8 11 14 - valuewalk.com · most recent quarter ended. pitchbook’s most recent fund returns data...

TRANSCRIPT

Shortest closing time for PE funds since 2008

Second-highest VC total raised

for the decade

76% of VC funds in 2015

outmatched predecessor

in size

PE fundraising

adapting to current

environment85 11 14

Credits & ContactPitchBook Data, Inc.

JOHN GABBERT Founder, CEO

ADLEY BOWDEN Vice President,

Market Development & Analysis

ContentGARRETT JAMES BLACK Senior Analyst

NIZAR TARHUNI Analyst

BRIAN LEE Data Analyst

JENNIFER SAM Senior Graphic Designer

JESS CHAIDEZ Graphic Designer

Contact PitchBook pitchbook.com

RESEARCH

EDITORIAL

SALES

COPYRIGHT © 2016 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means—graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems—without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.

Introduction 3

PE Fundraising Overview 4–5

PE Fundraising by Fund Size 6-7

PE Closing Times 8

PE Capital Overhang 9

Secondaries 10

VC Fundraising Overview 11-12

VC Fundraising by Fund Size 13-14

Micro VC Funds 15

Venture Capital Overhang 16

Select Open U.S. Funds 17

Methodology 18

Contents

2 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

How is fundraising evolving?Introduction

Investors’ perception of risk matters as much as the degree to which risk has

materialized. Over the past month, we’ve detailed how the private equity and

venture capital investment landscapes have been evolving in response to macro

concerns, volatility and corrections in public markets and more. Yet, when

we come to fundraising for PE and VC, we must consider the perspectives of

both fund investors and managers and how they are adapting to the current

environment.

In some ways, PE fund managers have become victims of their own success.

They must contend with an immense overhang of dry powder in a competitive

dealmaking environment, generated by the vast number of commitments

collected over the past few years from limited partners drawn by the asset class’s

strong historical performance. To assess how PE fundraisers have responded

to not only that overhang’s impetus to invest, but also investment trends, we

examine multiple datasets ranging from fundraising across different fund types

to fund size metrics.

When it comes to VC, currently, there is a general consensus that the venture

industry is experiencing the onset of cooling after overheating to the point of

overexuberance, with investors scrutinizing the fundamentals of startups more

closely than in years prior, primarily in response to concerns about liquidity

and growth. Venture fundraisers have had a stellar run as of late, judging by

the number of vehicles and sums of capital raised, yet how will they respond

to the cooling of the investment climate? In the following pages, we explore

trends across the venture fundraising market, particularly the micro fundraising

segment, given its especially rapid development in the past few years, to analyze

the nature of their potential responses.

One last thing to note: We have included brand-new datasets in this report,

including breakdowns of capital called compared to capital raised across both

PE and VC, among others. We hope this helps inform your decision-making in

the coming months, and feel free to reach out with any questions.

GARRETT JAMES BLACK

Senior Analyst

MAKE WAY FOR

SMARTER, ON-THE-FLY MEETING PREP

US +1 206.623.1986

UK +44 (0)207.190.9809

pitchbook.com

Introducing PitchBook

Mobile. The same

excellent data, technology

and service from the

PitchBook Platform, now

available on a mobile

device.

Search:

“PitchBook”

Available for

3 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

A shifting environmentPE fundraising overview

In an environment where cheap

debt contributed to a significant

rise in activity and LPs flocked to GPs

to reap outsized returns, PE managers

have amassed an enormous war chest

of capital over recent years. With

too much capital chasing a limited

amount of transactions, competition

has become fierce, with strategics

often able to win out in auction

processes. As dry powder levels have

continued to grow, 2015 finally saw

the fundraising trail begin to slow. The

massive vehicles raised just prior to the

financial crisis weren’t able to deploy

their forecasted amount of capital

during their respective investment

periods, leading to lagging returns, an

outcome that GPs and LPs alike are

working fervently to avoid in present

day.

Last year saw a divergence between capital raised and called

U.S. PE capital raised versus capital contributed by year

U.S. PE fundraising (#) by fund type U.S. PE fundraising ($) by fund type

Source: PitchBook

2015 saw GPs close on just over $185

billion in committed capital across

281 vehicles, a year-over-year decline

of near 7% and 14%, respectively.

On a historical basis, these figures

are certainly still strong, yet they fall

short of what we’ve seen in in the past

couple of years.

Given the shifting deal environment,

GP fundraising efforts were also

driven by evolving strategies last year

as more niche vehicles were raised

to focus on emerging opportunities

including distress, direct lending and

energy. The broader syndicated loan

market has seen a bit of a crunch, and

-$100

-$50

$0

$50

$100

$150

$200

$250

$300

$350

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Net PE capital Contributions ($B) Capital raised ($B)

Source: PitchBook

0%

20%

40%

60%

80%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

0%

20%

40%

60%

80%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

OtherEnergy Mezzanine Restructuring Co-Investment PE growthBuyout

Note: The LP reporting cycle is two quarters behind the

most recent quarter ended. PitchBook’s most recent

fund returns data is through 2Q 2015, with capital

raised figures through the end of 2015.

4 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

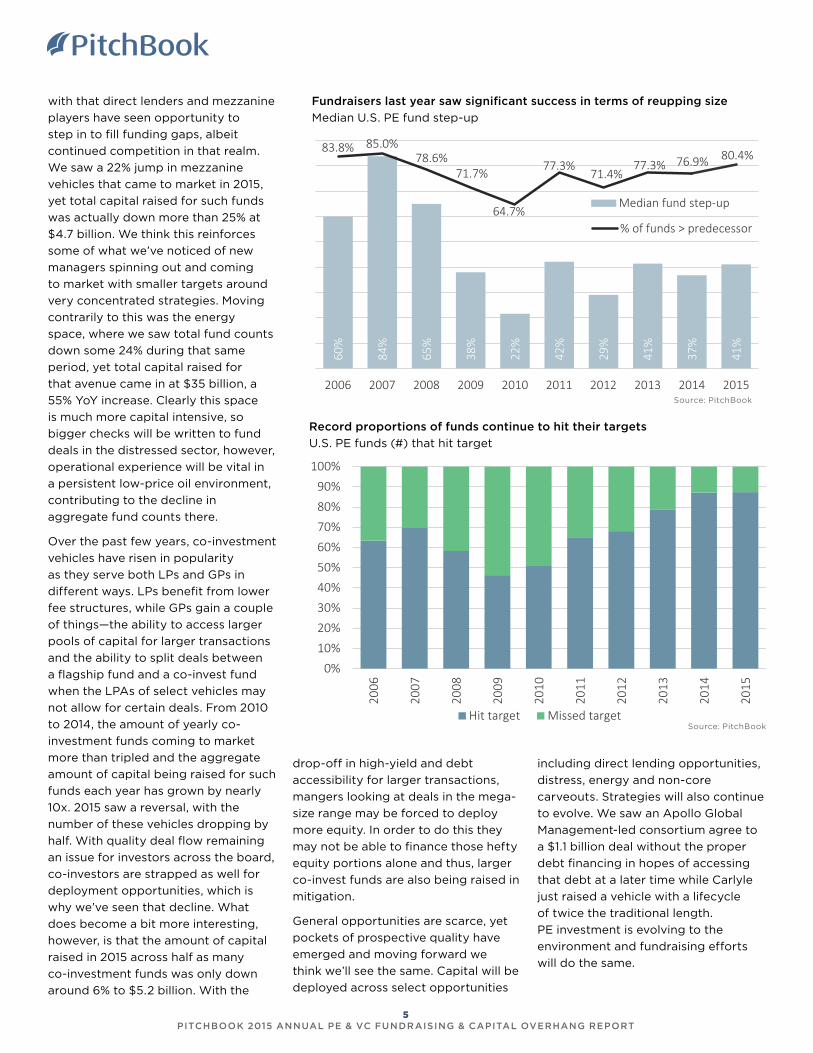

Fundraisers last year saw significant success in terms of reupping size

Median U.S. PE fund step-up

Record proportions of funds continue to hit their targets

U.S. PE funds (#) that hit target

60%

84%

65%

38%

22%

42%

29%

41%

37%

41%

83.8% 85.0%78.6%

71.7%

64.7%

77.3%71.4%

77.3% 76.9% 80.4%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Median fund step-up

% of funds > predecessor

Source: PitchBook

0%10%20%30%40%50%60%70%80%90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Hit target Missed targetSource: PitchBook

with that direct lenders and mezzanine

players have seen opportunity to

step in to fill funding gaps, albeit

continued competition in that realm.

