a model for analyzing emerging - new york university...

TRANSCRIPT

A Model for Analyzing Emerging A Model for Analyzing Emerging A Model for Analyzing Emerging A Model for Analyzing Emerging Market Corporate CreditsMarket Corporate CreditsMarket Corporate CreditsMarket Corporate Credits

Dr. Edward Altman

NYU Stern School of Business

A Model for Analyzing Emerging Market Corporate Credits

Dr. Edward I. AltmanMax L. Heine Professor of Finance

New York UniversityLeonard N. Stern School of Business

212-998-0709Email: [email protected]

Website: http://www.stern.nyu.edu/~ealtman

Step 1: U.S. Bond Rating Equivalent

•Evaluate each bond by its EM Score and classify it as to its stand

alone U.S. bond rating equivalent. We use a model based on the

well documented and established U.S. Z-Score Approach

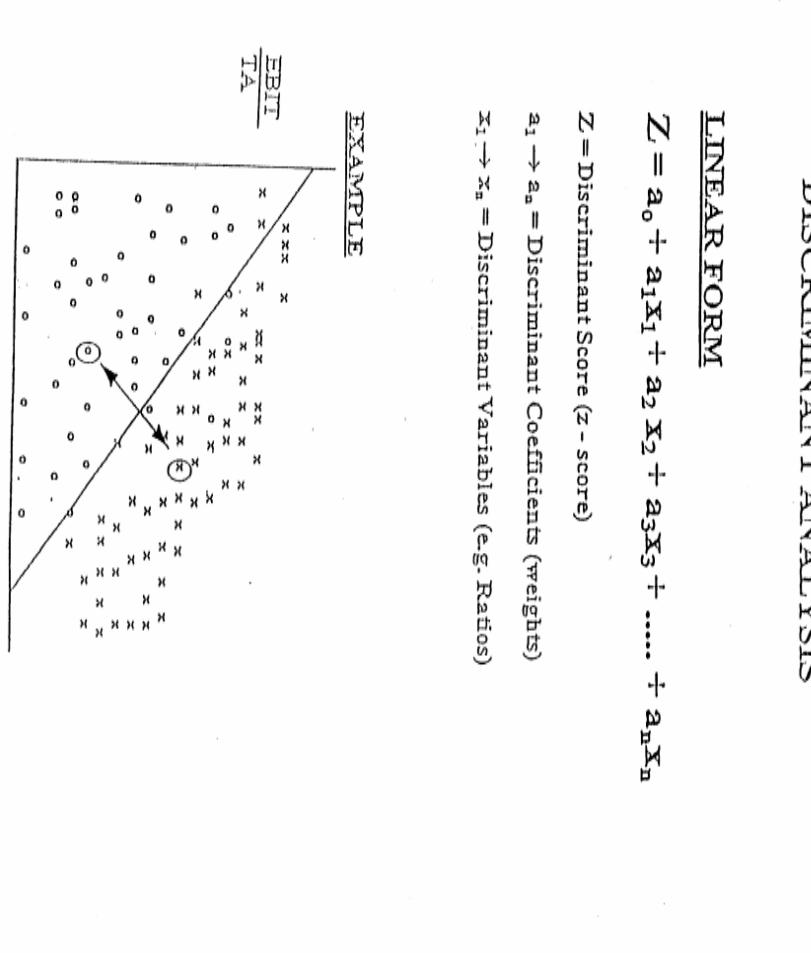

EM Score = 3.25 + 6.56 (X1) + (3.26) (X2) + 6.72 (X3) + 1.05 (X4)

Where X1 = Working Capital/Total Assets

X2 = Retained Earnings/Total Assets

X3 = EBIT/Total Assets

X4 = Book Value Equity/Total Liabilities

*An enhancement of E. Altman’s Z”-Score model, Corporate Financial Distressand Bankruptcy, John Wiley & Sons, N.Y. (1993), Chapter 8.

