6 - formulating regional logistics development policy the case of asean

TRANSCRIPT

PLEASE SCROLL DOWN FOR ARTICLE

This article was downloaded by: [2007-2008-2009 Korea Maritime University]On: 24 January 2011Access details: Access Details: [subscription number 907466557]Publisher Taylor & FrancisInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

International Journal of Logistics Research and ApplicationsPublication details, including instructions for authors and subscription information:http://www.informaworld.com/smpp/title~content=t713435362

Formulating regional logistics development policy: the case of ASEANRuth Banomyonga; P. Cookb; P. Kentb

a Department of International Business, Logistics & Transport, Thammasat University, Bangkok,Thailand b Nathan Associates Inc., Virginia, USA

To cite this Article Banomyong, Ruth , Cook, P. and Kent, P.(2008) 'Formulating regional logistics development policy: thecase of ASEAN', International Journal of Logistics Research and Applications, 11: 5, 359 — 379To link to this Article: DOI: 10.1080/13675560802389114URL: http://dx.doi.org/10.1080/13675560802389114

Full terms and conditions of use: http://www.informaworld.com/terms-and-conditions-of-access.pdf

This article may be used for research, teaching and private study purposes. Any substantial orsystematic reproduction, re-distribution, re-selling, loan or sub-licensing, systematic supply ordistribution in any form to anyone is expressly forbidden.

The publisher does not give any warranty express or implied or make any representation that the contentswill be complete or accurate or up to date. The accuracy of any instructions, formulae and drug dosesshould be independently verified with primary sources. The publisher shall not be liable for any loss,actions, claims, proceedings, demand or costs or damages whatsoever or howsoever caused arising directlyor indirectly in connection with or arising out of the use of this material.

International Journal of Logistics: Research and ApplicationsVol. 11, No. 5, October 2008, 359–379

Formulating regional logistics development policy: the caseof ASEAN

Ruth Banomyonga*, P. Cookb and P. Kentb

aDepartment of International Business, Logistics & Transport, Thammasat University, Bangkok, Thailand;bNathan Associates Inc., Virginia, USA

(Received 2 January 2008; final version received 8 July 2008 )

The Association of South East Asian Nations (ASEAN) is a regional economic grouping that is composedof Brunei, Cambodia, Indonesia, Lao PDR, Malaysia, Myanmar, Philippines, Singapore, Thailand, andVietnam. An ASEAN-wide logistics development policy has been developed and endorsed by ASEAN inAugust 2007. This logistics development policy is based on the work done by the authors as requestedby the ASEAN Secretariat. The authors provided the guiding principles, the six major policy areas aswell as the draft of the logistics sector integration roadmap that was finalised and endorsed by ASEAN.It is hoped that the formal endorsement of this important sector for ASEAN economic integration willsupport logistics liberalisation and development within ASEAN. The purpose of this paper is to explainthe methodology utilised in the formulation of the ASEAN logistics development policy that was endorsedby ASEAN member countries.

Keywords: ASEAN; logistics policy development; policy formulation; service liberalisation

1. Introduction

Logistics plays a key role in national and regional economies in two significant ways. First, logis-tics is one of the major expenditures for businesses, thereby affecting and being affected by othereconomic activities. Second, logistics supports the movement of many economic transactions; itis an important aspect of facilitating the sale of all goods and services (Grant et al. 2006).

Logistics is not only confined within national borders or markets. In each country or region,export and import firms face logistics attributes that may differ from those experienced in thedomestic market. International logistics management requires an understanding of the rela-tive transportation efficiencies in different countries. It requires that managers understand thetransportation capabilities and characteristics of primary trading countries (Rodrigues et al. 2005).

There is within international logistics a complex cross-border environment in which governmentactors play a prominent part. Moreover, wasteful transaction costs arise in cross-border operationsbetween business actors and government executive agencies (Grainger 2007). Any national orregional logistics policy that is formulated must be able to address these difficult issues.

*Corresponding author. Email: [email protected]

ISSN 1367-5567 print/ISSN 1469-848X online© 2008 Taylor & FrancisDOI: 10.1080/13675560802389114http://www.informaworld.com

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

360 R. Banomyong et al.

The purpose of this paper is to explain the methodology as well as the process utilised in theformulation of a logistics development policy for a regional economic grouping known as theAssociation of South East Asian Nations (ASEAN). ASEAN is a regional economic groupingthat is composed of Brunei, Cambodia, Indonesia, Lao PDR, Malaysia, Myanmar, Philippines,Singapore, Thailand, and Vietnam.

2. Components of a national/regional logistics system

In the global logistics environment, customs plays a very important facilitating role. Importingand exporting firms also rely heavily on specialised service providers to facilitate the flow ofgoods across borders (Banomyong 2004). ASEAN countries now realise that even with customsimprovements, trade can still be impeded by a variety of other factors including the logistics systemthat is handling the flow of goods between the border and hinterland of origin or destination points(Price 2006). As information flow needs to accompany the cargo along its routes, the accommo-dation of information exchange and the infrastructure systems through which cargo moves havebecome additional items of interest in trade and logistics facilitation. While trade facilitation wasoriginally meant to primarily address needed customs reform, the scope of trade facilitation hasbeen broadened to address virtually all of the barriers constraining the seamless flow objectivefor cargo movements. Trade facilitation has evolved into whatever is needed to improve supplychain performance, encompassing transportation and national/regional logistics systems.

The Arvis et al. (2007) World Bank publication is a good illustration of the expansion of scopein trade facilitation as it aimed to shed light on how different countries are doing in the area of tradelogistics, and what they can do to improve their performance. It was based on a worldwide surveyof the global freight forwarders and express carriers who are the most active in international trade.In the study, the cost and quality of logistics are determined not just by infrastructure and theperformance of public agencies but also by the availability of quality, competitive private services.Moreover, in many developing countries, problems of adverse geography are compounded by aweak modern services sector due to poor institutions or over-regulation.

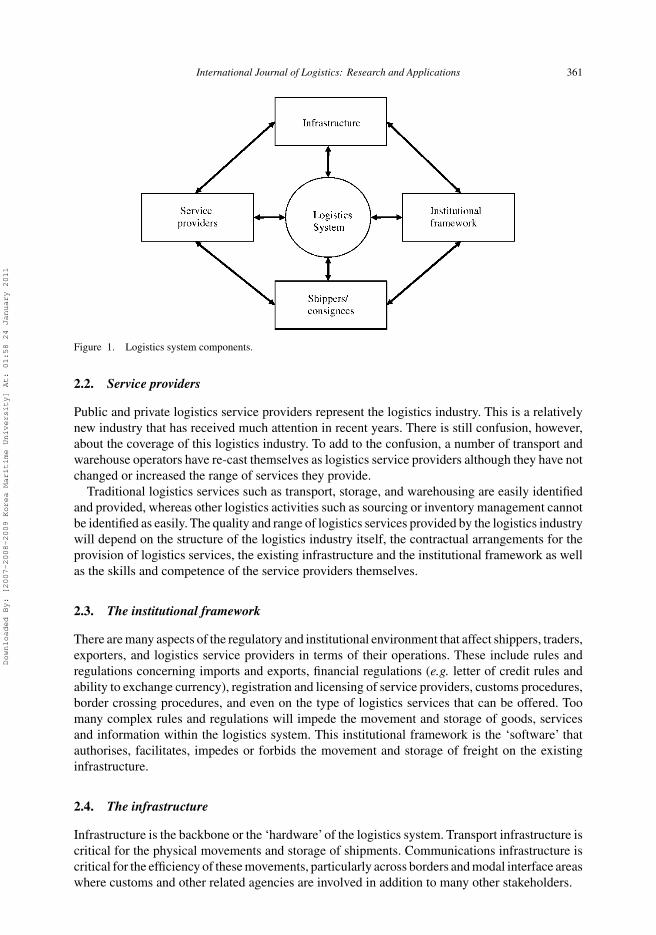

The ASEAN logistics system, like other macro level logistics systems, is composed of (1) ship-pers, traders, and consignees; (2) public and private service providers; (3) regional and nationalinstitutions, policies, and rules; and (4) transport and communications infrastructure (Asian Devel-opment Bank 2007). Figure 1 shows how these four components combine to determine to affectthe performance of the regional logistics system. The performance of the ASEAN logistics systemwill reflect both the international competitiveness of ASEAN logistics services and the level ofintegration of the ASEAN logistics system. The sum of all these factors will determine ASEAN’sinternational competitiveness (Banomyong et al. 2006).

