a conceptual framework for information technology project

TRANSCRIPT

A CONCEPTUAL FRAMEWORK FOR INFORMATION

TECHNOLOGY PROJECT MANAGEMENT AUDITING

By:

Jean-Paul M. MUKA

DISSERTATION

Submitted in fulfilment of the requirements for the degree of

MASTER OF TECHNOLOGY

In the

DEPARTMENT OF BUSINESS INFORMATION TECHNOLOGY

At the

UNIVERSITY OF JOHANNESBURG

SUPERVISED BY Dr. Carl Marnewick

CO-SUPERVISED BY Prof. Les Labuschagne

(SEPTEMBER 2011)

i

ACKNOWLEDGEMENTS

To Shila, Andy and Flory.

First of all, I wish to thank the Almighty God for the gift of life and good health, without which I

would never have been able to complete this project.

I also wish to extend my gratitude to all those who, directly or indirectly, helped me in completing

this work. This includes family and friends who supported me in various ways. These people are

too numerous to mention by name, but I wish to single out my parents who first taught me the

value of hard work and sacrifice.

Dr. C. Marnewick, my supervisor, has helped me immensely in completing this dissertation. His

rigorous critiques proved to be exactly what was needed. Many thanks to him and to all the

University of Johannesburg (UJ) staff who contributed. I am also absolutely grateful to Prof. L.

Labuschagne, my co-supervisor, whose insights were invaluable in the conception of this

research.

Last but not least, I wish to thank my dear wife [Shila] and our two boys [Andy and Flory] for their

unfailing love and support. They were certainly robbed of precious family time during the long

hours required to complete this project. This work is dedicated to them!

To God be the glory.

ii

ABSTRACT

In this age of ever-increasing competition, organisations are facing unprecedented pressure to

meet the combined obligations of showing returns to shareholders, and staying ahead of the

competition. To meet these obligations, organisations have become increasingly dependent on

technology, as an enabler. This dependency suggests that technology projects have become

strategically more important than ever for organisations; yet the success of technology projects

remains questionable. Furthermore, organisations do not have simple mechanisms to allow them

to quickly and accurately trace the causes of IT project management failures. One of the causes

of project management failures is the inability and/or unwillingness of project managers to adhere

to project management best practices adopted by their organisations.

This research proposes a simple and repeatable model to help organisations determine whether

they are indeed following the project management best practices which they purport to follow.

The research methods consisted firstly of a wide review of relevant literature on auditing, project

management, and IT governance. Secondly, empirical data was collected and analysed. Thirdly,

modelling was used to develop a conceptual model for auditing IT project management.

The empirical study is based on a semi-structured interview, involving ten project managers in

charge of IT projects. The findings from this research confirm that project managers do not

adhere to project management best practices which they purport to follow. Consequently, this

dissertation concludes that IT project managers must adhere to best practices adopted by their

organisations, regardless of how impractical or inconvenient that may seem; the proposed model

for auditing IT project management helps them achieve just that.

Keywords: project management, auditing, model, Information Technology, IT governance.

iii

TABLE OF CONTENTS

ABSTRACT.................................................................................................................................. i ACKNOWLEDGEMENTS............................................................................................................ ii LIST OF TABLES...................................................................................................................... vii LIST OF FIGURES.................................................................................................................... vii 1 CHAPTER 1 – DISSERTATION INTRODUCTION ..............................................................1

1.1 Introduction.................................................................................................................1 1.1.1 Background........................................................................................................1 1.1.2 Research Goals .................................................................................................2 1.1.3 Research Objectives ..........................................................................................2 1.1.4 Layout ................................................................................................................3

1.2 Problem statement......................................................................................................3 1.3 Research process.......................................................................................................4

1.3.1 Explore...............................................................................................................4 1.3.2 Propose .............................................................................................................4 1.3.3 Prepare ..............................................................................................................4 1.3.4 Execute..............................................................................................................5 1.3.5 Analyse ..............................................................................................................5 1.3.6 Publish...............................................................................................................5

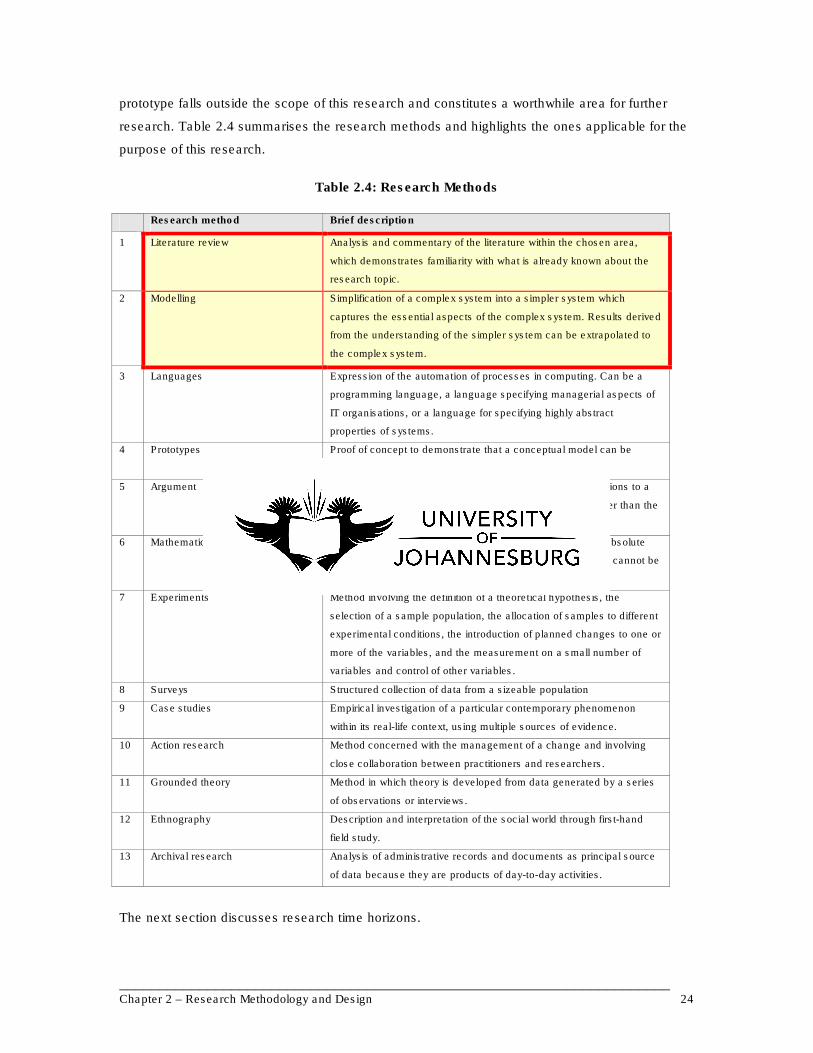

1.4 Research deliverables ................................................................................................5 1.4.1 Literature review.................................................................................................5 1.4.2 Audit guidelines..................................................................................................7 1.4.3 Project management components ......................................................................7 1.4.4 Guideline for auditing IT projects ........................................................................8 1.4.5 Current state of project management..................................................................8 1.4.6 Conceptual model ..............................................................................................8

1.5 Dissertation Layout .....................................................................................................9 2 CHAPTER 2 – RESEARCH METHODOLOGY AND DESIGN ...........................................11

2.1 Introduction...............................................................................................................11 2.1.1 Background......................................................................................................11 2.1.2 Goal .................................................................................................................11 2.1.3 Objectives ........................................................................................................11 2.1.4 Chapter Layout.................................................................................................12 2.1.5 Research design ..............................................................................................12 2.1.6 Research methodology.....................................................................................13

2.1.6.1 Research philosophy................................................................................14 2.1.6.2 Research approaches ..............................................................................16 2.1.6.3 Research types ........................................................................................20 2.1.6.4 Research methods...................................................................................22 2.1.6.5 Research time horizons............................................................................25 2.1.6.6 Data collection and analysis techniques ...................................................26

2.2 Conclusion................................................................................................................37 3 CHAPTER 3 – LITERATURE REVIEW ON AUDITING......................................................40

