a crash course on legal issues arising in the animation...

TRANSCRIPT

ENTERTAINMENT LAW 101A Crash Course on Legal Issues Arising in the

Animation Industry

Friday, March 4, 2011

Paul Chodirker and Bob Tarantino, Heenan Blaikie LLP

1

Agenda

Introduction

Pre-production (chain-of-title, transfer of rights, E&O insurance, and clearance issues)

Principal Production (Performer agreements, crew, and unions/guilds)

Post-production (Music licensing, credits, and distribution)

Tax credits and Canadian content certification

How to use legal counsel effectively

Q and A

2

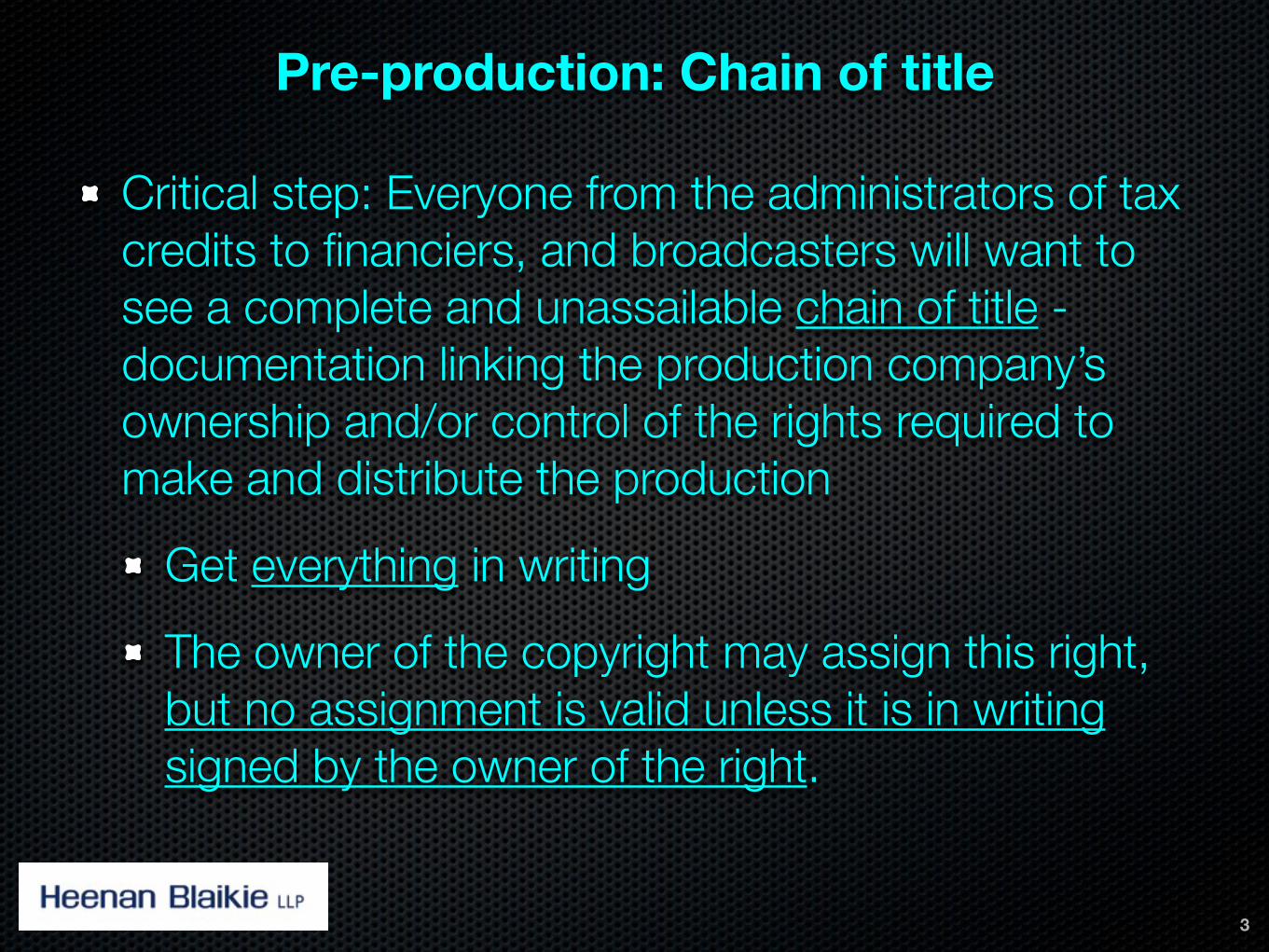

Pre-production: Chain of title

Critical step: Everyone from the administrators of tax credits to financiers, and broadcasters will want to see a complete and unassailable chain of title - documentation linking the production company’s ownership and/or control of the rights required to make and distribute the production

Get everything in writing

The owner of the copyright may assign this right, but no assignment is valid unless it is in writing signed by the owner of the right.

3

Pre-production: Chain of title

Overview:

Step 1: Do you have the underlying creative rights?

