56 capital revenue

TRANSCRIPT

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 1/17

Capital VS RevenueCapital VS Revenue

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 2/17

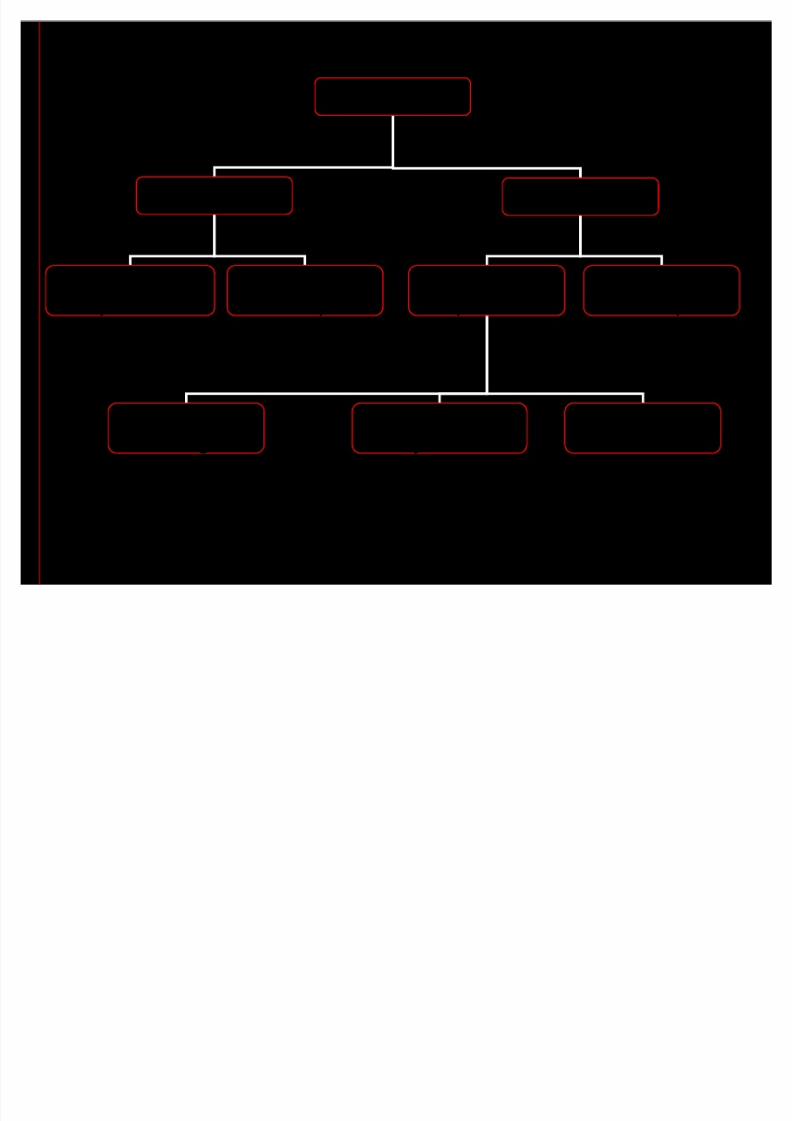

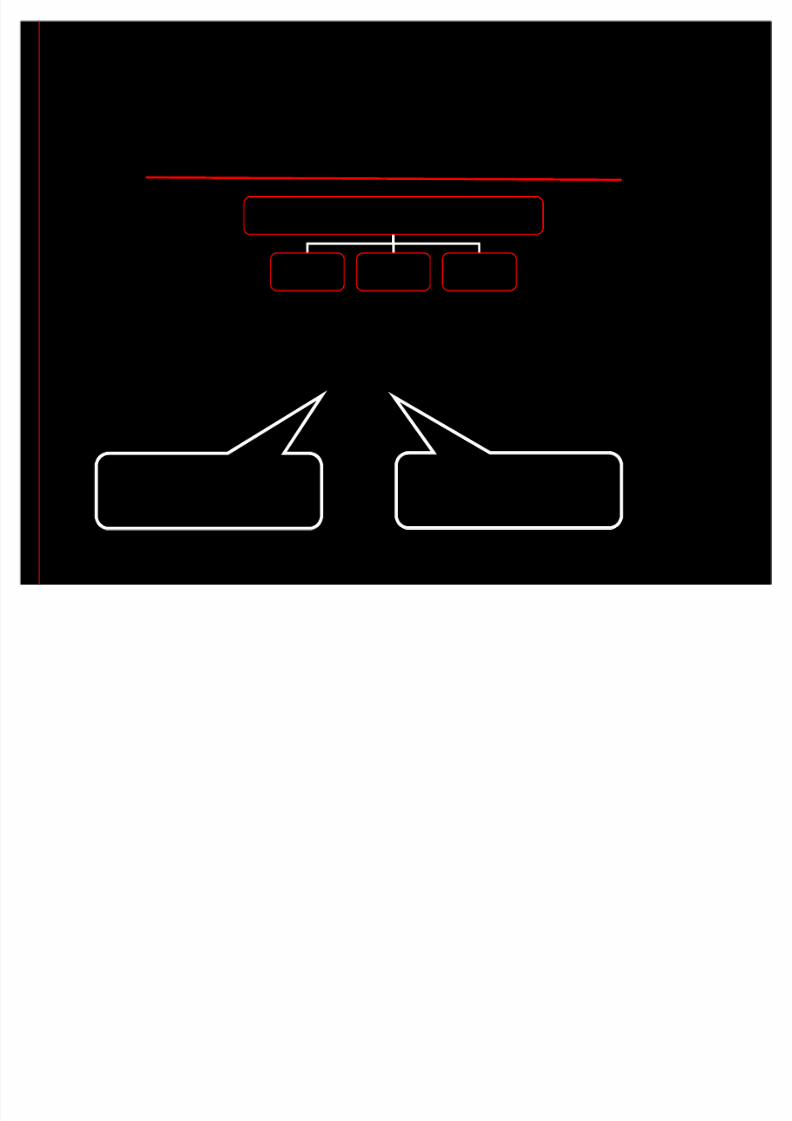

Tr ansactions

Capital Revenue

CapitalExpenditur e

CapitalReceipts

RevenueExpenditur e

RevenueReceipts

Wholly Curr entCharge

Par tly Curr ent &Par tly Deferr ed

