3193 tn2 study of cost issues in transport operation …s3.amazonaws.com/zanran_storage/©the tas...

TRANSCRIPT

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry Commission for Integrated Transport November 07 Final

Freedom of Information Act 2000

The TAS Partnership Limited regards the daily and hourly rates that are charged to clients, and the terms of engagement under which any projects are undertaken, as trade secrets, and therefore exempt from disclosure under the Act.

In many of the Reports and Task Notes we produce, The TAS Partnership Limited uses commercially or personally sensitive data provided under confidentiality agreements by third parties to inform projects, and disclosure of this information could constitute an actionable breach of confidence. The detailed content of such Reports and Task Notes is therefore likely to be exempt from disclosure under the Act.

Consequently, The TAS Partnership Limited will expect to be consulted before any content of our Reports and Task Notes is released under a Freedom of Information Act 2000 request.

Copyright

The contents of this document are copyright The TAS Partnership Ltd., with the exceptions set out below. Reproduction in any form, in part or in whole, is expressly forbidden without the written consent of a Director of The TAS Partnership Ltd.

Cartography derived from Ordnance Survey mapping is reproduced by permission of Ordnance Survey on behalf of the Controller of HMSO under licence number WL6576 and is © Crown Copyright – all rights reserved.

Other Crown Copyright material, including census data and mapping, policy guidance and official reports, is reproduced with the permission of the Controller of HMSO and the Queen’s Printer for Scotland under licence number C02W0002869.

Freedom of Information Act 2000

The TAS Partnership Limited regards the daily and hourly rates that are charged to clients, and the terms of engagement under which any projects are undertaken, as trade secrets, and therefore exempt from disclosure under the Act.

In many of the Reports and Task Notes we produce, The TAS Partnership Limited uses commercially or personally sensitive data provided under confidentiality agreements by third parties to inform projects, and disclosure of this information could constitute an actionable breach of confidence. The detailed content of such Reports and Task Notes is therefore likely to be exempt from disclosure under the Act.

Consequently, The TAS Partnership Limited will expect to be consulted before any content of our Reports and Task Notes is released under a Freedom of Information Act 2000 request.

Copyright

The contents of this document are copyright The TAS Partnership Ltd., with the exceptions set out below. Reproduction in any form, in part or in whole, is expressly forbidden without the written consent of a Director of The TAS Partnership Ltd.

Cartography derived from Ordnance Survey mapping is reproduced by permission of Ordnance Survey on behalf of the Controller of HMSO under licence number WL6576 and is © Crown Copyright – all rights reserved.

Other Crown Copyright material, including census data and mapping, policy guidance and official reports, is reproduced with the permission of the Controller of HMSO and the Queen’s Printer for Scotland under licence number C02W0002869.

Freedom of Information Act 2000

The TAS Partnership Limited regards the daily and hourly rates that are charged to clients, and the terms of engagement under which any projects are undertaken, as trade secrets, and therefore exempt from disclosure under the Act.

In many of the Reports and Task Notes we produce, The TAS Partnership Limited uses commercially or personally sensitive data provided under confidentiality agreements by third parties to inform projects, and disclosure of this information could constitute an actionable breach of confidence. The detailed content of such Reports and Task Notes is therefore likely to be exempt from disclosure under the Act.

Consequently, The TAS Partnership Limited will expect to be consulted before any content of our Reports and Task Notes is released under a Freedom of Information Act 2000 request.

Copyright

The contents of this document are copyright The TAS Partnership Ltd., with the exceptions set out below. Reproduction in any form, in part or in whole, is expressly forbidden without the written consent of a Director of The TAS Partnership Ltd.

Cartography derived from Ordnance Survey mapping is reproduced by permission of Ordnance Survey on behalf of the Controller of HMSO under licence number WL6576 and is © Crown Copyright – all rights reserved.

Other Crown Copyright material, including census data and mapping, policy guidance and official reports, is reproduced with the permission of the Controller of HMSO and the Queen’s Printer for Scotland under licence number C02W0002869.

Freedom of Information Act 2000

The TAS Partnership Limited regards the daily and hourly rates that are charged to clients, and the terms of engagement under which any projects are undertaken, as trade secrets, and therefore exempt from disclosure under the Act.

In many of the Reports and Task Notes we produce, The TAS Partnership Limited uses commercially or personally sensitive data provided under confidentiality agreements by third parties to inform projects, and disclosure of this information could constitute an actionable breach of confidence. The detailed content of such Reports and Task Notes is therefore likely to be exempt from disclosure under the Act.

Consequently, The TAS Partnership Limited will expect to be consulted before any content of our Reports and Task Notes is released under a Freedom of Information Act 2000 request.

Copyright

The contents of this document are copyright The TAS Partnership Ltd., with the exceptions set out below. Reproduction in any form, in part or in whole, is expressly forbidden without the written consent of a Director of The TAS Partnership Ltd.

Cartography derived from Ordnance Survey mapping is reproduced by permission of Ordnance Survey on behalf of the Controller of HMSO under licence number WL6576 and is © Crown Copyright – all rights reserved.

Other Crown Copyright material, including census data and mapping, policy guidance and official reports, is reproduced with the permission of the Controller of HMSO and the Queen’s Printer for Scotland under licence number C02W0002869.

Quality Assurance

DOCUMENT INFORMATION

Document Title

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry

First Draft Created On Last Revision Saved On Name of File File Size Version (Revision) Number Total Prep & Editing Time (Minutes) To Date

28/02/2007 16:41:00 01/11/2007 11:24:00 3193 TN2 Study of Cost Issues in Transport Operation Bus Industry FINAL APPROVED 1664512 kb 8 32

QUALITY ASSURANCE Revision Final Prepared by Checked by Approved by Date 01/11/2007 ER/PT/SW SW CC

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ Contents ▪ 1

Contents

Executive Summary .................................................................................5

1 Introduction and Objectives .........................................................7

1.1 Understanding the Trends and Drivers in Cost Inflation - Introduction .........7

1.2 Structure ............................................................................................8

1.3 Objectives...........................................................................................8

1.4 Projected Outcomes .............................................................................9

2 Key Elements of Cost for the Bus Industry ........................................11

2.1 Information Supply ............................................................................11

2.2 Identifying Cost and Revenue Trends – A Dilemma .................................12

2.3 Proportion of Costs.............................................................................14

2.4 Labour Costs .....................................................................................15

2.5 Pensions ...........................................................................................15

2.6 Fuel .................................................................................................15

2.7 Spares and Materials ..........................................................................15

2.8 Insurance Costs .................................................................................16

2.9 Finance, Capital and Tax .....................................................................16

2.10 Overheads ........................................................................................16

2.11 The Community Transport Sector .........................................................17

3 Comparison of Costs for Public and Private Transport Modes ...............19

3.1 Motoring Costs ..................................................................................19

3.2 Public Transport Fares ........................................................................24

3.3 Fare Structure ...................................................................................28

3.4 Perceptions of Travel Cost versus True Cost ...........................................32

3.5 Fares Comparisons between Public Transport Modes ...............................37

3.6 Light Rail ..........................................................................................41

3.7 Taxis................................................................................................41

3.8 Household Transport Expenditure .........................................................41

4 Core Cost Key Performance Indicators..............................................45

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ Contents ▪ 2

4.1 Cost Headings ...................................................................................45

4.2 Establishing KPIs ...............................................................................46

5 Core Sensitivities and Cost Drivers...................................................49

5.1 Wage Levels......................................................................................49

5.2 The Effect of Traffic Congestion............................................................49

5.3 Legislation ........................................................................................52

5.4 Corporate Costs .................................................................................52

5.5 Spares and Materials ..........................................................................53

5.6 Fuel and Utilities ................................................................................54

6 Growth Disparities in Current and Forecast Costs Compared to Other Sectors .................................................................................................55

