9-1 powerpoint presentation by douglas cloud professor emeritus of accounting pepperdine university...

Post on 22-Dec-2015

215 views

TRANSCRIPT

9-1

PowerPoint Presentation by PowerPoint Presentation by Douglas CloudDouglas Cloud

Professor Emeritus of AccountingProfessor Emeritus of AccountingPepperdine UniversityPepperdine University

© Copyright 2007 Thomson South-Western, a part of The Thomson Corporation. Thomson,

the Star Logo, and South-Western are trademarks used herein under license.

Task Force Image Gallery clip art included in this electronic presentation is used with the

permission of NVTech Inc.

Task Force Image Gallery clip art included in this electronic presentation is used with the

permission of NVTech Inc.

F1399Financing Financing ActivitiesActivities

Financial Accounting

Ingram and Albright

6th edition

Information for DecisionsInformation for Decisions

9-2

ObjectivesObjectivesObjectivesObjectives

Once you have completed this chapter, you should be able to—

Once you have completed this chapter, you should be able to—

9-3

1. Identify information that companies report about obligations to lenders and explain the transactions affecting long-term debt.

ObjectivesObjectivesObjectivesObjectives

2. Describe appropriate accounting procedures for contingencies and commitments, including capital leases.

3. Identify information reported in the stockholders’ equity section of a corporate balance sheet and distinguish contributed capital from retained earnings.

9-4

4. Explain transactions affecting stockholders’ equity and describe how these transactions are reported in a company’s financial statements.

ObjectivesObjectivesObjectivesObjectives

5. Distinguish between preferred stock and common stock, and discuss why corporations may issue more than one type of stock.

9-5

Liabilities refer to an organization’s

obligations to deliver payments, goods, or

services in the future.

Liabilities refer to an organization’s

obligations to deliver payments, goods, or

services in the future.

Types of ObligationsTypes of ObligationsTypes of ObligationsTypes of Obligations

9-6

Types of ObligationsTypes of ObligationsTypes of ObligationsTypes of Obligations

(1) A present responsibility exists to transfer resources to another entity at some future time.

(2) The organization cannot chose to avoid the transfer.

(3) The event creating the responsibility has already occurred.

Three attributes define a liability for an organization:

Three attributes define a liability for an organization:

9-7

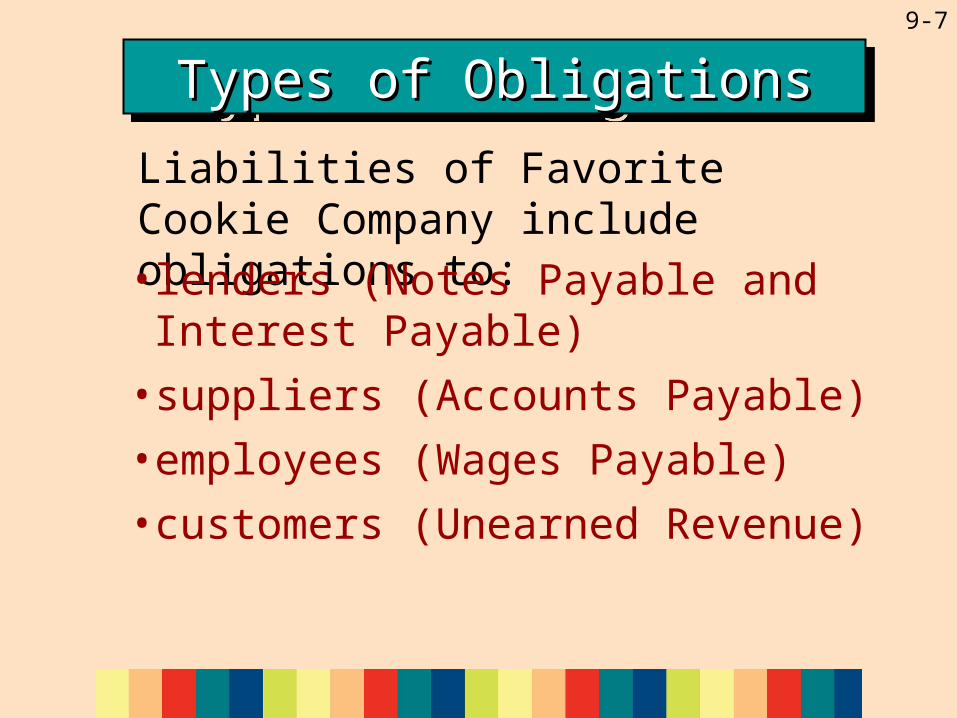

Liabilities of Favorite Cookie Company include obligations to:• lenders (Notes Payable and Interest

Payable)

• suppliers (Accounts Payable)

• employees (Wages Payable)

• customers (Unearned Revenue)

Types of ObligationsTypes of ObligationsTypes of ObligationsTypes of Obligations

9-8

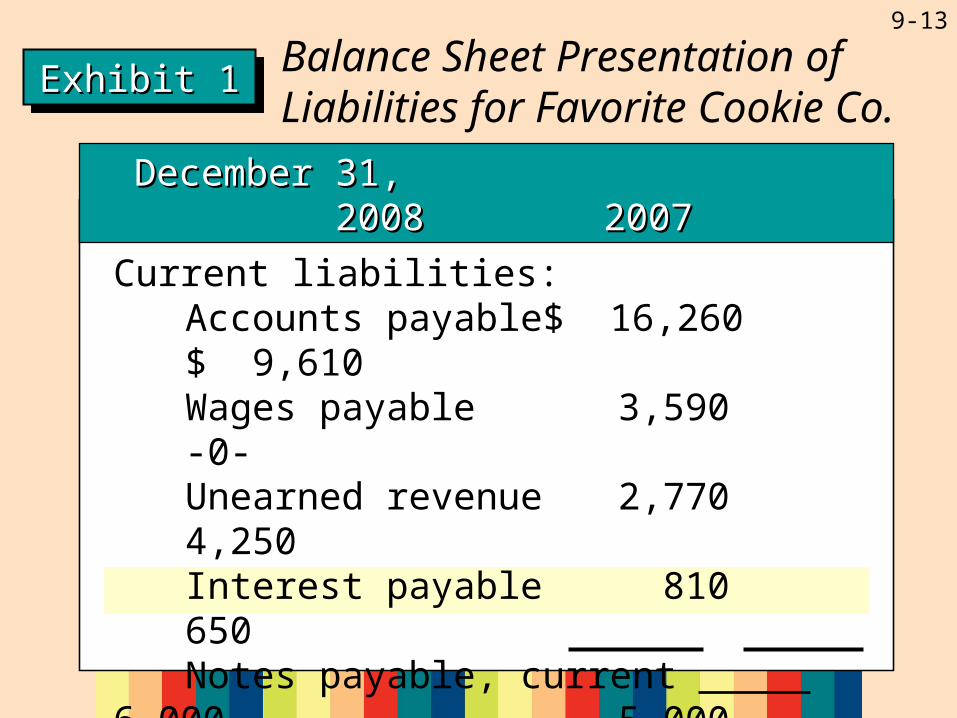

Exhibit 1Exhibit 1Exhibit 1Exhibit 1Balance Sheet Presentation of Liabilities for Favorite Cookie Co.