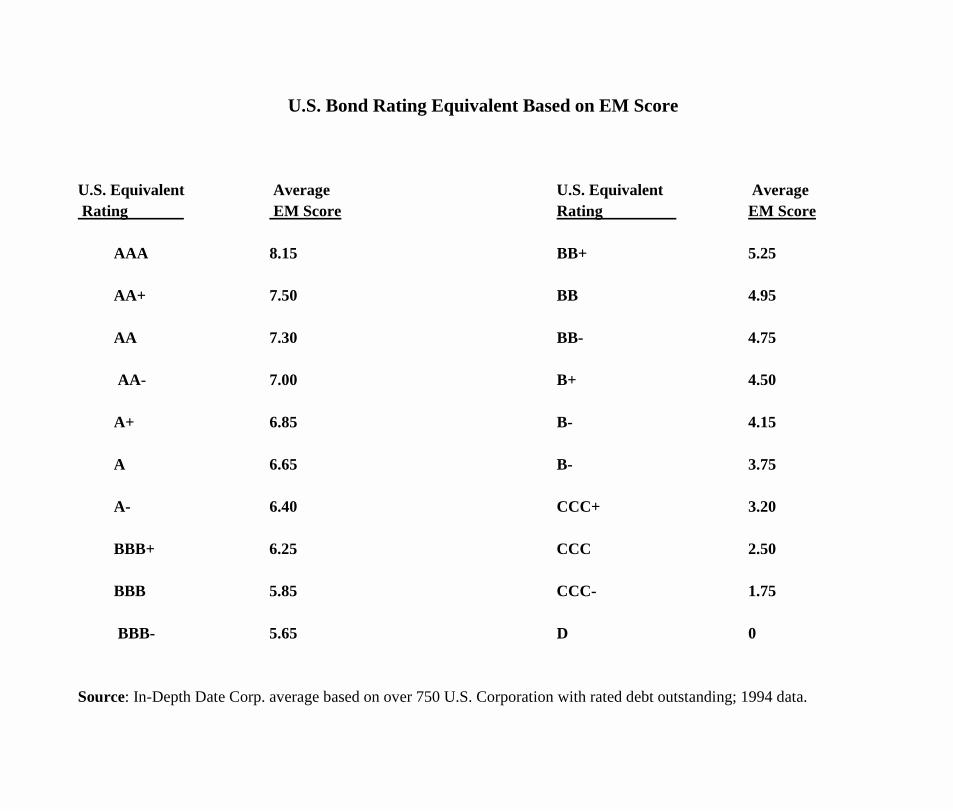

U.S. Bond Rating Equivalent Based on EM Score

U.S. Equivalent Average U.S. Equivalent AverageRating EM Score Rating EM Score

AAA 8.15 BB+ 5.25

AA+ 7.50 BB 4.95

AA 7.30 BB- 4.75

AA- 7.00 B+ 4.50

A+ 6.85 B- 4.15

A 6.65 B- 3.75

A- 6.40 CCC+ 3.20

BBB+ 6.25 CCC 2.50

BBB 5.85 CCC- 1.75

BBB- 5.65 D 0

Source: In-Depth Date Corp. average based on over 750 U.S. Corporation with rated debt outstanding; 1994 data.

Exhibit 1 – Mexican Corporate Issuers: EM Scores and Modified Ratings

DBBB+CCC-BBB+BB+A

BBB-B

BB-BB+BB-B-BB+BBB-BB-B+CCCBBB+B+AA+BB+B+A+BB+BBCCCCCC+

Modified Rating

NR/NR/NRNR/NR/BNR/NR/NRNR/NR/NRBa3/NR/NRBa2/NR/NRBa3/BB/BBNR/NR/NRNR/NR/NRNR/NR/NRNR/NR/CCCB3.NR/NRB1/BB-/B+NR/NR/NRBa2/NR/NRNR/NR/CCCNR/NR/NRBa2/NR/NRB1/BB-/NRNR/NR/NRNR/NR/NRNR/NR/NRNR/NR/NRBa2/BB-/NRNR/NR/NRNR/NR/NRNR/NR/CCCNR/NR/NR

DBBB-CCC

A-BB+AAABBB-BB-B

BB+BB-BBBBBBBB-BB+BB+CCC-AAB+

AAAA

BB-AAABB+BBB-BBB-B+CCC+

-4.425.542.596.375.408.485.574.674.235.284.684.855.965.565.185.171.597.294.518.966.644.789.855.345.515.454.423.34

