a ppendix 4d half year report for personal use only · includes the “harvey norman” and...

TRANSCRIPT

A

APPENDIX 4

Appendix Half-Year E

Key Dates

28 February

12 April 20136 May 2013 30 August 20

Contents

Company InResults for AChairman’s Directors’ ReStatement oIncome StatStatement oStatement oStatement oOperating SNotes to andfor the Half-YOther InformDirectors’ DeIndependen

Company InRegistered OA1 RichmondHomebush WPh: 02 9201 Fax: 02 9201Company SeMr Chris Men

4D / HALF –

4D / Half-YEnded 31 D

2013

3

013

nformation Announcemen

Report eport of Financial Potement of Comprehenof Changes in of Cash Flows Segments d forming parYear Ended 3

mation eclaration nt Review Rep

nformation Office: d Road

West NSW 2140 6111 6250

ecretary: ntis

– YEAR REPO

Year ReportDECEMBER 2

AnnouncemAnnouncemRecord datePayment of IAnnouncemAnnouncem

nt to the Marke

osition

nsive Income Equity

rt of the Financ1 December 2

port

0

Share RBoardroLevel 7,Sydney Ph: 02 AuditorErnst & Y

ORT

t 2012

ment of Half-Yement of Interim e for determiniInterim 2013 D

ment of Full Yeament of Final 20

et

cial Statemen2012

Registry: oom Pty Limite 207 Kent Stre NSW 2000 9290 9600 s: Young

ear Profit to 31 2013 Dividending entitlemen

Dividend ar Profit to 30 J013 Dividend

nts

ed eet

StocHarvsharSecu

SolicBrow

December 20d nt to Interim 20

June 2013

ck Exchange Lvey Norman Hes are quotedurities Exchang

citors: wn Wright Stein

012

013 Dividend

1111112

2444

Listing: Holdings Limited on the Austrage Limited (“A

n

1 2 3

12 14 15 16 17 19 21

26 41 42 43

ed alian

ASX”)

1

For

per

sona

l use

onl

y

2

RESULTS FOR ANNOUNCEMENT TO THE MARKET

Financial Highlights HY2011 Dec-10

HY2012 Dec-11

HY2013 Dec-12

No. of franchised outlets in Australia1

198

216

211

No. of franchisees in Australia

676

697

683

No. of company-operated stores2

95

73

77

Franchisee sales revenue1

$2.74bn

$2.58bn

$2.44bn

Company-operated sales revenue2

$804.13m

$806.88m

$676.94m

Other revenues and other income items

$590.38m

$584.11m

$548.82m

Earnings before interest and tax (EBIT)

$219.96m

$188.12m

$123.03m

Earnings before interest, tax, depreciation, amortisation and impairment

$265.11m

$230.87m

$167.36m Net Australian property revaluation (decrement) / increment

($4.98m)

$8.21m

($44.97m)

Profit after tax and non-controlling interests

$131.67m

$128.95m

$81.92m

Net cash flows from operating activities

$93.52m

$19.88m

$133.89m

Basic earnings per share

12.39c

12.14c

7.71c

Dividends per share (fully franked)

6.0c

5.0c

4.5c

Net debt to equity ratio (%)

25.12%

29.74%

27.24%

1 Sales made by franchisees in Australia do not form part of the financial results of the consolidated entity.

2 Includes the “Harvey Norman” and “Norman Ross” branded company-operated stores in New Zealand, Ireland, Northern Ireland, Singapore, Malaysia, Slovenia

and Croatia and the “Clive Peeters” and “Rick Hart” branded company-operated stores in Australia (prior to the restructure).

For

per

sona

l use

onl

y

CHAIRMAN’S REPORT

3

Business Performance Macroeconomic conditions in Australia and the global markets in which we operate remain tough. Whilst the aggressive discounting experienced in the second half of 2012 has stabilised, particularly in the last few months of the first half of 2013, and pleasingly we are seeing an uptick in sales. The historical lows we are seeing in interest rates and home loans should start moving the consumer back into the buying cycle from the savings cycle. Harvey Norman will be a beneficiary of this given the diverse homemaker categories in which Harvey Norman franchisees operate in. Homemaker retail will strengthen as housing and equities improve. Over the past year we have continued to execute the Harvey Norman omni channel strategy. The strategic initiatives require that Harvey Norman franchisees invest in their people, and deliver the best customer experience by focussing on the core mantras of “Quality”, “Value” and “Service”, in every communication, transaction and service with the customer. The critical focus on “best customer experience” is embodied in the new Harvey Norman “Shop with Confidence” marketing campaign, launched in February 2013.

The Harvey Norman digital, store and distribution channels are fully integrated. Consumers are clearly supporting the Harvey Norman franchisee click, pay and collect in store capability. This operating model enables Harvey Norman franchisees to deliver product and services to customers through the established wide network of Harvey Norman stores in metropolitan, regional and country areas. The integration of digital communication and transactions with physical franchised stores is a significant competitive advantage for Harvey Norman franchisees. The omni channel strategy, incorporating the Harvey Norman integrated retail, franchise, property and digital platform, is robust and the most viable format to effectively compete in a difficult market. The omni channel strategy and initiatives provide strategic advantages over competitors including: 1. The ability of Harvey Norman franchisees to diversify the product offering, focus on more profitable product

categories and adapt to the changing retail landscape - unlike many competitors which are solely exposed to the challenging audio visual and information technology (“AV/IT”) category. Harvey Norman franchisees operate in a number of different product categories that continue to perform solidly. The Harvey Norman franchise operating model is flexible and resilient, enabling diversification and tailoring of the product offering of franchisees towards the more profitable homemaker categories.

2. A strong balance sheet underpinned by real, tangible property assets – as at balance date, we have a total asset base of $4.27 billion which is inclusive of a property portfolio valued at $2.14 billion. Our strong balance sheet affords access to capital and seizes opportunities in the marketplace as they arise.

3. Our strong asset position and prudent management of working capital allows us to conservatively manage our debt levels and maintain a low net debt to equity ratio of 27.24%.

4. The integration of digital, e-commerce and physical stores enables complete customer choice and satisfaction with click, pay and collect in store capability.

The challenging retail environment resulted in a net profit before tax of $99.55 million for the half-year ended 31 December 2012 compared to $163.47 million for the previous period, a decrease of $63.92 million or 39.1%. This result is inclusive of a net property revaluation decrement of $44.97 million before tax for the period compared to a net property revaluation increment of $11.07 million before tax for the preceding half year ($8.20 million attributable to the Australian investment properties and $2.87 million attributable to the reversal of a previous property revaluation decrement in Slovenia), a deterioration of $56.04 million before tax. Excluding the impact of the net property revaluation adjustments from both periods, the net profit before tax would have been $144.52 million for the current period compared to $152.40 million for the previous period, a reduction of $7.88 million or 5.2%. F

or p

erso

nal u

se o

nly

4

CHAIRMAN’S REPORT (CONTINUED) Financial Analysis and Commentary: Net Profit After Tax and Non-Controlling Interests Net profit after tax and non-controlling interests was $81.92 million for the half-year ended 31 December 2012 compared with $128.95 million for the preceding period, a decrease of $47.02 million or 36.5%. This result is inclusive of a net revaluation decrement attributable to investment properties and joint ventures in Australia of $31.48 million after tax compared to a net revaluation increment in the previous period of $8.07 million after tax, a devaluation of $39.55 million since the previous corresponding period. If the effects of the net property revaluation adjustments were excluded from the result, the net profit after tax and non-controlling interests for the half-year ended 31 December 2012 would have been $113.40 million compared to $120.88 million for the prior period, a reduction of $7.48 million or 6.2%. Net profit was impacted by the following: the net property revaluation decrement of $44.97 million before tax ($31.48 million after tax) recorded by the

Australian investment property portfolio and joint venture entities for the current period compared to a net revaluation increment of $11.07 million before tax ($8.07 million after tax) in the prior period, a deterioration of $56.04 million before tax ($39.55 million after tax);

a reduction in the profitability of the franchising operations segment by $24.50 million or 25.6% before tax ($17.15 million after tax) due to lower franchise fees and a higher level of tactical support offered to franchisees during the current half and leading into the critical Christmas trading period. The aggregate amount of tactical support provided to franchisees was $63.80 million in the current period compared to $45.30 million in the preceding period (tactical support is included in other expenses from ordinary activities);

the profit of $10.00 million before tax ($7.00 million after tax) that was recognised on the successful completion and opening of the Springvale development during the previous half-year;

an increase of $9.72 million before tax ($6.80 million after tax) in rent received from franchisees and third party tenants;

an appreciation of $8.12 million before tax ($5.68 million after tax) in the market value of the listed public securities and dividends received by the consolidated entity; and

restructuring and closure costs recognised in the previous period for the restructure of the Clive Peeters and Rick Hart businesses of $8.07 million before tax ($5.65 million after tax).

The tax charge in the income statement was lower by $15.74 million for the half-year ended 31 December 2012 compared to prior period mainly due to a reduction in profit before tax from $163.47 million in the previous period to $99.55 million in the current period, a decrease of $63.92 million. This translated to a reduction in our tax liability by approximately $20 million which was offset by a reduction in income tax benefits by approximately $4 million.

Key Elements of an Integrated Retail, Franchise, Property and Digital System

Review of the Franchising Operations Segment in Australia: Franchise sales revenue generated by independent franchisees amounted to $2.44 billion for the half-year ended 31 December 2012 compared with $2.58 billion for the preceding period, a decline of 5.3%. The reduction in franchisee sales has translated into a reduction in the segment result recorded by our franchising operations. The AV/IT categories continue to be challenged with deflationary headwinds affecting average selling prices and margins. However, the consolidation that occurred in the AV/IT market in the second half of 2012 places our franchisees in good stead to take advantage of any resurgence in that category. The other Homemaker Retail categories of home appliances, furniture and bedding remain stable and the businesses are well-placed for any upturn in housing starts. The result before tax of the franchising operations segment was $71.01 million for the half-year ended 31 December 2012 compared to $95.51 million for the preceding half, a reduction of $24.50 million or 25.6%. The result is after the provision of tactical support of $63.80 million in the current period compared to $45.30 million in the preceding period. Included in the tactical support of $63.80 million is $7.60 million of tactical support provided to closed Harvey Norman and rebranded ex Clive Peeters / Rick Hart stores. In accordance with our strategic omni channel initiatives, we provided tactical support to our franchisees over the crucial Christmas trading period. This enabled franchisees to invest in their people to deliver the best customer experience in every communication, transaction and service whether in store or online. Franchise fees received from our franchisees have reduced relative to prior period. Gross revenue from the franchising operations segment has reduced from $466.26 million in the previous half-year to $444.38 million for the half-year ended 31 December 2012, a reduction of $21.88 million or 4.7%. The Harvey Norman omni channel strategy requires us to provide our franchisees with tactical support, when and where necessary to enable them to effectively compete in their local markets. The provision of tactical support to franchisees has increased relative to prior period.

For

per

sona

l use

onl

y

5

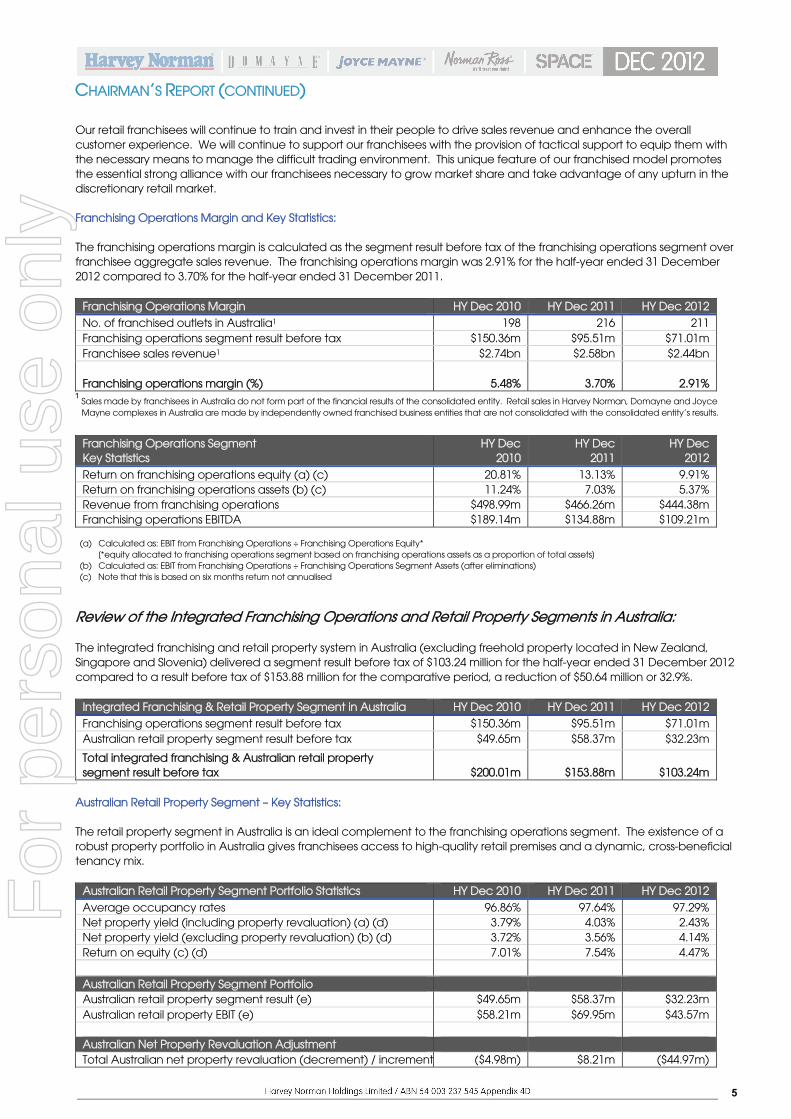

CHAIRMAN’S REPORT (CONTINUED) Our retail franchisees will continue to train and invest in their people to drive sales revenue and enhance the overall customer experience. We will continue to support our franchisees with the provision of tactical support to equip them with the necessary means to manage the difficult trading environment. This unique feature of our franchised model promotes the essential strong alliance with our franchisees necessary to grow market share and take advantage of any upturn in the discretionary retail market. Franchising Operations Margin and Key Statistics: The franchising operations margin is calculated as the segment result before tax of the franchising operations segment over franchisee aggregate sales revenue. The franchising operations margin was 2.91% for the half-year ended 31 December 2012 compared to 3.70% for the half-year ended 31 December 2011.

