5473 515rev2 en - european parliament · inflation decreased from 2.4% in 2001 to 1.4% in 2002,...

TRANSCRIPT

DIRECTORATE-GENERAL FOR RESEARCH

Directorate A: Medium and Long-Term Research

Division for Economic, Monetary and Budgetary Affairs

BRIEFING

ECON 515 EN/Rev.2

THE GERMAN ECONOMY

The opinions expressed are those of the author

and do not necessarily reflect the European Parliament's position.

Luxembourg, September 2003 PE 302.203/rev.2

GERMANY

PE 302.203/rev.2 2

This document is published in English (original), French and German.

You will find the full list of the "Economic Series" briefings at the end of this publication.

Summary

The aim of this briefing is to give a general overview of the German economy and its

prospects in the medium term. It is based on the list of criteria of the Stability and Growth

Pact and on the fourth update of the German Stability Programme, presented on 18 December

2002. Subsequent changes in the economic outlook were taken into account where new data

and forecasts have become available.

Publisher: European Parliament

L - 2929 Luxembourg

Author: Hanna Dahlberg, Agnieszka Ruminska

Responsible Official: Aila Asikainen

Directorate General for Research - Directorate A

Division for Economic, Monetary and Budgetary Affairs

Tel: (352) 4300 24114

Fax: (352) 4300 27721

E-mail: [email protected]

Reproduction and translation of this publication is authorised, except for commercial purposes,

provided that the source is acknowledged and that the publisher is informed in advance and

supplied with a copy.

Manuscript completed on 22 September 2003

GERMANY

PE 302.203/rev.2 3

Contents

GENERAL INTRODUCTION...............................................................................................................................5

BACKGROUND TO THE GERMAN STABILITY PROGRAMME ..............................................................6

EXCESSIVE DEFICIT PROCEDURE ............................................................................................................................6

RESULTS 2001–MID-2003.....................................................................................................................................7

ANALYSIS AND FUTURE PROSPECTS ...........................................................................................................8

ECONOMIC GROWTH ..............................................................................................................................................8

EXTERNAL BALANCE..............................................................................................................................................9

INFLATION............................................................................................................................................................10

EMPLOYMENT ......................................................................................................................................................11

PUBLIC DEFICIT ....................................................................................................................................................12

GOVERNMENT DEBT.............................................................................................................................................14

STRUCTURAL REFORMS.................................................................................................................................14

LABOUR MARKET .................................................................................................................................................15

PENSION SYSTEM REFORMS..................................................................................................................................16

TAX SYSTEM.........................................................................................................................................................17

HEALTHCARE REFORMS .......................................................................................................................................17

FURTHER REFORMS ..............................................................................................................................................18

POLITICAL BACKGROUND.............................................................................................................................19

THE POLITICAL SYSTEM .......................................................................................................................................19

PUBLIC OPINION ...................................................................................................................................................19

ECONOMIC AFFAIRS SERIES BRIEFINGS .................................................................................................21

Charts and tables

TABLE 1: KEY INDICATORS FOR 2001 - 2003............................................................................................................ 7

CHART 1: GROSS DOMESTIC PRODUCT 1990-2006.................................................................................................. 9

CHART 2: GERMANY'S BALANCE OF TRADE AND CURRENT ACCOUNT 1990-2002................................................... 9

CHART 3: GERMAN INFLATION 1996-2006............................................................................................................. 10

CHART 4: MONTHLY INFLATION 2001–2003.......................................................................................................... 10

CHART 5: UNEMPLOYMENT 1992-2002.................................................................................................................. 11

CHART 6: MONTHLY UNEMPLOYMENT 2001-2003 ................................................................................................ 12

CHART 7: GENERAL GOVERNMENT DEFICIT, 1993-2006....................................................................................... 13

CHART 8: GENERAL GOVERNMENT CONSOLIDATED GROSS DEBT 1993-2006........................................................ 14

TABLE 2: BUNDESTAG ELECTIONS 22 SEPTEMBER 2002 ....................................................................................... 19

* * *

GERMANY

PE 302.203/rev.2 4

GERMANY

PE 302.203/rev.2 5

General Introduction

Under Article 99 of the Treaty, all EU Member States – whether they fully participate in the

Single Currency or not – are required to regard their economic policies as a matter of

common concern, and to co-ordinate them within the Council. Co-ordination is carried out

within the framework of recommended "broad guidelines" for the economic policies of

Member States.

In addition, under the pre-Single-Currency transitional provisions outlined in Treaty Article

116, Member States wishing to join the € area were asked to adopt multi-annual programmes

intended to ensure the lasting convergence necessary for the achievement of economic and

monetary union. These formed the basis of the May 1998 decisions on € area membership.

The requirement to submit such "convergence programmes" remains for those countries

still outside the euro area. In the case of countries which have already adopted the €, the

Stability and Growth Pact and Article 4 of the EU Council regulation 1466/97 on tighter

surveillance of budgetary implementation calls for similar "stability programmes" to be

submitted. These are three-year rolling programmes, and focus on progress in meeting the

Pact’s two major objectives:

• a budget deficit below 3% of GDP in any one year; and

• an overall budgetary balance over the economic cycle.

The credibility of the Stability and Growth Pact has come under strain during the current

economic downturn as doubts have arisen concerning the commitment of some Member

States. As a response, the Commission proposed slight modifications to the interpretation of

the Pact 1. It emphasised that budgetary objectives should be set and outcomes analysed in

structural terms, i.e. after adjusting the nominal position to the economic cycle. A softer

interpretation of the balanced budget requirement would apply to Member States with a

relatively low debt burden (less than 60% of GDP) and sustainable public finances.

While adopting a common method of cyclical adjustment, the Council did not endorse this

proposal but emphasised the need to assess the Programmes case by case, putting weight on

the long-term sustainability of public finances and securing a sufficient safety margin,

including an allowance for automatic stabilisers to operate fully, without breaching the 3%

reference value. Further, the planned evolution and quality of public finances should be

coherent with the close-to-balance requirement. Finally, a rule by which structural deficit

should be reduced annually by 0.5% of GDP in Member States not having yet reached a

structurally balanced position received backing from the Council.

Each Stability/Convergence programme is the subject of a Commission assessment and a

Council opinion, and forms part of the input to the broad guidelines (BEPGs), together with

the overall annual implementation report published by the Commission in January.

