731 substance

TRANSCRIPT

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 1/20

ExPedite Note ACCA F7 Financial Reporti

Page |2.1 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.com

Chapter 2

IAS 1: Presentation of Financial

Statements

STARTThe Big Picture

IAS 1 is a cornerstone accounting standard that includes:

x Components of financial statements

x Core concepts

x True and fair override.

It is virtually certain to be tested in the ACCA paper F7 exam.

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 2/20

ExPedite Note ACCA F7 Financial Reporti

Page |2.2 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.com

Components of financial statements

A full set of IFRS financial statements comprises the following primary statements (ie

statements that must be shown with equal prominence as each other):

x Statement of financial position (previously called balance sheet)

x Statement of comprehensive income (comprising profit and loss statement and

statement of other comprehensive income)

x Statement of changes in equity

x Statement of cash flows

x Comparative data for the previous year for each of the above.

In addition, secondary statements are required being notes that explain the accounting

policies and other significant explanations or useful “drill down” information.

Question 2 of the F7 exam is likely to require presentation of financial statements from a

trial balance with adjustments. A starting point in the exam is to be able to produce a

skeleton set of which financial statements are required from memory. It’s therefore

necessary to memorise the formats on the following pages.

Core concepts

IAS 1 includes a number of core concepts, with some overlap with the Framework

document.

x Fair presentation – fair, neutral description of transactions.

x Going concern – entity assumed to continue trading into the foreseeable future.

x Accruals (matching) basis of accounting – match costs with associated revenues and

items to the time period incurred.

x Consistency of presentation – present similar transactions the same way within the

current year and year by year.

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 3/20

ExPedite Note ACCA F7 Financial Reporti

Page |2.3 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.com

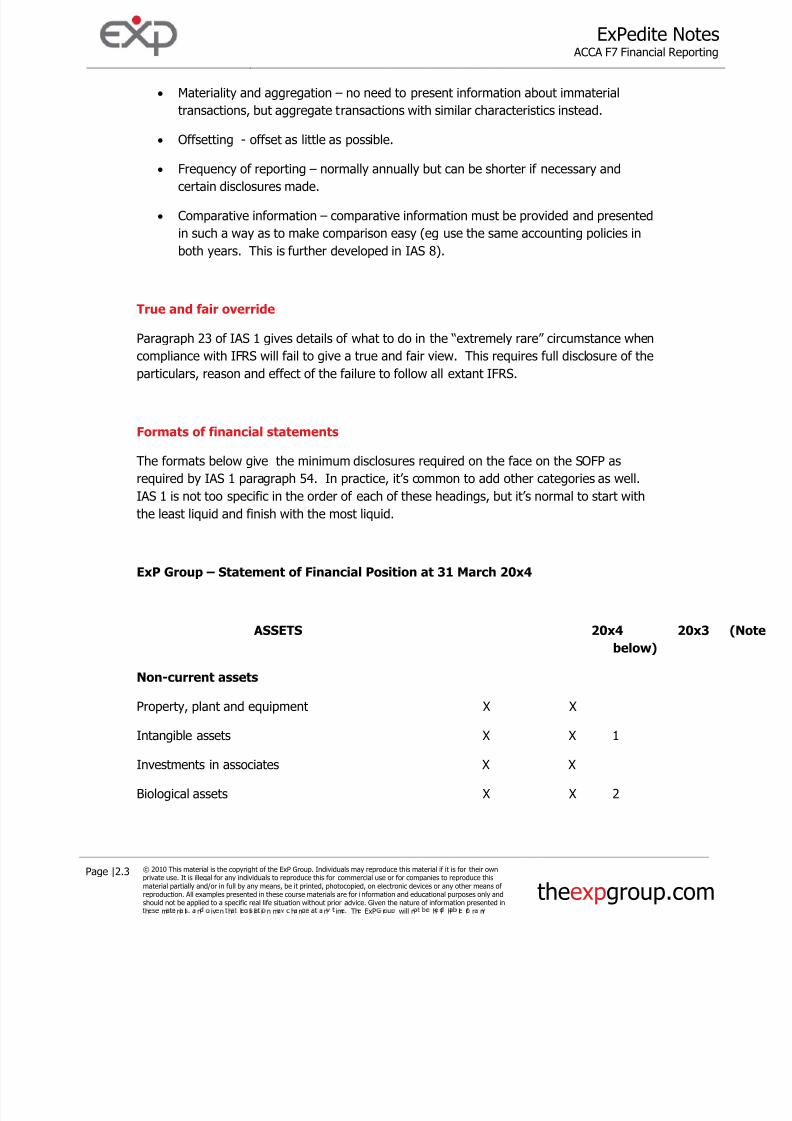

x Materiality and aggregation – no need to present information about immaterial

transactions, but aggregate transactions with similar characteristics instead.

x Offsetting - offset as little as possible.

x Frequency of reporting – normally annually but can be shorter if necessary and

certain disclosures made.

x Comparative information – comparative information must be provided and presented

in such a way as to make comparison easy (eg use the same accounting policies in

both years. This is further developed in IAS 8).

True and fair override

Paragraph 23 of IAS 1 gives details of what to do in the “extremely rare” circumstance when

compliance with IFRS will fail to give a true and fair view. This requires full disclosure of the

particulars, reason and effect of the failure to follow all extant IFRS.

Formats of financial statements

The formats below give the minimum disclosures required on the face on the SOFP as

required by IAS 1 paragraph 54. In practice, it’s common to add other categories as well.

