>30jaar> 30 jaar op de beurs - vfb - vfb - vfb · · 2015-04-30geosea deme blue energy...

TRANSCRIPT

> 30 JAAR> 30 JAAR OP DE BEURS

TOM BAMELIS – CFOAPRIL 25 2015APRIL 25, 2015

June 20, 1984: IPO AvH

2

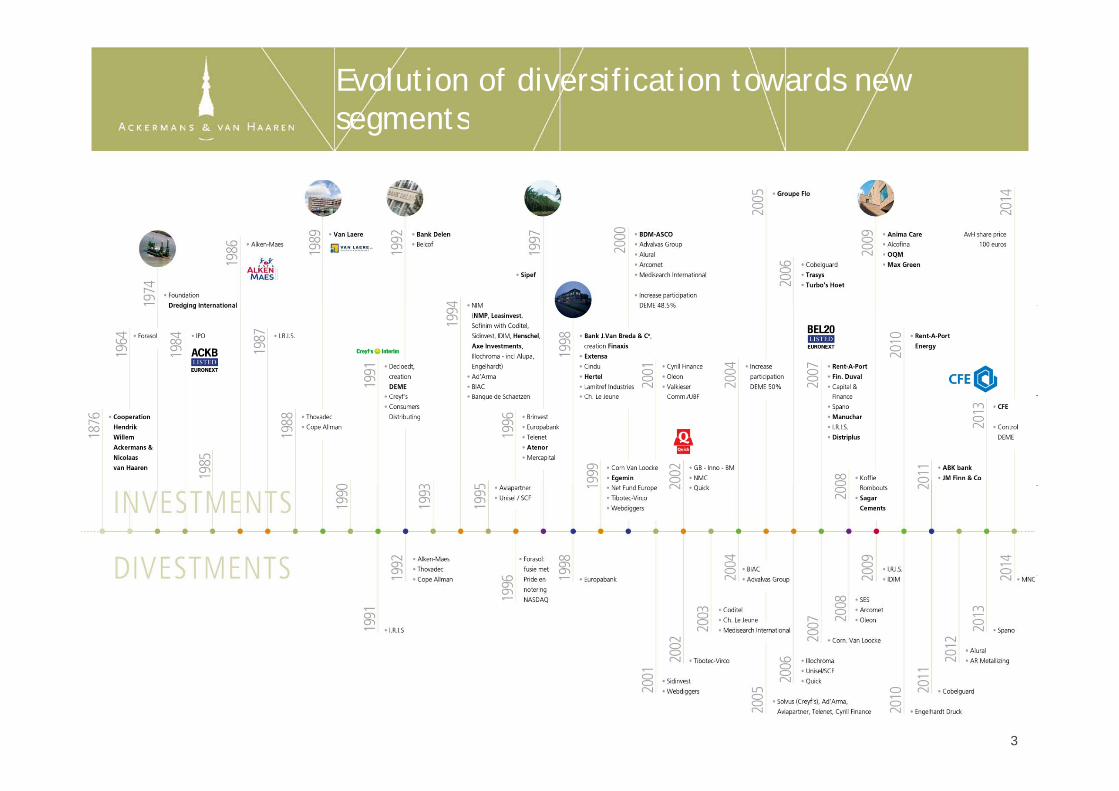

Evolution of diversification towards new segmentssegments

3

Tijd.be, 2/12/2014

Belga, 27/2/2015

L’Echo, 3/12/2014

De Tijd, 3/12/2014

44

De Standaard, 28/2/2015

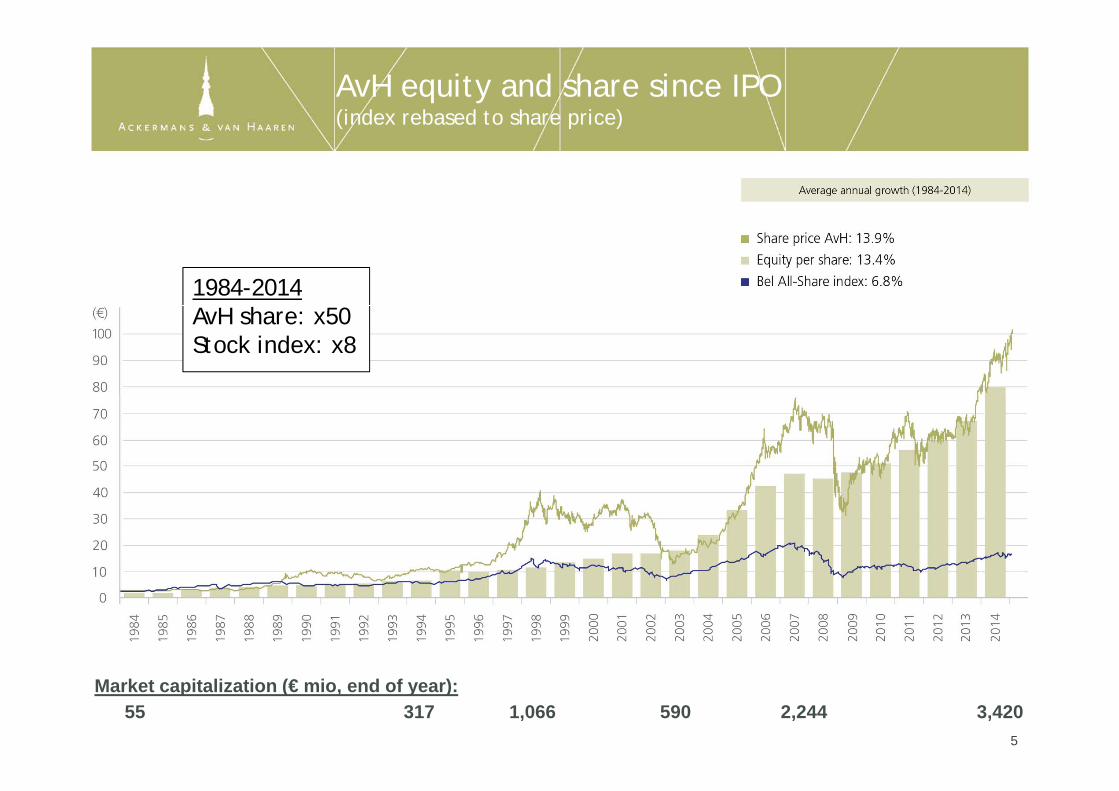

AvH equity and share since IPO(index rebased to share price)( p )

1984-2014AvH share: x50Stock index: x8

5

Market capitalization (€ mio, end of year):55 317 2,2445901,066 3,420

Evolution of AvH equity and share price since IPOsince IPO

CAGR (1984 2014) CAGR (1984 2014)CAGR (1984‐2014) Equity per share 13.4% Equity per share incl. dividend 14.2%

CAGR (1984‐2014) Share price 13.9% Share price incl. dividend 14.5%

6

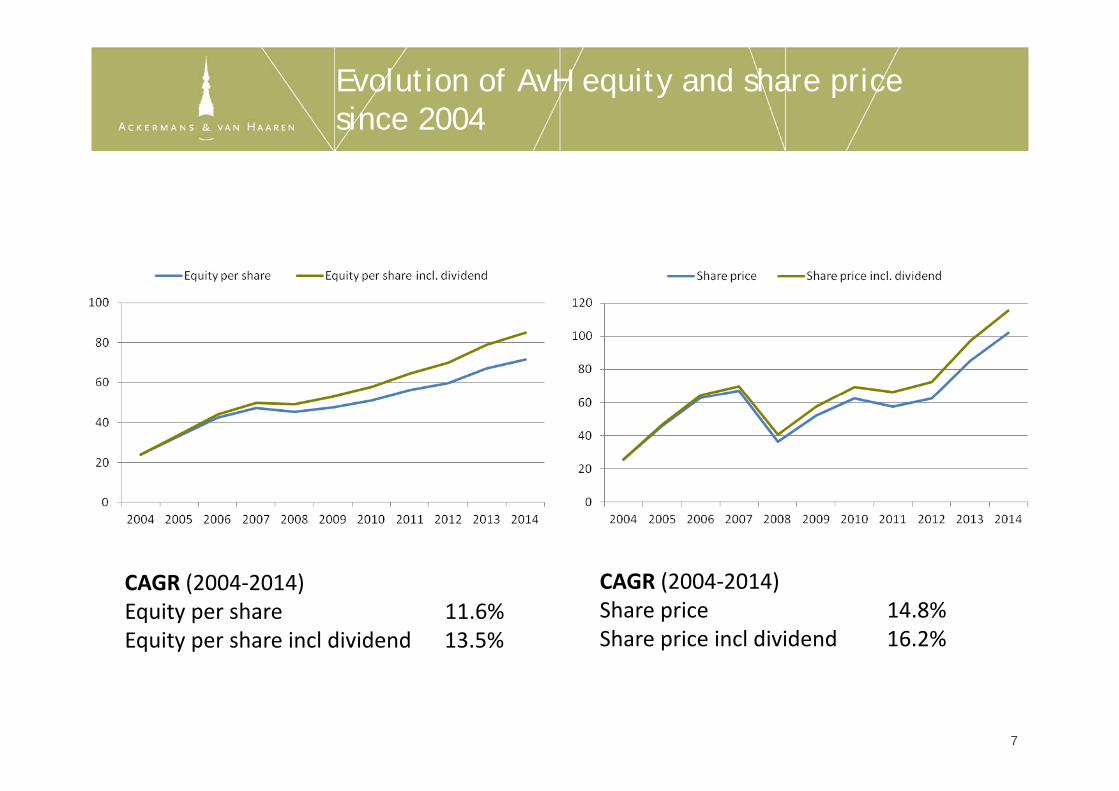

Evolution of AvH equity and share price since 2004since 2004

CAGR (2004 2014) CAGR (2004 2014)CAGR (2004‐2014) Equity per share 11.6% Equity per share incl dividend 13.5%

CAGR (2004‐2014) Share price 14.8% Share price incl dividend 16.2%

7

Value creation in Belgium

8

Source: Value Square, Fundamentele waardecreatie Belgische beursgenoteerde bedrijven 2003-2013

8

AvH strategy: We work for growth

Focus on strategic participationsEnsure equity growthAverage annual growth of

11.6% (2004-2014)

Create shareholder value Dividend of € 1.82AvHBelgian all

AvH share: x50Stock index: x8

(1984-2014)

Belgian all share index

Average annual growth of 10.8% (2004-2014)

9(until 24/2/15) 9

Ackermans & van Haaren: Introduction

• Providing development capital• From an industrial background

• Company values• Discretiong

• With a long term focus• Financed with own financial resources• Working for growth

• Independence• Common sense (“Hollandse

nuchterheid”)

• A pro-active shareholder within the participations

• Company strategy• Long term vision

• Selection of top-management• Definition of long-term strategy• Strategic focus

Strict operational and financial

• Diversificiation in a limited number of strategic participations

• Sound financial policy: positive net cash position• Strict operational and financial

discipline• Active board representations• Value creation fully aligned with

cash position• Opportunistic approach

Corporate governanceValue creation fully aligned with management

• Not a holding company

• Corporate governance• Board of directors (9 members):

majority of family representatives• Management (7 members): g p y

• No holding company inefficiencies• No shared financing structure / cross

guarantees 10

• Management (7 members): meritocracy

11

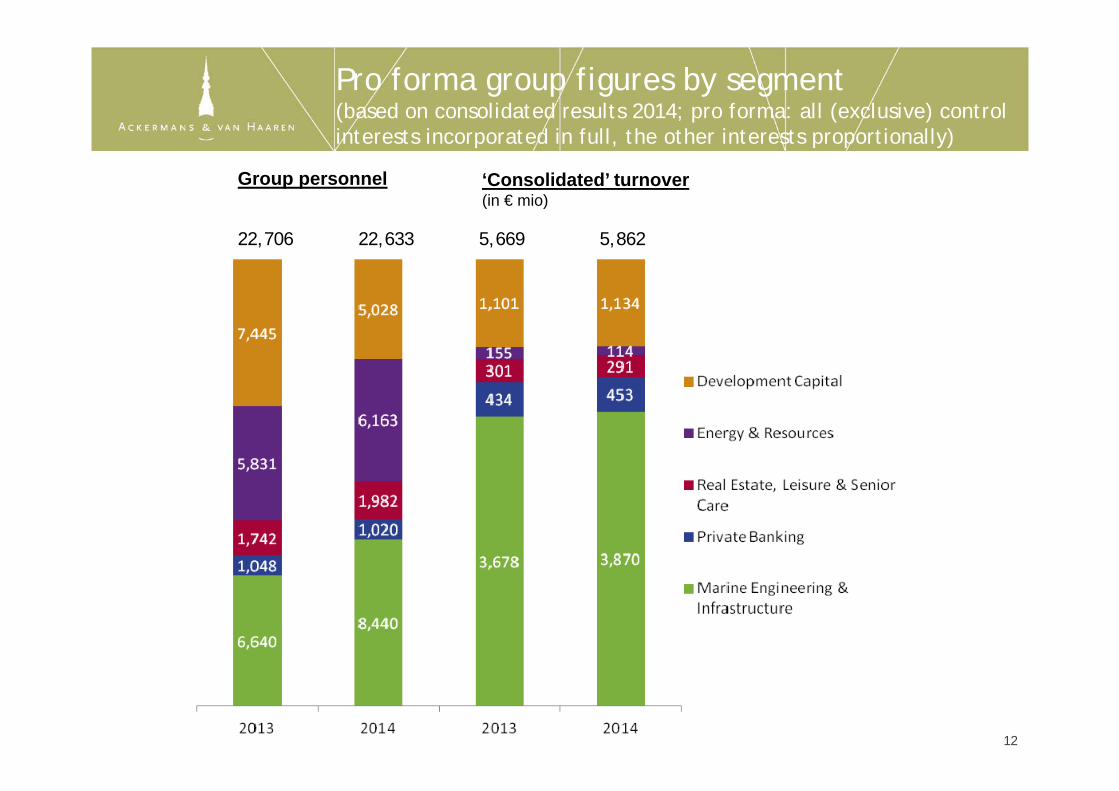

Pro forma group figures by segment(based on consolidated results 2014; pro forma: all (exclusive) control interests incorporated in full, the other interests proportionally)