While the BEPGs indicate the medium-term orientation for the Member States' policies, the

annual updates of the Stability/Convergence Programmes set out the measures decided by the

national governments for the achievement of the medium-term goals. They should reflect the

budget proposals for the following year. The annual updates should be submitted between

mid-October and the beginning of December.

The initial Convergence and Stability programmes were published in late 1998. They have

been updated four times. The fourth updates became available towards the end of 2002.

1 "Communication on strengthening the co-ordination of budgetary policies", COM(2002) 668 final.

GERMANY

PE 302.203/rev.2 6

Background to the German Stability programme

The update of the German Stability Programme covering the period from 2002 to 2006 was

published in December 20022. It is based on data available at the end of November as the

legislative elections in September resulted in the introduction of a completely new federal

budget at the beginning of December 2002.

In its opinion of 8 January 2003 the Commission came to the conclusion that the scenario of

1.5% economic growth annually for the period 2002-2006, underlying the German stability

programme, was very optimistic and subject to some risks3. The programme forecasts that,

from 2006 onwards, German government finances would meet the requirements of the

Stability and Growth Pact and that the budget would be close to balance or in surplus.

The Commission demanded commitment and urged German government to make progress in

adjusting the underlying budgetary position by achieving an annual improvement of 0.5 % of

GDP on average.

Moreover, in view of the extra burden on Germany's finances due to its ageing population, the

Commission urged Germany to make far-reaching structural reforms and to strengthen the

sustainability of general government finances.

The Council gave its opinion on the updated Stability Programme on 21 January 20034. It

observed that there was a major risk that the general government deficit would again exceed

the 3% reference value again in 2003. The growth forecast of 1.5% also appeared too

optimistic to the Council, which went on to note the commitment of the German government

to reduce the structural deficit in line with the Commission recommendation. In order to

achieve this improvement, structural reforms would be needed.

Excessive deficit procedure

After the Commission autumn forecast 2002 had indicated that the German deficit might

reach 3.8% of GDP in 2002, the Commission prepared a report on Germany in November

2002 and recommended that the Council take a decision on the existence of an excessive

deficit. The Council took such a decision on 21 January 20035. In its recommendation to

Germany, the Council requested the German Government to implement all measures

announced for 2003 by the deadline of 21 May 2003. The Council further emphasised that

structural reforms and better co-ordination of budgetary policy in different government levels

would be needed.

Germany's budgetary woes have continued and aggravated in 2003. First, the Government

was forced to admit that, contrary to what was announced in the 2002 Stability Programme

update, the budget deficit would exceed the 3% limit in 2003. By summer 2003, an excessive

deficit had also become very likely also for 2004, which brought the question of pecuniary

sanctions into the agenda.

2 German Stability Programme updated December 2002.

(http://www.bundesfinanzministerium.de/Anlage16208/Deutsches-Stabilitaetsprogramm-Aktualisierung-

Dezember-2002.pdf). 3 Commission assesses the German Stability Programme Update (2002-2006), Commission press release

IP/03/14. 4 Council opinion of 21 January 2003 on the updated stability programme for Germany, 2002 to 2006.

(http://europa.eu.int/smartapi/cgi/sga_doc?smartapi!celexapi!prod!CELEXnumdoc&lg=EN&numdoc=3200

3A0204(01)&model=guichett). 5 2480th Council meeting, Economic and financial affairs - Brussels, 21 January 2003, 5506/03 (Presse 15).

GERMANY

PE 302.203/rev.2 7

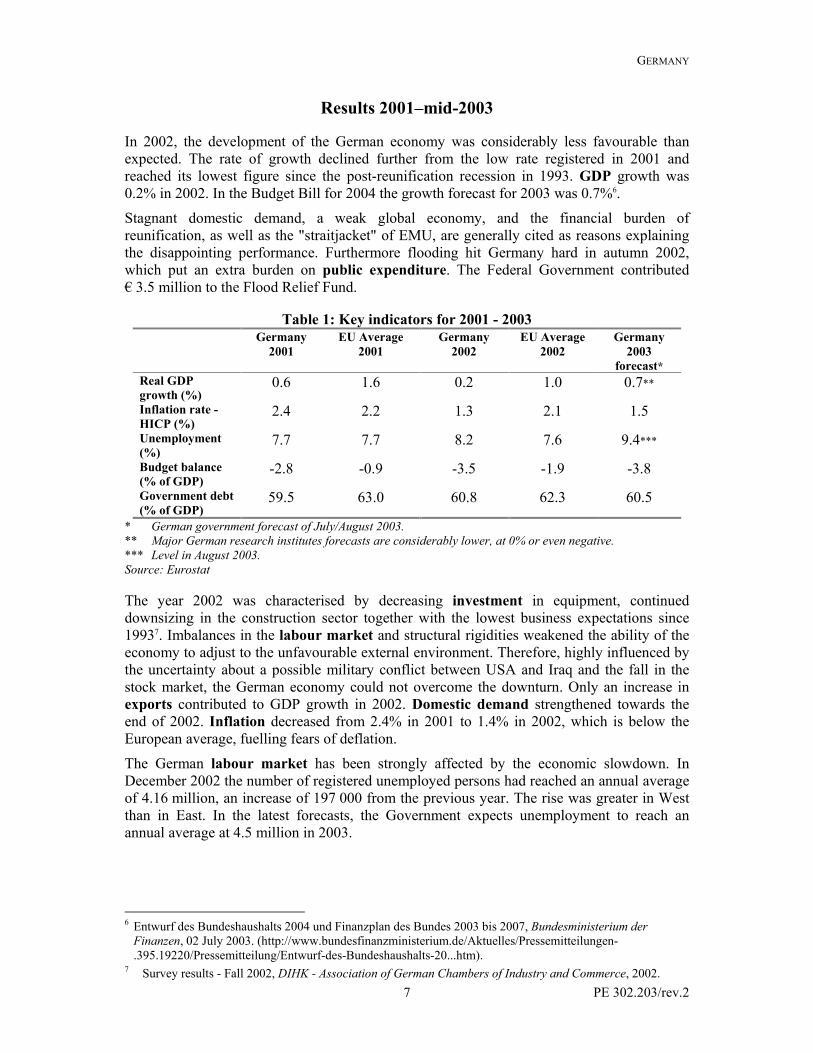

Results 2001–mid-2003

In 2002, the development of the German economy was considerably less favourable than

expected. The rate of growth declined further from the low rate registered in 2001 and

reached its lowest figure since the post-reunification recession in 1993. GDP growth was

0.2% in 2002. In the Budget Bill for 2004 the growth forecast for 2003 was 0.7%6.