WhollyDeferr ed

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 3/17

Capital Expenditur e

E.L. Kohler: Capital Expenditure is anexpenditur e intended to benefit future

period in contr ast to a r evenue expenditur e

which benefits a current period .

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 4/17

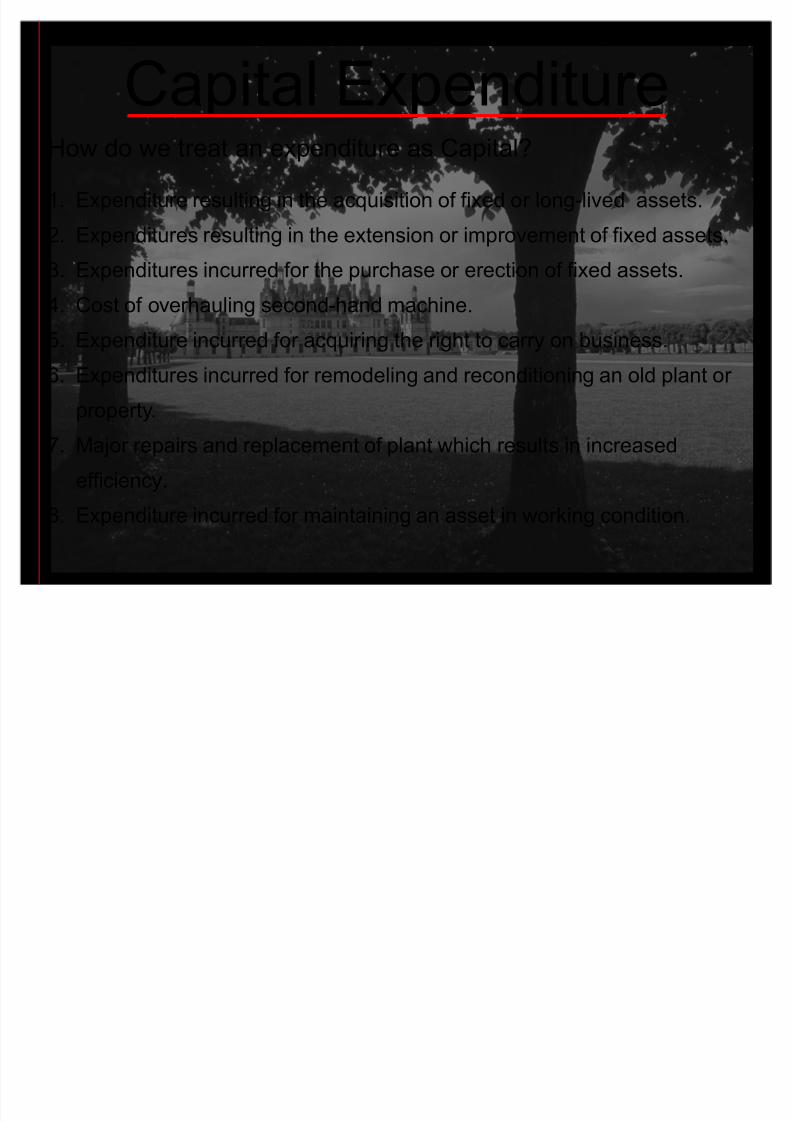

How do we tr eat an expenditur e as Capital?

