31march2009 schroderexempt · pdf filestatement of net assets 41 income and expenditure...

TRANSCRIPT

Schro

derExem

ptProperty

Unit

TrustANNUALREPORTANDAUDITEDFINANCIALSTAT

EMENTS

31MARCH2009

31 March 2009

Schroder ExemptProperty Unit TrustAnnual Report and AuditedFinancial Statements

Schroder Exempt Property Unit Trust31 Gresham Street, London EC2V 7QAwww.schroders.com/seput www.schroderproperty.com

designed

&prod

ucedbyto

thepoint,

london

0207378

6999ref8268

printed

bywilliam

slea,

londonwww.schroderproperty.com

Frontcover:London

EC1,4-7

Chisw

ellStreet

www.schroders.com/seput

Investment Objective and PolicySchroder Exempt Property Unit Trust (‘SEPUT’ or the ‘Trust’) wasestablished in 1971 as an open ended property unit trust under UK law.

The investment objective of the Trust is to achieve a blend of income andcapital growth for investors through investment in UK property. Risk isdiversified by the Trust holding a mixed portfolio of retail, office, industrialand other property (including leisure and alternative investments such asstudent accommodation) throughout the UK. The Trust may also hold landand undertake developments as well as use moderate levels of gearingfrom time to time.

The Trust incorporates a blend of direct and indirect investmentstrategies. Indirect investments provide further diversification byaccessing distinct areas of the UK property market, such as fashionparks, some larger properties, and specialist management associatedwith the alternative sectors.

The Trust seeks to provide a return of 0.5% per annum (net of fees) aboveits benchmark (Investment Property Databank UK Pooled Property FundIndices – All Balanced Funds Median) over rolling three year periods.

The Trust may be suitable for UK tax exempt pension funds and charitieswho wish to hold a direct property portfolio without the commitment ofconsiderable trustee oversight and management expertise. The propertyin the Trust is professionally and actively managed by chartered surveyorsemployed by the Property Manager, Schroder Property InvestmentManagement Limited.

The Manager welcomes the opportunity to meet unitholders, potentialunitholders and their advisers to explain more fully the strategy andprogress of the Trust. In this regard please contact either Hanne Hootonor Tamsin Frost.

Schroder Exempt Property Unit TrustSchroder Property Investment Management Limited31 Gresham StreetLondon EC2V 7QATel: +44 (0)20 7658 6000

Further information can be found on the websitewww.schroders.com/seput

01

Contents

REPORTS

FINANCIALSTATE

MENTS

02 Supervisory Board and Key Service Providers

03 Trust Analysis

06 Chairman’s Statement

09 Manager’s Statement

26 Purchases and Sales

27 Details of the Portfolio

35 Responsibilities of the Manager,Trustee and Supervisory Board

36 Independent Valuer’s Report to the Unitholders

37 Independent Auditor’s Report

40 Statement of Net Assets

41 Income and Expenditure Account

42 Statement of Total Recognised Gains and Losses

43 Cash Flow Statement

44 Notes to the Financial Statements

63 Additional Unitholder Information

66 Debt Analysis

67 General Meeting and General Information

02 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

Supervisory Board andKey Service Providers

Supervisory BoardH van der Klugt FCA (Chairman)* Humphreyvan der Klugt was a Director of SchroderInvestment Management Limited until hisretirement in 2004. Prior to joining Schrodersin 1982, he qualified as a Chartered Accountantwith KPMG. He is a non-executive Directorof Murray Income Trust PLC, BlackRockCommodities Income Investment Trust PLC,JPMorgan Claverhouse Investment Trust plcand Fidelity European Values PLC. Joined theSupervisory Board in 2002.

Professor A E Baum PhD FRICS AndrewBaum is Professor of Land Management at theUniversity of Reading, non-executive Chairmanof Cartesia Ltd and Chairman of PropertyFunds Research. Joined the SupervisoryBoard in 1999.

R R FoulkesRichard Foulkes was Vice Chairman ofSchroder Investment Management Limiteduntil his retirement in October 2005. He is anon-executive Director of Credit RenaissanceStructured Product Fund, Schroder PensionTrustee Limited and Schroder Credit RenaissanceFund; a member of the Investment Committeeof the Royal Opera House Pension Schemeand of Queens’ College, Cambridge. He is alsothe Chairman of the Investment Committee ofSt John Ambulance. Joined the SupervisoryBoard in 2003.

C J Hunter FRICSCharles Hunter was Head of Property at InsightInvestment (the investment managementsubsidiary of HBOS plc) for nine years until2004. Prior to that he was Property Directorof NM Fund Management. He is non-executiveChairman of AXA Property Trust plc and anon-executive Director of Lands ImprovementHoldings plc, and Protego Real Estate Fundsplc, and is Trustee of St Monica Trust. Joinedthe Supervisory Board in 2006.

R I Moore FSI*Roger Moore was previously Head of PropertyResearch at UBS Warburg. He is a foundermember of the BDO Stoy Hayward PropertyAccounts Awards judging panel. Joined theSupervisory Board in 2004.

J A Scott OBE FCA*James Scott is a former National ManagingPartner of Binder Hamlyn. He is currently anon-executive Director of the Vestey GroupLimited and Chairman of the Trustees of theLonmin Superannuation Scheme. Joined theSupervisory Board in 1991.

A F SykesAndrew Sykes was a Director of Schroders plcuntil March 2004. He is Chairman of InvistaFoundation Property Trust Limited, Chairman ofAbsolute Return Trust Limited, a non-executiveDirector of JP Morgan Asian Investment TrustPLC, Smith and Williamson Holdings Limited,Record plc, MBIA UK Insurance Limited,Schroder Pension Trustee Limited and GulfInternational Bank UK Limited. Joined theSupervisory Board in 2004.

Key Service ProvidersManager and Property ManagerSchroder Property InvestmentManagement Limited31 Gresham StreetLondon EC2V 7QA

Authorised and regulated bythe Financial Services Authority.

I D Mason MRICSIan Mason is Head of UK Property FundManagement for Schroders and is FundManager of the Trust. He has a BSc (Hons) inLand Management, is a member of the RoyalInstitution of Chartered Surveyors, a boardmember of the Association of Real EstateFunds (AREF) and Chair of AREF’s RegulationSub-Committee. Ian joined Schroders in April2008 after 23 years at BlackRock where he wasmanager of the BlackRock UK Property Fund.

N D Meredith MRICSNeil Meredith is Head of UK Property AssetManagement for Schroders and works principallyon the Trust’s portfolio. He has a BSc in LandManagement and is a member of the RoyalInstitution of Chartered Surveyors. Neil joinedSchroders in October 2006. Before joiningSchroders, he worked for English Welsh andScottish Railways Limited as Head of PropertyServices Group from 2004 to 2006. From 2003to 2004 he was a Director of GVA Connect atGVA Grimley. Prior to that he was a Partner atCushman & Wakefield, where his propertycareer started in 1982.

* J A Scott is the Chairman and H van der Klugt andR I Moore are members of the Audit Committee.

Peter Cooper MRICSPeter Cooper is responsible for UK retail assetmanagement strategy and the SchroderEmerging Retail Property Unit Trust (SERPUT).He has a BSC in Land Management and is amember of the Royal Institution of CharteredSurveyors. Peter joined Schroders in 2006.Before joining Schroders he was Retail Directorat Allied London Properties Ltd from 1997-2005. From 1994-1997 he was a Director ofRaglan Properties Plc. Prior to that he was aretail manager at Hillier Parker from 1987-1994and between 1984 and 1987 a RegionalProperty Manager at British Gas.

Mark Callender BA (Economics)Mark Callender is Head of Property Research.He joined Schroders in 2006. Before joiningSchroders he was Research Director forsixteen years at IPD, the leading providerof property market research and indices.1987-1990 he was Chief Economist at theHouse Builders Federation. He is a memberof the Society of Property Researchers, theInvestment Property Forum and thePan-European Common Interest Group.

W A Hill MRICS C Dip AFWilliam Hill is Head of Property for Schroders.He has a BSc (Hons) in Land Managementand a Certified Diploma in Accounting andFinance. He is a member of the RoyalInstitution of Chartered Surveyors and pastChairman of the Association of Real EstateFunds (AREF). Prior to joining Schroders in1989, William worked for seven years withDrivers Jonas. He is a member of SchrodersGlobal Investment Executive Committee.

TrusteeThe Royal Bank of Scotland plcThe Broadstone50 South Gyle CrescentEdinburgh EH12 9UZ

Independent AuditorPricewaterhouseCoopers LLPHay’s Galleria1 Hay’s LaneLondon SE1 2RD

Independent ValuerAtisreal LimitedNorfolk House31 St James’s SquareLondon SW1Y 4JR

03

Trust Analysis

SizeDuring the period the net asset value of the Trust decreased by £514.3 million, from £1,536.8million at 31 March 2008 to £1,022.5 million at 31 March 2009.

Distribution YieldThe Trust’s distribution yield was 5.4% at 31 March 2009 compared to 3.7% at 31 March 2008.

Net Asset Value per UnitThe Trust’s net asset value per unit was £29.45 at 31 March 2009, compared to £44.19 at 31March 2008, a decrease of 33.4%.

Trust Benchmark* IPD UK Pooled Property Fund Indices- All Balanced Funds Index Weighted Average

Source: Investment Property Databank (IPD) UK Pooled Property Fund Indices. Performance is calculated on anet asset value (NAV) to NAV price basis plus income distributions accrued for the relevant periods, compounded monthly,net of fees and based on an unrounded NAV per unit.

* Benchmark shown is the IPD UK Pooled Property Fund Indices - All Balanced Funds Index Median. The Trust benchmark haschanged over time and a composite for 10 years is available upon request.

The Weighted Average is shown for illustration purposes and is used for detailed analysis of the Trust’s property portfolio as theMedian does not provide appropriate detail.

Total ReturnsTwelve month performance %to 31 March

Annualised performance %to 31 March 2009

1 year

-30.4

-26.2

-27.1

-10.7

-7.9

-8.9

3 years

5 years

0.5

2.0

1.5

10 years

5.1

6.3

6.0

-10.7

2009

-30.4

-26.2

-27.1

-13.9

-11.5

-11.1

2008

2007

18.7

16.7

16.6

2006

22.4

20.3

21.0

2005

17.9

17.8

17.8

04 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

Asset Management AchievementsRent Reviews

In the directly held portfolio 29 rent reviews were settled totalling £5.1 million per annum, reflectingan uplift of 12.8% on the old rent and 9.1% on estimated rental value (ERV).