Stagnant domestic demand, a weak global economy, and the financial burden of

reunification, as well as the "straitjacket" of EMU, are generally cited as reasons explaining

the disappointing performance. Furthermore flooding hit Germany hard in autumn 2002,

which put an extra burden on public expenditure. The Federal Government contributed

€ 3.5 million to the Flood Relief Fund.

Table 1: Key indicators for 2001 - 2003

Germany

2001

EU Average

2001

Germany

2002

EU Average

2002

Germany

2003

forecast*

Real GDP

growth (%) 0.6 1.6 0.2 1.0 0.7**

Inflation rate -

HICP (%) 2.4 2.2 1.3 2.1 1.5

Unemployment

(%) 7.7 7.7 8.2 7.6 9.4***

Budget balance

(% of GDP) -2.8 -0.9 -3.5 -1.9 -3.8

Government debt

(% of GDP) 59.5 63.0 60.8 62.3 60.5

* German government forecast of July/August 2003.

** Major German research institutes forecasts are considerably lower, at 0% or even negative.

*** Level in August 2003.

Source: Eurostat

The year 2002 was characterised by decreasing investment in equipment, continued

downsizing in the construction sector together with the lowest business expectations since

19937. Imbalances in the labour market and structural rigidities weakened the ability of the

economy to adjust to the unfavourable external environment. Therefore, highly influenced by

the uncertainty about a possible military conflict between USA and Iraq and the fall in the

stock market, the German economy could not overcome the downturn. Only an increase in

exports contributed to GDP growth in 2002. Domestic demand strengthened towards the

end of 2002. Inflation decreased from 2.4% in 2001 to 1.4% in 2002, which is below the

European average, fuelling fears of deflation.

The German labour market has been strongly affected by the economic slowdown. In

December 2002 the number of registered unemployed persons had reached an annual average

of 4.16 million, an increase of 197 000 from the previous year. The rise was greater in West

than in East. In the latest forecasts, the Government expects unemployment to reach an

annual average at 4.5 million in 2003.

6 Entwurf des Bundeshaushalts 2004 und Finanzplan des Bundes 2003 bis 2007, Bundesministerium der

Finanzen, 02 July 2003. (http://www.bundesfinanzministerium.de/Aktuelles/Pressemitteilungen-

.395.19220/Pressemitteilung/Entwurf-des-Bundeshaushalts-20...htm). 7 Survey results - Fall 2002, DIHK - Association of German Chambers of Industry and Commerce, 2002.

GERMANY

PE 302.203/rev.2 8

Analysis and future prospects

Despite the uncertainty caused by prospects of a conflict in Iraq in late 2002, as the Stability

Programme update was being prepared, the assessment for 2003–2006 contains improved

growth, which was expected to arise partly as a result of increased export and domestic

demand. GDP growth was expected to be 1.5% in 2003 and 2.25% in average for the period

2004 to 2006. This macro-economic forecast was based on assumptions that world growth

would pick up during 2003 to 3.5% from a level of 2.5% in 2002 and that world trade would

grow by approximately 5.5% to 6% in 2003. The Iraq conflict was not assumed to have any

lasting negative effect on international financial markets, oil prices, and consumer or investor

confidence. Furthermore, it was assumed that capital markets would stabilise.

As it has turned out since then, the long-awaited recovery of the world and the euro area

economy had not materialised by mid-2003. Growth has stalled in the German economy. As

business and household confidence indicators were plummeting in early 2003, the German

government initiated a programme of reforms, with the aim of restoring confidence through a

series of structural reforms.

Economic growth

Growth in the German economy almost stalled in 2002. Relying on an optimistic outlook

with regard to the developments in the world economy, the Stability Programme update

foresaw a growth rate of 1.5% for 2003. Moderate wage trends, stable prices, increasing

corporate and asset income and low capital market interest rates were other factors assumed

to lift the German economy from the doldrums. Announced labour market reforms would

provide a further contribution to growth as the number of gainfully employed persons was

assumed to increase 0.5% per year over the programme period. The strongest input to higher

growth was to come from exports.

Since the beginning of 2003, growth forecasts have been scaled down more than once both

for the German and the world economies. The German Ministry of Finance8 now expects the

GDP to grow by 0.7% in 2003, while the major research institutes' forecasts range from 0%

to slightly negative numbers. For instance, the German Institute for Economic Research

(Deutsches Institut für Wirtschaftsforschung - DIW)9 expects a decline of 0.1%. Even if

growth were to resume in the second half of the year, as some expect, the pick-up in

Germany would have to be quite strong to bring the economy above the growth rate of 0.2%

registered in 2002.

8 Entwurf des Bundeshaushalts 2004 und Finanzplan des Bundes 2003 bis 2007, Bundesministerium der

Finanzen, 2 July 2003. (http://www.bundesfinanzministerium.de/Aktuelles/Pressemitteilungen-

.395.19220/Pressemitteilung/Entwurf-des-Bundeshaushalts-20...htm). 9 Deutschland: Stagnation schürt Deflationsgefahr. DIW Berlin stellt Sommer-Grundlinien 2003/2004 vor,

Deutsches Institut für Wirtschaftsforschung, 1 July 2003.

(http://www.diw.de/programme/jsp/presse.jsp?pcode=215&language=de).

GERMANY

PE 302.203/rev.2 9

Chart 1: Gross Domestic Product 1990-2006

(annual change in volume, %)

5

2,2 2,3

-1 ,1

5,7

1,7

0,81,4

2 2

2,9

0,20,6

1,5

2 ,25

0 ,5

2 ,252,25

-2-101234567

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

G ermany S tability programme 2001

S tability programme 2002 EU -15

Source: Eurostat and Stability Programme

External balance

Germany is the world's second largest exporter and importer (after the US), with a high

degree of economic openness. In the 90s there was a particularly marked expansion in

German exports. Germany's most important trading partners are the other EU countries, the

US, Japan and, increasingly, countries in Central and Eastern Europe.

In 2002 relatively high exports contributed largely to the modest overall GDP growth. At the

same time, a drop in domestic demand for imports resulted in a favourable trade balance that

reached its record level of €136 billion. Investment goods remained the main export category,

and transition economies were the destination that accounted for the biggest increase in trade

in terms of absolute value.