We saw a 22% jump in mezzanine

vehicles that came to market in 2015,

yet total capital raised for such funds

was actually down more than 25% at

$4.7 billion. We think this reinforces

some of what we’ve noticed of new

managers spinning out and coming

to market with smaller targets around

very concentrated strategies. Moving

contrarily to this was the energy

space, where we saw total fund counts

down some 24% during that same

period, yet total capital raised for

that avenue came in at $35 billion, a

55% YoY increase. Clearly this space

is much more capital intensive, so

bigger checks will be written to fund

deals in the distressed sector, however,

operational experience will be vital in

a persistent low-price oil environment,

contributing to the decline in

aggregate fund counts there.

Over the past few years, co-investment

vehicles have risen in popularity

as they serve both LPs and GPs in

different ways. LPs benefit from lower

fee structures, while GPs gain a couple

of things—the ability to access larger

pools of capital for larger transactions

and the ability to split deals between

a flagship fund and a co-invest fund

when the LPAs of select vehicles may

not allow for certain deals. From 2010

to 2014, the amount of yearly co-

investment funds coming to market

more than tripled and the aggregate

amount of capital being raised for such

funds each year has grown by nearly

10x. 2015 saw a reversal, with the

number of these vehicles dropping by

half. With quality deal flow remaining

an issue for investors across the board,

co-investors are strapped as well for

deployment opportunities, which is

why we’ve seen that decline. What

does become a bit more interesting,

however, is that the amount of capital

raised in 2015 across half as many

co-investment funds was only down

around 6% to $5.2 billion. With the

drop-off in high-yield and debt

accessibility for larger transactions,

mangers looking at deals in the mega-

size range may be forced to deploy

more equity. In order to do this they

may not be able to finance those hefty

equity portions alone and thus, larger

co-invest funds are also being raised in

mitigation.

General opportunities are scarce, yet

pockets of prospective quality have

emerged and moving forward we

think we’ll see the same. Capital will be

deployed across select opportunities

including direct lending opportunities,

distress, energy and non-core

carveouts. Strategies will also continue

to evolve. We saw an Apollo Global

Management-led consortium agree to

a $1.1 billion deal without the proper

debt financing in hopes of accessing

that debt at a later time while Carlyle

just raised a vehicle with a lifecycle

of twice the traditional length.

PE investment is evolving to the

environment and fundraising efforts

will do the same.

5 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

U.S. PE fundraising (#) by fund size U.S. PE fundraising ($) by fund size

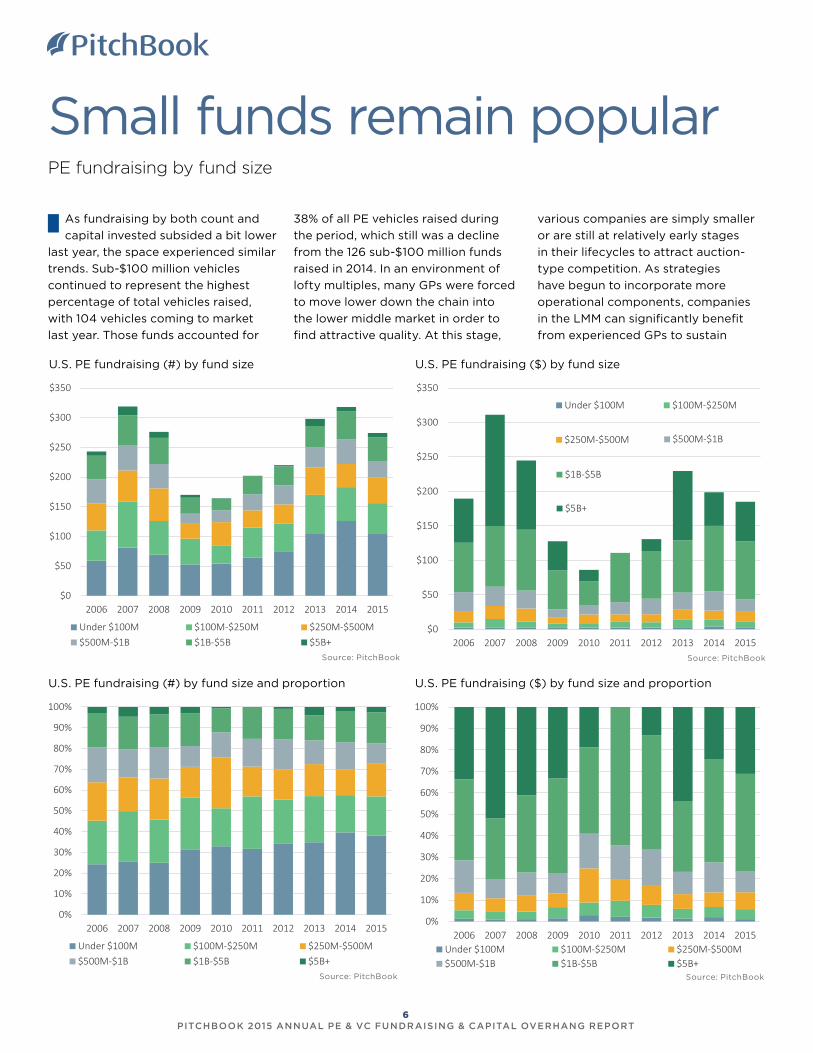

Small funds remain popularPE fundraising by fund size

As fundraising by both count and

capital invested subsided a bit lower

last year, the space experienced similar

trends. Sub-$100 million vehicles

continued to represent the highest

percentage of total vehicles raised,

with 104 vehicles coming to market

last year. Those funds accounted for

Source: PitchBook Source: PitchBook

U.S. PE fundraising (#) by fund size and proportion U.S. PE fundraising ($) by fund size and proportion

$0

$50

$100

$150

$200

$250

$300

$350

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Under $100M $100M-$250M

$250M-$500M $500M-$1B

$1B-$5B

$5B+

$0

$50

$100

$150

$200

$250

$300

$350

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Under $100M $100M-$250M $250M-$500M$500M-$1B $1B-$5B $5B+

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Under $100M $100M-$250M $250M-$500M$500M-$1B $1B-$5B $5B+

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015Under $100M $100M-$250M $250M-$500M$500M-$1B $1B-$5B $5B+

38% of all PE vehicles raised during

the period, which still was a decline

from the 126 sub-$100 million funds

raised in 2014. In an environment of

lofty multiples, many GPs were forced

to move lower down the chain into

the lower middle market in order to

find attractive quality. At this stage,

various companies are simply smaller

or are still at relatively early stages

in their lifecycles to attract auction-

type competition. As strategies

have begun to incorporate more

operational components, companies

in the LMM can significantly benefit

from experienced GPs to sustain

Source: PitchBook Source: PitchBook

6 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

Average U.S. fund size by PE fund type

Mean fund sizes reflect a greater number of large vehicles

Average & median U.S. PE fund size

$280 $250 $275

$184

$229 $200 $204 $187 $174 $187

$780

$976$887

$752

$525

$548$594

$771

$625 $675

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Median ($M) Average ($M)

Source: PitchBook

Fund type 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Buyout $846.1 $1,218.4 $888.9 $889.7 $635.2 $557.8 $617.0 $891.1 $692.4 $671.4

PE Growth $301.3 $243.2 $245.0 $226.1 $202.1 $244.5 $380.7 $281.4 $448.9 $392.1

Co-Investment $568.8 $305.3 $486.6 $289.1 $71.4 $143.8 $145.9 $285.9 $154.8 $306.9

Restructuring $760.8 $1,426.3 $2,399.8 $250.3 $811.9 $1,140.8 $974.8 $1,327.4 $1,805.4 $1,062.7

