6 - 1 ©2003 prentice hall business publishing, essentials of auditing 1/e, arens/elder/beasley...

TRANSCRIPT

6 - 1©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Audit Evidence

Chapter 6

6 - 2©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Learning Objective 1

Contrast audit evidence

with evidence used by

other professions.

6 - 3©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Nature of Evidence

The use of evidence isnot unique to auditors.

Evidence is also usedby scientists, lawyers,

and historians.

6 - 4©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Learning Objective 2

Identify the four audit evidence

decisions that are needed to

create an audit program.

6 - 5©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Audit Evidence Decisions

1. Which audit procedures to use

2. What sample size to select for a given procedure

3. Which items to select from the population

4. When to perform the procedures

6 - 6©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Audit Program

It includes a list of the audit proceduresthe auditor considers necessary.

Most auditors use computers to facilitatethe preparation of audit programs.

6 - 7©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Learning Objective 3

Specify the characteristics

that determine the

persuasiveness

of evidence.

6 - 8©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Persuasiveness of Evidence

Competence

Sufficiency

Combined effect

Persuasiveness and cost

6 - 9©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Competence

Relevance

Independence of provider

Effectiveness of internal controls

Auditor’s direct knowledge

Qualifications of individuals

Degree of objectivity

Timeliness

6 - 10©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Learning Objective 4

Identify and apply the

seven types of evidence

used in auditing.