Franchising Operations Margin HY Dec 2010 HY Dec 2011 HY Dec 2012 No. of franchised outlets in Australia1 198 216 211 Franchising operations segment result before tax $150.36m $95.51m $71.01m Franchisee sales revenue1 $2.74bn $2.58bn $2.44bn Franchising operations margin (%)

5.48%

3.70%

2.91%

Franchising Operations Segment Key Statistics

HY Dec 2010

HY Dec 2011

HY Dec 2012

Return on franchising operations equity (a) (c) 20.81% 13.13% 9.91% Return on franchising operations assets (b) (c) 11.24% 7.03% 5.37% Revenue from franchising operations $498.99m $466.26m $444.38m Franchising operations EBITDA $189.14m $134.88m $109.21m

Review of the Integrated Franchising Operations and Retail Property Segments in Australia: The integrated franchising and retail property system in Australia (excluding freehold property located in New Zealand, Singapore and Slovenia) delivered a segment result before tax of $103.24 million for the half-year ended 31 December 2012 compared to a result before tax of $153.88 million for the comparative period, a reduction of $50.64 million or 32.9%.

Integrated Franchising & Retail Property Segment in Australia HY Dec 2010 HY Dec 2011 HY Dec 2012 Franchising operations segment result before tax $150.36m $95.51m $71.01m Australian retail property segment result before tax $49.65m $58.37m $32.23m

Total integrated franchising & Australian retail property segment result before tax

$200.01m

$153.88m

$103.24m

Australian Retail Property Segment – Key Statistics: The retail property segment in Australia is an ideal complement to the franchising operations segment. The existence of a robust property portfolio in Australia gives franchisees access to high-quality retail premises and a dynamic, cross-beneficial tenancy mix.

Australian Retail Property Segment Portfolio Statistics HY Dec 2010 HY Dec 2011 HY Dec 2012

Average occupancy rates 96.86% 97.64% 97.29% Net property yield (including property revaluation) (a) (d) 3.79% 4.03% 2.43% Net property yield (excluding property revaluation) (b) (d) 3.72% 3.56% 4.14% Return on equity (c) (d) 7.01% 7.54% 4.47% Australian Retail Property Segment Portfolio Australian retail property segment result (e) $49.65m $58.37m $32.23m Australian retail property EBIT (e) $58.21m $69.95m $43.57m Australian Net Property Revaluation Adjustment Total Australian net property revaluation (decrement) / increment ($4.98m) $8.21m ($44.97m)

(a) Calculated as: EBIT from Franchising Operations ÷ Franchising Operations Equity* [*equity allocated to franchising operations segment based on franchising operations assets as a proportion of total assets] (b) Calculated as: EBIT from Franchising Operations ÷ Franchising Operations Segment Assets (after eliminations) (c) Note that this is based on six months return not annualised

1 Sales made by franchisees in Australia do not form part of the financial results of the consolidated entity. Retail sales in Harvey Norman, Domayne and Joyce

Mayne complexes in Australia are made by independently owned franchised business entities that are not consolidated with the consolidated entity’s results.

For

per

sona

l use

onl

y

6

CHAIRMAN’S REPORT (CONTINUED)

(a) Calculated as: EBIT from Australian Retail Property Segment (including Australian net revaluation increments / (decrements)) ÷ Australian Retail Property Segment Assets (after eliminations) (b) Calculated as: EBIT from Australian Retail Property Segment (excluding Australian net revaluation increments / (decrements)) ÷ Australian Retail Property Segment Assets (after eliminations) (c) Calculated as: EBIT from Australian Retail Property Segment (including Australian net revaluation increments / (decrements)) ÷ Australian Retail Property Equity* [*equity allocated to Australian retail property segment based on Australian retail property assets as a proportion of total assets] (d) Note that this is based on six months return not annualised (e) The Australian retail property segment result and EBIT figures are inclusive of the Australian net revaluation increments/ (decrements)

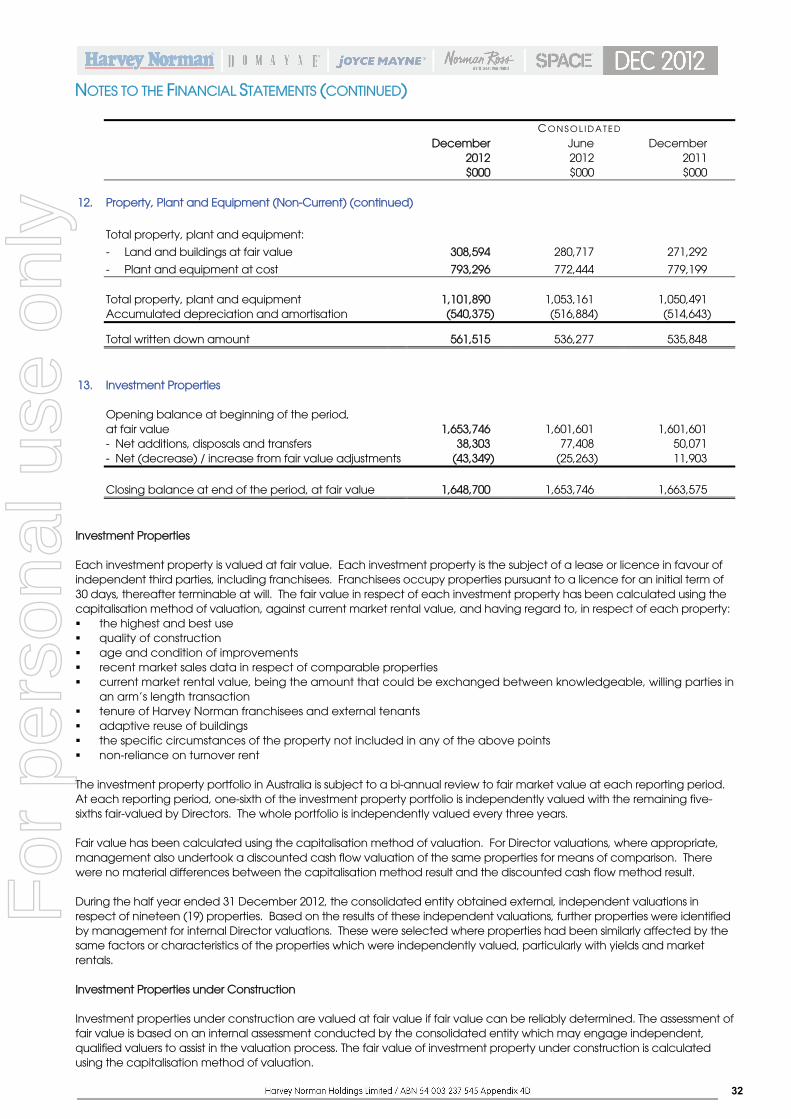

Australian Net Property Revaluation Adjustments: The investment property portfolio in Australia is subject to a bi-annual review to fair market value at each reporting period. At each reporting period, one-sixth of the investment property portfolio is independently valued with the remaining five-sixths fair-valued by Directors. The whole portfolio is independently valued every three years. During the half-year ended 31 December 2012, nineteen (19) properties in Australia have been independently valued. The balance of the portfolio was reviewed resulting in the preparation of internal valuations for seven (7) additional sites. The valuation for the period resulted in a net decrement of $44.97m in Australia. The decrements in Australia were generally the result of development losses and a revaluation of a property which was affected by flooding. The values of established properties within the portfolio have remained relatively stable. Recent developments in Springvale, Maroochydore and Devonport have generated the majority of the decrement. I believe these properties will contribute to increases in operating income in the future. The flooding in Queensland in 2011 affected the value of a property in Oxley, Queensland. No other properties in the portfolio have been significantly affected by the flooding that happened in 2011 and the recent flooding that occurred in January 2013, post the valuation date. Valuations are undertaken on the basis that Harvey Norman stores are on a 30 day licence arrangement. The occupancy rate is 97.29% in December 2012 compared to 96.94% in June 2012.

Review of the Property Portfolio of the Consolidated Entity: Total Property Portfolio of the Consolidated Entity (Inclusive of Freehold Property located in New Zealand, Singapore and Slovenia): A strong property portfolio is an essential component of the Harvey Norman omni channel strategy. Physical stores and distribution centres are key channels that are integrated with Harvey Norman e-commerce operations. Since inception, we have adopted a selective and prudent acquisition and development strategy. Overall, the property portfolio remains fundamentally strong. It has high occupancy rates, growing revenue streams and it is anticipated to have a strong upside for capital growth. Operating profits have been robust as the business continues to focus on improving revenue streams and operating costs. Harvey Norman has no new developments in the short term, but is well positioned to acquire quality investment grade properties to complement its existing portfolio. It continues to focus on opportunities to upgrade existing properties within the portfolio to improve income, building layouts, tenancy commitments and capital growth. Our consolidated property portfolio is valued at $2.14 billion as at 31 December 2012. This represents over 50% of our total asset base as at balance date. The result before tax generated by our property segments represents 40.8% of our consolidated profit before tax for the half-year ended 31 December 2012 if we excluded the impact of the net property revaluation decrement for the period. The segment result before tax of our property segments was $14.00 million for the half-year ended 31 December 2012 compared to a result of $68.77 million for the previous half, a decrease of $54.77 million or 79.6%. Included in the segment result before tax was a contribution of $6.19 million from mining camp accommodation ($1.25 million for the previous corresponding period). If the net property revaluation adjustments were excluded from both years, the segment result before tax would have been $58.97 million for the current period compared to $57.70 million for the preceding half, an increase of $1.27 million or 2.2%. The preceding half result included a one off $10 million profit on the successful completion and opening of the Springvale development.

For

per

sona

l use

onl

y

7

CHAIRMAN’S REPORT (CONTINUED)

Composition of the Property Portfolio

HY Dec 2010 $000

HY Dec 2011 $000

HY Dec 2012 $000

Investment properties 1,395,200 1,593,557 1,620,915 Investment properties under construction

148,879

70,018

27,785

Joint venture properties 163,630 154,495 162,512 Owned land & buildings in New Zealand, Singapore, Slovenia & Australia

252,196

271,292

308,594 Properties held for resale 17,626 26,651 23,757 Total Property Portfolio 1,977,531 2,116,013 2,143,563

Benefits of Property Ownership: Property ownership delivers the following benefits to the consolidated entity: The presence of Harvey Norman, Domayne or Joyce Mayne franchisees as anchor tenants in a complex is a key

drawcard to attract superior national third-party tenants and quality local operators to co-locate within the same complex. This provides us with a distinct advantage in its ability to create a solid, dynamic and cross-beneficial tenancy mix in order to maximise the profitability of the retail property segment.

Despite the softening retail sector, property ownership delivers a steady and reliable income stream in the form of rent charged to franchisees and complementary third-party tenants.

A large property portfolio under management creates economies of scale, delivers operational cost efficiencies and enhanced negotiating power in the property sector.

Breakdown of Owned and Leased Sites: Geographic Spread: This diagram displays the geographic spread of the franchised Harvey Norman (“HN”), Domayne (“DM”) and Joyce Mayne (“JM”) franchised complexes in the Australian market, the Harvey Norman and Norman Ross (“NR”) branded company-operated stores in New Zealand, Ireland, Northern Ireland, Singapore, Malaysia, Slovenia and Croatia as at 31 December 2012.

31 December 2012 Number of Owned

Sites

Number of Leased

Sites *

Total

Australia: Franchised complexes 79 132 211 New Zealand 17 15 32 Slovenia 5 - 5 Croatia - 1 1 Ireland & Northern Ireland - 15 15 Asia - 24 24 TOTAL 101 187 288

The Harvey Norman property portfolio consists of Harvey Norman, Domayne and Joyce Mayne complexes in Australia, Harvey Norman and Norman Ross stores in New Zealand, properties located in Singapore, Harvey Norman stores in Slovenia, properties held under joint venture agreements and land and buildings in Australia for development and resale at a profit.

