403(b) retirement plan compliance gary mauger and christine dailey managing partners (704) 900-5566...

TRANSCRIPT

403(b) Retirement Plan Compliance

Gary Mauger and Christine Dailey

Managing Partners

(704) 900-5566

www.newpcg.com

Agenda

Key 403(b) regulations First year audit findings Employer responsibilities Next steps Resources for help Questions and discussion

New 403(b) Regulations

Major Changes and Requirements Written plan document Nondiscrimination testing changes Transfers In-service distributions Form 5500

New 403(b) Regulations

Written Plan Document Required for ERISA and non-ERISA plans Must be congruent with vendor

contracts/custodial agreements SPD requirements

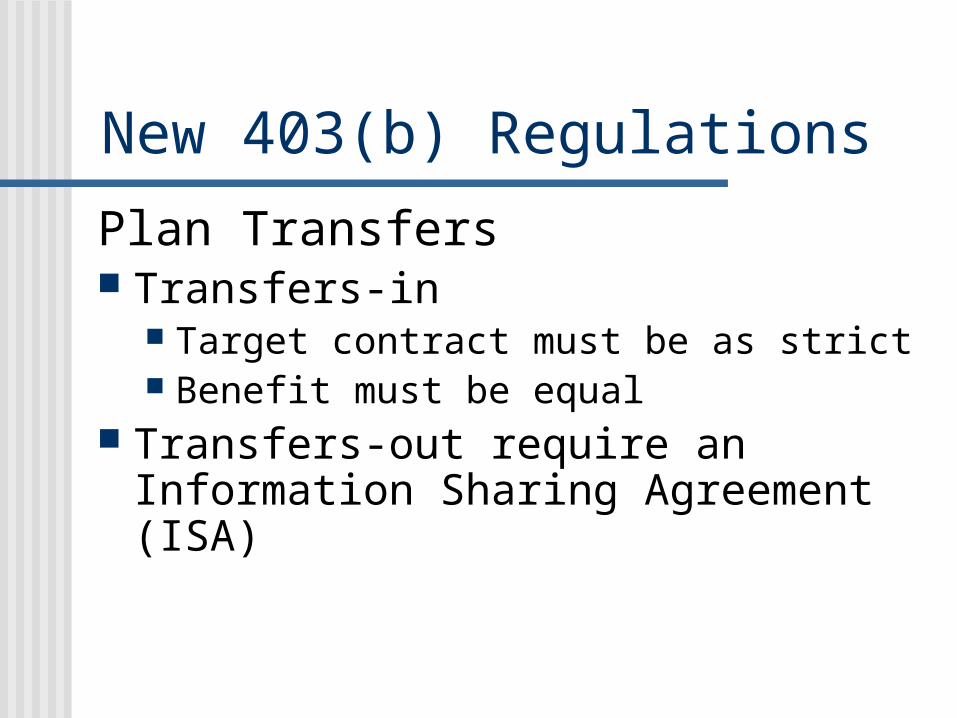

New 403(b) Regulations

Plan Transfers Transfers-in

Target contract must be as strict Benefit must be equal

Transfers-out require an Information Sharing Agreement (ISA)

