8/21/2017 - ncpers

TRANSCRIPT

8/21/2017

1

1Opportunities for Pension Funds in the Age of Trumponomics: Infrastructure Investments

September 11, 2017

Opportunities for Pension Funds in the Age of Trumponomics:

Infrastructure Investments

Presented by Allan Emkin

2Opportunities for Pension Funds in the Age of Trumponomics: Infrastructure Investments

• President Trump’s $1 trillion infrastructure plan remains unveiled – likely to be pushed to next year― The plan seeks $200 billion in federal spending and $800 billion from private investors over the

course of 10 years― An effort to boost private investment, increasing state and city-level public private partnership

(“PPP” or “P3”) projects• P3s currently account for less than 5% of infrastructure investment in the U.S.

• States continue to pass P3 legislation― 35 states, the District of Columbia and one U.S. territory have now passed P3 legislation

• Executive order issued to establish an infrastructure advisory council – with a focus across allinfrastructure sectors

― Required overhaul of tax codes needed, tax reform likely to come first, along with the finalizationof the federal budget

• Meanwhile, as local municipalities await more details on federal funding, less bonds are being issuedfor infrastructure projects

―Municipal deals to fund projects are down 19.4% compared to last year, outpacing the drop inthe U.S. bond market with total issuance down 13.1%

―Deals coming to market are priced high

• Initial news of the infrastructure plan is already drawing interest from global investors―Will U.S. institutional investors follow?

INFRASTRUCTURE INITIATIVES UNDER PRESIDENT TRUMP

Source: Bloomberg, Meridiam, U.S. Department of Transportation, Thomson Reuters

8/21/2017

2

3Opportunities for Pension Funds in the Age of Trumponomics: Infrastructure Investments

• Established $186 billion long-term infrastructure plan via direct government spending and private sector /state-controlled institutional investor investments

― Canada Infrastructure Bank – operational by year end 2017

• Canada’s largest pension plans significantly invest in infrastructure with large, established infrastructureportfolios and continue to target global opportunities

― Caisse de Dépôt (CDPQ) ($15 billion infrastructure portfolio)• $6 billion investment in a new commuter train network in Montreal (51% ownership stake)• Established subsidiary, CDPQ Infra, to efficiently complete public infrastructure projects

― Ontario Municipal Employees Retirement System ($18 billion infrastructure portfolio)• Established infrastructure investment manager, Borealis Infrastructure• Recently entered the South American infrastructure market

― Canada Pension Plan Investment Board ($24 billion infrastructure portfolio)• $1 billion investment in a Spanish gas distribution business• Will invest up to C$4 billion in a single investment

• While Canadian pension plans are leaders in direct investing in infrastructure, investing globally, there hasbeen little activity in domestic investments

― Significant interest in foreign ports (Australia and New Zealand) and airports (London City Airport)― The infrastructure bank is expected to aid in securing investments from domestic investors― However, the public is wary of privatization and current P3 opportunities in Canada are below

institutional investing levels

CASE STUDY: CANADA

Source: 2016 Canadian Infrastructure Report Card

4Opportunities for Pension Funds in the Age of Trumponomics: Infrastructure Investments

CASE STUDY: AUSTRALIA

• Australian pension plans have been investing substantial amounts of capital into local infrastructure projectswell before the rest of the world

― Australian retirement funds account for $A100 billion in infrastructure assets― They are only now eyeing U.S. opportunities as they seek global opportunities

• AustralianSuper – Cautious on all opportunities, including U.S. opportunities, due to high pricing;recent global investment with a $A6 billion stake in New South Wales state power network

• Established government organizations dedicated to infrastructure― Infrastructure Australia – founded in 2008, creates long-term infrastructure plans on national and state

levels• Across all sectors, the plan pushes for privatizing assets

• Australia is on the move to sell infrastructure assets in an effort to fund new infrastructure projects― Offering tax incentives for offshore funds that operate infrastructure assets