6 - 11©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

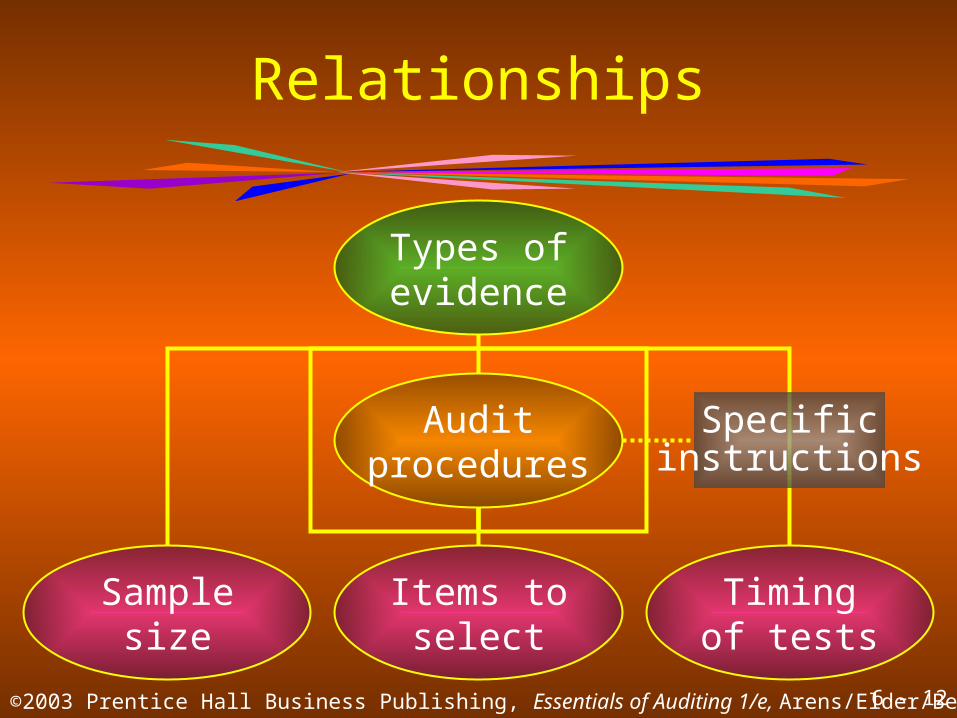

Relationships

Auditingstandards

Qualificationsand conduct

ReportingEvidence

accumulation

Types ofevidence

Broadguidelines

Broadcategories

6 - 12©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Relationships

Types ofevidence

Auditprocedures

Samplesize

Timingof tests

Items toselect

Specificinstructions

6 - 13©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

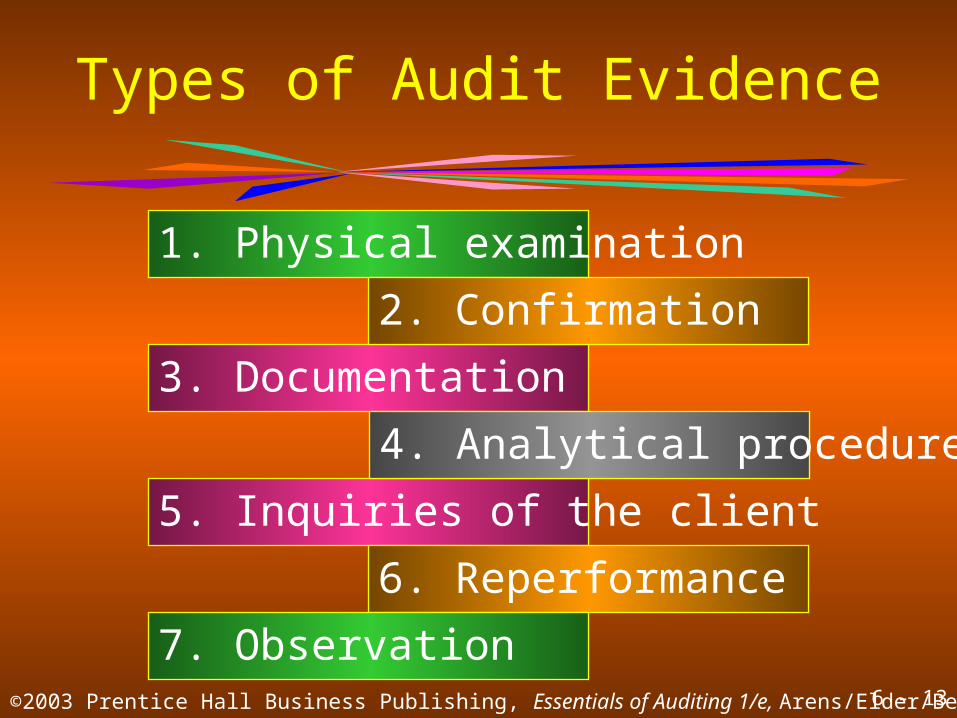

Types of Audit Evidence

1. Physical examination

3. Documentation

5. Inquiries of the client

6. Reperformance

2. Confirmation

4. Analytical procedures

7. Observation

6 - 14©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

InformationOften Confirmed

Information SourceAssetsCash in bank BankAccounts receivable CustomerNotes receivable MakerOwned inventory out on consignment ConsigneeInventory held in public warehouses WarehouseCash surrender value of life insurance Insurance co.

6 - 15©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

InformationOften Confirmed

Information SourceLiabilitiesAccounts payable CreditorNotes payable LenderAdvances from customers CustomerMortgages payable MortgagorBonds payable Bondholder

6 - 16©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

InformationOften Confirmed

Information SourceOwners’ EquityShares outstanding Registrar and

transfer agent

6 - 17©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

InformationOften Confirmed

Information SourceOther InformationInsurance coverage Insurance companyContingent liabilities Bank, lender, and

client’s counselBond indenture agreements BondholderCollateral held by creditors Creditor

6 - 18©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Criteria to DetermineCompetence

Type ofevidence

Independenceof provider

Effectiveness ofclient’s

internal controls

Auditor’sdirect

knowledge

Qualificationsof provider

Objectivityof evidence

6 - 19©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Terms and Types of Evidence

Terms Types of Evidence

Examine Documentation

Scan Analytical procedures

Read Documentation

Analytical proceduresCompute

Recompute Reperformance

Foot Reperformance

6 - 20©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Terms and Types of Evidence

Terms Types of Evidence

Trace Documentation

Compare Documentation

Count Physical examination

ObservationObserve

Inquire Inquiries of client

Vouch Documentation

6 - 21©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Learning Objective 5

Understand the purposes

of audit documentation.