December 31 2008 2007

Current Liabilities:Accounts payable $ 16,260

$ 9,610Wages payable 3,590Unearned revenue 2,770

4,250Interest payable 810

650Notes payable, current 6,000

5,000Total current liabilities $ 29,430

$19,510Notes payable, long-term 80,200

73,200Total liabilities $109,630

$92,710

9-9

11ObjectiveObjectiveObjectiveObjective

Identify information that companies report about obligations to lenders and explain the transactions affecting long-term debt.

9-10

Debt ObligationsDebt ObligationsDebt ObligationsDebt Obligations

A firm’s short-term and long-term borrowings are obligations to creditors.

A firm’s short-term and long-term borrowings are obligations to creditors.

9-11

Debt ObligationsDebt ObligationsDebt ObligationsDebt Obligations

As you can see in the next two slides, Favorite Cookie

Company, debt is separated into short-term debt (current

liabilities) and long-term debt.

As you can see in the next two slides, Favorite Cookie

Company, debt is separated into short-term debt (current

liabilities) and long-term debt.

9-12

December 31, 2008 2007December 31, 2008 2007

Liabilities:Current liabilities:

Accounts payable $ 16,260$ 9,610Wages payable 3,590-0-Unearned revenue 2,7704,250Interest payable 810650Notes payable, current 6,000 5,000

Total current liabilities 29,43019,510

Notes payable, long-term 80,200 73,200

Total liabilities $109,630$92,710

Exhibit 1Exhibit 1Exhibit 1Exhibit 1Balance Sheet Presentation of Liabilities for Favorite Cookie Co.

9-13

Liabilities:Current liabilities:

Accounts payable $ 16,260$ 9,610Wages payable 3,590-0-Unearned revenue 2,7704,250Interest payable 810650Notes payable, current 6,000 5,000

Total current liabilities 29,43019,510

Notes payable, long-term 80,200 73,200

Total liabilities $109,630$92,710

Exhibit 1Exhibit 1Exhibit 1Exhibit 1Balance Sheet Presentation of Liabilities for Favorite Cookie Co.

December 31, 2008 2007December 31, 2008 2007

9-14

Long-term debt includes notes and

bonds payable.

Long-term debt includes notes and

bonds payable.

Debt ObligationsDebt ObligationsDebt ObligationsDebt Obligations

Notes and bonds payable are contracts between borrowers

and creditors.

Notes and bonds payable are contracts between borrowers

and creditors.

9-15

Company debts secured by company assets are referred to

as secured debts. Major companies often issue

debentures, or unsecured debts.

Company debts secured by company assets are referred to

as secured debts. Major companies often issue

debentures, or unsecured debts.

Debt ObligationsDebt ObligationsDebt ObligationsDebt Obligations

9-16

These commonly are issued by governments.These commonly are

issued by governments.

Bond issues that require a portion of the bonds to be repaid each year are

called serial bonds.

Bond issues that require a portion of the bonds to be repaid each year are

called serial bonds.

Debt ObligationsDebt ObligationsDebt ObligationsDebt Obligations

9-17

Callable bonds are bonds that a company can reacquire after the bonds have been outstanding for

a specific period.

Callable bonds are bonds that a company can reacquire after the bonds have been outstanding for

a specific period.

Debt ObligationsDebt ObligationsDebt ObligationsDebt Obligations

9-18

Callable bonds are bonds that a company can reacquire after the bonds have been outstanding for

a specific period.

Callable bonds are bonds that a company can reacquire after the bonds have been outstanding for

a specific period.

Debt ObligationsDebt ObligationsDebt ObligationsDebt Obligations

A company might issue 30-year bonds that are callable after five years at 102% of maturity value.

A company might issue 30-year bonds that are callable after five years at 102% of maturity value.

9-19

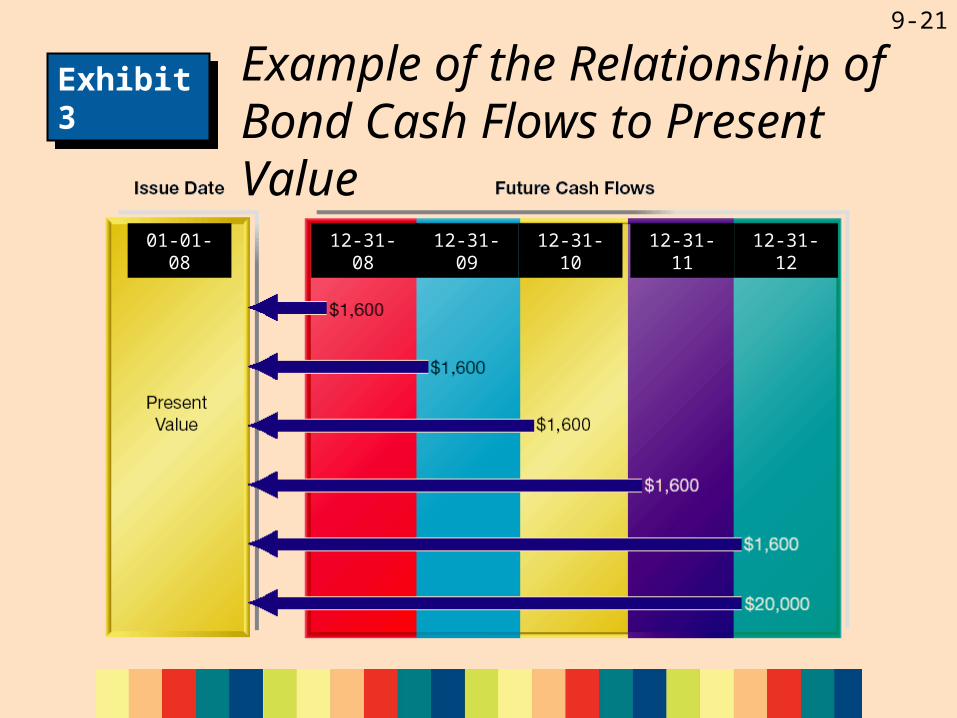

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

Favorite Cookie Company issued $20,000 of five-year bonds on January 1, 2008. The bonds pay 8% annually

($1,600) at the end of each year.

Favorite Cookie Company issued $20,000 of five-year bonds on January 1, 2008. The bonds pay 8% annually

($1,600) at the end of each year.

maturity value or face value Stated rate

of interest

9-20

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

If Favorite Cookie Company’s bonds are sold to provide the investor with a 9% return, then this actual rate of return is known as the effective rate of interest.

If Favorite Cookie Company’s bonds are sold to provide the investor with a 9% return, then this actual rate of return is known as the effective rate of interest.

How is the issue price of Favorite’s 8% bonds

determined if the effective rate of interest is 9%?

How is the issue price of Favorite’s 8% bonds

determined if the effective rate of interest is 9%?

