6 - tom blue.ppt - firt · tom blue blue, johnson & associates, inc. 6101marble ne.,suite 8...

TRANSCRIPT

BLUE, JOHNSON & ASSOCIATES, INC. FERTILIZERS CHEMICALS MINERALS ENERGY

TFI FERTILIZER OUTLOOK &

TECHNOLOGY CONFERENCE

November 17, 2010

NITROGEN OUTLOOK Presentation Visuals

by Tom Blue

Blue, Johnson & Associates, Inc.

6101 MARBLE NE., SUITE 8 829 PINEHURST PLACE 2233 GLENBAR DRIVE ALBUQUERQUE, NEW MEXICO 87110 SAN RAMON, CALIFORNIA 94583 GERMANTOW N, TENNESSEE 38139

FAX (505) 254-2159 FAX (925) 833-9054 FAX (901) 757-4179

THOMAS A. BLUE (505) 254-2157 DENNIS R. JOHNSON (925) 833-1699 DAVID C. CENTKO (901) 757-4494 BLUEABQ@QW EST.NET GAYLE E. JOHNSON (925) 833-1699 [email protected]

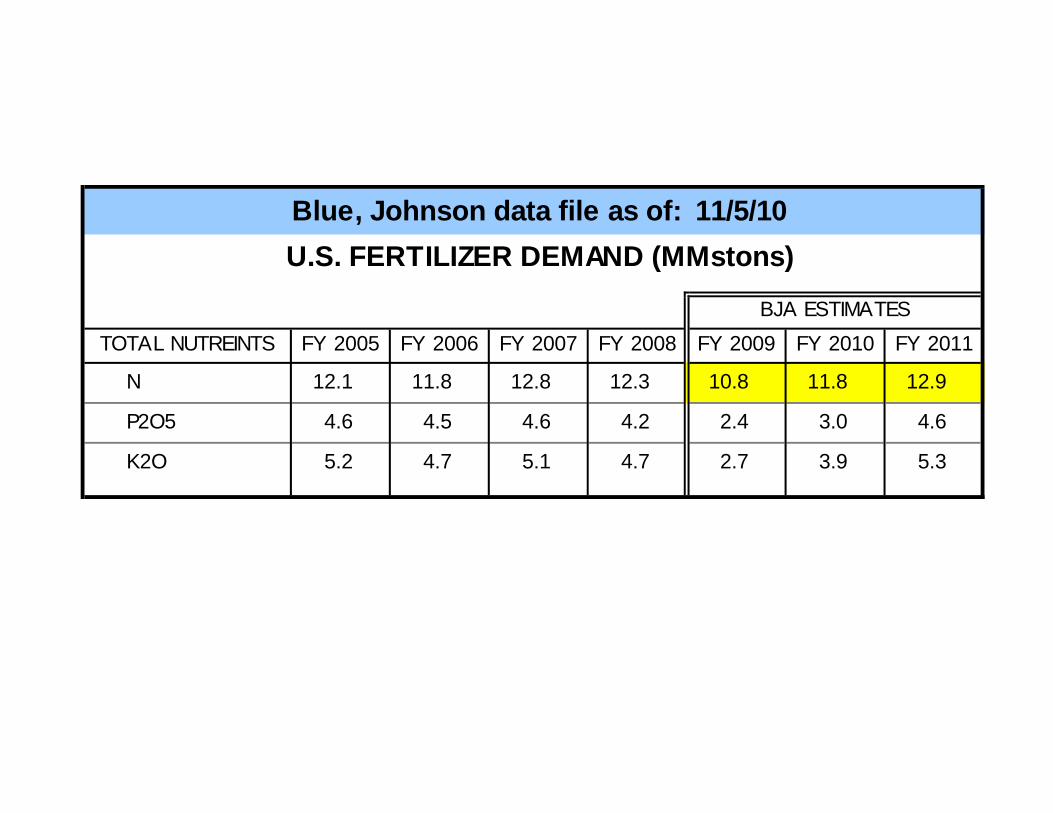

Blue, Johnson data file as of: 11/5/10U.S. FERTILIZER DEMAND (MMstons)

BJA ESTIMATESTOTAL NUTREINTS FY 2005 FY 2006 FY 2007 FY 2008 FY 2009 FY 2010 FY 2011

N 12.1 11.8 12.8 12.3 10.8 11.8 12.9

P2O5 4.6 4.5 4.6 4.2 2.4 3.0 4.6

K2O 5.2 4.7 5.1 4.7 2.7 3.9 5.3

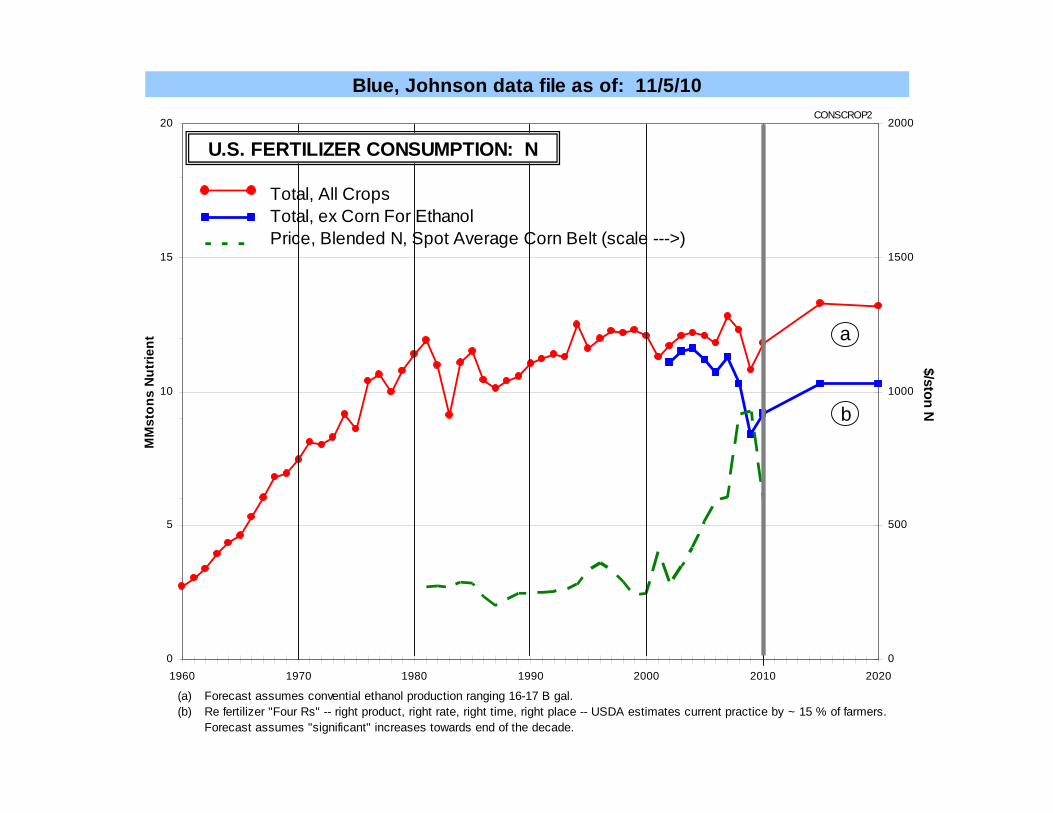

Blue, Johnson data file as of: 11/5/10

0

5

10

15

20

1960 1970 1980 1990 2000 2010 20200

500

1000

1500

2000

U.S. FERTILIZER CONSUMPTION: N

CONSCROP2

MM

ston

s N

utrie

nt

Total, All CropsTotal, ex Corn For EthanolPrice, Blended N, Spot Average Corn Belt (scale --->)

$/ston Nb

a

Forecast assumes convential ethanol production ranging 16-17 B gal.Re fertilizer "Four Rs" -- right product, right rate, right time, right place -- USDA estimates current practice by ~ 15 % of farmers. Forecast assumes "significant" increases towards end of the decade.