IAS 1 is not too specific in the order of each of these headings, but it’s normal to start with

the least liquid and finish with the most liquid.

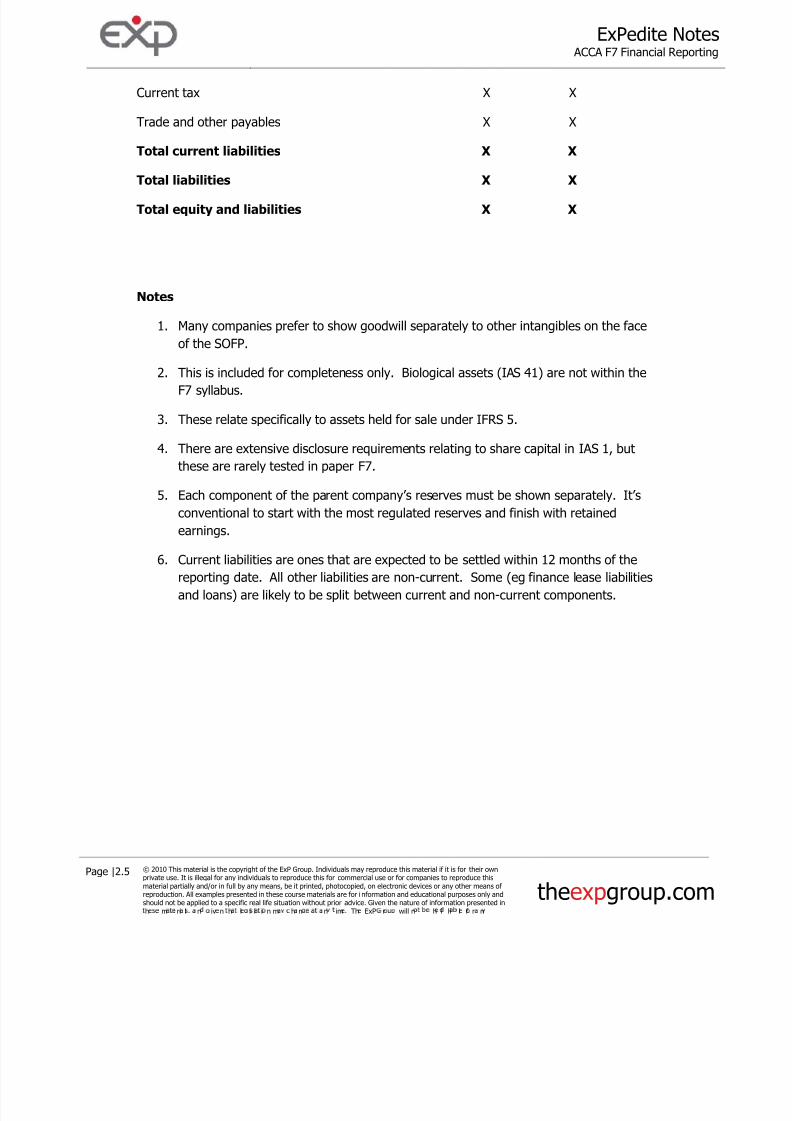

ExP Group – Statement of Financial Position at 31 March 20x4

ASSETS 20x4 20x3

below)

