9 october 2017 q2fy18 results preview - sakshi business · space, we reiterate our buy rating on...

TRANSCRIPT

Gradual path to recovery GST continues to drag earnings growth in second quarter but certain pockets of market like Auto, Cement & Metals & Mining showing early signs of pick up. Cement is expected to report double digit volume growth, which coupled with stable pricing will lead to healthy earnings growth amongst the larger players. Within the auto space, all the three Auto Ancillary stocks under coverage are expected to report strong growth. We expect higher YoY as well as QoQ earnings across the board from our metals & mining universe, led by favourable outcomes on three key areas – i) higher volumes, ii) higher realisations and iii) lower RM costs. We expect the Pharma sector to continue to report subdued numbers due to GST implementation & pricing pressure in the US generic market. Similarly, GST is expected to impact both broadcasters and print players as FMCG, Retail & Real estate companies cut advertising spends. We expect our banking universe to report modest growth in both NII / PAT following weak loan growth, NIM compression, lower other income (both fees and treasury gains) and accelerated provisioning. Our preferred picks are certain gems with strong future outlook like Tata Metaliks, Orient Refractories, Ramco Cement, JK Cement, Deccan Cement, Jagran Prakashan, FIEM Industries, Mayur Uniquoters, Aurobindo Pharma, Sanofi India & CARE.

Sector View: Outlook on the Metals & Mining universe to continue to remain positive on back of uptick in volumes, realizations & lower raw material costs. We expect our banking universe to report modest growth in both NII / PAT following weak loan growth, NIM compression, lower other income (both fees and treasury gains) and accelerated provisioning. For the Auto sector considering GST and BS-IV transitions are behind now, we believe 2HFY18 will witness stronger performance from CVs whereas PVs and 2Ws are likely to benefit on account of good monsoon progression, government focus on rural India and 7th pay commission. We continue to remain positive on the cement sector and expect companies under coverage to report double digit volume growth on YoY basis, however EBIDTA growth would remain under check due to cost pressures. In the media sector GST is expected to impact all players due to cut in ad spends across categories. We expect the pharma sector to remain under pressure due to GST implementation and pricing pressure in the US market.

Earnings: Within the metal & mining space we expect strong YoY earnings growth from HZL/Vedanta/JSW among largecaps and Graphite/Tata Sponge/Tata Metaliks in midcaps. We expect weak results from IFGL and Ratnamani. On account of good volume growth across different segments, Fiem, Mayur Uniquoters & Swaraj Engine are likely report strong numbers in this quarter. We expect a positive earnings surprise from Karnataka Bank in the banking space & GIC Housing Finance in the NBFC space. We expect micro-lending institutions to report weak NII growth / report losses for the quarter. In consumer companies we expect IFB Industries & Mirza to post healthy revenue growth, while the Dish TV could disappoint on both subscriber addition & ARPU. Within the cement sector we expect strong EBITDA growth from ACC & Ambuja in the large cap space and Star cement in the mid cap space. From the pharma space we expect a positive earnings surprise from Dr. Reddy’s Labs & Aurobindo Pharma.

Valuations: The quarter gone by was another strong quarter for Indian and global indices, with both BSE midcap and smallcap indices registering 5% return with the gush of domestic liquidity finding its way to the equity market & leading to multiple expansions across sectors and ideas. We like within the metals space stocks like Hindalco/Vedanta in largecaps and Orient Refractories/Tata Metaliks in midcaps. In the cement space we like JK Cement and the two south-India based cement companies, TRCL & Deccan Cement. In the Auto space we like Fiem Industries and Mayur uniquoters. In the media/consumer space we like Jagran Prakashan, La opala & Info edge. From the banking space, we like ICICI Bank/SBI in largecaps, Karnataka Bank in midcaps. Our Top Sells remain as M&M Financials, JK Lakshmi Cement & Orient Cement.

Positive earnings surprise

Y/E Mar (Rs mn) EBITDA

Q2FY18E YoY (%) QoQ (%)

Hindustan Zinc 30,570 47.2 28.2 Vedanta 61,454 31.8 26.1 JSW Steel 32,873 11.1 25.6 Graphite India 807 472.6 127.2 Tata Sponge 432 154.9 11.8 Tata Metaliks 672 47.4 35.7 Karnataka Bank 3192 37.2 3.1 GICHF 808 36.0 (8.6) Orient Cement 873 426.5 (25.3) ACC 3,831 40.0 (39.8) Ambuja Cement 4,155 15.9 (17.7) Star Cement 821 39.4 (48.3) IFB Industries 403 22.9 92.8 Mirza International 497 31.5 13.7 Abbott India 1,260 19.0 104.5 Aurobindo Pharma 10,265 10.5 22.0 Marksans Pharma 330 NA 13.8 Sanofi India 1,805 24.7 56.4

Source: Companies, Centrum Research Estimate, #PPOP

Negative earnings surprise

Y/E Mar (Rs mn) EBITDA

Q2FY18E YoY (%) QoQ (%)

IFGL Refactories 277 (5.0) 12.6 Ratnamani Metals 534 3.1 13.4 Shree Cement 4,382 (33.2) (35.6) Ramco Cements 2,223 (27.6) (11.8) Dish TV 2,102 (20.5) 4.5 ENIL 267 15.6 60.1 DB Corp 1,440 (4.3) (22.7) Sun Pharma 15,090 (52.4) 37.7 FDC 730 (12.4) 105.6

Source: Companies, Centrum Research Estimates

Top Buys Co. Name Rating CMP* (Rs) TP (Rs)

JK Cements Buy 972 1,310

Star Cement Buy 104 152 Ramco Cements Buy 705 820

FIEM Industries Buy 916 1,260

Mayur Uniquoters Buy 383 435

SUN TV Buy 780 840

Jagran Prakashan Buy 177 235

Info Edge Buy 1,060 1,090

Dish TV Buy 71 96

Aurobindo Pharma Buy 746 970 Sanofi India Buy 4,076 4,900

Orient Refractories Buy 149 170

Tata Metaliks Buy 717 890

Source: Centrum Research, *as on 6 October 2017

Top Sells Co. Name Rating CMP* (Rs) TP (Rs)

Ambuja Sell 279 200

JK Lakshmi Sell 395 360

Orient Cement Sell 155 114

Shree Cement Sell 18,775 13,340 Glaxo SmithKline Pharma Sell 2,415 1,390

MMFS Sell 419 250

Source: Centrum Research, *as on 6 October 2017

Centrum Equity Research Team +91 22 4215 9000

9 October 2017

INDIA

Q2FY18 Results Preview

In the interest of timeliness, this document is not edited.

Centrum Equity Research is available on Bloomberg, Thomson Reuters and FactSet

2 Q2FY18 Results Preview

Table of Contents

Cement & Building materials .......................................................................................................................................... 3

Financials ........................................................................................................................................................................... 12

Media / Consumer ......................................................................................................................................................... 21

Metals & Mining .............................................................................................................................................................. 27

Pharmaceuticals ............................................................................................................................................................. 35

Miscellaneous .................................................................................................................................................................. 46

Volume growth momentum picking up We expect aggregate EBITDA of the cement companies under our coverage to rise 6% YoY in Q2FY18 led by strong 12% YoY volume growth and 2% NSR increase amid 4% YoY cost inflation. Companies in the north and east markets have registered strong volume during the quarter. We expect strong EBITDA growth by Orient Cement, ACC, Ambuja Cements and Star Cement. Weak demand in south (ex-AP/Telangana should lead to YoY EBITDA decline for Ramco Cements and Deccan Cements under our coverage). We also estimate sharp EBIDTA fall YoY for Shree Cement. In the building materials segment, we expect Visaka Ind (VIL) to sustain its strong margin YoY.

Aggregate volume of companies under coverage to grow 12% YoY: We estimate strong industry sales in Q2FY18, driven by increased offtake in the north markets and continued demand momentum in the eastern and AP/Telangana markets. West and central markets sales are expected to be flat/marginally down YoY. In south, poor offtake in Tamil Nadu and Kerala markets continues to hurt overall growth. Thus the aggregate sales volume of the 10 companies under our coverage is expected to rise 12% YoY. We estimate strong 10%+ YoY volume growth from UltraTech, ACC, Ambuja, JK Cement, and JK Lakshmi. Star Cement’s volume dipped 23% YoY in Q2FY18 as the company has been cutting sales outside NE region (low margin business).

Aggregate EBITDA to rise 6% YoY: We expect average cement NSR (net of GST benefits) of companies in north/central/eastern regions to decline ~5%/3%/4% QoQ and by ~1%/3% QoQ in the west/south regions. Thus, average pan-India NSR should be lower by ~2% QoQ (seasonal impact of good monsoon across most parts in India). Thus, we expect average NSR of the 10 companies under our coverage to fall 2% QoQ but to rise 2% YoY. However, in our view, aggregate opex of these 10 companies should rise 4% YoY owing to higher fuel and diesel prices YoY (even though these have flattened on QoQ basis) despite operating leverage gains. Hence, unitary EBITDA should moderate 4% YoY to Rs859/MT. Among the covered companies, we estimate Orient Cement to see maximum upswing in its EBITDA (427% YoY on low base of last year), followed by 35%+ YoY increase in EBITDA of ACC, Ambuja and Star Cement. We estimate 27%+ EBITDA decline in case of Shree Cement and Ramco Cements and 14% YoY EBITDA fall for Deccan Cement.

Other building products – Visaka’s strong margin to sustain during the quarter: We expect sales uptick in ACS roofing business should boost building product segment margin amid lower offtake in textiles. Thus, we estimate VIL to deliver a modest 2% YoY EBITDA decline on the high base of last year. Lower tax, however, should aid 6% YoY PAT growth.

Stock recommendations: In our view, cement demand should remain buoyant led by sustained government led projects and good monsoon for second consecutive year. These alongwith slowing pace of new capacity addition and increased industry consolidation should boost pricing power. Thus, industry’s margin should expand despite fuel/freight inflation. GST is also expected to reduce logistics cost for the cement sector. In the large cap space, we like the market leader – UltraTech (strong volume growth visibility for next 2-3 years alongwith efficient cost structure) and recommend Buy on declines. In the mid cap space, we reiterate our Buy rating on Ramco Cements and Deccan Cement (debt free, superior return ratios, strong free cashflow outlook), Star Cement (leadership presence in lucrative NE region, strong return ratios). We remain negative on Shree Cement (expensive valuations), Ambuja Cements (expensive valuations amid limited growth outlook), JK Lakshmi and Orient Cement (both have large ongoing/expected capex to keep leverage at elevated levels). Even ACC would suffer on volume growth next year onwards. We continue to like VIL on account of its steady operational performance and growth outlook across all its three business segments.

