8:30am cst or - pension-specialists.compension-specialists.com/webinars/sep/seps.pdf · 8:30am cst...

TRANSCRIPT

Rev 5/10/2017

Copyright 2017 © Collin W. Fritz & Associates, Ltd. “The Pension Specialists” All rights reserved. No part of this presentation may be reproduced in any form and by any means

without prior written permission from Collin W. Fritz & Associates, Ltd.

The webinar will be starting shortly

8:30am CST or 12:30pm CST

We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar

Just a Reminder

This is Copyrighted Material

No Video or Audio Recording is permitted without prior written consent from Collin W. Fritz & Associates, Ltd.

Thank you for your Compliance

The Audio Portion of this presentation is available either by phone or by using the speakers and microphone on your PC. The phone number is provided to you in the confirmation from CWF and again at the time you join the meeting. You will need the access code that was emailed to you in the confirmation from CWF. The confirmation code is 9 digits in length e.g. 123-456-789 You will also need the Audio Pin # which is shown to you at the time you join this meeting

If you have trouble re-connecting please call CWF at 800-346-3961

4

• Established by Congress to encourage businesses to set-up a retirement

plan, including a one-person business

• Supplement to Social Security and any Private or Governmental pension

plan

• 1978

5

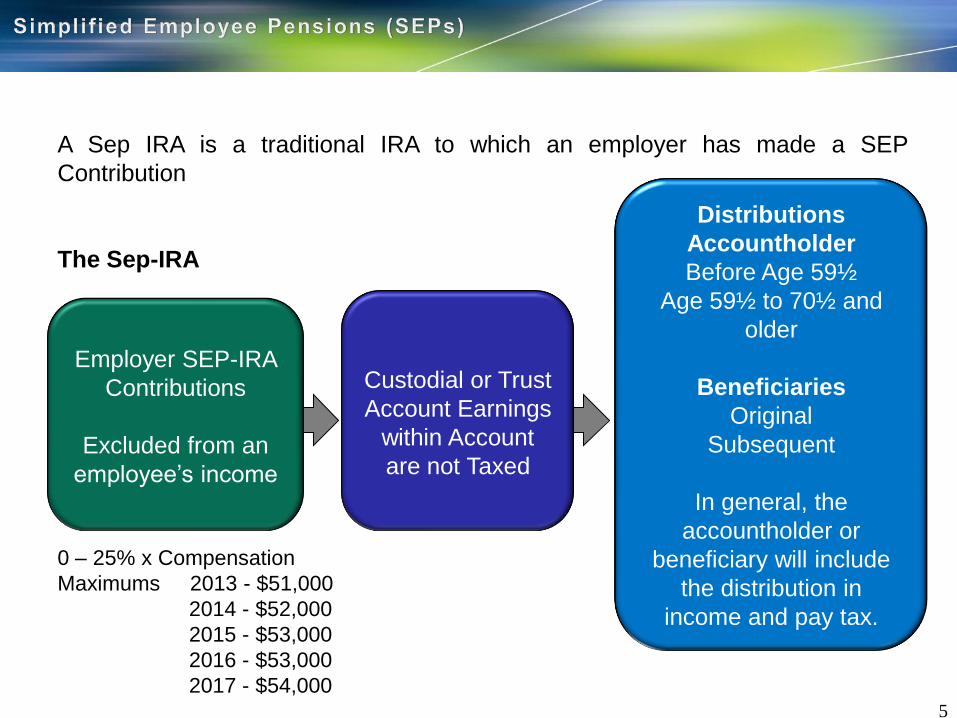

A Sep IRA is a traditional IRA to which an employer has made a SEP

Contribution

The Sep-IRA

Distributions

Accountholder

Before Age 59½

Age 59½ to 70½ and

older

Beneficiaries

Original

Subsequent

In general, the

accountholder or

beneficiary will include

the distribution in

income and pay tax.

0 – 25% x Compensation

Maximums 2013 - $51,000

2014 - $52,000

2015 - $53,000

2016 - $53,000

2017 - $54,000

Employer SEP-IRA

Contributions

Excluded from an

employee’s income

Custodial or Trust

Account Earnings

within Account

are not Taxed

6

Types of IRAs

• Traditional IRAs – An individual IRA

• SEP IRAs – An employer plan IRA, including a one-person business. Uses

a traditional IRA to handle the investments

• SIMPLE IRAs – An employer plan IRA, including a one-person business

• Roth IRAs – An individual IRA

7

Types of SEPs

• Regular

• 1 Person

• 2-10 Employees

• 10-99 Employees

• 100 and over Employees

• SAR-SEPs

• In general, repealed but certain plans grand-fathered. (1997)

8

Who Can Establish a SEP?

SEPs are established by owners of businesses, including incorporated and

unincorporated businesses, sole proprietors, and partnerships. All employees who

meet the eligibility requirements established by the employer when the plan was

adopted must be included in the plan.

Sole Proprietors - While SEPs are often established by employers with

numerous employees, these plans can also be used by a self-employed

individual where that person is the only participant in the plan. A sole owner for

purposes of the SEP rules is both an employee (actually an owner-employee

since he owns more than 10% of his business) and an employer. As an

employee of the sole proprietorship, he may participate in a SEP. As an

employer (the sole proprietor) he can make employer contributions to the SEP.

9

Who Can Establish a SEP?

SEPs are established by owners of businesses, including incorporated and

unincorporated businesses, sole proprietors, and partnerships. All employees who

meet the eligibility requirements established by the employer when the plan was

adopted must be included in the plan.

Partnerships - In the case of a partnership, a partner who is an owner-

employer, may, as an employee of the partnership, participate in a SEP, and

the partnership entity, as the employer, would contribute to the SEP. The

partnership should pass a formal resolution evidencing their intent to adopt a

SEP plan. This resolution should be in writing and be kept with all other

partnership business records.

Note: If a partnership established a SEP for the benefit of its employees, and

the partnership terminated and was thereafter run as a sole proprietorship,

continued employer contributions to the partnership SEP are not permitted. The

IRS reasons that since the partnership established the SEP only for its

employees, contributions to the SEP made by the sole proprietors could not be

contributions to partnership employees. If the new sole proprietor wishes to

continue to have a SEP plan, the employer would have to adopt a new SEP

plan agreement in their new employer capacity.

10

Who Can Establish a SEP?

SEPs are established by owners of businesses, including incorporated and

unincorporated businesses, sole proprietors, and partnerships. All employees who

meet the eligibility requirements established by the employer when the plan was

adopted must be included in the plan.

Corporations - A corporation can also adopt a SEP plan. There is no limitation

on the size of the corporation that adopts the SEP plan. The corporate board of

directors should pass a corporate resolution stating the corporation’s intention to

adopt a SEP plan. This again needs to be documented in writing and retained

with all other corporate business records.

Non-Profit Corporations - Even non-profit corporations can establish SEPs.

SAR-SEPs were not available to non-profits, however.

11

Business Goals of Offering SEP Services

1. Large cash deposits

2. New client relationship may be created

3. Existing client relationship may be expanded or strengthened.

12

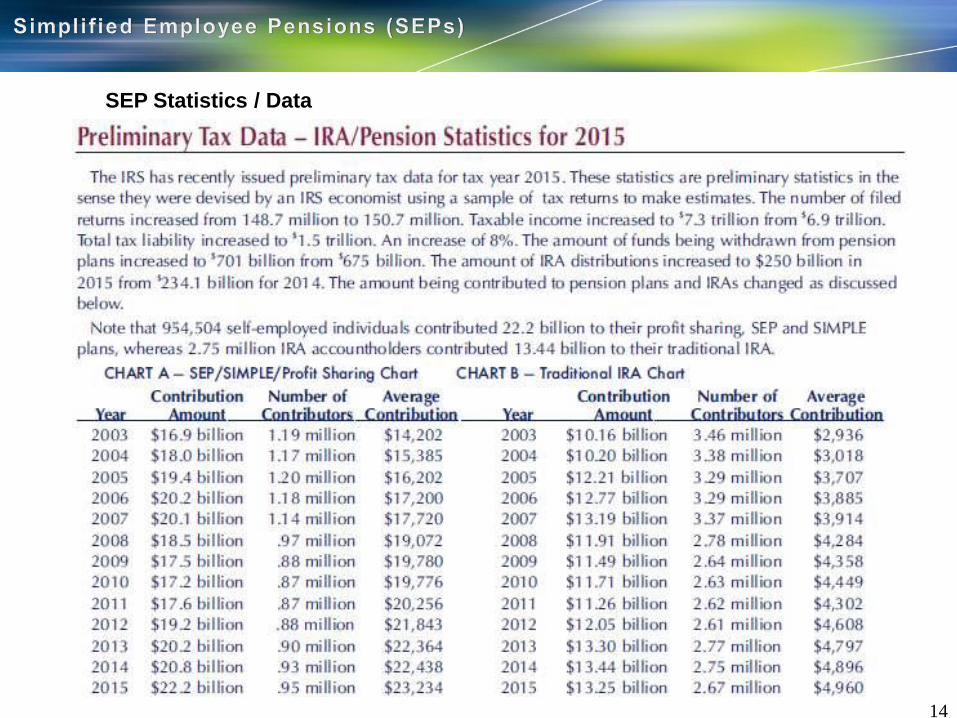

SEP Statistics / Data

1. The percentage begin contributed to each type of IRA has been quite consistent

for the five years or 2004 – 2008 as follows:

2. End-of-Year Fair Market Value 2008

Number of Tax

Payers

FMV Value Percent

Traditional 43,054,097 $3,257,294,689 88.49%

SEP 3,726,835 $201,497,706 5.47%

SIMPLE 2,896,031 $45,634,790 1.24%

Roth 15,951,065 $176,638,800 4.80%

Total 54,497,580 $3,681,065,985 100.00%

IRA Type Percent

Roth IRAs 32.10%

SEP-IRAs 27.00%

Traditional IRAs 24.90%

SIMPLE-IRAs 16.00%

Total 100.00%

13

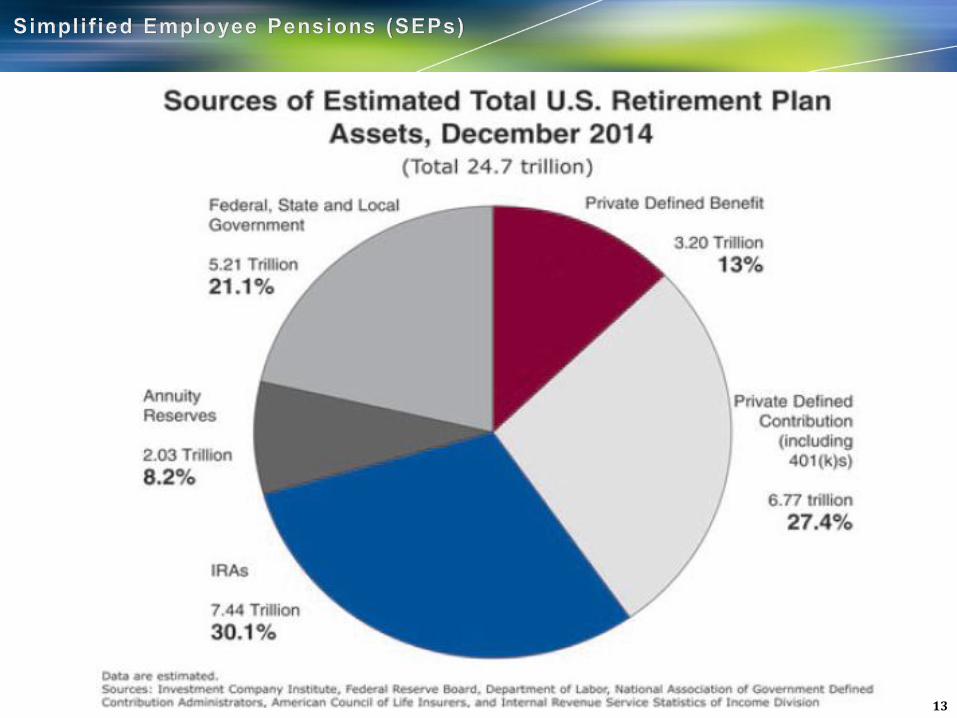

____ 4.8 Trillion

14

SEP Statistics / Data

15

SEP Statistics / Data

16

Tax Benefits of a SEP-IRA

• Tax deferred income. Compounding Growth.

• Contribution is Excludable from Income for numerous taxes: Income, Social

Security, Unemployment, etc.

Example – Betsy Ryan * Wage Income $30,000

SEP Contribution (0-25%) $6,000 (20%)

“Total” Compensation $36,000

*Taxes apply to the $30,000, but not to the $6,000.

Taxes means income, social security, Medicare and

unemployment.

* Betsy is an employee. A special calculation applies

for a self-employed individual.

17

Establishing a SEP

1. Employer signs a SEP plan document

a. IRS Model Form 5305-SEP

b. SEP Prototype, or

c. Customized SEP Document – Prohibitively expensive

2. Each eligible employee, including an employee who is the only employee, must

establish a traditional IRA (a SEP IRA).

Employer has authority to sign on behalf of an employee who refuses to sign.

18

Types of SEP Plan Documents

To establish a SEP, the employer must execute a SEP plan document by the

deadline for filing the business tax return, including extensions. (Treasury Regulation

section 16.408-7) The type of SEP plan the employer executes or adopts may vary,

as SEP plans may be adopted using the IRS Form 5305-SEP (the IRS model SEP

form), a prototype SEP, or an individually-designed SEP. (The IRS also provides a

model salary-deferral SEP plan, Form 5305-A SEP, however, new SAR-SEPs can no

longer be adopted.) The following material discusses some of the features of these

different SEP plans.

19

IRS Form 5305-SEP

A financial institution should, at a minimum, have the IRS Model Form 5305-SEP

available. This form may be obtained at no charge from the IRS, or at a nominal fee

from most forms vendors, such as Collin W. Fritz and Associates. The actual plan

document form is very short and very easy to complete. The portion of the document

to be completed is set forth below.

*

20

Financial institutions should note that the customer has responsibility for accuracy. If

customer uncertainty exists, consultation with his or her tax advisor may be

warranted. Although the customer bears ultimate responsibility for completing these

forms, it’s relatively easy for a financial institution to provide basic assistance, and

therefore reap the benefits of maintaining their SEP account. Filling out the Form

5305-SEP is easy: A. Fill out the name of the business (blank #1);

21

B. Define minimum age for plan participation (blank #2). This is usually 21, or

could be N/A (not applicable) if a one-person business;

C. Set years-of-service requirement (blank #3). This is commonly three years. But

remember that for new businesses a contribution can’t be made until the

requirement is met. N/A may also apply here;

22

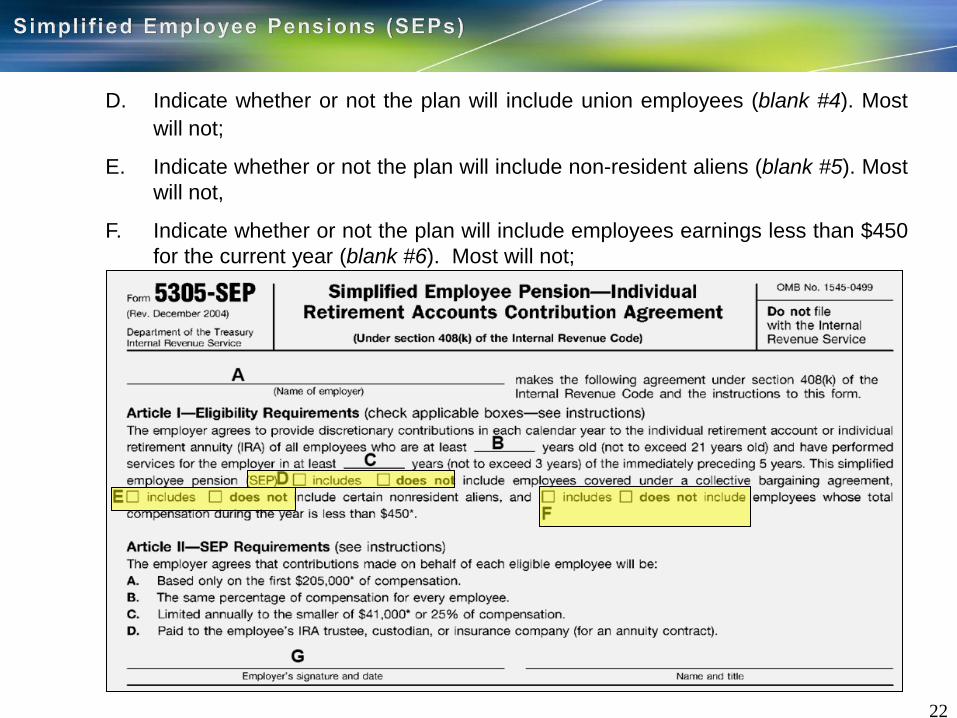

D. Indicate whether or not the plan will include union employees (blank #4). Most

will not;

E. Indicate whether or not the plan will include non-resident aliens (blank #5). Most

will not,

F. Indicate whether or not the plan will include employees earnings less than $450

for the current year (blank #6). Most will not;