6.1 Trends in Wage Costs .........................................................................55

6.2 The Effect upon Bus Drivers.................................................................56

6.3 Trends in Weekly Earnings ..................................................................57

6.4 Regional Comparisons ........................................................................58

6.5 Paid Hours ........................................................................................58

6.6 Productivity.......................................................................................64

6.7 Comparisons with Wages in other Transport Sectors ...............................66

6.8 Comparisons with Other Sectors...........................................................68

6.9 Sample Data .....................................................................................69

6.10 Custom and Practice...........................................................................71

6.11 The Workforce ...................................................................................72

6.12 Barriers to Employment ......................................................................73

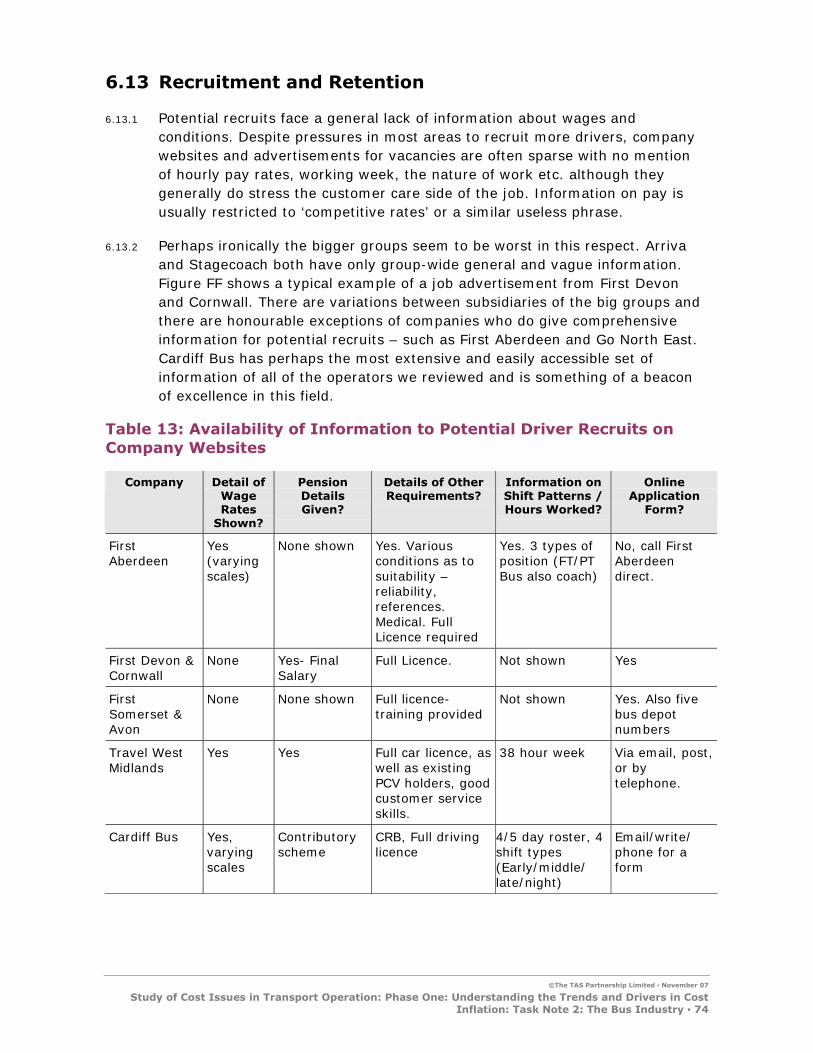

6.13 Recruitment and Retention ..................................................................74

6.14 Other Issues .....................................................................................76

6.15 Trends in Service Provision..................................................................78

6.16 Depot and Crew Change Locations........................................................83

6.17 Opportunities for Cost Control..............................................................84

6.18 Tender Preparation Costs ....................................................................85

6.19 Public Support for Buses .....................................................................85

7 Effect of Pension Issues and Additional Social Legislation in Labour Intensive Industries ...............................................................................87

7.1 Pensions ...........................................................................................87

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ Contents ▪ 3

7.2 Potential Impact of the EU Working Time Directive..................................90

7.3 National Insurance .............................................................................91

7.4 Social Legislation- Maternity, Paternity and Parental Leave ......................92

7.5 Child and Working Tax Credit Limits......................................................93

7.6 Overall Impact...................................................................................94

8 Compliance Costs and Legislative Change .........................................95

8.1 Disability Compliance Issues................................................................95

8.2 Environmental Legislation ...................................................................96

8.3 Traffic Commissioners.........................................................................96

8.4 Changes to Drivers’ Hours Regulations ..................................................99

8.5 Contract Compliance ..........................................................................99

8.6 Quality Contracts ............................................................................. 100

8.7 The EU Driver Training Directive......................................................... 102

9 Trends in Fuel and Fuel Consumption ............................................. 103

9.1 Fuel and Fuel Duty ........................................................................... 103

9.2 Vehicle Specification......................................................................... 107

9.3 Euro Engine Standards...................................................................... 110

10 Trends in Accident and Insurance Costs.......................................... 113

10.1 Insurance Issues.............................................................................. 113

10.2 The Predominant Approach................................................................ 114

10.3 Insurance Premium Increases ............................................................ 114

10.4 Insurance Costs Containment ............................................................ 116

10.5 Employers Liability Insurance ............................................................ 117

11 Base Composition of Apparently Fixed Costs ................................... 119

11.1 Fixed Costs ..................................................................................... 119

12 Trends in Capital Costs ................................................................. 121

12.1 New Vehicle Cost ............................................................................. 121

12.2 Vehicle Depreciation ......................................................................... 123

12.3 Coaches.......................................................................................... 125

12.4 The Second-Hand Market .................................................................. 126

12.5 Buy or Lease?.................................................................................. 126

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ Contents ▪ 4

12.6 Motoring Comparisons ...................................................................... 127

12.7 Cost Increases in Highway Infrastructure Projects................................. 128

13 Cost of Capital............................................................................. 131

13.1 Current Investment Climate .............................................................. 131

13.2 Cost and Types of Capital .................................................................. 131

13.3 Rates of Return ............................................................................... 133

13.4 Is this Achievable? ........................................................................... 134

14 Effect on Financial Outputs within the Various Scenarios................... 137

14.1 Future Modelling .............................................................................. 137

15 Effect of Operators Restoring Eroded Margins by more than Cost Recovery Fare Increases ....................................................................... 139

15.1 Historical Fares Policy ....................................................................... 139

15.2 Fares Trends Since 1986 ................................................................... 140

15.3 Effects of Fare Increases and Other Factors ......................................... 142

15.4 TAS Fares Model .............................................................................. 143

15.5 The Sheffield Experience ................................................................... 144

15.6 Is There a Better Way? Alternative Approaches to Fares ........................ 144

16 Summary and Conclusions ............................................................ 147

16.1 Scenario Summary........................................................................... 147

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 5

Executive Summary

Trends in Cost in the Bus Industry

Above inflation cost increases in the bus industry have been of some concern for a few years. Operators are seeing decreasing profit margins, local authorities are faced with further deregistrations of services and increasing tender prices, while the passenger faces more frequent and significant fare increases. This exercise set out to establish the main drivers of this level of increased cost.

Wages are the main item of expenditure for bus operators, accounting for just under 70% of all costs. Thus any increase in wages has a significant effect. Wages in the wider economy have been rising above the level of inflation for several years and this is equally true of the bus industry.