AirlinesAuto ManufacturingAutopartsBottlingBottlingCementCementChemicalsConglomerateConglomerateConglomerateConstructionConstructionFood ProcessingGlassHotel and TourismTextile/ApparelCable and MediaPaper and Forest ProductsPaper and Forest ProductsPaper and Forest ProductsRetailRetailShippingSteelSteelSteelSteel Pipes

AeromexicoGrupo DinaSan LuisFemsaGemexApascoCemexCydsaDESCModernaSidekGMDEmpresas ICAGrumaVitroSiturSynkroTelevisaGIDUSA (Durango)Kimberly-Clark de MexicoPonderesaCCMLiverpoolTMMHylsamexUSASimecTAMSA

RatingsM/S&P/D&P

Bond-Rating Equivalent

EM Scores

IndustryCompany

NR: No rating: M: Moody’s; S&P: Standard & Poors; D&P: Duff & Phelps: Ratings are for senior long-term foreign debt Unless otherwise specified.Sources: Salomon Brothers Inc.

Step 2: Adjusted Bond Rating for Foreign Currency Fluctuation Vulnerability

•Each bond is analyzed as to the issuing firm’s vulnerability to problemsin servicing its foreign currency denominated debt if the local currencyis devalued

•Vulnerability is assessed based on (1) the relationship between non-localcurrency revenues minus costs compared to non-local currency interestexpense and (2) non-local currency revenues vs. non-local currency debt.Finally, (3) the level of cash is compared with the debt coming due in thenext year.

•If the firm has high vulnerability, e.g., low or zero non-local currencyrevenues and/or low or zero revenues/debt, and/or a substantial amountof foreign currency debt coming due with little cash liquidity, then the bond rating equivalent in step 1 is lowered by a full rating class, e.g.,BB+ to B+. Average vulnerability results in a one-notch, e.g., BB+ to BB,reduction. There is no upgrade for a good vulnerability assessment.

Step 3:Adjustment for Industry Risk

•The original (step 1) bond rating equivalent is compared to the generic

industry bond rating equivalent. For up to one full letter grade difference

between the two ratings, step 2’s bond rating equivalent is adjusted up or

down by one notch. For example, if the rating from step 1 is BBB and the

industry’s rating is BBB-, BB+, or BB, then the adjustment is one notch

down. If the difference is more than one full rating class but less than two

full ratings, there is a 2 –notch adjustment, etc.

Average Credit Safety of Industry Groups – Salomon Brothers

Average Sector Credit Safety12/94 12/00

Telecommunication High A High BBB1

Independent Finance High A Low ANatural Gas Utilities High A Low ABeverages High A Mid AHigh Quality Electric Utilities High A High BBBRailroads High A Low AFood Processing Mid A Mid BBBBottling Mid A Mid ADomestic Bank Holding Low A High ATobacco Low A Low BBMedium-Quality Electric Utilities Low A Mid BBBConsumer Products Industry Low A Mid AH.G. Diversified Mfg./Conglomerates Low A Low BBBLeasing Low A ----Auto Manufacturers Low A Mid BB

Chemicals Low A Low BB

Average Sector Credit Safety12/94 12/00

Energy Low A Mid BBBNatural Gas Pipelines High BBB Mid BBBPaper/Forest Products Mid BBB Low BBBRetail Mid BBB Mid BBP&C Insurance Mid BBB Mid BBAerospace/Defense Mid BBB Mid BBBInformation/Data Technology Mid BBB Mid BBBSupermarkets High BB High BBCable and Media High BB High BBBVehicle Parts High BB Mid BTextile/Apparel High BB Low BBLow-Quality Electric Utilities Mid BB Low BBGaming Mid BB Low BBRestaurants Mid BB Low BBConstruction Mid BB Mid BHotel/Leisure Mid BB Mid BBLow Quality Manufacturing Mid BB Mid BBAirlines Low BB Mid BBMetals High B -----

Source: Adapted from Six-Month Credit Quality Overview, Salomon Brothers Inc., January 18, 1995 and six month High-Grade Rankings, Salomon Smith Barney, January 2001 (terminology for rankings changed to numerical).