For the second time since the beginning of the 90s, the current account closed in 2002 with a

credit balance. At 1.9% of GDP and €40.8 million, it reached its record level since the

German reunification.

Chart 2: Germany's balance of trade and current account 1990-2002

(% of GDP)

1 ,1 1 ,42 2 ,3 2 ,6 3 3 ,4 3 ,6 3 ,4 3 ,1

4 ,8

- 0 ,5 - 0 ,8- 0 , 3 - 0 , 3

5 ,9 6 ,3

- 0 , 1

3 ,5

- 1 - 0 ,7 - 1 ,2 - 1- 0 , 8

0 ,5

1 ,9

- 2

0

2

4

6

8

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

B a la n c e o f T r a d e C u r r e n t a c c o u n t

Source: Eurostat

GERMANY

PE 302.203/rev.2 10

Inflation

Consumer prices remained stable in 2002. German prices registered an increase of barely

1.4% the lowest inflation rate in the euro area, where the average rate was 2.1%. This was in

particular due to falling import prices and subdued growth. The European Commission

expects the German inflation to remain at low levels and prices to increase in 2003 and 2004

by 1.3% and 1.2% respectively.

Chart 3: German inflation 1996-2006

(HICP, annual change, %)

1 ,2

1 ,9

1 ,5 1 ,5 1 ,5 1 ,51 ,5

0 ,6 0 ,6

1 ,4

1 ,31 ,5

0

0 ,5

1

1 ,5

2

2 ,5

3

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

G erm an y S tab ility P rog ram m e 2 0 02 E U -1 5

Source: Eurostat and Stability Programme

The low inflation figures have not been universally welcome. There have been warnings

about the risks of a vicious deflation cycle, which would be about to hit Germany. The

common monetary policy, leading to higher real short-term interest rates in Member States

with low inflation, is deemed by some to be too tight for Germany. Some even consider

deflation to be such a risk that it should be given priority over short-term fiscal consolidation.

Others warn, on the contrary, that the mere fact that the prices of some goods fall, as has

happened in Germany, is no evidence of a general fall in price level. The most recent price

developments indicate a slight increase in the German inflation rate.

Chart 4: Monthly inflation 2001–2003

(HICP, month-to-month change over 12 months, %)

0

1

2

3

4

Jan-01

Mar-01

May-01

Jul-01

Sep-01

Nov-01

Jan-02

Mar-02

May-02

Jul-02

Sep-02

Nov-02

Jan-03

Mar-03

May-03

Jul-03

EU-15 Germany

Source: Eurostat

GERMANY

PE 302.203/rev.2 11

Employment

At the end of the 80s the German economy had the lowest unemployment rates in the EU.

After re-unification in 1990, the situation gradually changed. Particularly in the new Länder

there were many cutbacks in jobs due to restructuring. In mid-90s, an economic downturn led

to still higher unemployment, the unemployment rate rising from 4.8% in 1990 to 8.2% in

1994 and peaking at 9.7% in 1997. Over the following years, the number of the unemployed

declined somewhat but less than hoped for. The trend is currently in the rise again, and will

exceed the 9% mark in 2003.

Chart 5: Unemployment 1992-2002

8,27,77,88,49,19,78,7

88,27,76,4

0

2

4

6

8

10

12

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

G ermany EU-15

Source: Eurostat

In December 2002 there were 4.2 million people (8.2% of civilian labour force) without jobs,

the highest rate for the last three years10. The increase of 197 000 since the end of 2001

reflects persisting adverse conditions in the German labour market. The number of gainfully

employed persons fell by 0.5%, which is significantly less than the increase in the number of

unemployed persons. Unemployment is increasing more rapidly in West than in the new

Länder. Nevertheless, the unemployment rate is still around 10 percentage points higher in

the East than in the West.

Nor is the situation improving in 2003 despite the gradual implementation of labour market

reforms (Hartz scheme), as the effect of these reforms will only be seen later (see also section

on Structural reforms). The Commission expects an increase of 350 000 unemployed in 2003.

In its September outlook, the German government expected unemployment to reach 4.5

million on average in 2003. In August 2003, the German unemployment was stable at the

same level as in the previous months (9.4%)11.

10 European Economy; Economic forecast Spring 2003, European Commission, No. 2/2003. However, the

German Council of Economic Experts states in "Annual Report 2002/03" the figure of 9.8% for

unemployment according to the definition of the Federal Labour Office. 11 The Federal Labour Office (www.arbeitsamt.de/hst/services/ statistik/english/s001e.pdf ).

GERMANY

PE 302.203/rev.2 12

Chart 6: Monthly unemployment 2001-2003

77,58

8,59

9,510

Jan-01

Mar-01

May-01

Jul-01

Sep-01

Nov-01

Jan-02

Mar-02

May-02

Jul-02

Sep-02

Nov-02

Jan-03

Mar-03

May-03

Jul-03

EU-15 Germany

Source: Eurostat

The monthly unemployment rate started to deviate from the EU-average during 2001. It is

expected in the draft budget for 2004 (Entwurf des Bundeshaushalts 2004), however, that

unemployment will stop rising in 200412.

Public deficit

The ratio of public deficit to GDP reached 3.5% in 2002 and was thereby considerably higher

than planned the year before. This was primarily due to weaker growth and, as a

consequence, lower revenue than expected.

With this perspective, important consolidation and savings measures were agreed on in the

coalition agreement, after the legislative elections in autumn 2002, and submitted in the first

budget proposal in October 2002. Nevertheless, as subsequent projections indicated higher

expenditure and lower revenue, the budget proposal had to be revised no later than one month

after it had been put forward. The Bundestag approved the final version of the federal budget

2003 on 3 December 2002. It includes an additional savings programme (around €14 billion

or approximately 0.7% of GDP) for all government bodies.

An emergency package with respect to pensions, environmental taxes and health care,

foreseeing reductions in tax allowances and reforms in the labour market, was designed to

improve public finances. Based on this programme and the 1.5% of GDP growth forecast, an

aggregate deficit of 2.75% was expected for 2003 (€18.9 billion)13.