(a)(b)

Blue, Johnson data file as of: 11/5/10

0

5

10

15

20

1960 1970 1980 1990 2000 2010 2020

U.S. NUTRIENT CONSUMPTION: N

CONSCROP2M

Mst

ons

Nut

rient

Fertilizer,Total ex Corn For Ethanol (a)Energy (b)Other Industrial

Re fertilizer "Four Rs" -- right product, right rate, right time, right place -- USDA estimates current practice by ~ 15 % of farmers. Forecast assumes "significant" increases towards end of the decade.Energy includes corn for ethanol, AN for coal mining, and NH3-urea for emissions control (power plants, diesel engines).

(a)

(b)

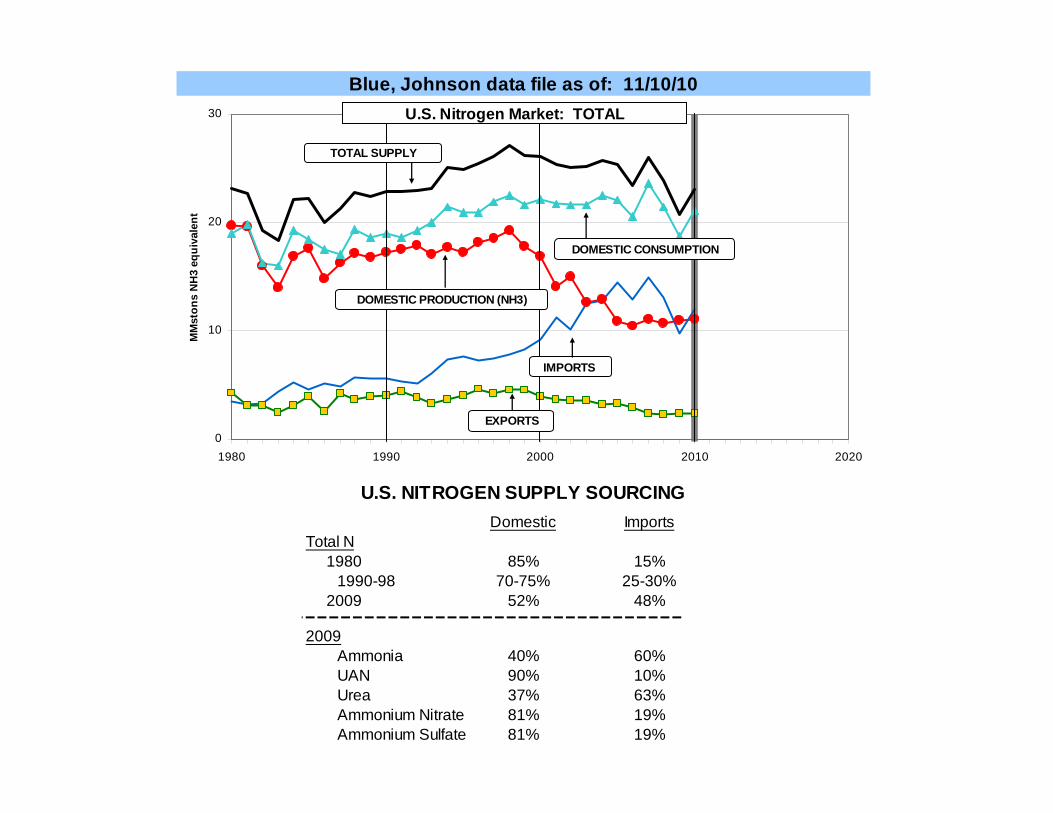

Blue, Johnson data file as of: 11/10/10

U.S. NITROGEN SUPPLY SOURCINGDomestic Imports

Total N1980 85% 15%

1990-98 70-75% 25-30%2009 52% 48%

2009 Ammonia 40% 60% UAN 90% 10% Urea 37% 63% Ammonium Nitrate 81% 19% Ammonium Sulfate 81% 19%

0

10

20

30

1980 1990 2000 2010 2020

MM

ston

s N

H3

equi

vale

nt

U.S. Nitrogen Market: TOTAL

DOMESTIC PRODUCTION (NH3)