3.1 Introduction...............................................................................................................40 3.1.1 Background......................................................................................................40 3.1.2 Goal .................................................................................................................40 3.1.3 Objectives ........................................................................................................40 3.1.4 Layout ..............................................................................................................40

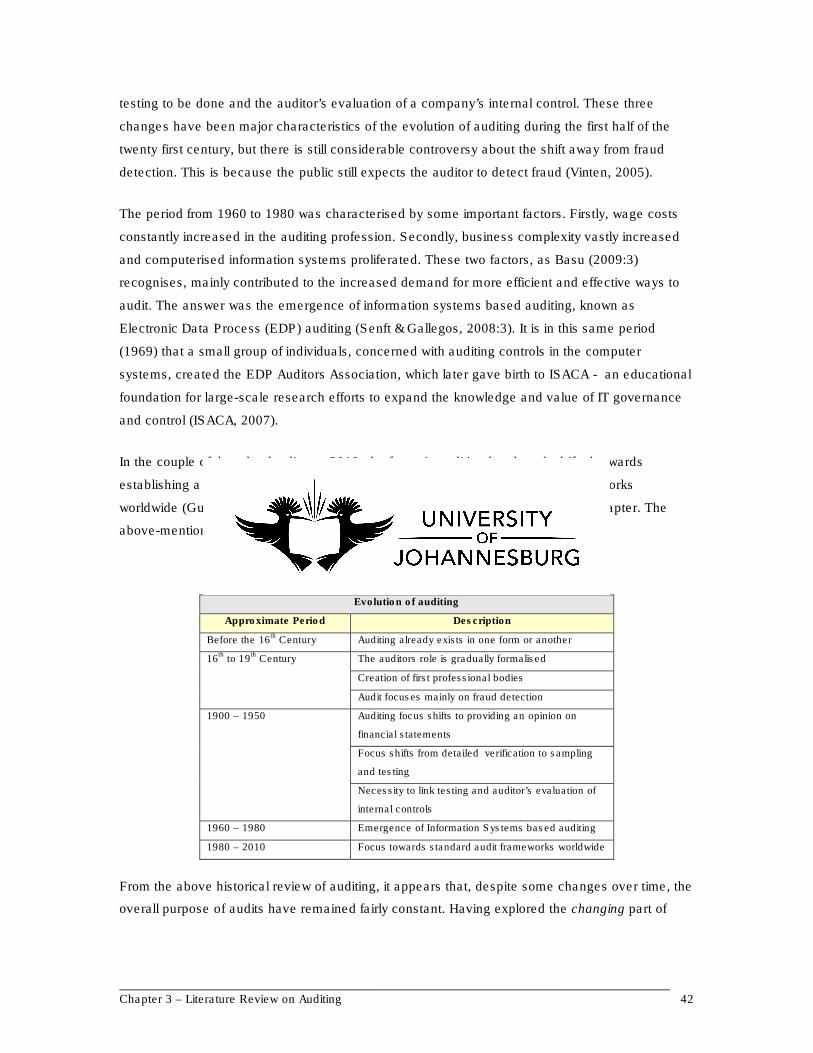

3.2 Brief historical overview on auditing ..........................................................................41 3.3 Defining auditing.......................................................................................................43

3.3.1 Types of audit...................................................................................................44 3.3.2 Types of auditors..............................................................................................47

iv

3.4 Auditing Standards ...................................................................................................48 3.4.1 Generally Accepted Auditing Standards (GAAS)...............................................49

3.5 Project management auditing....................................................................................51 3.5.1 Defining project management auditing..............................................................52 3.5.2 Types of project management audit ..................................................................53 3.5.3 Types of project management auditors .............................................................54 3.5.4 The project management audit process ............................................................54

3.6 Conclusion................................................................................................................56 4 CHAPTER 4 – LITERATURE REVIEW ON PROJECT MANAGEMENT ............................58

4.1 Introduction...............................................................................................................58 4.1.1 Background......................................................................................................58 4.1.2 Goal .................................................................................................................58 4.1.3 Objectives ........................................................................................................58 4.1.4 Layout ..............................................................................................................58

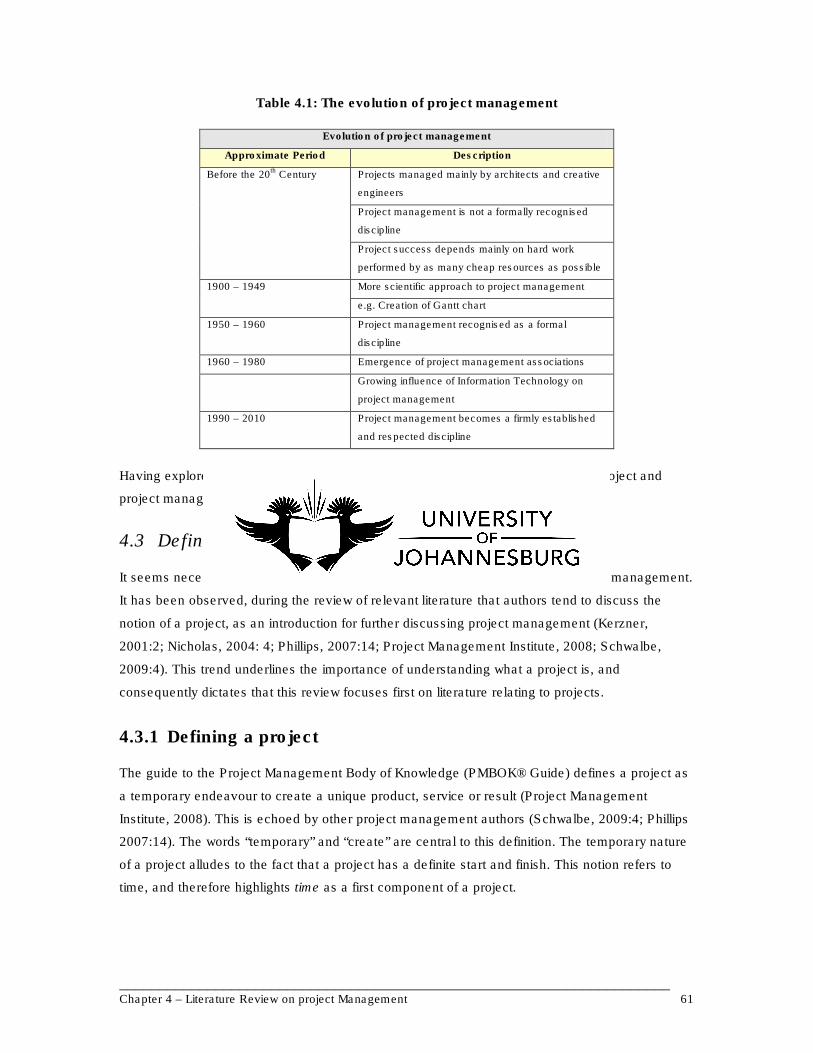

4.2 Brief historical overview on project management.......................................................59 4.3 Defining project management ...................................................................................61

4.3.1 Defining a project .............................................................................................61 4.3.2 Defining project management ...........................................................................64

4.3.2.1 Knowledge...............................................................................................65 4.3.2.2 Skills........................................................................................................65 4.3.2.3 Tools and techniques...............................................................................66

4.4 Project management best practices ..........................................................................67 4.4.1 A Guide to the Project Management Body of Knowledge (PMBOK® Guide)......68

4.5 Conclusion................................................................................................................71 5 CHAPTER 5 – LITERATURE REVIEW ON INFORMATION TECHNOLOGY GOVERNANCE.........................................................................................................................73

5.1 Introduction...............................................................................................................73 5.1.1 Background......................................................................................................73 5.1.2 Goal .................................................................................................................73 5.1.3 Objectives ........................................................................................................73 5.1.4 Layout ..............................................................................................................73