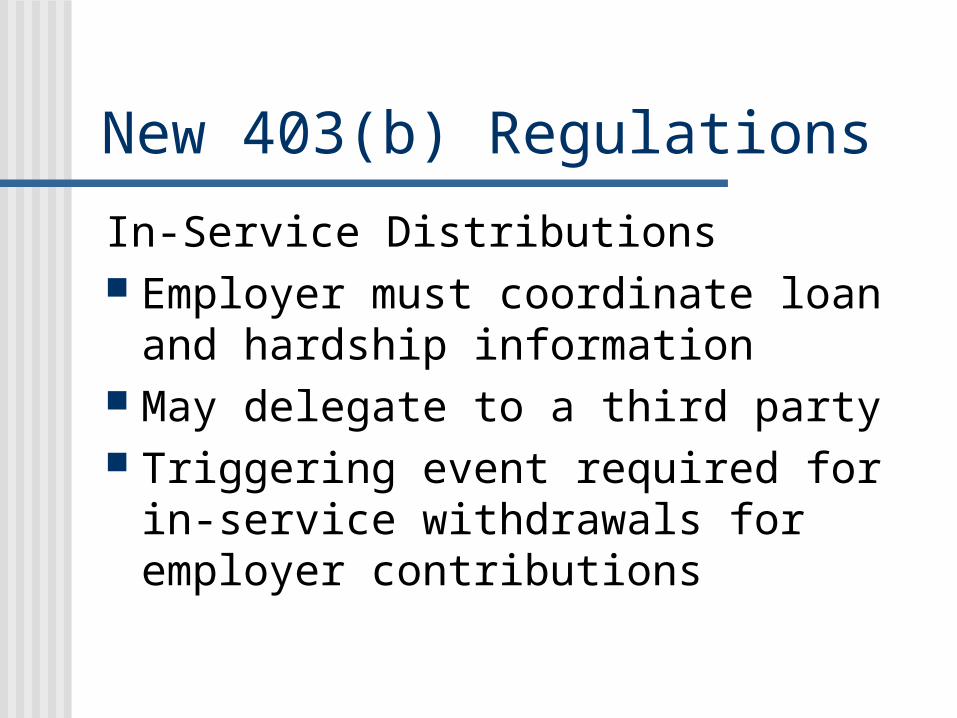

New 403(b) Regulations

In-Service Distributions Employer must coordinate loan and

hardship information May delegate to a third party Triggering event required for in-service

withdrawals for employer contributions

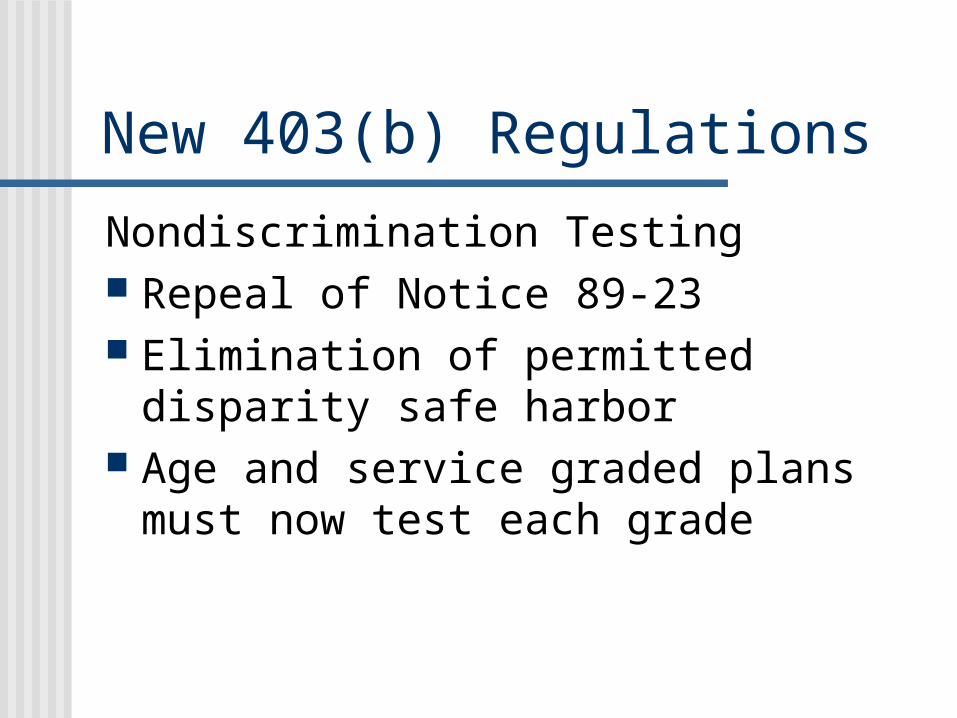

New 403(b) Regulations

Nondiscrimination Testing Repeal of Notice 89-23 Elimination of permitted disparity safe

