a contrarian look at hcit vendors

TRANSCRIPT

Steven A. Rubis [email protected] (202) 778-4780

Stifel Equity Trading Desk (800) 424-8870

Industry Update

Initiating Coverage on HCIT: CERN, CPSI, MDRX; A Contrarian Look at HCIT Vendors

We are initiating coverage on the enterprise EHR (electronic health record) industry with a negatively biasedHold rating, including Hold ratings on the shares of Cerner, Allscripts, and CPSI. We believe enterprise EHRsrepresent a structurally flawed business model set to face significant disruption over the next several years.

Overview. The flaws of the enterprise EHR industry revolve around: exorbitant costs, lengthy implementation cycles, lack

of interoperability, and ROI. We believe enterprise EHR vendors focus on transactional infrastructure for healthcare, a

commodity product. We believe the healthcare industry is shifting away from basic technology infrastructure investment

towards performance based technology investment driven by value-add software-enabled services (SES). We see the

shift manifesting itself via an unbundling of the EHR, whereby traditional vendors will dominate transactional functions, but

third party innovators will lead the value-added services.

The Unbundling of the EHR. The purpose of driving EHR adoption across the U.S. healthcare system revolved around

building a digital transactional foundation to facilitate the modernization of healthcare. We believe an unbundling of the

EHR is underway, whereby the services within an EHR are segmented into one of two areas: (1) transactions and (2)

value-added services. For the most part, we believe traditional EHR vendors focus on the transactional functions, and

have just begun to focus on value-add services. While some vendors are developing population health management and

revenue cycle solutions, we believe the core opportunity for these vendors revolves around the core transaction business.

The Triple Aim of Worry. Our industry outlook revolves around three questions: (1) can technology bend the national

health expenditure cost curve? We think bending the NHE cost curve represents the fundamental presupposition of digital

health and HCIT. (2) Will HCIT spend increase or decrease? We believe clients seek low cost, and agile solutions. We

believe performance driven solutions will put pricing pressure on non-performance driven solutions. (3) Will tech

investment revolve around performance? We believe operating margin pressure, reimbursement pressure, et al., will force

clients to make investment decisions according to performance not simply adoption.

The Shift from Infrastructure Driven to Performance Driven Technology Investment. We believe the unbundling of

the EHR revolves around the ongoing shift from infrastructure and mandate driven technology investment towards

performance driven technology investment. We believe the healthcare system yearns for agile, low cost solutions. We

believe the value proposition associated with high cost adoption and lengthy implementation cycles will erode over the

next several years. In our view, the rip and replace market opportunity will be extremely slow to develop and a new value

proposition (low cost and agile) will be required to gain share.

We See Drivers of Valuation, Such As Backlog, Recurring and Visible Revenue, As Negatives. Many investors view

massive backlogs as a positive for EHR vendors because such backlogs create recurring and visible revenue streams. In

our view, stability alone does not drive a valuation premium, but significant sustainable growth driven by a proprietary

technological advantage does. We believe massive backlogs present a problem for EHR vendors because backlogs

represent an impediment to innovation, and prevent a pivot to evolving growth opportunities.

Important Themes. The DoD EHR contract, competition from Apple and Google, athenahealth’s inpatient product

development efforts, digital health/mHealth, and the increasing importance of driving performance improvement and

operational efficiency throughout the continuum of care.

April 6, 2015

Internet & MediaDigital Healthcare

Stifel does and seeks to do business with companies covered in its research reports. As a result, investors shouldbe aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investorsshould consider this report as only a single factor in making their investment decision.

All relevant disclosures and certifications appear on pages 69 - 72 of this report.

Introduction

The Fundamental Question of Digital Healthcare. We believe investors can use one fundamental question as a way to distinguish between entities with significant long-term viability versus the possibility of looming uncertainty. The fundamental question of digital healthcare asks, “Does this business exist in and of itself without government sponsored mandates associated with Healthcare IT?”

In our view, the application of this question allows an investor to distinguish between infrastructure versus data driven and outcomes based services. We believe digital healthcare can be divided into two groups: traditional vendors, which are for the most part focused on infrastructure solutions and software-enabled services (SES) entities focused on developing data driven and outcomes based services. In our view, investors are currently willing to pay a premium for businesses with solid recurring and visible revenue streams despite unimpressive revenue growth. We believe valuation premiums should be driven by the underlying proprietary technological advantage of a specific company or platform. In our view, while businesses levered to government mandates may provide perceived stability, we believe government mandates do not represent a significant competitive advantage in a performance driven environment. We believe a government mandate environment creates an “I am in the business of making sure you need to do business with me” environment. A major problem we see with these mandates is that hospitals and physicians are not necessarily required to meet each component of each mandate. Often times, hospitals and physicians only need to meet a smaller portion of the entire mandate. Ironically, mandate deadlines are often delayed because of vendor, hospital, or physician complaints.

The Digital Healthcare Business Model Triptych. We believe digital healthcare and HCIT businesses can be segmented into three categories: (1) Businesses focused mostly on helping clients achieve government mandates (e.g., Meaningful Use, etc.). (2) Businesses focused on helping clients achieve mandates, but also providing some form of software-enabled services (SES). (3) Businesses primarily focused on developing software-enabled services, which utilize data, analytics, and technology to drive meaningful ROI and deliver meaningful performance improvement and operational efficiencies throughout the care continuum. In our view, the traditional electronic health records (EHR) vendors fall in categories one and two. We believe athenahealth and other small, nimble innovators fall into category three. We believe a key characteristic of category three revolves around revenue models with a risk-sharing component. Additionally, these businesses are attractive because these services help pay for themselves through meaningful performance.

The Unbundling of the EHR. We believe the functions of the EHR can be divided into two segments: transactional services, and value-add software-enabled services. In our view, transactional services are those parts of the EHR, which facilitate the day-to-day transactions of a hospital system. These services are typically aimed at meeting a government mandate and ensure regulatory requirement. We believe value-add software-enabled services are focused on those areas of an EHR that can drive performance improvement or operational efficiency across the care continuum. In our view, the industry is evolving to a point where smaller, more nimble innovators are able to develop solutions in the value-add software-enabled service area. Significant backlogs and government mandates keep traditional EHR vendors focused on the transactional services of the EHR, despite recent efforts to develop both revenue cycle management and population health management solutions.

Page 2

Internet & MediaDigital Healthcare April 6, 2015

Industry Is Shifting from Infrastructure to Software-Enabled Services (SES). We believe the digital healthcare industry and HCIT industry are undergoing a shift from a focus on infrastructure driven technology investment to performance driven technology investment. Given the government mandate environment driven by HITECH/ARRA, Meaningful Use, ICD-10, etc., we believe hospitals and physicians alike are experiencing installation fatigue. These numerous government mandates seem to have created an environment of incomplete foundational systems perpetuating a continuous cycle of upgrades and new module implementations. In our view, the high cost and long implementation cycles associated with traditional HCIT solutions are driving frustration. Based on industry commentary, we believe hospitals and physician groups recognize the value of a digitized healthcare system, but remain frustrated by a lack of low cost, and agile solutions. We believe many entities are likely to keep the technology systems in which they have invested. However, we believe these entities seek tools that can optimize and improve the function of their core technology investment. In our view, a robust rip and replace cycle will not materialize until a vendor introduces a product driven by low installation costs and short implementation cycles, which would mark a significant departure from the norms of traditional enterprise EHR vendors.

Which Is the Better Foundation, EHRs or Revenue Cycle Management? Given our view that the industry continues to shift towards performance driven technology investment, we believe a key question facing companies revolves around what makes for a better foundation, the EHR or revenue cycle management? In our view, the performance driven models of revenue cycle management are better positioned to succeed in a performance driven technology investment environment.

We think that the shift to SES creates a faceoff between EHRs and revenue cycle management. Many investors believe that because Epic and Cerner (CERN, Hold, $72.77) are the industry standards and that these vendors will dominate the industry in the future. We disagree with this view because, in our view, Epic and Cerner represent a standard around facilitating the baseline transaction. In our view, just because these platforms represent a standard for baseline transaction does not necessarily mean these same vendors will dominate the growth areas of the future (e.g., revenue cycle, population health management, telehealth, cost transparency, second opinions, precision medicine, or even patient engagement). Based on industry sources, we believe these vendors currently dominating the industry are not likely to lead consolidation of innovative SES companies because of their significant backlogs. In our view, traditional HCIT vendors, while they are now talking about new offerings around revenue cycle and even population health, remain focused on system installations and maintenance. We believe that these traditional HCIT vendors need to pivot or adjust their value propositions away from installation and maintenance to driving performance to dominate the industry in the future.

At the same time, we believe that health reform places a greater importance on efficient and automated RCM solutions. In our view, the next five to 10 years will be characterized by a greater emphasis on data and outcomes driven solutions providing meaningful ROI via performance improvement and operational efficiencies. In our view, EHR vendors will have trouble navigating the shift, and we do not believe their current dominance will translate to an SES environment.

