31, fund other moderator: presenter: douglas l. robbins ... · douglas l. robbins, fsa, maaa...

TRANSCRIPT

Session 31, Statistical Techniques for Fund Mapping and Other Applications

Moderator:

Douglas L. Robbins, FSA, MAAA

Presenter: Douglas L. Robbins, FSA, MAAA

Douglas L. Robbins

August 29, 2016

Statistical Techniques for Fund Mapping and Other Applications

2

Topics

Fund Mapping: What, Why, How?

Where do Linear Models Fit?

What Can Go Wrong?

Other Statistical Thoughts

3

Topics

Fund Mapping: What, Why, How?

4

DefinitionsFund – A subaccount within a

Variable Product Held within the Separate Account Has an objective (growth, income, etc) Many managed outside the ins co

Index – An indicator or measure of the performance of a certain broad asset class; may be real (e.g., S&P500) or notional (e.g., Large Cap)

5

How are the Two Related?One of them truly exists within typical

variable products

The other, at least for VA / VL, exists only w/i models

What does thatmean? Why doesit matter?

6

Fund Mapping GoalsBy its nature, every fund probably has

different risk & expected return characteristics Conservative funds tend to be low on both Aggressive funds have the opposite tendency

But there’s more to it, as asset blends all have their own tendencies

Fund mapping is an attempt at capturing these tendencies

7

What will this Affect?For recent business, conservatism will

generally reduce rider costs – bonds especially so (more on that below)

For seasoned business, it’s less clear:For an AB or DB may still be trueFor an IB or WB, think about the

possible futures for Cash and/or BondsBonds can end up being a worst case

once a contract is deeply in the money

8

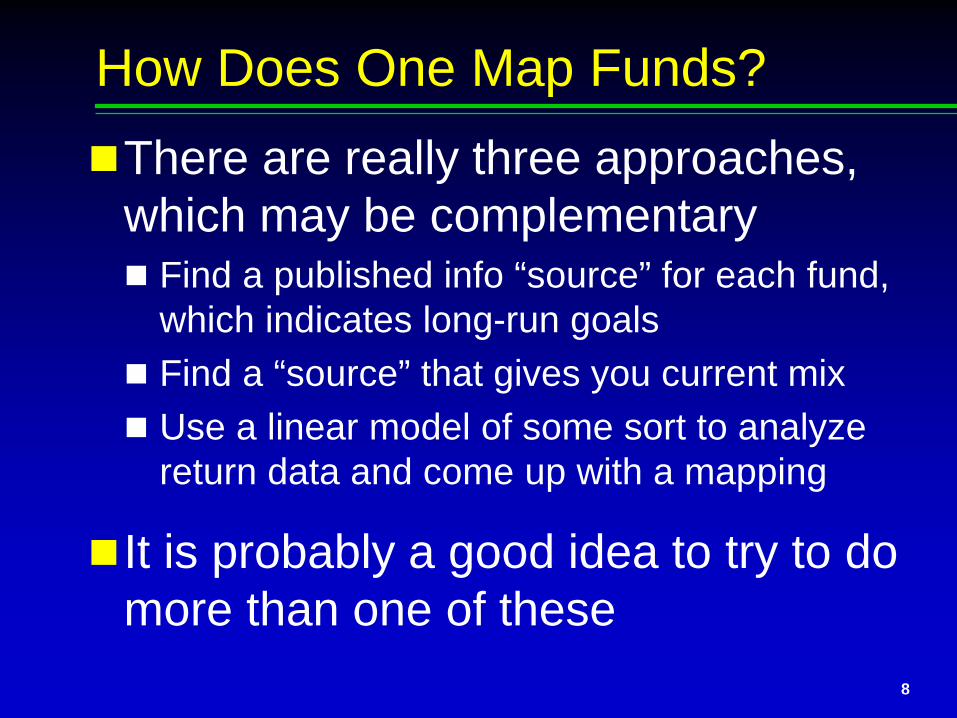

How Does One Map Funds?There are really three approaches,

which may be complementary Find a published info “source” for each fund,

which indicates long-run goals Find a “source” that gives you current mix Use a linear model of some sort to analyze