harbor Age and service graded plans must now

test each grade

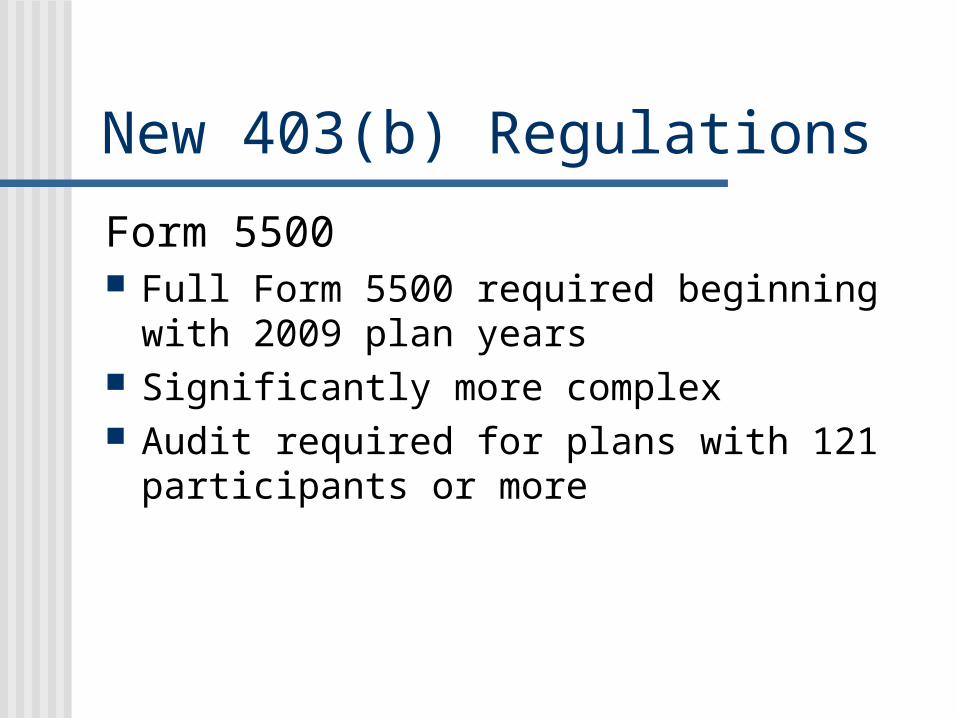

New 403(b) Regulations

Form 5500 Full Form 5500 required beginning with 2009

plan years Significantly more complex Audit required for plans with 121 participants or