9-21

Exhibit 3Exhibit 3 Example of the Relationship of Bond Cash Flows to Present Value

01-01-08 12-31-08 12-31-09 12-31-10 12-31-11 12-31-12

9-22

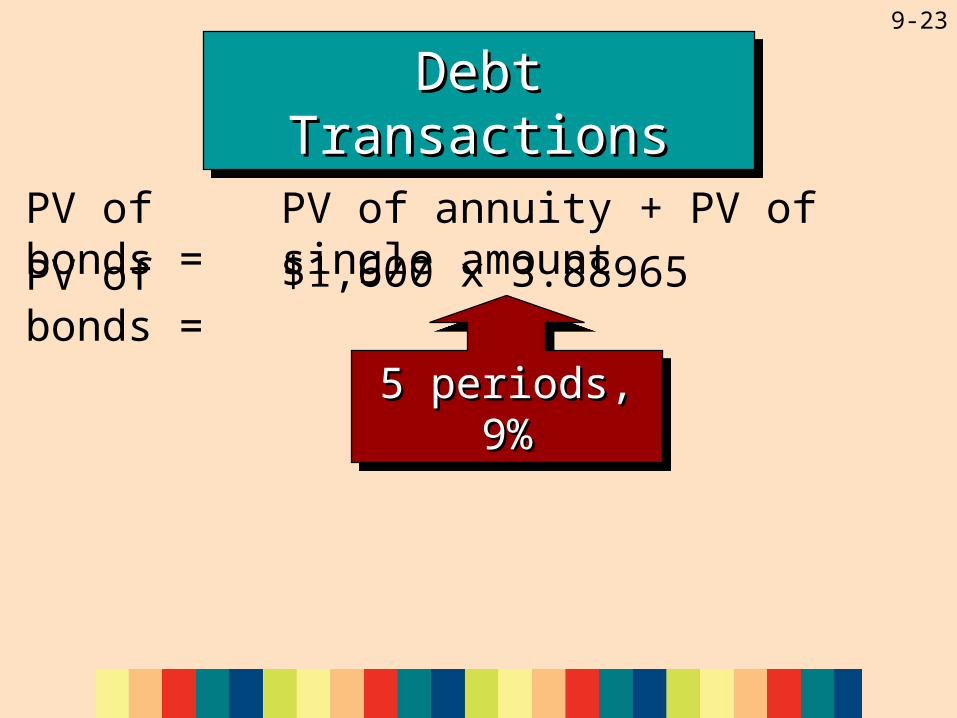

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

PV of bonds = PV of annuity + PV of single amount

PV of bonds = $1,600

$20,000 x .08$20,000 x .08$20,000 x .08$20,000 x .08

Maturity value of bond

Maturity value of bond

9-23

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

PV of bonds = PV of annuity + PV of single amount

PV of bonds = $1,600 x 3.88965

5 periods, 9%5 periods, 9%5 periods, 9%5 periods, 9%

9-24

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

PV of bonds = PV of annuity + PV of single amount

PV of bonds = $1,600 x 3.88965 + $20,000

Maturity value Maturity value of bondof bond

Maturity value Maturity value of bondof bond

9-25

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

PV of bonds = PV of annuity + PV of single amount

PV of bonds = $1,600 x 3.88965 + $20,000 x 0.64993

5 periods, 9%5 periods, 9%5 periods, 9%5 periods, 9%

9-26

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

PV of bonds = PV of annuity + PV of single amount

PV of bonds = $1,600 x 3.88965 + $20,000 x 0.64993

PV of bonds = $6,223 + $12,999

PV of bonds = $19,222

9-27

ExhibitExhibit 4ExhibitExhibit 4 Bond Amortization Table

20082009201020112012Total 8,777 777

9-28

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

ASSETS =ASSETS = LIABILITIELIABILITIESS

+ OWNERS’ EQUITY+ OWNERS’ EQUITY

Date AccountsCash

Other Assets

ContributedCapital

RetainedEarnings

1/1 Cash 19,222Bonds Payable 19,222

Favorite Cookie Company would record the bond sale on January 1, 2008.

Favorite Cookie Company would record the bond sale on January 1, 2008.

9-29

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

ASSETS =ASSETS = LIABILITIELIABILITIESS

+ OWNERS’ EQUITY+ OWNERS’ EQUITY

Date AccountsCash

Other Assets

ContributedCapital

RetainedEarnings

12/31 Interest Expense –1,730Bonds Payable 130Cash –1,600

At the end of 2008, Favorite Cookie Company would record the interest

paid and the interest expense.

At the end of 2008, Favorite Cookie Company would record the interest

paid and the interest expense.

9-30

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

ASSETS =ASSETS = LIABILITIELIABILITIESS

+ OWNERS’ EQUITY+ OWNERS’ EQUITY

Date AccountsCash

Other Assets

ContributedCapital

RetainedEarnings

12/31 Bonds Payable –20,000Cash –20,000

When the bond matures on December 31, 2012, the liability is removed when the

maturity value of the bond is paid.

When the bond matures on December 31, 2012, the liability is removed when the

maturity value of the bond is paid.

9-31

Financial Reporting of DebtFinancial Reporting of DebtFinancial Reporting of DebtFinancial Reporting of DebtBalance SheetLiabilities:

Long-term debt

$19,352 Income StatementNonoperating expenses:

Interest expense

1,730 Statement of Cash FlowsCash flow from operating activities:

Interest paid

(1,600)Cash flow from financing activities:

Long-term debt issued

19,222

Dec. 31, 2008Dec. 31, 2008Dec. 31, 2008Dec. 31, 2008

9-32

Balance SheetLiabilities:

Long-term debt

$19,494Income StatementNonoperating expenses:

Interest expense

1,742 Statement of Cash FlowsCash flow from operating activities:

Interest paid

(1,600)

Financial Reporting of DebtFinancial Reporting of DebtFinancial Reporting of DebtFinancial Reporting of Debt

Dec. 31, 2009Dec. 31, 2009Dec. 31, 2009Dec. 31, 2009

9-33

Balance SheetLiabilities:

Long-term debt

$19,648Income StatementNonoperating expenses:

Interest expense

1,754 Statement of Cash FlowsCash flow from operating activities:

Interest paid

(1,600)

Financial Reporting of DebtFinancial Reporting of DebtFinancial Reporting of DebtFinancial Reporting of Debt

Dec. 31, 2010Dec. 31, 2010Dec. 31, 2010Dec. 31, 2010

9-34

Balance SheetLiabilities:

Long-term debt

$19,816Income StatementNonoperating expenses:

Interest expense

1,768 Statement of Cash FlowsCash flow from operating activities:

Interest paid

(1,600)

Financial Reporting of DebtFinancial Reporting of DebtFinancial Reporting of DebtFinancial Reporting of Debt

Dec. 31, 2011Dec. 31, 2011Dec. 31, 2011Dec. 31, 2011

9-35

Balance SheetLiabilities:

Long-term debt

---- Income StatementNonoperating expenses:

Interest expense

$ 1,783 Statement of Cash FlowsCash flow from operating activities:

Interest paid

(1,600)Cash flow from financing activities:

Debt repaid

(20,000)

Financial Reporting of DebtFinancial Reporting of DebtFinancial Reporting of DebtFinancial Reporting of Debt

Dec. 31, 2012Dec. 31, 2012Dec. 31, 2012Dec. 31, 2012

9-36

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

When the effective rate of interest on debt is less than the stated rate, the

debt is said to be issued at a premium.

