7355347 valuation ratios

TRANSCRIPT

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 1/136

Integrated Financial Management Oct 24, 20081

Financial Statement Analysis for Modeling

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 2/136

Integrated Financial Management Oct 24, 20082

Financial Statement Analysis Contents

• Overview and objective of financial statement analysis

• Review and Re-formatting Statements for Financial Model

Income Statement – EBITDA and NOPLAT

Cash Flow Statement - Free Cash Flow and Equity Cash Flow

• Financial ratio analysis

Management Performance

Valuation

Credit Analysis

Financial Model Drivers

• Reference

Financial Ratio Calculations

Discussion of Economic Profit

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 3/136

Integrated Financial Management Oct 24, 20083

Financial Statement Analysis - Introduction

• Corporate models involve making a projection of the financial statements

of a company or a segment of a company.

• You should be comfortable in reading various different financial

statements to be effective at financial modeling and financial analysis.

• Financial statement analysis is also important in:

Assessing management performance of a company and whether projections of improvement or sustainability are reasonable.

Assessing the value of a company from historic performance.

Assessing the reasonableness of financial projections provided by acompany or the validity of earnings projections

Assessing whether the financial structure of a company is of investment grade quality

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 4/136

Integrated Financial Management Oct 24, 20084

Objectives of Financial Statement Analysis

• Financial Statement Analysis is Like Detective Work – How can we use

information in financial statements to make assessments of various issue:

How can we quickly review the income statement, balance sheetand cash flow statement to determine how the stock market value of a company compares to inherent value.

How can we look the financial statements and assess risksassociated with a company and whether the company has sufficientcash flow to pay off debt.

Finance and valuation are about projecting the future -- how canfinancial statement analysis be used in making projections.

The problem in any financial analysis and valuation is thatmeasuring risk is very difficult

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 5/136

Integrated Financial Management Oct 24, 20085

Financial Statement Analysis and Financial Projections

• In corporate models, financial performance is measured and value is assessed

with various financial ratios. Some of the uses of financial ratios in assessing

corporate models include:

Relate financial ratios to economic drivers in making financial forecasts

Use financial ratios to determine whether management is generating

economic profit – compute ROIC and growth to examine sustainability.

Evaluate the sustainability of economic profit over the long-term in financialmodels – attempt to gather 10 years of data to find trends.

Assess the potential for growth in economic profit – ROIC less WACC

Value the equity of the company relative to the stock price

Review the credit quality of the firm with financial ratios

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 6/136

Integrated Financial Management Oct 24, 20086

Double Counting and Judgments in Financial Ratio Analysis

• In analyzing financial statements judgments must be made in computing key datasuch as EBITDA and in developing financial ratios.

• Examples

Other Income in or out of EBITDA

If not in EBITDA, then mush add non-consolidated subsidiarycompanies

Exploration Expenses taken out of EBITDA

Make consistent between companies with different accounting policies

Goodwill (ROIC without goodwill)

Minority Interest (Include or exclude income and balance)

Total in EBITDA, must account for minority interest in financing of totalEBITA

Deferred Debit Amortization

• A key principle is that the financial data and the financial ratios are consistent andlogical – work through simple examples

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 7/136Integrated Financial Management Oct 24, 20087

Income Statement

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 8/136Integrated Financial Management Oct 24, 20088

Income Statement

• Review trends in EBITDA, EBIT, EBT and Net Income and explain what ishappening to the company

• EBITDA includes operating earnings and other income, but it does not includeforeign exchange gains or losses, minority interest, extraordinary income or interest income.

EBITDA is a rough proxy for free cash flow

EBITDA is not generally shown on Income Statement

Potential Adjustments for items such as exploration expense

Compare EBIT to Net Assets and Net Capital

• Ratio of EBITDA to Revenues should be shown for historic and projected periods

• EBITDA is related to un-levered cash flow while Net Income and EPS are after leverage

• NOPLAT is computed by EBIT less adjusted taxes, where taxes are computedthrough adjusting income taxes.

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 9/136Integrated Financial Management Oct 24, 20089

Problems with EBITDA

• EBITDA is useful in its simplicity, and can be a good reference for

comparison of debt and value, but it has weaknesses:

EBIT is more important than DA

In credit analysis, EBITDA works better for low rated credits than

high rated credits. (Moody’s)EBITDA is a better measure for companies with long-lived assets

EBITDA can be manipulated through accounting policies (operatingexpenses versus capital expenditures)

EBITDA ignores changes in working capital, does not consider required re-investment, says nothing about the quality of earnings,and it ignores unique attributes of industries.

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 10/136Integrated Financial Management Oct 24, 200810

Simplified Income Statement

• Sales- COGS

• = Gross Margin- SG&A- Other Expenses

• + Other Income

•= EBITDA

• - Depreciation and Amortization

• = EBIT

• - Interest Expense (income)

• = EBT- Income Taxes

• - Minority Interest

• = Net Income

NOPLAT = EBIT x (1-tax rate)

NOPLAT = Net Income + Interest Expense x (1-tax)

There is a debate about how to handle

other income from non-consolidated

subsidiary companies.

One school of thought (McKinsey) is that

they should be valued separately sincethey will have different cost of capital etc.

In this case, do not include in EBITDA

and remove the asset balance from the

invested capital. Must be consistent

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 11/136Integrated Financial Management Oct 24, 200811

Analysis of Income Statement – Computation of EBITDA,

Minority Interest, Preferred Dividends, Exploration Expense

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 12/136Integrated Financial Management Oct 24, 200812

Income Statement Analysis

• Example of Adjustments to EBITDA

Exploration Expenses (EBITDAX)

Rental and Lease Payments (EBITDR)

• EBITDA Computation

Top Down – move other income

Bottom-up (Indirect)

• EBITDA Notes

Interest Income out of EBITDA

Interest Expense not in EBITDA

Understand Non-cash Expenses

Deferred Mining Costs

Equity Income

Minority Interest

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 13/136Integrated Financial Management Oct 24, 200813

Employee Stock Options

• One can debate the treatment of employee stock options for EBITDA,

free cash flow and valuation.

• Think of options as giving stock to employees

If the treatment has changed over the years and it is a significant

expense, make adjustments to current or prior statements for consistency.

Think of options as giving free shares to employees. The value of existing shareholders is diluted.

One can argue that this is two things

First, employees are compensated and the cash should beaccounted for

Second, invested capital is increased and the new equityshould be refelected

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 14/136Integrated Financial Management Oct 24, 200814

Cash Flow Statement

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 15/136Integrated Financial Management Oct 24, 200815

Cash Flow Statement

• Cash Flow has fundamental separation between

Operations

Capital expenditures (to maintain and grow operations) and

Financing

• Operating Cash Flow

Add back items from the income statement that do not use cash(depreciation, dry hole costs etc)

• Analyze how much cash flow the company generated and how it raised funds or

disposed funds

• Use Cash Flow statement as a basis to compute free cash flow although cash flow

not presented on the statement

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 16/136Integrated Financial Management Oct 24, 200816

Cash Flow Statement

• A. Operating Cash Flows

• 1) “Cash Flow from Operations”

• 2) Cash Collections

• 3) Cash Outflows

• 4) Interest & Dividends Received

• 5) Interest Paid

• 6) Taxes

• B. Investing Cash Flows

• 1) “Cash Flow from Investments”

• 2) Cap Ex (Purchases)

• 3) Sale of Property, Plant, & Equipment

• 4) Inter-Corporate Investment

• C. Financing Cash Flows

• 1) “Cash Flow from Financing”

• 2) Dividend Payments

• 3) Proceeds from Equity or Debt Issuance

• 4) Equity Repurchased

• 5) Debt Principal Payments

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 17/136Integrated Financial Management Oct 24, 200817

Cash Flow Statement Example

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 18/136Integrated Financial Management Oct 24, 200818

The Notion of Free Cash Flow

• In practice the term cash flow has many uses. For example, operatingcash flow is net income plus depreciation.

• Free cash flow is the cash flow that is available to investors – FREE of obligations such as capital expenditures and taxes -- to both debt andequity investors – after re-investing in plant, and financing and paying

taxes.• Accountants define cash flow from operations as net income plus

depreciation and other non-cash items less changes in working capital.However, this cash flow is not available for distribution to equity holdersand debt holders. The free cash flow must account for capitalexpenditures, repayments of debt, deferred items and other factors.