Notable rent reviews

Old Rent ERV New RentProperty Tenant (per annum) (per annum) (per annum)

Parker Tower Unit Trust British Telecommunications Plc £1,950,000 £2,135,000 £2,289,500

Crayford, Acorn Industrial Estate 15 tenancies £702,306 £764,554 £798,111

Cardiff, Cardiff Bay Retail Park 3 tenancies £247,826 £255,226 £294,156

New Lettings

In the directly held portfolio 25 new lettings were completed adding £1.8 million per annum to the rent roll.

Notable new lettings

Old Rent ERV New RentProperty Tenant (per annum) (per annum) (per annum)

London W14, Kensington Village Blue Marlin Design Limited n/a £680,500 £653,759Universal Music Operations Limited

Manchester, 8/10 Exchange Street Fat Face Limited n/a £567,000 £567,500Henri-Lloyd LimitedFloral Limited (trading as Camper Shoes)Rohan Designs Limited

Woking, Woking Business Park Carrier Rental Systems (UK) Limited n/a £123,600 £128,798Jennifer Ulisse LimitedISS Facility Services LimitedMcLaren Automotive Limited

Lease Renewals

In the directly held portfolio seven leases were renewed totalling £678,000 per annum, reflectingan uplift of 1.6% on the old rent and approximately 4.8% below estimated rental values.

Notable renewals

Old Rent ERV New RentProperty Tenant (per annum) (per annum) (per annum)

Bracknell, Unit 11 Bracknell Beeches Overbury Plc £152,646 £104,100 £137,000

Manchester, 8/10 Exchange Street Tushingham Moore LLP £100,201 £114,700 £114,094Cobalt Consulting (UK) Limited

Trust Analysis (continued)

05

Portfolio by SectorOverweight/underweight relative to benchmark*

Source: IPD, 31 March 2009. Subject to rounding.

* IPD UK Pooled Property Fund Indices – All Balanced Funds Index Weighted Average (% Gross Asset Value (GAV)): March 2008 and March 2009.The weighted average has been used as this level of information is not available in the median.

March 2008March 2009

Planning Initiatives for the RecoveryBracknellCompulsory Purchase Order confirmed to allow site assembly to be completed.

CroydonCroydon Council’s Compulsory Purchase Order against the site was not confirmed by theSecretary of State for Communities and Local Government. The property adviser is now workingconstructively with Croydon Council on the redevelopment of this key site. The mixed usescheme is to be known as Ruskin Square and is designed by Foster & Partners.

HackbridgeSutton Council has identified this site for major sustainable regeneration. The investment visionis a mixed use scheme incorporating mainly residential with retail community/leisure andemployment use. The property adviser is working to secure outline planning permission forlonger term redevelopment.

Void Profile31 March 2008 SEPUT(%) IPD (%)²

Void rate (as a % of estimated rental value 6.9 8.0of total portfolio excluding developments)¹

31 March 2009

Void rate (as a % of estimated rental value 8.0 10.4of total portfolio excluding developments)¹Source: IPD, 31 March 2009

1 Henderson and AH Medical at Q4 2008. UNITE is excluded2 IPD UK Monthly All Property Index, March 2009

Retail W

areho

uses

Standa

rdReta

il

– Rest o

f UK

Shopp

ingCen

tres

Offices

– Rest o

f UK

Offices

– Wes

t End

&M

idTo

wnOffices

– City Offices

– Rest o

f

South

Easter

nInd

ustria

ls

– South

Easter

n Cash

Other

Prope

rty

Indus

trials

– Rest o

f UK

Listed

Inves

tmen

ts

Standa

rdReta

il

– South

Easter

n

0.0

-5.9 -5.6

-1.5-0.6

-2.1 -1.4 -1.1

-2.9

-5.9

-2.9

-5.8-8.9

-8.0

0.71.9

7.5 7.88.7

5.4 6.1

3.1 2.41.1 1.8

6.1

06 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

Chairman’s Statement

OverviewDuring the year ending 31 March 2009 theperformance of the Trust has been affected bythe continuing impact of the global credit crisisand the deepening of the UK economicdownturn. Liquidity is still to return to thecommercial property market. Whilst there aresome signs of easing, market conditions arevery challenging. As a result, the Trust hassuffered a fall in its net asset value as propertyvalues across sectors have continued todecline. Since the peak in the UK commercialproperty market in June 2007, capital valueshave now fallen by over 40% (source: IPD UKMonthly Property Index).

Net Asset ValueDuring the twelve months to 31 March 2009,the net asset value per unit decreased by 33.4%from £44.19 to £29.45. Over the period underreview, the Trust’s total net asset valuedecreased by £514.3 million (33.4%), from£1,536.8 million at 31 March 2008 to £1,022.5million at 31 March 2009 as falling capital valuesand some redemptions impacted the Trust.

Units in Issue andSecondary MarketAt 31 March 2009, the Trust had 460unitholders, the largest of which held 3.9%of the units in issue. During the year no unitswere created on the primary market.

Redemptions have been at a low level.However, where they have taken place, theManager has continued with a policy ofapplying an adjustment to the net asset valueof the Trust in calculating the redemption price,in order to take account of the exceptionalmarket conditions into which assets would besold. 54,579 units were redeemed during theyear, resulting in a fall in the number of units inissue of 0.2%, from 34,783,299 to 34,728,720.

Activity on the secondary market was alsolimited, with 132 matched bargain tradestotalling £13.4 million.

PerformanceThe total return for the Trust for the twelvemonths under review was -30.4%,underperforming the benchmark, the IPD UKPooled Property Fund Indices – All BalancedFunds Median, which returned -26.2%. Theabsolute performance demonstrates the effecton the Trust of the severity of the marketconditions. The longer term record over three,five and ten years has also been negativelyimpacted so that the Trust’s returns have alsolagged the benchmark over these periods. Ananalysis of relative performance is provided inthe Manager’s Statement.

Whilst the relative performance of the directlyheld standing investments has been broadly inline with the IPD benchmark over the year, theperformance of the indirect investments held bythe Trust has been disappointing. This hasbeen largely due to debt held within a numberof the indirect investments, which has had ageared effect on the decline in values. TheTrust’s land holdings being held for futuredevelopment have, in the absence of anycontracted income, also performed poorly ina falling property market.

The recessionary pressures in the UK economyhave continued since the banking crisis in thefinal quarter of last year. Unemployment figureshave risen to over two million for the first timesince 1997, and UK GDP is expected to fall by-4.5% during 2009 (source: Schroders).Investment transactional activity remains weak,reflecting in part the lack of liquidity in thebanking sector. In the immediate future furtherdownward valuations are expected. However,there is evidence that the outlook for someareas of the property market is beginningto improve.

Trust DeedIn November 2008 the redemption policy wasamended by resolution of the unitholders. Thepurpose of the amendments was to allowgreater flexibility in the redemption process,together with a clearer pricing structure. TheSupervisory Board believes that the changesmade to the Trust Deed will be helpful in themanagement of the Trust.

07

H van der KlugtChairmanSchroder ExemptProperty Unit TrustSupervisory Board16 June 2009

Investment andBorrowing GuidelinesThe Supervisory Board is responsible forensuring that the Manager operates within theagreed investment and borrowing guidelines.The guidelines have been set in order toprotect the interests of unitholders and arereviewed on a regular basis. There are nobreaches to report against the currentguidelines.

The Manager would be pleased to give furtherdetails of the guidelines to unitholders on request.

GearingAt 31 March 2009 the Trust’s direct borrowingswere £5.0 million, representing 0.5% of the netasset value. To the extent that there has beendebt during the year, this has been drawn onthe Trust’s £100 million loan facility with LloydsTSB Banking Group; it has been used typicallyfor transactional purposes. There is, however,also debt within a number of the indirectinvestments held by the Trust, which is fullydisclosed in note 4(c) of the FinancialStatements and in the debt analysis tableshown on page 66.

The borrowing guideline set by the SupervisoryBoard is for a maximum debt level of 25.0% ofunitholders’ funds (including the Trust’s share ofdebt within the indirect vehicles). At the start ofthe financial year, gearing was 18.2% but by 31March 2009 this had risen to 20.6%, almostentirely due to the effect of falling asset values.Should asset values continue to fall, thengearing will rise further. In addition, a number ofthe indirect investments need to manage theirown debt situations in relation to their bankingcovenants. This is a situation that theSupervisory Board is monitoring closely toensure that appropriate action is taken wherepossible by the Manager.

GovernanceWith effect from 1 April 2009, the SupervisoryBoard formally appointed Schroder InvestmentManagement Limited as the CorporateSecretary to the Trust.

The Supervisory Board is satisfied that theTrust has been managed in accordance withthe guidelines set and with due regard tosound governance practice.

OutlookThe current market conditions areunprecedented. However, the Manager believesthat we may have seen the worst of the falls incapital values although rental values are likelyto fall further. As outlined in the Manager’sReport an investment strategy is in place toaddress the current market challenges and tobenefit from any upturn in markets. There aresome signs of improvement which it is hopedwill strengthen in the current year.

Vacant possession of retailobtained in early 2008

Redeveloped to provide doubleheight shopfronts and twounits split to into four wellconfigured retail units

Pre-lets agreed to:– Links (London) Limited– Fat Face Limited– Henri-Lloyd Limited– Floral Limited

(trading as Camper Shoes)

Opened for tradingChristmas 200808 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

09

Manager’s Statement

UK Property Market Review and OutlookThe year to 31 March 2009 has been a very challenging period for the UK commercial propertymarket as the credit crisis continued, the global economic downturn gathered pace, and the UKeconomy entered recession. There were large falls in value with the IPD UK Monthly Property Indexproducing a total return for All Property of -25.5% in the year to end March 2009. The falls werepredominantly driven by rising property yields and, more recently, declining rental values. The rateof decline has slowed in more recent months (source: IPD UK Monthly Property Index).

All sectors in the IPD UK Monthly Property Index produced negative returns over the year. Officetotal returns to 31 March 2009 were -25.9% whilst retail property fared worse, returning -27.1%.Industrial returns were -21.4%.