• The P3 market in Australia continues to grow― Established National PPP Policy and Guidelines―All levels of government will consider a P3 for any project with a capital cost greater than $A50 million

Source: Bloomberg, Infrastructure Australia, EY Infrastructure

8/21/2017

3

5Opportunities for Pension Funds in the Age of Trumponomics: Infrastructure Investments

• According to a 2017 analysis by the American Society of Civil Engineers, the U.S. has more than a $2trillion gap between current funding and estimated needs for surface transportation, airports, water,wastewater, inland waterways, and other infrastructure projects

― Significant need for public funding

• U.S. pension plan infrastructure portfolios are growing―CalPERS - $2.6 billion infrastructure portfolio – 1% of total fund; 1% target, included in Real Assets

allocation―CalSTRS - $2.3 billion committed - <1% of total fund; part of 2% target Inflation Sensitive allocation―Oregon Investment Council – Infrastructure accounts for 25% of the Fund’s alternatives

allocation representing $1.2 billion; target increasing to $2.2 billion

• In addition to larger pension plans, many smaller plans are also investing in infrastructure― SCDCL LiUNA – implemented a $35 million targeted infrastructure investment platform focused

on Southern California― Employees Retirement System of Rhode Island – increasing policy target for infrastructure

CASE STUDY: UNITED STATES

Source: American Society of Civil Engineers, Moody’s, Meridiam

6Opportunities for Pension Funds in the Age of Trumponomics: Infrastructure Investments

• Private U.S. infrastructure projects have been slow to gain momentum―As states pass legislation and gain best practice experience, utilization of P3s in infrastructure

projects are expanding to include transportation, social and schools

• More investment managers are entering the P3 space generating potential opportunities forinstitutional investors:

―Meridiam• Strategy: greenfield focus, P3 structures, contract based revenues• U.S. projects: Presidio Parkway, Long Beach Courts, La Guardia, Port of Miami Tunnel

―Global Infrastructure Partners• Recent close of the $15.8 billion GIP III• Track record includes several airports and ports including London City Airport, London

Gatwick Airport, and Port of Brisbane

• P3s are not without risk― Chicago Skyway – private owner bankruptcy resulted in significant construction delays on a

partially completed road with the project falling back onto government to complete― Texas 130 toll road – toll revenues did not meet expectations

• Many infrastructure needs are for projects that do not generate direct revenue, making them lessappealing as a P3 structure

― Is government funding is the only option for projects lacking revenue streams?

CASE STUDY: UNITED STATES

Source: American Society of Civil Engineers, Moody’s, Meridiam

+@E6?E:2=�)6H�#656C2=�+@=:4J�/@@=D�E@�"?4@FC286+6?D:@?�#F?5�&?G6DE>6?E�:?�+F3=:4�&?7C2DECF4EFC6

)2E:@?2=� @?76C6?46�@?�+F3=:4�">A=@J66�-6E:C6>6?E�.JDE6>D

+F3=:4�+6?D:@?�#@CF> � .2?�#C2?4:D4@

.6AE6>36C���������

!2G:5 .6=EK6C

=�429�,1)4$5647&674(�,18(560(16�%;����64,//,21�28(4�� �;($45

9,6+��� �%,//,21�)420�6+(�)('(4$/�%7'*(6�> �%�&���!'��"!��������%( #

�29�'2(5�6+$6�&203$4(�62�62'$;<5�&$3,6$/�53(1',1*�

�

��

���

���

���

���

���

���

+F3=:4 +C:G2E6

"?6C8J��DD6ED

@>>F?:42E:@?D

.@4:2=�&?7C2

12E6C��DD6ED

/C2?DA@CE2E:@?