We have established that drivers in London have received pay rises well above inflation year on year, yet outside London drivers have received increases in line with general wage rises, although there has been a reduction in their working week (hence more drivers for the same work). In one region – the North West – bus drivers are now worse off in real terms than in 1994. There have also been additional add-on costs to wage bills caused by social legislation and EU regulations.

Maintaining funding for pension schemes has been problematical. The major groups have used reserves or proceeds of sale to top up pension funds.

The industry has been exposed to significant fuel price rises (particularly in 2005). As modern vehicles are less fuel efficient than their predecessors the level of consumption has increased too.

Traffic congestion and the need to schedule reliable services in the face of it, has imposed additional cost on bus operators. In areas where there is day -long congestion operators are forced to increase resources to maintain the same level of service, or look at widening headways or removing sections of route in order to implement an achievable timetable.

Local authority support for bus services has grown significantly, but almost all of the extra expenditure has been in London. Budgets outside London have just about kept pace with inflation and hence can support fewer services. Local authority budgets are also under pressure to maintain funding for the continuation of challenge-funded services when that funding expires.

Overhead costs are an increasing proportion of bus company cost, be they additional management or supervisory staff, or headquarters overheads passed down to the operating companies. This is despite the closure of many depot and bus station facilities.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 6

Insurance and accident costs have been escalating in recent years, largely due to the increasing claims culture. Companies have been able to stem the increase in motor insurance, but the area of major concern is Employers’ Liability insurance, for which a doubling or trebling of premium over five years is not unknown.

Whilst passengers have undoubtedly faced some significant fare increases, we believe that the level of these increases has not been as steep as official figures show. Moreover, the highest fare increases have applied only to single or return fares, which are purchased by a decreasing proportion of passengers. Multi-journey tickets, conversely, seem to have largely increased at or below the rate of inflation.

The industry faces significant future costs with the introduction of the EU Driver Training Directive from 2008 and full DDA compliance between 2015 and 2020.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 7

Introduction and Objectives 1

1.1 Understanding the Trends and Drivers in Cost Inflation - Introduction

1.1.1 The problems of cost escalation and cost pressures within the passenger transport industry are well documented and are of major concern for transport co-ordinators and operators.

1.1.2 Bus operating costs are currently rising well ahead of RPI. This is despite the bus industry operating in a competitive market with relatively low entry barriers. Labour is a major proportion of the industry’s costs and competition within the job market has intensified. The industry has faced staff shortages in recent years resulting in steep increases in wages in order to recruit and retain adequate personnel. Rapid expansion in bus provision in London has exacerbated the problem in the capital.

1.1.3 Above-inflation cost increases impact upon commercial services in a number of ways. Operators can raise fares or reduce services in order to maintain profit levels. Core commercial services are affected by increasing wages, higher cost of new vehicles, rising fuel costs and ever-increasing traffic congestion.

1.1.4 Marginal services may become unprofitable requiring the local authority to step in if it wishes services to remain. Budgets also face pressures from increasing cost for existing supported services. This is set against a general decline in local authority bus service support budgets as councils face pressures to fund other activities. Tender prices are also related in many cases to the level of revenue taken. Evening trade for the bus industry has all but evaporated in many areas, leading to further increases in cost.

1.1.5 This leads local authorities to prioritise supported services in order to maintain those which either fulfil the greatest social need or offer the best value for money. In some cases marginal services have simply been lost, while the local authorities have continued to support more poorly patronised services. This approach leads to increased costs per tendered journey as the passenger base on the remaining secured journeys is so much lower.

1.1.6 Cost escalation poses a serious threat to continued spending on the transport network as it raises the question of public ‘value for money’. Many local authorities have some measure of VFM in terms of subsidy per passenger and this threshold can be breached in the face of continuing price increases. It is vital that costs are controlled so that the industry can reinvest in expanding and strengthening the network – at an affordable cost and not by additional public expenditure.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 8

1.1.7 Infrastructure investment is also called into question as local authorities have suffered significant cost increases in highway infrastructure and also have reservations about the continuation of services for which bus priorities are being designed. Conversely, the continuation of the levels of service may depend upon the priorities offered by the infrastructure provision.

1.1.8 Although not within the remit of this work, it must be acknowledged that overall the bus industry remains in the decline which started in the late 1950’s. The whole subject of bus regulation or deregulation has risen up the political agenda. But statistics clearly show that deregulation was not the cause of this decline, though there is some evidence that it may have slowed it down.

1.1.9 It is against this background that the Commission for Integrated Transport (CfIT) is looking to conduct an analysis of cost trends within the bus and rail industry and possible mitigating strategies.

1.2 Structure

1.2.1 This Task Note is arranged into a series of sections with each devoted to a question as asked by CfIT in the original brief. At the head of each section of this Task Note the questions asked by CfIT are reproduced verbatim in red and the issues raised are addressed within the section.

1.2.2 There is some overlap in subject headings within the questions. To avoid repetition of subject matter and disjointed discussion of subjects, reference is made to key sections, such as section 9, which deals with all matters related to fuel, for example.

1.3 Objectives

1.3.1 This project has three objectives specified by CfIT:

• To understand the trends in cost inflation in the transport sector, and the reasons for it;

• To examine the impacts of these trends on behaviour of operators, financiers, local authorities, government; hence on transport policy objectives (congestion, pollution, accessibility); and

• To identify possible solutions (and their impacts).

1.3.2 The first phase of the project, researching and understanding the trends and drivers in cost inflation, will be dealt with in a series of Task Notes covering the key modes of bus, rail, tube / light rail, air and road / rail freight.

1.3.3 This first Task Note considers the bus industry:

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 9

• Key elements of cost for buses and how they are changing.

• How public and private transport modes compare in their costs.

• Core cost Key Performance Indicators.

• Core sensitivities and cost drivers.

• Growth disparities in current and forecast costs compared to other sectors.

• Effect of pension issues and additional social legislation in labour intensive industries

• Existing and forthcoming compliance costs and legislative change.

• Trends in fuel and fuel consumption.

• Trends in accident and insurance costs.

• Base composition of apparently fixed costs.

• Trends in capital costs.

• Cost of capital.

• Effect on financial outputs within the various scenarios.

1.4 Projected Outcomes

1.4.1 The research will provide a policy response to cost escalation within the transport industry and strategies available to minimise or control costs. It is hoped the report will provide a useful stimulus for engagement between Government, local authorities and operators on industry costs. The research will also add to the scientific evidence base, of which there is little published analysis of trends and mitigating strategies.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 11

Key Elements of Cost for the Bus Industry 2

CfIT Question 8: What are the key elements of costs for key modes - rail, bus, tube, air, freight (road and rail); and how are they changing?

• Labour

• Pensions

• Fuel

• Materials

• Finance

• Capital

• Tax.

2.1 Information Supply

2.1.1 Within this Task Note we have tried to be as representative as possible, given the available data. However, we do acknowledge that it is much easier to obtain information from larger operators, and particularly the five ‘big groups’ than it is to gather equivalent information from smaller operators. In particular, many of the statistics on bus usage, extent of operations and income are chiefly derived from DfT sources, gathered from those larger operators which complete the annual ‘Stats100’ form.

2.1.2 Information from small operators is difficult to obtain. Many such companies are family firms and even when they are constituted as limited companies, only submit abbreviated accounts to Companies House, which allow little financial analysis. The breakdown of costs and those key cost drivers may well be totally different for an operator surviving on school and private hire work.

2.1.3 GoSkills has calculated that around 75% of bus companies have ten or fewer vehicles, but conversely that 80% of bus drivers and a slightly higher proportion of local bus service mileage form part of or are provided by the major groups.