Stock Price Performance (%)*

Company Name 1M 3 M 6 M 12 M

ACC (3.7) 8.1 16.8 6.7

Ambuja Cements (1.4) 10.0 14.5 10.3

Deccan Cement 0.0 0.4 (3.3) 8.3

JK Cements (4.6) 0.4 5.0 6.8

JK Lakshmi (7.8) (16.0) (12.8) (22.2)

Orient Cement (5.2) 0.1 6.9 (30.1)

Ramco Cements (2.2) (0.1) 5.0 13.4

Shree Cement 2.4 2.2 6.7 6.9

Star Cement (8.6) (17.1) (1.4) 35.6

UltraTech Cement (5.3) (4.1) (4.4) (0.7)

Visaka industries (VIL) 6.2 31.7 121.2 278.5

Nifty 0.6 3.2 7.7 14.6

Source: Bloomberg; * as on 06 October 2017

Current Rating and Target Prices

Company Name Rating *CMP (Rs) TP (Rs)

ACC Hold 1,740 1,520

Ambuja Cement Sell 279 200

Deccan Cement Buy 572 740

JK Cements Buy 972 1,310

JK Lakshmi Sell 395 360

Orient Cement Sell 155 114

Ramco Cements Buy 705 820

Shree Cement Sell 18,775 13,340

Star Cement Buy 104 152

UltraTech Cement Hold 3931 3,790

Visaka industries (VIL) Buy 709 620

Source: Centrum Research Estimates, * as on 06 October 2017

Rajesh Kumar Ravi, [email protected]; 91 22 4215 9643 Vinay Menon, [email protected]; 91 22 4215 9141

Quarterly Estimates Summary

Y/E Mar (Rs mn) Net Sales (Rs mn) EBITDA (Rs mn) EBITDA Margin (%) Adj. PAT (Rs mn)

Q2FY18E YoY (%) QoQ (%) Q2FY18E YoY (%) QoQ (%) Q2FY18E YoY (pp) QoQ (pp) Q2FY18E YoY (%) QoQ (%)

ACC ** 29,801 18.2 (13.7) 3,831 40.0 (39.8) 12.9 2.0 (5.6) 1,515 84.7 (53.6) Ambuja ** 23,554 15.9 (17.7) 4,155 37.1 (36.2) 17.6 2.7 (5.1) 3,625 30.8 (7.6) Deccan Cement 1,323 3.6 (2.4) 233 (14.3) (5.2) 17.6 (3.7) (0.5) 110 (18.2) (3.3) JK Cement 10,761 16.5 3.3 1,792 12.8 (9.4) 16.7 (0.6) (2.3) 564 37.9 (28.9) JK Lakshmi 7,714 17.7 (14.4) 928 (0.9) (22.9) 12.0 (2.3) (1.3) 116 (53.6) (59.1) Orient Cement 5,068 31.7 (10.8) 873 426.5 (25.3) 17.2 12.9 (3.3) 176 (54.7) Ramco Cements 9,610 (0.9) (3.0) 2,223 (27.6) (11.8) 23.1 (8.5) (2.3) 1,338 (35.4) (14.1) Shree Cement 20,936 4.3 (17.5) 4,382 (33.2) (35.6) 20.9 (11.8) (5.9) 1,964 (32.6) (55.4) Star Cement 2,708 (18.6) (36.8) 821 39.4 (48.3) 30.3 12.6 (6.7) 237 5,835.9 (77.9) UltraTech Cement 63,850 17.0 (3.6) 12,987 12.5 (16.8) 20.3 (0.8) (3.2) 4,203 (30.1) (52.8) Aggregate 1,75,325 13.7 (10.3) 32,225 5.7 (26.7) 18.4 (1.4) (4.1) 17,814 (15.6) (45.2) Visaka Industries 1,939 (3.2) (37.3) 260 (1.7) (44.4) 13.4 0.2 (1.7) 94 6.4 (59.3)

Source: Companies, Centrum Research Estimates Note: ** Y/E Dec (Data for Q3CY17E)

INDIA

Cement & Building materials 9 October 2017

.

Centrum Equity Research is available on Bloomberg, Thomson Reuters and FactSet

4 Q2FY18 Results Preview

Exhibit 1: Estimates Summary – Cement Companies

Company Rating CMP*

(Rs) TP (Rs) Adj EPS (Rs) EV/EBITDA (x) EV/MT (USD) RoCE (%)

FY17 FY18E FY19E FY17 FY18E FY19E FY17 FY18E FY19E FY17 FY18E FY19E

ACC Hold 1,740 1,520 34.2 43.6 62.3 18.0 16.7 13.0 123 144 140 7.3 9.1 12.4

Ambuja Cement Sell 279 200 4.9 7.0 8.4 15.0 21.8 18.2 131 212 211 6.7 7.2 8.3

Deccan Cement Buy 572 740 33.3 40.2 55.5 6.8 6.8 4.8 46 51 46 11.5 12.7 15.9

JK Cements Buy 972 1,310 35.4 55.2 79.8 10.5 10.3 8.0 87 100 92 8.9 11.1 13.7

JK Lakshmi Sell 395 360 7.0 11.0 19.7 17.5 13.2 10.0 90 88 84 7.8 7.3 9.4

Orient Cement Sell 155 114 (1.6) 6.2 6.1 25.1 13.2 10.0 86 89 87 1.4 7.7 7.0

Ramco Cements Buy 705 820 27.3 35.4 43.5 13.9 13.5 10.9 154 181 175 11.9 14.7 16.3

Shree Cement Sell 18,775 13,340 384.4 507.4 484.0 21.4 21.8 18.2 286 351 248 19.4 21.0 17.0

Star Cement Buy 104 152 4.1 6.9 7.8 9.5 8.4 6.9 177 191 127 12.0 16.5 17.0

UltraTech Cement Hold 3931 3,790 96.2 103.6 147.2 19.3 18.4 13.5 218 209 193 9.0 9.1 10.1

Source: Companies, Centrum Research Estimates, * as on 06 October 2017, (1USD= Rs65)

Exhibit 2: Estimates Summary – Other Building Materials

Company Rating CMP* (Rs) TP (Rs) Adj EPS (Rs) EV/EBITDA (x) P/E (x) RoCE (%)

FY17 FY18E FY19E FY17 FY18E FY19E FY17 FY18E FY19E FY17 FY18E FY19E

Visaka Ind BUY 709 620 32.1 34.0 40.9 4.0 10.3 8.6 5.7 20.9 17.4 8.4 9.3 10.5

Source: Companies, Centrum Research Estimates, * as on 06 October 2017

,,

Exhibit 3: Operational Estimates for Cement Companies

Y/E Mar (Rs mn) Sales Volume (mn MT) NSR (Rs/ MT) EBITDA (Rs/ MT))

Q2FY18E YoY (%) QoQ (%) Q2FY18E YoY (%) QoQ (%) Q2FY18E YoY (%) QoQ (%)

ACC ** 5.85 15.4 (13.2) 4,700 3.0 (2.2) 623 21.3 (31.9)

Ambuja Cement** 5.10 11.1 (16.0) 4,619 4.4 (2.0) 815 23.4 (24.0)

Deccan Cement 0.34 - (0.4) 3,890 3.6 (2.0) 685 (14.3) (4.8)

JK Cement 2.20 14.6 3.5 4,887 1.6 (0.2) 814 (1.6) (12.4)

JK Lakshmi 1.96 13.9 (14.4) 3,944 3.3 - 474 (13.0) (9.9)

Orient Cement 1.26 7.2 (10.0) 4,028 22.9 (0.9) 694 391.3 (17.0)

Ramco Cements 2.13 4.6 (1.0) 4,515 (5.3) (2.0) 1,044 (30.8) (11.0)

Shree Cement 4.96 8.5 (15.7) 4,021 1.2 (3.0) 869 (33.2) (25.0)

Star Cement 0.47 (23.0) (33.4) 5,471 8.8 (3.0) 1,735 80.9 (22.3)

UltraTech Cement 12.96 15.9 (1.7) 4,926 0.9 (2.0) 1,002 (3.0) (15.3)

Aggregate 37.23 12.1 (9.0) 4,618 2.3 (1.7) 859 (4.1) (19.8)

Source: Companies, Centrum Research Estimates, **Q3CY17. For JK Cement and UltraTech, Sales volume, NSR and EBITDA/Mt are blended numbers (Grey+White)

5 Q2FY18 Results Preview

Major input costs trends during Q2FY18

Exhibit 4: Crude price (Brent) up 2% QoQ, +11% YoY Exhibit 5: Diesel prices up 1% QoQ and up 7% YoY

Source: Bloomberg, Centrum Research Source: Bloomberg, Centrum Research

Exhibit 6: Domestic petcoke price were flat QoQ but were 17% higher YoY in Q2FY18

Exhibit 7: Indonesian coal is down 4% QoQ, but is still higher by 40% YoY

Source: Bloomberg, Centrum Research Source: Bloomberg, Centrum Research

Exhibit 8: Domestic HR Coil prices (used for Pre Engg Buildings) down 1% QoQ but is higher by 24% YoY

Source: Industry, Centrum Research

20

30

40

50

60

70

Jan

-15

Ap

r-15

Jul-1

5

Oct

-15

Jan

-16

Ap

r-16

Jul-1

6

Oct

-16

Jan

-17

Ap

r-17

Jul-1

7

Oct

-17

USD

/Bb

l

Brent

40

45

50

55

60

65

Jan

-15

Ap

r-15

Jul-1

5

Oct

-15

Jan

-16

Ap

r-16

Jul-1

6

Oct

-16

Jan

-17

Ap

r-17

Jul-1

7

Oct

-17

Rs/K

G

Diesel prices

3,000

4,000

5,000

6,000

7,000

8,000

Jan

-15

Ap

r-15

Jul-1

5

Oct

-15

Jan

-16

Ap

r-16

Jul-1

6

Oct

-16

Jan

-17

Ap

r-17

Jul-1

7

Oct

-17

Rs/M

T

Domestic Petcoke

3,000

4,000

5,000

6,000

7,000

8,000Ja

n-1

5

Ap

r-15

Jul-1

5

Oct

-15

Jan

-16

Ap

r-16

Jul-1

6

Oct

-16

Jan

-17

Ap

r-17

Jul-1

7

Oct

-17

Rs/M

T

Indonesian Coal

20,000

25,000

30,000

35,000

40,000

45,000

Jan

-15

Ap

r-15

Jul-1

5

Oct

-15

Jan

-16

Ap

r-16

Jul-1

6

Oct

-16

Jan

-17

Ap

r-17

Jul-1

7

Oct

-17

Domestic ex-mill HRC (Rs/MT)

6 Q2FY18 Results Preview

Building Materials - Cement

ACC (Rating: HOLD; Target price: Rs1,520)

Exhibit 9: Result Expectation - Consolidated

Particulars Q3CY17E Q3CY16 YoY (%) Q2CY17 QoQ (%)

Sales Volume (mn MT) 5.9 5.1 15.4 6.7 (13.2)

NSR (Rs/MT) 4,700 4,562 3.0 4,805 (2.2)

Sales (Rs mn) 29,801 25,215 18.2 34,533 (13.7)

EBITDA (Rs mn) 3,831 2,737 40.0 6,369 (39.8)

EBITDA margin (%) 12.9 10.9 200bps 18.4 (559)bps

EBITDA (Rs/MT) 623 513 21.3 914 (31.9)

Net profit (Rs mn) 1,515 820 84.7 3,262 (53.6)

Adj PAT margin (%) 5.1 3.3 183bps 9.4 (436)bps

Source: Company, Centrum Research Estimates

We expect ACC to deliver strong earnings growth during the quarter led by good ramp up in east sales. We estimate overall volume to increase 15% YoY. We also estimate 3% NSR increase YoY.

We expect higher NSR and volume YoY to boost unitary EBITDA by 21% YoY to Rs623/MT.

Thus, these should drive consolidated revenue/ EBITDA/PAT growth of 18%/40%/85% YoY.

Ambuja Cements (Rating: SELL; Target price: Rs200)

Exhibit 10: Result Expectation - Standalone Particulars Q3CY17E Q3CY16 YoY (%) Q2CY17 QoQ (%)

Sales Volume (mn MT) 5.10 4.6 11.1 6.1 (16.0)

NSR (Rs/MT) 4,619 4,426 4.4 4,714 (2.0)

Sales (Rs mn) 23,554 20,314 15.9 28,613 (17.7)

EBITDA (Rs mn) 4,155 3,032 37.1 6,510 (36.2)

EBITDA margin (%) 17.6 14.9 272bps 22.8 (511)bps

EBITDA (Rs/MT) 815 660 23.4 1,073 (24.0)

Net profit (Rs mn) 3,625 2,770 30.8 3,922 (7.6)

Adj PAT margin (%) 15.4 13.6 175bps 13.7 168bps

Source: Company, Centrum Research Estimates

Buoyed by higher demand in the north and east markets, we expect Ambuja’s sales volume to rise 11% YoY. Strong price recovery in the west and east markets should drive 4% NSR growth YoY.

Thus, we estimate unitary EBITDA to rise 23% YoY to Rs815/MT. We factor in a modest 1% cost inflation as operating leverage gain should offset input/freight cost inflation.

Subsequently, we expect its standalone Net sales/EBITDA/PAT to grow 16%/37%31% YoY.

