660 fico and/or >45% dti - mwf wholesale · for borrowers with a fico under 660 fico and/or...

TRANSCRIPT

This information is not intended or authorized for consumer use. Credit and collateral are subject to approval. Terms a nd conditions may apply. This is not a commitment to lend.

Page 1 of 9

Copyright © 2015-2018 Mountain West Financial, Inc. All rights reserved. The mountain logo is the register ed trademark of Mountain West Financial, Inc. Rev 03-25-2020

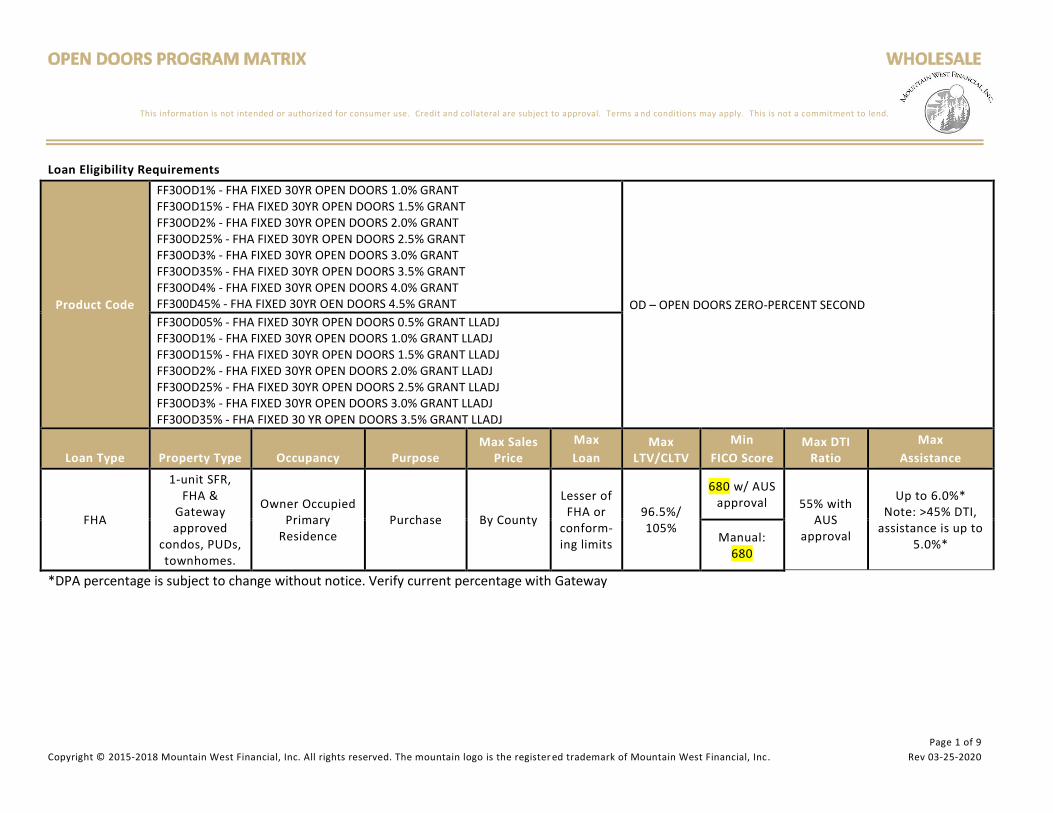

Loan Eligibility Requirements

Product Code

FF30OD1% - FHA FIXED 30YR OPEN DOORS 1.0% GRANT FF30OD15% - FHA FIXED 30YR OPEN DOORS 1.5% GRANT FF30OD2% - FHA FIXED 30YR OPEN DOORS 2.0% GRANT FF30OD25% - FHA FIXED 30YR OPEN DOORS 2.5% GRANT FF30OD3% - FHA FIXED 30YR OPEN DOORS 3.0% GRANT FF30OD35% - FHA FIXED 30YR OPEN DOORS 3.5% GRANT FF30OD4% - FHA FIXED 30YR OPEN DOORS 4.0% GRANT FF300D45% - FHA FIXED 30YR OEN DOORS 4.5% GRANT OD – OPEN DOORS ZERO-PERCENT SECOND