return data and come up with a mapping

It is probably a good idea to try to do more than one of these

9

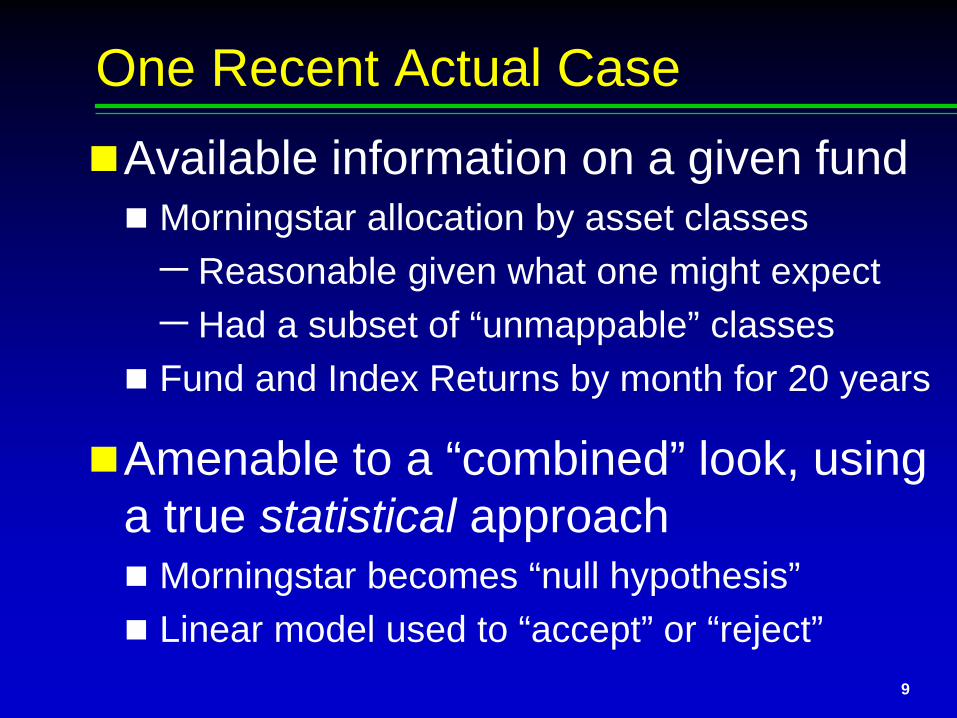

One Recent Actual CaseAvailable information on a given fund Morningstar allocation by asset classes−Reasonable given what one might expect−Had a subset of “unmappable” classes

Fund and Index Returns by month for 20 years

Amenable to a “combined” look, using a true statistical approach Morningstar becomes “null hypothesis” Linear model used to “accept” or “reject”

10

Topics

Where do Linear Models Fit?

11

DefinitionsWhat does “Linear Model” even

mean?

At the end of the day, it means you are mapping predictors to predictees using linear factors

One way to think about this involves matrices (something from WAY back)

12

What do you mean?

13

A Couple Important PointsThe matrix of predictors and the vector

of coefficients can have “n” dimensions

There is no scientific reason you need a column of constants (i.e., the “1s”), or a least squares goal

Then why is it the most common textbook example? Because it’s elegant, intuitive, & easy to visualize And also, this . . . .

Does it look linearly related?

What will happen if I model w/o a constant?14

Here is Some Data

Does it look linearly related?

What will happen if I model w/o a constant?15

Here is Some Data

16

With the Constant, This Happens:

Bingo!!

17

Anything Else we should Know?

Yeah: For one, that isn’t the only plausible “answer”

Here’s another, within 95% confidence limits18

Anything Else we should Know?

19

When that can Haunt YouWhen does this matter “a little”?

When would it matter “a lot”?

Should this issue concern me, vis-à-vis Fund Mapping?

What else, related to Fund Mapping?− Using a zero constant is a practical necessity− Multiple “X” variables are a key feature

20

As an Aside . . . .

Does this data set look like a good candidate for linear modeling? Why?

21

Here is my Linear-Modeling Result

22

Here is my Linear-Modeling Result In Linear Models, only coefficients must be linear

Data can be anything, which is part of what makes the technique so powerful

23

A couple more asides:Does this data look linear?

24

A couple more asides:Does this data look linear?

It is, in fact; but what is the equation?

25

A couple more asides:Does this data look linear?

