3. profile of information technology...

TRANSCRIPT

3. PROFILE OF INFORMATION

TECHNOLOGY INDUSTRY

3. PROFILE OF INFORMATION TECHNOLOGY INDUSTRY

3.1 Introduction:

The Indian economy has undergone substantial changes since the introduction of economic

reforms in 1991. The economy of India is the tenth-largest in the world by nominal

GDP and the third-largest by purchasing power parity (PPP). The country is one of the G-

20 major economies, a member of BRICS and a developing economy that is among the top

20 global traders according to the WTO. IMF projects India's GDP to pick up in 2015 to

6.4 per cent. As per Central Statistical Organization, in 2015, India's GDP at current prices

is expected to be 120973.81 billion Indian Rupee.101

India has the second fastest growing services sector with its compound annual growth rate

at nine per cent, as per the Economic Survey for 2013-14. The services sector is a vital

component of the Indian economy and has emerged as one of the largest and fastest-

growing sectors not just in the country but in the global landscape; subsequently, its

contribution towards global output and employment has been substantial.

As per the Economic Survey, 102

in India, the growth of services-sector GDP has been

higher than that of overall GDP between the periods FY2001- FY2014. Services constitute

a major portion of India’s GDP with a 57 per cent share in GDP at factor cost (at current

prices) in 2013-14. During FY 2014–15, the sector is projected to grow at a healthy 5.6 per

cent, according to National Council of Applied Economic Research (NCAER).

The survey highlighted that some services like software and telecom were big ticket items

that gave India a brand image in services. The Indian IT-BPM industry is relentlessly

continuing its growth path. The IT industry demonstrated flexibility and resolves to adjust

to turbulent economic conditions and experience double digit growth. Overall revenue

(exports + domestic) for FY2015 is expected at USD 146 billion, a growth of ~13 per cent

over last year, an overall y-o-y addition of ~USD 17 billion.103

101

http://mospi.nic.in/Mospi_New/site/inner.aspx?status=2&menu_id=92 102

http://timesofindia.indiatimes.com/budget-2015/economic-survey-2014/Economic-Survey-2014-15-GDP-growth-seen-at-5-4-5-9/articleshow/38066583.cms? 103

The IT-BPM Sector in India: Strategic Review 2015, Report by Nasscom

85

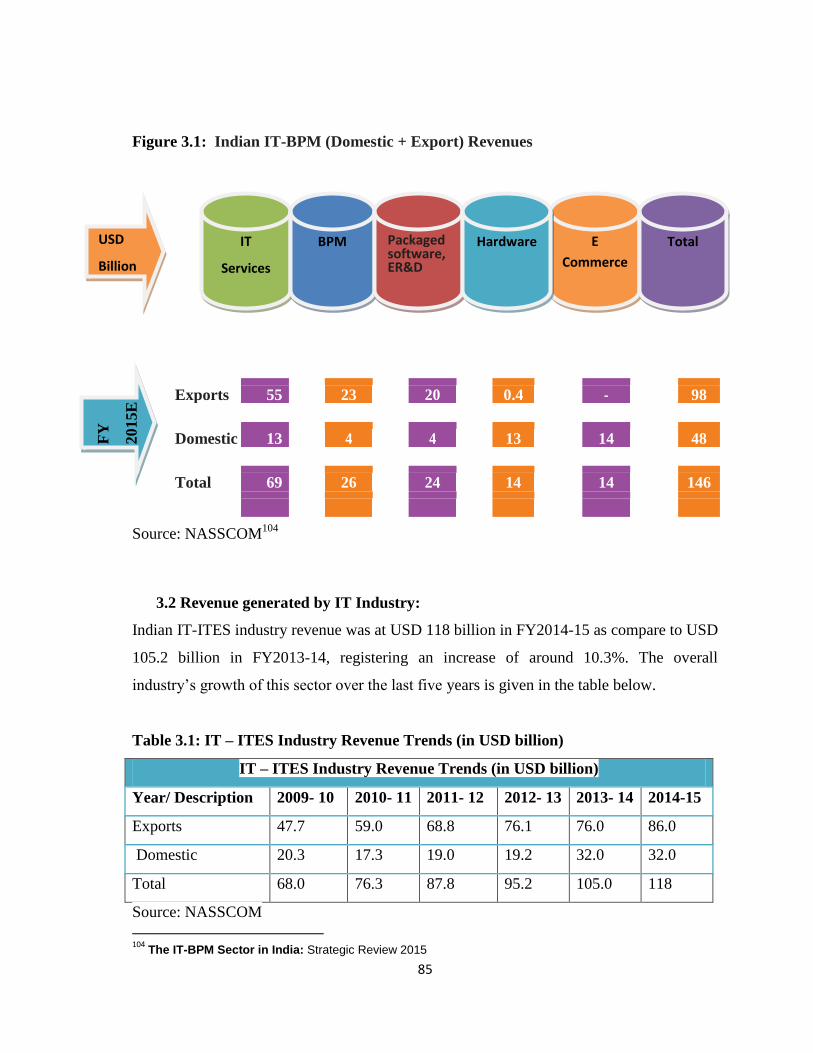

Figure 3.1: Indian IT-BPM (Domestic + Export) Revenues

Source: NASSCOM104

3.2 Revenue generated by IT Industry:

Indian IT-ITES industry revenue was at USD 118 billion in FY2014-15 as compare to USD

105.2 billion in FY2013-14, registering an increase of around 10.3%. The overall

industry’s growth of this sector over the last five years is given in the table below.

Table 3.1: IT – ITES Industry Revenue Trends (in USD billion)

IT – ITES Industry Revenue Trends (in USD billion)

Year/ Description 2009- 10 2010- 11 2011- 12 2012- 13 2013- 14 2014-15

Exports 47.7 59.0 68.8 76.1 76.0 86.0

Domestic 20.3 17.3 19.0 19.2 32.0 32.0

Total 68.0 76.3 87.8 95.2 105.0 118

Source: NASSCOM

104

The IT-BPM Sector in India: Strategic Review 2015

Exports 55 23 20 0.4 - 98

Domestic

13 4 4 13 14 48

Total

69 26 24 14 14 146

IT

Services

E

Commerce

BPM Packaged software, ER&D

Hardware Total USD

Billion

FY

2015E

86

Figure: 3.2 IT BPM Revenues in FY 2014

Source: NASSCOM105

3.2.1 Exports of IT Industry-

FY2015 is expected to see the exports market at over USD 98 billion, recording a 12.3 per

cent growth over last year. ER&D and product development segment is the fastest growing

at 13.2 per cent, driven by higher value-added services from existing players and an

105

www.nasccom.in

87

increased business from GICs. IT services exports are to grow at industry rate of 12.6 per

cent. Value-added services around SMAC – upgrading legacy systems to be SMAC

enabled, greater demand for ERP, CRM, mobility from manufacturing segment and user

experience technologies in retail segment is driving growth in IT services.

Figure 3.3: Exports of IT Services

Source: NASSCOM

88

3.2.2 Domestic Market-

The need for Indian firms to effectively compete in a globalized world presents an

immense untapped opportunity for the supply side. As an economy, India is beginning to

stabilize post elections. With the government’s clear policies and economic growth agendas

particularly Digital India and Make in India, have helped drive a vision of a technology

enabled India. A further push in this direction is coming from the government’s Digital

India campaign which envisages a USD 20 billion investment covering mobile connectivity

throughout the country, re-engineering of government process via technology and enabling

e-delivery of citizen services.

The domestic IT-BPM market is rapidly approaching the USD 50 billion mark. In FY2015,

the market is expected to be a little over USD 48 billion, an annual growth of 14%. This is

faster than industry growth that is largely being driven by the growth in e-commerce

segment.

IT services (USD 13 billion) and software products (USD 4 billion) segments are the next

fast growing segment at 10 per cent and 12 per cent respectively. IT services is being

driven by SMAC-cloud enablement, custom developing application for mobile; with the

return of focus on infrastructure projects During FY2014-15, domestic IT services growth is likely to be at 9.7% as large enterprises

exhibit cautious spending pattern; driven by technology upgrades in BFSI, telecom and

State Governments, and compliance of MIS investments. The domestic BPO services

growth is estimated at 12% in FY2013-14, driven by demand from select customers

reverting to outsourcing business processes, especially from the BFSI, automotive and

retail sectors. Domestic software products is estimated at 9.5% due to increased demand for

retail, healthcare, education, manufacturing (vertical-specific) and SMAC (Social media,

mobility, analytics and cloud) -based solutions. With the advent of cloud, the next

opportunity is India’s 47 million SMBs, who are able to rapidly bridge the technology

adoption gap.