Non-current assets

Property, plant and equipment X X

Intangible assets X X 1

Investments in associates X X

Biological assets X X 2

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 4/20

ExPedite Note ACCA F7 Financial Reporti

Page |2.4 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.com

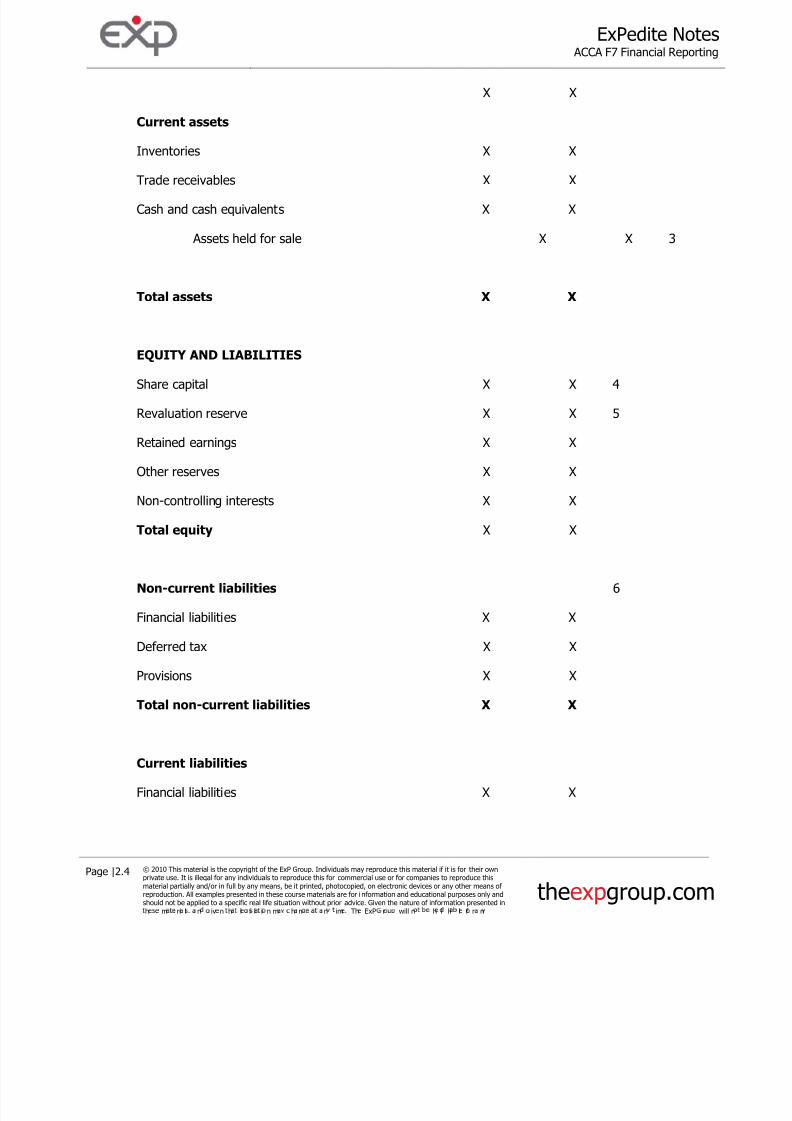

X X

Current assets

Inventories X X

Trade receivables X X

Cash and cash equivalents X X

Assets held for sale X X 3

Total assets X X

EQUITY AND LIABILITIES

Share capital X X 4

Revaluation reserve X X 5

Retained earnings X X

Other reserves X X

Non-controlling interests X X

Total equity X X

Non-current liabilities 6

Financial liabilities X X

Deferred tax X X

Provisions X X

Total non-current liabilities X X

Current liabilities

Financial liabilities X X

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 5/20

ExPedite Note ACCA F7 Financial Reporti

Page |2.5 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.com

Current tax X X

Trade and other payables X X

Total current liabilities X X

Total liabilities X X

Total equity and liabilities X X

Notes

1. Many companies prefer to show goodwill separately to other intangibles on the face

of the SOFP.

2. This is included for completeness only. Biological assets (IAS 41) are not within the

F7 syllabus.

3. These relate specifically to assets held for sale under IFRS 5.

4. There are extensive disclosure requirements relating to share capital in IAS 1, but

these are rarely tested in paper F7.

5. Each component of the parent company’s reserves must be shown separately. It’s

conventional to start with the most regulated reserves and finish with retained

earnings.

6. Current liabilities are ones that are expected to be settled within 12 months of the

reporting date. All other liabilities are non-current. Some (eg finance lease liabilities

and loans) are likely to be split between current and non-current components.

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 6/20

ExPedite Note ACCA F7 Financial Reporti

Page |2.6 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.com

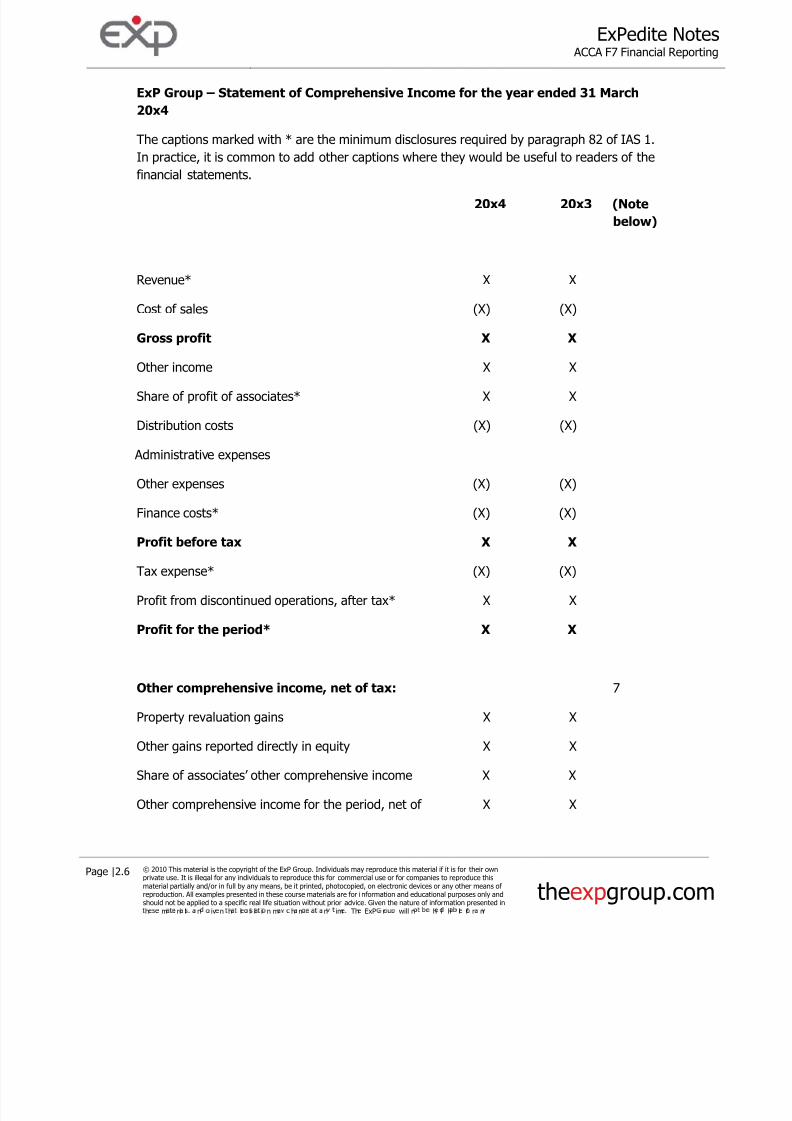

ExP Group – Statement of Comprehensive Income for the year ended 31 March

20x4

The captions marked with * are the minimum disclosures required by paragraph 82 of IAS 1.