It is, in fact; but what is the equation? That’s right: y = 15 (plus “e”) Including X is not useful

26

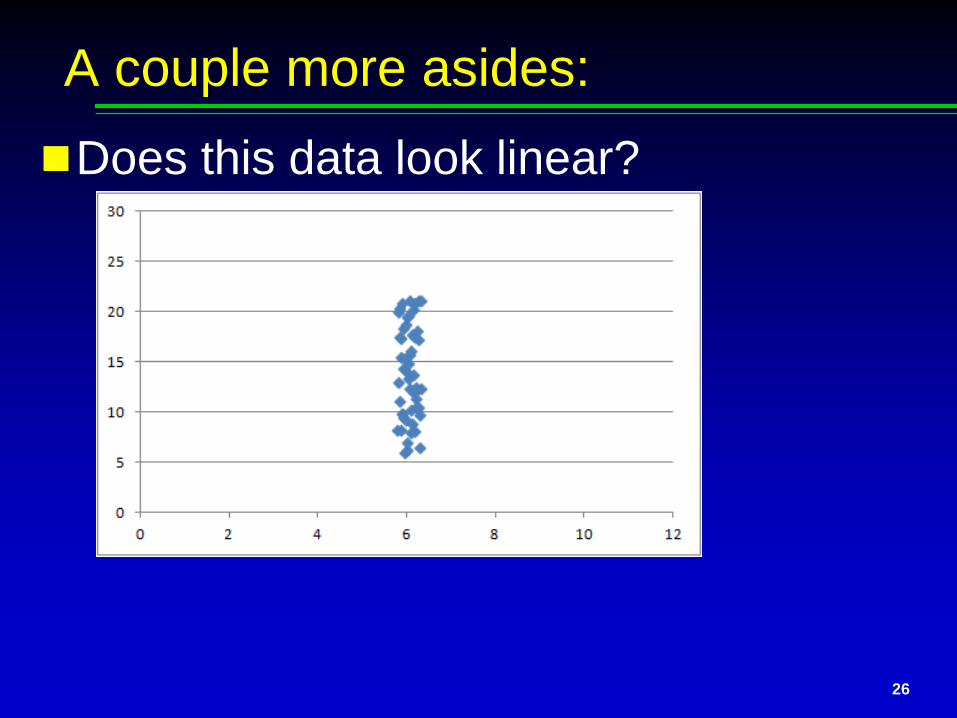

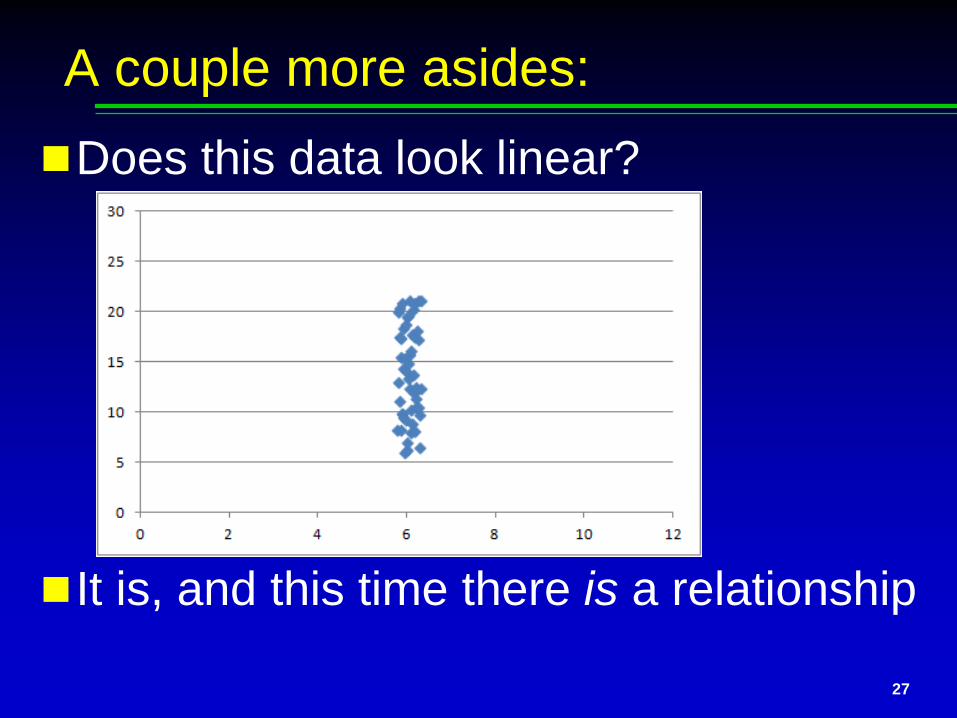

A couple more asides:Does this data look linear?