89

3.3 Information Technology in India:

The Information Technology (IT) industry is one of the fastest growing sectors in India.

India has successfully established itself as a competitive and prominent destination for

outsourcing IT & IT enabled services over the last decade.

Government of India and the State Governments have put up efforts like, liberalization of

external trade, elimination of duties on imports of information technology products,

relaxation of controls on both inward and outward investments and foreign exchange,

setting up of Export Oriented Units (EOU), Software Technology Parks (STP), and Special

Economic Zones (SEZ), which helped IT industry to gain dominant position in world’s IT

scenario. Over the past decade, the IT / ITeS industry in India has been a story of

unparalleled growth. The compounded annual growth rate (CAGR) of the industry has

been over 25 % in the last 5 years. Most of the Indian firms, across all other sectors, largely

depend on the IT & ITeS service providers to make their business processes efficient and

streamlined. The Indian manufacturing sector has the highest IT spending followed by

automotive, chemicals and consumer products industries. (International Data Corporation-

IDC's Manufacturing Insight Report 2012*1)106

Indian organizations are turning to IT to help them grow business in the current economic

environment. IT is seen as a change enabler and a source of business value for

organizations by 85 per cent of the respondents, according to a study conducted by

VMware Inc (.*2.) Over these years four main components have formed the industry – IT

Services, BPO, Engineering Services and Hardware. Banking and financial services

account for the dominant share in India’s total IT export revenues. Telecom and

Manufacturing, the other consumers of India’s IT services have also witnessed increase in

share over this period resulting in a rise in concentration of the 3 sectors from 64% to 78%.

Exports from IT sector are rapidly growing which ultimately contributes to economy.

106

International Data Corporation-IDC's Manufacturing Insight Report 2012

90

Table 3.2: IT Professionals Employed by India

Employment in IT-ITeS Industry (in millions)

Year/ Segment 2009-10 2010- 11 2011- 12 2012- 13 2013- 14 2014-15

IT Services & Exports 1.0 1.15 1.29 1.4 1.5 1.6

BPO Exports 0.77 0.83 0.88 0.92 0.95 1.1

Domestic Market 0.53 0.56 0.60 0.64 0.68 0.80

Total Employment 2.30 2.54 2.77 2.96 3.13 3.50

Source: NASSCOM Strategic Review107

The industry currently employs 3.5 million – India’s largest private sector employer. It is

also playing a key role in promoting diversity within the industry women employees (>34

per cent share), 170,000 foreign nationals and a greater share of employees from non-Tier I

Indian cities.

3.4 Indirect impact of IT/ ITes on Indian Economy:

NASSCOM and Deloitt conducted joint study and came up with the findings of indirect

impact of IT/ITes on Indian Economy. 108

Below figure 3.4 states the same

Figure 3.4: Indirect contribution of IT and ITeS to the Indian Economy

107

NASSCOM Strategic Review 2015 108

Indian IT and ITeS Industry: Impacting Economy and Society (2007 – 2008) , NASSCOM and Deloitt

Employment generation

Growth in other sectors

Balanced regional

development Growth in PE/VC funding

Indirect

Impact of

IT/ ITes

sector on

Indian

Economy

Spurring first generation

entrepreneurship Improving product &

service quality Front runner in

corporate governance Boost to country’s image

globally

91

a. Additional employment generation: The indirect employment generated, at the rate

of 4 additional jobs created in the economy for every 1 job created in the sector, is

even more socially relevant as nearly 75% of the workforce employed in those

additional jobs are SSC/HSC or less educated.

b. Driving growth of other sectors of the economy: Apart from contributing to the

growing income of its direct stakeholders (promoters, shareholders and employees),

the IT/ITeS industry has a multiplier effect on other sectors of the economy with an

output multiplier of almost 2 through its non-wage operating expenses, capital

expenditure and consumption spending by professionals.

c. Encouraging balanced regional development: By gradually spreading their business

operations to smaller Tier II/III cities, the IT sector (besides generating revenue and

employment) is also assisting in improving the supply of talent pool and

development of physical and social infrastructure, either directly by themselves or

by spurring the Government to action.

d. Fuelling the growth of PE/VC funding: The worldwide dot com boom and growth

in the IT sector kick-started VC activity in India which led to the creation of first

generation of India centric VC funds.IT/ITES continues to be the favourite sector

with the largest share (28%) of PE/VC funding,

e. Spurring first generation entrepreneurship: As per information available with

Software Technology Parks of India (STPI), 1,905 new units were registered during

the period FY01 to FY05, most of which are likely to be set up by first generation

entrepreneurs. While many first-generation entrepreneurs became billionaires in the

process, the practice of Employee Stock Option Plan (ESOP), first started by the

IT/ITeS industry, shared this wealth among employees as well thereby creating

many salaried millionaires.

f. Improving the product/service quality level: The fact that IT/ITeS companies cater

to and compete with global players has led to their adopting the highest quality

standards. This high quality of services and products has been the driver and

sustainer of growth which has helped move India out of the mediocrity, low

92

quality image and has in fact raised the bar for other industries as well. Nearly

75% of Fortune 500 and 50% of Global 2000 corporations source their technology

related services from India with an increasing number of MNCs outlining their

investment plans for setting up R&D operations in India.

g. Front runner in practicing good corporate governance: The industry has been a front

runner in practicing good corporate governance and their commitment to infuse it in

their business activities have led to a creating a positive pressure within the

industry, as well as in other industries, with more and more companies adopting

global standards in corporate governance practices.

h. Boosting the image of India in the global market: Widely travelled Indians have

watched with ride as different countries and people look at India and Indians with

hitherto unknown respect and admiration. The India IT/ITeS industry has

contributed to what brand India stands for in today‘s global market.

3.5 Impact of IT and ITES Sector on India’s Growth:

The rapid adoption of Internet and mobile is creating enormous opportunities for

entrepreneurship in the country. A growing ecosystem of early stage funding, incubation

and peer learning is creating innovative start-ups building technology solutions and

products for India and the global market. Initiatives like creating a strong and robust

ecosystem for start-ups, innovation clusters and centers of excellence (CoEs) will

encourage entrepreneurship and build the next generation of Global companies from

India”.

IT-BPO sector has become one of the most significant growth catalysts for the Indian

economy. In addition to fuelling India’s economy, this industry is also positively

influencing the lives of its people through an active direct and indirect contribution to the

various socio-economic parameters such as employment, standard of living and diversity

among others. The industry has played a significant role in transforming India’s image

from a slow moving bureaucratic economy to a land of innovative entrepreneurs and a

global player in providing world class technology solutions and business services. The

93

industry has helped India transform from a rural and agriculture-based economy to a

knowledge based economy.

Increasing adoption of technology and Telecom by consumers and focused Government

initiatives – leading to increased ICT adoption

IT/ITeS sector has become one of the most significant growth catalysts for the Indian

economy. In addition to fuelling India‘s economy, this industry is also positively

influencing the lives of its people through an active direct and indirect contribution to the

various socio-economic parameters such as employment, standard of living and diversity

among others. The industry has played a significant role in transforming India‘s image

from a slow moving bureaucratic economy to a land of innovative entrepreneurs and a

global player in providing world class technology solutions and business services. The

industry has helped India transform from a rural and agriculture-based economy to a

knowledge based economy.

Key Highlights of the growth are as follows

1. Economic Development of country

2. Fast emerging as a growth story driven by a growing middle class, consumer

spending, and technology innovation.

3. Increasing adoption of technology and Telecom by consumers and focused

Government initiatives – leading to increased ICT adoption.

Due to above mentioned reasons; IT sector is looked up as fast growing sector, which

greatly influence the Indian economy and has great impact on people through its

contribution to the growth and sustainability.