Page 3

Internet & MediaDigital Healthcare April 6, 2015

We do believe that revenue cycle vendors are uniquely positioned to thrive in a shift from transactions (EHRs) to SES. Ultimately, RCM represents the foundation of software-enabled services, especially when the RCM solution revolves around automating and codifying billing and reimbursement via technology on a unified system. Additionally, the risk-based revenue model of RCM is better positioned to compete in a SES environment compared to the traditional installation and maintenance revenue model of EHRs. Finally, due to the analytic and data driven nature of RCM, we believe it provides a strong foundation from which to build an eco-system of SES solutions via internal development, partnership, or acquisition.

Closed/Introverted Systems or Open Application Programming Interfaces (APIs). Another major controversy of healthcare technology revolves around the philosophy associated with the underlying technology. We believe the majority of traditional EHR vendors operate closed / introverted systems consisting of home grown technology solutions. For the most part, these vendors avoid acquiring or partnering with third party innovators for technology solutions. There are other vendors, typically cloud-based, who welcome open collaboration and support an ecosystem of technology innovators through application programming interfaces. We note that most companies can easily develop, maintain, and operate open APIs, but many do a poor job of this in reality. In our view, companies operating with an open and collaborative infrastructure will be best positioned for the shift to performance based technology investment.

We believe our views are illustrated in two ways. First, when most HCIT vendors acquire technology they do not typically re-write the code of the acquired technology or fully integrate it into their core system. In our view, examples include several acquisitions done by Allscripts and most recently Cerner’s acquisition of Siemens Health Services. The second proxy for system openness revolves around interest in collaborating with third party developers. In our view, the most collaborative vendors are athenahealth via More Disruption Please and Allscripts via the Allscripts Developer Program.

The Triple Aim of Worry

Our industry outlook revolves around three questions: (1) can technology bend the national health expenditure cost curve? We think bending the NHE cost curve represents the fundamental presupposition of digital health and HCIT. (2) Will HCIT spend increase or decrease? We believe clients seek low cost, and agile solutions. We believe performance driven solutions will put pricing pressure on non-performance driven solutions. (3) Will tech investment revolve around performance? We believe operating margin pressure, reimbursement pressure, et al., will force clients to make investment decisions according to performance not simply adoption.

Question 1: Can Technology Bend the National Health Expenditure Cost Curve? We believe the answer is yes. In our view, the fundamental presupposition of investing in and developing healthcare IT products and digital healthcare products revolves around driving performance and efficiency throughout the continuum of care. In our view, new technologies should facilitate a more efficient and productive health care complex in the United States. Furthermore, we believe that the ability to bend the cost curve will ultimately determine the success and long-term viability of healthcare IT and digital healthcare. We doubt that the U.S. healthcare complex will continue to increase IT spending if the underlying technology provides no cost reduction, performance improvement, or operational efficiency.

Page 4

Internet & MediaDigital Healthcare April 6, 2015

Question 2: Will HCIT Spending Increase or Decrease in the Future? We believe legacy vendors believe spending will continue to increase because of successful new products and technology e.g., population health management and analytics. While we believe these new offerings will become necessary products to drive success in health care, we believe the inherent success of performance based technology will call into question the pricing of non-performance based technology. In our view, the industry will likely focus on shifting budget dollars away from commoditized technology to invest in technology that provides an outcome or improvement.

Question 3: Will Healthcare Technology Investment Shift Away from Simple Adoption to Performance? We believe performance and revenue pressure stemming from the shifting reimbursement landscape, narrow operating margins, and increasing consumerism will force the health care system to move towards performance based technology investment. Once an industry begins to provide solutions based on cost reductions or performance, clients begin to ponder why all of their technological investments cannot drive cost reductions or performance.

The biopharmaceutical industry represents a major example. As patent cliffs forced the industry to become more efficient, new technologies brought to bear around sales reps caused companies to then question the efficiency of their advertising. We believe a similar trend will develop in HCIT over the next several years. As the success of Outsourced IT / Managed Hosting provides clients a performance based and ROI driven product, the hospital essentially shifts all of its functional IT costs to the outsourced vendor, clients will start to ponder why or how can I get better performance / efficiency from my EHR investment? We believe the successful shift revolving around EHR vendors providing outsourced IT services to clients will come to represent a double-edged sword. On one hand, the ROI driven service will drive significant revenue growth. On the other hand, the ROI driven nature of the service will cause clients to question the value propositions of non-ROI driven services offered by the vendor.

Page 5

Internet & MediaDigital Healthcare April 6, 2015

Part 1: The Current State of Healthcare Digitization

The digitization of the U.S. healthcare system remains a major focal point for the healthcare technology industry. We note that over the past five to seven years adoption of electronic health records (EHRs) has increased substantially. Currently, we believe the industry is entering a phase whereby digital infrastructure investments shift from a transactional focus to a focus on software-enabled services (SES) that facilitate performance improvement and operational efficiencies throughout the care continuum. We are skeptical that the traditional healthcare IT (HCIT) players will lead the shift toward SES. At the same time, we believe SES innovators must focus on developing solutions that truly drive meaningful ROI in order to sustain possible hospital IT budget wallet share gains.

We believe healthcare digitization develops through four stages. The focus of Stage 1 is developing a basic digital infrastructure that moves the clinical back-office (medical records, billing, etc.) from pen and paper to digital. Stage 2 is driven by the development of new digital healthcare technologies that leverage the wireless infrastructure digitizing the clinical front-office (communication with patients, scheduling, monitoring, diagnostics, et al.). The focus of Stage 2 is on

developing digital healthcare solutions that facilitate performance improvement and operational efficiencies throughout the care continuum. In our view, an important aspect of Stage 2 lies in driving consumer adoption and closing the digital healthcare eco-system. We believe without patient buy-in, the digitization of healthcare will likely begin and end with the government mandates driving the digitization of the clinical back-office.

In Stage 3, companies will begin to integrate developments achieved in Stage 1 and Stage 2. At this point, we believe companies will focus on how to close the eco-system in terms of their respective business models. We believe the best positioned companies are those that can help facilitate the development of a software-enabled services (SES) eco-system that can be successfully integrated with the digital foundation to drive performance improvement and operational efficiencies.

Lastly, in Stage 4, constituents will begin to focus on driving meaningful analysis off of the vast data created by a digitized healthcare system. We believe Stage 4 represents the greatest opportunity for the digitization of healthcare, but also represents the least defined opportunity, as we remain in the relatively early innings of healthcare digitization. Additionally, we believe that in Stage 4 the U.S. healthcare system will operate more rationally by favoring the highest quality clinicians and care givers who operate at the lowest cost. We provide an illustration of “The Four Stages of Healthcare Digitization” in Exhibit 1.

Exhibit 1: U.S. Healthcare Digitization Development Cycle

Source: Stifel

The Four Stages of Healthcare DigitizationTechnological

FocusBeneficiaries Investment Area(s)

Stage 1• Digitizing the Clinical Back-Office

Stage 2• Digitizing the Clincial Front-Office

Stage 3• Integration

Stage 4• Monetization

EMRs/EHRsRCMsPBMsCROs

Digital Healthcare

Combines Stage 1 and

Stage 2

Entire Healthcare Supply Chain

CliniciansHospitals

ConsumersClinicians

Closes the Eco-system by

Integrating Stage 1 and Stage 2

Constituents

Focus on Leveraging the Value of

Data

Healthcare IT Companies

Digital Healthcare Companies

In Stage 3, we believe Healthcare IT companies will acquire Digital Healthcare

companies. Additionally, Digital Healthcare companies will become IPO candidates

The Entire Eco-system: Healthcare IT

Digital Healthcare TechnologyManaged Care Organizations (MCO)s

Pharmaceuticals

Page 6

Internet & MediaDigital Healthcare April 6, 2015

In Exhibit 2, we illustrate the current state of digitization across the U.S. healthcare system. According to The Office of the National Coordinator for Health Information Technology (ONC), electronic health record (EHR) adoption is high and has increased substantially since the implementation of incentive payments as part of HITECH / ARRA, which facilitated EHR adoption.

We note that office-based physicians exhibit significant adoption of EHRs. According to ONC, roughly 78% of office-based physicians utilize any EHR system, and 48% utilize a basic EHR system. Additionally, only 53% of primary care physicians utilize an EHR that meets the criteria of a basic EHR system. Hospital adoption of EHRs seems to be stronger than that of office-based physicians. According to ONC, roughly 94% of hospitals use a certified EHR, and roughly 59% of hospitals utilize a basic EHR system. In 2013, roughly 89% of Critical Access Hospitals (CAHs) used an EHR system with roughly 49% of CAHs planning to install or upgrade an EHR system within a year. In 2012, roughly 90% of Federally Qualified Health Centers (FQHCs) adopted an EHR system, and 50% had adopted an EHR with basic capabilities.

While government incentive programs have driven increased adoption, the digital foundation of healthcare remains incomplete. We believe the digital infrastructure of U.S. healthcare is incomplete for several reasons: (1) adoption is close to but not ubiquitous, (2) the current foundation was developed around transactions based on government mandates, rather than true performance improvement and operational efficiency, and (3) ongoing interoperability issues.