23

SEP Limits for 2013 - 2016

2013

2014

2015 & 2016

2017

Maximum Contribution Per Individual $51,000 $52,000 $53,000 $54,000

Required Compensation for Current Year $550 $550 $600 $600

Maximum Compensation which may be

used

$255,000 $260,000 $265,000 $270,00

0

24

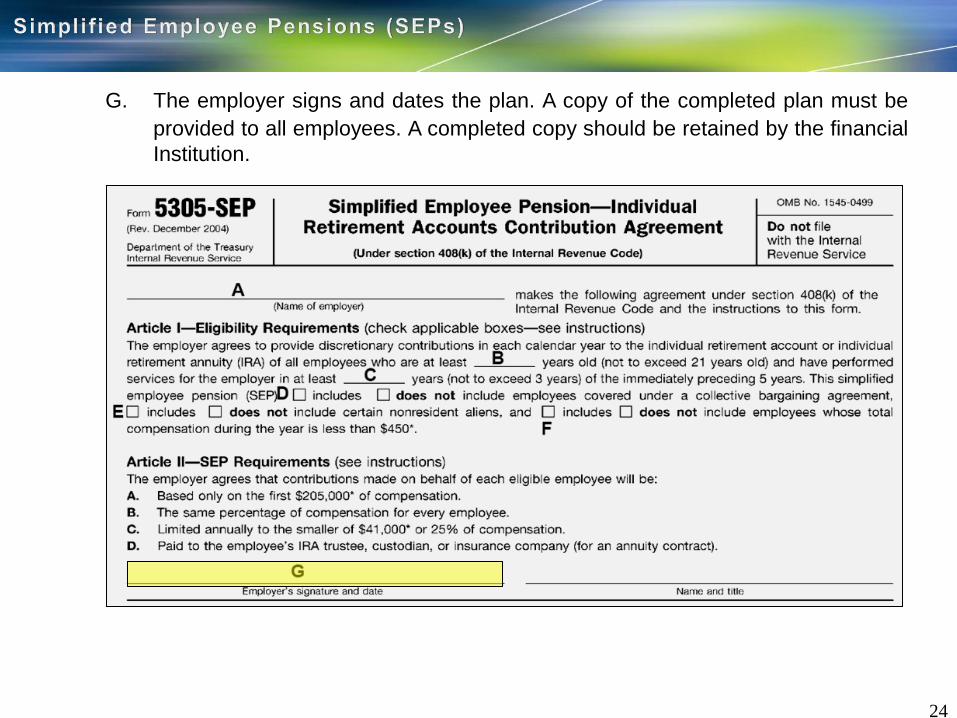

G. The employer signs and dates the plan. A copy of the completed plan must be

provided to all employees. A completed copy should be retained by the financial

Institution.

25

Few plans are simpler to open. If a SEP plan is unavailable to employees, an IRA

custodian/trustee cannot accept deposits in excess of the annual limits of

$5,500/$6,500 as applicable, unless the contribution is a rollover. A signed copy of

Form 5305-SEP is sufficient verification to accept such a contribution.

26

Although many businesses can use IRS Form 5305-SEP, certain employers cannot,

including the following:

• An employer who currently maintains any other retirement plan. Note that this

restriction prevents an employer who has a QP/Keogh plan from using the IRS

Model Form 5305-SEP as the SEP plan document. A SEP prototype, however,

could be used. This restriction does not apply if there are two different

employers.

Example: If a person working for John Deere, Inc. participates in the company’s

profit sharing plan, and this person also farms, then he or she may establish a

SEP for their farm income. As an employer, this person only has one plan—the

SEP. As an employee, he/she participates in two plans. This participation does

not disqualify use of the IRS 5305-SEP form.

• An employer who now, or who has ever, maintained a defined-benefit plan.

• An employer who has any eligible employees for whom IRAs have not been

established.

• An employer who uses the services of leased employees (as described in Code

section 414(n)).

27

Although many businesses can use IRS Form 5305-SEP, certain employers cannot,

including the following:

• An employer who is a member of an affiliated service group (as described in

section 414(m)), a controlled group of corporations (as described in section

414(b)), or trades or businesses under common control (as described in section

414(c)), UNLESS all eligible employees of all the members of such groups,

trades, or businesses, participate under the SEP.

• The 5305-SEP form should only be used if the employer will pay the cost of the

SEP contributions. This form is not suitable for a SEP that provides for

contributions at the election of the employee whether or not made pursuant to a

salary-reduction agreement.

These limits do not apply to employers who adopt either a prototype SEP or an

individually-designed SEP. For example, even though an employer already has a

Keogh plan, he could adopt a SEP plan if he adopted a prototype or individually-

designed SEP.

28

29

30

31

Prototype SEPs

Probably the second most widely used SEP plans are prototype SEPs. Prototype

SEPs are specially designed and drafted plans, typically provided by attorneys and

pension consulting firms. These SEP plans offer all the features of the basic Form

5305-SEP and some additional features which simply are not available with the IRS

SEP document. Prototypes are typically submitted to the IRS for approval. This

means that the form of the plan meets the requirements for a SEP established in the

Internal Revenue Code and Treasury Regulations. Because of this special drafting

and submission to the IRS, prototypes have administrative expenses which either the

financial institution or the adopting employer must absorb. Prototypes can offer

several benefits which are not included in Model SEPs. These benefits are discussed

later.

32

Individually-Designed SEP Plans

Certainly the least common of the different types of SEP plans, the individually-

designed SEP is—as it sounds—individually designed for a particular employer. This

is almost certain to be considerably more expensive than a prototype SEP, as the

drafter, probably an attorney, must bill many hours of work to one employer. Social

Security integration is permissible with the individually-designed SEP, if this feature is

provided for in the plan. However, rather than incurring this expense for a

nonqualified plan, employers are probably going to get more plan for their pension

dollar by using either a prototype SEP or a qualified plan.

Cost prohibitive IRS filing Fee.

33

The Role of the Financial Institution

Important Determination – Are you servicing the employer and the

employee or just an employee? In some cases you will be servicing a

person who works for a company which sponsors a SEP. You may have no

relationship with the employer. An employer is required to furnish a copy of

its SEP plan to every eligible employee. You will want to ask your customer

to furnish you with a copy also. Be aware of section 1.12 of Article VIII

which reads as follows:

Special Terms Regarding SEP-IRA Contributions. Your IRA may accept

SEP-IRA contributions which are made either by your employer or, if you are

self-employed, by yourself. You hereby acknowledge that we have no

responsibility or duty to determine your eligibility for such contributions or the

correctness of the contribution amount. This is true even if we furnished you a

copy of the IRS model Form 5305-SEP or Form 5305A-SEP or SEP prototype.

You also acknowledge that you could well have excess IRA contributions if your

employer (or you, as the employer) makes a mistake as to which employees of

the sponsoring business are entitled to be allocated a share of the employer

contribution and the amount of each allocation. Other administrative errors

could also occur. Therefore, you agree to hold us harmless with respect to any

and all adverse tax consequences (e.g. excess contributions) which arise or

may arise as a result of your employer (or you, as the employer) making such

administrative error(s).

34

The Role of the Financial Institution

General approach — the employer will look to a financial institution to

provide a SEP plan document. A financial institution that is considering

entering the SEP market needs to decide what type of SEP plan document

they will make available to their employer customers and what role the

institution will play in the administration of the SEP plan.

35

The Role of the Financial Institution

Most financial institutions will not want to render administrative services.

Most financial institutions choose to limit their role to being the IRA

custodian. This is true for both one-person businesses and businesses with

more than one person. Some institutions may choose to render

administrative services.

36

The Role of the Financial Institution

We strongly recommend that the institution at which the employer

establishes the SEP plan use a SEP service agreement. The purpose of the

agreement is to make clear to the customer exactly what your financial

institution will do and to make clear the fact that your institution does not

have the duty to make sure the business customer is administering the SEP

correctly.

A sample service agreement follows.

The IRA custodian/trustee does have the duty to prepare the Form 5498

and Form 1099-R with respect to SEPs. Since 1996, there has been a

check box added to Form 5498, Individual Retirement Arrangement (IRA)

Information, to indicate if the IRA is part of a SEP. This enables the Service

to match this information with an IRA owner’s W-2, to identify employers

maintaining SEPs.

37

CWF 702

IRS Form 5305-SEP or

IRS Form 5305A-SEP

38

FAQs regarding SEPs

What is a SEP?

A SEP is a simplified employee pension plan. A SEP plan provides employers with a

simplified method to make contributions toward their employees’ retirement and, if

self-employed, their own retirement. Contributions are made directly to an Individual

Retirement Account of Annuity (IRA) set up for each employee (a SEP-IRA).

Note: The IRS has a system of correction programs for sponsors of retirement plans,

including SEPs, which are intended to satisfy Internal Revenue Code requirements

but have not met the requirements for a period of time. This system, the Employee

Plan Compliance Resolution System (EPCRS), permits employers to correct plan

failures and thereby continue to provide their employees with retirement benefits on a

tax-favored basis.

39

How is a SEP established ?

A SEP is established by adopting a SEP agreement and having eligible employees

establish SEP-IRAs. There are three basic steps in setting up a SEP, all of which

must be satisfied.

• A formal written agreement must be executed. This written agreement may be

satisfied by adopting an Internal Revenue Service (IRS) model SEP using Form

5305-SEP, Simplified Employee Pension – Individual Retirement Accounts

Contribution Agreement. A prototype SEP that was approved by the IRS may

also be used. Approved prototype SEPs are offered by banks, insurance

companies, and other qualified financial institutions. Finally, an individual

designed SEP may be adopted.

• Each eligible employee must be given certain information about the SEP. If the

SEP was established using the Form 5305-SEP, the information must include a

copy of the Form 5305-SEP, its instructions, and the other information listed in

the Form 5305-SEP instructions. If a prototype SEP or individually designed

SEP was used, similar information must be provided.

• A SEP-IRA must be set up for each eligible employee. SEP-IRAs can be set up

with banks, insurance companies, or other qualified financial institutions. The

SEP-IRA is owned and controlled by the employee and the employer sends the

SEP contributions to the financial institution where the SEP-IRA is maintained.

40

If an employer sets up a SEP plan for its employees, can each employee

choose different financial institutions for his or her SEP-IRA ?