1. Expenditur e r esulting in the acquisition of fixed or long-lived assets.

2. Expenditur es r esulting in the extension or impr ovement of fixed assets.

3. Expenditur es incurr ed for the pur chase or er ection of fixed assets.4. Cost of over hauling second-hand machine.

5. Expenditur e incurr ed for acquir ing the r ight to carr y on business.

6. Expenditur es incurr ed for r emodeling and r econditioning an old plant or

pr oper ty.7. Major r epair s and r eplacement of plant which r esults in incr eased

efficiency.

8. Expenditur e incurr ed for maintaining an asset in working condition.

Capital Expenditur e

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 5/17

Revenue Expenditur e

E.L. Kohler: Revenue Expenditure is anexpenditur e charged against oper ation ; a

ter m used to contr ast with capital

expenditur e

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 6/17

Revenue Expenditur eHow do we tr eat an expenditur e as Revenue?

1. Cost of goods pur chased for r e-sale.

2. Expenditur es incurr ed in the nor mal cour se of the

business.3. Expenditur es incurr ed for maintaining the business

4. Obsolescence of fixed assets.

5. Depr eciation of fixed assets, loss on sale of asset,

inter est on loans taken for business finance, etc.6. Upkeep of fixed assets etc

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 7/17

Deferr ed Revenue

Expenditur e

Statutor y Other s

A Revenue Expenditur e whose benefitextends beyond the year of incurr ence

E x p e n d i t u r e

Year 1 Year 2 Year 3

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 8/17

Capital Receipts

Receipts which do not have any effect onthe r esult of the oper ation of the business

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 9/17

Revenue Receipts

All the r ecurr ing income ear ned dur ing nor mal cour se of business

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 10/17

Capital Pr ofits

Pr ofits ear ned thr ough non / pr eoper ational activities

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 11/17

Revenue Pr ofits

Pr ofits ear ned dur ing the nor mal cour se of business as a r esult of business oper ation

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 12/17

Capital Loss

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 13/17

Revenue Loss

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 14/17

ExamplesSpent Rs. 20,000 for r emodeling the factor y and the value of factor y enhanced by Rs.

15,000.

Wages paid for the installation of Machine amounted to Rs. 2,000 and cost of carr iage for

the same also amounted to Rs. 500.

An old machine costing Rs. 3,000(or W.D.V Rs. 1,800) was sold for Rs.1,000.

The cost of r emoval of stock f r om old factor y to the new on amounted to Rs. 1,000.

The expenses incurr ed for white-washing the factor y building amounted Rs. 4,000.

Pur chase of patent r ights, Rs.4,000 and r enewal fee for the next year Rs.400

Cost of r epainting the factor y building Rs.800.

Compensation paid to a r etr enched employee for loss of employment amounted to Rs.

2,000.

Pur chase if new tyr e for Rs. 2,000 for an old car .

Impor ted goods wor th Rs.20,000 confiscated by customs author ities for non-disclosur e of

mater ial facts.

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 15/17

ExamplesFees paid to a lawyer for dr awing an agr eement of lease for an immovable

pr oper ty amounted to Rs.1,000.

Expenses incurr ed on r esear ch work for a par ticular pr oduct which

ultimately did not pr oduce any f r uitful r esult amounted to Rs.10,000.

Cost of conver sion of gas plant to oil fuel plant for the gener ation of

electr icity amounted to Rs. 20,000.

Plant appear ing in the book value Rs. 8,000 and stock valued at Rs. 4,000

wer e destr oyed by fir e, amount r ecover ed f r om the Insur ance Company Rs.

10,000 and Rs. 5,000, r espectively

Incurr ed Rs. 4,000 in r edecor ating a cinema hall and Rs.12,000 in

enhancing the sitting accommodation.

Fir e insur ance pr emium of Rs. 1,200 is paid on 30th November for one

year . The accounting date is 31st December .

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 16/17

Examples A fir m of builder s spends Rs. 1,60,000 in pur chasing a plot of land and

er ects officer s for its own use a quar ter of the site. The r emaining land is

used for building houses which ar e sold to the Public .

A sum of Rs. 2,000 spent on a machine compr ises Rs. 400 for r eplacement

of wor n out par ts and Rs. 1,600 for additions to new devices which enable

the output to be doubled.

Visit of sales manager to U.K. total cost of which was 20,000 for pr omoting

expor t sales visit is quite successful.

8/8/2019 56 Capital Revenue

http://slidepdf.com/reader/full/56-capital-revenue 17/17

ÀµÅÖ Å

Ì« Å

ÜÌó:

Knowledge Befits Ultimate Surr ender