As growth forecasts were being scaled down starting from January 2003, the expected deficit

rose. While the impact of lower growth was believed or at the very least, declared to be

"marginal" on the deficit in late January, the Government had to admit by mid-year that the

3% limit would certainly be breached for the second year in 2003. In July 2003 the Ministry

of Finance revised the forecast budget deficit to 3.5% of GDP in 2003. The latest indications

from the German Government point to a worse outcome still for 2003: gross deficit reaching

almost 3.8% of GDP. This forecast is due to a combination of worse-than-expected growth

and the Government's plans to cut income taxes without an offsetting revenue increase from

elsewhere. While the Government maintains that it aims at bringing the deficit below the 3%

12 Entwurf des Bundeshaushalts 2004 und Finanzplan des Bundes 2003 bis 2007, Bundesministerium der

Finanzen, 2 July 2003. (http://www.bundesfinanzministerium.de/Aktuelles/Pressemitteilungen-

.395.19220/Pressemitteilung/Entwurf-des-Bundeshaushalts-20...htm). 13 The situation of the world economy and the German economy in Autumn 2001, Working Community of

German Economic Research Institutes, Berlin; 2001.

GERMANY

PE 302.203/rev.2 13

limit in 2004, the risk of the limit being breached for the third year in a row seems to be

growing14.

Chart 7: General Government Deficit, 1993-2006

(net borrowing -/net lending + as a % of GDP)

-3,1-2,4 -2,7 -2,2

-1,5

1,3

-3,5-2,8

-3,5-3,4

-1-1,5-2,75

-3,75

0

-6

-4

-2

0

21993

1994

1995

1996

1997

1998

1999

2000*

2001

2002

2003

2004

2005

2006

Germany Stability Programme 2001

Stability Programme 2002 EU-15

* Including the proceeds from the sales of the UMTS licences. Germany without these proceeds -1.2%.

Source: Eurostat and Stability Programme 2002

Already in 2002, the need to ensure that budgetary discipline be maintained at all levels of

government was recognised. Therefore, the Financial Planning Council agreed on a National

Stability Pact, imposing financial discipline on regional and local authorities15 and amending

the Haushaltsgrundsätzegesetz (Budgetary Principles Act). On 27 November 2002, Federal

Government and the Länder on the basis of the amended §51a of the Act Maintenance of

budgetary discipline within the framework of European Economic and Monetary Union

approved the timetable and a plan of six joint actions for attaining balanced general

government budget in the year 2006. In its Opinion of 21 January 2003, the Council "noted

with satisfaction the approval and implementation of the new §51a".

In the 2003 BEPGs16 Germany was asked to reduce its gross deficit by 1 percentage point of

GDP in 2003 and to put an end to the excessive deficit no later than 2004. Furthermore it was

considered unlikely that Germany would be able to reach the target of a budgetary position

"close to balance" in 2006, if no additional structural reforms were effected. Germany was

advised to implement urgent reforms in the labour market as well as in the social security and

benefit systems in general, and to reduce the regulatory burden on the economy. Moreover,

the cyclically-adjusted deficit should be reduced by at least 1 percentage point of GDP

between the end of 2003 and 2005.

14 Finanzpolitik stützt Konjunktur! Ministry of Finance, Press release of 29 August 2003

(http://www.bundesfinanzministerium.de/BMF-.336.20042/Pressemitteilung/.htm) 15 National Stability Pact, The Federal Government.

(http://text.bundesregierung.de/frameset/ixnavitext.jsp?nodeID=8547). 16 The 2003 Broad Economic Policy Guidelines, ECOFIN, 3 June 2003.

GERMANY

PE 302.203/rev.2 14

Government debt

Gross government debt rose from 46.9% of GDP in 1993 to some 61% in 1997. Ever since

the German government debt has fluctuated around 60% of GDP, on both sides of the

Maastricht criterion of 60%.

Chart 8: General government consolidated gross debt 1993-2006

(% of GDP)

59,5 60,8

46,9 49,357 59,8 61

60,9 61,2 60,2

0

20

40

60

80

1993 1995 1997 1999 2001 2003 2005

Germ any Stability Programme 2001

Stability Programme 2002 EU-15

Source: Eurostat and Stability Programme

The 2002 update of the Stability Programme foresaw an increase to 61.5% in the debt ratio in

2003, although a smaller deficit and an economic recovery were assumed. In the following

years the debt ratio was expected to decline slowly, reaching 57% of GDP in 2006. The

Commission was more pessimistic about the developments already in its 2003 spring

forecast, expecting it to rise to 62.7% in 2003 and further to 63% in 2004. In its most recent

previsions, the German Government has indicated that it expects the outcome for 2003 to be

around 63% of GDP, higher than the previous peak of 61.2% registered in 1999.

Structural Reforms

The German economy has suffered from low growth for the last decade. Only in two years

did the German GDP growth exceed 2%. Structural rigidities have been identified as a major

cause for this disappointing performance. Some attempts to remove such rigidities and to

raise the potential growth rate of the German economy have been made. The first phase of a

tax reduction scheme has been implemented and a pension reform has been undertaken,

lowering compulsory contributions to the public scheme and providing incentives to save in

individual pension plans as well as measures to stimulate employment.

Since the election in September 2002, as the economy was coming close to a standstill, the

Government became more ambitious in planning measures to reduce structural rigidities. On

14 March 2003 Chancellor Schröder launched a reform package named Agenda 2010 that

should help boost the German economy, in particular by reducing rigidities. Agenda 2010,

together with the final phase of the tax reform, which has been brought forward to 2004, are

hoped to boost economic growth, safeguard the social security systems in the long term, and

strengthen Germany as a business location17. In the 2003 BEPGs these reforms are expressed

to "constitute important steps towards solving Germany's structural problems"18.

17 The most frequently asked questions on Agenda 2010, Bundesregierung.

(http://eng.bundesregierung.de/dokumente/Artikel/ix_500463_4317.htm). 18 The 2003 Broad Economic Policy Guidelines, ECOFIN, 3 June 2003.

GERMANY

PE 302.203/rev.2 15

Labour market

The year 2002 was marked by series of reforms aiming to improve the conditions for growth

and employment. The Job-AQTIV Act was implemented to promote the provision of job

placement and counselling, actions reducing unemployment among severely handicapped and

among young people, measures facilitating women’s insertion to active life were taken

through the new legislation on active labour market policies (ALMPs). These reforms were in

line with the 2002 BEPGs but they were not sufficient to reduce chronic unemployment.

In August 2002 the Hartz Commission presented a comprehensive plan on creating jobs.