That depends on the SEP plan the employer chooses. Each employee (including the

business owner) eligible to participate in the SEP generally must establish his or her

own SEP-IRA to receive employer contributions. Although the law does not require

each participant’s SEP-IRA to be at the same financial institution, the institution that

offers or administers the SEP may require the employer to deposit SEP contributions

initially into SEP-IRAs maintained at that institution. Employers should read the SEP

plan document carefully and make sure they understand the plan’s terms before

signing.

41

What types of employers can establish a SEP ?

Any employer can establish a SEP.

42

If an employer has a SEP can it also have other retirement plans ?

An employer can maintain both a SEP and another plan. However, unless the other

plan is also a SEP, the employer cannot use Form 5305-SEP, the employer must

adopt either a prototype SEP or an individually designed SEP.

43

If an employee participates in his or her employer’s retirement plan, can he or

she set up a SEP for self-employment income ?

Yes. A SEP can be set up for a person’s business even if he or she participates in

another employer’s retirement plan.

44

Is there a deadline to set up a SEP ?

A SEP can be set up for a year as late as the due date (including extensions). Of the

business’s income tax return for that year.

45

Can each partner in a partnership maintain a separate SEP plan ?

No. Only an employer can maintain and contribute to a SEP plan for its employees.

For retirement plan purposes, each partner or member of an LLC taxed as a

partnership is an employee of the partnership.

The Partnership:

• Deducts plan contributions for employees other than the partners as a business

expense on Form 1065. U.S. Return of Partnership income (instructions).

• Reports plan contributions for partners on each partner’s Schedule K-1 (Form

1065), Partner’s Share of Income, Deductions, Credits, etc. (instructions).

46

What happens if an employee elects not to participate ?

The employer may establish a SEP-IRA on behalf of an employee who is entitled to a

contribution under the SEP if the employee is unable or unwilling to establish a SEP-

IRA.

47

How much may be contributed to a SEP ?

Annual contributions an employer makes to an employee’s SEP-IRA cannot exceed

the lesser of:

1. 25% of compensation, or

2. $52,000 for 2014, $53,000 for 2015 & 2016, and $54,000 for 2017 (subject to

annual cost-of-living adjustments for later years).

The limits in the preceding sentence apply in the aggregate to contributions an

employer makes for its employees to all defined contribution plans, which includes

SEPs. Only up to $267,000 in 2017 (subject to annual cost-of-living adjustments for

later years) of an employee’s compensation may be considered. Contributions must

be made in cash. Property cannot be contributed.

48

What is considered compensation ? Are bonuses and overtime included ?

Compensation considered is defined by the Internal Revenue Code and would

include bonuses not overtime.

49

How much may a self-employed individual contribute ?

The same limits on contributions made to employees’ SEP-IRAs also apply to

contributions made to a self-employed individual’s SEP-IRA. However, special rules

apply when figuring out the maximum deductible contribution. See Publication 560

for details on determining the contribution amount.

50

Must the same percentage of salary/wages be contributed for all participants ?

Most SEPs, including the IRS model Form 5305-SEP, require that allocations to all

employees’ SEP-IRA be proportional to their salary/wages. A self-employed owner’s

contribution is based on net profit minus one-half self-employment tax for him or

herself. See IRS Publication 560 on determining the contribution amount.

51

Can SEP plan participants make tax-deductible IRA contributions to their SEP-

IRAs ?

Employers contribute under a SEP plan to each participant’s SEP-IRA, and a SEP-

IRA is generally no different from any traditional IRA. Employer SEP contributions do

not affect the amount a participant can contribute to an IRA. SO, assuming the SEP-

IRA permits non-SEP contributions, regular IRA contributions can be made by the

participant to his or her SEP-IRA, up to the maximum annual limit. However, the

amount of the regular IRA contribution that can be deducted on the employee’s

income tax return may be reduced or eliminated due to the employee’s participation

in the SEP plan. See Publication 590, Individual Retirement Arrangements (IRAs),

for more information on contribution and deduction limits.

52

Can catch-up contributions be made to a SEP ?

No. SEPs are funded by employer contributions only. However, catch-up

contributions can be made to the IRAs that hold the SEP contributions if the SEP-IRA

documents allow. The catch-up IRA contribution amount (for employees age 50 and

older) is $1,000.

53

Can a contribution be made to a SEP-IRA of a participant over age 70 ½?

Contributions must be made for each eligible employee in a SEP, even if over age

70½. Such an employee must take minimum distributions, however.

54

Must contributions be made to the SEP every year ?

No. Contributions are not required to be made every year, but in years contributions

are made to the SEP, the must be made to the SEP-IRA of all eligible employees.

55

Do contributions have to be made for a participant who is no longer employed

on the last day of the year ?

A SEP cannot have a last-day-of-the-year employment requirement. If the employee

is otherwise eligible, they must share in any SEP contribution. This includes eligible

employees who die or quit working before the contribution is made.

56

What is the timeframe for depositing contributions into SEP IRAs ?

The employer must deposit contributions for a year by the due date (including

extensions) for filing its Federal income tax return for the year. Note: If the employer

extends its tax return the it has until the end of that extension period to deposit the

contribution, regardless of when it filed the tax return. However, if the employer did

not deposit the contribution timely, it must amend the tax return and pay any tax,

interest and penalties that may apply.

57

Are employer contributions taxable to employees ?

No. Contributions to employee’ SEP-IRAs are not included in their gross income,

unless they are excess contributions.

58

What are the consequences to employees if excess contributions are made ?

If contributions are made in an amount that is more than is allowed, there are tax

implications for the employer and the employees. Excess contributions are included

in the employees’ gross income. If an employee withdraws the excess contribution,

and earnings on such amount, before the due date for filing his or her return,

including extensions, the employee will avoid a 6% excise tax imposed in excess

SEP contributions in an IRA. Excess contributions left in the employee’s SEP-IRA

after that time may result in adverse tax consequences to the employer and

employee. If the employer contributes more than it may deduct, it may be subject to

a 10% excise tax.

59

If a SEP fails to meet the SEP requirements, are the tax benefits for the

employer and employees lost ?

Generally, tax benefits are lost if the SEP fails to satisfy the Internal Revenue Code

requirements. However, the employer can retain the tax benefits if it uses one of the

IRS Correction programs to correct a failure. In general, when correcting a failure

under the program, the correction should put employees in the position they would

have been had the failure not occurred.

60

Why is the 2015 contribution that was made in 2016 for the SEP-IRA shown on

the 2016 Form 5498 and not on a 2015 Form 5498 ?

The IRS requires that contributions to a SEP-IRA be reported on the Form 5498 for

the year they are actually deposited to the account, regardless of the year for which

they are made.

61

Can I contribute to both a SEP-IRA and a Roth IRA ?

A SEP-IRA is a traditional IRA that holds contributions made by an employer under a

SEP plan. An employee can both receive employer contributions to a SEP-IRA and

make regular, annual contributions to a traditional or Roth IRA. Employer

contributions made under a SEP plan do not affect the amount an employee can

contribute to an IRA on the own behalf.

Because a SEP-IRA is a traditional IRA, an employee may be able to make regular,

annual IRA contributions to this IRA. Any such dollars contributed by the employee

to his or her SEP-IRA will reduce the amount that could otherwise be contributed to

other IRAs, including Roth IRAs, for the year.

62

Does a SEP have to be amended for the new law before it terminates ?

Generally, the IRS has not required SEPs to be amended for new law prior

termination. Check with your plan professional.

63

Does a SEP have to be funded in the year of termination ?

SEPs can be terminated at any time. The employer can stop funding these plans

once they are terminated.

64

What are the notification requirements to participants, etc., when a SEP

terminates ?

When terminating a SEP plan, it is a good idea to notify the employees that the plan

has been discontinued. The financial institution that was chosen to handle the plan

may need to be notified that there will be no more contributions. The employer may

also need to let the institution know that it will terminate the contract or agreement

with it. The IRS should not be notified of the plan’s termination.

65

If the employer goes out of business or the employee terminates service, can

the amount in a SEP-IRA be left untouched ?

Yes.

66

SEP: Overview of Rules and Tax Regulations

What amount can the employer deduct each

year?

The maximum amount is 25% of the eligible

employees’ compensation paid to them during

the year. Compensation for common-law

employees is their income as shown on Form

W-2. Compensation for a self-employed

individual is defined to be his or her net earnings

from self-employment as reduced by the

deduction one is allowed for one-half of his or

her self-employment tax and the deduction of

contributions on his or her behalf to the plan.

How much can be contributed on my behalf?

In general, the lesser of 25% of compensation or

$53,000.

67

SEP: Overview of Rules and Tax Regulations

What is meant by the term “Self-Employed

Person’s Rate Table”?

Because a self-employed person’s deduction

amount and his or her compensation are each

dependent on the other, the adjustment to net

earnings can be made indirectly by using an

adjusted contribution rate as determined from

the chart on this page.

What are net earnings from self-

employment?

For SEP purposes, your net earnings are your

gross income from your business minus

allowable deductions for that business.

Allowable deductions include contributions to

your employees’ SEP-IRAs. You also take into

account the deduction allowed for one-half of

yourself-employment tax, and the deduction for

contributions to your own SEP-IRA

68

SEP: Overview of Rules and Tax Regulations

Include the following items in your net earnings.