2.1. Shippers and consignees

Shippers and consignees are the principal users or the ‘customers’ of the logistics system. Theyrequire that their goods be moved through the logistics system effectively and efficiently, both asinputs to and outputs from their businesses. Logistics systems serving shippers and consigneesmust also interface and integrate effectively with suppliers’ and customers’ own logistics systemsboth within and outside of the domestic environment.

Shippers and consignees have different levels of knowledge and understanding of their logisticssystem but it is important that the national or regional logistics system they are using can meettheir requirements and facilitate their economic transactions.

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

International Journal of Logistics: Research and Applications 361

Figure 1. Logistics system components.

2.2. Service providers

Public and private logistics service providers represent the logistics industry. This is a relativelynew industry that has received much attention in recent years. There is still confusion, however,about the coverage of this logistics industry. To add to the confusion, a number of transport andwarehouse operators have re-cast themselves as logistics service providers although they have notchanged or increased the range of services they provide.

Traditional logistics services such as transport, storage, and warehousing are easily identifiedand provided, whereas other logistics activities such as sourcing or inventory management cannotbe identified as easily. The quality and range of logistics services provided by the logistics industrywill depend on the structure of the logistics industry itself, the contractual arrangements for theprovision of logistics services, the existing infrastructure and the institutional framework as wellas the skills and competence of the service providers themselves.

2.3. The institutional framework

There are many aspects of the regulatory and institutional environment that affect shippers, traders,exporters, and logistics service providers in terms of their operations. These include rules andregulations concerning imports and exports, financial regulations (e.g. letter of credit rules andability to exchange currency), registration and licensing of service providers, customs procedures,border crossing procedures, and even on the type of logistics services that can be offered. Toomany complex rules and regulations will impede the movement and storage of goods, servicesand information within the logistics system. This institutional framework is the ‘software’ thatauthorises, facilitates, impedes or forbids the movement and storage of freight on the existinginfrastructure.

2.4. The infrastructure

Infrastructure is the backbone or the ‘hardware’of the logistics system. Transport infrastructure iscritical for the physical movements and storage of shipments. Communications infrastructure iscritical for the efficiency of these movements, particularly across borders and modal interface areaswhere customs and other related agencies are involved in addition to many other stakeholders.

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

362 R. Banomyong et al.

3. Methodology

In a declaration issued in 2003 during a summit held in Indonesia, ASEAN leaders agreed toestablish the ASEAN Economic Community through enhanced economic integration startingwith 11 priority sectors. These priority sectors were subsequently identified as the industriesrelated to rubber, automotive, garments and textiles, wood-based, agricultural, fisheries, and themanufacture and processing of electronics. Also identified were four priority service sectors,involving information and communication technology (ICT), dubbed e-ASEAN, air transport,tourism, and healthcare. Logistics was included as a priority sector for integration in 2004 butthe actual formulation of the roadmap started in the mid-2006 by the authors at the request of theASEAN Secretariat.

It was therefore important for the authors to develop a methodology that could be utilised to helpsupport ASEAN in the formulation of their logistics policy development roadmap. The first stepof the methodology was based on a rapid assessment of the ASEAN logistics sector. This meantthat the status of the sectors related to logistics services needed to be understood in terms of:

• the general condition of the transport network and fleet for each mode;• the level of modernisation of customs and trade facilitation initiatives;• the level of development and liberalisation of transport and logistics services;• the structure and scope of the freight forwarding industry and related logistics services; and• the level of modernisation of the information and communications system.

The authors therefore developed seven questionnaires relating to the major advances intro-duced in the past few decades in these related logistics sectors. These major advances weremostly identified from trade literature. The data collected described which of these advanceshave been introduced or are planned to be introduced. The purpose of the questionnaires was toassess the capacity of all logistics-related sectors in each of the ASEAN member countries. Thequestionnaires covered the following sectors.

• Customs;• Ports and maritime transport;• Rail transport;• Road transport;• Inland waterway transport;• Air transport;• Logistics services.

In consultation with and with support from the ASEAN Secretariat, the authors conducted ane-mail survey to collect data from relevant governmental and private agencies in the 10 membercountries. In each country, there would be one identified respondent for each of the questionnairesdelivered. These respondents were high-level policy makers in their respective ministries and wereidentified with the help of the ASEAN Secretariat. The individual national respondents for thelogistics services questionnaires were selected from high-ranking executives of each ASEANcountry’s national logistics association.

The questionnaires were then delivered after the second consultative meeting for the priorityintegration sectors held at theASEAN Secretariat in June 2006. That consultative meeting allowedthe authors to introduce the research to the various stakeholders and to request support in termsof data collection. Weekly follow-ups were conducted requesting responses to the questionnaires.Some national agencies did not respond, and the data are therefore not complete for all sectors.A description of the response rate is provided in Table 1. There is sufficient data, however, to

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

International Journal of Logistics: Research and Applications 363

Table 1. ASEAN questionnaire response rate.

Country Customs Ports Rail Road IWT∗ Air LSP∗∗

Brunei X N/A X XCambodia X X XIndonesia X XLao PDR X N/A X X XMalaysia X X XMyanmar X X X X X X XPhilippines X X X XSingapore X X N/A X N/A X XThailand X X X X X X XVietnam X X X X X X

∗Inland waterway transport.∗∗Logistics service providers.

analyse most of the underlying issues in logistics sector development in the ASEAN region. Theresults of this survey are described in the following section of this paper.

In the second step of the methodology, the survey findings were then presented in August2006 at the first logistics consultative meeting held in Vietnam in conjunction with the guidingprinciples that were identified, based on the survey’s gap analysis of the ASEAN logistics sector.This gap analysis enabled the identification of common weaknesses in the ASEAN logistics sectorthat needed to be addressed from a policy perspective. The survey results were then validated andthe proposed guiding principles endorsed by the meeting.

The third step of the methodology was a final validation meeting which was held in Indonesiaduring November 2006. The purpose of this meeting was to agree upon the specific issues thatneeded to be included in the guiding principles. These issues would then be negotiated betweenASEAN member countries for inclusion in the final logistics development policy roadmap. Thiswas finally endorsed by ASEAN in August 2007 (see Appendix 1).

4. Survey results

The survey revealed that the logistics capacity of ASEAN member countries varied widely,primarily because these countries are currently at different levels of economic development. Thelevel of economic development correlates strongly with the types of logistics services offered.The following is an analysis of the data gathered from the questionnaires distributed to all ASEANmember countries.

