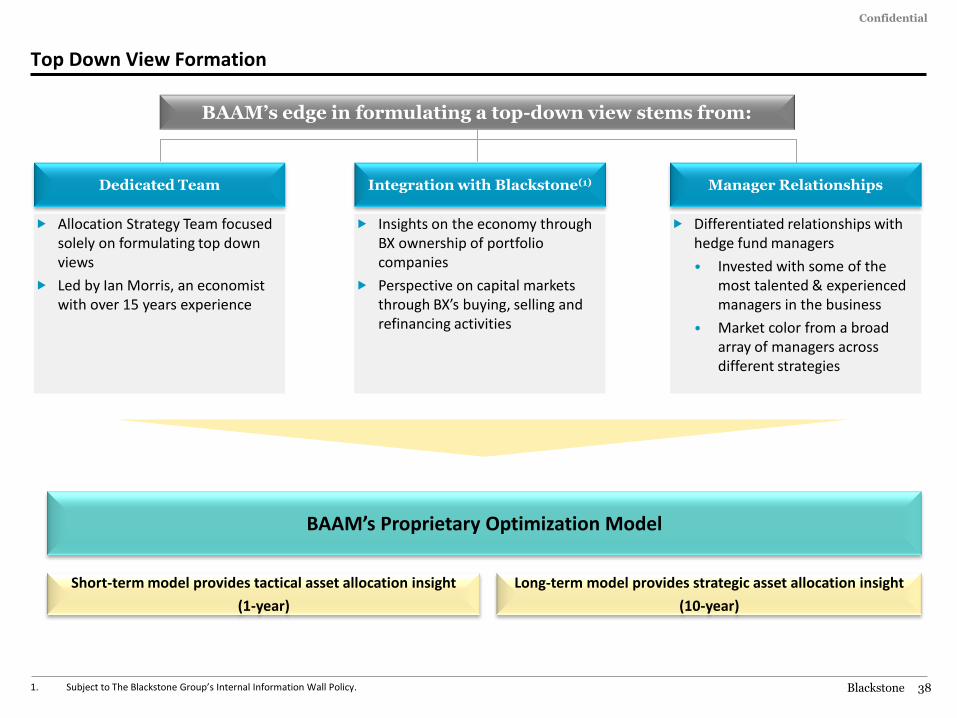

BAAM’s Approach to Allocation Strategy

The Seven Steps of Scenario Based Investing

Foundations

How Why Who

Forecasts

Decisions

1. Structural economic and market themes

2. Cyclical economic and market roadmaps

To understand and adapt to the current macroeconomic environment

To anticipate potential surprises in future market performance

BAAM Allocation Strategy Team

To help achieve your investment goals

BAAM Allocation Strategy Team

3. Create relevant macroeconomic scenarios

4. Probability weight the scenarios

5. Predict market performance for each scenario

BAAM Investment Committee

7. Strategy decisions based on scenarios

The Investment Committee combines the views of the Allocation Strategy Team with the views of our Strategy Heads to decide on appropriate strategy allocations for each client’s portfolio

6. Take into account client risk tolerance To mitigate downside

risk and meet guidelines BAAM Portfolio

Management Team

Confidential

Blackstone 6

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

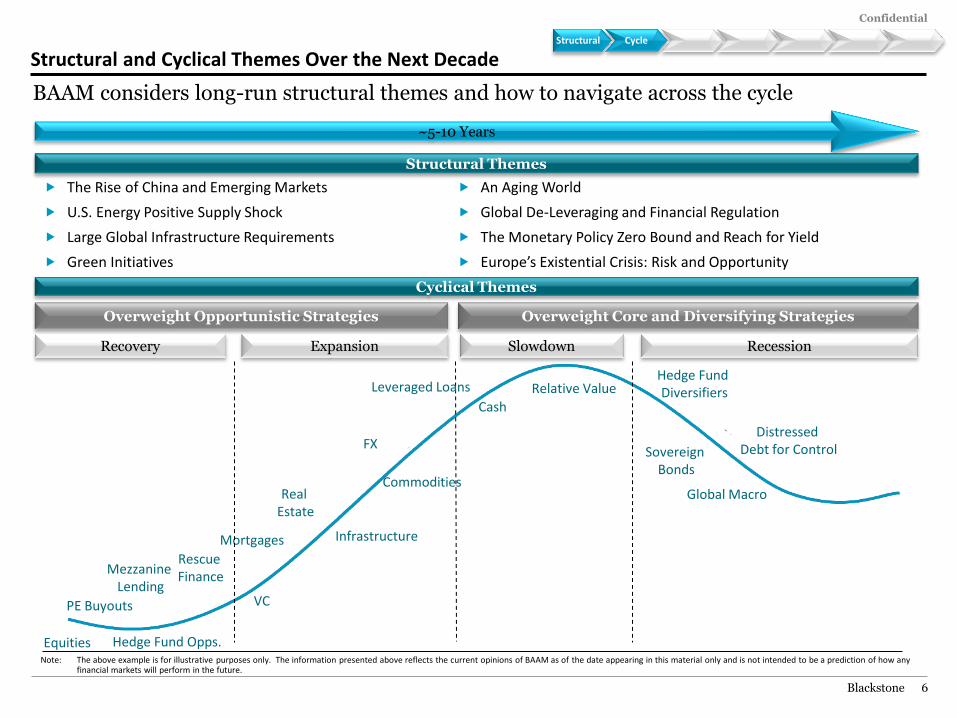

Structural and Cyclical Themes Over the Next Decade

~5-10 Years

Cyclical Themes

Structural Themes

The Rise of China and Emerging Markets

U.S. Energy Positive Supply Shock

Large Global Infrastructure Requirements

Green Initiatives

An Aging World

Global De-Leveraging and Financial Regulation

The Monetary Policy Zero Bound and Reach for Yield

Europe’s Existential Crisis: Risk and Opportunity

Overweight Opportunistic Strategies Overweight Core and Diversifying Strategies

Recovery Expansion Slowdown Recession

Mortgages Infrastructure

Mezzanine Lending

PE Buyouts

Equities

Real Estate

Hedge Fund Opps.

VC

FX

Rescue Finance

Commodities

Cash

Relative Value Hedge Fund Diversifiers

Sovereign Bonds

Global Macro

Distressed Debt for Control

Note: The above example is for illustrative purposes only. The information presented above reflects the current opinions of BAAM as of the date appearing in this material only and is not intended to be a prediction of how any financial markets will perform in the future.

BAAM considers long-run structural themes and how to navigate across the cycle

Leveraged Loans

Structural Themes Cycle

Confidential

Blackstone 7

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

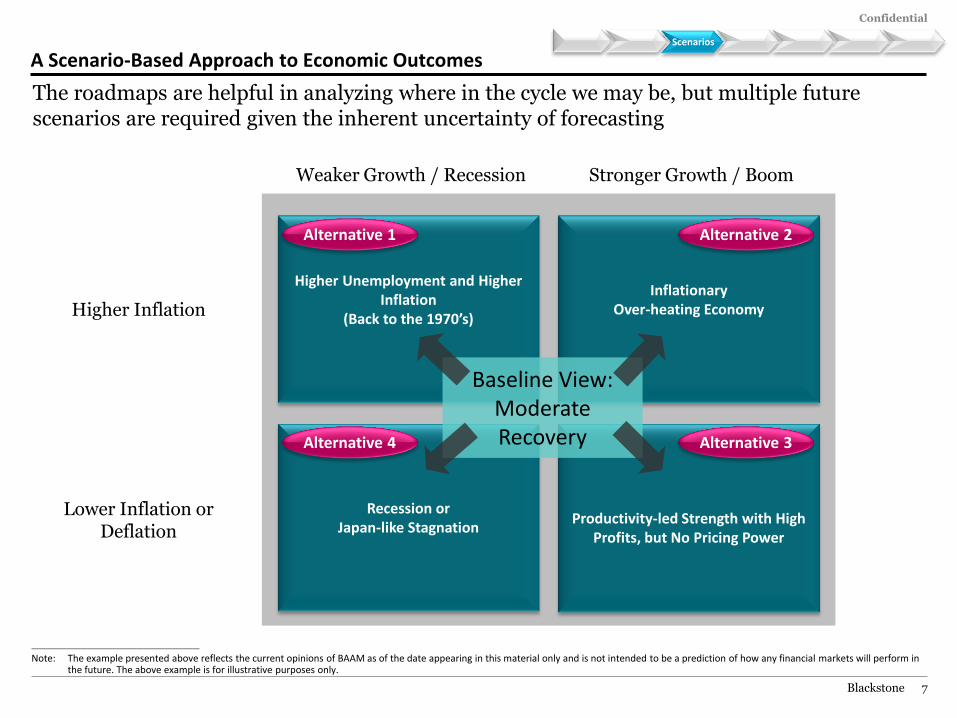

A Scenario-Based Approach to Economic Outcomes

Productivity-led Strength with High

Profits, but No Pricing Power

Higher Unemployment and Higher Inflation

(Back to the 1970’s)

Inflationary Over-heating Economy

Recession or Japan-like Stagnation

Higher Inflation

Lower Inflation or Deflation

Weaker Growth / Recession Stronger Growth / Boom

________________________________________________

Note: The example presented above reflects the current opinions of BAAM as of the date appearing in this material only and is not intended to be a prediction of how any financial markets will perform in the future. The above example is for illustrative purposes only.

Baseline View: Moderate Recovery

Alternative 1 Alternative 2

Alternative 4 Alternative 3

The roadmaps are helpful in analyzing where in the cycle we may be, but multiple future scenarios are required given the inherent uncertainty of forecasting

Scenarios Scenarios

Confidential

Blackstone 8

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

2%

2%

13%

1%

5%

5%

16%

6%

5%

2%

10%

8%

7% 3%

7%

3%

3%

2%

QE Proves Effective (1)

New Economy, Zero Inflation

Europe Improves

Global Decoupling

Moderate Growth

Financial Healing

China Bust, Developed Markets Up

Inflationary Overheating

Deflationary Slog

Europe Worsens

Greece Exit Triggers Chaos

EMU Disintegrates

Double Dip Light

Stagflation Fears

Double Dip Heavy

China Bust, Developed Markets Down

Germany Leaves Euro

BeautifulInflation

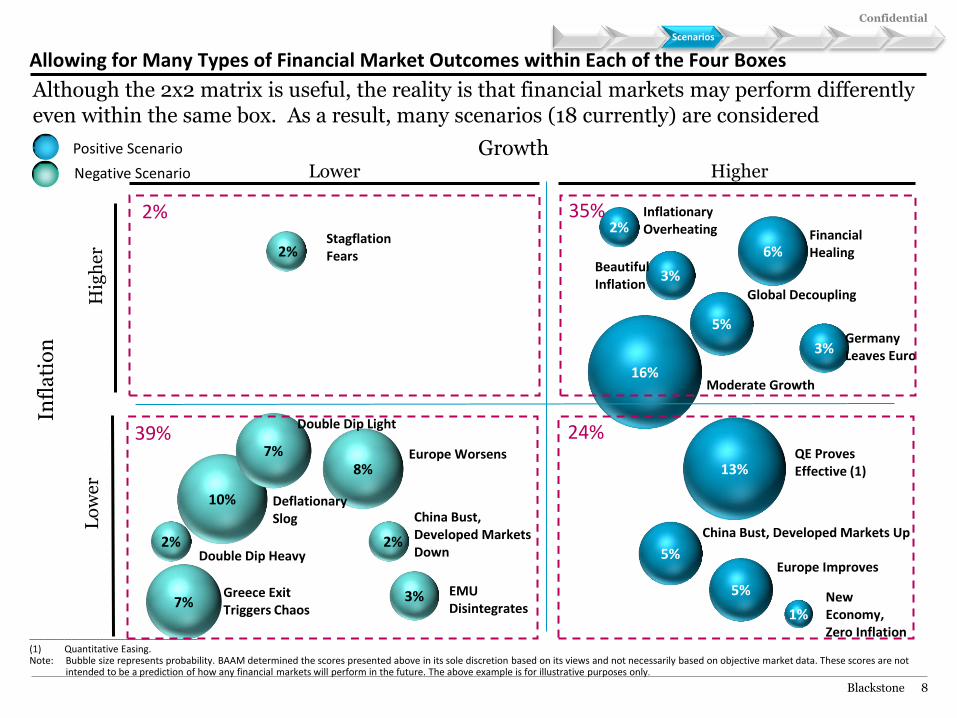

Allowing for Many Types of Financial Market Outcomes within Each of the Four Boxes

________________________________________________

(1) Quantitative Easing. Note: Bubble size represents probability. BAAM determined the scores presented above in its sole discretion based on its views and not necessarily based on objective market data. These scores are not

intended to be a prediction of how any financial markets will perform in the future. The above example is for illustrative purposes only.

Growth

Infl

ati

on

Lower Higher

Lo

we

r H

igh

er

Positive Scenario

Negative Scenario

2%

39%

35%

24%

Although the 2x2 matrix is useful, the reality is that financial markets may perform differently even within the same box. As a result, many scenarios (18 currently) are considered

Scenarios

Confidential

Blackstone 9

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

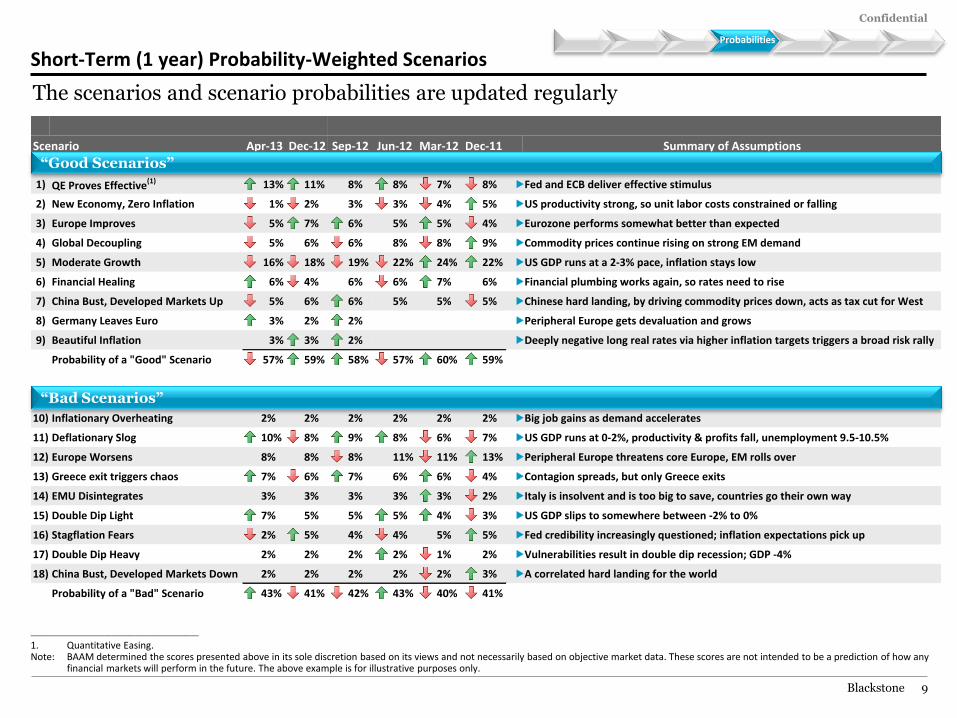

Scenario Sep-12 Jun-12 Mar-12 Dec-11 Summary of Assumptions

"Good" Scenarios

1) QE Proves Effective(1) 13% 11% 8% 8% 7% 8% Fed and ECB deliver effective stimulus

2) New Economy, Zero Inflation 1% 2% 3% 3% 4% 5% US productivity strong, so unit labor costs constrained or falling

3) Europe Improves 5% 7% 6% 5% 5% 4% Eurozone performs somewhat better than expected

4) Global Decoupling 5% 6% 6% 8% 8% 9% Commodity prices continue rising on strong EM demand

5) Moderate Growth 16% 18% 19% 22% 24% 22% US GDP runs at a 2-3% pace, inflation stays low

6) Financial Healing 6% 4% 6% 6% 7% 6% Financial plumbing works again, so rates need to rise

7) China Bust, Developed Markets Up 5% 6% 6% 5% 5% 5% Chinese hard landing, by driving commodity prices down, acts as tax cut for West

8) Germany Leaves Euro 3% 2% 2% Peripheral Europe gets devaluation and grows

9) Beautiful Inflation 3% 3% 2% Deeply negative long real rates via higher inflation targets triggers a broad risk rally

Probability of a "Good" Scenario 57% 59% 58% 57% 60% 59%

"Bad" Scenarios

10) Inflationary Overheating 2% 2% 2% 2% 2% 2% Big job gains as demand accelerates

11) Deflationary Slog 10% 8% 9% 8% 6% 7% US GDP runs at 0-2%, productivity & profits fall, unemployment 9.5-10.5%

12) Europe Worsens 8% 8% 8% 11% 11% 13% Peripheral Europe threatens core Europe, EM rolls over

13) Greece exit triggers chaos 7% 6% 7% 6% 6% 4% Contagion spreads, but only Greece exits

14) EMU Disintegrates 3% 3% 3% 3% 3% 2% Italy is insolvent and is too big to save, countries go their own way

15) Double Dip Light 7% 5% 5% 5% 4% 3% US GDP slips to somewhere between -2% to 0%

16) Stagflation Fears 2% 5% 4% 4% 5% 5% Fed credibility increasingly questioned; inflation expectations pick up

17) Double Dip Heavy 2% 2% 2% 2% 1% 2% Vulnerabilities result in double dip recession; GDP -4%

18) China Bust, Developed Markets Down 2% 2% 2% 2% 2% 3% A correlated hard landing for the world

Probability of a "Bad" Scenario 43% 41% 42% 43% 40% 41%

Dec-12Apr-13

________________________________________________

1. Quantitative Easing. Note: BAAM determined the scores presented above in its sole discretion based on its views and not necessarily based on objective market data. These scores are not intended to be a prediction of how any

financial markets will perform in the future. The above example is for illustrative purposes only.