A. Foreign earned income and housing cost amounts.

B. If you are a partner, your distributive share of partnership income or loss (other

than separately treated items such as capital gains and losses).

C. If you are a limited partner, guaranteed payments for services to or for the

partnership.

D. Elective contributions or deferrals under any of the following plans.

1. 401(k) plans.

2. 403(b) plans (tax-sheltered annuities).

3. SEP plans (salary-reduction arrangements).

4. Savings incentive match plans for employees (SIMPLE plans).

5. Cafeteria plans.

6. 457 plans (plans of state and local governments and certain tax-exempt

organizations).

Do not include the following items in your net earnings.

• Tax-free items (or deductions related to them).

• If you are a limited partner, distributions of income or loss.

69

SEP: Overview of Rules and Tax Regulations

In addition to the tax deduction limits, are there any limits on the amount an

employer can contribute to one or more retirement plans on behalf of any one

participant?

Yes. In general, an employer, for 2002 and subsequent years, cannot contribute on

behalf of any participant, more than the lesser of 100% of compensation, or $40,000.

For 2001, the percentage limitation was 25%.

• The $40,000 increased to $41,000 for 2004,

• $42,000 for 2005,

• $44,000 for 2006,

• $45,000 for 2007,

• $46,000 for 2008 and

• $49,000 for 2009-2011

• $50,000 for 2012.

• $51,000 for 2013.

• $52,000 for 2014

• $53,000 for 2015-2016

• $54,000 for 2017

Special tax rules will apply if the

employer sponsors plans in addition

to a SEP, such as a profit sharing,

money purchase, or defined benefit

plan.

70

SEP: Overview of Rules and Tax Regulations

When can a SEP be established?

SEPs can be established for a particular year after that year has ended. They can be

established as late as the latest time prescribed by law for making deductible

employer contributions (that is, no later than the due date, including extensions, of

the employer’s tax return for the year). This is more generous than the rule for

qualified plans under IRC section 401(a). A qualified plan must be executed by the

end of the taxable year for which the employer wants to take a deduction.

What is the contribution deadline?

The employer’s contribution deadline is the due date of that year's business tax

return, including any extensions. For many corporations, this is March 15, plus

extensions. For most individuals, this is April15, plus extensions.

Can an employer prohibit distributions from an employee’s SEP-IRA?

No. Also, an employer cannot condition its SEP contributions on the keeping of any

part of them in the IRA.

71

SEP: Overview of Rules and Tax Regulations

When must a person start to withdraw the money from the SEP-IRA?

With certain exceptions, a person must begin distributions by the first day of April

following the calendar year in which he or she attains age 70½, and December 31 of

each year thereafter.

Can an employee make regular IRA contributions into a SEP-IRA?

The answer is generally “Yes." However, the extent to which a deduction will be

allowed for the contribution may be limited by participation in the SEP or any other

qualified pension plan. The employee should consult with their tax advisor to

determine the amount of deductible and nondeductible contribution(s) available to

them.

How will distributions be taxed?

Distributions will be taxed as ordinary income. If the participant is under age 59½,

penalties may apply.

72

SEP: Overview of Rules and Tax Regulations

How do my employer’s contributions affect my taxes?

Your employer’s contributions to your SEP-IRA are excluded from your income rather

than deducted from it. Your employer’s contributions to your SEP-IRA should not be

included in your wages on your Form W-2 unless there are contributions under a

salary-reduction arrangement.

Unless there are excess contributions, you do not include any contributions in your

gross income; nor do you deduct any of them.

What are excess contributions?

If your employer contributes more than is allowed, you must include the excess in

your gross income, without any offsetting deduction.

How do I correct an excess contribution?

You should follow the instructions set forth in IRS Publication 590.

73

SEP: Overview of Rules and Tax Regulations

What happens to a SEP-IRA when the participant dies?

The funds in a SEP will be paid to a participant’s beneficiaries. Depending on their

relationship to the participant, they may have the potential to partially continue to

shelter the funds from current taxation. The standard IRA rules apply.

May a SEP be integrated with social security?

Yes. An integrated SEP will permit a somewhat higher contribution percentage to be

given to the more highly compensated employees. Integration may be permissible

with a SEP prototype, but it is not permissible under the IRS Model Form 5305-SEP.

Who is responsible to administer the SEP?

The sponsoring employer is responsible for the SEP’s administration. The employer

may well need to consult with its tax and legal advisor. A financial institution’s general

role is to serve as the depository and not as the plan administrator.

74

SEP: Overview of Rules and Tax Regulations

What is a Salary-Reduction SEP (SAR-SEP), and what advantages does it

offer?

An employer is not permitted to establish a salary-reduction SEP after December 31,

1996. SAR-SEPs established before January 1, 1997, can continue to receive

contributions under present rules, and new employees of the employer, hired after

December 31, 1996, can participate in the SAR-SEP in accordance with the rules.

You should review IRS Publications 560 and 590 for additional information.

Is a SEP deposit insured by the FDIC?

If a SEP-IRA is invested in time deposits or savings instruments in an insured

financial institution, it is insured by the appropriate government agency up to

$250,000, aggregated with any traditional IRA, Roth IRA and any self-directed Keogh

plan, eligible deferred compensation plans, and any individual account as defined in

section 3(34) of ERISA. This $250,000 aggregate limit applies on a per-participant,

per-institution basis.

If the SEP-IRA is not invested in time deposits or savings accounts of an insured

institution, then such investments are not insured by the FDIC.

75

Trustee-to-Trustee Transfer

• Move IRA Asset from one IRA to another , one IRA custodian/trustee to another

IRA custodian/trustee, on a Tax-Free Basis

• Requirements:

Check/Draft/Wire made payable to new IRA Custodian/trustee

• No IRS Limit

Reasonable Custodian/trustee restrictions allowed

Not Reportable to IRS

• Federal Income Tax withholding rules do not apply

“ABC Financial Institution as Custodian/Trustee for John Jones’

(traditional, SEP, SIMPLE, Roth) IRA”

76

Trustee-to-Trustee Transfer

• Transfer must be from same type of IRA

• Traditional IRA to Traditional IRA

• Traditional IRA to SEP IRA

• SEP IRA to SEP IRA

• SEP IRA to Traditional IRA

• Roth IRA to Roth IRA

• SIMPLE IRA to SIMPLE IRA

• SIMPLE IRA to Traditional IRA (SIMPLE 2 Year Holding Period)

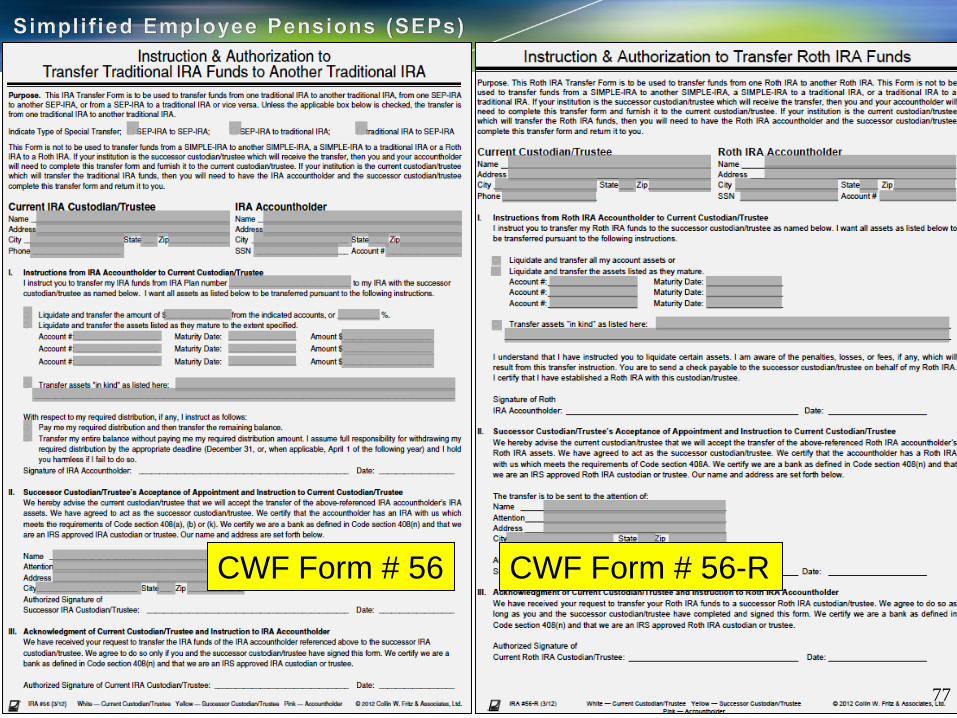

CWF Form # 56 CWF Form # 56-R

77

78

IRA to IRA Rollovers

• Purpose

Usually to move IRA assets from one IRA to another IRA

Rollover can be brought back to the same IRA

• Requirements

• One rollover per IRA, per 12 month period – Not one per investment

• Check/Draft/Wire is made payable to or for the IRA accountholder

• IRA Assets must be deposited into IRA within 60 calendar days

• Must be same type of IRA

• Traditional IRA to Traditional IRA

• Traditional IRA to SEP IRA

• SEP IRA to SEP IRA

• SEP IRA to Traditional IRA

• Roth IRA to Roth RIA

• SIMPLE IRA to SIMPLE IRA

• SIMPLE IRA to Traditional IRA (SIMPLE 2 Year Holding Period)

79

IRA to IRA Rollovers

• Requirements (Continued)

• Rollovers are reportable to the IRS

• Distributions for Form 1099-R – Regular IRA Reporting Codes

• Rollover contributions on Form 5498 Box 2

• 60 Day Rule

80

Summary of Reporting Duties for SEPs

Form 5498, IRA Contribution Information, must be submitted to the Service by the

trustee or issuer of a SEP-IRA to report contributions to the SEP-IRA under a SEP

plan. A separate Form 5498 must be submitted for each SEP-IRA.

