4g - coming soon! - careratings.com global anal… · the global analyst | april 2014 24 4g -...

TRANSCRIPT

The Global AnAlyst | aPRIl 201424

4G - Coming Soon! Network infrastructure is one of the constraints for the launch of 4G as it requires good backhaul connectivity like Optical Fiber Cable (OFC) network. For the existing telecom operators which provide 2G and 3G services, 4G roll-out would be relatively easy as the 4G Base Transceiver Station (4G) can be accommodated within the same premises as compared to a new

Telecom

S P O T L I G H T

India is a rare success story where telecom infiltrated the vast hinterlands before other major infrastructure. Indian wireless telephony, primarily voice-based, has completed almost two decades predominantly dominated by 2G, marked with launch of 3G and 4G in recent times. While 3G was launched couple of years after the allocation of

spectrum in 2010, 4G has taken little longer; it has been launched in only a few cities so far, and it seems others have to wait for some more time. Ecosystem challenges, apprehensions about de-mand for high-end data services, lack of voice capa-bility, stretched balance-sheets resulting into less room for capex for intensive roll-outs, regulatory uncertainty, etc., were the prominent reasons for delays in 4G launches. As the commercial launches expand multifold globally, with LTE subscrip-tions witnessing more than 100 per cent growth rates Y-o-Y, there is a good pick up in Smartphone penetration and data growth back home, preparing the ground for 4G. Recently concluded spectrum

entrants like Reliance Jio who will have to go for a complete greenfield roll-out, say Revati Kasture and Anand Kulkarni of CARE Ratings.

auctions in India have paved the way for use of globally popular 1800 MHz spectrum for 4G. In the coming years, war for grabbing the data pie is going to get intense, with some possible overlap and can-nibalization between 2G, 3G and 4G technologies.

Global Scenario–LTE growing exponentiallyLong Term Evolution (LTE), the most prominent 4G technology, constitutes less than 3 per cent of the global mobile subscriber base of 6.8 billion, but has been growing at a phenomenal pace as the sub-scriber base exploded from a mere 11 million at the end of 2011 to more than 200 million at the end of 2013. Worldwide LTE technology is being adopted in 152 countries by 524 operators. 471 operators have made firm deployment commitments in 143 countries, of which 274 operators have launched commercial services in 101 countries. By the end of 2014, total 350 commercial LTE networks are expect-ed to be in place. North America represents around 50 per cent of the total LTE subscriber base of 200.1 million, Asia Pacific represents next 39 per cent and Europe constitutes around 8.2 per cent. LTE subscriptions have clocked gigantic growth i.e., 166

The Global AnAlyst | aPRIl 2014 25

per cent in 2013 vis-à-vis total subscriber growth of 6.25 per cent in 2013. (Source: Global Mobile Sup-pliers’ Association).

Ecosystem ChallengesOne of the biggest challenges for adoption of LTE is lack of established ecosystem primarily because

of the existence of two different technologies, viz., – Frequency Division Duplex (FDD) primarily used by American and European operators and Time Division Duplex (TDD) embraced by Chinese and Indian operators. Also, there are dozens of bands across these two technologies across different spec-trum frequencies. Nevertheless, the number of LTE devices available globally has more than doubled to 1,371 in December 2013 available from 132 differ-ent manufacturers which itself grew by 52 per cent Y-o-Y. With allocation of 2300 MHz spectrum in 2010, In-dian players went for TD-LTE along with their Chi-nese counterparts like China Mobile. Their decision to shift towards FD-LTE in 1800 MHz will help 4G to grow in India as it is the most widely used LTE band globally with 44 per cent of the total launches

4G - Coming Soon!

9 18 28 47

75

103

129

158

200

0

50

100

150

200

250

Dec-1

1

Mar

-12

Jun-

12

Sep-

12

Dec-1

2

Mar

-13

Jun-

13

Sep-

13

Dec-1

3

LTE

Subs

crin

ers

(Mn)

LTE Subscribers (Mn)

Sour

ce: G

loba

l Mob

ile S

uppl

iers

’ Ass

ocia

tion

(GSA

)

Countries with Commercial LTD ServiceCountries with LTD Commercial network deployments plannedCountries with LTD trial system (pre-commitment)