Group personnel ‘Consolidated’ turnover(in € mio)

22,633 5,86222,706 5,669

12

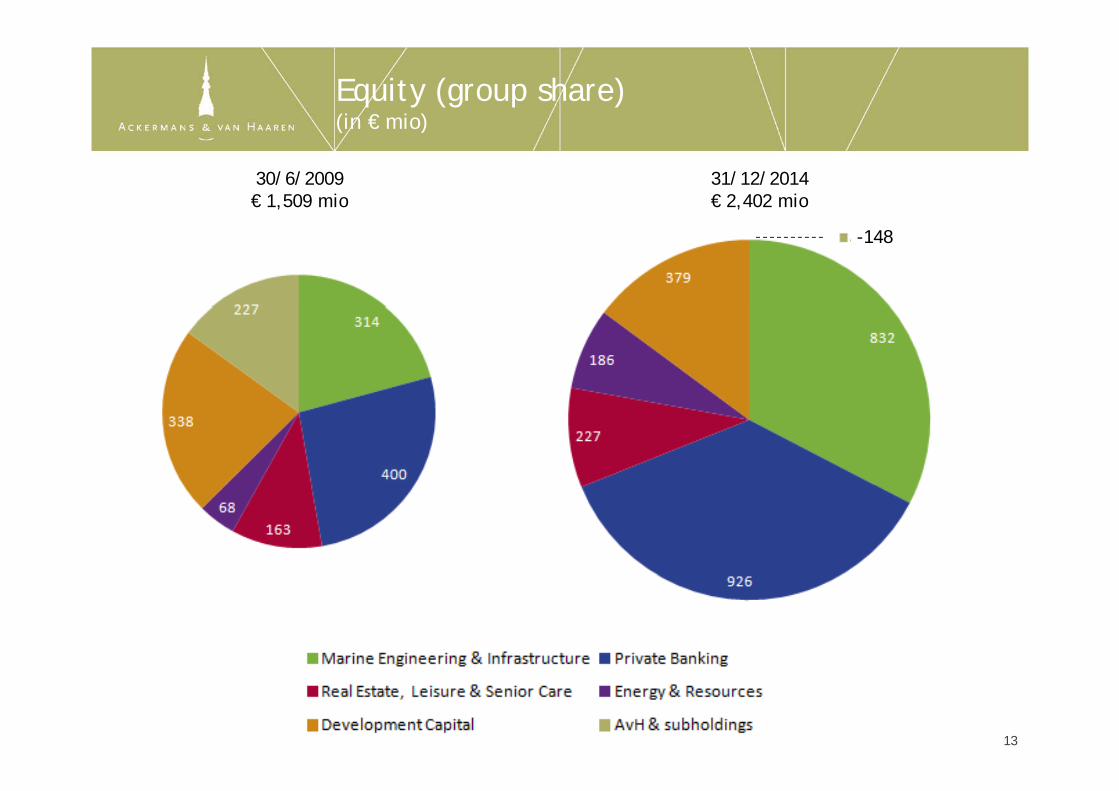

Equity (group share)(in € mio)(in € mio)

30/6/2009€ 1,509 mio

31/12/2014€ 2,402 mio

-148

13

Consolidated group result

(in € mio) 2014 2013 2012(2) 2011 2010( )

Marine Engineering & Infrastructure 106.2 59.7 51.7 54.6 58.7Private Banking 91.4 84.5 71.5 88.1 63.6Private Banking 91.4 84.5 71.5 88.1 63.6Real Estate, Leisure & Senior Care 14.7 15.8 3.6 4.5 8.6Energy & Resources 19.5 8.7 16.4 19.0 16.5Development Capital -6 7 -6 6 5 9 8 6 13 3Development Capital -6.7 -6.6 5.9 8.6 13.3

Result from participations 225.1 162.1 149.1 174.8 160.7C it l g i d l t it l 15 4 29 5 22 7 0 9 0 3Capital gains development capital -15.4 29.5 22.7 -0.9 -0.3Result from participations (incl. capital gains) 209.7 191.6 171.8 173.9 160.4

AvH & subholdings -7.1 -7.2 -3.9 -0.9 -0.1

Other non-recurrent result 12.5 109.5(1) -0.6 4.5 0.5Consolidated group result 215.1 293.9(1) 167.3 177.5 160.8

(1) Incl. € 109.4 mio result on the “remeasurement” of AvH’s existing 50% stake in DEME when taking full control over DEME in December 2013

(2) Restated financial statements 2012 (IAS19)14

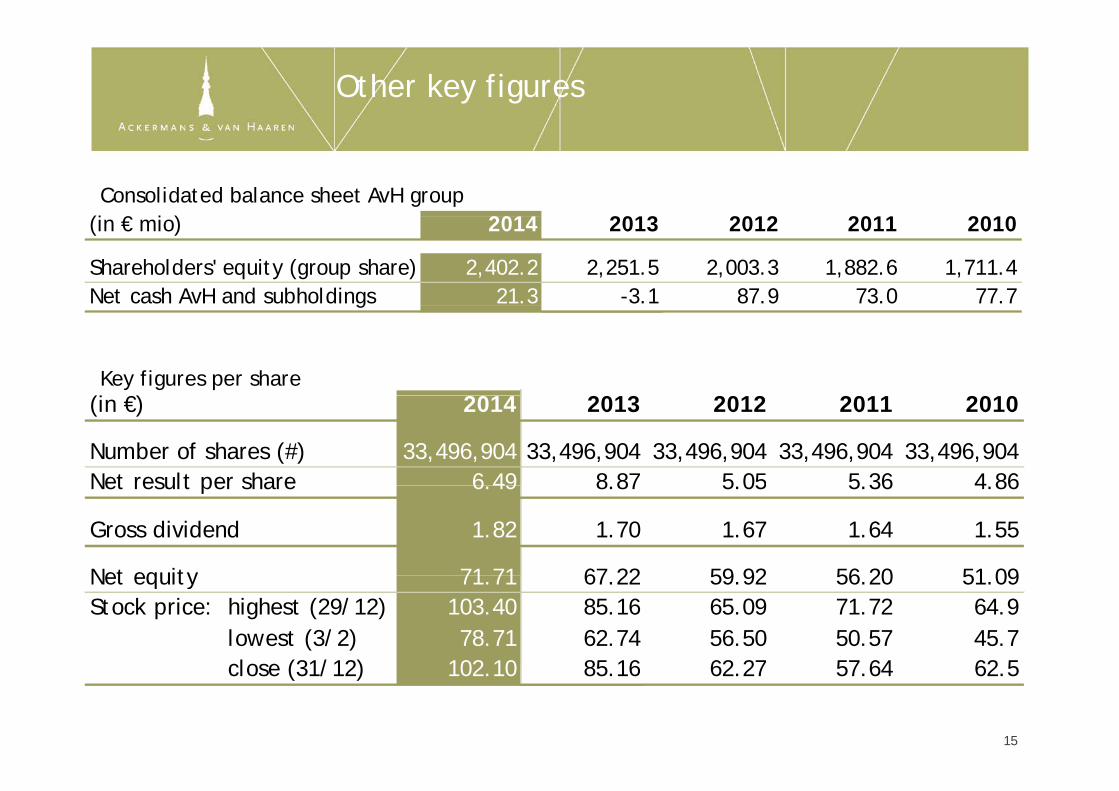

Other key figures

(i € i ) 2014 2013 2012 2011 2010Consolidated balance sheet AvH group

(in € mio) 2014 2013 2012 2011 2010

Shareholders' equity (group share) 2,402.2 2,251.5 2,003.3 1,882.6 1,711.4Net cash AvH and subholdings 21.3 -3.1 87.9 73.0 77.7g

(i €) 2014 2013 2012 2011 2010Key figures per share

(in €) 2014 2013 2012 2011 2010

Number of shares (#) 33,496,904 33,496,904 33,496,904 33,496,904 33,496,904Net result per share 6 49 8 87 5 05 5 36 4 86Net result per share 6.49 8.87 5.05 5.36 4.86

Gross dividend 1.82 1.70 1.67 1.64 1.55

Net equity 71 71 67 22 59 92 56 20 51 09Net equity 71.71 67.22 59.92 56.20 51.09Stock price: highest (29/12) 103.40 85.16 65.09 71.72 64.9 lowest (3/2) 78.71 62.74 56.50 50.57 45.7 close (31/12) 102 10 85 16 62 27 57 64 62 5 close (31/12) 102.10 85.16 62.27 57.64 62.5

15

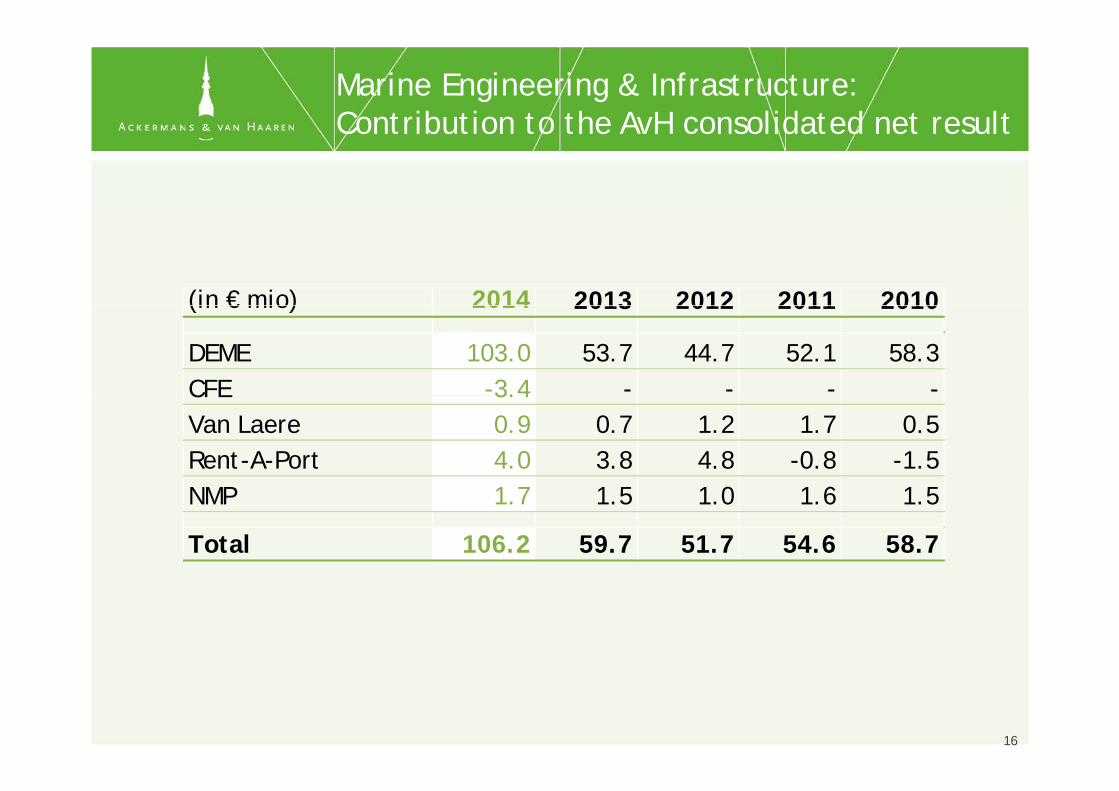

Marine Engineering & Infrastructure: Contribution to the AvH consolidated net resultContribution to the AvH consolidated net result

(in € mio) 2014 2013 2012 2011 2010(in € mio) 2014 2013 2012 2011 2010

DEME 103.0 53.7 44.7 52.1 58.3CFE -3.4 - - - -CFE 3.4Van Laere 0.9 0.7 1.2 1.7 0.5Rent-A-Port 4.0 3.8 4.8 -0.8 -1.5NMP 1.7 1.5 1.0 1.6 1.5

Total 106.2 59.7 51.7 54.6 58.7

16

Marine Engineering & Infrastructure

• One of the largest and most diversified dredging and marine DEME

CFE

One of the largest and most diversified dredging and marine engineering companies in the world

DEME

• An industrial group active in Contracting, Real Estate CFE

VAN LAERE • General contractor of large residential, office and civil

g p g,Development, Public-Private Partnership and Concessions

construction projects; focus on PPS projects and parkings• 2014: Increase of turnover to € 167 mio• Order book at € 176 mio