When the effective rate of interest on debt is less than the stated rate, the

debt is said to be issued at a premium.

The borrower receives more for the bonds when they are sold than the

maturity value of the bonds.

The borrower receives more for the bonds when they are sold than the

maturity value of the bonds.

9-37

Debt TransactionsDebt TransactionsDebt TransactionsDebt Transactions

When the effective rate of interest on debt is more than the stated rate, the

debt is said to be issued at a discount.

When the effective rate of interest on debt is more than the stated rate, the

debt is said to be issued at a discount.

The borrower receives less for the bonds when they are sold than the

maturity value of the bonds.

The borrower receives less for the bonds when they are sold than the

maturity value of the bonds.

9-38

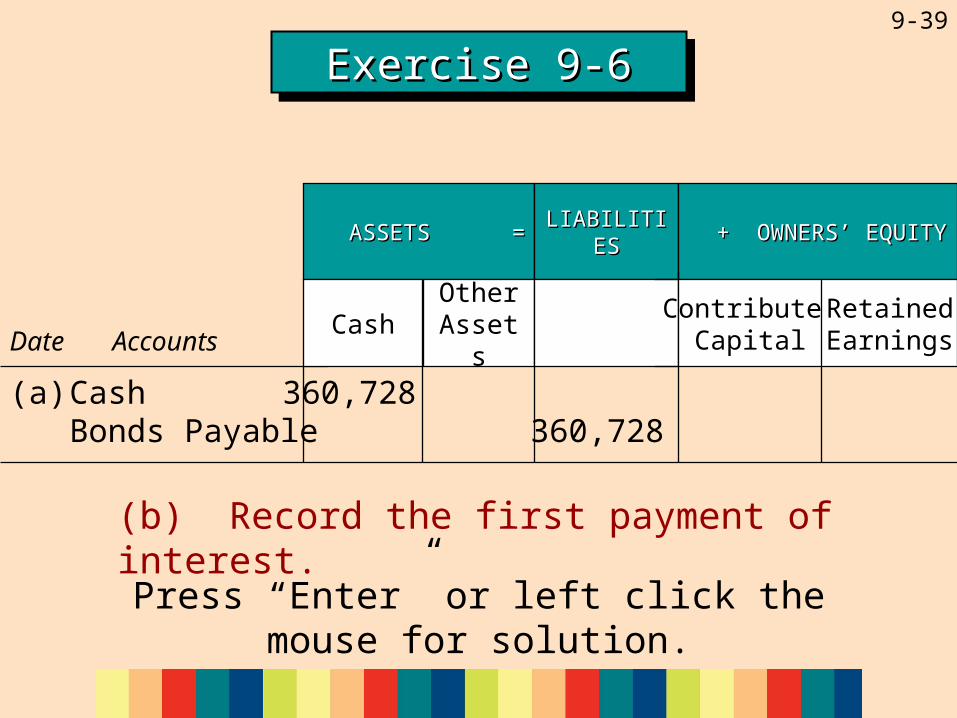

Exercise 9-6Exercise 9-6Exercise 9-6Exercise 9-6

Click the button to skip this exercise.If you experience trouble making the button work, type 42 and press “Enter.”

Watercrest Company sold 20-year bonds having a face value of $400,000 at a price of $360,728. The bonds pay annual interest at 7% and were priced to yield an effective rate of 8%. (a) Using the format presented in the chapter, record the issuance of the bonds.

Press “Enter” or left click the mouse for solution.

9-39

ASSETS =ASSETS = LIABILITIELIABILITIESS

+ OWNERS’ EQUITY+ OWNERS’ EQUITY

Date AccountsCash

Other Assets

ContributedCapital

RetainedEarnings

(a) Cash 360,728Bonds Payable 360,728

Exercise 9-6Exercise 9-6Exercise 9-6Exercise 9-6

(b) Record the first payment of interest.

Press “Enter” or left click the mouse for solution.

9-40

Exercise 9-6Exercise 9-6Exercise 9-6Exercise 9-6

ASSETS =ASSETS = LIABILITIELIABILITIESS

+ OWNERS’ EQUITY+ OWNERS’ EQUITY

Date AccountsCash

Other Assets

ContributedCapital

RetainedEarnings

(b) Interest Expense –28,858Bonds Payable 858Cash 28,000

(c) Record the repayment of principal at maturity. Assume that the last payment of interest has already been made and recorded.

Press “Enter” or left click the mouse for solution.

9-41

Exercise 9-6Exercise 9-6Exercise 9-6Exercise 9-6

ASSETS =ASSETS = LIABILITIELIABILITIESS

+ OWNERS’ EQUITY+ OWNERS’ EQUITY

Date AccountsCash

Other Assets

ContributedCapital

RetainedEarnings

(c) Bonds Payable –400,000Cash –400,000

9-42

22Determine appropriate accounting procedures for contingencies and commitments, including capital leases.

ObjectiveObjectiveObjectiveObjective

9-43

ContingenciesContingenciesContingenciesContingencies

A contingency is an existing condition that may result in an

economic effect if a future event occurs.

A contingency is an existing condition that may result in an

economic effect if a future event occurs.

9-44

ContingenciesContingenciesContingenciesContingencies

If a contingency probably will result in a loss, and the amount of the loss

can be reasonably estimated, it should be included as a liability on a

company’s balance sheet.

If a contingency probably will result in a loss, and the amount of the loss

can be reasonably estimated, it should be included as a liability on a

company’s balance sheet.

9-45

CommitmentsCommitmentsCommitmentsCommitments

A commitment is a promise to engage in some future activity that will have an

economic effect.

A commitment is a promise to engage in some future activity that will have an

economic effect.

Commitments usually involve agreements to purchase or sell

something in the future.

Commitments usually involve agreements to purchase or sell

something in the future.

9-46

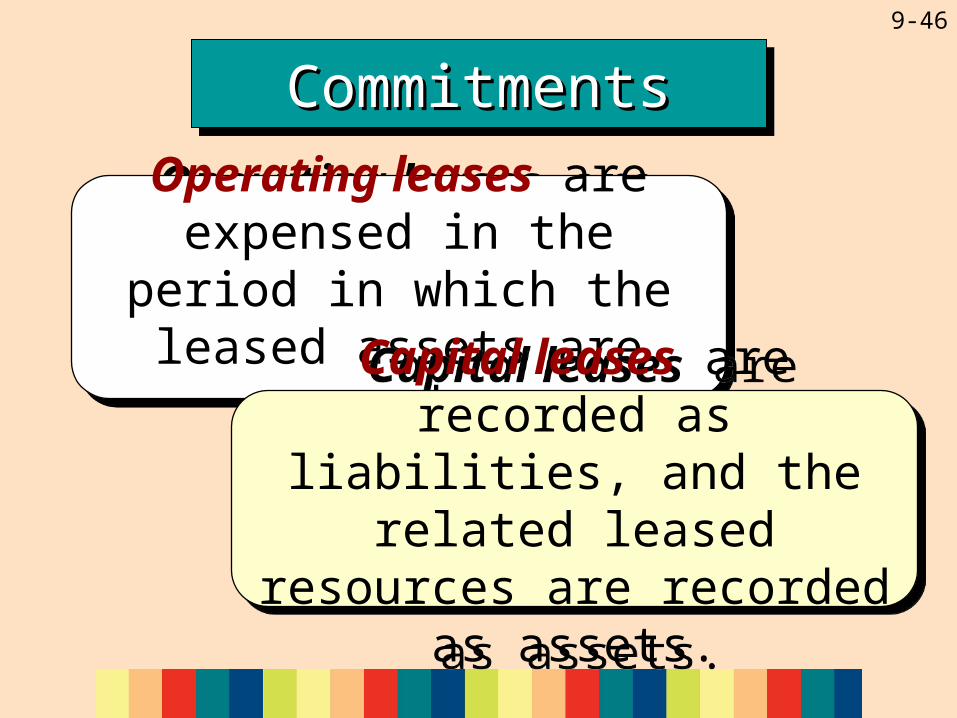

Operating leases are expensed in the period in which the

leased assets are used.