7 Q2FY18 Results Preview

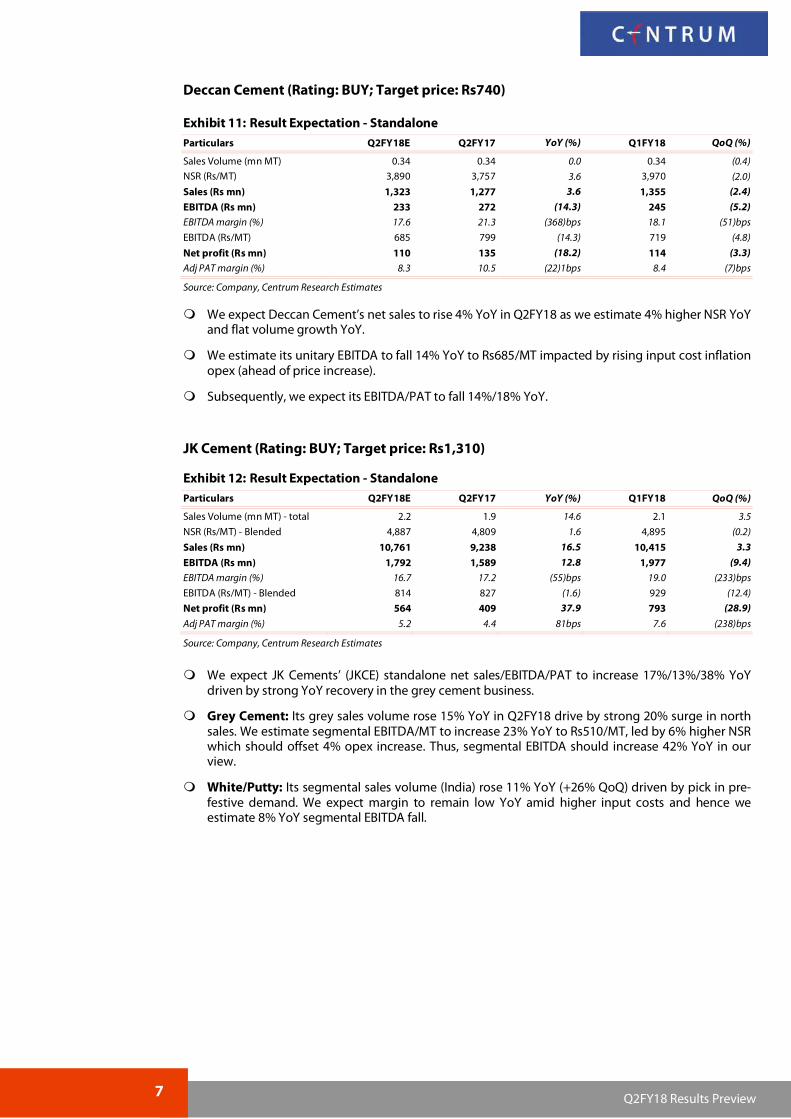

Deccan Cement (Rating: BUY; Target price: Rs740)

Exhibit 11: Result Expectation - Standalone Particulars Q2FY18E Q2FY17 YoY (%) Q1FY18 QoQ (%)

Sales Volume (mn MT) 0.34 0.34 0.0 0.34 (0.4)

NSR (Rs/MT) 3,890 3,757 3.6 3,970 (2.0)

Sales (Rs mn) 1,323 1,277 3.6 1,355 (2.4)

EBITDA (Rs mn) 233 272 (14.3) 245 (5.2)

EBITDA margin (%) 17.6 21.3 (368)bps 18.1 (51)bps

EBITDA (Rs/MT) 685 799 (14.3) 719 (4.8)

Net profit (Rs mn) 110 135 (18.2) 114 (3.3)

Adj PAT margin (%) 8.3 10.5 (22)1bps 8.4 (7)bps

Source: Company, Centrum Research Estimates

We expect Deccan Cement’s net sales to rise 4% YoY in Q2FY18 as we estimate 4% higher NSR YoY and flat volume growth YoY.

We estimate its unitary EBITDA to fall 14% YoY to Rs685/MT impacted by rising input cost inflation opex (ahead of price increase).

Subsequently, we expect its EBITDA/PAT to fall 14%/18% YoY.

JK Cement (Rating: BUY; Target price: Rs1,310)

Exhibit 12: Result Expectation - Standalone Particulars Q2FY18E Q2FY17 YoY (%) Q1FY18 QoQ (%)

Sales Volume (mn MT) - total 2.2 1.9 14.6 2.1 3.5

NSR (Rs/MT) - Blended 4,887 4,809 1.6 4,895 (0.2)

Sales (Rs mn) 10,761 9,238 16.5 10,415 3.3

EBITDA (Rs mn) 1,792 1,589 12.8 1,977 (9.4)

EBITDA margin (%) 16.7 17.2 (55)bps 19.0 (233)bps

EBITDA (Rs/MT) - Blended 814 827 (1.6) 929 (12.4)

Net profit (Rs mn) 564 409 37.9 793 (28.9)

Adj PAT margin (%) 5.2 4.4 81bps 7.6 (238)bps

Source: Company, Centrum Research Estimates

We expect JK Cements’ (JKCE) standalone net sales/EBITDA/PAT to increase 17%/13%/38% YoY driven by strong YoY recovery in the grey cement business.

Grey Cement: Its grey sales volume rose 15% YoY in Q2FY18 drive by strong 20% surge in north sales. We estimate segmental EBITDA/MT to increase 23% YoY to Rs510/MT, led by 6% higher NSR which should offset 4% opex increase. Thus, segmental EBITDA should increase 42% YoY in our view.

White/Putty: Its segmental sales volume (India) rose 11% YoY (+26% QoQ) driven by pick in pre-festive demand. We expect margin to remain low YoY amid higher input costs and hence we estimate 8% YoY segmental EBITDA fall.

8 Q2FY18 Results Preview

JK Lakshmi Cement (Rating: SELL; Target price: Rs360)

Exhibit 13: Result Expectation - Standalone Particulars Q2FY18E Q2FY17 YoY (%) Q1FY18 QoQ (%)

Sales Volume (mn MT) 2.0 1.7 13.9 2.3 (14.4)

NSR (Rs/MT) 3,944 3,816 3.3 3,944 0.0

Sales (Rs mn) 7,714 6,556 17.7 9,011 (14.4)

EBITDA (Rs mn) 928 937 (0.9) 1,203 (22.9)

EBITDA margin (%) 12.0 14.3 (226)bps 13.4 (132)bps

EBITDA (Rs/MT) 474 545 (13.0) 527 (9.9)

Net profit (Rs mn) 116 249 (53.6) 283 (59.1)

Adj PAT margin (%) 1.5 3.8 (230)bps 3.1 (164)bps

Source: Company, Centrum Research Estimates

We expect JK Lakshmi Cement’s net sales to rise 18% YoY in Q2FY18 led by strong 14% volume growth and 3% higher NSR YoY. In our view, its volume growth should benefit from higher sales in north and east markets.

Unitary EBITDA should fall 13% YoY to Rs474/MT driven by higher opex. Thus, we expect EBITDA to fall marginally by 1% YoY.

We estimate PAT to decline 54% YoY driven by higher capital charges and higher tax outgo.

Orient Cement (Rating: SELL; Target price: Rs114)

Exhibit 14: Result Expectation - Standalone Particulars Q2FY18E Q2FY17 YoY (%) Q1FY18 QoQ (%)

Sales Volume (mn MT) 1.3 1.2 7.2 1.4 (10.0)

NSR (Rs/MT) 4,028 3,278 22.9 4,065 (0.9)

Sales (Rs mn) 5,068 3,848 31.7 5,682 (10.8)

EBITDA (Rs mn) 873 166 426.5 1,169 (25.3)

EBITDA margin (%) 17.2 4.3 1,292bps 20.6 (334)bps

EBITDA (Rs/MT) 694 141 391.3 836 (17.0)

Net profit (Rs mn) 176 (294) 389 (54.7)

Adj PAT margin (%) 3.5 (7.6) 1,112bps 6.9 (337)bps

Source: Company, Centrum Research Estimates

We expect Orient Cement’s net sales to rise 32% YoY in Q2FY18 as we factor in 7% YoY volume increase (-10% QoQ) and 23% higher NSR YoY (-1% QoQ).

We expect its unitary cost to rise 6% YoY. However, a strong NSR on last year’s low base should lead to unitary EBITDA increasing 391% to Rs694/MT. Hence, we estimate EBITDA to rebound 427% YoY.

Thus, buoyed by strong operating results, we expect the company to report PAT of Rs176mn vs. a loss of Rs294mn YoY.

9 Q2FY18 Results Preview

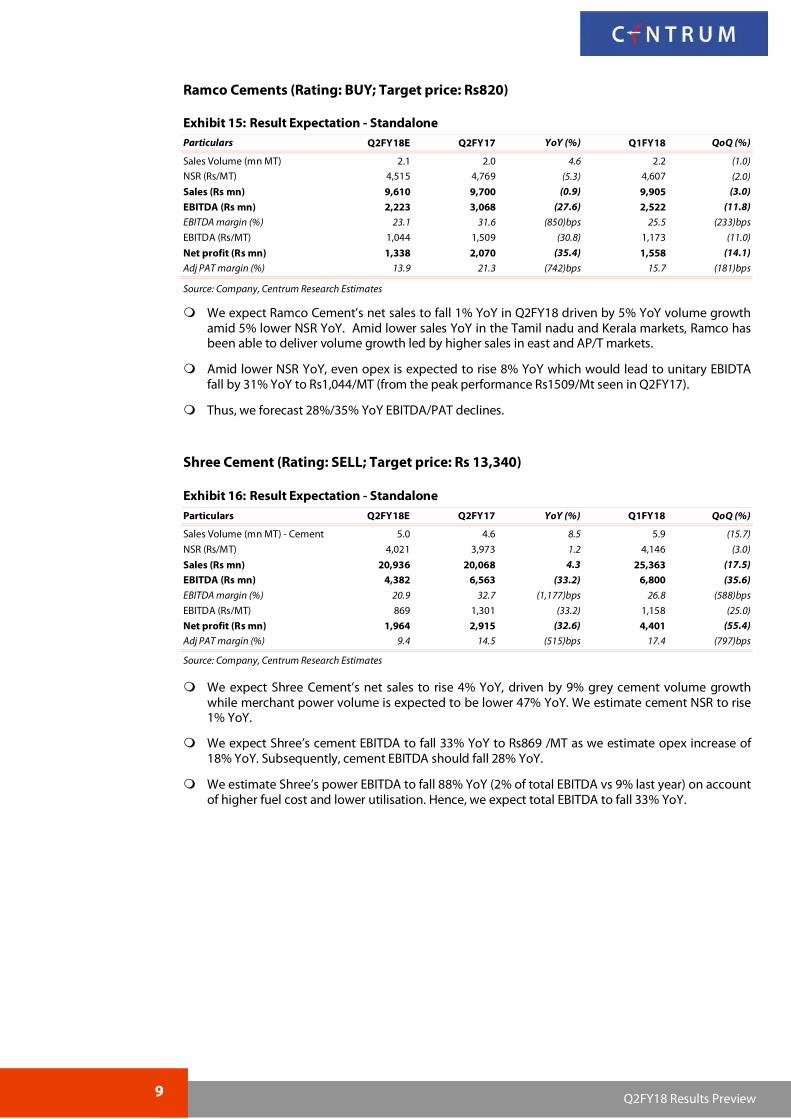

Ramco Cements (Rating: BUY; Target price: Rs820)

Exhibit 15: Result Expectation - Standalone Particulars Q2FY18E Q2FY17 YoY (%) Q1FY18 QoQ (%)

Sales Volume (mn MT) 2.1 2.0 4.6 2.2 (1.0)

NSR (Rs/MT) 4,515 4,769 (5.3) 4,607 (2.0)

Sales (Rs mn) 9,610 9,700 (0.9) 9,905 (3.0)

EBITDA (Rs mn) 2,223 3,068 (27.6) 2,522 (11.8)

EBITDA margin (%) 23.1 31.6 (850)bps 25.5 (233)bps

EBITDA (Rs/MT) 1,044 1,509 (30.8) 1,173 (11.0)

Net profit (Rs mn) 1,338 2,070 (35.4) 1,558 (14.1)

Adj PAT margin (%) 13.9 21.3 (742)bps 15.7 (181)bps

Source: Company, Centrum Research Estimates

We expect Ramco Cement’s net sales to fall 1% YoY in Q2FY18 driven by 5% YoY volume growth amid 5% lower NSR YoY. Amid lower sales YoY in the Tamil nadu and Kerala markets, Ramco has been able to deliver volume growth led by higher sales in east and AP/T markets.

Amid lower NSR YoY, even opex is expected to rise 8% YoY which would lead to unitary EBIDTA fall by 31% YoY to Rs1,044/MT (from the peak performance Rs1509/Mt seen in Q2FY17).