2.1.4 We acknowledge, therefore, that this Task Note’s findings will under-represent the small operators and the coaching sector and this must be borne in mind when interpreting the results.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 12

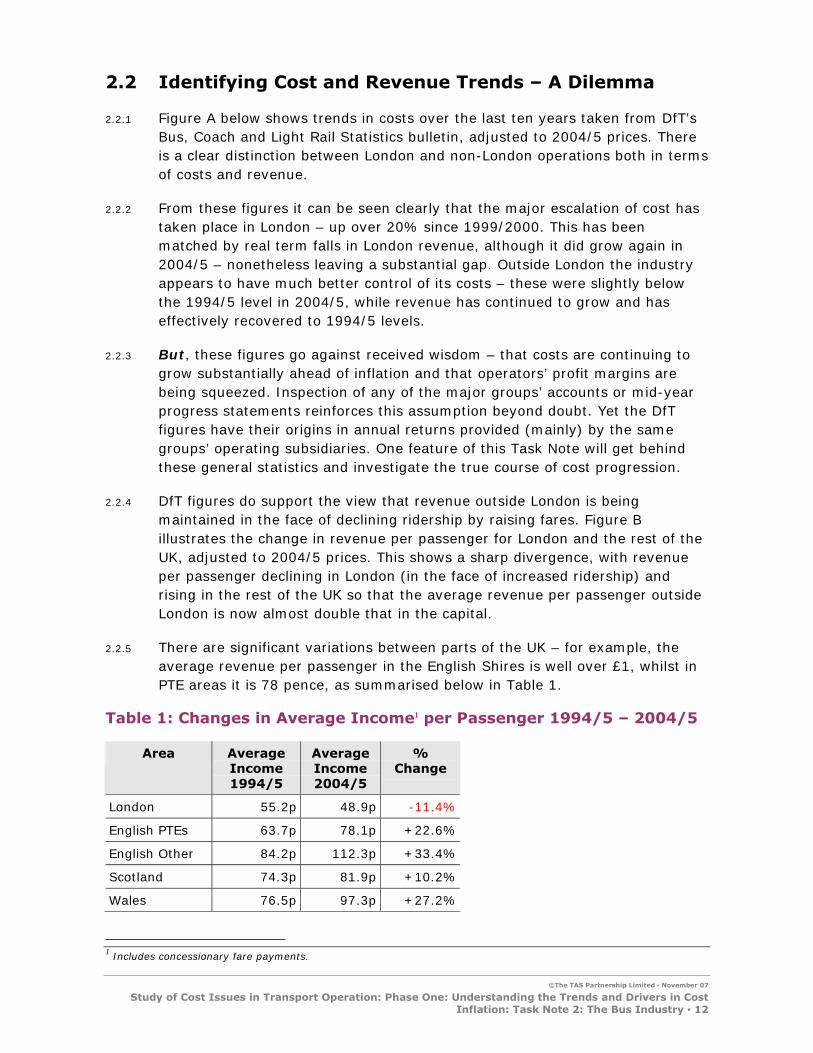

2.2 Identifying Cost and Revenue Trends – A Dilemma

2.2.1 Figure A below shows trends in costs over the last ten years taken from DfT’s Bus, Coach and Light Rail Statistics bulletin, adjusted to 2004/5 prices. There is a clear distinction between London and non-London operations both in terms of costs and revenue.

2.2.2 From these figures it can be seen clearly that the major escalation of cost has taken place in London – up over 20% since 1999/2000. This has been matched by real term falls in London revenue, although it did grow again in 2004/5 – nonetheless leaving a substantial gap. Outside London the industry appears to have much better control of its costs – these were slightly below the 1994/5 level in 2004/5, while revenue has continued to grow and has effectively recovered to 1994/5 levels.

2.2.3 But, these figures go against received wisdom – that costs are continuing to grow substantially ahead of inflation and that operators’ profit margins are being squeezed. Inspection of any of the major groups’ accounts or mid-year progress statements reinforces this assumption beyond doubt. Yet the DfT figures have their origins in annual returns provided (mainly) by the same groups’ operating subsidiaries. One feature of this Task Note will get behind these general statistics and investigate the true course of cost progression.

2.2.4 DfT figures do support the view that revenue outside London is being maintained in the face of declining ridership by raising fares. Figure B illustrates the change in revenue per passenger for London and the rest of the UK, adjusted to 2004/5 prices. This shows a sharp divergence, with revenue per passenger declining in London (in the face of increased ridership) and rising in the rest of the UK so that the average revenue per passenger outside London is now almost double that in the capital.

2.2.5 There are significant variations between parts of the UK – for example, the average revenue per passenger in the English Shires is well over £1, whilst in PTE areas it is 78 pence, as summarised below in Table 1.

Table 1: Changes in Average Income1 per Passenger 1994/5 – 2004/5

Area Average Income 1994/5

Average Income 2004/5

% Change

London 55.2p 48.9p -11.4%

English PTEs 63.7p 78.1p +22.6%

English Other 84.2p 112.3p +33.4%

Scotland 74.3p 81.9p +10.2%

Wales 76.5p 97.3p +27.2%

1 Includes concessionary fare payments.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 13

Figure A: Trends in Bus Industry Costs and Revenue2

75

95

115

135

155

175

195

215

1994/95 1995/96 1996/97 1997/98 1998/99 1999/00 2000/01 2001/02 2002/03 2003/04 2004/05

Co

st o

r R

even

ue (

pen

ce)

London Cost per km Non London Cost per km London Rev per km Non London Rev per km

Figure B: Trends in Revenue per Passenger3

45

50

55

60

65

70

75

80

85

90

95

1994/95 1995/96 1996/97 1997/98 1998/99 1999/00 2000/01 2001/02 2002/03 2003/04 2004/05

Pen

ce p

er

Pase

ng

er

London Outside London

2 Source www.dft.gov.uk/transstats 3 At 2005 prices

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 14

2.3 Proportion of Costs

2.3.1 Figure C shows the breakdown of bus industry costs for 2006 whilst a similar breakdown for 1978 is shown in Figure D. It is notable that despite labour costs being significantly lower (in real terms) than in 1978 they are broadly the same proportion of the total costs.

2.3.2 The proportion of industry expenditure devoted to maintenance has declined by about 50% since the late 1970s whilst the proportion of costs devoted to overheads has roughly doubled. However both of these categories of cost have fallen in real terms.

Figure C: Breakdown of Bus Industry Costs4 2006

Labour 68%

Bus Maintenance 9%

Depreciation 4%Overheads

10%

Fuel 9%

Figure D: Breakdown of Bus Industry Costs – National Bus Company, 19785

Fuel 6%

Overheads 5%

Depreciation 3%

Bus Maintenance 17%

Labour 69%

4 Source – Bus Industry Monitor 2006 5 Source – National Bus Company Annual Report for 1978.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 15

2.4 Labour Costs

2.4.1 The major influence on costs is labour, this accounts for over two thirds of bus operating costs, as illustrated in Figure C. Labour costs are now significantly lower in real terms than in 1978 although recent years have seen above inflation increases.

2.4.2 Driver recruitment and retention continues to be an issue in some areas, particularly where unemployment is low. Substantial pay increases have affected the viability of commercial bus services, resulting in greater pressure on the local authorities’ subsidised bus service budgets. Despite initial optimism, some driver shortages remain. A full investigation of wage trends and comparisons with other sectors is included in section 6.

2.5 Pensions

2.5.1 Pensions have become a major issue in all industries, and particularly affect labour-intensive industries such as the bus industry. The pension situation is discussed fully in section 7.