Investment transaction activity fell by 59.5%, from £47.4 billion in the year to 31 March 2008 to£19.2 billion in the year to 31 March 2009 (source: The Property Investors Bulletin, April 2009).Bank lending was restricted and only available at higher margins than previously offered. Despitethe gathering economic downturn many sellers were slow to recognise this in their pricingexpectations. In contrast the few buyers in the market were looking for bargains, creating a standoff with the sellers. As a result, there was a disconnect between valuations in the property marketindices and actual transactional prices for assets. There was virtually no market for units in closedended property funds. Many of these have borrowings. Fears over breaching loan to valuecovenants meant any trades were at big discounts to published net asset values (NAVs), despitethe quality of the underlying property assets. It was therefore a difficult environment for valuers withthe low level of transactions limiting valuation evidence.

Mar

89

Mar

91

Mar

93

Mar

95

Mar

97

Mar

99

Mar

01

Mar

03

Mar

05

Mar

07

Mar

09

40

30

20

10

0

-10

-20

-30

-40

%

Components of UK Property Market ReturnsRolling 12 Month IPD Monthly Returns to 31 March 2009

Income return Total returnRental value growth

Source: IPD UK Monthly Property Index, 31 March 2009

Yield impact

10 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

Manager’s Statement (continued)

-10,000

-8,000

-6,000

2,000

0

4,000

6,000

Institutions Property Companies Private InvestorsOverseas Investors Others

Net Investment £ million

-4,000

-2,000

8,000

UK Commercial Property Net InvestmentYear to 31 March 2009

Purchases Sales Net Investment

Source: The Property Investors Bulletin

UK Property Market Review and Outlook(continued)

Surprisingly, since the property market peak in June 2007, prime property fell more than secondaryproperty, perhaps reflecting a lack of transactions in the latter part of the market (source: PropertyData/CBRE). However, this trend began to reverse in the second half of the period as investorsfocused on the risks of lower quality assets (especially focusing on income security) as the UKeconomic environment deteriorated. We expect prime to outperform secondary property over thecoming year. The level of property market voids as a percentage of the IPD UK Monthly PropertyIndex total rental value, rose from 8.0% at the end of March 2008 to 10.4% at the end of March2009.

-20

-10

0

10

20

30

40

-40

-20

20

40

60

80

100

120

0

1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008

Rents are generally affordableLimited new supply in most locations

Real rental values Building starts (right hand scale)

Source: IPD UK Annual Property Index, ONS, Schroders to 31 December 2008

Real rents, % deviation from trend Starts, % deviation from trend

11

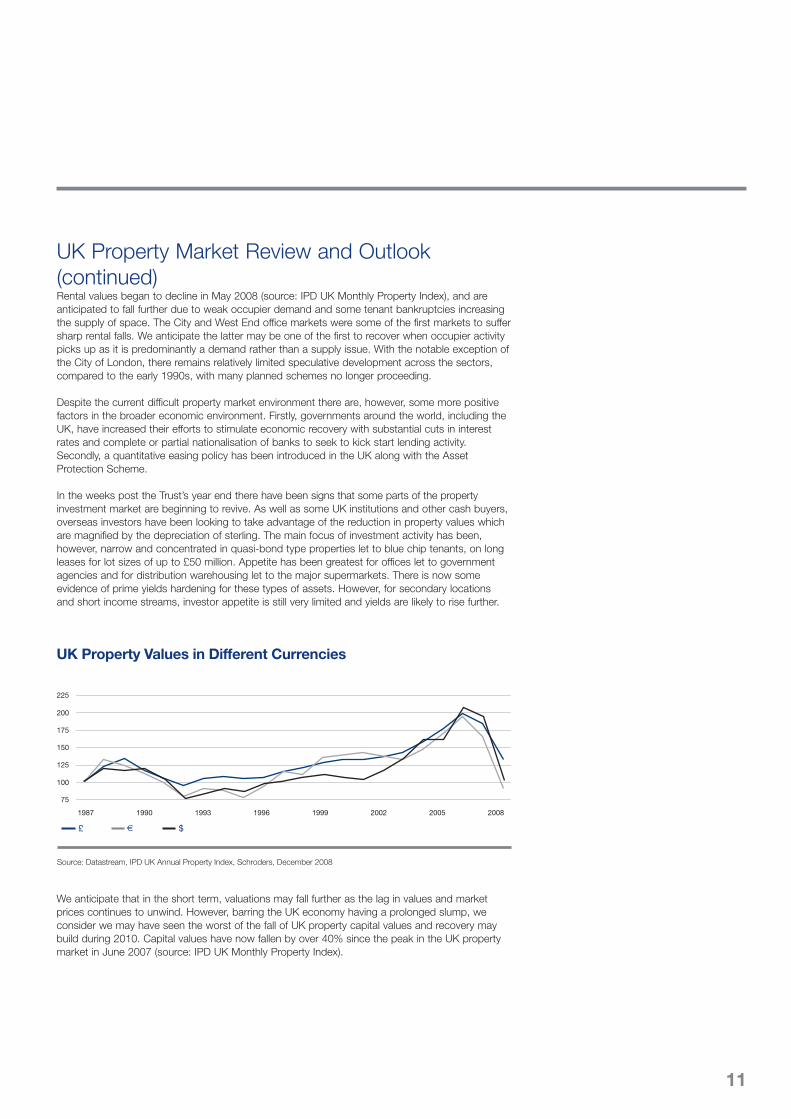

We anticipate that in the short term, valuations may fall further as the lag in values and marketprices continues to unwind. However, barring the UK economy having a prolonged slump, weconsider we may have seen the worst of the fall of UK property capital values and recovery maybuild during 2010. Capital values have now fallen by over 40% since the peak in the UK propertymarket in June 2007 (source: IPD UK Monthly Property Index).

75

100

125

150

175

200

225

1987 1990 1993 1996 1999 2002 2005 2008

UK Property Values in Different Currencies

£ € $

Source: Datastream, IPD UK Annual Property Index, Schroders, December 2008

UK Property Market Review and Outlook(continued)Rental values began to decline in May 2008 (source: IPD UK Monthly Property Index), and areanticipated to fall further due to weak occupier demand and some tenant bankruptcies increasingthe supply of space. The City and West End office markets were some of the first markets to suffersharp rental falls. We anticipate the latter may be one of the first to recover when occupier activitypicks up as it is predominantly a demand rather than a supply issue. With the notable exception ofthe City of London, there remains relatively limited speculative development across the sectors,compared to the early 1990s, with many planned schemes no longer proceeding.

Despite the current difficult property market environment there are, however, some more positivefactors in the broader economic environment. Firstly, governments around the world, including theUK, have increased their efforts to stimulate economic recovery with substantial cuts in interestrates and complete or partial nationalisation of banks to seek to kick start lending activity.Secondly, a quantitative easing policy has been introduced in the UK along with the AssetProtection Scheme.

In the weeks post the Trust’s year end there have been signs that some parts of the propertyinvestment market are beginning to revive. As well as some UK institutions and other cash buyers,overseas investors have been looking to take advantage of the reduction in property values whichare magnified by the depreciation of sterling. The main focus of investment activity has been,however, narrow and concentrated in quasi-bond type properties let to blue chip tenants, on longleases for lot sizes of up to £50 million. Appetite has been greatest for offices let to governmentagencies and for distribution warehousing let to the major supermarkets. There is now someevidence of prime yields hardening for these types of assets. However, for secondary locationsand short income streams, investor appetite is still very limited and yields are likely to rise further.

Comprehensively refurbishedearly 2008

Lettable floor area increasedfollowing reconfiguration ofground floor reception

New lettings achieved to mediarelated tenants

Rents improved from around£25 per sq ft to in excess of£30 per sq ft

12 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

13

Manager’s Statement (continued)

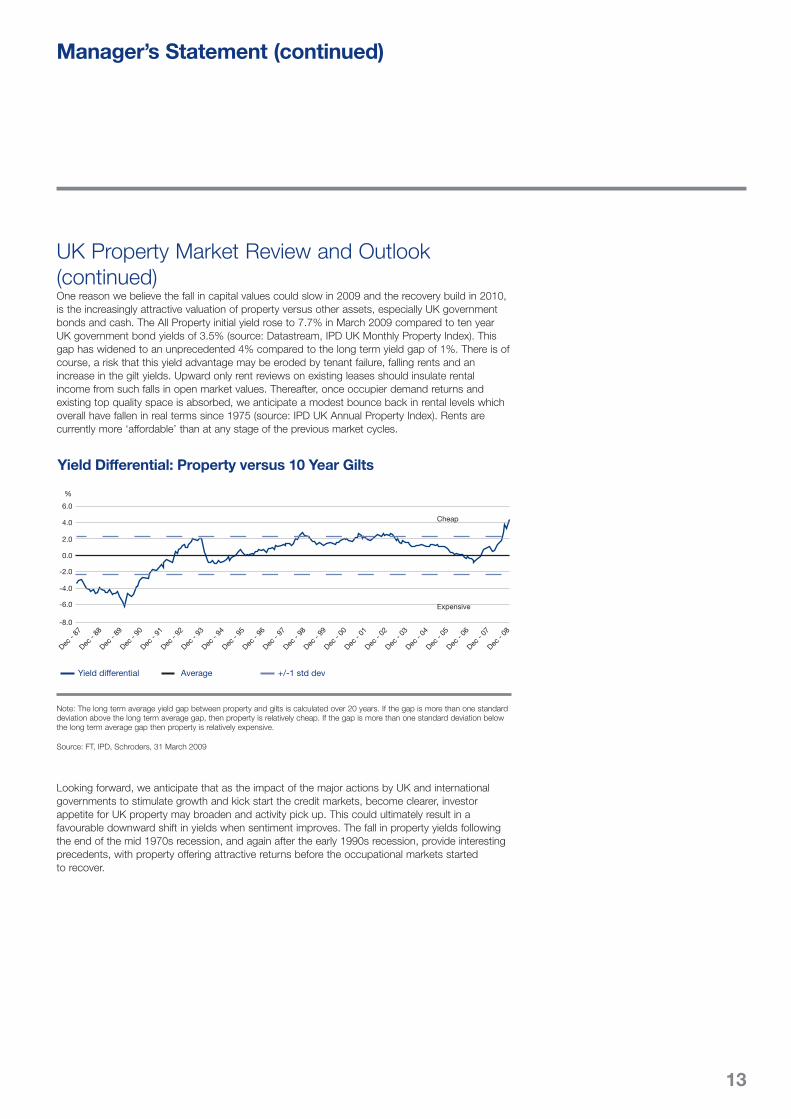

UK Property Market Review and Outlook(continued)One reason we believe the fall in capital values could slow in 2009 and the recovery build in 2010,is the increasingly attractive valuation of property versus other assets, especially UK governmentbonds and cash. The All Property initial yield rose to 7.7% in March 2009 compared to ten yearUK government bond yields of 3.5% (source: Datastream, IPD UK Monthly Property Index). Thisgap has widened to an unprecedented 4% compared to the long term yield gap of 1%. There is ofcourse, a risk that this yield advantage may be eroded by tenant failure, falling rents and anincrease in the gilt yields. Upward only rent reviews on existing leases should insulate rentalincome from such falls in open market values. Thereafter, once occupier demand returns andexisting top quality space is absorbed, we anticipate a modest bounce back in rental levels whichoverall have fallen in real terms since 1975 (source: IPD UK Annual Property Index). Rents arecurrently more ‘affordable’ than at any stage of the previous market cycles.