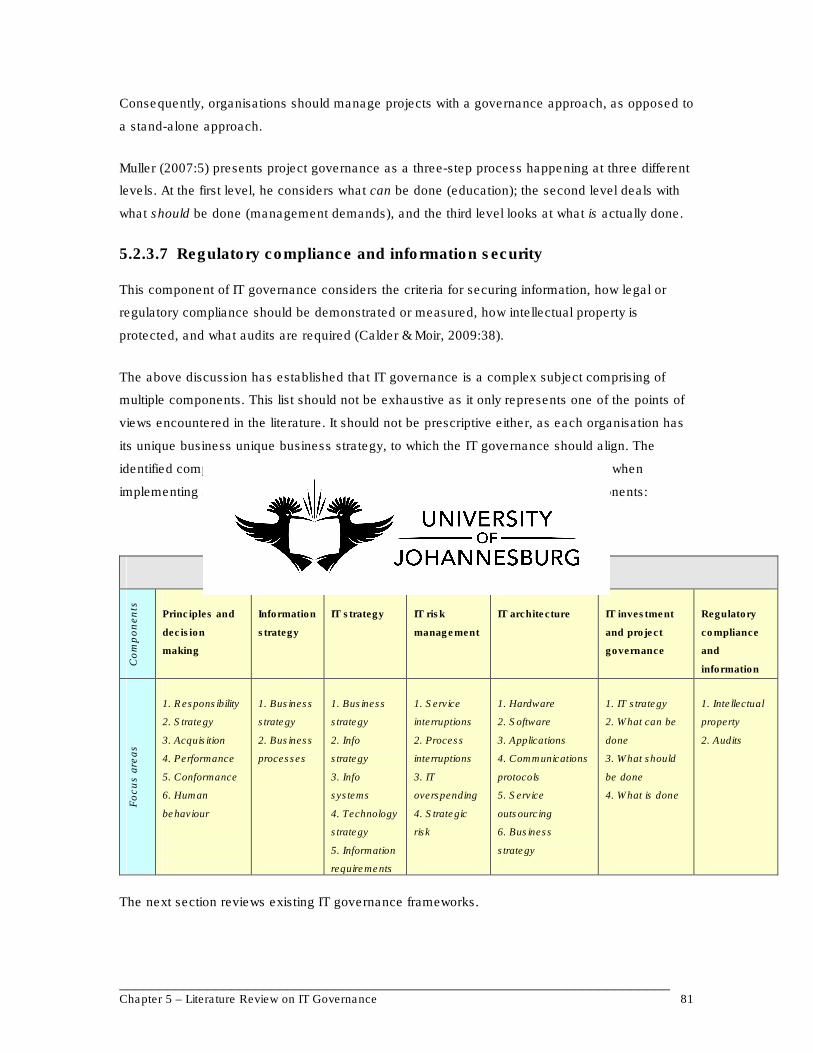

5.2 Overview of IT governance .......................................................................................74 5.2.1 Defining IT governance ....................................................................................74 5.2.2 The importance of IT governance .....................................................................76 5.2.3 IT governance components ..............................................................................78

5.2.3.1 IT governance principles and decision-making hierarchy ..........................78 5.2.3.2 Information strategy .................................................................................79 5.2.3.3 IT strategy................................................................................................79 5.2.3.4 IT risk management .................................................................................79 5.2.3.5 IT architecture..........................................................................................80 5.2.3.6 IT investment and project governance......................................................80 5.2.3.7 Regulatory compliance and information security.......................................81

5.3 IT governance sources .............................................................................................82 5.4 COBIT as an IT governance framework ....................................................................83

5.4.1 Brief historical overview and current perspectives.............................................83 5.4.2 What is the COBIT framework? ........................................................................84 5.4.3 COBIT structure ...............................................................................................84

5.4.3.1 IT processes ............................................................................................84 5.4.3.2 IT resources.............................................................................................85 5.4.3.3 Quality criteria..........................................................................................86

5.4.4 COBIT approach ..............................................................................................87 5.4.4.1 COBIT control mechanism .......................................................................88 5.4.4.2 Project management audit steps ..............................................................91

5.5 Conclusion................................................................................................................92 6 CHAPTER 6 – DATA COLLECTION AND ANALYSIS.......................................................94

6.1 Introduction...............................................................................................................94

v

6.1.1 Background......................................................................................................94 6.1.2 Goal .................................................................................................................94 6.1.3 Objectives ........................................................................................................95 6.1.4 Layout ..............................................................................................................95

6.2 Overview of the data collection .................................................................................95 6.2.1 Data collection steps ........................................................................................95 6.2.2 Interview questions...........................................................................................97 6.2.3 Data collection techniques................................................................................99 6.2.4 Data analysis techniques................................................................................100 6.2.5 Target population ...........................................................................................100 6.2.6 Sampling........................................................................................................100 6.2.7 Recruitment of interview respondents .............................................................101 6.2.8 Ethical considerations.....................................................................................101

6.3 Presentation of data................................................................................................102 6.4 Data analysis and recommendations.......................................................................109 6.5 Conclusion..............................................................................................................120

7 CHAPTER 7 – A CONCEPTUAL AUDIT MODEL............................................................122 7.1 Introduction.............................................................................................................122

7.1.1 Background....................................................................................................122 7.1.2 Goal ...............................................................................................................122 7.1.3 Objectives ......................................................................................................122 7.1.4 Layout ............................................................................................................122

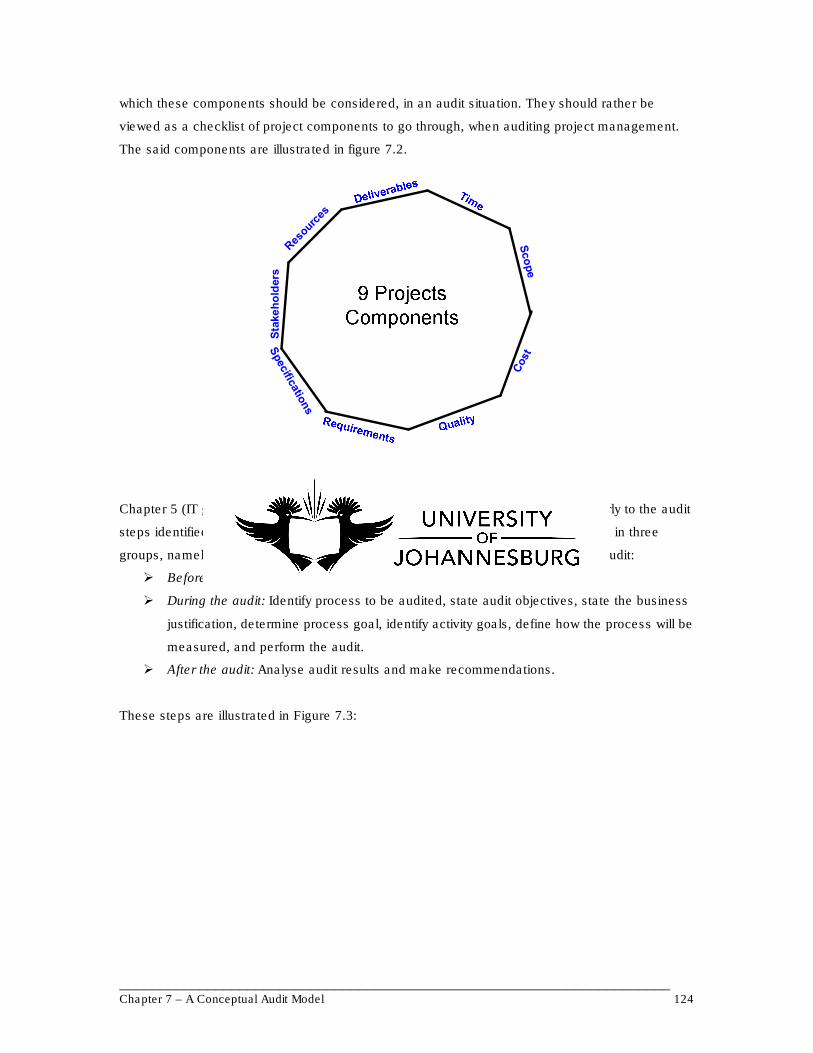

7.2 Existing knowledge .................................................................................................123 7.3 The role of project components in the model ...........................................................125