more

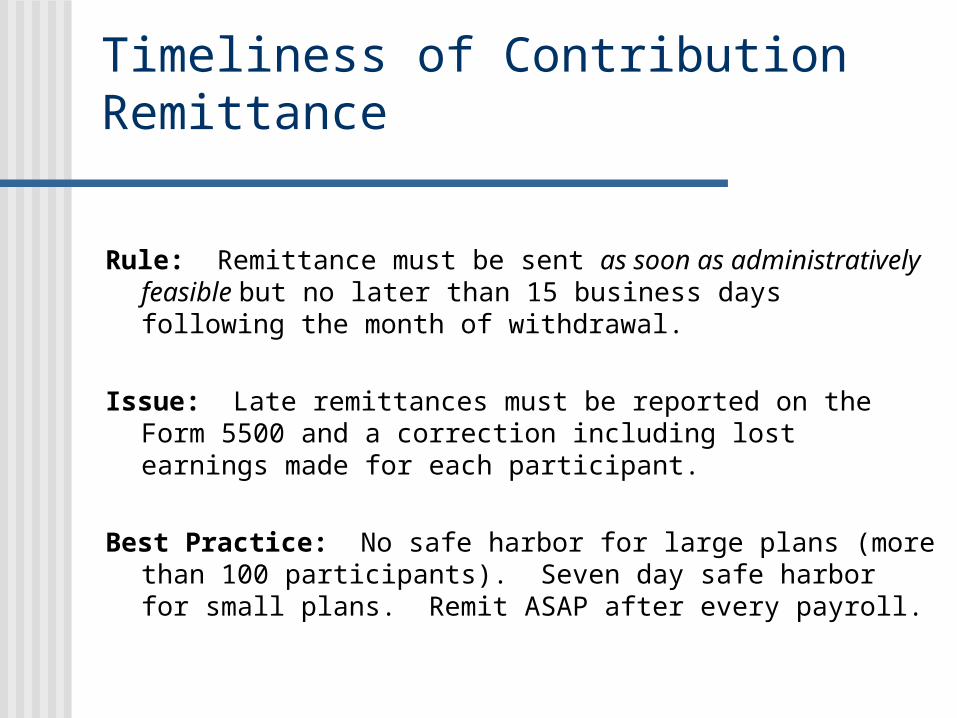

Timeliness of Contribution Remittance

Rule: Remittance must be sent as soon as administratively feasible but no later than 15 business days following the month of withdrawal.

Issue: Late remittances must be reported on the Form 5500 and a correction including lost earnings made for each participant.

Best Practice: No safe harbor for large plans (more than 100 participants). Seven day safe harbor for small plans. Remit ASAP after every payroll.

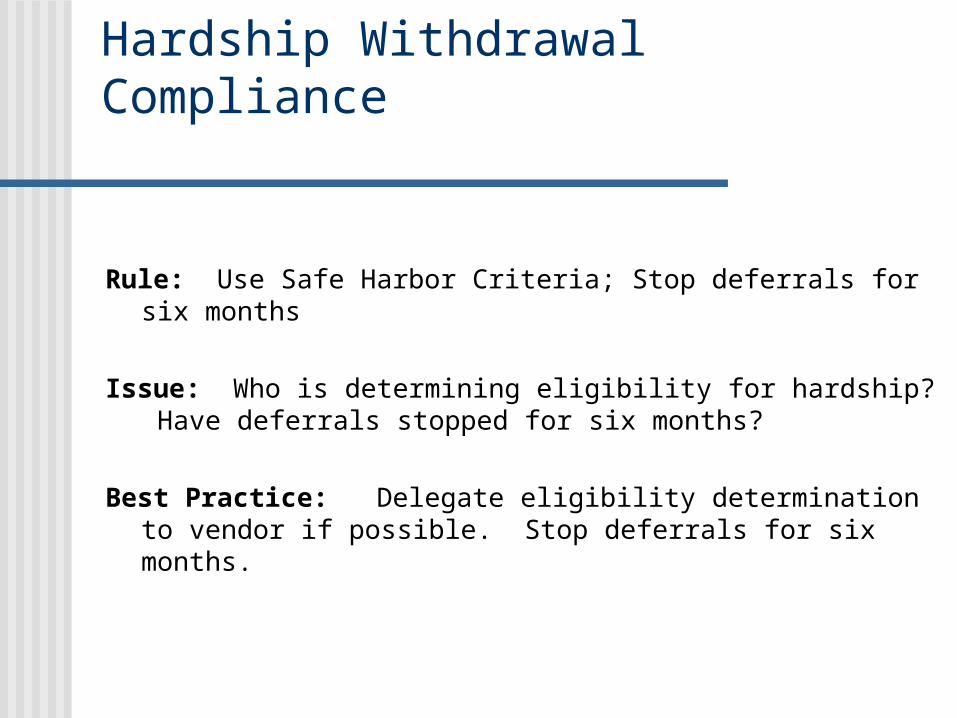

Hardship Withdrawal Compliance

Rule: Use Safe Harbor Criteria; Stop deferrals for six months

Issue: Who is determining eligibility for hardship? Have deferrals stopped for six months?

Best Practice: Delegate eligibility determination to vendor if possible. Stop deferrals for six months.