• Free cash flow consists of

Cash flow to equity holders

Cash flow to debt holders

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 19/136Integrated Financial Management Oct 24, 200819

Importance of Free Cash Flow

• Alternative Definitions, but one correct concept

Free Cash Flow Is Also Known As Unleveraged Cash Flow

Unleveraged Cash Flow Is Not Distorted By The Capital Structure

Free Cash Flow should not change when the capital structure changes

Free Cash Flow should be the same as equity cash flow if no debt isoutstanding and not cash balances are built up.

• Free Cash Flow in Valuation

PV of Free Cash Flow Defines Enterprise Value

The Relevant Discount Rate Is The Unlevered Discount Rate or theWeighted Average Cost of Capital

IRR on Free Cash Flow is the Project IRR

Free Cash Flow in Economic Value

FCF – Carrying Charge = Economic Profit

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 20/136Integrated Financial Management Oct 24, 200820

Fundamental Distinction in Financial Analysis – Free Cash

Flow and Equity Cash Flow

• Free Cash flow that is independent from financing

Valuation

Performance in managing assets

Claims on free cash flow

Cash flow to pay debt obligations

Comparisons unbiased by capital structure policy

• Equity cash flow

Valuation of equity securities

Performance for shareholders

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 21/136Integrated Financial Management Oct 24, 200821

Cash Flow Statement in Financial Model

• Analysis in Cash Flow Statements

Compute Cash Flow before Financing

Operating Cash Flow minus Capital Expenditures

Use Cash Flow Before Financing in Deriving Free Cash Flow

Equity Cash Flow

Dividends less Cash Investments

Cash Flow Before Financing less Maturities plus New Debt Issues

Last Line on Cash Flow Statement Includes

Change in Cash Balance

Change in Short-term Debt or Overdrafts

Beginning Balance + Change = Ending Cash

Beginning Balance of STD + Change = Ending Short-term Debt

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 22/136Integrated Financial Management Oct 24, 200822

Free Cash Flow Formulas

• Free cash flow can be computed from the income statement or from the cash flow statement.

• From the cash flow statement, the formula is:

Cash Before Financing

Plus: Interest Expense

Less: Tax Shield on Interest

• From the income statement, the formula is:

EBITDA

Less: Taxes on EBIT

Less: Working Capital Investment

Less: Capital Expenditures

• From Net Income

Net Income

Add: Net of Tax Interest

Add Depreciation, Deferred Taxes and Other Non-Cash Changes

Less: Changes in Working Capital

Less: Capital Expenditures

Some argue that free cash flow

should not include non-operating

items. Here the non-consolidated

companies are treated in a similar

manner as liquid investments

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 23/136

Integrated Financial Management Oct 24, 200823

Free Cash Flow from NOPLAT

• Free cash flow can be computed using the notion of net operating profit lessadjusted tax as follows (assuming no extraordinary income)

• Step 1: Compute NOPLAT

Net Income

Plus Net Interest after Tax

Plus Deferred tax

Equals NOPLAT

• Step 2: Compute Free Cash Flow

NOPLAT

Plus: Depreciation

Less: Change in Working Capital

Less: Capital Expenditures

Equals Free Cash Flow

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 24/136

Integrated Financial Management Oct 24, 200824

Free Cash Flow Example

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 25/136

Integrated Financial Management Oct 24, 200825

Balance Sheet

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 26/136

Integrated Financial Management Oct 24, 200826

Balance Sheet Issues

• Treat surplus cash as negative debt and debt as negative cash

Rule of thumb – cash is 2% of revenues

Example – when developing a basic cash flow model, group thecash and the debt as one account and then separate this accounton the balance sheet.

Unfunded pension expenses should be treated like debt – theyinvolve a fixed obligation and they can be replaced with debt whenthey are funded.

Deferred taxes depend on the way deferred taxes are modelled for cash flow purposes. If you model future changes in deferred taxesand take account of these in projections, do not put deferred taxesas a component of equity.

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 27/136

Integrated Financial Management Oct 24, 200827

Plant Balances and Retirements

• You can account for capital expenditures by subtracting accounts fromthe balance sheet.

Be careful with retirements

Retirements reduce both the plant balance and the accumulateddepreciation

Accumulated depreciation difference can be compared to thecurrent depreciation expense and the difference is retirement.

The retirements are then use along with plant balance changes toderive the capital expenditures

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 28/136

Integrated Financial Management Oct 24, 200828

Balance Sheet

• Maintains value of assets – from original cost rather than market valueand may be conservative

• Used for base for many financial ratios – debt to capital, depreciation

rates, return on average equity, return on invested capital

• Use to establish the historical analysis and where money was earned andwhere it is spent

• Important as an audit tool in financial modeling

• Total Assets = Total Liabilities + Total Equity

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 29/136

Integrated Financial Management Oct 24, 200829

Balance Sheet Adjustment

• In modeling the balance sheet, a number of adjustments should be madefrom actual balance sheets:

Surplus cash must be separated from other current assets

Short-term debt should be separated from other current liabilities

Current Portion of Long-term Debt should be classified as long-termdebt for reconciliation

Common equity can be aggregated

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 30/136

Integrated Financial Management Oct 24, 200830

Balance Sheet Issues

• Selected Balance Sheet Issues for Financial Analysis

Definition of Capital

Minority Interests

Short-term Debt

Preferred Stock

All Common Equity

Components of Equity Capital

Definition of Book Value per Share

Deferred Debits and Credits

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 31/136

Integrated Financial Management Oct 24, 200831

Balance Sheet

• Total Assets” breaks into:• A. Current Assets

1) Cash & Cash Equivalents2) Marketable Securities

• 3) Accounts Receivable4) Inventories

• B. Fixed Assets1) Net Property Plant and Equipment2) Goodwill (Type 1)3) Other

• “Total Liabilities” breaks into:

• A. Current Liabilities1) Accounts Payable2) Current Portion of Long-Term Debt3) Current Capital Lease Obligation

• B. Long Term Liabilities1) Long-Term Debt2) Capital Leases3) Pension Liabilities4) Others (Deferred Tax Liability, etc)

• “Total Equity” breaks into:• A. Stock

1) Preferred2) Common3) Treasury

• B. Retained Earnings

• C. Other (Translation Gains/Losses, etc)

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 32/136

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 33/136

Integrated Financial Management Oct 24, 200833

Balance Sheet Issues in Modeling

• Compute Debt Balance from Separate Debt Balance

• Understand Deferred Debits and Deferred Credits (for example deferred

compensation or long-term pre-paid expenses)