Based on these recommendations, two acts on Modern Services in the Labour Market (Hartz

Acts I and II) were implemented in January 2003. The acts focus mainly on "improving the

basic conditions for rapid and lasting job placement and on building more bridges to

employment and creating new areas of employment"19.

The Harz reform introduced in November 2002, included the so-called "Capital for Work"

(Kapital für Arbeit) programme. The aim of the programme is to encourage companies to

hiring unemployed people by offering them a loan facility of up to €100 000 for each

appointment. After five months, 2 600 unemployed had got a new job. The programme also

aims to improve training opportunities for young people by extending the same loan offer

for training places created.

From January 2003 self-employed people receive a subsidy during the first three years after

founding a so-called Ich AG ("I-plc") and, since April 2003, people in mini jobs, earning up

to €400, do not have to pay taxes and social welfare contributions. The Government expects

that another 320 000 jobs will be created by this measure.

On 13 August 2003 the German cabinet approved two new bills aiming to further improve

the functioning of the labour market. The Third Bill on Modern Service in the Labour Market

(Hartz III) will change Germany's national employment administration to be more active

in helping the unemployed to find work. Subsequently the Fourth Bill on Modern Services in

the Labour Market (Hartz IV) consists of various measures, such as reforming the local

government finances and providing basic security for job seekers. It also important changed

to unemployment benefits. The entitlement period for the assistance to the unemployed

(Arbeitslosengeld) is to be restricted to a maximum 12 months from the current 32 months (to

18 months for those over 55 years old) and the income of the unemployed person's partner is

to be taken into account 20. Sanctions on unemployed persons refusing to take up work are to

be tightened. Furthermore, the level of the new unemployment benefit for the long-term

unemployed (Arbeitslosengeld II) is to decrease to the level of the social assistance

(Sozialhilfe). These two types of benefits are to be merged21. The law is planned to come into

force on 1 January 200422.

The Hartz proposals have so far primarily been seen as leading to greater wage flexibility for

low-skilled workers and helping to create jobs in the low-income sector.

In the 2003 BEPGs Germany is encouraged to promote job creation and adaptability and

mobilise the unutilised employment potential. Further recommendations to Germany are to

continue the tax cuts in order to ensure sufficient incentives to take up work or to move into a

higher income bracket. Germany is moreover asked to ensure that wages reflect better

19 Labour Market, Bundesregierung, 1 August 2003. (http://eng.bundesregierung.de/frameset/index.jsp). 20 Public Finances in EMU 2003, European Commission, 2003. 21 German cabinet approves bills aimed at bringing far-reaching reforms, Bundersregierung, 14 August 2003. 22 Germany's national employment agency to undergo modernization, Bundersregierung, 14 August 2003.

GERMANY

PE 302.203/rev.2 16

productivity differences across skills and regions and carry forward the reforms to improves

the efficiency of ALMPs.

Pension system reforms

The social security system in Germany is one of the most generous in the world. The need for

fundamental reform has long been recognised, in view of Germany’s ageing and declining

population. Demographic changes increase the uncertainty about the level of future

contributions and expected benefits.

In order to secure future pensions without creating excessive burden to public finances,

Chancellor Schröder's first cabinet introduced a pensions reform in 2001. The following are

some of the key element.

• Gradual lowering of the statutory contribution rates and keeping them at the level of

maximum 20% of gross pay. (The rate was reduced from 20.3% in 1998 to 19.1% in

2002, before the budget gap forced the Government to raise it to 19.5% in 2003.)

• Return to the principle of wage-related pensions.

• Creation of voluntary additional pension schemes with capital coverage and government

support.

• Gradual lowering of the statutory pension levels from the present 69% of average net

income to not less than 67% in 2030.

Future reductions in the state pension scheme, functioning on a pay-as-you-go (PAYG) basis,

will be compensated for through the second and third pillars of the pensions system:

funded occupational and private pensions. In the Pension Reform Act of 2001 employers are

required to provide employees with access to an occupational pension. Employers are free to

choose from different types of insurance arrangements. Some among these qualify for tax

advantages. As a private pension scheme, the so-called Riester Pension (Riester-Rente) was

introduced on 1 January 2002 as voluntary contributions. The contribution will increase

gradually from 1% of gross salary in 2002 to 4% in 2008. Among other measures introduced

was a phase-out of early retirement programmes23. Moreover, amendments to the Civil

Servants' Pension Act and the Military Pension Act were introduced in 2002 aiming to slow

the rise in pensions burden in the future.

In view of the difficulties in limiting the budget deficit for 2003, the Government raised

compulsory pensions contributions in the 2003 budget from 19.1% to 19.5% of gross salary,

expecting to raise an additional €5.7 billion in revenue. Despite this emergency measure, the

core of the new concept – moving toward capital-funded pension schemes – has not been

abandoned. The Government has set itself a target level of 40%, to which it intends to reduce

the compulsory pension, health, unemployment and disability insurance payments, which

currently amount to 41.7% of the gross wage.

The discussion about further reforms continues, especially after the Rürup Commission

presented its report on the financing of the social security on 28 August 2003. Among the

recommendations with regard to pensions system, the Commission advocated raising the

statutory retirement age from 65 to 67 years. However, the two major political parties, CDU

and SPD, have so far seemed to prefer concentrating their efforts on raising the effective

retirement age from the current 60 years.

23 OECD Economic Survey: Germany, OECD, December 2002.

GERMANY

PE 302.203/rev.2 17

Tax system

Since the beginning of 2000, the German government has introduced several tax reform

measures aiming to reduce the tax burden borne by individuals and businesses and thereby to

support economic activity.

The rate of the corporate tax for the joint stock companies was reduced to 25% in 2001 from

45% in 1998. The system of shareholders' income tax was simplified, guaranteeing equal

treatment to national and international investors. Comparable conditions were created for

partnerships. New measures were expected to reinforce Germany's status as an investment

location.

Income tax reform was originally planned to be implemented in three steps, the second step

being scheduled to enter into force in 2003 and the third in 2005. The implementation of the

second step was postponed in the context of the flooding that occurred in 2002, as public

finances were already about to breach the deficit limit of 3% of GDP. With the further

declining economic activity in the course of 2003, the Government decided not only to

implement the second step in 2004, but also to bring forward the third step and implement it

together with the second step in 200424. The reform scheduled to take effect as of 1 January

2004 includes the following measures:

• The basic rate of the taxation is to be lowered from the current 19% to 15%.