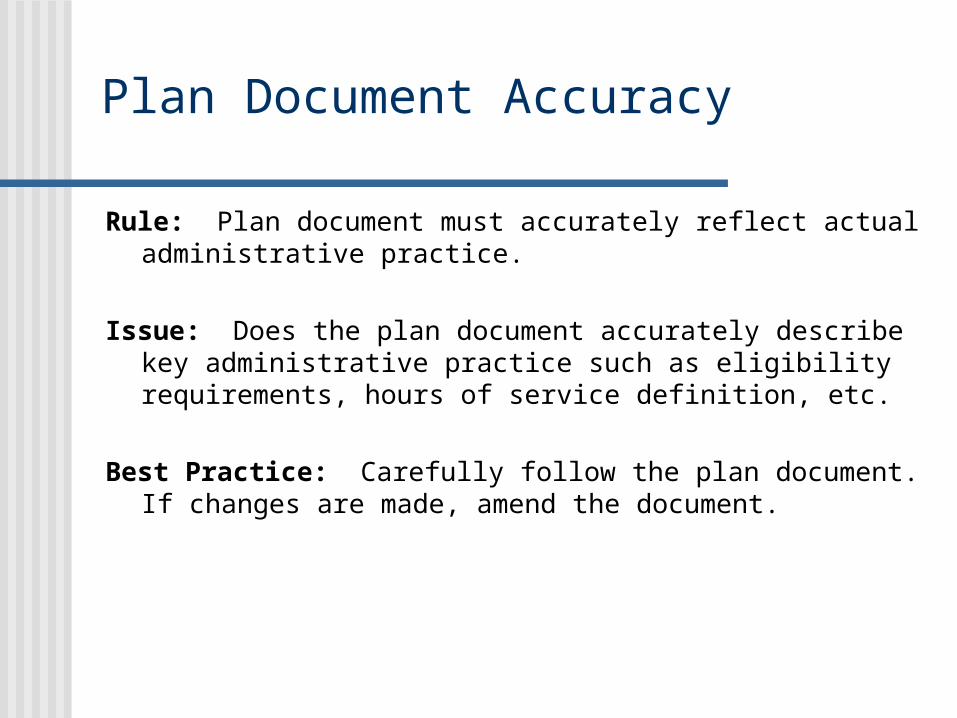

Plan Document Accuracy

Rule: Plan document must accurately reflect actual administrative practice.

Issue: Does the plan document accurately describe key administrative practice such as eligibility requirements, hours of service definition, etc.

Best Practice: Carefully follow the plan document. If changes are made, amend the document.