Exhibit 2: Hospital and Physician Electronic Health Record (EHR) Adoption

Source: The Office of the National Coordinator for Health Information Technology (ONC) Office of the Secretary, United States Department of Health and Human Services and Stifel

We believe this shift from the transactional systems and solutions of an EHR to the software-enabled services is analogous to the shift from Internet service providers (ISPs) to algorithmic search. When the Internet first developed, Internet service providers represented the main access point to the Internet. The core value proposition of these businesses revolved around simply connecting the user with the Internet; essentially the value of ISPs resided in the ability to facilitate a transaction. We believe the traditional EHR systems are the ISPs of today’s digital healthcare infrastructure. These systems provide a sound transactional foundation, but were not designed for the next generation of solutions, which use technology, data, and analytics to drive performance improvements and operational efficiencies in the hospital.

Currently, we see the advent and development of several SES verticals as analogous to the Internet Portal era. Internet portals facilitated data aggregation and compilation of important data in a central place and facilitated a customized or personalized experience. We believe population health management and

11% 12%

17%

22%

28%34%

40%

48%

18% 17% 17%21%

24%29%

35%

42%48%

51%

57%

72%78%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Office-Based Physicians

Any EHR System Basic System

9% 12%16%

28%

44%

59%

72%

85%

94%

2008 2009 2010 2011 2012 2013

Non-Federal Acute Care Hospitals

Basic System Certified EHR

Page 7

Internet & MediaDigital Healthcare April 6, 2015

precision medicine are good examples within digital healthcare. Ultimately, the digitization of healthcare seeks to move toward algorithmic search.

We note that algorithmic search seemingly unified the Internet, making information capture a somewhat frictionless process. The value lies in delivering the right information at the right time to the right user. In our view, the algorithmic search environment represents the Holy Grail for the digitization of healthcare. Healthcare’s version of algorithmic search revolves around an integrated eco-system of SES providers who can deliver the right care at the right cost to the right person. More importantly, the system utilizes these technology systems to ensure patients are directed to the highest quality care givers operating at the lowest price. We illustrate the ISP to algorithmic search transition in Exhibit 3.

Exhibit 3: Electronic Health Records (EHRs) and the Shift to Algorithmic Search

Source: Stifel

In our view, the shift toward software-enabled services provides an opportunity for innovators to focus on specific tasks that unbundle, yet optimize the EHR. We believe that traditional HCIT vendors seek to provide platforms that provide all services possible. A major problem with this view lies in the slow pace of innovation and closed / introverted systems offered by traditional HCIT vendors. Many of these solutions are primarily focused on developing software solutions that digitize transactions in order to help facilitate Meaningful Use attestation.

While we recognize hospitals seem to prefer a single vendor for healthcare technology infrastructure, we believe the view stems from the high cost of infrastructure and need for information fidelity, rather than true technological advantage. Based on industry discussions, we note that within the past six months hospitals have been more interested in working with smaller innovators than say 18 months ago.

We believe hospitals will increasingly look to work with innovators that can provide services that can optimize the core EHR investment. These SES offerings will focus on unbundling the EHR, by developing best-in-breed solutions around a single friction point. The key in maximizing the long-term value of the opportunity will lie in SES innovators developing solutions that produce meaningful ROI through performance improvement and operational efficiencies. We believe that if hospital IT budgets are going to continually increase, the majority of the increased spend will be allocated to SES solutions versus building and maintaining the core EHR infrastructure.

What The Development of Algorithmic Search Means for EHRs

Value Lies in Connecting to

Information

Internet Service Provider

Value Lies in Data Aggregation in a Central Location

Customized Experience

Value Lies in Delivery of Right Info, At Right Time, To Right Spot Configurable Experience

Algorithmic SearchInternet Portals

Move Away From Transactional Value to Software Enabled Services That Drive Value and Optimize

EHRs Today:Value Lies in Transactions

Population Health Management Precision Medicine Will EHR Be Able to Facilitate?

Development of a Healthcare Internet Ability To Drive Care to Best Quality at Lowest Price

Page 8

Internet & MediaDigital Healthcare April 6, 2015

In Exhibit 4, we provide an illustration of what the unbundling of the EHR might look like. The illustration identifies the key areas of the EHR that can be optimized by third party innovators. We believe the inherent functions of an EHR or digitized health system fall into two categories: transactions and value-add software-enabled services. In our view, traditional EHR vendors currently dominate and will dominate the transactions inherent in the EHR, which we believe are commodity. These transactions certainly improve the quality of care and workflow, but often times these improvements are not apparent financially. The value-added services portion of an EHR not only improves the quality of care and workflow, but also has an ability to impact the bottom line. We believe the unbundling of the EHR will result in the development of numerous niche vendors, which compete to provide the best solution focused on a particular value-added service area. Importantly, we do not believe EHR vendors possess a first move advantage. We believe the unbundling and creation of SES offerings benefits smaller, nimble innovators who can focus on developing solutions that remove key friction points and at the same time impact the bottom line of a hospital or health system.

Exhibit 4: The Unbundling of the Electronic Health Record (EHR)

Source: Jonathan Govette, CEO of Referral MD and Stifel

We believe the unbundling of the EHR coupled with the reform environment will help give rise to new provider business models. We illustrate several evolving provider business models in Exhibit 5. New provider models are aimed at driving quality improvement and system efficiency. These new models range from treating patients prior to getting sick to tearing down the traditional four walls of the clinic to driving greater specialization around chronic care.

We believe several of these new provider models will require technology solutions that can drive performance improvement and operational efficiency where it may be lacking currently. In our view, hospitals will increasingly seek to invest in these evolving business models in order to supplement and offset declining revenues. We believe that several of these evolving care models revolve around software-enabled services (SES), especially telehealth, medical home, and mobile and home care.

In our view, the EHR system that can successfully integrate technology services associated with these evolving business models will be well-positioned for the years to come. Currently, we believe that the traditional EHR vendors will face challenges in trying to both develop solutions around these evolving models, as well as face challenges in terms of integrating third party solutions into their core EHR system.

Unbundling the Electronic Medical Record (EHR) Through Software Enabled Services (SES)

CaredoxPersonal Health

Tracker

ZocDocOnline Patient

Appointments

PatientPayBilling

EligibleInsurance API

Castlight HealthPricing Transparency

Filament LabsPatient Engagement

GrandRoundsSecond Opinion

Services

visiblehealthPatient Education

referral MDPatient Referrals

Precision MedicineSyapse

Zapp RxPrescription

Management

surescriptsPrescription Filling

evolent healthPopulation Health

Management

TeladocTelehealth /

Telemedicine

Page 9

Internet & MediaDigital Healthcare April 6, 2015

Exhibit 5: Examples of Evolving Provider Business Models

Source: IBM Global Business Services, IBM Institute for Business Value, and Stifel

Our 2015 Outlook and Investment Scenarios

As we enter 2015, we believe there are several possible investment scenarios that may unfold throughout the year. These scenarios range from being positive on select companies to being negative on the entire industry.

We believe there are five macro drivers of our 2015 HCIT investment scenarios, including: underlying proprietary technological advantages, the shift from transactional infrastructure driven technology investment to performance driven technology investment, the inertia associated with backlog, digital biomarkers, small, nimble third-parties leading innovation, and the interest rate environment.

Understanding the Difference Between SaaS and HCIT SaaS. We think healthcare investors may think of SaaS models somewhat differently from traditional technology investors. In our view, there are several characteristics of a strong SaaS investment, including: strong, sustainable revenue growth over the long-term, driven by a significant proprietary technological advantage, and characterized by high renewal rates, and high revenue visibility. Based on our discussions, we believe high renewal rates and high revenue visibility may represent the key drivers of a SaaS premium in healthcare technology. We justify a SaaS premium in digital healthcare by focusing on how the underlying proprietary technological advantages drive strong, sustainable long-term revenue growth. The ability to drive high renewal rates, high visibility, and improving margins provide additional support for the premium. We believe the best example of the HCIT SaaS valuation phenomenon revolves around companies operating businesses primarily levered to government mandates rather than underlying performance, (i.e., ROI).

Wellness / Prevention Acute Care Chronic Care

Wellness Centers

Retail Clinics

Complimentary Medicine

Concierge Medicine

Medical Home

Telehealth, Telemedicine, e-Visits

Medical Tourism

Ambulatory Surgery Centers

Centers of Excellence

Specialty Hospitals

Mobile and Home Care

Page 10

Internet & MediaDigital Healthcare April 6, 2015

We Think 2015 Will Be About the Shift from Technology Investment to Performance-Based Technology Investment. In our view, a major theme facing healthcare remains developing tools and solutions that can help extract costs and drive long-term sustainable cost reductions throughout the care continuum. For the past five to 10 years, the majority of technology investment seems to have revolved around implementing infrastructure. In our view, the next five to 10 years will revolve around optimizing the technology infrastructure now in place. We believe the major change between these eras will be a shift away from need based infrastructure technology investment towards performance and value driven technology investment. We see this shift manifesting itself via the unbundling of the EHR, which essentially separates the functions of the EHR or digital healthcare infrastructure into commoditized transactional services or value-added software-enabled services.

The Drivers of Inertia Will Help Digital Healthcare Innovators. We believe the main driver of inertia among traditional HCIT companies revolves around large backlogs. In our view, investors love these backlogs because they provide visibility into the future. However, backlog also removes an impetus for traditional HCIT companies to truly lead the industry in terms of innovation. As the industry shifts from transactional infrastructure technology investment to performance-driven technology investment, we believe an unbundling of the EHR will occur. In our view, the traditional HCIT vendors are mostly focused on the commodity transactional functions of the EHR. We believe these entities have unwittingly ceded the performance, value-add service functions to third-party innovators.