"DE:>2E65��??F2=�&?7C2DECF4EFC6�&?G6DE>6?E��L�����3:==:@?�J62C

�

"+$6�)240�5+27/'�6+(�342325('��('(4$/�5+$4(�2)��� �%,//,21�$5570(�

�?J�?6H�#656C2=�:?7C2DECF4EFC6�A@=:4J�D9@F=5�36�32=2?465�=:<6�2���=68865�DE@@=�

� +C@G:56�2 !�'���!�!��!����!���' E@�E96�AC@;64E�DA@?D@C

� *776C�2�4@>A6E:E:G6 %�&�����(&'���%�'(%! E@�E96�:?G6DE@C

� �6�762D:3=6�@?�#656C2= #"���+��!���(���'�&�"%�!� 8C@F?5D

�.,'" 0��-,+/,.�+2"/0,.

�"!".�)��,2".+*"+0

�

�256�(1(),6��203$4,521�2)

�26(16,$/��('(4$/��2/,&;�!22/5�)24��1)4$5647&674(�+,*+/;�5,03/,),('�

1!$"0�.5

�,/0

�&+�+ &�)� "+"#&0�0,

�.,'" 0��-,+/,.

� -68F=2E@CJ�.EC62>=:?:?8

� #656C2=� C65:E��DD:DE2?46

� /2I� @56�&?46?E:G6D

� $C2?ED

�

�%"���'��#"!&"%&

((.,1*��29&256�!$:�:(036��,1$1&,1*

��!&�"!��(!�&

((.,1*��203(6,6,8(�!$:$%/(�#,(/'5

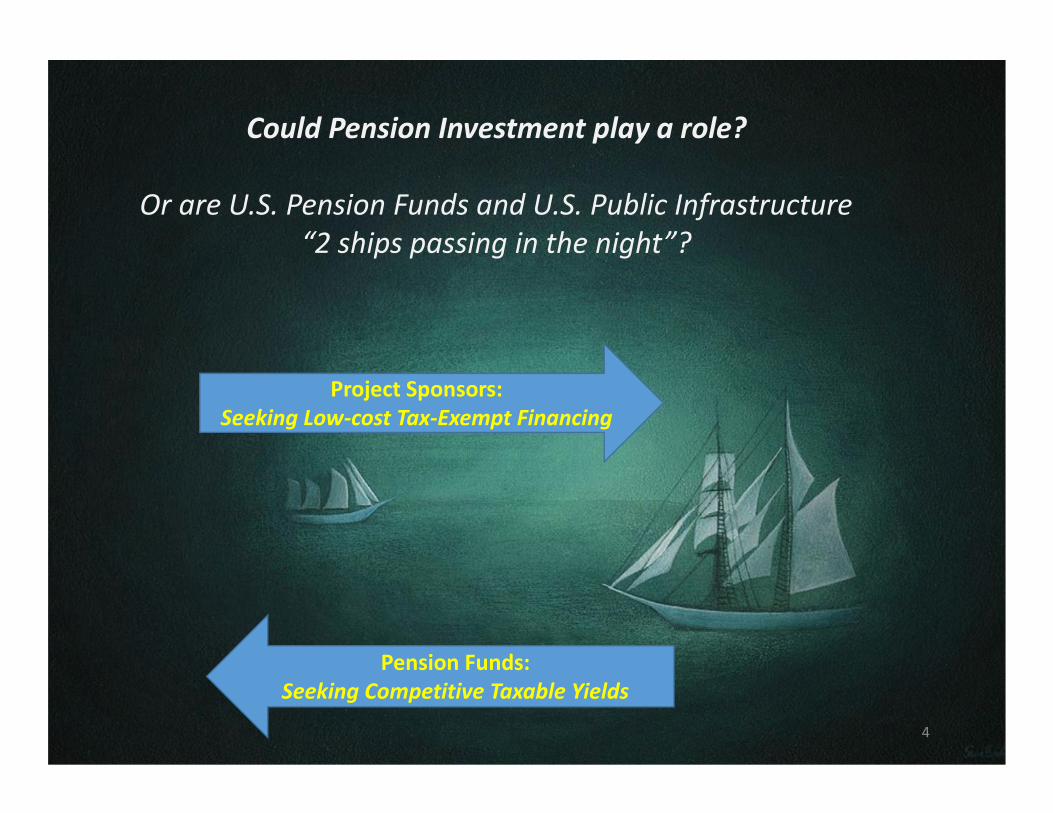

�27/'��(15,21��18(560(16�3/$;�$�42/(�

�.��."�������"+/&,+��1+!/��+!�������1�)& ��+#.�/0.1 01."