Revati Kasture

The Global AnAlyst | aPRIl 201426

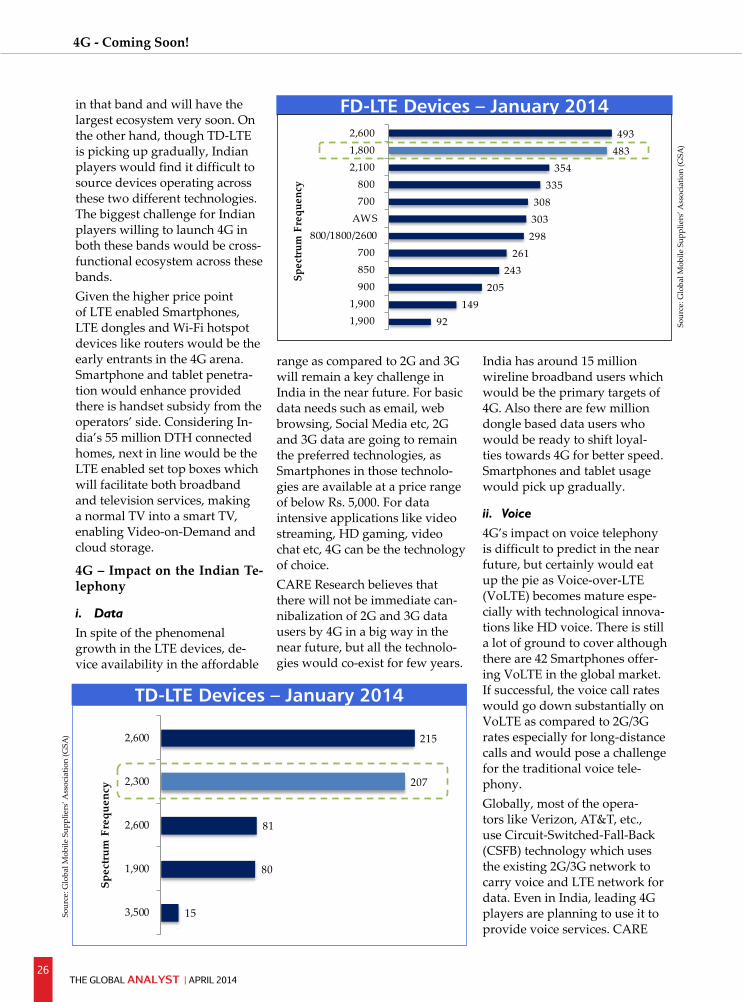

in that band and will have the largest ecosystem very soon. On the other hand, though TD-LTE is picking up gradually, Indian players would find it difficult to source devices operating across these two different technologies. The biggest challenge for Indian players willing to launch 4G in both these bands would be cross-functional ecosystem across these bands. Given the higher price point of LTE enabled Smartphones, LTE dongles and Wi-Fi hotspot devices like routers would be the early entrants in the 4G arena. Smartphone and tablet penetra-tion would enhance provided there is handset subsidy from the operators’ side. Considering In-dia’s 55 million DTH connected homes, next in line would be the LTE enabled set top boxes which will facilitate both broadband and television services, making a normal TV into a smart TV, enabling Video-on-Demand and cloud storage.

4G – Impact on the Indian Te-lephony

i. DataIn spite of the phenomenal growth in the LTE devices, de-vice availability in the affordable

India has around 15 million wireline broadband users which would be the primary targets of 4G. Also there are few million dongle based data users who would be ready to shift loyal-ties towards 4G for better speed. Smartphones and tablet usage would pick up gradually.

ii. Voice4G’s impact on voice telephony is difficult to predict in the near future, but certainly would eat up the pie as Voice-over-LTE (VoLTE) becomes mature espe-cially with technological innova-tions like HD voice. There is still a lot of ground to cover although there are 42 Smartphones offer-ing VoLTE in the global market. If successful, the voice call rates would go down substantially on VoLTE as compared to 2G/3G rates especially for long-distance calls and would pose a challenge for the traditional voice tele-phony. Globally, most of the opera-tors like Verizon, AT&T, etc., use Circuit-Switched-Fall-Back (CSFB) technology which uses the existing 2G/3G network to carry voice and LTE network for data. Even in India, leading 4G players are planning to use it to provide voice services. CARE

FD-LTE Devices – January 2014

Sour

ce: G

loba

l Mob

ile S

uppl

iers

’ Ass

ocia

tion

(GSA

)

range as compared to 2G and 3G will remain a key challenge in India in the near future. For basic data needs such as email, web browsing, Social Media etc, 2G and 3G data are going to remain the preferred technologies, as Smartphones in those technolo-gies are available at a price range of below Rs. 5,000. For data intensive applications like video streaming, HD gaming, video chat etc, 4G can be the technology of choice. CARE Research believes that there will not be immediate can-nibalization of 2G and 3G data users by 4G in a big way in the near future, but all the technolo-gies would co-exist for few years.