Could 2015 Represent the Year of the Digital Biomarker? Based on our meetings and recent news flow, we believe mHealth devices are poised to unlock value in the clinic. We believe that biosensor and even diagnostic companies realize the inherent value of the data generated and collected by their devices. Biosensor companies such as iRhythm recognize the value of the data sets generated by the use of its ZIO device. Furthermore, we believe recent collaborations between Novartis and Qualcomm Life illustrate the interest major biopharmaceutical companies have in mHealth. In December 2014, Biogen gave away fitness tracking devices to 250 MS sufferers in order to evaluate how the biometric device may provide additional insight into adherence and medication impact. Lastly, we think the approval of Dexcom Share provides proof of concept and validates the value of the digital biomarker. We believe successful development around the digital biomarker could come to represent a more robust data set for population health management compared to the data contained in EHR systems today. We do not believe the traditional EHR vendors are prepared to truly integrate a plethora of mHealth devices. Our view is rooted in their closed / introverted natures, as well as the fact that vendors like Epic have struggled with the early development of their apps / tools for Apple’s Health Kit.

We Believe Innovation Comes from Outside the Core HCIT EHR Vendors. A major theme of digital healthcare revolves around the fact that small, nimble third-parties are driving innovation rather than traditional HCIT vendors. We believe small, nimble innovators focus on developing solutions to major friction points rather than specific government mandates. For example, we believe the Dexcom Share tool represents the natural innovation of a product focused on removing major friction points from a process or experience. We believe a focus on removing major friction points from a process or experience in healthcare represents a key differentiator between digital health innovators and traditional HCIT companies. Ultimately, we think the Dexcom Share approval illustrates how friction points in healthcare technology may be solved inadvertently in other parts of biotech, healthcare, and med tech. Based on our discussions, we believe technologists such as Apple and Google will likely represent the facilitators of innovation rather than enterprise EHR vendors.

Page 11

Internet & MediaDigital Healthcare April 6, 2015

The Importance of the Interest Rate Environment to HCIT Companies. We believe the low interest rate environment represents a main driver of investor interest in both CPSI (Hold, $53.33) and Quality Systems (QSII, $15.85, Not Covered). The dividend yields associated with these companies are 4.8% and 4.4%, respectively. In our view, these dividend yields may be attractive to investors especially compared to current rates on U.S. Government bonds. While we view the dividend payments negatively, we believe investors may be attracted to these names until their dividend payments deteriorate, or debt yields become more attractive.

Given the five macro drivers of our 2015 outlook, we provide our thoughts on five investment scenarios, below.

Scenario 1: Bullish on athenahealth and SES, but neutral on traditional HCIT

We subscriber to scenario one, as we believe athenahealth represents the best positioned healthcare IT company to benefit from the shift to software-enabled services. Based on our industry discussions, only athenahealth (ATHN, Buy, $117.65)seems to be eschewing a closed / introverted system. Through the More Disruption Please program, the company continues to build and support the development of an eco-system of software-enabled services that provide performance improvement and operational efficiencies throughout the care continuum.

Furthermore, we believe athenaNet continues to represent a key proprietary technological advantage. The fact that athenahealth’s foundation revolves around the digitization of revenue cycle management positions the company well to drive a SES eco-system and help clients tackle increasingly more complex payment constructs.

In this scenario, we believe investors should also familiarize themselves with public and private companies operating within the Fab 5 of digital healthcare verticals: cost transparency, telehealth, second opinion services, analytics (population health management and precision medicine), and patient engagement.

We are bullish on SES because we believe that hospitals will increasingly look to shift spending towards technology solutions that improve the bottom line. In our view, hospitals currently prefer to work with a single technology vendor due to costs and information fidelity, rather than a true technological advantage. We believe that as SES vendors prove their ability to drive meaningful ROI that these entities will be able to gain greater wallet share of hospital IT spend.

Scenario 2: Bullish on Cerner, but neutral on athenahealth, SES, and the rest of traditional HCIT

In scenario two, investors remain focused on Cerner (CERN, Hold, $72.77) due to its competitive position within the acute care market, and its historical stability. Investors believe the status quo will remain intact for Cerner for several years to come, and that the company is not likely susceptible to uncertainties stemming from healthcare reform and new payment models. Investors in scenario two are likely negative on athenahealth due to valuation and a belief that the company will be unable to easily gain traction in the hospital market. Investors in this scenario may also be negative on SES because they likely believe that hospitals will seek to work with only one vendor rather than many.

Page 12

Internet & MediaDigital Healthcare April 6, 2015

Scenario 3: Bullish on Value/Turnarounds, e.g., Allscripts, Quality Systems, CPSI, but neutral on the rest of HCIT

Investors in scenario three prefer the turnarounds and value players to the market leaders. These investors are likely disinterested in market leaders due to valuation and seek to time the bottom in turn arounds like Allscripts (MDRX, Hold, $11.77) and Quality Systems. These investors are also likely attracted to the dividend payments provided by Quality Systems and CPSI. We are not advocates of this scenario, as we believe technology turnarounds can prove quite difficult, especially when the competitive set may exhibit technological advantages and a greater pace of innovation.

Scenario 4: Bullish on athenahealth and Cerner, but neutral on the rest of HCIT

Investors in scenario four primarily focus on the market leaders and exhibit a neutral to negative stance towards other HCIT players. These investors prefer the historical stability and market leading position of Cerner in the acute market. Additionally, these investors prefer the strong revenue growth rates exhibited by athenahealth. These investors believe that Cerner will be able to maintain its market dominance and face little negative impact from changes stemming from healthcare reform. Additionally, these investors likely believe that athenahealth can continue to meet a 20% year over year revenue growth target for the next few years.

Scenario 5: Bearish on all of HCIT

We believe some investors may be negatively inclined regarding the entire HCIT industry group. These investors view population health management as a compelling opportunity not yet ready for prime time. Additionally, the bearish view holds that revenue growth will likely be difficult in an industry with little to no greenfield opportunity. The replacement super-cycle will likely take longer than expected to develop, and when it does the replacement super-cycle will be characterized by very long replacement cycle times. Additionally, those vendors who have been experiencing client attrition likely continue to do so, (e.g., Quality Systems and Allscripts).

Page 13

Internet & MediaDigital Healthcare April 6, 2015

Part 2: The Shift to Software-Enabled Services (SES)

What Are SES and Why Are They Important?

Software-enabled services are solutions that provide performance improvement and operational efficiencies throughout the care continuum. These solutions are delivered via software and revolve around a proprietary technological advantage, and characterized by delivering meaningful ROI. SES solutions address a myriad of issues facing hospitals and providers ranging from revenue cycle to utilization and volumes to patient engagement among others. In our view, the environment of health reform and significant infrastructure investment will lead many hospitals and providers to seek ways to optimize their organizations. We believe that over time, hospitals and physicians will seek to shift their HCIT investment dollar towards data and outcomes driven services that drive performance improvement and operational efficiencies throughout the care continuum.

Electronic Health Records (EHRs) represent the digital foundation for a digitized healthcare system in the United States. These systems are often incomplete in that users only need to perform a subset of functions outlined within government adoption mandates. Furthermore, these systems are plagued by inter and intraoperability issues and often represent close / introverted systems (meaning they avoid working with third party technologists). While we recognize that Epic and Cerner represent the standard in terms of EHRs, we do not believe these EHR vendors will necessarily become the leaders in SES. For the most part, these entities while offering some SES offerings (population health and revenue cycle) are primarily focused on increasing and expanding the footprint of their EHR system user base.

In the future, we believe hospitals and providers will increasingly look for ways to extract value and performance from their HCIT investments. In our view, best-in-breed SES offerings can develop and thrive regardless of who represents the standard in EHRs. We believe SES offerings thrive no matter what because they are services that would exist regardless of whether or not government driven HCIT adoption mandates existed. The common thread of data and outcomes driven solutions that provide meaningful ROI through performance improvement and operational efficiency drives SES independence. In our view, as the health reform environment strives for greater cost reduction and moves toward increasingly complex reimbursement structures, we believe SES will play an integral role in hospitals and physicians maintaining the long-term viability of their businesses.

We believe the movement from transactional infrastructure investment to SES offerings evolves in three parts. First, the hospital and physician decides the organization needs to move beyond the digital foundation to be successful. The decision may manifest itself in the organization striving for EHR optimization or seeking to defend against operating margin degradation. Secondly, the organization actively decides that technology investments need to provide meaningful ROI. Lastly, organizations make an active shift to leveraging SES offerings because they realize they need to employ solutions that actually do what the organization needs / wants to remain successful.