Thus, we forecast 28%/35% YoY EBITDA/PAT declines.

Shree Cement (Rating: SELL; Target price: Rs 13,340)

Exhibit 16: Result Expectation - Standalone Particulars Q2FY18E Q2FY17 YoY (%) Q1FY18 QoQ (%)

Sales Volume (mn MT) - Cement 5.0 4.6 8.5 5.9 (15.7)

NSR (Rs/MT) 4,021 3,973 1.2 4,146 (3.0)

Sales (Rs mn) 20,936 20,068 4.3 25,363 (17.5)

EBITDA (Rs mn) 4,382 6,563 (33.2) 6,800 (35.6)

EBITDA margin (%) 20.9 32.7 (1,177)bps 26.8 (588)bps

EBITDA (Rs/MT) 869 1,301 (33.2) 1,158 (25.0)

Net profit (Rs mn) 1,964 2,915 (32.6) 4,401 (55.4)

Adj PAT margin (%) 9.4 14.5 (515)bps 17.4 (797)bps

Source: Company, Centrum Research Estimates

We expect Shree Cement’s net sales to rise 4% YoY, driven by 9% grey cement volume growth while merchant power volume is expected to be lower 47% YoY. We estimate cement NSR to rise 1% YoY.

We expect Shree’s cement EBITDA to fall 33% YoY to Rs869 /MT as we estimate opex increase of 18% YoY. Subsequently, cement EBITDA should fall 28% YoY.

We estimate Shree’s power EBITDA to fall 88% YoY (2% of total EBITDA vs 9% last year) on account of higher fuel cost and lower utilisation. Hence, we expect total EBITDA to fall 33% YoY.

10 Q2FY18 Results Preview

Star Cement (Rating: BUY; Target price: Rs 152)

Exhibit 17: Result Expectation - Consolidated

Particulars Q2FY18E Q2FY17 YoY (%) Q1FY18 QoQ (%)

Sales Volume (mn MT) - external 0.5 0.6 (23.0) 0.7 (33.4)

NSR (Rs/MT) 5,471 5,027 8.8 5,640 (3.0)

Sales (Rs mn) 2,708 3,328 (18.6) 4,287 (36.8)

EBITDA (Rs mn) 821 589 39.4 1,586 (48.3)

EBITDA margin (%) 30.3 17.7 1,261bps 37.0 (670)bps

EBITDA (Rs/MT) 1,735 959 80.9 2,234 (22.3)

Net profit (Rs mn) 237 4 5,835.9 1,075 (77.9)

Adj PAT margin (%) 8.8 0.1 864bps 25.1 (1,630)bps

Source: Company, Centrum Research Estimates

We expect Star Cement’s consolidated net sales to fall 19% YoY driven by 23% YoY fall in sales volume. Volume decline is driven by both lower sales in NE region as well as Star’s sales reduction outside NE region where margin is lower vs NE region sales.

Amid weak offtake, NSR should increase 9% YoY, owing to strong price rebound across east and NE region YoY. Further, unitary opex should also reduce 8% YoY boosted by lower fuel cost, overhead cost rationalisation and lead distance reduction (ie fall in outside NE region sales).

Thus, we estimate unitary EBIDTA to soar 81% YoY to Rs1735/MT, thus boosting consolidated EBITDA growth by 39%. On a low base of last year, PAT should zoom 58x YoY.

UltraTech Cement (Rating: Hold; Target price: Rs3,790)

Exhibit 18: Result expectation - Standalone Particulars Q2FY18E Q2FY17 YoY (%) Q1FY18 QoQ (%)

Sales Volume (mn MT) 13.0 11.2 15.9 13.2 (1.7)

NSR (Rs/MT) 4,926 4,883 0.9 5,026 (2.0)

Sales (Rs mn) 63,850 54,589 17.0 66,265 (3.6)

EBITDA (Rs mn) 12,987 11,548 12.5 15,601 (16.8)

EBITDA margin (%) 20.3 21.2 (81)bps 23.5 (320)bps

EBITDA (Rs/MT) 1,002 1,033 (3.0) 1,183 (15.3)

Net profit (Rs mn) 4,203 6,011 (30.1) 8,906 (52.8)

Adj PAT margin (%) 6.6 11.0 (443)bps 13.4 (686)bps

Source: Company, Centrum Research Estimates

We expect UltraTech Cement’s standalone sales volume to soar 16% YoY driven by both organic volume uptick and impact of JPA amalgamation. We estimate NSR to increase 1% YoY. Thus, net sales should rise 17% YoY in Q2FY18.

However, we estimate unitary EBITDA to marginally fall by 3% YoY to Rs1,002/MT as we estimate higher input costs as well as higher opex for JPA’s assets initially. Thus, we estimate EBITDA to grow 13% YoY.

Despite EBITDA growth, we estimate PAT to fall 30% YoY due to the impact of JPA amalgamation (lower utilisation and increase in capital cost).

11 Q2FY18 Results Preview

Building Materials – Others

Visaka Industries (Rating: BUY; Target price: Rs620)

Exhibit 19: Result Expectation Particulars Q2FY18E Q2FY17 YoY (%) Q1FY18 QoQ (%)

BP Sales Volume (K MT) 156.9 145.8 7.6 252.8 (37.9)

Yarn Sales Volume ( MT) 1.9 2.5 (24.7) 2.6 (28.2)

Sales (Rs mn) 1,939 2,004 (3.2) 3,092 (37.3)

EBITDA (Rs mn) 260 264 (1.7) 467 (44.4)

EBITDA margin (%) 13.4 13.2 20bps 15.1 (172)bps

Adj PAT (Rs mn) 94 88 6.4 230 (59.3)

Adj PAT margin (%) 4.8 4.4 44bps 7.4 (260)bps

Source: Company, Centrum Research Estimates

We expect Visaka Industries’ net revenues to decline 3% YoY in Q2FY18 largely led by fall in textiles revenues amid pick up in Building product sales. We expect overall EBITDA to fall a modest 2% YoY (on a good base of last year) impacted by lower textiles offtake (GST impact). Lower tax outgo should however lead to PAT increase of 6% YoY.

Building product segment: We expect segmental revenue to rise 8% YoY driven by uptick in ACS sales YoY and as CBP exports bottom out during the quarter. Overall, we estimate segmental OPM to further expand by 50bps YoY on the high base of 14.2% in Q2FY17, boosting segmental EBITDA by 11% YoY.

Textile segment: Segmental utilisation has been hit post GST thus leading to both lower revenues and EBITDA. We estimate segmental EBITDA to fall 52% YoY to Rs29mn.

Subdued performance On a broader basis, we expect our banking universe to report yet another quarter of subdued performance on both revenue / profitability front. Weak loan growth, decline in NIM (QoQ), lower treasury gains and elevated provisioning are the key negatives for the quarter. On the flip-side, sequential decline in slippages (across all major banks), investment gains following sale of stake in subsidiaries (SBI, ICICI Bank) and QoQ improvement in NIM (Karnataka Bank, ICICI Bank) are the key positives. We stick to our preference for ICICI Bank and SBI in the large-cap space; prefer the old private sector banking space. Asset financing companies will report strong quarter on both growth / profitability front. Affordable housing space (GICHF) is expected to report lower growth / challenges on recovery front. The micro-lending space will continue to report loss as they provide for past dues / operating related costs following transition. Underlying business activities remains slow, yet steady and is positive for the overall rating agencies space.

Banking: Systemic credit growth has remained anaemic and with elevated deposit growth has impacted the margins on an aggregate basis. Adjusted for SBI, we expect our banking universe to report modest growth in both NII / loans. The trend in fee income growth is set to remain muted; a favourable yield movement during the quarter, however will see banks report decent treasury gains (though on a lower side QoQ). The quarter saw ICCI Bank and SBI sell part of the stake in their insurance business. These investment gains, in our view will be utilised towards creation of contingent provisions. Slippages for the coverage universe are set to moderate/decline QoQ; however following lower recovery (unlike the previous quarter), overall GNPA are expected to remain at elevated levels on both YoY / QoQ basis. Provisions will remain higher as banks provide for NPA ageing and regulatory requirement towards certain stressed accounts in addition to standard asset provisions. We thus expect profit growth to remain muted for the quarter.

NBFCs –AFCs and HFCs: Industry-wide auto volumes, especially PV, tractors and LCV have been on a rise and bodes well for AFCs coverage – MMFS and Sundaram Finance. Our channel checks have pointed for relatively better recoveries on a YoY basis; and also on a QoQ basis (following the seasonality factor). We thus expect our AFC universe to report 18.4% / 23.3% growth in NII / PPOP on back of healthy ~14% YoY growth in AuM. Provisioning will remain elevated for MMFS (ageing of older NPAs); however on the back of a low-base and recovery in earnings, we see MMFS report strong 92% YoY growth in PAT. Sundaram Finance will see stable loan-loss provisioning/ 5% YoY growth in PAT. While we remain positive on the opportunities in the affordable housing space (EWS / MIG – I and MIG-II), the pace of activities therein remains slow YTD. This in addition to implementation of RERA has impacted overall loan growth. Further, the after effect of demonetisation and longer than expected time towards effective implementation of GST has impacted the cash flow of the end-user, thus impacting asset quality trends in the LAP portfolio. We thus see GICHF report lower loan growth / continued elevated slippages. However, a favourable borrowing profile, positively impacting spreads will see overall NII / PAT grow 29.6% YoY / 20% YoY.

Rating Agencies; Micro-Lending Institutions: While systemic banking credit growth has remained muted and will impact BLR linked rating revenues, underlying trends in the corporate bond market has remained encouraging. This in addition to continued efforts by the regulatory authorities in reviving the overall rating opportunity bodes well for both CARE and CRISIL. We expect CARE and CRISIL (combined) to report 9.1% YoY / 7.4% YoY growth in Sales/ EBIDTA. Micro-lending institutions - our channel checks including commentaries from rating agencies have pointed to improvement in collection efficiency. According to ICRA, the collection efficiency in the microfinance sector has increased to 93% in July 2017 from a low of 87% in December 2016. Excluding certain pockets of Maharashtra, overall recovery trends have been encouraging and broad based (ie across all states). However, with stickiness in PAR-90, overall provisioning is set to remain elevated. Transition to the Small Finance Bank (SFB) model will see operating costs remain higher. This in addition to providing for unpaid dues will impact profitability. We see Ujjivan to report yet another quarter of loss.

Recommendation: Our choice of stocks remain the same - we continue to prefer ICICI Bank and SBI in the large-cap banking space given the healthy core operating profit and strong capital position. We like the old private sector banks as they offer a strong play on both earnings and valuation multiple expansions. On the NBFC front, loan growth momentum remains intact and we stick with our preference for Sundaram Finance over MMFS. Even as we factor in strong earnings growth, we believe current valuations for MMFS are expensive for the given set of RoE’s. Micro-lending institutions will report losses following transition related costs (SFB perspective) and provisioning for unpaid dues. While we remain structurally positive on the rating agencies (CARE, CRISIL) and the housing space (GICHF), near term concerns on growth/ current valuations offer limited upside.