* leased from external parties

For

per

sona

l use

onl

y

8

CHAIRMAN’S REPORT (CONTINUED)

1.20

1.22

1.24

1.26

1.28

1.30

0

100

200

300

400

Dec 2010 Dec 2011 Dec 2012

New Zealand Sales Revenue

NZ Sales in $AUD NZ Sales in $NZD FX Rates

Acquisitions, New Complex and Store Openings, Closures and Conversions: Franchised Complex Openings, Conversions and Closures Six (6) new franchised Harvey Norman complexes, located at Gunnedah (NSW), Tura Beach (NSW), Eden (NSW), Ararat (VIC), Broken Hill (NSW) and Maroochydore (QLD) commenced trading during the half-year ended 31 December 2012. One (1) new franchised Domayne complex commenced trading at Maroochydore, QLD. We continue to assess the viability of all of our stores and during the current period we closed nine (9) stores, two (2) of which were incorporated into the landmark development at Maroochydore which commenced trading in November 2012. There were 211 franchised complexes in Australia as at 31 December 2012 under the following brand names: Harvey Norman 180 Domayne 17 Joyce Mayne 14

Company-Operated Store Openings and Closures in Offshore Markets As at 31 December 2012 there were 77 company-operated stores located in offshore markets. One (1) new store was opened in Mt. Roskill, New Zealand in November 2012 bringing the total number of stores in New Zealand to thirty-two (32) trading under the Harvey Norman and Norman Ross brand names. One (1) new store was opened in Ampang Point, Malaysia in December 2012, bringing the total number of Harvey Norman stores in Malaysia to eleven (11). The Mullingar store in Ireland closed in August 2012 as part of the restructure in Ireland that was announced in July 2012. There are now thirteen (13) stores trading in Ireland and two (2) stores in Northern Ireland. There were no store openings or closures in Singapore (13 stores), Slovenia (5 stores) or Croatia (1 store).

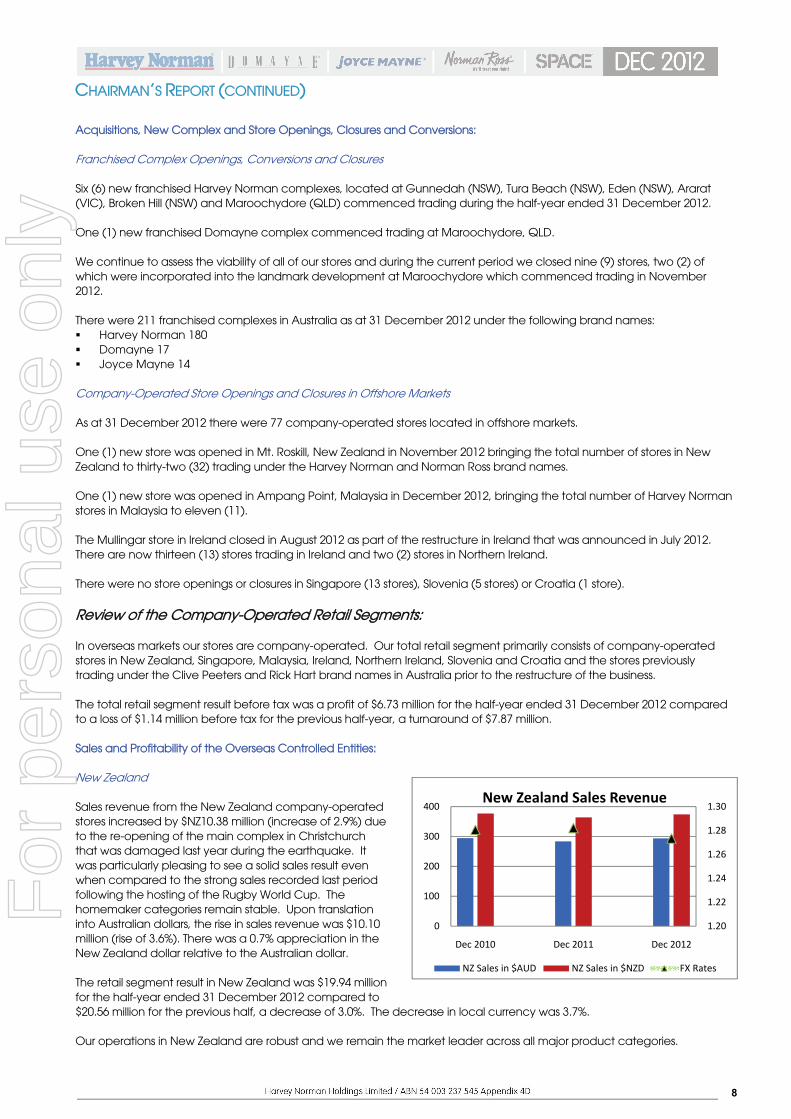

Review of the Company-Operated Retail Segments: In overseas markets our stores are company-operated. Our total retail segment primarily consists of company-operated stores in New Zealand, Singapore, Malaysia, Ireland, Northern Ireland, Slovenia and Croatia and the stores previously trading under the Clive Peeters and Rick Hart brand names in Australia prior to the restructure of the business. The total retail segment result before tax was a profit of $6.73 million for the half-year ended 31 December 2012 compared to a loss of $1.14 million before tax for the previous half-year, a turnaround of $7.87 million. Sales and Profitability of the Overseas Controlled Entities: New Zealand Sales revenue from the New Zealand company-operated stores increased by $NZ10.38 million (increase of 2.9%) due to the re-opening of the main complex in Christchurch that was damaged last year during the earthquake. It was particularly pleasing to see a solid sales result even when compared to the strong sales recorded last period following the hosting of the Rugby World Cup. The homemaker categories remain stable. Upon translation into Australian dollars, the rise in sales revenue was $10.10 million (rise of 3.6%). There was a 0.7% appreciation in the New Zealand dollar relative to the Australian dollar. The retail segment result in New Zealand was $19.94 million for the half-year ended 31 December 2012 compared to $20.56 million for the previous half, a decrease of 3.0%. The decrease in local currency was 3.7%. Our operations in New Zealand are robust and we remain the market leader across all major product categories.

For

per

sona

l use

onl

y

9

CHAIRMAN’S REPORT (CONTINUED)

1.23

1.24

1.25

1.26

1.27

1.28

1.29

1.30

0

50

100

150

200

250

Dec 2010 Dec 2011 Dec 2012

Asian Sales Revenue

Asian Sales in AUD Asian Sales in SGD FX Rates

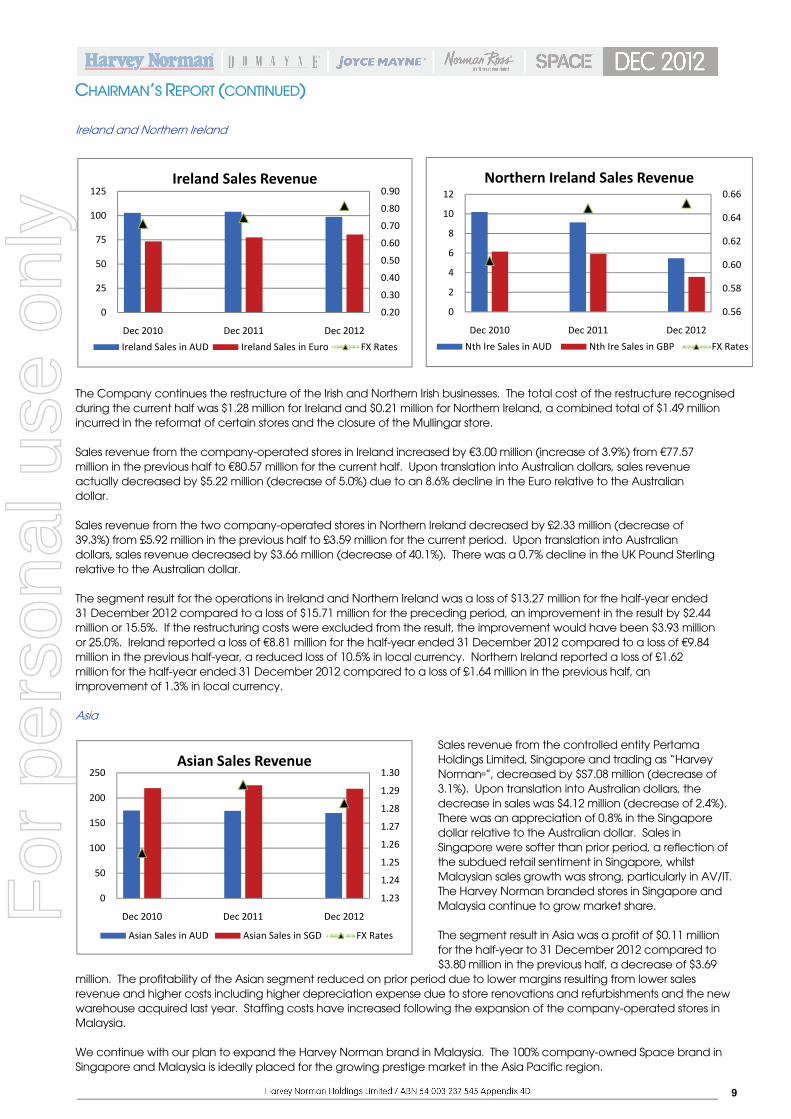

Ireland and Northern Ireland The Company continues the restructure of the Irish and Northern Irish businesses. The total cost of the restructure recognised during the current half was $1.28 million for Ireland and $0.21 million for Northern Ireland, a combined total of $1.49 million incurred in the reformat of certain stores and the closure of the Mullingar store. Sales revenue from the company-operated stores in Ireland increased by €3.00 million (increase of 3.9%) from €77.57 million in the previous half to €80.57 million for the current half. Upon translation into Australian dollars, sales revenue actually decreased by $5.22 million (decrease of 5.0%) due to an 8.6% decline in the Euro relative to the Australian dollar. Sales revenue from the two company-operated stores in Northern Ireland decreased by £2.33 million (decrease of 39.3%) from £5.92 million in the previous half to £3.59 million for the current period. Upon translation into Australian dollars, sales revenue decreased by $3.66 million (decrease of 40.1%). There was a 0.7% decline in the UK Pound Sterling relative to the Australian dollar. The segment result for the operations in Ireland and Northern Ireland was a loss of $13.27 million for the half-year ended 31 December 2012 compared to a loss of $15.71 million for the preceding period, an improvement in the result by $2.44 million or 15.5%. If the restructuring costs were excluded from the result, the improvement would have been $3.93 million or 25.0%. Ireland reported a loss of €8.81 million for the half-year ended 31 December 2012 compared to a loss of €9.84 million in the previous half-year, a reduced loss of 10.5% in local currency. Northern Ireland reported a loss of £1.62 million for the half-year ended 31 December 2012 compared to a loss of £1.64 million in the previous half, an improvement of 1.3% in local currency. Asia

Sales revenue from the controlled entity Pertama Holdings Limited, Singapore and trading as “Harvey Norman®”, decreased by $S7.08 million (decrease of 3.1%). Upon translation into Australian dollars, the decrease in sales was $4.12 million (decrease of 2.4%). There was an appreciation of 0.8% in the Singapore dollar relative to the Australian dollar. Sales in Singapore were softer than prior period, a reflection of the subdued retail sentiment in Singapore, whilst Malaysian sales growth was strong, particularly in AV/IT. The Harvey Norman branded stores in Singapore and Malaysia continue to grow market share. The segment result in Asia was a profit of $0.11 million for the half-year to 31 December 2012 compared to $3.80 million in the previous half, a decrease of $3.69

million. The profitability of the Asian segment reduced on prior period due to lower margins resulting from lower sales revenue and higher costs including higher depreciation expense due to store renovations and refurbishments and the new warehouse acquired last year. Staffing costs have increased following the expansion of the company-operated stores in Malaysia. We continue with our plan to expand the Harvey Norman brand in Malaysia. The 100% company-owned Space brand in Singapore and Malaysia is ideally placed for the growing prestige market in the Asia Pacific region.

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0

25

50

75

100

125

Dec 2010 Dec 2011 Dec 2012

Ireland Sales Revenue

Ireland Sales in AUD Ireland Sales in Euro FX Rates

0.56

0.58

0.60

0.62

0.64

0.66

0

2

4

6

8

10

12

Dec 2010 Dec 2011 Dec 2012

Northern Ireland Sales Revenue

Nth Ire Sales in AUD Nth Ire Sales in GBP FX Rates

For

per

sona

l use

onl

y

10

CHAIRMAN’S REPORT (CONTINUED)