FF30OD05% - FHA FIXED 30YR OPEN DOORS 0.5% GRANT LLADJ FF30OD1% - FHA FIXED 30YR OPEN DOORS 1.0% GRANT LLADJ FF30OD15% - FHA FIXED 30YR OPEN DOORS 1.5% GRANT LLADJ FF30OD2% - FHA FIXED 30YR OPEN DOORS 2.0% GRANT LLADJ FF30OD25% - FHA FIXED 30YR OPEN DOORS 2.5% GRANT LLADJ FF30OD3% - FHA FIXED 30YR OPEN DOORS 3.0% GRANT LLADJ FF30OD35% - FHA FIXED 30 YR OPEN DOORS 3.5% GRANT LLADJ

Loan Type Property Type Occupancy Purpose Max Sales

Price

Max

Loan Max

LTV/CLTV

Min

FICO Score Max DTI

Ratio

Max

Assistance

FHA

1-unit SFR, FHA &

Gateway approved

condos, PUDs, townhomes.

Owner Occupied Primary

Residence Purchase By County

Lesser of FHA or

conform-ing limits

96.5%/ 105%

680 w/ AUS approval 55% with

AUS approval

Up to 6.0%* Note: >45% DTI,

assistance is up to 5.0%*

Manual: 680

*DPA percentage is subject to change without notice. Verify current percentage with Gateway

Page 2 of 9

Rev 03-25-2020

These program parameters pertain to the housing agency’s guidelines as of the status date noted on this Program Overview. Program

guidelines should be confirmed with the respective agency prior to loan submission to ensure the use of the most current para meters.

When combined with any program, the stricter underwriting guidelines will always prevail.