Operating leases are expensed in the period in which the

leased assets are used.

CommitmentsCommitmentsCommitmentsCommitments

Capital leases are recorded as liabilities, and the related leased resources are recorded as assets.

Capital leases are recorded as liabilities, and the related leased resources are recorded as assets.

9-47

Favorite Cookie Company signs a lease on January 1, 2008 to acquire computer equipment. The lease is for three years, the assumed life of

the equipment. The company agrees to pay $10,000 a year,

including 8% interest.

Favorite Cookie Company signs a lease on January 1, 2008 to acquire computer equipment. The lease is for three years, the assumed life of

the equipment. The company agrees to pay $10,000 a year,

including 8% interest.

Capital LeasesCapital LeasesCapital LeasesCapital Leases

9-48

Using a table:

PVA = A x IF (Table 4)

PVA = $10,000 x 2.57710

$25,771 = $10,000 x 2.57710

Using Excel:

Enter: =PV(0.08,3,-10000)

Capital LeasesCapital LeasesCapital LeasesCapital Leases

9-49

ASSETS =ASSETS = LIABILITIELIABILITIESS

+ OWNERS’ EQUITY+ OWNERS’ EQUITY

Date AccountsCash

Other Assets

ContributedCapital

RetainedEarnings

1/1 Leased Assets 25,771Capital Lease Obligation 25,771

On January 1, 2008, Favorite Cookie Company records the present value of lease payments.

On January 1, 2008, Favorite Cookie Company records the present value of lease payments.

Capital LeasesCapital LeasesCapital LeasesCapital Leases

9-50

ASSETS =ASSETS = LIABILITIELIABILITIESS

+ OWNERS’ EQUITY+ OWNERS’ EQUITY

Date AccountsCash

Other Assets

ContributedCapital

RetainedEarnings

12/31 Capital Lease Obligation –7,938Interest Expense –2,062Cash –10,000

On December 31, 2008, Favorite Cookie Company records the $10,000 payment, which includes interest expense.

On December 31, 2008, Favorite Cookie Company records the $10,000 payment, which includes interest expense.

Capital LeasesCapital LeasesCapital LeasesCapital Leases

$25,771 x .08$25,771 x .08

9-51

33Identify information reported in the stockholders’ equity section of a corporate balance sheet and distinguish contributed capital from retained earnings.

ObjectiveObjectiveObjectiveObjective

9-52

Stockholders’ equity:Common stock, $1 par value,

50,000 shares authorized,20,000 and 10,000 issued $ 20,000 $ 10,000

Paid-in capital in excess of par 190,000 90,000 Retained earnings 130,417 42,990 Treasury stock, 1,000 shares

at cost (12,000) 0Total stockholders’ equity $328,417 $142,990

Exhibit 8Exhibit 8Exhibit 8Exhibit 8 Stockholders’ Equity for Favorite Cookie Company

December 31, 2008 2007December 31, 2008 2007

9-53

Stockholders’ EquityStockholders’ EquityStockholders’ EquityStockholders’ Equity

Contributed capital is the direct investment made by stockholders

in a corporation.

Contributed capital is the direct investment made by stockholders

in a corporation.

9-54

Stockholders’ EquityStockholders’ EquityStockholders’ EquityStockholders’ Equity

Retained earnings is the accumulation of profits

reinvested in a corporation.

Retained earnings is the accumulation of profits

reinvested in a corporation.

Treasury stock is stock repurchased by a company

from its stockholders.

Treasury stock is stock repurchased by a company

from its stockholders.

9-55

Contributed CapitalContributed CapitalContributed CapitalContributed Capital

Corporations primarily issue shares of stock in exchange for cash. Common stock or capital stock

represents the ownership rights of investors in a corporation.

Corporations primarily issue shares of stock in exchange for cash. Common stock or capital stock

represents the ownership rights of investors in a corporation.

9-56

Contributed CapitalContributed CapitalContributed CapitalContributed Capital

A charter is the legal right granted by a state that permits a

corporation to exist.

A charter is the legal right granted by a state that permits a

corporation to exist.

The par value of stock is the value assigned to each share by a

corporation in its corporate charter.

The par value of stock is the value assigned to each share by a

corporation in its corporate charter.

9-57

Contributed CapitalContributed CapitalContributed CapitalContributed Capital

Paid-in capital in excess of par value is the amount in excess of the stock’s par

value received by a corporation from the sale

of its stock.

Paid-in capital in excess of par value is the amount in excess of the stock’s par

value received by a corporation from the sale

of its stock.

9-58

Contributed CapitalContributed CapitalContributed CapitalContributed Capital

Issued shares are shares that have been sold by a corporation

to investors.

Issued shares are shares that have been sold by a corporation

to investors.Outstanding shares are shares currently held by investors.

Outstanding shares are shares currently held by investors.

9-59

Retained EarningsRetained EarningsRetained EarningsRetained Earnings

YearYearNet Net

IncomeIncome DividendsDividends

Increase in Increase in Retained Retained EarningsEarnings

Balance of Balance of Retained Retained EarningsEarnings

2006 $ 0 2007 $ 52,990 $10,000 $42,990 42,990 2008 107,427 20,000 87,427 130,417

Favorite Cookie CompanyFavorite Cookie Company

9-60

Exercise 9-13Exercise 9-13Exercise 9-13Exercise 9-13

Click the button to skip this exercise.If you experience trouble making the button work, type 66 and press “Enter.”

The charter of Pelenova, Inc. states that it may issue up to one million shares of common stock. Over the life of the company 255,000 shares have been sold to investors. Total profits over the life of the company have been $876,000, and exactly one-half of that amount has been paid out in dividends. As of today’s balance sheet date, the company holds 13,000 shares that have been bought back from shareholders. What is the number of authorized shares?

Press “Enter” or left click the mouse for solution.

9-61

Exercise 9-13Exercise 9-13Exercise 9-13Exercise 9-13

Since the authorized shares is the number permitted by the company’s charter, the answer is one million shares.

ContinuedContinuedContinuedContinued

9-62

Exercise 9-13Exercise 9-13Exercise 9-13Exercise 9-13

The charter of Pelenova, Inc. states that it may issue up to one million shares of common stock. Over the life of the company 255,000 shares have been sold to investors. Total profits over the life of the company have been $876,000, and exactly one-half of that amount has been paid out in dividends. As of today’s balance sheet date, the company holds 13,000 shares that have been bought back from shareholders. What is the number of issued shares?