• Equity Balance from Retained Earnings Statement can be Incorporated in

Statement

• Incorporation of Asset write-ups or write-downs

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 34/136

Integrated Financial Management Oct 24, 200834

Financial Ratio Analysis

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 35/136

Integrated Financial Management Oct 24, 200835

Contents

• Introduction

• Management Performance Ratios

• Valuation Ratios

• Credit Analysis Ratios

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 36/136

Integrated Financial Management Oct 24, 200836

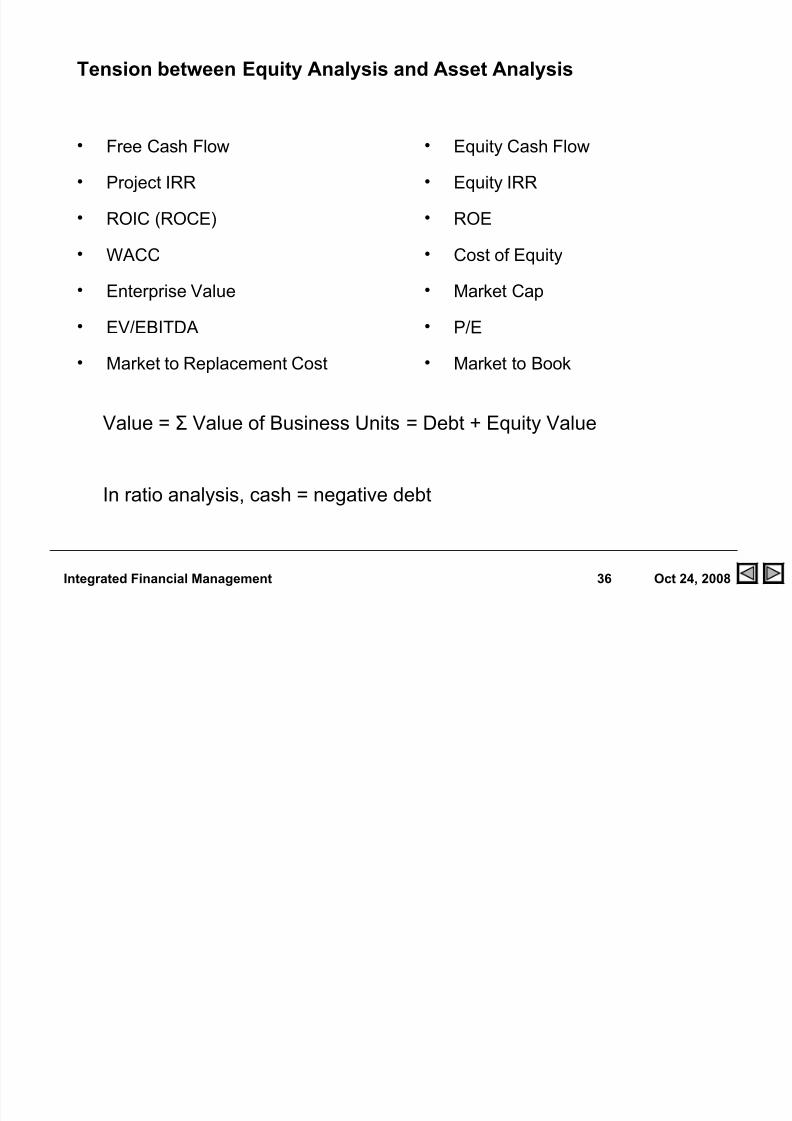

Tension between Equity Analysis and Asset Analysis

• Free Cash Flow

• Project IRR

• ROIC (ROCE)

• WACC

• Enterprise Value

• EV/EBITDA

• Market to Replacement Cost

• Equity Cash Flow

• Equity IRR

• ROE

• Cost of Equity

• Market Cap

• P/E

• Market to Book

Value = Σ Value of Business Units = Debt + Equity Value

In ratio analysis, cash = negative debt

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 37/136

Integrated Financial Management Oct 24, 200837

Financial Ratio Analysis

• Purpose :

Evaluate relation between two or more economically important items (one isthe starting point for further analysis)

Cautions:

Accounting analysis is important (deferred taxes etc.)

• Interpretation is key

What does the P/E mean

Is an interest coverage of 3.5 good

Why is the ROIC low

Should we use MB, PE or EV/EBITDA

• Document financial ratios (numerator and denominator) with footnotes andcomments

• Show components of numerator and denominator in rows above the ratiocalculation

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 38/136

Integrated Financial Management Oct 24, 200838

• Financial Ratios Often Compares Income Statement or Cash Flow with BalanceSheet

In developing ratios, understand why the formula is developed (e.g. other income and other investments in return on invested capital)

• There is Not Necessarily One Single Correct Formula

For example, pre-tax or after-tax return on assets.

Keep the numerator consistent with the denominator

• Financial Ratios should be evaluated in the context of benchmarks

Credit ratios and bond rating standards

Returns and cost of capital

Operating ratios and history

General Discussion of Financial Ratios

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 39/136

Integrated Financial Management Oct 24, 200839

Classes of Financial Ratios

• Management Performance

Ratios that measure the historic economic performance of management andevaluate whether the economic performance can be maintained (e.g. ROIC)

• Valuation

Ratios that are used to give an indication of the value of the company (e.g.

P/E)

• Credit Analysis

Ratios that gauge the credit quality and liquidity of the company (e.g.Interest coverage and current ratio)

• Model Evaluation

Ratios used to evaluate the assumptions and mechanics of financialforecasts

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 40/136

Integrated Financial Management Oct 24, 200840

Ratios that Measure Management

Performance

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 41/136

Integrated Financial Management Oct 24, 200841

• Evaluate Whether Management is Doing a Good Job with Investor Funds (Not if the company is appropriately valued)

Return on Invested Capital

Return on Assets

Return on Equity

Market/Book Ratio

Market Value/Replacement Cost

• Key Issue

Evaluate relative to risk

ROE versus Cost of Equity

ROIC versus WACC

Class 1: Financial Indicators of Management Performance

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 42/136

Integrated Financial Management Oct 24, 200842

Basic Economic Principles, ROIC and Financial Analysis

• When you measure value, you are gauging the ability of a firm to realizeeconomic profit. For example, when you compare the equity IRR with the

equity cost of capital.

• When you assess assumptions in a financial forecast, you must assess

whether economic profit implicit in the assumptions can in fact be

realized. For example, if the financial forecast has a very high ROE, isthat reasonable.

• When you interpret financial statistics, you are gauging the strategy of the

company in terms of whether economic profit is being realized. In

reviewing the return on invested capital, does this demonstrate that the

company has the potential to earn economic profit.

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 43/136

Integrated Financial Management Oct 24, 200843

Return on Invested Capital Analysis

• ROIC is not distorted by the leverage of the company

• ROIC can be used to gauge economic profit and whether the company

should grow operations

• ROIC can be used to assess the reasonableness of projections

For example, if ROIC is very high and the company is in acompetitive business with few barriers to entry, the forecast isprobably not realistic.

• ROIC can be computed on a division basis EBIT and allocation of capital

to divisions from net assets to gauge the profit of parts of the company

• ROIC comes from sustainable competitive advantage and high market

share

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 44/136

Integrated Financial Management Oct 24, 200844

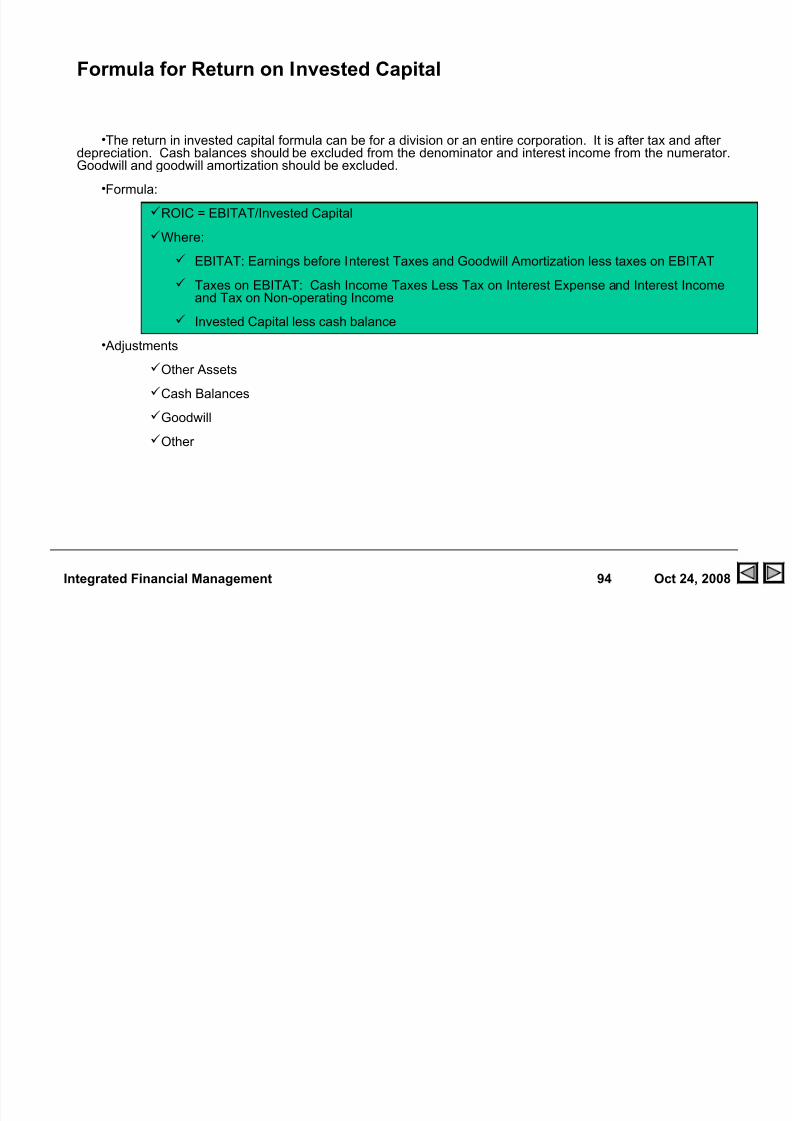

Formula for Return on Invested Capital

• The return in invested capital formula can be for a division or an entire corporation. It is after tax and after depreciation. Cash balances should be excluded from the denominator andinterest income from the numerator. Goodwill and goodwill amortization should be excluded.