The scenarios and scenario probabilities are updated regularly

Probabilities

“Good Scenarios”

“Bad Scenarios”

Short-Term (1 year) Probability-Weighted Scenarios

Confidential

Blackstone 10

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

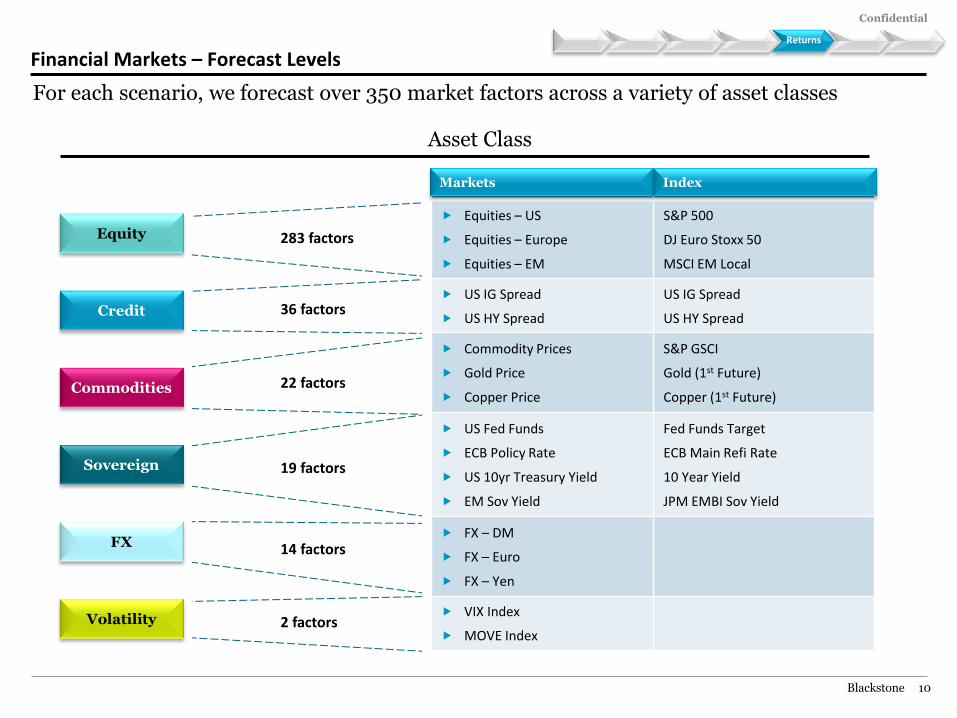

Financial Markets – Forecast Levels

For each scenario, we forecast over 350 market factors across a variety of asset classes

Asset Class

283 factors

22 factors

19 factors

14 factors

2 factors

36 factors

Themes Returns

Equity

Credit

Commodities

Sovereign

FX

Volatility

Markets Index

Equities – US

Equities – Europe

Equities – EM

S&P 500

DJ Euro Stoxx 50

MSCI EM Local

US IG Spread

US HY Spread

US IG Spread

US HY Spread

Commodity Prices

Gold Price

Copper Price

S&P GSCI

Gold (1st Future)

Copper (1st Future)

US Fed Funds

ECB Policy Rate

US 10yr Treasury Yield

EM Sov Yield

Fed Funds Target

ECB Main Refi Rate

10 Year Yield

JPM EMBI Sov Yield

FX – DM

FX – Euro

FX – Yen

VIX Index

MOVE Index

Markets Index

Confidential

Blackstone 11

BEAR BASE BULL

Do

ub

le D

ip H

eav

y

EMU

dis

inte

grat

es

Ch

ina

Bu

st, D

M

Do

wn

De

flat

ion

ary

Slo

g

Do

ub

le D

ip L

igh

t

Stag

flat

ion

Fe

ars

Gre

ece

exi

t

trig

gers

ch

aos

Infl

atio

nar

y

Ove

rhe

atin

g

Euro

pe

Wo

rse

ns

Fin

anci

al H

eal

ing

Mo

de

rate

Gro

wth

QE

Pro

ves

Effe

ctiv

e

Glo

bal

De

cou

plin

g

Ge

rman

y Le

ave

s

Euro

Be

auti

ful I

nfl

atio

n

Ch

ina

Bu

st, D

M U

p

Euro

pe

Imp

rove

s

Ne

w E

con

om

y,

Zero

Infl

atio

n

Pro

bab

ility

-

We

igh

ted

Probability 2% 3% 2% 10% 7% 2% 7% 2% 8% 6% 16% 13% 5% 3% 3% 5% 5% 1% 100%

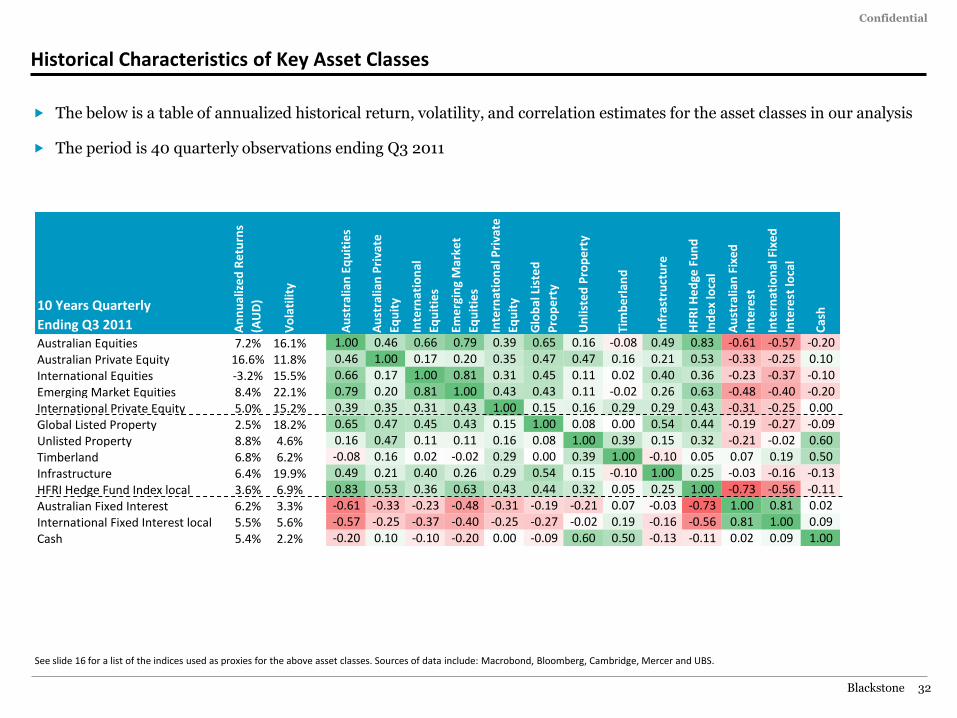

Australian Equities -31.8% -19.2% -31.8% -4.0% -10.8% -5.3% -4.1% -1.1% -4.8% 9.0% 16.7% 22.8% 19.4% 21.0% 13.2% 18.2% 25.5% 31.9% 6.9%

Australian Private Equity -62.6% -37.4% -67.6% -7.0% -20.6% -9.6% -7.2% -1.1% -8.6% 19.1% 34.4% 46.5% 39.9% 12.4% 27.4% -2.6% 52.0% 64.8% 11.7%

International Equities -32.6% -32.1% -16.1% -8.3% -16.4% -9.9% -10.1% -4.6% -4.3% 8.3% 18.1% 25.8% 21.6% 20.0% 34.6% 30.0% 34.3% 37.4% 7.8%

Emerging Market Equities -32.0% -27.1% -31.2% 13.6% -11.0% -9.3% -6.2% -4.0% 0.0% 9.0% 18.9% 26.6% 43.0% 24.4% 25.0% -12.0% 30.1% 22.8% 9.6%

International Private Equity -68.7% -67.7% -35.7% -20.1% -36.4% -23.4% -23.8% -12.8% -12.1% 13.1% 32.7% 48.1% 39.7% 5.6% 65.6% 56.5% 65.1% 71.3% 11.1%

Global Listed Property -22.0% -16.0% -22.0% -2.4% -9.8% 10.8% -5.8% 15.6% -4.3% 10.6% 12.2% 17.0% 17.5% 14.7% 15.4% 1.8% 16.2% 8.2% 5.0%

Unlisted Property -28.8% -21.3% -28.8% -4.2% -13.5% 12.2% -8.5% 18.3% -6.7% 11.9% 13.9% 19.9% 20.6% 17.0% 17.9% 0.9% 18.9% 8.9% 5.0%

Timberland/Natural Resources -20.9% -4.6% -20.9% -1.4% -11.1% 21.4% -4.6% 31.1% -4.6% 10.3% 10.3% 18.1% 18.1% 11.6% 18.1% -7.9% 11.6% 5.1% 5.1%

Infrastructure -25.0% -4.8% -25.0% -1.5% -11.3% 21.2% -4.8% 35.0% -4.8% 10.2% 10.2% 18.0% 18.0% 15.0% 25.0% -8.0% 11.5% 5.0% 5.2%

Hedge Funds -9.2% -6.9% -4.1% 2.4% -1.3% 0.9% -0.3% 2.1% 1.7% 4.7% 8.0% 9.7% 10.6% 8.2% 9.9% 8.6% 11.7% 11.3% 4.9%

Australian Fixed Interest 7.5% 7.4% 7.2% 6.6% 6.1% -6.2% 6.3% -7.3% 5.6% -2.3% 2.0% 2.6% 1.5% 5.0% 2.6% 6.1% 0.4% 4.8% 3.4%

International Fixed Interest 7.2% 7.0% 6.8% 6.2% 5.6% -8.1% 5.8% -9.3% 5.1% -3.8% 1.1% 5.6% 0.4% 4.4% 1.7% 5.6% -0.8% 4.1% 3.1%

Cash 0.2% 1.2% 1.2% 1.7% 1.2% 2.7% 1.7% 4.2% 1.7% 2.2% 2.2% 2.7% 2.7% 1.7% 2.7% 1.5% 2.5% 2.2% 2.0%

AUD per 1 USD 40.2% 22.3% 64.0% -7.4% 2.6% -11.8% 15.0% -8.3% 8.4% 0.4% -2.7% 2.6% -9.2% 2.6% -7.4% 22.3% -9.2% 2.6% 3.5%

Probability 2% 3% 2% 10% 7% 2% 7% 2% 8% 6% 16% 13% 5% 3% 3% 5% 5% 1% 100%

Australian Equities -31.8% -19.2% -31.8% -4.0% -10.8% -5.3% -4.1% -1.1% -4.8% 9.0% 16.7% 22.8% 19.4% 21.0% 13.2% 18.2% 25.5% 31.9% 6.9%

Australian Private Equity -62.6% -37.4% -67.6% -7.0% -20.6% -9.6% -7.2% -1.1% -8.6% 19.1% 34.4% 46.5% 39.9% 12.4% 27.4% -2.6% 52.0% 64.8% 11.7%

International Equities -13.6% -21.4% 21.6% -13.1% -14.9% -17.4% -0.7% -10.2% 1.4% 8.7% 15.9% 28.1% 13.8% 22.1% 27.6% 50.3% 25.7% 39.9% 9.8%

Emerging Market Equities -18.4% -19.0% -9.2% 9.4% -9.8% -14.6% 0.8% -8.0% 4.2% 9.3% 17.3% 28.2% 36.4% 26.0% 20.4% -2.2% 24.1% 24.4% 10.6%

International Private Equity -59.9% -62.6% -6.8% -24.3% -35.3% -29.7% -15.8% -17.8% -6.9% 13.5% 30.3% 50.8% 30.7% 7.5% 57.0% 80.9% 54.4% 74.4% 12.5%

Global Listed Property -0.1% -2.9% 12.9% -7.4% -8.1% 1.7% 4.1% 8.9% 1.3% 10.9% 10.1% 19.1% 10.0% 16.7% 9.4% 17.7% 8.7% 10.1% 6.9%

Unlisted Property -28.8% -21.3% -28.8% -4.2% -13.5% 12.2% -8.5% 18.3% -6.7% 11.9% 13.9% 19.9% 20.6% 17.0% 17.9% 0.9% 18.9% 8.9% 5.0%

Timberland/Natural Resources -20.9% -4.6% -20.9% -1.4% -11.1% 21.4% -4.6% 31.1% -4.6% 10.3% 10.3% 18.1% 18.1% 11.6% 18.1% -7.9% 11.6% 5.1% 5.1%

Infrastructure -25.0% -4.8% -25.0% -1.5% -11.3% 21.2% -4.8% 35.0% -4.8% 10.2% 10.2% 18.0% 18.0% 15.0% 25.0% -8.0% 11.5% 5.0% 5.2%

Hedge Funds 12.7% 5.6% 32.8% -2.2% 0.3% -6.3% 8.7% -3.0% 6.8% 4.9% 6.3% 11.4% 4.5% 9.9% 5.0% 23.2% 5.5% 13.1% 6.9%

Australian Fixed Interest 7.5% 7.4% 7.2% 6.6% 6.1% -6.2% 6.3% -7.3% 5.6% -2.3% 2.0% 2.6% 1.5% 5.0% 2.6% 6.1% 0.4% 4.8% 3.4%

International Fixed Interest 7.2% 7.0% 6.8% 6.2% 5.6% -8.1% 5.8% -9.3% 5.1% -3.8% 1.1% 5.6% 0.4% 4.4% 1.7% 5.6% -0.8% 4.1% 3.1%

Cash 0.2% 1.2% 1.2% 1.7% 1.2% 2.7% 1.7% 4.2% 1.7% 2.2% 2.2% 2.7% 2.7% 1.7% 2.7% 1.5% 2.5% 2.2% 2.0%

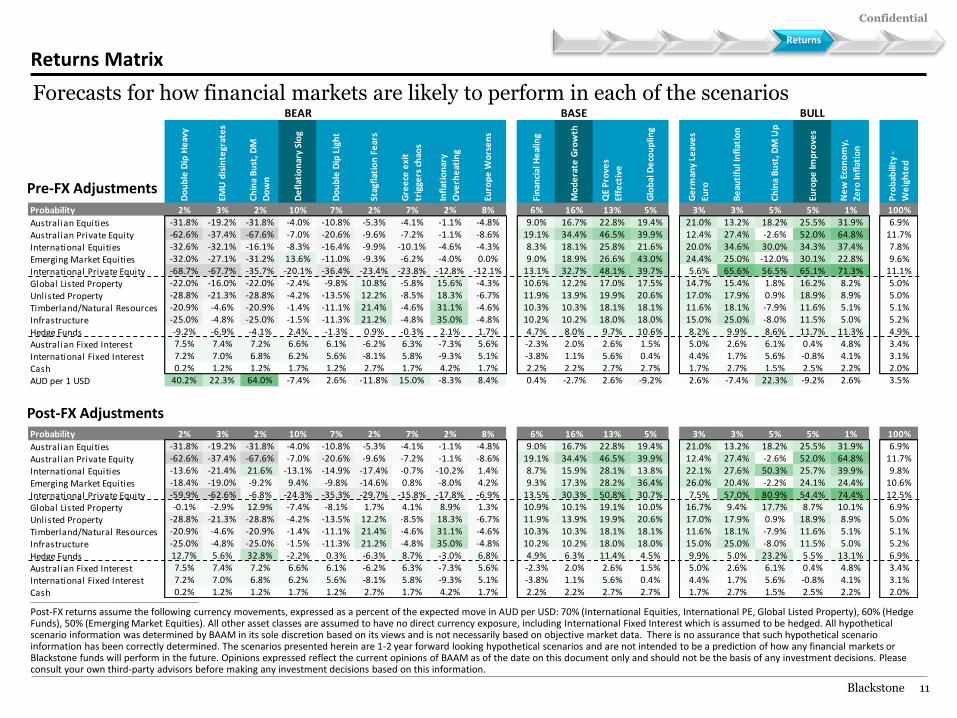

Returns Matrix

________________________________________________

Post-FX returns assume the following currency movements, expressed as a percent of the expected move in AUD per USD: 70% (International Equities, International PE, Global Listed Property), 60% (Hedge Funds), 50% (Emerging Market Equities). All other asset classes are assumed to have no direct currency exposure, including International Fixed Interest which is assumed to be hedged. All hypothetical scenario information was determined by BAAM in its sole discretion based on its views and is not necessarily based on objective market data. There is no assurance that such hypothetical scenario information has been correctly determined. The scenarios presented herein are 1-2 year forward looking hypothetical scenarios and are not intended to be a prediction of how any financial markets or Blackstone funds will perform in the future. Opinions expressed reflect the current opinions of BAAM as of the date on this document only and should not be the basis of any investment decisions. Please consult your own third-party advisors before making any investment decisions based on this information.