In practice, it is common to add other captions where they would be useful to readers of the

financial statements.

20x4 20x3 (Note

below)

Revenue* X X

Cost of sales (X) (X)

Gross profit X X

Other income X X

Share of profit of associates* X X

Distribution costs (X) (X)

Administrative expenses

Other expenses (X) (X)

Finance costs* (X) (X)

Profit before tax X X

Tax expense* (X) (X)

Profit from discontinued operations, after tax* X X

Profit for the period* X X

Other comprehensive income, net of tax: 7

Property revaluation gains X X

Other gains reported directly in equity X X

Share of associates’ other comprehensive income X X

Other comprehensive income for the period, net of X X

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 7/20

ExPedite Note ACCA F7 Financial Reporti

Page |2.7 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.com

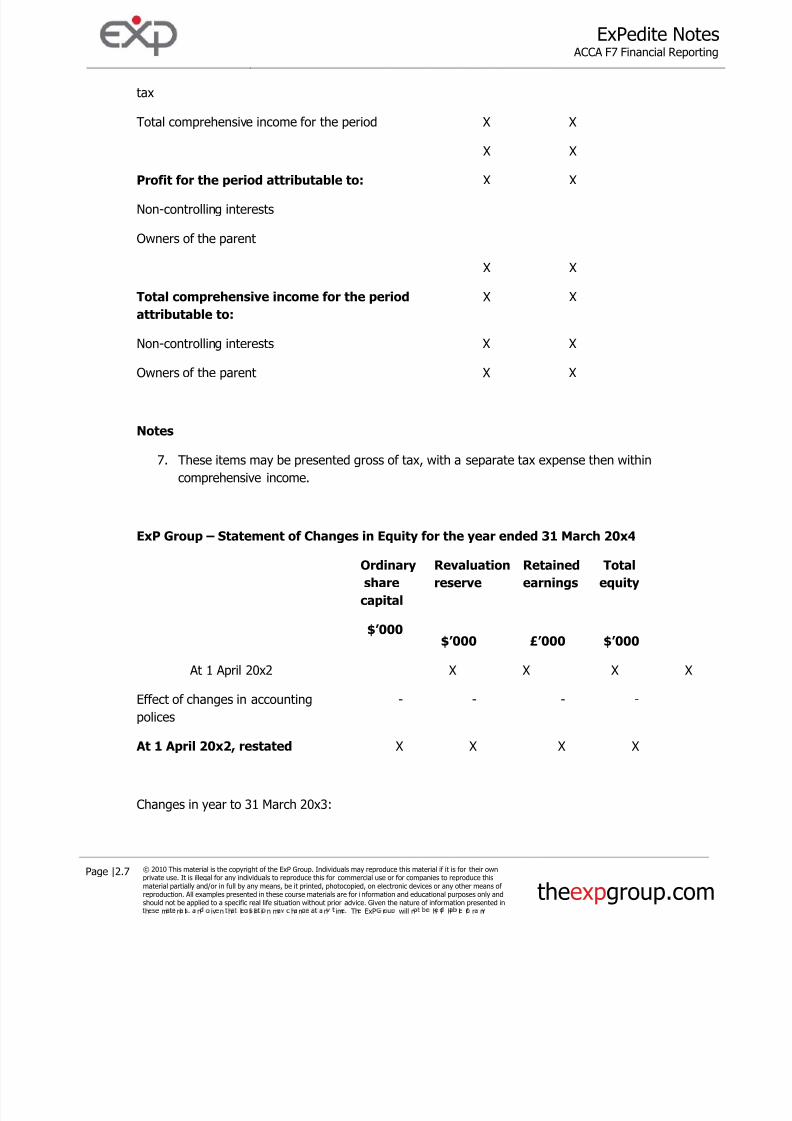

tax

Total comprehensive income for the period X X

X X

Profit for the period attributable to: X X

Non-controlling interests

Owners of the parent

X X

Total comprehensive income for the period

attributable to:

X X

Non-controlling interests X X

Owners of the parent X X

Notes

7. These items may be presented gross of tax, with a separate tax expense then within

comprehensive income.

ExP Group – Statement of Changes in Equity for the year ended 31 March 20x4

Ordinary

share

capital

$’000

Revaluation

reserve

$’000

Retained

earnings

£’000

Total

equity

$’000

At 1 April 20x2 X X X X

Effect of changes in accountingpolices

- - - -

At 1 April 20x2, restated X X X X

Changes in year to 31 March 20x3:

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 8/20

ExPedite Note ACCA F7 Financial Reporti

Page |2.8 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.com

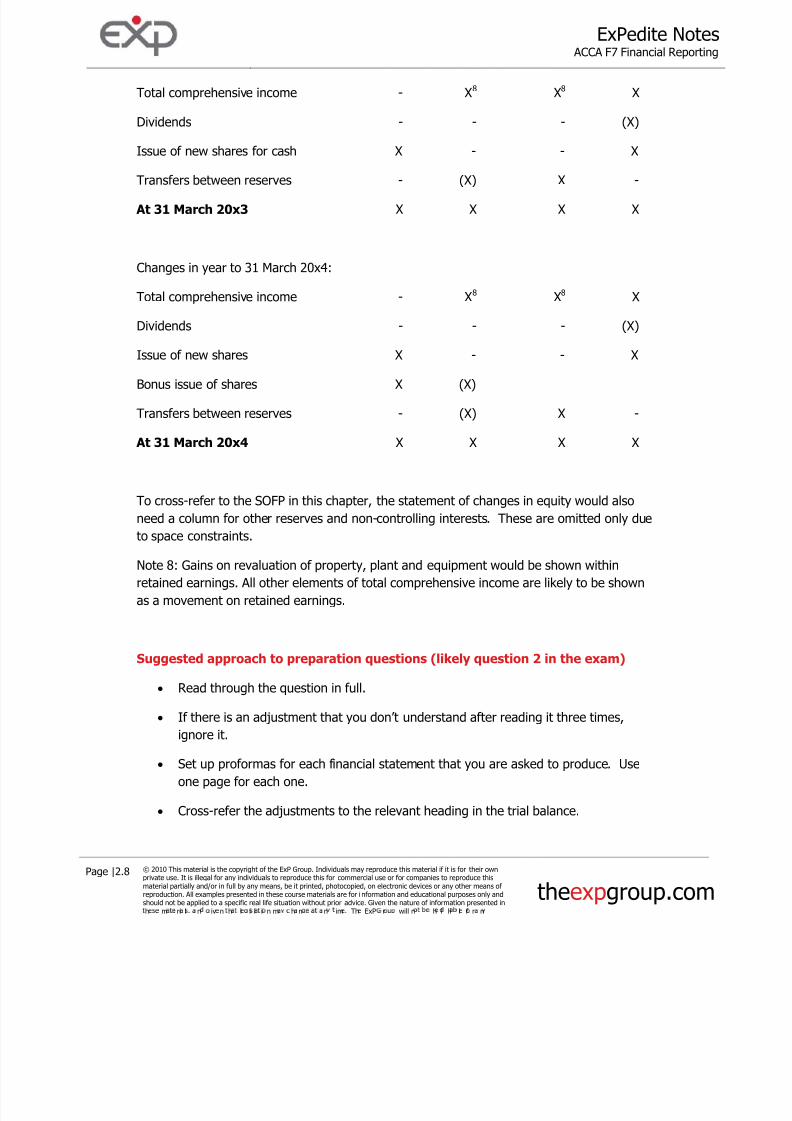

Total comprehensive income - X8 X8 X

Dividends - - - (X)

Issue of new shares for cash X - - X

Transfers between reserves - (X) X -

At 31 March 20x3 X X X X

Changes in year to 31 March 20x4:

Total comprehensive income - X8 X8 X

Dividends - - - (X)

Issue of new shares X - - X

Bonus issue of shares X (X)

Transfers between reserves - (X) X -

At 31 March 20x4 X X X X

To cross-refer to the SOFP in this chapter, the statement of changes in equity would also

need a column for other reserves and non-controlling interests. These are omitted only due

to space constraints.

Note 8: Gains on revaluation of property, plant and equipment would be shown within

retained earnings. All other elements of total comprehensive income are likely to be shown

as a movement on retained earnings.

Suggested approach to preparation questions (likely question 2 in the exam)

x Read through the question in full.

x If there is an adjustment that you don’t understand after reading it three times,

ignore it.

x Set up proformas for each financial statement that you are asked to produce. Use

one page for each one.

x Cross-refer the adjustments to the relevant heading in the trial balance.

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 9/20

ExPedite Note ACCA F7 Financial Reporti

Page |2.9 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.com

x For each item in the trial balance that does not have a cross-reference next to it,

cross it off and lift the relevant figure directly into your proforma answers.

x Work through the adjustments in order of which ones you find the most easy.

Record your adjustments in workings and refer workings to your proforma answer.

x When you run out of time allocated to the question, move on! Do not expect to

finish the question in full.

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 10/20

ExPedite Note ACCA F7 Financial Reporti

Page |2.10 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.com

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 11/20

ExPedite Note ACCA F7 Financial Reporti

Page |3.1 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.co

Chapter 3

Substance and IAS 18 Revenue

STARTThe Big Picture

Substance over Form

The Framework document and IAS 1 both state that for information to be reliable, it must

be reported in accordance with its commercial substance, rather than strictly in adherence

to its legal form.

We have already encountered one example of substance over form in the context of finance

leases, where a reporting entity records assets held under a finance lease in the SOFP,

although it’s not owned by them. In substance, the degree of control means it’s “their”

asset although legally it quite possibly never is.

There are a wide range of transactions where identifying the true commercial substance

may be difficult. The most common types of transactions in the exam are:

x Inventory sold on a sale or return basis (“consignment inventory”)

x Debt factoring

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 12/20

ExPedite Note ACCA F7 Financial Reporti

Page |3.2 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.co

x Loans secured on assets that will be repurchased.

In order to reach a sensible conclusion in any substance over form scenario, it is necessary

to identify:

x What assets are in question?

x What are the intrinsic risks and rewards of holding that asset?

x Which party to the transaction is, on balance, more exposed to the risks and rewards

of that asset?

The asset with the greater exposure to risks and rewards recognises the asset on its SOFP.

If it involves initial recognition of an asset, this often generates recognition of a gain also.