Press “Enter” or left click the mouse for solution.

9-63

Exercise 9-13Exercise 9-13Exercise 9-13Exercise 9-13

Issued shares is the number that have been sold to investors. For Pelenova, Inc., the number of issued shares is 255,000.

ContinuedContinuedContinuedContinued

9-64

Exercise 9-13Exercise 9-13Exercise 9-13Exercise 9-13

The charter of Pelenova, Inc. states that it may issue up to one million shares of common stock. Over the life of the company 255,000 shares have been sold to investors. Total profits over the life of the company have been $876,000, and exactly one-half of that amount has been paid out in dividends. As of today’s balance sheet date, the company holds 13,000 shares that have been bought back from shareholders. What is the number of outstanding shares?

Press “Enter” or left click the mouse for solution.

9-65

Exercise 9-13Exercise 9-13Exercise 9-13Exercise 9-13

Pelenova, Inc. has 242,000 shares outstanding. These shares are the ones currently held by stockholders (255,000 – 13,000).

9-66

44Explain transactions affecting stockholders’ equity and describe how these transactions are reported in a company’s financial statements.

ObjectiveObjectiveObjectiveObjective

9-67

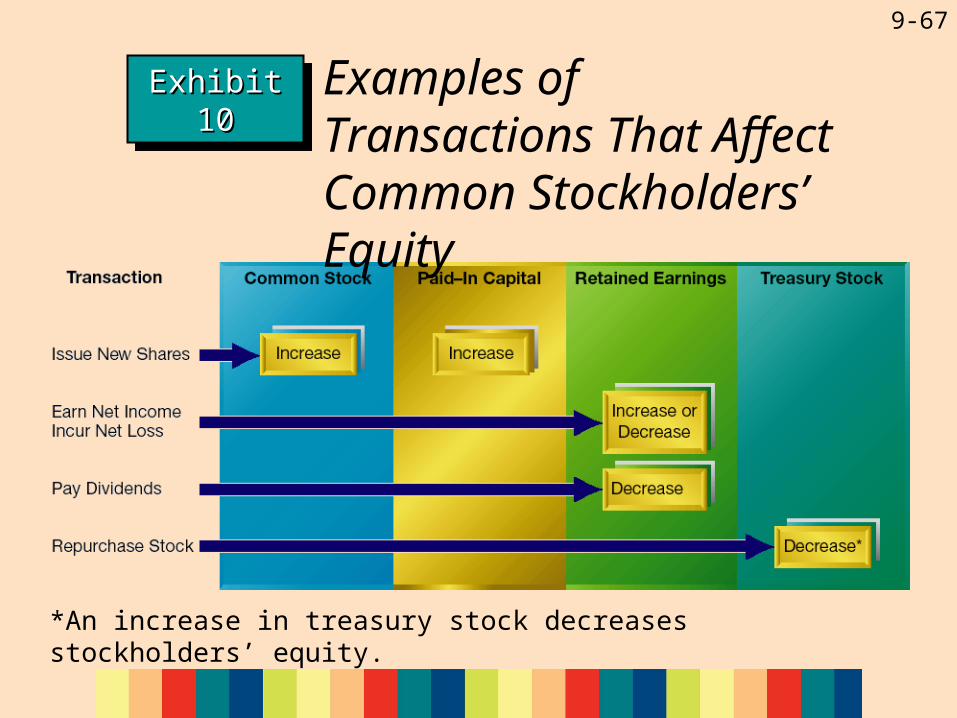

Exhibit Exhibit 1010Exhibit Exhibit 1010 Examples of Transactions That Affect Common Stockholders’ Equity

*An increase in treasury stock decreases stockholders’ equity.

9-68

Equity TransactionsEquity TransactionsEquity TransactionsEquity Transactions

Dec. 31, 2008

Dec. 31, 2008

Dec. 31, 2008

Dec. 31, 2008

–107,427107,427

9-69

Equity TransactionsEquity TransactionsEquity TransactionsEquity Transactions

Dec. 31, 2008

Dec. 31, 2008

Dec. 31, 2008

Dec. 31, 2008

Transfers net Transfers net income earned income earned during 2008 to during 2008 to

Retained EarningsRetained Earnings

Transfers net Transfers net income earned income earned during 2008 to during 2008 to

Retained EarningsRetained Earnings

–107,427107,427

9-70

Equity TransactionsEquity TransactionsEquity TransactionsEquity Transactions

Dec. 31, 2008

Dec. 31, 2008

Dec. 31, 2008

Dec. 31, 2008

Deducts the amount of Deducts the amount of dividends paid during dividends paid during 2008 from 2008 from Retained Retained

EarningsEarnings

Deducts the amount of Deducts the amount of dividends paid during dividends paid during 2008 from 2008 from Retained Retained

EarningsEarnings

–107,427107,427

9-71

Equity TransactionsEquity TransactionsEquity TransactionsEquity Transactions

Dec. 31, 2008

Dec. 31, 2008

Dec. 31, 2008

Dec. 31, 2008

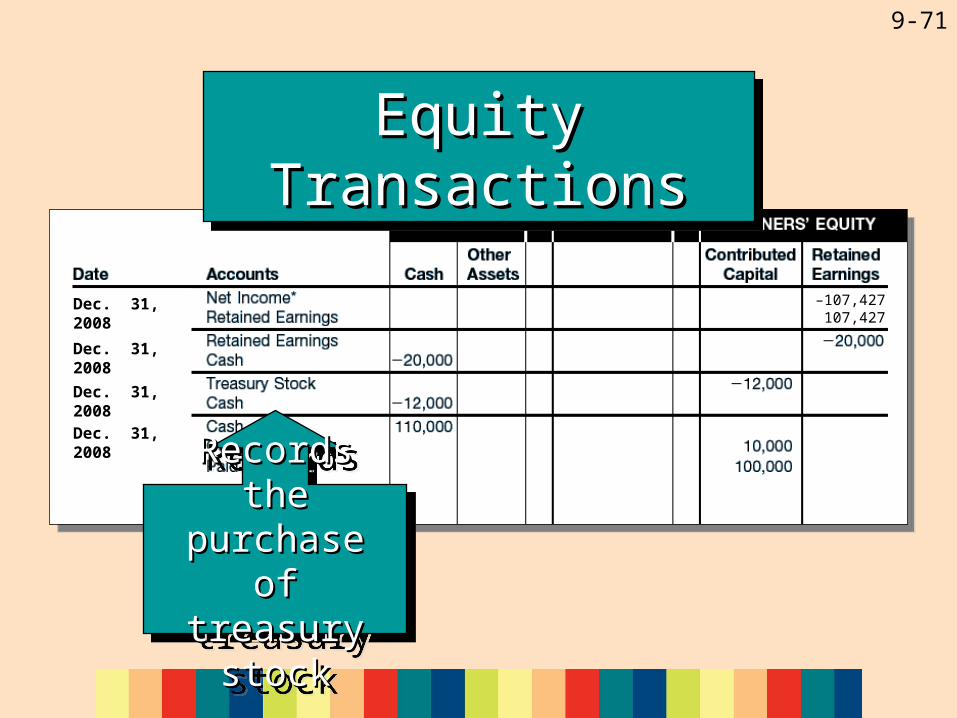

Records the Records the purchase of purchase of

treasury stocktreasury stock

Records the Records the purchase of purchase of

treasury stocktreasury stock

–107,427107,427

9-72

Equity TransactionsEquity TransactionsEquity TransactionsEquity Transactions

Dec. 31, 2008

Dec. 31, 2008

Dec. 31, 2008

Dec. 31, 2008

Records the Records the amount received amount received from the sale of from the sale of common stock.common stock.