Stock Price performance (%)*

Co. Name 1-Mth 3-Mth 6-Mth YTD

Axis Bank 2.1 0.0 (1.1) (5.2)

ICICI Bank (7.9) (6.1) 6.5 19.1

City Union Bank 1.4 (0.7) 17.9 31.8

DCB Bank (1.0) (3.9) 9.2 48.4

Karnataka Bank (4.0) (11.5) 0.3 18.8

SBIN (6.4) (8.3) (12.4) (0.0)

GICHF (6.2) (8.7) 15.7 53.5

MMFS (6.0) 16.4 25.6 11.0

SUF (1.0) 4.7 2.4 23.7

CARE Ratings (8.2) (11.8) (13.7) (4.2)

CRISIL (6.4) (10.3) (9.9) (27.4)

Ujjivan Financial (10.9) 4.0 (16.7) (28.2)

Bank Nifty (0.4) 3.2 11.9 24.7

PSU Bank Nifty (4.6) (8.2) (12.3) (2.8)

Nifty 0.6 3.2 7.7 14.6

Source: Bloomberg; * as on 6 October 2017

Rating and target prices

Co Name Rating CMP* TP (Rs)

Axis Bank Hold 503 530

ICICI Bank Buy 273 340

City Union Bank Hold 164 150

DCB Bank Ltd Hold 186 172

Karnataka Bank Buy 147 200

SBI Buy 257 340

GIC Housing Fin. Hold 513 530

MMFS Sell 419 250

Sundaram Finance Buy 1,680 2,000

CARE Hold 1,399 1,600

CRISIL Hold 1,781 2,160

Ujjivan Finance Hold 334 350

Source: Centrum Research Estimates; * as on 6 October 2017

Aalok Shah, [email protected]; 91 22 4215 9075

Gaurav Jani, [email protected]; 91.22 4215 9110

INDIA

Financials 9 October 2017

Centrum Equity Research is available on Bloomberg, Thomson Reuters and FactSet

13 Q2FY18 Results Preview

Exhibit 20: Quarterly preview

Co Name Net interest income (Rs mn) Pre-provisioning profit (Rs mn) Net profit (Rs mn)

Q2FY18E % YoY % QoQ Q2FY18E % YoY % QoQ Q2FY18E % YoY % QoQ

Axis Bank 47,204 4.6 2.3 42,084 2.6 (1.9) 11,557 262.6 (11.5)

ICICI Bank# 56,597 7.7 1.2 73,127 (31.2) 41.1 23,977 (22.7) 17.0

City Union Bank 3,379 12.2 (1.3) 2,886 21.9 (2.8) 1,311 6.0 (6.6)

DCB Bank 2,366 24.3 1.5 1,307 29.6 (4.2) 587 21.1 (10.0)

Karnataka Bank 4,444 11.9 4.7 3,192 37.2 3.1 1,370 10.7 2.4

SBIN# 1,93,054 33.7 9.7 1,72,652 53.8 45.4 24,660 (2.8) 22.9

GIC Housing 955 29.6 (2.4) 808 36.0 (8.6) 413 20.1 2.3

MMFS 9,468 20.9 10.1 5,799 28.7 18.5 1,817 91.6 283.5

Sundaram Finance 3,225 11.6 1.0 2,189 11.0 12.8 1,337 4.7 13.9

CARE Ratings 871 7.5 41.8 635 6.2 62.0 463 7.1 30.5

CRISIL* 4,249 9.5 4.5 1,161 8.2 13.2 750 (6.0) 11.6

Ujjivan Financial 1,795 (19.7) 8.0 451 (62.3) 1.3 -230.1 NA NA

Source: Centrum Research Estimates. * denotes Net sales /EBIDTA. *CRISIL is a Dec ending company. #includes gains on stake sale.

Exhibit 21: Valuation summary

Bank / NBFC Rating CMP (Rs)*

TP (Rs)

P/ ABV (x) P/ E (x) RoA (%) RoE (%)

FY17 FY18E FY19E FY17 FY18E FY19E FY17 FY18E FY19E FY17 FY18E FY19E

Axis Bank Hold 503 530 2.6 2.3 1.9 32.7 16.6 12.7 0.6 1.2 1.4 6.8 12.4 14.5

ICICI Bank Buy 273 340 2.2 2.1 2.0 16.3 16.4 15.1 1.3 1.3 1.3 10.7 11.0 11.9

City Union Bank Hold 164 150 3.1 2.7 2.3 19.6 17.6 15.2 1.5 1.5 1.5 15.2 14.7 15.0

DCB Bank Ltd Hold 186 172 2.9 2.3 2.1 26.6 22.3 17.3 0.9 1.0 1.0 10.8 11.3 12.0

Karnataka Bank Buy 147 200 1.1 1.0 0.9 9.2 7.3 5.7 0.7 0.9 1.0 10.2 10.7 12.4

SBI Buy 257 340 2.1 1.8 1.5 19.5 21.1 9.1 0.4 0.3 0.6 7.0 5.5 10.2

GIC Housing Fin. Hold 513 530 3.3 2.8 2.4 18.7 16.2 13.3 1.7 1.6 1.6 18.8 18.8 19.7

MMFS Sell 419 250 4.9 4.7 3.9 59.2 27.8 20.8 0.9 1.6 1.9 6.4 12.6 15.1

Sundaram Finance Buy 1,680 2,000 5.1 4.5 3.9 37.7 32.9 27.3 2.7 2.8 2.9 14.0 14.2 15.1

CARE Hold 1,399 1,600 8.3 7.4 6.7 27.2 25.5 22.1 47.3 45.5 47.2 33.4 30.7 31.8

CRISIL Hold 1,781 2,160 19.4 16.8 14.5 38.9 34.4 28.9 49.2 52.4 56.9 32.3 34.5 37.4

Ujjivan Finance Hold 334 350 2.3 2.4 2.1 38.0 19.1 19.3 2.9 0.8 2.2 14.1 4.2 13.1

Source: Company, Centrum Research Estimates. *as on 6th Oct, 2017 #ROA for rating agencies is RoCE.

14 Q2FY18 Results Preview

Banking

Axis Bank - HOLD; Target price Rs530

We expect loans to grow 12.5% YoY led by continued focus at retail / SME portfolio. NII at Rs47.2bn is expected to grow 4.6% YoY. We expect NIM at 3.06% to decline 24bps YoY / remain flat QoQ.

Operating profit at Rs42.1bn is expected to grow 2.6% YoY. We do not expect any major surprise either on fee income front / operating costs end.

Q2FY17 saw bank report elevated slippages and thus the accelerated provisioning as the quarter large part of its watchlist portfolio slip into NPA. We do not expect a similar trend in the current quarter. However, while we see slippages run-rate stabilise, provisioning cost is set to remain high as the bank provides for a) NPA ageing b) IBC related cases and c) standard asset provisioning.

Adjusted for provisioning and taxes, we expect PAT at Rs11.6bn. Management commentaries on watch list exposure will be closely monitored.

Stock trades at 1.9x FY19E ABV. We have a Hold rating on the stock with TP at Rs530.

Exhibit 22: Quarterly Estimates Rs mn Q2FY18E Q2FY17 % YoY Q1FY18 % QoQ

Net interest income 47,204 45,139 4.6 46,161 2.3 Pre-provisioning profit 42,084 41,002 2.6 42,912 (1.9) Profit after tax 11,557 3,187 262.6 13,056 (11.5) GNPA 2,35,963 1,63,787 44.1 2,20,309 7.1 GNPA (%) 5.94 4.17 177bps 5.03 91bps NIM (%) calc. 3.06 3.31 (24bps) 3.06 1bp

Source: Company, Centrum Research Estimates.

ICICI Bank – BUY; Target price Rs 340

We expect ICICI Bank to report 7.7% yoy growth in NII led by 4.5% YoY growth in loans and further improvement in margins to 2.9%. Loan growth would continue to be driven by strong traction in its domestic loans, especially retail segment.

Q2’17 included profit on sale of investment in life insurance business. The current quarter saw ICICI Bank sell stake in its general insurance business.

Growth in fee income is expected to remain modest. Reported operating profit at Rs73.1bn is expected to decline 31.2% YoY. However, adjusted for the investment gains, operating profit at Rs52.1bn have grown 5.2% YoY.

The pace of incremental slippages is set to decline QoQ. We however have built in accelerated provisions including creation of provision buffers as the bank utilises the gain on sale of stake in its general insurance business towards provisions.

Reported net profit for the quarter at Rs23.9bn is expected to decline 23% YoY. Retain Buy, with an SOTP-based TP of Rs340. ICICI Bank is our preferred pick in the large-cap banking space.

Exhibit 23: Quarterly Estimates Rs mn Q2FY18E Q2FY17 % YoY Q1FY18 % QoQ

Net interest income 56,597 52,533 7.7 55,898 1.2

Pre-provisioning profit 73,127 1,06,364 (31.2) 51,833 41.1

Profit after tax (reported) 23,977 31,026 (22.7) 20,490 17.0

GNPA 4,51,486 3,21,786 40.3 4,31,476 4.6

GNPA (%) 9.47 6.82 265bps 7.99 148bps

NIM (%) calc. 2.94 2.84 10bps 2.92 2bps

Source: Company, Centrum Research Estimates.

15 Q2FY18 Results Preview

City Union Bank - HOLD; Target price Rs150

We expect CUBK to report 12.2% YoY growth in NII on the back of 15% YoY growth in loans and hence we expect a contraction in margins owing to the NIM being at its peak. We expect NIM (calc) at 3.7% to decline 2bps YoY/ 17bps QoQ.

Operating profit at Rs2.9bn is expected to rise 21.9% YoY.

Management has guided for 175-200bps of slippages and we have factored the same into our estimates. We are building in credit cost at 175bps for Q2’18.

Net profit, after adjusting for the same at Rs1.3bn is set to grow 5.9% YoY. Stock trades at 2.3x FY19E ABV. We have a Hold rating with TP at Rs150.

Exhibit 24: Quarterly Estimates Rs mn Q2FY18E Q2FY17 % YoY Q1FY18 % QoQ

Net interest income 3,379 3,012 12.2 3,424 (1.3) Pre-provisioning profit 2,886 2,368 21.9 2,970 (2.8) Profit after tax 1,311 1,238 6.0 1,403 (6.6) GNPA 7,861 5,980 31.5 7,350 7.0 GNPA (%) 3.11 2.69 42bps 3.05 6bps NIM (%) calc. 3.69 3.71 (2bps) 3.86 (17bps)

Source: Company, Centrum Research Estimates

DCB Bank – HOLD; Target price Rs172

We expect DCB Bank to report 24.3%/ 22% YoY growth in NII/ loans for the quarter. NIM at 3.71% is expected to contract 14bps QoQ / improve 5bps YoY.

We expect cost / average assets to stabilise and improve as the bank now focuses at improving efficiency. Operating profit at Rs1.3bn is expected to rise 29.6% YoY.

While the recent past has seen constraints on working capital cycle, we do not foresee any major delinquencies risk for DCB bank given its customer profile and appraisal policies.

After adjusting for provisions and taxes, we see net profit at Rs587mn rise 21% YoY.

Exhibit 25: Quarterly Estimates Rs mn Q2FY18E Q2FY17 % YoY Q1FY18 % QoQ

Net interest income 2,366 1,903 24.3 2,332 1.5

Pre-provisioning profit 1,307 1,009 29.6 1,364 (4.2)

Profit after Tax 587 485 21.1 652 (10.0)

GNPA 3,179 2,554 24.5 2,853 11.4

GNPA (%) 1.80 1.75 5bps 1.74 6bps

NIM (%) calc. 3.71 3.66 5bps 3.85 (14bps)

Source: Company, Centrum Research Estimates

Karnataka Bank – BUY; Target price Rs200

We expect the bank to report 11.9% YoY growth in NII led by 11% YoY growth in loans and QoQ expansion in NIM to 2.7% levels. Our NIM expansion is based on the premise of a) improvement in the loan-deposit ratio b) move towards reduction in saving bank deposit rates (the bank has ~70% of its SA deposits in less than Rs10mn) and c) further reduction in RIDF portfolio.

Operating profit at Rs3.2bn is set to improve 37% YoY. We expect slippages to come in at 440bps; credit cost is built in at 145bps.

Net profit, adjusted for the same at Rs1.37bn is expected to grow 10.7% YoY. We have a Buy rating on the stock with TP of Rs200.

Exhibit 26: Quarterly Estimates Rs mn Q2FY18E Q2FY17 % YoY Q1FY18 % QoQ

Net interest income 4,444 3,973 11.9 4,244 4.7

Pre-provisioning profit 3,192 2,328 37.2 3,097 3.1

Profit after Tax 1,370 1,238 10.7 1,339 2.4

GNPA 18,495 13,445 37.6 16,910 9.4

GNPA (%) 4.55 3.64 91bps 4.34 21bps

NIM (%) calc. 2.73 2.72 1bp 2.66 7bps

Source: Company, Centrum Research Estimates

16 Q2FY18 Results Preview

State Bank of India – BUY; Target price Rs340

We expect SBI to report healthy growth in NII on both YoY and QoQ basis. Loan growth, on a QoQ basis, though is expected to remain lower. We are building in 33.7% YoY / 9.7% QoQ growth in NII. NIM (calc) at 2.4% is expected to improve both on a YoY and QoQ basis.