Form 1099-R, Distributions from Pensions, Annuities, Retirement or Profit-Sharing

Plans, IRAs, Insurance Contracts, etc., is used to report distributions from a SEP-

IRA.

81

Reporting Contributions

Reporting SEP contributions continues to be an unnecessarily complex problem. The

procedure is actually quite logical and easy. The problem is that software has not

caught up with the 1996 change. SEP contributions are reported on the IRS Form

5498 based on the calendar year of receipt by the custodian/trustee, not based on

the tax year the contribution is for. Said another way, SEP contributions are reported

IN the year they are received NOT FOR the year they are received. Even though the

custodian/trustee must report the contributions in the year they are received, the

employer can deduct the SEP contributions in the proper tax year on their tax

returns, as long as the contributions were made correctly and timely.

82

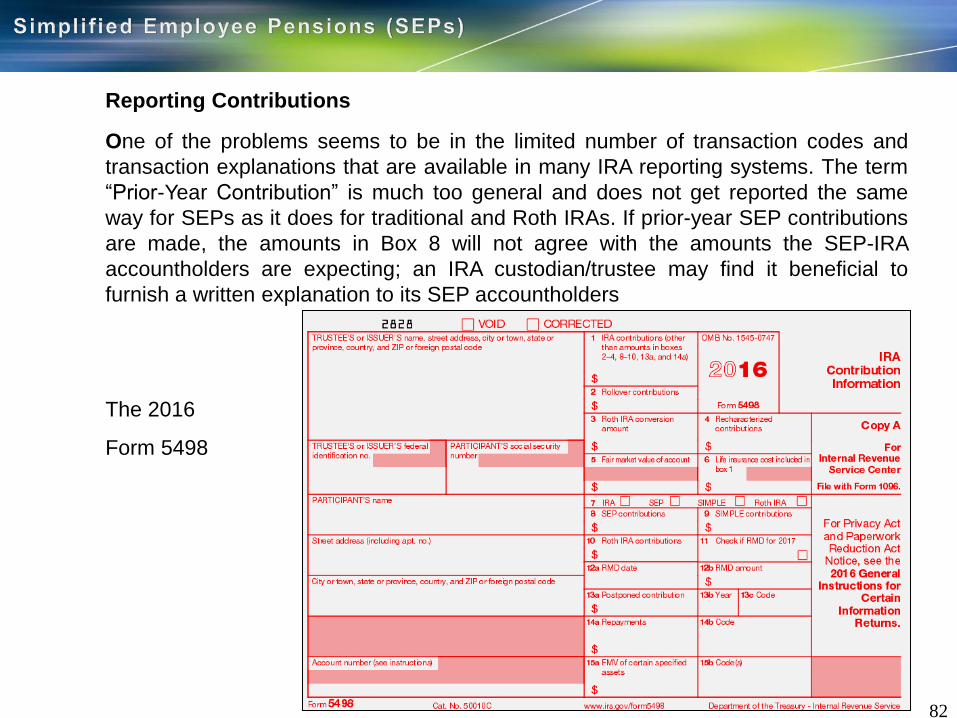

Reporting Contributions

One of the problems seems to be in the limited number of transaction codes and

transaction explanations that are available in many IRA reporting systems. The term

“Prior-Year Contribution” is much too general and does not get reported the same

way for SEPs as it does for traditional and Roth IRAs. If prior-year SEP contributions

are made, the amounts in Box 8 will not agree with the amounts the SEP-IRA

accountholders are expecting; an IRA custodian/trustee may find it beneficial to

furnish a written explanation to its SEP accountholders

The 2016

Form 5498

83

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

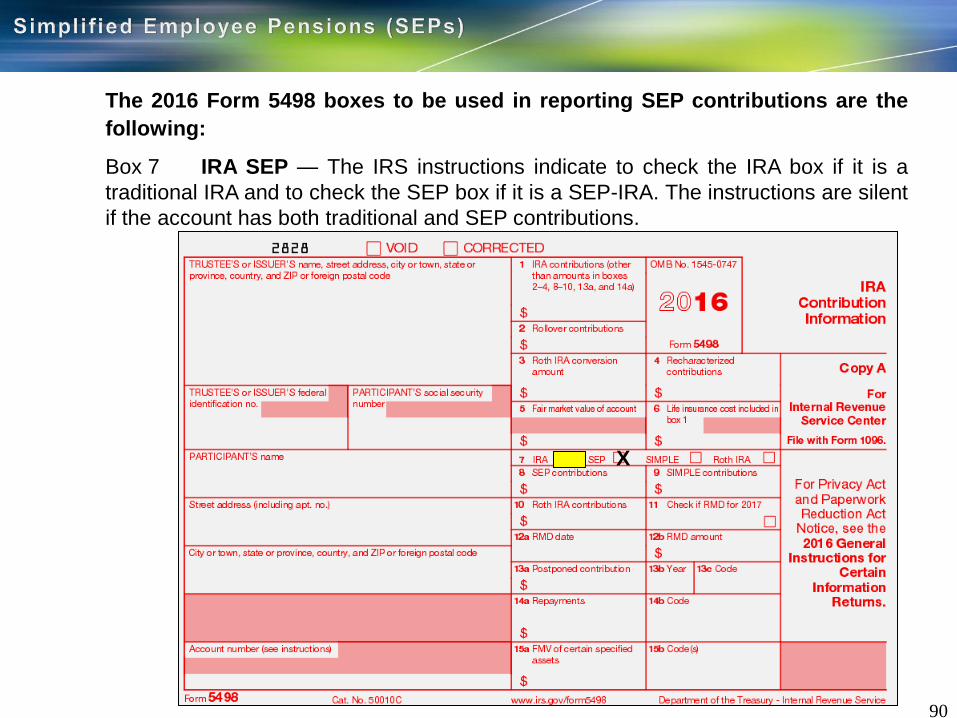

Box 7 IRA SEP — The IRS instructions indicate to check the IRA box if it is a

traditional IRA and to check the SEP box if it is a SEP-IRA. The instructions are silent

if the account has both traditional and SEP contributions.

X

84

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

Box 8 SEP Contributions — Insert the aggregate amount of employer

contributions made from January 1 to December 31, 2016, regardless of the tax year

for which the contribution(s) were made.

X

20000.00

85

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

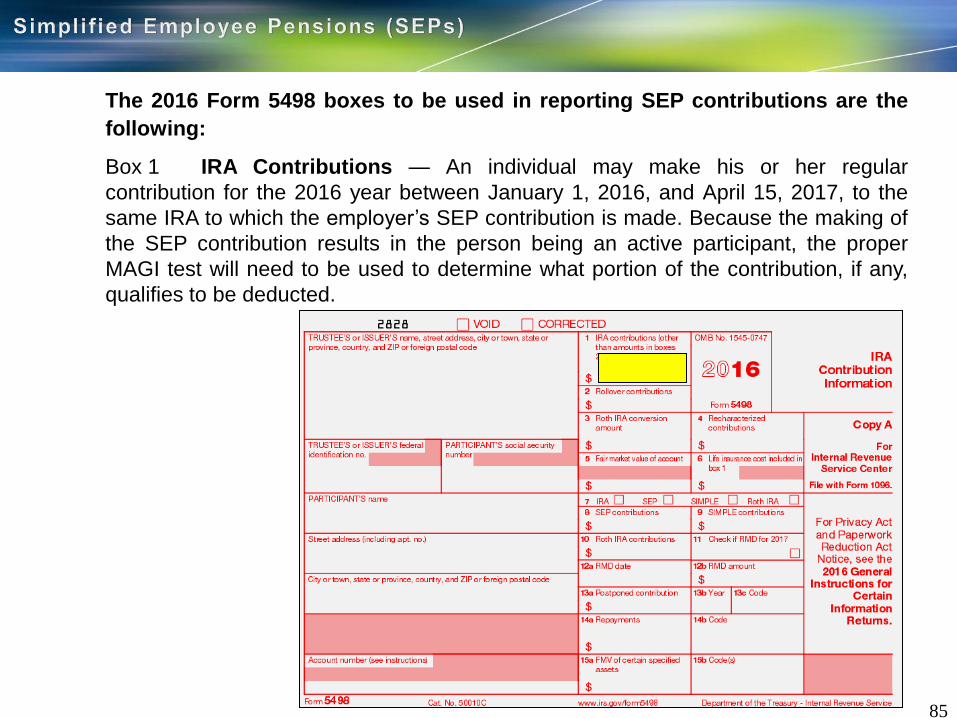

Box 1 IRA Contributions — An individual may make his or her regular

contribution for the 2016 year between January 1, 2016, and April 15, 2017, to the

same IRA to which the employer’s SEP contribution is made. Because the making of

the SEP contribution results in the person being an active participant, the proper

MAGI test will need to be used to determine what portion of the contribution, if any,

qualifies to be deducted.