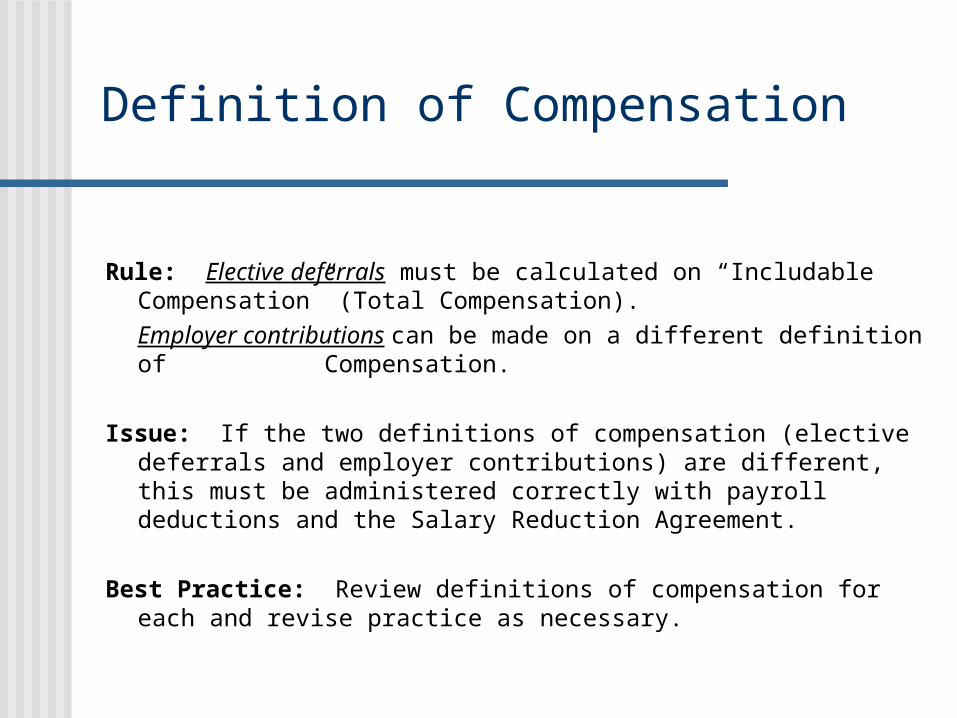

Definition of Compensation

Rule: Elective deferrals must be calculated on “Includable Compensation” (Total Compensation).

Employer contributions can be made on a different definition of Compensation.

Issue: If the two definitions of compensation (elective deferrals and employer contributions) are different, this must be administered correctly with payroll deductions and the Salary Reduction Agreement.

Best Practice: Review definitions of compensation for each and revise practice as necessary.

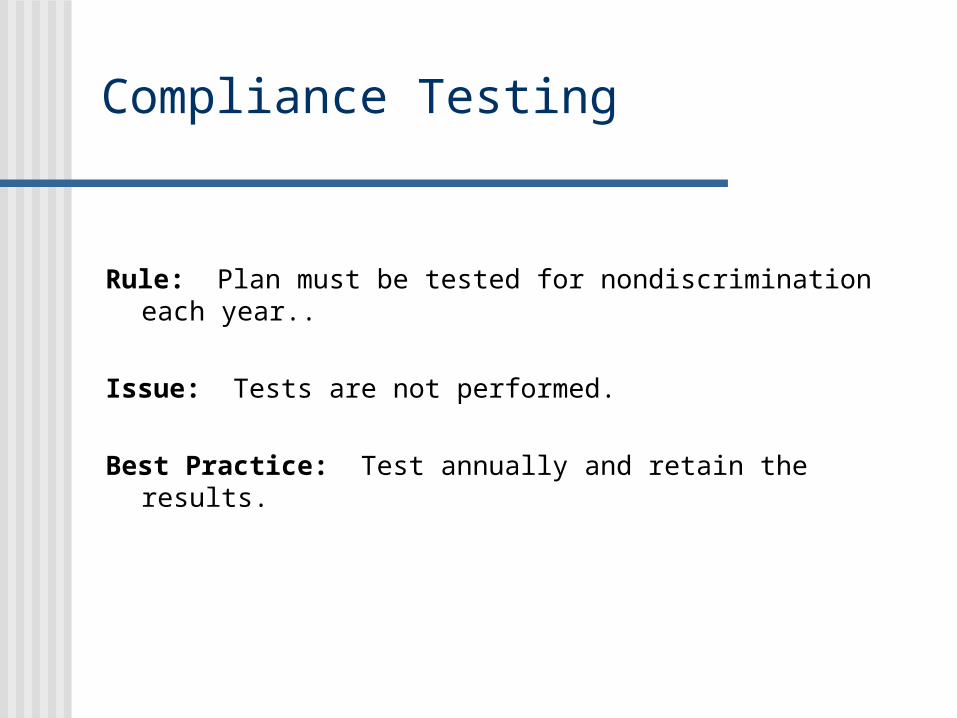

Compliance Testing

Rule: Plan must be tested for nondiscrimination each year..

Issue: Tests are not performed.

Best Practice: Test annually and retain the results.