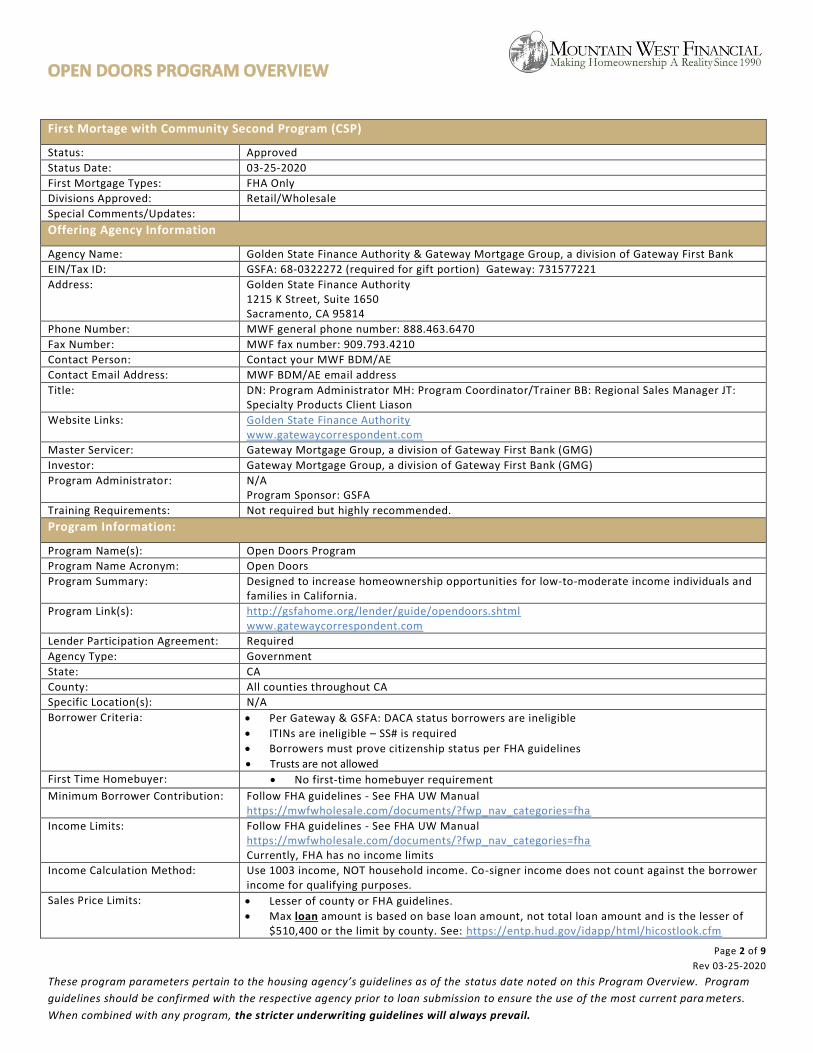

First Mortage with Community Second Program (CSP)

Status: Approved

Status Date: 03-25-2020

First Mortgage Types: FHA Only

Divisions Approved: Retail/Wholesale

Special Comments/Updates:

Offering Agency Information

Agency Name: Golden State Finance Authority & Gateway Mortgage Group, a division of Gateway First Bank

EIN/Tax ID: GSFA: 68-0322272 (required for gift portion) Gateway: 731577221

Address: Golden State Finance Authority 1215 K Street, Suite 1650 Sacramento, CA 95814

Phone Number: MWF general phone number: 888.463.6470

Fax Number: MWF fax number: 909.793.4210

Contact Person: Contact your MWF BDM/AE

Contact Email Address: MWF BDM/AE email address

Title: DN: Program Administrator MH: Program Coordinator/Trainer BB: Regional Sales Manager JT: Specialty Products Client Liason

Website Links: Golden State Finance Authority www.gatewaycorrespondent.com

Master Servicer: Gateway Mortgage Group, a division of Gateway First Bank (GMG)

Investor: Gateway Mortgage Group, a division of Gateway First Bank (GMG)

Program Administrator: N/A Program Sponsor: GSFA

Training Requirements: Not required but highly recommended.

Program Information:

Program Name(s): Open Doors Program

Program Name Acronym: Open Doors

Program Summary: Designed to increase homeownership opportunities for low-to-moderate income individuals and families in California.

Program Link(s): http://gsfahome.org/lender/guide/opendoors.shtml www.gatewaycorrespondent.com

Lender Participation Agreement: Required

Agency Type: Government

State: CA

County: All counties throughout CA

Specific Location(s): N/A

Borrower Criteria: Per Gateway & GSFA: DACA status borrowers are ineligible

ITINs are ineligible – SS# is required

Borrowers must prove citizenship status per FHA guidelines

Trusts are not allowed

First Time Homebuyer: No first-time homebuyer requirement

Minimum Borrower Contribution: Follow FHA guidelines - See FHA UW Manual https://mwfwholesale.com/documents/?fwp_nav_categories=fha

Income Limits: Follow FHA guidelines - See FHA UW Manual https://mwfwholesale.com/documents/?fwp_nav_categories=fha Currently, FHA has no income limits

Income Calculation Method: Use 1003 income, NOT household income. Co-signer income does not count against the borrower income for qualifying purposes.

Sales Price Limits: Lesser of county or FHA guidelines.

Max loan amount is based on base loan amount, not total loan amount and is the lesser of $510,400 or the limit by county. See: https://entp.hud.gov/idapp/html/hicostlook.cfm

Page 3 of 9

Rev 03-25-2020

These program parameters pertain to the housing agency’s guidelines as of the status date noted on this Program Overview. Program

guidelines should be confirmed with the respective agency prior to loan submission to ensure the use of the most current para meters.

When combined with any program, the stricter underwriting guidelines will always prevail.

Homebuyer Education Required: Follow FHA guidelines - See FHA UW Manual https://mwfwholesale.com/documents/?fwp_nav_categories=fha

Currently, FHA does not have a Homebuyer Education requirement

High Balance Loan Amount: HB not allowed

Maximum Assistance Amount: Note: DPA percentage is subject to change without notice. Confirm current percentage with Gateway. Up to 6.0% of the total 1st mortgage loan amount, including MIP, in the form of a 2.0% deferred 2nd lien and up to 4.0% as a gift.

The Gift from GSFA does not need to be rounded up or down.