• Specialised in port development and logistics• 2014: Lower net result, as 2014 is transition year for Dinh Vu

(Vi t )

RENT-A-PORT

NMP • Operator of pipelines for chemicals2014: Results in line with expectations

(Vietnam)

• 2014: Results in line with expectations

17

Solutions for global challenges

1818

DEME: long term track record of long term shareholding and entrepreneurial growthshareholding and entrepreneurial growth

(in 000 euro) Turnover Equity

2.000.000

2.500.000

1.000.000

1.500.000

‐

500.000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 20141974 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 201497

ScaldisDBM Creation DEME

Holding G SCTOWCreation Dredging

International (AvH Tideway

DEC

(Building Materials)

Holding(Acquisition Decloedt)

GeoSea DEME Blue EnergyOceanflore

International (AvH + CFE dredging) Power@Sea

Tideway

AvH 39.5% AvH 48.5% AvH 50% AvH 60.4%

Consolidation Partnership

AvH 45%

Control

1919

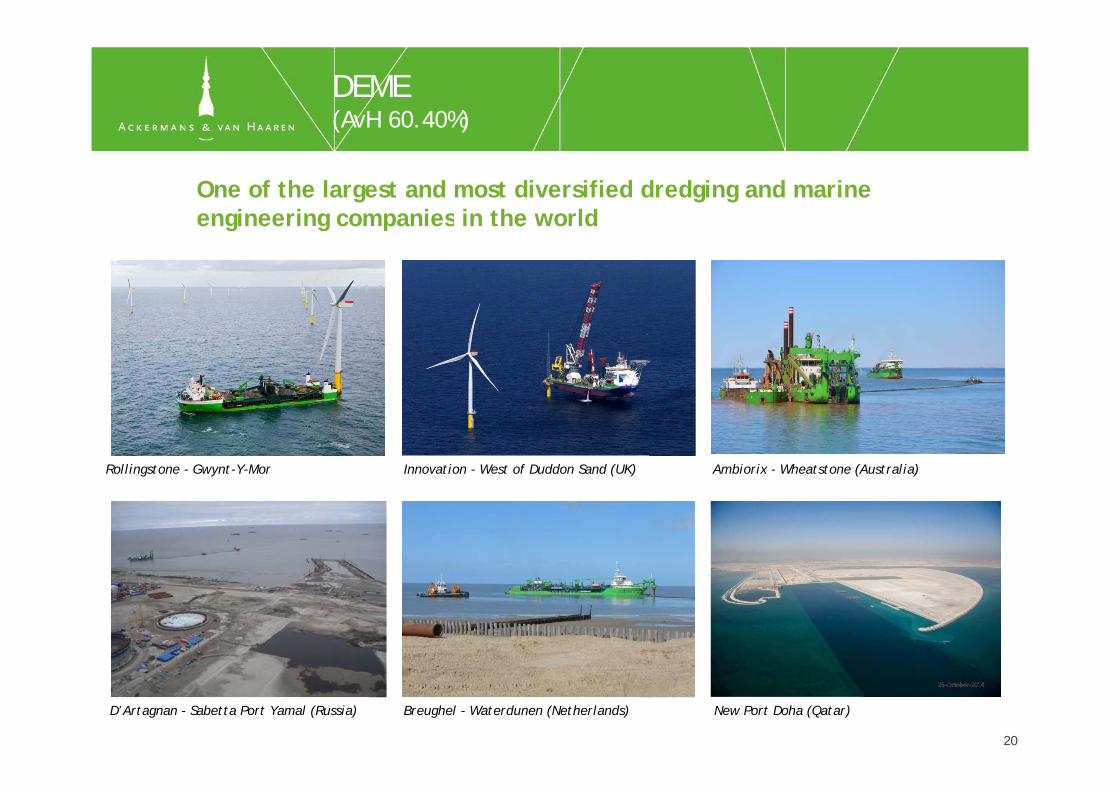

DEME(AvH 60.40%)

One of the largest and most diversified dredging and marine engineering companies in the world

(AvH 60.40%)

engineering companies in the world

Rollingstone - Gwynt-Y-Mor Innovation - West of Duddon Sand (UK) Ambiorix - Wheatstone (Australia)

20

Breughel - Waterdunen (Netherlands) New Port Doha (Qatar)D’Artagnan - Sabetta Port Yamal (Russia)

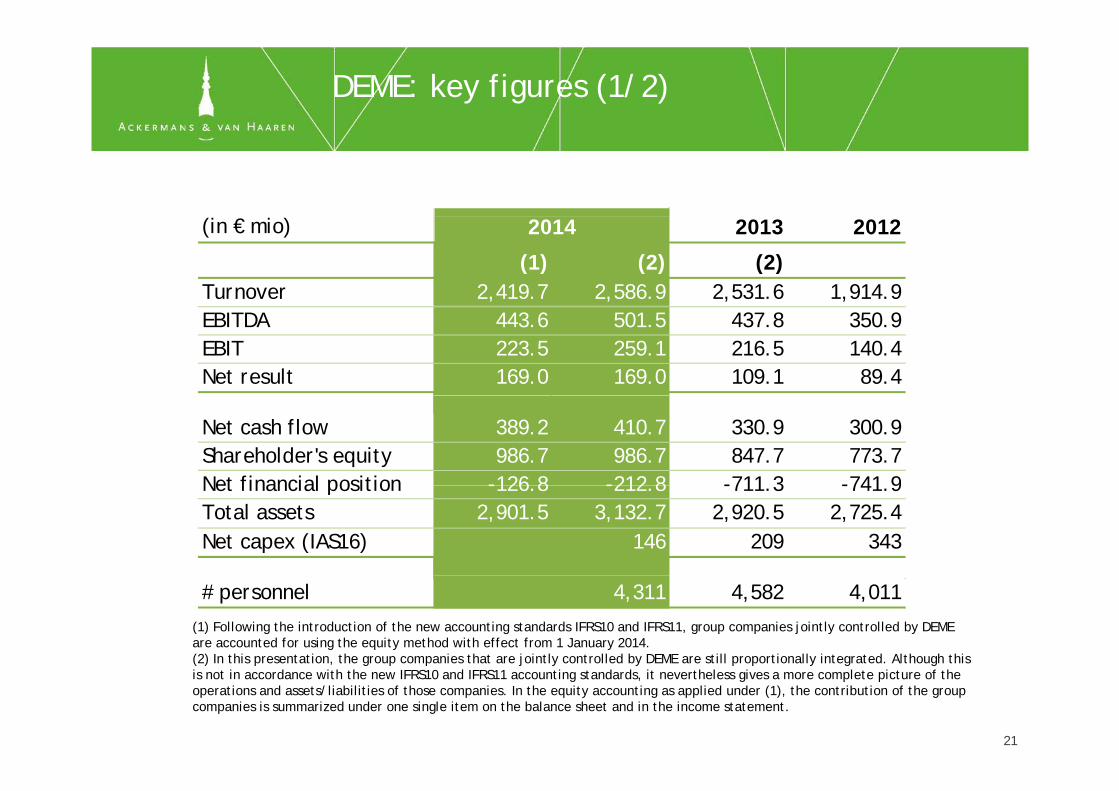

DEME: key figures (1/2)

(in € mio) 2013 2012

(1) (2) (2)Turnover 2,419.7 2,586.9 2,531.6 1,914.9

2014

EBITDA 443.6 501.5 437.8 350.9EBIT 223.5 259.1 216.5 140.4Net result 169.0 169.0 109.1 89.4

Net cash flow 389.2 410.7 330.9 300.9Shareholder's equity 986.7 986.7 847.7 773.7Net financial position -126 8 -212 8 -711 3 -741 9Net financial position -126.8 -212.8 -711.3 -741.9Total assets 2,901.5 3,132.7 2,920.5 2,725.4Net capex (IAS16) 146 209 343

# personnel 4,311 4,582 4,011

(1) Following the introduction of the new accounting standards IFRS10 and IFRS11, group companies jointly controlled by DEME are accounted for using the equity method with effect from 1 January 2014.(2) In this presentation, the group companies that are jointly controlled by DEME are still proportionally integrated. Although this ( ) p , g p p j y y p p y g gis not in accordance with the new IFRS10 and IFRS11 accounting standards, it nevertheless gives a more complete picture of the operations and assets/liabilities of those companies. In the equity accounting as applied under (1), the contribution of the group companies is summarized under one single item on the balance sheet and in the income statement.

21

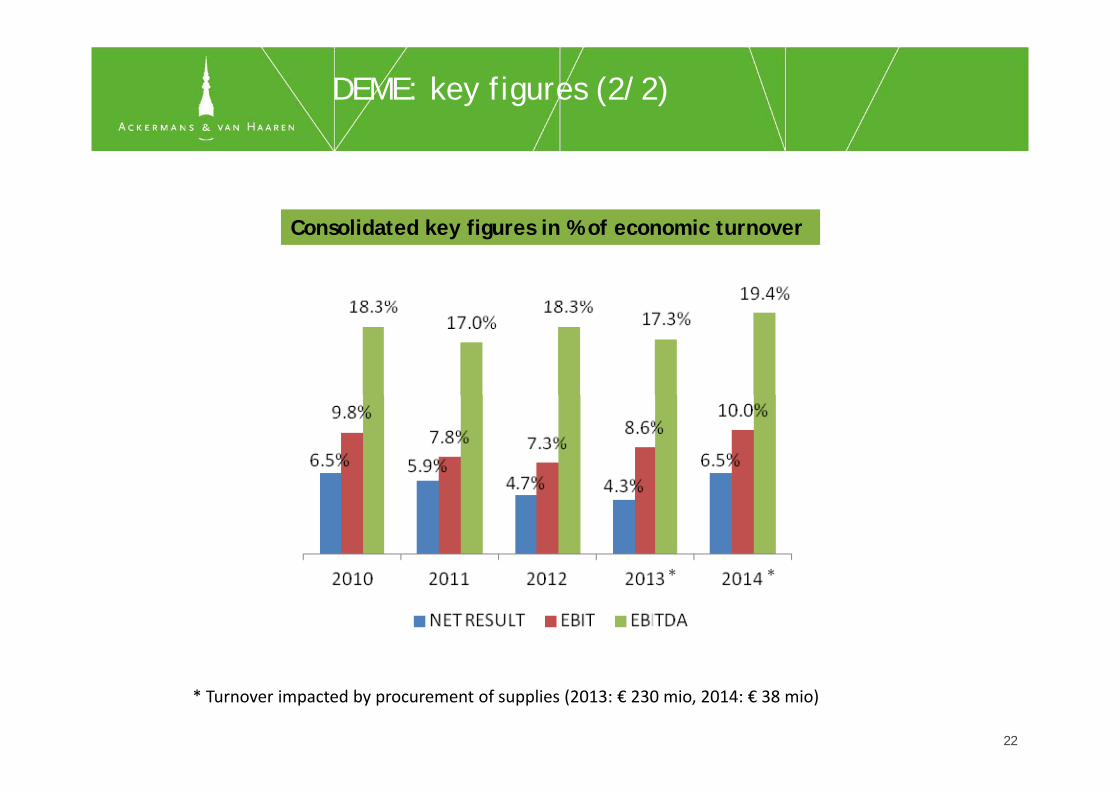

DEME: key figures (2/2)

Consolidated key figures in % of economic turnover

** ** *

* Turnover impacted by procurement of supplies (2013: € 230 mio, 2014: € 38 mio)

22

DEME: breakdown of economic turnover

Per region

2013 2014

Per activity

2013 2014

Per type of customer

2013 2014

23

DEME: order book (€ mio)(€ mio)

Other 33%

Middle East + IndiaAsia

Europe

7%14%

26%

O d b k 2014 i i d hi h l l € 2 420 i ( 3 049 i d f 2013)

Benelux20%

Order book 2014 maintained at a high level: € 2,420 mio (vs 3,049 mio end of 2013), with orders across different regions and activities• Construction of approach channel and harbour basis of service port for new LNG terminal

in Yamal (Russia)in Yamal (Russia)• Deepening and widening of Suez canal (Egypt): contract of € 421 mio (DEME 75%)• Offshore wind farms Gode Wind (2013) and Nordsee One (Germany)

E l 2015 i d f l l f € 1 600 i M i i • Early 2015, new contracts signed for a total value of € 1,600 mio. Most important one is Tuas project in Singapore: construction of 8.6 km quay wall, reclamation of 300 ha new land and dredging of fairways over period of 6 years