• The basic tax free allowance per person is to be raised from the current €7 235 to €7 664.

• The top rate of income tax is to be lowered to 42% and will only be applied to taxable in

excess of €52 152.

• Tax progression will be less steep for taxpayers in middle income brackets.

All in all, the cuts would amount to €21.8 billion in lower taxes to individuals and firms. The

overall impact would, however, be smaller due to the planned reduction of various subsidies.

The Government expects a decrease of €15.6 billion in tax revenue for 200425. According to

the Government, the Federal level would lose €7.1 billion and the Länder and municipalities

together €8.5 billion. Apart from reducing subsidies, the Government intends to finance the

reform by widening the base for VAT and by selling government assets. Further privatisation

should contribute at least €2 billion in 2004 to the federal budget. The rest would be financed

by increased government borrowing26.

Healthcare reforms

Reforming the expensive health care system, which provides Germans with generous

benefits, is necessary to support the Government’s long-term goal of sustainable public

finances. To this end, the Government has already taken steps to modify the System of

Statutory Health Insurance. On 1 January 2000 the Statutory Health Insurance Reform Bill

became law. This was not, however, sufficient to put the system on sustainable footing.

Faced with the rising cost and the overall deterioration of public finances, the Government

adopted in November 2002 an emergency bill with new measures expected to provide

24 Federal Ministry of Finance website, press releases of July and August 2003

(http://www.bundesfinanzministerium.de/). 25 Entwurf des Bundeshaushalts 2004 und Finanzplan des Bundes 2003 bis 2007, Bundesministerium der

Finanzen, 2 July 2003. (http://www.bundesfinanzministerium.de/Aktuelles/Pressemitteilungen-

.395.19220/Pressemitteilung/Entwurf-des-Bundeshaushalts-20...htm). 26 Early tax cut to be financed by reducing subsidies, privatization, and additional borrowing,

Bundesregierung, 17 July 2003.

GERMANY

PE 302.203/rev.2 18

savings of €3.5 billion. They include the freeze of doctors' fees, a price cut on refunded

pharmaceuticals and a rise in the rebate paid by pharmacies to the public health insurance

system. On the other hand, the healthcare contributions remained unchanged by the Act on

Securing the Rate of Contribution (Beitragssatzsicherungsgesetz), which came into force in

January 2003.

More far-reaching reforms were proposed in the bill on the modernisation of the health

service, which is a part of the Agenda 2010 reform package. After negotiations with the

opposition (CDU/FDP), a package was presented to the Bundestag for the first reading in

September 2003. Among other aims, it seeks to improve the efficiency of medical care by

cutting bureaucracy and developing competition. The measures include

• removing some benefits from the public health system and financing them by taxation,

• limiting the level of subsidy available from the system,

• abolishing some benefits altogether,

• requiring patients to take additional insurance for certain services,

• liberalising the supply of medicines by permitting a pharmacist to have up to three

pharmacies (business locations) and by allowing the ordering of medicines via Internet,

• increasing attention to preventive health care.

These measures are expected to bring down the average health insurance contribution rate

from around 14.4% of gross income to 13% in the long-term, cut add-on costs, and provide

more employment. In 2004 the average health insurance contribution rate should decline to

13.6% and in 2005 below 13%27. Furthermore, it permits insurers to negotiate costs directly

with doctors. Cost sharing should raise the patient's cost awareness. However, some of these

measures, such as the tax financing of the versicherungsfremde Leistungen28, may pose a risk

to the consolidation programme announced in the 2002 Stability Programme update. Parts of

the programme were prepared by the respective ministries, while the Rürup Commission

outlined the financing in its first report, presented in May 2003.

These reform initiatives seem to be in line with the recommendations of the 2003 BEPGs,

according to which the health care sector should increase its efficiency by introducing

economic incentives for health care providers and recipients. However, some observers fear

that the reductions in health care benefits in the context of the reforms may undermine the

hoped impact of tax cuts, as consumers may decide to save the extra amount of money they

get from the tax cuts instead of spending them29.

Further reforms

To relieve further the structural rigidities, Chancellor Schröder has also made changes within

other areas. Measures that liberalise regulations for crafts and reduce bureaucracy, especially

for small and medium sized companies, are to be introduced. The easing of the craft

regulations means that the prerequisite of a master craftsman's diploma to entering a

profession is abolished as long as the craft businesses are not subject to registration, i.e. they

are not among the around 30 crafts out of 90 considered to be dangerous.

27 Health, Bundesregierung, 1 August 2003. 28 Benefits currently paid by health insurance system, deemed not to be covered by contributions. 29 German Health-Care Cuts May Offset Boost From Tax Reductions, Bloomberg.com, 22 July 2003.

GERMANY

PE 302.203/rev.2 19

Political background

The political system

Germany is a parliamentary, democratic and federal republic, whose constitution (the

Grundgesetz), enacted on 23 May 1949, became the constitution of a united Germany in

1990.

At the head of the executive but with a primarily representative role is the Federal president,

Johannes Rau (SPD), elected for a five-year period by the Federal Assembly in May 1999.

The legislature consists of the Bundestag (the lower house of the German Parliament) – of the

656 deputies, half are elected by simple majority in the constituencies and half are elected

from Land lists - and the Bundesrat (the upper house), representing the 16 Länder (Baden-

Württemberg, Bavaria, Berlin, Brandenburg, Bremen, Hamburg, Hessen, Mecklenburg-

Vorpommern, Niedersachsen, Nordrhein-Westfalen, Rheinland-Pfalz, Saarland, Sachsen,

Sachsen-Anhalt, Schleswig-Holstein and Thüringen).

The highest body of the judiciary is the Federal Constitutional Court in Karlsruhe

(Bundesverfassungsgericht).

Table 2: Legislative elections of 22 September 2002

Second vote Party

% Change from

1998 (%)

Seats in Parliament

SPD 39.0 -1.9 251

CDU 29.5 +1.1 190

CSU 9.0 +2.3 58

Bündnis 90/DieGrünen 8.6 +1.9 54

F.D.P. 7.4 +1.2 47

PDS 4.0 -1.1 2

Source: The Federal Returning Officer, Press Release, http://www.bundeswahlleiter.de

The 15th Bundestag elections took place in 22 September 2002. The turnout was 79.1%

compared with 82.2% in 1998. After 4 years in office the coalition consisting of the SPD and

the Greens and led by Chancellor Gerhard Schröder, was able to renew its majority in the

Bundestag. However, the majority narrowed to 9 seats from 21 in 1998. Since then, a number

of State elections have indicated a sharp swing away from the Government.