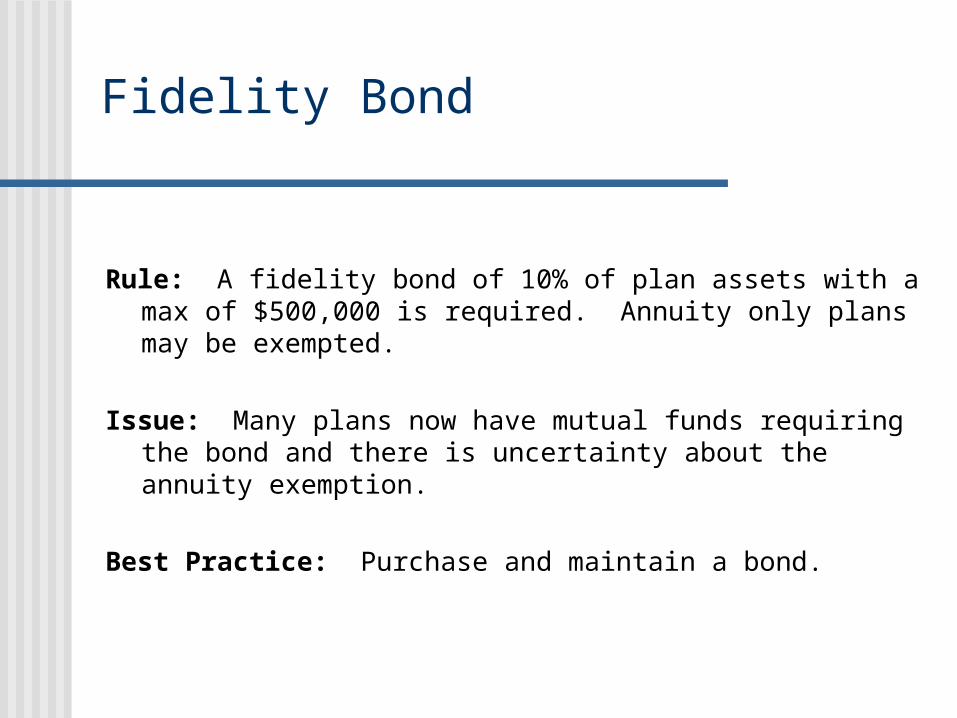

Fidelity Bond

Rule: A fidelity bond of 10% of plan assets with a max of $500,000 is required. Annuity only plans may be exempted.

Issue: Many plans now have mutual funds requiring the bond and there is uncertainty about the annuity exemption.

Best Practice: Purchase and maintain a bond.