1Established telecommunications firms (Low B for most others)

Step 4:Adjustment for Competitive Position

•Step 3’s rating is adjusted up (or down) one notch if the firm is a dominant

(or not) company in its industry or if it is a domestic power in terms of

size, political influence and quality of management. It is possible that the

consensus competitive position result is neutral (no change in rating).

Step 5:Adjustment for Market Value vs. Book Value of Equity

Most Emerging Market Eurobond Issuers have public equity sharesoutstanding. Since market equity value should reflect expectations andbook equity reflects historical values, we adjust the bond rating equivalent (BRE) for the market/book equity ratio. EM Scores and their bond ratingequivalents are compared using the two measures of equity value. Wheresignificant differences manifest, a further adjustment is made:

Adjustment Process:

BRE (Book) vs. BRE (Market)

BRE Difference Adjustment

± 0,1 Notch = None

± 2 Notches = ± 1 Notch

≥≥≥≥ ± 3 Notches = ± 2 Notches

Step 6:Bond Specific Adjustment

•Any unique aspects of the bond, e.g., collateral, guarantees, etc., could

impact the final rating and spread.

Figure 1. Mexican Corporate Issuers – December 1995 Modified Ratings

NR/NR/NRNR/NR/NRBa2/NR/NRNR/NR/NRNR/NR/NRBa3/BB.BBNR/NR/NRNR/NR/BBNR/NR/NRB1/BB-/B+NR/NR/NRBa3/NR/NRB1/BB-/NRB3/NR/NRNR/NR/NRNR/NR/NRNR/NR/NRNR/NR/NRNR/NR/NRNR/NR/NRNR/NR/NRNR/NR/NRNR/NR/NRNR/NR/NRNR/NR/NRNR/NR/CCCNR/NR/CCCNR/NR/CCCNR/NR/NRNR/NR/NRNR/NR/NRBa2/NR/NR Ba3/BB/BBBa2/BB-/NRB1/B+/B NR/NR/NR

CCC+BBB-BB-BAA-BB+BBB-BBB+BBB+BB+B+BBBCCCBBB-ABBB+BB-BBB-BA+A+BBB-A+B-CCC-B+CCC-DB+AA-BBB-A-BBBCCCB

DNRBBB+BNRBBB-BBNRBB+BB-BBB-BB-BB+CCC+BBB+NRBB-BB-NRNRAA-A+BBBBBBB-B-BCCC+CCCB+AA-BBB+NRBB+CCC+BB-

DNRAB+NRBBB-B+NRBB+BBBBB+BB+BBB-BBB+NRBBBB-NRNRAAA+BB+BBCCC-BB-BCCCBAA-BBB+NRBB+B-BB

AirlinesSteel/ChemicalsCementRetailConglomerateCementChemicalsSteelConglomerateConstructionBottlingBottlingPaper & Forest ProductsConstructionFood ProcessingMiningSteelSteelSteelTelecommunicationPaper & Forest ProductsRetailConglomeratePaper & Forest ProductsAutopartsConglomerateSteelHotel and TourismTextile/ApparelSteel PipesTelecommunicationCable and MediaCementShippingConstructionGlass

AeromexicoAltaApascoCCMCarsoCemexCydsaCondumexDESCEmpresas ICAFemsaGemexDurangoGMDGrumaGrupo MexicoHylsamexIMSAIspal MexicanaIusacellKimberly-Clark De MexicoLiverpoolModernaEmpaques PonderosaSan LuisSidekSimecSiturSynkroTamsaTELMEXTelevisaTolmexTMMTribasaVitro

RatingsM/S&P/D&P

Dec 1995ModifiedRating

July 1995ModifiedRating

May 1995ModifiedRating

IndustryCompany

NR: No rating; M: Moody’s; S&P: Standard & Poor’s; D&P: Duff & Phelps.

