a sacco annual general meeting in lango, northern uganda ... · a sacco annual general meeting in...

TRANSCRIPT

125125

Chapter Five

SACCOs and MFIs

A SACCO Annual General Meeting in Lango, Northern Uganda

126126

5.1 Failing SACCOs: Who Cares?1

– thus SACCOs seldom live their “full lives”. They therefore do not serve their full purpose before dying.

ii) In the remote rural areas, SACCOs are often the only providers of financial services for most people. When the SACCOs fail, this leaves people with little or no alternative services.

iii) SACCO collapses leave people poorer and more desperate as they lose their meager savings

iv) Losing their money in failing SACCOs makes poor people more cynical of using financial institutions. Such a

Section 1 Evidence of Failure Why should anybody care about failing, missing or untraceable SACCOs? Are not institutions, like biological organisms, supposed to be subject to the immutable law of entropy? Are they not supposed to be born, grow, decline and die? And, given this pattern, should the failing of SACCOs be an issue?

There are three principal reasons why we should all be concerned about the failure rate of SACCOs in Uganda:

i) Whereas in countries like Kenya the life of a SACCO spans over decades, the failure rate in Uganda suggests that most SACCOs fail after only a few years

1 Author: Andrew Obara, FRIENDS Consult

Visiting a member of MAMIDECOT, a successfully managed SACCO in Masaka.

127

2 The one produced by the MoFPED study team and the one drawn from the Dept. of Cooperatives

polluting effect entrenches financial exclusion as more low-income / poor people get discouraged from accessing financial institutions’ services.

Therefore, SACCO failures have overall adverse negative effects on the rural economy and on the fight against poverty.

There has always been confusion over the number of SACCOs in Uganda, with most estimates putting it above 1,000. In 2006, the Ministry of Finance, Planning and Economic Development and the DFID-funded FSDU project conducted a SACCO census to ascertain the true number of SACCOs operating in Uganda. The results of the census revealed a significant difference between the number of institutions that were legally registered and the ones that were found operational by the census team. Compared to a number of 1,724 registered by the Department of Cooperatives, the team found only 628 (about half) traceable and operational SACCOs.

A follow-on study jointly commissioned by AMFIU and FSDU and conducted by FRIENDS Consult in 2007 was very revealing. The assignment was to track and report on the status of “missing SACCOs” in Uganda. This was to qualify and better understand the status or fate of the missing SACCOs. On the basis of discussions with SACCO stakeholders and generally known conditions, the study set out to test the following possible hypotheses about the reasons for the disparity:

i. The “missing SACCOs” actually operate but without a fixed location;

ii. The “missing SACCOs” were in the gap between registration and receipt of their registration certificates, yet the census team only counted institutions that could produce a registration certificate;

iii. While the census team was remarkably thorough, there may have been some institutions which exist but were simply hard to find;

iv. An unknown number of institutions have become dormant or collapsed and disappeared;

v. Some SACCOs were registered but have never actually operated on the ground (briefcase institutions).

The actual problem was bigger than anecdotal discussions and the MoFPED census had revealed. While reconciling SACCO lists2 before going to the field, the FRIENDS Consult study team found that of the 628 SACCOs that the MoFPED team had identified, 194 were not in the Register of Cooperatives. This meant that only 434 of the SACCOs that were in the register had been identified by the census team. By implication, 840 or 66% of the SACCOs that then existed in the registry had not been traced by the census team. These were for the time being labeled “missing SACCOs”.

A pre-testing of several possible causes found the above hypotheses (i. to v.) to be the most credible, and thus the study proceeded to empirically test each of them. On the basis of a rigorous and robust sampling framework, tool development, field survey, consultative meetings and document reviews, the study concluded that hypothesis iv. (collapse of SACCOs) accounted for 57% of the missing SACCOs; hypothesis iii. (SACCOs existing but difficult to find) accounted for 30% while the other three in aggregate accounted for 13%. The interpretation was clear: SACCOs were missing because they collapse and disappear fast, in most cases without anyone keeping track of them. They thus continue to appear in the Register even after collapsing.

Chap

ter 5

SAC

COs

and

MFI

s

127

128128

Table 1 below summarizes the study findings on the reasons for the absence of the “missing SACCOs”.

The foregoing paragraphs present the tenets concerning an otherwise vital sector that is unorganized, poorly facilitated, weak and struggling due to macro and micro level failures – which brings us to the vital question: “Why are the SACCOs failing?”

Section 2 Reasons for the Failures

The widespread SACCO failures principally stem from macro (national) level failures that trickle down into regional and eventually institutional (SACCO) failures.

2.1 National level

The structures and performance of the rural economy are weak. When the people who are now in their 40s and 50s were school children, cooperatives including SACCOs were the true engines of rural development. The whole agricultural production, marketing, input -supply and payment system was organized in a clear and highly functioning way from the national level (marketing boards) down to the village level (primary cooperatives).

SACCOs were the people-owned financial service arm of a highly integrated rural economy. The integrated system has since broken down and SACCOs are today inappropriately seen as part of the

microfinance industry, a stand-alone rural financial infrastructure or as financial service set-ups only remotely related to other drivers of the rural economy.

With the production and marketing system fragmented and somewhat unorganized, there are no obvious economic flows that at the local level feed into the SACCOs. Overall, failure to resuscitate the whole rural cooperative sector which fuels business culture and strengthens the production-processing-marketing chain in the rural economy is likely to leave SACCOs largely weak and prone to failure.

Minimal success with implementation of SACCO-focused strategies. Whereas Government has a well thought-out policy for rural development, implementation has faced chronic challenges ranging from poor understanding by implementers, inept personnel, inadequate logistics and conflicts of interest, all the way to fraudulent practices.

Government’s sound broad policy for harnessing SACCOs to provide financial services in rural areas has, for instance, not yet produced a significant impact. There has for long been confusion over what, in the context of the one-SACCO-per-subcounty move, Prosperity for All (which when translated is even more misleading) really means. This has not been helped by the sometimes flawed mobilization by inadequately trained and

Table 1: Reasons for Missing SACCOs according to hypotheses

Reason for absence

Proportion (%)

No fixed locations

4.3%

Difficult to find

30%

No registration certificate

1.4%

Collapsed3

57.1%

Never operated

7.1%

Total

100%

3 But not de-registered.

129129

questionably motivated local leaders (who have founded SACCOs on the expectation that ‘easy’ money will come to them from Government).

The “missing SACCOs” study confirmed the above observations. According to the study findings, the key national-level causes of SACCO failure are:

• SACCOs formed alongside productionand marketing cooperative societies have collapsed following the change in market trends which have rendered the business of production and marketing cooperatives ineffective

• Some institutions which wereformed with short-term objectives of obtaining resources from Government programmes such as Poverty Alleviation Project (PAP) collapsed when and before the programmes ended

• Inadequatesupervisionandmonitoringof the SACCOs by the District Commercial officers (DCOs) due to inadequate facilitation and low-skills capacity.

• Theclosureof theCooperativeBank in1999, which affected the performance of SACCOs because the Cooperative Bank was the main bank for these institutions. The SACCOs which had their accounts in Cooperative Bank were unable to recover their money in time to continue their activities. Some SACCOs closed because as soon as the members could access their savings, they quit.

• Lack of effective external audit andfinancial management assistance, causing SACCOs to fall under the burden of ill governance, poor management and financial imprudence.

2.2 Regional level

Geographical location also plays a part in the relative success of SACCOs. SACCOs and other community based financial organizations are particularly weak in the North and North-East regions of the country, where conflict and insecurity have adversely affected community solidarity. They are relatively stronger in the west and central regions. Part of the reason also lies in the fact that unlike the central and western regions that rely on coffee (perennial crop with a ready market and relatively clear marketing channels despite weakness of cooperatives), the north and east have traditionally relied on cotton which is labour intensive and needs more market and extension linkages. With the rebuilding of the northern region communities and national efforts to revive the entire cooperative system, SACCOs will hopefully be less vulnerable to failure in future.

2.3 Micro level

At the institutional level, things are not any better. SACCOs typically suffer from bad governance, incompetent management, interference, abuse by the more powerful members, financial illiteracy of most members and related vices.

According to the findings of the “Missing SACCOs” study, the most frequent causes of collapse included the following:

• Failure to cope with competitionespecially from commercial banks, MDIs and other MFIs which offer similar services. SACCOs have lost their members to these institutions which offer better services and look more stable.

Chap

ter 5

SAC

COs

and

MFI

s

130130

• Fraud–lossoffundsleadingtoacompletecripplingandclosureoftheSACCOs.