IMPORTS

DOMESTIC CONSUMPTION

EXPORTS

TOTAL SUPPLY

250

750

1250

1750

J 2006 J 2007 J 2008 J 2009 J 2010 J

Mst

ons

prod

uct

25

50

75

100O

AMMONIA

U.S. PRODUCTION<--- scale

U.S. OPERATING RATEscale --->

Percent

U.S. IMPORTS<--- scale

Blue, Johnson data file as of: 11/5/10

25

50

75

100

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

PE

RC

ENT

0

5

10

15

$/MM

Btu

2008 2009 2010

U.S. AMMONIA PRODUCTION vs. NATURAL GAS PRICE prdvsgas

AMMONIA INDUSTRYOPERATING RATE

<---- scale

NATURAL GAS PRICE:CENTRAL PLAINS DLV NH3 PLANTS,

BIDWEEK INDEX BASISscale ---->

Blue, Johnson data file as of: 9/27/10

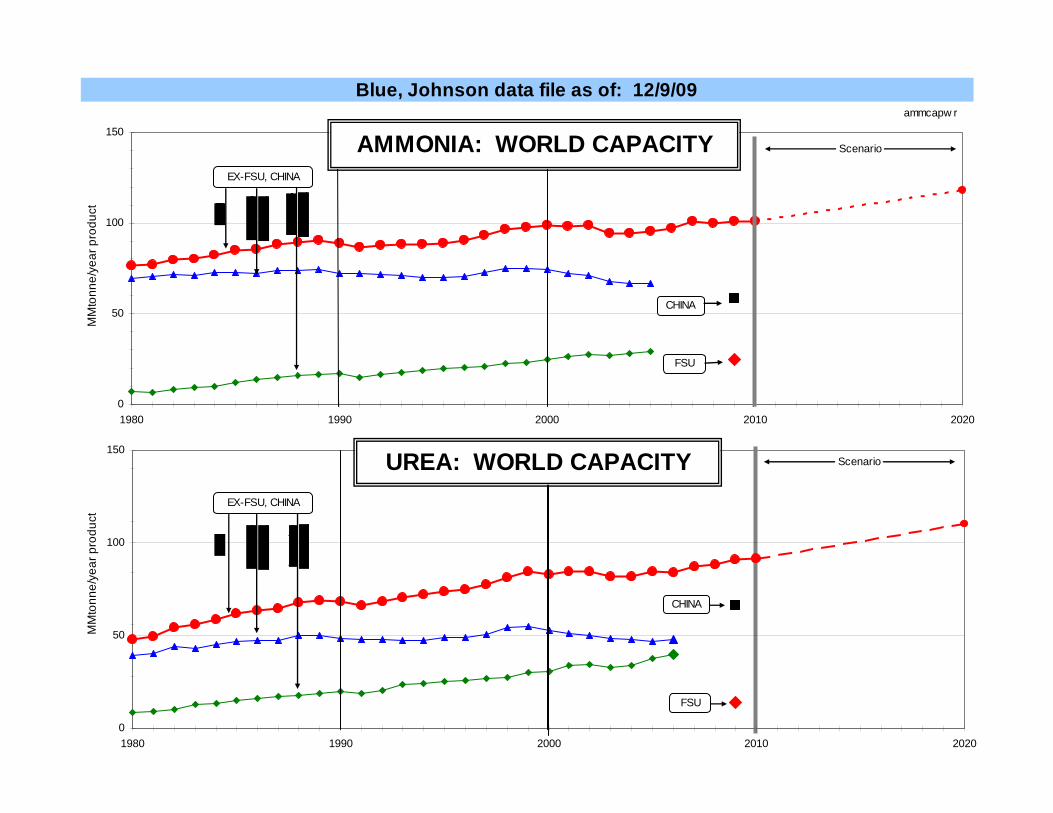

U.S. NITROGEN CAPACITY TRENDS

5

10

15

20

1995 2000 2005 2010 2015

MM

ston

s

NSOL(UAN 32 Basis)

DRY UREA

DRY AMMONIUMNITRATE

AMMONIA

nitcapgr

New modern nitrogen capacity continues to be put in place:

-- Growth in world demand,

-- Replacement and/or revamp expansions of older, less

efficient facilities.

-- Most new projects in areas with feedstock cost

advantages (e.g., North Africa, West Asia), and in China.

New projects considered outside China based on gasification

technologies (coal, petcoke). In the U.S., at least ten

specifically designed to produce ammonia and (mostly) urea.

All were large, i.e., base capacities at or near 0.9-1 MMstpy

NH3. A few are still active but most are not, for one or more

of the following reasons:

-- Drop in prices for nitrogen products. -- Drop in prices for natural gas. -- Tougher standards/costs for CO2

management/sequestering requirements, including issues about “ownership” of CO2 liabilities.

-- Overall high construction/capital costs. -- Tighter investment climate.

If any such projects get off the ground, none likely hit the

market much before 2015.

Blue, Johnson file as of: 11/10/10

MAJOR N PRODUCTS: ESTIMATED DOMESTIC SUPPLY

H2 2010 (H1 FY 2011) vs.

H2 2008

H2 2009

AMMONIA + 7% + 14%

UREA + 4% + 15%

UAN - 9% - 3%

AN - 26% - 2%

AS + 8% + 16%

NET N + 1% + 9%

Blue, Johnson data file as of: 11/5/10

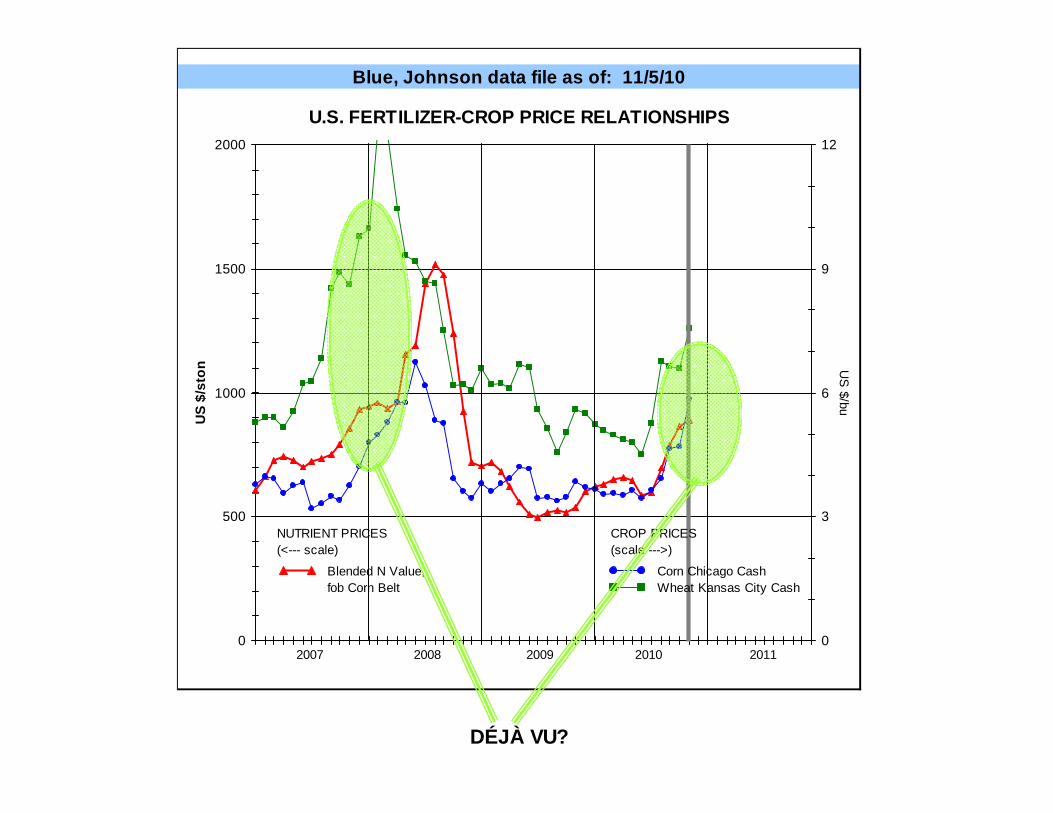

U.S. FERTILIZER-CROP PRICE RELATIONSHIPS

DÉJÀ VU?