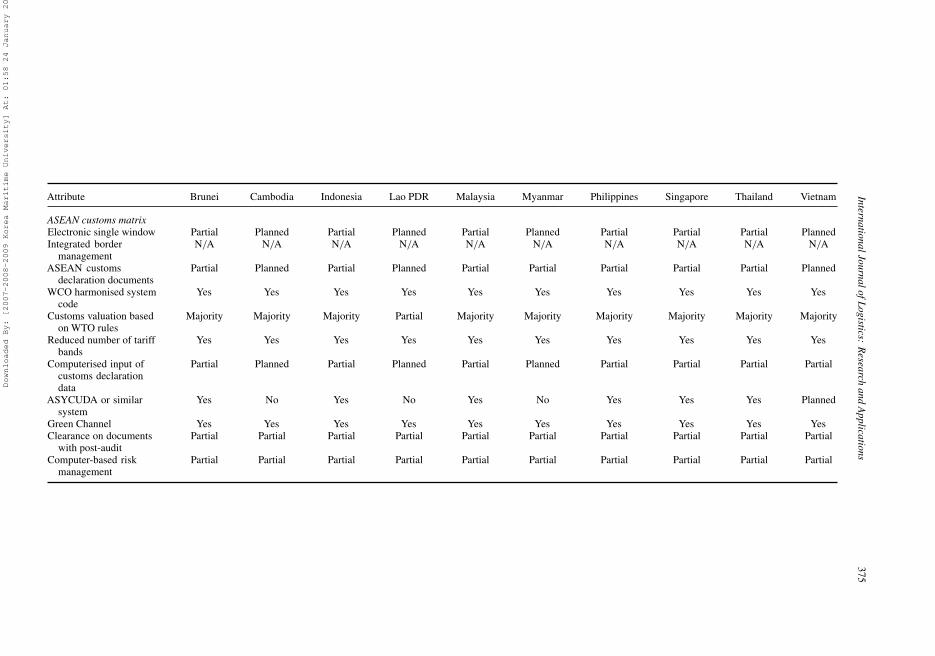

4.1. Customs

All ASEAN countries, except Lao PDR, are members of the World Trade Organisation (WTO).This means that that all ASEAN countries have to follow WTO-based rules for customs valuation.Strangely enough from the survey, it seemed that in practice not all WTO-based valuation rules areimplemented. Lao PDR is not a member of the WTO but has started to follow some WTO-basedrules in order to ease the negotiation of its entry into the WTO. The country is still lagging farbehind.

Most customs issues related to logistics, such as the ASEAN customs declaration form, havebeen only partially implemented or are at the planning stage for implementation. Full implemen-tation of this declaration form, the same declaration form for all member countries, will facilitatetrade among member countries even further. A significant step toward this single declaration form

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

364 R. Banomyong et al.

is the adoption by ASEAN member countries of the United Nations Conference on Trade andDevelopment (UNCTAD) key layout form, which standardises administrative documents.

The full implementation of the ASEAN electronic single window is important to the develop-ment of logistics services in the ASEAN region, but this implementation is still at the planningstage in a number of ASEAN countries. The ASEAN electronic single window has been partiallyimplemented in the selected ASEAN countries in 2006. The objective is to have implementationby 2008 with an extended grace period for the less developed member countries.

The implementation of computerised risk management and the clearance of documents withpost-audit need to be accelerated to facilitate the efficient and effective flow of goods acrossborders. Both activities are currently only partially implemented.

4.2. Ports and maritime transport

Ports are often the chief facilities linking an economic system with the international market andtherefore the main trade hubs. Based on the survey results, some ASEAN countries have no directservice with mainline carriers. This is partly because of their low container volume compared withthe container volume of other more developed ASEAN member countries. All ASEAN membercountries are served by shuttle feeder services to main regional hubs such as Singapore or HongKong. The ASEAN region has developed a system of shipping networks in which individualports are linked into intricate patterns of dependency in hub–feeder relationships as well as intoend-to-end shipping linkages that reflect the increasing dependency between national, regional,and global economies (Flemming and Hayuth 1994).

Singapore is the only country where the major port operates as a landlord port, the port authorityis separate from the operating organisation, and private sector management participates heavily.The concept of landlord ports exists in other ASEAN countries as well, although it is not as fullyimplemented as in Singapore. This concept was not applicable in Myanmar. This means that thereare strong differences in terms of how major ports in each ASEAN country operate.

Port ICT plays an important role in the integration of ports with their stakeholders, includingthe shipping lines, exporters, importers, and customs. However, not all national ports havecomputerised information systems enabling ports and port users to exchange information onthe status of cargo moving through the port or on regulatory procedures.

4.3. Rail transport

Rail usually offers an efficient interface between maritime and land transportation systems,especially since container shipping has become prevalent. Rail logistics are complex, however,requiring management of capacity, schedule, shipment characteristics, origin, and destinations.From the questionnaire results, rail transport can be considered to be one of the weakest links inthe ASEAN logistics infrastructure.

Singapore, Malaysia, and Thailand are linked by a metre-gauge network, which was linked in thepast to a metre-gauge system in Cambodia. The ASEAN rail freight system is characterised by:

• access charges that are high compared with road transport;• poor international routeing, leading to excessive transit times and poor service quality; and• lack of priority given in timetables, resulting in poor reliability.

The ASEAN rail transport system is heavily constrained because most of the railway systemin ASEAN is not double-tracked and there is no dedicated track for freight operations. Freightoperations are also hindered by the lack of a centralised train control system or any other type

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

International Journal of Logistics: Research and Applications 365

of advanced train control system that can monitor train movements with train identification andautomatic route setting.

Other limitations of the ASEAN railway system are that it cannot handle wagons that carry80 tons or more, or trains longer than 50 wagons. Based on the collected data, the implementationof the following rail transport components would support the development of theASEAN logisticssector.

• Double tracks and dedicated track for freight services.• Centralised or advanced train control systems.• Wagons that can carry more than 80 tons.• Trains that can operate with more than 50 wagons.

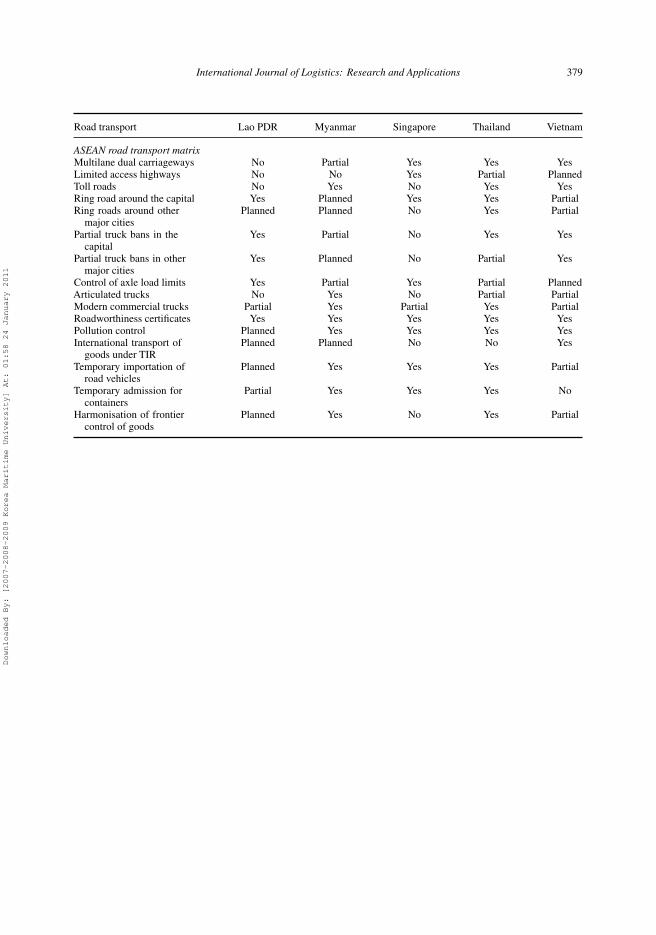

4.4. Road transport

Road is the main mode of transport in ASEAN, however, but there is still a need for harmonisationand standardisation among ASEAN countries. The problem is greatest for Cambodia, Lao PDR,Myanmar, and Vietnam, where road infrastructure lags behind the infrastructure of the othermembers of ASEAN. Multilane dual carriageways and limited-access highways are seen mostlyin the more developed economies of ASEAN. Urban congestion limits the efficient flow of goodsmoved by trucks, especially during peak hours, and toll roads and ring roads seen as part of thesolution to this, as are total or partial truck bans in large ASEAN cities.