EXAMPLE

Sale or return inventory

Bookworm is a book store. It takes delivery of books from publishers on the condition that

it can return books at any time to the publisher, at the cost of Bookworm. Bookworm does

not charge publishers a fee for displaying their books.

The agreements with publishers are that Bookworm buys the books from the publisher at

the moment when they are sold on to a customer, or when 24 months passes from delivery;

whichever is the sooner. Bookworm has an inventory management system that monitors

which books have been in inventory for a long time and it returns almost all books before

the 24 months expires.

Bookworm’s accounting policy is to recognise all books as purchases at cost at the time of

delivery from the publisher. Any returns to the publishers are then recorded as purchase

returns.

At 30 June 20x4, Bookworm conducts a physical inventory count and determines that it hasinventory at a purchase price of $459,500.

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 13/20

ExPedite Note ACCA F7 Financial Reporti

Page |3.3 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.co

Required

Determine whether Bookworm’s accounting policy complies with IFRS.

Solution to example

Intrinsic risk/ return of

books

Borne mostly by Reason

Obsolescence Publishers Obsolete inventory can be

returned with no penalty.

Theft Bookworm Stolen inventory could not be

returned within 24 months,

so must be purchased by

Bookworm.

Ability to sell at a profit Bookworm Bookworm has physical

custody.

Physical damage, eg fire Bookworm Damaged goods would not

be returnable.

Slow moving inventory Publishers Bookworm can return under-

performing inventory for no

penalty.

Although Bookworm bears most of the identified risks, the biggest risk is obsolescence and

slow moving inventory. The others are risks, but not ones that are likely to cause nearly the

same level of losses as obsolescence.

Consequently, Bookworm should only recognise the purchase of inventory at either the point

of sale to a customer, or passage of 24 months.

This means that the current accounting policy does not comply with IFRS. The inventory

should be derecognised by Bookworm and recognised by the relevant publishers.

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 14/20

ExPedite Note ACCA F7 Financial Reporti

Page |3.4 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.co

Review and self-test 1

Shaky has trade receivables of $1.6 million. It has decided that it will be beneficial to

request a debt factoring company to collect these receivables on its behalf. It has split the

receivables into two groups of $800,000 each and given one block of receivables to Stephen

Co and the other $800,000 to Fry Co. The terms of each agreement are:

Stephen Co: Stephen Co advanced $600,000 to Shaky Co upon legal transfer of the right

to receive the receivable’s payment. Stephen Co will contact receivables and

take legal action where necessary to recover payment. Stephen Co bears all

such costs itself. In the event that receivables never pay, Stephen Co has no

right to recover any of the $600,000 advanced to Shaky, nor is it under any

obligation to pay Shaky any greater amount if all the receivables pay quickly.

Fry Co: Fry Co advanced $700,000 to Shaky Co upon legal transfer of the right to

receive the receivable’s payment. Fry Co will contact receivables and take

legal action where necessary to recover payment. Fry Co charges Shaky Co

an administration fee of 1% of the receivable’s book value for each month

before payment is received. This administration fee is also increased by any

legal costs incurred.

In the event that receivables do not pay Fry Co within six months from the

start of the agreement, Fry Co has a “put” option to sell the receivable’s debt

back to Shaky Co for the original value of the debt.

Required

Analyse each of the above agreements and determine an appropriate treatment, both in

SOFP and SOCI for each transaction.

Review and self-test 2

Pretence Co is a maker of brandy. It sells premium “mature” brandy as its main brand that

is aged for ten years before sale.

At 30 September 20x1, it sold inventory with a work-in-progress value (correctly according

to IAS 2) of $458,000 to a bank. The bank bought the inventory for $458,000 in cash. The

inventory had an average age of two years at the date of sale.

The bank has a put option to sell the brandy back to Pretence at any date before 30

September 20x7 at a price equal to $458,000 plus a mark-up, which is calculated on a

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 15/20

ExPedite Note ACCA F7 Financial Reporti

Page |3.5 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.co

compound basis at EURIBOR + 4% per annum. Pretence has a call option that it can buy

the brandy back at this same price on 30 September 20x7 only.

Pretence has recorded the sale of brandy as revenue and derecognised the inventory from

its SOFP.

Required

Analyse the above transaction and determine whether Pretence’s accounting treatment

complies with IFRS. If not, suggest a better treatment.

IAS 18: Revenue

Revenue recognition is clearly a key issue in preparation of financial statements. The rulesare different depending upon whether a sale is for goods or for services. This means that

the first step in the exam is to identify whether a transaction is for goods or services. If it’s

for a construction contract, follow the rules specifically of IAS 11.

Recognition of revenue: goods

x Recognise revenue when most of the more important inherent risks and rewards of

the goods have passed from the seller to the buyer.

x This might well be earlier or later than when legal title passes or when payment

occurs.

Recognition of revenue: services

x Recognise revenue as the costs of providing the service are incurred. Where a

service is paid for up front, revenue often must be deferred as a liability in the SOFP

until the revenue is earned.

Valuation of revenue

If sales are made with long-term payment terms, recognise the sale and the receivable at its

net present value using an appropriate discount rate. This then shows finance income over

time.

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 16/20

ExPedite Note ACCA F7 Financial Reporti

Page |3.6 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.co

Bundled sales

Where goods are sold with serviced bundled (eg after-sales servicing for two years), then

unbundle into separate components.