Mezzanine $768.8 $1,118.3 $701.1 $443.8 $286.7 $364.7 $652.8 $639.0 $374.3 $215.2

Energy $1,264.4 $1,031.2 $799.3 $2,093.8 $767.3 $1,317.1 $825.4 $1,163.9 $944.6 $1,949.0

Median U.S. fund size by PE fund type

Fund type 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Buyout $305.0 $270.0 $266.0 $221.0 $285.0 $200.0 $205.0 $216.5 $187.2 $152.5

PE Growth $162.0 $107.5 $150.0 $118.0 $86.0 $90.0 $49.0 $134.5 $130.9 $131.7

Co-Investment $450.0 $154.0 $168.8 $192.0 $60.4 $110.0 $97.9 $108.8 $80.2 $55.0

Restructuring $750.0 $900.0 $1,550.0 $179.0 $229.0 $753.4 $575.0 $550.0 $1,210.5 $825.4

Mezzanine $307.0 $217.5 $300.0 $243.0 $195.0 $227.0 $204.0 $150.0 $227.0 $162.5

Energy $566.0 $1,020.0 $434.8 $820.0 $807.3 $600.0 $376.0 $400.0 $325.0 $475.0

Source: PitchBook

Source: PitchBook

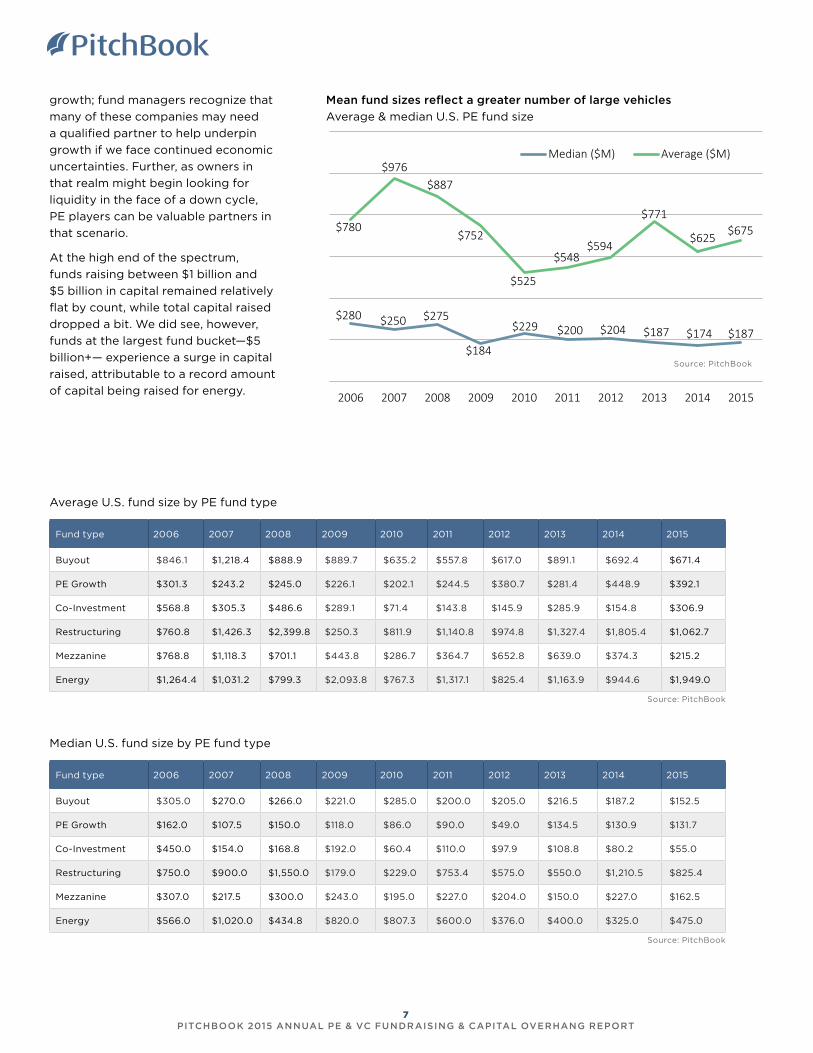

growth; fund managers recognize that

many of these companies may need

a qualified partner to help underpin

growth if we face continued economic

uncertainties. Further, as owners in

that realm might begin looking for

liquidity in the face of a down cycle,

PE players can be valuable partners in

that scenario.

At the high end of the spectrum,

funds raising between $1 billion and

$5 billion in capital remained relatively

flat by count, while total capital raised

dropped a bit. We did see, however,

funds at the largest fund bucket—$5

billion+— experience a surge in capital

raised, attributable to a record amount

of capital being raised for energy.

7 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

Niche strategies succeedingPE fund closing times

In what may seem counterintuitive

given an increasingly sluggish deal

environment, GPs coming to market

with new vehicles in 2015 found

success in terms of the time it took

to hold final closes on those funds.

Median and average fund sizes were

up relative to what we saw in 2014,

yet at $187.4 million, the median U.S.

PE fund size came in fairly low on a

historical basis. Further, only growth

and energy vehicles posted increases

in YoY median fund sizes, highlighting

a dataset that was skewed by the 14%

decline in the population of vehicles

coming to market.

The median close time for vehicles

completing raises in 2015 came in at

12.8 months, the lowest figure we’ve

seen since 2008, which saw GPs able

to close in just 12 months. With a

PE firms have had little need to raise quickly, given the

amount of dry powder

Time between U.S. PE funds (years)

Fundraisers have enjoyed fairly rapid closes to new

vehicles as of late

Average & median U.S. PE fund time to close

12.011.0

12.014.0

20.0

15.2 14.0 14.6 14.512.8

14.3

12.6

14.215.9

18.016.5 16.3

18.2

14.8

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Median (months) Average (months)

Source: PitchBook

4.6

3.2

3.3

3.4

4.1

4.5

4.2

4.7

4.3

5.4

4.5

4.0

4.0

3.9

4.5

4.6

4.3

4.3

4.4

5.6

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Median Average

Source: PitchBook

record amount of capital being raised

that year, those fund IRRs are under

significant pressure stemming from

the recession and, subsequently, GPs

coming to market in the few years

following had faced some difficulties

in persuading various LPs. In light

of scarce deal flow, we think that

GPs were able to find success in

rounding up capital quickly last year

due to niche and targeted strategies,

as well as a greater focus on the

process they employed to chase LP

dollars. As LPs have become more

sophisticated, the opportunities that

have presented themselves in light

of a global slowdown across equities

and fixed income have made certain

PE strategies fairly attractive. LPs are

certainly aware of the profits that can

be realized when deploying capital in

a downturn, and the long-term horizon

these investors employ match well with

the investment strategy of new, niche

managers. Further, GPs have been able

to increase the amount of targeted

investor relations campaigns they

utilize to court LPs, which becomes

a vital component of the fundraising

trail during a period where LPs have

also begun shrinking the number

of managers they work with and

instead writing bigger checks to fewer

managers.

The median time between funds

rose significantly in 2015 to 5.4 years

from just 4.3 years in 2014, a further

testament to the difficulty managers

have faced in deploying ample

amounts of legacy dry powder.

8 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

Peak overhang?U.S. PE capital overhang

PE capital overhang remains

an issue for the industry, with

cumulative dry powder growing

nearly 2% in 2015 to $543.4 billion.