• Formula:

ROIC = EBITAT/Invested Capital

Where:

EBITAT: Earnings before Interest Taxes and Goodwill Amortization less taxeson EBITAT

Taxes on EBITAT: Cash Income Taxes Less Tax on Interest Expense andInterest Income and Tax on Non-operating Income

Invested Capital less cash balance

• Adjustments

Other Assets

Cash Balances

Goodwill

Other

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 45/136

Integrated Financial Management Oct 24, 200845

Issues in Management Performance Evaluation

• Basic Formula: ROIC versus WACC How to compute ROIC

NOPLAT/Average Invested Capital

May or may not include goodwill – If goodwill is not included, computeNOPLAT without subtracting goodwill write-off and subtract netgoodwill from invested capital

Reduce the invested capital by surplus cash balances

Some don’t include other income – then the invested capital should bereduced by other investments

Can compute with ratios

EBIT Margin x (1-t) * Asset Turn

Asset Turn = Sales/Assets; EBIT Margin = EBIT/Sales

ROCE vs ROIC

ROCE is generally computed in an indirect way by starting with netincome, and adding net of tax interest and adding minorities

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 46/136

Integrated Financial Management Oct 24, 200846

• Return on average capital employed (ROCE) is a performance measure ratio.From the perspective of the business segments, ROCE is annual business

segment earnings divided by average business segment capital employed

(average of beginning and end-of-year amounts).

• These segment earnings include ExxonMobil’s share of segment earnings of

equity companies, consistent with our capital employed definition, and exclude the

cost of financing.

• The corporation’s total ROCE is net income excluding the after-tax cost of

financing, divided by total corporate average capital employed. The corporation

has consistently applied its ROCE definition for many years and views it as the

best measure of historical capital productivity in our capital intensive long-

term industry, both to evaluate management’s performance and to

demonstrate to shareholders that capital has been used wisely over the long term. Additional measures, which tend to be more cash flow based, are used for

future investment decisions.

Exxon Mobil Return on Average Capital Employed

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 47/136

Integrated Financial Management Oct 24, 200847

Exxon Mobil Return on Capital Employed – Where are they

making expenditures

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 48/136

Integrated Financial Management Oct 24, 200848

Exxon Mobil Return on Capital

Return on average capital employed 2005 2004 2003

-millions of dollars

Net income $ 36,130.00 $ 25,330.00 $ 21,510.00

Financing costs -after tax

Third-party debt (1.00) (137.00) (69.00)

ExxonMobil share of equity companies (144.00) (185.00) (172.00)

All other financing costs – net -1 (295.00) 54.00 1,775.00

Total financing costs (440.00) (268.00) 1,534.00

Earnings excluding financing costs $ 36,570.00 $ 25,598.00 $ 19,976.00

Average capital employed $ 116,961.00 $ 107,339.00 $ 95,373.00

Return on average capital employed – corporate total 31.30 23.80 20.90

“All other financing costs – net” in 2003 includes

interest income (after tax) associated with the

settlement of a U.S. tax dispute.

(1)

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 49/136

Integrated Financial Management Oct 24, 200849

Illustration of Invested Capital Computation

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 50/136

Integrated Financial Management Oct 24, 200850

ROE and ROIC – Note how to compute growth rates from ROE

and Retention

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 51/136

Integrated Financial Management Oct 24, 200851

Example of Return on Capital Employed (Return on Invested Capital)

in Financial Analysis

•The argument has been made that the best measure to evaluate managementperformance that is not distorted by leverage (as in the case of ROE) or has theproblems of ROA is the return on invested capital. An example of use of this ratio isin the Exxon Mobile Merger:

J.P. Morgan reviewed and analyzed the return on capital employed("ROCE") of both Exxon and Mobil since 1993. J.P. Morgan observed thatExxon's ROCE has consistently been 2-3% above that of Mobil.

J.P. Morgan's analysis indicated that if Mobil were to be merged withExxon, the combined entity's capital productivity would eventually behigher than the pro forma capital productivity of Exxon and Mobil.

J.P. Morgan indicated that it would be reasonable to assume that thebenefits of this capital productivity increase would occur within three years of

the closing of the merger.

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 52/136

Integrated Financial Management Oct 24, 200852

Profitability

Gross Margin = Gross profit/ Sales

Less: Operating costs/ Sales

Equals EBIT Margin (EBIT/ Sales)

Asset Utilization

Working Capital/ SalesPlus:

Long-term capital/ Sales

Equals:Capital employed/ Sales

1 divided by Capital Employed/ Sales

Equals: Asset Turnover

(Sales/ Capital Employed)

ROCE(EBIT/ Capital Employed )

Multiplied by

Multiplied by (1 minus Tax Rate)

ROCE(EBIT after Tax/ Capital Employed )

Relationship Between Various Ratios and DuPont Analysis

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 53/136

Integrated Financial Management Oct 24, 200853

Drivers of Value and Free Cash Flow from Financial Ratios

• Revenues

Growth in Revenues

• EBITDA Margin

Multiplied by

• Revenues = EBITDA

• Less: Depreciation Rate

Multiplied by

• Fixed Assets = EBIT

• Fixed Assets = Sales x Sales/Assets (Turnover)

• Ratios Needed: Growth in Revenues, EBITDA Margin, DepreciationRate and Asset Turnover

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 54/136

Integrated Financial Management Oct 24, 200854

Example of Using Ratios to Compute Free Cash Flow

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 55/136

Integrated Financial Management Oct 24, 200855

Class 2: Financial Indicators of Market Value

• Financial Ratios can be used to analyze whether the valuation of a company isappropriate. Analysts should understand the drivers of different ratios. Valuation

Ratios include:

Universal Financial Ratios

Price to Earnings Ratio

Enterprise Value/EBITDA

PEG (P/E to Earnings Growth) Ratio

Market to Book Ratio

Industry Specific Financial Ratios

Value/Reserve

Value/Customer

Value/Plane Seat

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 56/136

Integrated Financial Management Oct 24, 200856

Valuation Ratios and Benchmarks

• Valuation ratios measure the stock market value of a company relative tosome accounting measure such as EPS, EBITDA, Book Value/Share or

growth in EPS

• The ratios can be used as benchmarks in valuing non-traded companies

by using industry average valuation ratios.

• Example to value non-traded company:

Value of company = EPS of Company x Industry Average P/E Ratio

• Valuation ratios will be further discussed in the portion of the course

where corporate models are used to value companies.

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 57/136

Integrated Financial Management Oct 24, 200857

• The P/E Ratio is the most prominent valuation ratio. It is affected by estimatedearnings growth, the ability of a company to earn economic profits and the growthin profitable operations.

• Formula:

Share Price/Earnings per Share

• Issues Trailing Twelve Months and Forward Twelve Months – Generally use

forward EPS

Formula: (1-g/r)/(k-g)

• Problems

Affected by earnings adjustments

Causes too much focus on EPS

Distortions created by financing

P/E Ratio

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 58/136

Integrated Financial Management Oct 24, 200858

Illustration of EV Ratios and Computation of Market Value of

Balance Sheet Components

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 59/136

Integrated Financial Management Oct 24, 200859

Investment Banker Analysis of Comparable Multiples

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 60/136

Integrated Financial Management Oct 24, 200860

Investment Banker Analysis of Multiples

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 61/136

Integrated Financial Management Oct 24, 200861

Use of PE in Valuation

• The long-run P/E ratio is often used in valuation. This process involves:

Project EPS

Compute Stable EPS

Compute P/E Ratio using formula

P/E = (1-g/r)/(k-g)

g – growth in EPS or Net Income

r – rate of return earned on equity

k – cost of equity capital

Related Formula for terminal value with NOPLAT (EBITAT)

(1-g/ROIC)/(WACC – g)

The formula demonstrates where value really comes from

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 62/136

Integrated Financial Management Oct 24, 200862

Liquidity and Solvency

Liquidity

Ability to meet short-term obligations Focus:

• Current Financialconditions

• Current cash flows

•Liquidity of assets

Solvency

Ability to meet long-termobligations

Focus:

• Long-term financialconditions

• Long-term cash flows

• Extended profitability

Credit worthiness: Ability to honor credit obligations

(downside risk)

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 63/136

Integrated Financial Management Oct 24, 200863

Solvency Ratios

• Ratios are the center of traditional credit analysis that assesses whether acompany can re-pay loans. These ratios should be compared to benchmarks.