2.6 Fuel

2.6.1 Large increases in fuel cost have driven many operators to introduce multiple fare rises in 2005. The cost of fuel is internationally influenced and users of fuel suffer price fluctuations as a result. Despite increasing world demand and an acknowledgement of supplies of oil being finite, the cost of fuel has not followed a uniformly upward curve. There are signs that 2005’s severe increases are not being followed through into 2006 – reflected in price competition by the major supermarkets.

2.6.2 The current government has imposed only one increase in the level of fuel duty since 2000, thus the major driver of fuel cost is the cost of the fuel itself. Trends in fuel costs and fuel consumption are discussed fully in section 9.

2.7 Spares and Materials

2.7.1 The prime components of materials (engineering) costs are spare parts and labour. Evidence from the analysis of industry costs suggests that expenditure on spares and materials has remained roughly constant in real-terms since the early 1990s6, although the industry periodically has supply problems with particular spares and particular suppliers. None of the company reports we examined raised increases in costs for spare parts as a particular issue, although some increases in wages for engineering staff were apparent.

6 TAS Bus Industry Monitor 1991 to date.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 16

2.7.2 Real price increases have been offset by reductions in fleet size, the elimination of older, more maintenance-intensive vehicle types and improved designs. However, early low floor designs are now showing higher maintenance costs as they reach mid-life. There are signs that tyres, especially, are increasing in price well ahead of RPI. Further discussion of trends in spares and materials is contained in section 5.5.

2.8 Insurance Costs

2.8.1 Insurance costs for bus operation have increased very substantially in the last few years. This would appear to have resulted from a number of pressures on the insurance industry such as some high profile international incidents, an increasing “claims culture” in the UK and a reduction in the number of insurers willing to offer policies in respect of bus operation. The motor insurance industry has also become extremely competitive to the point that claims have exceeded premiums, which is obviously unsustainable.

2.8.2 Existing bus operators are finding that all premiums have been increasing substantially year on year, although there is evidence that motor insurance premiums are now levelling out. Operators are also expected to take on policies with higher levels of excess, so that their level of effective self-insurance has risen substantially.

2.8.3 New entrants to the industry are finding that without a low / no claims record, they are unable to find any insurer willing to take their risk without a disproportionately high initial premium.

2.8.4 Employers and Public Liability (EL) Insurance, however, continues to rise significantly. Premia have risen by up to three times in five years and EL insurance is now exceeding motor insurance costs significantly at many companies. The cost of EL insurance is particularly onerous for small to medium concerns. A fuller discussion of insurance issues is contained in section 10.

2.9 Finance, Capital and Tax

2.9.1 The raising of finance is an area of major difference between large and small operators, with the big groups able to borrow capital at just above the base rate, while smaller companies pay market rates of interest. Finance and capital issues are discussed fully in section 13.

2.10 Overheads

2.10.1 The immediate post-privatisation period saw huge reductions in company overheads, with central works facilities closed, bus depots and bus station sites sold off and layers of management and administrative staff removed.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 17

However, recent trends have reversed the reduction in overhead costs. A detailed analysis of overheads is contained in section 11.

2.11 The Community Transport Sector

2.11.1 There has been significant growth in the Community Transport (CT) sector over the last fifteen years. However, the sector has a very different breakdown of cost from that of the mainstream public transport industry, despite a general CT sector trend to develop away from the traditional volunteer-led organisational structure to more professional, business-led approaches.

2.11.2 Figure E shows a breakdown of costs for a typical mid-sized, 11-vehicle CT operator, taken from its annual accounts. Note that labour costs and vehicle running costs are reduced to around 30% of costs each, maintenance becomes a very unimportant cost heading as CT vehicles are generally operating low mileages and not subject to the degree of wear and tear suffered by buses in the mainstream.

2.11.3 Depreciation constitutes roughly five times the proportion of costs in the mainstream – CT vehicles are major items of expenditure but tend to have much shorter operating lives, and overheads account for 17% of all costs, much higher proportionally than the bus industry. There is logic to this as a CT organisation typically has premises, management and some sort of booking agency supported by only a small number of vehicles.

2.11.4 Figure F shows the five year trend in costs for the same organisation at outturn prices. It is difficult to identify any particular trends other than increases in both labour costs and running costs (principally fuel).

2.11.5 It can be fairly safely assumed that the CT sector will experience similar levels of cost increases to the mainstream sector, but in different proportions, thus, for example, labour cost increases are less critical to the CT sector while the effect of a significant increase in new vehicle cost becomes more critical.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 18

Figure E: Breakdown of Industry Costs – Community Transport Sector

Depreciation20%

Labour29%

Repairs and Maintenance3%

Overheads17%

Vehicle Running Costs31%

Figure F: Five Year Trends in Costs – Community Transport Sector

0

10,000

20,000

30,000

40,000

50,000

60,000

2001 2002 2003 2004 2005

£ S

pen

t P

er

Year

Vehicle Running Costs Overheads Depreciation Labour Repairs and Maintenance

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 19

Comparison of Costs for Public and PrivateTransport Modes

3

CfIT Question 9: How do public and private transport modes compare in their costs – and would we expect the divergence between the cost of motoring and public transport fares to continue?

3.1 Motoring Costs

3.1.1 Figure G below illustrates trends in indices for various aspects of motoring costs in addition to a total cost index and RPI since 1987. Total motoring cost has followed RPI closely, although there is wide divergence in the factors making up total cost. Motoring costs and public transport fares followed the same general trend until 2001 since when public transport fares have continued to rise at the same level while increases in RPI and motoring costs have levelled off since 2001.

3.1.2 The purchase cost of vehicles (both new and secondhand) has continued to decline in real terms since 1996 and is now only 11% above the 1987 base level, despite the increased sophistication of cars. Fuel costs grew significantly in the late 1990s as did tax and insurance although both levelled off in more recent years. The one area of motoring cost which has consistently climbed at a rate much higher than RPI is maintenance (parts, accessories, labour costs and roadside recovery) and there is little evidence of any alteration to this trend.

3.1.3 Recent evidence7, however, indicates that the running costs of a car are set to increase significantly due to fuel price increases above 10% in one year and with one of the major insurers increasing premiums by an average of 16% due principally to the increase in personal injury claims and increased liability due to the number of uninsured drivers on the road. The impact of new pay-as-you-drive car insurance schemes is likely to be another significant factor as this will ‘de-fix’ another substantial element of motoring costs.

3.1.4 Parking charges can be a significant element of the cost of journeys by car. There is some evidence to suggest that parking charges are increasing significantly, both as a result of real increases in charges for existing car parks and the introduction of charges in areas which once offered free parking, including hospitals, colleges and some major businesses. In West Yorkshire, for example, parking in the district council controlled car parks increased by between 18 and 38% in the four years between 1997 and 20018. However, a

7 Report from Sainsbury’s Bank detailed on BBC News website 5-9-2006 and insurance details on 31-8-2006. 8 Source: West Yorkshire Local Transport Plan 2001-5

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 20

study of car-borne commuters by the RAC in 200325 showed that at that time some 51% still had free parking provided by their employers at their place of work.

Figure G: Trends in Aspects of Motoring Costs9

0

50

100

150

200

250

300

350

1987 1991 1996 2001 2004 2005

Cost

In

dex

Vehicle tax and insurance MaintenancePetrol and oil Purchase of vehiclesAll motoring expenditure RPI

3.1.5 In order to demonstrate the relative importance of each of the cost headings shown in Figure G, a sample breakdown of motoring cost is shown in Figure H. This is prepared from RAC data from 2005 with the fuel price per litre updated to April 200612.

3.1.6 It can be seen that for new cars at least, depreciation takes up the major share of car costs at 40%, followed by fuel which accounts for 32% of motoring costs. Despite experiencing the highest rises in cost over the years since 1987, insurance and maintenance together make up only around 20% of running costs. On its own, tax (excluding fuel duty) accounts for a small proportion, just under 3%, of the total costs.