94

Figure 3.5: Impact of India’s growth

Source: http://www.nasscom.in/impact-indias-growth#sthash.j3oOuGWg.dpuf

Source: NASSCOM

Opportunities

in smaller

towns

employment

for

differently

abled

Employment

For

Non

technical

Promoting

woman

entrepreneur

high growth

opportunity

for youth

employment

for out of the

main stream

candidate

Impact of Employment practices adopted by IT/ITes

95

a. Creating employment opportunities in smaller towns/cities: By recruiting talent

from non-metro towns and rural background, the industry has reached out to the

educated resource pool in these places and created employment opportunities,

which hitherto was largely limited. Large IT/ITES companies often have 33 to 50%

of their employees coming from non-metro/rural areas.

b. Encouraging employment of differently abled: Through their policy and practice of

employing differently abled people, training them and creating a conducive

working environment, IT/ITES companies are initiating a trend which could have a

significant impact on employment opportunities for the differently abled in India.

c. Opening opportunities for non-technical personnel: The growing employment

opportunities in this sector (both direct and indirect) are not restricted to the bet ter

educated or technically educated people alone While 75% of the employment

generated through the indirect route are filled in by candidates who are SSC/ HSC

or less educated, companies also help under qualified candidates to reach a desired

skill level by investing in their training and skill upgradation.

d. Promoting women empowerment: The growing trends in the number of women

employed in this sector indicates that not only does the industry offer equal

opportunity to women but also has in place proactive and sensitive mechanisms

which counter the common causes that discourage women from pursuing

employment in the corporate sector.

e. Providing high growth opportunities for the youth: The industry has created

excellent employment and fast track growth opportunities for the younger section of

the population and is likely to become one of the largest employers of a growing

‘young population’ of India. The overall median age group of the sector is 28.9

years with 70% of the workforce being in the age-group 26-35 years.

f. Creating opportunities for the ‘out-of-the-main-stream’ candidates: The IT industry

through its innovative recruitment practices has also hired persons who would not

typically be considered employable such as retired persons and housewives.

96

3.6 The benefits of doing business with India:

India’s investment friendly policies, forward–thinking reforms, higher disposable incomes

and rising middle class have made it an attractive outsourcing destination for foreign

investors. Young Workforce: Opportunity to work with enthusiastic and career–focused

Indians, who constantly upgrade their skills through training and certificate programs.

Fluency of Language: language or communication barriers will not be faced as over 350

million people in India are fluent in the English language. India has been successful in the

outsourcing industry mainly because of the fluency with which Indians speak English.

Robust Education created talent: You get access to a huge talent pool of experienced

specialists. The high value placed on education in India has resulted in a highly educated

workforce who has experience and knowledge in varied fields.

Cultural Diversity: You will face fewer cultural challenges when you share new business

ideas and endeavors with Indians, as they are always open to new ideas and opportunities

Organizations get dedicated employees to work for them, as many Indians work eight hour

shifts for six days a week. Indians also willingly work around the clock to compensate for

the time difference between India and the US or UK. Only India can give you access to

committed employees who are more than willing to work long shifts over odd hours.109

3.6.1 Advantage India -

On a yearly basis, 3.1 million students graduate from Indian universities in various fields

such as software programming, accounting or law. Currently India has 2, 297 engineering

colleges that graduate 500, 000 engineering students every year.

India can give you access to young talent, as more than half of India’s population is below

the age of 25. Over 60% in Indians are in the age group of 15–59.The higher education

system in India is the world’s third largest, after China and the US.India currently has 100

deemed universities, 215 state universities, 13 national institutions and 20 central

universities. There are 16000 colleges spread across India. The Indian Institutes of

Technology enroll about 8000 students every year.

109

INDIA IN BUSINESS PREFERRED INVESTMENT DESTINATION, Report by Investment & Technology Promotion Division, Ministry of External Affairs, Government of India. 2014

97

3.7 Investment in IT Sector:

Indian IT's core competencies and strengths have placed it on the international canvas,

attracting investments from major countries.

According to data released by the Department of Industrial Policy and Promotion (DIPP)110

, the computer software and hardware sector attracted foreign direct investment (FDI)

worth Rs 60,503.21 crore (US$ 10.01 billion) between April 2000 and June 2014.

Some of the major investments in the Indian IT and ITeS sector are as follows:

Tata Communications plans to invest more than US$ 200 million to double its data centre

capacity in India to 1,000,000 square feet over three years.

Wipro has bagged a US$ 1.2 billion outsourcing deal from Canadian utilities major ATCO.

As part of the deal, Wipro will take over the IT subsidiary of ATCO, ATCO I-Tek, in an

all-cash deal worth US$ 195 million. L&T Technology Services has bought 74 per cent

equity stake in Thales Software India Pvt Ltd, to strengthen its avionics business. This

collaboration will enhance L&T's expertise in high-end avionics software. The Techno

park-Technology Business Incubator plans to set up 'OpeniSpace', an open innovation

space on its campus, for innovators and young student entrepreneurs.

The 'OpeniSpace' start-up space will provide plug-and-play facilities with 4 to 12 seats

along with Wi-Fi internet connectivity for young entrepreneurs.

Mphasis has announced the launch of an e-Surveillance and Power Efficiency Solution

'ProTecht', in partnership with Delta Power Solutions. The partnership will enable Mphasis

Payment Managed Services (MPMS), to offer the most comprehensive single window

solution for ATM security and power efficiency innovation across the ATM industry.

Apax Partners has bought a 1.5 per cent stake worth Rs 57.84 crore (US$ 9.56 million) in

software products and services provider Persistent Systems in a public market transaction.

110

Department of Industrial Policy and Promotion (DIPP) statistics, Department of Information and Technology

98

3.7.1 Government Initiatives-

India has been ranked the third–best country in Asia, with excellent investment potential

The Government of India played a key. The Central Government and the respective state

governments are expected to collectively spend US$ 6.4 billion on IT products and services

in 2014, an increase of 4.3 per cent over 2013, according to a study by Gartner.

Some of the major initiatives taken by the government to promote IT and ITeS sector in

India are as follows:

The Indian Government has implemented the "National IT Task Force" 108 point Action

Plan to promote the growth of Information Technology in India

India’s government has set up a Ministry of Information Technology to quickly approve

and implement IT projects and also to streamline the regulatory process in India

In May 2000, the Indian Parliament passed an Information Technology Bill, known as the

IT Act 2000. This bill mentions out severe punishment to cyber criminals and has also

brought E–commerce within the purview of the Indian law. India is now one among the 12

nations that has cyber laws.

India plans to set up industrial parks in the pharmaceutical and information technology (IT)

sectors in China to strengthen India-China trade and investment ties. 111

More than 20 small and medium enterprises (SMEs) in the IT sector have recently received

land allotment letters from the Government of Punjab to set up their units with an

investment of Rs. 500 Crore (US$ 82.71 million).

Government initiatives such as Mobile Seva, Digital India, and Pradhan Mantri Jan Dhan

Yojana will also trigger adoption of software solutions in the coming years, the IDC report

said.

Going forward, IDC expects the software market to grow at a stable pace in the next five

years (2014-2018) with a compound annual growth rate (CAGR) of 10.5%.

Some of the sectors to watch out for in the future, according to IDC, include entertainment,

retail and e-commerce, education, and hospitality.

Source: NASSCOM

111

http://planningcommission.gov.in/plans/mta/mta-9702/mta-ch27.pdf

99

Table 3.3: Information Technology Clusters

Sr. No City Illustrative list of companies

1 Mumbai/ Navi Mumbai Oracle Financial Services, TCS, Cognizant, iGate,

Deloitte, L & T Infotech

2 Delhi(NCR) HCL Technologies, Hewitt Associates, Infosys, Tech

Mahindra, TCS, Genpact

3 Bangaluru IBM, Infosys, Wipro, Siemens, TCS, Mhapsis, HCL

4 Chennai Oracle, TCS, Cognizant, Syntel, Microsoft, Wipro,

Capgemini

5 Hyderabad HSBC, Microsoft, Infosys, Wipro, Cognizant, Google

Inc.