In an uncertain environment, we

think that GPs continued to come to

market to insure they could access

capital before an adverse series of

events may dry up the amount of LP

commitments available. While we

understand that the PE asset class

still remains highly sought, the newer

strategies we’ve seen from GPs can

take a considerable amount of time

before the opportunities are ripe for

capital deployment, slightly inflating

the amount of dry powder remaining in

PE coffers. Although the energy sector

has raised by far the most amount of

capital in 2015 outside of traditional

buyout vehicles, we’ve seen slim deal

flow in the space. As GPs continue

U.S. PE capital overhang ($B) by year

to wait for the opportune moment

and potential bankruptcies, not much

capital has been called down on that

front. Given the capital-heavy nature of

those transactions, we think we’ll see

overhang begin to slip over the next

12 to 18 months as more opportunities

arise. Interestingly, 2012 vintages hold

at minimum 103%—in the $100 million

to $250 million range—more dry

powder than 2011 vintages, with mega

funds that raised over $5 billion sitting

on 337% more unused capital than

funds making their first investment in

2011. That discrepancy appears fairly

uncharacteristic, which is likely due to

distributions being recycled back into

those vehicles. 2013 saw capital raised

jump 76%, while the median time to

close came in at nearly 15 months,

again highlighting redistributions

as LPs began committing capital to

$426

$539$509 $501

$470 $474$499

$530 $533 $543

$0

$100

$200

$300

$400

$500

$600

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

2016

2015

2014

2013

2012

2011

2010

2009

2008

CUMULATIVEOVERHANG

OVERHANG BY VINTAGE

Source: PitchBook

*As of 6/30/15

Note: The LP reporting cycle is two quarters behind the

most recent quarter ended. PitchBook’s most recent

fund returns data is through 2Q 2015. 2H 2015 and 2016

numbers are from vehicles that have begun reporting

yet have not fully closed.

many funds that closed in 2013 at least

a year prior. Lastly, with the ability

to overcome stretched valuations

becoming an issue for various GPs

last year, buyer-to-seller discrepancies

became more pronounced, in turn

dragging deals out longer. Our

overhang datasets are lagged by

two quarters, and thus, transactions

that close after that lag aren’t yet

subtracted from our reported dry

powder number. As our data continues

to roll in, the next iteration of this

report will give the most complete

snapshot of 2015 aggregate PE capital

overhang.

9 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

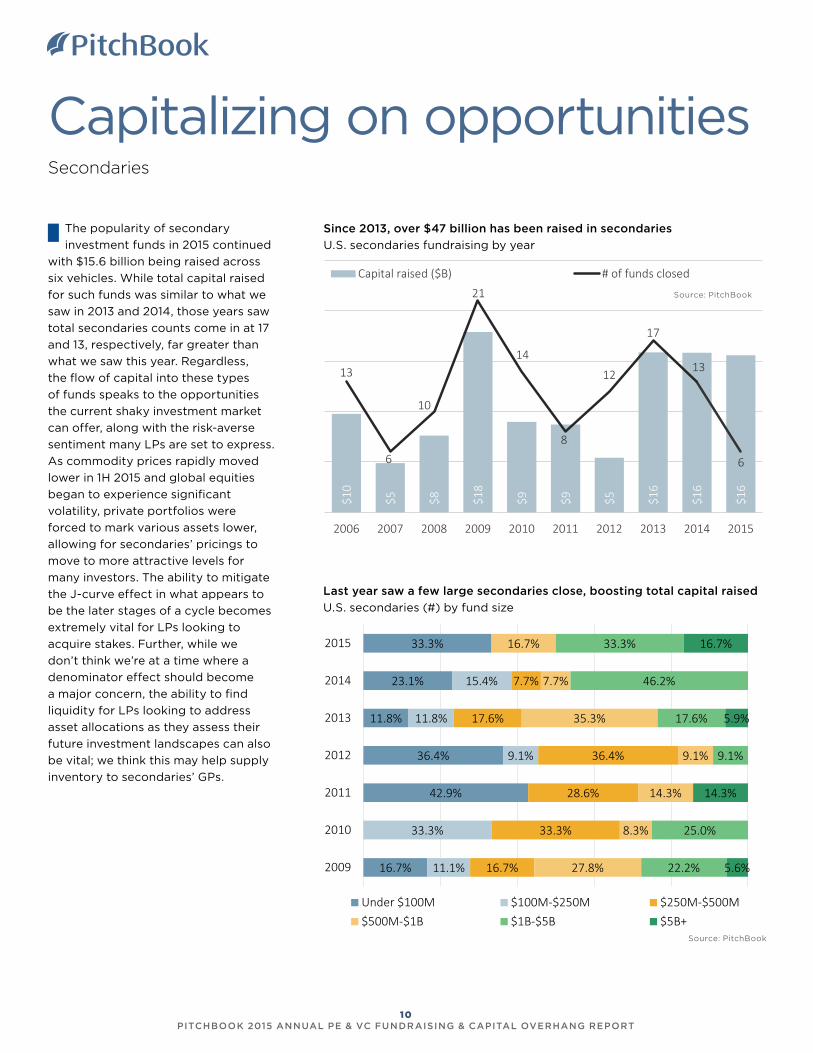

Capitalizing on opportunitiesSecondaries

The popularity of secondary

investment funds in 2015 continued

with $15.6 billion being raised across

six vehicles. While total capital raised

for such funds was similar to what we

saw in 2013 and 2014, those years saw

total secondaries counts come in at 17

and 13, respectively, far greater than

what we saw this year. Regardless,

the flow of capital into these types

of funds speaks to the opportunities

the current shaky investment market

can offer, along with the risk-averse

sentiment many LPs are set to express.

As commodity prices rapidly moved

lower in 1H 2015 and global equities

began to experience significant

volatility, private portfolios were

forced to mark various assets lower,

allowing for secondaries’ pricings to

move to more attractive levels for

many investors. The ability to mitigate

the J-curve effect in what appears to

be the later stages of a cycle becomes

extremely vital for LPs looking to

acquire stakes. Further, while we

don’t think we’re at a time where a

denominator effect should become

a major concern, the ability to find

liquidity for LPs looking to address

asset allocations as they assess their

future investment landscapes can also

be vital; we think this may help supply

inventory to secondaries’ GPs.

Since 2013, over $47 billion has been raised in secondaries

U.S. secondaries fundraising by year

Last year saw a few large secondaries close, boosting total capital raised

U.S. secondaries (#) by fund size

$10

$5 $8 $18

$9 $9 $5 $16

$16

$16

13

6

10

21

14

8

12

17

13

6

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Capital raised ($B) # of funds closed