Overloading of cargo is another issue that many ASEAN countries face. Axle load limits doexist, but enforcement can be lacking. Articulated trucks can be found in many ASEAN countriesbut they are not the majority of trucks moving cargo. Roadworthiness certificates are required inmost ASEAN countries, but enforcement is again often lacking.

4.5. Inland waterway transport

The inland water transport system in the ASEAN region serves largely domestic traffic. Somescheduled inland waterway services exist in ASEAN countries, especially countries that areriparian to the Mekong river. Linkages to the main seaports are not readily available, hinder-ing the development of inland waterway transport as a key component in the ASEAN logisticssystem.

When compared with maritime ports, inland waterway port facilities, equipment, and ICT sys-tems are poorly developed. There is a lack of container vessels and container-handling capability,although some river ports do handle containers on an ad hoc basis.

4.6. Air transport

A draft for the ASEAN Multilateral Agreement on the Full Liberalisation of Air Freight Serviceshas been developed, and the 11th ASEAN Transport Ministers’ meeting endorsed the imple-menting agreements to finalise this multilateral agreement in 2006. However, according to thesurvey, mostASEAN member countries have only partially opened up air freight services, whereasVietnam and Lao PDR have not even started the liberalisation process.

Pure freighter services are not common in ASEAN, especially in Cambodia, Lao PDR,Myanmar, and Vietnam, but many ASEAN countries would like to be considered as major airfreight hubs. This desire is reflected in the national air development policies of some membercountries. Being an air freight hub would also require on-site operations at airports and cargovillages. These facilities do not exist in some of the countries that aspire to be air freight hubs,

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

366 R. Banomyong et al.

such as Thailand and Vietnam. Cold storage, dangerous goods storage, and competitive groundhandling services are also important factors in the development of an air freight hub. Quick clear-ance and electronic data interchange (EDI) for cargo manifests are closely related to such servicesbut again are lacking in many countries. Large pallet scanners that facilitate the examination offreight shipped on aircrafts are also needed but are only available in major air transportation hubssuch as those in Thailand and Singapore.

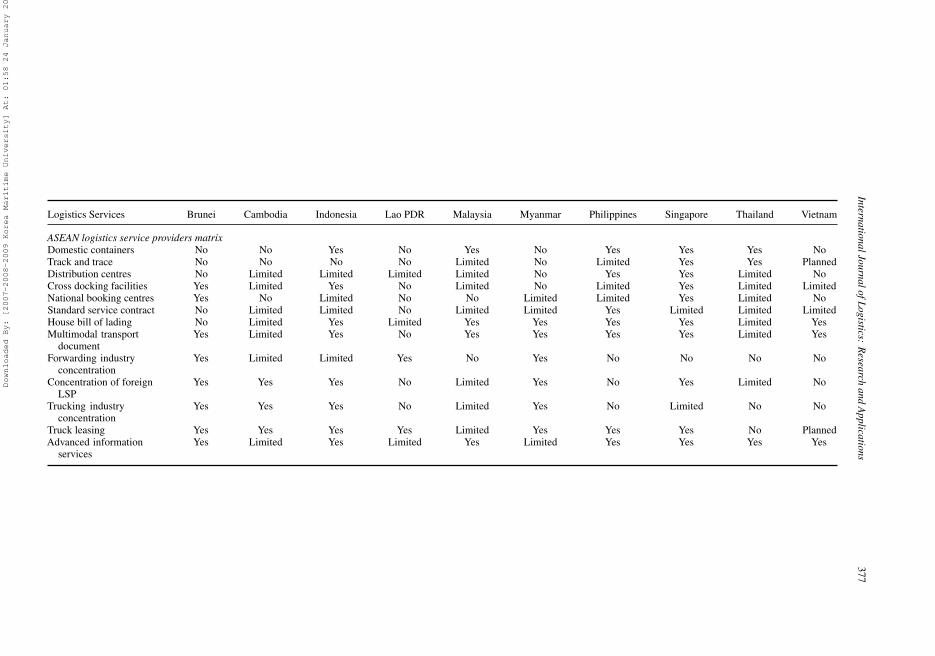

4.7. Logistics services sector

Logistics services available in ASEAN reflect the economic development achieved by individualmember countries, with more sophisticated services available in the more developed countries.Freight forwarders and logistics service providers in the more developedASEAN countries provideextensive logistical and supply chain services, whereas freight forwarders from less developedASEAN countries provide only basic logistics services such as trucking, warehousing, or customsbrokerage. Local customers have become more demanding in the more developed economies ofASEAN because of the multitude of global logistics services providers offering their services inthe region.

The usage of domestic containers for internal freight movement can play an important rolein the development of a country’s logistics system. Brunei, Cambodia, Lao PDR, Myanmar,and Vietnam, however, have no such domestic containers and domestic freight is being carriedin break-bulk form. Track and trace, distribution, and cross-docking centres are now consideredprerequisites for a modern logistics system, and the logistics service sector must be able to providethese activities to clients. Only service providers in Singapore and Thailand can provide trackand trace; however, service providers in Malaysia and the Philippines have partially implementedtrack and trace, whereas the other ASEAN member countries do not have this capability. Thismeans that the movement of freight in ASEAN is hampered by a lack of visibility in the majorityof member countries.

Distribution and cross-docking activities are more common, and many service providers inASEAN countries have started to partially offer these services. Foreign logistics service providersdominate the market in many ASEAN countries. This is understandable, because small serviceproviders are not capable of providing track-and-trace, distribution, and cross-docking servicesas well as service providers from more developed countries can. This is particularly true inCambodia, Lao PDR, Myanmar, and Vietnam. The local freight forwarding industry in eachASEAN member country is much less concentrated because most freight forwarding companiesare small and medium-sized enterprises. For trucking services, the picture is more balanced, withBrunei, Cambodia, Indonesia, and Myanmar having a concentrated trucking industry. Concentra-tion in itself is not a bad thing, as long as shippers and consignees can receive the best logisticsservices at the lowest price.

A critical point for logistics sector integration relates to standard service contracts. It is importantfor the logistics service industry to provide logistics services on the basis of standard servicecontracts, but this is not the case in ASEAN member countries, with the exception of Singapore.The use of standard service contracts is only partial in most ASEAN countries. A harmonisedstandard service contract would protect both clients and service providers.

5. ASEAN logistics cost assessment

The purpose of this section is to discuss ASEAN logistics related cost and how the existing levelof logistics-related cost can be a hindrance or a competitive tool. Until recently, logistics cost

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

International Journal of Logistics: Research and Applications 367

was a big unknown in the region. ASEAN shippers and consignees have been complaining aboutthe high cost of logistics and how long it took for exports and imports to be processed. ASEANgovernments were also unsure about their national logistics costs, but many felt that their nationallogistics costs were high compared with their gross domestic product (GDP).

When data were available, the range of national logistics costs per GDP has been estimated ataround 14% for Singapore (Rodrigues et al. 2005), 20% for Vietnam (Meyrick and Associates2006), and 24% for Thailand (Banomyong 2007) but all these estimates were based on differentmethodology and different base years. Although these ratios are just an aggregation of nationallogistics expenditure and cannot really reflect the logistics costs for a particular product or com-modity, they do indicate that logistics costs are relatively high for ASEAN countries other thanSingapore.