EXAMPLE

If a car is sold for $30,000 with three years of free servicing, recognise this as:

$

Total sales value 30,000

Less: Market value of three year servicing agreement

(to be recognised over 3 years) (3,000)

Value of goods sold (recognise immediately) 27,000

Review and self-test 3

FlyHigh Co is an airline. It generally receives bookings for customers’ flights one month

before the flight takes place.

During the year to 31 December 20x7, it received bookings, and simultaneous payment for

flights, of $1.2 million per month. The previous year, it had received bookings and

payments of $800,000 per month. Bookings are not seasonal.

Required

x What would be the opening balance on deferred revenue?

x What would be the closing balance on deferred revenue?

x What revenue would be recognised for the year ended 31 December 20x7?

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 17/20

ExPedite Note ACCA F7 Financial Reporti

Page |3.7 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.co

Solution to review and self-test 1

Applying the model of risk and rewards to Stephen Co

Intrinsic risk/ return of

receivables

Borne

mostly by

Reason

Slow payment Stephen Co Shaky is unaffected by how quickly Stephen

collects the receivables.

Non-payment Stephen Co If receivables do not pay, there is no

adjustment to the amount paid by Stephen

to Shaky to recover the debt.

Creating administration costs

eg by disputing balances in a

petty way

Stephen Co Once the legal transfer of debts is complete,

there is no recourse to Shaky for any

problems in collection of the debt.

An appropriate accounting presentation of the transfer of the debts from Shaky to Stephen

is therefore to derecognise the debts from Shaky’s SOFP and recognise them in Stephen’s

SOFP. Shaky will derecognise an asset of $800,000 in return for cash of $600,000 so

recognise a loss on derecognition of $200,000. This will be presented as a finance cost or

as a distribution cost, depending on Shaky’s accounting policy.

Applying the model of risk and rewards to Fry Co

Intrinsic risk/ return of receivables

Bornemostly by

Reason

Slow payment Shaky Fry has a right to charge an additional cost

to Shaky for the time taken to recover

payment. The slower the payment, the

greater the income of Fry and the greater

the expenses of Shaky.

Non-payment Shaky Fry has a put option to give the non-

recovered debts back to Shaky, including

amounts due for the 1% monthly charge.

Creating administration costs

eg by disputing balances in a

petty way

Shaky Legal costs incurred are passed onto Shaky

by Fry.

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 18/20

ExPedite Note ACCA F7 Financial Reporti

Page |3.8 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.co

An appropriate accounting presentation for this transaction is to continue to recognise the

receivables on the SOFP of Shaky, since Shaky is exposed to the risks and rewards

associated with these receivables. The cash advanced by Fry to Shaky should be presented

as a secured loan and the finance costs charged to Shaky by Fry should be presented as a

cost of collecting debts, however that is classified in the financial statements by the

accounting policy of Shaky.

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 19/20

ExPedite Note ACCA F7 Financial Reporti

Page |3.9 © 2010 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own

private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce thismaterial partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of reproduction. All examples presented in these course materials are for information and educational purposes only andshould not be applied to a specific real life situation without prior advice. Given the nature of information presented inh m ri l n iv n h l i l i n m h n n im Th ExP r will n h l li l f r n