27

A couple more asides:Does this data look linear?

It is, and this time there is a relationship

28

A couple more asides:Does this data look linear?

It is, and this time there is a relationship But the picture looks like: x = 6 (or very nearly) And for that reason, a regression is hopeless

29

Summary - A Fund-Mapping Linear Model:

Examines a fund’s returns (“Y”)

Has no constant (row of 1s)

Has dimensions (“Xs”) equal to the number of indices being mapped to

Coefficients more or less constrained: Must all be positive Must sum to 100%

30

Topics

What Can Go Wrong?

31

Cash is Typically Tough to Map

32

Cash is Typically Tough to MapRecall this data from earlier:

Use about 0.2% instead of 6 for “X” above, and it’s about what you get

33

Most Funds won’t map well to all 5 Indices

Some will have a trivial or essentially a “0 coefficient” relationship to the fund’s returns

If your process doesn’t sort these out, future “predictability” will be hurt

Additionally, due to constraints, and since Cash has minimal impact on final return, it will tend to rise or fall very fluidly; result?

May need to estimate Cash outside of your Linear Model (as in my Morningstar example – can’t reject “null hypothesis,” really)

34

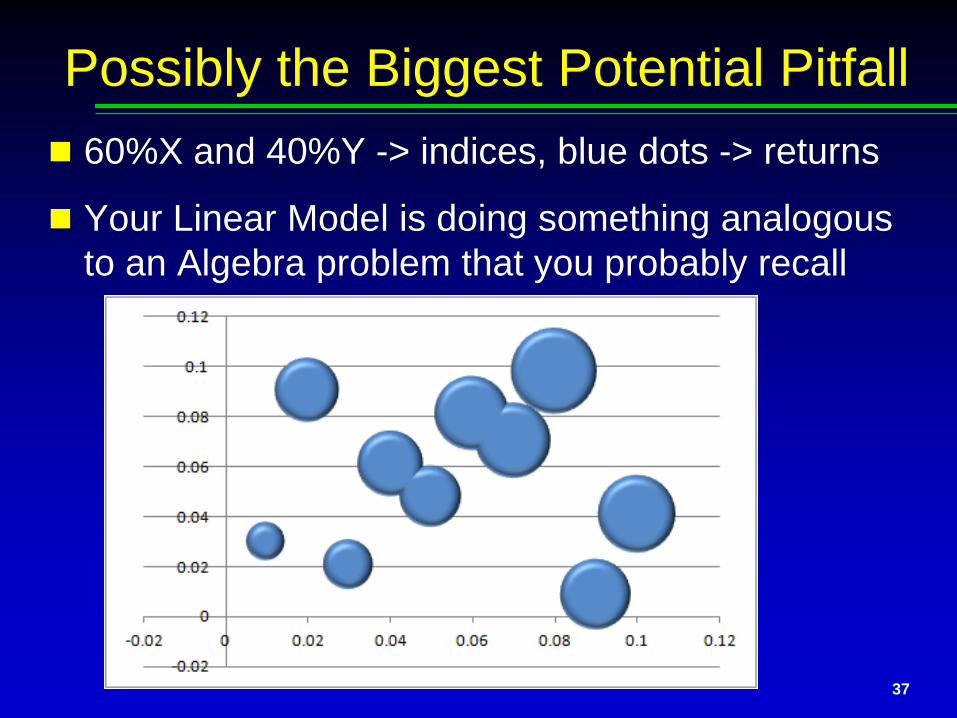

Possibly the Biggest Potential Pitfall

35

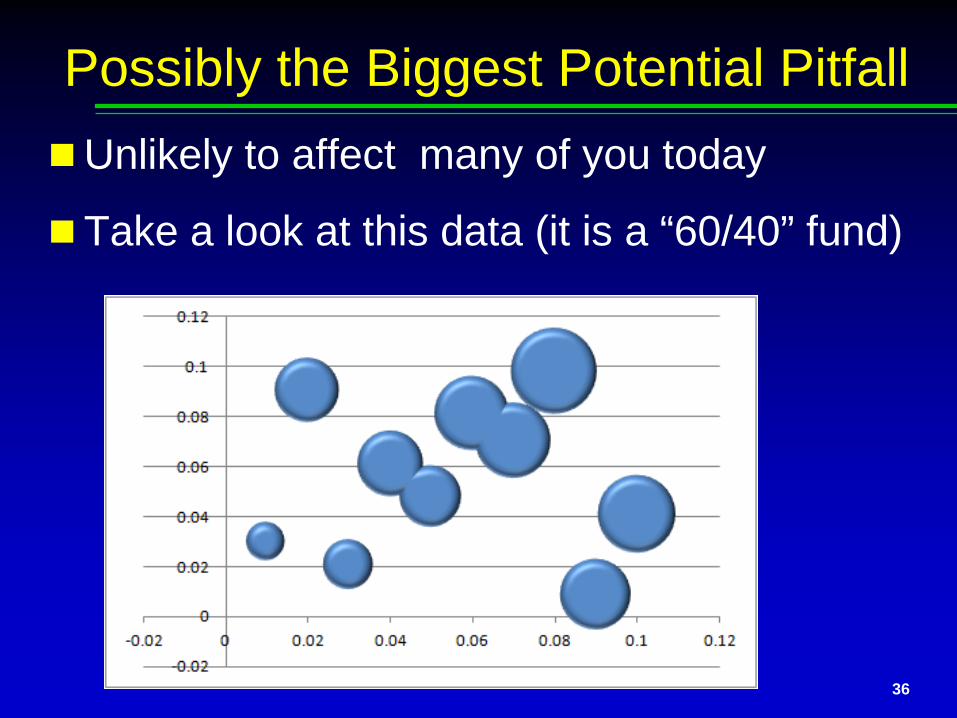

Possibly the Biggest Potential PitfallUnlikely to affect many of you today

36

Possibly the Biggest Potential PitfallUnlikely to affect many of you today

Take a look at this data (it is a “60/40” fund)

37

Possibly the Biggest Potential Pitfall 60%X and 40%Y -> indices, blue dots -> returns

Your Linear Model is doing something analogous to an Algebra problem that you probably recall

38

Possibly the Biggest Potential PitfallIt’s something like the following: X + Y = 20 X – Y = 14

You have 2 equations and two unknowns, so you quickly solve

39

Possibly the Biggest Potential PitfallIt’s something like the following: X + Y = 20 X – Y = 14

You have 2 equations and two unknowns, so you quickly solve

X = 17, so Y = 3

40

Possibly the Biggest Potential PitfallIt’s something like the following: X + Y = 20 X – Y = 14

You have 2 equations and two unknowns, so you quickly solve

X = 17, so Y = 3

Yay!

41

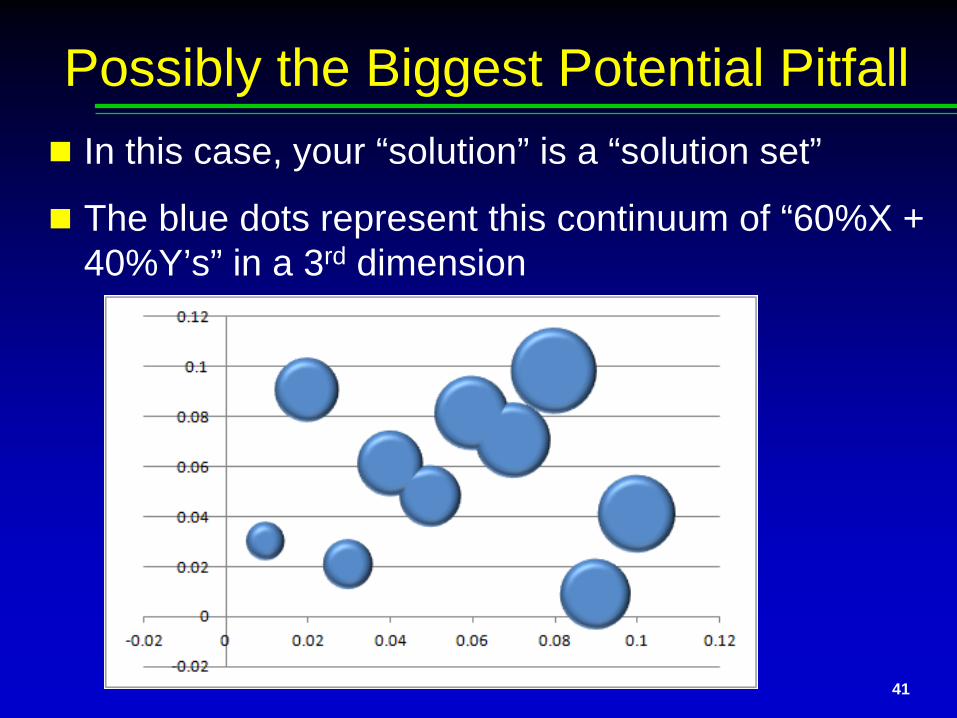

Possibly the Biggest Potential Pitfall In this case, your “solution” is a “solution set”