Looking forward, we anticipate that as the impact of the major actions by UK and internationalgovernments to stimulate growth and kick start the credit markets, become clearer, investorappetite for UK property may broaden and activity pick up. This could ultimately result in afavourable downward shift in yields when sentiment improves. The fall in property yields followingthe end of the mid 1970s recession, and again after the early 1990s recession, provide interestingprecedents, with property offering attractive returns before the occupational markets startedto recover.

Yield Differential: Property versus 10 Year Gilts

6.0

4.0

2.0

0.0

-2.0

-4.0

-6.0

-8.0

Dec- 87

Dec- 88

Dec- 89

Dec- 90

Dec- 91

Dec- 92

Dec- 93

Dec- 94

Dec- 95

Dec- 96

Dec- 97

Dec- 98

Dec- 99

Dec- 00

Dec- 01

Dec- 02

Dec- 03

Dec- 04

Dec- 05

Dec- 06

Dec- 07

Dec- 08

Cheap

Expensive

%

Yield differential Average +/-1 std dev

Note: The long term average yield gap between property and gilts is calculated over 20 years. If the gap is more than one standarddeviation above the long term average gap, then property is relatively cheap. If the gap is more than one standard deviation belowthe long term average gap then property is relatively expensive.

Source: FT, IPD, Schroders, 31 March 2009

Performance AttributionThe global credit crunch and the resultantrecession impacted the short term performanceof the Trust. Strategies that drove goodperformance including leverage over the threeyears preceding the ‘crunch’ have seen a sharpreversal. Whilst this reversal has only happenedover a relatively short period, the effect hasbeen severe enough to cause the Trust tounderperform its benchmark over the last one,three, five and ten years (annualised). In afalling property market the leverage in theindirect vehicles has contributed to a significantamount of the underperformance.

Over the period, the different strategies in theTrust have responded in varying ways to theweak market conditions. The impact of assetallocation positions had a neutral impact onthe overall relative performance versus thebenchmark over the year. It was at a stock levelwhere the underperformance has beenattributed by IPD. Attribution can however bebroken into three main areas:

Standing investmentsThe Trust’s standing investments provided apositive contribution to relative performanceversus the benchmark over the year. Overall,yields rose less than the benchmark and theincome return was slightly ahead of thebenchmark. This in part, reflected the impactof asset management initiatives and the focusof the portfolio on multi-let assets withoccupier appeal.

Land and regeneration opportunitiesThe more ‘opportunistic’ holdings such as thelonger term regeneration holding in Bracknelland the development site in Croydon were hithard, due to the effect of rising yields, fallingrental values and construction cost inflation.We believe their valuations are likely to respondpositively to indications of recovery in theUK economy.

Manager’s Statement (continued)

Indirect investmentsThe indirect strategies produced varied resultsas might be expected from the diversifiedrange of funds. Whilst returns from holdingssuch as UNITE UK Student AccommodationFund (UNITE) and The Residential Property UnitTrust (ResPUT) (tenanted residential) have beenrelatively resilient, funds with prime, high qualityproperty, such as Hercules Unit Trust (HUT)(fashion parks), West End of London PropertyUnit Trust (WELPUT) (West End of Londonoffices) and The Chiswick Park Unit Trust(ChisPUT) (South East offices), sufferedsubstantial falls in value. These falls wereaccentuated due to the impact of debt in thefunds as values continued to decline. In thecase of WELPUT, it was particularly severe asthe West End office market was one of the firstlocations to also be impacted by falling rents.Like a number of leveraged, unlisted vehicles,HUT and the Henderson UK Retail WarehouseFund, came close to breaching their loan tovalue covenants as a result of falling propertyvalues. The managers of these funds thereforesold properties to reduce debt levels which,again, had an impact on performance.

SEPUT StrategiesWhilst it might be expected that differentinvestments perform in different ways over thewhole property cycle, underperformance hasfor this phase, been focused on some of thelarger holdings in the portfolio. It is thereforeimportant to revisit the rationale behind theseassets, and the themes that are evidentthroughout our sector strategies.

As the table shows, the Trust comprises arange of strategies which combined to provide,at 31 March 2009, ownership or partownership of:

– Total gross property assets of £5.4 billion– 238 properties²– 1,080 tenancies– Total gross rent roll of approximately £324

million³ per annum

The investment philosophy behind theconstruction of all strategies embraces our corebelief that consistent, sustainable, long termreturns come from the recognition that:

– Occupier demand is always evolving.Building owners therefore need to anticipatechange and have the conviction to make longterm investments.

– Sustainability and regeneration issues arehigh on investors’ and occupiers’ agendas.It is not just buildings, but traditional locationswhich are being challenged by evolvingstructural trends.

– With change comes increasing risk,particularly as occupiers in all propertysectors are increasingly requiring shorter,more flexible leases to meet theiroperational needs.

– With shorter leases, the constant threat ofobsolescence becomes more acute. Incomeis an important driver of property returns, butsustainable income comes from investing orcreating buildings and environments thathave the right quality to meet and adapt tooccupiers’ needs.

14 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

15

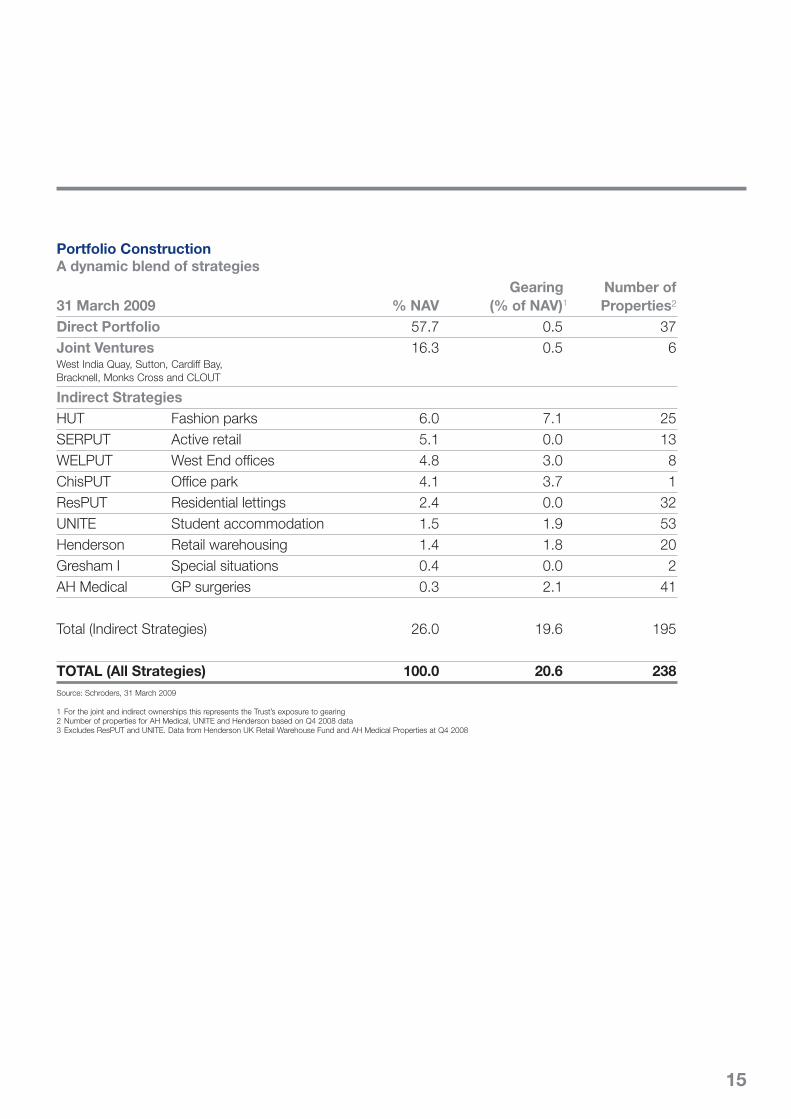

Portfolio ConstructionA dynamic blend of strategies

Gearing Number of31 March 2009 % NAV (% of NAV)1 Properties²Direct Portfolio 57.7 0.5 37Joint Ventures 16.3 0.5 6West India Quay, Sutton, Cardiff Bay,Bracknell, Monks Cross and CLOUT

Indirect StrategiesHUT Fashion parks 6.0 7.1 25SERPUT Active retail 5.1 0.0 13WELPUT West End offices 4.8 3.0 8ChisPUT Office park 4.1 3.7 1ResPUT Residential lettings 2.4 0.0 32UNITE Student accommodation 1.5 1.9 53Henderson Retail warehousing 1.4 1.8 20Gresham I Special situations 0.4 0.0 2AH Medical GP surgeries 0.3 2.1 41

Total (Indirect Strategies) 26.0 19.6 195

TOTAL (All Strategies) 100.0 20.6 238Source: Schroders, 31 March 2009

1 For the joint and indirect ownerships this represents the Trust’s exposure to gearing2 Number of properties for AH Medical, UNITE and Henderson based on Q4 2008 data3 Excludes ResPUT and UNITE. Data from Henderson UK Retail Warehouse Fund and AH Medical Properties at Q4 2008

16 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

17

Schroder Exempt Property Unit Trust

IPD UK Pooled Property Fund Indices –All Balanced Funds Index Weighted Average

All Retail Segment Weightingsat 31 March 2009% of gross asset value

Source: IPD

5.6

5.6

4.7

5.8

2.3

8.2

18.9

16.9

Manager’s Statement (continued)

RetailHercules Unit Trust (HUT) gives investorsaccess to a unique portfolio of some of thebest and, therefore, often the largest, out oftown fashion parks.