Step 2: Do you have a written contract with everyone who makes any contribution whatsoever to the production (this is critical for obtaining E&O insurance coverage)

Subsequent Steps: Option Agreement, performers, writers, etc.

4

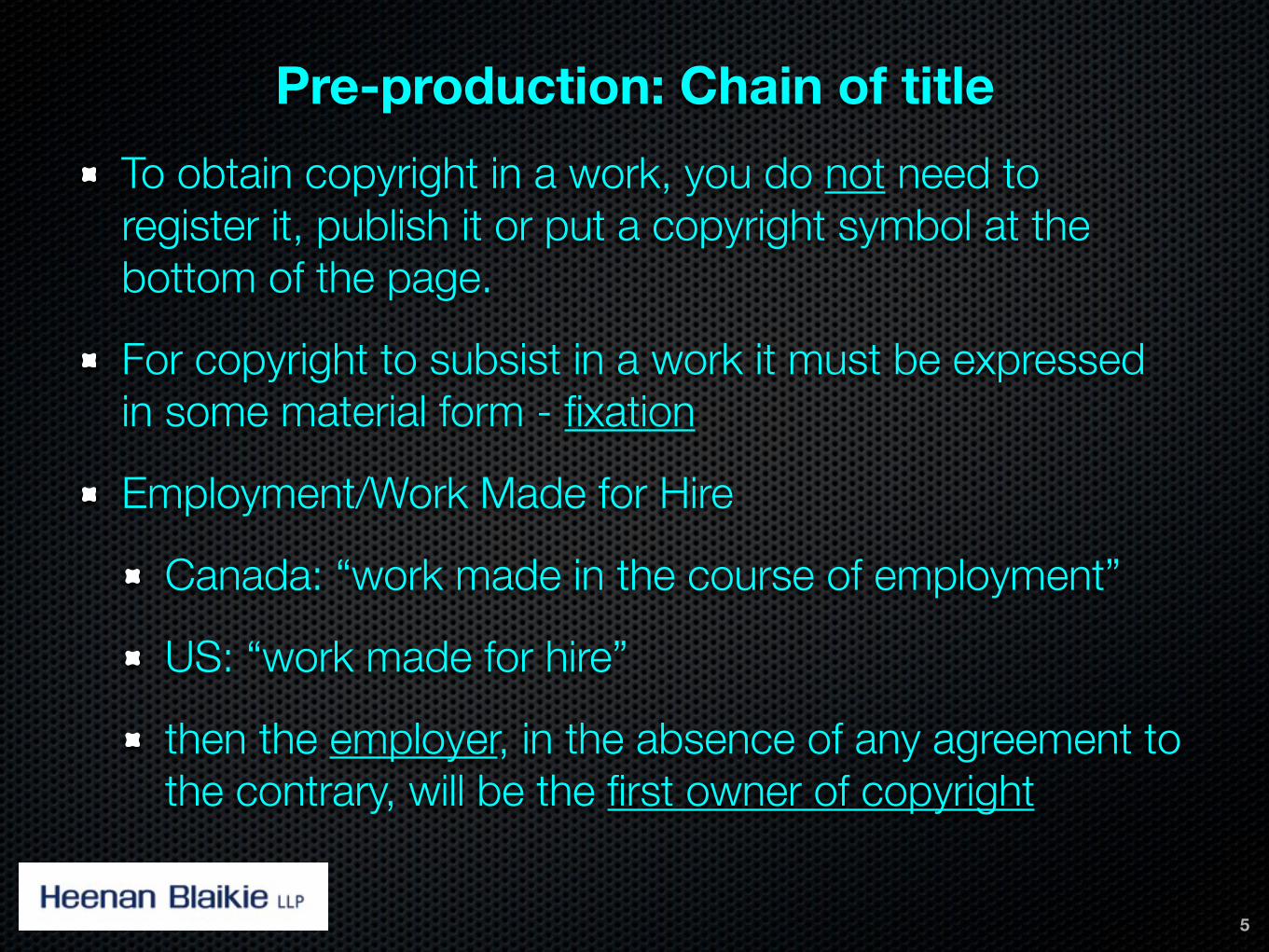

Pre-production: Chain of title

To obtain copyright in a work, you do not need to register it, publish it or put a copyright symbol at the bottom of the page.