86

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

Box 2 Rollover contributions — If there are any rollovers into the SEP-IRA

during the period of January 1 - December 31, 2016, the amounts are reported here.

87

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

Box 4 Recharacterizations — It is possible for a SEP-IRA to also have

traditional IRA contributions. Therefore it is possible to have a recharacterization in

an IRA that has both SEP and traditional IRA contributions. However, SEP

contributions cannot be recharacterized.

88

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

Box 5 Fair market value of account — The December 31, 2016, FMV is

reported here. It must agree with the year-end FMV statement sent to the

accountholder in January 2017.

89

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

Box 6 Life insurance cost included in box 1 — This box is not used for SEP-

IRAs.

90

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

Box 7 IRA SEP — The IRS instructions indicate to check the IRA box if it is a

traditional IRA and to check the SEP box if it is a SEP-IRA. The instructions are silent

if the account has both traditional and SEP contributions.

X

91

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

Box 8 SEP Contributions — Insert the aggregate amount of employer

contributions made from January 1 to December 31, 2016, regardless of the tax year

for which the contribution(s) were made. Any elective deferral contributions made

under a SAR-SEP are deemed to be employer contributions.

X

20000.00

92

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

Box 10 Roth IRA contributions — Since Roth IRA contributions cannot be made

into a traditional or SEP-IRA, this box is not used for SEP-IRAs.

93

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

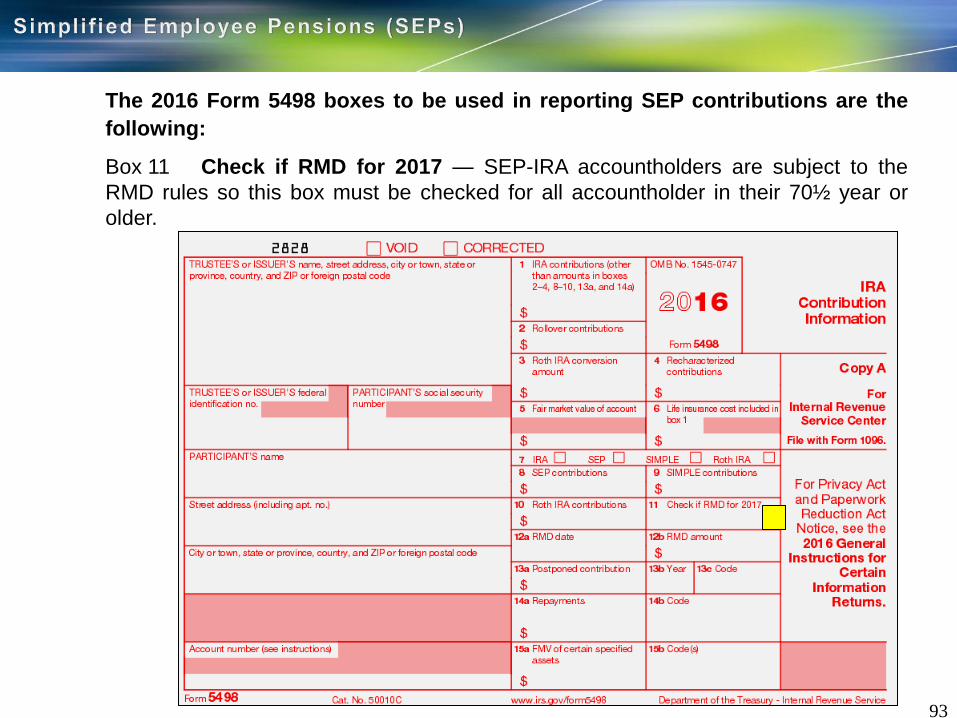

Box 11 Check if RMD for 2017 — SEP-IRA accountholders are subject to the

RMD rules so this box must be checked for all accountholder in their 70½ year or

older.

94

The 2016 Form 5498 boxes to be used in reporting SEP contributions are the

following:

Boxes 12a through 14b — Any of the transactions that apply to traditional IRAs, can

also apply to SEP-IRAs. Consequently any of these boxes can be used with SEP-

IRAs.

Example 1: James Smith, self-employed consultant, contributes his 2015 SEP

contribution, in the amount of $5,000, on April 15, 2016. This must be reported by the

custodian/trustee on the 2016 5498, NOT THE 2015 5498. However, Mr. Smith is

allowed to deduct the contribution on his 2015tax return.

Example 2: James Smith, self-employed consultant, contributes his 2015 SEP

contribution, in the amount of $4,000, on August 15, 2016. This must be reported by

the custodian/trustee on the 2016 5498.

95

Reporting Distributions

Trustees and custodians of IRAs must keep track of SEP-IRA activity and also report

when there are distributions from the SEP-IRA. Form 1099-R is used to report all

distributions from the SEP-IRA. There is no specific distribution code for distributions

from a SEP-IRA.

96

Special Explanation for Your SEP Customers—Reporting SEP Contributions to

the IRS

An IRA custodian may use the following explanation (by making a copy) to explain to

your SEP customer how SEP contributions are reported to the IRS. The purpose of

this explanation is to detail how an IRA custodian is required to report contributions to

an employer’s SEP-IRA to the IRS on Form 5498.

When an IRA custodian receives a contribution to an employer’s SEP-IRA, the

custodian is to consider the contribution made by the “employer” for benefit the

“employee.” If a business is unincorporated, the “employer” is considered to be self-

employed, and will either be an individual (i.e. sole proprietor) or a partnership. When

an individual is self-employed, he/she is both the “employee” and the “employer.”

The SEP-IRA custodian reports the SEP-IRA contribution in Box 8 of the Form 5498

for the year in which the contribution is received, regardless of the employer’s tax

year for which it was contributed. The reason for this is that the employer’s deadline

for making its SEP contribution is its tax-filing dead-line plus extensions.

The April 15 deadline which applies to traditional and Roth IRAs does not apply to

SEP-IRA contributions. The “plus extension” rule means that a business (i.e. the

employer) may make its contribution for the prior year after May 31 of the current

year (e.g. on August 13, 2017, an employer may contribute funds for the 2016 tax

year).

97

The IRS instructions to the participant for Box 8 of the 2016 Form 5498 read as

follows:

“Shows SEP contributions made in 2016 including contributions made in 2016 for

2015, but not including contributions made in 2017 for 2016. If made by your

employer, do not deduct on your income tax return. If you made the contributions as

a self-employed person (or partner), they may be deductible. See Publication 560.”

Tax Reporting by the Employer— The business entity is entitled to claim a tax

deduction on the tax return for which the contribution was designated. The Form

5498 does not inform the IRS of the employer’s tax year for which the contribution

was made. It merely informs the IRS of the fact that an employer made a contribution

on behalf of an employee during a specific calendar year.

98

Special Rules for Self-Employed Individuals

Special rules apply for self-employed individuals. A self-employed individual does

take a deduction for his or her SEP contribution. That is, the contribution amount is

not excluded from their gross income, as their gross income includes their business

income. It appears that a self-employed person is required to pay FICA (self-

employment, too) on the amount of his or her pension contributions. However, a

special calculation is used to determine the “compensation” that a self-employed

individual uses to determine his or her contributions. The person must reduce their

earned income by the amount of the contribution to be made for himself or herself

and by the deduction they are permitted for a portion of the self-employment tax they

pay.

The mathematical formula to be used for “net earnings” is:

Step 1 Self-Employed Earned Income

Step 2 Minus ½ Self-Employment Tax

Step 3 Minus Pension Contribution for the Self-Employed Individual

Step 4 Equals Adjusted Earnings

Step 5 Multiplied by Contribution Percentage Per Plan

Step 6 Equals Pension Contribution for Self-Employed Individual

99

Special Rules for Self-Employed Individuals

In general, the deduction amount for self-employment taxes equals 50% of the

amount which he or she must pay in self-employment taxes.

Most financial institutions leave it up to the self-employed individual and his or her tax

advisor to determine the maximum deductible contribution. Because the deduction

amount and the net earnings amount are each dependent on the other, this

adjustment can present a problem. To solve this problem, adjustments are made

indirectly by reducing the contribution rate called for in the plan, in figuring the

maximum deduction.

Internal Revenue Code section 1401 and 1402 define the assessment of the self-

employment tax. Section 1402(a) defines net earnings as gross income from a trade

or business, less related business expenses, less the deduction provided by

1402(a)(12). Subsection (12) provides for a special deduction equal to the net

earnings (determined without regard to this paragraph) times 50% of the sum of the

tax rates of section 1401(a) and (b) for such year.

100

Special Rules for Self-Employed Individuals

Set forth below is a an example of how the formula works. Net earnings are

$100,000.

This example assumes the self-employment tax to be $13,266. Thus, the $100,000 is

to be reduced by $6,633 (50% of $13,266 and then multiplied by the special

percentage of 20.00%). The proper contribution amount is then $18,673.00.

This chart can be used to determine steps 2 and 3 of the calculation.