• Over-indebtednessofSACCOsresultingfrompoorfinancialmanagement.Coupledwithpoor management of the loan portfolio, this means liabilities build up as asset values shrink till the SACCO is insolvent.

• Retrenchmentand/orclosureofmotherinstitutions(foremployee-basedSACCOs).

• Lackofcompetenthumanresources-inadequatelyskilledpersonnelandmanagementwithinsufficient experience to run microfinance operations.

• InsomeSACCOs,onlyonepersonbearsthevisionforthewholeinstitutionandreservesthe right to make final decisions. When such a person is not experienced in microfinance, leaves, dies, or even decides to run down the institution, it collapses.

• Poorgovernance:SomeSACCOshaveilliteratecommitteememberswholackbasicskillsto effectively supervise operations and thus they get defrauded by management who take advantage of their ignorance. There are also increasing cases of highly placed individuals – in politics, Government or SACCO boards – influencing SACCOs to lend them large sums of money (often without security) which they later fail to service in time or totally default on. There are documented cases where such instances have led to severe crippling of the affected SACCO.

• Fraudandmismanagementbyboardexecutivesandmanagement.

Case 1Kaiffe Brokers SACCO in Kamuli was dormant for 8 years following the death of the charismatic founder and sole vision holder who rallied all the members around a common cause during his life time. The SACCO eventually collapsed due to loss of morale and lack of direction by members.

Case 2“…Kiryansaka SACCO in Masaka obtained a capacity building grant which was diverted to purchase land that was fraudulently registered under the name of the SACCO Treasurer. An annual audit revealed the fraud which led to the arrest of the Treasurer and the use of SACCO funds for litigation. The Treasurer was never convicted, resources dwindled to a trifle and members lost morale in the SACCO leading to its collapse…” DCO Masaka

131131

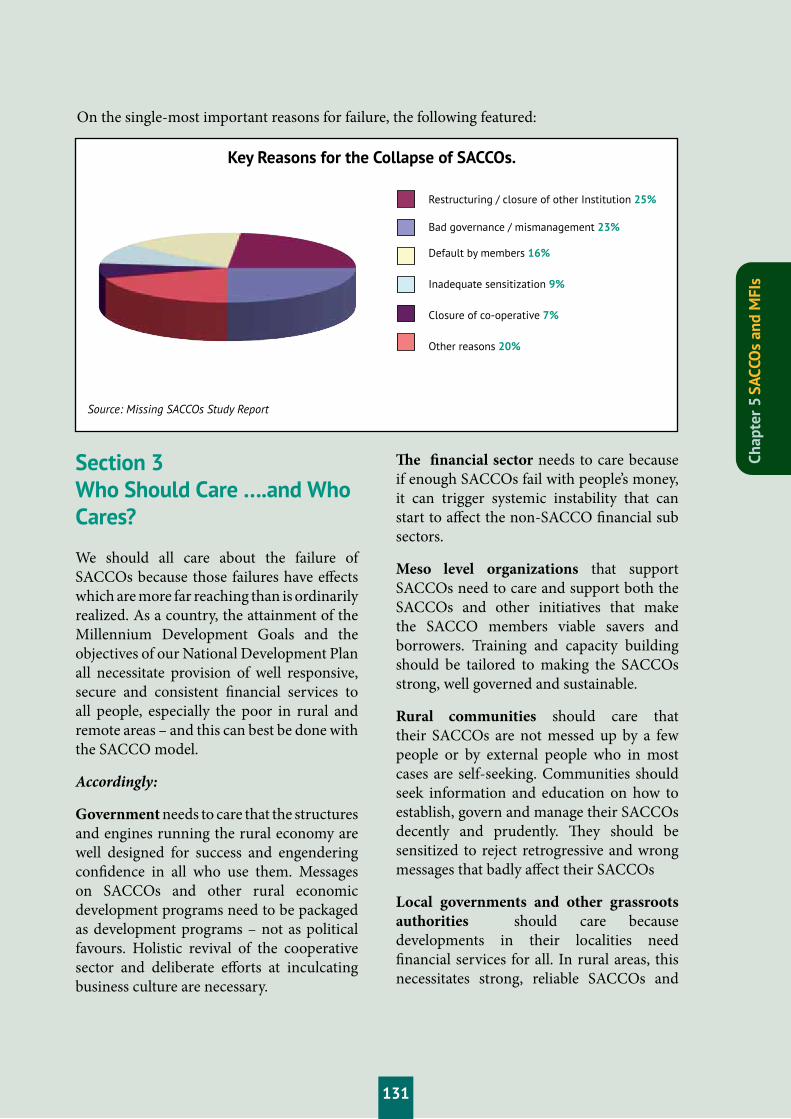

Key Reasons for the Collapse of SACCOs.

Restructuring / closure of other Institution 25%

Bad governance / mismanagement 23%

Default by members 16%

Inadequate sensitization 9%

Closure of co-operative 7%

Other reasons 20%

Source: Missing SACCOs Study Report

Section 3 Who Should Care ….and Who Cares?

We should all care about the failure of SACCOs because those failures have effects which are more far reaching than is ordinarily realized. As a country, the attainment of the Millennium Development Goals and the objectives of our National Development Plan all necessitate provision of well responsive, secure and consistent financial services to all people, especially the poor in rural and remote areas – and this can best be done with the SACCO model.

Accordingly:

Government needs to care that the structures and engines running the rural economy are well designed for success and engendering confidence in all who use them. Messages on SACCOs and other rural economic development programs need to be packaged as development programs – not as political favours. Holistic revival of the cooperative sector and deliberate efforts at inculcating business culture are necessary.

The financial sector needs to care because if enough SACCOs fail with people’s money, it can trigger systemic instability that can start to affect the non-SACCO financial sub sectors.

Meso level organizations that support SACCOs need to care and support both the SACCOs and other initiatives that make the SACCO members viable savers and borrowers. Training and capacity building should be tailored to making the SACCOs strong, well governed and sustainable.

Rural communities should care that their SACCOs are not messed up by a few people or by external people who in most cases are self-seeking. Communities should seek information and education on how to establish, govern and manage their SACCOs decently and prudently. They should be sensitized to reject retrogressive and wrong messages that badly affect their SACCOs

Local governments and other grassroots authorities should care because developments in their localities need financial services for all. In rural areas, this necessitates strong, reliable SACCOs and

On the single-most important reasons for failure, the following featured:

Chap

ter 5

SAC

COs

and

MFI

s

132132

other rural financial institutions. They should ensure that the SACCOs are well nurtured, supervised and overseen so that they operate prudently and sustainably.

The financial sector regulator, BoU, should care because a simple cancer that begins with a tiny organ can spread to the rest of the body. The not-in-my-back-yard approach, which would confine BoU to only concentrating on regulating Tiers 1 to 3 and to avoid blame for all else, is a temporary solution to a long -term problem as it mounts.

Section 4 Solutions

So what should we do to help? The problems identified suggest their own solutions. The areas of concern and causes of failure mean that strategic activities should be implemented along the following lines:

i. Intensify and sustain the revival of the rural cooperative sector in a holistic way.

ii. Re-examine and if necessary revamp, equip or change and strictly task the

SACCO registration and supervision authority for better performance.

iii. Promote and pass legislation for financial cooperatives either alongside the rest of Tier 4 financial organizations or as a stand-alone law. Either way, financial cooperatives should be regulated and supervised with the prudence necessary to oversee financial institutions. They should not be supervised merely as if they were trading cooperatives.

iv. Place the SACCO supervisory authority under the purview of BoU so that minimum financial sector prudence can be demanded of both SACCOs and their regulator.

v. Establish and facilitate an effective SACCO audit and investigations facility, perhaps under a strengthened supervisory organization.

vi. Support the re-establishment of a sustainable, prudently run bank for cooperatives - including for SACCOS.

133133

5.2 A Typical, Troubled and Tired SACCO in Northern Uganda 1

b) A night-time robbery was committed by highly skilled thieves, who broke into the SACCO’s strong room and used an oxy-acetylene torch to crack open the safe. They took off with UGX 20M.

These problems come on top of a poorly performing loan portfolio, which is mainly funded by externally borrowed funds which is around 60% of the total loan portfolio.

The members of this SACCO are drawn from thirteen sub-counties within three districts of West Lango region. Agriculture is the main economic activity and major livelihood source in West Lango region. It

Section 1 Agriculture in the SACCO’s Area of Operation

The typical, troubled and tired SACCO in Northern Uganda discussed in this article is a net borrower SACCO with a poorly performing loan portfolio in terms of quality and productivity. It is faced with serious governance and management challenges. These challenges include two recent blows to the SACCO:

a) Loans worth some UGX 44 million were disbursed to an individual close to the Board, who is highly placed in one of the key Government ministries. These advances are currently in arrears. It is also believed that these loans were made without security.