This segment of the market evolved throughoutthe 1990s. Shoppers have increasingly soughtan alternative to congested town centres, withgood main road access and abundant, (usuallyfree), car parking, as a lifestyle choice.

For high street retailers, whose margins havebeen under pressure for many years, the largerunits offered in fashion parks, (often more thanfive times larger than traditional unit shops),have allowed them to increase their marginsthrough a more flexible and affordable format.

During the buoyant property market conditionsthe investment market recognised the sector’sattractions and bid yields down to record lowlevels. The pricing correction has been severewith yields almost doubling.

We believe that demand for the best retailfashion parks will be sustained by the relativeaffordability of the space offered. They willcontinue to evolve as more traditional highstreet brands expand out of town whenconsumer spending strengthens.

Despite the current weak economic environment,retailers are still taking space when goodopportunities present themselves. At MonksCross in York, (pictured opposite) a fashionpark in which the Trust owns a third share, therecent willingness of PC World to surrendertheir lease gave us the ability to introduce anew and reconfigured Debenhams anchorstore. This benefits the retailer mix and, in turn,has attracted new retailers to Monks Cross.This has resulted in potential competition fornew units from retailers able to pay higherrental levels.

The Trust’s holding in Bracknell has been aninvestment in the Trust since 2001 when it wasrecognised as an attractive opportunity to createa new retail destination for the affluent catchmentarea surrounding the town. Bracknell’s centrehas not evolved since it was built as a NewTown in the late 1950s.

In a 50/50 partnership with Legal and General,the Trust owns, not just a shopping centre, butthe vast majority of the town centre, on a 98.3acres (39.8 hectare) site. This provides a totalincome of approximately £10 million per annumfrom 420 tenancies in approximately 785,000sq ft (72,930 sq m) of existing accommodation.

The regeneration of this town remains anattractive investment proposition, albeit thatthe current outline planning consent for aredevelopment scheme was originally conceivedfor more buoyant economic and propertymarket conditions. We now have an opportunityto deliver a more appropriate scale ofdevelopment for the post ‘credit crunch’economic conditions. The current work streamsare focused on identifying ‘early wins’ whichcould allow the process of regeneration to getunderway in a series of phases.

At the other end of the retail spectrum,Schroder Emerging Retail Property Unit Trust(SERPUT) continues with its active managementstrategy of identifying new locations that meetthe needs of today’s multiple and strong,independent retailers. We utilise our contactswithin the retail industry to identify new retailerconcepts, as much as ‘Clever Towns’, Schroder’sproprietary research tool, which identifieslocations that have the right characteristics tomeet evolving retailer demand.

Our property research supports our convictionthat this strategy, focusing on these differentends of the retail spectrum, is still appropriate.The Trust is, importantly, well positioned toavoid any substantial exposure to the weakerbrands in the mid-range fashion market. This iswhere the majority of tenant failures are occurring,especially in locations where weak demand andoversupply may be an issue for the foreseeablefuture.

Whilst the strategy of the retail portfolio isfocused on specific segments of the market,the manager has concluded that the Trust’sexposure to indirect holdings and gearing inthis sector are too dominant. This should, overthe medium term, be rebalanced into directproperty ownership where the team has provenskills in identifying attractive opportunities.Although the property investment market isstarting to stabilise this transition is, however,best executed in more buoyant marketconditions to allow investors to benefit from anyrecovery.

London WC2, Covent Garden,Seven Dials

Bought in May 1998 for£22.3 million

Redeveloped in early 2006

Pre-let to Expedia.com inDecember 2007

Sold in May 2008 for a net priceof £55 million reflecting a netinitial yield of 5.3%

Five years total return to sale12.1% per annum

Three years total return to sale16.8% per annum18 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

Computer generated image

19

Schroder Exempt Property Unit Trust

IPD UK Pooled Property Fund Indices –All Balanced Funds Index Weighted Average

All Office Segment Weightingsat 31 March 2009% of gross asset value

Source: IPD

5.3

5.9

14.7

8.6

18.2

9.5

5.6

0.0

Manager’s Statement (continued)

OfficesFollowing the successful sales programmeexecuted at the end of 2007 and into 2008, theoffice portfolio is defensively positioned, weightedtowards the diversified South East economy.

Whilst rents have fallen, particularly in centralLondon, rents in cities like Manchester andBirmingham still appear to be holding firm athistorically high levels, despite falling demandand increasing supply. We anticipate that thesemarkets will not be immune as the economicdownturn impacts further. Accordingly, theTrust is continuing to maintain an underweightposition versus the benchmark.

The West End of London Property Unit Trust(WELPUT) office portfolio significantly reduced insize as the property market slowed, through aprogramme of sales of mature or weakerassets. The portfolio delivered strong returnsbefore the ‘credit crunch’, assisted by gearing.Despite implementing this prudent salesstrategy, the severity of the economic downturnhas meant that the values of the remainingproperties have fallen sharply, especially thedevelopments in the portfolio. Performancewas also impacted by the effect of gearing inWELPUT (this was 38.5% at 31 March 2009.The loan to value covenant on the debt facilityis 70%).

We believe WELPUT offers a diversified portfolioof high quality West End office properties whichhas the potential to outperform in the near term.We anticipate that the manager may start seekingnew opportunities to expand the portfolio, intoan improving market.

Despite opportunistically reducing the Trust’sexposure to the office sector over the yearthrough the sale of Seven Dials, in CoventGarden, WC2, we have maintained thestrategic overweight position to the West End,in anticipation of a potentially sharp recovery.This contrasts with an underweight exposureto the City of London office market where ourapproach is more opportunistic. This is due tothe volatility of development supply and also oftenant demand from the finance sector. Inrecognition of this, the Trust sold its interest inCity Point, a large office building in the City ofLondon, early in 2007 for a yield of 4.8%. Thisand other sales moved the portfolio to itscurrent underweight position. In the City, theTrust holds two development sites, one inMoorgate, the other in Mark Lane.

Ruskin Square, the focus of the CroydonGateway Scheme, shares the vision ofChiswick Park. It represents an opportunityto deliver an urban regeneration scheme inLondon’s second largest borough.

The nine acre site is immediately adjacent toEast Croydon station (the third busiest Londoninterchange), 15 minutes from Victoria Stationand 17 minutes from Gatwick Airport. Rarely forsuch schemes, the site is in single ownershipand has all necessary planning consents fora mixed (predominantly office) use schemetotalling approximately 1.5 million sq ft(139,350 sq m). A Compulsory Purchase Orderwas successfully defeated during the year andthe site is now able to be offered to the market.In partnership with Croydon Council, RuskinSquare forms a central part of their regenerationplans for this important commercial centre.All occupier requirements are being activelypursued, together with a possible residentialscheme, in order to kick start the project.

As with Chiswick, we believe that Ruskin Squareoffers an excellent opportunity to participate inthe creation of another office ‘community’,based on the best principles of sustainabledevelopment, to create a new income streamfor the Trust.

Over the short term, the values of these siteshave been severely hit. However, off currentvaluation levels, with planning consents in placeand new office schemes already designed, theyare ready for potential delivery into a recoveringmarket. However we anticipate that this maynot be until 2011/12.

Outside the major core office locations, webelieve that many out-of-town and businesspark locations are increasingly under threatfrom growing occupier awareness about issuessuch as sustainability and corporateresponsibility. Many office schemes wereconceived and built in the 1980s and 1990saround motorway locations. This means theseoccupiers are almost entirely dependent uponthe car to travel to work.

The Trust holds a 19.6% stake in The ChiswickPark Unit Trust in West London. The vision forthis scheme was to create an attractivebusiness park environment in an affluentsuburban location, which benefited from goodaccess to Heathrow via the M4 motorway andeasy access to three commuter stations.Employees are therefore able to use publictransport to travel to and from work rather thanrely on the car. The Park currently comprisesover 1 million sq ft (92,900 sq m) of offices innine buildings in what is widely regarded asone of the best examples in Europe of an‘urban’ business park. The site can potentiallyaccommodate a further three propertiestotalling approximately 690,000 sq ft(64,103 sq m).

Although the first building was completed overeight years ago, it was conceived as a placewhere businesses could make a statementabout their corporate responsibility, by sharingin the Park’s commitment to creating a unique,attractive working environment for employees.

For the Trust, whilst the part ownership andgearing have detracted in the short term, itgives an exposure to a diversified incomestream of £24.8 million per annum from 31occupiers. The risks of shorter leases andbuilding obsolescence are mitigated by thecommitment which the owners have made toproviding facilities and an environment so thatoccupiers can literally ‘Enjoy-Work’.™

20 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

21

Schroder Exempt Property Unit Trust

IPD UK Pooled Property Fund Indices –All Balanced Funds Index Weighted Average

All Industrial SegmentWeightings at 31 March 2009% of gross asset value

Source: IPD

16.3

10.2

1.3

9.3

Manager’s Statement (continued)

IndustrialAs with the office sector, the industrial portfoliohas been deliberately focused towards theSouth East, again as a consequence of thesales programme which took place last year.In a weak market, our preference is for therelative defensiveness of the South East wherealternative land uses have eroded industrialsupply in recent years and which supportcurrent land values. For example, the Trustholds the Felnex Industrial Estate in Hackbridge,in South West London which is a mixture ofunits of different ages and styles, on 19.1 acres(7.7 hectares). This site is surrounded by greenbelt land and residential properties and isadjacent to the commuter station servingLondon Bridge and London Victoria stations.In the current market, the estate provides theTrust with a high level of income from amulti-let cash flow. We expect long term tenantdemand to be sustainable in this location.However, from the Local Authority’s point ofview, it represents a strategic site where theywould prefer to see a mixed use (primarilyresidential) scheme regenerating the centreof the town.

Accordingly, we are working with the localplanners to gain a mixed use planning consentfor up to 1 million sq ft (92,900 sq m). If we aresuccessful in obtaining the mixed use consent,we consider the potential uplift to existing usevalue could be substantial.

Elsewhere in the portfolio the key assets arefocused on core locations around London andthe M25 motorway, which have inherently goodsupply and demand dynamics such as:

– Matrix, Park Royal, London NW10: 290,052sq ft (26,947 sq m) in 14 units occupying amain road position in one of the premierindustrial locations serving the western sideof Central London.

– Electra, Canning Town, London E16: 224,000sq ft (20,000 sq m) in ten units located on theeastern side of London, one mile from CanaryWharf and close to the 2012 Olympic complex.