Q2’18 saw SBI sell its 8% stake in its life insurance business. Operating profit (including gains on sell of stake) is expected to increase 54% YoY. Adjusted for the same, we expect operating profit to grow by mere 4% YoY.

We expect overall trend in fresh delinquencies to decline on a QoQ basis. The pace of provisioning however is expected to remain higher and we have factored the same into our estimates. We also see SBI utilise the gains on stake sale to create excessive provisioning against certain accounts. Commentaries on watchlist exposure for the combined entity will be closely watched.

Adjusted for the above including taxes, we expect the bank to post net profit at Rs24.7bn. Retain Buy, with an SOTP-based TP of Rs340.

Q2’17 nos are on a standalone basis due to non-availability of data .

Exhibit 27: Quarterly Estimates

Rs mn Q2FY18E Q2FY17

(standalone) % YoY

Q1FY18

% QoQ

Net interest income 1,93,054 1,44,375 33.7 1,76,060 9.7

Pre-provisioning profit 1,72,652 1,12,242 53.8 1,18,745 45.4

Profit after tax 24,660 25,382 (2.8) 20,065 22.9

GNPA 19,65,680 10,57,830 85.8 18,80,685 4.5

GNPA (%) 10.84 7.14 370bps 9.97 87bps

NIM (%) calc 2.42 2.20 22bps 2.39 3bps

Source: Company, Centrum Research Estimates.

17 Q2FY18 Results Preview

Housing Finance Companies

GIC Housing Finance – HOLD; Target price Rs530

We expect GICHF to report 29.6% YoY growth in NII led by 17.7% YoY growth in its loans. NIM (calc) at 3.8% is expected to improve on a YoY basis. On a QoQ basis, the same however is expected to see moderation as GICHF a) resorts to lowering its lending rates to retain its customers and b) overall reduction in lending yields on incremental business.

However, with a comfortable borrowing profile, we do not see any major risk to spreads in the current quarter.

Operating profit at Rs808mn is expected to rise 36% YoY.

Asset quality related pressure persists and management have highlighted for stickiness in NPA’s for the next two quarters. We thus have built in accelerated provisions into our estimates.

After providing for the same including taxes, we expect PAT to grow 20.1% YoY to Rs413mn.

While we remain positive on the stock, post the sharp run-up, current valuations at 2.3x FY19E ABV offer limited upside. We retain Hold on the stock with TP at Rs530.

Exhibit 28: Quarterly Estimates Rs mn Q2FY18E Q2FY17 % YoY Q1FY18 % QoQ

Net interest income 955 737 29.6 979 (2.4)

Pre-provisioning profit 808 594 36.0 884 (8.6)

Profit after tax 413 344 20.1 404 2.3

NIM (calc) 3.80 3.46 34bps 4.07 (27bps)

Source: Company, Centrum Research Estimates.

18 Q2FY18 Results Preview

Asset financing companies

M&M Financial Services – SELL; Target price Rs250

We expect MMFS to report 20.9% YoY growth in NII led by 14.5% YoY growth in AuM’s. Value of asset financed for Q2’18 is expected to grow 13% YoY.

Shift in AuM portfolio towards high yielding segments and a soft borrowing regime will aid MMFS report improvement in its NIM. We expect NIM to improve on both YoY and QoQ basis.

Operating profit at Rs5.8bn is expected to grow 28.7% YoY. Better monsoon, improved crop yield and income levels in our view will aid in lower incremental slippages and higher recoveries. One, though needs to watch for underlying trend with respect to earlier dues.

We thus expect NPA to increase 15% YoY. After providing for the same including tax related provisioning, we expect net profit at Rs1.8bn to increase 91.6% YoY.

Even as we factor in strong earnings growth over FY17-19E, we believe valuations are at the higher end of the band when seen in the context of exit RoEs as at end-FY19E. Retain Sell. Higher-than-expected volume growth, lower-than-expected fresh delinquencies remain key risks to our estimates.

Exhibit 29: Quarterly Estimates

Rs mn Q2FY18E Q2FY17 % YoY Q1FY18 % QoQ

Net interest income 9,468 7,830 20.9 8,597 10.1

Pre-provisioning profit 5,799 4,504 28.7 4,894 18.5

Profit after tax 1,817 948 91.6 474 283.5

GNPA 54,603 47,481 15.0 50,142 8.9

GNPA (%) 10.87 11.00 (13bps) 10.54 34bps

Source: Company, Centrum Research Estimates

Sundaram Finance – BUY; Target price Rs2,000

We expect Sundaram Finance to report 11% YoY growth in disbursements / 11.6% YoY rise in NII for Q2’18. On the AuM front, we expect growth to come in at 13.5% YoY.

In our recent interactions, management have pointed to increased focus towards segments of CV, tractors and CE segment. Growth trajectory therein will be closely watched.

Operating profit at Rs2.19bn is expected to rise 11.0% YoY.

Asset quality trends remain comfortable, and after providing for the same including tax related provisioning, we expect SUF to report 4.7% YoY growth in net profit to Rs1.34bn.

As for the Sundaram Home Finance business, we will watch for management’s commentaries following its slow pace of growth and asset quality related risks. We will also watch for developments in the insurance business and the AMC segment.

Value unlocking through demerger of non-financial services into a separate entity and subsequent listing of the same remains the near term trigger.

Exhibit 30: Quarterly Estimates

Rs mn Q2FY18E Q2FY17 % YoY Q1FY18 % QoQ

Net interest income 3,225 2,889 11.6 3,191 1.0

Pre-provisioning profit 2,189 1,972 11.0 1,941 12.8

Profit after tax 1,337 1,277 4.7 1,173 13.9

Source: Company, Centrum Research Estimates

19 Q2FY18 Results Preview

Credit Rating Agencies

CARE Rating – HOLD; TP Rs1,600

While banking credit growth has remained muted and will impact BLR linked rating revenue, corporate bond market continues to witness stronger growth. SME related rating business too will aid in overall growth in revenue.

We expect CARE to report 7.5% YoY growth in revenues and will be led by 11.1% YoY growth in overall volume of debt rated. Pricing pressure continues and will impact revenue growth.

EBIDTA is expected to grow 6.2% YoY to Rs635mn. We expect EDBITA margins to come in at ~73% levels (moderation of 91bps over Q2’17 levels). The compression in EBIDTA margins is also following larger focus on the SME rating business.

Trend in non-interest income is expected to be along the past quarters. Adjusted for taxes, net profit at Rs463mn is expected to grow 7.1% YoY.

Exhibit 31: Quarterly Estimates Rs mn Q2FY18E Q2FY17 % YoY Q1FY18 % QoQ

Net sales 871 810 7.5 614 41.8

EBIDTA 635 598 6.2 392 62.0

EBIDTA margins (%) 73.0 73.9 (91bps) 63.9 910bps

Profit after Tax (reported) 463 432 7.1 355 30.5

Source: Company, Centrum Research Estimates

CRISIL– HOLD; TP Rs2,160

We expect CRISIL to report 9.5% YoY growth in overall revenues led by 11% YoY growth in research revenues and 15% YoY growth in advisory services. Rating revenues are expected to grow by 5.5% YoY, led by traction on domestic business (the corporate bond market) in addition to continued traction from GAC.

EBIDTA is expected to grow 8.2% YoY to Rs1.16bn. We expect EDBITA margins at 27.3%

Reported PAT is expected to decline 6% YoY to Rs750mn.

CRISIL owns 8.9% stake in CARE. Q3’17 results will see negative impact (MTM) of this investment under the other comprehensive income line item.

Exhibit 32: Quarterly Estimates

Rs mn Q3CY17E Q3CY16 % YoY Q2CY17 % QoQ

Net sales 4,249 3,881 9.5 4,065 4.5

EBIDTA 1,161 1,074 8.2 1,026 13.2

EBIDTA margins (%) 27.3 27.7 (33bps) 25.2 211bps

Profit after Tax (reported) 750 798 (6.0) 673 11.6

Source: Company, Centrum Research Estimates.

20 Q2FY18 Results Preview

Micro-lending institutions

Ujjivan Financial Services – Hold; Target Price – Rs350

We expect the pace of disbursements in Q2FY18, to be a tad better as compared to the last quarter as most of the demonetisation related pain is behind however stress in certain states remains, which will arrest AuM growth to some extent. Consequently, we expect AuM to increase by 2.4% YoY which is also owing to a higher base effect, as Q2FY17 was characterised by healthy disbursements and lower repayments (AuM growth was ~60% in that quarter).

On the operational front we don’t expect a negative surprise in terms of the operating expenses but due to subdued total income the cost to income ratio to be 77% and resultantly the operating profit is expected to be Rs 451mn (-62.3% YoY).

Q1’18 GNPA stood at 6.16%. With relatively slow pace of recovery in affected areas of Karnataka, and Maharashtra, we expect provisioning to remain elevated. Resultantly we are factoring in credit costs of Rs 800mn for the quarter.

Consequently, we expect Ujjivan to report net loss of Rs230mn.

Exhibit 33: Quarterly Estimates

Rs mn Q2FY18E Q2FY17 % YoY Q1FY18 % QoQ

Net Interest Income# 1,795 2,235 (19.7) 1,662 8.0

Pre-provisioning profit 451 1,196 (62.3) 446 1.3

Profit after tax (230) 730 NA (749) NA

Source: Company, Centrum Research Estimates # ex-other income

Washout quarter Ad revenue is expected to be impacted for all players due to cut in ad spends across categories. Months of July and August posted significant decline while early festive season offered some relief to the companies. Broadcasters such as ZEEL and Sun TV are expected to post 2% ad growth each. Hindi print companies would likely post 2-4% ad growth. In a seasonally weak quarter, Dish TV would disappoint both on subscriber addition and ARPU. While overall margins for our media coverage would post a decline, we believe the companies would benefit from GST due to input credit set-off. We expect positive surprises from IFB Industries, Mirza International and negative surprises from Dish TV, ENIL, DB Corp.

GST continues to impact advertisement growth: There was significant decline in ad revenues in the months of July & August due to implementation of GST as key categories such as FMCG, retail, real estate cut spends. Broadcasters such as ZEEL and Sun TV are expected to post ad growth of 2% each. Print industry continues to be impacted with ad revenue growth of mere 4% for DB Corp and 2.2% for Jagran Prakashan. HMVL and English business of HT Media are expected to post a decline of 2% and 5% respectively. Radio players like Music Broadcast would post ad growth of 6.5% while ENIL would post flat ad revenues. Dish TV would post disappointing revenues on the back of flat QoQ subscriber addition and mere 1.3% QoQ growth in ARPU.

Operating profit to decline on margin compression: Operating profit for our media coverage is expected to decline by 2.2% YoY on the back of lower revenues and margin compression of 21bps. ZEEL is expected to post margin expansion on the back of sale of sports business while Sun TV would post a decline of 175bps. Among print companies, we expect HT Media to post margin expansion on prudent cost management while both DB Corp and Jagran would post margin compression. Dish TV would post a steep margin decline on higher fixed cost, low revenue growth. Info Edge would continue to post double digit growth in recruitment leading to margin expansion.

Consumer demand continues to remain low: Consumer companies continue to be impacted on the back of subdued demand and implementation of GST. La Opala is expected to post a 9.7% revenue growth while we expect Speciality Restaurants to post 6.7% revenue decline on closure of restaurants and lower same store sales growth. Mirza International is expected to post 8% YoY growth lead by domestic business while exports would post a decline. IFB Industries is expected to post healthy 29% revenue growth due to market share gain.

Recommendation: We have a Buy recommendation on Sun TV while maintaining Hold on ZEEL due to valuations. Among print companies, Jagran continues to be our top pick followed by DB Corp and HT Media. While we maintain our Sell rating on ENIL on steep valuations, we have a BUY rating on Info Edge and Dish TV. In the consumer space we have a Buy on Mirza International and La Opala, while we have a Hold on IFB Industries.