1 Authors: Patrick Kawanguzi (Best Africa Consult) and Justine Kasoma (GIZ/FSD)

Record keeping

134134

provides employment to over 90,000 people who constitute 94 percent of the working population, the majority being women. They are mainly engaged in subsistence farming with an average farm holding of some two acres per household, under the customary clan land tenure system. They use rudimentary and traditional technology, producing numerous farm commodities characterized by highly variable quality (Oyam 2007 and RALNUC 2009). This makes it difficult for them to bulk produce in order to attract buyers offering better prices. This resulting lack of competitiveness leads to lower returns for farmer-members of the SACCO.

One of the positive factors about the troubled SACCO is the close proximity of two large village markets: Loro Market (Oyam District) and Anekapiri Market (Kole District). These markets attract buyers from West Lango region and beyond including Gulu, Lira, Masindi, Nakasongola and Southern Sudan.

The dominant agricultural activities in the SACCO’s area of operation are: crop production, fish farming, livestock and poultry rearing.

• The crop sub-sector includes: cassava,sweet potatoes, millet, beans and pigeon peas. These are the dominant crops, produced both for home consumption and for commercial purposes. Sunflower and tobacco are the main traditional cash crops, while maize, simsim, ground nuts and rice are non-traditional crops grown for sale in the SACCO’s area of operation. Grafted mangoes and citrus fruits, namely lemon, oranges and tangerines are the fruits being promoted by the National Agricultural Advisory Services (NAADS) as perennial crops in the area.

• The livestock and poultry sub-sectoris not well developed. Both animals and birds are kept mainly as savings for meeting emergencies and other social financial needs, rather than as agribusiness enterprises.

• Aquaculture and apiculture are otheremerging income-generating activities in the area. Fish farming is mainly carried on in the areas which are far away from the River Nile. The main varieties of fish stocked include tilapia, mirror carp and Claris catfish. (Oyam 2007)

The region has water bodies that can be used for farming purpose. Members from the parishes of Amati, Nora, Kamudi and Atula can use the Nile while those from the villages of Atapar a and Amwa can tap water from Tochi River for vegetable production, fruit and timber tree nurseries. The Okole swamp has the potential for rice production, vegetable growing, tree nurseries and fish farming.

Section 2 Basic Information about the SACCO

The troubled SACCO under discussion in this article shares the common philosophy “it is cheaper to serve an existing client than to satisfy a new one”. Good selection, caring and building of mutual relationships with members by the management staff has resulted in high client retention rates and promotion of the SACCO to attract new members. The SACCO is known for its strong belief in growth. Since inception, the SACCO has been able to mobilize over 4,600 members with 98% of them being engaged in farming or farming-related

135135

Details Year

2005 2006 2007 2008 2009Male

Female

Groups

Institutions

Total Farming %

Non –farming %

Disbursements UGX ‘000

Outstanding balance UGX ‘000

Number of accounts

Share capital contribution UGX ‘000

Savings mobilization in UGX ‘000

Membership

Loan Portfolio

805

156

98

24

1,083100

0

8,112.3

104,676

245,779

147,360

326

1,014

321

132

37

1,50498

2

21,200

198,003

571,452

309,480

895

1,572

430

185

58

2,24595

5

34,095

466,702

565,415

418,348

1,020

3,091

748

299

83

4,22195

5

116,315

456,128

1,325,958

735,271

1,328

3,283

908

347

93

4,63195

5

136,605

548,455

1,210,962

988,926

1,385

Source: SACCO Management Accounts and Reports

Table 1: Membership, Savings and Loan Portfolio at the SACCO

Table 2: Quantified Capacity Building by Development Partners

Development Partner Period and Nature of Intervention Value in UGX ‘000

Rabobank Foundation

UNDP/Government of Uganda

Microfinance Support CentreSUFFICE EU/GoU Project GIZ/FSD Programme.

Total

Grant for operation, purchase of motorcycle, completing the SACCO banking hall and loan revolving fund (2005-2007)In kind technical backstopping coaching and mentoring in product development, financial information management system, strategic business planning. Borrowed funds for on-lending and training Capacity grant for training, safe and motorcycle Computerisation using the MBWin platform, training and motorcycles

58,000

30,000

408,000

15,000

90,000

601,000

Source: SACCO records. (This support spans several years)

activities along agricultural value chains. Details of membership, and membership growth, are given in Table 1 below. By December 2010 the members share capital totalled UGX 136.6 million, while savings deposits were UGX 548.5 million. At the same time the loan portfolio was UGX 988.9 million outstanding to 1,385 member-borrowers.

The SACCO pursues a vision of becoming a leading, self–reliant microfinance institution, serving the active poor in West Lango region. It hopes to achieve this by economically empowering the enterprising rural poor (micro-entrepreneurs and farmers) in the area by providing accessible and affordable financial services. It has developed a number of strategic arrangements with development partners sharing these objectives. These interventions are outlined in Table 2 below, and are valued at approximately UGX 600 million over the last several years.

Chap

ter 5

SAC

COs

and

MFI

s

136

West Lango region is considered to be an important food basket for Lira Municipality, Apac Town Council, parts of Kampala and southern Sudan. This forms good farming prospects for the SACCO members. The SACCO operates in an area underserved with formal financial institutions. All existing financial institutions have outlets in Lira and Gulu towns with only an ATM (Stanbic Bank) at Oyam District Headquarters in Acaba, targeting civil servants. This leaves the SACCO minimal competition in its market segment.

Despite the SACCO being in a great potential area surrounded by opportunities, minimal competition from formal financial institutions, good farming prospects for the members, good level of donor and other forms of assistance, the SACCO is tired and very troubled.

Section 3 The Effective Demand for Finance for Agriculture and Related Investments

The effective demand for finance for agriculture and the related investment by the members of the SACCO has its premise in three farm profitability-enhancing factors namely:

1. Improved terms of trade for oil seed growers has resulted from the increasing demand for oilseeds by Mukwano Industries Limited, Mount Meru Millers and small and medium enterprise (SME) oil processors. This buying market has made oil seed production attractive in the Lango region;

2. Increasing demand for food especially

dry rations, fruits, vegetables, and livestock and poultry products is attributed to the rapid per-capita growth in the two fast-growing municipalities of Gulu and Lira. Currently much of the demand, especially for vegetables such as tomatoes, cabbages and onions is met by supplies from Mbale and Kapchorwa; livestock are from Nakasongola and Mbarara while the poultry products are mainly supplied by Kampala, Jinja and Mukono Districts. All these suppliers are outside Northern Uganda region.

3. The net food-deficit position in southern Sudan has increased the demand for non-traditional cash crops such as beans, rice, simsim and maize.

These opportunities together with the introduction of affordable irrigation kits have prompted the farming community in the SACCO’s area of operation to start transforming from subsistence and rain-fed agriculture to semi-commercial farming. This would involve moving to year-round production, for both commercial purposes and home consumption.

This shift calls for adoption of new and appropriate farming technologies and better marketing systems by the farming community in the SACCO’s area of operation. The improved farming technologies are now being promoted by NAADS. The desire by many members to start using these technologies has led to a growing demand for finance for agricultural and related investments. This demand is summarized in three thematic areas namely:

• Productivity enhancement: Increase primary farm production through the provision of farm working capital and acquisition of farm production assets

137137

• Value addition: Improve the quality and shelf life of farm products and increase farm income though improved production along the value chain, value addition to primary products.

• Market access: Develop local agricultural marketing systems that enable small holder farmers to increase their farm incomes and earn positive returns through bulking and collective marketing.

While the demand from the SACCO members is for both seasonal and medium/longer term loans, the SACCO is only able to meet part of the demand for seasonal advances, i.e. short-term finance. This leaves a serious gap in the range of financial products available to members.

Section 4 The SACCO’s Performance as a Lender

The troubled and tired SACCO is just surviving and has continued to muddle through with a high Portfolio at Risk (PAR). This went as high as 66 percent in 2009 and just dropped, slightly, to 62 percent at the end of December 2010.

For this article the performance of the SACCO as a lender is discussed under three sub-themes namely: Loan Disbursement and Portfolio Composition, Portfolio Quality and Portfolio Productivity. Table 3 illustrates the performance of the SACCO as a lender.