24

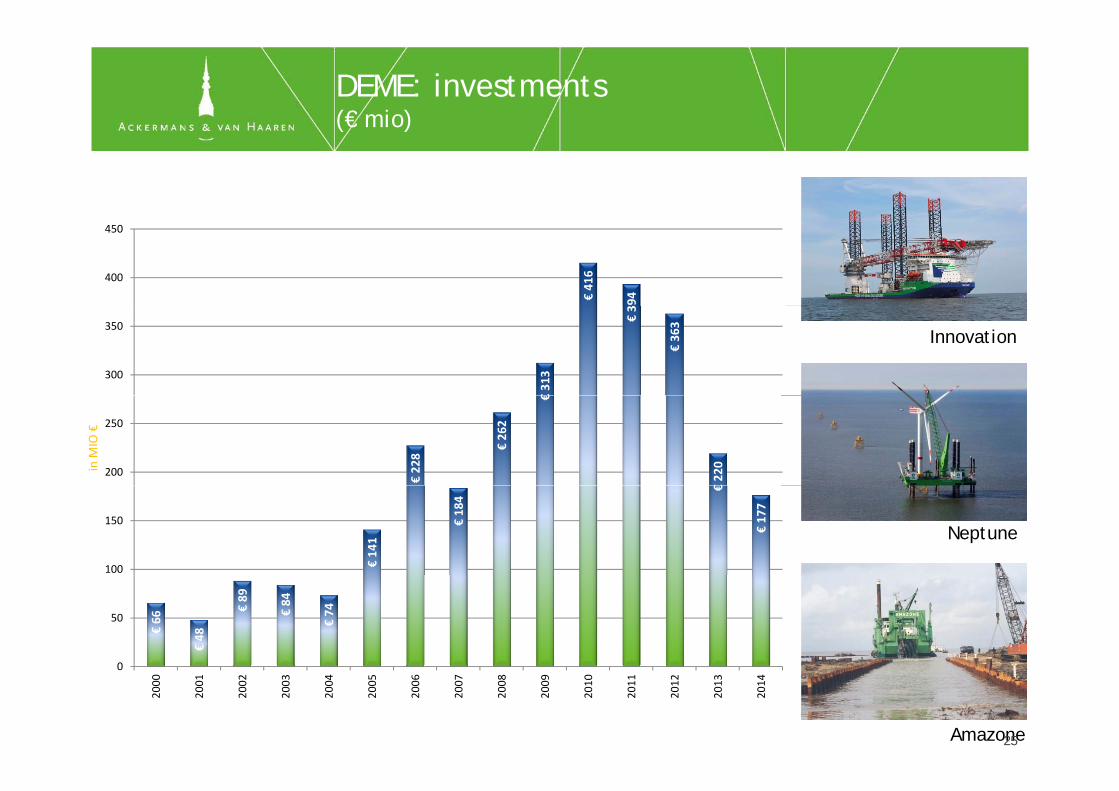

DEME: investments(€ mio)(€ mio)

€416

94

400

450

Innovation

€313

€3

€363

300

350

€228

€262

€

€220

200

250

in M

IO €

Neptune

€141

€184

€

€177

100

150

€66

€48

€89

€84

€74

0

50

Amazone25

0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

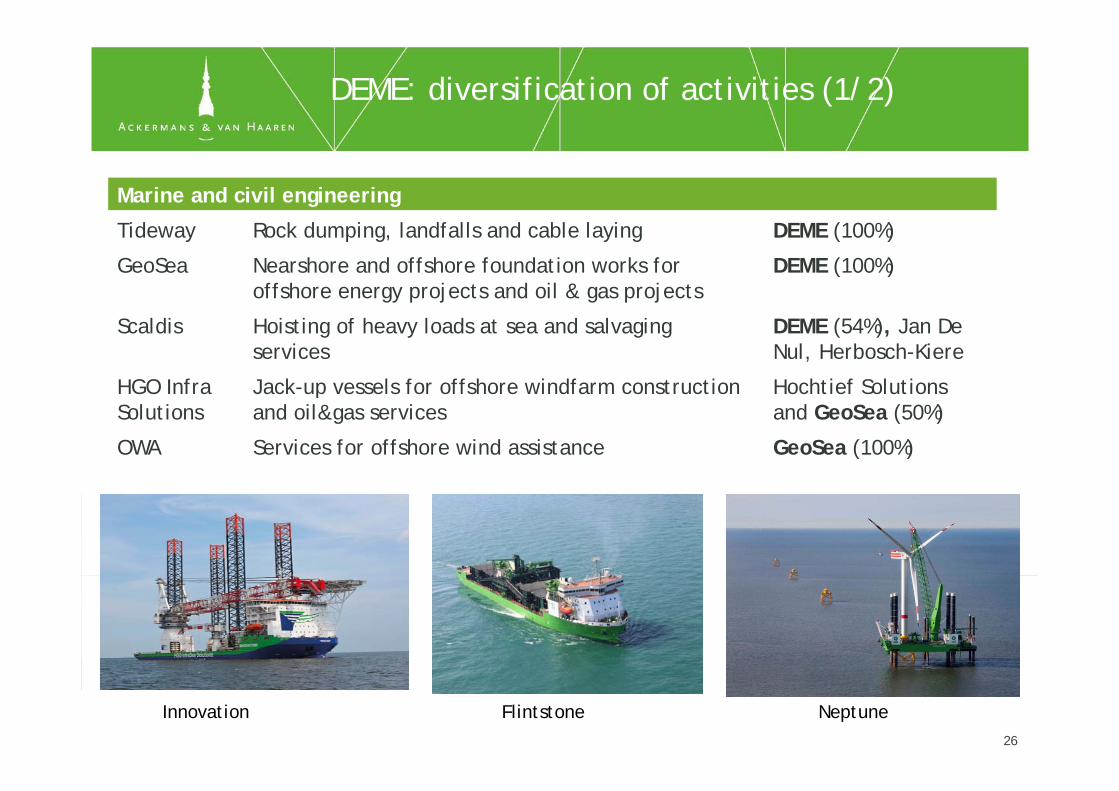

DEME: diversification of activities (1/2)

Marine and civil engineering

Tideway Rock dumping, landfalls and cable laying DEME (100%)

GeoSea Nearshore and offshore foundation works for offshore energy projects and oil & gas projects

DEME (100%)

Scaldis Hoisting of heavy loads at sea and salvaging services

DEME (54%), Jan De Nul, Herbosch-Kiere

HGO Infra Jack-up vessels for offshore windfarm construction Hochtief Solutions Solutions

pand oil&gas services and GeoSea (50%)

OWA Services for offshore wind assistance GeoSea (100%)

Innovation Flintstone Neptune26

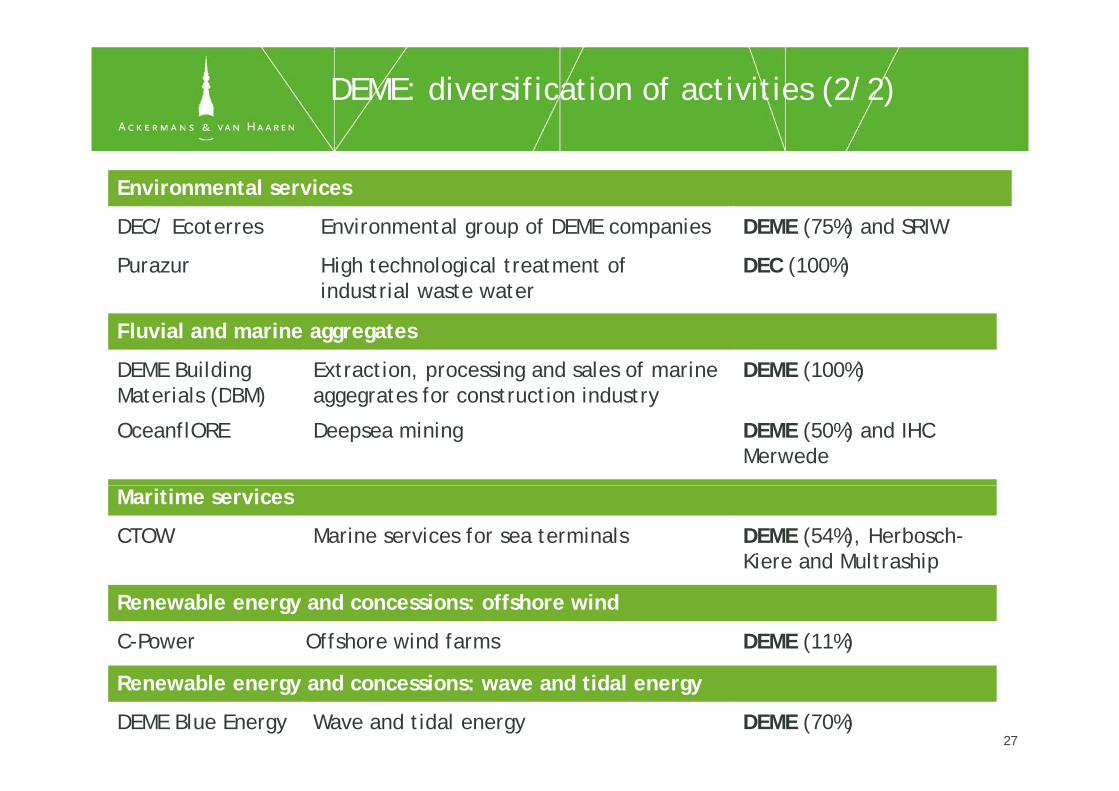

DEME: diversification of activities (2/2)

Environmental services

DEC/ Ecoterres Environmental group of DEME companies DEME (75%) and SRIW

Purazur High technological treatment of industrial waste water

DEC (100%)

Fluvial and marine aggregates

DEME Building Materials (DBM)

Extraction, processing and sales of marine aggegrates for construction industry

DEME (100%)Materials (DBM) aggegrates for construction industry

OceanflORE Deepsea mining DEME (50%) and IHC Merwede

Maritime services

CTOW Marine services for sea terminals DEME (54%), Herbosch-Kiere and Multraship

Renewable energy and concessions: offshore wind

C-Power Offshore wind farms DEME (11%)

Renewable energy and concessions: wave and tidal energy

DEME Blue Energy Wave and tidal energy DEME (70%)27

Vlaamse Baaien (Flanders Bays)

• A comprehensive plan (11 projects) that combines a long-term vision for sustainablecoastal protection with proposals for short-term actioncoastal protection with proposals for short term action

• Fosters an integrated, flexible development of the Belgian coast and Scheldt mouth

• Changes threats (climate change) into opportunities:• restoring attractiveness of an overbuilt coast• generating green and blue energy production• harmoniously expanding urbanisation tourism and harbour activitiesharmoniously expanding urbanisation, tourism and harbour activities

28

Energy storage atoll

29

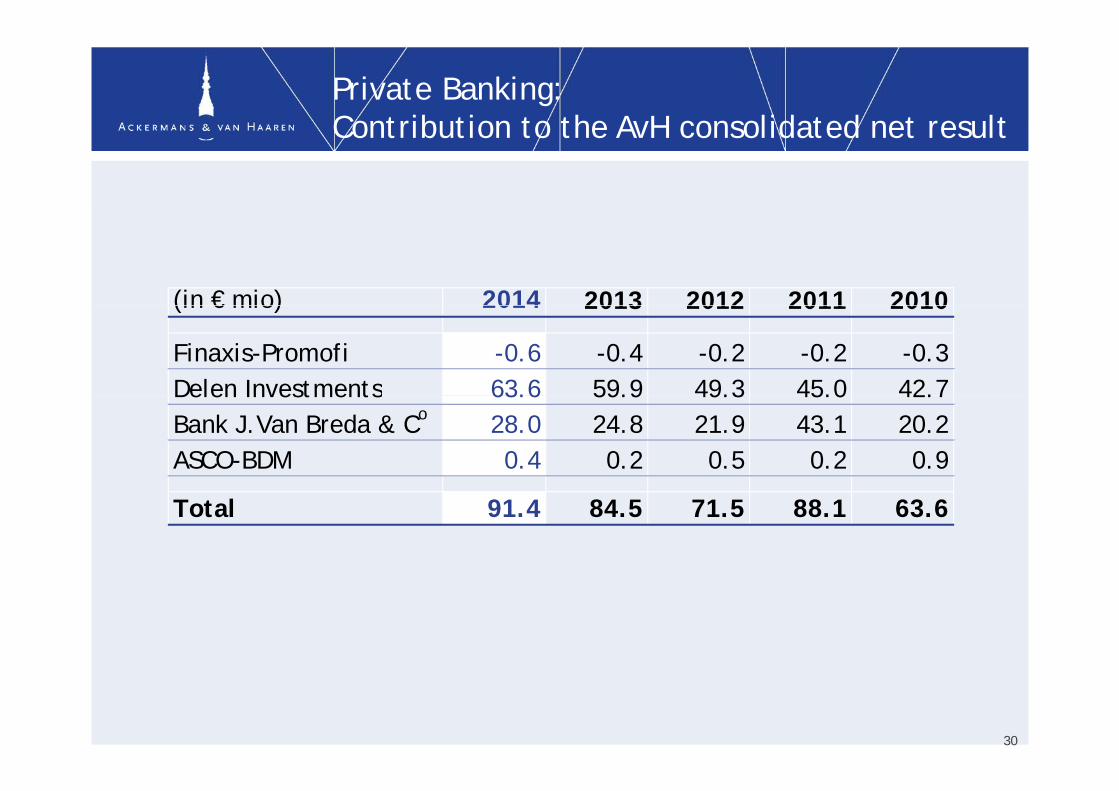

Private Banking: Contribution to the AvH consolidated net resultContribution to the AvH consolidated net result

(in € mio) 2014 2013 2012 2011 2010(in € mio) 2014 2013 2012 2011 2010

Finaxis-Promofi -0.6 -0.4 -0.2 -0.2 -0.3Delen Investments 63.6 59.9 49.3 45.0 42.7Delen Investments 63.6 59.9 49.3 45.0 42.7Bank J.Van Breda & Co 28.0 24.8 21.9 43.1 20.2ASCO-BDM 0.4 0.2 0.5 0.2 0.9