For borrowers with DTI >45% (not cumulative), they will have a 1.00% gift adjustment paid for with DPA funds, meaning 5.0% total assistance. Use product codes with LLADJ

2nd lien is to be rounded down to nearest dollar.

Gateway will not allow a 3rd lien on the property. Other MWF approved DPA programs that do not have a lien must have prior Gateway approval

There is no minimum 2nd mortgage amount

Use of Subordinate Funds: Down Payment and/or Closing Costs

Minimum Reserves: Program has no minimum reserves requirement - Follow FHA guidelines

Maximum Assets: Follow FHA guidelines - See FHA UW Manual https://mwfwholesale.com/documents/?fwp_nav_categories=fha

Debt to Income Ratio: Max DTI is 55% with AUS approval

For DTI >45% with AUS approval, Lenders must use the pricing grid on the rate sheet labeled “GOVERNMENT GSFA OpenDoors-LLADJ”.

For manual underwrite:

Max 50% DTI, meet FHA guidelines including compensating factors- DU/LP findings must be included

Minimum FICO: 680 with AUS approval

All borrowers must have at least one credit score.

>45% DTI (not cumulative) will have a 1.00% gift adjustment paid for with DPA funds i.e. up to 5.0% assistance

Maximum LTV/CLTV: FHA guidelines which is 96.5%/105%

Occupancy: Borrower(s) must occupy as primary residence

MCC Permitted (Y/N): Yes

1st Loan/Repayment Terms:

Interest Rate: Rates are available in PML

Term: Fully Amortized 30-Year fixed

Loan Purpose Type: Purchase only

Mortgage Insurance: FHA UFMI 1.75%

2nd Loan/Repayment Terms:

Interest Rate: 0%

Term: 30-Year

Repayment-If Deferred, # of Months

Due upon sale, refinance or payoff of 1st mortgage. Re-subordinations are not allowed

Forgiveness of Debt (if any): None

Lien Position (2nd, 3rd, 4th): 2nd only. GSFA & Gateway will not subordinate to allow the borrower to refinance to a lower rate

If using a different MWF-approved DPA in lieu of Open Doors standard assistance, prior Gateway approval is required.