0

500

1000

1500

2000

US

$/st

on

0

3

6

9

12

US

$/bu

2007

NUTRIENT PRICES(<--- scale)

CROP PRICES(scale --->)

Blended N Value,fob Corn Belt

Corn Chicago CashWheat Kansas City Cash

2008 2009 2010 2011

Blue, Johnson data file as of: 11/5/10

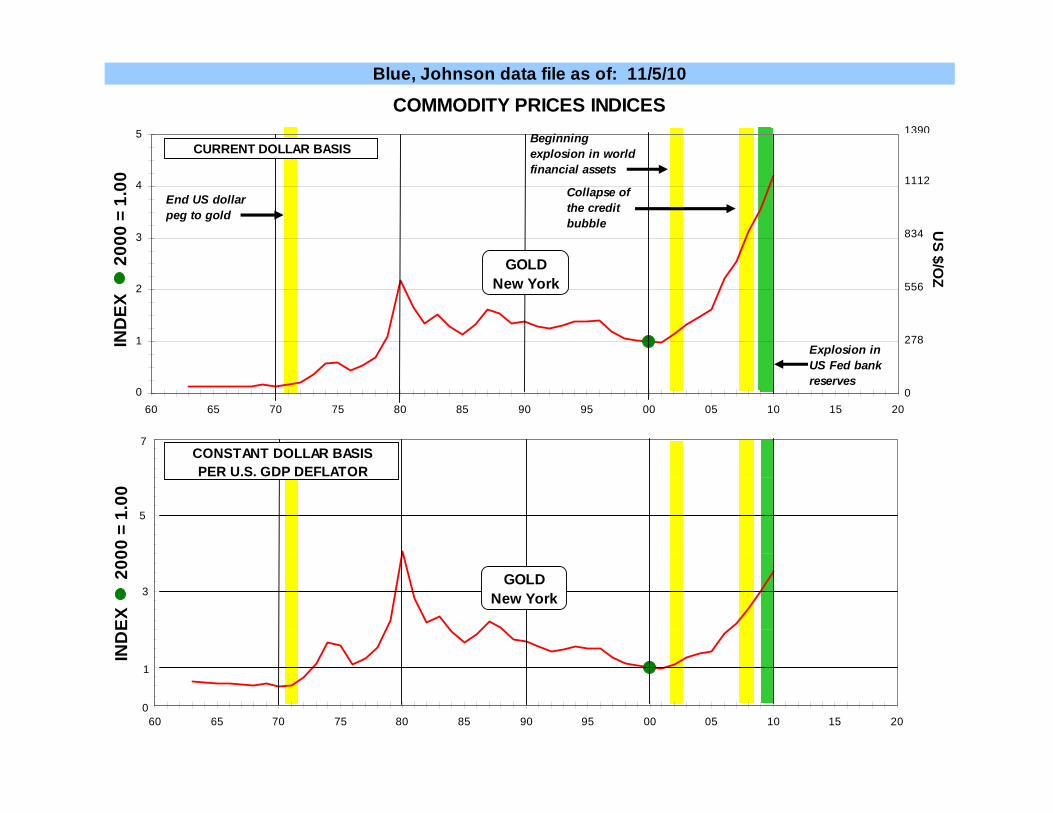

COMMODITY PRICES INDICES

0

1

2

3

4

5

60 65 70 75 80 85 90 95 00 05 10 15 20

CURRENT DOLLAR BASIS

60 65 70 75 80 85 90 95 00 05 10 15 20

CONSTANT DOLLAR BASISPER U.S. GDP DEFLATOR

IND

EX

20

00 =

1.0

0

GOLDNew York

IND

EX

20

00 =

1.0

0

GOLDNew York

0

1

3

5

7

US $/O

Z

0

278

556

834

1112

1390

End US dollarpeg to gold

Beginning explosion in world financial assets

Explosion in US Fed bank reserves

Collapse of the credit bubble

Blue, Johnson data file as of: 11/5/10

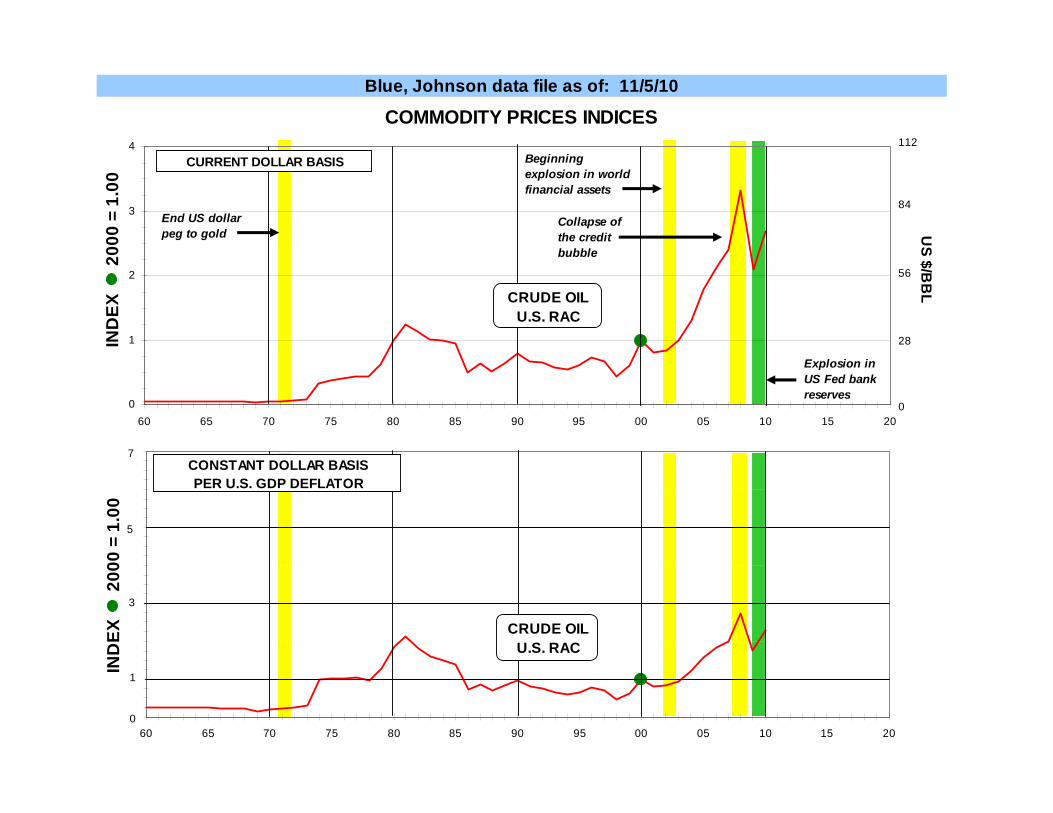

COMMODITY PRICES INDICES

60 65 70 75 80 85 90 95 00 05 10 15 20

CONSTANT DOLLAR BASISPER U.S. GDP DEFLATOR

0

1

2

3

4

60 65 70 75 80 85 90 95 00 05 10 15 20

CURRENT DOLLAR BASIS

End US dollarpeg to gold

Beginning explosion in world financial assets

Explosion in US Fed bank reserves

IND

EX

20

00 =

1.0

0

CRUDE OILU.S. RAC

IND

EX

20

00 =

1.0

0

CRUDE OILU.S. RAC

0

1

3

7

5

112

84

56

28

0

US $/B

BL

Collapse of the credit bubble