Public opinion

The latest Eurobarometer survey analysing public opinion on various issues related to the

European Union was carried out in all Member States in spring 200330. In overall, EU citizens

have a confidence in the European Union institutions, are worried about the thread of the

armed conflict and about prospects for the national economy and for employment.

The majority of the EU citizens share the support for the EU's political initiatives. Germany

is, among all Member States, one of their strongest advocates. 77% of respondents is in

favour of the Common Foreign policy (67% EU average) and 81% approves of the Common

Security and Defence policy (73% in the EU).

30 Eurobarometer: Public opinion in the European Union, European Commission, Report No. 59, Edition, July

2003.

GERMANY

PE 302.203/rev.2 20

Approval of EU membership is higher in Germany than the EU average and according to

the survey, 59% of respondents considers EU membership to be a good thing, while only 8%

hold the opposite view. Germans are more likely to support membership than the European

citizen on average (54% in favour, and 11% against). The majority of German respondents

have a confidence in the European Commission: 44% are in favour and 26% against.

However, this figure is lower than the EU average of 50%.

Regarding the level of support for the enlargement of the EU, the results show that public

opinion varies considerably in the Member States. While in Greece 71% are in favour of

enlargement, in France only 31% have a positive opinion. A majority of Europeans (46%)

expressed opinions in favour and 35% against in the latest survey. In Germany, a scant

majority supports the enlargement, with 42% in favour, 39% against. The number of those in

favour has decreased by 4 percentage points since the previous survey in autumn 2002.

67% of EU citizens strongly support the euro, compared to 27% who are against it. This is a

slight increase of 3% from the last survey. In the euro area, 75% are in favour of the euro.

The support for the euro has increased in Germany from 62% to 70%. At the same time,

however, 88% of Germans think that prices rose when they changed the currency31.

The euro banknotes and coins are generally well accepted. 77% of EU citizens were against

the issuing of a new €1 bill, the highest rejection score was registered in Germany by 93%.

The support for a European constitution has declined slightly in EU, from 65% to 63%. In

Germany 62% of the population is in favour, while 12% are against. Still only 33% of the

population in EU-15 know that the Convention had elaborated a draft constitutional treaty.

36% of the Germans are aware of the work of the Convention32.

* * *

31 The Euro one year later, European Commission, Flash EB N°139. 32 Convention of the Future of Europe, European Commission, Flash EB N° 142.

GERMANY

PE 302.203/rev.2 21

Economic Affairs Series Briefings

The following publications are available on line on the Intranet at: http://www.europarl.ep.ec/studies. To obtain

paper copies please contact the responsible official (see page 2) or Fax (352) 43 00 27721.

Number Date Title Languages

ECON 543 Sept. 2003 The Taxation of parent and subsidiary companies EN, FR, DE

ECON 542 June 2003 VAT on services EN, FR, DE

ECON 541 July 2003 VAT on postal services EN, FR, DE

ECON 540 July 2003 The Rates of VAT: including recent proposals (rev1) EN, FR, DE

ECON 540 May 2003 The Rates of VAT EN, FR, DE

ECON 539 forthcoming Stability and convergence programmes 2002/2003 updates EN, FR, DE

ECON 538 June 2003 The Public Debt EN, FR

ECON 537 February 2003 Consequences of Rating & Accountancy Industries Oligopoly on

competition EN, FR, DE

ECON 536 February 2003 State aid and the European Union EN, FR, DE

ECON 535 March 2003 Financial Services and the application of Competition Policy EN, FR, DE

ECON 534 July 2002 Corporate Governance EN, FR, DE

ECON 533 Nov. 2002 Potential Ouput & the output gap (provisional version) EN

ECON 532 June 2002 The Luxembourg Economy EN, FR, DE

ECON 531 March 2003 The Taxation of Energy EN, FR

ECON 530 July 2002 The Irish Economy EN, FR

ECON 529 June 2002 The Austrian Economy EN, FR, DE

ECON 528 July 2002 The taxation of income from personal savings EN, FR, DE

ECON 527 May 2002 VAT on Electronic Commerce EN, FR, DE

ECON 526 May 2002 VAT and Travel Agents EN, FR, DE

ECON 525 May 2002 Currency Boards in Bulgaria, Estonia and Lithuania EN, FR, DE

ECON 524 May 2002 The Greek Economy (rev) EN, FR, EL

ECON 523 April 2002 Stability and Convergence Programmes: the 2001/2002

updates EN, FR, DE

ECON 522 May 2003 The Italian Economy (rev.2 ) EN, FR, IT

ECON 521 Sept. 2001 Competition Rules in the EEA EN, FR

ECON 520 Sept. 2001 Background to the € EN, FR, DE

ECON 519 July 2002 The Belgian Economy (rev) EN, FR, NL

ECON 518 Dec. 2002 Enlargement and Monetary Union (rev7) EN, FR, DE

ECON 517 July 2001 The Taxation of Pensions EN, FR, DE

ECON 516 July 2002 The Finnish Economy (rev) EN, FI, FR

ECON 515 Sept. 2003 Die deutsche Wirtschaft (rev2) DE, EN, FR

ECON 514 April 2001 The Euro and the Blind EN, FR, DE

ECON 513 May 2001 Tobacco Tax EN, FR, DE

ECON 512 May 2001 The Euro: Counterfeiting and Fraud EN, FR, DE

ECON 511 May 2002 The Consequences of EMU for the EEA/EFTA countries EN, FR, DE

ECON 510 April 2001 Margine di Solvibilità IT, EN

ECON 509 March 2001 Stability and Convergence Programmes: the 2000/2001 Updates EN, FR, DE

ECON 508 Sept. 2003 The Swedish Economy (rev. 2) EN, FR, SV

ECON 507 March 2002 The Economy of the Netherlands (rev) EN, FR, NL

ECON 505 forthcoming The Portuguese Economy (rev) EN

ECON 504 July 2000 The French Economy EN, FR

ECON 503 July 2002 The Spanish Economy (rev. 2) EN, FR,ES

ECON 502 June 2000 Le "Troisième système" FR

ECON 501 April 2002 The Danish Economy (rev) EN, FR, DA

* * *