For copyright to subsist in a work it must be expressed in some material form - fixation

Employment/Work Made for Hire

Canada: “work made in the course of employment”

US: “work made for hire”

then the employer, in the absence of any agreement to the contrary, will be the first owner of copyright

5

Pre-production: The Option

Contract which confers the exclusive right to purchase the underlying material

Rights being Optioned/Purchased (i.e. screenplay, book, character designs, film shorts)

Option Price (For payment of the option price, the Producer is granted the exclusive right to acquire a license to produce a production based on the optioned “material”)

Purchase Price (Is there a minimum?) 6

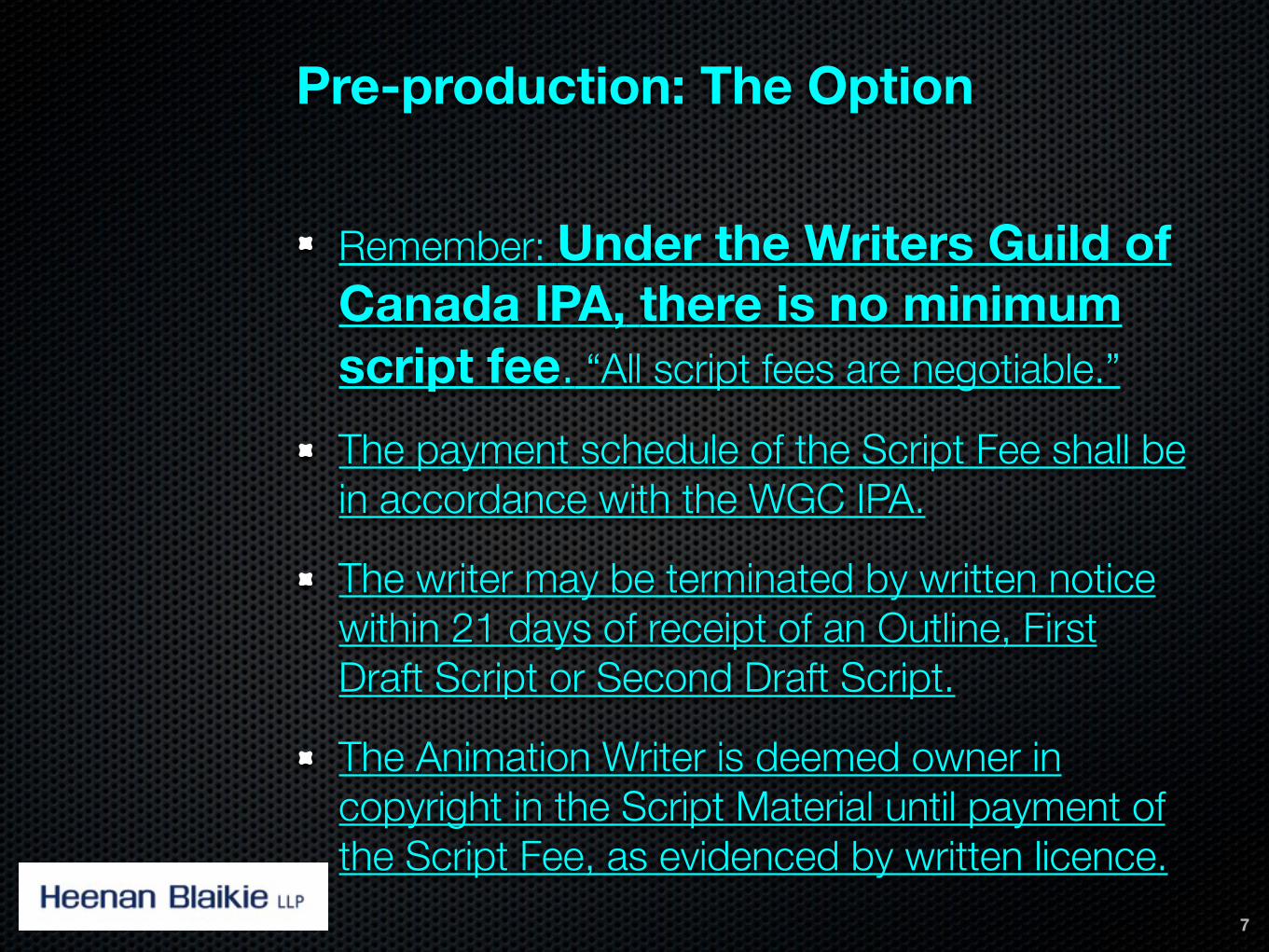

Pre-production: The Option

Remember: Under the Writers Guild of Canada IPA, there is no minimum script fee. “All script fees are negotiable.”

The payment schedule of the Script Fee shall be in accordance with the WGC IPA.

The writer may be terminated by written notice within 21 days of receipt of an Outline, First Draft Script or Second Draft Script.

The Animation Writer is deemed owner in copyright in the Script Material until payment of the Script Fee, as evidenced by written licence.

7

Acquisition of Property: The Option

Option Term (Eq. The initial option period shall be for a period of two years with an option to renew for one year)

Remember: An option agreement does not in itself constitute a license to produce

Reserved Rights/Reversion (What rights will be retained by the author, or revert to author?)

8

Pre-production: E&O Insurance

Producers and distributors are constantly at risk of being exposed to lawsuits as a result of a production’s content such as invasion of privacy, defamation, infringement of copyrights and/or trademarks

Errors and omissions insurance protects against such lawsuits (such policies are usually extended to distributors, financiers, and other third parties)

Remember: E&O does not protect producers from everything (i.e. contract-related claims, intentional wrongdoing and injunctions brought against the production)

9

Pre-production: E&O Insurance

Timing of when to bind the coverage is a matter of judgement.