6 Pune Infosys, Persistent, BMC Software, Tech Mahindra,

Zensar, IBM

7 Kolkata TCS, Delhi solutions, HCL, Tech Mahindra, Wipro,

Genpact

Source: ibid, 112

3.8 Global Sourcing Trends:

In the face of a volatile economic environment, 2012 recorded a steady growth for

technology and related services sector, with worldwide spending of USD 1.9 trillion, a

growth rate of 4.8 per cent over 2011. BPM services with 4.9 per cent (slightly above

industry average) contributed majorly to the growth; followed by IT services and packaged

software each with 3.3 per cent growth. IT, BPM services and software products continued

to lead, accounting for over USD 1 trillion – 58 per cent of the total IT spend. IT hardware

with growth rate of 7 per cent, touched USD 797 billion and accounted for the remaining

42 per cent of the worldwide technology spend in 2012.

112

Key highlights of the NASSCOM.IDC study on the domestic services (IT-ITES) Market opportunity

100

In line with growth in global IT spend, global sourcing market also grew to USD 124-130

billion, growth of 9 per cent over 2011 – nearly twice the growth of global IT spend.

APAC spend grew 6 per cent, nearly 1.6X faster than mature geographies. IT spends of

America remained steady at 5 per cent and EMEA recorded a minimal growth of 1 per cent

over 2011. The impact was also visible on the vertical spending with emerging verticals

driving incremental growth in 2012. While BFSI and manufacturing segment remained the

two largest verticals in terms of total share in IT spending with more than ~40 per cent

share, emerging verticals like healthcare, retail, government and utilities contributed ~30

per cent of total IT spend in 2012.

Lingering concerns about the global economy also impacted contracts; volume fell ~13 per

cent, however Average Contract Value (ACV) remained fairly steady at USD 21 billion

largely due to a number of mega-deals in BPM. In terms of regional contracts, APAC was

the sole market to have registered significant growth over 2011, 55 per cent (value terms)

and increased its share in total contract value to 15 per cent; EMEA contracts declined 13

per cent and the Americas by about 2.5 per cent.113

3.9 Indian IT Industry -Analysis by NASSCOM:

According to survey from Fortune, almost the biggest 100 companies in America treat

India as their first choice of abroad software. NASSCOM has highlighted the prevailing

trends of IT Industry in their strategic analysis- NASSCOM Strategic Review 2015.114

While worldwide IT-BPM spend was USD 2.3 trillion, growing at 4.6 per cent over 2013,

global sourcing of services grew by 10 per cent, and India continued to hold on to its

leadership position with a 55 per cent market share. In FY2015, the Indian IT-BPM

industry is estimated to account for revenues of USD 146 billion, growing by 13 per cent

over last year, Industry exports are over USD 98 billion growing at 12.3 per cent, while the

domestic segment, which has benefited from the inclusion of ecommerce and mobile app

industry, is estimated to touch USD 48 billion. The industry today is India’s largest and

113

NASSCOM Annual Report 2012-13 114

NASSCOM Strategic Review 2015

101

most diverse private sector employer, with a direct workforce nearing 3.5 million,and

effecting over 10 million indirect jobs. At the same time the industry’s relative share in

India’s GDP has swelled to 9.5 per cent, it offsets more than 70 per cent of India’s oil

import bill, attracts a major share of PE/VC investments into the country, has effected

balanced regional growth and empowered diverse sections of the society, and is the face of

the Indian MNC story. The Indian IT-BPM industry has exhibited rapid evolution – in

terms of expanding their vertical and geographic markets, attracted new customer

segments, transformed from technology partners to strategic business partners imbibing a

shared vision, offering considerably wider spectrum of services over the years. Today, the

Indian IT-BPM industry has already begun moving from enterprise services to providing

‘enterprising solutions‘. These are not standard lift and shift solutions – key to this world is

a high degree of proactivism, maturity, business understanding and entrepreneurship.

The Indian IT-BPM industry is leading the drive to design solutions incorporating SMAC

(Social, Mobile, Analytics Cloud,) to offer innovative, enterprising answers. These

enterprising solutions are able to create client impact on not only cost, but also revenues,

profit margins and cash flows.

3.9.1 Indian IT-BPM Performance-

The Industry contribution relative to India’s GDP is set to touch an estimated 9.5 per cent

and share in total services exports >38 per cent. Exports (incl. hardware) are likely to record a 12.3 per cent growth to reach over USD 98

billion, up by ~USD 11 billion last year. Domestic IT-BPM market at USD 48 billion is set

to grow faster than exports market at 14 per cent, driven largely by the addition of

ecommerce into the picture.

3.9.2 Indian IT-BPM Value Proposition-

India continues to reinforce its position as the only country in the world from where one

can do anything and everything. India has continued to maintain its first mover advantage

and retained its leadership position in the global sourcing arena with a share of 55 per cent

102

in FY2015. At the foundation of this value proposition are four robust growth pillars,

which defines its attractiveness as a key destination.

1. A highly connected and a digital ready economy-

India remains a high potential market worldwide, offering multiple opportunities for unmet

needs. With the world’s second largest population (~1.2 billion), India also presents a

large, burgeoning end-user market. Additionally, with 937 million mobile subscribers, 278

million internet users, an USD 14 billion ecommerce market, and an economic growth rate

that is soon expected to surpass that of China, India is set to leapfrog into the digital world.

The Government’s Digital India and Make in India initiatives are only expected to

accelerate India’s plunge into the connected digital world.

2. India, remains an excellent business delivery center for the IT-BPM industry-

Currency movements and increased operational efficiencies have ensured that India’s

position as the world’s most cost competitive sourcing destination has only become

stronger in the past year. Even Tier I cities in India like Bengaluru continue to be between

8-10 times cheaper than source countries and significantly cheaper than other low-cost

destinations. Additional cost benefits have been passed on to customers through astute

internal initiatives including moderate wage inflation, adopting automation and nonlinear

models to control salary expenses, introducing newer career bands, flattening

organizational pyramid, etc. India is home to the highest volume of diverse, employable

talent in the world. India is expected to churn out nearly 5.8 million graduates and

postgraduates in FY2015, out of which 1.5 million people form an industry suitable, ready

to hire pool. At the same time, the IT-BPM industry has been growing in size, scale,

maturity and domain expertise and focused in addressing what customer businesses’

demand. The industry has been catalyzing business transformation for global clients

through its established global delivery chain – ~640 ODCs across >78 countries, acquiring

local talent for language skills and cultural compatibility with clients. The variety and scale

on offer in India again allows for multiple collaborative models to exist. This unique

diversity gives ample opportunities to providers to choose their organization size, business

models to adopt, and what kind of partnerships to create. The agile start-up ecosystem

103

(3,100+ start-ups) in the country has impacted large enterprises too – the need to be nimble

has prompted larger firms to re-organize their structure with advanced decision-making

capabilities, while the need to offer innovative, unmet needs has led them to build

partnerships with smaller firms.

3. The Indian technology industry is today a global “Digital Skills Hub”-

Today, the country hosts ~7,000 digital focused firms with start-ups fueling innovation by

investing further in futuristic technologies. India has been creating a future-ready digital

workforce, with more than 1, 50,000 employees with SMAC skills. ~50,000 employees are

skilled in analytics 30,000 people in enterprise mobility and >50,000 in cloud and social

media & collaboration.

4. A strong innovation backed ecosystem–

Organizations in India are consistently innovating around products, processes and business

models to deliver enhanced value propositions to the clients. While start-ups are

increasingly driving innovation around emerging tech-dependent areas like edu-tech,

health-tech, ad-tech etc., large firms are looking to benefit by investing, co-creating and

partnering with innovative startups.

The above initiatives are ensuring consistently high CSAT scores from clients, with over

85 per cent agreeing that transformative work can be delivered out of India, and further

reinforce India’s leadership position in the global sourcing market.