A number of studies conducted in ASEAN in relation to product and industry logistics costshave found that the range of export logistics cost based on an FOB basis was between 5% and25% for most products (ALMEC 2002, TNSC 2005, USAID 2006). The reason behind this widerange is related to the nature and value of the exported product. Higher-value products will havea lower ratio of logistics costs than lower-value goods.

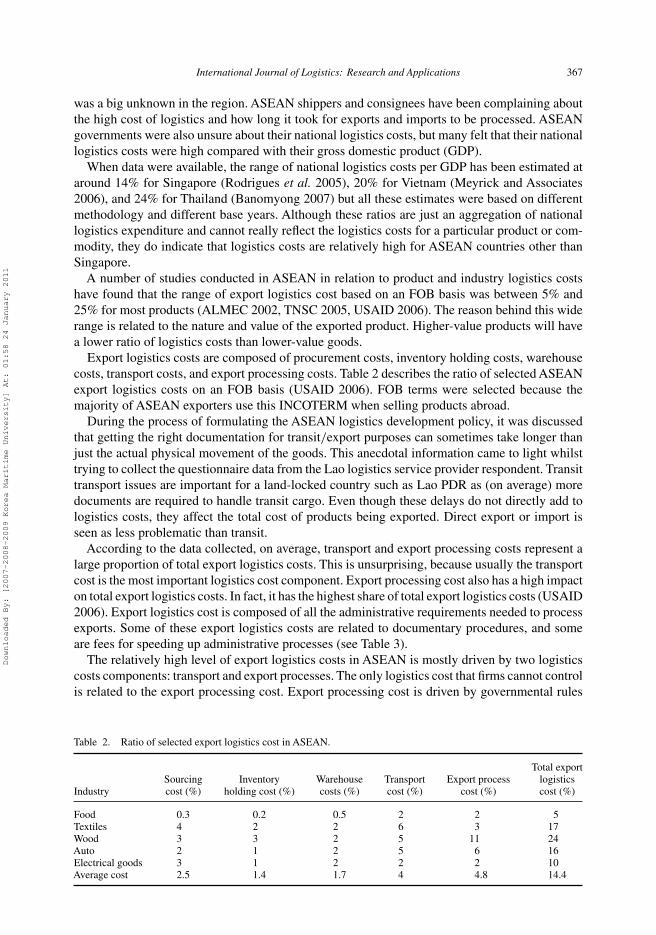

Export logistics costs are composed of procurement costs, inventory holding costs, warehousecosts, transport costs, and export processing costs. Table 2 describes the ratio of selected ASEANexport logistics costs on an FOB basis (USAID 2006). FOB terms were selected because themajority of ASEAN exporters use this INCOTERM when selling products abroad.

During the process of formulating the ASEAN logistics development policy, it was discussedthat getting the right documentation for transit/export purposes can sometimes take longer thanjust the actual physical movement of the goods. This anecdotal information came to light whilsttrying to collect the questionnaire data from the Lao logistics service provider respondent. Transittransport issues are important for a land-locked country such as Lao PDR as (on average) moredocuments are required to handle transit cargo. Even though these delays do not directly add tologistics costs, they affect the total cost of products being exported. Direct export or import isseen as less problematic than transit.

According to the data collected, on average, transport and export processing costs represent alarge proportion of total export logistics costs. This is unsurprising, because usually the transportcost is the most important logistics cost component. Export processing cost also has a high impacton total export logistics costs. In fact, it has the highest share of total export logistics costs (USAID2006). Export logistics cost is composed of all the administrative requirements needed to processexports. Some of these export logistics costs are related to documentary procedures, and someare fees for speeding up administrative processes (see Table 3).

The relatively high level of export logistics costs in ASEAN is mostly driven by two logisticscosts components: transport and export processes. The only logistics cost that firms cannot controlis related to the export processing cost. Export processing cost is driven by governmental rules

Table 2. Ratio of selected export logistics cost in ASEAN.

Total exportSourcing Inventory Warehouse Transport Export process logistics

Industry cost (%) holding cost (%) costs (%) cost (%) cost (%) cost (%)

Food 0.3 0.2 0.5 2 2 5Textiles 4 2 2 6 3 17Wood 3 3 2 5 11 24Auto 2 1 2 5 6 16Electrical goods 3 1 2 2 2 10Average cost 2.5 1.4 1.7 4 4.8 14.4

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

368 R. Banomyong et al.

Table 3. Total logistics cost components.

Category Share of total (%)

Procurement costs 17Inventory holding costs 10Warehousing costs 11Transport costs 28Export processing costs 34Export logistics costs 100

and regulations and is totally outside the control of firms’ own logistics systems. This is an areathat needs to be addressed by ASEAN and by all member countries individually.

Reducing export processing costs in all member countries must now become a top priorityfor ASEAN. Reducing export processing costs does not necessarily mean a loss of revenue forASEAN governments because facilitation measures can increase the volume of related exporttransactions. Reducing the export processing cost will not only reduce the total export logisticscost of ASEAN but also improve ASEAN competitiveness in the global market.

In terms of time requirement, it takes on average about 22 to 23 days for all documentaryprocesses to be completed for both export and import. This is another factor that affects thecompetitiveness of ASEAN exporters and importers both in terms of responsiveness capabilityand costs. As manufacturing systems become more global, delays in documentary procedure willimpact on the ability of ASEAN to become a single integrated production base. Each day lostbecause of administrative delays increases not only firms’ inventory holding costs but also reducesASEAN trade (Djankov et al. 2006).

6. Formulation of the regional logistics development policy

The ASEAN logistics sector is characterised by relative high cost, long lead time for export andimport processes and an uneven level of logistics sector development across member countries.Customs facilitation issues seemed to be relatively well co-ordinated within ASEAN even thoughLao PDR is not yet required to follow WTO-based customs valuation rules.

The ports and maritime sector are probably the most developed logistics sub-sector in theregion, whereas rail and inland waterway remain relatively underdeveloped. Road transport needsan expanded regional institutional framework that can help support international road transportbetween member countries. Air transport should have become liberalised since 2006 but imple-mentation has not been executed. The regional logistics industry is quite competitive but foreignservice providers are now starting to offer more advanced logistical services.

The proposed regional logistics development policy should address all the strengths and weak-nesses identified from the survey findings. This regional logistics development framework startswith two agreed upon ASEAN basic development objectives that help to determine the prioritiesin the development policy.

1. Create an ASEAN single market by 2015 by strengthening ASEAN economic integrationthrough the liberalisation and facilitation measures in logistics services; and

2. Support the establishment and enhance the competitiveness of an ASEAN production basethrough the creation of an integrated ASEAN logistics environment.

These objectives refer back to the ASEAN vision statement and define the role of logisticsas playing a supporting role for trade development and integration. To reach these objectives,stakeholders based on the study findings have recommended that ASEAN member countries take

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

International Journal of Logistics: Research and Applications 369

action in six major policy areas:

• Encourage the integration of ASEAN national logistics systems, by improving communicationat the regional level to identify actions in the logistics sector to support and facilitate trade flowsbetween ASEAN countries.

• Encourage the progressive liberalisation of logistics service providers, to enable themto respond better to the opportunities available for ASEAN integration and increasingcompetitiveness.

• Increase trade, logistics and investment facilitation, to identify the means needed to improvetransport logistics facilities and the priorities for investment.

• Build ASEAN logistics capacity, by encouraging human resource development in the sector andan environment conducive to use of best practice in the sector, especially for small and mediumenterprises.