3.1.7 Evidence from a Motor Insurance report by BW-Deloitte-Touche10 indicates a growing gap between new car purchase price and secondhand prices, with prices for used cars falling at a greater rate in real terms than the trend in new car prices.

9 Data taken from ONS Social Trends Report, 2005 10 http://www.bw-deloitte.com/documents/BWDeloitte_UKMotorInsurance.pdf

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 21

3.1.8 Figure I then breaks down the motoring costs to the average family by category11 (although in this case purchase and finance are included under the same heading). It is notable how the effect of multiple car ownership within households shifts the proportions of expenditure so that insurance and maintenance become much more significant items of expenditure.

3.1.9 Figure J relates these categories to their effect on average household expenditure over time. Although the biggest proportionate increase has been in the insurance and tax category, it is notable that the average household now spends around 80% more on vehicle purchase than in 1981, despite real terms drops in car prices. This has reflected the growing trend toward multiple car households and an increased tendency to purchase new cars.

3.1.10 The percentage of households owning two or more cars grew from 17% in 1981 to 30% by 2003. Over the same period households that previously had no access to a car have acquired a car for the first time. Consequently the proportion of households owning a single car has remained broadly constant since 1967 at around 43-44%.

Figure H: Sample Breakdown of Annual Motoring Costs (2005)12

Insurance & Tax13%

Maintenance & Breakdown Cover

9%

Finance6%

Fuel32%

Depreciation40%

11 Source – Social Trends 36, April 2006, Office of National Statistics 12 Sample data taken from RAC cost of motoring index quarter three 2005. Figures based on VW Golf 1.6 over four year life at 12,000 miles per annum, fuel price updated to 93 pence per litre and fuel consumption at 41.5 miles per gallon.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 22

Figure I: Breakdown of Household Motoring Expenditure

Insurance and tax18.4%

Fuel27.0%

Repairs and servicing12.8%

Purchase41.8%

Figure J: Index of Average Household Expenditure on Motoring Costs

0

50

100

150

200

250

300

1981 1986 1991 1996/97 2001/02 2004/05

Exp

en

dit

ure

In

dex (

19

81

=1

00

)

Purchase Repairs and servicing Insurance and tax Fuel

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 23

3.1.11 Trends in the total amount of fuel (petrol) consumed by cars show some remarkable variations, illustrated in Figure K. This does not show any real trend in total consumption although there is a distinct fall in the last two years for which there is data.

3.1.12 The rate of fuel consumed by cars in terms of kilometres per litre is illustrated in Figure L. This shows clearly that cars have become considerably more fuel efficient over the ten year period being examined, with average fuel consumption improving by two kilometres per litre (5.6 miles per gallon) over ten years. This overall figure for improvements in fuel consumption probably masks even better performance by standard cars as it will be affected by significantly worse fuel consumption figures produced by the growing numbers of MPVs and 4x4s.

Figure K: Total Fuel Used by Cars 1994 -2004

28500

29000

29500

30000

30500

31000

31500

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Million

Lit

res

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 24

Figure L: Trends in Fuel Consumption by Cars 1994 – 200413

10.50

11.00

11.50

12.00

12.50

13.00

13.50

14.00

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Kilom

etr

es

per

Lit

re

3.2 Public Transport Fares

3.2.1 Figure M, taken from the ‘Social Trends’ report shows how DfT calculates that public transport fares, and more specifically bus and rail fares, have increased consistently ahead of RPI since 1987. Increases in bus and rail fares are now some 30% ahead of RPI. It is not a new development for bus fares to grow ahead of RPI. Between 1976 and 1985 fares grew by around 15% above RPI14. ‘Other’ fares, (taxi, ferry and air travel), have generally followed RPI, as have motoring costs, as demonstrated in Figure G above.

3.2.2 Although rail fares have consistently increased above RPI since 1987, bus fares remained in line with RPI until 1991, since which time they have risen consistently ahead of RPI.

13 Fuel Consumed: - Transport Statistics GB, Energy and Efficiency tables 2005. Kilometres Travelled: - Transport Trends 2005 14 Transport Statistics Great Britain 1976 - 1986

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 25

Figure M: Public Transport Fare Trends9

100

120

140

160

180

200

220

240

260

1987 1991 1996 2001 2004 2005

Cost

In

dex

Bus and coach fares Rail faresOther All fares and other travelRetail prices index

3.2.3 We have calculated our own fare index based upon the simple calculation of revenue (including payments for concessionary travel) divided by the number of passengers taken from DfT figures, with all figures adjusted to current prices and using 1994/95 as the base year with an index of 100. Figure N and Figure O show our estimates of how fares have risen in real terms since 1994/95. This period should have eliminated the deregulation effect and therefore illustrates the general ongoing trend in fare levels. Other than in Wales, income per passenger has grown around 10% above RPI.

3.2.4 The DfT’s own bus fare index does not include revenue in its calculation. The DfT figures generally show a higher increase than that indicated by our calculation, with a very wide difference shown in London. It must be noted, however, that the fares do not all relate to the same base level of income per passenger in 1994/199515 (which may reflect different journey lengths).

3.2.5 Table 2 below shows the actual income per passenger (adjusted to current prices) in each area. Note that the highest average income per passenger in 1994/95 was in English non-PTE areas and that these areas have suffered the highest percentage fare increases in subsequent years.

15 See Figure B

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 26

3.2.6 Figures for each country show that fares have risen in England and Scotland by around 10% in real terms over ten years, while Wales has seen a larger increase of 26% following significant progressive increases after the turn of the century. The Welsh figure may reflect changes in travel habits after the introduction of free concessionary travel, but there has been no equivalent shift in Scotland.

Breaking England’s figures down by area type in Figure O shows that there is considerable variation within the English results. While the non-PTE areas have increased by over 30% in real terms, PTE areas have incurred an increase just over 20% while London has seen a fall of just over 10%.

3.2.7 Table 3 goes on to show that this general pattern of fares increases by area type above does not apply uniformly as it compares changes in fares over ten years in a PTE area (South Yorkshire) and a shire area (County Durham). Overall there has been a lower level of increase in the shire area. RPI increased by around 52% in this period thus all single fares have increased well above RPI. At the foot of Table 3 the prices of weekly season tickets are shown – it is notable how the prices of these have increased at or below the level of RPI. This is discussed further in section 3.3.

Table 2: Average Income per Passenger 1994/1995 and 2004/2005

Year / Area London English PTE areas

English non-PTE areas

England Scotland Wales

1994/1995 £0.55 £0.64 £0.84 £0.68 £0.74 £0.77

2004/2005 £0.49 £0.78 £1.12 £0.75 £0.82 £0.97

Change -10.9% +21.9% +33.3% +10.3% +10.8% +26.0%

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 27

Table 3: Comparison of Fare Changes over 10 Years PTE and Shire

Fare in 1996

First South Yorkshire Fare 2006

% Change since 1996

Go Northern County Durham

Fare 2006 % Change since 1996

£0.45 £1.00 +122.2% £0.85 +88.9%

£0.65 £1.50 +130.8% £1.30 +100.0%

£0.75 £1.50 +100.0% £1.40 +86.7%

£0.85 £1.80 +111.8% £1.50 +76.5%

£0.95 £1.80 +89.5% £1.95 +105.3%

£1.10 £2.10 +90.9% £2.05 +86.4%

First Week16

£10.95 £15.00 +37.0%

Go n Save16

£12.50 £19.00 +52.0%

Figure N: Indices of Bus Fares in the UK (Current Prices) since 1994

90

100

110

120

130

140

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/200

0

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

Ind

ices

England Scotland Wales Great Britain

16 In both cases the prices for the ‘all routes’ versions bought on-bus is shown.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 28

Figure O: Indices of Bus Fares in England (Current Prices) since 1994

80

90

100

110

120

130

140

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/200

0

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

Ind

ices

London English PTE areas English non-PTE areas Great Britain

3.3 Fare Structure

3.3.1 One aspect of fares for bus journeys which has changed in many areas is the structure of ticketing. Prior to deregulation bus fare structures focussed principally upon single (and sometimes return) fares with a limited range of multi-journey tickets, which usually required some sort of photocard and a visit to a travel office to carry out each renewal. This approach has now changed radically. The majority of larger companies now offer day and weekly tickets which are bought on the bus. Initially, most of these were introduced (or relaunched) at very attractive prices to retain patronage and market share in competitive situations. It is perhaps worth noting that such tickets have an influence on the accuracy of passenger counts, since there is always a tendency to under-record non-fare-paying passengers.