Indian IT- BPM Industry is demonstrating its existence and establishment on the five core

pillars that it has nurtured and evolved over the past couple of years. With customers

increasingly engaging with Indian service providers as a ‘strategic partner’, rather than just

a pure ‘technology service provider’, key players in the Indian sourcing industry have re-

aligned and capitalized

3.9.3 Future Outlook-

The future of the global technology industry will be shaped by economic forces, and

adoption of new technologies. To survive in a globally connected, and increasingly

competitive world, IT enabled enterprise digital transformation will be a must. With

rapidly-evolving technologies, changing consumer preferences and oftentimes competing

104

channels, many organizations struggle with how to transform internally to meet the

challenges of this new, always connected digital world. Organizations therefore need to

carefully walk the path towards a comprehensive digital transformation with a concrete

strategy to utilize its strengths and alleviate its challenges. As the global economy

improves, and consumer confidence increases, investing in new technologies such smart

computing products, internet of things, products and platforms, cloud computing, mobility

and analytics will enable vendors to gain efficiency, agility, access to consumers, and

innovation which when properly leveraged will provide tremendous opportunity for the

delivery of real competitive value to clients.

The Indian IT-BPM industry is expected to continue to partner and handhold clients to

enable business success in the digital era, and is well set on its goal to reach revenues of

USD 300 billion by 2020. At the same time, challenges around economic volatility,

protectionism, competition and customer

new services, technologies, verticals and geographies.

FY2014 total revenues (domestic + exports; excludes hardware) is expected to grow by

about 13-15 per cent to reach USD 106-111 billion; of this, exports are likely to be about

USD 84-87 billion, a growth of about 12-14 per cent. For the industry to continue on the

growth path and to counter the challenges of understanding will need to be addressed by

concerned stakeholders.

The global economy has improved 2013 onwards, with global GDP increase by 3.5 per

cent in 2013 and further by 4.1 per cent in 2014. Simultaneously, the growing importance

of the BRIC economies in world trade means that these markets are maturing from just

being sources of cheap labour to sources of innovation. Five major technology changes are

expected to open new opportunities for service providers – smart computing (expected to

drive industry-specific solutions), Software-as-a- Service (SaaS to play a dominant role),

social technologies (empower all elements of an industry’s value chain including suppliers,

employees, customers, and business partners), mobility (access to anytime, anywhere

information) and analytics (real-time intelligence). Another mega trend is around buyers of

technology: the expanding role of IT means that the stakeholder has expanded beyond

105

CIOs; employees now are influencing corporate tech adoption and IT’s role is also shifting

from a reactive back-end support operation to a proactive enabler of innovation.115

India continues to be the global sourcing leader, but the total global sourcing (IT+ BPM)

market of USD 124-130 billion accounts for only a little over 10 per cent of global IT-BPM

spend – highlighting the still large, untapped market opportunity. Indian IT-BPM firms are

well set to take advantage of this opportunity by working towards enhancing their existing

capabilities, developing new capabilities and expanding their focus to emerging alternative

outsourcing destinations, it will have to mitigate various challenges it faces at the macro,

operational and ecosystem level.

At the same time, for the industry to continue on the growth path and to counter the

challenges of emerging alternative outsourcing destinations, it will have to mitigate various

challenges it faces at the macro, operational and ecosystem level.

Macro level challenges: The ongoing global recession is having a fairly big impact on

business sentiments and customer confidence, particularly in the main markets of US and

Europe. With challenging labour market conditions in these geographies, governments are

increasingly resorting to protectionism to boost their economies. Changes in their policies

are impacting availability of work permits and visas; the threat of taxation on outsourcing

firms is another challenge. Within India market, the upcoming elections of 2014, the

continuously rising wage inflation and currency volatility continue to be areas of concern.

The industry is also facing certain challenges thrown up by newer technologies that are

disrupting the traditional services and traditional forms of delivery. For e.g. cloud-based

technologies have the potential to cannibalize business through automation and platform

based delivery.

Operational challenges: The industry will need to explore new avenues of growth – shift

from services to IP-led growth, adapt and take advantage of the changing technology

landscape to offer differentiated products/services to customers and showcase value beyond

cost. These efforts will go a long way in transforming India’s image from a low cost

destination to an innovation hub.

115

NASSCOM Strategic Review 2014

106

Ecosystem: India’s competitiveness as the foremost outsourcing destination is being

threatened by wage inflation, the rise of other locations, particularly the Philippines and

China as alternative sourcing destinations and also the customers’ desire to de-risk

geographic concentration. India is also likely to face a talent shortage (in terms of the

quality of people available rather than the quantity) in the medium terms. Cyber espionage

is a serious, emerging threat that could lead to security compromise and data breaches,

compromise of personal information, risks of insider threats due to liberal access to client

networks, and access sensitive IPR information.

Keeping these challenges and variations in mind, the Indian IT-BPM firms will need to

keep continuing the transformation of its business models and strategies for future growth.

The need for expansion to new markets, further enhancing customer centricity, flexible

delivery models, and continue to make strategic investments.

In order to achieve the next level of growth, it is imperative for industry stakeholders to

work together on five core agendas that will enable India to retain and enhance its status as

the world’s most favored outsourcing destination. On the one hand, efforts must be made to

improve the industry ecosystem: in terms of establishing world-class infrastructure,

enhancing India’s corporate governance and risk/ security framework, thus, enhancing

confidence in India as a business destination. The government should make it a top-most

priority to significantly improving the quality of education. Another important factor in

establishing India as an innovation hub is the need to foster entrepreneurship – having a

very strong and robust funding system to finance various start-ups, setting up of a plethora

of innovation clusters, Centres of Excellence (CoEs) and research labs to drive primary

research and correspondingly, a very strong IP protection and implementation framework.

As technology is rapidly emerging as a platform to deliver social change, it is also

necessary for the government to ensure that the technology infrastructure is well

established for the delivery of technology- enabled services in healthcare, education,

financial and public services. Finally, both the industry and NASSCOM must look to

expand beyond core markets – explore opportunities in new, emerging geographies,

underpenetrated verticals that have long-term potential and meet and expand customer base

– SMBs, India’s domestic market and other developing nations.

107

3.10 Indian IT/ITES Industry: Impacting Economy And Society:116

Indirect contribution to the Indian economy: The growth of the IT/ITES sector and its

resultant contribution to the economic growth and development has also resulted in certain

wider impacts, which in many cases have had a rub-off effect and set bench- marks for

other sectors of the economy while boosting the image of India in the global market.

i. Additional employment generation: The indirect employment generated, at the rate

of 4 additional jobs created in the economy for every 1 job created in the sector, is

even more socially relevant as nearly 75% of the workforce employed in those

additional jobs are SSC/HSC or less educated

ii. Driving growth of other sectors of the economy: Apart from contributing to the

growing income of its direct stakeholders (promoters, shareholders and employees),

the IT/ITES industry has had a multiplier effect on other sectors of the economy

with an output multiplier of almost 2 through its non-wage operating expenses,

capital expenditure and consumption spending by professionals

iii. Study show that USD 15.85 billion spent by the IT/ITES industry in the domestic

economy in FY06 generate an additional output of USD 15.5 billion

iv. Encouraging balanced regional development: By gradually spreading their business

operations to smaller Tier II/III cities, the IT sector (besides generating revenue and

v. Employment) is also assisting in improving the supply of talent pool and

development of physical and social infrastructure, either directly by themselves or

by spurring the Government to action

In case of Bhubaneswar (a Tier III city), some of the key impact of the IT/ITES sector has

been as follows:

1. Increase in software exports - Software ex- ports from the state reached USD 183

million in 06- 07, a 60% rise over exports in 05-06, on track to reach the target of

500mn USD by 2011-12.