theexpgroup.co

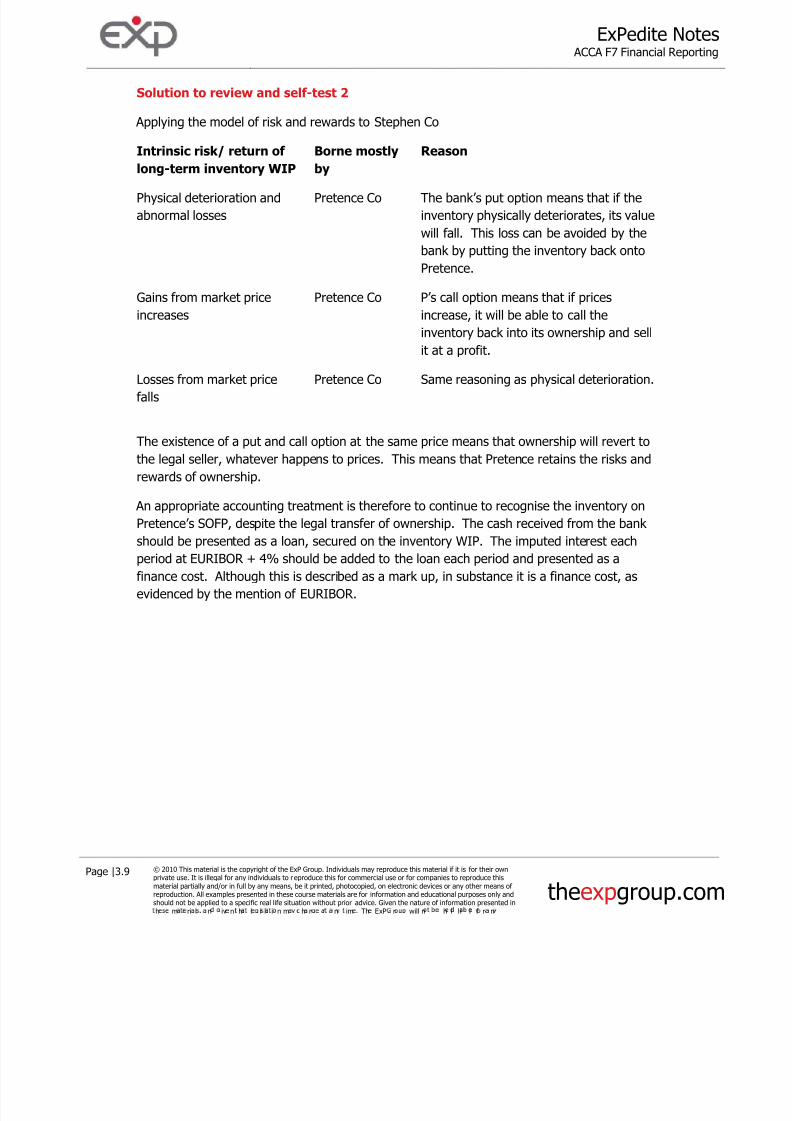

Solution to review and self-test 2

Applying the model of risk and rewards to Stephen Co

Intrinsic risk/ return of

long-term inventory WIP

Borne mostly

by

Reason

Physical deterioration and

abnormal losses

Pretence Co The bank’s put option means that if the

inventory physically deteriorates, its value

will fall. This loss can be avoided by the

bank by putting the inventory back onto

Pretence.

Gains from market price

increases

Pretence Co P’s call option means that if prices

increase, it will be able to call the

inventory back into its ownership and sell

it at a profit.

Losses from market price

falls

Pretence Co Same reasoning as physical deterioration.

The existence of a put and call option at the same price means that ownership will revert to

the legal seller, whatever happens to prices. This means that Pretence retains the risks and

rewards of ownership.

An appropriate accounting treatment is therefore to continue to recognise the inventory on

Pretence’s SOFP, despite the legal transfer of ownership. The cash received from the bank should be presented as a loan, secured on the inventory WIP. The imputed interest each

period at EURIBOR + 4% should be added to the loan each period and presented as a

finance cost. Although this is described as a mark up, in substance it is a finance cost, as

evidenced by the mention of EURIBOR.

8/3/2019 731 Substance

http://slidepdf.com/reader/full/731-substance 20/20

ExPedite Note ACCA F7 Financial Reporti

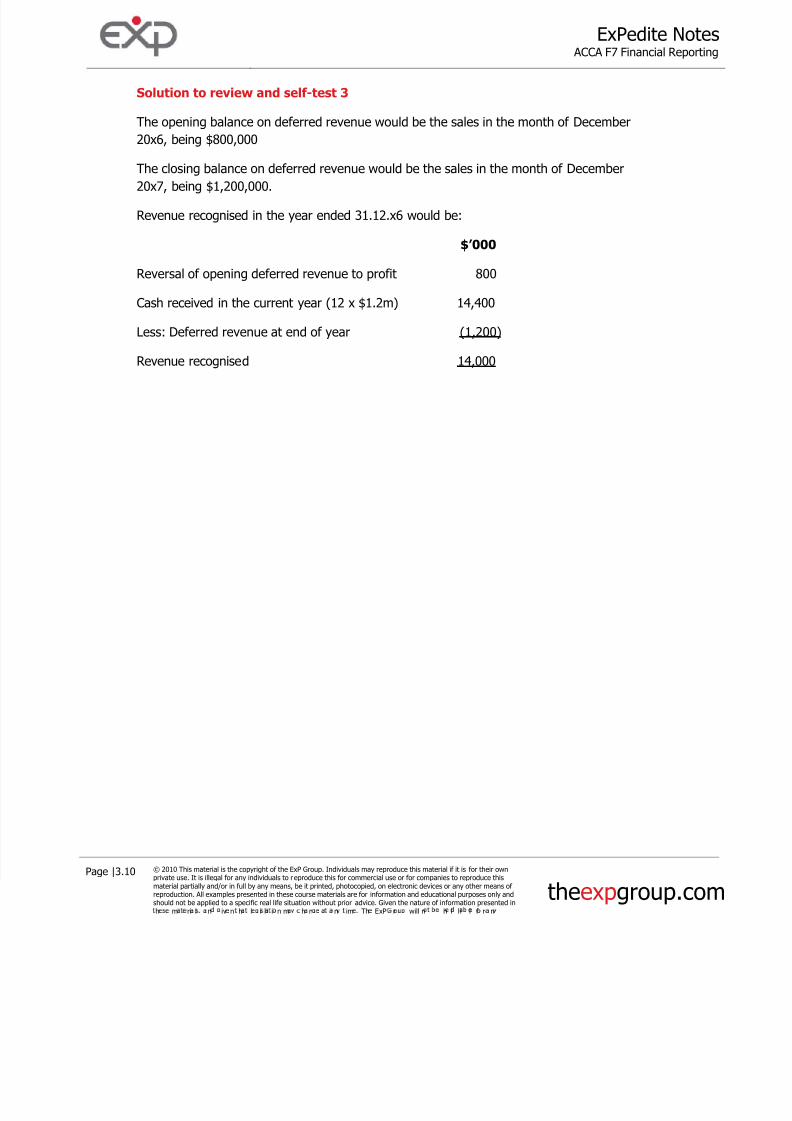

Solution to review and self-test 3

The opening balance on deferred revenue would be the sales in the month of December

20x6, being $800,000

The closing balance on deferred revenue would be the sales in the month of December

20x7, being $1,200,000.

Revenue recognised in the year ended 31.12.x6 would be:

$’000

Reversal of opening deferred revenue to profit 800

Cash received in the current year (12 x $1.2m) 14,400

Less: Deferred revenue at end of year (1,200)

Revenue recognised 14,000