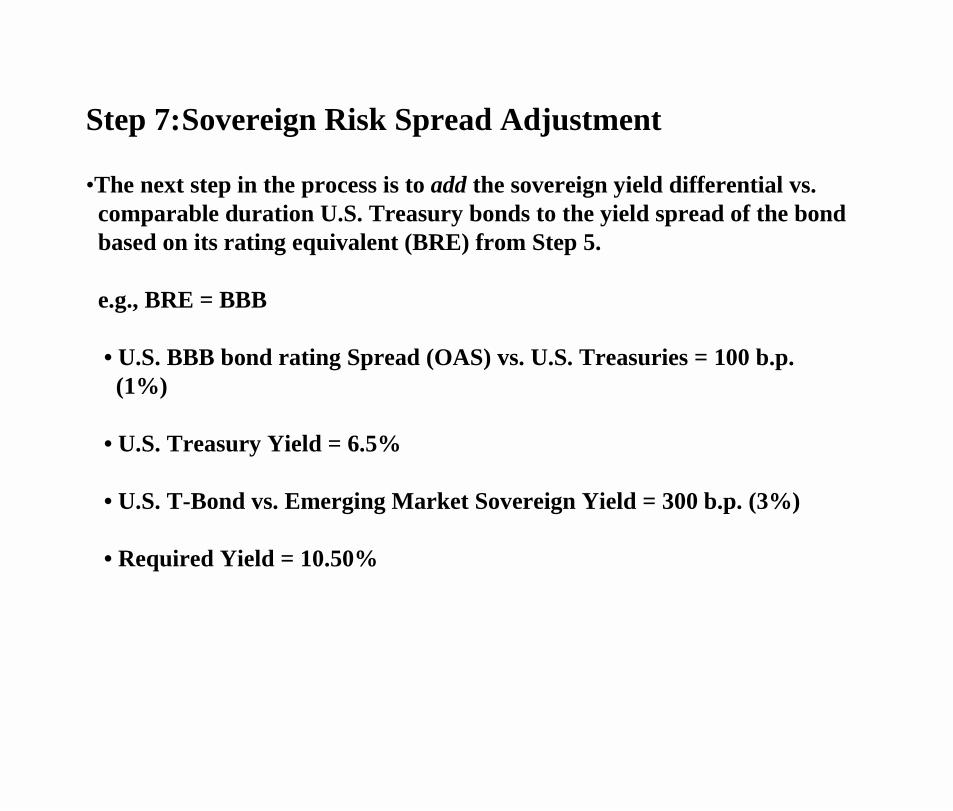

Step 7:Sovereign Risk Spread Adjustment

•The next step in the process is to add the sovereign yield differential vs.comparable duration U.S. Treasury bonds to the yield spread of the bondbased on its rating equivalent (BRE) from Step 5.

e.g., BRE = BBB

• U.S. BBB bond rating Spread (OAS) vs. U.S. Treasuries = 100 b.p. (1%)

• U.S. Treasury Yield = 6.5%

• U.S. T-Bond vs. Emerging Market Sovereign Yield = 300 b.p. (3%)

• Required Yield = 10.50%

EM Scores & Bond Rating EquivalentsMexican Companies

CCC-B

BBB+

DB-

DB

DCCC

2.4084.379

3.8675.512

(0.140)4.087

0.0844.405

(1.007)2.659

Jul-99

May-99

Mar-99

Mar-96

Oct-95

Construction

Automotive

Construction

Diversified Property

Apparel

Bufete Industrial S.A

Cons. G Grupo Dina S.A. De C.V.

Grupo Tribasa S.A. De C.V.

Grupo Situr S.A. De C.V.

Synkro S.A. De C.V.

Bond Rating Equivalent

EM Score(T-1/T-2)

Default Date

IndustryCompany

CCC+CCC

BBB-AA

B-BB-

CCCCCC

DCCC-

3.7434.379

5.6937.409

4.0104.087

2.7252.837

1.7242.328

Oct-99

Oct-97

Jul-97

Jul-97

Jul-97

Electronics

Electronics

Automotive Mfg.

Automotive Mfg

Metal Producer

Orion Electric Co. Ltd.

Tae IL Media Co., Ltd

Asia Motors Co., Ltd

Kia Motors Corp.

Kia Steel Co., Ltd.