0.65

0.70

0.75

0.80

0.85

0

10

20

30

40

50

Dec 2010 Dec 2011 Dec 2012

Slovenian & Croatian Sales Revenue

Slov Sales in AUD Slov Sales in Euro FX Rates

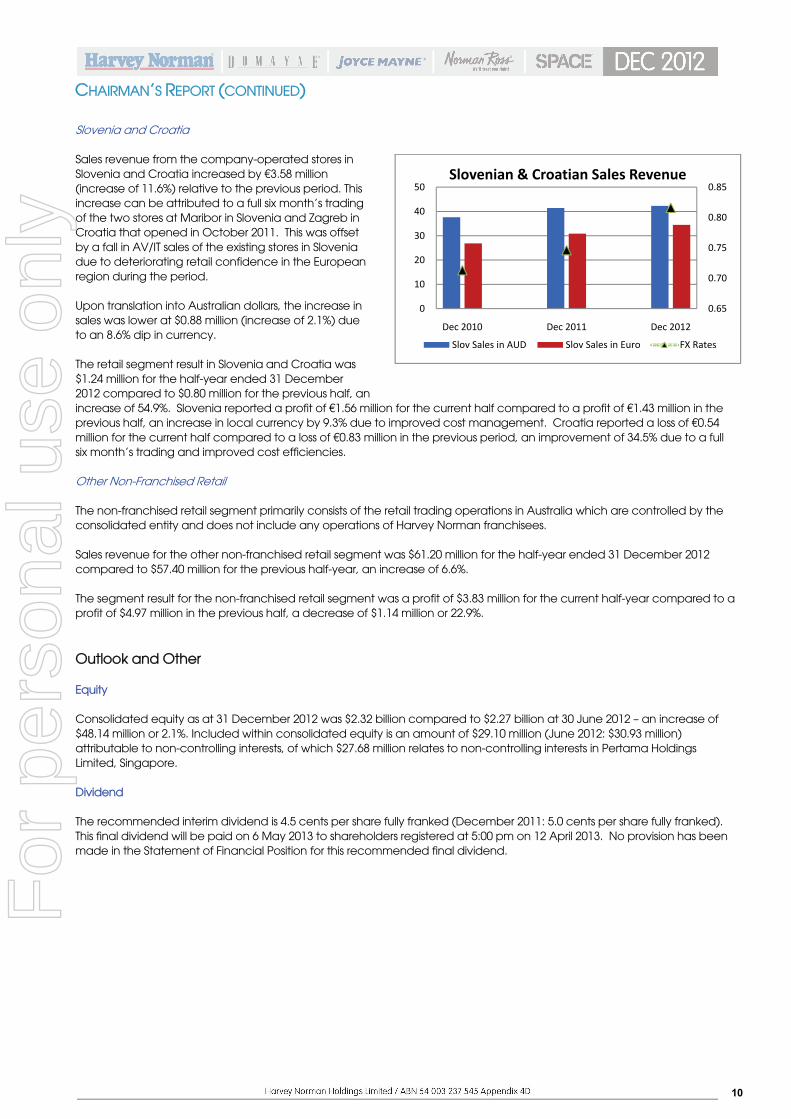

Slovenia and Croatia Sales revenue from the company-operated stores in Slovenia and Croatia increased by €3.58 million (increase of 11.6%) relative to the previous period. This increase can be attributed to a full six month’s trading of the two stores at Maribor in Slovenia and Zagreb in Croatia that opened in October 2011. This was offset by a fall in AV/IT sales of the existing stores in Slovenia due to deteriorating retail confidence in the European region during the period. Upon translation into Australian dollars, the increase in sales was lower at $0.88 million (increase of 2.1%) due to an 8.6% dip in currency. The retail segment result in Slovenia and Croatia was $1.24 million for the half-year ended 31 December 2012 compared to $0.80 million for the previous half, an increase of 54.9%. Slovenia reported a profit of €1.56 million for the current half compared to a profit of €1.43 million in the previous half, an increase in local currency by 9.3% due to improved cost management. Croatia reported a loss of €0.54 million for the current half compared to a loss of €0.83 million in the previous period, an improvement of 34.5% due to a full six month’s trading and improved cost efficiencies. Other Non-Franchised Retail The non-franchised retail segment primarily consists of the retail trading operations in Australia which are controlled by the consolidated entity and does not include any operations of Harvey Norman franchisees. Sales revenue for the other non-franchised retail segment was $61.20 million for the half-year ended 31 December 2012 compared to $57.40 million for the previous half-year, an increase of 6.6%. The segment result for the non-franchised retail segment was a profit of $3.83 million for the current half-year compared to a profit of $4.97 million in the previous half, a decrease of $1.14 million or 22.9%.

Outlook and Other Equity Consolidated equity as at 31 December 2012 was $2.32 billion compared to $2.27 billion at 30 June 2012 – an increase of $48.14 million or 2.1%. Included within consolidated equity is an amount of $29.10 million (June 2012: $30.93 million) attributable to non-controlling interests, of which $27.68 million relates to non-controlling interests in Pertama Holdings Limited, Singapore. Dividend The recommended interim dividend is 4.5 cents per share fully franked (December 2011: 5.0 cents per share fully franked). This final dividend will be paid on 6 May 2013 to shareholders registered at 5:00 pm on 12 April 2013. No provision has been made in the Statement of Financial Position for this recommended final dividend.

For

per

sona

l use

onl

y

11

CHAIRMAN’S REPORT (CONTINUED) Outlook We will continue to execute the Harvey Norman omni channel strategy. In Australia, Harvey Norman franchisees are committed to the “Customer First” program. Franchisees will benefit from the continued improvements in the Harvey Norman digital platform, merchandising and supply chain systems. Within the Australian franchising operations segment, the Entertainment and Technology category continues to be challenging. Product rationalisation and improved market share in key categories in the year ahead, led by the Customer First strategy, will provide opportunity for improved performance. Furniture, Bedding and Home Appliance categories continue to outperform the market. The New Zealand operation remains strong. The main complex in Christchurch has reopened. There is increasing consumer confidence in New Zealand. The Irish business has had a period of solid improvement. The balance sheet of the company remains strong. We are well placed to take advantage of emerging opportunities. I would like to thank my fellow directors, Harvey Norman employees, franchisees and their staff for their continuing efforts and loyalty.

G. HARVEY Chairman Sydney, 28 February 2013

For

per

sona

l use

onl

y

12

DIRECTORS’ REPORT The directors of Harvey Norman Holdings Limited (the “Company”) submit their report for the half-year ended 31 December 2012. Unless otherwise indicated, all directors (collectively termed “the Board”) held their position as a director throughout the entire financial period and up to the date of this report.

■ Directors Gerald Harvey Executive Chairman

Chris Mentis Director and Chief Financial Officer

Christopher Herbert Brown Non-Executive Director

Kay Lesley Page Director and Chief Executive Officer

Michael John Harvey Non-Executive Director

Kenneth William Gunderson-Briggs Non-Executive Director

John Evyn Slack-Smith Director and Chief Operating Officer

Ian John Norman Non-Executive Director

Graham Charles Paton AM Non-Executive Director

David Matthew Ackery Director

■ Committee Membership As at the date of this report, the Company had an Audit Committee, a Remuneration Committee and a Nomination Committee. Members acting on the committees of the board during the half year were: ■ Audit Committee: G.C. Paton AM (Chairman) C.H. Brown K.W. Gunderson-Briggs

■ Remuneration Committee: C.H. Brown (Chairman) K.W. Gunderson-Briggs G.C. Paton AM

■ Nomination Committee: C.H. Brown (Chairman) K.W. Gunderson-Briggs G.C. Paton AM

■ Principal Activities The principal activities of the consolidated entity are that of an integrated retail, franchise and property enterprise including: Franchisor; Sale of furniture, bedding, computers, communications and consumer electrical products in Australia, New Zealand,

Slovenia, Croatia, Ireland and Northern Ireland; Property investment; Lessor of premises to Harvey Norman franchisees and other third parties; Media placement; and Provision of consumer finance and other commercial advances.

The consolidated entity holds a controlling interest in Pertama Holdings Limited (“Pertama”). Shares in Pertama are listed on the Stock Exchange of Singapore. The principal activities of Pertama are retail sales of furniture, bedding, computers, communications and consumer electrical products in Singapore and Malaysia.

■ Review of Group Operations The total equity of the consolidated entity for the half-year ended 31 December 2012 increased over the total equity at 30 June 2012 due to the following: Profit attributable to the franchising operations segment; and Profit attributable to the property segment.

■ Significant Changes in the State of Affairs In the opinion of the directors, there were no significant changes in the state of affairs of the consolidated entity that occurred during the half-year ended 31 December 2012.

■ Significant Events After Balance Date There have been no circumstances arising since balance date which have significantly affected or may significantly affect: the operations; the results of those operations; or the state of affairs of the entity or consolidated entity in future financial years.

For

per

sona

l use

onl

y

DIRECTOR

■ Dividend The directors 2013 to sharePosition for th

■ Corpora The CompanASX Corporafor the entire

■ Auditor I The directors

Auditor’s In In relation to 2012, to the brequirements

Ernst & Young

Katrina ZdrilicPartner Sydney 28 February 2 This report ha

G. HARVEY Chairman Sydney 28 February 2

RS’ REPORT (

ds

recommend eholders registhis recommen

ate Governanc

ny is committeate Governance financial peri

Independenc

received the

ndependen

our review of best of my knos of the Corpo

g

c

2013

as been made

2013

(CONTINUED

a fully frankedtered at 5:00 p

nded interim d

ce

ed to good coce Council's "Piod, unless oth

ce

following dec

nce Declar

the financial owledge and orations Act 20

e in accordan

D)

d interim dividpm on 12 Apri

dividend.

orporate govePrinciples of Gherwise stated

claration from

ration to the

report of Harv belief, there h001 or any app

nce with a reso

dend of 4.5 cel 2013. No pro

ernance and dGood Corporad.

m the auditors o

e Directors

vey Norman Hhave been noplicable code

olution of direc

K.L. PAGE Chief Exec Sydney 28 Februar

ents per share.ovision has be

disclosure. Theate Governanc

of Harvey Nor

of Harvey N

Holdings Limiteo contraventioe of profession

ctors.

cutive Officer

ry 2013

This interim den made in th

e Company hace and Best P

rman Holdings

Norman Ho

ed for the half-ons of the audnal conduct.

Liability under P

dividend will behe Statement

as substantiallyPractice Recom

s Limited

oldings Limit

-year ended 3ditor independ

limited by a sProfessional Sta

e paid on 6 M of Financial

y adopted themmendations

ted

31 December dence

scheme approandards Legis

13

May

e s"

oved slation.

For

per

sona

l use

onl

y

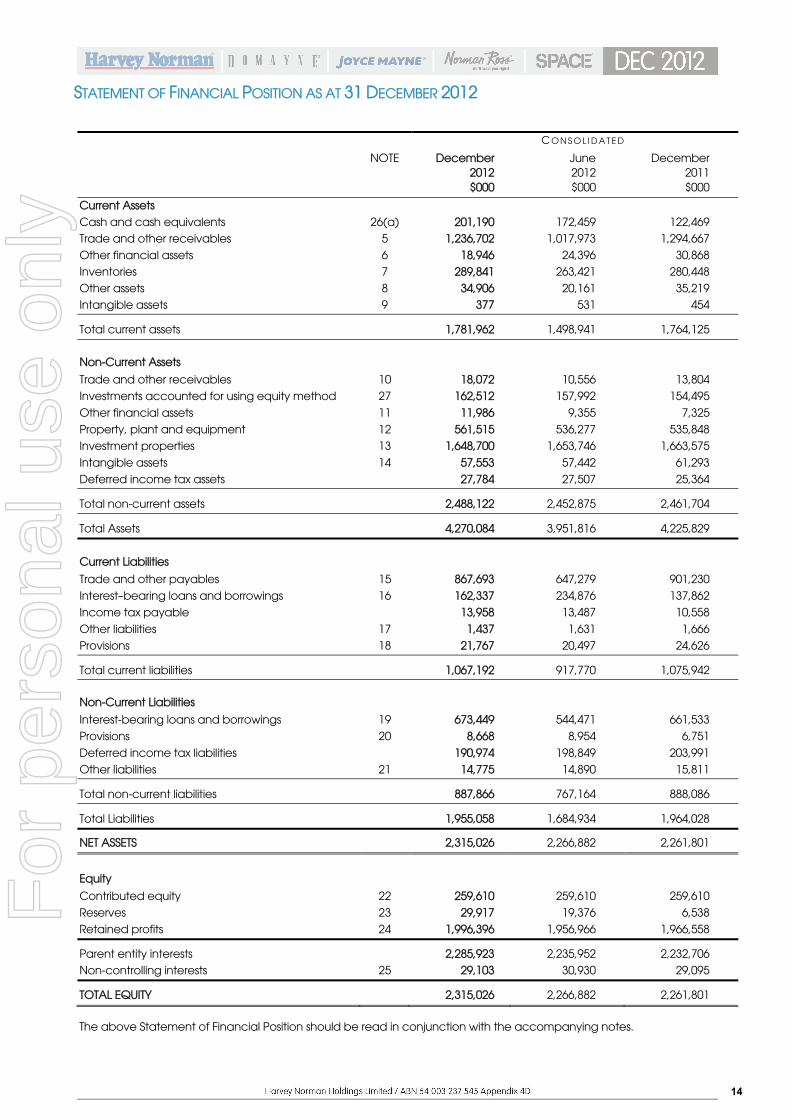

STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 2012

14

C O N S O L I D A T E D

NOTE December 2012

June 2012

December 2011

$000 $000 $000

Current Assets

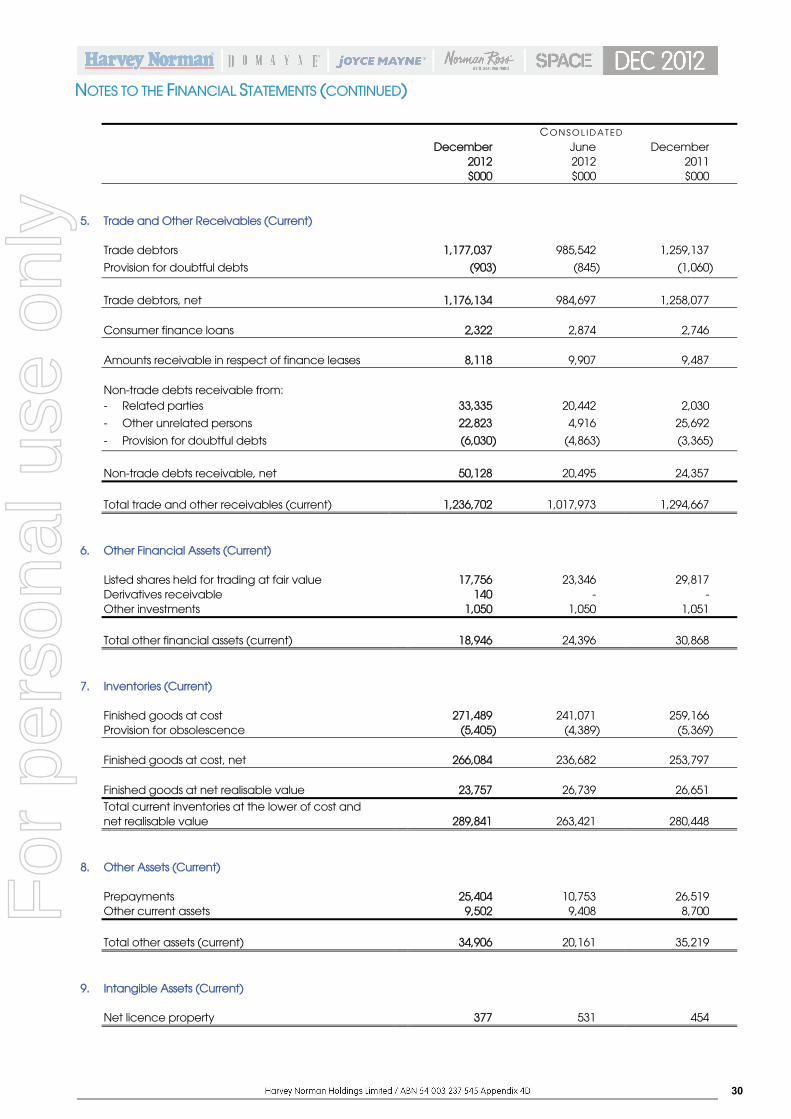

Cash and cash equivalents 26(a) 201,190 172,459 122,469 Trade and other receivables 5 1,236,702 1,017,973 1,294,667 Other financial assets 6 18,946 24,396 30,868 Inventories 7 289,841 263,421 280,448 Other assets 8 34,906 20,161 35,219 Intangible assets 9 377 531 454