• Promote ASEAN logistics service providers, by identifying them and providing channels fortheir greater participation in the sector.

• Promote multimodal transport capacity, especially for containerised transport.

These six major policy areas cover the four components of theASEAN regional logistics systemand the performance issues identified above, while building on the capacity of existing ASEANlogistics service providers.

7. Conclusions

The six major policy areas and the roadmap for the integration of the ASEAN logistics sectorwere finally endorsed by ASEAN in August 2007. This paper has described the experience ofASEAN in formulating and adopting its regional logistics policy.

The proposed policies and integration roadmap were derived from survey results from sevenlogistics sub-sectors: customs; ports, rail, road, inland waterway, air and logistics serviceproviders. A gap analysis was utilised to identify strong and weak areas in the ASEAN logisticssystem.

Even with support from ASEAN, the main limitation of the methodology was that the authorswere not able to gather data from all member countries, even though all member countries agreedto cooperate in this formulation policy. The second limitation was that all member countries agreedvery quickly on facilitation measures but were much more reluctant to discuss logistics serviceliberalisation issues. This is reflected in the actual wording of the roadmap where it is requestedthat ASEAN member countries shall endeavour to achieve substantial liberalisation of logisticsservices.

Logistics service liberalisation is a difficult topic as many ASEAN member countries are quiteafraid to open up their logistics markets. However, gradual liberalisation within ASEAN is neededbefore the sector is forced to open under the WTO General Agreement on Trade and Services.

The authors hope that this methodology could be replicated in other regions of the world in needof regional logistics development policy. The methodology provides a comprehensive comparativeassessment of the existing regional logistics sector. Based on this first-level assessment, gaps areidentified and policy guiding principles are derived that must be agreed upon for further detaileddevelopment.

References

ALMEC, 2002. ASEAN maritime development study. Jakarta, Indonesia: ASEAN Secretariat.Arvis, J.F., Mustra, M.A., Panzer, J., Ojala, L., and Naula, T. 2007. Connecting to compete-trade logistics in the global

economy. Washington: The World Bank.

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

370 R. Banomyong et al.

Asian Development Bank, 2007. Logistics development study of the greater Mekong sub-region north south economiccorridor. Manilla, Philippines: Asian Development Bank.

Banomyong, R., 2004. Assessing import channels for Lao PDR. Asia Pacific Journal of Marketing & Logistics, 16 (2),62–81.

Banomyong, R., 2007. Thammasat logistics research papers.Vol. 3. Centre for Logistics Research, Thammasat University,Bangkok, Thailand.

Banomyong, R., Wasusri, T. and Kritchanchai, D., 2006. Implementing the 2010 ASEAN-China FTA: a Thailogistics perspective. Proceedings of the 11th annual international symposium on logistics (ISL), Beijing, China,98–104.

Djankov, S., Freund, C. and Pham, C.S., 2006. Trading on time. Washington: The World Bank.Flemming, D.K. and Hayuth, Y., 1994. Spatial characteristics of transportation hubs: centrality and intermediacy. Journal

of Transport Geography, 2 (1), 3–18.Grainger, A., 2007. Government actors in international supply chain operations: assessing requirements for skills

and capabilities. Logistics research network conference proceedings 2007, 5–7 September 2007, Hull, England,293–298.

Grant, D.B. et al., 2006. Fundamentals of logistics management. European Edition. Berkshire, UK: McGraw-Hill.Meyrick and Associates, 2006. Vietnam multimodal transport regulatory review. Vietnam Ministry of Transport and The

World Bank, Final Report, Hanoi, Vietnam: The World Bank.Price, P.M., 2006. A model for logistics management in a post-Soviet central Asian transitional economy. Journal of

Business Logistics, 27 (2), 301–331.Rodrigues, A.M., Bowersox, D.J. and Calantone, R.J., 2005. Estimation of global and national logistics expenditures:

2002 data update. Journal of Business Logistics, 26 (2), 1–16.TNSC, 2005. A survey of logistics export cost. Bangkok, Thailand: Thai National Shippers’ Council.USAID, 2006. Towards a roadmap for integration of the ASEAN logistics sector. Washington, USA: United State Agency

for International Development.

Appendix 1. Roadmap for the integration of ASEAN logistics

(As endorsed by the 39th AEM, 24 August 2007, Makati city, the Philippines).

I. Objectives

The objectives of this initiative are to:

• create an ASEAN single market by 2015 by strengthening ASEAN economic integration through liberalisation andfacilitation measures in the area of logistics services; and

• support the establishment and enhance the competitiveness of an ASEAN production base through the creation ofan integrated ASEAN logistics environment.

II. Measures

This roadmap provides concrete actions that ASEAN member countries shall pursue to achieve greater and significantintegration of logistics services in ASEAN, through progressive implementation of the measures, which includethe liberalisation of logistics services, enhancing competitiveness of ASEAN logistics services providers throughtrade and logistics services facilitation, expanding capability of ASEAN logistics service providers, human resourcedevelopment, and enhancing multi-modal transport infrastructure and investment.

III. Coverage

The scope of the measures will cover freight logistics and related activities.The implementation of the specific measures shall be subject to the relevant national laws and regulations.

IV. Coordination

The Senior Economic Officials Meeting (SEOM) shall be the overall coordinating and monitoring body in theimplementation of this roadmap, with Vietnam as the country coordinator.

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

International Journal of Logistics: Research and Applications 371

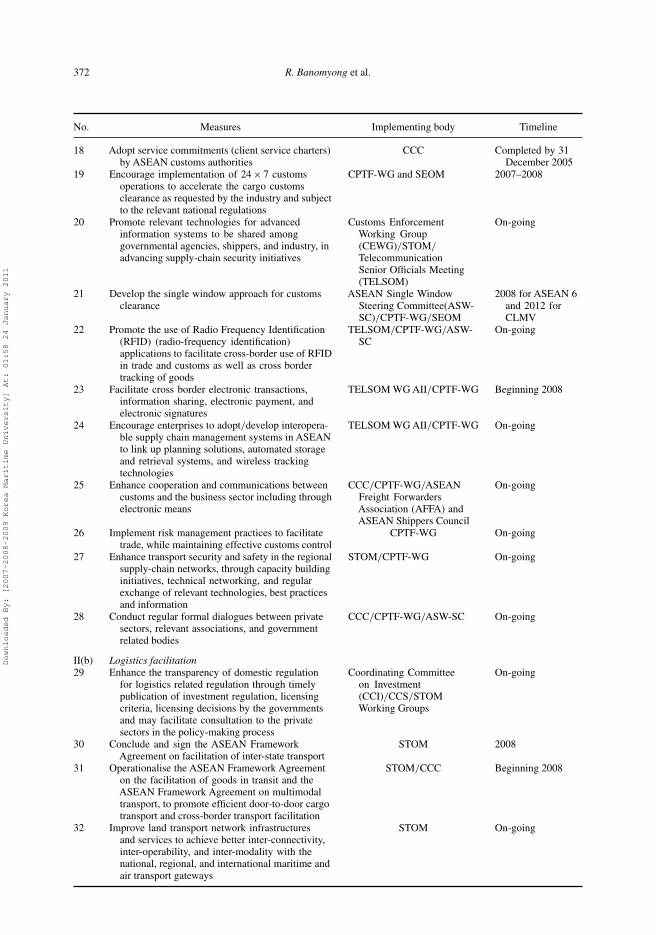

No. Measures Implementing body Timeline

Specific issuesI Member country shall endeavour to achieve substantial liberalisation of logistics services in the

following sectors∗1 Maritime cargo handling services CPC 741 Coordinating committee

on services (CCS)2013

2 Storage and warehousing services CPC 742 CCS 20133 Freight transport agency services CPC 748 CCS 20134 Other auxiliary services† CPC 749 CCS 20135 Courier services‡ CPC 7512 CCS 20136 Packaging services CPC 876 CCS 20137 Customs clearance services§ CCS and Customs Coor-

dinating Committee(CCC)