Total 91.4 84.5 71.5 88.1 63.6

30

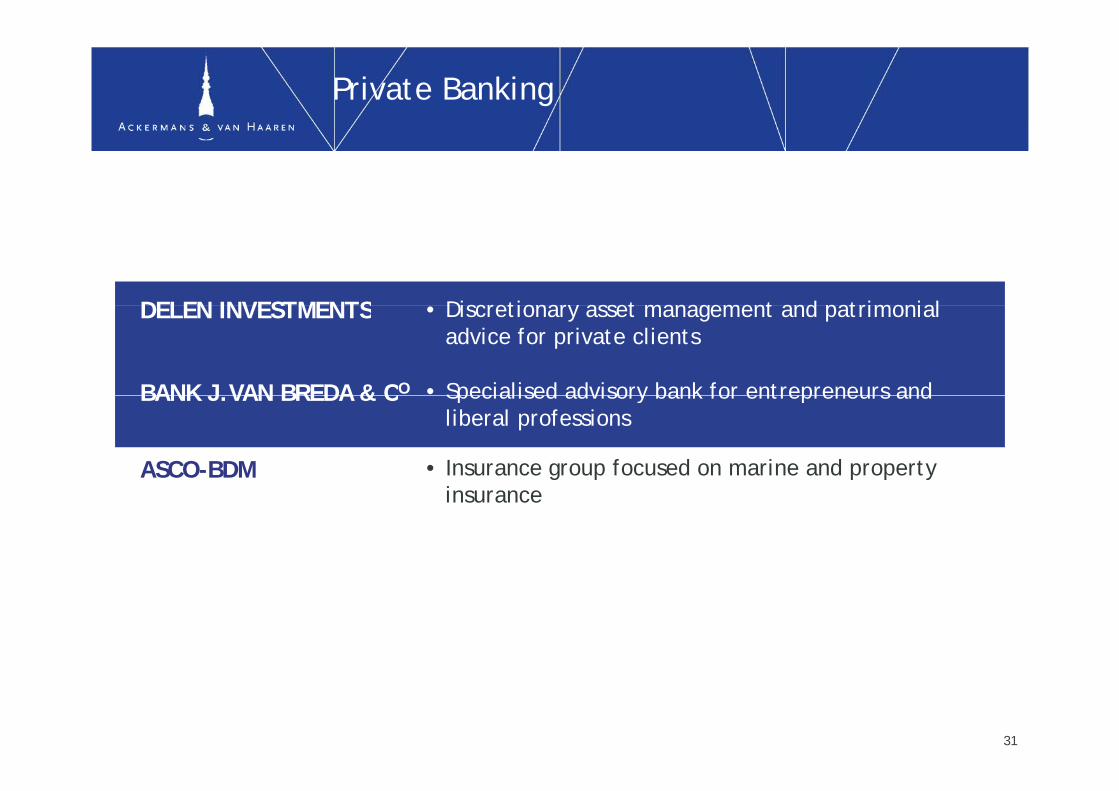

Private Banking

DELEN INVESTMENTS Discretionary asset management and patrimonial DELEN INVESTMENTS

• Specialised advisory bank for entrepreneurs and

• Discretionary asset management and patrimonial advice for private clients

BANK J VAN BREDA & CO Specialised advisory bank for entrepreneurs and liberal professions

BANK J.VAN BREDA & C

• Insurance group focused on marine and property ASCO-BDMinsurance

31

Delen Investments: funds under management(AvH 78.75%)(AvH 78.75%)

Private banking and wealth management. Focused on discretionary g g yasset management for private clients, in Belgium and UK

AuM CAGR 2005-2014:

JM Finn

17.9%

Capfi

1992

32

1992

Assets under management

(in € mio) 2014 2013 2012

Total assets under management

Delen Investments 32,866 29,536 25,855 Delen Private Bank 22,808 20,210 17,884 JM Finn & Co 10,058 9,326 7,971

Van Breda: bancassurance products 1,567 1,507 1,496Van Breda: AuM at Delen* 3,603 3,036 2,504Van Breda: client deposits 3,815 3,683 3,424(*) Already included in Delen Private Bank AuM

33

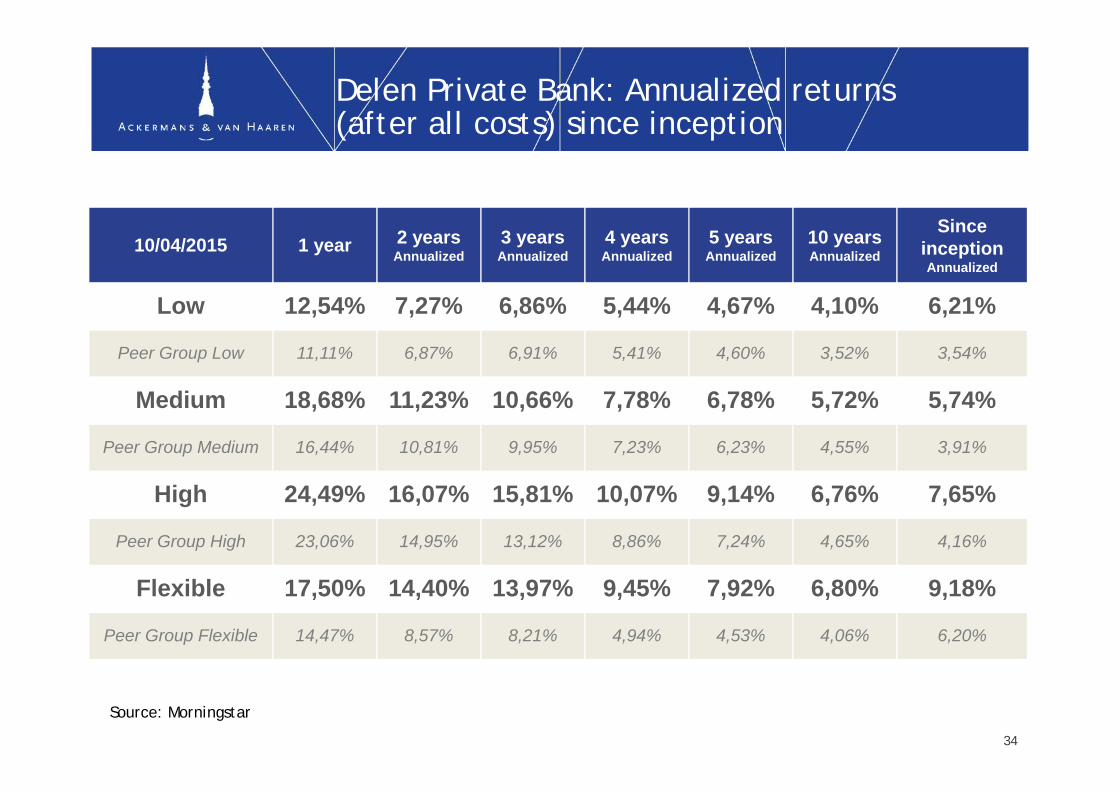

Delen Private Bank: Annualized returns (after all costs) since inception(after all costs) since inception

10/04/2015 1 year 2 years Annualized

3 years Annualized

4 years Annualized

5 years Annualized

10 years Annualized

Since inception Annualized

Low 12 54% 7 27% 6 86% 5 44% 4 67% 4 10% 6 21%Low 12,54% 7,27% 6,86% 5,44% 4,67% 4,10% 6,21%

Peer Group Low 11,11% 6,87% 6,91% 5,41% 4,60% 3,52% 3,54%

Medium 18 68% 11 23% 10 66% 7 78% 6 78% 5 72% 5 74%Medium 18,68% 11,23% 10,66% 7,78% 6,78% 5,72% 5,74%

Peer Group Medium 16,44% 10,81% 9,95% 7,23% 6,23% 4,55% 3,91%

Hi h 24 49% 16 07% 15 81% 10 07% 9 14% 6 76% 7 65%High 24,49% 16,07% 15,81% 10,07% 9,14% 6,76% 7,65%

Peer Group High 23,06% 14,95% 13,12% 8,86% 7,24% 4,65% 4,16%

Flexible 17,50% 14,40% 13,97% 9,45% 7,92% 6,80% 9,18%

Peer Group Flexible 14,47% 8,57% 8,21% 4,94% 4,53% 4,06% 6,20%

Source: Morningstar

3434

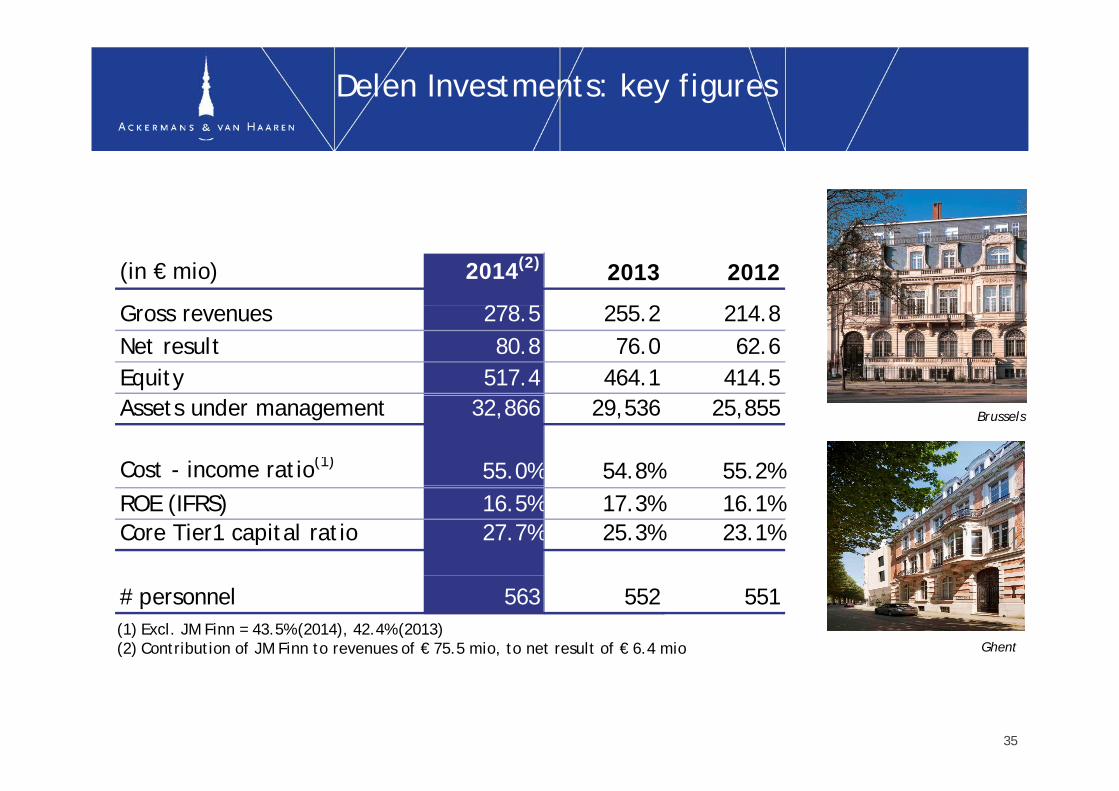

Delen Investments: key figures

(in € mio) 2014(2) 2013 2012

G 278 5 255 2 214 8Gross revenues 278.5 255.2 214.8Net result 80.8 76.0 62.6Equity 517.4 464.1 414.5Assets under management 32,866 29,536 25,855

Cost - income ratio(1) 55.0% 54.8% 55.2%

Brussels

ROE (IFRS) 16.5% 17.3% 16.1%Core Tier1 capital ratio 27.7% 25.3% 23.1%

# personnel 563 552 551(1) Excl. JM Finn = 43.5% (2014), 42.4% (2013)(2) Contribution of JM Finn to revenues of € 75.5 mio, to net result of € 6.4 mio Ghent