Source: PitchBook

16.7%

42.9%

36.4%

11.8%

23.1%

33.3%

11.1%

33.3%

9.1%

11.8%

15.4%

16.7%

33.3%

28.6%

36.4%

17.6%

7.7%

27.8%

8.3%

14.3%

9.1%

35.3%

7.7%

16.7%

22.2%

25.0%

9.1%

17.6%

46.2%

33.3%

5.6%

14.3%

5.9%

16.7%

2009

2010

2011

2012

2013

2014

2015

Under $100M $100M-$250M $250M-$500M$500M-$1B $1B-$5B $5B+

Source: PitchBook

10 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

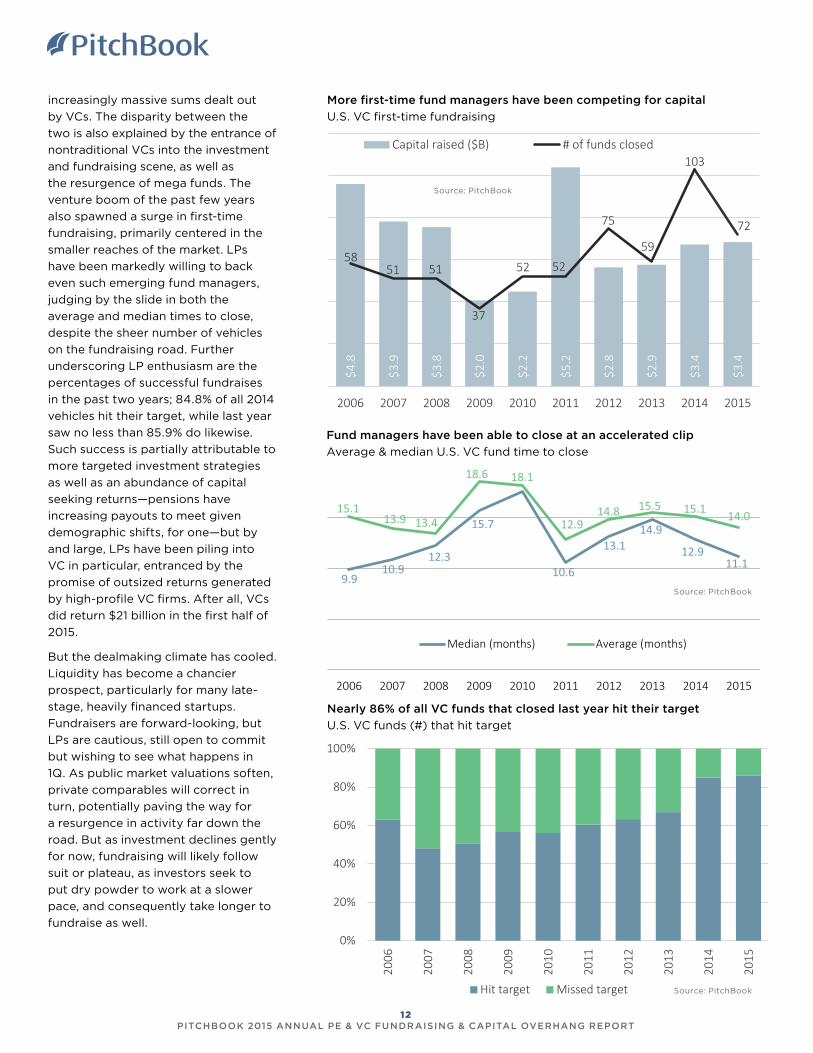

Second-highest sum raisedVC fundraising overview

Nontraditional investors raising large vehicles geared toward venture investing help explain the disparity

U.S. VC raised versus capital contributed ($B) by year

A massive $35.5 billion was raised in 2015, second-highest of the decade

U.S. VC fundraising by year

VC fundraisers have been on a tear

recently. From 2014 through the

end of last year, 500 venture vehicles

were closed on a gargantuan $69.4

billion in commitments. 2015 alone

saw a staggering $35.5 billion in total

capital committed to VC funds, the

second-highest total of the decade.

On a quarterly basis, fund counts slid

in the back half of 2015, with the 53

pools closed in 4Q the lowest tally

since 3Q 2013, even though capital

raised remained hefty. In short,

investor uncertainty that has been

evidenced by the decline in activity

on the dealmaking side has yet to

substantively lead to a slowdown in

VC fundraising as firms take longer to

cut deals. Such elevated fundraising

as of late had to keep pace with the

$36.

4

$34.

1

$33.

1

$11.

7

$19.

2

$24.

5

$24.

3

$20.

4

$33.

9

$35.

5

191 179 184

117

150

134

190 193

258

242

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Capital raised ($B)

# of funds closed

Source: PitchBook

Source: PitchBook

-$20

-$10

$0

$10

$20

$30

$40

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Net venture capital Contributions ($B) Capital raised ($B)

Note: The LP reporting cycle is two quarters behind the

most recent quarter ended. PitchBook’s most recent

fund returns data is through 2Q 2015, with capital

raised figures through the end of 2015.

11 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

More first-time fund managers have been competing for capital

U.S. VC first-time fundraising

Fund managers have been able to close at an accelerated clip

Average & median U.S. VC fund time to close

Nearly 86% of all VC funds that closed last year hit their target

U.S. VC funds (#) that hit target

$4.8

$3.9

$3.8

$2.0

$2.2

$5.2

$2.8

$2.9

$3.4

$3.4

5851 51

37

52 52

75

59

103

72

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Capital raised ($B) # of funds closed

Source: PitchBook

9.910.9

12.3

15.7

10.6

13.114.9

12.911.1

15.113.9 13.4

18.6 18.1

12.914.8 15.5 15.1 14.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Median (months) Average (months)

Source: PitchBook

0%

20%

40%

60%

80%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Hit target Missed target Source: PitchBook

increasingly massive sums dealt out

by VCs. The disparity between the

two is also explained by the entrance of

nontraditional VCs into the investment

and fundraising scene, as well as

the resurgence of mega funds. The

venture boom of the past few years

also spawned a surge in first-time

fundraising, primarily centered in the

smaller reaches of the market. LPs

have been markedly willing to back

even such emerging fund managers,

judging by the slide in both the

average and median times to close,

despite the sheer number of vehicles

on the fundraising road. Further

underscoring LP enthusiasm are the

percentages of successful fundraises

in the past two years; 84.8% of all 2014

vehicles hit their target, while last year

saw no less than 85.9% do likewise.

Such success is partially attributable to

more targeted investment strategies

as well as an abundance of capital

seeking returns—pensions have

increasing payouts to meet given

demographic shifts, for one—but by

and large, LPs have been piling into

VC in particular, entranced by the

promise of outsized returns generated

by high-profile VC firms. After all, VCs

did return $21 billion in the first half of

2015.

But the dealmaking climate has cooled.

Liquidity has become a chancier

prospect, particularly for many late-

stage, heavily financed startups.

Fundraisers are forward-looking, but

LPs are cautious, still open to commit

but wishing to see what happens in

1Q. As public market valuations soften,

private comparables will correct in

turn, potentially paving the way for

a resurgence in activity far down the

road. But as investment declines gently

for now, fundraising will likely follow

suit or plateau, as investors seek to

put dry powder to work at a slower

pace, and consequently take longer to

fundraise as well.

12 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

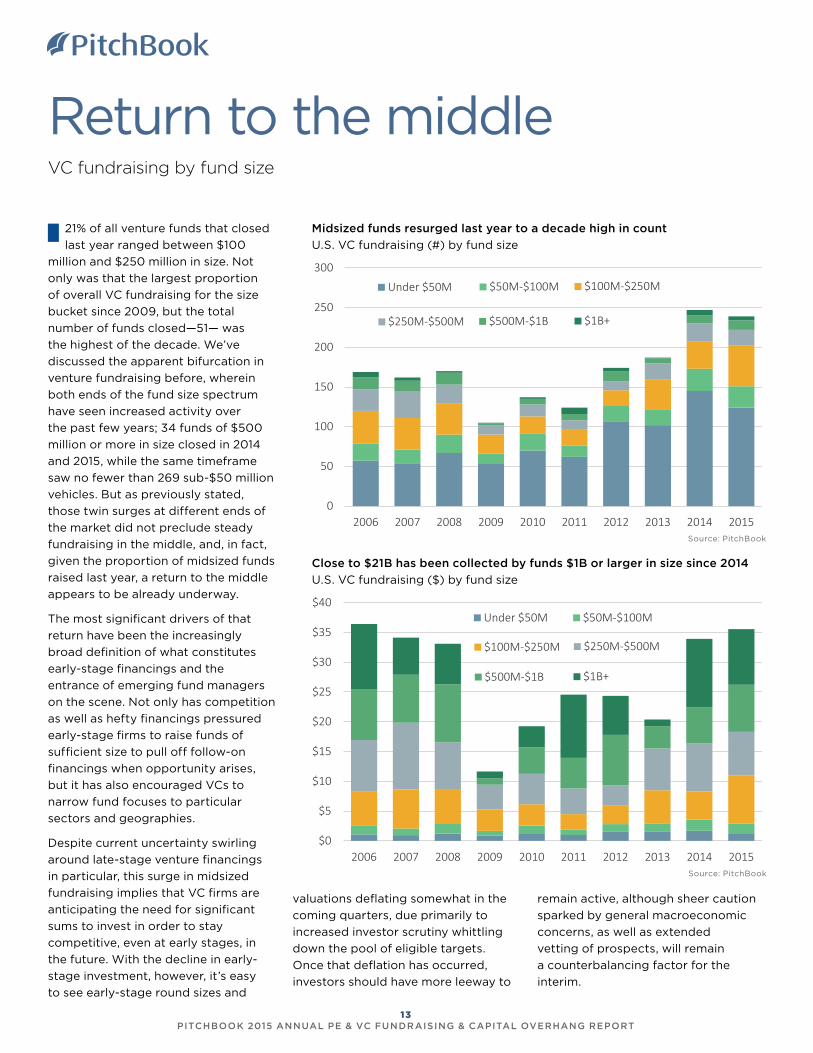

Midsized funds resurged last year to a decade high in count

U.S. VC fundraising (#) by fund size

Close to $21B has been collected by funds $1B or larger in size since 2014

U.S. VC fundraising ($) by fund size

21% of all venture funds that closed

last year ranged between $100

million and $250 million in size. Not

only was that the largest proportion

of overall VC fundraising for the size

bucket since 2009, but the total

number of funds closed—51— was

the highest of the decade. We’ve

discussed the apparent bifurcation in

venture fundraising before, wherein

both ends of the fund size spectrum

have seen increased activity over

the past few years; 34 funds of $500

million or more in size closed in 2014

and 2015, while the same timeframe

saw no fewer than 269 sub-$50 million

vehicles. But as previously stated,

those twin surges at different ends of

the market did not preclude steady

fundraising in the middle, and, in fact,

given the proportion of midsized funds

raised last year, a return to the middle

appears to be already underway.