Total current assets 1,781,962 1,498,941 1,764,125

Non-Current Assets

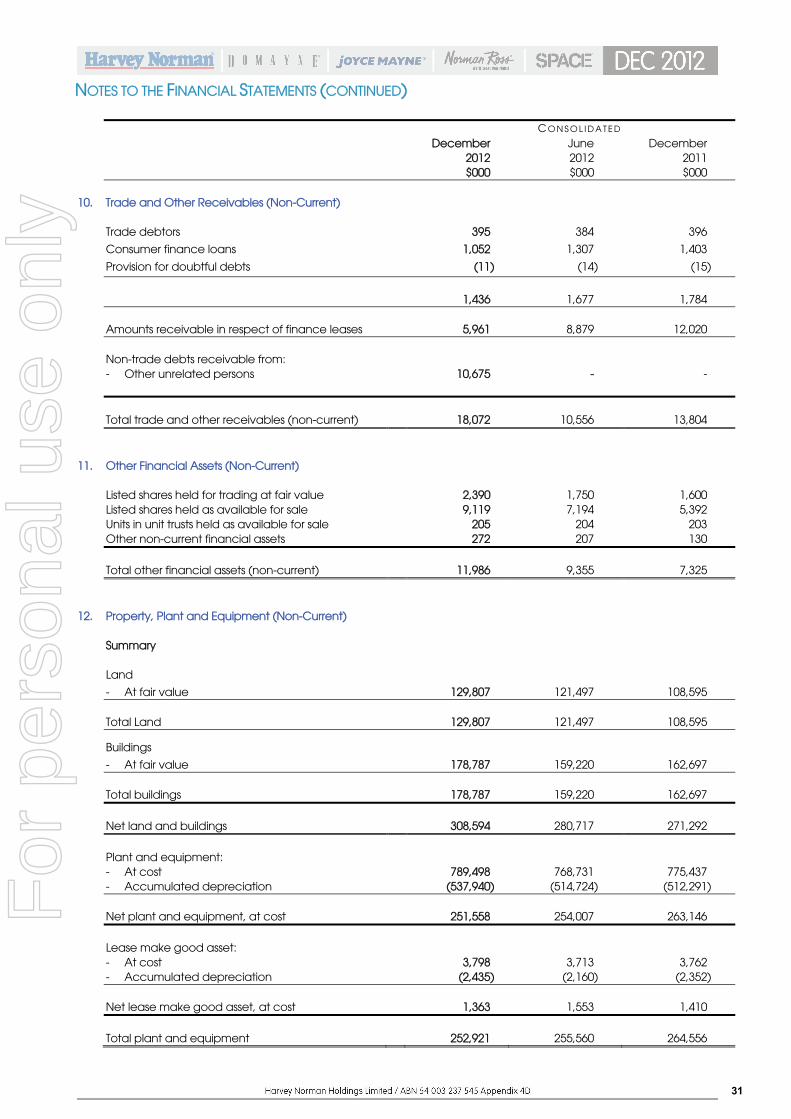

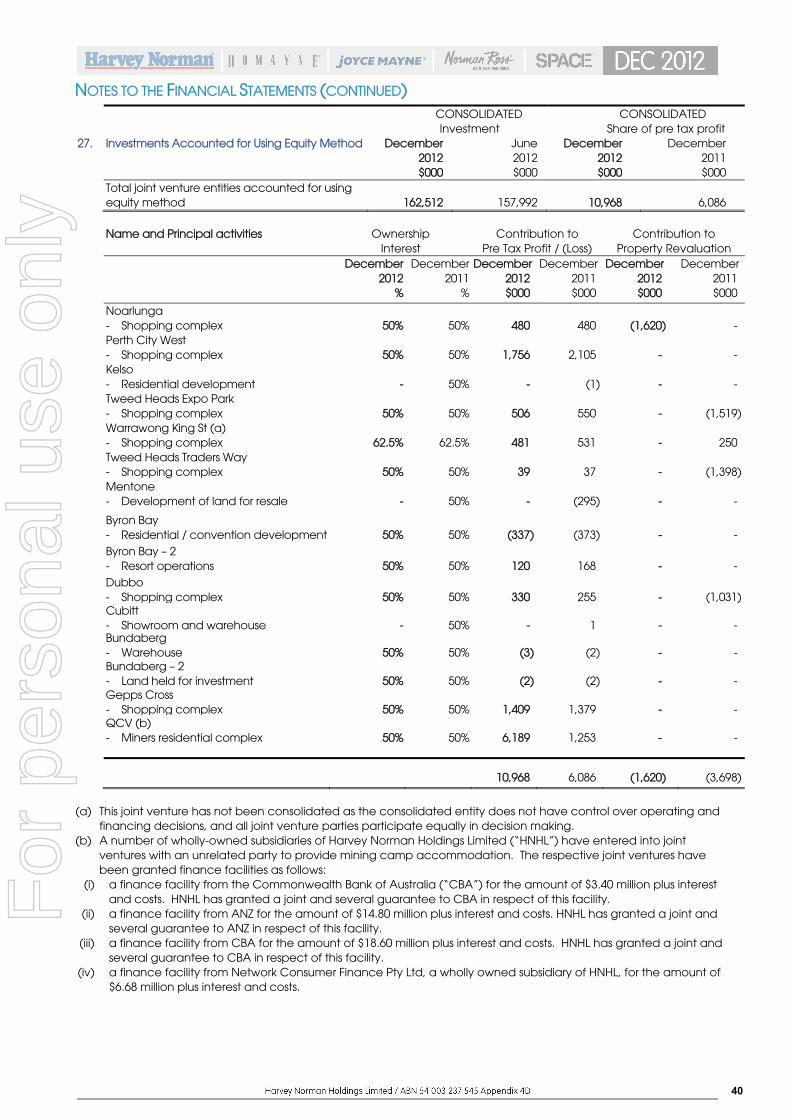

Trade and other receivables 10 18,072 10,556 13,804 Investments accounted for using equity method 27 162,512 157,992 154,495

Other financial assets 11 11,986 9,355 7,325 Property, plant and equipment 12 561,515 536,277 535,848 Investment properties 13 1,648,700 1,653,746 1,663,575

Intangible assets 14 57,553 57,442 61,293 Deferred income tax assets 27,784 27,507 25,364

Total non-current assets 2,488,122 2,452,875 2,461,704

Total Assets 4,270,084 3,951,816 4,225,829

Current Liabilities

Trade and other payables 15 867,693 647,279 901,230 Interest–bearing loans and borrowings 16 162,337 234,876 137,862 Income tax payable 13,958 13,487 10,558

Other liabilities 17 1,437 1,631 1,666 Provisions 18 21,767 20,497 24,626

Total current liabilities 1,067,192 917,770 1,075,942

Non-Current Liabilities

Interest-bearing loans and borrowings 19 673,449 544,471 661,533 Provisions 20 8,668 8,954 6,751

Deferred income tax liabilities 190,974 198,849 203,991 Other liabilities 21 14,775 14,890 15,811

Total non-current liabilities 887,866 767,164 888,086

Total Liabilities 1,955,058 1,684,934 1,964,028

NET ASSETS 2,315,026 2,266,882 2,261,801

Equity

Contributed equity 22 259,610 259,610 259,610 Reserves 23 29,917 19,376 6,538 Retained profits 24 1,996,396 1,956,966 1,966,558

Parent entity interests 2,285,923 2,235,952 2,232,706 Non-controlling interests 25 29,103 30,930 29,095

TOTAL EQUITY 2,315,026 2,266,882 2,261,801

The above Statement of Financial Position should be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

INCOME STATEMENT FOR THE HALF-YEAR ENDED 31 DECEMBER 2012

15

C O N S O L I D A T E D

NOTE December 2012

December 2011

$000 $000

Sales revenue 2 676,935 806,879 Cost of sales (488,686) (601,877)

Gross profit

188,249

205,002

Revenues and other income items 2 548,819 584,110

Distribution expenses (5,360) (5,468) Marketing expenses (189,912) (204,630) Occupancy expenses 3 (152,879) (111,167)

Administrative expenses (188,544) (210,364) Other expenses from ordinary activities (86,695) (71,748) Finance costs 3 (23,478) (24,653)

Share of equity accounted entities: - Share of net profit of joint venture entities (a) 2, 27 10,968 6,086 - Share of joint venture property revaluation (a) 3, 27 (1,620) (3,698)

Profit before income tax

99,548

163,470

Income tax expense

(16,894)

(32,637)

Profit after tax

82,654

130,833

Attributable to:

Owners of the parent 81,923 128,947

Non-controlling interests 731 1,886

82,654

130,833

Earnings Per Share: Basic earnings per share (cents per share) 4 7.71 cents 12.14 cents Diluted earnings per share (cents per share) 4 7.71 cents 12.14 cents Dividends per share (cents per share)

4.5 cents

5.0 cents

The above Income Statement should be read in conjunction with the accompanying notes. (a) The total share of net profit of joint venture entities, including the share of joint venture property revaluation, was

$9.35 million before tax for the half-year ended 31 December 2012 (December 2011: $2.39 million before tax).For

per

sona

l use

onl

y

16

STATEMENT OF COMPREHENSIVE INCOME FOR THE HALF-YEAR ENDED 31 DECEMBER 2012

C O N S O L I D A T E D

December 2012

December 2011

$000 $000

Profit for the period 82,654 130,833 Items that may be reclassified subsequently to profit or loss

Foreign currency translation 6,155 (6,209) Net fair value gains/(losses) on available-for-sale investments 1,833 (599) Net movement on cash flow hedges 2,514 (15,384)

Income tax effect on net movement on cash flow hedges (533) 4,645 Items that will not be reclassified subsequently to profit or loss

Fair value revaluation of land and buildings 3,932 817 Income tax effect on fair value revaluation of land and buildings (2,888) (1,616)

Other comprehensive income / (loss) for the period (net of tax)

11,013

(18,346)

Total comprehensive income for the period (net of tax)

93,667

112,487

Total comprehensive income attributable to: - Owners of the parent 92,400 110,283

- Non-controlling interests 1,267 2,204

93,667

112,487

The above Statement of Comprehensive Income should be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

STA

TEM

ENT

OF

CH

AN

GES

IN E

QU

ITY

FOR

TH

E H

ALF

-YEA

R E

ND

ED 3

1 D

ECEM

BER

201

2

1

7

A

ttrib

uta

ble

to

Eq

uity

Ho

lde

rs o

f th

e P

are

nt

Co

ntr

ibu

ted

Eq

uity

R

eta

ine

d

Pro

fits

A

sse

t R

eva

lua

tion

R

ese

rve

Fo

reig

n

Cu

rre

nc

y Tr

an

slatio

n

Re

serv

e

A

vaila

ble

fo

r Sa

le R

ese

rve

C

ash

Flo

w

He

dg

e

Re

serv

e

Em

plo

yee

Eq

uity

Be

ne

fits

Re

serv

e

A

cq

uisi

tion

R

ese

rve

N

on

-c

on

tro

llin

g

Inte

rest

s

TO

TAL

EQU

ITY

$0

00

$000

$0

00

$000

$0

00

$000

$0

00

$000

$0

00

$000

At 1

Ju

ly 2

012

25

9,61

0

1,95

6,96

6

72,2

29

(3

5,36

9)

3,

354

(1

3,88

6)

7,

786

(1

4,73

8)

30

,930

2,26

6,88

2 O

the

r co

mp

reh

en

sive

inc

om

e:

Re

valu

atio

n o

f la

nd

an

d b

uild

ing

s -

- 1,

044

- -

- -

- -

1,04

4 R

eve

rse

exp

ired

or r

ea

lise

d c

ash

flo

w h

ed

ge

rese

rve

s -

- -

- -

73

7 -

- -

73

7 C

urre

nc

y tr

an

slatio

n d

iffe

ren

ce

s -

- -

5,61

9 -

- -

- 53

6 6,

155

Fair

valu

e o

f in

tere

st ra

te s

wa

ps

- -

- -

- 1,

231

- -

- 1,

231

Fair

valu

e o

f fo

rwa

rd fo

reig

n

exc

ha

ng

e c

on

tra

cts

-

- -

- -

13

-

- -

13

Fa

ir va

lue

of a

vaila

ble

for s

ale

fin

an

cia

l ass

ets

-

- -

-

1,83

3 -

- -

-

1,83

3 O

the

r co

mp

reh

en

sive

inc

om

e

- -

1,

044

5,

619

1,

833

1,

981

- -

53

6

11,0

13

Pro

fit fo

r th

e p

erio

d

- 81

,923

-

- -

- -

- 73

1 82

,654

To

tal c

om

pre

he

nsiv

e in

co

me

fo

r th

e p

erio

d

-

81,9

23

1,

044

5,

619

1,

833

1,

981

- -

1,

267

93

,667

Co

st o

f sh

are

ba

sed

pa

yme

nts

-

- -

- -

- 64

-

- 64

D

ivid

en

ds

pa

id

- (4

2,49

3)

- -

- -

- -

(1,0

25)

(43,

518)

D

istrib

utio

n to

me

mb

ers

-

- -

- -

- -

- (2

,069

) (2

,069

) A

t 31

De

ce

mb

er 2

012

25

9,61

0

1,99

6,39

6

73,2

73

(2

9,75

0)

5,

187

(1

1,90

5)

7,

850

(1

4,73

8)

29

,103

2,31

5,02

6

For

per

sona

l use

onl

y

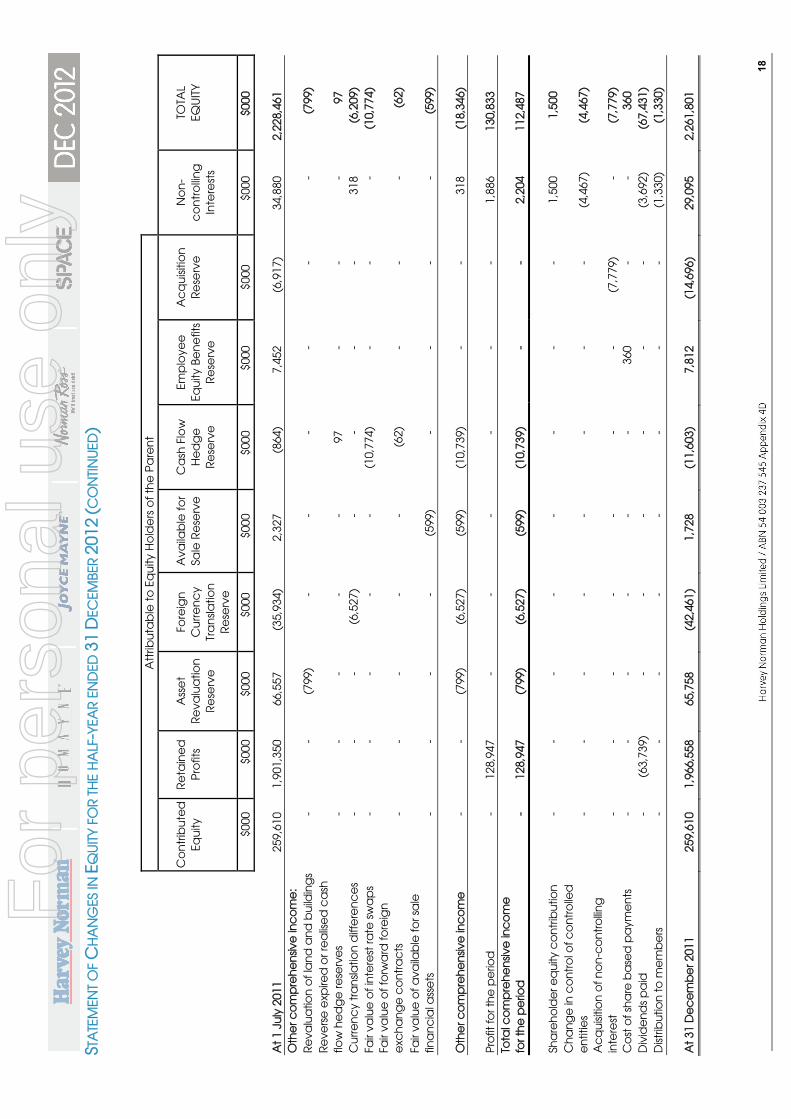

18

STA

TEM

ENT

OF

CH

AN

GES

IN E

QU

ITY

FOR

TH

E H

ALF

-YEA

R E

ND

ED 3

1 D

ECEM

BER

201

2 (C

ON

TIN

UED

)

Att

ribu

tab

le t

o E

qu

ity H

old

ers

of t

he

Pa

ren

t

Co

ntr

ibu

ted

Eq

uity

R

eta

ine

d

Pro

fits

A

sse

t R

eva

lua

tion

R

ese

rve

Fo

reig

n

Cu

rre

nc

y Tr

an

slatio

n

Re

serv

e

A

vaila

ble

fo

r Sa

le R

ese

rve

C

ash

Flo

w

He

dg

e

Re

serv

e

Em

plo

yee

Eq

uity

Be

ne

fits

Re

serv

e

A

cq

uisi

tion

R

ese

rve

N

on

-c

on

tro

llin

g

Inte

rest

s

TO

TAL

EQU

ITY

$0

00

$000

$0

00

$000

$0

00

$000

$0

00

$000

$0

00

$000

At 1

Ju

ly 2

011

25

9,61

0

1,90

1,35

0

66,5

57

(3

5,93

4)

2,32

7

(864

)

7,45

2

(6,9

17)

34

,880

2,22

8,46

1 O

the

r co

mp

reh

en

sive

inc

om

e:

Re

valu

atio

n o

f la

nd

an

d b

uild

ing

s -

- (7

99)

- -

- -

- -

(799

) R

eve

rse

exp

ired

or r

ea

lise

d c

ash

flo

w h

ed

ge

rese

rve

s -

- -

- -

97

-

- -

97

C

urre

nc

y tr

an

slatio

n d

iffe

ren

ce

s -

- -

(6,5

27)

- -

- -

318

(6,2

09)

Fair

valu

e o

f in

tere

st ra

te s

wa

ps

- -

- -

- (1

0,77

4)

- -

- (1

0,77

4)

Fair

valu

e o

f fo

rwa

rd fo

reig

n

exc

ha

ng

e c

on

tra

cts

-

- -

- -

(6

2)

- -

-

(62)

Fa

ir va

lue

of a

vaila

ble

for s

ale

fin

an

cia

l ass

ets

-

- -

-

(599

) -

- -

-

(599

) O

the

r co

mp

reh

en

sive

inc

om

e

- -

(7

99)

(6

,527

)

(599

)

(10,

739)

-

-

318

(1

8,34

6)

Pr

ofit

for t

he

pe

riod

-

128,

947

- -

- -

- -

1,88

6 13

0,83

3 To

tal c

om

pre

he

nsiv

e in

co

me

fo

r th

e p

erio

d

-

128,

947

(7

99)

(6

,527

)

(599

)

(10,

739)

-

-

2,20

4

112,

487

Sh

are

ho

lde

r eq

uity

co

ntr

ibu

tion

-

- -

- -

- -

- 1,

500

1,50

0 C

ha

ng

e in

co

ntr

ol o

f co

ntr

olle

d

en

titie

s -

- -

- -

- -

-

(4,4

67)

(4

,467

) A

cq

uisi

tion

of n

on

-co

ntr

ollin

g

inte

rest

-

- -

- -

- -

(7

,779

) -

(7

,779

) C

ost

of s

ha

re b

ase

d p

aym

en

ts

- -

- -

- -

360

- -

360

Div

ide

nd

s p

aid

-

(63,

739)

-

- -

- -

- (3

,692

) (6

7,43

1)

Dist

ribu

tion

to m

em

be

rs

- -

- -

- -

- -

(1,3

30)

(1,3

30)

At 3

1 D

ec

em

be

r 201

1

259,

610

1,

966,

558

65

,758

(42,

461)

1,72

8

(11,

603)

7,81

2

(14,

696)

29,0

95

2,

261,

801

For

per

sona

l use

onl

y

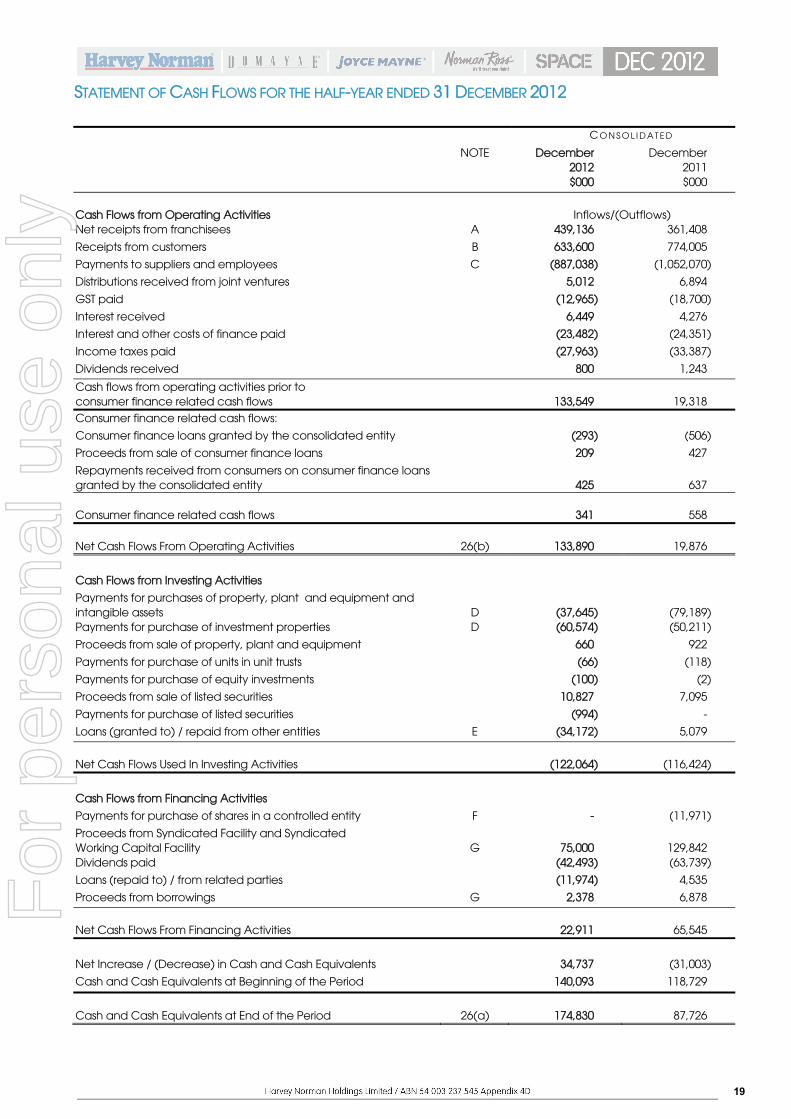

STATEMENT OF CASH FLOWS FOR THE HALF-YEAR ENDED 31 DECEMBER 2012

19

C O N S O L I D A T E D

NOTE December 2012

December 2011

$000 $000

Cash Flows from Operating Activities

Inflows/(Outflows)

Net receipts from franchisees A 439,136 361,408

Receipts from customers B 633,600 774,005

Payments to suppliers and employees C (887,038) (1,052,070)

Distributions received from joint ventures 5,012 6,894

GST paid (12,965) (18,700)

Interest received 6,449 4,276

Interest and other costs of finance paid (23,482) (24,351)

Income taxes paid (27,963) (33,387)

Dividends received 800 1,243

Cash flows from operating activities prior to consumer finance related cash flows

133,549

19,318

Consumer finance related cash flows:

Consumer finance loans granted by the consolidated entity (293) (506)

Proceeds from sale of consumer finance loans 209 427

Repayments received from consumers on consumer finance loans granted by the consolidated entity

425

637

Consumer finance related cash flows

341

558

Net Cash Flows From Operating Activities

26(b)

133,890

19,876

Cash Flows from Investing Activities

Payments for purchases of property, plant and equipment and intangible assets

D

(37,645)

(79,189)

Payments for purchase of investment properties D (60,574) (50,211)

Proceeds from sale of property, plant and equipment 660 922

Payments for purchase of units in unit trusts (66) (118)

Payments for purchase of equity investments (100) (2)

Proceeds from sale of listed securities 10,827 7,095

Payments for purchase of listed securities (994) -

Loans (granted to) / repaid from other entities E (34,172) 5,079

Net Cash Flows Used In Investing Activities

(122,064)

(116,424)

Cash Flows from Financing Activities

Payments for purchase of shares in a controlled entity F - (11,971)

Proceeds from Syndicated Facility and Syndicated Working Capital Facility

G

75,000

129,842

Dividends paid (42,493) (63,739)

Loans (repaid to) / from related parties (11,974) 4,535

Proceeds from borrowings G 2,378 6,878

Net Cash Flows From Financing Activities

22,911

65,545

Net Increase / (Decrease) in Cash and Cash Equivalents 34,737 (31,003)

Cash and Cash Equivalents at Beginning of the Period 140,093 118,729

Cash and Cash Equivalents at End of the Period

26(a)

174,830

87,726

For

per

sona

l use

onl

y

STATEMENT OF CASH FLOWS FOR THE HALF-YEAR ENDED 31 DECEMBER 2012 (CONTINUED)