Records the Records the amount received amount received from the sale of from the sale of common stock.common stock. –107,427

107,427

9-73

Equity TransactionsEquity TransactionsEquity TransactionsEquity Transactions

A company cannot earn profit from equity transactions. When treasury stock is sold at a price

higher than its cost, a profit is not recorded. The incremental amount

is added to paid-in capital.

A company cannot earn profit from equity transactions. When treasury stock is sold at a price

higher than its cost, a profit is not recorded. The incremental amount

is added to paid-in capital.

9-74

Cash DividendsCash DividendsCash DividendsCash DividendsThree dates are important for dividend transactions:1) The date of declaration is the date on

which a corporation’s board of directors announces that dividends will be paid.

2) The date of record is the date used to determine who will receive the dividend.

3) The date of payment is the date on which the dividends are mailed to those receiving dividends.

9-75

Issuing New StockIssuing New StockIssuing New StockIssuing New Stock

The right to maintain the same percentage of ownership when

new shares are issued is the stockholder’s preemptive right.

The right to maintain the same percentage of ownership when

new shares are issued is the stockholder’s preemptive right.

9-76

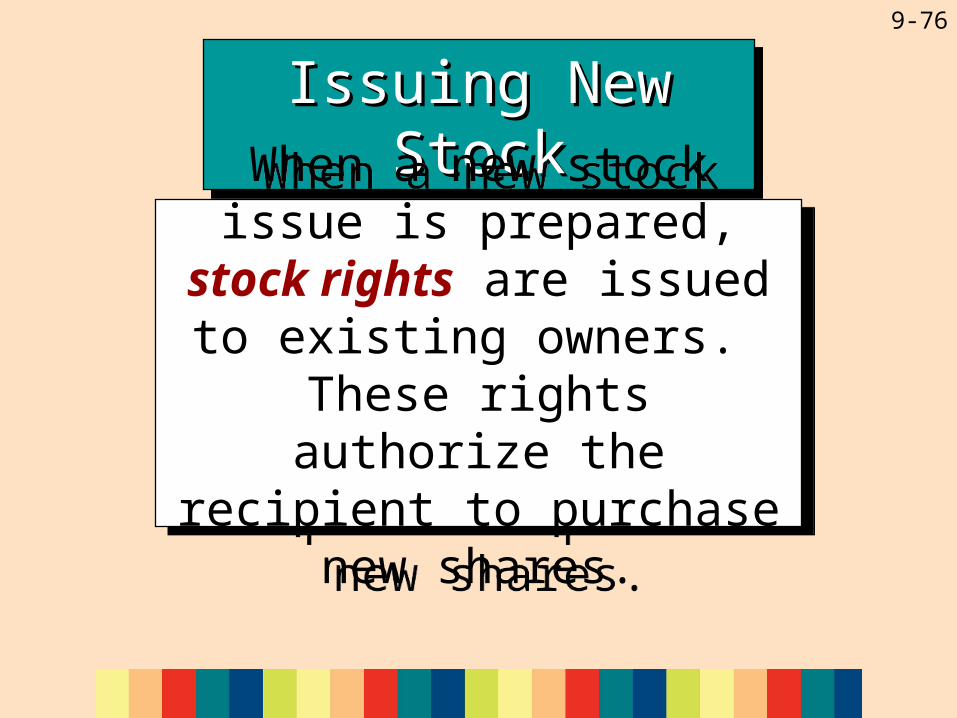

Issuing New StockIssuing New StockIssuing New StockIssuing New Stock

When a new stock issue is prepared, stock rights are issued to existing owners. These rights

authorize the recipient to purchase new shares.

When a new stock issue is prepared, stock rights are issued to existing owners. These rights

authorize the recipient to purchase new shares.

9-77

Stock DividendsStock DividendsStock DividendsStock Dividends

Stock dividends are shares of stock distributed by the company to the stockholders without

any charge. Assume Druid Company distributed a 5% stock dividend on June 1,

2007. If you owned 1,000 shares before the stock dividend, on June 1, 2007 you would receive 50 additional shares (1,000 shares x

5%).

Stock dividends are shares of stock distributed by the company to the stockholders without

any charge. Assume Druid Company distributed a 5% stock dividend on June 1,

2007. If you owned 1,000 shares before the stock dividend, on June 1, 2007 you would receive 50 additional shares (1,000 shares x

5%).

9-78

Stock DividendsStock DividendsStock DividendsStock Dividends

An important point about stock dividends is that the firm’s total stockholders’ equity does not change when a stock dividend

is declared or issued.

An important point about stock dividends is that the firm’s total stockholders’ equity does not change when a stock dividend

is declared or issued.

9-79

Stock SplitStock SplitStock SplitStock Split

When a corporation issues a stock split, it issues a multiple of

the number of shares of stock outstanding before the split.

When a corporation issues a stock split, it issues a multiple of

the number of shares of stock outstanding before the split.

9-80

Exercise 9-17Exercise 9-17Exercise 9-17Exercise 9-17

Click the button to skip this exercise.If you experience trouble making the button work, type 89 and press “Enter.”

Refer to page 347 of your textbook for the selected portion of the company’s recent financial statements. Use this data to answer questions involving Fast Start Corporation, a manufacturer of automobile ignitions. (a) What was Fast Start’s total contributed capital at year end?

Press “Enter” or left click the mouse for solution.

$8,900,000 ($700,000 common stock plus $8,200,000 paid-in capital in excess of par value)

ContinuedContinuedContinuedContinued

9-81

Exercise 9-17Exercise 9-17Exercise 9-17Exercise 9-17

Refer to page 347 of your textbook for the selected portion of the company’s recent financial statements. Use this data to answer questions involving Fast Start Corporation, a manufacturer of automobile ignitions. (b) How many shares of common stock were outstanding at year end?

Press “Enter” or left click the mouse for solution.

1,340,000 shares (1,400,000 issued less 60,000 treasury shares)

ContinuedContinuedContinuedContinued

9-82

Exercise 9-17Exercise 9-17Exercise 9-17Exercise 9-17

Refer to page 347 of your textbook for the selected portion of the company’s recent financial statements. Use this data to answer questions involving Fast Start Corporation, a manufacturer of automobile ignitions. (c) What dollar amount of treasury stock did Fast Start hold at year end?

Press “Enter” or left click the mouse for solution.