3rd liens are not allowed Grant is forgiven at closing – no lien position

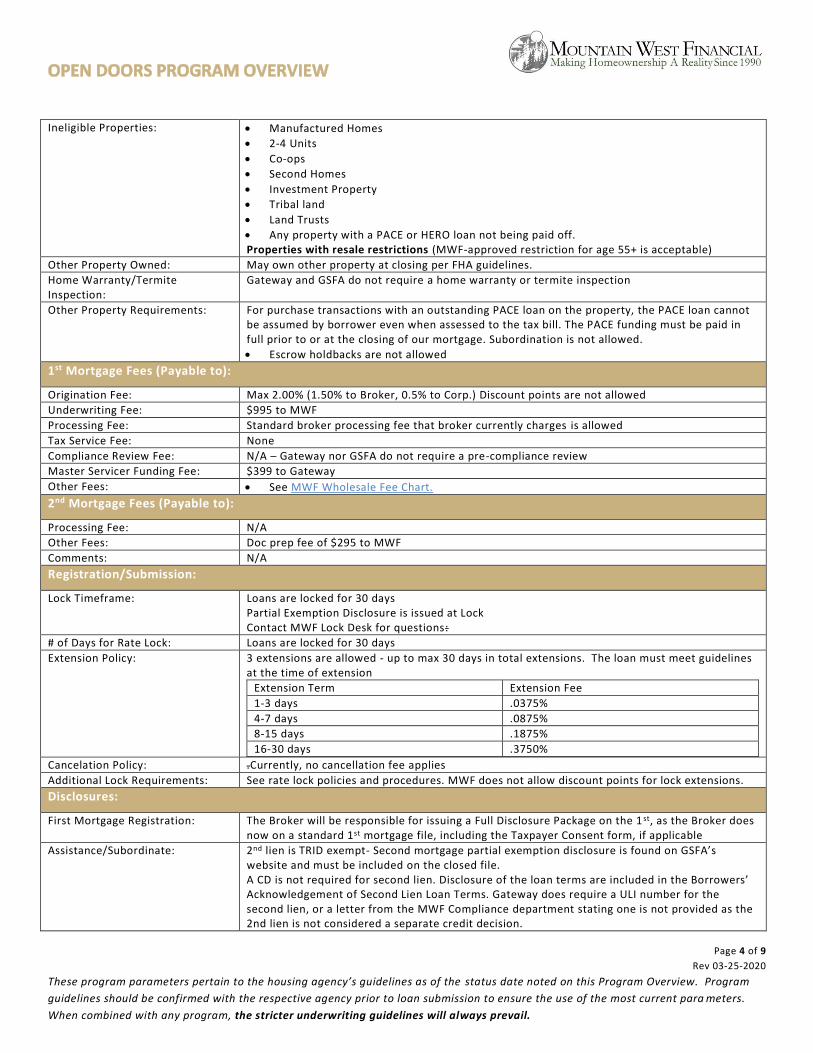

Property Requirements:

Eligible Properties: Single family properties only; 1-unit SFR, FHA & Gateway approved condos, PUDs, townhomes. GSFA allows for the following condo project approval process:

https://www.hud.gov/sites/dfiles/OCHCO/documents/4000.1hsgh.pdf FHA Spot approvals are allowed

Page 4 of 9

Rev 03-25-2020

These program parameters pertain to the housing agency’s guidelines as of the status date noted on this Program Overview. Program

guidelines should be confirmed with the respective agency prior to loan submission to ensure the use of the most current para meters.

When combined with any program, the stricter underwriting guidelines will always prevail.

Ineligible Properties: Manufactured Homes

2-4 Units

Co-ops

Second Homes

Investment Property

Tribal land

Land Trusts

Any property with a PACE or HERO loan not being paid off. Properties with resale restrictions (MWF-approved restriction for age 55+ is acceptable)

Other Property Owned: May own other property at closing per FHA guidelines.

Home Warranty/Termite Inspection:

Gateway and GSFA do not require a home warranty or termite inspection

Other Property Requirements: For purchase transactions with an outstanding PACE loan on the property, the PACE loan cannot be assumed by borrower even when assessed to the tax bill. The PACE funding must be paid in full prior to or at the closing of our mortgage. Subordination is not allowed.

Escrow holdbacks are not allowed

1st Mortgage Fees (Payable to):

Origination Fee: Max 2.00% (1.50% to Broker, 0.5% to Corp.) Discount points are not allowed

Underwriting Fee: $995 to MWF

Processing Fee: Standard broker processing fee that broker currently charges is allowed

Tax Service Fee: None

Compliance Review Fee: N/A – Gateway nor GSFA do not require a pre-compliance review

Master Servicer Funding Fee: $399 to Gateway

Other Fees: See MWF Wholesale Fee Chart.

2nd Mortgage Fees (Payable to):

Processing Fee: N/A

Other Fees: Doc prep fee of $295 to MWF

Comments: N/A

Registration/Submission:

Lock Timeframe: Loans are locked for 30 days Partial Exemption Disclosure is issued at Lock Contact MWF Lock Desk for questions:

# of Days for Rate Lock: Loans are locked for 30 days

Extension Policy: 3 extensions are allowed - up to max 30 days in total extensions. The loan must meet guidelines at the time of extension

Extension Term Extension Fee

1-3 days .0375%

4-7 days .0875%

8-15 days .1875%

16-30 days .3750%

Cancelation Policy: .Currently, no cancellation fee applies

Additional Lock Requirements: See rate lock policies and procedures. MWF does not allow discount points for lock extensions.

Disclosures:

First Mortgage Registration: The Broker will be responsible for issuing a Full Disclosure Package on the 1 st, as the Broker does now on a standard 1st mortgage file, including the Taxpayer Consent form, if applicable

Assistance/Subordinate: 2nd lien is TRID exempt- Second mortgage partial exemption disclosure is found on GSFA’s website and must be included on the closed file. A CD is not required for second lien. Disclosure of the loan terms are included in the Borrowers’ Acknowledgement of Second Lien Loan Terms. Gateway does require a ULI number for the second lien, or a letter from the MWF Compliance department stating one is not provided as the 2nd lien is not considered a separate credit decision.