Page 14

Internet & MediaDigital Healthcare April 6, 2015

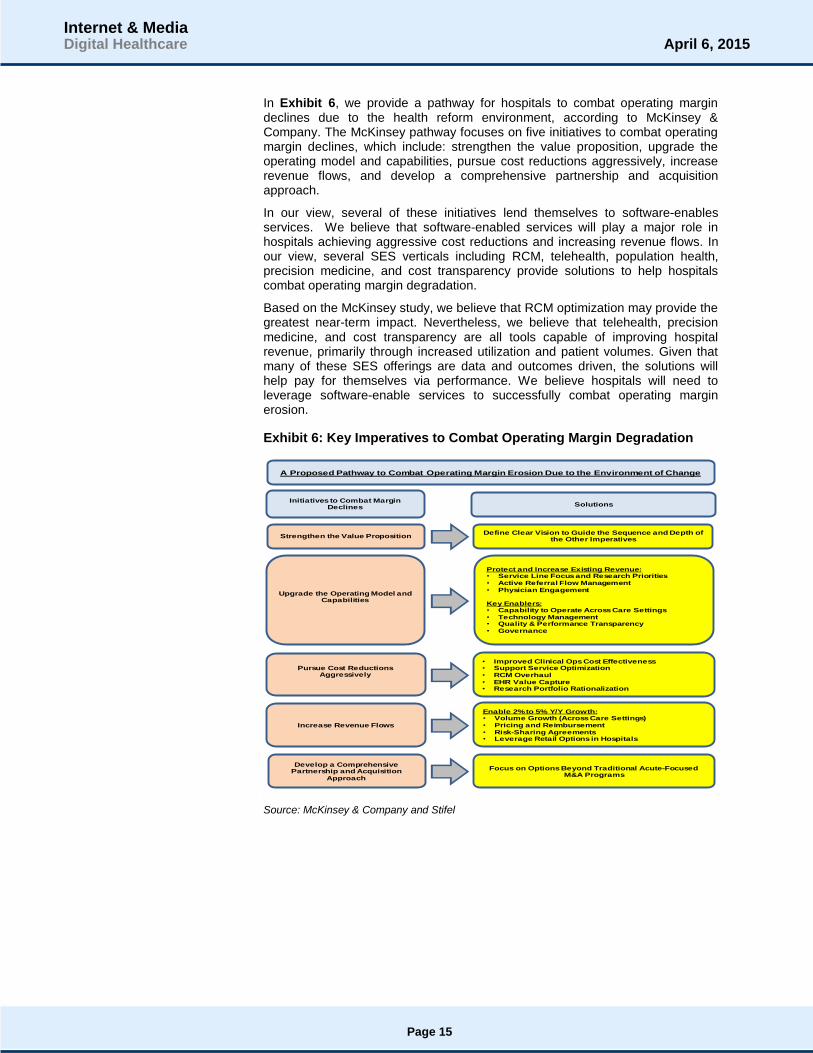

In Exhibit 6, we provide a pathway for hospitals to combat operating margin declines due to the health reform environment, according to McKinsey & Company. The McKinsey pathway focuses on five initiatives to combat operating margin declines, which include: strengthen the value proposition, upgrade the operating model and capabilities, pursue cost reductions aggressively, increase revenue flows, and develop a comprehensive partnership and acquisition approach.

In our view, several of these initiatives lend themselves to software-enables services. We believe that software-enabled services will play a major role in hospitals achieving aggressive cost reductions and increasing revenue flows. In our view, several SES verticals including RCM, telehealth, population health, precision medicine, and cost transparency provide solutions to help hospitals combat operating margin degradation.

Based on the McKinsey study, we believe that RCM optimization may provide the greatest near-term impact. Nevertheless, we believe that telehealth, precision medicine, and cost transparency are all tools capable of improving hospital revenue, primarily through increased utilization and patient volumes. Given that many of these SES offerings are data and outcomes driven, the solutions will help pay for themselves via performance. We believe hospitals will need to leverage software-enable services to successfully combat operating margin erosion.

Exhibit 6: Key Imperatives to Combat Operating Margin Degradation

Source: McKinsey & Company and Stifel

Strengthen the Value Proposition

Upgrade the Operating Model and Capabilities

Pursue Cost Reductions Aggressively

Increase Revenue Flows

Develop a Comprehensive Partnership and Acquisition

Approach

Initiatives to Combat Margin Declines Solutions

Define Clear Vision to Guide the Sequence and Depth of the Other Imperatives

Protect and Increase Existing Revenue:• Service Line Focus and Research Priorities• Active Referral Flow Management• Physician Engagement

Key Enablers:• Capability to Operate Across Care Settings• Technology Management• Quality & Performance Transparency• Governance

• Improved Clinical Ops Cost Effectiveness• Support Service Optimization• RCM Overhaul• EHR Value Capture• Research Portfolio Rationalization

Enable 2% to 5% Y/Y Growth:• Volume Growth (Across Care Settings)• Pricing and Reimbursement• Risk-Sharing Agreements• Leverage Retail Options in Hospitals

Focus on Options Beyond Traditional Acute-FocusedM&A Programs

A Proposed Pathway to Combat Operating Margin Erosion Due to the Environment of Change

Page 15

Internet & MediaDigital Healthcare April 6, 2015

According to a 2013 McKinsey & Company report titled “The ‘Big Data’ Revolution in Healthcare: Accelerating Value and Innovation,” the application of early successes in big data applied to healthcare at scale could drive an annual cost savings between $300 billion and $450 billion, Exhibit 7. We believe these estimates are achievable based on the verticals identified in Exhibit 7. In our view, the value cost savings derived from the categories will increase as the big data and analytics solutions being developed become increasingly more sophisticated. For example, health tracking starts simply with devices such as activity trackers, but becomes more sophisticated once adherence programs are included. Essentially, the $300 billion to $450 billion in possible savings will either increase or decrease as a function of the data-driven performance improvements and operational efficiencies provided by SES innovators. In our view, the digital foundation of EHRs cannot achieve these cost reductions alone.

Exhibit 7: Impact of Analytics & Big Data on National Health Expenditures

Source: American Diabetes Association, American Hospital Association, HealthPartners Research Foundation, McKinsey Global Institute, National Bureau of Economic Research (NBER), U.S. Census Bureau, and Stifel

In Exhibit 8, we estimate what the total addressable revenue opportunity associated with McKinsey’s cost savings estimates driven by analytics and big data. We apply a 5% to 10% take-rate to estimate the possible revenue opportunity for each vertical identified by the McKinsey report. We believe that these estimates likely prove conservative, as the verticals represent broad categories. In our view, there are several SES verticals that currently represent addressable markets of several billion dollars and growing.

Exhibit 8: Market Opportunity by Vertical Driven by Analytics & Big Data

Source: Stifel

$70

$90

$50 $50

$40

$-

$20

$40

$60

$80

$100

$120

HealthTracking

CoordinatedCare

Best Provider AccountableCare

DigitalHealthcare

Es

tim

ate

d S

avin

gs ($b

illion

s)

Estimated Cost Savings: Low Estimate

$100

$110

$70

$100

$70

$-

$20

$40

$60

$80

$100

$120

HealthTracking

CoordinatedCare

Best Provider AccountableCare

DigitalHealthcare

Es

tim

ate

d S

avin

gs ($b

illion

s)

Estimated Cost Savings: High Estimate

Total Estimated Costs Savings (Low Estimate) = $300 Billion

Total Estimated Costs Savings (High Estimate) = $450 Billion

$5.0 $5.5

$3.5

$5.0

$3.5

$10.0

$11.0

$7.0

$10.0

$7.0

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

HealthTracking

CoordinatedCare

Best Provider AccountableCare

DigitalHealthcare

Low TAM High TAM

$3.5

$4.5

$2.5 $2.5 $2.0

$7.0

$9.0

$5.0 $5.0

$4.0

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

$10.0

HealthTracking

CoordinatedCare

Best Provider AccountableCare

DigitalHealthcare

Low TAM High TAM

TAM Estimates Based on $300 Billion Cost Savings

TAM Estimates Based on $450 Billion Cost Savings

Page 16

Internet & MediaDigital Healthcare April 6, 2015

We highlight what we believe to be the total addressable market opportunity for several SES verticals in Exhibit 9. Revenue cycle management (RCM) represents a $50 billion opportunity according to estimates from Accretive Health, athenahealth, and Quality Systems. The RCM opportunity can be split into two markets: ambulatory and acute. We note that Teladoc estimates its telehealth total addressable market to be between $12 billion and $15 billion. We note that the opportunity for telehealth may be greater when one considers additional telehealth / telemedicine models (e.g., American Well and MDLive). We break the analytics vertical into population health management and precision medicine. In our illustration below, we value the population health management opportunity at $9 billion, but recognize that industry sources estimate the opportunity could increase to $40 billion to $50 billion over the next several years. In terms of precision medicine, we estimate the total addressable market at $7.0 billion based on SEC filings from Foundation Medicine; we believe the market opportunity is likely much higher. Our $1.0 billion estimate for patient engagement focuses on patient portals. In our view, the patient engagement addressable market opportunity could be $20 billion or greater when consumer wearables and other products / services are included.