Pre-FX Adjustments

Post-FX Adjustments

Forecasts for how financial markets are likely to perform in each of the scenarios

Themes Returns

Confidential

Blackstone 12

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

-10% -5% 0% 5% 10%

Uti

lity

Return

Lambda = 0 (risk neutral, straightline)

Lambda = 5

Lambda = 15

Lambda = 25 (very risk averse,very curved)

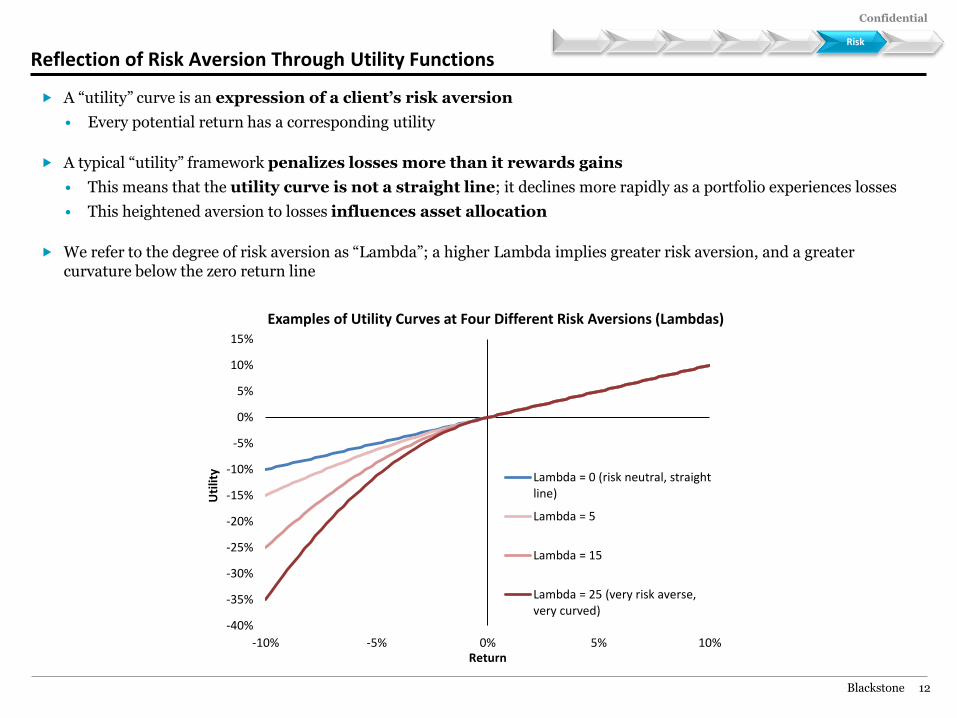

Reflection of Risk Aversion Through Utility Functions

A “utility” curve is an expression of a client’s risk aversion

• Every potential return has a corresponding utility

A typical “utility” framework penalizes losses more than it rewards gains

• This means that the utility curve is not a straight line; it declines more rapidly as a portfolio experiences losses

• This heightened aversion to losses influences asset allocation

We refer to the degree of risk aversion as “Lambda”; a higher Lambda implies greater risk aversion, and a greater curvature below the zero return line

6 Themes Risk

Examples of Utility Curves at Four Different Risk Aversions (Lambdas)

Confidential

Blackstone 13

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

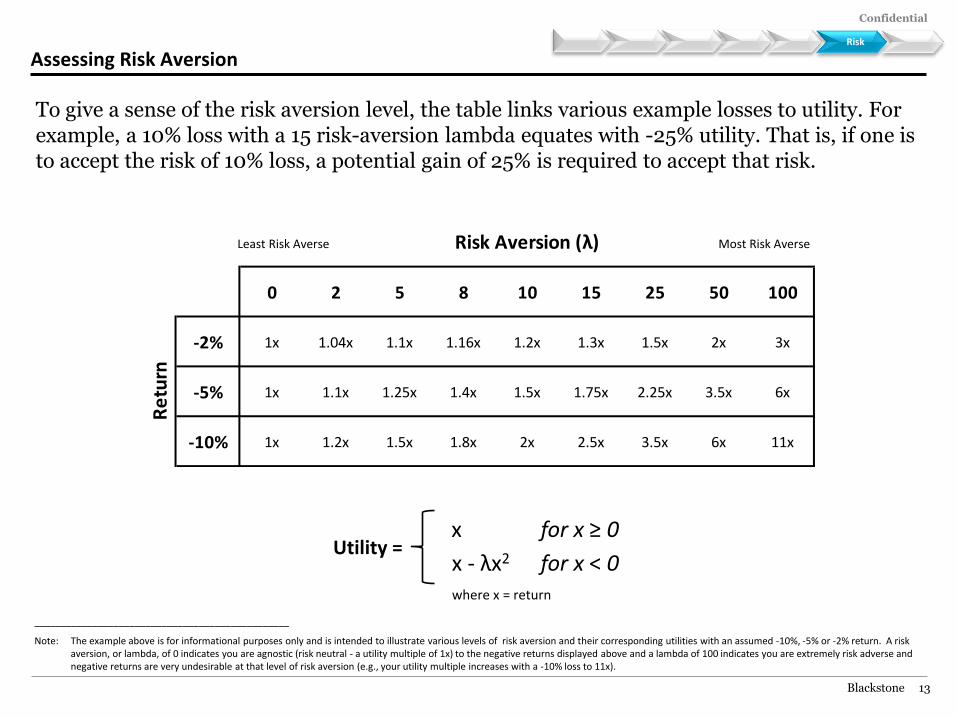

0 2 5 8 10 15 25 50 100

-2% 1x 1.04x 1.1x 1.16x 1.2x 1.3x 1.5x 2x 3x

-5% 1x 1.1x 1.25x 1.4x 1.5x 1.75x 2.25x 3.5x 6x

-10% 1x 1.2x 1.5x 1.8x 2x 2.5x 3.5x 6x 11x

Risk Aversion (λ)

Re

turn

Assessing Risk Aversion

To give a sense of the risk aversion level, the table links various example losses to utility. For example, a 10% loss with a 15 risk-aversion lambda equates with -25% utility. That is, if one is to accept the risk of 10% loss, a potential gain of 25% is required to accept that risk.

________________________________________________

Note: The example above is for informational purposes only and is intended to illustrate various levels of risk aversion and their corresponding utilities with an assumed -10%, -5% or -2% return. A risk aversion, or lambda, of 0 indicates you are agnostic (risk neutral - a utility multiple of 1x) to the negative returns displayed above and a lambda of 100 indicates you are extremely risk adverse and negative returns are very undesirable at that level of risk aversion (e.g., your utility multiple increases with a -10% loss to 11x).

Least Risk Averse Most Risk Averse

Utility = x for x ≥ 0

for x < 0 x - λx2

where x = return

6 Themes Risk

Confidential

Blackstone 14

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

- 0% +

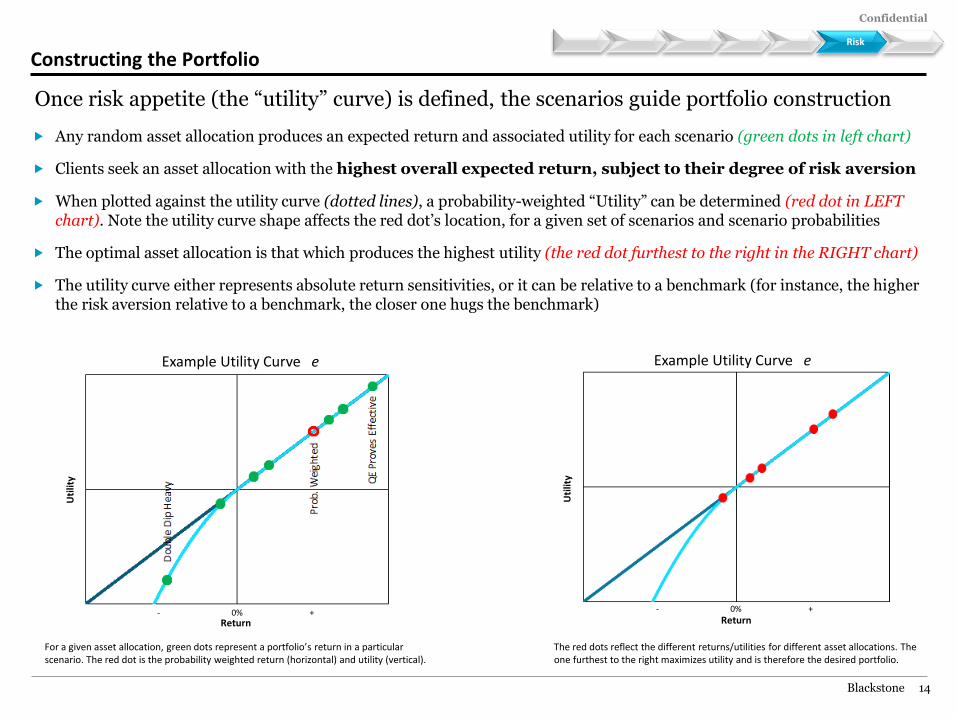

Constructing the Portfolio

Any random asset allocation produces an expected return and associated utility for each scenario (green dots in left chart)

Clients seek an asset allocation with the highest overall expected return, subject to their degree of risk aversion

When plotted against the utility curve (dotted lines), a probability-weighted “Utility” can be determined (red dot in LEFT chart). Note the utility curve shape affects the red dot’s location, for a given set of scenarios and scenario probabilities

The optimal asset allocation is that which produces the highest utility (the red dot furthest to the right in the RIGHT chart)

The utility curve either represents absolute return sensitivities, or it can be relative to a benchmark (for instance, the higher the risk aversion relative to a benchmark, the closer one hugs the benchmark)

Once risk appetite (the “utility” curve) is defined, the scenarios guide portfolio construction

Example Utility Curve e

6 Themes Risk

For a given asset allocation, green dots represent a portfolio’s return in a particular scenario. The red dot is the probability weighted return (horizontal) and utility (vertical).

The red dots reflect the different returns/utilities for different asset allocations. The one furthest to the right maximizes utility and is therefore the desired portfolio.

Uti

lity

Uti

lity

Return Return - 0% +

Example Utility Curve e

II. Insights from Our Views and Framework for Australian Portfolios

Allocations

Decisions

Confidential

Blackstone 16

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

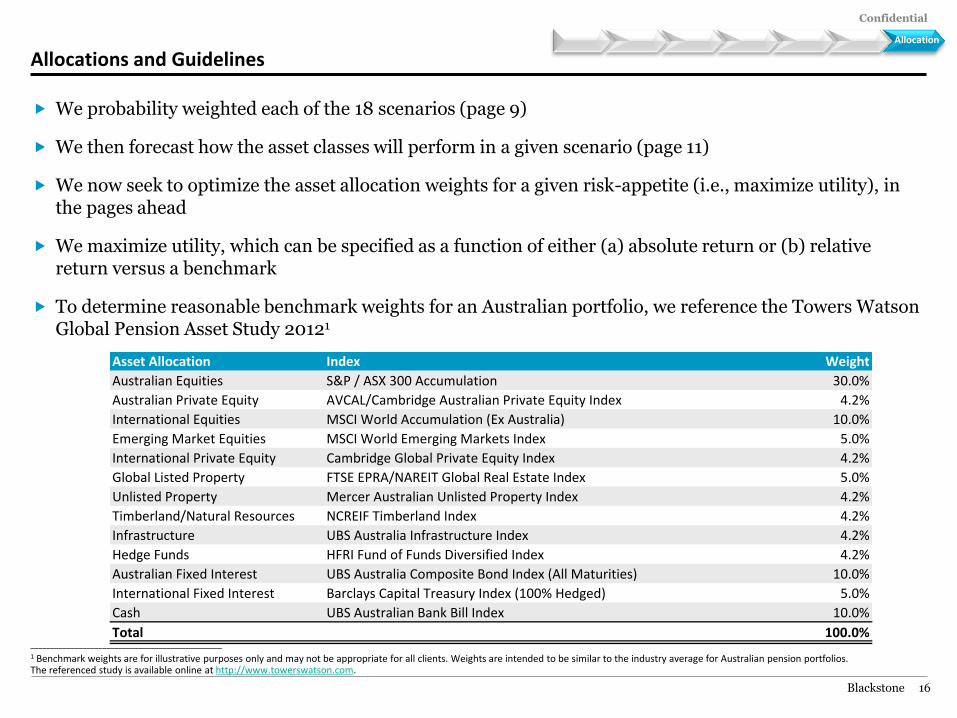

Asset Allocation Index Weight

Australian Equities S&P / ASX 300 Accumulation 30.0%

Australian Private Equity AVCAL/Cambridge Australian Private Equity Index 4.2%

International Equities MSCI World Accumulation (Ex Australia) 10.0%

Emerging Market Equities MSCI World Emerging Markets Index 5.0%

International Private Equity Cambridge Global Private Equity Index 4.2%

Global Listed Property FTSE EPRA/NAREIT Global Real Estate Index 5.0%

Unlisted Property Mercer Australian Unlisted Property Index 4.2%

Timberland/Natural Resources NCREIF Timberland Index 4.2%

Infrastructure UBS Australia Infrastructure Index 4.2%

Hedge Funds HFRI Fund of Funds Diversified Index 4.2%

Australian Fixed Interest UBS Australia Composite Bond Index (All Maturities) 10.0%

International Fixed Interest Barclays Capital Treasury Index (100% Hedged) 5.0%

Cash UBS Australian Bank Bill Index 10.0%

Total 100.0%

Allocations and Guidelines

We probability weighted each of the 18 scenarios (page 9)

We then forecast how the asset classes will perform in a given scenario (page 11)

We now seek to optimize the asset allocation weights for a given risk-appetite (i.e., maximize utility), in the pages ahead

We maximize utility, which can be specified as a function of either (a) absolute return or (b) relative return versus a benchmark

To determine reasonable benchmark weights for an Australian portfolio, we reference the Towers Watson Global Pension Asset Study 20121

________________________________________________

1 Benchmark weights are for illustrative purposes only and may not be appropriate for all clients. Weights are intended to be similar to the industry average for Australian pension portfolios. The referenced study is available online at http://www.towerswatson.com.

Allocation

Confidential

Blackstone 17

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

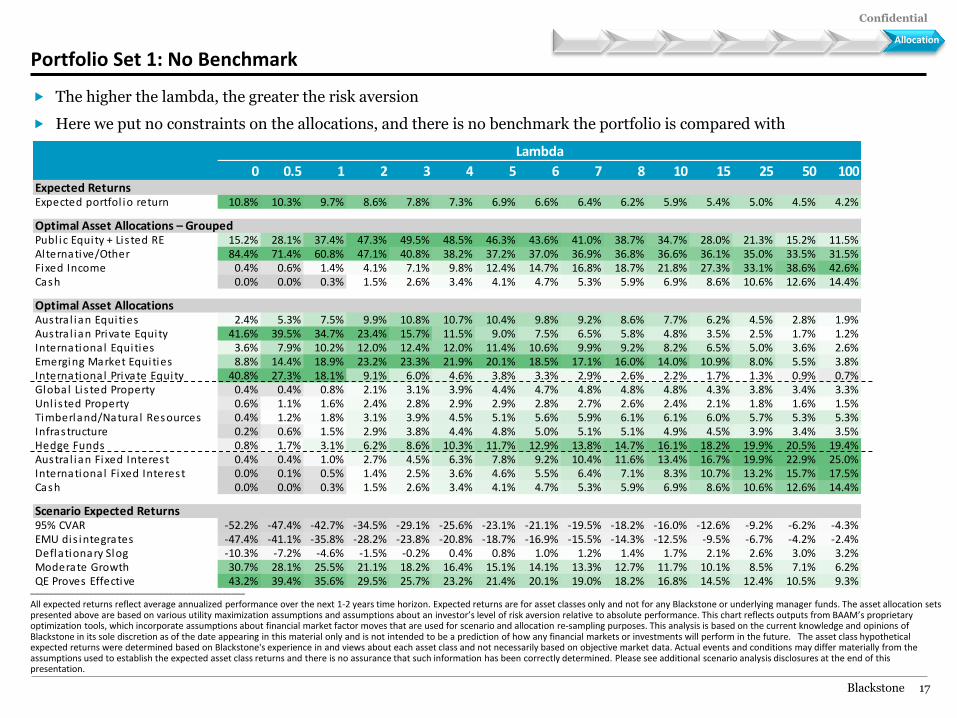

Lambda

0 0.5 1 2 3 4 5 6 7 8 10 15 25 50 100Expected ReturnsExpected portfol io return 10.8% 10.3% 9.7% 8.6% 7.8% 7.3% 6.9% 6.6% 6.4% 6.2% 5.9% 5.4% 5.0% 4.5% 4.2%

Optimal Asset Allocations – GroupedPubl ic Equity + Lis ted RE 15.2% 28.1% 37.4% 47.3% 49.5% 48.5% 46.3% 43.6% 41.0% 38.7% 34.7% 28.0% 21.3% 15.2% 11.5%Alternative/Other 84.4% 71.4% 60.8% 47.1% 40.8% 38.2% 37.2% 37.0% 36.9% 36.8% 36.6% 36.1% 35.0% 33.5% 31.5%Fixed Income 0.4% 0.6% 1.4% 4.1% 7.1% 9.8% 12.4% 14.7% 16.8% 18.7% 21.8% 27.3% 33.1% 38.6% 42.6%Cash 0.0% 0.0% 0.3% 1.5% 2.6% 3.4% 4.1% 4.7% 5.3% 5.9% 6.9% 8.6% 10.6% 12.6% 14.4%