20

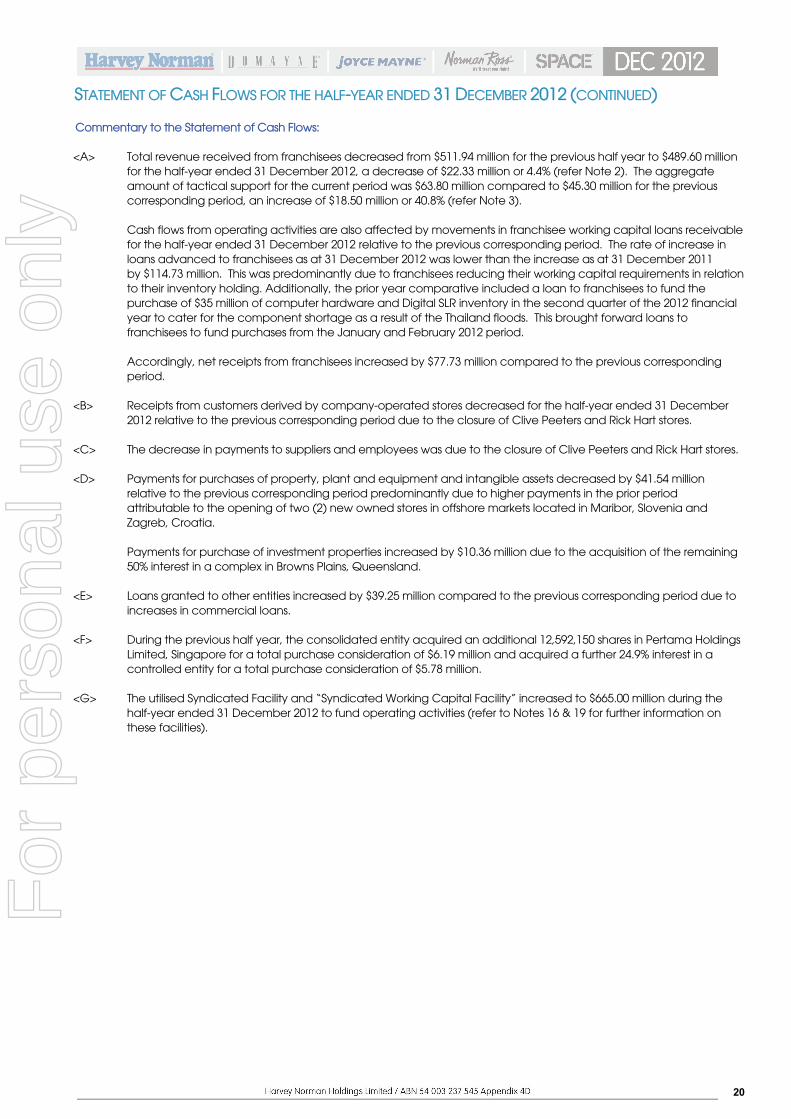

Commentary to the Statement of Cash Flows: <A> Total revenue received from franchisees decreased from $511.94 million for the previous half year to $489.60 million

for the half-year ended 31 December 2012, a decrease of $22.33 million or 4.4% (refer Note 2). The aggregate amount of tactical support for the current period was $63.80 million compared to $45.30 million for the previous corresponding period, an increase of $18.50 million or 40.8% (refer Note 3). Cash flows from operating activities are also affected by movements in franchisee working capital loans receivable for the half-year ended 31 December 2012 relative to the previous corresponding period. The rate of increase in loans advanced to franchisees as at 31 December 2012 was lower than the increase as at 31 December 2011 by $114.73 million. This was predominantly due to franchisees reducing their working capital requirements in relation to their inventory holding. Additionally, the prior year comparative included a loan to franchisees to fund the purchase of $35 million of computer hardware and Digital SLR inventory in the second quarter of the 2012 financial year to cater for the component shortage as a result of the Thailand floods. This brought forward loans to franchisees to fund purchases from the January and February 2012 period. Accordingly, net receipts from franchisees increased by $77.73 million compared to the previous corresponding period.

<B> Receipts from customers derived by company-operated stores decreased for the half-year ended 31 December 2012 relative to the previous corresponding period due to the closure of Clive Peeters and Rick Hart stores.

<C> The decrease in payments to suppliers and employees was due to the closure of Clive Peeters and Rick Hart stores.

<D> Payments for purchases of property, plant and equipment and intangible assets decreased by $41.54 million relative to the previous corresponding period predominantly due to higher payments in the prior period attributable to the opening of two (2) new owned stores in offshore markets located in Maribor, Slovenia and Zagreb, Croatia. Payments for purchase of investment properties increased by $10.36 million due to the acquisition of the remaining 50% interest in a complex in Browns Plains, Queensland.

<E>

Loans granted to other entities increased by $39.25 million compared to the previous corresponding period due to increases in commercial loans.

<F> During the previous half year, the consolidated entity acquired an additional 12,592,150 shares in Pertama Holdings Limited, Singapore for a total purchase consideration of $6.19 million and acquired a further 24.9% interest in a controlled entity for a total purchase consideration of $5.78 million.

<G> The utilised Syndicated Facility and “Syndicated Working Capital Facility” increased to $665.00 million during the half-year ended 31 December 2012 to fund operating activities (refer to Notes 16 & 19 for further information on these facilities).

For

per

sona

l use

onl

y

21

OPERATING SEGMENTS OPERATING SEGMENTS – 31 December 2012

SEGMENT REVENUE Sales to Customers

Outside the Consolidated Entity

Other Revenues from Outside the

Consolidated Entity

Share of Net

Profit/(Loss) of Equity Accounted

Investments

Segment Revenue

Dec 2012 $000

Dec 2012 $000

Dec 2012 $000

Dec 2012 $000

FRANCHISING OPERATIONS 2,381 442,001 - 444,382

Retail – New Zealand 293,942 5,205 - 299,147 Retail – Asia 170,177 1,827 - 172,004

Retail – Slovenia & Croatia 42,283 333 - 42,616

Retail – Ireland & Northern Ireland 104,206 1,420 - 105,626

Non-Franchised Retail – Clive Peeters & Rick Hart

-

8

-

8

Other Non-Franchised Retail 61,203 1,556 - 62,759

TOTAL RETAIL

671,811

10,349

-

682,160

Retail Property 65 96,351 10,985 107,401 Property Under Construction for Retail - 64 (17) 47

Property Development for Resale 2,678 288 - 2,966 TOTAL PROPERTY

2,743

96,703

10,968

110,414

Equity Investments - 5,705 - 5,705

Other - 9,663 - 9,663

Inter-company eliminations - (15,602) - (15,602)

Total segment revenue

676,935

548,819

10,968

1,236,722

For

per

sona

l use

onl

y

22

OPERATING SEGMENTS (CONTINUED)

Operating Segments – 31 December 2012 (continued)

SEGMENT RESULT Segment Result Before Interest,

Taxation, Depreciation, Impairment & Amortisation

Interest Expense

Depreciation

Expense

Amortisation & Impairment

Expense

Segment

Result Before Tax

Dec 2012 $000

Dec 2012 $000

Dec 2012 $000

Dec 2012 $000

Dec 2012 $000

FRANCHISING OPERATIONS 109,210 (7,797) (25,007) (5,396) 71,010

Retail – New Zealand 23,422 (3) (3,465) (11) 19,943 Retail – Asia 3,504 (17) (3,364) (15) 108 Retail – Slovenia & Croatia 2,652 (618) (758) (34) 1,242 Retail – Ireland & Northern Ireland (10,593) (1,482) (1,196) - (13,271) Non-Franchised Retail – Clive Peeters & Rick Hart

(4,791)

(330)

-

-

(5,121)

Other Non-Franchised Retail 5,231 (624) (746) (29) 3,832 TOTAL RETAIL

19,425

(3,074)

(9,529)

(89)

6,733

Retail Property 43,491 (11,901) (2,534) - 29,056 Property Under Construction for Retail (12,634) (230) - - (12,864) Property Development for Resale (2,012) (179) - - (2,191) TOTAL PROPERTY

28,845

(12,310)

(2,534)

-

14,001

Equity Investments 5,705 (127) - - 5,578 Other 4,609 (604) (1,779) - 2,226

Inter-company eliminations (434) 434 - - - Total segment result before tax

167,360

(23,478)

(38,849)

(5,485)

99,548

Income tax expense (16,894) Profit attributable to non-controlling interests

(731)

Net profit for the period attributable to owners of the parent

81,923

For

per

sona

l use

onl

y

23

OPERATING SEGMENTS (CONTINUED) OPERATING SEGMENTS – 31 December 2011

SEGMENT REVENUE Sales to Customers

Outside the Consolidated Entity

Other Revenues from Outside the

Consolidated Entity

Share of Net

Profit/(Loss) of Equity Accounted

Investments

Segment Revenue

Dec 2011 $000

Dec 2011 $000

Dec 2011 $000

Dec 2011 $000

FRANCHISING OPERATIONS 2,393 463,866 - 466,259

Retail – New Zealand 283,841 4,681 - 288,522 Retail – Asia 174,292 1,386 - 175,678

Retail – Slovenia & Croatia 41,401 342 - 41,743

Retail – Ireland & Northern Ireland 113,085 2,002 - 115,087

Non-Franchised Retail – Clive Peeters and Rick Hart

134,412

8,002

-

142,414

Other Non-Franchised Retail 57,399 1,687 - 59,086

TOTAL RETAIL

804,430

18,100

-

822,530

Retail Property 56 100,089 5,054 105,199 Property Under Construction for Retail - 199 10 209 Property Development for Resale - 10,175 1,022 11,197 TOTAL PROPERTY

56

110,463

6,086

116,605

Equity Investments - 1,243 - 1,243

Other - 6,275 - 6,275

Inter-company eliminations - (15,837) - (15,837)

Total segment revenue

806,879

584,110

6,086

1,397,075

F

or p

erso

nal u

se o

nly

24

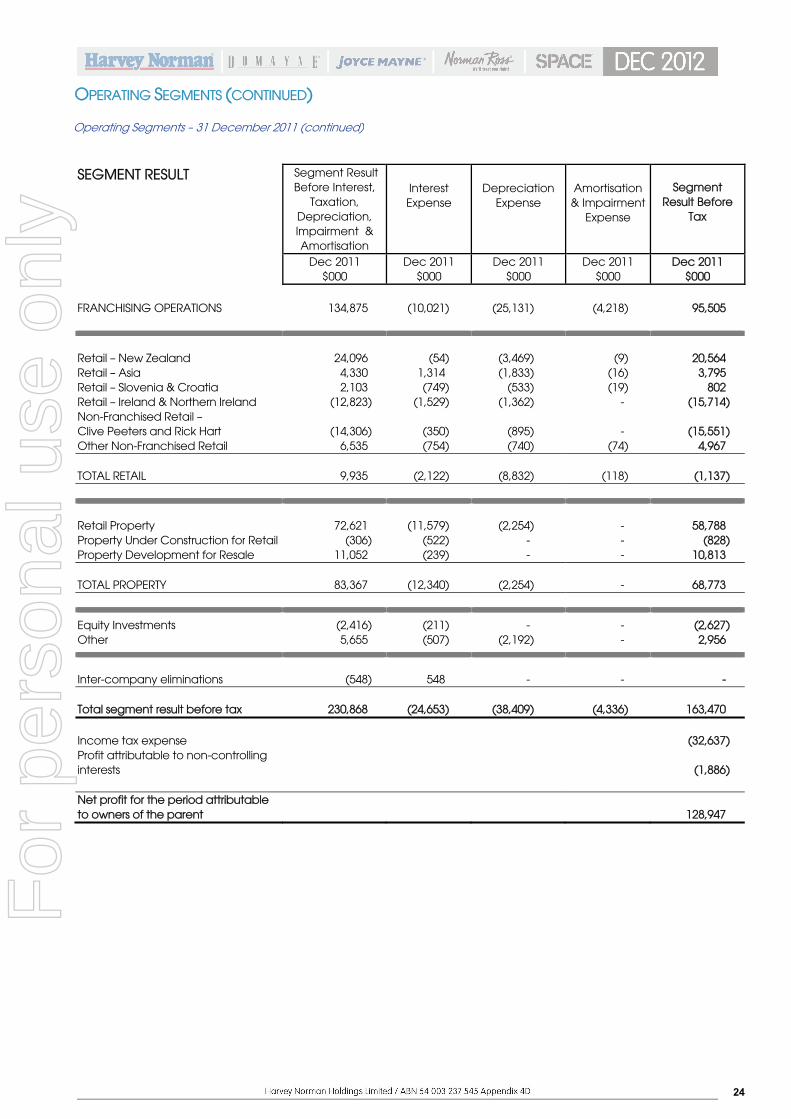

OPERATING SEGMENTS (CONTINUED) Operating Segments – 31 December 2011 (continued)

SEGMENT RESULT Segment Result Before Interest,

Taxation, Depreciation, Impairment & Amortisation

Interest Expense

Depreciation

Expense

Amortisation & Impairment

Expense

Segment

Result Before Tax

Dec 2011 $000

Dec 2011 $000

Dec 2011 $000

Dec 2011 $000

Dec 2011 $000

FRANCHISING OPERATIONS 134,875 (10,021) (25,131) (4,218) 95,505

Retail – New Zealand 24,096 (54) (3,469) (9) 20,564 Retail – Asia 4,330 1,314 (1,833) (16) 3,795 Retail – Slovenia & Croatia 2,103 (749) (533) (19) 802 Retail – Ireland & Northern Ireland (12,823) (1,529) (1,362) - (15,714) Non-Franchised Retail – Clive Peeters and Rick Hart

(14,306)

(350)

(895)

-

(15,551)

Other Non-Franchised Retail 6,535 (754) (740) (74) 4,967 TOTAL RETAIL

9,935

(2,122)

(8,832)

(118)

(1,137)