3.3.2 In many urban areas – and particularly in PTE areas - the predominance of these tickets means that fewer than 25% of passengers now travel by purchasing single tickets and in many areas the day ticket acts as a default maximum value for a return ticket. A particular case in point exists in south Manchester, where Stagecoach’s day ticket at £2.70 is cheaper than two single fares for all but the shortest journeys.

3.3.3 Thus the significance of single fare levels can be significantly overstated and the importance of the pricing of day tickets overlooked. For example, in South

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 29

Yorkshire First implemented three fare increases in 2005 which led to criticism from the PTE, press and local elected representatives. The headline figures all related to the effects upon single fare values, which had indeed increased significantly, but this focus masked some very large increases and structural changes to day and weekly tickets which potentially affected far more users. In particular, the previous users of off-peak day tickets – priced at £2.20 at the beginning of 2005, found their only alternative (other than reverting to single fares) at the end of the year to be a £3.50 day ticket, or a 59% increase in one year. Conversely, those who continued to purchase the all-routes weekly ticket saw only a small price rise across the year.

3.3.4 The chart shown in Figure P illustrates changes to single fares over a range of distances and weekly ticket17 prices for First South Yorkshire since 1995, including the Retail Price Index for comparison, with all values scaled to 100 in 1995 for comparative purposes. Single fares are shown for one, two, three and seven mile journeys.

3.3.5 This shows clearly that there has been a steady rate of increase above RPI in all of the single fares, with fares for shorter distances increasing by the greatest proportion (equivalent to 9½% per year for the one mile fare) and longer journeys by a lower proportion (around 7½% per year). In the intervening period RPI has grown by an average of 2½% per year. It is notable, however, that the price growth of weekly tickets has remained at or below the rate of increase in RPI throughout this period.

3.3.6 It is perhaps unfair to concentrate on one company in one area. Some operators have applied significant price increases to multi-journey tickets with every price increase applied to single fares and there are also those who have not imposed the same level of single fare increases as the case above. But there does appear to be an overlying trend for single fares to rise well above the level of RPI while the cost of multi-journey tickets has risen roughly in line with RPI.

3.3.7 A similar exercise was performed using data for Go Northern’s operations in County Durham. The single fares which ranged between 50p and 180p at November 1996 have once again been scaled to 100 for comparative purposes. Figure Q shows a much lower rate of increase to single fares, except for the low-value short distance fares and once again its weekly Go’n’Save (GNS) season ticket has roughly followed RPI. There is one significant similarity to the First data in that fares in County Durham took a major upward divergence from RPI in 2005, again in response to fuel price increases18.

3.3.8 To look at another range of multi journey tickets, Figure R illustrates the price trend of Lothian Buses’ day and weekly tickets since 1991. After an initial

17 The price for the all day network-wide FirstDay ticket is shown here. 18 www.simplygo.com

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 30

period of above-inflation increases, prices have generally followed the trend of RPI since 1996 until 2005 when there was a significant increase in weekly ticket price but the day ticket price is now below the rate of growth of RPI.

3.3.9 The figures from both County Durham and Lothian support our findings from South Yorkshire that the price of multi journey tickets generally follows RPI much more closely. This also helps to explain why shire areas have shown a higher rate of overall increase in fares (expressed in terms of revenue per passenger) than the PTE areas. Shire areas tend to have lower availability of multi-journey tickets and a greater dependency upon off-peak passengers who are less likely to purchase multi-journey tickets. The level of single fares is therefore much more germane to shire areas.

Figure P: Trends in Bus Fares for First South Yorkshire 1995 – 2006

50

70

90

110

130

150

170

190

210

230

250

Dec-9

5

Apr-96

Aug-

96

Dec-9

6

Apr-97

Aug-

97

Dec-9

7

Apr-98

Aug-

98

Dec-9

8

Apr-99

Aug-

99

Dec-9

9

Apr-00

Aug-

00

Dec-0

0

Apr-01

Aug-

01

Dec-0

1

Apr-02

Aug-

02

Dec-0

2

Apr-03

Aug-

03

Dec-0

3

Apr-04

Aug-

04

Dec-0

4

Apr-05

Aug-

05

Fare

s In

dex (

19

95

=1

00

)

1 mile 2 miles 3 miles 7 miles Weekly RPI

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 31

Figure Q: Trends in Fares since 1996 – Go Northern, County Durham

100

120

140

160

180

200

220

240

260

Nov-

96

Mar

-97

Jul-9

7

Nov-

97

Mar

-98

Jul-9

8

Nov-

98

Mar

-99

Jul-9

9

Nov-

99

Mar

-00

Jul-0

0

Nov-

00

Mar

-01

Jul-0

1

Nov-

01

Mar

-02

Jul-0

2

Nov-

02

Mar

-03

Jul-0

3

Nov-

03

Mar

-04

Jul-0

4

Nov-

04

Mar

-05

Jul-0

5

Nov-

05

Mar

-06

Ind

ex (

Base

19

96

= 1

00

)

50 80 110 150 180 GNS RPI

Figure R: Trends in Day and Weekly Ticket Prices at Lothian Buses 1991 - 2006

100

110

120

130

140

150

160

170

180

190

May-9

1

Nov-

91

May-9

2

Nov-

92

May-9

3

Nov-

93

May-9

4

Nov-

94

May-9

5

Nov-

95

May-9

6

Nov-9

6

May-9

7

Nov-

97

May-9

8

Nov-

98

May-9

9

Nov-9

9

May-0

0

Nov-

00

May-0

1

Nov-

01

May-0

2

Nov-0

2

May-0

3

Nov-

03

May-0

4

Nov-

04

May-0

5

Nov-

05

Ind

ex (

19

91

= 1

00

)

All Day One Week RPI

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 32

3.4 Perceptions of Travel Cost versus True Cost

3.4.1 Motorists owning their own cars ostensibly face the same types of costs as bus operators:

• Overheads – purchase cost of the car, tax, insurance, MOT.

• Depreciation – this can be translated as an allowance against the purchase price of the next car or, more likely, finance costs against the existing vehicle. New cars can depreciate by around 40% as soon as they are driven from the garage forecourt.

• Semi-variable Cost – repairs, replacement tyres etc.

• Labour Costs – but in this case a value of the owner’s time spent driving.

• Marginal Costs – the marginal cost of fuel plus parking charges.

3.4.2 However, most motorists in calculating the cost of a journey consider only the marginal cost of such journeys – typically fuel at around 10 pence per mile. The true cost per mile of motoring has been shown to vary considerably dependent upon the owner’s annual mileage and the period of intended ownership. Using figures for a mid-range new car (Vauxhall Astra 1.4) the average cost per mile – excluding parking charges - varies between 23 pence for an owner driving 40,000 miles per year and the vehicle having a four year life to 76 pence per mile for an owner driving 10,000 miles per year and selling the car in year one19.