Loan disbursement and portfolio composition

Over the four years from 2007-2010 the amount disbursed in the SACCO has

continued to increase. In 2010 it increased by 133% from UGX 566 million in 2007 to UGX 1.325 billion, facilitating the people of West Lango region to invest over UGX 4.10 billion in agricultural, trade and household/community activities.

As shown in Table 3, the portfolio outstanding has progressively grown in a similar trend. In 2010 it grew by 136% from UGX 418.3 million in 2007 to UGX 988.9 million. The SACCO has a special focus on agricultural loans since the majority of its members are farmers. Indeed, it has developed special products to address the financial needs at the three key levels along the agricultural value chain and the current agriculture loan portfolio (as at 31 December 2010) of UGX 404.64 million to 766 member borrowers is further diversified into three sub-products according to the core purpose of the loan namely:

Farm Production Loan for enhancing farm productivity with a total of UGX 317.17 million constituting 78% of the agricultural loan portfolio. The average loan size is UGX 700,000 shillings for a period of six months with a grace period of three months on principal repayments, though interest payments are due during the grace period.

Processing Loan for facilitating the value addition process constitutes 3% (UGX 12.13M) of the current agriculture loan portfolio. The average loan size is UGX 2.5M, for a period of six months with a grace period of three months on principal repayments, though interest payments are due during the grace period.

Agricultural Marketing Loan for financing the marketing of agricultural products is 19% of the agriculture loan portfolio with

Chap

ter 5

SAC

COs

and

MFI

s

138138

a value of UGX 77.26 million and is used to finance produce buying. It is for a period of six months with a grace period of three months on principal repayments, though interest payments are due during the grace period.

Portfolio quality

Using Portfolio at Risk (PAR) as the measure of portfolio quality, the performance is alarming, as depicted in Table 3, ranging from 37 - 66% across the years. This is far and above the recommended microfinance good practice of less that 5% and average of the SACCO industry in Uganda which is believed to be in the region of 20%.

The issue of portfolio quality in the SACCO is further made worse by the SACCO failing to create and update the loan-loss reserve on

Source: SACCO records

DetailsNumber of accounts

Amount UGX ‘000

Number of accounts

Amount UGX ‘000

Number of accounts

Amount UGX ‘000

Number of accounts

Amount UGX ‘000

Year

2007 2008 2009 2010

Loan disbursements

Agric. Loan portfolio

Commercial portfolio (pf)

General purpose pf

Total Loan pf outstanding

Agric. as % of total

Comm. as % of total

General as % of total

Portfolio at Risk

Income from agric.

Income from comm. pf

Income from general

Total income from loans

Yield of loan portfolio %

287

473

167

927

565,415

129,688

213,357

75,303

418,348

31%

51%

18%

45%

21,663

42,575

14,707

78,946

19%

246

829

45

1,120

997,400

131,195

441,289

23,853

596,337

22%

74%

4%

37%

24,384

79,264

4,223

107,872

18%

515

599

278

1,392

1,325,958

272,050

316,167

147,054

735,271

37%

43%

20%

66%

83,680

96,854

43,177

223,711

30%

766

474

363

1,603

1,210,962

404,646

392,236

192,044

988,926

40.9%

39.7%

19.4%

62%

133,533

113,748

39,885

287,166

29%

Table 3: Performance of the SACCO’s loan portfolio

a regular basis, putting itself in a situation of having no default risk coverage.

Portfolio productivity

We have used yield of the portfolio to measure the productivity. Yield of loan portfolio measures the amount of loan income collected from every UGX 100 of the average portfolio. The yield of portfolio of 19% in 2007, 18% in 2008, 30% in 2009 and 29% of 2010 is very low compared to its effective interest rate of 45%. This persistent yield gap is an indication of poor loan collection.

139139

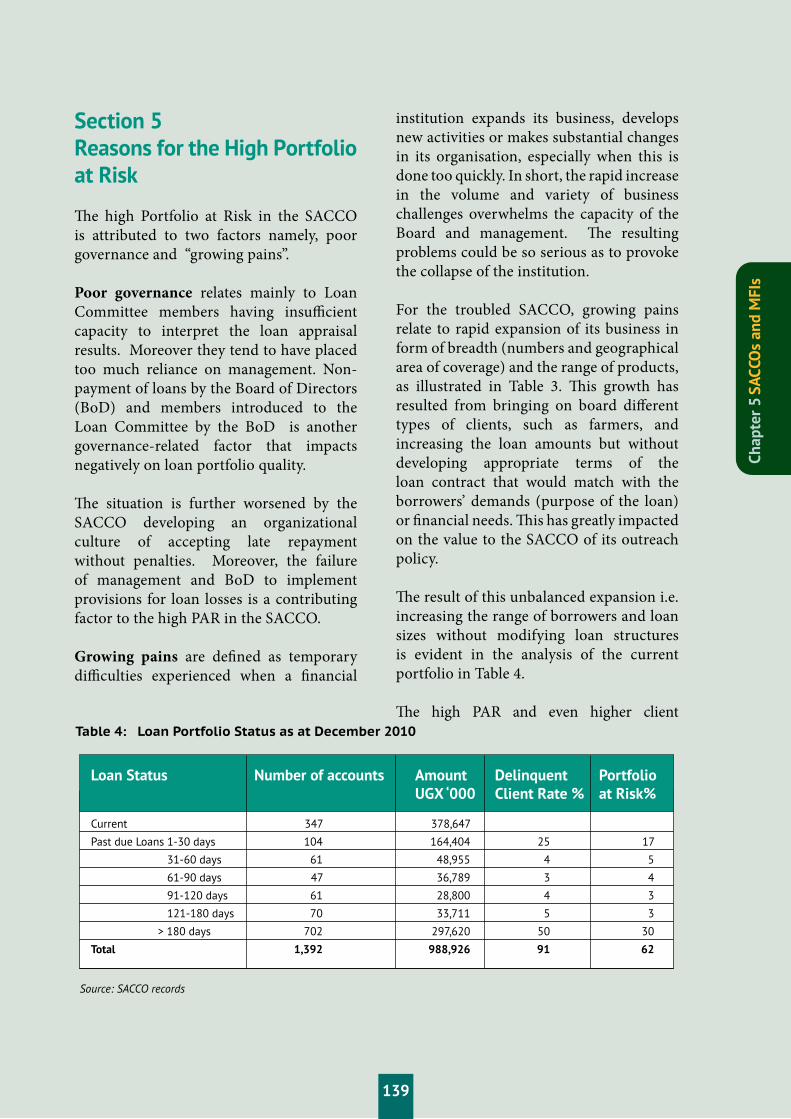

Table 4: Loan Portfolio Status as at December 2010

Loan Status Number of accounts Amount UGX ‘000

Current

Past due Loans 1-30 days

31-60 days

61-90 days

91-120 days

121-180 days

> 180 days

Total

347

104

61

47

61

70

702

1,392

378,647

164,404

48,955

36,789

28,800

33,711

297,620

988,926

Delinquent Client Rate %

25

4

3

4

5

50

91

Portfolio at Risk%

17

5

4

3

3

30

62

Source: SACCO records

Section 5 Reasons for the High Portfolio at Risk

The high Portfolio at Risk in the SACCO is attributed to two factors namely, poor governance and “growing pains”.

Poor governance relates mainly to Loan Committee members having insufficient capacity to interpret the loan appraisal results. Moreover they tend to have placed too much reliance on management. Non-payment of loans by the Board of Directors (BoD) and members introduced to the Loan Committee by the BoD is another governance-related factor that impacts negatively on loan portfolio quality.

The situation is further worsened by the SACCO developing an organizational culture of accepting late repayment without penalties. Moreover, the failure of management and BoD to implement provisions for loan losses is a contributing factor to the high PAR in the SACCO.

Growing pains are defined as temporary difficulties experienced when a financial

institution expands its business, develops new activities or makes substantial changes in its organisation, especially when this is done too quickly. In short, the rapid increase in the volume and variety of business challenges overwhelms the capacity of the Board and management. The resulting problems could be so serious as to provoke the collapse of the institution.

For the troubled SACCO, growing pains relate to rapid expansion of its business in form of breadth (numbers and geographical area of coverage) and the range of products, as illustrated in Table 3. This growth has resulted from bringing on board different types of clients, such as farmers, and increasing the loan amounts but without developing appropriate terms of the loan contract that would match with the borrowers’ demands (purpose of the loan) or financial needs. This has greatly impacted on the value to the SACCO of its outreach policy.

The result of this unbalanced expansion i.e. increasing the range of borrowers and loan sizes without modifying loan structures is evident in the analysis of the current portfolio in Table 4.