7.3.1 The role of generic auditing steps ...................................................................125 7.3.2 The role of project components.......................................................................126 7.3.3 The role of the IT project auditing guideline in the model.................................126

7.4 The conceptual model.............................................................................................126 7.4.1 Phase 1: Merge generic audit steps and project components..........................126

7.4.1.1 Before the audit......................................................................................127 7.4.1.2 During the audit......................................................................................127 7.4.1.3 After the audit ........................................................................................127

7.4.2 Phase 2: Merge the output of phase 1 and the guidelines for auditing IT projects 128

7.4.2.1 Before the audit......................................................................................128 7.4.2.2 During the audit......................................................................................128 7.4.2.3 After the audit ........................................................................................128

7.4.3 Integrated model for IT project management auditing......................................128 7.4.3.1 Before the audit......................................................................................129 7.4.3.2 During the audit: planning ......................................................................129 7.4.3.3 During the audit: fieldwork......................................................................129 7.4.3.4 After the audit ........................................................................................129

7.4.4 Application of the conceptual audit model on the Develop project charter process 130

7.4.4.1 Before the audit......................................................................................131 7.4.4.2 During the audit: planning ......................................................................131 7.4.4.3 During the audit: fieldwork......................................................................132 7.4.4.4 After the audit ........................................................................................134

7.5 Conclusion..............................................................................................................134 8 CHAPTER 8 – DISSERTATION CONCLUSION..............................................................135

8.1 Introduction.............................................................................................................135 8.2 Revisiting the problem ............................................................................................136

8.2.1 Research Goal ...............................................................................................136 8.2.2 Research Objectives and Findings..................................................................137

8.2.2.1 Objective 1 – Guideline for the auditing process .....................................137 8.2.2.2 Objective 2 – Project components ..........................................................137

vi

8.2.2.3 Objective 3 – Guideline for auditing IT projects.......................................138 8.2.2.4 Objective 4 – Collect and analyse data through an empirical study .........138 8.2.2.5 Objective 5 – A conceptual model ..........................................................139

8.3 From findings to conclusions...................................................................................139 8.3.1.1 Conclusion 1..........................................................................................139 8.3.1.2 Conclusion 2..........................................................................................139 8.3.1.3 Conclusion 3..........................................................................................139 8.3.1.4 Conclusion 4..........................................................................................140 8.3.1.5 Conclusion 5..........................................................................................140

8.4 Research limitations ...............................................................................................140 8.4.1 Limited sampling ............................................................................................140 8.4.2 Cross-sectional time horizon for data collection ..............................................140 8.4.3 Conceptual model limited to IT project management.......................................141

8.5 Research value.......................................................................................................141 8.6 Recommendations for further research ...................................................................142

8.6.1 Larger sample for empirical study ...................................................................142 8.6.2 Conduct a longitudinal study...........................................................................142 8.6.3 Develop a conceptual model applicable to both IT and non-IT project management auditing......................................................................................................142

8.7 Self reflections........................................................................................................142 LIST OF REFERENCES..........................................................................................................144 APPENDIX A: Interview invitation letter ...................................................................................168 APPENDIX B: Interview Transcripts.........................................................................................169

vii

LIST OF TABLES

Table 1.1: Summary of research deliverables, main chapter and value ........................................8 Table 1.2: Research philosophies..............................................................................................16 Table 2.1: Deductive vs inductive research approaches.............................................................20 Table 2.3: Summary of research types.......................................................................................22 Table 2.4: Research methods....................................................................................................24 Table 2.5: Research time horizons.............................................................................................26 Table 2.6: Data collection techniques ........................................................................................31 Table 2.7: Data analysis techniques ..........................................................................................36 Table 3.1: Evolution of auditing..................................................................................................42 Table 3.2: Types of audit identified vs types of audit used for the purpose of this research.........46 Table 4.1: Evolution of project management ..............................................................................61 Table 5.1: IT governance components.......................................................................................81 Table 5.2: The four COBIT domains and their respective IT processes ......................................85 Table 5.3: The four COBIT IT resources and their respective focus............................................86 Table 5.4: The seven COBIT information criteria and their respective focus ...............................87 Table 6.1: Interview questions and answers.............................................................................103 Table 6.2: Interview data categories ........................................................................................104

LIST OF FIGURES

Figure 1.1: The Literature Review Process ..................................................................................7 Figure 1.2: Dissertation layout ...................................................................................................10 Figure 2.1: Hourglass research design.......................................................................................13 Figure 2.2: Research onion .......................................................................................................37 Figure 3.1: Three-step process of auditing.................................................................................43 Figure 3.2: Simplified triple dimension of auditing.......................................................................48 Figure 3.3: Expanded triple dimension of auditing......................................................................51 Figure 3.4: Three-step process for auditing project management ...............................................53 Figure 3.5: Four-step process for auditing project management .................................................55 Figure 3.6: Expanded process for auditing project management ................................................55 Figure 4.1: Project components .................................................................................................64 Figure 4.2: Project management components............................................................................67 Figure 4.3: Process components ...............................................................................................69 Figure 4.4: Flow of data in the “Develop project charter” process ...............................................70 Figure 5.1: Governance pyramid................................................................................................76 Figure 5.2: The COBIT control mechanism ................................................................................90 Figure 5.3: Guideline for auditing IT projects..............................................................................92 Figure 7.1: Four-step audit process .........................................................................................123 Figure 7.2: Nine project components .......................................................................................124 Figure 7.3: Guideline for auditing IT projects............................................................................125 Figure 7.4: Generic audit process merged with project components.........................................127 Figure 7.5: Integrated conceptual model for auditing project management ...............................130 Figure 8.1: Mapping between Bloom’s taxonomy of cognitive learning and this dissertation .....136

_____________________________________________________________________ Chapter 1 – Dissertation Introduction 1

CHAPTER 1 – DISSERTATION INTRODUCTION

1.1 Introduction

1.1.1 Background

In today’s business environment marked by intense competition, organisations face ever-

increasing pressures to meet shareholders’ expectations (Murray, 2002:165; McMullin, 2007;

Wyman, 2007). Achieving profitability objectives – increasing revenue and/or decreasing cost – is

an integral part of the said shareholders’ expectations (Grant & Abate, 2001:45; Australian

Shareholders’ Association, 2005:1). Successful Information Technology (IT) project management

is also recognised as a catalyst in achieving an organisation’s profitability objectives, and

ultimately in creating shareholder value (Floyd, 1997: 229-233; Cooke-Davies, 2002; Hartman &

Ashrafi, 2002). Thus, there is a link between the need to create shareholder value in business

organisations and the need to manage projects successfully.

Although people have worked on projects for centuries, several authors agree that project

management - which is defined as the application of knowledge, skills, tools and techniques to

project activities to meet project requirements (Lewis, 2007; Project Management Institute, 2008;

Schwalbe, 2009) - became recognised as a modern discipline in the mid-twentieth century. As

such, project management is nowadays applied in virtually every industry, thereby greatly

influencing the way organisations do business (Nicholas, 2004; Cleland & Ireland, 2006; Haugan,

2006; Nicholas & Steyn, 2008; Kloppenborg, 2009:5; Schwalbe, 2009).

While similarities exist between Project Management principles across disciplines (Hartman &

Ashrafi, 2002; Haugan, 2011:275), IT project management differs substantially from project

management in other disciplines (Otto, Dhillon & Watkins, 1993; Roetzheim, 1993; Raybould,

1996; Samuels, 1996; Stepanek, 2005). Notwithstanding these differences, there is a need to

understand what makes the difference between failure and success in managing projects.

Baccarini (1999:25) describes project success as consisting of project management success on

the one side, and project product success on the other. While the former focuses on how well the

project management processes are followed, the latter focuses on the project’s end-result.

Considering this description of project success, it can be said that an effort to identify whether a

project is a success or a failure should follow either or both of the following approaches: either

verifying how well project management processes were followed, or verifying the presence or

absence of the project’s end result. The goals and objectives of this research are best addressed

through the former approach. The next section sets the goals and objectives for this research.