35

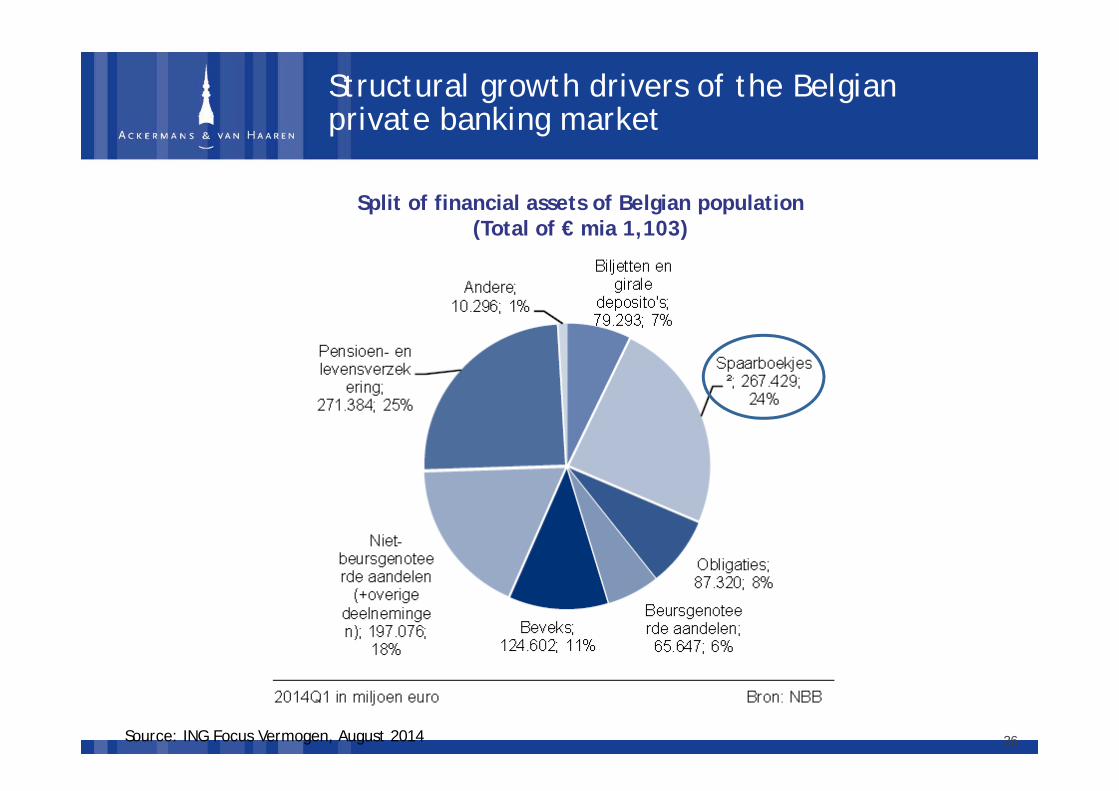

Structural growth drivers of the Belgian private banking marketprivate banking market

Split of financial assets of Belgian population (Total of € mia 1,103)

Source: ING Focus Vermogen, August 2014 36

Bank J.Van Breda & C°: client assets(AvH 78 75%)(AvH 78.75%)

Relationship bank focused on private as well as professional needs p p pfor entrepreneurs and liberal professions

Total deposits & fundsCAGR 2005-2014: 12.2%

37

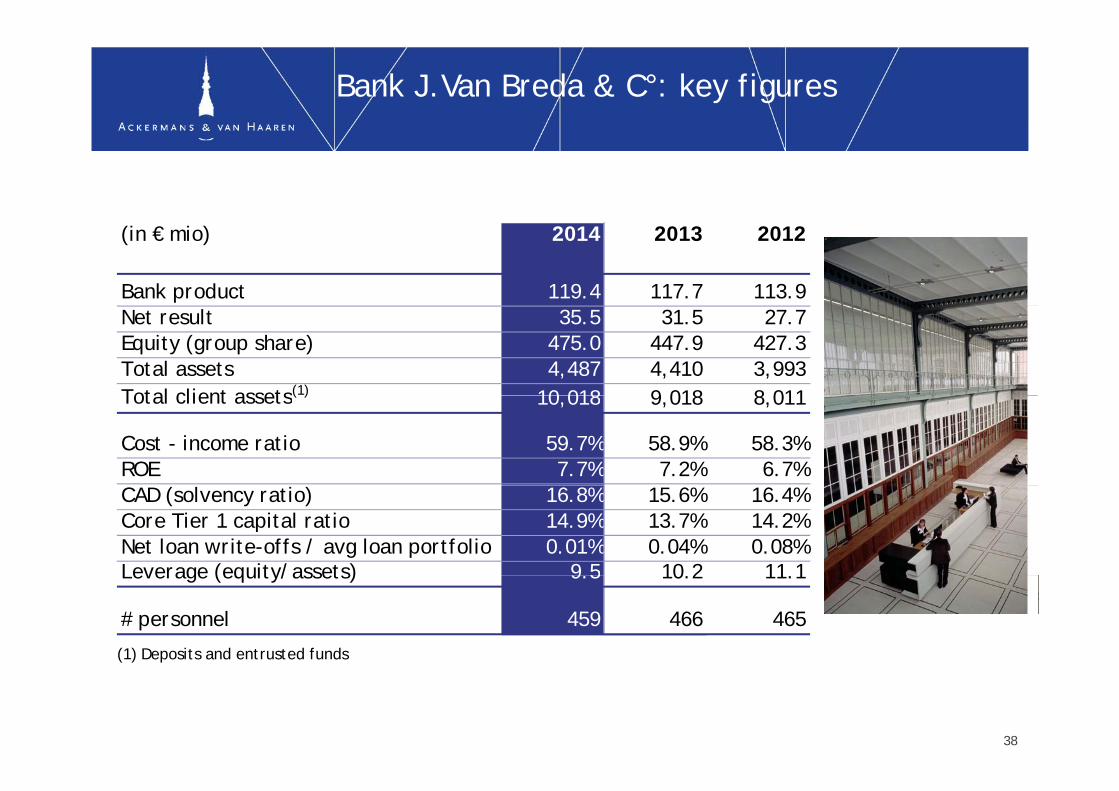

Bank J.Van Breda & C°: key figures

(in € mio) 2014 2013 2012

Bank product 119.4 117.7 113.9Net result 35.5 31.5 27.7Equity (group share) 475.0 447.9 427.3Total assets 4,487 4,410 3,993Total client assets(1) 10 018 9 018 8 011Total client assets( ) 10,018 9,018 8,011

Cost - income ratio 59.7% 58.9% 58.3%ROE 7.7% 7.2% 6.7%CAD (solvency ratio) 16.8% 15.6% 16.4%Core Tier 1 capital ratio 14.9% 13.7% 14.2%Net loan write-offs / avg loan portfolio 0.01% 0.04% 0.08%Leverage (equity/assets) 9 5 10 2 11 1Leverage (equity/assets) 9.5 10.2 11.1

# personnel 459 466 465

(1) Deposits and entrusted funds

38

Real Estate, Leisure & Senior Care: Contribution to the AvH consolidated net resultContribution to the AvH consolidated net result

(in € mio) 2014 2013 2012 2011 2010(in € mio) 2014 2013 2012 2011 2010

Leasinvest Real Estate 10.3 8.7 6.5 4.2 5.0Extensa 3.4 4.5 -5.3 -2.8 1.2Extensa 3.4 4.5 5.3 2.8 1.2Groupe Financière Duval 0.5 2.0 1.8 2.6 1.4Anima Care 0.5 0.6 0.6 0.4 0.0Cobelguard 0.1 1.0

Total 14.7 15.8 3.6 4.5 8.6

39

Real Estate, Leisure & Senior Care

LEASINVEST REAL ESTATE • Public regulated real estate comany for retail, offices and logistics in Luxembourg Belgium and Switzerland

EXTENSA • Real estate and land development in Belgium and Luxembourg

and logistics in Luxembourg, Belgium and Switzerland

FINANCIERE DUVAL • Real estate group with activities in real estate promotion, tourism (Odalys: 118,000 beds, 350 sites) and golf (NGF: 47 golf sites of which 20 in Paris)

• 2014 negatively impacted by lower real estate activities • 2014 negatively impacted by lower real estate activities and impact of VAT increase on tourism; Disposal of parking activities Park’A

• 2015: Sale of Residalya to AvH. AvH will swap first part 2015: Sale of Residalya to AvH. AvH will swap first part (20.57%) of stake in Fin. Duval with stake of 37.2% in Patrimoine & Santé (RE assets of Residalya)

ANIMA CARE • Health & senior care sector in Belgiumg• 2014: Increase of turnover driven by portfolio

expansion, start up costs linked to opening of new buildings

• Total portfolio of more than 1,300 beds and service flats (965 beds and 120 service flats in operation)

40RESIDALYA • Senior care sector in France

Leasinvest Real Estate(AvH 30%)(AvH 30%)

Public regulated real estate company for retail, offices and logistics in Luxembourg Belgium and Switzerlandin Luxembourg, Belgium and Switzerland

Hornbach (Luxembourg) Knauf Pommerloch (Luxembourg)Avenue Monterey (Luxembourg)

41

Yverdon-les-Bains (Switzerland) Pré Neuf Villeneuve (Switzerland) Littoral Park Etoy (Switzerland)

Leasinvest Real Estate: key figures

Real estate portfolio

(in € mio) 2014 2013 2012Operational result 38.6 34.2 29.0Net result 32 6 26 9 20 5

Retail

Offices

Logistics/semi-industral

portfolio

Net result 32.6 26.9 20.5Net equity 336.4 335.3 256.0

Portfolio real estate (fair value) 756.3 718.2 617.8 45%

20%

g

o t ol o eal estate ( a value) 56.3 8. 6 .8Rental yield (%) 7.23 7.31 7.30Occupancy rate (%) 96.2 96.9 94.9Net debt ratio (%)(1) 54.3 53.5 56.2

35%

( )

Per share (€) Net asset value 68.10 67.90 63.80

5%

Luxembourg Belgium

Switzerland

(1) Total net debt: € 406 mio (2013), € 407 mio (1H14)

Stock price - closing 91.61 73.60 67.10 High/Low 93.90/73.10 82.45/65.10 69.58/61.50

Dividend 4.55 4.50 4.40

59%36%

42

Extensa Group(AvH 100%)(AvH 100%)

Real estate developer with focus on residential and mixed projects in Belgium and LuxembourgBelgium and Luxembourg

Tour&Taxis (Brussel) Brussels Environment (Tour&Taxis) De Meander (Tour&Taxis) (artist impression)

43

Cloche d’Or (Luxembourg) (artist impression) Cloche d’Or (Luxembourg) (artist impression) Trnava (Slowakia)

Anima Care(AvH 100%)(AvH 100%)

Anima Care focuses on high quality senior care residences in Belgium ( l it ti d l t t )(exploitation and real estate)

(in € mio) 2014 2013 2012 2011 2010Turnover 37 9 27 4 20 5 15 4 8 8 Azur Soins et SantéTurnover 37.9 27.4 20.5 15.4 8.8EBITDA 5.4 3.4 2.4 2.1 1.2Net result 0.5 0.6 0.6 0.4 0.0

Shareholder's equity 35.7 32.4 21.2 12.0 9.9Net financial position -60.2 -40.8 -15.2 -13.7 -8.4

Zonnesteen (Zemst)

Highlights 2014• Increase of turnover driven by portfolio expansion with new built residences: Zemst (93

beds, 24 service flats) and Haut-Ittre (127 beds, 36 service flats)

Zonnesteen (Zemst)

beds, 24 service flats) and Haut Ittre (127 beds, 36 service flats) • Net result impacted by startup losses from opening of new residences• Total portfolio of more than 1,300 beds and service flats (of which 965 beds and 120

service flats in operation), spread over 10 senior care residencesA ij id i K l (143 b d 63 i fl 25 l i d • Aquamarijn residence in Kasterlee (143 beds, 63 service flats, 25 places in day care centre) opening spring 2015

44

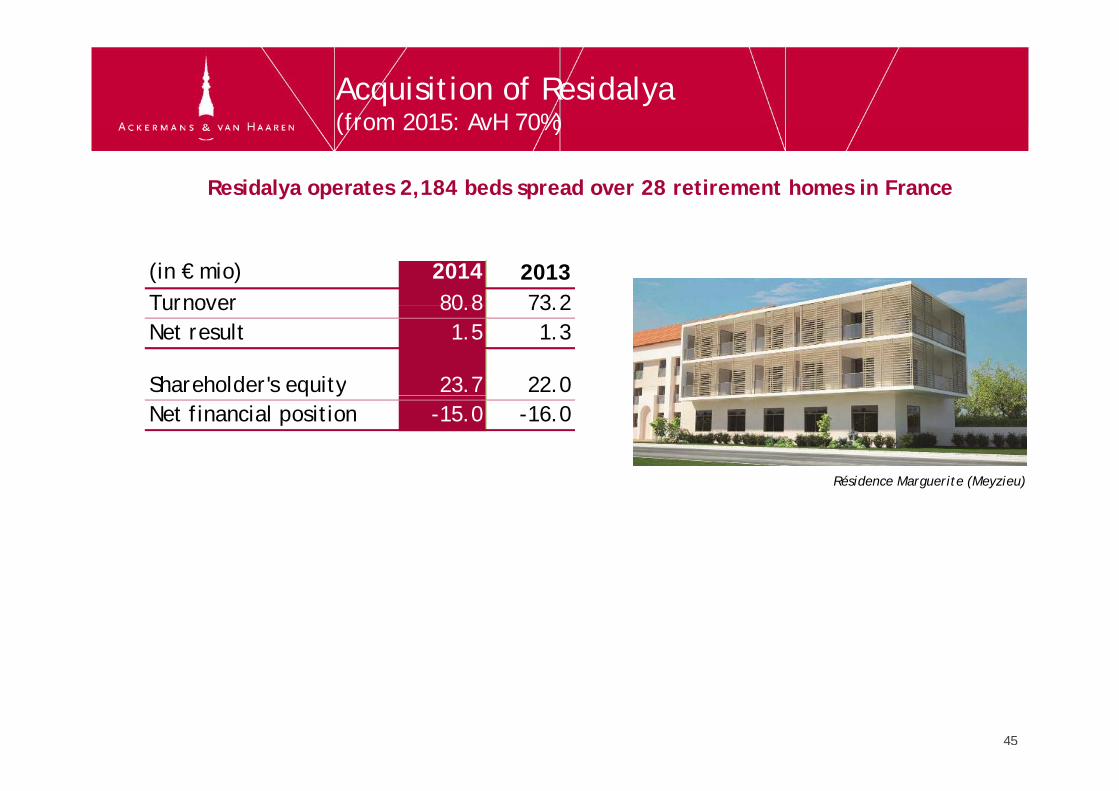

Acquisition of Residalya(from 2015: AvH 70%)(from 2015: AvH 70%)