Solvency

Debt Payback Ratios

Funds from Operations to Total Debt

Debt to EBITDA

Leverage Ratios

Debt to Capital (Include Short-term Debt)

Market Debt to Market Capital

Payment Ratios

Interest Coverage

Debt Service Coverage [Cash Flow/(Interest + Principal)]

Capital Investment Coverage

Operating Cash Flow/Capital Expenditures

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 64/136

Integrated Financial Management Oct 24, 200864

Liquidity

• Current Ratio

Current Assets to Current Liabilities

Current Assets less Inventory to Current Liabilities

• Model Working Capital

Current Assets less Cash and Temporary Securities minus Current liabilitiesless Short-term Debt

• Liquidity Assessment

Debt Profile (Maturities)

Bank Lines (Availability, amount, maturity, covenants, triggers)

Off Balance Sheet Obligations (Guarantees, support, take-or-pay contracts,contingent liabilities)

Alternative Sources of Liquidity (Asset sales, dividend flexibility, capitalspending flexibility)

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 65/136

Integrated Financial Management Oct 24, 200865

Financial Ratios in Credit Analysis

• Analyze financial ratios after determining the riskiness of a company.

• There are hundreds of ratios that could be analyzed, only certain key

ratios need to be analyzed to complete an effective assessment.

• Four ways to assess ratios:

Absolute Levels

Trends in historic ratios

Forecast ratios

Comparison with industry peers

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 66/136

Integrated Financial Management Oct 24, 200866

• Measure how many times the company’s earned income covers interestcharges, etc .

Used to determine the probability of default

A coverage ratio of 1 indicates that income just covers interest

Can be calculated either before- or after-tax

Consistency is important

• Analysts also consider the stability and trend of earnings

Interest and Debt Service Coverage Ratios

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 67/136

Integrated Financial Management Oct 24, 200867

S&P Benchmarks

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 68/136

Integrated Financial Management Oct 24, 200868

S&P Benchmark for Manufacturing and Service Companies –

Funds from Operations/Total Debt

• The benchmark ratios differ according to the risk profile of a company asillustrated on the chart below.

35%25%Well Below Average

45%35%25%Below Average

55%40%30%15% Average

60%50%40%25%20% Above Average

70%60%50%40%30%Well Above

Average

BBBBB A AA AAACompany BusinessRisk Profile

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 69/136

Integrated Financial Management Oct 24, 200869

S&P Benchmarks

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 70/136

Integrated Financial Management Oct 24, 200870

S&P Utility Benchmarks

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 71/136

Integrated Financial Management Oct 24, 200871

S&P Benchmarks

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 72/136

Integrated Financial Management Oct 24, 200872

S&P Ratio Definitions

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 73/136

Integrated Financial Management Oct 24, 200873

Objective of Analysis is Bankruptcy Probability

• Credit agencies use the ratios that differ by industry in establishing rating criteria

• Criteria can often be determined by industry

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 74/136

Integrated Financial Management Oct 24, 200874

Bond Ratings and Yield Spread

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 75/136

Integrated Financial Management Oct 24, 200875

Don’t Put Miscellaneous Un-Explained Factors

• Test

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 76/136

Integrated Financial Management Oct 24, 200876

Class 4: Model Assessment

• Various ratios that some use to assess management performance are mostappropriate for testing the validity of a model. Examples of these ratios include:

EBITDA/Revenue

Working Capital – Activity Ratios

Inventory Turnover

AR/Revenues;

AP/Expenses

Income Tax Payable/Income Taxes

Depreciation Rate – Depreciation Expense/Gross PP&L

Depreciation Expense to Cap Exp

Average Interest Rate – Interest Expense/Average Debt

Capital Expenditure/Capacity

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 77/136

Integrated Financial Management Oct 24, 200877

Other Ratios in Financial Modeling

• Other ratios should be computed in financial models to test the validity of assumptions and the structure of the model. For these ratios, the historic levels

can be used to make forecasts of relevant assumptions.

• Examples include average interest rate, depreciation rate, working capital ratios,

dividend payout ratio, EBITDA/Sales

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 78/136

Integrated Financial Management Oct 24, 200878

Financial Ratio Assignment - Work with the

PE Ratio

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 79/136

Integrated Financial Management Oct 24, 200879

PE Ratio Exercise

• Find the file named P/E Ratio exercise

• Complete the cork screw for determining the equity balance

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 80/136

Integrated Financial Management Oct 24, 200880

Steps in the PE Ratio Exercise – Open the File

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 81/136

Integrated Financial Management Oct 24, 200881

Step 1: Enter Switch Variables for the Holding Period

• Use true, false switches to establish the holding period and the terminalperiod

• Do not use if statement

• Rather,

= year <= final_year for the holding period

= year = final_year for the terminal period

• When you multiply variables by the true or false, the then the numbers

are zero or one

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 82/136

Integrated Financial Management Oct 24, 200882

Step 2: Compute the Equity Balance, Net Income and

Dividends with a Cork Screw

• Start with the beginning equity balance

Income = ROE x Beginning balance

Dividends = Income x Payout Ratio

Ending Balance = Beginning Balance + Income – Dividends

• In subsequent periods

Beginning balance = Prior Period Ending Balance

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 83/136

Integrated Financial Management Oct 24, 200883

Step 3: Compute Cash Flow in Holding Period and in Terminal

Period

• In the holding period

Cash flow = dividends

• In the terminal period

Cash flow = dividends + Multiple x earnings per share

Where

Multiple = P/E Ratio from formula (1-g/r)/(k-g)

• Use switch to make sure cash flow is not counted after the holding period

Cash Flow = dividends x switch

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 84/136

Integrated Financial Management Oct 24, 200884

Step 4: Compute the Value of Cash Flow

• Assume the discount rate is the hurdle rate

• Each year the discount factor is

1/(1+r)^year

• The value of cash flow is:

Discount factor x cash flow

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 85/136

Integrated Financial Management Oct 24, 200885

Step 5: Compute the P/E Ratio

• Compute the total value of the share

Value = ∑ cash flow x discount factor

• Fill in Components

P/E = Value/First Year Earnings

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 86/136

Integrated Financial Management Oct 24, 200886

Experiment with P/E Ratio Using Microsoft Data

• Assume ROE = 17%

Cost of Equity = 17%

Payout Ratio = 50%

What is the P/E

Why

• Assume

ROE = 17%

Cost of Equity = 12%

Payout Ratio = 100%

What is the P/E

Why

E i t ith P/E R ti

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 87/136

Integrated Financial Management Oct 24, 200887

Experiment with P/E Ratio

• Assume

ROE = 17%

Cost of Equity = 12%

Dividend Payout = 50%

What is the P/E

Why

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 88/136

Integrated Financial Management Oct 24, 200888

Reference: Financial Ratio Formulas to

Assess Management Performance

I t d ti T C t f T d

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 89/136

Integrated Financial Management Oct 24, 200889

Introduction: Two Components of Trade

The heart of any financial analysis is measurement of value throughassessing risk and return. The primary subject in financial statement

analysis is how can we read financial statements and evaluate the return of

a company relative to the risk of a company.

As the growth of trade transformed the principles of gambling into the

creation of wealth, the inevitable result was capitalism, the epitome of risk-taking. But capitalism could not have flourished without two new activities …

The first was bookkeeping , a humble activity but one that encouraged the

dissemination of the new techniques of numbering and counting.

The other was forecasting , a much less humble and far more challenging

activity that links risk taking with direct payoffs.

“The Remarkable Story of Risk”

C St d f Fi i l St t t A l i

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 90/136

Integrated Financial Management Oct 24, 200890

Case Study of Financial Statement Analysis

• Examples of Financial Statement Review

You receive financial projections as part of an offeringmemorandum or as part of a financing proposal. How would youdetermine whether the projections are reasonable by comparing theprojections to history.

You are assigned to perform a valuation of a company. You mustassess whether the earnings guidance from investment analysts arereasonable.

You are structuring an M&A transaction. You must determine theamount of debt and equity that can be used in the transaction.

P fit bilit A l i

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 91/136

Integrated Financial Management Oct 24, 200891

Profitability Analysis

• ROE = Net Income/ Avg. Common Equity

• ROA = EBIT/ Total Assets

• ROIC = EBIT x (1-t)/ (Avg. Total Debt + Avg. Total Equity)

• Market Value per Share/Book Value per Share

• Market Value of Assets/Replacement Cost of Assets

• Gross Profit Margin = Gross Profit/ Sales

• Operating Margin = EBITDA/Sales

• Profit Margin = Net Income/ Sales

R t E it

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 92/136

Integrated Financial Management Oct 24, 200892

Return on Equity

•Defines how much income management has made from the equity investment made byinvestors – the return is net income and the investment is the equity.