_____________________________________________________________________ Chapter 1 – Dissertation Introduction 2

1.1.2 Research Goals

The goal of this research is to develop a model to guide organisations, through practical steps, in

determining whether they are following project management processes which they purport to

follow.

The following objectives need to be achieved, in order to meet these goals.

1.1.3 Research Objectives

� Objective 1 – To propose a guideline for the auditing process, in alignment with the

research problem, based on existing audit principles and guidelines. This objective is

achieved in Chapter 3, through the following sub-objectives:

o Sub-objective 1: Explore the evolution of auditing over time, and define auditing.

o Sub-objective 2: Identify and critically evaluate existing auditing standards.

o Sub-objective 3: Explore project management auditing, to understand the

relevance of auditing in project management.

� Objective 2 – To identify project components, based on existing project management

best practices. This objective is achieved in Chapter 4, through the following sub-

objectives:

o Sub-objective 1: Explore the evolution of project management over time, to its

current state.

o Sub-objective 2: Review project management and identify the various aspects to

take into account when auditing project management.

o Sub-objective 3: Identify recognised project management good practices

documentations, and review the project management approach on one of these

documentations.

� Objective 3 – Propose an adequate guideline for auditing IT projects, which aligns with

recognised IT governance frameworks. This objective is achieved in Chapter 5, through

the following sub-objectives: Review and evaluate different perspectives on IT

governance.

o Sub-objective 1: Review and evaluate different perspectives on IT governance.

o Sub-objective 2: Identify and review IT governance sources and frameworks.

o Sub-objective 3: Explore project governance and the relevance of governance in

project management.

_____________________________________________________________________ Chapter 1 – Dissertation Introduction 3

� Objective 4 – Find out the extent to which recognised project management practices are

applied in practice within project management entities. This objective is achieved in

Chapter 6, through the following sub-objectives:

o Sub-objective 1: Collect data on how project managers manage project

management processes.

o Sub-objective 2: Analyse the collected data and identify emerging trends and

issues.

o Sub-objective 3: Present the findings of the data analysis and make

recommendations.

� Objective 5 – propose a conceptual model for auditing IT project management. This

model should integrate the essential principles and knowledge gathered through the

above four objectives. This objective is addressed in Chapter 7.

1.1.4 Layout

The remainder of this chapter is laid out as follows:

Firstly, the research problem is introduced, and then the research process followed throughout

this dissertation is outlined. Having outlined the research process, the specific research

deliverables are listed and summarily discussed. This chapter ends by presenting the layout of

this dissertation.

1.2 Problem statement

The success rate of IT projects remains questionable (Gibbs, 1994; Standish Group, 1995;

Bailey, 1996; Grenny, Maxfield & Simberg, 2007; Labuschagne, Marnewick & Jakovljevic, 2008).

To ensure greater success rates of IT projects, it is necessary to have processes in place to

guide the project execution in a consistent manner. Consistently following these processes

should ensure that the project succeeds both in terms of delivering the expected end-product

(project product success), and in terms of delivering optimal efficiency of project execution by

following the right project management processes (project management success).

Many organisations have such processes in place, namely in the form of project offices (Bridges

& Crawford, 2000; Kent Crawford, 2002; Project Management Institute, 2008). Yet in reality,

these processes do not seem to be followed consistently. As a result, not only the success of the

project is made unpredictable, but also in case of project failure it becomes difficult to identify

what went wrong.

_____________________________________________________________________ Chapter 1 – Dissertation Introduction 4

This creates the opportunity for a mechanism to verify whether processes which were supposed

to be followed in managing a project were indeed followed. In pursuing this opportunity, this

research seeks to propose a model for auditing IT project management. Thus, the research

problem is formulated as follows:

Many organisations claim to manage projects according to some form of established best

practices. However, in reality these best practices do not seem to be followed

consistently; hence the need for a guideline to verify whether project management entities

really follow the project management best practices which they claim to follow.

In addressing this problem, this dissertation follows the following research process:

1.3 Research process

In line with recommendations by Olivier (2009), the following research process was followed:

1.3.1 Explore

This phase lays the basic foundation and determines the appropriateness of the research

problem. During this phase, literature review is conducted, including but not limited to reviewing

books, articles, journals and web sites. In this phase, generic knowledge is gathered on central

themes of this research, namely auditing (Chapter 3), project management (Chapter 4), and IT

governance (Chapter 5). As part of the exploration phase, and in direct relation to Chapter 4, an

enquiry is conducted (Chapter 6) to identify the extent to which recognised project management

practices are applied in practice within project management entities.

1.3.2 Propose

This phase seeks to establish that investigating the problem is worthwhile and realistic. Indeed,

considering low success rates in IT projects, and the resulting need to verify whether projects

managers follow the processes which they are supposed to (or claim to) follow, this research

proposes a conceptual model for auditing IT project management (Chapter 7). At this stage, the

research achieves its goal.

1.3.3 Prepare

Preparation is done to determine the main guidelines on how this research should be conducted.

This includes the research methodology and design presented in Chapter 2.

_____________________________________________________________________ Chapter 1 – Dissertation Introduction 5

1.3.4 Execute

This phase entails collecting data, to determine a relevance of the claim according to which

project managers do not seem to consistently follow project management processes which they

purport to follow.

1.3.5 Analyse

During this phase, the collected data is presented and analysed qualitatively, and

recommendations are made. This is done in Chapter 6.

1.3.6 Publish

This is the final phase of the research, which consists of publishing the final dissertation, and

preparing an article for submission at a project management conference.

1.4 Research deliverables

The sum total of each chapter’s deliverable constitutes the research deliverable. The researcher

also intends to propose, later in the research, a whole is indeed greater than the sum of its parts;

that is, to propose a model for auditing IT project management, by integrating individual research

deliverables created throughout the research. This deliverable constitutes the overall research

value of this dissertation. For now, here is a list of individual research deliverables:

� Literature review;

� Generic audit steps;

� Project components considered in a project management audit;

� Guideline for auditing IT projects;

� A conceptual audit model for IT project management;

Each of these deliverables is discussed in the next section.

1.4.1 Literature review

Neither the author’s interest, nor the relative popularity of the project management discipline

should constitute sound justification for yet another research project in the said discipline. What is

required is to narrow the issue to a relevant problem currently faced in the industry, and find a

methodical and realistic solution to the problem. The first deliverable of this research is therefore

a literature review, which aims to establish the researchability of this topic upfront, and to create

in the author a rigorous research attitude towards the topic at hand, and towards the

_____________________________________________________________________ Chapter 1 – Dissertation Introduction 6

determination of the appropriate research design and methodology in the time available (Hart,

1998:13).

The following steps are followed while conducting this literature review (Machi & McEvoy,

2009:5):

1. Select a topic: The research topic has emerged as a result of the author’s interest in a

practical problem. This interest is expressed through ideas that form a researchable topic. This

topic is stated as the research problem, which specifies and frames the next step.

2. Search the literature: By narrowing the vast amount of available information to only the data

that provides the strongest evidence to support the theses, this step determines what information

will be featured in the literature review. This explores and catalogs the next step.

3. Develop the argument: To argue the dissertation successfully, the case is formed and then

presented. To form the case, the claims need to be arranged logically. To present the case,

relevant data is organised into a body of evidence that explains what is known about the topic.

This organises and forms the next step.

4. Survey the literature: This step assembles, synthesises and analyses the data to form the

argument about the current knowledge on the topic. A logical set of defensible conclusions or

claims is created, which in turn provides a basis for addressing the research question. This

documents and discovers the next step.

5. Critique the literature: The current understanding of the topic is interpreted by analysing how

previous knowledge answers the research question. This step advocates and defines the next

step.

6. Write the review: This step intends to accurately convey the research, so as to be understood

by the intended audience. This step addresses step 1 above, thereby closing the loop of the

literature review cycle.

The literature review is delivered throughout this dissertation, particularly in Chapters 2 through 5.