The high PAR and even higher client

Chap

ter 5

SAC

COs

and

MFI

s

140140

delinquency rate are threats to the viability of the SACCO. The following steps should be taken as a strategy to improve the quality of the SACCO’s loan portfolio and restore stake holders’ confidence.

Section 6 Recommended Ways Forward to Restore Confidence in the SACCO2

A. The SACCO should immediately adopt the philosophy of creating disciplined borrowers. This philosophy implies a culture where late payments are simply unacceptable and the consequences of loan default are serious. For this philosophy to work the loan recovery efforts should start by mounting stern pressure on Board members and on those related to them, to demonstrate to the rest of member borrowers that default is strictly unacceptable in the SACCO.

B. Maintenance of high standards of governance and management is paramount. For example it is outrageous that a highly-placed civil servant has apparently been able to bamboozle SACCO officials into granting him substantial loans, without security – loans that he has failed to repay.

C. The SACCO should adopt the microfinance financial discipline practice of maintaining adequate loan-loss reserves throughout the year.

D. Financial literacy training or consumer financial education should be made a core activity for members of the SACCO.

Just like in any other financial institution, for the troubled SACCO, “An informed customer makes for a better bottom line”. Teaching its clients good money management practices regarding earning, spending, saving, and borrowing would go a long way in improving the PAR of the SACCO.

E. The Board should recruit a credit or operations manager, who would be a middle-line manager. He/she would assist in dealing with growing pain stresses and would assist the General Manager in the daily monitoring of the loan portfolio at a corporate level, permitting the General Manager to concentrate more on strategic issues.

F. A strong financial cooperative law detailing the obligations and privileges of the Board of Directors, SACCO performance standards; and improved supervision of SACCOs are critical recipes for ensuring soundness of the SACCOs and protecting the hard-earned member savings. This will also go a long way in reducing the unnecessary pressure by the Board of Directors on the management.

G. Finally, and of crucial importance for the financial health of rural SACCOs, farming loans must be tailored to the expected farm family cash flow, and not simply be an echo of trading loans. Keeping loans impossibly short term is not being sensibly risk-averse. Rather it is the opposite. Through careful loan design the SACCO’s agricultural loan portfolio can be a sustainable source of profit, with maximum customer value.

2 Editors’ Note: This section focuses mainly on actions within the SACCO itself. External initiatives, such as specific legislation for financial cooperatives and improved supervision, are only mentioned briefly here (under F), but are clearly relevant. See further suggestions on the last page of Article 5.1 in this Yearbook.

141141

References:

Report: Oyam District (2007) “2002 Uganda Population and Housing Census District Analytical Report”. Uganda Bureau of Statistics Kampala

Report: RALNUC (June 2009) “SACU End of Project Report and Evaluation”. Restoration of Agricultural Livelihoods in Northern Uganda Component (RALNUC) Nutrition, Gender and HIV/AIDS Project implemented by Send A Cow Uganda (SACU) in Apac, Lira and Oyam

Chap

ter 5

SAC

COs

and

MFI

s

142142

5.3 What Makes a Guarantor Effective in MFI Lending?1

Joint-liability group lending mechanism is by far the most celebrated microfinance innovation. It has also been studied widely, especially how peer pressure and social sanctions among group members work in different types of groups and contexts. A widely cited study carried out among FINCA group borrowers in Peru showed that socially close borrowing groups have better loan repayment outcomes (see Karlan 2007). Also conflicting results can be found from the literature (e.g. Ahlin & Townsend 2007)4.

1 Author: Anni Heikkilä, Aalto University School of Economics, Finland. The author wishes to express her appreciation for the cooperation of the Board and Management of MAMIDECOT in the research project on which this article is based.

2 Census of Tier 4 Financial Institutions in Uganda was carried out by the MoFPED.3 Giné, Xavier and Karlan, Dean (2009) “Group versus Individual Liability: Long Term Evidence from Philippine Microcredit

Lending Groups.” Yale University Economics Department Working Paper No. 61.4 Karlan, Dean (2007) “Social Connections and Group Banking” Economic Journal, 117(517), pp. 52–84. Ahlin, Christian

and Townsend, Robert (2007) “Using Repayment Data to Test across Models of Joint Liability Lending.” Economic Journal, 117(517), pp. 11–51.

Section 1 Introduction

A vast majority of Tier 4 financial institutions in Uganda use individual-based lending methodology. A census study conducted in 2006 showed that 37 percent of Tier 4 institutions rely only on individual lending, 57 percent use both individual and group lending approaches, and 6 percent use only group lending methodology. Also worldwide, different variants of individual-based lending methodology2 are rapidly gaining ground among MFIs (see e.g. Giné & Karlan 2009)3.

A Guarantor.

143143

Guarantors are an important element of individual-based lending systems. It is surprising how little the effectiveness of the guarantor system has been studied, compared to the popularity of individual-based MFI lending in practice. It might be tempting to generalize the results of the famous joint-liability group lending studies to concern the individual loans’ guaranteeing system as well. One should not do that, however, as the role of the individual loans’ guarantors is likely to differ from that of the jointly liable group members in many respects, for example:

• In the individual-based system, thereare typically one or two guarantors per one individual loan. In joint-liability lending groups, there are typically at least 5 members who all cross-guarantee each others’ loans.

• Joint-liability group borrowers meetfrequently and make their repayment instalments during these meetings. In the individual-based lending system, borrowers typically make their repayment instalments privately to the MFI officials.

• Group borrowers are expected to solvepossible repayment problems among

themselves, and bail out the defaulting group members. In the individual-based system, the MFI officials like loan officers, typically have a key role in solving the repayment problem situations.

This article examines the role and effectiveness of guarantors in the context of an interesting case MFI, Masaka Microfinance and Development Cooperative Trust Ltd. (MAMIDECOT). The empirical material utilized in this article is based on extensive MAMIDECOT Member Survey data collected in August-September 2009, as well as staff interviews carried out during several field visits in 2009 and 2010. The MAMIDECOT Member Survey had 1596 respondents, out of which 1058 respondents had taken at least one individual loan from MAMIDECOT since the beginning of 2007.

The rest of this article describes the case institution and its lending policies in detail, and analyses the role played by guarantors and other repayment incentives in the loan recovery process. The article concludes with the recommendation that guarantors’ effectiveness should be assessed and developed hand-in-hand with other repayment incentives.

Chap

ter 5

SAC

COs

and

MFI

s

144144

2.1 Facts about MAMIDECOT

MAMIDECOT was established in 1999 by 34 founding members, with the help of the United Nations Development Programme (UNDP) funded Private Sector Development Programme. The objective of this programme was to motivate the creation of community based savings and credit cooperatives (SACCOs) in the rural areas. MAMIDECOT is also a SACCO by its constitution, and thus owned by its members, whose delegates gather once a year at the Annual General Meeting.

Today MAMIDECOT has approximately 12,000 members in four branches: Nyendo (the headquarters), Lukaya, Kalungu, and Bukomansimbi. The two largest branches of Nyendo and Lukaya have been running the FAO-GTZ MicroBanking System for Windows (MBWin) software since 20075.

MAMIDECOT has had an ambitious expansion strategy with the target of opening a new branch every two years. The institution

faces relatively intensive competition from other MFIs, MDIs (Microfinance Deposit-Taking Institutions) and commercial banks operating in its catchment area.

MAMIDECOT offers a variety of micro-credit and savings services, as well as training for its members. Its product offering includes: ordinary savings and time deposit accounts, school savings accounts, and loans for business investments, agricultural improvements, buying boda bodas or paying for school fees. Loan interest rate is 2.5 percent per month, except for agricultural loans (2 percent per month). MAMIDECOT has continuously improved its offering to suit better the needs of its clientele. For example, it has adjusted the terms of its agricultural loan product to be a better fit with the farmers’ cash flows.

About 25 percent of MAMIDECOT’s customers are active borrowers. In 2009, MAMIDECOT issued loans for a total value

Section 2Case Institution and Its Lending Policies

5 This was with support from the former USAID Project, Rural SPEED and the BoU/GTZ/Sida/FSD Programme.

MAMIDECOT. Lukaya Branch

145145

Table 1. Has MAMIDECOT ever required that one or both of the guarantors you proposed in your loan application should be changed?

Percentage

Yes, at least once

No, never

Totals

48

1010

1058

5

95

100

Frequency

Data Source: MAMIDECOT Member Survey 2009

of approximately 4,000,000,000 UGX. Of the total volume, 89 percent was lent to individuals, 3 percent to groups and the rest for organizations, institutions and staff members.