8�/%&-/�-�//&+$�&+�0%"�+&$%09�

�

��1(9��('(4$/��2/,&;��42325$/5�&27/'�3428,'(

57%56$16,$/�23324671,6,(5�)24��(15,21��71'��18(560(16

� $C2?E�&?46?E:G6����O�DD6E�-64J4=:?8P

"BF:EJ�:?G6DE>6?E�:?�+F3=:4�+C:G2E6�+2CE?6CD9:AD��+�ND�24BF:C:?8

6I:DE:?8�C6G6?F6�86?6C2E:?8�O3C@H?7:6=5P�AC@;64ED�7C@>�AF3=:4�@H?6CD

� /2I @56 &?46?E:G6��/2I� C65:ED�7@C�?6H�AF3=:4 ,.

AC:G2E6�:?7C2DECF4EFC6�:?G6DE>6?E

+6?D:@?�#F?5D�4@F=5�>@?6E:K6�E2I�4C65:ED�2EE24965�E@�!63E�@C

"BF:EJ�&?G6DE>6?ED

�

� ��$C2?E�&?46?E:G6� �DD6E�-64J4=:?8

+C@G:56�����#656C2=�&?46?E:G6�$C2?ED�E@��.E2E6�'@42=�$@G6C?>6?ED�E92E�D6==�@C

=62D6�C6G6?F6�86?6C2E:?8�:?7C2DECF4EFC6�2DD6ED�E96J�@H?M

-.,2&!"! E96�?6E�AC@4665D�2C6�C6:?G6DE65�:?�?6H�AC@;64ED

.E2E6�@C

'@42=�0?:E

+C:G2E6

"?E:EJ

�:,56,1* �+#.�/0.1 01."��.,'" 0

/,)!�,.�)"�/"!�0,��.&2�0"��" 0,.

#,.����

��*

�����+C@;64E��

+F3=:4�@C

+C:G2E6

-6E:C6�����@7

*FEDE2?5:?8

+C@;64E�!63E

)6H�#656C2=�����&?46?E:G6

$C2?E�+C@8C2>

������"0���)"��., ""!/

����"!".�)��.�+0

0,��"3��.,'" 0

�����.& "