Figure 1.1 illustrate the above-mentioned literature review cycle:

_____________________________________________________________________ Chapter 1 – Dissertation Introduction 7

Figure 1.1: The Literature Review Process. Source: Machi & McEvoy (2009:5)

1.4.2 Audit guidelines

This research aims to propose a new model for auditing. This implies that auditing is a central

theme in the research. To ensure the relevance and correctness of the audit model, it is

necessary to align it with existing audit principles and guidelines. Audit guidelines are presented

in the form of audit steps that serve to guide the auditor in conducting the audit (Moeller,

2009:248). This research therefore intends to tap into existing knowledge in the audit discipline, in

order to review relevant approaches or guidelines to auditing, and retain auditing steps as a

guideline. This is delivered in Chapter 3.

1.4.3 Project management components

The multi-faceted aspect of project management implies that this discipline consists of several

components (Pitagorsky, 2007:30). For a new model for auditing IT project management to be

effective, these components need to be identified upfront. They constitute the various aspects to

take into account when performing the audit. Addressing each of the identified components

should ensure the effectiveness and repeatability of the audit. Consistently doing so should make

the audit process repeatable. The identified project management components are delivered in

Chapter 4.

_____________________________________________________________________ Chapter 1 – Dissertation Introduction 8

1.4.4 Guideline for auditing IT projects

Having identified generic audit guidelines, it becomes possible to adapt these guidelines to the IT

industry. This adaptation should be informed by recognised IT governance best practices, as

done in Chapter 5.

1.4.5 Current state of project management

The research problem states that many project managers do not always put into practice the

project management theory which they purport to adhere to. This deliverable therefore focuses on

determining the extent to which this statement is valid. This is achieved in Chapter 6, by

collecting, analysing and interpreting data, and making recommendations.

1.4.6 Conceptual model

Having delivered (a) an auditing guideline, (b) project management components, and (c) IT

project management audit guidelines, it then becomes necessary to propose a conceptual model

integrating the above, and guiding the application of the above in an audit situation. This

conceptual model is proposed in Chapter 7.

Table 1.1 summarises the above-mentioned research deliverables and indicates where these

deliverables feature in the dissertation.

Table 1.1: Summary of research deliverables, main chapter and value

Deliverables

Main

Chapter(s)

Value of the deliverable(s)

Deliverable 1: Literature review. 3, 4, 5 Provides an understanding of existing knowledge

in the field being studied.

Deliverable 2: Generic audit guidelines. 3 Highlights the relevant audit guideline for this

research, after exploring existing guidelines.

Deliverable 3: Project management components. 4 Identifies specific “facets” of project management

which can be audited.

Deliverable 4: IT project management audit guidelines 5 Provides audit guidelines which are aligned to

both established audit guidelines and IT

governance principles.

Deliverable 5: Current state of the application of project

management theory.

6 Determines the extent to which project managers

put their project management theory into practice.

Deliverable 6: Conceptual model 7 Ensures consistency and repeatability of the

model by elaborating it in a pre-defined pattern.

The next section presents the layout of this dissertation.

_____________________________________________________________________ Chapter 1 – Dissertation Introduction 9

1.5 Dissertation Layout

This dissertation consists of eight chapters, grouped into five sections. Terms and concepts are

defined when they are first introduced. This implies that the best way to read this dissertation is to

read the chapters by following the order indicated in the figure 1.2.

The first section consists of the problem definition. In this section, the rationale for this research is

presented, and the research problem outlined. This section contains one chapter - Chapter 1. The

second section consists of the research design and structure. In this section, the author

investigates existing knowledge related to research design and highlights the design used for this

specific research. This section contains one chapter – Chapter 2. The third section consists of

literature review. In this section the author investigates existing knowledge in the fields being

researched, as a basis for proposing a solution. This section contains three chapters – Chapters

3, 4, and 5.

The fourth section consists of data collection and analysis. This section focuses on conducting a

basic inquiry in order to understand the extent to which project managers currently follow the

project management theory which they claim to follow. This section contains one chapter –

Chapter 6. The fifth section addresses the research solution. This section contains two chapters,

namely Chapter 7, which proposes a conceptual model and Chapter 8, which presents the

dissertation conclusions and recommendations.

A brief description of each chapter is provided below.

Chapter 1 – Provides the background information and motivation for this research. This chapter

presents the research problem, elaborates on the research process followed in addressing the

problem, and lists the research deliverables.

Chapter 2 – Provides background information and literature review on scientific research. The

knowledge gathered in this exercise allows the author to make informed choices on the design of

this research.

Chapter 3 – Investigates the field of auditing, includes its evolution to its current state. This

chapter also explores generic audit guidelines and derives the relevant audit guideline for the

purpose of this research.

Chapter 4 – Investigates the project management discipline and highlights key project

management components. These components direct the audit focus onto specific facets of

project management.

_____________________________________________________________________ Chapter 1 – Dissertation Introduction 10

Chapter 5 – Investigates IT governance frameworks, as an authoritative sources from which the

identified generic audit guidelines can be adapted into detailed guidelines for auditing IT projects.

Chapter 6 – Is directly related to Chapter 4, and should be read as such. After providing the

overview on project management (Chapter 4), it became necessary to devote a chapter to a

formal enquiry aimed at determining the extent to which project managers follow best practices

which they purport to follow.

Chapter 7 – Proposes a conceptual model. This chapter integrates the knowledge gathered as

part of the previous chapters, into a conceptual model.

Chapter 8 – Concludes this research. This chapter summarises the research deliverables

presented throughout the dissertation and presents the unique value of this research. The

chapter also discusses some closing points, including key learning points, areas for further

research, research limitations, and final thoughts from the author.

Figure 1.2 illustrates the flow of the above-mentioned sections and chapters.

Figure 1.2: Dissertation Layout

The next chapter discusses the research methodology and design.

_____________________________________________________________________ Chapter 2 – Research Methodology and Design 11

2 CHAPTER 2 – RESEARCH METHODOLOGY AND DESIGN

2.1 Introduction

2.1.1 Background

The previous chapter presented an overview of this research, including the research problem,

process and deliverables. It has been highlighted that there is a need to systematically verify

whether an organisation consistently applies the project management theory which it claims to

adhere to. This chapter focuses on how the research is designed, to arrive at the said model.

Research is a gathering of data, information and facts for the advancement of knowledge

(Shuttleworth, 2008). This definition aligns with Saunders, Lewis and Thornhill (2009), who define

research as “…something that people undertake in order to find out things in a systematic way,

thereby increasing their knowledge…” The latter definition highlights two important phrases,

namely “systematic way” and “to find out things”.

“Systematic” suggests that research is based on logical relationships and not just beliefs (Ghauri

& Grønhaug, 2005); “to find out things” suggests that there are various possible purposes for

which to conduct research. These may include describing, explaining, understanding, criticising

and analysing (Ghauri & Grønhaug, 2005).

The next section sets the goals and objectives for this chapter.

2.1.2 Goal

The goal of this chapter is to articulate the research methodology used throughout this research.

The following objectives need to be achieved, in order to meet this goal.

2.1.3 Objectives

� Objective 1: Review the literature on research philosophies and highlight the one(s)

adopted for the purpose of this research.

� Objective 2: Review the literature on research approaches and highlight the one(s)

adopted for the purpose of this research.

� Objective 3: Review the literature on research methods and highlight the one(s) adopted

for the purpose of this research.

� Objective 4: Review the literature on alternative research time horizons and highlight the

one(s) adopted for the purpose of this research.

_____________________________________________________________________ Chapter 2 – Research Methodology and Design 12

� Objective 5: Review the literature on data collection and data analysis methods and

highlight the one(s) adopted for the purpose of this research.

2.1.4 Chapter Layout

The remainder of this chapter is laid out as follows:

The first section discusses the flow of this research project, from a research design perspective.

The second section reviews research philosophies and highlights the philosophy used for the

purpose of this research. The third section reviews research approaches and highlights the

approach used for the purpose of this research.

The fourth section reviews research methods and highlights the method(s) used for the purpose

of this research. The fifth section reviews research time horizons and highlights the time horizon

of this specific research. The last section reviews data collection and analysis techniques and

highlights the ones used for this research.