•Formula:

Net Income/(Beginning + Ending Equity)/2

Net Income after Preferred Dividends/(Average Common Equity)

•The problem with ROE it that it mixes operating performance with financial structure, making

it difficult to understand the underlying performance.

•Return on equity should be related to the risk associated with earnings -- volatile earningsshould imply a higher average return on equity

•High or low return on equity in models

High returns – check your assumptions

Low returns – problems with management performance

Return on Assets

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 93/136

Integrated Financial Management Oct 24, 200893

• Return in assets measures the amounts of income produced relative toinvestment in assets. The ratio is generally pre-tax and total assets candistort the ratio.

• Formula:

• EBIT/Average Total Assets

• Problems:

Difference between capital and asset balance means thatinvestment not measured (examples, deferred taxes, deferredcredits).

Pre-tax means that taxes not considered even though taxes arereal.

Financing by current liabilities not considered (for example ROA isthe same for businesses that have different funding from suppliers)

Return on Assets

Formula for Return on Invested Capital

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 94/136

Integrated Financial Management Oct 24, 200894

•The return in invested capital formula can be for a division or an entire corporation. It is after tax and after

depreciation. Cash balances should be excluded from the denominator and interest income from the numerator.Goodwill and goodwill amortization should be excluded.

•Formula:

ROIC = EBITAT/Invested Capital

Where:

EBITAT: Earnings before Interest Taxes and Goodwill Amortization less taxes on EBITAT

Taxes on EBITAT: Cash Income Taxes Less Tax on Interest Expense and Interest Incomeand Tax on Non-operating Income

Invested Capital less cash balance

• Adjustments

Other Assets

Cash Balances

Goodwill

Other

Formula for Return on Invested Capital

ROIC and Economic Profit

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 95/136

Integrated Financial Management Oct 24, 200895

ROIC and Economic Profit

• ROIC is the foundation for analyzing performance in EVA. If a division or company, then it should be earning economic profit. Alternative measures can beused to measure economic profit:

• Economic Profit Formula:

Economic profit = Invested Capital x (ROIC - WACC)

Economic profit = EBITAT - Capital Charge

Economic profit = EBITAT - WACC x Invested Capital

Market to Book Value

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 96/136

Integrated Financial Management Oct 24, 200896

•Management performance can be evaluated by measuring what equity investors think about

the value of the company. Today’s market value compared to the amount invested byshareholders (directly or indirectly through not retaining earnings) is measured by the market tobook ratio. The ratio measures how much value management has created relative to the amountinitially invested. If the ratio is 1.0, management has not created value, if it is 2.0, managementhas doubled value relative to the amount invested.

•The ratio is related to ROE because if the ROE is greater than the cost of capital, the marketvalue should be above the book value.

•Formula:

Market Price/Book Value per Share

•Problems:

Investment does not inflate

Incorporates benefits or costs of equity value from changes in the liability structure of the company.

Market to Book Value

Example of Market to Book Ratio

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 97/136

Integrated Financial Management Oct 24, 200897

Example of Market to Book Ratio

Market Value to Replacement Cost (Tobin’s Q)

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 98/136

Integrated Financial Management Oct 24, 200898

•Theoretical problems with the market to book ratio are addressed with a ratioknown as Tobin’s Q. This ratio compares market value to replacement cost rather than book value. If replacement cost is lower than market value, then shareholdersare better off by liquidating the company and selling assets in the market. The morethe value is above replacement cost, the better job management is doing in managingassets:

•Formula

Tobin’s Q = Enterprise Value/Replacement CostWhere

Enterprise Value = Market Value of Equity plus market value of Debt

•Problems

How to measure replacement cost

Adjusting replacement cost for asset age

Market Value to Replacement Cost (Tobin s Q)

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 99/136

Integrated Financial Management Oct 24, 200899

Reference: Formulas for Valuation Ratios

Enterprise Value Equity Value and Equity Value per Share

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 100/136

Integrated Financial Management Oct 24, 2008100

Enterprise Value, Equity Value and Equity Value per Share

• Before discussing valuation ratios it is helpful to define market capitalization and enterprise

value.

• Formulas:

Market Capitalization = Share Price x Number of Outstanding Shares (fully diluted)

Enterprise value = Market Capitalization plus Market Value of Debt

• In theory, enterprise value is the present value of free cash flow plus the present value of residual.

• In practice, the value of debt can often be estimated by the book value as long as theaverage interest rate is similar to the market yields on the company debt.

P/E Ratio

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 101/136

Integrated Financial Management Oct 24, 2008101

• The P/E Ratio is the most prominent valuation ratio. It is affected by estimatedearnings growth, the ability of a company to earn economic profits and the growthin profitable operations.

• Formula:

Share Price/Earnings per Share

• Issues

Trailing Twelve Months and Forward Twelve Months

Formula: (1-r/g)/(k-g)

• Problems

Affected by earnings adjustments

Causes too much focus on EPS

Distortions created by financing

P/E Ratio

Enterprise Value/EBITDA

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 102/136

Integrated Financial Management Oct 24, 2008102

Enterprise Value/EBITDA

• Some of the problems with the P/E ratio are rectified by the ratio of EV/EBITDA. This ratio is not affected by leverage, accounting

adjustments and can more effective comparisons across companies can

be made. EBITDA - Pre-tax, pre depreciation operating income is a

proxy for cash flow, so market value is compared to cash flow:

•Formula:EV/EBITDA = Enterprise Value/EBITDA

Where

Enterprise Value = Book value of debt plus market value of equity

Price to Cash Flow

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 103/136

Integrated Financial Management Oct 24, 2008103

Price to Cash Flow

• To correct the P/E ratio for accounting adjustments that are non-cashsuch as depreciation and goodwill amortization, a ratio known as Price to

cash flow is computed. This is similar to the P/E ratio except the

denominator is cash flow rather than earnings.

• Cash Flow measure is very simple and not generally the free cash flow

• Cash Flow is generally the net income plus depreciation

Price to Earnings Growth (PEG)

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 104/136

Integrated Financial Management Oct 24, 2008104

Price to Earnings Growth (PEG)

• Due to the importance of earnings growth in the P/E ratio, this ratio attempts tomeasure the relative value of a company after accounting for earnings growth. If a company has higher earnings growth, its price should be higher. Therefore, thevaluation of two companies can be compared even if they have different earningsgrowth.

• Formula:

PEG = PE Ratio/Consensus Earnings Growth

Internal Rate of Return

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 105/136

Integrated Financial Management Oct 24, 2008105

Internal Rate of Return

• Application to project finance rather than investment analysis

• Equity IRR analogous to the ROE

• Project IRR analogous to the ROIC

• Free cash flow used for project IRR

• Equity cash flow used for equity IRR

• Return on Equity Cash Flow in Gaza Strip Project

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 106/136

Integrated Financial Management Oct 24, 2008106

Reference: Financial Ratio Formulas for

Credit Analysis

Ratio Analysis

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 107/136

Integrated Financial Management Oct 24, 2008107

Ratio Analysis

• Activity Analysis

Inventory Turnover = COGS/Avg. Inventory

Avg. Days in Stock = 365/ Inventory TO

Receivables Turnover = Sales/ Avg. Receivables

Avg. Days Receivables Out = 365/ Receivables

Working Capital Turnover = Sales/ Avg. Working Cap

Total Asset Turnover = Sales/ Average Total Assets

•Liquidity Analysis

Operating Cycle = Avg. Days in Stock +

Avg. Days Receivables OutCash Cycle will be less, depending on use of credit

Current Ratio = CA/CL

Quick Ratio = (CA - Inventories)/ CL

CFO Ratio = CFO/ CL

•Solvency Analysis

Debt-to-Cap = Total Debt/Total Capital

Debt to Equity = Total Debt/ Total Equity

(market values are preferable in this ratio)Times Interest Earned = EBIT/ Interest Expense

Fixed Charge Coverage = EBIT (and before other fixed expenses)/Fixed Charges

Cap Ex Ratio = CFO/ Cap Ex

Credit Analysis Ratios

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 108/136

Integrated Financial Management Oct 24, 2008108

y

• A traditional use of financial ratios has been to assess the value of debtand the chance of default. Liquidity ratios measure the ability of a

company to meet short-term obligations while interest coverage, debt

service and capitalization ratios measure the ability to meet long-term

obligations.