Residalya operates 2,184 beds spread over 28 retirement homes in France

(in € mio) 2014 2013Turnover 80 8 73 2Turnover 80.8 73.2Net result 1.5 1.3

Shareholder's equity 23.7 22.0q yNet financial position -15.0 -16.0

Résidence Marguerite (Meyzieu)Résidence Marguerite (Meyzieu)

4545

From real estate leasing over real estate development to real estate servicesdevelopment to real estate services

Extensa

it140

160 (€ mio)

equity

100

120

140

40

60

80

‐

20

40

AvH 100% Acquisition -Creation of LRE AvH 60% AvH 100% Extensa(real estate development)

(investment trust)-Acquisition Brixton(real estate management)

AvH 60%(equipment & real estate leasing)

Diversification into ‘Real estate services’:

Groupe Duval (41%) France (real estate exploitation & services)

Anima Care (100%)Senior care facilities & services

46

Residalya (70%)Senior care in France

46

Energy & Resources: Contribution to the AvH consolidated net resultContribution to the AvH consolidated net result

(in € mio) 2014 2013 2012 2011 2010(in € mio) 2014 2013 2012 2011 2010

Sipef 11.4 11.2 14.1 16.9 14.3Sagar Cements 6.0 -0.4 0.3 1.3 0.0Sagar Cements 6.0 0.4 0.3 1.3 0.0Telemond 1.8 3.0 1.0 -0.1 0.9Other 0.3 -5.1 1.0 0.9 1.3

Total 19.5 8.7 16.4 19.0 16.5

47

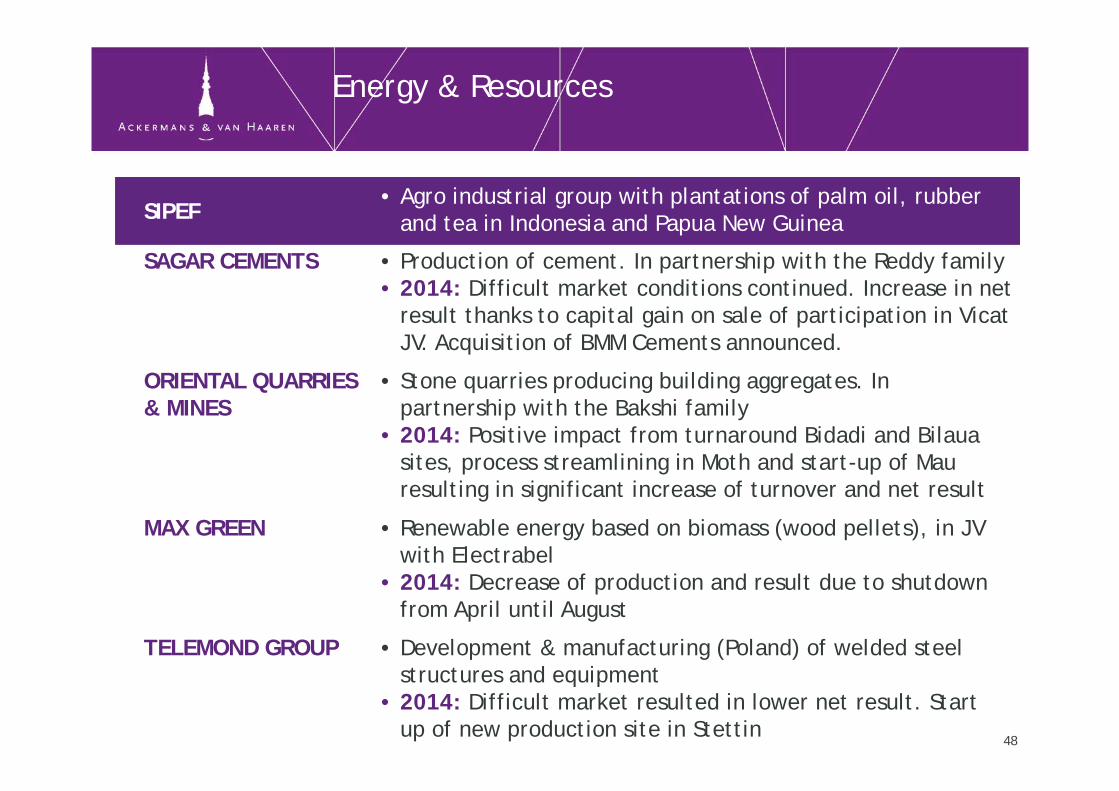

Energy & Resources

SIPEF• Agro industrial group with plantations of palm oil, rubber

d t i I d i d P N G i SIPEF and tea in Indonesia and Papua New Guinea

• Production of cement. In partnership with the Reddy family• 2014: Difficult market conditions continued. Increase in net

SAGAR CEMENTS

result thanks to capital gain on sale of participation in Vicat JV. Acquisition of BMM Cements announced.

ORIENTAL QUARRIES • Stone quarries producing building aggregates. In & MINES partnership with the Bakshi family

• 2014: Positive impact from turnaround Bidadi and Bilaua sites, process streamlining in Moth and start-up of Mau resulting in significant increase of turnover and net resultresulting in significant increase of turnover and net result

MAX GREEN • Renewable energy based on biomass (wood pellets), in JV with Electrabel2014 D f d ti d lt d t h td • 2014: Decrease of production and result due to shutdown from April until August

• Development & manufacturing (Poland) of welded steel TELEMOND GROUPstructures and equipment

• 2014: Difficult market resulted in lower net result. Start up of new production site in Stettin

48

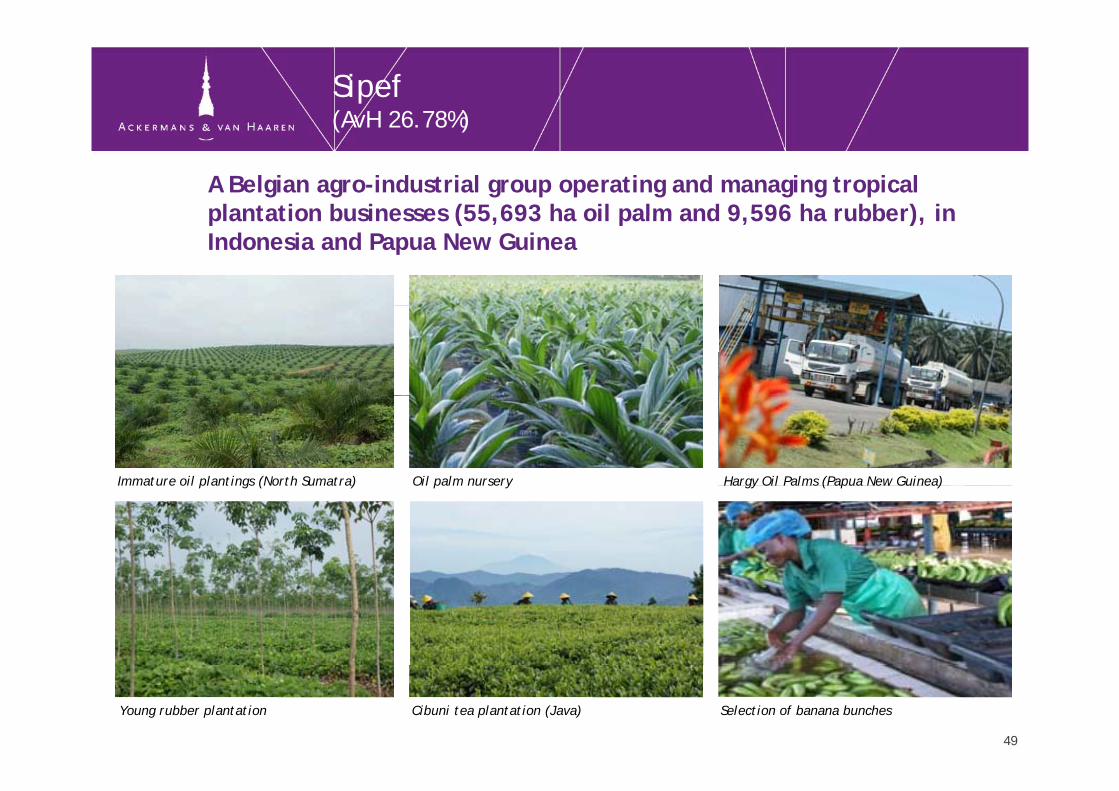

Sipef(AvH 26.78%)(AvH 26.78%)

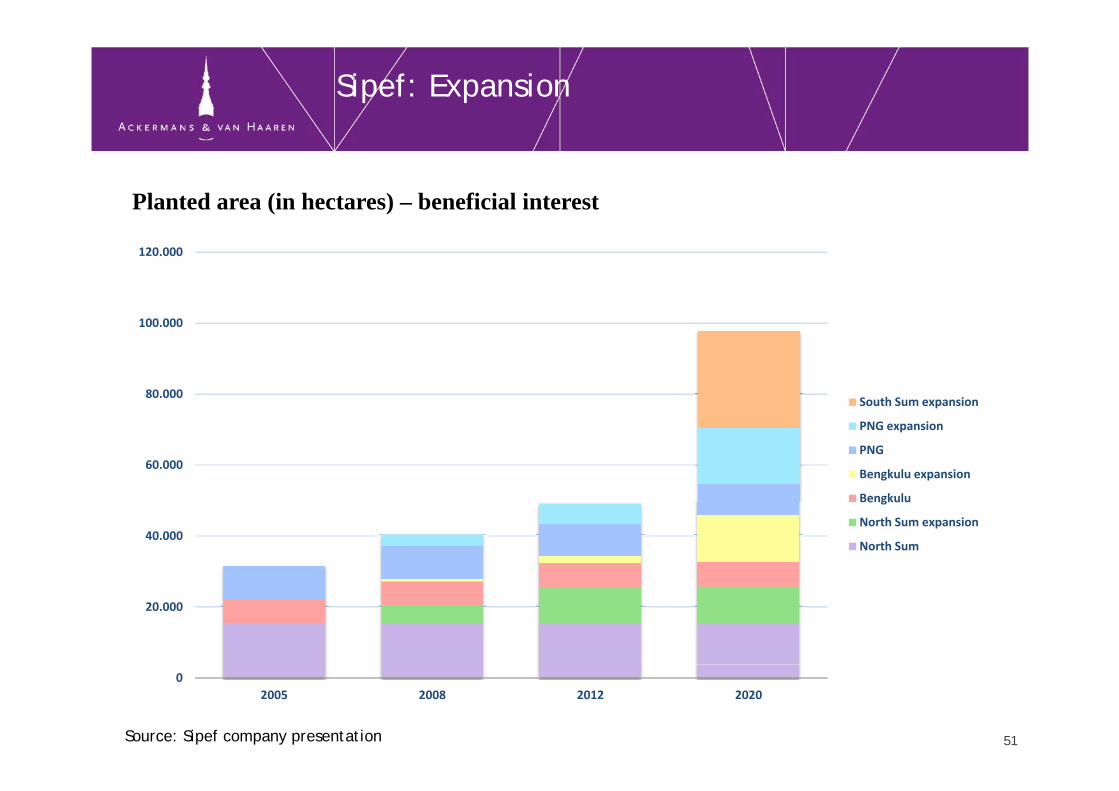

A Belgian agro-industrial group operating and managing tropical plantation businesses (55 693 ha oil palm and 9 596 ha rubber) in plantation businesses (55,693 ha oil palm and 9,596 ha rubber), in Indonesia and Papua New Guinea

Immature oil plantings (North Sumatra) Oil palm nursery Hargy Oil Palms (Papua New Guinea)Immature oil plantings (North Sumatra) Oil palm nursery Hargy Oil Palms (Papua New Guinea)

49

Selection of banana bunchesYoung rubber plantation Cibuni tea plantation (Java)