Bond Rating Equivalent

EM Score(T-1/T-2)

Default Date

IndustryCompany

EM Scores & Bond Rating EquivalentsKorean Companies

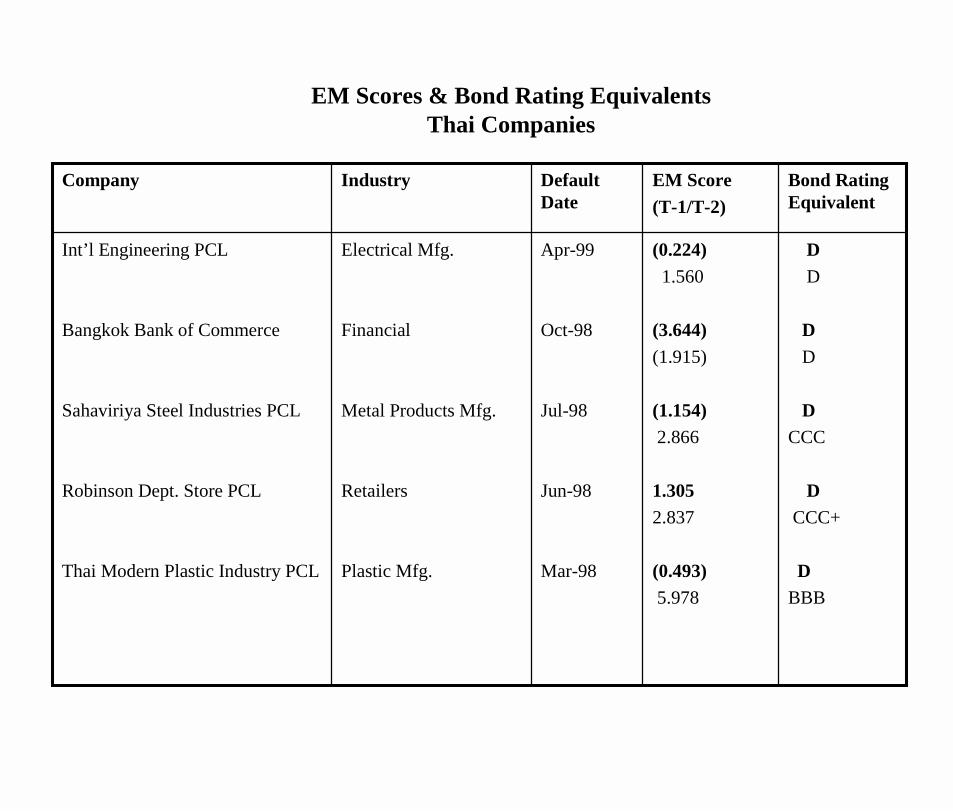

DD

DD

DCCC

DCCC+

DBBB

(0.224)1.560

(3.644)(1.915)

(1.154)2.866

1.3052.837

(0.493)5.978

Apr-99

Oct-98

Jul-98

Jun-98

Mar-98

Electrical Mfg.

Financial

Metal Products Mfg.

Retailers

Plastic Mfg.

Int’l Engineering PCL

Bangkok Bank of Commerce

Sahaviriya Steel Industries PCL

Robinson Dept. Store PCL

Thai Modern Plastic Industry PCL

Bond Rating Equivalent

EM Score(T-1/T-2)

Default Date

IndustryCompany

EM Scores & Bond Rating EquivalentsThai Companies

EM Scores & Bond Rating EquivalentsMalaysian Companies – 1998 (Fiscal Year)

B

BB

AAA

B

B+

CCC+

BB+

Bond Rating Equivalent

Airlines

Hotel & Leisure

Construction

Construction

Construction

Construction

Manufacturing

Industry

Malaysia

Country

Malaysian Airlines

Metroplex

YTL

KL Industries

United Engineers

Renong (1)