• Credit ratios have been formalized into regression analysis by relating the

defaults on companies to various financial ratios. (Note that credit ratios

are not considered adequate for many assessments, but they are a

starting point.)

Classes of Credit Ratios

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 109/136

Integrated Financial Management Oct 24, 2008109

• Interest Coverage

EBIT/Interest

Debt Service Coverage Ratio

After tax coverage

• Debt to Capital

Total debt to capital

Debt to equity

Long term versus short term

Market value versus book value

• Debt to Cash Flow

• Liquidity

Current Ratio

Quick Ratio

Interest and Debt Service Coverage

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 110/136

Integrated Financial Management Oct 24, 2008110

g

• The interest coverage and debt service ratios measure the amount of buffer or comfort above interest expense and/or debt service that cash

flow provides before obligations cannot be met from current operations.

EBIT/Interest is used more than the debt service coverage in corporate

modeling because of the lumpiness in cash flow that occurs from bullet

maturities:

• Formula:

EBIT/Interest = EBIT/(Long + Short term Interest)

DSCR = (Operating Cash + Interest)/(Interest + Maturities)

Debt to Capital Ratio

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 111/136

Integrated Financial Management Oct 24, 2008111

p

• The debt to capital ratio measures from a book perspective, the amountof debt that is financing assets. The ratio has not been a very good

predictor of bankruptcy. It should include long and short term debt as

well as capitalized lease payments. In some cases, the capitalized value

of contracts has been included.

• Formula:

Debt to Capital = (Long-term debt + Short-term debt)/(Long andShort term debt + Equity)

Debt to Cash Flow

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 112/136

Integrated Financial Management Oct 24, 2008112

• This ratio compares the cash flow with the amount of debt. The less cashflow relative to debt, the worse the credit and the higher the probability of

default. Inquisitively, the ratio can be considered the number of years of

cash flow it takes to pay-off all of the debt.

• Formula:

Debt/Cash Flow = (Long and Short term debt)/EBITDA

• Note that EBITDA is an approximation of cash flow and it does not

include capital expenditures.

Liquidity Ratios

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 113/136

Integrated Financial Management Oct 24, 2008113

•Liquidity ratios measure the ability of a company to meet obligations thatare coming due in the short-term. Liquidity ratios are relevant for suppliersand contractors. A ratio below 1.0 suggests that more is coming due then ison hand to pay the liabilities. The quick ratio excludes inventories becausethey are not liquid.

•Formulas:

•Current Ratio

Current Assets/Current Liabilities

•Quick Ratio

Current Assets – Inventory/Current Liabilities

(Cash + Marketable Securities + A/R)/Current Liabilities

q y

Activity Ratios

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 114/136

Integrated Financial Management Oct 24, 2008114

• Inventory turnover CGS/Average Inventory

Days Inventory in Stock = 365/Inventory Turnover

Receivables Turnover = Sales/AR

Days Receivables Outstanding = 365/Receivables Turnover

Depreciation Rate

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 115/136

Integrated Financial Management Oct 24, 2008115

• In simple models, forecasts of depreciation expense can be made by applying the

depreciation rate to gross plant property and equipment.

• Depreciation Rate

Formula:

Depreciation Rate = Depreciation Expense/Gross Plant

Depreciation Expense divided by average gross plant balance

One divided by depreciation rate gives you the average life of plant

• Accumulated Depreciation/Plant Balance

Indication of average age of the plant

Higher depreciation is older average age of the plant

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 116/136

Integrated Financial Management Oct 24, 2008116

Financial Ratio Formulas for Model

Assessment

EBITDA Margin

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 117/136

Integrated Financial Management Oct 24, 2008117

• As explained above, the EBITDA margin can be a good ratio todetermine if assumptions are reasonable:

Relationship between revenues and operating expenses

Compare forecast to history and evaluate why changes are occurring

Average Interest Rate

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 118/136

Integrated Financial Management Oct 24, 2008118

• The average interest rate is the interest expense divided by the average debt

balance. This can be used to assess whether the project interest rate is

reasonable – particularly for long-term debt.

Average interest rate is the interest expense divided by the average debtbalance

The average interest rate can be compared to prevailing interest rates

Capital Intensity

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 119/136

Integrated Financial Management Oct 24, 2008119

• Capital intensity is often discussed in finance. The capital intensity does not affect

value or credit, but it is helpful in background on the business.

• Formula:

Capital Intensity = Capitalization/Revenues

• Driven by

Life of Asset Capital Cost Relative to Operating Cost

Required Return on Assets

Financial Ratio Output in Corporate Models

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 120/136

Integrated Financial Management Oct 24, 2008120

•Use financial ratios to test the validity of models (can the industry reallysustain high profits)

• Use financial ratios to develop valuation from earnings multiples (P/E and

EBIDA/Enterprise Value)

• Use financial ratios in residual value calculations

Examples of Financial Ratio Analysis in Corporate Model

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 121/136

Integrated Financial Management Oct 24, 2008121

Examples of Financial Ratio Analysis in Corporate Model

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 122/136

Integrated Financial Management Oct 24, 2008122

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 123/136

Integrated Financial Management Oct 24, 2008123

Financial Ratios and Ability to Earn

Economic Profit

The Economics of Value Creation and Strategic Planning

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 124/136

Integrated Financial Management Oct 24, 2008124

In this section we review how value is created by business activity including how

valuation relates to economic profit. The section covers the basic economic drivers of value in different circumstances and the actual value creation activities of variousfirms.

1. Microeconomics and the creation of value

2. Models of strategic choice and value3. Assumption of efficient financial markets

4. Value Drivers, strategy and financial management

Why Does Economic Profit Depend on Barriers to Entry

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 125/136

Integrated Financial Management Oct 24, 2008125

Recall your basic economics course:

Economic profit is the net revenuesearned by a company less all costsincluding opportunity cost(opportunity cost includes the riskadjusted cost of capital).

If companies are earning economicprofit, more firms will enter the

industry. If companies are notmaking economic profit, firms willexit the industry. Therefore, tosustain economic profit (asustainable competitive advantage),firms must be able to keep upbarriers to entry.

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 126/136

Examples of Economic Profit that Could not be Sustained

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 127/136

Integrated Financial Management Oct 24, 2008127

• Internet Companies

The internet bubble occurred because companies had “business models” thatsuggested high growth. But in order to really make profit, there had to bebarriers to entry. In the industry, the business models were easy to copy andeconomic profit was very hard to realize.

• Enron

Enron’s business plan was to make money from being a player in commoditymarkets where there is a zero sum game. It is difficult to realize long termsignificant economic profit by making trades where there is an equal number of winners and losers.

Examples of Economic Profit that Could not be Sustained

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 128/136

Integrated Financial Management Oct 24, 2008128

• Investments in Electricity Generation

After price spikes in electricity, many firms such as Calpine and Natural Gascompanies made significant investments in electricity generation. Theinvestments caused prices to decline and only early entrants made money.

• AT&T and NCR

The merger between AT&T and NCR did not contemplate achieving cost

savings from the merger. Without cost savings or revenue enhancements,the merger could not add value and it turned out to be a disaster.