Exhibit 9: Software-Enabled Services (SES) Addressable Market Opportunity for Select SES Verticals

Source: athenahealth, Best Doctors, Castlight Health, Foundation Medicine, Frost & Sullivan, Markets2Markets, Quality Systems, Teladoc, and Stifel

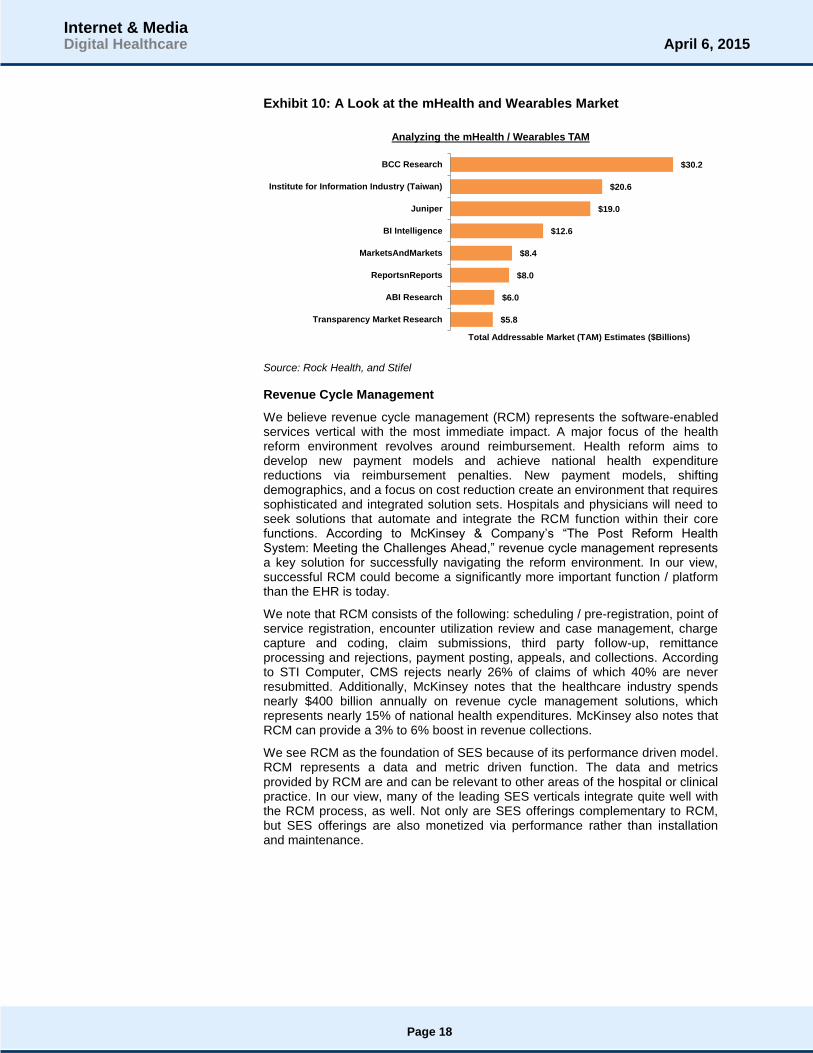

In Exhibit 10, we illustrate the size of the mHealth and wearables market based on several different estimates developed between January 2013 and the present. The TAM estimates below provide a glimpse into what the mHealth and wearables opportunity may be in 2018E. We note that the largest estimates represent the most recent estimates. In our view, the mHealth and wearables market may become an important part of the patient engagement opportunity and ecosystem over time.

$36.0

$15.0 $14.0

$9.0 $7.0

$6.0 $6.0

$1.0

RCMAmbulatory

Telehealth RCM Acute PopulationHealth Mgmt.

PrecisionMedicine

CostTransparency

SecondOpinions

PatientEngagement

Select SES Vertical Total Addressable Market Opportunities

Page 17

Internet & MediaDigital Healthcare April 6, 2015

Exhibit 10: A Look at the mHealth and Wearables Market

Source: Rock Health, and Stifel

Revenue Cycle Management

We believe revenue cycle management (RCM) represents the software-enabled services vertical with the most immediate impact. A major focus of the health reform environment revolves around reimbursement. Health reform aims to develop new payment models and achieve national health expenditure reductions via reimbursement penalties. New payment models, shifting demographics, and a focus on cost reduction create an environment that requires sophisticated and integrated solution sets. Hospitals and physicians will need to seek solutions that automate and integrate the RCM function within their core functions. According to McKinsey & Company’s “The Post Reform Health System: Meeting the Challenges Ahead,” revenue cycle management represents a key solution for successfully navigating the reform environment. In our view, successful RCM could become a significantly more important function / platform than the EHR is today.

We note that RCM consists of the following: scheduling / pre-registration, point of service registration, encounter utilization review and case management, charge capture and coding, claim submissions, third party follow-up, remittance processing and rejections, payment posting, appeals, and collections. According to STI Computer, CMS rejects nearly 26% of claims of which 40% are never resubmitted. Additionally, McKinsey notes that the healthcare industry spends nearly $400 billion annually on revenue cycle management solutions, which represents nearly 15% of national health expenditures. McKinsey also notes that RCM can provide a 3% to 6% boost in revenue collections.

We see RCM as the foundation of SES because of its performance driven model. RCM represents a data and metric driven function. The data and metrics provided by RCM are and can be relevant to other areas of the hospital or clinical practice. In our view, many of the leading SES verticals integrate quite well with the RCM process, as well. Not only are SES offerings complementary to RCM, but SES offerings are also monetized via performance rather than installation and maintenance.

$5.8

$6.0

$8.0

$8.4

$12.6

$19.0

$20.6

$30.2

Transparency Market Research

ABI Research

ReportsnReports

MarketsAndMarkets

BI Intelligence

Juniper

Institute for Information Industry (Taiwan)

BCC Research

Total Addressable Market (TAM) Estimates ($Billions)

Analyzing the mHealth / Wearables TAM

Page 18

Internet & MediaDigital Healthcare April 6, 2015

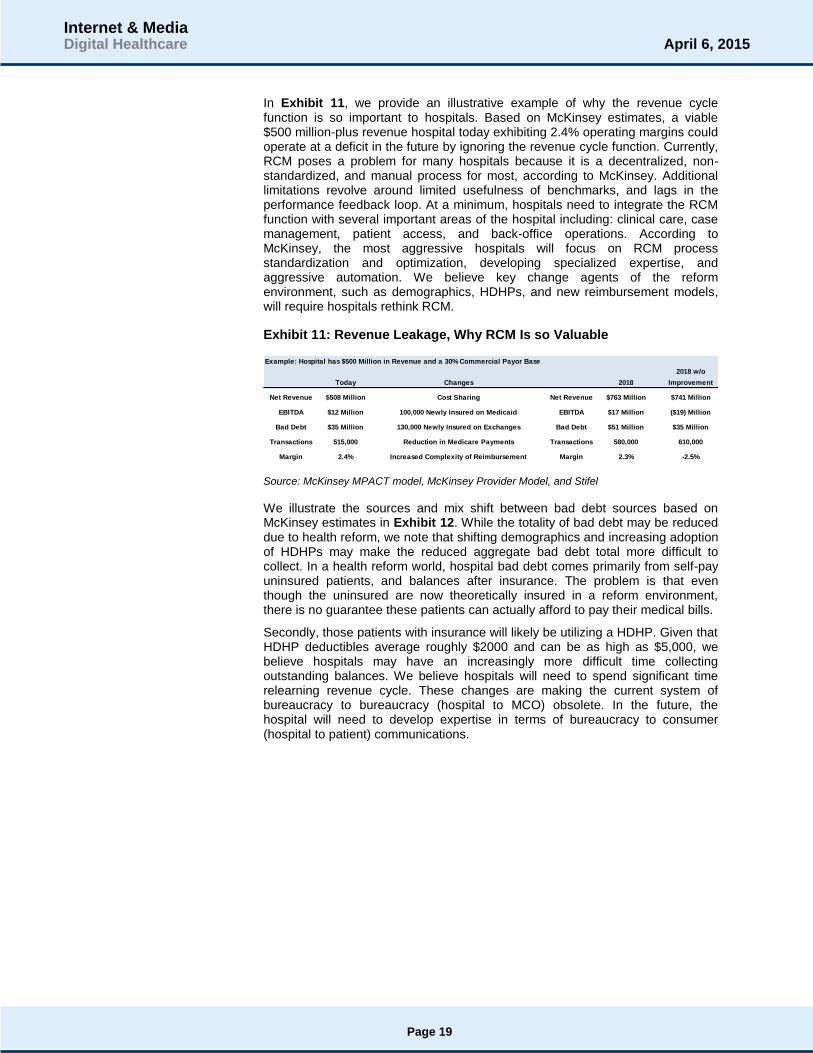

In Exhibit 11, we provide an illustrative example of why the revenue cycle function is so important to hospitals. Based on McKinsey estimates, a viable $500 million-plus revenue hospital today exhibiting 2.4% operating margins could operate at a deficit in the future by ignoring the revenue cycle function. Currently, RCM poses a problem for many hospitals because it is a decentralized, non-standardized, and manual process for most, according to McKinsey. Additional limitations revolve around limited usefulness of benchmarks, and lags in the performance feedback loop. At a minimum, hospitals need to integrate the RCM function with several important areas of the hospital including: clinical care, case management, patient access, and back-office operations. According to McKinsey, the most aggressive hospitals will focus on RCM process standardization and optimization, developing specialized expertise, and aggressive automation. We believe key change agents of the reform environment, such as demographics, HDHPs, and new reimbursement models, will require hospitals rethink RCM.