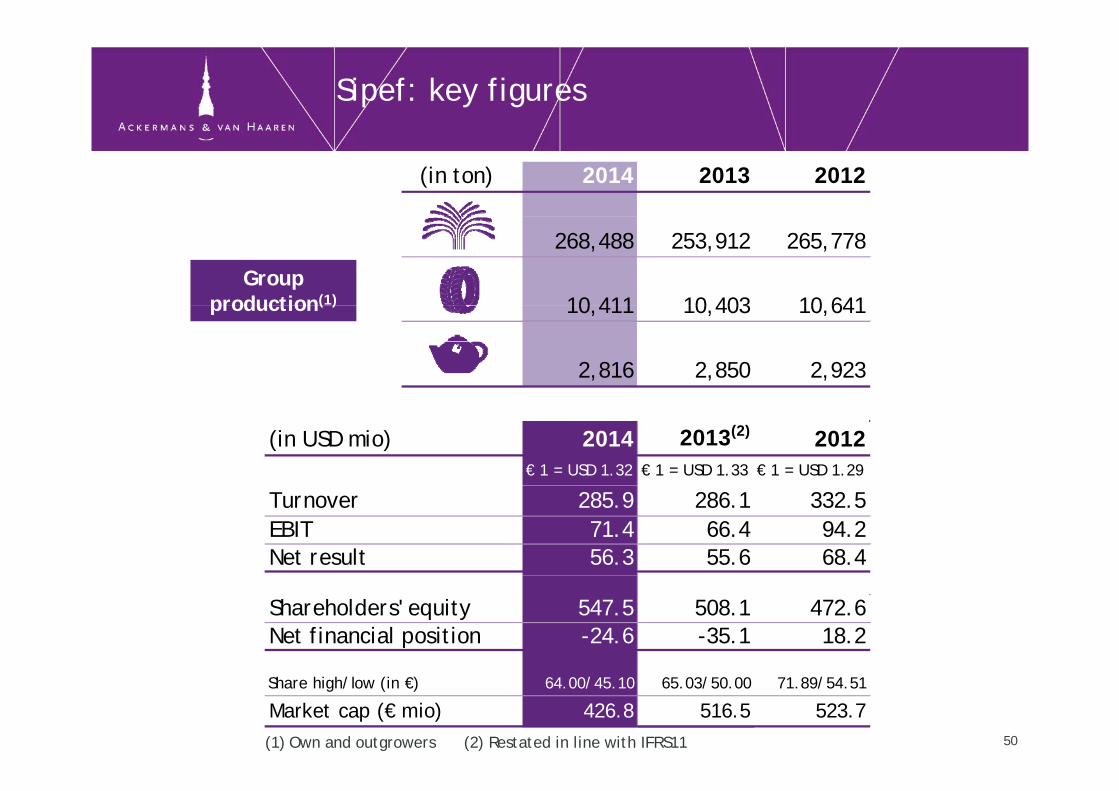

Sipef: key figures

(in ton) 2014 2013 2012

268,488 253,912 265,778

10 411 10 403 10 641Group

production(1) 10,411 10,403 10,641

2,816 2,850 2,923

production( )

(in USD mio) 2014 2013(2) 2012€ 1 = USD 1.32 € 1 = USD 1.33 € 1 = USD 1.29

Turnover 285.9 286.1 332.5EBIT 71.4 66.4 94.2Net result 56.3 55.6 68.4

Shareholders' equity 547.5 508.1 472.6Net financial position -24.6 -35.1 18.2

(1) Own and outgrowers

Share high/low (in €) 64.00/45.10 65.03/50.00 71.89/54.51

Market cap (€ mio) 426.8 516.5 523.750(2) Restated in line with IFRS11

Sipef: Expansion

Planted area (in hectares) – beneficial interest

120.000

80 000

100.000

60.000

80.000South Sum expansion

PNG expansion

PNG

Bengkulu expansion

40.000

Bengkulu

North Sum expansion

North Sum

20.000

02005 2008 2012 2020

Source: Sipef company presentation 51

5252

Development Capital: Contribution to the AvH consolidated net resultContribution to the AvH consolidated net result

(in € mio) 2014 2013 2012 2011 2010

Sofinim -2.9 -2.8 -1.3 -0.8 -0.5Contribution participations Sofinim 3.0 -6.3 4.3 6.3 10.6C ib i i i i GIB 6 8 2 5 2 9 3 1 3 2Contribution participations GIB -6.8 2.5 2.9 3.1 3.2

Development capital -6.7 -6.6 5.9 8.6 13.3

Capital gains/ impairments -15.4 29.5 22.7 -0.9 -0.3

Total (including capital gains) -22.1 22.9 28.6 7.7 13.0

53

Development Capital

Atenor: Brasseries de Neudorf (Luxembourg) Egemin: Handling Automation Corelio: Mediahuis

HertelDistriplus: Planet Parfum (Antwerp) Euro Media Group

54Turbo’s Hoet Groep Manuchar Trasys

Development Capital: adjusted net asset valueasset value

(in € mio) 2014 2013 2012 2011 2010

Sofinim 492.1 493.2 466.4 437.3 437.1

Unrealised capital gain Atenor 10.8 8.2 6.2 1.5 7.3p gShare price Atenor (in €) 40.00 34.25 32.05 24.21 33.54

Market value Groupe Flo / Trasys 5.8 10.0 8.4 12.9 24.0Sh i G Fl (i €) 2 50 3 00 3 00 3 56 4 89Share price Groupe Flo (in €) 2.50 3.00 3.00 3.56 4.89

Total Development Capital 508.7 511.4 481.0 451.7 468.5

55

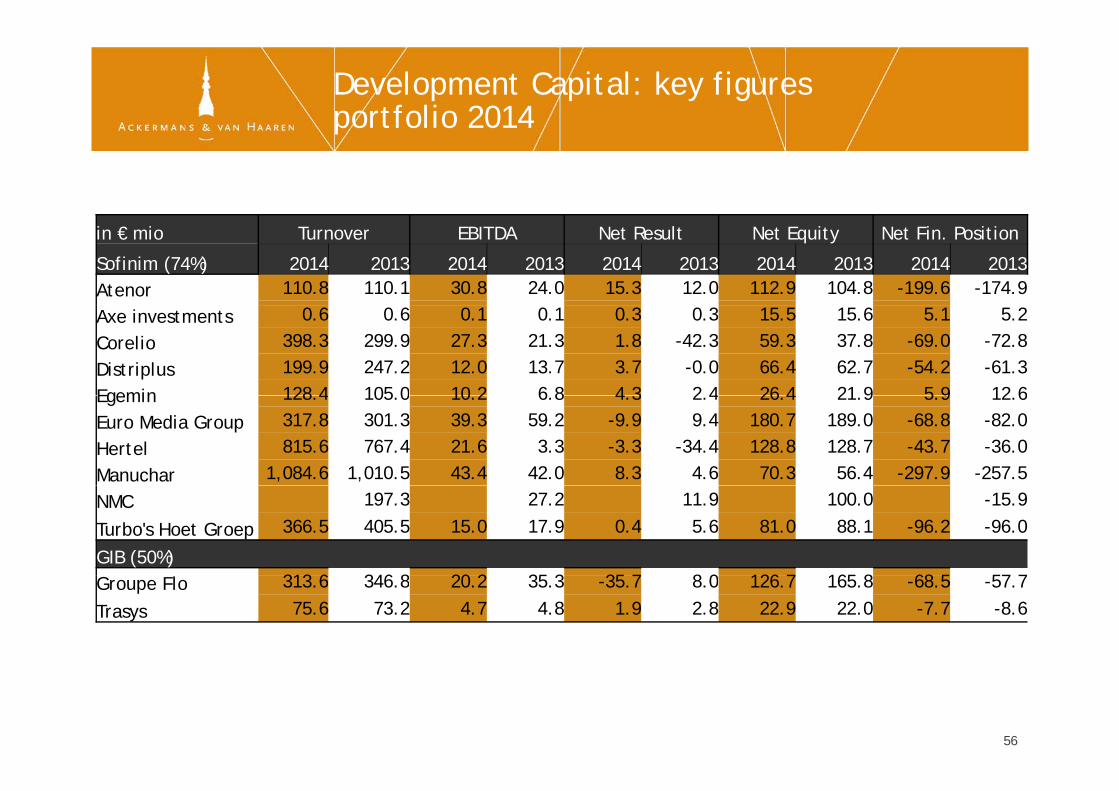

Development Capital: key figures portfolio 2014portfolio 2014

in € mio Turnover EBITDA Net Result Net Equity Net Fin. Position

Sofinim (74%) 2014 2013 2014 2013 2014 2013 2014 2013 2014 2013Atenor 110.8 110.1 30.8 24.0 15.3 12.0 112.9 104.8 -199.6 -174.9

Axe investments 0.6 0.6 0.1 0.1 0.3 0.3 15.5 15.6 5.1 5.2

Corelio 398.3 299.9 27.3 21.3 1.8 -42.3 59.3 37.8 -69.0 -72.8

Distriplus 199.9 247.2 12.0 13.7 3.7 -0.0 66.4 62.7 -54.2 -61.3

Egemin 128 4 105 0 10 2 6 8 4 3 2 4 26 4 21 9 5 9 12 6Egemin 128.4 105.0 10.2 6.8 4.3 2.4 26.4 21.9 5.9 12.6

Euro Media Group 317.8 301.3 39.3 59.2 -9.9 9.4 180.7 189.0 -68.8 -82.0

Hertel 815.6 767.4 21.6 3.3 -3.3 -34.4 128.8 128.7 -43.7 -36.0

Manuchar 1,084.6 1,010.5 43.4 42.0 8.3 4.6 70.3 56.4 -297.9 -257.5

NMC 197.3 27.2 11.9 100.0 -15.9

Turbo's Hoet Groep 366.5 405.5 15.0 17.9 0.4 5.6 81.0 88.1 -96.2 -96.0

GIB (50%)313 6 346 8 20 2 35 3 35 7 8 0 126 7 165 8 68 5 57 7Groupe Flo 313.6 346.8 20.2 35.3 -35.7 8.0 126.7 165.8 -68.5 -57.7

Trasys 75.6 73.2 4.7 4.8 1.9 2.8 22.9 22.0 -7.7 -8.6

56

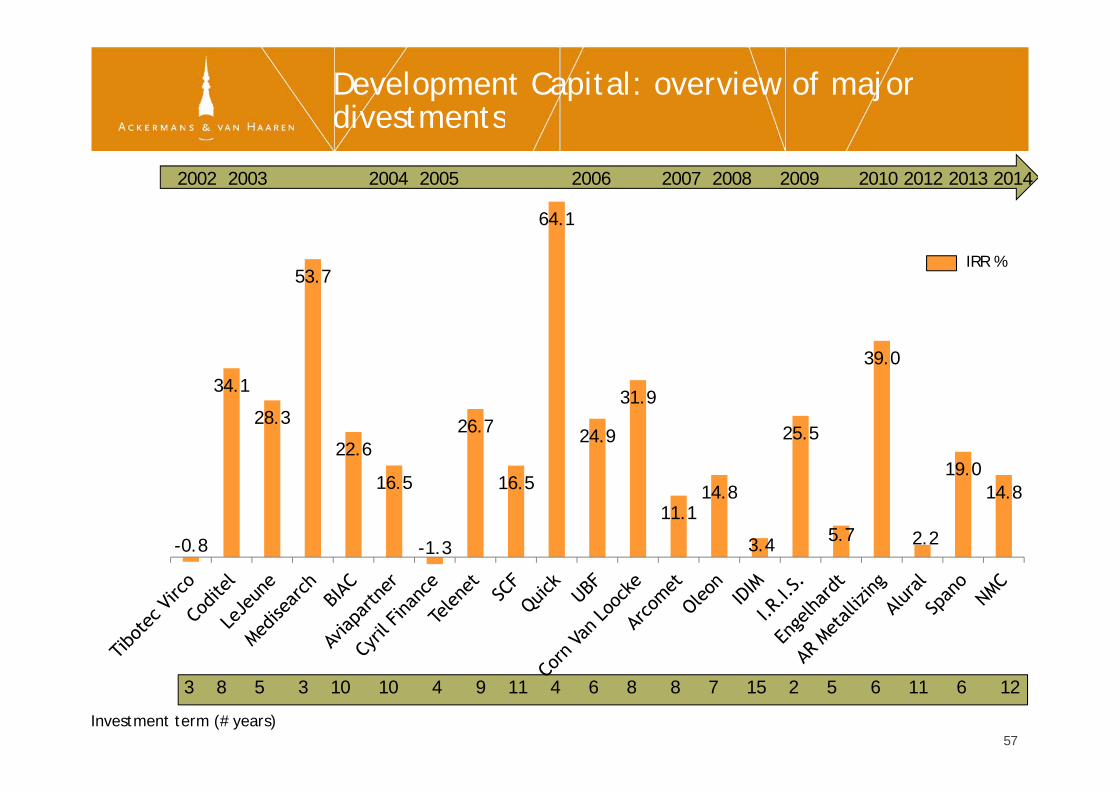

Development Capital: overview of major divestmentsdivestments

64 1

2002 2003 2004 2005 2006 2007 2008 2009 2010 2012 2013 2014

53.7

64.1

IRR %

34.131 9

39.0

28.3

22.6

16 5

26.7

16 5

24.9

31.9

14 8

25.5

19.014 8

-0.8

16.5

-1.3

16.5

11.114.8

3.4 5.7 2.2

14.8

3 8 5 3 10 10 4 9 11 4 6 8 8 7 15 2 5 6 11 6 12

Investment term (# years)57

Outlook 2015

‘AvH made a positive start to 2015 with some AvH made a positive start to 2015 with some significant transactions such as the acquisition of 100% of the Tour&Taxis site the restructuring of 100% of the Tour&Taxis site, the restructuring of the shareholding of Holding Groupe Duval, where the acquisition of Residalya has given AvHwhere the acquisition of Residalya has given AvHaccess to the French retirement home market, and above all the 1 6 billion euros worth of new and above all the 1.6 billion euros worth of new orders won by DEME.

The board of directors is confident for the year 2015 ’ 2015.

58

For further questions or additional information, please consult our website: www.avh.be

Contact:Luc BertrandCh i f th E ti C ittChairman of the Executive Committee

Jan SuykensMember of the Executive Committee

Tom BamelisMember of the Executive Committee

T +32 3 231 87 79E [email protected]

59