Blue, Johnson data file as of: 11/5/10

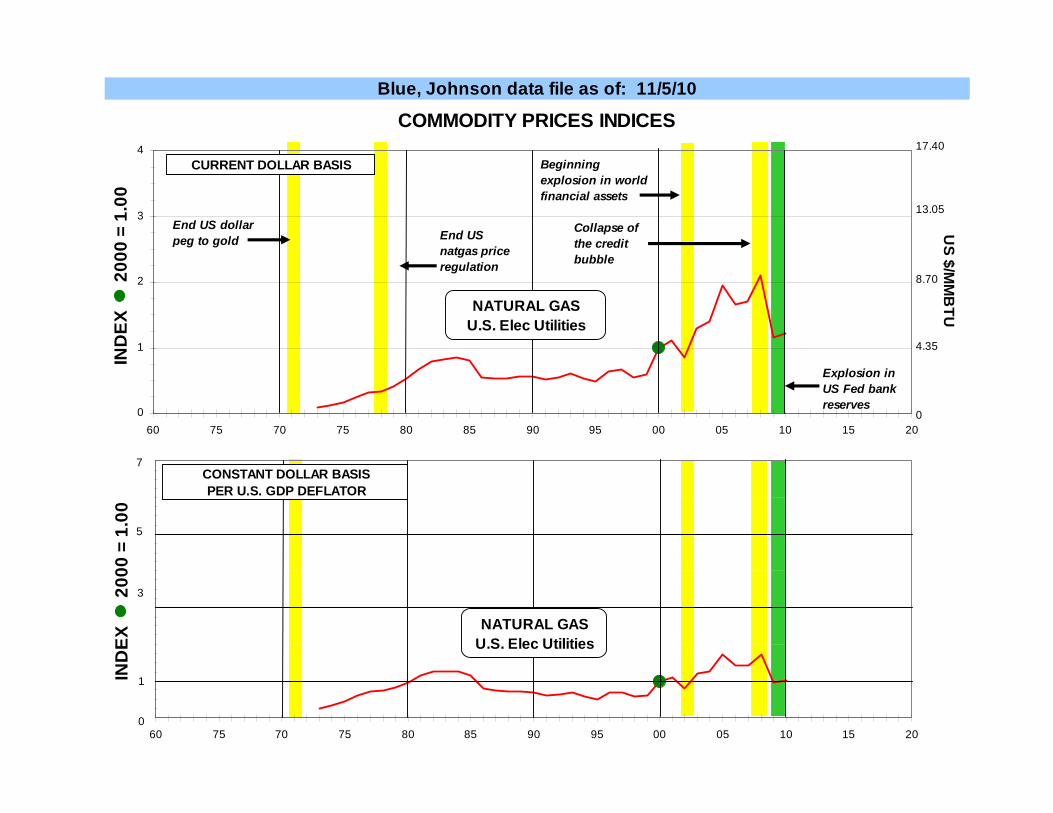

COMMODITY PRICES INDICES

0

1

2

3

4

60 75 70 75 80 85 90 95 00 05 10 15 20

CURRENT DOLLAR BASIS

End US dollarpeg to gold

Beginning explosion in world financial assets

Explosion in US Fed bank reserves

End US natgas price regulation

60 75 70 75 80 85 90 95 00 05 10 15 20

CONSTANT DOLLAR BASISPER U.S. GDP DEFLATOR

IND

EX

20

00 =

1.0

0

NATURAL GASU.S. Elec Utilities

IND

EX

20

00 =

1.0

0

NATURAL GASU.S. Elec Utilities

0

1

3

5

7

17.40

13.05

8.70

4.35

0

US $/M

MB

TU

Collapse of the credit bubble

Blue, Johnson data file as of: 11/5/10

COMMODITY PRICES INDICES

60 65 70 75 80 85 90 95 00 05 10 15 20

CONSTANT DOLLAR BASISPER U.S. GDP DEFLATOR

0

1

2

3

4

60 65 70 75 80 85 90 95 00 05 10 15 20

CURRENT DOLLAR BASIS

End US dollarpeg to gold

Beginning explosion in world financial assets

Explosion in US Fed bank reserves

IND

EX

20

00 =

1.0

0

UREANOLA Barge

IND

EX

20

00 =

1.0

0

UREANOLA Barge

0

1

3

5

7

US $/STO

N

0

143

286

429

572

Collapse of the credit bubble

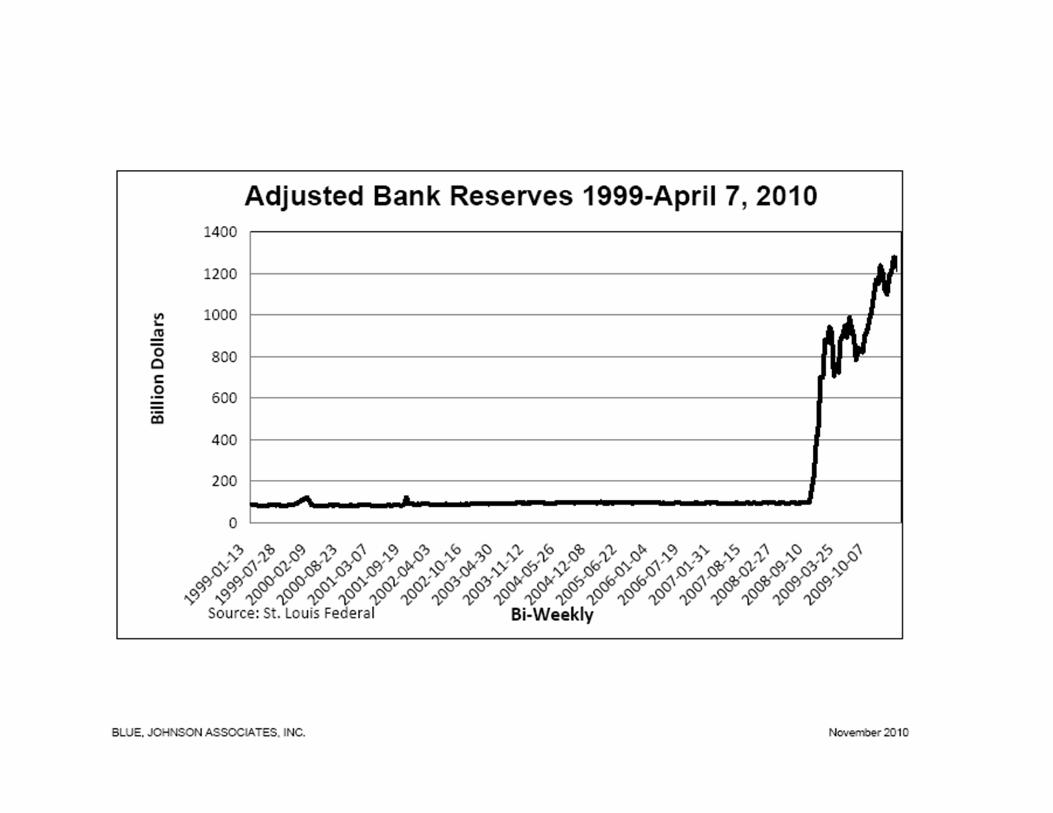

Blue, Johnson data file as of: 4/29/10

0

100

200

300

1980 1990 2000 2010 2020

$ tri

llion

1

2

3

4

WORLD "WEALTH"

FINANCIAL ASSETSGDPRATIO: Assets to GDP(scale --->)

?