Page 5 of 9

Rev 03-25-2020

These program parameters pertain to the housing agency’s guidelines as of the status date noted on this Program Overview. Program

guidelines should be confirmed with the respective agency prior to loan submission to ensure the use of the most current para meters.

When combined with any program, the stricter underwriting guidelines will always prevail.

Disclosures for the 2nd are found at GSFA/NHF website: https://nhfresportal.nhfloan.org/login.aspx?ReturnUrl=%2f The gift is listed as GSFA Gift Funds. The Open Doors docs must come from the GSFA/NHF website: No exceptions per GSFA

Loan Submission: See http://www.gatewaycorrespondent.com/overlay-matrix/forms/ for required docs.

QM: Standard procedures apply – 1st lien must comply

HPML: Standard procedures apply – Gateway allows 1st lien HPML

Appraisal

Appraisal Requirements: Appraisal condition ratings of C 5 and C 6 are ineligible

Condos require an HOA Certification form

Underwriting

AUS: 55% max DTI with LPA approval

Income worksheet or explanation of income calculation must be included in the loan file.

2nd lien should show as an Affordable Second in AUS

Trusts are not allowed

Manual Underwriting: Allowed if credit score is 680 or higher, with restrictions: Per Gateway, max 50% DTI, meet FHA guidelines including compensating factors & LP findings. File must include copy of LPA finding of Caution/Refer/Ineligible

Co-Signors: Allowed. Follow FHA guidelines - See FHA UW Manual https://mwfwholesale.com/documents/?fwp_nav_categories=fha

Non-Occupant Co-Borrowers: Allowed. Follow FHA guidelines - See FHA UW Manual https://mwfwholesale.com/documents/?fwp_nav_categories=fha

Gift Funds: Allowed

Seller Contribution: Allowed up to Interested Party Contributions guidelines: 6% max

Prior-to-Doc Conditions: Standard prior to doc conditions apply

Prior-to-Funding Conditions: Standard prior to funding condidtions apply

Compliance File: No pre-compliance review required

MWF Overlays: Note: Standard Gateway overlays do not apply to Open Doors. Do not refer to Gateway’s Overlay matrix

MWF: 2-4 units are ineligible property types

Loan Documents/Funding

Linked Loan: The Open Doors 2nd lien is the linked loan

Closing Disclosure: Closing Instructions (both general and loan specific) must be included in the file

Hazard Insurance Information: Beneficiary for the 1st mortgage: Mountain West Financial, Inc. its sucessors and assigns. Upon MWF sale of 1st to Gateway, MWF will update endorsement to read: Gateway Mortgage Group, a division of Gateway First Bank ISAOA/ATIMA, PO Box 5013, Troy, Michigan, 48007-5013 Beneficiary for the 2nd mortgage: Gateway Mortgage Group, a division of Gateway First Bank ISAOA/ATIMA, PO Box 5013, Troy, Michigan, 48007-5013

Hazard/Flood Insurance Max Deductible:

If Flood Insurance is applicable, it must include both the 1st & 2nd lien max deductible is the greater of 2.5% or $2,500 Flood insurance must show Gateway as the beneficiary within 5 days of loan purchase. Flood insurance provider must be a NFIP provider or a FHA approved flood insurance private carrier

MERS: MERS registration is required for the 1 st lien only. Gateway’s MERS # is 1002877

Cash Back allowed? Yes, with limitations: MRI must be met/remaining cash back cannot exceed sourced EMD

Max Cash to Borrower: MRI must be met/remaining cash back cannot exceed sourced EMD

Page 6 of 9

Rev 03-25-2020

These program parameters pertain to the housing agency’s guidelines as of the status date noted on this Program Overview. Program

guidelines should be confirmed with the respective agency prior to loan submission to ensure the use of the most current para meters.

When combined with any program, the stricter underwriting guidelines will always prevail.