$480,000

ContinuedContinuedContinuedContinued

9-83

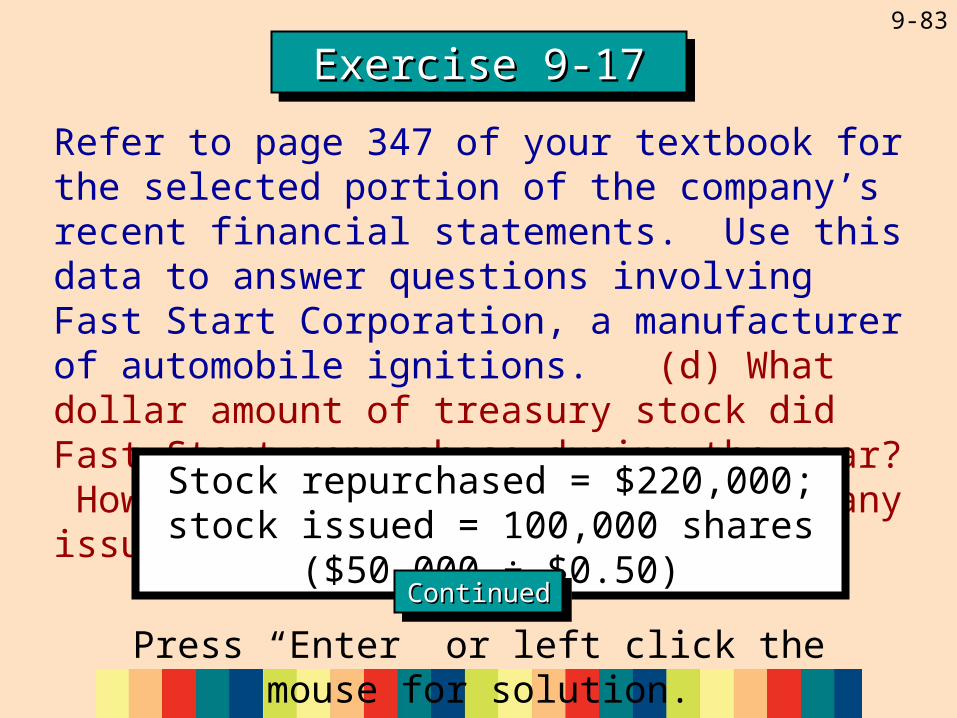

Exercise 9-17Exercise 9-17Exercise 9-17Exercise 9-17

Refer to page 347 of your textbook for the selected portion of the company’s recent financial statements. Use this data to answer questions involving Fast Start Corporation, a manufacturer of automobile ignitions. (d) What dollar amount of treasury stock did Fast Start repurchase during the year? How much common stock did the company issue?

Press “Enter” or left click the mouse for solution.

Stock repurchased = $220,000; stock issued = 100,000 shares ($50,000 ÷ $0.50)

ContinuedContinuedContinuedContinued

9-84

Exercise 9-17Exercise 9-17Exercise 9-17Exercise 9-17

Refer to page 347 of your textbook for the selected portion of the company’s recent financial statements. Use this data to answer questions involving Fast Start Corporation, a manufacturer of automobile ignitions. (e) What was the amount of dividends paid during the year?

Press “Enter” or left click the mouse for solution.

$335,000

ContinuedContinuedContinuedContinued

9-85

Exercise 9-17Exercise 9-17Exercise 9-17Exercise 9-17

Refer to page 347 of your textbook for the selected portion of the company’s recent financial statements. Use this data to answer questions involving Fast Start Corporation, a manufacturer of automobile ignitions. (f) How much cash flow came from financing activities associated with shareholders’ equity during the current year, excluding the effect of net income?

Press “Enter” or left click the mouse for solution.

ContinuedContinuedContinuedContinued

9-86

Exercise 9-17Exercise 9-17Exercise 9-17Exercise 9-17

Cash flow: Paid for dividends $(335,000)Purchase of stock (220,000)Sale of stock 800,000Net cash flow $245,000

ContinuedContinuedContinuedContinued

(f)

9-87

Exercise 9-17Exercise 9-17Exercise 9-17Exercise 9-17

Refer to page 347 of your textbook for the selected portion of the company’s recent financial statements. Use this data to answer questions involving Fast Start Corporation, a manufacturer of automobile ignitions. (f) What was the source of that cash flow?

Press “Enter” or left click the mouse for solution.

The sale of stock, $800,000

ContinuedContinuedContinuedContinued

9-88

Exercise 9-17Exercise 9-17Exercise 9-17Exercise 9-17

Refer to page 347 of your textbook for the selected portion of the company’s recent financial statements. Use this data to answer questions involving Fast Start Corporation, a manufacturer of automobile ignitions. (g) How much net income came from financing activities associated with stockholders’ equity during the current year?

Press “Enter” or left click the mouse for solution.

$0; financing activities do not create net income

9-89

55Distinguish between preferred stock and common stock, and discuss why corporations may issue more than one type of stock.

ObjectiveObjectiveObjectiveObjective

9-90

Preferred StockPreferred StockPreferred StockPreferred Stock

Preferred stock is stock with a higher claim on dividends and

assets than common stock.

Preferred stock is stock with a higher claim on dividends and

assets than common stock.

9-91

Preferred StockPreferred StockPreferred StockPreferred Stock

Preferred stock is stock with a higher claim on dividends and

assets than common stock.

Preferred stock is stock with a higher claim on dividends and

assets than common stock.

Cash dividends must be paid to preferred stockholders before they can be paid to

common stockholders.

Cash dividends must be paid to preferred stockholders before they can be paid to

common stockholders.

9-92

Preferred stockholders normally do not have voting rights in a corporation.

Preferred stockholders normally do not have voting rights in a corporation.

Preferred StockPreferred StockPreferred StockPreferred Stock

9-93

Preferred stockholders normally do not have voting rights in a corporation.

Preferred stockholders normally do not have voting rights in a corporation.

Preferred StockPreferred StockPreferred StockPreferred Stock

Preferred stock often is issued at par value or has no par value. In some cases

a liquidation value is reported for preferred stock.

Preferred stock often is issued at par value or has no par value. In some cases

a liquidation value is reported for preferred stock.

9-94

Some companies issue redeemable preferred stock. This is stock the issuing company

plans to repurchase at a particular time

in the future.

Some companies issue redeemable preferred stock. This is stock the issuing company

plans to repurchase at a particular time

in the future.

Preferred StockPreferred StockPreferred StockPreferred Stock

9-95

Some companies issue redeemable preferred stock. This is stock the issuing company

plans to repurchase at a particular time

in the future.

Some companies issue redeemable preferred stock. This is stock the issuing company

plans to repurchase at a particular time

in the future.

Redeemable preferred stock is not included

as part of stockholders’ equity.

It is reported as a separate item between

liabilities and stockholders’ equity.

Redeemable preferred stock is not included

as part of stockholders’ equity.

It is reported as a separate item between

liabilities and stockholders’ equity.

Preferred StockPreferred StockPreferred StockPreferred Stock

9-96

Preferred stock that can be converted into shares of

common stock is referred to as convertible preferred stock.

Preferred stock that can be converted into shares of

common stock is referred to as convertible preferred stock.

Preferred StockPreferred StockPreferred StockPreferred Stock

9-97

THE ENDTHE END

CCHAPTERHAPTER 9 9

9-98