Stock price performance (%)*

Company Name 1 Mth 3 Mth 6 Mth 1 Yr

DB Corp 0.9 (0.2) (3.2) (1.9)

Dish TV (11.5) (10.3) (30.9) (25.8)

ENIL (7.6) (16.1) (3.0) (2.8)

HT Media 0.1 19.4 15.4 14.3

Info Edge 11.0 2.2 26.8 8.2

Jagran Prakashan 1.1 (2.5) (4.8) (10.3)

Sun TV Network (5.0) (4.9) (0.2) 49.7

Zee Entertainment 0.2 4.1 (5.7) (6.0)

IFB Industries (0.3) (2.6) 14.7 65.9

La Opala 9.9 0.5 (6.1) (4.3)

Mirza International 2.3 3.1 84.6 70.5

Speciality Rest (9.5) (6.2) 34.0 31.5

Sarla Performance 3.2 (3.9) (20.1) (30.5)

Nifty 0.6 3.2 7.7 14.6

Source: Bloomberg; *as on 6 Oct 2017

Recommendations & target prices

Companies Rating TP (Rs) *CMP (Rs)

DB Corp Buy 470 377

Dish TV Buy 96 71

ENIL Sell 565 807

HT Media Buy 102 97

Info Edge Buy 1,090 1,060

Jagran Prakashan Buy 235 177

Sun TV Network Buy 840 780

Zee Entertainment Hold 545 521

IFB Industries Hold 605 732

La Opala Buy 555 508

Mirza International Buy 205 165

Speciality Restaurant Hold UR 111

Sarla Performance Buy 75 50

Source: Centrum Research; *as on 5 Oct 2017

Ankit Kedia, [email protected]; 91 22 4215 9634

VVarshit Shah, [email protected]; 91 22 4215 9495

Summary Estimates

Y/E March (Rsmn) Net Sales (Rsmn) EBITDA (Rsmn) EBITDA Margin (%) Adj. PAT (Rsmn)

Q2FY18E YoY (%) QoQ (%) Q2FY18E YoY (%) QoQ (%) Q2FY18E Q2FY17 Q1FY18 Q2FY18E YoY (%) QoQ (%)

DB Corp 5,590 3.7 (5.9) 1,440 (4.3) (22.7) 25.8 27.9 31.4 838 (5.3) (23.9)

Dish TV 7,537 (2.9) 2.0 2,102 (20.5) 4.5 27.9 34.0 27.2 (104) NM NM

ENIL 1,288 (0.6) 23.4 267 15.6 60.1 20.8 17.8 16.0 82 3.9 396.7

HT Media 5,807 (3.6) (3.1) 727 44.0 (9.0) 12.5 8.4 13.3 345 11.7 (16.9)

Info Edge 2,289 9.0 2.9 794 14.2 12.9 34.7 33.1 31.6 664 (17.1) 3.4

Jagran Prakashan 5,791 3.0 (2.1) 1,541 0.7 (4.5) 26.6 27.2 27.3 815 3.2 (5.9)

Sun TV Network 6,543 4.6 (16.8) 4,763 2.1 6.2 72.8 74.5 57.0 2,667 (1.4) 6.0

Zee Entertainment 15,766 (7.0) 2.4 4,666 (4.6) (3.7) 29.6 28.9 31.4 3,217 0.1 5.6

Total 50,611 (1.5) (2.2) 16,300 (2.2) (1.1) 32.2 32.4 31.8 8,524 (10.1) 0.7 IFB Industries 5,688 29.4 15.7 403 22.9 92.8 7.1 7.5 4.3 216 21.3 192.7

La Opala 766 9.7 64.0 317 31.0 70.4 41.4 34.7 39.8 212 23.3 67.9

Mirza International 2,703 8.0 7.2 497 31.5 13.7 18.4 15.1 17.3 240 46.7 19.1

Speciality Restaurant 743 (6.7) 2.9 (1) NM NM (0.2) 0.6 (2.8) (44) NM NM

Sarla Performance 834 3.0 5.5 179 (11.4) 14.0 21.5 24.9 19.9 109 (19.9) 21.1

Total 10,734 16.7 14.0 1,395 20.8 44.0 13.0 12.6 10.3 732 17.4 71.6

Source: Companies, Centrum Research Estimates

INDIA

Media / Consumer 9 October 2017

Centrum Equity Research is available on Bloomberg, Thomson Reuters and FactSet

22 Q2FY18 Results Preview

Exhibit 34: Valuation Summary

Company Rating TP

(Rs) *CMP

(Rs)

Adj. EPS dil. (Rs) P/E (x) EV/EBITDA (x) RoE (%)

FY17 FY18E FY19E FY17 FY18E FY19E FY17 FY18E FY19E FY17 FY18E FY19E

DB Corp Buy 470 377 20.4 22.9 26.9 18.3 16.5 14.0 10.4 9.1 7.6 25.1 25.0 26.4

Dish TV Buy 96 71 1.1 0.7 2.1 85.9 99.1 33.5 10.8 8.3 6.8 23.4 13.5 28.5

ENIL Sell 565 807 11.4 13.7 23.5 66.4 59.0 34.3 28.7 26.2 18.4 6.6 7.4 11.6

HT Media Buy 102 97 7.4 9.7 11.0 11.1 10.0 8.8 2.2 1.9 0.9 7.9 9.5 9.9

Info Edge Buy 1,090 1,060 17.2 21.2 25.4 48.8 49.9 41.7 38.7 38.5 30.7 11.0 12.4 13.5

Jagran Prakashan Buy 235 177 10.6 13.5 15.3 16.8 13.1 11.6 8.2 7.1 6.1 18.4 19.9 21.8

Sun TV Network Buy 840 780 26.1 29.9 35.5 18.9 26.1 22.0 9.9 14.6 12.3 27.5 27.8 29.6

Zee Entertainment Hold 545 521 12.7 14.6 17.9 37.2 35.8 29.2 22.6 22.5 18.3 21.2 19.6 20.8

IFB Industries Hold 605 732 12.6 17.4 27.6 34.9 42.1 26.6 17.6 23.3 15.9 11.5 14.0 18.8

La Opala Buy 555 508 9.9 13.1 17.7 53.6 39.0 28.7 32.2 24.7 17.7 21.7 24.1 26.7

Mirza International Buy 205 165 5.9 7.5 8.9 15.1 22.0 18.4 7.6 10.9 9.2 15.0 16.7 17.3

Speciality Restaurant Hold UR 111 -4.8 -2.0 0.0 NM NM NM 441.2 65.4 21..3 NM NM NM

Sarla Performance Buy 75 50 4.9 5.1 5.8 10.2 9.8 8.7 12.8 7.6 6.5 14.8 13.9 14.3

Source: Company, Centrum Research Estimates; *as on 06 Oct 2017

DB Corp (Rating: BUY; Target Price: Rs470)

Exhibit 35: Quarterly Estimates

(Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 5,590 5,391 5,943 (5.9) 3.7

EBIDTA 1,440 1,505 1,864 (22.7) (4.3)

EBIDTA Margin (%) 25.8 27.9 31.4 (560)bps (216)bps

PAT 838 885 1101 (23.9) (5.3)

Source: Company, Centrum Research Estimates

We expect 4% YoY growth in print ad revenues, while radio business is expected to grow by 15%. Digital revenues are expected to decline by 10% YoY. Circulation revenue growth is expected to be 9% on the back of increase in circulation and pricing.

Operating margins are expected to decline by 216bps to 25.8% while operating profit is expected to decline 4.3% YoY to Rs1,440mn. Investment in circulation would impact margins.

We expect PAT to de-grow 5.3% to Rs838mn.

Dish TV (Rating: BUY; Target Price: Rs96)

Exhibit 36: Quarterly Estimates

(Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 7,537 7,763 7,389 2.0 (2.9)

EBIDTA 2,102 2,642 2,012 4.5 (20.5)

EBIDTA Margin (%) 27.9 34.0 27.2 66 bps (615)bps

PAT (104) 701 (139) (25.5) (114.8)

Source: Company, Centrum Research Estimates

We expect an addition of 0.19mn net subscribers in the quarter while ARPU is expected to increase 1.3% QoQ to Rs149. Dish TV could post a revenue of Rs7,537mn, down 3% YoY.

We expect operating margins to decline by 615bps YoY to 27.9%, with operating profit at Rs2,102mn.

We expect the company to post PAT loss of Rs104mn.

23 Q2FY18 Results Preview

ENIL (Standalone) (Rating: Sell; Target Price: Rs565)

Exhibit 37: Quarterly Estimates

(Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 1,288 1,296 1,044 23.4 (0.6)

EBIDTA 267 231 167 60.1 15.6

EBIDTA Margin (%) 20.8 17.8 16.0 476bps 291bps

PAT 82 79 17 396.7 3.9

Source: Company, Centrum Research Estimates

Revenue is expected to be flat at Rs1,288mn due to low spends on rollout of GST and management strategy to increase yields.

Margins are expected to expand by 291bps YoY to 20.8%. Operating profit would grow by 15.6% YoY to Rs267mn.

Adjusted PAT is set to grow by 4% YoY to Rs82mn.

HT Media (Consolidated) (Rating: BUY; Target Price: Rs102)

Exhibit 38: Quarterly Estimates

(Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 5,807 6,022 5,990 (3.1) (3.6)

EBIDTA 727 505 799 (9.0) 44.0

EBIDTA Margin (%) 12.5 8.4 13.3 (82)bps 413bps

PAT 345 309 415 (16.9) 11.7

Source: Company, Centrum Research Estimates

We expect total revenues to decline by 3.6% to Rs5807mn. Overall ad revenue to decline 5% YoY, led by 7% decline for English while Hindi would decline by 2% YOY. Radio revenue is expected to grow 24% YoY on new station launches.

We estimate operating margin at 12.5%, up 413bps YoY, due to stable newsprint prices and cost cutting initiatives. Operating profit to grow 44% YoY to Rs727mn.

We expect PAT to grow 11.7% YoY to Rs345mn.

Info Edge (Standalone) (Rating: BUY; Target Price: Rs1,090)

Exhibit 39: Quarterly Estimates

(Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 2,289 2,100 2,225 2.9 9.0

EBIDTA 794 695 703 12.9 14.2

EBIDTA Margin (%) 34.7 33.1 31.6 (150)bps 160bps

PAT 664 801 642 3.4 (17.1)

Source: Company, Centrum Research Estimates

We expect 9% YoY increase in sales on the back of healthy 11% growth in the recruitment business and healthy 22%YoY growth in jeevansaathi.com. 99acres is expected to post a low single digit decline.

OPM is expected to expand by 160bps to 34.7%. Operating profit will grow 14.2% YoY to Rs794mn.

PAT would decline 17.1% to Rs664mn on the back of lower other income.

24 Q2FY18 Results Preview

Jagran Prakashan (Consolidated) (Rating: BUY; Target Price: Rs235)

Exhibit 40: Quarterly Estimates

(Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 5,791 5,620 5,913 (2.1) 3.0

EBIDTA 1,541 1,530 1613 (4.5) 0.7

EBIDTA Margin (%) 26.6 27.2 27.3 (67)bps (61)bps

PAT 815 790 866 (5.9) 3.2

Source: Company, Centrum Research Estimates

We expect a 3% YoY growth in revenues, with 2.2% YoY growth in print ad revenues while circulation revenue growth is expected at 1.5% YoY. We expect the radio business to post 6.5% YoY growth.

Operating margin is expected to decline by 61bps to 26.6%, while operating profit is set to remain flat at Rs1,541mn.

Adjusted PAT could grow by 3.2% YoY to Rs815mn.

Sun TV (Rating: Buy; Target Price: Rs840)

Exhibit 41: Quarterly Estimates

(Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 6,543 6,255 7,863 (16.8) 4.6

EBIDTA 4,763 4,663 4,484 6.2 2.1

EBIDTA Margin (%) 72.8 74.5 57.0 1,577 bps (175)bps

PAT 2,667 2,704 2516 6.0 (1.4)

Source: Company, Centrum Research Estimates

We expect the company to post a 4.6% YoY growth in revenue and a 2% growth in ad revenue. We expect 10.6% YoY growth in DTH revenues and a 21% increase in cable subscription revenues.

EBITDA margin is expected to contract by 175bps, with mere 2% YoY growth in operating profit to Rs4,763mn.

PAT is expected to decline 1.4% YoY to Rs2,667mn.

Zee Entertainment Enterprises (Rating: Hold; Target Price: Rs545)

Exhibit 42: Quarterly Estimates

(Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 15,766 16,954 15,403 2.4 (7.0)

EBIDTA 4,666 4,892 4,844 (3.7) (4.6)

EBIDTA Margin (%) 29.6 28.9 31.4 (185)bps 74 bps

Adj PAT 3,217 3,213 3,047 5.6 0.1

Source: Company, Centrum Research Estimates

Revenue is expected to decline 7% YoY on the sale of its sports business. Ad revenue is expected to grow by mere 2%. Subscription revenues would post a decline of 15% YoY while international subscription revenues would decline by 13% on appreciating Rupee.