In October 2010, the portfolio at risk was 43 percent and portfolio in arrears 12 percent in the largest branch of Nyendo. Typical for loan repayment in MAMIDECOT is that several instalments are paid late, even if the final repayment outcomes may be on a decent level. In the branch of Nyendo in January 2009 – October 2010, 34 percent of all loan instalments were paid at least 30 days late. In the same period, 8 percent of instalments were paid at least 90 days late.

2.2 Lending policies for individual loans

When a borrower candidate is willing to apply for an individual loan, he first goes to meet the branch manager. The manager sensitizes him about the lending procedure, requirements and charges, then gives him a

loan application form and allocates him to one of the loan officers. If the applicant is a repeat borrower, he goes to the same officer as before.

Next the borrower candidate fills in the application form, indicating the desired loan amount, purpose of the loan, collateral and guarantors. Physical collateral, such as a land plot, motor vehicle log book or household items, is required to back up all individual loans. In case the collateral is a property item, the local council needs to verify, in writing, that the asset really belongs to the applicant in question.

All individual loans need to be guaranteed by two other members of MAMIDECOT. If the loan applied for is smaller than 1,000,000 UGX, one guarantor may be sufficient. The guarantors need to be good savers, and they should not have experienced serious repayment problems in the past. However, no explicit criteria exist for the assessment of the guarantors’ repayment capacity.

Table 1 indicates that only 5 percent of MAMIDECOT individual borrowers have ever been requested to change one or both guarantors they proposed in their loan application form.

After the application form is filled, the loan officer goes to visit the applicant’s business premise and place of residence. During this visit the officer also verifies that the security is genuine. After this inspection, the loans officer judges how much money

Chap

ter 5

SAC

COs

and

MFI

s

146146

he recommends to be advanced to that client. Next the application is examined by the branch manager, and after that the loan committee will have a final say in the credit allocation decision.

Only a few percent of loan applications are rejected in MAMIDECOT. The reasons for complete rejection are usually applicant’s poor repayment history or unreliable collateral security. On the other hand, it is very common to grant the applicants only a proportion of the total amount for which they applied. In 2009, the loans committee granted on average 87 percent of the loan amount originally applied for. The committee may judge that the amount applied for is too

much for a certain purpose. Sometimes the reason for reduction is that the institution’s funds are scarce due to a high credit demand season 6.

Final recommendations for this situation are included in Section 4.

2.3 Who are the guarantors?

In the MAMIDECOT Member Survey we asked the individual borrowers questions about their guarantors. Table 2 presents information about social connections between borrowers and their guarantors for loans taken since the beginning of 2007.

Table 2. Relationship between the borrower and his/her guarantors

Percentage

Close relatives

Other Relatives

Close Friends

Other Friends and acquaintancies

Neighbours

Workmates

They dont know each other personally

No answer

Total

153

178

868

917

29

78

17

2

2,242

7

8

39

41

1

3

1

0

100

Frequency

Data Source: MAMIDECOT Member Survey 2009

Survey responses in Table 2 indicate that 80 percent of guarantors are borrowers’ friends, either close friends or more distant acquaintances. Relatives account for 15 percent of the guarantors. In only 1 percent of the cases the borrower does not know his guarantor personally. In these rare cases the borrower may have asked a stranger from

the MAMIDECOT branch to become his guarantor. In such cases, it is questionable whether the guarantor has really understood his responsibilities.

The MAMIDECOT MBWin database includes information about the guarantors’ own membership in the institution.

6 MAMIDECOT management explain that “appraisals of loan applications follow the usual examination, covering: a) capacity to pay back, b) disposable income, c) value of collateral, d) the actual monetary missing gap as witnessed on site / ground / on visit and e) character (especially for the 1st borrowers.” The SACCO further states that “usually less than 10 percent (of applicants) get less than their applications”.

147147

According to this data source, 80 percent of the guarantors are also borrowers themselves. These guarantors may have loans outstanding at the same time with the borrower or at different times. In addition, 65 percent of the borrower-guarantor pairs have cross-guaranteed each others’ loans at least once.

Section 3 Guarantors’ Role and Importance for Loan Repayment Performance

3.1 Guarantors’ role in the loan recovery process

In MAMIDECOT, the borrower monitoring and loan recovery process is largely driven by the loan officers. Guarantors, however, have their own important role in the process, as the following description indicates. Loan officers’ monitoring and enforcement duties begin when a borrower’s monthly loan instalment is late. After a few days of delay, the loan officer calls the borrower by phone to remind him of the payment. If the phone call does not help, very shortly after that the loans officer goes to visit the borrower. If the instalment remains unpaid after one month has passed, a warning letter is sent to the borrower.

At this point the officer also contacts the guarantors. The guarantors are expected to put pressure on the borrower, help the loan officer to track the defaulting borrower, and also give other tips, for instance if the borrower is trying to sell his collateral. MAMIDECOT can also deduct money from the guarantor’s savings account to cover at least part of the missing payments. The borrower is obliged to pay this money back to the guarantor.

If none of the previously mentioned measures helps, next step is sending the borrower a notification that MAMIDECOT intends to sue him. The last step is taking the borrower to court and finally seizing the collateral. There are only a few cases every year that need to be taken to court, and even with these cases the collateral very rarely gets seized. The borrowers usually try their best to get the missing balance from the guarantors or from their relatives before the process has reached the collateral seizure stage.

Neither the borrower nor the guarantor will get new loans from MAMIDECOT before the missing instalments have been covered. It will also be hard to get loans from competing financial institutions in the area, as they unofficially share information about defaulters.

Notable features in the guarantors’ role are:

• Guarantorshavenoofficialwayofgettingto know about the borrower’s repayment problems before the loan officer informs them. At this stage the repayment problems may already be serious.

• The guarantor is expected to act as asource of information for the loan officer, which is very important in cases when the borrower has escaped with the money. The guarantor should also liaise with the borrowers’ relatives when the situation requires action.

• Thehardestpotentialpunishmentfortheguarantor is that he cannot get future loans from the institution, unless the borrower has paid back his loan. This might not be very effective in cases when the guarantor is not a borrower and has no interest in borrowing from MAMIDECOT in the foreseeable future.

Chap

ter 5

SAC

COs

and

MFI

s

148148

Table 3. Guarantors’ actions in case of repayment problems

Table 4. Loan officer’s actions in case of repayment problems

Percentage

Yes

No

No answer

Total

53

197

9

259

20

76

3

100

FrequencyA. Were your quarantors contacted by our MAMIDECOT staff?

Data Source: MAMIDECOT Member Survey 2009

Percentage

Yes

No

Total

42

217

259

16

84

100

FrequencyB. Did your guarantors put pressure on you?

Data Source: MAMIDECOT Member Survey 2009

Percentage

Yes

No

No answer

Total

139

116

4

259

54

45

2

100

FrequencyB. Did a loan officer visit your home or business ?

Percentage

Yes

No

No answer

Total

192

66

1

259

74

25

0

100

FrequencyA. Did a loan officer contact you after your repayent difficulties?

3.2 Is it guarantors or other incentives that matter for repayment performance?

Do guarantors actually liaise with the loan officer and put pressure on the borrower the way they are supposed to? How actively do loan officers carry out their monitoring and enforcement duties? Borrowers’ responses to repayment problem related questions in the MAMIDECOT Member Survey shed light on these issues.

Table 3 below tells about the borrowers’ perception of loan officer - guarantor collaboration and the pressure they have experienced from the guarantors’ side. Table 4 shows loan officers’ actions in case of repayment problems. Total number of respondents is 259 in Tables 3 and 4. This indicates that 24 percent of all interviewed individual borrowers admitted that they had had repayment problems.

Table 3 shows that in 20 percent of the repayment problem cases the borrower reports that his guarantors have been contacted by a MAMIDECOT staff member. Some 16 percent of defaulting borrowers have experienced pressure from their guarantors. Thus, it seems that after the guarantors have been informed about the situation by the loan officer, most of them take action.

An evident challenge seems to be the low frequency with which the officers liaise with the guarantors. When portfolio at risk figure is above 40 percent, one would expect closer collaboration between loan officers and the guarantors.

Table 4 indicates that in 74 percent of the repayment problem cases the officer has contacted the borrower, and in 54 percent of the cases he has also visited the borrower’s home and / or business. Hence, loan officers seem to take a relatively active approach towards the defaulting borrowers. A highly relevant question is why the officers do not involve guarantors in their guarantees’ repayment problems more often. Possible reasons may include:

• Officers may believe that contactingthe guarantors does not help to solve the borrowers’ problems. It is hard to quantify guarantors’ effect on repayment

149149

outcomes, and the officers may base their belief on some negative experiences they have had about negligent guarantors.