The most significant drivers of that

return have been the increasingly

broad definition of what constitutes

early-stage financings and the

entrance of emerging fund managers

on the scene. Not only has competition

as well as hefty financings pressured

early-stage firms to raise funds of

sufficient size to pull off follow-on

financings when opportunity arises,

but it has also encouraged VCs to

narrow fund focuses to particular

sectors and geographies.

Despite current uncertainty swirling

around late-stage venture financings

in particular, this surge in midsized

fundraising implies that VC firms are

anticipating the need for significant

sums to invest in order to stay

competitive, even at early stages, in

the future. With the decline in early-

stage investment, however, it’s easy

to see early-stage round sizes and

Return to the middleVC fundraising by fund size

0

50

100

150

200

250

300

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Under $50M $50M-$100M $100M-$250M

$250M-$500M $500M-$1B $1B+

$0

$5

$10

$15

$20

$25

$30

$35

$40

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Under $50M $50M-$100M

$100M-$250M $250M-$500M

$500M-$1B $1B+

Source: PitchBook

Source: PitchBook

valuations deflating somewhat in the

coming quarters, due primarily to

increased investor scrutiny whittling

down the pool of eligible targets.

Once that deflation has occurred,

investors should have more leeway to

remain active, although sheer caution

sparked by general macroeconomic

concerns, as well as extended

vetting of prospects, will remain

a counterbalancing factor for the

interim.

13 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

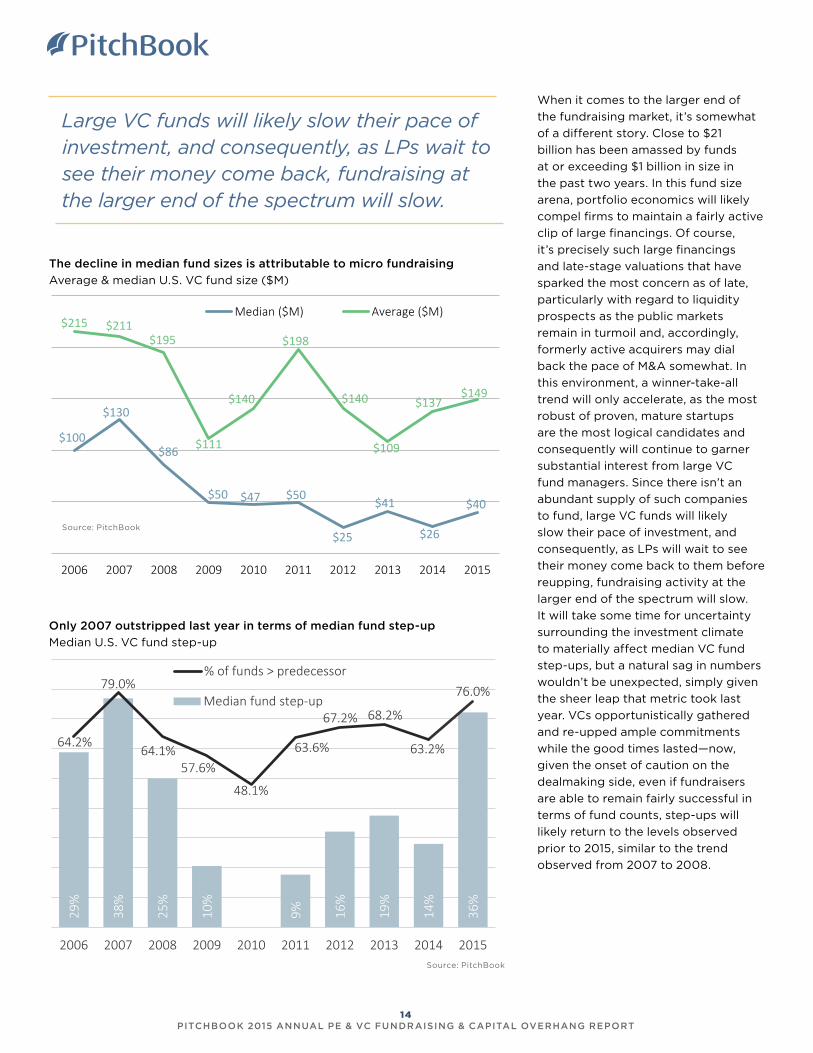

The decline in median fund sizes is attributable to micro fundraising

Average & median U.S. VC fund size ($M)

Only 2007 outstripped last year in terms of median fund step-up

Median U.S. VC fund step-up

$100

$130

$86

$50 $47 $50

$25

$41

$26

$40

$215 $211$195

$111

$140

$198

$140

$109

$137$149

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Median ($M) Average ($M)

Source: PitchBook

29%

38%

25%

10%

0% 9% 16%

19%

14%

36%

64.2%

79.0%

64.1%57.6%

48.1%

63.6%

67.2% 68.2%

63.2%

76.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Median fund step-up

% of funds > predecessor

Source: PitchBook

Large VC funds will likely slow their pace of investment, and consequently, as LPs wait to see their money come back, fundraising at the larger end of the spectrum will slow.

When it comes to the larger end of

the fundraising market, it’s somewhat

of a different story. Close to $21

billion has been amassed by funds

at or exceeding $1 billion in size in

the past two years. In this fund size

arena, portfolio economics will likely

compel firms to maintain a fairly active

clip of large financings. Of course,

it’s precisely such large financings

and late-stage valuations that have

sparked the most concern as of late,

particularly with regard to liquidity

prospects as the public markets

remain in turmoil and, accordingly,

formerly active acquirers may dial

back the pace of M&A somewhat. In

this environment, a winner-take-all

trend will only accelerate, as the most

robust of proven, mature startups

are the most logical candidates and

consequently will continue to garner

substantial interest from large VC

fund managers. Since there isn’t an

abundant supply of such companies

to fund, large VC funds will likely

slow their pace of investment, and

consequently, as LPs will wait to see

their money come back to them before

reupping, fundraising activity at the

larger end of the spectrum will slow.

It will take some time for uncertainty

surrounding the investment climate

to materially affect median VC fund

step-ups, but a natural sag in numbers

wouldn’t be unexpected, simply given

the sheer leap that metric took last

year. VCs opportunistically gathered

and re-upped ample commitments

while the good times lasted—now,

given the onset of caution on the

dealmaking side, even if fundraisers

are able to remain fairly successful in

terms of fund counts, step-ups will

likely return to the levels observed

prior to 2015, similar to the trend

observed from 2007 to 2008.