2. Increase in registered IT/ITES units – The number of registered and exporting units

has risen steadily showing a CAGR of 118 and 170% respectively as compared to

116

NASSCOM & DELOITTE REPORT, 2008

108

98-99. Besides the capacity expansion of existing units, many of the big companies

are also setting up operations in the city

3. Employment – Supply of IT professionals, which was higher than demand till 2004,

now have a shortfall of 62,697. Demand for IT professionals is expected to reach

430,000 by 2011-12 with the corresponding figures on indirect employment being

1,720,000

4. Education – While building and expanding capacity of educational institutes are

underway, IT majors are undertaking training initiatives to improve student quality.

a. Infrastructure and other amenities – Keeping in line with the expansion/entry plans

of major IT/ITES companies, IT parks and townships are being built with a

corresponding improvement in other amenities like roads, housing, retail and

entertainment facilities Spurring first generation entrepreneurship: Corporate

India consisted of either large family owned businesses or multinational companies

till the advent of the IT/ITES industry, and it was rare to see a first generation

entrepreneur. The shift of focus from physical capital to intellectual capital and the

advent of the PE/VC funding enabled a large number of first generation

entrepreneurs with no wealth to try their hand at starting new enterprises. The

demonstrated success of these entrepreneurs created an aspiration among the

middle class and spurred them to exploit their potential with confidence.

b. As per information available with Software Technology Parks of India (STPI),

1,905 new units were registered during the period FY01 to FY05, most of which

are likely to be set up by first generation entrepreneurs While many first-generation

entrepreneurs became billionaires in the process, the wealth created was not

restricted among the founders alone. The practice of Employee Stock Option Plan

(ESOP), first started by the IT/ITES industry before it was adopted by many other

industries as well, shared this wealth among employees as well thereby creating

many salaried millionaires.117

117

www.stpi.in

109

c. Improving the product/service quality level: The fact that IT/ITES companies cater

to and compete with global players has led to their adopting the highest quality

standards. This high quality of services and products has been the driver and

sustainer of growth which has helped move India out of the “mediocrity”, low

quality image and has in fact raised the bar for other industries as well. Indian

exports had traditionally been restricted to low end, low-technology oriented

products like gems and jewelries and garments/apparels. It is with the advent of

IT/ITES industry that the world began to recognize that Indian products and

services could also compete and win against global competitors on quality

parameters. India is now also emerging as a research and development centre for

some of the large IT/ITES companies in the world, once again demonstrating that

India now stands for quality.

d. 30% of companies worldwide who have reached Level 5 of Capability Maturity

Model Integration (CMMI) are Indian IT/ITES firms.

e. Nearly 75% of Fortune 500 and 50% of Global 2000 corporations source their

technology related ser- vices from India with an increasing number of MNCs

outlining their investment plans for setting up R&D operations in India.

f. Front runner in practicing good corporate governance: The industry has been a

front runner in practicing good corporate governance and their commitment to

infuse it in their business activities have led to a creating a positive pressure within

the industry, as well as in other industries, with more and more companies adopting

global standards in corporate governance practices.

g. The major IT/ITES companies in India have in recent times received national and

international recognition for their corporate governance initiatives.

h. Boosting the image of India in the global market: Widely travelled Indians have

watched with pride as different countries and people look at India and Indians with

hitherto unknown respect and admiration. The India IT/ITES industry has

contributed to what brand ‘India’ stands for in today’s global market. While India

Inc. has been witnessing an acquisition spree of overseas companies in recent

110

years; the IT/ITES sector has led this phenomenon with the highest share (23%) of

outbound M&A deals in 2006 .

i. Human Resource Development: The fast growing IT/ITES industry has been

struggling with several issues concerning availability and quality of talent. The

industry has responded to this issue by evolving sustainable and innovative

solutions. Since the educational institutes lagged behind in supplying the requisite

number of trained people required for the industry and their curriculum could not

keep pace with the changing trends in technology, the IT/ITES industry themselves

came forward and made massive in- house training investments, which helped

them power their growth and compete at par with international giants in the global

market. The industry has also gone beyond and collaborated with the government,

private educational institutions as well as industry associations to contribute

towards capacity building, skill development and continual training of existing and

potential employees to enhance their capabilities and competitive skills. The

industry is also making efforts to ensure that employees are provided a stimulating

and healthy working environment for improving their level of satisfaction and

productivity.

j. Training of workforce: The industry has played a pioneering and pro-active role in

developing the talent pool in the country by forging links with the academia and

the Government. It has not restricted its efforts to developing its own employees

but is also investing in raising the overall standard of education. The industry has

collaborated with academic institutions for the bridging the gap between the

education imparted to students and the actual requirements in the job scenario.

Collaborations have been in the areas of curriculum development and course

design, training for students. NASSCOM has been involved in developing

standards for training and recruitment at entry level to make students more

employable. These training address both the technical and soft skills training needs.

k. The top 5 software companies are investing close to USD 430 million in FY08 to

train around 100,000 engineers hired during this period. Companies on an average

111

conduct 163 training programmes annually; with almost 80% spend on training

entry level hires.

l. Promoting higher education: The industry has emphasized upon developing its

workforce by encouraging and aiding up gradation of skills and abilities. It has

done so through various means including provision of scholarships as well as

training and development activities. Many companies have tie-ups with educational

institutes for supporting the higher education needs of their employees and provide

full/partial scholarships thus supporting their career goals. NASSCOM has been

involved in building the talent base for high end skills in areas like multimedia

convergence and bio-informatics while working with the Ministry to develop

institutes that produce highly specialized professionals.

m. Improving the work environment: Improving the work environment: IT/ITES

companies have been taking the lead in providing a conducive work environment

to employees leading to increased productivity and better morale. The facilities

provided focus on health of employees by providing gymnasium; yoga/meditation

facilities as well as their safety through pick and drop facilities. • To cater to the

need of providing a work-life balance, particularly to women employees, 90% of

the companies surveyed offer flexible working hours while 59% offer a work from

home option.

3.11 Road Ahead:

Globalization has had a profound impact in shaping the Indian IT industry with India

capturing a sizeable chunk of the global market for technology sourcing and business 118

Services. Over the years, the growth drivers for this sector have been the verticals of

manufacturing, telecommunication, insurance, banking, and finance and of late, the

fledgling retail revolution. As the new scenario unfolds, it is getting clear that the future

growth of IT and ITeS will be fuelled by the verticals of climate change, mobile

applications, healthcare, energy efficiency and sustainable energy. Traditional business

118

http://www.ibef.org/archives/detail/b3ZlcnZpZXcmMzY2OTgmODk, accessed on 5th

Dec 2014

112

strongholds will make way for new geographies, there would be new customers and more

and more of SMEs will go for IT application and services. As the new scenario unfolds, it

is getting clear that the future growth of IT and ITeS will be fuelled by the verticals of

climate change, mobile applications, healthcare, energy efficiency and sustainable energy.

Traditional business strongholds will make way for new geographies, there would be new

customers and more and more of SMEs will go for IT application and services.

Demand from emerging countries is expected to show strong growth going forward. Tax

holidays are today extended to the IT sector for STPI and SEZs. Further, the country is

providing procedural ease and single window clearance for setting up facilities.

For India to fully capitalize on the opportunity and sustain a disproportionate lead in the

global IT-ITES space, stakeholders need to continue working towards timely and coherent

execution of initiatives to address supply-side concerns across the following areas

1. Augmenting Talent Supply

2. Creating world-class infrastructure

3. Strengthening information security

4. Enhancing operational excellence

5. Providing regulatory support

6. Catalyzing domestic market development

7. Fostering an ecosystem for innovation

Nasscom recently projected that the Indian IT Industry would grow to about $300 billion

by 2020, and would create different verticals that would focus on specific areas such as

domestic IT Market, Software products & e commerce. Incremental revenue is a measure

of market share that has evolved as the new benchmark for the IT sector.

Industry exports expected to reach USD 84-87 billion, with growth rate of 12-14 per cent

Domestic revenues to grow by 13-15 per cent.

SMAC (Social media, Mobility, Analytics, and Cloud) technologies to fuel growth

Future of industry -- a complete blend of services, products, solutions and platforms

Some of the key growth drivers that are expected to open new opportunities for the

industry are smart computing, ‘anything’-as-a-service, technology enablement in emerging

verticals and the SMB market. “Technology can also play a critical role in enabling

113

transformation in India and add to India’s GDP. The domestic market in India is maturing,

it was the fastest growing market in the year and NASSCOM will look to partner with the

government in enhancing technology adoption in the country”,

India is the only country that offers the depth and breadth of offerings across different

segment of this industry – IT Services, BPM, Engineering & R&D, Internet & Mobility

and Software Products. IT Services is a USD 50 billion sector, BPM is a USD 20 billion

sector, Engineering crossed USD 10 billion and Software products, Internet & Mobility are

emerging opportunities with 9 billion. Today, existing and new companies are expanding

their offerings to build India as the hub for analytics, mobility, cloud, social collaboration

and emerging verticals like healthcare and medical devices.