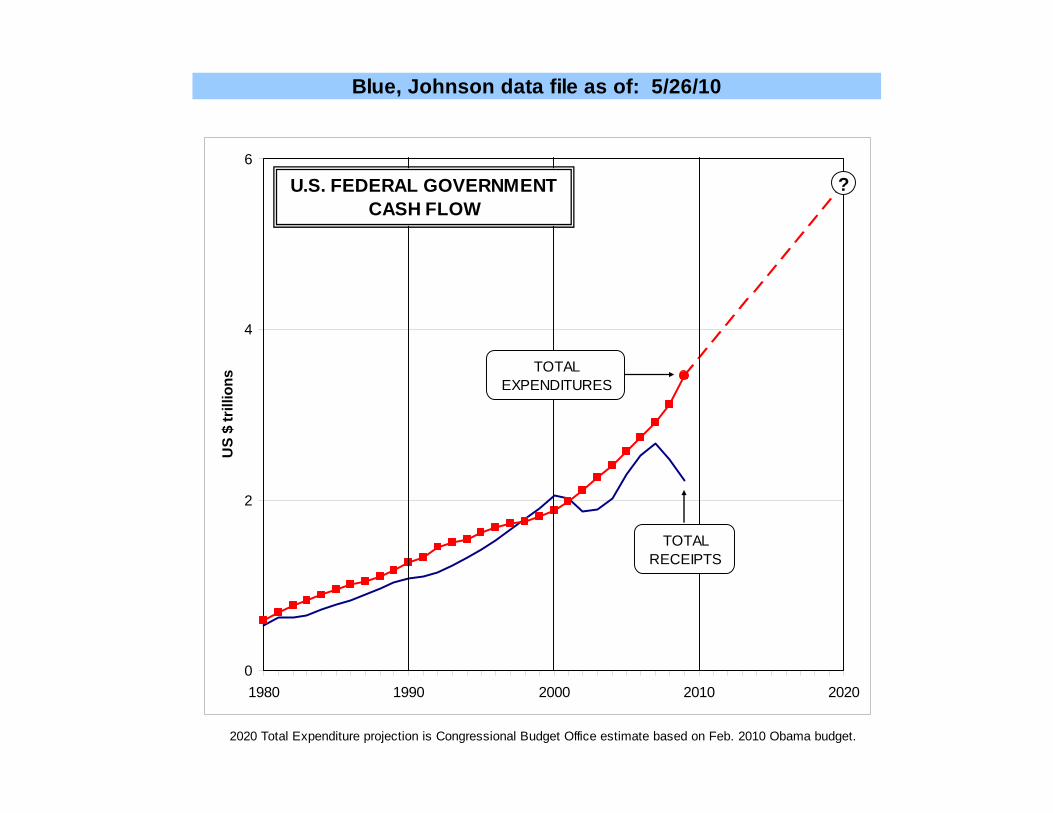

Blue, Johnson data file as of: 5/26/10

0

2

4

6

1980 1990 2000 2010 2020

US

$ tr

illio

ns

U.S. FEDERAL GOVERNMENT CASH FLOW

TOTAL RECEIPTS

2020 Total Expenditure projection is Congressional Budget Office estimate based on Feb. 2010 Obama budget.

?

TOTAL EXPENDITURES

Blue, Johnson data file as of: 11/5/10

0

500

1000

1500

J 2004 J 2005 J 2006 J 2007 J 2008 J 2009 J 2010

U.S

. $/s

ton

0

5

10

15

US

$/MM

Btu

AMMONIA: Monthly Prices vs. Gas Prices

Ammonia Price, Avg Corn Belt fob (<--- scale)Natural Gas Price, Central Plains Bidweek (scale --->)Central Plains Natural Gas Cost in Ammonia (<--- scale)

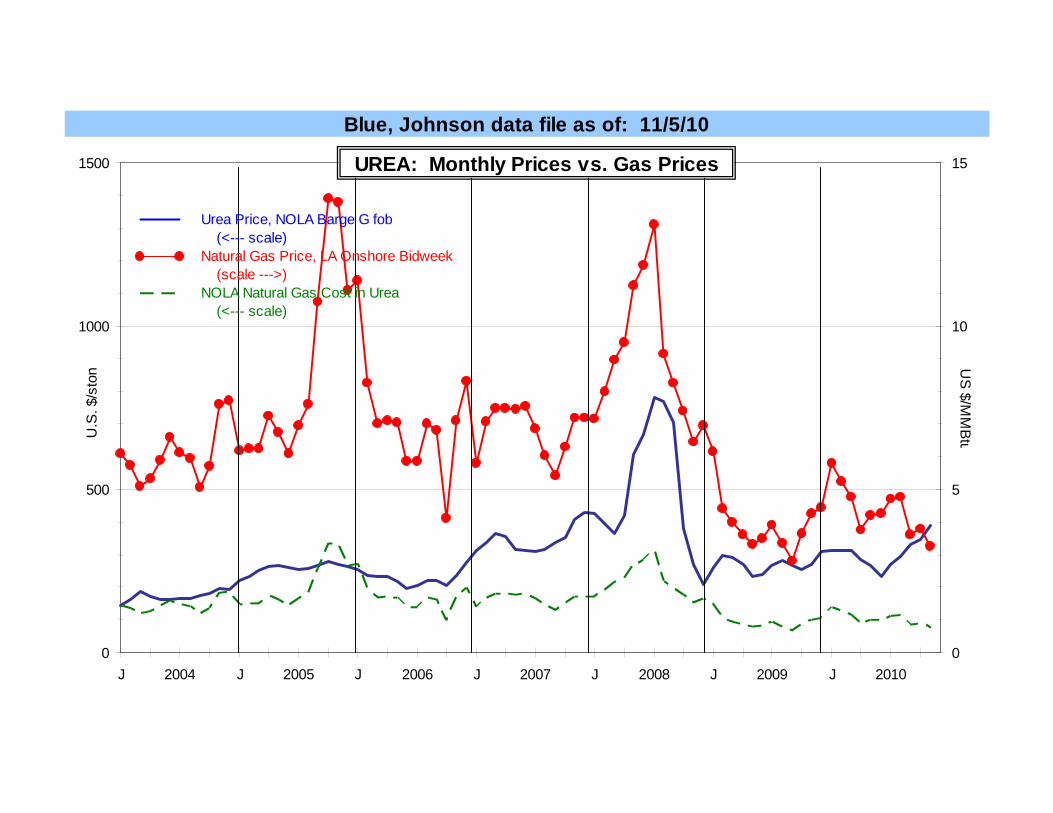

Blue, Johnson data file as of: 11/5/10

0

500

1000

1500

J 2004 J 2005 J 2006 J 2007 J 2008 J 2009 J 2010

U.S

. $/s

ton

0

5

10

15

US

$/MM

Btu

UREA: Monthly Prices vs. Gas Prices

Urea Price, NOLA Barge G fob (<--- scale)Natural Gas Price, LA Onshore Bidweek (scale --->)NOLA Natural Gas Cost in Urea (<--- scale)