– Acorn Industrial Estate, Crayford: 62 unitscomprising a total of 431,914 sq ft (40,126sq m) serving South East London.

As the examples illustrate, our preference isfor multi-let estates which in the current marketprovide a diversified cash flow. They alsoprovide the opportunity to engineer incomegrowth by actively managing the assets inanticipation of a recovery in occupier activity.

22 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

23

Schroder Exempt Property Unit Trust

IPD UK Pooled Property Fund Indices –All Balanced Funds Index Weighted Average

Other Property SegmentWeightings at 31 March 2009% of gross asset value

Source: IPD

10.2

7.8

2.1

0.3

Manager’s Statement (continued)

Alternative InvestmentsAn allocation to alternative or ‘other’ propertysectors provides exposure to parts of theeconomy, such as healthcare (AH MedicalProperties plc), (0.3% of the Trust’s NAV) andstudent accommodation (UNITE) (1.5% of theTrust’s NAV) which perform in different ways tothe main commercial property sectors. Theycan provide valuable diversification and relativelysecure income streams with little correlationwith the demand for shops, offices andindustrial units.

However, these strategies usually require theskills of specialist managers so are bestaccessed via the indirect vehicles which areheld by the Trust.

In addition, the leisure sector provides analternative exposure to the consumer,diversified away from ‘pure’ retail consumerspending, which has been under pressure forsome time. Whilst not immune from theeconomic slowdown, the Trust’s leisureholdings at West India Quay, adjacent toCanary Wharf, and at Mermaid Quay, CardiffBay, have held up relatively well. As with retail,the restaurant sector is dynamic. Consumersare still eating out, but are becoming increasinglyvalue conscious. It is therefore important toensure that, just like a shopping centre, suchinvestments are actively managed to providethe right mix of brands to ensure that the ‘offer’matches customer demand. At Mermaid Quay,success has come from the management skillswe have used to maintain a good blend ofoperators for the family orientated visitors whoare attracted to the scheme, as well as from acommitment to maintaining a modern, safe andwelcoming environment.

In the residential sector, ResPUT (representing2.4% of the Trust’s NAV), a fund which investsin short term let flats and houses, is beingwound up. This is because the manager hasnot been able to attract a sufficient number ofinvestors into the fund to get the portfolio to asuitable critical mass. The liquidation willcontinue over the next twelve months, returningcash to the Trust and reducing the overallexposure to indirect investments.

Residential remains, however, an important andestablished sector, despite, having failed toattract widespread institutional investors to date.It is increasingly a significant planning requirementof any urban regeneration scheme, (Bracknelland Croydon are good examples of this), as thegovernment is keen to ensure that sufficienthousing is delivered to meet increasing demand.

Recently, the Homes and Communities Agency(HCA) announced an initiative to work withinstitutional investors and site owners to kickstart a new approach to the private rentedsector to provide high quality accommodationrestricted to leasing rather than sale. This couldcreate a new investment opportunity forinstitutional investors seeking a potentiallyhigher and more sustainable cash flow thanthat offered by ResPUT.

Alternative sectors have proved relativelyresilient to the severe valuation falls across theproperty market in general. The challenge,however, is to ensure that they continue toprovide competitive risk adjusted returnscompared to the traditional commercialsectors, once these markets start to recover.

24 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

Owned by Chiswick Park Unit Trust (www.enjoy-work.com)

25

Manager’s Statement (continued)

I D MasonFund Manager16 June 2009

GearingThe level of gearing in the Trust is a measurewhich we monitor closely, as shown by thetable on page 66.

The current investment and borrowing guidelineslimit total gearing (including the Trust’s share ofborrowing within indirect vehicles) to 25.0% ofnet asset value, subject to market movements.The gearing breakdown is shown below:

31 March 2008 31 March 2009Borrowings Borrowings£m % NAV £m % NAV

Direct 80.0 5.2 5.0 0.5Indirect 197.7 13.0 205.3 20.1Total 277.7 18.2 210.3 20.6

As can be seen above, whilst the totalamount of debt has fallen, the percentage hasincreased due to the fall in the Trust’s overallnet asset value.

The major issue affecting many propertyborrowers, private investors, public propertycompanies and unlisted vehicles and the like isthe potential for a breach of loan to value (LTV)covenants, caused by the large fall in values.This has impacted even the most highlyregarded and more conservative managementteams who have sought to manage their debtinto the downturn, but who have been caughtout by the collapse in values.

Over the year we have, in particular beenclosely monitoring:

– Hercules Unit Trust and Henderson UK RetailWarehouse Fund as they have both beenclose to breaching LTVs,

– The Chiswick Park Unit Trust and the Suttonindustrial joint venture with Valad PropertyGroup, which are both facing renewal of loanfacilities over the next twelve months.

In respect of the two retail warehouse funds weare looking to the managers to come up with along term solution that puts the funds ‘on thefront foot’, so that the portfolios can be managedto add value into the recovery and to stimulatea return to secondary market liquidity for investors.

Therefore, the Trust voted against a Hendersonproposal to allow the manager to capitaliseincome to pay down an amortisation schedulewhich had already been agreed with the banks.For the Trust, it did little to create liquidity andwould have eliminated the income return.

By contrast, Hercules approached unitholdersfor consent to issue up to £200 million ofconvertible bonds to help solve the LTV issueand allow some of the existing loans to berepaid. This comes as part of a package that iscontinuing to progress a programme of salesas well as negotiating to ease the terms on theexisting debt facilities. The Trust voted in favourof this proposal as we were satisfied that theobjective is to provide a long term solution forfinancing the fund.

The debt renewal at Chiswick is tied to aunitholder vote in the second half of the year todecide if the fund should be extended beyondthe original life of the Trust, which expires inDecember 2009. At Sutton we have variousstrategies prepared depending on what isrequired by the bank.

SummaryThe Trust has performed disappointingly overthe last 18 months against a background ofexceptionally weak market conditions. Weconsider the underlying quality of the propertyassets is sound. The investment visioncontinues to focus on building a long term,sustainable portfolio of standing investments,together with the selective use of indirectvehicles to access different strategies.

We reviewed the Trust's strategy in Spring2008 and stated at that time the intention torebalance the portfolio away from some of thelarger indirect holdings and more towardsincome producing standing investments tosmooth the returns from the opportunisticstrategies.

However, now is not the time to force througha sale of indirect holdings as this would involvethe crystallisation of potentially large losses.Accordingly, we have signalled thatrepositioning of the portfolio is likely to be amedium term strategy. This reflects the viewthat, rather than deleveraging risk at this lowpoint in the commercial property market cycle,repositioning into a recovering market shouldproduce a more optimal solution. We willcontinue to seek to realise the attractive latentpotential in the portfolio, through activemanagement, and are currently working on anumber of initiatives to help deliver this for thebenefit of unitholders.

26 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

Purchases and Sales

PurchasesNo purchases

SalesProperty Date Sale Price (£)Coventry, Seven Stars Industrial Estate¹ April 2008 11,200,000

Great Tower Street, London EC3²,³ April 2008 7,250,000

London WC1, Seven Dials² May 2008 55,022,582

Basinghall Street Unit Trust (being wound up) June 2008/December 2008 1,337,750

Athena Court³ September 2008 22,352,512

The Residential Property Unit Trust (being wound up) September 2008/March 2009 5,182,142

102,344,986

Source: Schroders, 31 March 20091 This sale was reported in the 31 March 2008 Annual Report and Audited Financial Statements. This sale occurred in March 2008

with completion taking place in April 2008.2 These sales were reported in the 31 March 2008 Annual Report as sales which completed following the year end of 31 March

2008 and these sales are included in this current year Audited Financial Statements.3 The Trust disposed of its interest in single property unit trusts holding the underlying properties.

City of London OfficesBetween £25 million and £50 millionCity Property Unit Trust (CPUT) Direct holdingA closed ended Jersey property unit trust owning two office sites in the City of London;Mark Lane near Fenchurch Street Station and 8-10 Moorgate.The Trust’s interest represents 95.9% of CPUT.

Between £10 million and £25 millionLombard Street Unit Trust (LSUT) Direct holdingA closed ended Jersey property unit trust owning a freehold 1930s office building, extensivelyrefurbished in 1998, totalling 39,000 sq ft (3,600 sq m) over seven floors. The Trust’s interestrepresents 99.0% of LSUT.Principal tenant:Regus Group Plc

London EC1, 4-7 Chiswell Street Direct holdingVirtual freehold office building on basement, ground and seven upper floors completedin 1991 with a total floor area of 38,700 sq ft (3,595 sq m).Principal tenants:7 City Learning Limited / City Presentation Centre Limited / Anstey Horne Co Limited

Between £5 million and £10 millionLondon EC2, 11/12 Appold Street Direct holdingFreehold office building completed in 1992 providing basement, ground and five upper floorswith a total area of 23,500 sq ft (2,185 sq m).Principal tenants:Das Business Furniture Limited / PIPC (UK) Limited / Yolus Limited

Under £1 millionCity of London Office Unit Trust (CLOUT) Joint VentureA closed ended Jersey property unit trust owning a leasehold interest in Moorfields House,Moorgate, in the City of London. The Trust’s interest represents 26.8% of CLOUT.

Austral House Unit Trust (AHUT) Joint VentureA closed ended Jersey property unit trust that has developed an office building at Coleman Street,London EC2 under an agreement entered into in March 2005. The building was practicallycompleted in February 2007. Residual assets remain in AHUT. The Trust’s interest represents26.8% of AHUT.

Basinghall Street Unit Trust (BSUT) Joint VentureA closed ended Jersey property unit trust that has developed an office building at Basinghall Street,London EC2, under a forward sale agreement entered into in March 2005. At practical completion inJune 2007, the sale completed for £118.4 million. Residual assets remain in BSUT. The Trust’sinterest represents 26.8% of BSUT.