The E&O application will set forth a non-exhaustive list of procedures to be followed:

Copyright report and title report must be obtained

Chain of title

Releases and licenses

Synchronization and master-use licenses

10

Pre-production: E&O Insurance

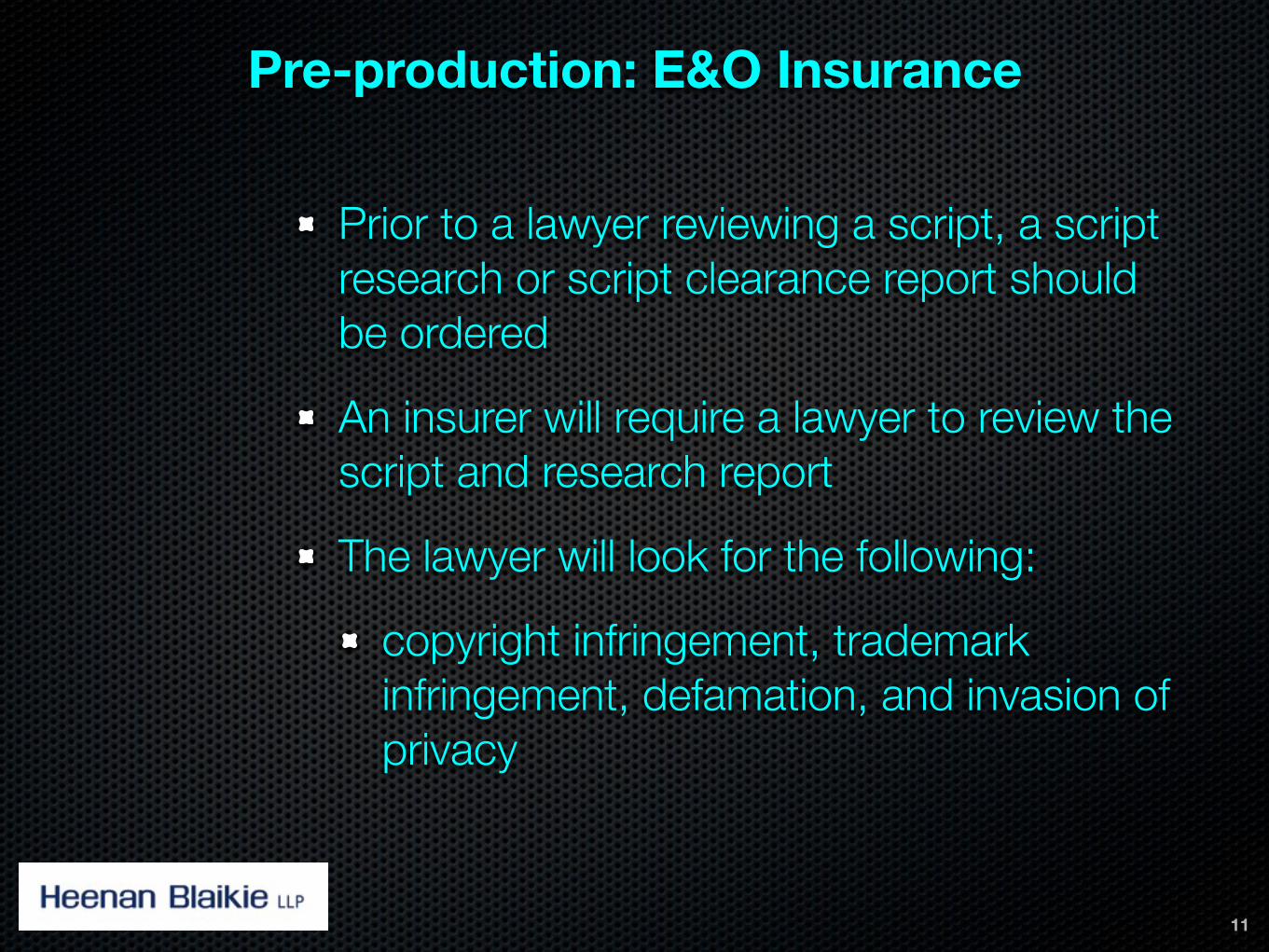

Prior to a lawyer reviewing a script, a script research or script clearance report should be ordered

An insurer will require a lawyer to review the script and research report

The lawyer will look for the following:

copyright infringement, trademark infringement, defamation, and invasion of privacy

11

Pre-production: E&O Insurance

12

Tips Checklist:

Do not use real names for people or organizations

If real names are used, do not make any defamatory statements about them

Do not use identifiable locations and addresses

Do not use trademarks and logos

Do not make dialogue references to companies and products

Do not use music without permission

Obtain all necessary consents, licenses and releases

Principal Production: Talent

Deal Memo:

Assists the producer with obtaining financing based on secured talent

Forms basis for formal contract - Performers Agreement

Exclusivity of Services

During principal photography and re-shoots or Alternative Dialogue Replacement

Rights granted by artist to producer:

Results and proceeds belong to producer to allow for exploitation of the performance

“Name and Likeness” and appearances for marketing and promotional purposes

Production, casting/staffing and shooting schedule control

IMPORTANT: GET A WAIVER OF INJUNCTIVE RELIEF

13

Principal Production: Talent

14

Animation Performers:

Members of a guild - such as ACTRA

Different regulations regarding animation

Minimum fees for animation performers and for short animated productions

Dubbing of animated productions - Dubbing Section

Initial recording session of an animated series shall include 8 hours of work at the rate of a regular 4 hour call

Doubling - additional roles by principal animation performers without additional payment (role shall not exceed 10 consecutive words)

Crowd noises or incidental sounds and words are not considered a performance

Post-Production: Music Licenses

All music should be cleared before using it to avoid having to remove it

Required licenses:

Synchronization - from publishers

Master Use - usually from record label

Soundtrack use rights

Consider using a music clearance house - for a percentage fee based on the music budget

Music Composition Agreements - details the ownership of composed work

15

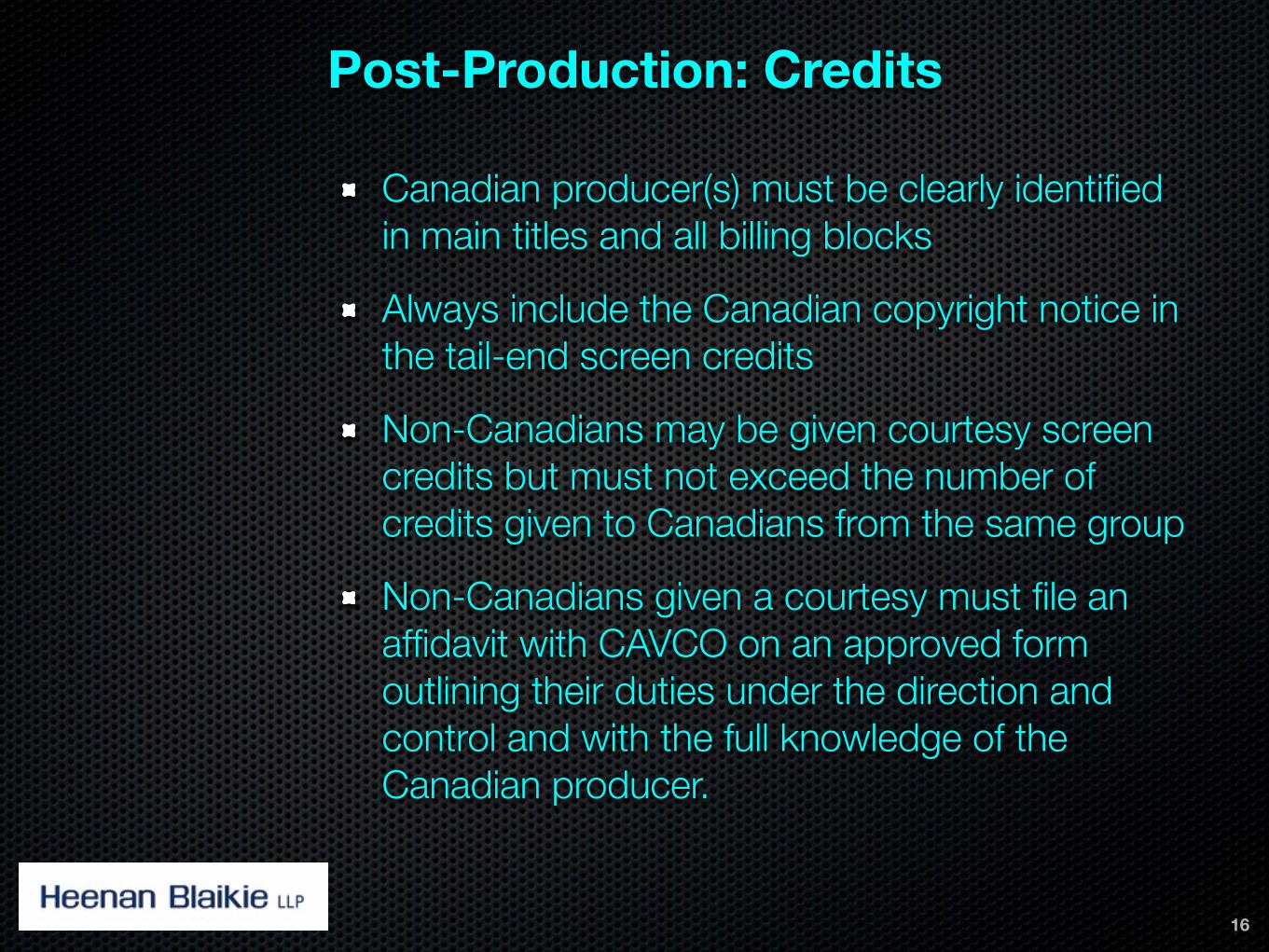

Post-Production: Credits

Canadian producer(s) must be clearly identified in main titles and all billing blocks

Always include the Canadian copyright notice in the tail-end screen credits

Non-Canadians may be given courtesy screen credits but must not exceed the number of credits given to Canadians from the same group

Non-Canadians given a courtesy must file an affidavit with CAVCO on an approved form outlining their duties under the direction and control and with the full knowledge of the Canadian producer.