Although the above paragraphs have discussed calculating the permissible SEP

contribution for a self-employed individual, it is desirable to have the customer

assume the responsibility of determining the proper contribution after consulting with

his/her tax advisor.

The IRS has devised the following worksheet as shown in Publication 560,

Retirement Plans for Small Businesses.

$100,000.00 (Net Income)

-6,633.00 (½ of Social Security Tax)

$93,367.00

X .20 (Equivalent of 25%)

$18,673.00 (SEP Contribution)

101

SEP Contributions and IRA Contributions for the Same Year

A person may make both a traditional IRA contribution and a SEP contribution for the

same tax year, or a person may make a traditional IRA contribution even though his

or her employer has made a SEP contribution for the same tax year. The general

rule, however, is that the SEP contribution will make a person an active participant

for IRA deduction purposes. Whether or not the person will be able to claim a tax

deduction will depend upon applying the appropriate modified adjusted gross income

limits. A person may also make a Roth IRA contribution and a SEP contribution for

the same tax year.

A person is eligible to make a Roth IRA contribution even though a SEP contribution

is also made.

102

SEP Contributions = Active Participant for Traditional IRA Purposes

SEP Contributions = Active Participant

– Calculating the amount of the IRA contribution which cannot be deducted.

• The amount equal to or in excess of the AGI phase-out level.

• Non-deductible amount =

• Deductible amount =

103 103

$5,500 - Nondeductible amount

(or $6,500)

As applicable

$5,500 X MAGI- Threshold Level

(or $6,500) $10,000 or $20,000

As applicable As applicable

104

Income Restriction - Active Participants ONLY

SEP Contribution = Active Participant

104

Year AGI Threshold Level AGI Phase-out Level

Single 2009 $55,000 $65,000

2010-2011 $56,000 $66,000

2012 $58,000 $68,000

2013 $59,000 $69,000

2014 $60,000 $70,000

2015-2016 $61,000 $71,000

2017 $62,000 $72,000

Married, Joint Return 2009-2010 $89,000 $109,000

2011 $90,000 $110,000

2012 $92,000 $112,000

2013 $95,000 $115,000

2014 $96,000 $116,000

2015-2016 $98,000 $118,000

2017 $99,000 $119,000

Married, Separate Return 1997 to Present $0 $10,000

105

Income Restriction - One Spouse Active Participant

One Spouse NOT Active Participant

SEP Contribution = Active Participant

105

Year AGI Threshold

Level

AGI Phaseout

Level

Non-Active

Participant

Spouse

2008 $159,000 $169,000

2009 $166,000 $176,000

2010 $167,000 $177,000

2011 $169,000 $179,000

2012 $173,000 $183,000

2013 $178,000 $188,000

2014 $181,000 $191,000

2015 $183,000 $193,000

2016 $184,000 $194,000

2017 $186,000 $196,000

106

SEP Contributions and IRA Contributions for the Same Year

Set forth below are five situations. They will illustrate the applicable rules. Situations

#1 to #3 illustrate the tax analysis for someone who is an employee. Situations #4 &

#5 illustrate the tax analysis for someone who is self employed.

Situation #1. David, age 48, works for ABC, Inc. His filing status is single. His

compensation is $30,000. His modified adjusted gross income is $30,000. David

made a contribution of $5,000 to his traditional IRA on October 15, 2013, for 2013.

On February 26, 2014, ABC, Inc. contributed $7,500 to David’s SEP-IRA for tax year

2013. This was 25% of his compensation. ABC Inc. also contributed 25%to every

other eligible employee.

The $7,500 SEP contribution is excluded from David’s income for federal income tax

and social security tax purposes. David will be able to claim a tax deduction for his

$5,000 contribution to a traditional IRA, since his MAGI is less than the threshold

level.

107

SEP Contributions and IRA Contributions for the Same Year

Set forth below are five situations. They will illustrate the applicable rules. Situations

#1 to #3 illustrate the tax analysis for someone who is an employee. Situations #4 &

#5 illustrate the tax analysis for someone who is self employed.

Situation #2. Ann, age 55, works for ABC, Inc. Her filing status is single. Her

compensation is $50,000. Her modified adjusted gross income is $98,000. Ann made

a contribution of $6,000 to her traditional IRA on September 15, 2012, for 2012. On

January 26, 2013, ABC, Inc. contributed $5,000 to Ann’s SEP-IRA for tax year 2012.

This was 10% of her income. ABC Inc. also contributed 10% to every other eligible

employee.

The $5,000 SEP contribution is excluded from Ann’s income for federal Income tax

and social security tax purposes. Ann will NOT be able to claim a tax deduction for

her $6,000 contribution to a traditional IRA, since her MAGI of $98,000 is greater

than the phaseout level.

108

SEP Contributions and IRA Contributions for the Same Year

Summary. The purpose of this section has been to discuss the various tax rules

which apply to making SEP contributions and traditional IRA contributions. Of course,

the IRA custodian is not to be a tax advisor. However, if you wish to receive SEP and

IRA deposits, the likelihood of receiving such deposits increases the more you

understand the applicable tax rules.

109

110

111

SEP Data Processing Capabilities

IRA/SEP software should be designed to allow an employer to make a SEP

contribution into an employee’s traditional IRA when that person has already made

an annual traditional IRA contribution into such IRA. A SEP-IRA is simply a traditional

IRA to which an employer makes a SEP-IRA contribution. The employee is allowed to

make his or her annual traditional IRA contribution into the same IRA. It appears that

some large software providers have not written their software to have this capability.

In fact, when one such software provider asked by their customer why this capability

was not available, the company asked to be furnished the authority for being able to

make a SEP-IRA contribution to the same traditional IRA to which traditional IRA

contributions have been made or vice versa.

One of the cardinal rules of IRA/pension law is that the plan document controls. This

rule applies to this situation. Article I of the IRS model From 5305-A defines the rules

applying to IRA contributions. The main purpose of Article I is to define the

permissible types of contributions and the amounts which are eligible to be

contributed. Article I indicates there are four permissible types of contributions:

1. Annual contributions(s);

2. Rollover contributions;

3. SEP contributions; and

4. Recharacterized contributions.

112

SEP Data Processing Capabilities

Article I clearly contains a limit as to how much the annual contributions may be. This

limit is $5,000 or $6,000 for 2008-2012. The IRA custodian may not accept any

amount in excess of the annual contribution limit. However, such limits do not apply

to a rollover contribution, an employer SEP contribution or a recharacterized

contribution. The “annual limit” as to the SEP contributions is incorporated by

referencing Code section 408(k). It is $46,000 for 2008, and $49,000 for 2009 and

2010. A contribution qualifies to be rolled over only if the rollover rules have been

met.

All four of the contribution types described above may be made to an individual’s

traditional IRA. In addition, most IRA plan agreements are written to also authorize

the receipt of a transfer contribution of annual and/or SEP contributions.

Note there is no language in Article I stating a SEP contribution is impermissible

when there has already been an annual contribution made or vice versa. Obviously,

such contributions are to be reported in different boxes on the From 5498.

• Box 1 is used to report annual traditional IRA contributions;

• Box 2 is used to report rollover contributions;

• Box 4 is used to report recharacterized contributions

• Box 8 is used to report SEP contributions.

113

SEP Data Processing Capabilities

Note that Article I of the From 5305-A does not contain any discussion of SIMPLE-

IRA contributions. This is as it should be since a person is not authorized to make a

SIMPLE-IRA contribution to a traditional IRA. The plan document does not permit it

because the law does not authorize it. Similarly, the Form 3505-SA does not

authorize a person to make traditional IRA contributions or SEP contributions to a

SIMPLE-IRA.

114

SEP Distributions

A SEP must permit employees to withdraw employer contributions at any time.

Employer contributions to an employee’s SEP-IRA cannot be conditioned on the

retention in such SEP-IRA of any amount contributed.

Since IRAs are the funding vehicles for SEPs, the rules governing distributions from

SEP-IRAs are similar to the rules for regular IRAs. (See Publication 590 for details on

IRA distribution rules.)

In a SAR-SEP, transfer or rollover of contributions is prohibited before a

determination as to whether the deferral percentage test has been satisfied, see IRC

section 408(d)(7).

115

SEP Reports and Disclosure to the IRS, DOL, Participants and Beneficiaries

IRS Model SEP Rules for Disclosures to Employees. The IRS requires an employer

who adopts a Form 5305-SEP to furnish each participant with information about the

SEP and the SEP agreement. This requirement will be satisfied by furnishing the

participant with a copy of the completed Form 5305-SEP contribution agreement, the

questions and answers that are printed on Form 5305-SEP, and a statement each

year showing any contribution made to the participant’s individual retirement account

or annuity (IRA). The employer should retain the original Form 5305-SEP agreement.

It should not be sent to the IRS. Remember, all SAR-SEP plans had to be adopted

by December 31, 1996.

This concludes this Webinar

We thank you for attending

If you have any questions regarding the subject

covered in this Webinar please feel free to

call us at 800.346.3961 or

send an e-mail to [email protected]

or visit us on the Internet at www.pension-specialists.com

Copyright 2017 © Collin W. Fritz & Associates, Ltd. “The Pension Specialists” All rights reserved. No part of this presentation may be reproduced in any form and by any means

without prior written permission from Collin W. Fritz & Associates, Ltd.