2.1.5 Research design

Research design is the process through which a research question is transformed into a research

project (Robson, 2002). The “hourglass design” is one of many ways to conceptualise the

research design (Trochim, 2006). This entails picturing a research project in the shape of an

hourglass - wide at the top, narrow in the middle and wide again at the bottom.

Below is a brief elaboration of the “hourglass design”:

The research process starts at the top of the hour glass with the research problem that the

researcher intends to study. However, this initial problem is often too wide to effectively cover in a

single study, hence the need to narrow the problem down to a question that can reasonably be

addressed in a single study. This might imply formulating a hypothesis or a focus question. In the

current research, the wider area of interest relates to project management. This area is narrowed,

through literature review, to specific topic which can reasonably be explored in a single research,

namely the proposal of a new model for auditing IT project management.

The next step in the hourglass process corresponds to the narrowest point of the hour glass (the

middle). At this point, the actual measurement or observation of the question at hand is

performed. In the current research, this step corresponds to determining the extent to which the

research hypothesis is valid.

_____________________________________________________________________ Chapter 2 – Research Methodology and Design 13

The scope of the hour glass then widens, as the researcher starts to analyse and apply the

research results in a variety of ways. At this stage, some initial conclusions are formulated,

subsequently to the outcome of the data analysis. In the current research, this step corresponds

to presenting data analysis findings and making recommendations.

The final stage refers to the bottom of the hour glass. At this point, the researcher attempts to

address the original goal of the study at hand, by generalising the research results to other

related situations (Trochim, 2006). In the current research, this step corresponds proposing a

conceptual model.

Figure 2.1 illustrates the above-mentioned hourglass design, and highlights its relevance to this

particular research.

Figure 2.1: Hourglass research design (Adapted from Trochim, 2006)

While the above-mentioned design provides a picture of how this research project is organised, it

does not precisely inform the reader on how the researcher went about conducting this research.

This clarity is provided in the research methodology, discussed in the next section.

2.1.6 Research methodology

_____________________________________________________________________ Chapter 2 – Research Methodology and Design 14

Research methodology is the theory of how research should be undertaken, including the

theoretical and philosophical assumptions upon which research is based and the implications of

these for the method(s) adopted (Saunders et al., 2009). Since a research question has been

defined for this research, the researcher might consider beginning thinking of this research

project in terms of how to collect and analyse data to answer the research question. However,

some authors argue that it is important to first of all define the philosophy and paradigm

underpinning the research (Guba & Lincoln, 1994:105; Johnson & Clark, 2006; Saunders et. al,

2009). This refers to the important assumptions from which the author embarks in this research,

and serves to inform the researcher about the appropriate methods to be used, in line with the

research goals.

2.1.6.1 Research philosophy

Research philosophy relates to the development of knowledge and the nature of that knowledge

(Saunders et. al, 2009). The philosophy adopted in this research is influenced, on the one hand

by practical considerations, and on the other hand, by the researcher’s view of the relationship

between the knowledge being sought and the process by which this knowledge is developed.

Ultimately, the important issue should be for the researcher to be able to reflect upon the

philosophical choices used and defend them in relation to the alternatives which could have been

used.

The aim is not to argue on which philosophy is better than the other, but rather to highlight which

philosophy best allows the researcher to answer the research question within the practical

limitations of this research project. Some possible overlaps may exist between the alternatives

chosen, but for the purpose of this research, the researcher attempts as much as possible to

present the various choices as distinct and separate alternatives. The philosophical choices

discussed in this section include pragmatism, interpretivism, realism, and positivism. This list in

by no means exhaustive, but these are some of the most common philosophies used in

management research (Saunders et al. 2009).

a) Pragmatism

Pragmatism argues that the research question is the most important determinant of the ontology,

epistemology and axiology adopted by the researcher (Tashakkori & Teddlie, 1998:26; Saunders

et al., 2009). The pragmatism philosophy considers that the researcher should study the topic of

interest in the different ways deemed appropriate, and use the results in ways which can

generate positive consequences within the researcher’s value system (Tashakkori & Teddlie,

1998:30).

_____________________________________________________________________ Chapter 2 – Research Methodology and Design 15

b) Interpretivism

Interpretivism focuses primarily on the understanding of that which is being studied (Olivier,

2009). This philosophy advocates that the researcher should understand the differences between

conducting research among human beings, rather than objects. This implies interpreting the

meaning and actions of actors according to their own subjective frame of reference, with as little

generalisation as possible, even though avoiding generalisation is nearly impossible in any kind

of research (William, 2000:2).

c) Realism

Realism advocates that objects exist independently of our knowledge of their existence. The

essence of realism is that there is a reality quite independent of the mind. This philosophy

assumes a scientific approach to the development of knowledge. This assumption underpins the

collection and understanding of data (Saunders et al., 2009).

d) Positivism

Positivism advocates working with an observable social reality. This philosophy emphasises on

highly structured methodologies to facilitate replication. It argues that the purpose of science is

simply to stick to what can be observed and measured. Any knowledge beyond this is impossible,

according to the positivist philosophy (Trochim, 1996). The end product of positivism is therefore

generalisations, similar to those produced by the physical and natural scientists.

Table 2.1 summarises the philosophical alternatives considered in this research and highlights

the one used.

_____________________________________________________________________ Chapter 2 – Research Methodology and Design 16

Table 2.1. Research philosophies

Positivism Realism Interpretivism Pragmatism

Ontology: The

researcher’s view

of the nature of

reality or being

External, objective

and independent of

social actors

Objective. Exists

independently of

human thoughts and

beliefs or knowledge

of their existence

Subjective. Socially

constructed

External, multiple view

chosen to best enable

answering of the

research question

Epistemology:

The researcher’s

view of what

constitutes

acceptable

knowledge

Focus on causality

and generalisations.

Only observable

phenomena can

provide credible data

Observable

phenomena provide

credible data, facts.

Subjective meanings

and social phenomena.

Focus upon the details

of a situation, the

reality behind these

details, and subjective

meanings motivating

actions

Either or both

observable phenomena

and subjective

meanings can provide

acceptable knowledge

depending on the

research question.

Axiology: The

researcher’s view

of the role of

values in research

Research undertaken

in a value-free way.

Researcher is

objective and

independent from data

Researcher is

biased by world

views, cultural

experiences and

upbringing.

Research is value

bound. Researcher is

part of is being

researched.

Values play a large role

in interpreting results.

Researcher’s view both

objective and

subjective

From an ontological point of view, the researcher’s view is mainly subjective. This view is

exemplified by the focus, during data analysis, on perceptions of respondents. From an

epistemological point of view, this research focuses mainly on the details of situations and

understanding the realities behind those details. This view is exemplified by the drive, during data

collection and analysis, to not only understand the state of the phenomena being studied, but also

gather as much insight as possible on why the human beings behind these phenomena act in the

way they do. From an axiology point of view, the researcher is actively involved in the research,

as opposed to being detached from it.

In line with the aim the drive, in this research, to interpret the meaning of data according to the

respondents own subjective perceptions, and the need to avoid generalisations as much as

possible, the interpretivist philosophy seems to be most appropriate. Table 2.1 contrasts the

above-mentioned research philosophies and highlights the one used for in this research.

2.1.6.2 Research approaches

Most research involves the use of theory (Saunders et al. 2009) and this research project is no

exception. This section discusses the options available for the research to relate to the theory.

The researcher has two alternatives. The first option is to develop a theory and related hypothesis

_____________________________________________________________________ Chapter 2 – Research Methodology and Design 17

(or hypotheses), and design an appropriate research method to test the theory and hypothesis;

the second option is to build the theory as a result of data collection and analysis. The first option

refers to the deductive approach, and the second one refers to the inductive approach (Saunders

et al. 2009). Both of these approaches are discussed, in an effort to identify the most appropriate

for the purpose of this research.

a) Deductive approach

Robson (2002) suggests that deductive approach follows five sequential steps, namely:

(i) Deducing the hypothesis from the theory; that is, developing the theory into a testable

proposition about the relationship between two or more concepts or variables.