16

Post-Production: Distribution

Distribution Rights:

Theatrical/Non-Theatrical

Standard TV/Non-Standard TV

Video/Online

Territorial Rights (Regional/National/International)

Revenue Guarantees and Advances - production financing

Net and Gross Receipts

Choose a distributor - www.telefilm.gc.ca

Consider hiring a sales agent to assist with entering distribution agreements outside Canada

17

Tax Credits

What is it?

Total production costs are reduced by federal and provincial tax credits in the form of a refundable income tax credit

Available to Canadian-controlled taxable corporations whose primary business is the production of Canadian films and videos

Federal (Canadian and non-Canadian services), provincial (Canadian and non-Canadian services), Ontario Computer Animation and Special Effects (“OCASE”) tax credit, and inter-provincial

18

Tax Credits

How much?

Ontario: 35% of eligible Ontario labour expenditures

Federal: 25% of labour expenditures

OCASE: 20% of eligible Ontario labour expenditures; qualifying corporations can include animation or visual effects houses, post-production houses, etc.

Note: The OCASE credit does not reduce the Ontario credit, though both reduce the production budget for the purpose of the Federal calculation

19

Tax Credits

Who is eligible?

Ontario and Federal credit: “Canadian-controlled production corporation”

OCASE: A “Canadian corporation” that is Canadian or foreign-owned (create digital animation or digital visual effects at a permanent establishment in Ontario)

Ontario and Federal: 75% of total production costs are Ontario/Canadian expenditures

Eligible productions must have a minimum of 6 out of 10 Canadian Content points as defined by the Canadian Audio-Visual Certification Office (“CAVCO”)

20

Tax Credits

To be recognized as a Canadian production, an animation production must be allocated a total of at least six (6) points according to the following scale (points are allocated to individual(s) who are Canadian):

Director, 1 point / Screenwriter and storyboard supervisor, 1 point / lead voice (1st or 2nd highest paid), 1 point / design supervisor, 1 point / camera operator where camera operation is done in Canada, 1 point / music composer, 1 point / picture editor, 1 point

Layout and background, 1 point / key animation, 1 point / assistant animation and in-betweening, 1 point

For the production to be considered Canadian, the following conditions must be fulfilled: either the director, or the screenwriter and storyboard supervisor must be Canadian; the lead voice for which the highest or second highest remuneration was payable must be Canadian; and the key animation must be done in Canada

21

Federal Tax Credits

The Canadian Film or Video Production Tax Credit (“CPTC”)

Refundable tax credit for 25% of labour expenditures

The Canadian Film or Video Production Services Tax Credit (“PSTC”)

Refundable tax credit for 16% of labour expenditures paid to Canadian residents

Scientific Research and Expiremental Development Tax Incentive Program

Up to 35% of the first $3 million of qualified expenditures carried out in Canada by a Canadian-controlled private corporation

Experimental development, applied research and basic research

22

Ontario Tax Credits

Film and Television Tax Credit

35% of eligible labour expenditures - not capped

First time producers - 40% on the first $240,000

Production Services Tax Credit

25% of all qualifying production expenditures in Ontario

Canadian and foreign production companies are eligible

No content requirements beyond having a permanent establishment in Ontario (including a production office during filming)

23

Ontario Tax CreditsInteractive Digital Media Tax Credit

Ontario supports the development of the digital media industry through OIDMTC.

40% of eligible labour expenditures (no maximum) as well as eligible marketing and distribution expenses up to $100,000 - “in the development of an interactive digital media product.”

35% of eligible labour expenditures with respect to “specified products” - interactive digital media products that are developed under a fee-for-service arrangement under the terms of an agreement between the qualifying corporation and and arm’s length purchaser corporation

“Interactive Digital Media Product” - Primary purpose is to educate, inform, and entertain, and achieves that by presenting information in at least two of the following: text/sound/images