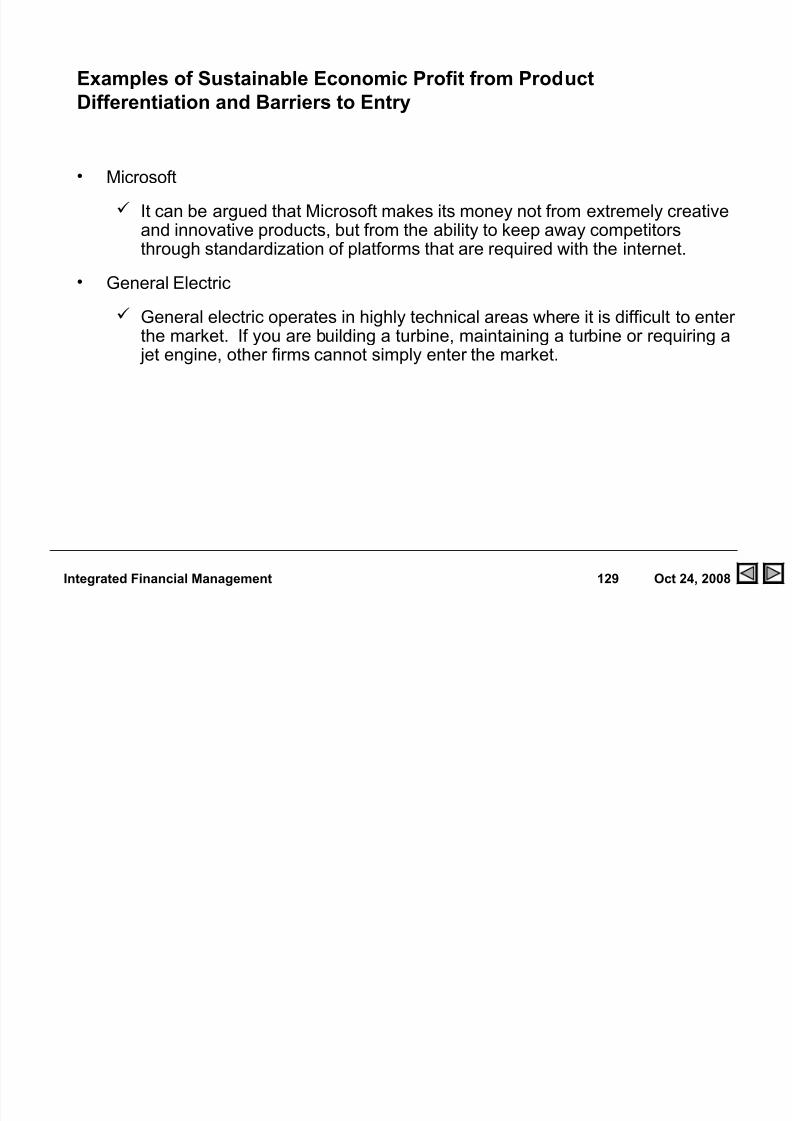

Examples of Sustainable Economic Profit from Product

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 129/136

Integrated Financial Management Oct 24, 2008129

Differentiation and Barriers to Entry

• Microsoft

It can be argued that Microsoft makes its money not from extremely creativeand innovative products, but from the ability to keep away competitorsthrough standardization of platforms that are required with the internet.

• General Electric

General electric operates in highly technical areas where it is difficult to enter the market. If you are building a turbine, maintaining a turbine or requiring a jet engine, other firms cannot simply enter the market.

Example of Economic Profit from an Efficient Cost Structure

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 130/136

Integrated Financial Management Oct 24, 2008130

• Southwest Airlines versus United Airlines

Southwest Airlines has the same type of planes, motivates its employees, hasextremely short layovers, low prices and high load factors. United Airlineshas union problems, higher prices and lower load factors.

• Freeport McMoran

Freeport developed a copper mine in a remote part of Indonesia where theore grade was high and the copper could be mined from the surface.

Barriers to Entry

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 131/136

Integrated Financial Management Oct 24, 2008131

In thinking about barriers to entry, the types of business activities that lead to

barriers can be complex:

In classic economic theory, capital intensive industries such as steel firmsand automobile firms were thought to have market power from barriers toentry. However, excess capacity can exist in the capital intensive businesses

and size alone has not turned out to be an effective barrier.

More interesting barriers to entry are from a strong name – in theadvertising and financial services business, a highly skilled work force infinancial services and software, standardization of computer platforms andeven barrier to entry from high stock prices.

Planning

Financial Statements and Reflection of Business Activities

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 132/136

Integrated Financial Management Oct 24, 2008132

PlanningInvesting

Current:q Cashq Accounts Receivableq Inventoriesq Marketable Securities

Noncurrent:

q Land, Buildings, &Equipment

q Patentsq Investments

Assets

Balance Sheet

FinancingCurrent:q Notes Payableq Accounts Payableq Salaries Payableq Income Tax Payable

Noncurrent:q

Bonds Payableq Common Stockq Retained Earnings

Liabilities & Equity

Balance Sheet

Statement of

Shareholders’ Equity

Operating

q Salesq Cost of Goods Soldq Selling Expenseq Administrative Expenseq Interest Expense

q Income Tax Expense

Net Income

Income statement

Cash Flow

Statement of

Cash Flows

Traditional Financial Ratio Analysis – Comparative Trend

Analysis

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 133/136

Integrated Financial Management Oct 24, 2008133

Analysis

• Purpose of trend analysis:

Evaluation of consecutive financial statements

• Output of trend analysis:

Determine the direction, speed, and extent of any trends to evaluatewhether the trends will continue

• Types of trend analysis:

Year-to-year Change Analysis

(Ln(revenue(t)/revenue(t-1))

(revenue(t)/revenue(t-1)-1)

Index-Number Trend Analysis

Prior x (1+growth)

Accounting Analysis in Financial Statements

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 134/136

Integrated Financial Management Oct 24, 2008134

Comparability problems — across firms and across time

Manager estimation error

Distortion problems Earnings management

Distortion of business

Accounting

Risk

Process to evaluate and adjust financialstatements to better reflect economic reality

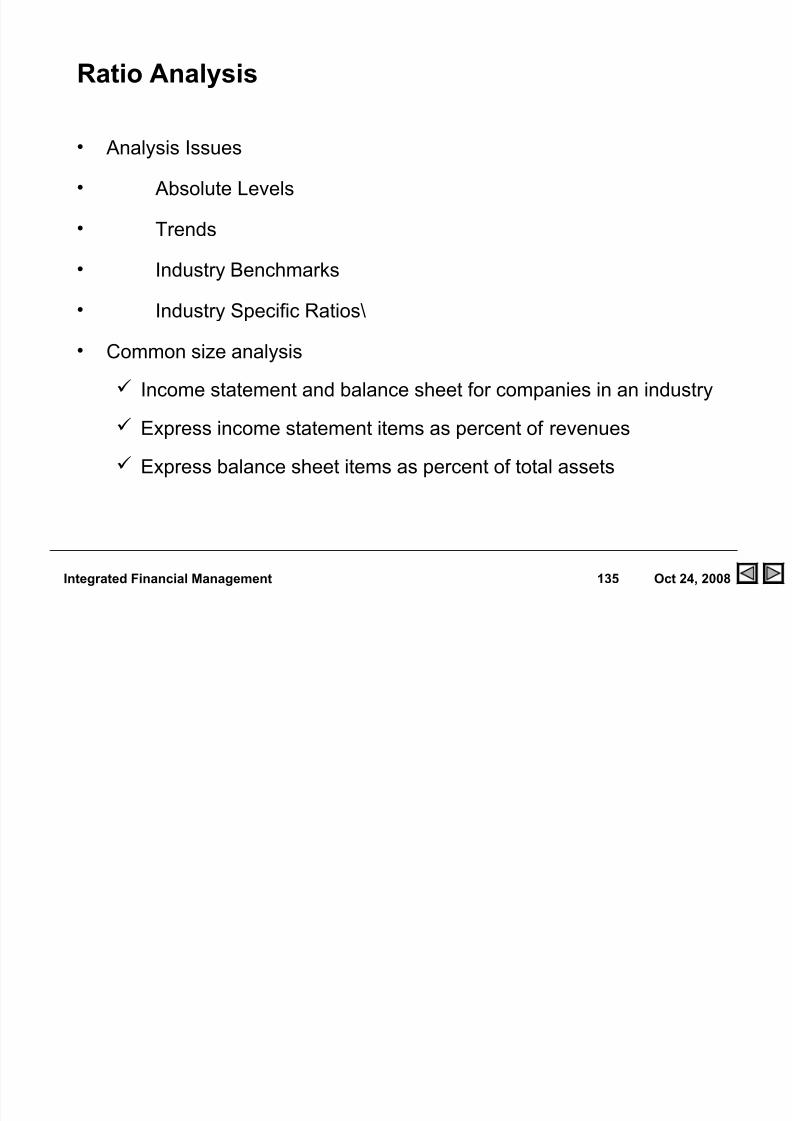

Ratio Analysis

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 135/136

Integrated Financial Management Oct 24, 2008135

• Analysis Issues

• Absolute Levels

• Trends

• Industry Benchmarks

• Industry Specific Ratios\

• Common size analysis

Income statement and balance sheet for companies in an industry

Express income statement items as percent of revenues

Express balance sheet items as percent of total assets

Example of P/E and PEG

7/29/2019 7355347 Valuation Ratios

http://slidepdf.com/reader/full/7355347-valuation-ratios 136/136