Details of the Portfolio – Office

27

Details of the Portfolio – Office (continued)

28 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

West End and Mid Town London OfficesBetween £25 million and £50 millionWest End of London Property Unit Trust (WELPUT) Indirect holdingA closed ended Jersey property unit trust investing in eight office/mixed use properties orvehicles in the West End of London. The Trust’s interest represents 16.5% of WELPUT.Principal tenants:BAE Systems Plc / Transport for London (TFL) / Orange PCS Limited

London EC4, Chancery Exchange, 10 Furnival Street Direct holdingFreehold office building with a total floor area of 81,706 sq ft (7,591 sq m) over basement,lower ground, ground and four upper floors.Principal tenants:Aerion Fund Management Limited / Arcadis AYH Plc / Burges Salmon LLP / MacFarlanes LLP

Parker Tower Unit Trust (PTUT) Direct holdingA closed ended Jersey property unit trust owning Parker Tower, London WC2, a freehold officebuilding providing 54,000 sq ft (5,000 sq m) over 13 floors and 53 Parker Street, London WC2,a long leasehold office building providing 15,900 sq ft (1,480 sq m) over five floors. The Trust’sinterest represents 99.0% of PTUT.Principal tenants:British Telecommunications Plc / IAC Search and Media UK Limited

London W14, Kensington Village Direct holdingLong leasehold office complex refurbished in 1991/92 comprising two buildings totalling89,500 sq ft (8,310 sq m).Principal tenants:Blue Marlin Brand Design Limited / GLU Mobile Limited / RDF Media Limited / The Hot Group Plc

Between £10 million and £25 millionLondon W1, 81-82 Dean Street Direct holdingTwo freehold office buildings providing a total of 32,800 sq ft (3,047 sq m) over seven floors.Principal tenant:TBWA UK Group Limited

South East OfficesOver £50 millionCroydon Gateway Property Unit Trust (CGPUT) Direct holdingA closed ended Jersey property unit trust, investing in land and buildings in Croydon, in whichthe Trust holds a 97.3% interest.Principal tenants:HSBC Bank Plc / Secretary of State for Communities & Local Government / Surridge Dawson Limited

29

South East Offices (continued)

Between £25 million and £50 millionThe Chiswick Park Unit Trust (ChisPUT) Indirect holdingA closed ended Jersey property unit trust which owns the freehold of the Chiswick Park officedevelopment. The Trust’s interest represents 19.6% of ChisPUT.Principal tenants:Technicolor Network Services / Discovery Content (UK) Limited / Regus Business Centres (UK) Limited

Between £10 million and £25 millionLondon SE1, Palace House Direct holdingFreehold office building in Southwark with a total floor area of 44,724 sq ft (4,155 sq m) overbasement, ground and four upper floors.Principal tenants:Nero Holdings Limited / Det Norske Veritas UK Holding Limited / Kaplan Financial Limited

Bracknell, Bracknell Beeches Direct holdingFreehold office park completed in 1990/91 comprising 13 units with a total floor area of68,760 sq ft (6,388 sq m).Principal tenants:Cadence Design Systems UK Limited / Overbury Plc / Sunguard Availability Services (UK) Limited

Between £5 million and £10 millionReading, New Century Place Direct holdingTwo freehold office buildings with a total floor area of 42,700 sq ft (3,970 sq m) on basement,ground and three upper floors.Principal tenants:Airwide Solutions UK Limited / Capita Business Services Limited

Capital Point Slough Unit Trust (CPSUT) Direct holdingA closed ended Jersey property unit trust owning a freehold office building completed in1998 with a total floor area of 53,000 sq ft (4,900 sq m). The Trust’s interest represents99.0% of CPSUT.Principal tenant:Lego (UK) Limited

Between £1 million and £5 millionUxbridge, Willowbank House Direct holdingThree freehold office buildings with a total floor area of 34,000 sq ft (3,200 sq m).Principal tenants:Airspan Communications Limited / BurgerKing Limited

Cranford, Europa House Direct holdingFreehold office building over two floors with a total floor area of 14,940 sq ft (1,390 sq m) andproviding parking for 50 cars.Principal tenants:Alpha Airport Holdings (UK) Limited

Bracknell, Eagle House Limited Joint ventureA freehold office and retail property providing six retail units with seven floors of offices above,with a total floor area of 74,000 sq ft (6,877 sq m), owned by Eagle House Limited. The Trust’sinterest represents 50.0% of Eagle House Limited.Principal tenants:IRI Infoscan Limited / McDonalds Property Company Limited / Secretary of State for the Environment

30 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

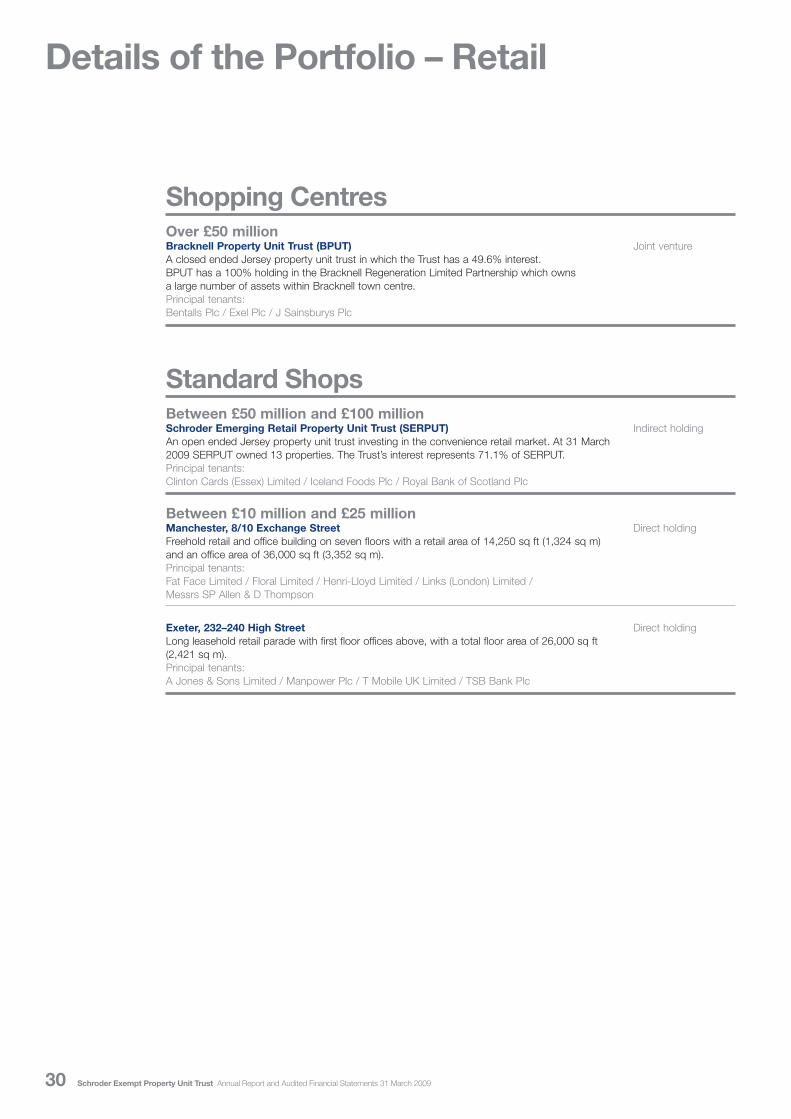

Details of the Portfolio – Retail

Shopping CentresOver £50 millionBracknell Property Unit Trust (BPUT) Joint ventureA closed ended Jersey property unit trust in which the Trust has a 49.6% interest.BPUT has a 100% holding in the Bracknell Regeneration Limited Partnership which ownsa large number of assets within Bracknell town centre.Principal tenants:Bentalls Plc / Exel Plc / J Sainsburys Plc

Standard ShopsBetween £50 million and £100 millionSchroder Emerging Retail Property Unit Trust (SERPUT) Indirect holdingAn open ended Jersey property unit trust investing in the convenience retail market. At 31 March2009 SERPUT owned 13 properties. The Trust’s interest represents 71.1% of SERPUT.Principal tenants:Clinton Cards (Essex) Limited / Iceland Foods Plc / Royal Bank of Scotland Plc

Between £10 million and £25 millionManchester, 8/10 Exchange Street Direct holdingFreehold retail and office building on seven floors with a retail area of 14,250 sq ft (1,324 sq m)and an office area of 36,000 sq ft (3,352 sq m).Principal tenants:Fat Face Limited / Floral Limited / Henri-Lloyd Limited / Links (London) Limited /Messrs SP Allen & D Thompson

Exeter, 232–240 High Street Direct holdingLong leasehold retail parade with first floor offices above, with a total floor area of 26,000 sq ft(2,421 sq m).Principal tenants:A Jones & Sons Limited / Manpower Plc / T Mobile UK Limited / TSB Bank Plc

31

Retail WarehousesBetween £50 million and £100 millionHercules Unit Trust (HUT) Indirect holdingA closed ended Jersey property unit trust investing in retail parks. At 31 March 2009 it owned25 retail parks including Glasgow Fort Shopping Park, Glasgow and Parkgate Shopping Park,Rotherham. The Trust’s interest represents 8.0% of HUT.Principal tenants:Home Retail Group plc / Next plc / Boots The Chemist plc

York, Monks Cross Shopping Park Joint ventureA freehold shopping park in which the Trust has a 33.3% interest. The park incorporates 27 unitsand two further units on Monks Cross Drive and three units on Julia Avenue Retail Park.Principal tenants:Bhs Limited / Boots the Chemist Limited / Mamas and Papas Limited / Marks and Spencer Plc / Next Plc /River Island Clothing Co Limited / Starbucks Coffee Company (UK) Limited

Between £10 million and £25 millionHenderson UK Retail Warehouse Fund (HRWF) Indirect holdingA closed ended Jersey property unit trust investing in retail parks. At 31 March 2009 it contained20 retail parks including Craigleith Retail Park, Edinburgh and The Brewery, Romford. The Trust’sinterest represents 3.7% of HRWF.Principal tenants:Argos Group Plc / DSG Retail Limited / Home Retail Group Limited / JJB Sports Plc / NBC Apparel

Cardiff, Cardiff Bay Retail Park Joint ventureA freehold retail park of 15 units with a total floor area of 195,300 sq ft (18,144 sq m) in whichthe Trust has a 50.0% interest.Principal tenants:Bhs Limited / Boots the Chemists Limited / JD Sports / McDonalds Restaurants Limited

Between £5 million and £10 millionLondon SE7, 403/433 Woolwich Road Direct holdingA freehold retail warehouse built in 1985 with a total floor area of 37,000 sq ft (3,406 sq m).Principal tenant:Wickes Building Supplies Limited

Under £5 millionHartlepool, Jacksons Landing Direct holdingFreehold retail factory outlet built in the mid 1990s with a total floor area of 75,600 sq ft (7,025 sq m).