Optimal Asset AllocationsAustra l ian Equities 2.4% 5.3% 7.5% 9.9% 10.8% 10.7% 10.4% 9.8% 9.2% 8.6% 7.7% 6.2% 4.5% 2.8% 1.9%Austra l ian Private Equity 41.6% 39.5% 34.7% 23.4% 15.7% 11.5% 9.0% 7.5% 6.5% 5.8% 4.8% 3.5% 2.5% 1.7% 1.2%International Equities 3.6% 7.9% 10.2% 12.0% 12.4% 12.0% 11.4% 10.6% 9.9% 9.2% 8.2% 6.5% 5.0% 3.6% 2.6%Emerging Market Equities 8.8% 14.4% 18.9% 23.2% 23.3% 21.9% 20.1% 18.5% 17.1% 16.0% 14.0% 10.9% 8.0% 5.5% 3.8%International Private Equity 40.8% 27.3% 18.1% 9.1% 6.0% 4.6% 3.8% 3.3% 2.9% 2.6% 2.2% 1.7% 1.3% 0.9% 0.7%Global Lis ted Property 0.4% 0.4% 0.8% 2.1% 3.1% 3.9% 4.4% 4.7% 4.8% 4.8% 4.8% 4.3% 3.8% 3.4% 3.3%Unl is ted Property 0.6% 1.1% 1.6% 2.4% 2.8% 2.9% 2.9% 2.8% 2.7% 2.6% 2.4% 2.1% 1.8% 1.6% 1.5%Timberland/Natura l Resources 0.4% 1.2% 1.8% 3.1% 3.9% 4.5% 5.1% 5.6% 5.9% 6.1% 6.1% 6.0% 5.7% 5.3% 5.3%Infrastructure 0.2% 0.6% 1.5% 2.9% 3.8% 4.4% 4.8% 5.0% 5.1% 5.1% 4.9% 4.5% 3.9% 3.4% 3.5%Hedge Funds 0.8% 1.7% 3.1% 6.2% 8.6% 10.3% 11.7% 12.9% 13.8% 14.7% 16.1% 18.2% 19.9% 20.5% 19.4%Austra l ian Fixed Interest 0.4% 0.4% 1.0% 2.7% 4.5% 6.3% 7.8% 9.2% 10.4% 11.6% 13.4% 16.7% 19.9% 22.9% 25.0%International Fixed Interest 0.0% 0.1% 0.5% 1.4% 2.5% 3.6% 4.6% 5.5% 6.4% 7.1% 8.3% 10.7% 13.2% 15.7% 17.5%Cash 0.0% 0.0% 0.3% 1.5% 2.6% 3.4% 4.1% 4.7% 5.3% 5.9% 6.9% 8.6% 10.6% 12.6% 14.4%

Scenario Expected Returns95% CVAR -52.2% -47.4% -42.7% -34.5% -29.1% -25.6% -23.1% -21.1% -19.5% -18.2% -16.0% -12.6% -9.2% -6.2% -4.3%EMU dis integrates -47.4% -41.1% -35.8% -28.2% -23.8% -20.8% -18.7% -16.9% -15.5% -14.3% -12.5% -9.5% -6.7% -4.2% -2.4%Deflationary Slog -10.3% -7.2% -4.6% -1.5% -0.2% 0.4% 0.8% 1.0% 1.2% 1.4% 1.7% 2.1% 2.6% 3.0% 3.2%Moderate Growth 30.7% 28.1% 25.5% 21.1% 18.2% 16.4% 15.1% 14.1% 13.3% 12.7% 11.7% 10.1% 8.5% 7.1% 6.2%QE Proves Effective 43.2% 39.4% 35.6% 29.5% 25.7% 23.2% 21.4% 20.1% 19.0% 18.2% 16.8% 14.5% 12.4% 10.5% 9.3%

Portfolio Set 1: No Benchmark

The higher the lambda, the greater the risk aversion

Here we put no constraints on the allocations, and there is no benchmark the portfolio is compared with

Allocation

________________________________________________

All expected returns reflect average annualized performance over the next 1-2 years time horizon. Expected returns are for asset classes only and not for any Blackstone or underlying manager funds. The asset allocation sets presented above are based on various utility maximization assumptions and assumptions about an investor’s level of risk aversion relative to absolute performance. This chart reflects outputs from BAAM’s proprietary optimization tools, which incorporate assumptions about financial market factor moves that are used for scenario and allocation re-sampling purposes. This analysis is based on the current knowledge and opinions of Blackstone in its sole discretion as of the date appearing in this material only and is not intended to be a prediction of how any financial markets or investments will perform in the future. The asset class hypothetical expected returns were determined based on Blackstone's experience in and views about each asset class and not necessarily based on objective market data. Actual events and conditions may differ materially from the assumptions used to establish the expected asset class returns and there is no assurance that such information has been correctly determined. Please see additional scenario analysis disclosures at the end of this presentation.

Confidential

Blackstone 18

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

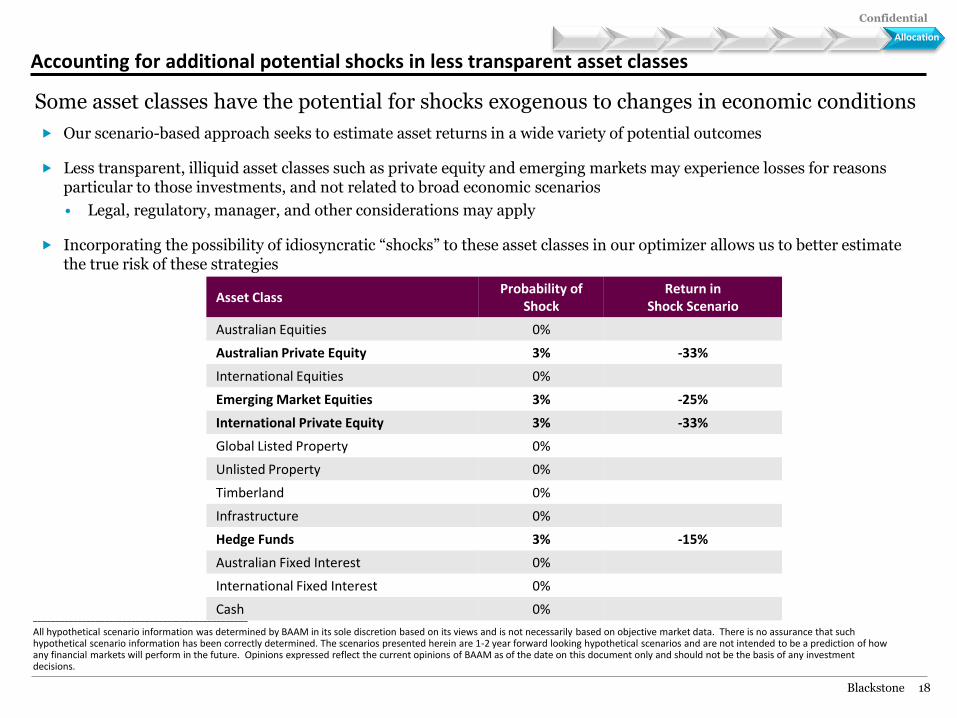

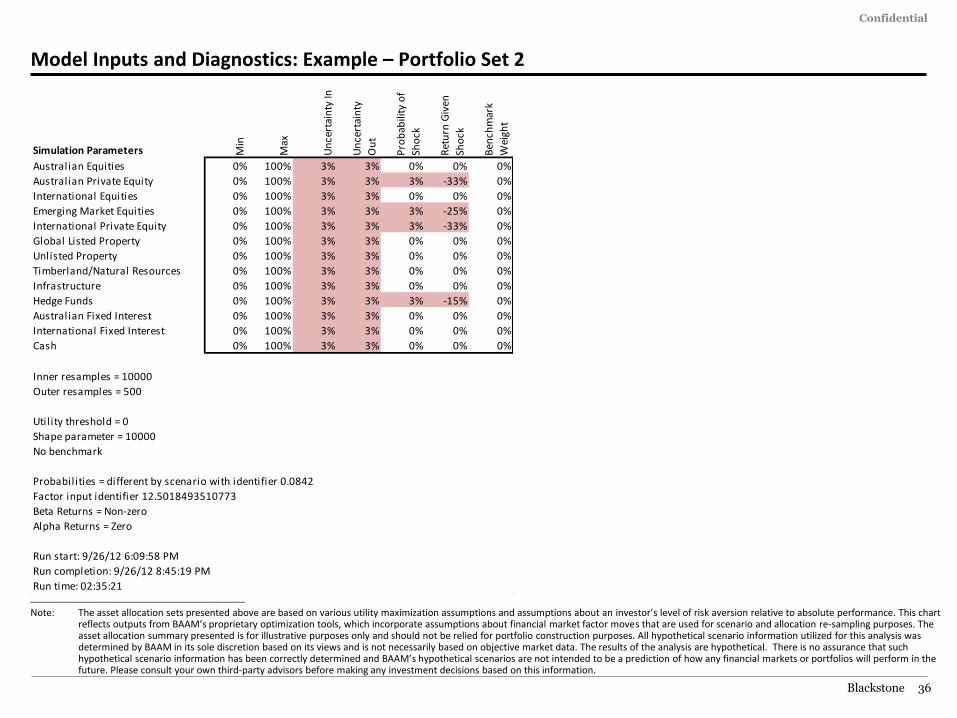

Accounting for additional potential shocks in less transparent asset classes

Our scenario-based approach seeks to estimate asset returns in a wide variety of potential outcomes

Less transparent, illiquid asset classes such as private equity and emerging markets may experience losses for reasons particular to those investments, and not related to broad economic scenarios

• Legal, regulatory, manager, and other considerations may apply

Incorporating the possibility of idiosyncratic “shocks” to these asset classes in our optimizer allows us to better estimate the true risk of these strategies

Some asset classes have the potential for shocks exogenous to changes in economic conditions

Asset Class Probability of

Shock Return in

Shock Scenario

Australian Equities 0%

Australian Private Equity 3% -33%

International Equities 0%

Emerging Market Equities 3% -25%

International Private Equity 3% -33%

Global Listed Property 0%

Unlisted Property 0%

Timberland 0%

Infrastructure 0%

Hedge Funds 3% -15%

Australian Fixed Interest 0%

International Fixed Interest 0%

Cash 0%

Allocation

________________________________________________

All hypothetical scenario information was determined by BAAM in its sole discretion based on its views and is not necessarily based on objective market data. There is no assurance that such hypothetical scenario information has been correctly determined. The scenarios presented herein are 1-2 year forward looking hypothetical scenarios and are not intended to be a prediction of how any financial markets will perform in the future. Opinions expressed reflect the current opinions of BAAM as of the date on this document only and should not be the basis of any investment decisions.

Confidential

Blackstone 19

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Lambda

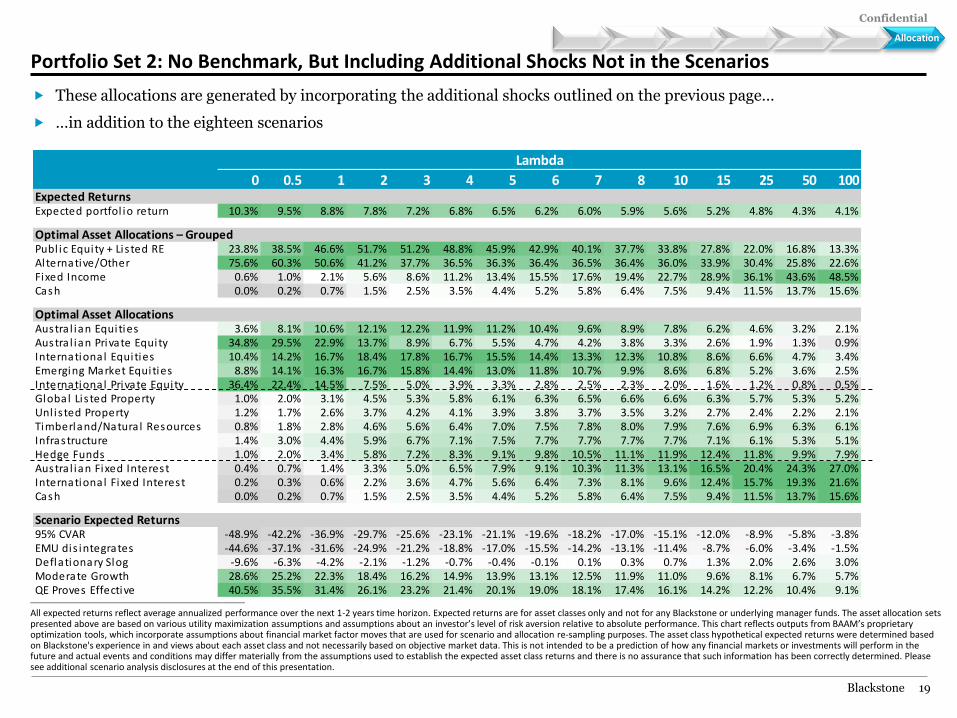

0 0.5 1 2 3 4 5 6 7 8 10 15 25 50 100Expected ReturnsExpected portfol io return 10.3% 9.5% 8.8% 7.8% 7.2% 6.8% 6.5% 6.2% 6.0% 5.9% 5.6% 5.2% 4.8% 4.3% 4.1%

Optimal Asset Allocations – GroupedPubl ic Equity + Lis ted RE 23.8% 38.5% 46.6% 51.7% 51.2% 48.8% 45.9% 42.9% 40.1% 37.7% 33.8% 27.8% 22.0% 16.8% 13.3%Alternative/Other 75.6% 60.3% 50.6% 41.2% 37.7% 36.5% 36.3% 36.4% 36.5% 36.4% 36.0% 33.9% 30.4% 25.8% 22.6%Fixed Income 0.6% 1.0% 2.1% 5.6% 8.6% 11.2% 13.4% 15.5% 17.6% 19.4% 22.7% 28.9% 36.1% 43.6% 48.5%Cash 0.0% 0.2% 0.7% 1.5% 2.5% 3.5% 4.4% 5.2% 5.8% 6.4% 7.5% 9.4% 11.5% 13.7% 15.6%

Optimal Asset AllocationsAustra l ian Equities 3.6% 8.1% 10.6% 12.1% 12.2% 11.9% 11.2% 10.4% 9.6% 8.9% 7.8% 6.2% 4.6% 3.2% 2.1%Austra l ian Private Equity 34.8% 29.5% 22.9% 13.7% 8.9% 6.7% 5.5% 4.7% 4.2% 3.8% 3.3% 2.6% 1.9% 1.3% 0.9%International Equities 10.4% 14.2% 16.7% 18.4% 17.8% 16.7% 15.5% 14.4% 13.3% 12.3% 10.8% 8.6% 6.6% 4.7% 3.4%Emerging Market Equities 8.8% 14.1% 16.3% 16.7% 15.8% 14.4% 13.0% 11.8% 10.7% 9.9% 8.6% 6.8% 5.2% 3.6% 2.5%International Private Equity 36.4% 22.4% 14.5% 7.5% 5.0% 3.9% 3.3% 2.8% 2.5% 2.3% 2.0% 1.6% 1.2% 0.8% 0.5%Global Lis ted Property 1.0% 2.0% 3.1% 4.5% 5.3% 5.8% 6.1% 6.3% 6.5% 6.6% 6.6% 6.3% 5.7% 5.3% 5.2%Unl is ted Property 1.2% 1.7% 2.6% 3.7% 4.2% 4.1% 3.9% 3.8% 3.7% 3.5% 3.2% 2.7% 2.4% 2.2% 2.1%Timberland/Natura l Resources 0.8% 1.8% 2.8% 4.6% 5.6% 6.4% 7.0% 7.5% 7.8% 8.0% 7.9% 7.6% 6.9% 6.3% 6.1%Infrastructure 1.4% 3.0% 4.4% 5.9% 6.7% 7.1% 7.5% 7.7% 7.7% 7.7% 7.7% 7.1% 6.1% 5.3% 5.1%Hedge Funds 1.0% 2.0% 3.4% 5.8% 7.2% 8.3% 9.1% 9.8% 10.5% 11.1% 11.9% 12.4% 11.8% 9.9% 7.9%Austra l ian Fixed Interest 0.4% 0.7% 1.4% 3.3% 5.0% 6.5% 7.9% 9.1% 10.3% 11.3% 13.1% 16.5% 20.4% 24.3% 27.0%International Fixed Interest 0.2% 0.3% 0.6% 2.2% 3.6% 4.7% 5.6% 6.4% 7.3% 8.1% 9.6% 12.4% 15.7% 19.3% 21.6%Cash 0.0% 0.2% 0.7% 1.5% 2.5% 3.5% 4.4% 5.2% 5.8% 6.4% 7.5% 9.4% 11.5% 13.7% 15.6%

Scenario Expected Returns95% CVAR -48.9% -42.2% -36.9% -29.7% -25.6% -23.1% -21.1% -19.6% -18.2% -17.0% -15.1% -12.0% -8.9% -5.8% -3.8%EMU dis integrates -44.6% -37.1% -31.6% -24.9% -21.2% -18.8% -17.0% -15.5% -14.2% -13.1% -11.4% -8.7% -6.0% -3.4% -1.5%Deflationary Slog -9.6% -6.3% -4.2% -2.1% -1.2% -0.7% -0.4% -0.1% 0.1% 0.3% 0.7% 1.3% 2.0% 2.6% 3.0%Moderate Growth 28.6% 25.2% 22.3% 18.4% 16.2% 14.9% 13.9% 13.1% 12.5% 11.9% 11.0% 9.6% 8.1% 6.7% 5.7%QE Proves Effective 40.5% 35.5% 31.4% 26.1% 23.2% 21.4% 20.1% 19.0% 18.1% 17.4% 16.1% 14.2% 12.2% 10.4% 9.1%

Portfolio Set 2: No Benchmark, But Including Additional Shocks Not in the Scenarios

These allocations are generated by incorporating the additional shocks outlined on the previous page…

…in addition to the eighteen scenarios

Allocation

________________________________________________

All expected returns reflect average annualized performance over the next 1-2 years time horizon. Expected returns are for asset classes only and not for any Blackstone or underlying manager funds. The asset allocation sets presented above are based on various utility maximization assumptions and assumptions about an investor’s level of risk aversion relative to absolute performance. This chart reflects outputs from BAAM’s proprietary optimization tools, which incorporate assumptions about financial market factor moves that are used for scenario and allocation re-sampling purposes. The asset class hypothetical expected returns were determined based on Blackstone's experience in and views about each asset class and not necessarily based on objective market data. This is not intended to be a prediction of how any financial markets or investments will perform in the future and actual events and conditions may differ materially from the assumptions used to establish the expected asset class returns and there is no assurance that such information has been correctly determined. Please see additional scenario analysis disclosures at the end of this presentation.