2013

Maritime transport services8 International freight transportation

excluding CabotageCPC 7212 CCS 2013

Air freight services9 Implement ASEAN Multilateral

Agreement of the Full Lib-eralisation of Air FreightServices

Senior Transport OfficialsMeeting (STOM)

December 2008

Rail freight transport services10 International rail freight transport services CPC 7112 CCS and relevant STOM

Working GroupsBeginning 2008

Road freight transport services11 International road freight transport services CPC 7213 CCS and relevant STOM

Working GroupsBeginning 2008

II Enhancing competitiveness of ASEAN logistics services providers through trade (including documentationsimplification) and logistics (transport) facilitation

II(a) Trade and customs facilitation12 Implement provisions in the WTO Customs coordinating committee On-going

agreement on customs valuation (CCC)/Customs procedures and tradefacilitation working group (CPTF-WG)

13 Implement the WCO immediate releaseguidelines and review, as appropriate,the de minimus levels (value thresholds)for express delivery of air shipments andimplement/introduce EDI to speed up customsclearance

CCC/CPTF-WG On-going

14 Promote the implementation of the WCOframework of standards to secure and facilitateglobal trade

CCC/CPTF-WG On-going

15 Identify suitable standards to secure theinteroperability and interconnectivity infacilitating trade within customs jurisdiction,including those of ICT

CPTF-WG 2007—2009

16 Enact domestic legislation to providelegal recognition of electronicdocuments/transactions

TELSOM/CPTF-WG 2007—2008

17 Encourage application of standardised trade dataand documents for trade facilitation throughthe adoption of international standards likeWCO data model, UNTDED – United NationsTrade Data Elements Directory (UNTDED),UN-eDocs and the electronic submissionof trade data and documents for customsclearance

CPTF-WG and SEOM 2008 for ASEAN-6and 2012 forCLMV

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

372 R. Banomyong et al.

No. Measures Implementing body Timeline

18 Adopt service commitments (client service charters)by ASEAN customs authorities

CCC Completed by 31December 2005

19 Encourage implementation of 24 × 7 customsoperations to accelerate the cargo customsclearance as requested by the industry and subjectto the relevant national regulations

CPTF-WG and SEOM 2007–2008

20 Promote relevant technologies for advancedinformation systems to be shared amonggovernmental agencies, shippers, and industry, inadvancing supply-chain security initiatives

Customs EnforcementWorking Group(CEWG)/STOM/

TelecommunicationSenior Officials Meeting(TELSOM)

On-going

21 Develop the single window approach for customsclearance

ASEAN Single WindowSteering Committee(ASW-SC)/CPTF-WG/SEOM

2008 for ASEAN 6and 2012 forCLMV

22 Promote the use of Radio Frequency Identification(RFID) (radio-frequency identification)applications to facilitate cross-border use of RFIDin trade and customs as well as cross bordertracking of goods

TELSOM/CPTF-WG/ASW-SC

On-going

23 Facilitate cross border electronic transactions,information sharing, electronic payment, andelectronic signatures

TELSOM WG AII/CPTF-WG Beginning 2008

24 Encourage enterprises to adopt/develop interopera-ble supply chain management systems in ASEANto link up planning solutions, automated storageand retrieval systems, and wireless trackingtechnologies

TELSOM WG AII/CPTF-WG On-going

25 Enhance cooperation and communications betweencustoms and the business sector including throughelectronic means

CCC/CPTF-WG/ASEANFreight ForwardersAssociation (AFFA) andASEAN Shippers Council

On-going

26 Implement risk management practices to facilitatetrade, while maintaining effective customs control

CPTF-WG On-going

27 Enhance transport security and safety in the regionalsupply-chain networks, through capacity buildinginitiatives, technical networking, and regularexchange of relevant technologies, best practicesand information

STOM/CPTF-WG On-going

28 Conduct regular formal dialogues between privatesectors, relevant associations, and governmentrelated bodies

CCC/CPTF-WG/ASW-SC On-going

II(b) Logistics facilitation29 Enhance the transparency of domestic regulation

for logistics related regulation through timelypublication of investment regulation, licensingcriteria, licensing decisions by the governmentsand may facilitate consultation to the privatesectors in the policy-making process

Coordinating Committeeon Investment(CCI)/CCS/STOMWorking Groups

On-going

30 Conclude and sign the ASEAN FrameworkAgreement on facilitation of inter-state transport

STOM 2008

31 Operationalise the ASEAN Framework Agreementon the facilitation of goods in transit and theASEAN Framework Agreement on multimodaltransport, to promote efficient door-to-door cargotransport and cross-border transport facilitation

STOM/CCC Beginning 2008

32 Improve land transport network infrastructuresand services to achieve better inter-connectivity,inter-operability, and inter-modality with thenational, regional, and international maritime andair transport gateways

STOM On-going

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

International Journal of Logistics: Research and Applications 373

No. Measures Implementing body Timeline

33 Strengthen intra-ASEAN maritime and shippingtransport services

STOM On-going

34 Establish enabling and conducive policyenvironment for increased private sectorinvolvement and/or public–private partnershipsin the development of transport logisticsinfrastructure and the provision and operationof transport logistics facilities and services

STOM On-going

35 Identify and develop other mechanisms to furtherfacilitate the movement of natural personsinvolving logistics services

CCS On-going

III Expanding capability of ASEAN logistics service providers36 Adopt best practices in the provision of logistics

services and support the development of smalland medium enterprises (SMEs) in the sector,including the formation of SME networks

SEOM/STOM Beginning 2007

37 Promote regional cooperation to assist CLMVcountries especially least developed countries

STOM Beginning 2007

38 Develop and update an ASEAN database onlogistics services providers with a view toenhance the development of networkingactivities

ASEAN Secretariat withinputs from STOM andAFFA

Beginning 2007

IV Hyman resource development39 Develop and upgrade skills and capacity building

through joint trainings and workshopsSTOM, CCCAFFA and other

related bodiesBeginning 2007

40 Encourage the development of national skillscertification system for logistics serviceproviders

AFFA and other related bodies On-going

41 Encourage the development of an ASEANcommon core curriculum for logisticsmanagement

AFFA and other related bodies On-going

42 Encourage the establishment of national/sub-regional centre of excellence (trainingcentre)

STOM and AFFA Beginning 2007

V Enhance multimodal transport infrastructure and investment43 Identify and develop the ASEAN transport

logistics corridor network and formulatethe necessary infrastructure developmentrequirements, to support the improvementof inland transport network infrastructure,the inter-modal linkages between connectingmodes of transport, to match inland withmaritime transport infrastructure and toimprove connectivity between ASEANlogistics gateways, among others

STOM Beginning 2007

44 Promote the usage of trade terms and practicesrelated to multimodal transport, includingthe INCOTERMS (International CommercialTerms)

STOM/AFFA On-going

∗The individual schedule of specific commitments shall be negotiated by the CCS and relevant negotiating bodies. Flexibility to be providedfor some member countries in implementation using the ASEAN minus X formula.†Include the following activities: bill auditing; freight brokerage services; freight inspection, weighing and sampling services; freightreceiving and acceptance services; and transportation document preparation services. These services are provided on behalf of cargoowners.‡‘Express Delivery Services’ will be included in the list of services to be liberalised. These services are recognised to be distinct andseparate from postal services.§‘Customs clearance services’ (alternatively ‘customs house brokers’ services’) means activities consisting in carrying out on behalf ofanother party customs formalities concerning import, export or through transport of cargoes, whether this service is the main activity ofthe service provider or a usual complement of its main activity.