Blue, Johnson data file as of: 11/5/10

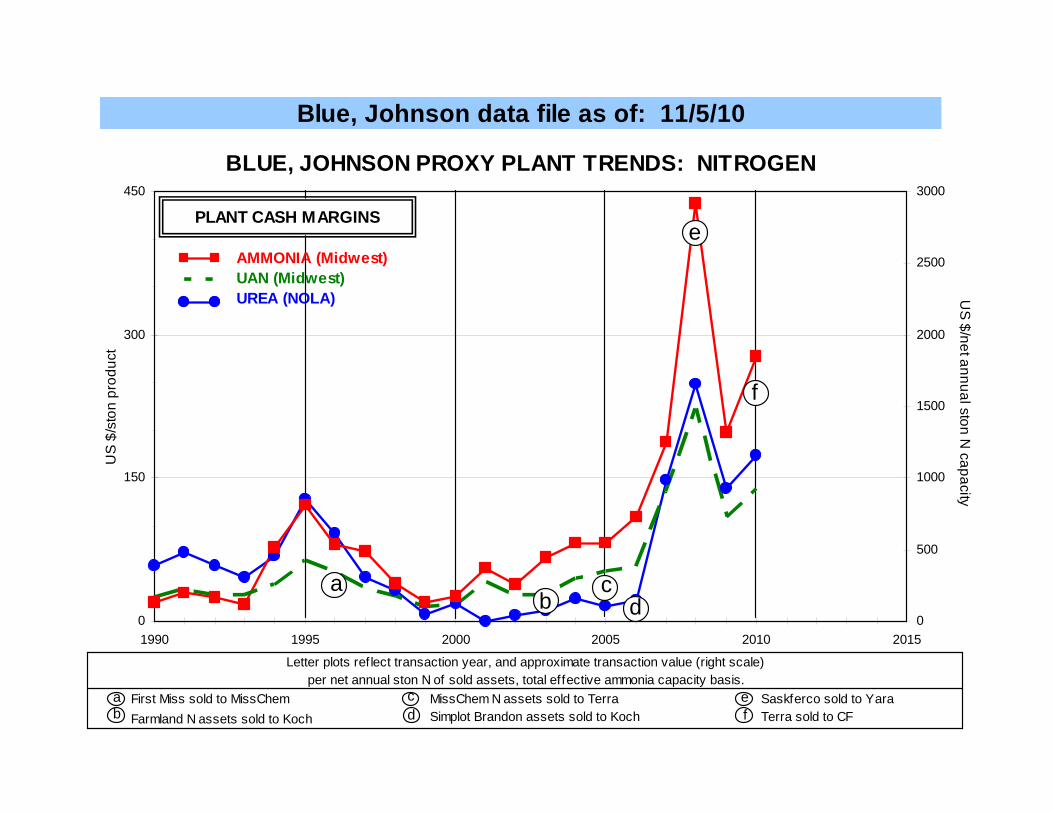

BLUE, JOHNSON PROXY PLANT TRENDS: NITROGEN

0

150

300

450

1990 1995 2000 2005 2010 2015

US

$/s

ton

prod

uct

0

500

1000

1500

2000

2500

3000

PLANT CASH MARGINS

Letter plots ref lect transaction year, and approximate transaction value (right scale)per net annual ston N of sold assets, total effective ammonia capacity basis.

MissChem N assets sold to TerraSimplot Brandon assets sold to Koch

e

f

dba

Saskferco sold to YaraTerra sold to CF

First Miss sold to MissChemFarmland N assets sold to Koch

a

US

$/net annual ston N capacity

bcd

e

c

f

AMMONIA (Midwest)UAN (Midwest)UREA (NOLA)