19 Source Glass’s Whole Life Costs – www.virtual-showroom.co.uk

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 33

Figure S: Comparisons of Whole Life Average Mileage Cost – Based on Vauxhall Astra 1.4 new in 2006.

0

10

20

30

40

50

60

70

80

1 Year 2 Years 3 Years 4 Years

Vehicle Life

Lif

e C

ost

- P

en

ce p

er

Mil

e

10000 mpa 20000 mpa 30000 mpa 40000 mpa

3.4.3 The range of whole life average mileage costs is shown above in Figure S. Note that for a motorist driving 10,000 miles per year the average cost is never below 47 pence per mile. 10,000 miles per year equates to around 32 miles per day over six days per week. The RAC has recently reported that a significant proportion of motorists make daily journeys of five miles and under20 - these people will therefore incur average mileage costs exceeding those shown for the 10,000 miles per annum category above as the overhead cost of owning the car must be spread over fewer miles driven. Conversely, it is clear from the above figures that for high mileage drivers covering 40,000 miles per year, the average mileage cost varies little between a three or four year vehicle life.

3.4.4 The costs above reduce for second-hand cars, with a three year old car costing £7,000 spreading the reduced purchase cost over the life of the vehicle. Over a four year life this reduces the average cost per mile by between 17.5 pence (10,000 miles per annum) and 4.4 pence (40,000 miles per annum) but this must be set against the increased maintenance cost as the vehicle grows older.

3.4.5 Thus the motorist’s perceived cost of motoring of around 10 pence per mile for fuel fails by some margin to reflect the true costs of motoring. One true advantage perceived by the motorist, however, is that additional passengers

20 RAC 2006 Annual Report at www.rac.co.uk

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 34

effectively travel free – incurring marginal additional fuel costs for transporting additional weight but again this is ignored by the motorist in estimating journey costs. Public transport fares generally do relate to individual passengers – group discounts are rare in public transport fares and, where they exist, cannot offer the same level of discount offered by the occupation of spare seats in cars.

3.4.6 Conversely, public transport fares are often perceived at the other extreme in that potential users, particularly infrequent travellers, perceive the headline maximum fares – standard open return fares for rail and basic single fares for bus which disguise the availability of other discounted tickets.

3.4.7 The need to interchange to complete a journey usually adds a disproportionate fares penalty to public transport journeys, particularly where there is also a change of operator. In general, the rail industry retains through ticketing across operating companies, but unlike the bus industry, there are actually many instances when the fare for a journey involving interchange is cheaper if the passenger purchases separate tickets21.

3.4.8 The difficulty is that whereas the car is an instantly available means of transport, even if there is a bus or train available to make the journey within a few minutes, the cheapest fare option is likely to involve some sort of pre-booking or prepayment. It could be considered that information is the key element here and the current information systems for public transport are flawed. Particularly for those unused to public transport, Traveline has many deficiencies and the National Rail Enquiry Service is prevented from informing intending passengers of situations where cheaper fares are available by purchasing separate tickets.

3.4.9 The following examples in Table 4 and Table 5 compare the mileage costs of two distinct journeys based on Preston. The first is a regular commuting trip within Preston from Ribbleton to the Royal Preston Hospital, while the second relates to a longer-distance trip from Preston to Newcastle. For car cost comparisons, the first assumes a driver covering 10,000 miles per annum, the second 30,000 miles per annum. The comparative public transport costs use the same mileage figure as the car journey, even though in both cases the route taken is longer than the direct car journey and both involve a change of vehicle.

3.4.10 Although in a more thorough comparison of journey costs, a generalised cost model would include values of time, this exercise simply compares out-of-pocket expenses.

21 This is an ongoing subject in Barry Doe’s ‘Fare Dealer’ column in Rail magazine – see issue 546 for examples.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 35

Table 4: Cost Comparisons – Local Commuting Journey

Mode

Daily Cost (Round

Trip) Cost per

Mile Notes

Car Journey

Car (Full Cost)22 £4.04 £0.64 Based on 10,000 mpa and 4 yr life

Car (Marginal Cost) £0.86 £0.27 Marginal fuel only

Parking Charges £1.50 Hospital Daily Parking Charge

Distance (miles) 8.6 Ribbleton - RPH from route planner

Bus Options

Single Fares £4.40 £0.51

Day Ticket23 £3.00 £0.35

Weekly Ticket23 £1.80 £0.21 Assuming over 5 working days

Monthly Ticket23 £1.45 £0.17 Assuming 22 working days per month

3-Monthly Ticket23 £1.32 £0.15 Assuming 22 working days per month

3.4.11 Table 4 shows that the true motoring cost for the local commuting journey is the most expensive of all travel options. Perhaps even more so, as the estimated annual commuting mileage is only 2,270 miles – needing significant ‘other’ mileage to spread the vehicle purchase cost over 10,000 miles.

3.4.12 Note that the public transport season ticket options are less expensive than even the marginal motoring cost. The key here is that the perceived cost comparison will be between the marginal motoring cost and the upfront single bus fares, hence the view that ‘catching the bus is twice as expensive as the car’.

22 Using figures shown in Figure S 23 Restricted to single operator only.

©The TAS Partnership Limited ▪ November 07

Study of Cost Issues in Transport Operation: Phase One: Understanding the Trends and Drivers in Cost Inflation: Task Note 2: The Bus Industry ▪ 36

Table 5: Cost Comparisons – Long Distance Journey

Mode

Cost (Round

Trip) Cost per

Mile Notes

Car Journey

Car (Full Cost)22 £71.14 £0.29 Based on 30,000 mpa and 4 yr life

Car (Marginal Cost) £27.36 £0.13 Marginal Fuel only

Parking Charges £7.30 Parking for 4-6 hours NCP Newcastle

Distance 273.6 Preston City Centre - Newcastle from route planner

Rail Ticket Options

Saver £54.20 £0.20 Through ticket - any train, any time walk-on fare

2 Saver £42.70 £0.16 Rebook at Carlisle - any train, any time walk-on fares

Saver + 2 Singles24 £31.90 £0.12 Pre-booked singles Preston - Carlisle and rebook at Carlisle.

3.4.13 Once again, for the long distance journey, all of the public transport options cost less per mile than the full car cost. The cost per mile of the cheapest version of rail fares is lower than the marginal car cost. The perception, however, will set the marginal car cost against the most expensive standard rail ticket.

3.4.14 However, the key factors in both journey examples are flexibility, information and pre-planning. For the local example the cheapest public transport option involves a commitment to a single operator, a large upfront payment and the need for a special journey to go and purchase the ticket.

3.4.15 The second example produces the cheapest travel option by purchasing three separate rail tickets but the need to commit to specific train journeys and considerable knowledge of rail ticketing.

3.4.16 These comparisons, however, only apply for single person journeys. Each additional person would face the same public transport cost while up to four additional people could share the car journey at no extra cost.

3.4.17 Some data from the RAC Report on Motoring25 on regular car drivers, reproduced in Table 6, provides illustration of the difficulties faced in dealing with issues of perception. The average car commuter drives in his or her car alone and their 14-mile journey takes them about 25 minutes. However, if they were to go on public transport, they estimate that it would have taken

24 Single tickets are Virgin Value Advance tickets, must be booked by 1800 the day before travel on specified trains and not valid on Fridays. 25 Taken from presentation ‘Commuting and Travel Choices (Aug 2003) at www.racfoundation.org

©The TAS Partnership Limited ▪ November 07