Confidential

Blackstone 20

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Lambda

0 0.5 1 2 3 4 5 6 7 8 10 15 25 50 100Expected ReturnsExpected portfol io return -0.5% -0.8% -0.9% -0.9% -0.7% -0.6% -0.5% -0.4% -0.4% -0.4% -0.3% -0.2% -0.2% -0.2% -0.2%

Optimal Asset Allocations – GroupedPubl ic Equity + Lis ted RE 8.6% 10.4% 9.2% 4.4% 1.7% 0.3% -0.4% -0.7% -0.8% -0.9% -0.9% -0.1% 0.8% 1.6% 1.8%Alternative/Other -8.8% -11.0% -10.1% -5.9% -3.1% -1.6% -0.9% -0.6% -0.5% -0.4% -0.7% -2.2% -4.7% -7.6% -9.0%Fixed Income 0.2% 0.5% 0.6% 1.5% 1.5% 1.4% 1.0% 0.8% 0.8% 0.8% 0.9% 1.6% 3.0% 5.0% 6.0%Cash 0.0% 0.2% 0.3% 0.0% -0.1% 0.0% 0.3% 0.5% 0.5% 0.6% 0.6% 0.8% 0.9% 1.1% 1.2%

Optimal Asset AllocationsAustra l ian Equities 1.2% 2.7% 3.1% 2.2% 1.5% 1.2% 0.8% 0.6% 0.5% 0.3% 0.1% 0.1% 0.1% 0.3% 0.3%Austra l ian Private Equity -6.8% -10.0% -11.7% -9.8% -6.8% -4.8% -3.5% -2.8% -2.3% -2.0% -1.5% -1.0% -0.6% -0.4% -0.3%International Equities 6.8% 6.3% 6.5% 6.3% 5.5% 4.7% 4.2% 3.8% 3.4% 3.1% 2.6% 2.0% 1.6% 1.2% 0.8%Emerging Market Equities 0.0% -0.3% -2.6% -6.5% -7.5% -7.5% -7.1% -6.8% -6.4% -6.1% -5.5% -4.1% -2.9% -1.9% -1.3%International Private Equity -4.4% -4.8% -3.7% -1.6% -1.0% -0.7% -0.5% -0.4% -0.4% -0.3% -0.2% -0.2% -0.1% -0.1% -0.1%Global Lis ted Property 0.6% 1.6% 2.2% 2.4% 2.2% 1.8% 1.7% 1.7% 1.7% 1.8% 1.8% 1.9% 1.9% 1.9% 2.0%Unl is ted Property 0.6% 0.6% 1.0% 1.3% 1.5% 1.2% 1.1% 1.0% 0.9% 0.9% 0.7% 0.6% 0.6% 0.6% 0.6%Timberland/Natura l Resources 0.4% 0.6% 1.1% 1.5% 1.7% 1.9% 1.9% 1.9% 2.0% 1.9% 1.8% 1.5% 1.2% 1.0% 0.8%Infrastructure 1.2% 2.4% 2.9% 3.0% 2.9% 2.7% 2.7% 2.7% 2.7% 2.7% 2.7% 2.5% 2.3% 1.8% 1.6%Hedge Funds 0.2% 0.3% 0.3% -0.4% -1.3% -2.1% -2.6% -3.0% -3.3% -3.5% -4.1% -5.8% -8.1% -10.6% -11.5%Austra l ian Fixed Interest 0.0% 0.3% 0.4% 0.6% 0.4% 0.2% 0.1% -0.1% -0.1% -0.2% -0.3% -0.2% 0.5% 1.3% 1.9%International Fixed Interest 0.2% 0.2% 0.2% 0.8% 1.1% 1.1% 1.0% 0.9% 0.9% 1.0% 1.2% 1.8% 2.5% 3.7% 4.0%Cash 0.0% 0.2% 0.3% 0.0% -0.1% 0.0% 0.3% 0.5% 0.5% 0.6% 0.6% 0.8% 0.9% 1.1% 1.2%

Scenario Expected Returns95% CVAR 3.3% 5.2% 5.7% 4.8% 3.5% 2.6% 2.0% 1.6% 1.3% 1.1% 0.9% 0.5% 0.3% 0.4% 0.5%EMU dis integrates 2.8% 4.0% 4.2% 3.3% 2.5% 2.0% 1.6% 1.4% 1.3% 1.2% 1.0% 0.8% 0.7% 0.8% 0.9%Deflationary Slog 0.7% 0.9% 0.4% -0.6% -1.0% -1.1% -1.1% -1.1% -1.1% -1.1% -1.0% -0.8% -0.6% -0.4% -0.2%Moderate Growth -2.0% -2.9% -3.2% -2.7% -2.0% -1.5% -1.2% -1.0% -0.9% -0.8% -0.7% -0.5% -0.4% -0.4% -0.4%QE Proves Effective -2.7% -3.8% -4.2% -3.4% -2.4% -1.8% -1.4% -1.1% -0.9% -0.8% -0.6% -0.4% -0.2% -0.2% -0.2%

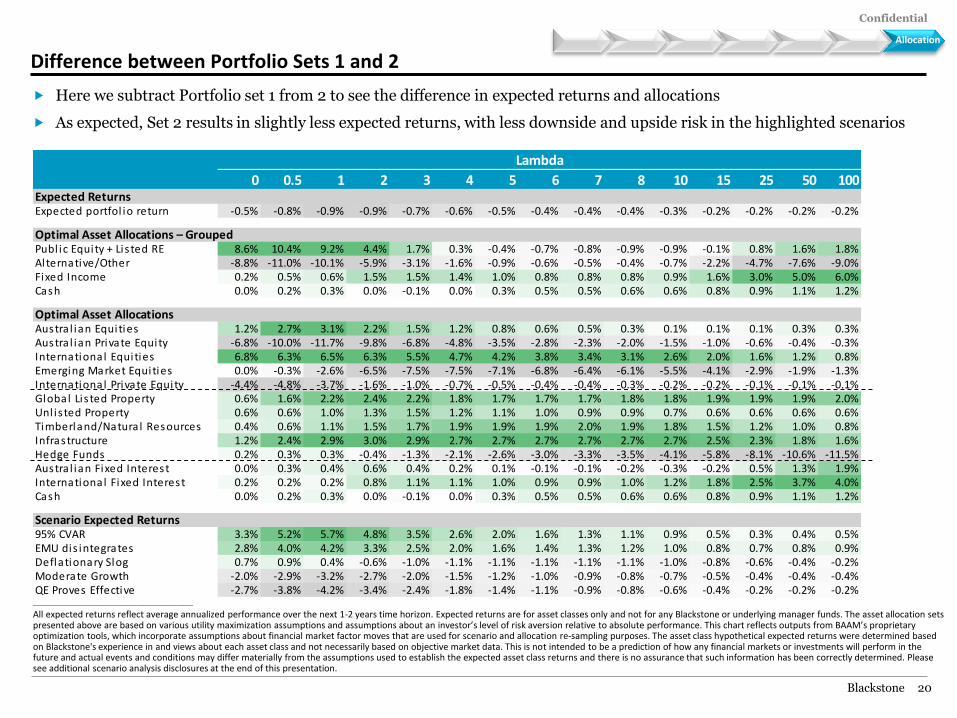

Difference between Portfolio Sets 1 and 2

Here we subtract Portfolio set 1 from 2 to see the difference in expected returns and allocations

As expected, Set 2 results in slightly less expected returns, with less downside and upside risk in the highlighted scenarios

Allocation

________________________________________________

All expected returns reflect average annualized performance over the next 1-2 years time horizon. Expected returns are for asset classes only and not for any Blackstone or underlying manager funds. The asset allocation sets presented above are based on various utility maximization assumptions and assumptions about an investor’s level of risk aversion relative to absolute performance. This chart reflects outputs from BAAM’s proprietary optimization tools, which incorporate assumptions about financial market factor moves that are used for scenario and allocation re-sampling purposes. The asset class hypothetical expected returns were determined based on Blackstone's experience in and views about each asset class and not necessarily based on objective market data. This is not intended to be a prediction of how any financial markets or investments will perform in the future and actual events and conditions may differ materially from the assumptions used to establish the expected asset class returns and there is no assurance that such information has been correctly determined. Please see additional scenario analysis disclosures at the end of this presentation.

Confidential

Blackstone 21

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Scenario Lambda

Probability 0 0.5 1 2 3 4 5 6 7 8 10 15 25 50 1002% Double Dip Heavy -55.3% -47.8% -41.6% -33.5% -29.1% -26.2% -24.1% -22.4% -20.9% -19.6% -17.5% -14.1% -10.6% -7.2% -4.9%

3% EMU disintegrates -44.6% -37.1% -31.6% -24.9% -21.2% -18.8% -17.0% -15.5% -14.2% -13.1% -11.4% -8.7% -6.0% -3.4% -1.5%

2% China Bust, DM Down -43.2% -39.3% -34.9% -28.3% -24.4% -22.0% -20.2% -18.7% -17.5% -16.4% -14.6% -11.6% -8.6% -5.7% -3.8%

10% Deflationary Slog -9.6% -6.3% -4.2% -2.1% -1.2% -0.7% -0.4% -0.1% 0.1% 0.3% 0.7% 1.3% 2.0% 2.6% 3.0%

7% Double Dip Light -24.0% -19.9% -17.0% -13.6% -11.7% -10.5% -9.5% -8.8% -8.1% -7.5% -6.5% -4.9% -3.2% -1.6% -0.6%

2% Stagflation Fears -13.2% -9.8% -7.2% -4.2% -2.7% -1.8% -1.1% -0.7% -0.3% -0.1% 0.1% 0.0% -0.3% -0.6% -0.6%

7% Greece exit triggers chaos -13.1% -10.5% -8.8% -6.9% -5.8% -5.1% -4.5% -4.0% -3.6% -3.2% -2.6% -1.5% -0.4% 0.7% 1.4%

2% Inflationary Overheating -4.8% -2.3% -0.3% 1.9% 2.9% 3.5% 3.9% 4.2% 4.4% 4.4% 4.3% 3.6% 2.7% 1.8% 1.4%

8% Europe Worsens -8.2% -6.6% -5.4% -4.0% -3.2% -2.7% -2.3% -2.0% -1.7% -1.5% -1.0% -0.3% 0.5% 1.3% 1.7%

6% Financial Healing 13.9% 12.7% 11.6% 9.9% 8.9% 8.2% 7.7% 7.3% 6.9% 6.6% 6.0% 5.0% 3.9% 2.8% 2.1%

16% Moderate Growth 28.6% 25.2% 22.3% 18.4% 16.2% 14.9% 13.9% 13.1% 12.5% 11.9% 11.0% 9.6% 8.1% 6.7% 5.7%

13% QE Proves Effective 40.5% 35.5% 31.4% 26.1% 23.2% 21.4% 20.1% 19.0% 18.1% 17.4% 16.1% 14.2% 12.2% 10.4% 9.1%

5% Global Decoupling 36.0% 33.2% 30.4% 26.1% 23.5% 21.7% 20.3% 19.2% 18.2% 17.3% 16.0% 13.8% 11.6% 9.4% 7.9%

3% Germany Leaves Euro 12.1% 14.3% 15.4% 15.9% 15.6% 15.0% 14.5% 13.9% 13.4% 12.9% 12.2% 10.9% 9.7% 8.5% 7.7%

3% Beautiful Inflation 40.6% 34.2% 29.9% 25.2% 22.7% 21.1% 19.8% 18.8% 17.9% 17.2% 15.9% 13.9% 11.8% 9.8% 8.5%

5% China Bust, DM Up 22.3% 15.8% 12.5% 9.7% 8.6% 7.9% 7.5% 7.1% 6.7% 6.4% 6.1% 5.6% 5.2% 4.8% 4.4%

5% Europe Improves 49.7% 42.6% 36.9% 29.8% 25.9% 23.4% 21.6% 20.2% 19.0% 17.9% 16.3% 13.8% 11.2% 8.8% 7.0%

1% New Economy, Zero Inflation 56.0% 47.0% 39.8% 30.9% 26.2% 23.5% 21.5% 20.0% 18.8% 17.7% 16.2% 13.9% 11.7% 9.6% 8.1%

100% Expected portfolio return 10.3% 9.5% 8.8% 7.8% 7.2% 6.8% 6.5% 6.2% 6.0% 5.9% 5.6% 5.2% 4.8% 4.3% 4.1%

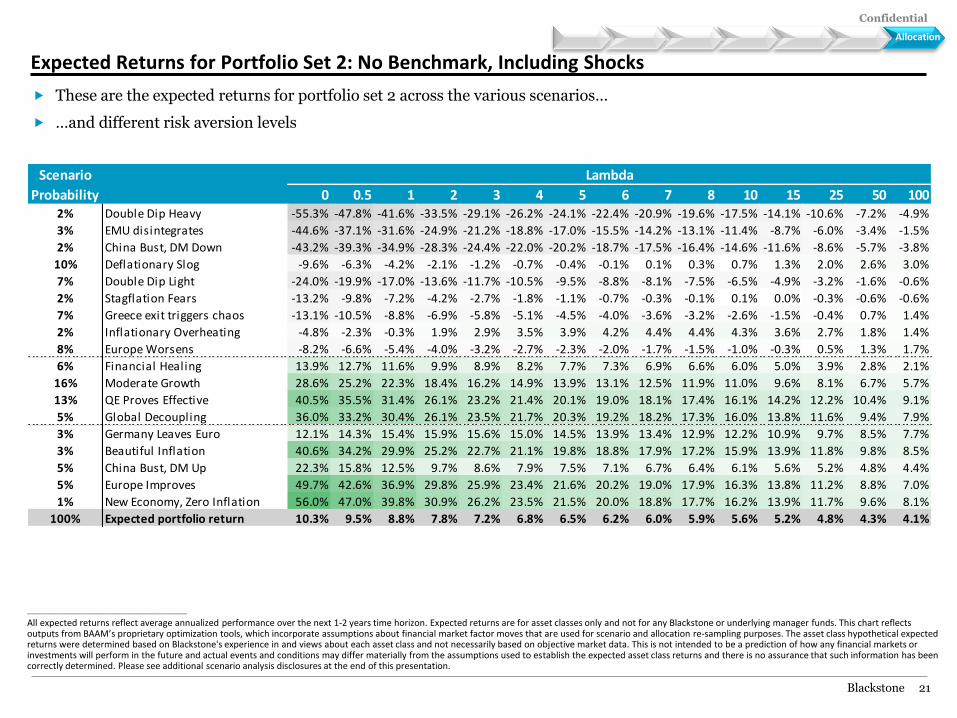

Expected Returns for Portfolio Set 2: No Benchmark, Including Shocks

These are the expected returns for portfolio set 2 across the various scenarios…

…and different risk aversion levels

Allocation

________________________________________________

All expected returns reflect average annualized performance over the next 1-2 years time horizon. Expected returns are for asset classes only and not for any Blackstone or underlying manager funds. This chart reflects outputs from BAAM’s proprietary optimization tools, which incorporate assumptions about financial market factor moves that are used for scenario and allocation re-sampling purposes. The asset class hypothetical expected returns were determined based on Blackstone's experience in and views about each asset class and not necessarily based on objective market data. This is not intended to be a prediction of how any financial markets or investments will perform in the future and actual events and conditions may differ materially from the assumptions used to establish the expected asset class returns and there is no assurance that such information has been correctly determined. Please see additional scenario analysis disclosures at the end of this presentation.