24

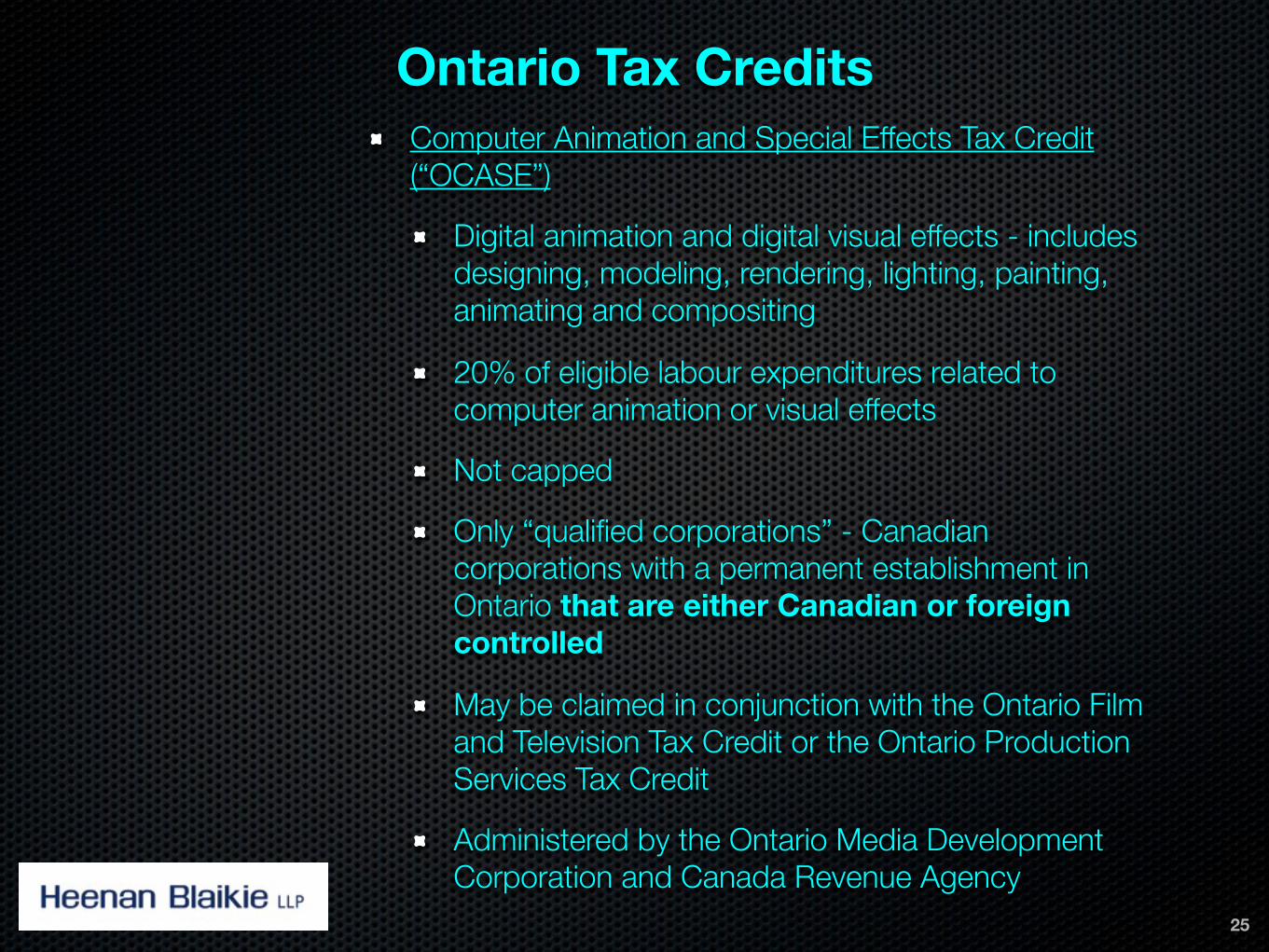

Ontario Tax CreditsComputer Animation and Special Effects Tax Credit (“OCASE”)

Digital animation and digital visual effects - includes designing, modeling, rendering, lighting, painting, animating and compositing

20% of eligible labour expenditures related to computer animation or visual effects

Not capped

Only “qualified corporations” - Canadian corporations with a permanent establishment in Ontario that are either Canadian or foreign controlled

May be claimed in conjunction with the Ontario Film and Television Tax Credit or the Ontario Production Services Tax Credit

Administered by the Ontario Media Development Corporation and Canada Revenue Agency

25

Tax Credits

In short..

Tax credits can provide 20-30% of total production budget

Remember that the 75% is a presumption - always get labour expenditure statements from suppliers

26

Federal Incentive ProgramsCanada Media Fund (“CMF”)

Formerly the Canadian Television Fund and Canada New Media Fund operating with a $350 million budget

Two streams: Experimental and Convergent

Experimental - for innovative and interactive digital content with maximum contribution of 75% of eligible costs or $1 million (whichever is less)

Convergent - for creation of TV shows and related digital media content for drama, documentary, children’s and youth, and variety and performing arts with at least one digital media platform and high levels of Canadian elements, including Canadian creative content

Canadian Independent Film and Video Fund

The Harold Greenberg Fund

Independent Production Fund

Scientific Research and Experimental Development Tax Incentive Program 27

Ontario Incentive ProgramsOntario Media Development Corporation Film Fund (“OMDC”)

Ontario producers for feature film projects

Development (final stage) - up to $25,000 interest free loan

Production - up to $400,000 repayable advance on last-in basis to complete financing

Minimum amount of 85% of the total number of days of key animation must be done in Ontario