Retail Property 72,621 (11,579) (2,254) - 58,788 Property Under Construction for Retail (306) (522) - - (828) Property Development for Resale 11,052 (239) - - 10,813 TOTAL PROPERTY

83,367

(12,340)

(2,254)

-

68,773

Equity Investments (2,416) (211) - - (2,627) Other 5,655 (507) (2,192) - 2,956

Inter-company eliminations (548) 548 - - - Total segment result before tax

230,868

(24,653)

(38,409)

(4,336)

163,470

Income tax expense (32,637) Profit attributable to non-controlling interests

(1,886)

Net profit for the period attributable to owners of the parent

128,947

For

per

sona

l use

onl

y

25

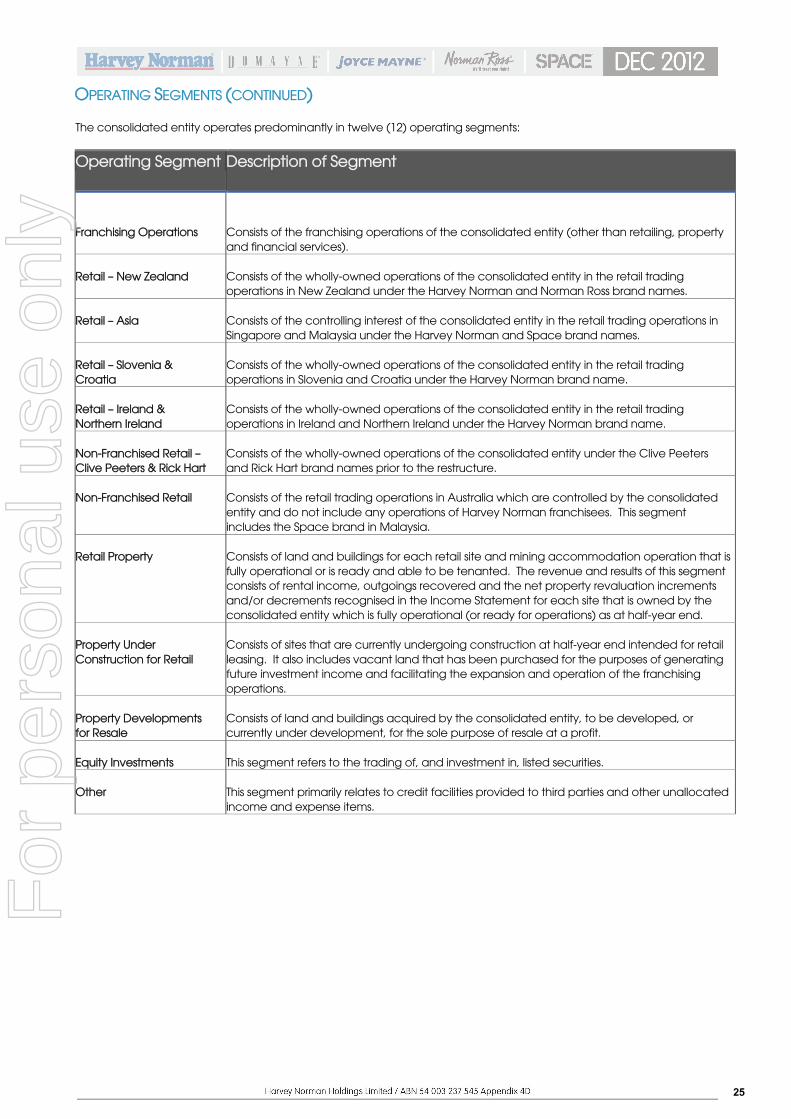

OPERATING SEGMENTS (CONTINUED) The consolidated entity operates predominantly in twelve (12) operating segments:

Operating Segment Description of Segment

Franchising Operations

Consists of the franchising operations of the consolidated entity (other than retailing, property and financial services).

Retail – New Zealand

Consists of the wholly-owned operations of the consolidated entity in the retail trading operations in New Zealand under the Harvey Norman and Norman Ross brand names.

Retail – Asia

Consists of the controlling interest of the consolidated entity in the retail trading operations in Singapore and Malaysia under the Harvey Norman and Space brand names.

Retail – Slovenia & Croatia

Consists of the wholly-owned operations of the consolidated entity in the retail trading operations in Slovenia and Croatia under the Harvey Norman brand name.

Retail – Ireland & Northern Ireland

Consists of the wholly-owned operations of the consolidated entity in the retail trading operations in Ireland and Northern Ireland under the Harvey Norman brand name.

Non-Franchised Retail – Clive Peeters & Rick Hart

Consists of the wholly-owned operations of the consolidated entity under the Clive Peeters and Rick Hart brand names prior to the restructure.

Non-Franchised Retail

Consists of the retail trading operations in Australia which are controlled by the consolidated entity and do not include any operations of Harvey Norman franchisees. This segment includes the Space brand in Malaysia.

Retail Property

Consists of land and buildings for each retail site and mining accommodation operation that is fully operational or is ready and able to be tenanted. The revenue and results of this segment consists of rental income, outgoings recovered and the net property revaluation increments and/or decrements recognised in the Income Statement for each site that is owned by the consolidated entity which is fully operational (or ready for operations) as at half-year end.

Property Under Construction for Retail

Consists of sites that are currently undergoing construction at half-year end intended for retail leasing. It also includes vacant land that has been purchased for the purposes of generating future investment income and facilitating the expansion and operation of the franchising operations.

Property Developments for Resale

Consists of land and buildings acquired by the consolidated entity, to be developed, or currently under development, for the sole purpose of resale at a profit.

Equity Investments

This segment refers to the trading of, and investment in, listed securities.

Other

This segment primarily relates to credit facilities provided to third parties and other unallocated income and expense items.

For

per

sona

l use

onl

y

26

1.

Statement of Significant Accounting Policies

(a) Corporate Information The financial report of Harvey Norman Holdings Limited for the half-year ended 31 December 2012 was authorised for issue in accordance with a resolution of the directors on 28 February 2013. Harvey Norman Holdings Limited (the “Company”) is a company limited by shares incorporated in Australia whose shares are publicly traded on the Australian stock exchange.

(b) Basis of Preparation The half-year financial report does not include all notes of the type normally included within the annual financial report and therefore cannot be expected to provide as full an understanding of the financial performance, financial position and financing and investing activities of the consolidated entity as the full financial report. The half-year financial report should be read in conjunction with the annual Financial Report of Harvey Norman Holdings Limited as at 30 June 2012. It is also recommended that the half-year financial report be considered together with any public announcements made by Harvey Norman Holdings Limited and its controlled entities during the half-year ended 31 December 2012 in accordance with the continuous disclosure obligations arising under the Corporations Act 2001. The half-year consolidated financial report is a general-purpose financial report, which has been prepared in accordance with the requirements of the Corporations Act 2001 and Accounting Standard AASB 134 “Interim Financial Reporting”. The financial report has been prepared on a historical cost basis, except for investment properties, land and buildings, derivative financial instruments, listed shares held for trading and available-for-sale investments, which have been measured at fair value. The carrying values of recognised assets and liabilities that are hedged items in fair value hedges, and are otherwise carried at cost, are adjusted to record changes in the fair values attributable to the risks that are being hedged. The financial report is presented in Australian dollars and all values are rounded to the nearest thousand dollars ($’000) unless otherwise stated under the option available to the consolidated entity under ASIC Class Order 98/0100. The consolidated entity is an entity to which the class order applies. (c) Summary of Significant Accounting Policies These consolidated financial statements have been prepared using the same accounting policies as used in the annual financial statements for the year ended 30 June 2012, except for the adoption of amending standards mandatory for annual periods beginning on or after 1 July 2012. The adoption of the amending standards did not have a significant impact on the consolidated entity.

NOTES TO THE FINANCIAL STATEMENTS

For

per

sona

l use

onl

y

27

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

C O N S O L I D A T E D

December 2012

December 2011

$000 $000

2.

Revenues

Revenue from the sale of products 676,935 806,879

Gross revenue from franchisees:

- Franchise fees 360,925 386,217

- Rent 112,763 109,458

- Interest 15,914 16,260

Total revenue received from franchisees

489,602

511,935

Rent received from other third parties 29,890 23,477

Interest received from other unrelated parties 6,449 4,276

Dividends from other unrelated parties 822 1,243

Total other revenues

526,763

540,931

Share of net profit from joint venture entities (Note 27)

10,968

6,086

Total revenues

1,214,666

1,353,896

Other Income Items:

Net property revaluation increment on Australian investment properties - 11,903

Reversal of a previous property revaluation decrement - 2,867

Net profit on the revaluation of equity investments to fair value 4,883 -

Net foreign exchange gains 740 538

Other revenue 16,433 27,871

Total other income items

22,056

43,179

Total revenues and other income items

1,236,722

1,397,075

Total revenue is disclosed on the Income Statement as follows:

Sales revenue 676,935 806,879

Other revenues 526,763 540,931

Other income items 22,056 43,179

Total other revenues and income items

548,819

584,110

Share of net profit of joint venture entities

10,968

6,086

Total revenues and other income items

1,236,722

1,397,075

For

per

sona

l use

onl

y

28

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

C O N S O L I D A T E D

December 2012

December 2011

$000 $000

3.

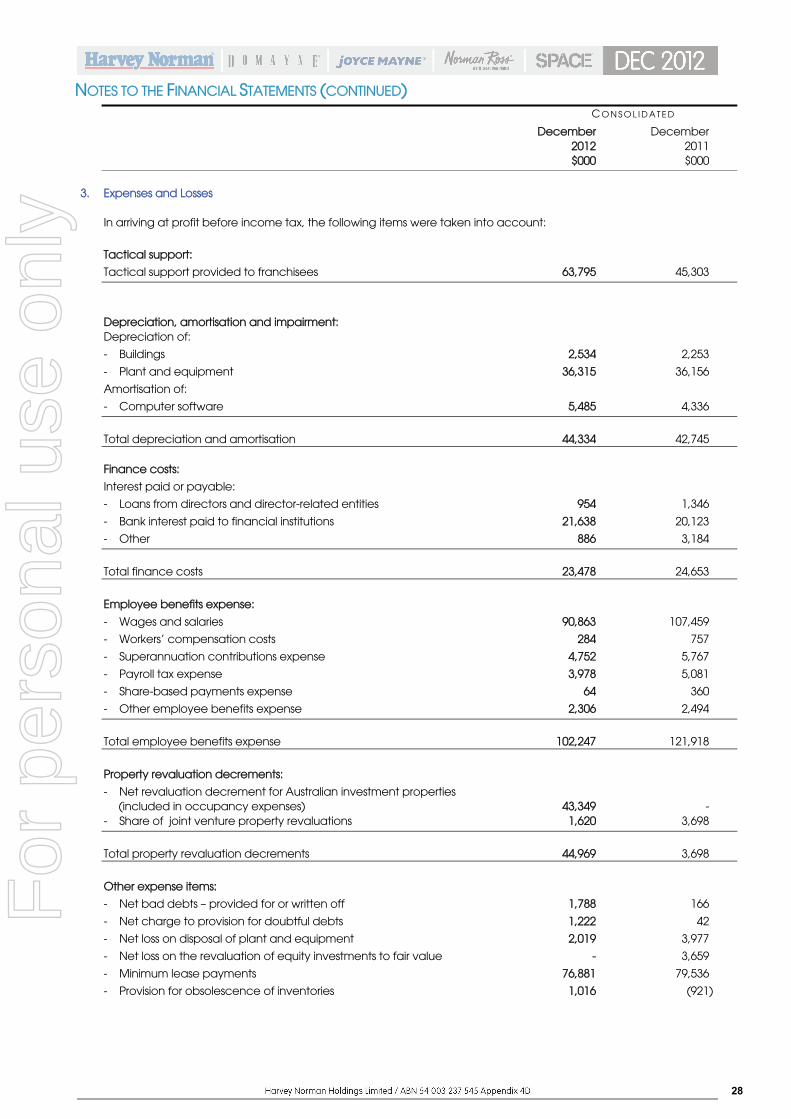

Expenses and Losses

In arriving at profit before income tax, the following items were taken into account:

Tactical support:

Tactical support provided to franchisees 63,795 45,303

Depreciation, amortisation and impairment:

Depreciation of:

- Buildings 2,534 2,253

- Plant and equipment 36,315 36,156

Amortisation of:

- Computer software 5,485 4,336

Total depreciation and amortisation

44,334

42,745

Finance costs:

Interest paid or payable:

- Loans from directors and director-related entities 954 1,346

- Bank interest paid to financial institutions 21,638 20,123

- Other 886 3,184

Total finance costs

23,478

24,653

Employee benefits expense:

- Wages and salaries 90,863 107,459

- Workers’ compensation costs 284 757

- Superannuation contributions expense 4,752 5,767

- Payroll tax expense 3,978 5,081

- Share-based payments expense 64 360

- Other employee benefits expense 2,306 2,494

Total employee benefits expense

102,247

121,918

Property revaluation decrements:

- Net revaluation decrement for Australian investment properties (included in occupancy expenses)

43,349

-

- Share of joint venture property revaluations 1,620 3,698

Total property revaluation decrements

44,969

3,698

Other expense items:

- Net bad debts – provided for or written off 1,788 166

- Net charge to provision for doubtful debts 1,222 42

- Net loss on disposal of plant and equipment 2,019 3,977

- Net loss on the revaluation of equity investments to fair value - 3,659

- Minimum lease payments 76,881 79,536

- Provision for obsolescence of inventories 1,016 (921)

For

per

sona

l use

onl

y

29

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)