6 - 22©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Audit Documentation

Purposes of audit documentation

Ownership of audit files

Confidentiality of audit files

6 - 23©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Learning Objective 6

Prepare organized

audit documentation.

6 - 24©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Audit File Contentsand Organization

Robinson AssociatesTrial Balance

12/31/2003

Cash $165,237Accounts Receivable 275,050Prepaid Insurance 37,795Interest Receivable 20,493

FinancialStatements andAudit Report

WorkingTrial Balance

AdjustingJournal Entries

ContingentLiabilities

Operations

Liabilities and Equity

Assets

AnalyticalProcedures

Test of Controls& Substantive

TOT

InternalControl

GeneralInformation

AuditPrograms

PermanentFiles

6 - 25©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Permanent Files

These files are intended to containdata of a historical or continuing

nature pertinent to the current audit.

6 - 26©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

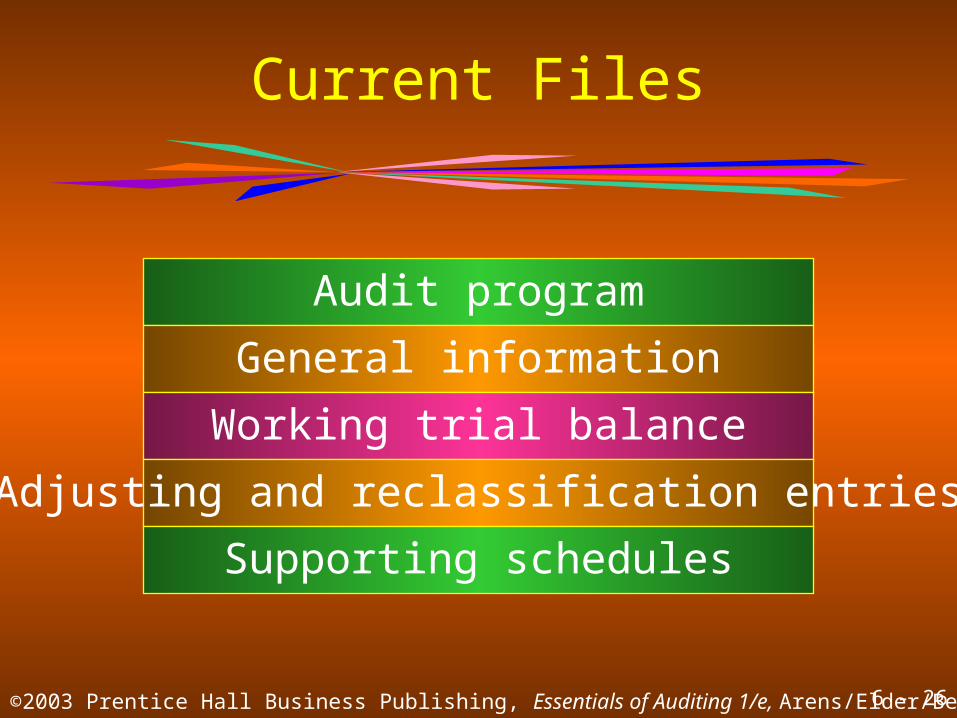

Current Files

Audit program

General information

Working trial balance

Adjusting and reclassification entries

Supporting schedules

6 - 27©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Learning Objective 7

Describe how e-commerce

affects audit evidence and

audit documentation.

6 - 28©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Effect of E-commerce

Audit evidence is increasingly in electronic form.

Auditors use computers to readand examine evidence.

Software programs are typically Windows-based.

6 - 29©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

Summary of Audit Documentation

Audit documentation is an essentialpart of every audit.

Audit documentation provides a record of the evidence accumulated and the result of the tests.

CPA firms make sure that audit documentationis properly prepared and is appropriate.

6 - 30©2003 Prentice Hall Business Publishing, Essentials of Auditing 1/e, Arens/Elder/Beasley

End of Chapter 6