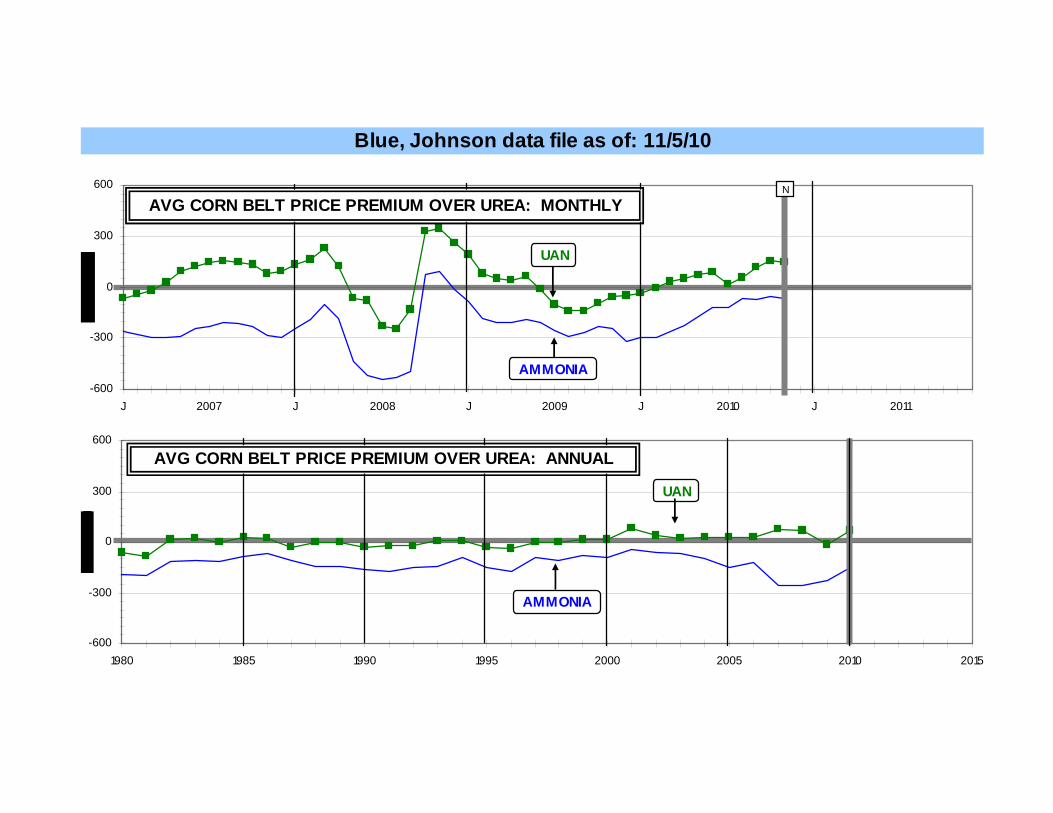

Blue, Johnson data file as of: 11/5/10

-600

-300

0

300

600

1980 1985 1990 1995 2000 2005 2010 2015

-600

-300

0

300

600

J 2007 J 2008 J 2009 J 2010 J 2011

AVG CORN BELT PRICE PREMIUM OVER UREA: MONTHLY

AMMONIA

N

AVG CORN BELT PRICE PREMIUM OVER UREA: ANNUAL

AMMONIA

UAN

UAN

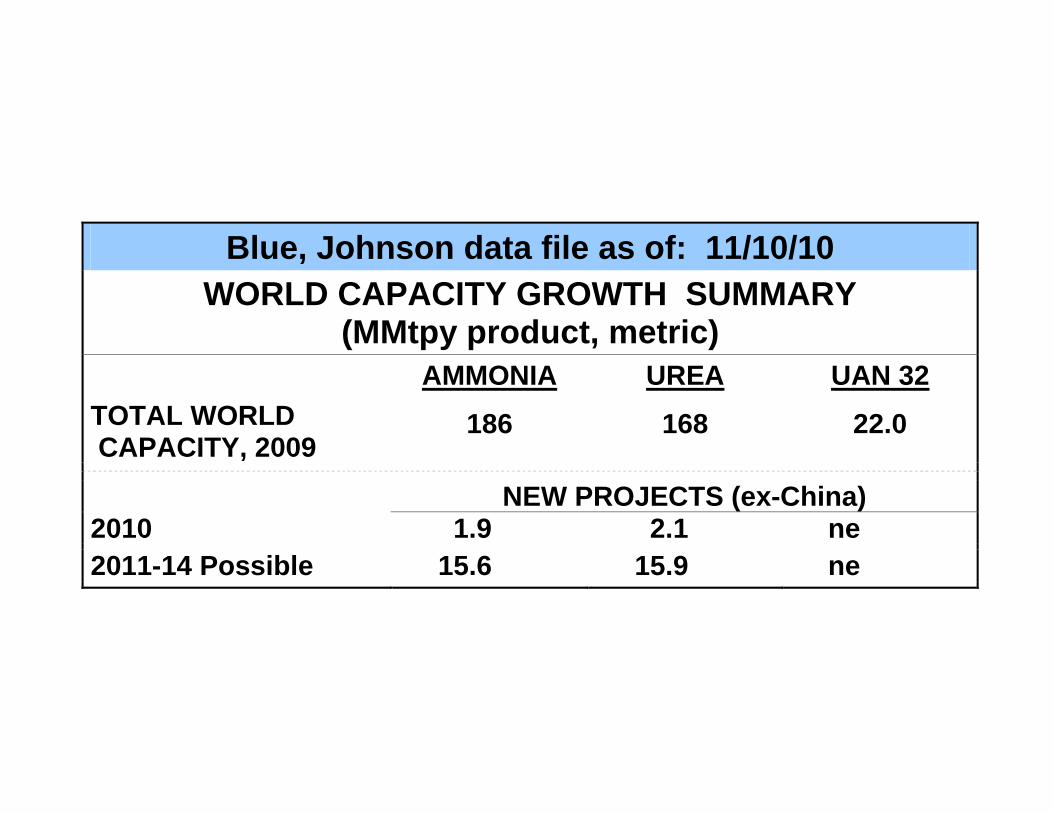

Blue, Johnson data file as of: 11/10/10 WORLD CAPACITY GROWTH SUMMARY

(MMtpy product, metric) AMMONIA UREA UAN 32 TOTAL WORLD CAPACITY, 2009

186 168 22.0 NEW PROJECTS (ex-China) 2010 1.9 2.1 ne 2011-14 Possible 15.6 15.9 ne

Blue, Johnson data file as of: 12/9/09

0

50

100

150

1980 1990 2000 2010 2020

0

50

100

150

1980 1990 2000 2010 2020

AMMONIA: WORLD CAPACITY

MM

tonn

e/ye

ar p

rodu

ct

EX-FSU, CHINA

FSU

CHINA

ammcapw r

MM

tonn

e/ye

ar p

rodu

ct

EX-FSU, CHINA

CHINA

FSU

UREA: WORLD CAPACITY

Scenario

Scenario

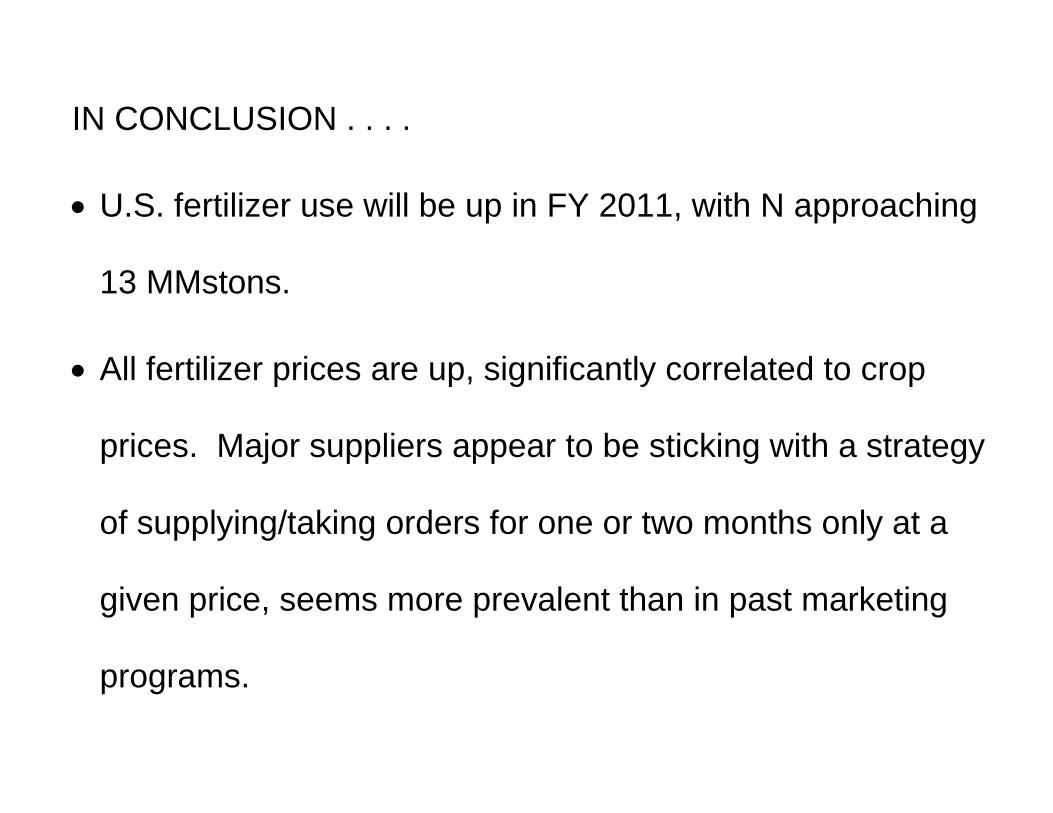

IN CONCLUSION . . . .

U.S. fertilizer use will be up in FY 2011, with N approaching

13 MMstons.

All fertilizer prices are up, significantly correlated to crop

prices. Major suppliers appear to be sticking with a strategy

of supplying/taking orders for one or two months only at a

given price, seems more prevalent than in past marketing

programs.

So, in a scenario where crop prices (especially corn) keep

ramping up, suppliers will have not “oversold” at “current”

prices (below opportunity). Or, if crop prices (corn) seriously

retreat for some reason, suppliers have the option to drop

prices so as to continue to move product. Lessons were

actually learned in 2007, 08, 09.

With corn harvest occurring relatively early, demand for P,

K, and ammonia for Fall application is/has been pretty

strong. Re P&K, though, the uncertainty becomes: if a lot

goes down now, to what degree will that impinge on Spring

demand?

In absolute terms, we see no basic, inherent shortage of N,

P & K supply capability for both the domestic and

international market. The principle issues are, as always,

supply at what price, and is it/will it be in the right place at

the right time?