EBITDA margin is expected to be at 29.6% on back of the sale of its sports business. EBITDA is set to decline 4.6% to Rs4666mn.

Adj PAT is expected to be flat to Rs3217mn.

25 Q2FY18 Results Preview

IFB Industries (Rating: HOLD; Target price: Rs605)

Exhibit 43: Quarterly Estimates (Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 5688 4394 4917 15.7 29.4

EBIDTA 403 328 209 92.8 22.9

EBIDTA Margin (%) 7.1 7.5 4.3 283bps (38)bps

PAT 216 178 74 192.7 21.3

Source: Company, Centrum Research Estimates

We expect sales to grow 29.4% on the back of healthy growth in the home appliance category.

We expect operating profit to increase by 23% to Rs403mn and margins to contract by 38bps YoY to 7.1% on the back of impact of GST.

Adjusted PAT is also expected to grow by 21.3% to Rs216mn.

La Opala RG (Rating: BUY; Target price: Rs555)

Exhibit 44: Quarterly Estimates (Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 766 698 467 64.0 9.7

EBIDTA 317 242 186 70.4 31.0

EBIDTA Margin (%) 41.4 34.7 39.8 156bps 671bps

PAT 212 172 126 67.9 23.3

Source: Company, Centrum Research Estimates

We expect sales to grow by healthy 9.7% on the back of double digit volume growth.

Operating profit will grow by 31% to Rs317mn. Operating margins are likely to expand 671bps on strong revenue growth and lower ad spends.

Adjusted PAT is expected to expand by 23% to Rs212mn on higher other income.

Mirza International (Rating: BUY; Target price: Rs205)

Exhibit 45: Quarterly Estimates (Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 2703 2503 2521 7.2 8.0

EBIDTA 497 378 437 13.7 31.5

EBIDTA Margin (%) 18.4 15.1 17.3 105 bps 329 bps

PAT 240 164 201 19.1 46.7

Source: Company, Centrum Research Estimates

We expect sales to grow by 8% on the back of a 10% decline in footwear exports and the leather business. The domestic branded business is expected to grow by 80% YoY.

Operating profit is expected to grow by 32% to Rs497mn, with margins expanding by 329bps to 18.4% on product mix change.

Adjusted PAT would grow by 46.7% to Rs240mn

26 Q2FY18 Results Preview

Speciality Restaurants (Rating: Hold; Target price: Under Review)

Exhibit 46: Quarterly Estimates (Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 743 796 722 2.9 (6.7) EBIDTA (1) 5 (20) (93.6) (127.1) EBIDTA Margin (%) (0.2) 0.6 (2.8) 265bps (78)bps PAT (44) (26) (65) (31.5) 72.4

Source: Company, Centrum Research Estimates

We expect sales to decline by 6.7% due to a significant slowdown in discretionary spends and closure of restaurants.

We expect the company to post an operating loss of a mere Rs1mn.

The company is expected to report a loss of Rs44mn against loss of Rs26mn in Q2FY17.

Sarla Performance Fibers (Rating: BUY; Target price: Rs75)

Exhibit 47: Quarterly Estimates (Rsmn) Q2FY18E Q2FY17 Q1FY18 QoQ (%) YoY (%)

Sales 834 810 791 5.5 3.0 EBIDTA 179 202 157 14.0 (11.4) EBIDTA Margin (%) 21.5 24.9 19.9 161 bps (348)bps PAT 109 136 90 21.1 (19.9)

Source: Company, Centrum Research Estimates

We expect sales to grow by 3% YoY to Rs834mn on the back of high single digit growth in the domestic business while the Sarla Flex would post a steep double digit decline.

We expect operating profit to decline by 11.4% to Rs179mn and operating margin to contract by 348bps on the back of losses in the US operations.

Adjusted PAT would decline by 20% to Rs109mn.

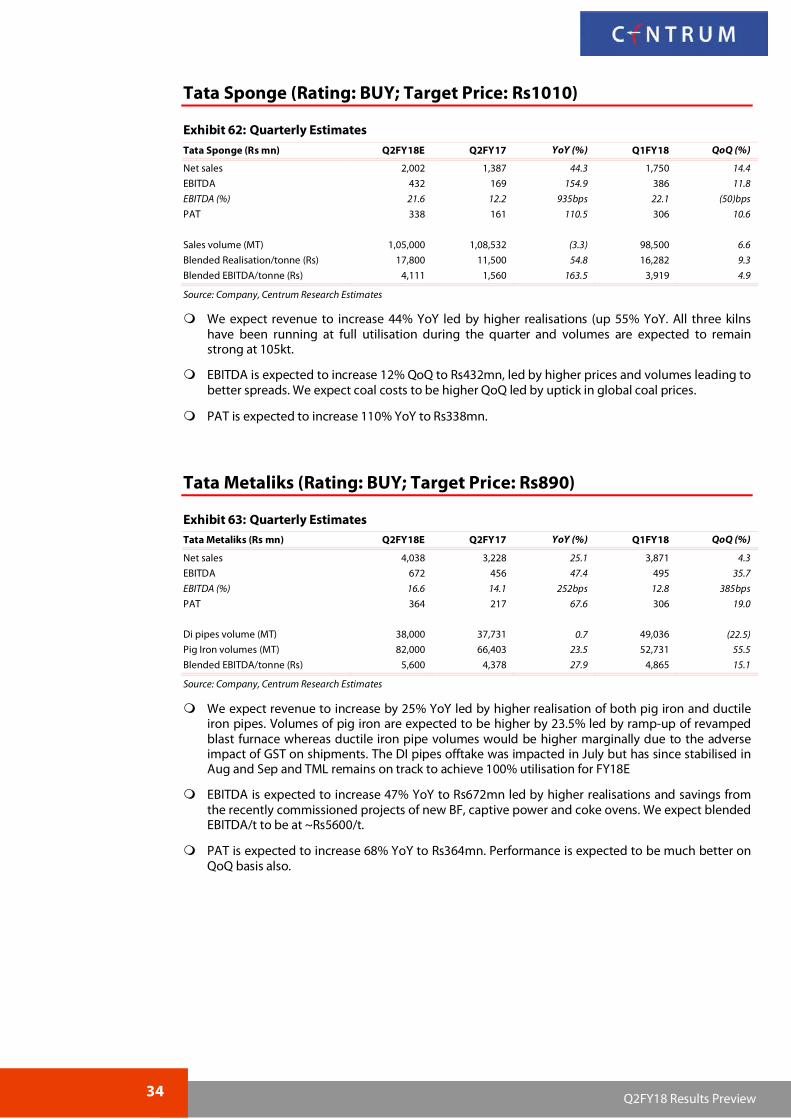

Good times continue We expect higher YoY as well as QoQ earnings across the board from our metals & mining universe, led by i) an uptick in volumes, largely steady realisations & lower RM costs for ferrous producers, ii) higher LME prices QoQ coupled with better volumes for non-ferrous producers, and iii) steady performance from refractory producers led by higher volume benefits (steel production up 5.1% YoY) mitigated by increasing RM costs. We expect strong YoY earnings growth from HZL/Vedanta/JSW among largecaps and Graphite India/ Tata Sponge/Tata Metaliks in midcaps. We expect weak results only from IFGL and Ratnamani. We maintain our preference for Hindalco/Vedanta and select midcaps like Orient Refractories/Tata Metaliks/Tata Sponge. Ferrous – better sequential spreads: Steel prices were higher in the domestic

market as global steel prices picked up materially (CIS & China prices up 20%+ QoQ) which led to domestic prices getting aligned to import parity but the price improvement was largely back-ended. We expect blended realisations to remain muted QoQ due to lag effect and inferior product mix. Volumes remained strong for large producers and EBITDA/t is expected to improve led by lower raw material costs. Tata Sponge’s earnings would recover sharply led by strong realisations & hence better spreads. Tata Metaliks is expected to report robust YoY growth led by higher pig iron volumes and cost optimisation projects. Ratnamani is expected to deliver flattish YoY earnings led by subdued volumes due to lower order book.

Non-Ferrous – sharp uptick in realisations to prop up earnings: LME prices for base metals were higher QoQ by 5-14% led by zinc & lead and rupee flat QoQ thereby impacting realisations positively. Coal costs are expected to increase due to higher e-auction prices & lower availability. HZL would deliver higher earnings QoQ led by higher LME prices. Earnings at Hindalco would remain solid, while Vedanta is expected to deliver a sharp QoQ increase in earnings led by higher contribution from majority of businesses on account of better realisations.

Refractories & midcaps – Solid performance to continue: Refractory producers are expected to deliver a steady quarter as the increase in domestic steel production (up 5.1% YoY in Q2) together with strong exports led by global pick up in steel production. However, increase in raw material costs is expected to put pressure on margins. Orient is expected to lead the revenue growth in the sector with benefit from higher export sales. Graphite India’s earnings would pick up materially led by higher realisations due to successful renegotiations of earlier contracts. Oriental carbon is expected to report earnings growth led by volume ramp-up at its new capacity.

Recommendation: In largecaps, we remain neutral on the ferrous space, while we remain constructive on the non-ferrous space and prefer Hindalco/Vedanta over Tata Steel/JSW Steel. Among midcaps, we continue to like Orient Refractories and Ratnamani Metals. We are positive on select ferrous midcap stocks like Tata Metaliks and Tata Sponge due to their strong business model and growth prospects. Graphite India which was initiated by us in June’17 has more than tripled from our IC price of Rs138 and we believe that further upside could be limited in the same.

Stock Price Performance (%)*

Company Name 1 M 3M 6 M 1 Yr

Tata Steel 5.9 25.0 37.8 77.4

JSW Steel (2.1) 19.3 26.4 46.2

Vedanta 2.5 26.9 20.7 65.2

Hindalco 2.1 28.7 29.4 58.4

Hindustan Zinc 4.1 19.3 10.7 27.6

Vesuvius India (2.7) 0.3 5.8 29.0

IFGL Refractories (12.6) 10.4 23.8 118.8

Orient Refractories (8.9) (1.1) 9.1 31.8

Graphite India 76.5 171.3 271.3 511.4

Ratnamani Metals (0.6) 7.2 11.8 58.9

Oriental Carbon 15.6 20.2 42.7 102.0

Tata Sponge 11.0 13.1 30.3 54.4

Tata Metaliks 2.8 (4.7) 16.6 75.4

NSE CNX Nifty 0.6 3.2 7.7 14.6

NSE CNX Metals 3.0 20.2 18.0 40.6

Source: Bloomberg; *as on 06 October2017

Rating and Target Prices Companies Rating CMP (Rs)* TP (Rs)

Tata Steel Hold 692 705

JSW Steel Hold 258 210

Vedanta Buy 327 300

Hindalco Buy 251 250

Hindustan Zinc Hold 319 270

Vesuvius India Hold 1,363 1,265

IFGL Refractories Hold 280 320

Orient Refractories Buy 149 170

Graphite India Buy 471 250

Ratnamani Metals Buy 893 935

Oriental Carbon Hold 1,412 1,140

Tata Sponge Buy 928 1010

Tata Metaliks Buy 717 890

Source: Centrum Research, * as on 06 October2017

Abhisar Jain, CFA [email protected]; 91 22 4215 992

Summary Estimates (Consolidated)

Y/E Mar (Rs mn) Net Sales EBITDA EBITDA % PAT-adj.*

Q2FY18E YoY (%) QoQ (%) Q2FY18E YoY (%) QoQ (%) Q2FY18E YoY(bps) QoQ (bps) Q2FY18E YoY (%) QoQ (%)

Tata Steel 3,21,808 22.4 9.5 48,204 62.3 (3.1) 14.9 365 (192) 15,328 NM (0.3)

JSW Steel 1,61,908 22.4 10.1 32,873 11.1 25.6 20.3 (206) 250 10,554 45.3 69.1

Vedanta 2,19,893 38.6 20.3 61,454 31.8 26.1 27.9 (146) 129 23,374 86.7 53.3

Hindalco (Std) 1,00,952 12.0 3.3 12,980 12.2 13.1 12.9 3 111 4,676 6.5 61.5