• Guarantors’ contact details may bemissing from the MFI’s registers or they may be outdated.

• Itmayalsobethattheofficersaresimplytoo busy to contact the guarantors and liaise with them, even if they believed that it would be useful and they have guarantors’ contact details readily available.

The empirical evidence presented above indicates that the guarantors’ effectiveness should be assessed together with other repayment incentives, especially loan officers’ monitoring and loan recovery actions. In the context of MAMIDECOT, it seems that the best way to improve the effectiveness of guarantors’ actions is first of all, to make them aware, more frequently and earlier, of their guarantees’ problems. In the current system, the loan officers act as information gatekeepers and a lot depends on their ability and resources to liaise with guarantors.

When it comes to other repayment incentives, such as collateral and promises of increasing loan amounts in the future, it is hard to assess the effectiveness of these measures compared to the effectiveness of the guarantor system. If MAMIDECOT changed its policy regarding one of the repayment incentives and kept the others same as before, under certain conditions it would be possible to statistically evaluate the impact of this change on repayment outcomes.

Section 4Towards Financial Health and Sustainable Lending Practices

In this final Section the bold type presents Recommendations. These are addressed to SACCOs and other MFIs and are intended to assist in the process of building financial health and sustainability through improved management of lending, with particular focus on the management of guarantors.

The analysis of MAMIDECOT’s guarantor system shows an important learning point both for MAMIDECOT and also for other MFIs that use guarantors. Guarantors’ effectiveness may be conditional on loan officers’ abilities and resources to inform guarantors about repayment problems. Loan officers’ actions are naturally less of a concern in a guaranteeing system where guarantors have another official channel to inform them about repayment problems (like public repayments). However, such systems are likely to be rare in the context of individual based lending.

While a lot may depend on loan officers’ effectiveness, the analysis of this article highlights a few ways how MAMIDECOT and other MFIs may sharpen up the guarantor selection process. First, the loan officer should make sure that the proposed guarantors understand what guaranteeing means, especially that they risk losing their own money and ability to borrow from the institution, if repayment problems get serious. Second, the officers should critically assess the guarantors’ repayment capacity.

Chap

ter 5

SAC

COs

and

MFI

s

150

It is unlikely that a guarantor, who is paying back a large loan himself, would have significant savings in the institution.

MAMIDECOT and other MFIs should also reflect on whether current sanctions for guarantors in the case of default are effective enough to motivate guarantors to do their job well. In the case of MAMIDECOT, for example, the threat of losing savings may not be a very strong incentive, because the guarantor may empty his savings account at any time.

MFIs should pay attention that both borrowers’ and guarantors’ contact details are checked and updated if needed, every time they come to do banking. People may change their mobile numbers rather frequently, and it is important to have the latest information available. Computerized

MFIs, like MAMIDECOT, should use their information system as the main repository of updated contact information.

Finally, also the loan acceptance policy could be critically reviewed in MFIs like MAMIDECOT, where the granted loan amounts are typically reduced. Loan officers and guarantors will have limited means to enforce loan payments in cases when the borrower has loans outstanding also from other MFIs or moneylenders. The need to top up the loan from other sources is evident when the original loan amount is not large enough for borrower’s investment needs. Hence, MFIs should make sure that granted loans are large enough for borrowers’ investment purposes, and perhaps accept a slightly smaller share of applications to ensure the borrower has adequate funds for the investment.

Data cleaning of MAMIDECOT SACCO records

5.4 Area Cooperative Enterprises: Are these an Effective Tool for Agricultural

Transformation in Uganda?1

inputs and marketing their output, where potential for economies of scale exist3. This paper presents explanatory arguments for recognising Area Cooperative Enterprises (ACEs) as effective tools for agricultural transformation and as a key innovation to correct market failures among small-holder farmers. The ACE model was devised by the Uganda Cooperative Alliance (UCA).

Introduction

Smallholder agriculture in Uganda is exposed to pervasive market failures, translating into missed opportunities and sub-optimal economic behavior. The lack of credit, for instance, severely constrains investment capacity. This is coupled with market failures2 that are often rooted in high transaction costs. Although often more efficient in production, smallholders tend to face a comparative disadvantage when it comes to accessing

1 Author: Nathan Were, The Microfinance Support Centre Limited. The author acknowledges with thanks the very useful comments and suggestions made on an earlier draft by the leadership of UCA.

2 Markets fail when the expected costs of transacting are greater than expected gains from transaction.3 Ruth Vargas Hill, Tanguy Bernard, & Reno Dewina (2005); Cooperative behavior in rural Uganda: Evidence from the

Uganda National Household Survey. IFPRI Uganda Strategy Support Program (USSP) Background Paper No. 2.

Kisiita ACE Warehouse in Western Uganda

151

152152

Section 1 The Gap

The National Development Plan (NDP) of 2010 recognizes the need for better access to agricultural credit by smallholders as a key catalyst for enhancing production, competitiveness and incomes. Uganda’s rural economy is based on subsistence agriculture and with poorly developed financial services in subsistence farming areas it is difficult to effectively mobilise savings for sustainable investment. Moreover, none of the recent poverty eradication programs have directly supported cooperative farming and marketing to address the bottlenecks of technology acquisition, crop finance, storage and value addition.

It is against this background that the Area Cooperative Enterprises (ACE) model was conceived. Created in 1998 the model seeks to address three critical areas: 1) Production 2) Productivity, 3) Value Addition and Marketing and access to Rural Finance. This approach envisions creating order in the entire agricultural value chain. This it achieves by bringing together supportive and collaborative linkages that include; a rural production organization (RPO), for production; a Savings and Credit Cooperative Society (SACCO) for finance and an Area Cooperative Enterprise (ACE) to handle value addition and marketing.

The ACE model seeks to address the critical challenges faced by an everyday farmer. These include: post harvest losses, lack of access to affordable equipment for production, limited access to irrigation systems and to high value inputs, and exploitation by middlemen through low farm-gate prices. In the absence of strong cooperative institutions the private sector has picked up the resulting business opportunities.

Driven, naturally, by profit maximization, the private sector tends to exploit farmers. Examples observed include: low prices are offered at farm level, use of shrewd weighing systems and provision of distorted market information. Supplier credit for input purchase is both limited and carries high costs. There is also evidence that tractor hire services are unduly expensive4.

Section 2 Description of the Area Cooperative Enterprise Model

2.1 Structural relationship between the farmer, RPO, ACE and the SACCO

Rural Production Organizations (RPOs) are primary level cooperatives, while Area Cooperative Enterprises are secondary level cooperatives, formed typically by 5-10 RPOs (at times jointly with farmers’ associations) within a given geographical area. Each level involves members coming together to achieve certain economies of scale. Whilst it is absolutely important that the number of primaries coming together is large enough for the purposes of forming a critical mass, they must neither be too many nor too far from each other in order to achieve the necessary efficiency on the one hand, and cohesion on the other.

Individual smallholder and large scale farmers belong to an RPO and each RPO usually has 30 to 200 farmers. The model is organized in such a way that there is only one ACE covering a sub-county, supported by RPOs from different villages that make up that sub-county.

4 For example, in Kisiita, the ACE tractor hire service costs UGX 65,000 per acre, while private contractors charge UGX 80,000 per acre.

153153

At an RPO there are mini storage facilities to handle bulking at that level. The ACE has a central storage facility for all produce collected by RPOs from farmers. The produce is usually moved from RPO stores to the central storage facility at the ACE, ready for cleaning, sorting, value addition and, eventually, marketing.

The ACE is also linked to a Savings and Credit Cooperative Society. The main function of the SACCO is to provide financial services to the ACE, RPO and individual farmers, using a quasi ware-house receipt system. All three (ACE, RPO and individual farmers) are members of the SACCO. After harvest, farmers deposit their produce with their RPO. This is then transferred to the ACE stores and the farmer is provided with a receipt. It is this receipt that acts as collateral security to access loans from the SACCO of up to 60% of the total value of bulked produce at the prevailing / current market prices.

The ultimate objective of the ACE is to enhance farmers’ bargaining power and ability to off-load their products onto the market, when the price is favourable to the seller. Once the produce is sold, the farmers who acquired inputs on credit, or had loans for tractor hire services or drying facilities through or from the ACE, are paid net of the due repayments. The net amount is deposited on the farmer’s account in the SACCO. This implies that money revolves within the community. Collectively the farmers are not only developing their productive capacity, but also strengthening the local institution through which marketing and value addition are carried out. Equally they are strengthening their financial services institution, the local SACCO. Fig. 1 illustrates the linkages and relationships between the actors in the ACE model.