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

374R

.Banom

yongetal.

Appendix 2. Detailed questionnaire results.

Attribute Brunei Cambodia Lao PDR Malaysia Myanmar Philippines Singapore Thailand Vietnam

ASEAN air transport matrixLiberalised air freight services Yes Partial No Partial Partial Partial Yes Partial PlannedPure freighter services Planned Partial No Yes No Partial Yes No NoHub for air freight Planned No No Yes No No Yes Yes PlannedOn-airport operations Partial Yes No Yes No Yes Yes Partial PartialCargo village Planned Partial Partial Yes No Yes Yes No YesOn-airport cold storage Partial Yes Planned Yes No Partial Yes Yes YesOn-airport storage for

dangerous goodsPlanned Yes Yes Yes No Partial Yes Yes Yes

Competitive ground handlingservices

Planned No No Partial No Partial Yes Partial Partial

Large pallet scanners Partial No No Yes No Partial Yes Yes PlannedQuick clearance Planned Yes Yes Partial Planned Partial Yes Yes NoEDI for cargo manifest Partial No No Yes No Partial Yes Yes Planned

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

InternationalJournalofLogistics:

Research

andA

pplications375

Attribute Brunei Cambodia Indonesia Lao PDR Malaysia Myanmar Philippines Singapore Thailand Vietnam

ASEAN customs matrixElectronic single window Partial Planned Partial Planned Partial Planned Partial Partial Partial PlannedIntegrated border

managementN/A N/A N/A N/A N/A N/A N/A N/A N/A N/A

ASEAN customsdeclaration documents

Partial Planned Partial Planned Partial Partial Partial Partial Partial Planned

WCO harmonised systemcode

Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes

Customs valuation basedon WTO rules

Majority Majority Majority Partial Majority Majority Majority Majority Majority Majority

Reduced number of tariffbands

Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes

Computerised input ofcustoms declarationdata

Partial Planned Partial Planned Partial Planned Partial Partial Partial Partial

ASYCUDA or similarsystem

Yes No Yes No Yes No Yes Yes Yes Planned

Green Channel Yes Yes Yes Yes Yes Yes Yes Yes Yes YesClearance on documents

with post-auditPartial Partial Partial Partial Partial Partial Partial Partial Partial Partial

Computer-based riskmanagement

Partial Partial Partial Partial Partial Partial Partial Partial Partial Partial

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

376R

.Banom

yongetal.

Brunei Lao PDR Myanmar Singapore Thailand Vietnam

ASEAN inland waterway transport matrixScheduled service N/A Yes Yes N/A No PlannedLinks to main seaport N/A No Partial N/A Partial NoContainer vessel for IWT N/A No Partial N/A Planned PlannedLandlord port N/A No Partial N/A No NoContainer terminal N/A Partial No N/A Partial PartialPortnet or equivalent N/A No No N/A No PartialDirect debit payment system N/A No No N/A No YesComputerised terminal control system N/A No No N/A No PartialAutomated gate entry N/A No No N/A No NoOff-dock yard N/A No No N/A No PartialBonded distribution facility N/A No No N/A No PlannedShunting lines to IWT terminal N/A No No N/A No No

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

InternationalJournalofLogistics:

Research

andA

pplications377

Logistics Services Brunei Cambodia Indonesia Lao PDR Malaysia Myanmar Philippines Singapore Thailand Vietnam

ASEAN logistics service providers matrixDomestic containers No No Yes No Yes No Yes Yes Yes NoTrack and trace No No No No Limited No Limited Yes Yes PlannedDistribution centres No Limited Limited Limited Limited No Yes Yes Limited NoCross docking facilities Yes Limited Yes No Limited No Limited Yes Limited LimitedNational booking centres Yes No Limited No No Limited Limited Yes Limited NoStandard service contract No Limited Limited No Limited Limited Yes Limited Limited LimitedHouse bill of lading No Limited Yes Limited Yes Yes Yes Yes Limited YesMultimodal transport

documentYes Limited Yes No Yes Yes Yes Yes Limited Yes

Forwarding industryconcentration

Yes Limited Limited Yes No Yes No No No No

Concentration of foreignLSP

Yes Yes Yes No Limited Yes No Yes Limited No

Trucking industryconcentration

Yes Yes Yes No Limited Yes No Limited No No

Truck leasing Yes Yes Yes Yes Limited Yes Yes Yes No PlannedAdvanced information

servicesYes Limited Yes Limited Yes Limited Yes Yes Yes Yes

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

378 R. Banomyong et al.

Lao PDR Myanmar Singapore Thailand Vietnam

ASEAN ports and maritime transport matrixDirect mainline services N/A No Yes Yes YesFeeder services N/A Yes Yes Yes YesRegional services (>1500 TEU) N/A No Yes Yes YesLandlord port N/A No Yes Partial PartialContainer terminal concessions N/A No No Yes YesDay of the week shipping services N/A No Yes No YesPortnet or equivalent N/A Planned Yes Yes YesPilot free entry for large vessels N/A No Partial No NoPost Panamax gantry cranes N/A No Yes Yes NoComputerised terminal control

systemN/A Planned Yes Yes Yes

Automated gate entry N/A No Yes Planned NoOff-dock container yard N/A Yes No Yes YesBonded distribution facilities N/A No Yes Yes YesFull truck scanners N/A Yes Yes Partial NoShunting lines to port N/A No No Yes No

Lao PDR Malaysia Myanmar Philippines Singapore Thailand Vietnam

ASEAN rail transport matrixUnified gauge Planned Single gauge Single gauge N/A Yes NoStandard gauge No No No N/A No NoDouble track No Partial No N/A No NoDedicated track for freight

servicesPlanned No No N/A No No

Centralised train control No No No N/A No PlannedAdvanced train control No No No N/A No PlannedElectrified lines No No No N/A No PlannedBogie wagons No Yes N/A N/A Yes YesHeavy load wagons Planned No N/A N/A No NoLong train No No N/A N/A No NoModern locomotives Planned Partial N/A N/A Partial PartialUnit container train

operationsPlanned Yes No N/A N/A Yes Yes

24 h freight terminaloperations

No Yes N/A N/A Yes Yes

Privately owned railwagons

Planned No N/A N/A Yes No

Private freight trainoperations

Planned Yes No N/A N/A Yes Partial

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011

International Journal of Logistics: Research and Applications 379

Road transport Lao PDR Myanmar Singapore Thailand Vietnam

ASEAN road transport matrixMultilane dual carriageways No Partial Yes Yes YesLimited access highways No No Yes Partial PlannedToll roads No Yes No Yes YesRing road around the capital Yes Planned Yes Yes PartialRing roads around other

major citiesPlanned Planned No Yes Partial

Partial truck bans in thecapital

Yes Partial No Yes Yes

Partial truck bans in othermajor cities

Yes Planned No Partial Yes

Control of axle load limits Yes Partial Yes Partial PlannedArticulated trucks No Yes No Partial PartialModern commercial trucks Partial Yes Partial Yes PartialRoadworthiness certificates Yes Yes Yes Yes YesPollution control Planned Yes Yes Yes YesInternational transport of

goods under TIRPlanned Planned No No Yes

Temporary importation ofroad vehicles

Planned Yes Yes Yes Partial

Temporary admission forcontainers

Partial Yes Yes Yes No

Harmonisation of frontiercontrol of goods

Planned Yes No Yes Partial

Downloaded By: [2007-2008-2009 Korea Maritime University] At: 01:58 24 January 2011