Exhibit 11: Revenue Leakage, Why RCM Is so Valuable

Source: McKinsey MPACT model, McKinsey Provider Model, and Stifel

We illustrate the sources and mix shift between bad debt sources based on McKinsey estimates in Exhibit 12. While the totality of bad debt may be reduced due to health reform, we note that shifting demographics and increasing adoption of HDHPs may make the reduced aggregate bad debt total more difficult to collect. In a health reform world, hospital bad debt comes primarily from self-pay uninsured patients, and balances after insurance. The problem is that even though the uninsured are now theoretically insured in a reform environment, there is no guarantee these patients can actually afford to pay their medical bills.

Secondly, those patients with insurance will likely be utilizing a HDHP. Given that HDHP deductibles average roughly $2000 and can be as high as $5,000, we believe hospitals may have an increasingly more difficult time collecting outstanding balances. We believe hospitals will need to spend significant time relearning revenue cycle. These changes are making the current system of bureaucracy to bureaucracy (hospital to MCO) obsolete. In the future, the hospital will need to develop expertise in terms of bureaucracy to consumer (hospital to patient) communications.

Example: Hospital has $500 Million in Revenue and a 30% Commercial Payor Base

2018 w/o

Today Changes 2018 Improvement

Net Revenue $508 Million Cost Sharing Net Revenue $763 Million $741 Million

EBITDA $12 Million 100,000 Newly Insured on Medicaid EBITDA $17 Million ($19) Million

Bad Debt $35 Million 130,000 Newly Insured on Exchanges Bad Debt $51 Million $35 Million

Transactions 515,000 Reduction in Medicare Payments Transactions 580,000 610,000

Margin 2.4% Increased Complexity of Reimbursement Margin 2.3% -2.5%

Page 19

Internet & MediaDigital Healthcare April 6, 2015

Exhibit 12: Sources of Bad Debt at U.S. Hospitals

Note: Self-pay is post discount for uninsured. All figures account for increased use of HDHPs (based on historical trends) and increased cost sharing for commercial plans in light of reform.

BAI stands for balance after insurance; HDHP stands for high deductible health plan.

Source: McKinsey MPACT and provider models; literature search; McKinsey Analysis, and Stifel

Not only is it a demographic and HDHP mix shift, but also an increase in volumes and complexity that makes RCM so important. In Exhibit 13, we provide an illustration of increasing payment volumes and the increasing sources of payment driven by health reform, according to McKinsey. With transaction volumes increasing, integrated and automated RCM systems that can prevent errors will become increasingly important.

BAI 5.4 8.8 14

2010 2018 (No Reform) 2018 (with Reform)

Non-Self-Pay 32%-33% 32% to 34% 53% to 55%

BAI 15% 15% to 17% 35%

Payor Dispute 17% to 18% 17% 18% to 20%

Self-pay 67% to 68% 66% to 68% 45% to 47%

$23.7 - $24.6

$33.6 - $35.9

$17.7 - $8.2

$6.2 - $6.3

$8.7 - $9.1

$7.2 - $8.0

$5.2 - $5.4

$8.2 - $8.8

$13.6 - $13.9

2010 2018 (No Reform) 2018 (with Reform)

Sources of U.S. Hospital Bad Debt (Billions, USD)

Self-pay/Uninsured Payor Dispute BAI

Page 20

Internet & MediaDigital Healthcare April 6, 2015

Exhibit 13: Hospital Payment Mix Shift Requires More Efficient RCM

Note: Includes both HDHP and traditional commercial plans; accounts for increasing use of HDHPs (based on historical trends) and increased cost sharing for commercial plans in light of reform.

BAI stands for balance after insurance; HDHP stands for high deductible health plan.

Source: McKinsey MPACT and provider models, literature search, McKinsey Analysis, and Stifel.

The “Fab 5” Software-Enabled Service Verticals of Digital Healthcare

We define the “Fab 5” of digital healthcare as the software-enabled service verticals, which reflect greatest investor interest and strongest fundamental performance. The verticals that comprise our “Fab 5” include: cost transparency, telehealth / telemedicine, second opinion services, analytics (population health management and precision medicine), and patient engagement.

Cost Transparency: We believe cost transparency solutions help both employers and consumers better manage and understand healthcare costs. These platforms provide dashboards and services for employers who wish to better understand and control the healthcare expenditures of their employee base. These tools allow Human Resources to then make decisions and implement policies, which can help to lower health expenditures for the organization.

Consumers benefit from cost transparency from a shopping for care perspective. Utilizing cost and quality data allows consumers to avoid over paying for routine healthcare and procedures. An extension of cost transparency revolves around platforms providing cost, quality, and provider locator services to consumers. These services utilize user-generated content to help identify the highest quality providers, and utilize carrier data to highlight cost information associated with the provider, clinic, or hospital in question.

Representative examples of Cost Transparency include: Platforms such as Castlight Health, Change Healthcare (acquired by Emdeon) ,and Healthx.

Representative examples of Cost, Quality, and Provider Locator Services include: Doximity, Vitals, and ZocDoc

101.5 102.557.0

0.0 0.060.0

55.5 68.572.5

78.083.0

102.5

101.5101.5

57.00.0

0.060.0

55.568.5

72.578.0

83.0

102.5

31.5

37.0

19.5

2010 2018 (No Reform) 2018 (with Reform)

Hospital Payment Volume Mix Is Changing

Self-Pay / Uninsured

Medicaid BAI

Medicare BAI

Exchange BAI

Commercial BAI

Medicaid

Medicare

Exchange

Commercial

Page 21

Internet & MediaDigital Healthcare April 6, 2015

Telehealth / Telemedicine: We believe telehealth / telemedicine solutions seek to tear down the four walls of the clinic. These solutions help to reduce the burden and cost of in-person visits, expand physician activity, and expand the knowledge networks in both acute and ambulatory care settings. We note that hospitals such as Thomas Jefferson University Hospital in Philadelphia view telehealth as a major tool for keeping patients out of the hospital. A major shift in reducing healthcare costs revolves around keeping patients away from the hospital. We believe telehealth represents a powerful tool because of its strong ROI and ability to help maintain utilization.

Representative examples of Telehealth / Telemedicine include: AmericanWell, Doctors On Demand, MDLive, Ringadoc, and Teladoc.

Second Opinion Services: The second opinion services vertical aims to ensure patients receive the right treatment in order to avoid unnecessary or suboptimal medical procedures. Additionally, second opinion services vendors seek to use analytics to better understand and risk-stratify healthy patients today in order to keep them from becoming chronic health cases.

Representative examples of Second Opinion Services include: Best Doctors and GrandRounds.

Analytics (Big Data – Population Health Management and Precision Medicine): We believe a major focus of the healthcare complex will revolve around the development of strong data architecture. Currently, the digital foundation of the U.S. healthcare system provides solid transactional data, but lacks robust outcomes data. For the most part, healthcare technologists are focused on bringing analytics to bear in terms of population health management. Based on our industry discussions, a need exists around collecting more outcomes based data. The collection of outcomes data will allow for strong and accurate predictive analytics. Meanwhile, the question is can healthcare develop prescriptive or suggestive analytics models?

While population health remains the primary analytic focus of healthcare IT, we believe diagnostic companies focused on precision medicine are developing prescriptive and suggestive analytics tools. A major focus of precision medicine revolves around using diagnostics and the mapping of the human genome to help oncologists identify the best course of treatment for the patient. Platforms such as Syapse allow oncologists to understand the tumor genome sequence, a data input from vendors such as Foundation Medicine (FMI, $48.74, Not Covered) among others, in conjunction with the patient’s clinical and treatment history. Doing so allows the oncologist to make more educated decisions about care going forward.

Representative examples of Population Health Management solutions include: The Advisory Board, Allscripts, athenahealth, Cerner, Evolent Health, Health Catalyst, Lumeris, Phytel, and Truven Analytics among others. We think investors should also pay close attention to entities working on digital biomarkers (e.g., iRhythm), as these companies may have an ability to generate important data sets for population health management.

Representative examples of Precision Medicine solutions include: Flatiron Health, Foundation Medicine, and Syapse among others.

Page 22

Internet & MediaDigital Healthcare April 6, 2015

Patient Engagement: The Patient Engagement vertical, in our view, represents difficult low hanging fruit. On one hand, engaging patients should be quite simple, but the difficulty lies in the fact that hospitals and HC IT vendors may not necessarily be well suited to drive engagement. We believe patient engagement represents an important tool given the requirements of Meaningful Use Stage 2. In our view, successful examples of platforms with strong patient engagement include athenaCommunicator and Everyday Health. We believe that patient engagement will come to represent wearable devices and health and wellness solutions that help consumers manage their health. Ultimately, we believe patient engagement will require more than a portal and likely involve developing or partnering to provide relevant content to consumers. We believe wearable devices will come to represent an important driver of patient engagement.

Representative examples of Patient Engagement solutions include: athenaCommunicator, Everyday Health, WebMD, Sharecare, health & wellness platforms such as RedBrick Health, consumer / fitness wearable devices such as Jawbone and Misfit, as well as more clinically focused devices such as Cohero and Propeller Health.