Confidential

Blackstone 22

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Scenario Lambda

Probability 0 0.5 1 2 3 4 5 6 7 8 10 15 25 50 1002% Double Dip Heavy -55.3% -59.2% -58.9% -56.0% -54.4% -53.8% -53.2% -52.5% -51.5% -50.4% -48.3% -44.1% -38.7% -33.2% -29.3%

3% EMU disintegrates -44.6% -44.0% -41.6% -37.3% -34.8% -33.0% -31.5% -30.0% -28.4% -27.0% -24.5% -20.1% -15.0% -9.1% -3.9%

2% China Bust, DM Down -43.2% -47.0% -47.1% -44.2% -42.3% -41.3% -40.5% -39.7% -38.8% -37.8% -35.8% -31.9% -27.0% -21.9% -18.4%

10% Deflationary Slog -9.6% -6.5% -4.3% -2.2% -1.2% -0.7% -0.4% -0.1% 0.1% 0.3% 0.7% 1.3% 2.0% 2.6% 3.0%

7% Double Dip Light -24.0% -21.9% -20.0% -17.2% -15.8% -14.8% -14.1% -13.4% -12.7% -12.0% -10.8% -8.5% -5.8% -2.9% -0.9%

2% Stagflation Fears -13.2% -10.3% -7.8% -4.6% -2.9% -1.9% -1.2% -0.7% -0.3% -0.1% 0.1% 0.0% -0.3% -0.8% -1.0%

7% Greece exit triggers chaos -13.1% -11.1% -9.6% -7.8% -6.8% -6.1% -5.5% -5.0% -4.5% -4.0% -3.2% -1.8% -0.4% 0.7% 1.4%

2% Inflationary Overheating -4.8% -2.3% -0.3% 1.9% 2.9% 3.5% 3.9% 4.2% 4.4% 4.4% 4.3% 3.6% 2.7% 1.8% 1.4%

8% Europe Worsens -8.2% -6.8% -5.7% -4.3% -3.5% -3.0% -2.6% -2.3% -1.9% -1.7% -1.2% -0.3% 0.5% 1.3% 1.7%

6% Financial Healing 13.9% 12.7% 11.6% 9.9% 8.9% 8.2% 7.7% 7.3% 6.9% 6.6% 6.0% 5.0% 3.9% 2.8% 2.1%

16% Moderate Growth 28.6% 25.2% 22.3% 18.4% 16.2% 14.9% 13.9% 13.1% 12.5% 11.9% 11.0% 9.6% 8.1% 6.7% 5.7%

13% QE Proves Effective 40.5% 35.5% 31.4% 26.1% 23.2% 21.4% 20.1% 19.0% 18.1% 17.4% 16.1% 14.2% 12.2% 10.4% 9.1%

5% Global Decoupling 36.0% 33.2% 30.4% 26.1% 23.5% 21.7% 20.3% 19.2% 18.2% 17.3% 16.0% 13.8% 11.6% 9.4% 7.9%

3% Germany Leaves Euro 12.1% 14.3% 15.4% 15.9% 15.6% 15.0% 14.5% 13.9% 13.4% 12.9% 12.2% 10.9% 9.7% 8.5% 7.7%

3% Beautiful Inflation 40.6% 34.2% 29.9% 25.2% 22.7% 21.1% 19.8% 18.8% 17.9% 17.2% 15.9% 13.9% 11.8% 9.8% 8.5%

5% China Bust, DM Up 22.3% 15.8% 12.5% 9.7% 8.6% 7.9% 7.5% 7.1% 6.7% 6.4% 6.1% 5.6% 5.2% 4.8% 4.4%

5% Europe Improves 49.7% 42.6% 36.9% 29.8% 25.9% 23.4% 21.6% 20.2% 19.0% 17.9% 16.3% 13.8% 11.2% 8.8% 7.0%

1% New Economy, Zero Inflation 56.0% 47.0% 39.8% 30.9% 26.2% 23.5% 21.5% 20.0% 18.8% 17.7% 16.2% 13.9% 11.7% 9.6% 8.1%

100% Expected portfolio utility 10.3% 8.7% 7.6% 6.3% 5.5% 5.0% 4.6% 4.4% 4.2% 4.0% 3.8% 3.6% 3.4% 3.2% 3.2%

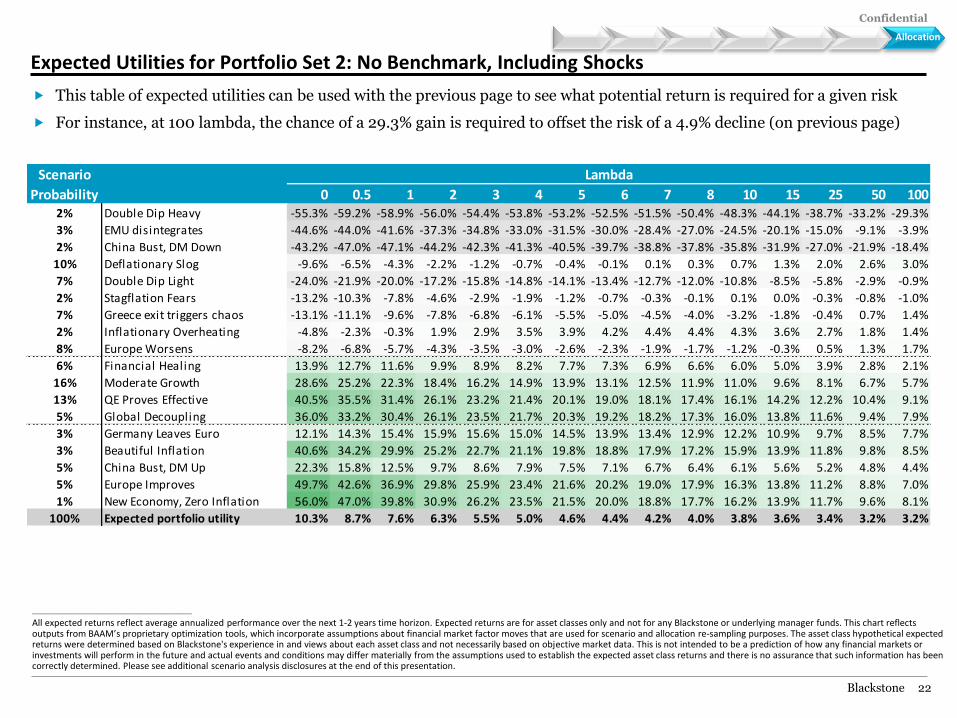

Expected Utilities for Portfolio Set 2: No Benchmark, Including Shocks

This table of expected utilities can be used with the previous page to see what potential return is required for a given risk

For instance, at 100 lambda, the chance of a 29.3% gain is required to offset the risk of a 4.9% decline (on previous page)

Allocation

________________________________________________

All expected returns reflect average annualized performance over the next 1-2 years time horizon. Expected returns are for asset classes only and not for any Blackstone or underlying manager funds. This chart reflects outputs from BAAM’s proprietary optimization tools, which incorporate assumptions about financial market factor moves that are used for scenario and allocation re-sampling purposes. The asset class hypothetical expected returns were determined based on Blackstone's experience in and views about each asset class and not necessarily based on objective market data. This is not intended to be a prediction of how any financial markets or investments will perform in the future and actual events and conditions may differ materially from the assumptions used to establish the expected asset class returns and there is no assurance that such information has been correctly determined. Please see additional scenario analysis disclosures at the end of this presentation.

Confidential

Blackstone 23

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Lambda

0 0.5 1 2 3 4 5 6 7 8 10 15 25 50 100Expected ReturnsExpected portfol io return 10.3% 9.8% 9.4% 8.7% 8.3% 8.0% 7.8% 7.7% 7.5% 7.4% 7.3% 7.1% 6.8% 6.6% 6.4%Expected benchmark return 6.1% 6.1% 6.1% 6.1% 6.1% 6.1% 6.1% 6.1% 6.1% 6.1% 6.1% 6.1% 6.1% 6.1% 6.1%Expected excess return 4.3% 3.8% 3.3% 2.6% 2.2% 1.9% 1.7% 1.6% 1.5% 1.4% 1.2% 1.0% 0.8% 0.5% 0.3%

Optimal Asset Allocations – GroupedPubl ic Equity + Lis ted RE 23.8% 33.9% 40.4% 47.8% 51.5% 53.4% 54.3% 54.8% 55.0% 55.1% 55.1% 54.7% 53.7% 52.6% 52.6%Alternative/Other 75.6% 65.2% 58.3% 49.5% 44.7% 41.9% 40.3% 39.4% 38.7% 38.2% 37.4% 36.4% 35.7% 34.1% 31.9%Fixed Income 0.6% 0.8% 1.1% 2.2% 3.0% 3.6% 4.1% 4.5% 4.8% 5.1% 5.7% 6.6% 7.7% 9.5% 11.2%Cash 0.0% 0.1% 0.2% 0.5% 0.8% 1.1% 1.2% 1.4% 1.5% 1.6% 1.8% 2.3% 2.9% 3.7% 4.2%

Optimal Asset AllocationsAustra l ian Equities 3.6% 7.0% 9.2% 12.3% 14.2% 15.3% 16.1% 16.6% 17.1% 17.6% 18.2% 19.0% 19.7% 20.4% 21.5%Austra l ian Private Equity 34.8% 31.8% 27.9% 21.4% 16.9% 14.1% 12.3% 11.1% 10.1% 9.4% 8.4% 6.9% 5.7% 4.8% 4.1%International Equities 10.4% 13.4% 15.7% 18.3% 19.6% 20.4% 20.7% 21.0% 21.0% 20.9% 20.7% 20.3% 19.3% 18.4% 18.0%Emerging Market Equities 8.8% 12.0% 13.3% 13.8% 13.5% 13.0% 12.3% 11.7% 11.2% 10.7% 9.9% 8.5% 7.1% 5.6% 4.7%International Private Equity 36.4% 26.9% 21.1% 15.1% 12.3% 10.9% 10.0% 9.3% 8.9% 8.6% 8.1% 7.3% 6.5% 5.6% 4.7%Global Lis ted Property 1.0% 1.7% 2.2% 3.3% 4.2% 4.8% 5.2% 5.5% 5.7% 5.9% 6.3% 6.9% 7.6% 8.3% 8.4%Unl is ted Property 1.2% 1.6% 2.3% 3.2% 3.8% 4.1% 4.3% 4.5% 4.7% 4.8% 5.0% 5.1% 5.3% 5.1% 4.8%Timberland/Natura l Resources 0.8% 1.3% 1.9% 2.7% 3.3% 3.7% 4.0% 4.3% 4.5% 4.6% 4.9% 5.4% 5.9% 6.2% 6.3%Infrastructure 1.4% 2.2% 3.1% 4.1% 4.7% 5.0% 5.4% 5.6% 5.8% 6.0% 6.2% 6.5% 6.9% 7.1% 6.9%Hedge Funds 1.0% 1.3% 1.9% 3.0% 3.6% 4.1% 4.4% 4.6% 4.7% 4.8% 4.9% 5.1% 5.3% 5.4% 5.0%Austra l ian Fixed Interest 0.4% 0.5% 0.8% 1.4% 1.9% 2.3% 2.5% 2.7% 2.9% 3.1% 3.5% 4.1% 4.8% 5.7% 6.6%International Fixed Interest 0.2% 0.2% 0.3% 0.8% 1.1% 1.3% 1.6% 1.7% 1.9% 2.0% 2.2% 2.5% 3.0% 3.8% 4.6%Cash 0.0% 0.1% 0.2% 0.5% 0.8% 1.1% 1.2% 1.4% 1.5% 1.6% 1.8% 2.3% 2.9% 3.7% 4.2%

Scenario Expected Excess Returns95% CVAR -30.0% -25.2% -21.6% -16.8% -14.0% -12.3% -11.1% -10.3% -9.6% -9.1% -8.3% -6.9% -5.4% -3.8% -2.6%EMU dis integrates -28.7% -23.9% -20.4% -15.9% -13.4% -11.8% -10.7% -10.0% -9.4% -8.8% -8.1% -6.8% -5.3% -3.7% -2.5%Deflationary Slog -8.0% -5.8% -4.5% -3.1% -2.5% -2.1% -1.9% -1.8% -1.8% -1.7% -1.7% -1.5% -1.4% -1.2% -1.0%Moderate Growth 15.2% 13.1% 11.3% 8.7% 7.1% 6.2% 5.5% 5.0% 4.6% 4.3% 3.9% 3.2% 2.4% 1.6% 1.0%QE Proves Effective 21.4% 18.3% 15.7% 12.2% 10.0% 8.7% 7.8% 7.1% 6.6% 6.2% 5.6% 4.6% 3.6% 2.5% 1.7%

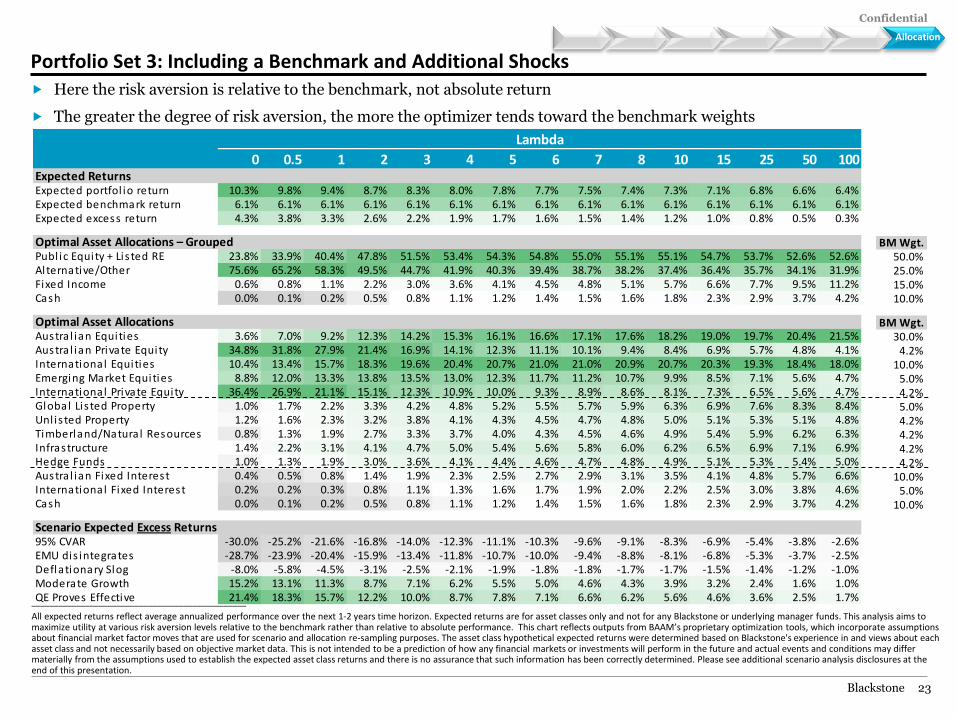

Portfolio Set 3: Including a Benchmark and Additional Shocks

Here the risk aversion is relative to the benchmark, not absolute return

The greater the degree of risk aversion, the more the optimizer tends toward the benchmark weights

Evaluation Allocation

BM Wgt.50.0%25.0%15.0%10.0%

BM Wgt.30.0%

4.2%10.0%

5.0%4.2%5.0%4.2%4.2%4.2%4.2%

10.0%5.0%

10.0%

________________________________________________

All expected returns reflect average annualized performance over the next 1-2 years time horizon. Expected returns are for asset classes only and not for any Blackstone or underlying manager funds. This analysis aims to maximize utility at various risk aversion levels relative to the benchmark rather than relative to absolute performance. This chart reflects outputs from BAAM’s proprietary optimization tools, which incorporate assumptions about financial market factor moves that are used for scenario and allocation re-sampling purposes. The asset class hypothetical expected returns were determined based on Blackstone's experience in and views about each asset class and not necessarily based on objective market data. This is not intended to be a prediction of how any financial markets or investments will perform in the future and actual events and conditions may differ materially from the assumptions used to establish the expected asset class returns and there is no assurance that such information has been correctly determined. Please see additional scenario analysis disclosures at the end of this presentation.

Confidential

Blackstone 24

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Lambda

0 0.5 1 2 3 4 5 6 7 8 10 15 25 50 100Expected ReturnsExpected portfol io return 0.0% 0.3% 0.6% 0.9% 1.1% 1.2% 1.3% 1.4% 1.5% 1.6% 1.7% 1.9% 2.1% 2.2% 2.3%

Optimal Asset Allocations – GroupedPubl ic Equity + Lis ted RE 0.0% -4.5% -6.2% -3.9% 0.3% 4.6% 8.5% 11.9% 14.9% 17.4% 21.3% 26.9% 31.7% 35.8% 39.3%Alternative/Other 0.0% 4.9% 7.6% 8.4% 6.9% 5.4% 4.0% 3.0% 2.2% 1.7% 1.4% 2.5% 5.3% 8.3% 9.3%Fixed Income 0.0% -0.3% -0.9% -3.4% -5.6% -7.6% -9.4% -11.1% -12.7% -14.3% -17.0% -22.3% -28.4% -34.1% -37.3%Cash 0.0% -0.1% -0.5% -1.0% -1.7% -2.4% -3.2% -3.8% -4.4% -4.9% -5.7% -7.1% -8.6% -10.0% -11.4%

Optimal Asset AllocationsAustra l ian Equities 0.0% -1.1% -1.3% 0.2% 1.9% 3.4% 4.9% 6.2% 7.5% 8.6% 10.4% 12.8% 15.1% 17.2% 19.4%Austra l ian Private Equity 0.0% 2.3% 5.0% 7.7% 8.0% 7.4% 6.8% 6.3% 6.0% 5.6% 5.1% 4.3% 3.8% 3.5% 3.2%International Equities 0.0% -0.9% -1.0% -0.1% 1.8% 3.7% 5.2% 6.5% 7.7% 8.6% 9.9% 11.7% 12.8% 13.6% 14.6%Emerging Market Equities 0.0% -2.1% -3.0% -2.9% -2.3% -1.4% -0.6% 0.0% 0.5% 0.9% 1.4% 1.8% 1.9% 1.9% 2.2%International Private Equity 0.0% 4.5% 6.7% 7.7% 7.4% 7.0% 6.7% 6.5% 6.4% 6.3% 6.1% 5.8% 5.3% 4.8% 4.2%Global Lis ted Property 0.0% -0.4% -0.9% -1.2% -1.1% -1.0% -0.9% -0.9% -0.8% -0.7% -0.3% 0.6% 1.9% 3.0% 3.2%Unl is ted Property 0.0% -0.1% -0.3% -0.5% -0.5% 0.0% 0.4% 0.7% 1.0% 1.3% 1.8% 2.4% 2.8% 2.9% 2.7%Timberland/Natura l Resources 0.0% -0.4% -1.0% -1.9% -2.3% -2.7% -3.0% -3.2% -3.4% -3.3% -3.0% -2.2% -1.0% 0.0% 0.2%Infrastructure 0.0% -0.7% -1.3% -1.8% -2.0% -2.1% -2.1% -2.1% -1.9% -1.8% -1.5% -0.5% 0.8% 1.8% 1.9%Hedge Funds 0.0% -0.7% -1.5% -2.8% -3.6% -4.2% -4.7% -5.3% -5.8% -6.3% -7.0% -7.3% -6.5% -4.6% -2.8%Austra l ian Fixed Interest 0.0% -0.2% -0.6% -1.9% -3.0% -4.3% -5.4% -6.4% -7.4% -8.2% -9.6% -12.4% -15.6% -18.6% -20.4%International Fixed Interest 0.0% 0.0% -0.3% -1.5% -2.5% -3.3% -4.0% -4.7% -5.4% -6.1% -7.4% -9.9% -12.8% -15.6% -16.9%Cash 0.0% -0.1% -0.5% -1.0% -1.7% -2.4% -3.2% -3.8% -4.4% -4.9% -5.7% -7.1% -8.6% -10.0% -11.4%