32 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

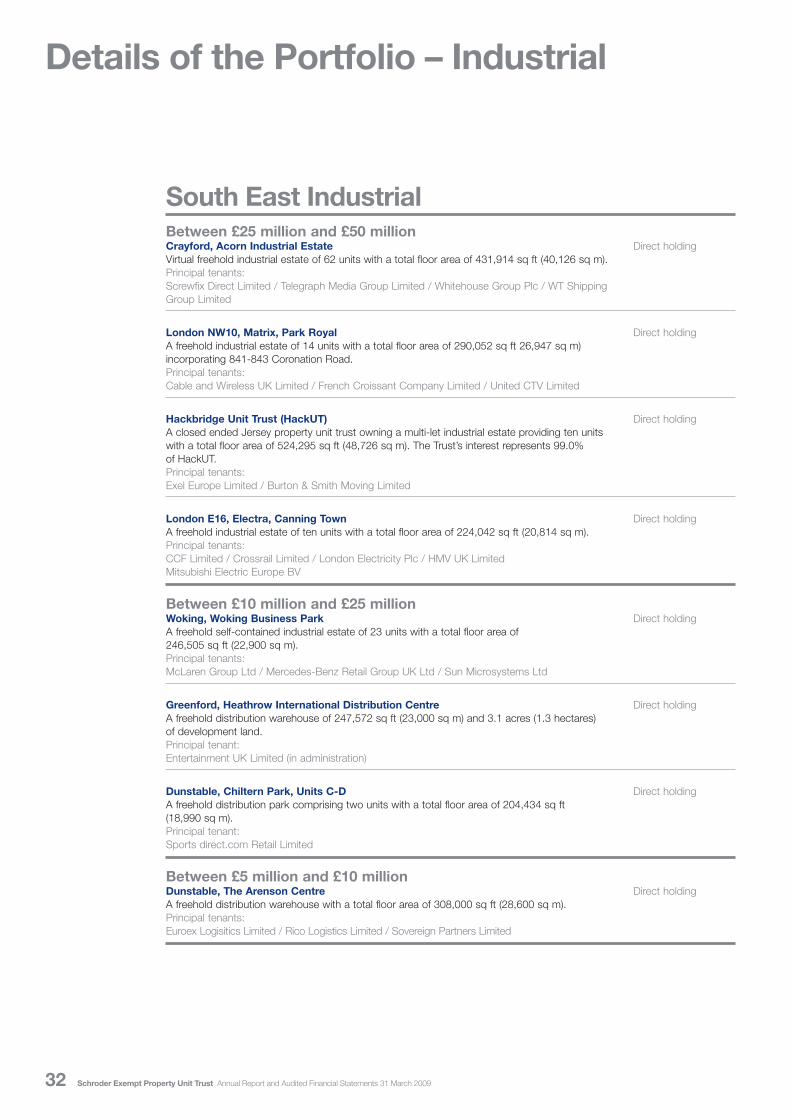

Details of the Portfolio – Industrial

South East IndustrialBetween £25 million and £50 millionCrayford, Acorn Industrial Estate Direct holdingVirtual freehold industrial estate of 62 units with a total floor area of 431,914 sq ft (40,126 sq m).Principal tenants:Screwfix Direct Limited / Telegraph Media Group Limited / Whitehouse Group Plc / WT ShippingGroup Limited

London NW10, Matrix, Park Royal Direct holdingA freehold industrial estate of 14 units with a total floor area of 290,052 sq ft 26,947 sq m)incorporating 841-843 Coronation Road.Principal tenants:Cable and Wireless UK Limited / French Croissant Company Limited / United CTV Limited

Hackbridge Unit Trust (HackUT) Direct holdingA closed ended Jersey property unit trust owning a multi-let industrial estate providing ten unitswith a total floor area of 524,295 sq ft (48,726 sq m). The Trust’s interest represents 99.0%of HackUT.Principal tenants:Exel Europe Limited / Burton & Smith Moving Limited

London E16, Electra, Canning Town Direct holdingA freehold industrial estate of ten units with a total floor area of 224,042 sq ft (20,814 sq m).Principal tenants:CCF Limited / Crossrail Limited / London Electricity Plc / HMV UK LimitedMitsubishi Electric Europe BV

Between £10 million and £25 millionWoking, Woking Business Park Direct holdingA freehold self-contained industrial estate of 23 units with a total floor area of246,505 sq ft (22,900 sq m).Principal tenants:McLaren Group Ltd / Mercedes-Benz Retail Group UK Ltd / Sun Microsystems Ltd

Greenford, Heathrow International Distribution Centre Direct holdingA freehold distribution warehouse of 247,572 sq ft (23,000 sq m) and 3.1 acres (1.3 hectares)of development land.Principal tenant:Entertainment UK Limited (in administration)

Dunstable, Chiltern Park, Units C-D Direct holdingA freehold distribution park comprising two units with a total floor area of 204,434 sq ft(18,990 sq m).Principal tenant:Sports direct.com Retail Limited

Between £5 million and £10 millionDunstable, The Arenson Centre Direct holdingA freehold distribution warehouse with a total floor area of 308,000 sq ft (28,600 sq m).Principal tenants:Euroex Logisitics Limited / Rico Logistics Limited / Sovereign Partners Limited

33

South East Industrial (continued)

Under £5 millionThe Teesland iDG Sutton Unit Trust (TiDGSUT) Joint VentureA closed ended unit trust investing in a leasehold industrial estate of 20 units with a total floorarea of 91,767 sq ft (8,520 sq m) and a development site of 5.75 acres (2.33 hectares) with aplanning consent for 131,000 sq ft (12,174 sq m). The Trust’s interest represents 50%of TiDGSUT.

London SE7, Maritime Industrial Estate, Carlton Direct holdingA freehold industrial estate of 14 units with a total floor area of 93,120 sq ft (8,651 sq m).Principal tenants:City Electrical Factors Limited / Claire Wines Limited / Multi-Tile Limited

Rest of UK IndustrialBetween £10 million and £25 millionBirmingham, Deykin Avenue Direct holdingA freehold site of 13.5 acres (5.5 hectares) on which two warehouse units of 150,000 sq ft(14,000 sq m) and 85,000 sq ft (7,900 sq m) were developed in 2005/06 by the Trust.Principal tenants:Innovate Logistics Limited (in administration) / WF Group Limited

Under £5 millionYork, Alexandra Court, James Street Direct holdingNine freehold warehouse units completed in 1982 providing a total floor area of 37,700 sq ft(3,500 sq m) on a site of 2.2 acres (0.9 hectares).Principal tenants:Edmundson Electrical Limited / Jewson Limited / Till & Whitehead Limited

Cannock, Walkmill Lane Direct holdingA freehold 8.1 acre (3.3 hectare) redevelopment, with a resolution for planning consentfor approximately 195,000 sq ft (18,115 sq m) of distribution warehousing.

34 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

Details of the Portfolio – Other Property

Other Property PortfolioOver £25 millionCardiff, Mermaid Quay Direct holdingA leisure and retail development fronting Cardiff Bay with a total floor area of140,000 sq ft (13,000 sq m).Principal tenants:Café Rouge Restaurants / Pizza Express Restaurants Limited / S A Brain & Co Limited /Tesco Stores Limited

Between £10 million and £25 millionThe Residential Property Unit Trust (ResPUT) Indirect holdingAn open ended Jersey property unit trust investing in the private rented residential sector.The Trust has a 41.6% interest in ResPUT.

West India Quay Unit Trust (WIQUT) Joint ventureA closed ended Jersey property unit trust investing in West India Quay North andSouth, a part freehold and part long leasehold leisure development totalling 134,000 sq ft(12,484 sq m) comprising a multiplex cinema, health and fitness club, multi-storey car park,restaurants, bars and eight retail units. The Trust’s interest represents 50.0% of WIQUT.Principal tenants:Cineworld Cinema Properties Limited / JD Wetherspoon Plc / LA Leisure Ltd /La Tasca Restaurants Ltd

UNITE UK Student Accommodation Fund (UNITE) Indirect holdingA closed ended Jersey property unit trust owning 53 student housing assets across17 towns. The Trust’s interest represents 4.1% of UNITE.

Under £5 millionGresham Property Partners, LP (Gresham) Indirect holdingJersey limited partnership with the ability to invest in any sector of the market wheresufficiently attractive returns are anticipated. The Trust’s interest represents 19.5%of Gresham.

AH Medical Properties plc Listed securityA publicly listed company investing in a portfolio of 41 primary care medical centres.The Trust’s interest represents 29.6% of AH Medical Properties plc.

Livingston, Limefield Direct HoldingTwo feuhold sites of 17.3 acres (7.0 hectares) and 5.4 acres (2.2 hectares) allocatedfor housing and employment use respectively.

35

Responsibilities of the Manager,Trustee and Supervisory Board

Manager’s and Trustee’sResponsibilities for theFinancial StatementsThe Trust Deed requires the Manager to prepareFinancial Statements for each financial yeardetailing the state of affairs of the Trust as atthe end of the financial year and its income orloss for the financial year. The Manager isresponsible for keeping proper accountingrecords and, along with the Property Manager,for taking reasonable steps to safeguard theassets of the Trust and to prevent and detectfraud and other irregularities. The Trustee isrequired to hold the underlying property of theTrust for the unitholders and is responsible forthe safe custody of that property and anydocumentation relating to it. The Managerconfirms that suitable accounting policies andappropriate accounting standards have beenused and applied consistently and reasonableand prudent judgements and estimates havebeen made in the preparation of the FinancialStatements for the year ending 31 March 2009.The Manager also confirms that the FinancialStatements have been prepared on the goingconcern basis.

Supervisory Board’sResponsibilitiesfor the FinancialStatementsThe Supervisory Board is responsible forapproving, on the Audit Committee’srecommendation, the Financial Statementsprepared for each financial year, including thecontent and the accounting policies adopted,and for reporting any corporate governanceissues relating to the Trust or other matters inconnection with the Financial Statements.

36 Schroder Exempt Property Unit Trust Annual Report and Audited Financial Statements 31 March 2009

Independent Valuer’s Reportto the Unitholders of Schroder Exempt Property Unit Trust

As independent valuer for the Trust, we havevalued properties held by the Trust at 31 March2009 in accordance with The Royal Institutionof Chartered Surveyors and InternationalValuation Standards. The Manager has beenprovided with a full valuation certificate andreport. The properties have been valued on thebasis of market value.