The blue dots represent this continuum of “60%X + 40%Y’s” in a 3rd dimension

42

Possibly the Biggest Potential PitfallAnyway, then your teacher did this: X + Y = 20 3X + 3Y = 60

43

Possibly the Biggest Potential PitfallAnyway, then your teacher did this: X + Y = 20 3X + 3Y = 60

And you threw your hands up in the air, and said, “But . . . the answer could be anything!!”

44

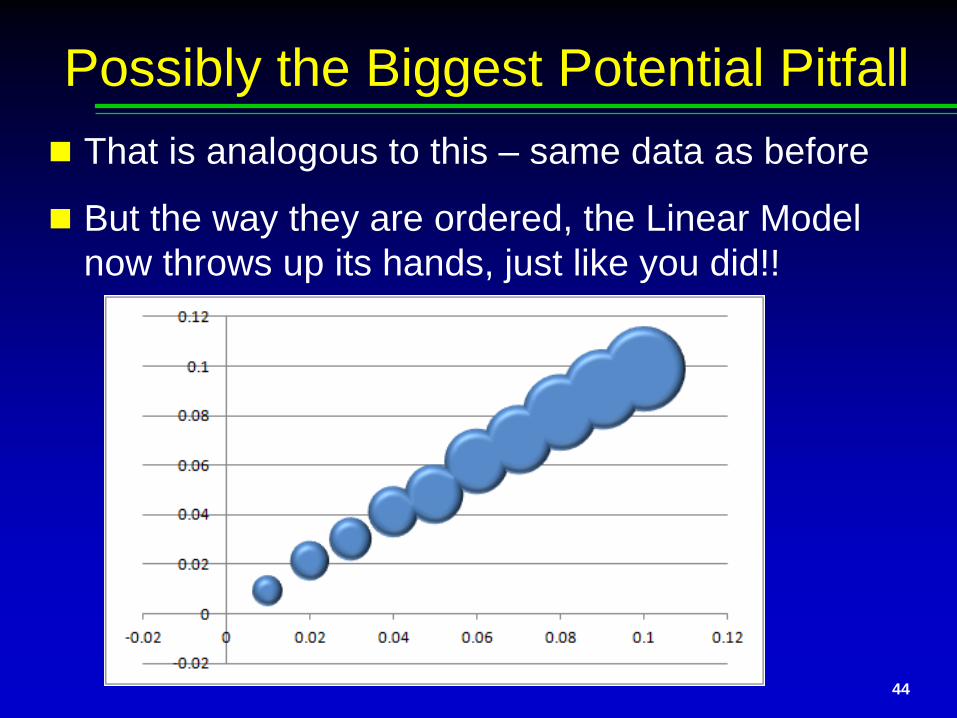

Possibly the Biggest Potential Pitfall That is analogous to this – same data as before

But the way they are ordered, the Linear Model now throws up its hands, just like you did!!

45

Possibly the Biggest Potential Pitfall In the first case, a regression’s output will

almost always be very accurate

46

Possibly the Biggest Potential Pitfall In the first case, a regression’s output will

almost always be very accurate

In the second, it will likely look roughly like:

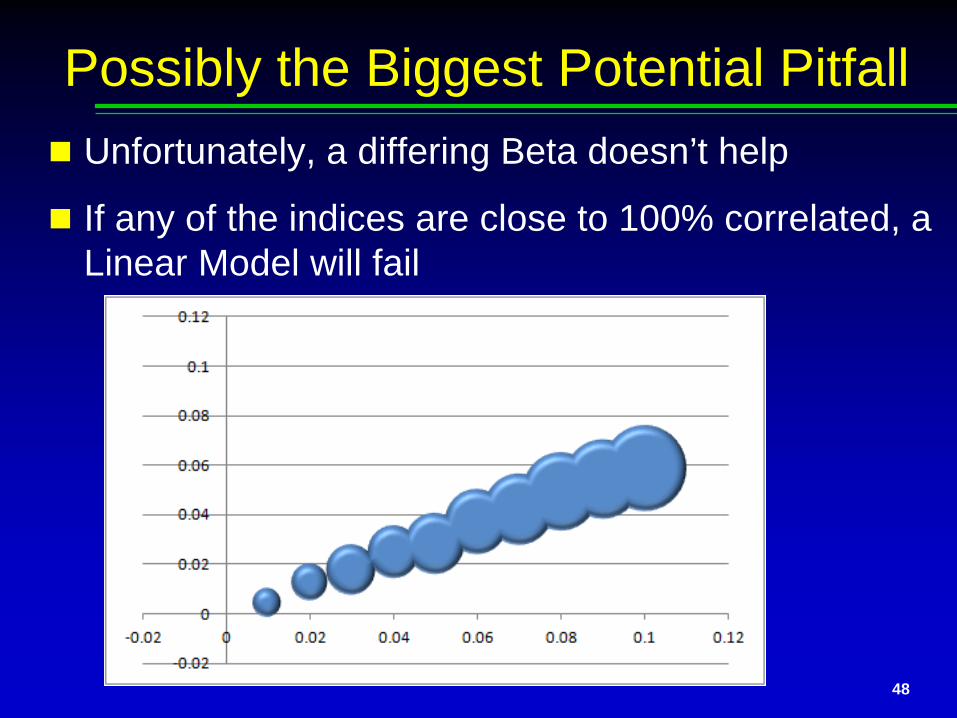

Unfortunately, a differing Beta doesn’t help

47

Possibly the Biggest Potential Pitfall

Unfortunately, a differing Beta doesn’t help

If any of the indices are close to 100% correlated, a Linear Model will fail

48

Possibly the Biggest Potential Pitfall

Why could this be quite important?

49

Possibly the Biggest Potential Pitfall

Why could this be quite important?

What do you think this data represents?50

Possibly the Biggest Potential Pitfall

Why could this be quite important?

What do you think this data represents?

Correct! It’s a portion of the 2008-2009 market 51

Possibly the Biggest Potential Pitfall

Analysis of a balanced fund here will likely fail

52

Possibly the Biggest Potential Pitfall

Analysis of a balanced fund here will likely fail

Your model will probably detect a relationship overall, but your coefficients may not even be close

53

Possibly the Biggest Potential Pitfall

Lack of variation in “X” data – e.g., Cash

Inclusion of variables that aren’t really statistically significant

Intercorrelation between “X” variables

54

Summary of 3 Potential Pitfalls

55

Topics

Other Statistical Thoughts

In my experience, actuaries tend to do stochastically only at the economy

What if assumptions are not independent? Some risk factors, like economy and lapse, may

be “prima facie dependent”

Others might seem independent, but not be

56

Something to Consider . . . .

In my experience, actuaries tend to do stochastically only at the economy

What if assumptions are not independent? Some risk factors, like economy and lapse, may

be “prima facie dependent”

Others might seem independent, but not be

A couple simple examples to try to make my meaning clear:

57

Something to Consider . . . .

Consider a proposed relationship between outside temperature, and how much ice cream you want (Sm, Md, Lg) I would claim this is “prima facie dependent”

The hotter it is, the more ice cream you want!

Now, what if you are considering your desire for ice cream, alongside your desire for Oreo cookies? Independent?

Let’s assume so; but what if . . . . 58

The Ice Cream / Oreo Paradox

. . . . you know your spouse will kill you if you go large on both, in a single day?

How effectively will you analyze the “Risk Margin” related to a given “snack,” if you hold the other “snack” at “expected”?

59

What If . . . .

. . . . you know your spouse will kill you if you go large on both, in a single day?

How effectively will you analyze the “Risk Margin” related to a given “snack,” if you hold the other “snack” at “expected”?

You won’t – you will die!

60

What If . . . .

. . . . you know your spouse will kill you if you go large on both, in a single day?

How effectively will you analyze the “Risk Margin” related to a given “snack,” if you hold the other “snack” at “expected”?

You won’t – you will die!

Moral: Two independent events can become dependent in terms of tail risk, especially when PV’ing future losses

61

What If . . . .