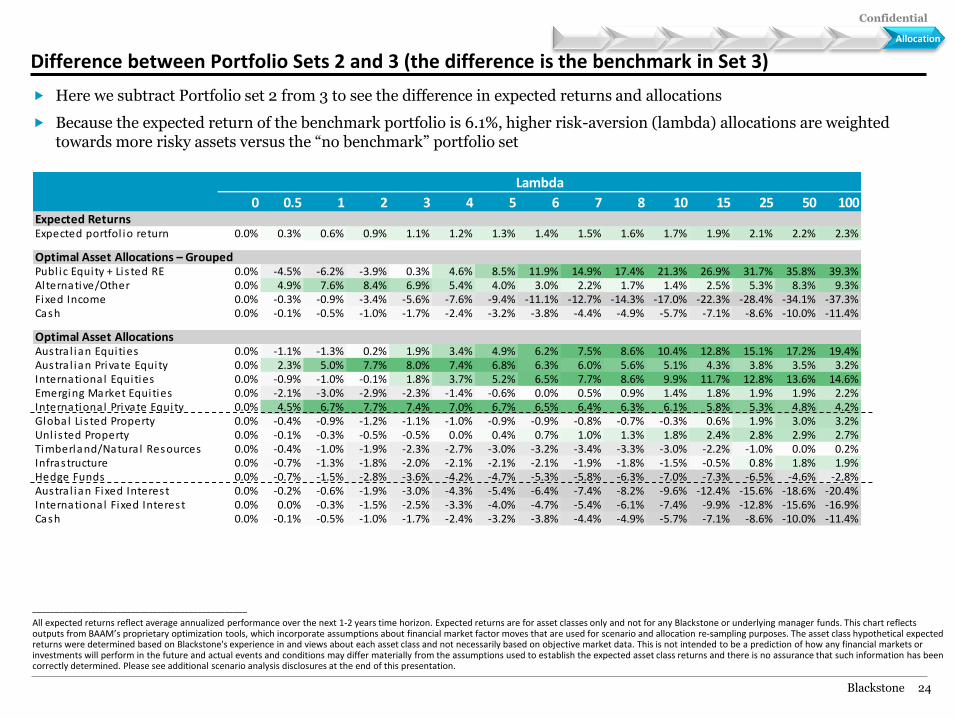

Difference between Portfolio Sets 2 and 3 (the difference is the benchmark in Set 3)

Here we subtract Portfolio set 2 from 3 to see the difference in expected returns and allocations

Because the expected return of the benchmark portfolio is 6.1%, higher risk-aversion (lambda) allocations are weighted towards more risky assets versus the “no benchmark” portfolio set

Evaluation Allocation

________________________________________________

All expected returns reflect average annualized performance over the next 1-2 years time horizon. Expected returns are for asset classes only and not for any Blackstone or underlying manager funds. This chart reflects outputs from BAAM’s proprietary optimization tools, which incorporate assumptions about financial market factor moves that are used for scenario and allocation re-sampling purposes. The asset class hypothetical expected returns were determined based on Blackstone's experience in and views about each asset class and not necessarily based on objective market data. This is not intended to be a prediction of how any financial markets or investments will perform in the future and actual events and conditions may differ materially from the assumptions used to establish the expected asset class returns and there is no assurance that such information has been correctly determined. Please see additional scenario analysis disclosures at the end of this presentation.

Confidential

Blackstone 25

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Lambda

0 0.5 1 2 3 4 5 6 7 8 10 15 25 50 100Expected ReturnsExpected portfol io return 11.3% 10.7% 10.3% 9.8% 9.5% 9.3% 9.1% 9.0% 8.9% 8.9% 8.7% 8.5% 8.2% 7.9% 7.7%Expected benchmark return 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5% 6.5%Expected excess return 4.7% 4.2% 3.7% 3.2% 2.9% 2.7% 2.6% 2.5% 2.4% 2.3% 2.2% 2.0% 1.7% 1.4% 1.1%

Optimal Asset Allocations – GroupedPubl ic Equity + Lis ted RE 28.2% 39.3% 46.5% 54.9% 58.9% 60.6% 61.5% 61.9% 62.2% 62.4% 62.6% 62.5% 61.8% 60.7% 60.0%Alternative/Other 71.2% 60.0% 52.6% 43.8% 39.5% 37.4% 36.1% 35.4% 34.9% 34.5% 34.0% 33.5% 33.3% 32.7% 31.7%Fixed Income 0.6% 0.7% 0.8% 1.2% 1.5% 1.8% 2.1% 2.3% 2.5% 2.6% 2.9% 3.3% 3.9% 4.9% 6.0%Cash 0.0% 0.0% 0.1% 0.1% 0.1% 0.2% 0.3% 0.3% 0.4% 0.5% 0.5% 0.8% 1.1% 1.7% 2.3%

Optimal Asset AllocationsAustra l ian Equities 2.2% 4.0% 5.4% 6.9% 7.8% 8.3% 8.6% 8.9% 9.2% 9.4% 9.8% 10.6% 11.6% 13.0% 14.9%Austra l ian Private Equity 23.0% 20.8% 18.2% 14.3% 12.2% 11.1% 10.4% 9.8% 9.4% 9.1% 8.5% 7.6% 6.7% 5.8% 5.1%International Equities 16.6% 21.7% 24.8% 28.3% 29.6% 30.0% 30.0% 29.9% 29.7% 29.5% 29.1% 27.8% 25.8% 23.4% 21.6%Emerging Market Equities 8.0% 10.8% 12.1% 13.2% 13.4% 13.2% 12.9% 12.6% 12.3% 12.0% 11.4% 10.5% 9.4% 8.5% 8.0%International Private Equity 45.0% 33.3% 26.1% 18.3% 14.4% 12.4% 11.1% 10.3% 9.7% 9.2% 8.4% 7.3% 6.2% 5.0% 4.1%Global Lis ted Property 1.4% 2.8% 4.3% 6.5% 8.1% 9.1% 9.9% 10.5% 11.0% 11.5% 12.3% 13.6% 14.9% 15.7% 15.5%Unl is ted Property 0.4% 1.0% 1.4% 1.7% 1.9% 2.0% 2.1% 2.2% 2.3% 2.4% 2.6% 2.9% 3.3% 3.6% 3.8%Timberland/Natura l Resources 0.4% 0.8% 1.3% 1.9% 2.3% 2.5% 2.7% 2.8% 3.0% 3.1% 3.3% 3.8% 4.6% 5.2% 5.6%Infrastructure 0.8% 1.5% 2.1% 2.8% 3.1% 3.3% 3.5% 3.6% 3.8% 3.9% 4.2% 4.8% 5.4% 6.1% 6.4%Hedge Funds 1.6% 2.5% 3.6% 4.8% 5.5% 6.0% 6.3% 6.6% 6.7% 6.8% 6.9% 7.0% 7.1% 7.0% 6.8%Austra l ian Fixed Interest 0.4% 0.5% 0.6% 0.9% 1.1% 1.3% 1.6% 1.7% 1.8% 1.9% 2.1% 2.3% 2.7% 3.4% 4.0%International Fixed Interest 0.2% 0.2% 0.2% 0.3% 0.4% 0.5% 0.6% 0.6% 0.7% 0.7% 0.8% 0.9% 1.1% 1.5% 2.0%Cash 0.0% 0.0% 0.1% 0.1% 0.1% 0.2% 0.3% 0.3% 0.4% 0.5% 0.5% 0.8% 1.1% 1.7% 2.3%

Scenario Expected Excess Returns95% CVAR -28.6% -22.5% -18.1% -12.8% -10.0% -8.7% -7.9% -7.3% -6.8% -6.4% -5.8% -4.8% -3.8% -3.0% -2.4%EMU dis integrates -29.3% -23.4% -19.1% -14.1% -11.5% -9.9% -8.9% -8.2% -7.6% -7.1% -6.4% -5.2% -3.9% -2.4% -1.5%Deflationary Slog -11.2% -8.9% -7.4% -5.8% -5.1% -4.7% -4.4% -4.2% -4.1% -4.0% -3.9% -3.6% -3.2% -2.7% -2.3%Moderate Growth 13.5% 11.2% 9.5% 7.3% 6.1% 5.4% 4.9% 4.6% 4.3% 4.1% 3.8% 3.2% 2.5% 1.9% 1.4%QE Proves Effective 22.1% 18.5% 15.8% 12.5% 10.8% 9.8% 9.1% 8.6% 8.2% 7.8% 7.3% 6.4% 5.4% 4.3% 3.4%

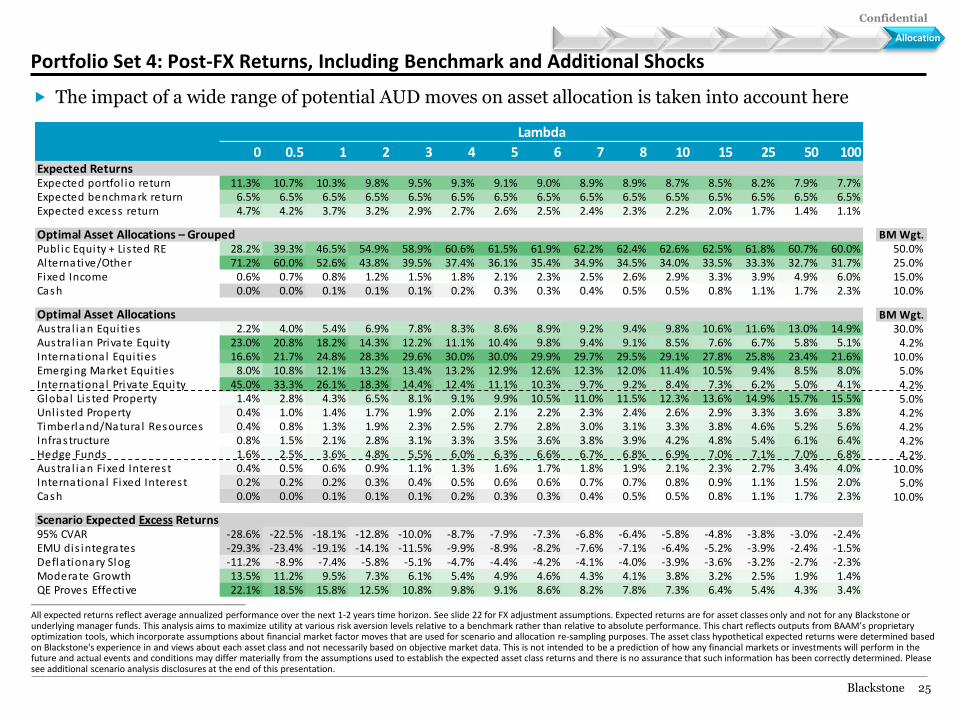

Portfolio Set 4: Post-FX Returns, Including Benchmark and Additional Shocks

The impact of a wide range of potential AUD moves on asset allocation is taken into account here

Allocation

BM Wgt.50.0%25.0%15.0%10.0%

BM Wgt.30.0%

4.2%10.0%

5.0%4.2%5.0%4.2%4.2%4.2%4.2%

10.0%5.0%

10.0%

________________________________________________

All expected returns reflect average annualized performance over the next 1-2 years time horizon. See slide 22 for FX adjustment assumptions. Expected returns are for asset classes only and not for any Blackstone or underlying manager funds. This analysis aims to maximize utility at various risk aversion levels relative to a benchmark rather than relative to absolute performance. This chart reflects outputs from BAAM’s proprietary optimization tools, which incorporate assumptions about financial market factor moves that are used for scenario and allocation re-sampling purposes. The asset class hypothetical expected returns were determined based on Blackstone's experience in and views about each asset class and not necessarily based on objective market data. This is not intended to be a prediction of how any financial markets or investments will perform in the future and actual events and conditions may differ materially from the assumptions used to establish the expected asset class returns and there is no assurance that such information has been correctly determined. Please see additional scenario analysis disclosures at the end of this presentation.

Confidential

Blackstone 26

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Lambda

0 0.5 1 2 3 4 5 6 7 8 10 15 25 50 100Expected ReturnsExpected portfol io return 0.9% 0.9% 0.9% 1.1% 1.2% 1.3% 1.3% 1.4% 1.4% 1.4% 1.4% 1.4% 1.4% 1.4% 1.3%Expected benchmark return 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5%Expected excess return 0.4% 0.4% 0.4% 0.6% 0.7% 0.8% 0.9% 0.9% 0.9% 0.9% 1.0% 1.0% 0.9% 0.9% 0.8%

Optimal Asset Allocations – GroupedPubl ic Equity + Lis ted RE 4.4% 5.4% 6.1% 7.1% 7.4% 7.2% 7.1% 7.2% 7.2% 7.3% 7.5% 7.8% 8.1% 8.1% 7.4%Alternative/Other -4.4% -5.3% -5.7% -5.7% -5.2% -4.6% -4.2% -4.0% -3.8% -3.7% -3.4% -2.9% -2.4% -1.4% -0.2%Fixed Income 0.0% -0.1% -0.3% -1.0% -1.5% -1.8% -1.9% -2.1% -2.3% -2.5% -2.8% -3.3% -3.9% -4.6% -5.2%Cash 0.0% 0.0% -0.1% -0.4% -0.7% -0.9% -1.0% -1.0% -1.1% -1.1% -1.3% -1.5% -1.8% -2.0% -2.0%

Optimal Asset AllocationsAustra l ian Equities -1.4% -2.9% -3.9% -5.4% -6.4% -7.0% -7.5% -7.7% -7.9% -8.1% -8.3% -8.4% -8.0% -7.3% -6.6%Austra l ian Private Equity -11.8% -11.0% -9.7% -7.1% -4.7% -3.0% -1.9% -1.2% -0.7% -0.4% 0.1% 0.7% 1.0% 1.0% 1.0%International Equities 6.2% 8.3% 9.1% 10.0% 10.0% 9.7% 9.3% 8.9% 8.7% 8.6% 8.3% 7.6% 6.5% 5.0% 3.6%Emerging Market Equities -0.8% -1.2% -1.2% -0.6% -0.1% 0.2% 0.6% 0.9% 1.1% 1.3% 1.5% 1.9% 2.4% 3.0% 3.4%International Private Equity 8.6% 6.4% 4.9% 3.1% 2.1% 1.5% 1.2% 0.9% 0.8% 0.6% 0.3% 0.0% -0.3% -0.5% -0.6%Global Lis ted Property 0.4% 1.2% 2.1% 3.1% 3.9% 4.3% 4.7% 5.0% 5.3% 5.5% 6.0% 6.7% 7.3% 7.4% 7.1%Unl is ted Property -0.8% -0.6% -0.9% -1.5% -1.9% -2.1% -2.2% -2.3% -2.4% -2.4% -2.4% -2.2% -2.0% -1.6% -1.1%Timberland/Natura l Resources -0.4% -0.5% -0.6% -0.8% -1.0% -1.2% -1.3% -1.4% -1.5% -1.5% -1.6% -1.5% -1.3% -1.0% -0.7%Infrastructure -0.6% -0.7% -1.0% -1.3% -1.6% -1.7% -1.9% -2.0% -2.0% -2.0% -1.9% -1.8% -1.5% -0.9% -0.6%Hedge Funds 0.6% 1.1% 1.7% 1.8% 1.9% 1.9% 1.9% 2.0% 2.0% 2.0% 2.0% 1.9% 1.8% 1.7% 1.7%Austra l ian Fixed Interest 0.0% -0.1% -0.2% -0.5% -0.8% -0.9% -1.0% -1.0% -1.1% -1.2% -1.4% -1.8% -2.0% -2.3% -2.6%International Fixed Interest 0.0% 0.0% -0.1% -0.4% -0.7% -0.8% -1.0% -1.1% -1.2% -1.3% -1.4% -1.6% -1.8% -2.3% -2.7%Cash 0.0% 0.0% -0.1% -0.4% -0.7% -0.9% -1.0% -1.0% -1.1% -1.1% -1.3% -1.5% -1.8% -2.0% -2.0%

Scenario Expected Excess Returns95% CVAR 1.4% 2.7% 3.5% 4.0% 4.0% 3.6% 3.2% 3.0% 2.8% 2.7% 2.5% 2.1% 1.6% 0.8% 0.2%EMU dis integrates -0.6% 0.6% 1.3% 1.8% 1.9% 1.9% 1.8% 1.8% 1.7% 1.7% 1.7% 1.6% 1.4% 1.3% 1.1%Deflationary Slog -3.3% -3.0% -2.9% -2.7% -2.6% -2.6% -2.5% -2.4% -2.3% -2.3% -2.2% -2.1% -1.8% -1.6% -1.3%Moderate Growth -1.7% -1.9% -1.8% -1.5% -1.1% -0.8% -0.6% -0.4% -0.3% -0.2% -0.1% 0.0% 0.1% 0.3% 0.4%QE Proves Effective 0.7% 0.2% 0.0% 0.4% 0.8% 1.1% 1.3% 1.4% 1.5% 1.6% 1.7% 1.8% 1.8% 1.8% 1.7%

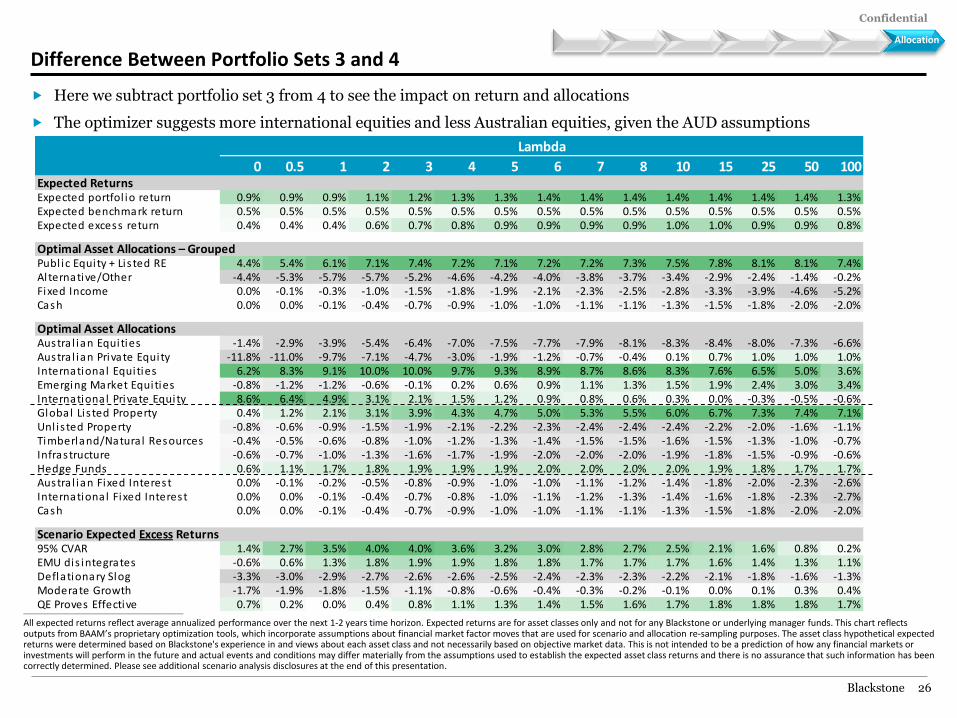

Difference Between Portfolio Sets 3 and 4

Here we subtract portfolio set 3 from 4 to see the impact on return and allocations

The optimizer suggests more international equities and less Australian equities, given the AUD assumptions

Evaluation Allocation

________________________________________________

All expected returns reflect average annualized performance over the next 1-2 years time horizon. Expected returns are for asset classes only and not for any Blackstone or underlying manager funds. This chart reflects outputs from BAAM’s proprietary optimization tools, which incorporate assumptions about financial market factor moves that are used for scenario and allocation re-sampling purposes. The asset class hypothetical expected returns were determined based on Blackstone's experience in and views about each asset class and not necessarily based on objective market data. This is not intended to be a prediction of how any financial markets or investments will perform in the future and actual events and conditions may differ materially from the assumptions used to establish the expected asset class returns and there is no assurance that such information has been correctly determined. Please see additional scenario analysis disclosures at the end of this presentation.