Figure 1 : Structural relationship between farmers, RPOs, ACEs and SACCOs

Savings & Credit Cooperative

(SACCO)

Area Cooperative

Enterprise

(ACE)

Primary Society

(RPO)

Members

(Individual farmers)

Shares plus ideasShares plus ideas

Marketing ServicesValue Addition

Farmers’ Advisory Services, Marketing Services

FinancialServices

FinancialServices

Shares & savings + ideasSavings facility, loans + other financial services

Shares & savings + ideasShares & savings + ideas

5 Figure 1 illustrates the integration and functioning of critical institutional arrangements in order to maximize service delivery to the farmers.

Chap

ter 5

SAC

COs

and

MFI

s

154154

2.2 Legal and management structure

Unlike the heavy organizational structure typical of many cooperative unions, ACEs have a very lean, small and flexible structure, with 2 -5 staff and a Board composition of between 5 – 11 members. The Board members of an ACE are elected from the constituent primary societies. The Board in turn appoints management and continues to maintain an oversight role over the business. Ideally, each ACE has a manager well qualified in Agribusiness or Agricultural Marketing, an accountant, and an input shop attendant. Other possible posts include: an extension worker, a store manager and a security guard.

Area Cooperative Enterprises are member managed, member used, member controlled and exist to provide benefits to members. This implies that farmers through their RPOs have full control and ownership over these enterprises. Decisions are taken collectively through their annual general meetings (AGMs).

2.3 Cost implications for starting and supporting an ACE over a 3-year period

Table 1.0 indicates the required resources for setting up one Area Cooperative Enterprise supported by 5 RPOs. The Uganda Cooperative Alliance (UCA), as the champion of the model, has worked tirelessly to popularize it among the already existing cooperatives and farmer groupings. Initial support can thus be harnessed from UCA. The Microfinance Support Centre Ltd. (MSC) has also designed financial and non-financial products and services dedicated to meeting ACEs’ short and long-term needs.

Note:

a) The training and monitoring for which budgetary provision is made above is carried out by UCA, with some assistance from MSC.

b) UCA expects the ACEs and their member RPOs to gain self-sufficiency within a reasonable period, with the target being three years.

Drying maize outside Kisiita ACE warehouse

155155

Table 1: Cost Estimates for Establishing one ACE with five RPOs (UGX ‘000)

Activity RPOs No.

ACEs No.

Unit CostUGX

1st year UGX

2nd year UGX

3rd year UGX

Total for3 years

Source: Adapted from Uganda Cooperative Alliance, Monthly Reports 2010.

5

5

5

1

1

5

5

5

5

5

1

1

1

1

1

1

1

1

1

1

1,000

1,000

100

10,000

10,000

150

4,000

50 pcm6

350

100

100 pcm

200 pcm

12,000

200 pcm

500

100

600 pa

2,000

6,000

6,000

500

10,000

10,000

150

4,000

36,650

600

1,750

500

6,000

2,400

12,000

2,400

500

1,200

3,600

2,000

7,500

40,450

77,100

0

3,000

0

6,000

5,000

0

4,000

18,000

600

500

6,000

2,400

6,000

2,400

1,200

4,000

2,000

3,250

28,350

46,350

0

3,000

0

6,000

5,000

0

4,000

18,000

600

250

6,000

2,400

6,000

2,400

600

4,000

2,000

24,250

42,250

72,650

93,050

165,700

Mobilise members

Mobilise membership fees and share

capital

Registration of primary societies

Train leaders & members in governance

Train leaders & managers in basic financial

management

Registration of the ACE

Monitoring

SUB-TOTALS

Office rent for RPOs

Basic furniture for RPOs

Basic stationery for RPOs

Management support to RPOs (salaries)

Management support to ACE (salary)

Training ACE leaders

ACE office rent

Basic furniture for ACE

Basic stationery & supplies for ACE

Vehicle maintenance & running cost (UCA

expense)

Monitoring

Contingency

SUB-TOTALS

GRAND TOTALS

Note: (a) The training and monitoring for which budgetary provision is made above is carried out by UCA with some assistance from MSC.

(b) UCA expects the ACEs and their member RPOs to gain self-sufficiency within a reasonable period, with the target being three years.

6 pcm = per calendar month

Chap

ter 5

SAC

COs

and

MFI

s

156156

Section 3 ACE Products, Services and Operations

3.1 The ACE business model

Area Cooperative Enterprises act as commission agents. They neither buy nor hold title to members’ commodities. Unlike traditional Unions, members under the ACE model have full control and ownership of their produce throughout the value chain until a buyer is identified. As commission agents, ACEs charge a percentage of the sold commodity on behalf of its members. This varies from ACE to ACE but ranges between 5 – 10 percent and is agreed upon collectively by the members in the AGM. They also charge for other services rendered to farmers. These might include: tractor hire, input supplies, sorting and cleaning farmers’ produce, drying and transportation. This commission is shared with the RPOs on an agreed sharing arrangement.

3.2 ACE products

Individual ACEs handle three commodities at any one time. The limit of three is selected since it gives enough spread to manage risk (including ensuring food security), while still permitting advantages of scale and specialization.

Because of their flexibility, ACEs can drop non-performing enterprises and replace them with profitable ones. For each of these enterprises, the ACE provides extension services and inputs to farmers to ensure standardization in output quality.

Within Uganda, ACEs are found marketing a whole range of commodities/products such as grains, fish (from ponds), livestock, milk, horticultural products, apiary products, and

others, in addition to the traditional export commodities i.e. coffee and cotton.

3.3 Services provided by ACEs

• Provision of market information. In collaboration with firms and organizations such as FIT-Uganda and the Uganda Commodities Exchange (UCE) ACEs provide information on prevailing market prices to their members via cellphone messages. They also have a public notice board where commodity prices are posted and updated daily.

• Input delivery. ACEs play an important role in the delivery of agricultural inputs. They form a link between farmers and input dealers. Each ACE has an input shop, where individual farmers can access improved inputs at favourable prices.

• Commodity bulking. Bulking is very essential considering that small-scale producers are scattered, making it difficult for them to access markets and also undermining their bargaining power in the market. ACEs come in as a second tier to further consolidate quantities which have already been mobilized by the members of primary societies. The aim of bulking (or assembly) is to attract good buyers.

• Linking farmers to markets. There are four ways in which ACEs link farmers to markets. i) Bulking and selling to competing buyers ii) Negotiating contract farming arrangements with buyers iii) Bulking and arranging warehouse receipts, thus enabling farmers to borrow while stocks are held and buyers are sought iv) Bulking and selling through the Uganda Commodity Exchange (UCE).

No. ACE District

1.

2.

3.

4.

5.

6.

Jinja9

Kyenjojo10

Mbale11

Mbarara12

Mukono13

Other regions14

Source: Uganda Cooperative Alliance monthly reports, June 2010

Total

Total Membership8

9,273

6,151

14,856

11,133

8,806

14,127

64,346

Turnover (UGX)

2,027,636,800

1,746,607,800

2,001,224,698

5,977,205,040

2,041,238,150

2,950,409,951

16,744,322,439

8

9

14

14

9

12

66

Notes8The total membership here represents the total individual farmers9The ACEs are located in Kaliro, Iganga, Kamuli and Jinja10The institution are located in Mubende, Kamwenge, Kibaale and Kasese11ACEs are located in Sironko, Manafwa, Kapchorwa, Kumi and Bududa12The districts include: Ntungamo, Masaka, Kanungu, Bushenyi and Rukungiri13The districts include: Kayunga, Mukono and Nakasongola14These districts include: Nebbi, Arua, Apach, Lira and Masindi

Table 2: Current spread of ACEs by region, total membership and annual turnover

• Quality assurance. ACEs ensure quality and standards enforcement for trade enterprises. A farmer whose produce does not meet the standards may have it rejected. ACEs thus undertake post-harvest handling activities such as drying grain to the required moisture level.

• Value addition. ACEs add value to farmers’ produce, giving them a better return on their commodities. The ACE only charges a small fee to the farmer for the value added. For example, instead of selling grain maize, farmers collectively grind the maize and sell flour to big institutions such as schools within the locality. Through ACEs, some farmers are also making wine and other products from bananas and other fruits.

• Linkage to financial services. ACEs, just like primary societies, are linked to SACCOs. Although farmers directly affiliate to SACCOs, when they borrow using the quasi warehouse receipt model, they need the assistance of their ACE. Once produce is deposited under the care of the ACE, the latter makes a recommendation to the SACCO for those farmers considered to be suitable borrowers. Indeed, it is the ACE itself that issues the Warehouse Receipt, which