14 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

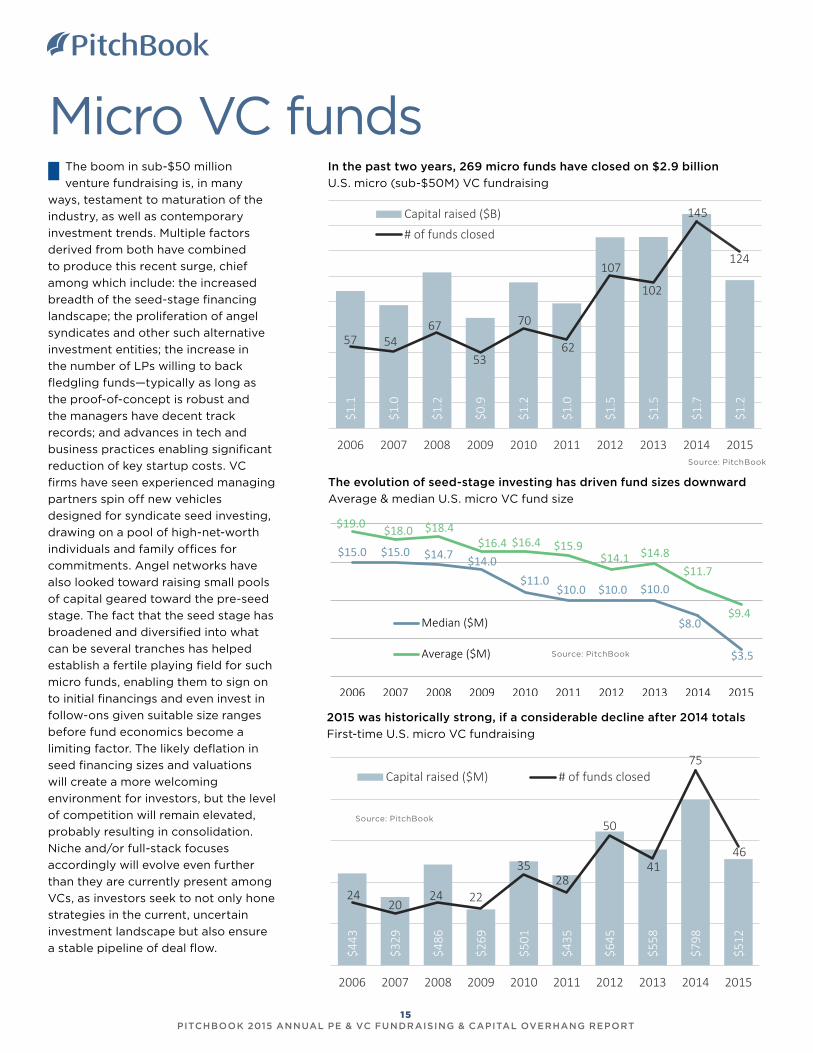

In the past two years, 269 micro funds have closed on $2.9 billion

U.S. micro (sub-$50M) VC fundraising

The evolution of seed-stage investing has driven fund sizes downward

Average & median U.S. micro VC fund size

The boom in sub-$50 million

venture fundraising is, in many

ways, testament to maturation of the

industry, as well as contemporary

investment trends. Multiple factors

derived from both have combined

to produce this recent surge, chief

among which include: the increased

breadth of the seed-stage financing

landscape; the proliferation of angel

syndicates and other such alternative

investment entities; the increase in

the number of LPs willing to back

fledgling funds—typically as long as

the proof-of-concept is robust and

the managers have decent track

records; and advances in tech and

business practices enabling significant

reduction of key startup costs. VC

firms have seen experienced managing

partners spin off new vehicles

designed for syndicate seed investing,

drawing on a pool of high-net-worth

individuals and family offices for

commitments. Angel networks have

also looked toward raising small pools

of capital geared toward the pre-seed

stage. The fact that the seed stage has

broadened and diversified into what

can be several tranches has helped

establish a fertile playing field for such

micro funds, enabling them to sign on

to initial financings and even invest in

follow-ons given suitable size ranges

before fund economics become a

limiting factor. The likely deflation in

seed financing sizes and valuations

will create a more welcoming

environment for investors, but the level

of competition will remain elevated,

probably resulting in consolidation.

Niche and/or full-stack focuses

accordingly will evolve even further

than they are currently present among

VCs, as investors seek to not only hone

strategies in the current, uncertain

investment landscape but also ensure

a stable pipeline of deal flow.

Micro VC funds

$1.1

$1.0

$1.2

$0.9

$1.2

$1.0

$1.5

$1.5

$1.7

$1.2

57 5467

53

70

62

107

102

145

124

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Capital raised ($B)

# of funds closed

Source: PitchBook

$15.0 $15.0 $14.7 $14.0$11.0

$10.0 $10.0 $10.0

$8.0

$3.5

$19.0 $18.0 $18.4$16.4 $16.4 $15.9

$14.1 $14.8$11.7

$9.4

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Median ($M)

Average ($M) Source: PitchBook

2015 was historically strong, if a considerable decline after 2014 totals

First-time U.S. micro VC fundraising

$443

$329

$486

$269

$501

$435

$645

$558

$798

$512

2420

24 22

3528

50

41

75

46

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Capital raised ($M) # of funds closed

Source: PitchBook

15 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

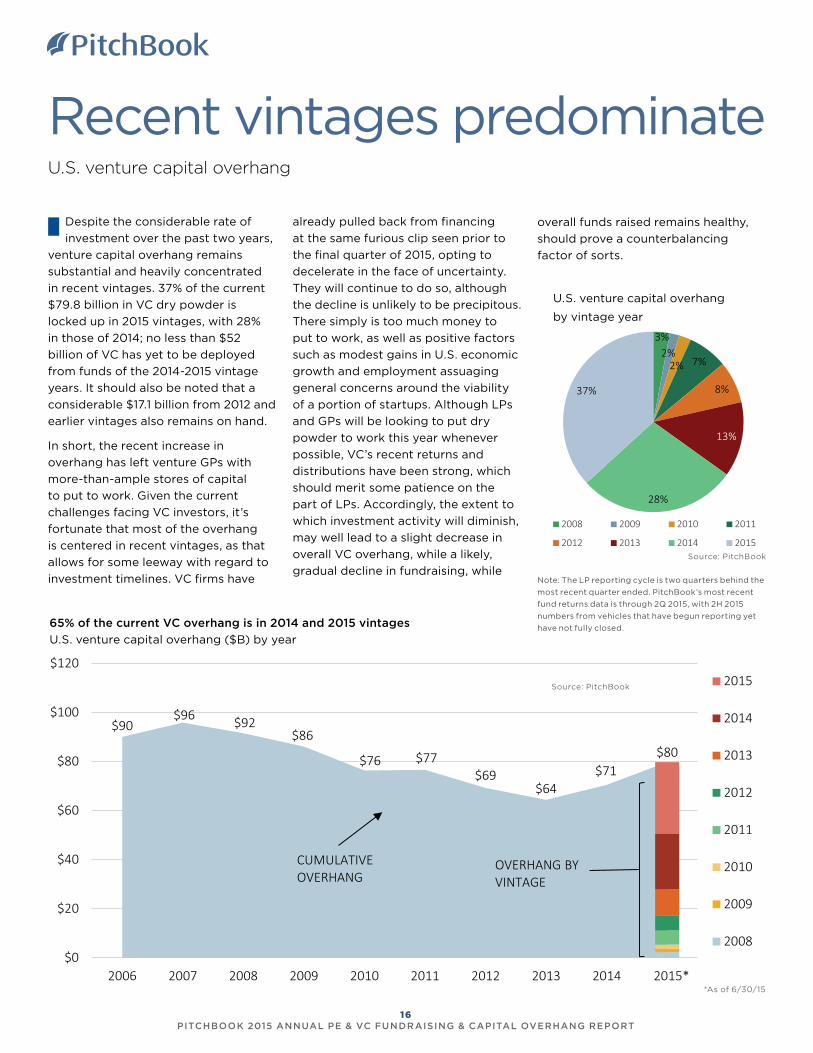

Recent vintages predominateU.S. venture capital overhang

Despite the considerable rate of

investment over the past two years,

venture capital overhang remains

substantial and heavily concentrated

in recent vintages. 37% of the current

$79.8 billion in VC dry powder is

locked up in 2015 vintages, with 28%

in those of 2014; no less than $52

billion of VC has yet to be deployed

from funds of the 2014-2015 vintage

years. It should also be noted that a

considerable $17.1 billion from 2012 and

earlier vintages also remains on hand.