Confidential

Blackstone 27

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

________________________________________________

Note: The BAAM procedures described in this presentation are a summary of procedures generally followed by BAAM in forming asset allocation views on behalf of a client and are not exhaustive of procedures performed and are subject to change. BAAM does not follow all of these procedures for all asset allocation decisions.

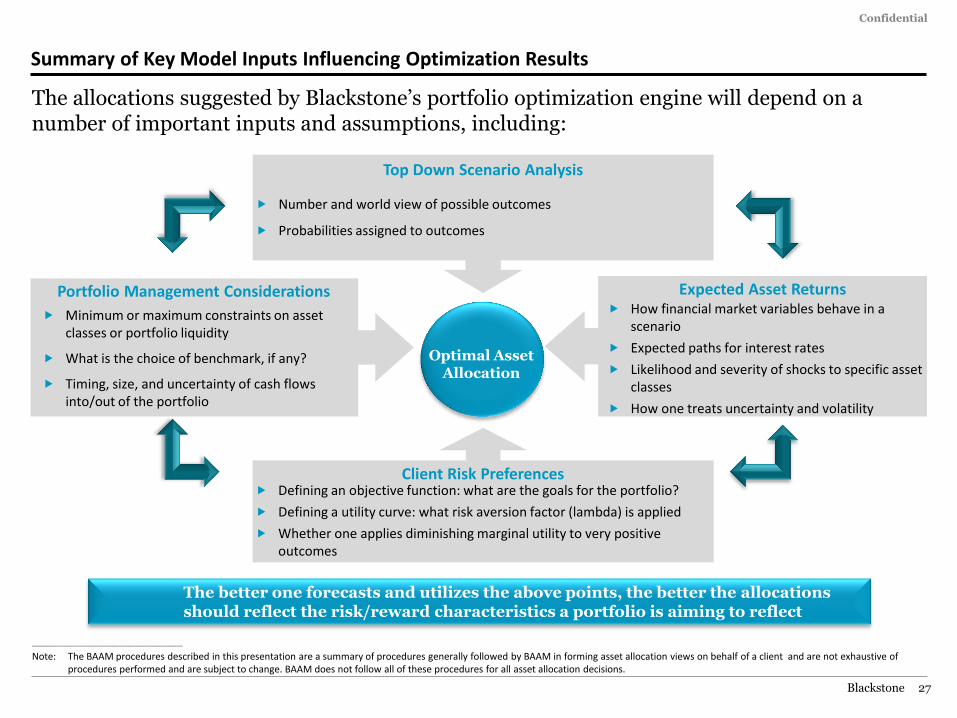

The better one forecasts and utilizes the above points, the better the allocations should reflect the risk/reward characteristics a portfolio is aiming to reflect

Optimal Asset

Allocation

Number and world view of possible outcomes

Probabilities assigned to outcomes

Minimum or maximum constraints on asset classes or portfolio liquidity

What is the choice of benchmark, if any?

Timing, size, and uncertainty of cash flows into/out of the portfolio

How financial market variables behave in a scenario

Expected paths for interest rates

Likelihood and severity of shocks to specific asset classes

How one treats uncertainty and volatility

Defining an objective function: what are the goals for the portfolio?

Defining a utility curve: what risk aversion factor (lambda) is applied

Whether one applies diminishing marginal utility to very positive outcomes

Top Down Scenario Analysis

Portfolio Management Considerations Expected Asset Returns

Client Risk Preferences

The allocations suggested by Blackstone’s portfolio optimization engine will depend on a number of important inputs and assumptions, including:

Summary of Key Model Inputs Influencing Optimization Results

III. Appendix 1

Confidential

Blackstone 29

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

Process and Methodology Summary

I. Economic & asset class scenarios are developed and maintained using BAAM’s in-house research and insights

a) For tactical asset allocation, BAAM currently maintains 18 economic scenarios that encompass a wide variety of possible outcomes for the next 1-2 years

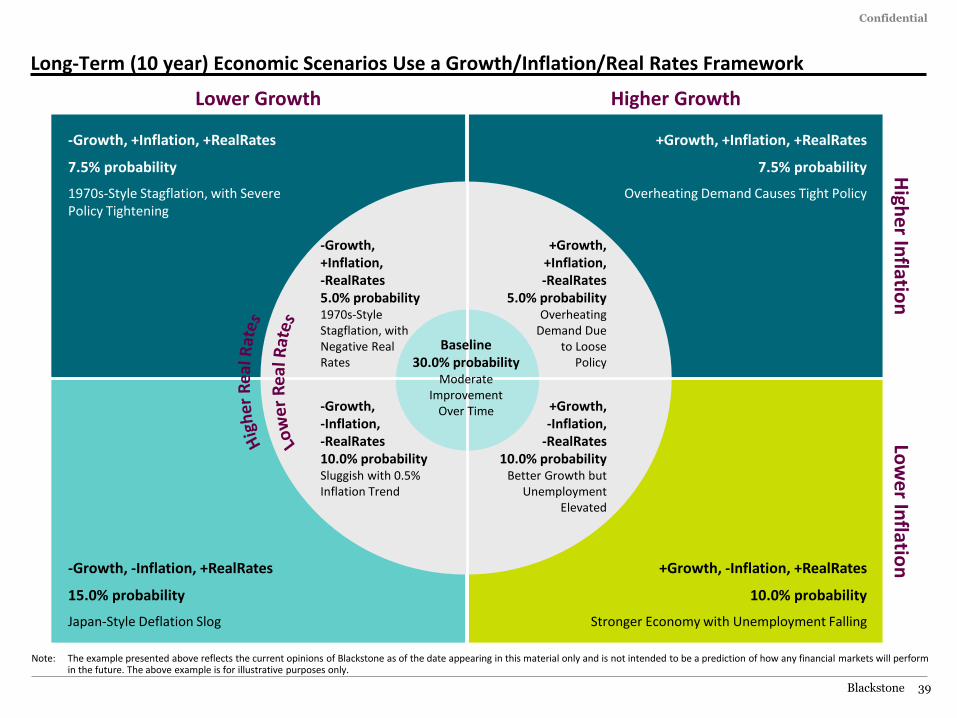

b) For strategic asset allocation, BAAM developed nine economic scenarios including a base case and combinations of higher and lower GDP growth, inflation, and real interest rates

c) BAAM created asset class return and interest rate assumptions for each year and scenario

d) BAAM has the ability to customize optimization model as appropriate to account for funding and expense information, portfolio mandate (ex. absolute return vs. lower volatility profile), and client specific risk preferences

II. BAAM uses Monte Carlo simulation and optimization to generate asset allocations for each portfolio objective

a) Monte Carlo simulation is employed to generate 250,000 paths in which the next ten years could play out, resampling from the scenarios with uncertainty and volatility. This includes asset class returns and key variables for specific mandate requirements as applicable (asset value, funding status, contributions, spending) and as a function of asset class weights

b) BAAM’s optimization engine identifies asset class weights that are optimal for each objective for a range of subjective risk aversions (“lambdas”)

c) The resulting optimal asset allocations are simulated a final time over ten years to determine percentiles for each variable’s expected distribution

d) We have short and long-term optimization tools with separate scenarios to derive tactical and strategic asset allocations, respectively

________________________________________________

Note: BAAM determines the scenario results and optimization allocations in its sole discretion based on its views and not necessarily based on objective market data. This is not intended to be a prediction of how any financial markets or asset classes will perform in the future.

Confidential

Blackstone 30

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

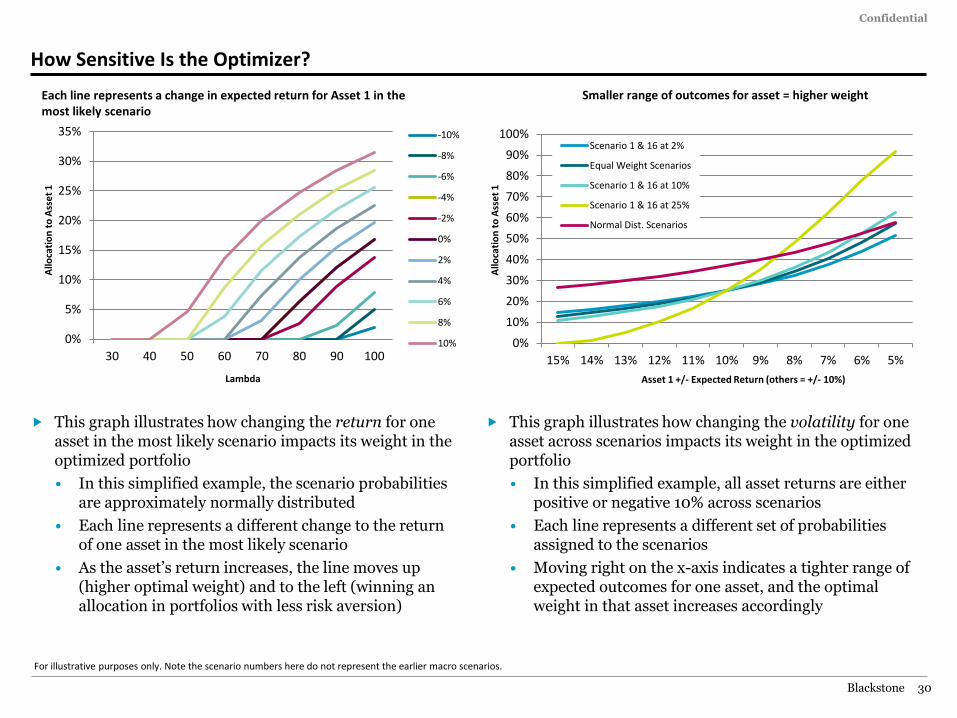

How Sensitive Is the Optimizer?

This graph illustrates how changing the return for one asset in the most likely scenario impacts its weight in the optimized portfolio

• In this simplified example, the scenario probabilities are approximately normally distributed

• Each line represents a different change to the return of one asset in the most likely scenario

• As the asset’s return increases, the line moves up (higher optimal weight) and to the left (winning an allocation in portfolios with less risk aversion)

This graph illustrates how changing the volatility for one asset across scenarios impacts its weight in the optimized portfolio

• In this simplified example, all asset returns are either positive or negative 10% across scenarios

• Each line represents a different set of probabilities assigned to the scenarios

• Moving right on the x-axis indicates a tighter range of expected outcomes for one asset, and the optimal weight in that asset increases accordingly

0%

5%

10%

15%

20%

25%

30%

35%

30 40 50 60 70 80 90 100

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Each line represents a change in expected return for Asset 1 in the most likely scenario

Lambda

Allo

cati

on

to

Ass

et

1

Asset 1 +/- Expected Return (others = +/- 10%)

Allo

cati

on

to

Ass

et

1

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

15% 14% 13% 12% 11% 10% 9% 8% 7% 6% 5%

Scenario 1 & 16 at 2%

Equal Weight Scenarios

Scenario 1 & 16 at 10%

Scenario 1 & 16 at 25%

Normal Dist. Scenarios

Smaller range of outcomes for asset = higher weight

For illustrative purposes only. Note the scenario numbers here do not represent the earlier macro scenarios.

Confidential

Blackstone 31

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120 0 115 99 0 171 146

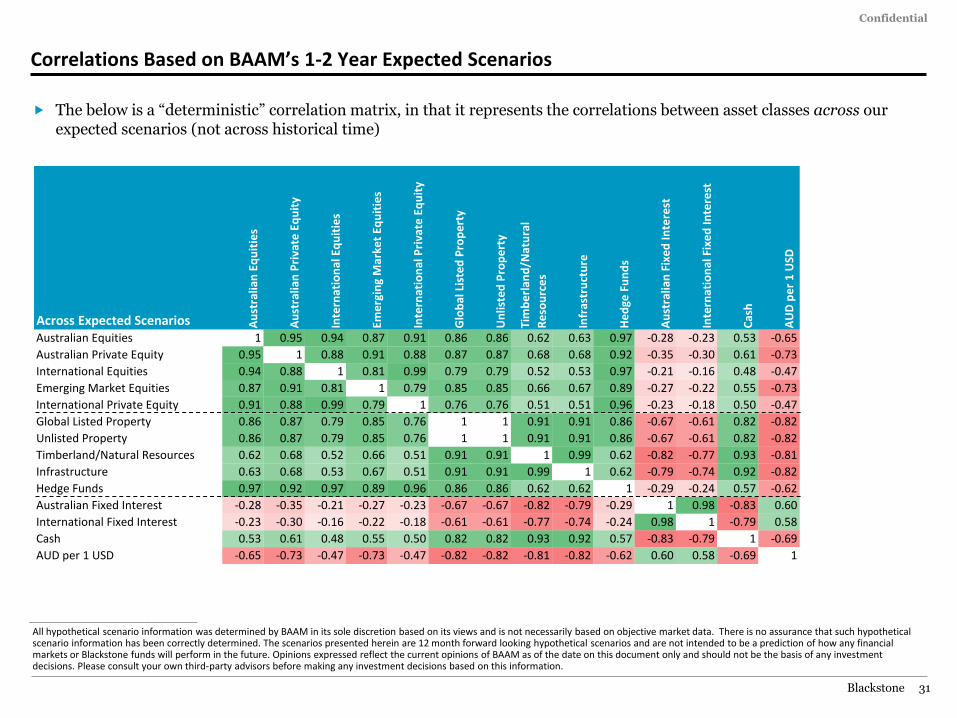

Correlations Based on BAAM’s 1-2 Year Expected Scenarios

________________________________________________

All hypothetical scenario information was determined by BAAM in its sole discretion based on its views and is not necessarily based on objective market data. There is no assurance that such hypothetical scenario information has been correctly determined. The scenarios presented herein are 12 month forward looking hypothetical scenarios and are not intended to be a prediction of how any financial markets or Blackstone funds will perform in the future. Opinions expressed reflect the current opinions of BAAM as of the date on this document only and should not be the basis of any investment decisions. Please consult your own third-party advisors before making any investment decisions based on this information.

The below is a “deterministic” correlation matrix, in that it represents the correlations between asset classes across our expected scenarios (not across historical time)

Across Expected Scenarios Au

stra

lian

Eq

uit

ies

Au

stra

lian

Pri

vate

Eq

uit

y

Inte

rnat

ion

al E

qu

itie

s

Eme

rgin

g M

arke

t Eq

uit

ies

Inte

rnat

ion

al P

riva

te E

qu

ity

Glo

bal

Lis

ted

Pro

pe

rty

Un

liste

d P

rop

ert

y

Tim

be

rlan

d/N

atu

ral

Re

sou

rce

s

Infr

astr

uct

ure

He

dge

Fu

nd

s

Au

stra

lian

Fix

ed

Inte

rest

Inte

rnat

ion

al F

ixe

d In

tere

st

Cas

h

AU

D p

er

1 U

SD

Australian Equities 1 0.95 0.94 0.87 0.91 0.86 0.86 0.62 0.63 0.97 -0.28 -0.23 0.53 -0.65

Australian Private Equity 0.95 1 0.88 0.91 0.88 0.87 0.87 0.68 0.68 0.92 -0.35 -0.30 0.61 -0.73

International Equities 0.94 0.88 1 0.81 0.99 0.79 0.79 0.52 0.53 0.97 -0.21 -0.16 0.48 -0.47