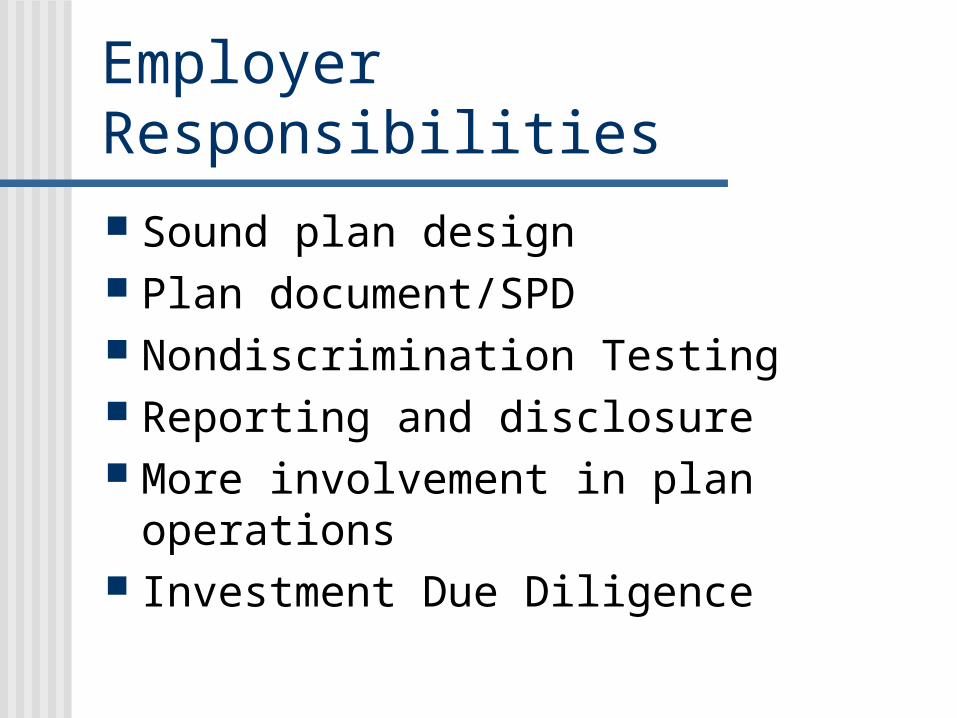

Employer Responsibilities

Sound plan design Plan document/SPD Nondiscrimination Testing Reporting and disclosure More involvement in plan operations Investment Due Diligence

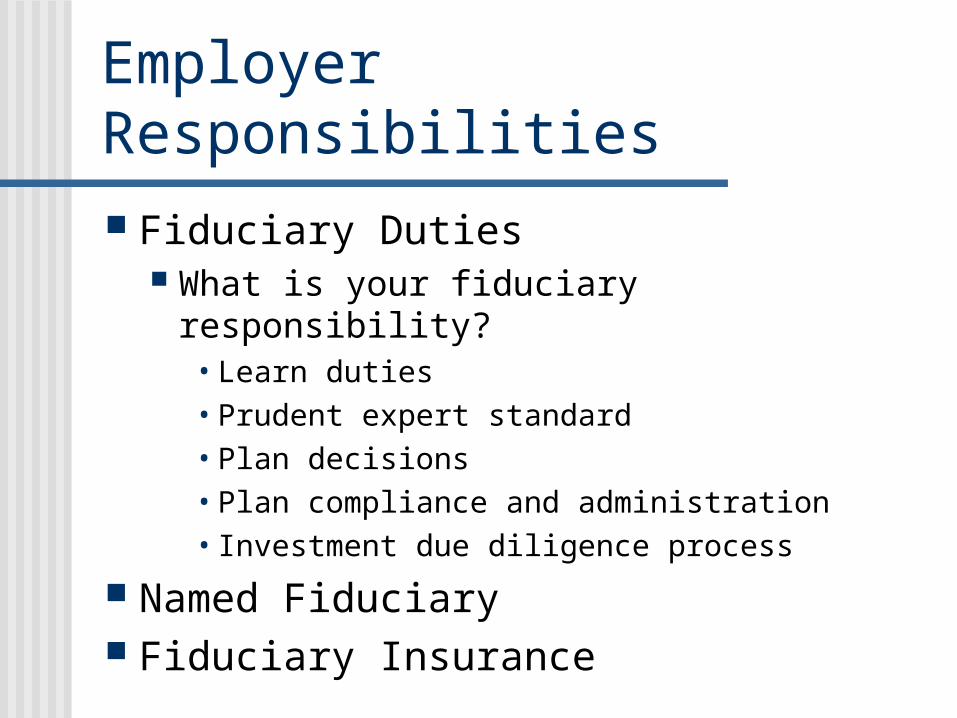

Employer Responsibilities

Fiduciary Duties What is your fiduciary responsibility?

• Learn duties• Prudent expert standard• Plan decisions• Plan compliance and administration• Investment due diligence process

Named Fiduciary Fiduciary Insurance

Next Steps

Compliance Audit Adherence to Plan Document Provisions Nondiscrimination Testing Required Reporting and Disclosure Investment Due Diligence Process

Resources

Advisor Vendor information Consultant Regulator publications

Resources Links Final 403(b) Regulations:

http://www.treasury.gov/press/releases/hp501.htm

IRS Information: http://www.irs.gov/retirement/article/0,,id=172430,00.html

Department of Labor Bulletin: http://www.dol.gov/ebsa/regs/fab2007-2.html

Questions and Discussion

Gary Mauger and Christine Dailey

Managing Partners

New Pinnacle Consulting Group, LLC

(704) 900-5566

www.newpcg.com