In short, the recent increase in

overhang has left venture GPs with

more-than-ample stores of capital

to put to work. Given the current

challenges facing VC investors, it’s

fortunate that most of the overhang

is centered in recent vintages, as that

allows for some leeway with regard to

investment timelines. VC firms have

65% of the current VC overhang is in 2014 and 2015 vintages

U.S. venture capital overhang ($B) by year

U.S. venture capital overhang

by vintage year

Source: PitchBook

3%2%

2% 7%

8%

13%

28%

37%

2008 2009 2010 2011

2012 2013 2014 2015

$90$96 $92

$86

$76 $77$69

$64$71

$80

$0

$20

$40

$60

$80

$100

$120

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

2015

2014

2013

2012

2011

2010

2009

2008

CUMULATIVEOVERHANG

OVERHANG BY VINTAGE

Source: PitchBook

already pulled back from financing

at the same furious clip seen prior to

the final quarter of 2015, opting to

decelerate in the face of uncertainty.

They will continue to do so, although

the decline is unlikely to be precipitous.

There simply is too much money to

put to work, as well as positive factors

such as modest gains in U.S. economic

growth and employment assuaging

general concerns around the viability

of a portion of startups. Although LPs

and GPs will be looking to put dry

powder to work this year whenever

possible, VC’s recent returns and

distributions have been strong, which

should merit some patience on the

part of LPs. Accordingly, the extent to

which investment activity will diminish,

may well lead to a slight decrease in

overall VC overhang, while a likely,

gradual decline in fundraising, while

overall funds raised remains healthy,

should prove a counterbalancing

factor of sorts.

*As of 6/30/15

Note: The LP reporting cycle is two quarters behind the

most recent quarter ended. PitchBook’s most recent

fund returns data is through 2Q 2015, with 2H 2015

numbers from vehicles that have begun reporting yet

have not fully closed.

16 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

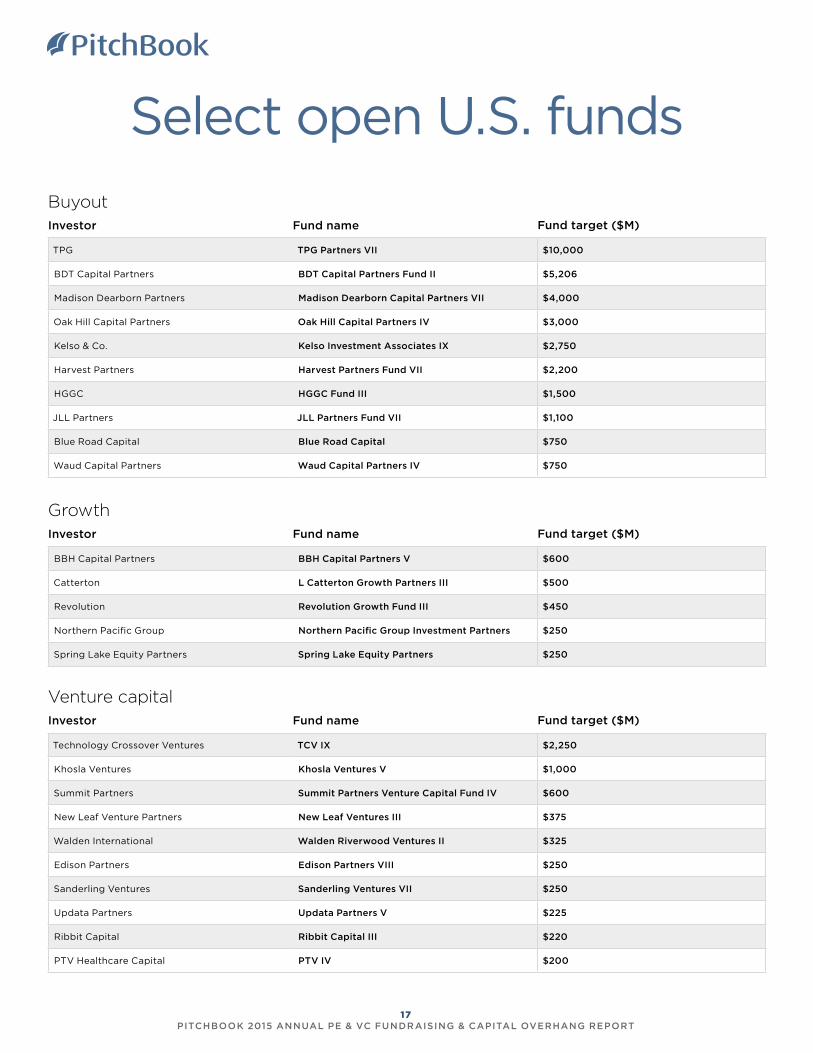

Select open U.S. funds

TPG TPG Partners VII $10,000

BDT Capital Partners BDT Capital Partners Fund II $5,206

Madison Dearborn Partners Madison Dearborn Capital Partners VII $4,000

Oak Hill Capital Partners Oak Hill Capital Partners IV $3,000

Kelso & Co. Kelso Investment Associates IX $2,750

Harvest Partners Harvest Partners Fund VII $2,200

HGGC HGGC Fund III $1,500

JLL Partners JLL Partners Fund VII $1,100

Blue Road Capital Blue Road Capital $750

Waud Capital Partners Waud Capital Partners IV $750

Investor Fund name Fund target ($M)

Buyout

Growth

Venture capital

BBH Capital Partners BBH Capital Partners V $600

Catterton L Catterton Growth Partners III $500

Revolution Revolution Growth Fund III $450

Northern Pacific Group Northern Pacific Group Investment Partners $250

Spring Lake Equity Partners Spring Lake Equity Partners $250

Investor Fund name Fund target ($M)

Technology Crossover Ventures TCV IX $2,250

Khosla Ventures Khosla Ventures V $1,000

Summit Partners Summit Partners Venture Capital Fund IV $600

New Leaf Venture Partners New Leaf Ventures III $375

Walden International Walden Riverwood Ventures II $325

Edison Partners Edison Partners VIII $250

Sanderling Ventures Sanderling Ventures VII $250

Updata Partners Updata Partners V $225

Ribbit Capital Ribbit Capital III $220

PTV Healthcare Capital PTV IV $200

Investor Fund name Fund target ($M)

17 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

MethodologyPRIVATE EQUITY FUNDS

The following fund types are used in PitchBook’s PE fundraising data: buyout, co-investment, mezzanine,

restructuring/distressed situations, energy and PE growth/expansion. This report only includes U.S.-based

funds that have held their final close. Note: for U.S. PE and VC contributions versus capital raised, the

contributions are the sums called down in the U.S. from limited partners by general partners, compared to

overall capital raised, in a given timeframe.

VENTURE CAPITAL FUNDS

In addition to traditional VC funds, PitchBook also includes corporate VC funds and seed-stage funds in our

VC fundraising total. Funds that identify themselves as growth-stage vehicles are classified as PE funds in

this report. Only U.S.-based funds that have held their final close are included in the fundraising numbers.

CLOSE DATE AND VINTAGE

Unless otherwise noted, the fundraising data in this report is based on a fund’s close date. The vintage year

is based on the vintage year reported by the GP and LPs, otherwise the year in which a fund holds its final

close is used.

CAPITAL OVERHANG

Calculated using the most recently available fund cashflow data, the capital overhang in this report is

updated through June 30, 2015. The capital overhang is based on vintage year and only capital that is held

in closed funds is considered (i.e. evergreen funds are not counted). If a fund closed on July 1, 2015 or later,

it is only included in the dry powder figure if it previously held a first close and has cashflow data available.

FUND LOCATION

A fund’s location is determined by the country or region where the majority of its investments have been, or

will be, made. Only U.S.-based funds are included in this report.

18 PITCHBOOK 2015 ANNUAL PE & VC FUNDRAISING & CAPITAL OVERHANG REPORT

Contact PitchBook

pitchbook.com

RESEARCH [email protected]

EDITORIAL [email protected]

SALES [email protected]

The data you need to be a better VC investor

With data on:

Companies

Investors

Deals

M&A

Limited partners

Funds

Financials

Advisors

People

Request a free trial

US +1 206.623.1986

UK +44 (0)207.190.9809

pitchbook.com

The PitchBook Platform for venture capital

• Know everything that happens in the venture space

• Make smarter investments

• Find LPs & raise funds faster

• Elevate your firm with kick-ass technology