Page 23

Internet & MediaDigital Healthcare April 6, 2015

Part 3: Understanding the Macro Economic Environment

We believe an important aspect of Healthcare IT (HCIT) and digital healthcare revolves around the macro-economic outlook. The main source of macro estimates revolve around healthcare expenditure forecasts provided by The Centers for Medicare and Medicaid Services (CMS). As of July 2014, CMS estimates that healthcare expenditures will reach $4.1 trillion in 2020, up from $2.7 trillion in 2013. We believe most investors, and most vendors accept these healthcare expenditures at face value. In our view, investors should consider a range of possible scenarios that consider a possible bending of the cost curve driven by performance improvement and operational efficiencies driven by technology. In our view, assuming that national health expenditures continuously rise with no bending of the cost curve suggests that the U.S. transition to a digitized health system will represent a massive failure.

In Exhibit 14, we illustrate the base case macro outlook for national health expenditures according to CMS. According to CMS, national health expenditures will increase at a 6.0% compound annual growth rate between 2014E and 2022E. As of 2013, national health expenditures (NHE) totaled roughly $2.7 trillion and roughly 16.3% of U.S. Gross Domestic Product (GDP). By 2015, national health expenditures are expected to reach $3.0 trillion and roughly 16.7% of U.S. GDP. By 2020, national health expenditures are expected to reach roughly $4.1 trillion and roughly 17.5% of U.S. GDP. We believe the main purpose of digital health care and SES offerings revolves around bending the national health expenditure cost cure, and at least attempting to slow the rate of growth to some extent. In our view, if CMS’ cost curve represents future reality, then we believe both traditional HCIT vendors and digital healthcare innovators will have trouble maintaining viable businesses in the future.

Exhibit 14: CMS estimates on National Healthcare Expenditures

Source: CMS and Stifel

2,893 3,041

3,213 3,396

3,602 3,834

4,085 4,341

4,610

16.7% 16.7%16.8%

16.9%17.0%

17.2%

17.5%

17.7%

18.0%

15.5%

16.0%

16.5%

17.0%

17.5%

18.0%

18.5%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E

U.S. National Health Expenditure Trends

National Health Expenditures (NHE) NHE as a % of GDP

Page 24

Internet & MediaDigital Healthcare April 6, 2015

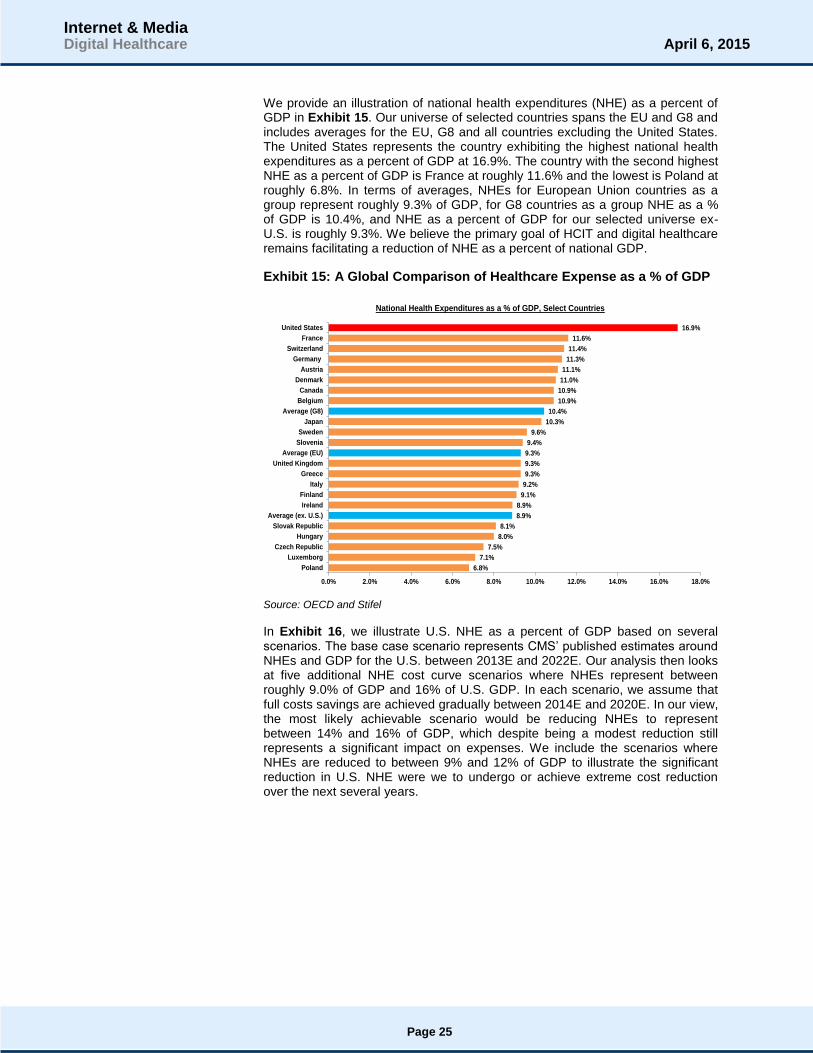

We provide an illustration of national health expenditures (NHE) as a percent of GDP in Exhibit 15. Our universe of selected countries spans the EU and G8 and includes averages for the EU, G8 and all countries excluding the United States. The United States represents the country exhibiting the highest national health expenditures as a percent of GDP at 16.9%. The country with the second highest NHE as a percent of GDP is France at roughly 11.6% and the lowest is Poland at roughly 6.8%. In terms of averages, NHEs for European Union countries as a group represent roughly 9.3% of GDP, for G8 countries as a group NHE as a % of GDP is 10.4%, and NHE as a percent of GDP for our selected universe ex-U.S. is roughly 9.3%. We believe the primary goal of HCIT and digital healthcare remains facilitating a reduction of NHE as a percent of national GDP.

Exhibit 15: A Global Comparison of Healthcare Expense as a % of GDP

Source: OECD and Stifel

In Exhibit 16, we illustrate U.S. NHE as a percent of GDP based on several scenarios. The base case scenario represents CMS’ published estimates around NHEs and GDP for the U.S. between 2013E and 2022E. Our analysis then looks at five additional NHE cost curve scenarios where NHEs represent between roughly 9.0% of GDP and 16% of U.S. GDP. In each scenario, we assume that full costs savings are achieved gradually between 2014E and 2020E. In our view, the most likely achievable scenario would be reducing NHEs to represent between 14% and 16% of GDP, which despite being a modest reduction still represents a significant impact on expenses. We include the scenarios where NHEs are reduced to between 9% and 12% of GDP to illustrate the significant reduction in U.S. NHE were we to undergo or achieve extreme cost reduction over the next several years.

6.8%

7.1%

7.5%

8.0%

8.1%

8.9%

8.9%

9.1%

9.2%

9.3%

9.3%

9.3%

9.4%

9.6%

10.3%

10.4%

10.9%

10.9%

11.0%

11.1%

11.3%

11.4%

11.6%

16.9%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0%

Poland

Luxemborg

Czech Republic

Hungary

Slovak Republic

Average (ex. U.S.)

Ireland

Finland

Italy

Greece

United Kingdom

Average (EU)

Slovenia

Sweden

Japan

Average (G8)

Belgium

Canada

Denmark

Austria

Germany

Switzerland

France

United States

National Health Expenditures as a % of GDP, Select Countries

Page 25

Internet & MediaDigital Healthcare April 6, 2015

Exhibit 16: Comparison of Several Scenarios Involving a Reduction in Healthcare Expense as a % of GDP

Source: CMS, OECD, and Stifel

We illustrate a few additional scenarios around U.S. NHEs as a percent of GDP in Exhibit 17. Once again, we start with the base case U.S. NHE assumptions published by CMS in July 2014. We then compare the base case to three additional cost curve scenarios. The first scenario assumes costs savings gradually reach $375 billion by 2020E driven by big data and analytics. The scenario represents the midpoint of McKinsey’s estimated annual savings of $300 billion to $450 billion associated with the application of analytics and big data to the U.S. healthcare system. The second scenario assumes that we can bend the NHE cost curve by gradually reducing NHEs to roughly 15% of U.S. GDP by 2020E. The final scenario assumes a gradual reduction in NHE, which reaches roughly $1.125 billion on an annual basis in 2020E. The final scenario consists of the midpoint of the McKinsey estimates and the removal of $750B in annual waste in U.S. NHE, according to Rock Health.

Each scenario assumes that we gradually reach a target annual reduction goal and holds NHE as a percent of GDP constant once the full savings are achieved. Our assumption revolves around our belief that SES offerings that provide significant ROI and drive performance improvement and operational efficiencies will allow the system to more easily maintain NHEs as a percent of U.S. GDP. In our view, the scenarios presented in Exhibit 16 and Exhibit 17 suggest that the scenarios where NHEs reach 14% to 16% of U.S. GDP are achievable. In our view, the biggest risk to our assumptions revolves around the fact that achieving full annual cost savings may not be achieved until after 2020E. Nevertheless, we believe these scenarios illustrate the real opportunity facing digital healthcare innovators and further illustrates why we believe the industry will continue to shift more towards SES over the coming years.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E

Bending the National Health Expenditure Cost Curve Scenario Analysis

NHE as a % of GDP NHE as 16% of GDP

NHE as 14% of GDP NHE as 12% of GDP (France Scenario)