Sungel Way

Company

NR/NRNR

NR/NR/NR

AA1/NR/NR

NR/NR/NR

NR/NR/NR

D/NR/NR

A3/NR/NR

CCC

BB-

AA+

CCC+

CCC+

D

BB+

3.70

4.94

8.48

4.33

4.55

3.30

5.82

RatingsRAM/M/S&P

ModifiedRating

EM Score

(1)Defaulted in 1997

Sources of Data: Bloomberg, Datastream and Dateline

NR/NRNR

NR/NR/NR

NR/NR/NR

NR/NR/NR

NR/NR/NR

NR/NR/NR

NR/NR/NR

NR/NR/NR

CCC-

D

AA-

A-

BBB

BBB-

AA

AAA

BBB-

D

AA+

A-

BBB

BBB-

AA+

AAA

5.66

-4.57

7.93

6.42

5.97

5.77

7.98

9.51

Computers

Infrastructure

Property

Property

Property

Beverages

Motor vehicle

Manufacturing

IPC

Van Der Horst(1)

First Capital Corp

City Development

DBS Land

Fraser & Neave

Cycle & Carriage

Venture Mfg.

Singapore

RatingsRAM/M/S&P

ModifiedRating

Bond Rating Equivalent

EM ScoreIndustryCompanyCountry

EM Scores & Bond Rating EquivalentsSingapore Companies – 1998 (Fiscal Year)

(1)Technical Default, 1997.Source of Data: Bloomberg, Datastream and Dataline.

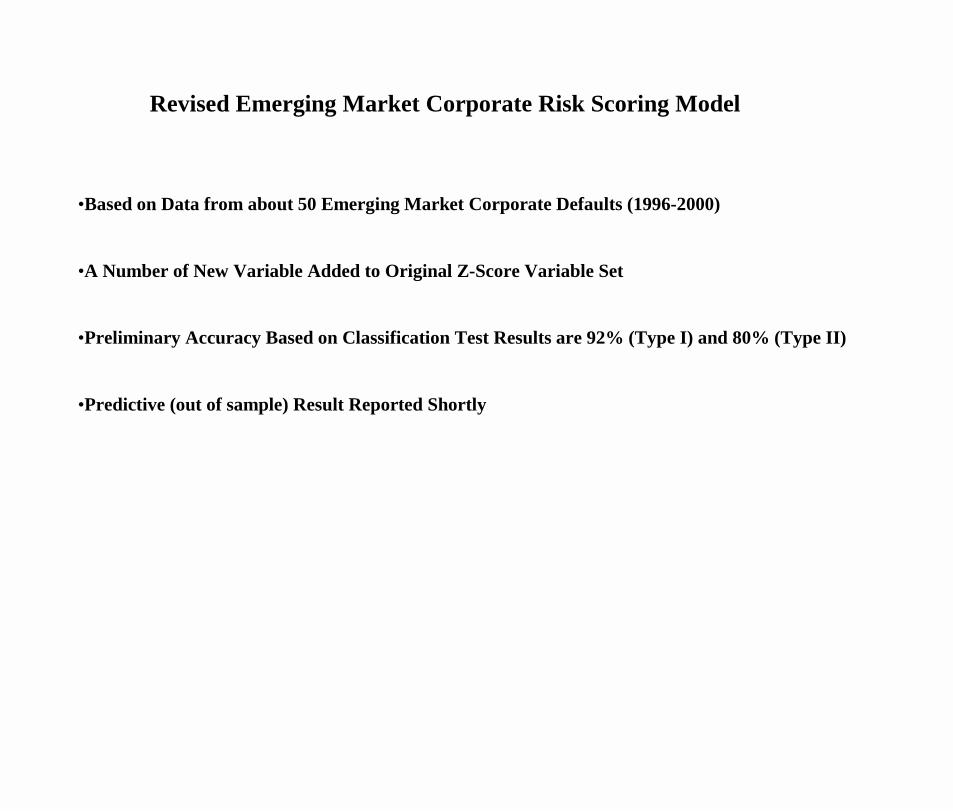

Revised Emerging Market Corporate Risk Scoring Model

•Based on Data from about 50 Emerging Market Corporate Defaults (1996-2000)

•A Number of New Variable Added to Original Z-Score Variable Set

•Preliminary Accuracy Based on Classification Test Results are 92% (Type I) and 80% (Type II)

•Predictive (out of sample) Result Reported Shortly