CJOH-TV/CTV Television Incorporation Development Fund

Ontario Arts Council

Toronto Arts Council Grants to Media Artists Program

TV Ontario28

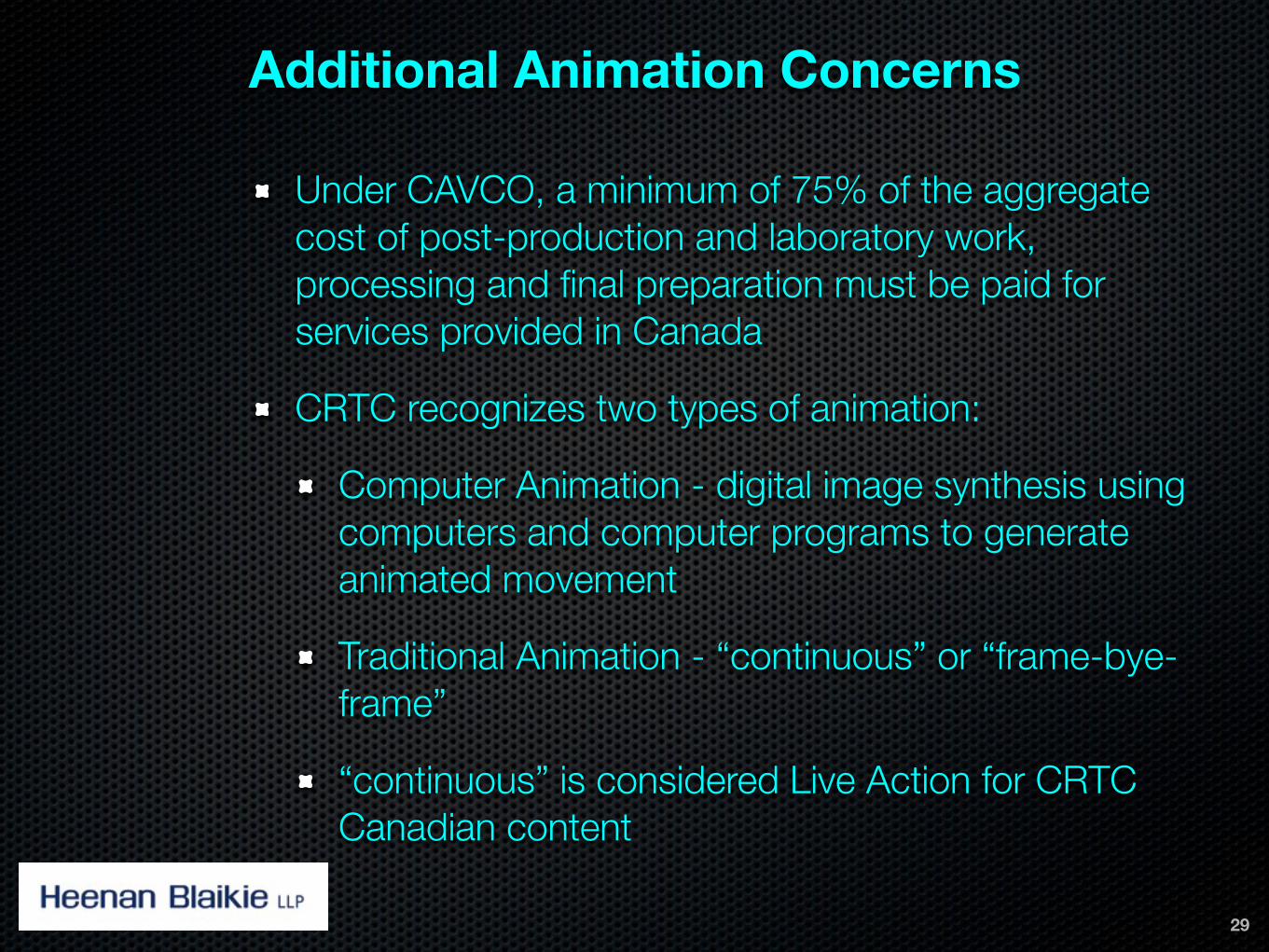

Additional Animation Concerns

Under CAVCO, a minimum of 75% of the aggregate cost of post-production and laboratory work, processing and final preparation must be paid for services provided in Canada

CRTC recognizes two types of animation:

Computer Animation - digital image synthesis using computers and computer programs to generate animated movement

Traditional Animation - “continuous” or “frame-bye-frame”

“continuous” is considered Live Action for CRTC Canadian content

29

How to use Legal Counsel Effectively?

Tasks we can assist with:

Acquiring/granting of rights and ownership

Acquiring/granting of options

Chain of Title opinions

E & O Insurance applications

Canadian content certification opinions

Production Financing (including applications for tax credits and incentive programs)

And remember...always ask first to avoid any major setbacks!

30

ANY QUESTIONS??

31

32

Bob Tarantino, Heenan Blaikie LLP

Phone: 416-643-6815

E-mail: [email protected]

Paul Chodirker, Heenan Blaikie LLP

Phone: 416-643-6907

E-mail: [email protected]

www.entertainmentmedialawsignal.com

CONTACT INFORMATION