62

Thoughts on Loss Distribution, and: How large a block is “large enough”?

Concept: “Velocity of Diversification,” Case StudyHow many of you are on the Life Side?Have your PD guys developed ROP

Term? If so, have you thanked them?

There is one stochastic / statistical sense in which ROP Term is far superior to ordinary Term

63

Ordinary 10-Year Term Example

A little corny: no “i”, no tax or “v”/RBC

64

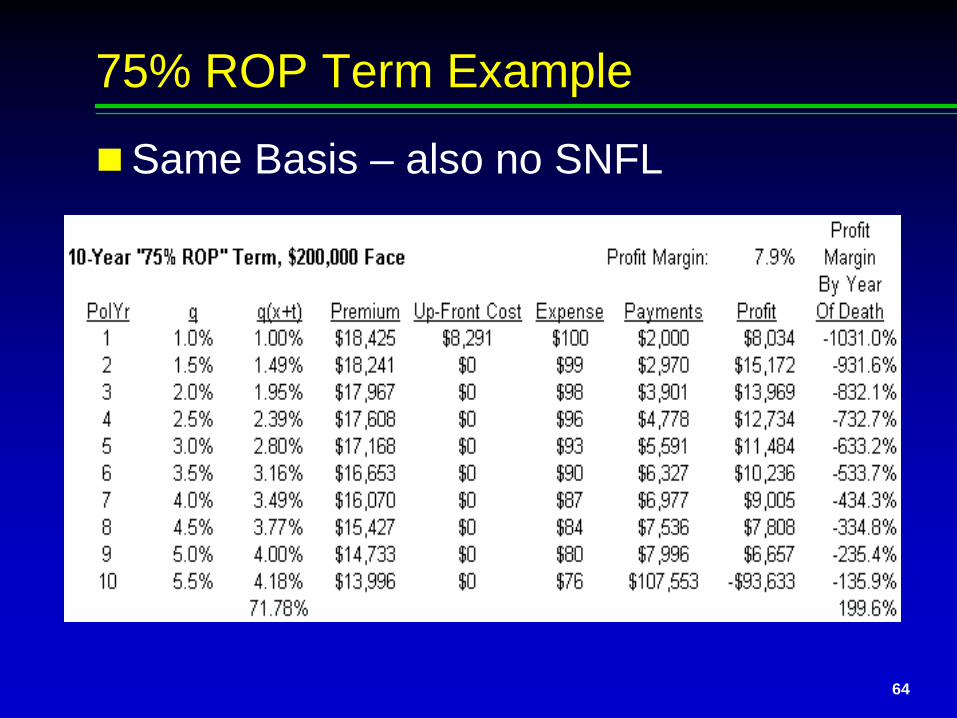

75% ROP Term Example

Same Basis – also no SNFL

65

How has ROP improved my Risk situation?

P(Any 1 policy sold having a positive profit margin) is the same – 72%

Standard Deviation of the profit margin of a single policy is massively betterFor straight Term it was 1493%For ROP it is now only 335%Those are not typos

66

How has ROP improved my Risk situation?

This, by the way, alludes to why Vegas works for both sides; and also part of “table limit theory”

E.g., Roulette black: Expected return = -5.3%; sigma ~= 100%

Bettor says, “Maybe I’ll win!”

House says, “I win in the long run!”

67

How has ROP improved my Risk situation?

But how about betting on 00?

Expected = -5.3%; sigma ~= 576%!

Bettor says, “Maybe I’ll win!”

House says, “I win in the long run, but you’re not going to bankrupt me in 1 spin!”

It takes the house 33 times as long to become “sure”(-ish) of winning

68

How has ROP improved my Risk situation?

By designing ROP Term, PD folks have done something similar

In my version, you must sell almost 34,000 straight Term policies to even get sigma = mu, for total profit

For the ROP term, it’s only ~1,700

ROP Term diversifies ~20x as fast

69

How has ROP improved my Risk situation?

Corollary: Any experience study estimates a time series, so . . . .

Early future is always more solid than distant future

If mortality in years 7+ ends up 0.5% higher than estimated:Term profit margin = -38.6%ROP Term margin = 0.5%

70

Moral

In at least some important ways, we cheat ourselves if the only assumption we think of stochastically is the economy

“Thinking” stochastically doesn’t have to mean modeling things that way

However, it may mean more than simple sensitivity testing