92 149

205 243

261 298 303 308

335 354

483 493

1,900 1,900

900 850 700

800/1800/2600AWS 700 800

2,100 1,800 2,600

Spec

trum

Fre

quen

cy

15

80

81

207

215

3,500

1,900

2,600

2,300

2,600

Spec

trum

Fre

quen

cy

TD-LTE Devices – January 2014

Sour

ce: G

loba

l Mob

ile S

uppl

iers

’ Ass

ocia

tion

(GSA

)

4G - Coming Soon!

The Global AnAlyst | aPRIl 2014 27

Research believes that CSFB would not have any substantial impact on voice-telephony as ul-timately 2G/3G networks would be used for voice. For CSFB, 4G operators with existing 2G or 3G operations would have an edge over a pure play 4G operators as the latter would have to tie up with a telecom operator for 2G voice and might have to give away some share of revenue.

Infrastructure Sharing – New Mantra for Quick TurnaroundNetwork infrastructure is one of the constraints for the launch of 4G as it requires good back-haul connectivity like Optical Fiber Cable (OFC) network. With Bharti’s 178,000 route km or (rkm), Rcom’s 190,000 rkm, Idea’s 80,000 rkm capacity and network from few other large players like BSNL and RailTel, existing network capacity offers opportunities for the 4G players to ink deals for sharing the OFC network similar to RJio-Rcom and RJio-Bharti deal. Simultane-ously, most of the players are in the process of increasing their own fiber capacity. Laying OFC is a capex intensive exercise as it requires Rs. 0.4-0.5 million per km on average, at times upto Rs. 100 million in Metros as the local governments charge exorbitantly for the Right of Way. On the tower front, India has over 400,000 towers spread across 22 circles owned by vari-ous telecom owned operators as well as third party operators. For the existing telecom opera-tors which provide 2G and 3G services, 4G roll-out would be relatively easy as the 4G Base Transceiver Station (4G) can be accommodated within the same premises as compared to a new entrants like Reliance Jio who will have to go for a complete greenfield roll-out. As there is

near over-supply situation in the tower business and also the new BTS are energy efficient, rentals for new deals are heading south, thus bringing down the roll- out costs for 4G operators.

Voice-over-LTE (VoLTE) – The ‘Achilles Heel’As India remains a voice-centric market with non-voice revenue contributing just 15-20 per cent to operators’ revenue, lack of cred-ible voice offering is keeping 4G on the back foot. Voice-over-LTE has been in the news for quite some time but has not yet estab-lished itself as a credible alterna-tive to the existing voice technol-ogy, even globally. In India on the regulatory front, 4G operators have been allowed to offer voice services by obtaining Unified License by paying Rs. 16.6 billion for a pan-India voice offering.Spectrum in 2300 MHz, auctioned in 2010 in India, is not suitable for carrying voice being in the higher frequency band. With the recently won spectrum in the 1800 MHz, operators would be able to effec-tively launch VoLTE if required. In spite of all the efforts to launch VoLTE, CSFB seems to be the technology of choice for the time being. Courtesy: CARE Research

4G Impact on IndustryThe impact of 4G is likely to be significant on the Indian telecom market when most of the Broadband Wireless Access (BWA) license holders will roll out LTE services across the nation in 2013. There will be substantial impact of 4G launch on the enterprise segment.LTE was first launched in Sweden in 2009. Growth has since been steady but slow, with exception of the United States, Canada, Japan and South Korea, which have seen faster take up. By end 2013, more than 200 operators in 75 countries will have launched a LTE network. About 300 LTE devices (smartphones, tablets and dongles) are expected to be available by year-end, including a growing range of sub-$100 smartphones. New pan-India players are likely to enter the market with 4G services soon. Lack of 4G-enabled devices working on 2300 MHz band are expected to be fulfilled by Mi-F, which will convert 4G signals into Wi-Fi signal, hence, extending its reach to all current smartphones, tablets, laptops and other devices in the market. This could impact the other players, both in 4G, as well as, 3G. LTE is more efficient in carrying data than 3G networks over a given amount of radio spectrum, meaning that the cost to the operator of carrying a gigabyte of data on an LTE network should be several factors lower than for 3G. Customers using 3G may move their relatively high data usage to LTE networks triggered by the availability of higher speeds. This is likely to be a disruptive trend for the 3G service providers who have paid large amounts towards license fees and infrastructure. Also the other 4G players (having 4G license in fewer circles) could be impacted with these low tariffs and bundled device offers. The launch of 4G will also be disruptive for fixed line broadband (although the penetration levels are not high). Due to the lack of optic fiber infrastructure, the bandwidth offered on fixed line in India is far from being competitive with 4G. Courtesy: Deloitte Research

Anand Kulkarni

4G - Coming Soon!