Excess Funds: Reduce the grant amount

Loan Doc Provider at Closing: Closing docs are pulled from GSFA lender portal for the 1 st

Closing docs are pulled from https://nhfresportal.nhfloan.org/login.aspx?ReturnUrl=%2f , 9:00 am to 4:00 pm M-F, excluding National Holidays for the 2nd.

The first lien and second lien closing docs need to be dated the same date.

eSign is prohibited per Gateway

Note Closed in the Name of: 1st is closed in MWF’s name, then endorsed to Gateway:

“Pay to the order of Gateway Mortgage Group, a division of Gateway First Bank without recourse”

2nd closes in GSFA’s name

Requesting Docs: MWF pulls the docs from GSFA website https://nhfresportal.nhfloan.org/login.aspx

Wiring of Funds: MWF funds both 1st & 2nd The 2nd and gift are included in the wire of the 1st.

Notice Prior to Funding: 48 hours

Title Insurance: Required. The 2nd lien does not require a separate policy

Impound Requirements: FHA guidelines

Required Documents: MWF will provide the closing documents for signing Note, Deed of Trust and Partial Exemption Disclosure. Locks will issue the Partial Exemption

Disclosure at Registration GSFA must be the beneficiary on the 2nd TD documents

Collateral Process: See checklist at http://www.gatewaycorrespondent.com/overlay-matrix/forms/

Post Closing

Credit Package Delivery/Checklist: See http://www.gatewaycorrespondent.com/overlay-matrix/forms/ for required docs, including the Fraud Report. Gateway credit/collateral checklist: Resource Center/Associated and GSFA Open Doors Checklist: Resource Library/GSFA Open Doors Client Checklist for 2 nd loan Docs/Delegated File Submission Checklist

Use the General and Open Doors checklists

Original 1st and 2nd Notes:

Gateway Mortgage Group LLC

Correspondent Note Custodian

244 South Gateway Place

Jenks, OK 74037-3448 Recorded 1st & 2nd TDs: Same address, attention Correspondent Final Documents

Compliance File Delivery/Checklist:

See http://www.gatewaycorrespondent.com/overlay-matrix/forms/ for required docs.

# of Days to Purchase File: Locks are available for 30 days

Extension Requests: See http://www.gatewaycorrespondent.com/overlay-matrix/forms/

Additional Requirements: None

Page 7 of 9

Rev 03-25-2020

These program parameters pertain to the housing agency’s guidelines as of the status date noted on this Program Overview. Program

guidelines should be confirmed with the respective agency prior to loan submission to ensure the use of the most current para meters.

When combined with any program, the stricter underwriting guidelines will always prevail.

BOLT: OBTAIN PRICING AND REGISTER

Step 1: From the Pricing screen, after entering the borrower and property information, enter the Appraised

Value and Sales Price.

Step 2: Select “Yes” for 2nd Financing.

Page 8 of 9

Rev 03-25-2020

These program parameters pertain to the housing agency’s guidelines as of the status date noted on this Program Overview. Program

guidelines should be confirmed with the respective agency prior to loan submission to ensure the use of the most current para meters.

When combined with any program, the stricter underwriting guidelines will always prevail.

Step 3: Insert the LTV % of the 1st and 2nd liens (Max 2nd is 2% of the 1st TD).

Step 4: Change Loan Originator is paid by to Borrower

Page 9 of 9

Rev 03-25-2020

These program parameters pertain to the housing agency’s guidelines as of the status date noted on this Program Overview. Program

guidelines should be confirmed with the respective agency prior to loan submission to ensure the use of the most current para meters.

When combined with any program, the stricter underwriting guidelines will always prevail.

Step 5: After running pricing, select "price 2nd lien" for the 1 st lien program you want to register.

Step 6: When the second lien program results screen appears, select “register” for the OD – OPEN DOORS ZERO-

PERCENT SECOND program.

Step 7: Once 1st and 2nd are registered, go to Page 2 on Application Information screen

Step 8: Enter GSFA Grant/Gift amount in Assets section under Cash Deposit (up to 4.5% of 1 st mortgage loan

amount).