(ii) Expressing the hypothesis in operational terms by indicating exactly how the

variables will be measured.

(iii) Testing the operational hypothesis through the appropriate research method(s)

(iv) Examine the specific results of the testing and determine whether they tend to

confirm or negate the theory.

(v) Depending on the findings in step IV, the theory may be modified if necessary.

These steps reflect several characteristics. First, there appears to be a focus on causal

relationships between variables. Secondly, these relationships are tested through the collection of

data which is most likely to be quantitative, even though Saunders et al. (2009) caution that this

data could also be qualitative; a third characteristic is that hypotheses needs to be tested within a

controlled environment to minimise the changes in how the different variables being tested relate

to each other. Additionally, Gill and Johnson (2002) advocate the use of a highly structured

methodology to facilitate replication and ensure reliability.

At this stage it can be said that scientific rigor behind the deductive approach requires the

researcher to be independent from what is being researched. The final characteristic transpiring

from this approach is the need to generalise the findings of the research. This need would be best

addressed if the sample selected is of sufficient numerical size.

In this specific research, a hypothesis would need to be made regarding whether project

managers adhered or not to the project management theory which they purport to follow. The

hypothesis would then be quantified in terms of what exactly is meant by “adhering to the theory”.

An example would be to clearly define whether “adherence” here refers to following the theory all

the time, or most of the time. The “project management theory” itself would also potentially be

broken down in just exactly what the term entails for the purpose of this research. This inquiry

_____________________________________________________________________ Chapter 2 – Research Methodology and Design 18

would need to be performed through an appropriate research method. Research methods are

further discussed later in this chapter.

b) Inductive approach

The inductive approach is concerned with developing the theory as a result of the observation of

empirical data (Saunders et al. 2009). While the deductive approach, discussed above, focuses

on the cause-effect link between particular variables, the inductive approach is wary of

developing such a cause-effect relationship without understanding the way in which human

beings interpret their social world (Saunders et al. 2009).

In this research project, it can be argued that treating project managers as human beings whose

adherence (or lack of) to the project management best practices professed within their

organisation is a more realistic approach. This approach opposes the deductive approach which

seems to insinuate that project managers are expected to respond in a mechanic way to certain

circumstances (in this case, adhering to professed project management best practices).

The methodology followed in inductive research is less rigid than the one typically used in the

deductive approach. This flexibility allows the researcher to find alternative explanations of what

is going on (Saunders et al., 2009). Research following inductive approach is likely to focus on

the context within which events happen. For this reason, it can be argued that when following the

inductive approach, samples tend to be small, as opposed to the typically large samples

recommended for the deductive approach (Easterby-Smith, Thorpe & Lowe, 2008).

It is necessary for the researcher to be clear on which research approach to follow in a particular

research project. This, according to Easterby-Smith et al (2008), is the case for three reasons:

Firstly, it enables the researcher to make an informed decision regarding the appropriate

research method and data collection and analysis technique to use in the research project.

Secondly, it helps the researcher to focus on the most appropriate research methods for the

purpose of the particular research project, thereby discarding the less appropriate methods.

Thirdly, understanding the alternative research approaches allow the researcher to adapt the

research design and methodologies to constraints faced by a particular research project. Such

constraints could include, but should not be limited to time, budget, and access to data.

While Easterby-Smith et al (2008) have proposed some benefits for making a clear choice on the

research approach, Cresswell (2003) suggests a number of practical criteria for making such

choice. The most important of these are that firstly, the nature of the research topic should be

taken into consideration when deciding which research approach to adopt; an established topic

on which abundant information is available might be more suitable for deductive than inductive

_____________________________________________________________________ Chapter 2 – Research Methodology and Design 19

approach. Secondly, the researcher should consider the time available to carry out the research

project. Deductive research can be quicker to complete and would typically require a single

iteration of data collection and analysis; the inductive approach, on the other hand, could be quite

protracted as the ideas, based on longer periods of data collection and analysis, tend to emerge

gradually. Thirdly, the researcher should determine the extent to which he or she wishes to

indulge in risk. A deductive approach potentially carries less risk, even though there are still some

non negligible risks, such as research subjects failing to return questionnaires. Inductive

approach, on the other hand, constantly carries the risk, despite multiple iterations, it may happen

that no useful data pattern or theory emerges.

It should be noted that the literature reflects some overlaps in the terminology. Cresswell

(2003:18) reflects such overlap when describing the main research approaches are (i) qualitative,

(ii) quantitative, and (iii) mixed approach. However, for the purpose of this research, deductive

and inductive are the research approaches used. Qualitative and quantitative are alternatives

which only play a role at the data collection and analysis stage (Saunders et al. 2009:11). Data

collection and analysis techniques are discussed later in this chapter.

The above discussion may convey the idea that a researcher needs to choose either of the

research approaches. However, Saunders et al (2009) disagree by arguing that a combined

approach in a single research project is both possible and advantageous in some cases. This

view is acknowledged, but for the purpose of this research, the combined approach is not used.

The alternative research approaches have been considered, including the selection criteria and

risks for either approach. The mixed approach has also been identified as possible and potentially

advantageous. For the purpose of this research the inductive approach will be followed.

Table 2.2 summarises the major differences between inductive and deductive approaches to

research, and highlights the approach followed in this research project.

_____________________________________________________________________ Chapter 2 – Research Methodology and Design 20

Table 2.2. Deductive vs. Inductive research approaches

Deduction emphasises Induction emphasises

1 Scientific principles Gaining an understanding of the meanings humans

attach to events.

2 Moving from theory to data Building the theory from empirical data

3 The need to explain causal relationships between variables A close understanding of the research context

4 The collection of mainly quantitative data The collection of mainly qualitative data

5 The application of controls to ensure the validity of data A more flexible structure to allow changes of research

emphasis as the research progresses

6 Researcher independence of what is being researched A realisation that the researcher is part of the research

process

7 The necessity to select large samples in order to generalise

conclusions

Small sample selections as there is less concern for the

need to generalise

The next section discusses research types.

2.1.6.3 Research types

Research types refer to how the research purpose is classified. For the purpose of this research,

“research type” and “research classification” are synonymous. Saunders et al (2009:139) identify

three main research types, depending on how the researcher intends to answer the research

question: exploratory, descriptive and explanatory. These authors argue that the research type is

tightly linked to the overall research purpose, and that a single research project can have multiple

purposes. This argument is echoed by Robson (2002), who points out that the purpose of a

research project may change over time.

Various research types are identified in the literature, including basic, applied and practical

research (Henrichsen, Smith & Baker, 1997a; Verma & Mallick, 1999:11; Miller & Salkind,

2002:3). Other research types identified in the literature include descriptive as opposed to

analytical, applied as opposed to basic (or fundamental) and conceptual as opposed to empirical

(Kothari, 2008).

Due to its specific link to the research purpose, this research focuses on the research types

proposed by Saunders et al (2009):

a) Exploratory research

This is a means of finding out what is happening, to seek out new insights, to ask questions and

to assess phenomena in new lights (Robson 2002:59). According to Saunders et al (2009), there

_____________________________________________________________________ Chapter 2 – Research Methodology and Design 21

are three main ways of conducting exploratory research, namely: searching the literature,

interviewing experts on the subject, and conducting focus group interviews. Exploratory research

is a research type which is flexible, yet does not lose direction. This means that this research type

typically starts with a broad focus, which tends to become progressively narrower as the research

progresses (Blankenship, Breen & Dutka, 1998:21; Saunders et al, 2009). While exploratory

research is a great way to seek new insights and establish greater understanding of the problem

at hand, it has an inherent risk of not delivering a definitive or conclusive answer to the research

problem (McGivern, 2006:88).

b) Descriptive research

This research type aims to portray an accurate profile of persons, events or situations (Robson,

2002:59). Descriptive research runs the risk of being perceived as not adding particular value,

unless the researcher goes further to evaluate and synthesise, and draw conclusions from the

data being described.

c) Explanatory research