Figure 3.6: Classification of Sector wise earnings

Source: NASSCOM

The growth in the Indian IT industry is expected to be around 30 per cent and the overall

sales are projected to touch US$ 17 billion in FY 15, according to Manufacturers

Association of Information Technology (MAIT).

IT Services, 56%

BPM, 23%

Engineering, 11%

Software Products, 10%

IT Services BPM Engineering Software Products

114

The IT services market in India is expected to grow at the rate of 8.4 per cent in 2014 to Rs

476,356 million (US$ 7.88 billion), according to International Data Corporation (IDC).119

Indian insurance companies plan to spend Rs 117 billion (US$ 1.93 billion) on IT products

and services in 2014, a 5 per cent increase from 2013, as per Gartner.

Indian enterprises are enhancing their IT security operations capabilities across

departments. The Indian market for security infrastructure and services is expected to grow

from US$ 989 million this year to US$ 1.4 billion by 2017, as per Gartner.

Majority of the fortune 500 and Global 2000 corporations are sourcing IT – ITES from

India. A number of reputed companies in electronic / IT / Telecom hardware have setup

their units in the country. India is rapidly becoming an R & D hub.

The contribution of the IT/ITES industry to India’s economy and society has been well

established and is indeed significant. This industry has at its call, the two most important

tools for making this impact, a young motivated work force and technology. Both together

can make a significant impact on improving the lives of the poor. The IT/ITES industry has

made a beginning it is on track to set an example that would encourage others to emulate

and help change the face of India.

3.12 Foreign Trade Policy (2015-20):

The new policy would boost exports and create jobs while supporting the Centre’s 'Make

In India' and 'Digital India' programmes. The broad objective is to focus on support to

services and merchandise exports, number of very important initiatives such as focus on

export of high value addition products, Focussed on improving ease of doing business,

debottlenecking, to make services globally competitive and Market diversification.

Moreover, FTP would focus on defense, Pharma, environment-friendly products and

value-added exports. The govt. will continue to incentivize units located in special

economic zones, with a focus on employment-creating sectors and also promote e-

commerce.

119 http://timesofindia.indiatimes.com/tech/it-services/IT-spending-in-Indian-manufacturing-to-double-by-

2016-IDC/articleshow/15341076.cms

115

By implementing Foreign Trade Policy, FTP 2015-2020, the India’s share in the World

Trade is expected to double from the present level of 3% by the year 2020. By taking

measures for import substitution at one side, the forthcoming Foreign Trade Policy focuses

on increasing exports at the present scenario of increasing current account deficit CAD.

The new FTP includes necessary measures to boost productivity and earn exportable

surplus at competitive rates in exports.120

According to senior Indian Revenue Service officials, the minimum alternate tax (MAT)

was imposed on SEZs because they were not reporting revenue correctly. There were also

cases of export units selling goods in the domestic market and passing these off as exports

to get incentives. Instances of smuggling had also been detected in some jewellery export

units but the commissioners of the SEZs did not allow these cases to be booked under the

more stringent customs act and preferred the SEZ Act instead.

3.13 SEZ Policy:

India was one of the first in Asia to recognize the effectiveness of the Export Processing

Zone (EPZ) model in promoting exports, with Asia's first EPZ set up in Kandla in 1965.

With a view to overcome the shortcomings experienced on account of the multiplicity of

controls and clearances; absence of world-class infrastructure, and an unstable fiscal

regime and with a view to attract larger foreign investments in India, the Special Economic

Zones (SEZs) Policy was announced in April 2000.

This policy intended to make SEZs an engine for economic growth supported by quality

infrastructure complemented by an attractive fiscal package, both at the Centre and the

State level, with the minimum possible regulations. SEZs in India functioned from

1.11.2000 to 09.02.2006 under the provisions of the Foreign Trade Policy and fiscal

incentives were made effective through the provisions of relevant statutes.

120

http://businesstoday.intoday.in/story/new-foreign-trade-policy-to-boost-exports

manufacturing/1/210901.html

116

After extensive consultations, the SEZ Act, 2005, supported by SEZ Rules, came into

effect on 10th February, 2006. The main objectives of the SEZ Act are:

(a) generation of additional economic activity

(b) promotion of exports of goods and services;

(c) promotion of investment from domestic and foreign sources;

(d) creation of employment opportunities;

(e) development of infrastructure facilities;

It is expected that this will trigger a large flow of foreign and domestic investment in SEZs,

in infrastructure and productive capacity, leading to generation of additional economic

activity and creation of employment opportunities.

The SEZ Act 2005 envisages key role for the State Governments in Export Promotion and

creation of related infrastructure.

The SEZ Rules provide for different minimum land requirement for different class of

SEZs.

Table 3.4: SEZs in India

Sr. No SEZ Area

1 SEEPZ Special Economic Zone

2 Kandla Special Economic Zone

3 Cochin Special Economic Zone

4 Madras Special Economic Zone

5 Visakhapatnam SEZ

6 Falta Special Economic Zone

7 Noida Export Processing Zone

Source: www.sezindia.nic.in

117

3.13.1 Importance of SEZ-

The incentives and facilities offered to the units in SEZs for attracting investments into the

SEZs, including foreign investment include:-

a. Duty free import/domestic procurement of goods for development, operation and

maintenance of SEZ units.

b. 100% Income Tax exemption on export income for SEZ units under Section 10AA

of the Income Tax Act for first 5 years, 50% for next 5 years thereafter and 50% of

the ploughed back export profit for next 5 years.

c. Exemption from minimum alternate tax under section 115JB of the Income Tax

Act.

d. External commercial borrowing by SEZ units’ upto US $ 500 million in a year

without any maturity restriction through recognized banking channels.121

e. Exemption from Central Sales Tax.

f. Exemption from Service Tax.

g. Single window clearance for Central and State level approvals.

h. Exemption from State sales tax and other levies as extended by the respective State

Governments.

The Government later imposed a Minimum Alternate Tax (MAT) of 18.5 per cent on the

book profits of SEZ developers and units with effect from April 2012. The concept of

MAT was introduced in 1987 to enable the government to raise revenue from companies

that paid no tax or very little tax. SEZs contribute to about 25 per cent of the country's total

exports. However, SEZ projects are being surrendered as imposition of taxes has

eliminated the incentives

The major incentives and facilities available to SEZ developers include:-

1. Exemption from customs/excise duties for development of SEZs for authorized

operations approved by the BOA.

2. Income Tax exemption on income derived from the business of development of

the SEZ in a block of 10 years in 15 years under Section 80-IAB of the IT Act.

121

www.sezindia.nic.in

118

3. Exemption from minimum alternate tax under Section 115 JB of the IT Act.

4. Exemption from dividend distribution tax under Section 115O of the IT Act.

5. Exemption from Central Sales Tax (CST).

6. Exemption from Service Tax (Section 7, 26 and Second Schedule of the SEZ Act).

Table 3.5: Performance of SEZ

Years Exports Growth over

previous year Value in Rs. Crores Billion USD

2005-2006 22,840 5.08 -

2006-2007 34,615 7.69 52%

2007-2008 66,638 14.81 93%

2008-2009 99,689 22.15 50%

2009-2010 2,20,711 49.05 121%

2010-2011 3,15,868 70.19 43.11%

2011-2012 3,64,478 81.00 15.39%

2012-2013 4,76,159 88.18 31%

2013-2014 4,94,077 82.35 4%

Source: www.sezindia.nic.in

3.14 Industry status in Maharashtra:

Maharashtra is the second largest state in India both in terms of population and

geographical area (3.08 lakh sq. km.). The State has a population of 11.74 crore (Census

2011) which is 9.3 per cent of the total population of India. The State is highly urbanized

with 45.2 per cent people residing in urban areas. Maharashtra is the most industrialized

State and has maintained leading position in the industrial sector in India. The State is

pioneer in Small Scale industries. The State continues to attract industrial investments from

both, domestic as well as foreign institutions. It has become a leading automobile

production hub and a major IT growth centre. It boasts of the largest number of special

export promotion zones.

119

3.14.1 GSDP of Maharashtra-

GSDP at constant (2004-05) prices is 8, 96,768 crores during 2013-14, as against 8, 35,929

crores in 2012-13, showing an increase of 7.3 per cent as per the first revised estimates.