+6?D:@?�#F?5

&?G6DE>6?E

$(�'++C@;64E�!63E

�

� /2I� @56 &?46?E:G6���(@?6E:K:?8�/2I� C65:ED

2EE24965�E@�!63E�@C�"BF:EJ�&?G6DE>6?E

�%5�*&$%0��,)& 5�*�("./�-."#".�1/&+$�0�4� ,!"�*"�/1."/�&+/0"�!�,#�$.�+0/�

�,."� ,*-)& �0"!���10��

� �G@:5D�2AAC@AC:2E:@?D 2?5�E96�9:89=J�4@?DEC2:?65�!:D4C6E:@?2CJ��F586E

DA6?5:?8�42AD

� /96�7:D42=�4@DEM��4��4-"+!&01."/6:D DAC625�@G6C�2����J62C�H:?5@H�&?�E96

(2?52E@CJ��F586E��2?5�D9@F=5�36�62D:6C�E@��23D@C3

� -6BF:C65�AC:G2E6�4@�:?G6DE>6?E D6CG6D�2D�2�=:E>FD�E6DE�@7

7:?2?4:2=�762D:3:=:EJ

� +9:=@D@A9:42==J���A@=:E:42==J��>2?J�(6>36CD�@7� @?8C6DD�A6C46:G6�E2I

4C65:ED�2D�2�7@C>�@7�OC65F4:?8�E2I�3FC56? P

�

!+(�!4,//,21��2//$4��7(56,21�

�29�&27/'�$ 1216$:$%/( �(15,21��71'�6$.(�$'8$16$*(

2) 6$:�&2'(�,1&(16,8(5 57&+�$5�6$:�&4(',65�

+6?D:@?�#F?5D�4@F=5�4@?G6CE ?@?C67F?523=6�E2I�4C65:ED E@�42D9�3J

2AA=J:?8�E96>�282:?DE�E96:C�=:23:=:EJ�E@�E96�0 . �/C62DFCJ�E@�C6>:E

C6E:C66 H:E99@=5:?8�E2I @?�A2:5�36?67:ED

"I2>A=6D�

� /2I�*C:6?E65 "BF:EJ �&?G6DE>6?E�/2I� C65:ED

��/"!�,+��,3��+ ,*"��,1/&+$���4��."!&0�-.,$.�*

� /2I�+C676CC65 !63E �,F2=:7:65�/2I� C65:E��@?5D

�*".& ����/0��,.3�.!� ,+!/���/�-.,-,/"!��5�����"0.,

�

.E2E6�+6?D:@?�#F?5

6(3������5570(�$��(15,21��71'�3$;5��� �0,//,21�;($4�,1

4(6,4(0(16�%(1(),65�62�$117,6$165�1(66,1*�276�� ��)('(4$/

,1&20(�6$:�9,6++2/',1*�'7(�62�!4($574;�

���������

�??F:E2?ED

0 . �/C62DFCJ

�����������1:E99@=5:?8

/2I�':23:=:EJ�����

)6E��6?67:E

+2J>6?ED�E@

-6E:C66D

�

.E2E6�+6?D:@?�#F?5

6(3������(15,21��71'�,18(565�,1����0,//,21�,1��42-(&6��21'5�

/96D6�2C6�2DDF>65�E@�36�:?G6DE>6?E�8C256�3@?5D��AC@G:5:?8�2�>2C<6E�J:6=5�@7

L����2??F2=�E2I�4C65:E������@7�AC:?4:A2=�:?�=:6F�@7�42D9�:?E6C6DE

+C:?4:A2=�C6A2:5�H:E9�FD6C�766D�@C�565:42E65�C6G6?F6D

�!)�&'���� ����"!��!��%"���'��"!�&

��������E2I�4C65:ED�J62C�2D�O:?E6C6DEP�

���>:==:@?�42D9�AC:?4:A2=�2E�>2EFC:EJ

&?7C2DECF4EFC6

+C@;64E

���D:>:=2C�2AAC@249�4@F=5�36�2AA=:65�E@�6BF:EJ�:?G6DE>6?E�@G6C����J62CD��2D�H:E9�'@H�&?4@>6�%@FD:?8�/2I� C65:ED

��

.E2E6�+6?D:@?�#F?5

6(3������(15,21��71'�$33/,(5��� �2)�6$:�&4(',65�($&+�;($4

$*$,156�6+(����0,//,21�9,6++2/',1*5�3$;$%/(�62�!4($574;�

���������

�??F:E2?ED

0 . �/C62DFCJ

���������)6E�+2J>6?E

@7�1:E99@=5:?8�/2I

)6E��6?67:E

+2J>6?ED�E@

-6E:C66D

������� C6E2:?65�3J�+6?D:@?�#F?5�

AC@G:5:?8����O42D9�C6EFC?P�@?���(�:?G6DE65

�"0&.""/7���&)&05�0,� )�&*��+�����0�4�."#1+!

F?27764E65�3J�A6?D:@?�7F?5ND�E2I�4C65:E ��

�(15,21��71'5�$1'��7%/,&��1)4$5647&674(�

�271'�62*(6+(4�21�$�&20021�&2745(�

��