GSDP during 2013-14 at current prices is 15, 10,132 crores, showing an increase of 14.2

per cent over the previous year.

Advance estimates for 2014-15 published by Central Statistics Office (CSO), GoI revealed

that GDP at constant (2004-05) prices is expected at 1, 06, 06, 476 crores with a growth of

5.0 per cent, whereas at current prices is expected at ` 1, 26, 53,762 crores

Since August, 1991 to October 2014, in all 18,709 industrial proposals with an

Investment of 10, 63,342 crore were approved. Out of these 8,376 projects (44.8 per cent)

with an investment of 2, 54,784 crore (23.9 per cent) with proposed employment of 10.95

lakh were commissioned and 2,115 projects with an investment of ` 88,086 crore &

proposed employment of 3.03 lakh are under execution.

The IT industry has attracted 441 proposals with highest investment of 3, 82,766 crore

(36 per cent), followed by fuel industry with an investment of 1, 42,283 crore (13.4 per

cent).These two industries accounted for almost 50 per cent of the total approved

investment.

Information Technology (IT) Policy, aims to make Maharashtra the most favored

destination for investments in the IT and ITES industry. This is intended to be achieved by

directing the State support at opening up large scale employment opportunities, facilitating

growth of skilled and globally employable man-power, unprecedented spurt in exports,

creating hassle-free and industry-friendly working environment, associating urban local

Governments as responsive key stakeholders in promoting business and enterprise in the IT

industry, and providing a legal framework for data protection and consumer privacy. The

policy aims to achieve the following:-

Promotion of public and private IT Parks; Cost effective and fully reliable telecom

connectivity to the IT & ITES units all over the State; Excellent road connectivity from

main Highways to the IT Parks; Permission to developers of IT Parks to invest funds to

construct connecting roads from highways to IT Parks; Ensuring reliable and quality power

120

supply round the clock in IT Parks by permitting unlimited back up power and captive

power generation; Levying power charges on IT and ITES units at industrial rates;

Exemption of IT & ITES units from statutory power cuts in power supply, etc.

3.14.2 FDI in Maharashtra-

Since August, 1991 to March, 2012, in all 4,246 Foreign Direct Investment (FDI) projects

(20,643 at all-India level) amounting to 97,799 crore (`4, 25,811 crore at all-India level)

were approved. Of these, 45 per cent were commissioned and 10 per cent are under

execution with a share of investment of 51 per cent & eight per cent respectively. During

2011-12, in all 105 FDI projects with an investment of ` 5,454 crore were approved. The

United States of America & Mauritius are the two prominent countries investing in

industrial sector of the State with 14 and 13per cent share respectively in total FDI.

Below are industry group wise approved FDI projects since Aug 91 to October 2014.122

Table 3.6: Industry wise approved FDI projects in Maharashtra

Industry Type No. Investment in Crore

IT Industry 762 12765

Financial Services 667 11858

Hotel & Tourism Industry 95 6326

Business Management Consultancy 369 4962

Transportation 108 4124

Cements & Ceramics 58 3727

Power & Fuel 39 2841

Total 4,246 97,799

Source: Economic Survey of Maharashtra 2014-15,*List is indicative

122 Economic Survey of Maharashtra 2014-15

121

3.14.3 Special Economic Zones in Maharashtra-

The State has adopted the Special Economic Zone (SEZ) policy with effect from February,

2006 to boost the economic growth. The State has received 236 SEZ proposals up to

December, 2014. Of these, 124 SEZs were approved by the Central Government (formal

approval 104 and in-principle approval 20) and 66 of them are notified. As on 31st

December 2014, twenty four SEZs were executed with total investment of 18,786 crore on

area of 3,059 ha. which generated employment of about 1.31 lakh. The division wise

approved and notified SEZs are given in Table (Up to December 2014)

Table 3.7: Approved and notified SEZs

Division No. of SEZ Proposed Employment (*Lakhs)

Approved Notified Executed Approved Notified Executed

Konkan 61 29 5 35.87 9.84 .46

Pune 36 21 14 10.63 6.17 0.83

NAshik 6 1 0 2.12 1.25 0

Aurangabad 11 7 3 1.37 0.31 0.01

Amaravati 3 3 0 0.40 0.40 0

Nagpur 7 5 2 5.46 3.92 0.01

Total 124 66 24 55.85 21.89 1.31

Source: Directorate of Industries, GoM, http://www.sezindia.nic.in/index.asp

3.14.4 Public & Private IT Parks -

Considering Maharashtra’s strengths in terms of human resources, connectivity and

infrastructure, and the special significance of Information Technology (IT) for generating

employment, increasing efficiency and improving the quality of life, the State Government

announced its first IT Policy in 1998. These Policies have been highly successful.

Maharashtra Industrial Development Corporation (MIDC) and CIDCO have developed 37

public IT parks. For getting private participation in creating world-class infrastructure for

IT industry, 479 private IT parks have been approved, out of which 144 have started

122

functioning with an investment of `3332 crore, and proposed employment of about 4.44

lakh. The remaining 321 IT parks with proposed investment of ` 8,955 crore have been

given Letter of Intent and are expected to generate 11.94 lakh employment opportunities.

The private IT parks are located in Pune (166) followed by Greater Mumbai (158), Thane

(128), Nagpur (5), Nasik (4), Aurangabad (3) and Wardha (1) districts.

During 2014-15, total 15 private IT parks were approved. Since the 2003 Policy, IT exports

from Maharashtra have increased by 135%, positioning Maharashtra among the top three

States. The growth rate of FDI in the State’s IT sector has been the highest in the country.

3.14.5 Exports from Maharashtra-

The main products exported from the State are gems & jewellery, software, textiles,

readymade garments, cotton yarn, metal & metal products, agro-based products,

engineering items, drugs & pharmaceuticals and plastic & plastic items. To recognize the

efforts put up by the exporters and to boost the exports, the State is taking initiatives like

giving awards based on export performance and implementing space rent subsidy scheme

for Small Scale Industries for participation in international exhibitions. Since 2007-08, the

State’s share remained at 27 per cent in the total exports from India.123

Table 3.8 Exports from the State and India

Source: Directorate of Industries, GoM *Till October 2014, Economic Survey of Maharashtra, 2014-2015

123

Directorate of Industries, GoM,Economic Survey of Maharashtra, 2014-2015

Year Maharashtra India

2009-2010 2,28,184 8,45,125

2010-2011 3,08,515 11,42,649

2011-2012 3,94,005 14,59,280

2012-2013 4,17,626 15,46,7666

2013-14* 2,88,384 10,68,089

123

3.15 Pune as an emerging IT hub:

NASSCOM, the apex industry body of Software and Service Companies in India, today,

revealed the findings of an extensive study conducted in association with Netscribes to

assess the competitiveness of nine Indian cities as destinations for IT Enabled Service

companies. The three-month long study evaluated the top nine cities including Ahmedabad,

Bangalore, Chennai, Hyderabad, Kolkata, Kochi, Mumbai (including Navi Mumbai), Pune

and NCR (Delhi, Noida and Gurgaon). The cities were assessed on factors such as

manpower availability, real estate, telecom infrastructure, policy initiatives, power

infrastructure, city perception and entrepreneurial history.

Table 3.9: Ranking of Indian IT Cities

CITY RANK

HYDERABAD 1

KOCHI 2

CHENNAI 3

KOLKATA 4

AHMEDABAD 5

BANGALORE 6

MUMBAI 7

NCR 8

PUNE 9

Source: NASSCOM releases findings of "Super Nine" Indian ITES Destinations.

Speaking on the study, Mr. Kiran Karnik, President, NASSCOM, said, "About 90% of all

ITES companies in India are concentrated in nine major cities while others have not been

able to attract more than two companies each. Our study reveals that despite a large number

of ITES companies being based in Mumbai, NCR and Bangalore, these cities are facing

increasing competition from other cities. Cities such as Hyderabad, and Kochi are

emerging as attractive ITES destinations primarily due to rapid improvements in

124

infrastructure (power, international bandwidth and urban transportation) and lower

manpower costs due to lower cost of living and lack of alternative employment