3 mo treasury yield borrowing costs dow industrials ny times 18 sept 2008 front page

Post on 20-Dec-2015

214 views

TRANSCRIPT

3 mo treasury yield

borrowing costs

Dow industrials

NY Times

18 Sept 2008

front page

Stat 153 - 16 Sept 2008 D. R. Brillinger

Chapter 3

mean function

)]([)( tXEt

variance function

)]([)(2 tXVart

autocovariance

)(),((),(2121

tXtXCovtt

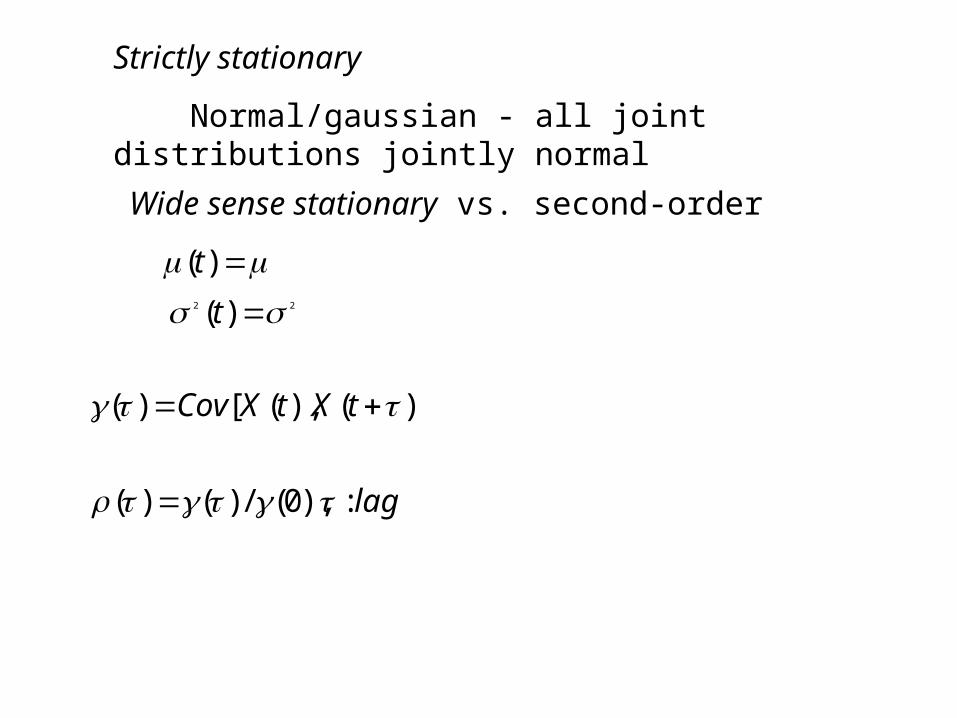

Strictly stationary

Normal/gaussian - all joint distributions jointly normal

Wide sense stationary vs. second-order

)(t22 )( t

)](),([)( tXtXCov

lag:),0(/)()(

Properties of autocovariance

)()(

1|)(|

Useful models

Purely random

Building block

0 ,0

0 ,1)(

k

kk

,...2/,1/ ,0

0 ,),()( 2

k

kZZCovk Zktt

Random walk

not stationary

0, 01 XZXX ttt

tXE t )(

2)( Zt tXVar

randompurelyZXXX tttt ,1

t

iit ZX

1

*

)()( )( YbEXaEbYaXE

)(),(2)( )( 22 YVarbYXabCovXVarabYaXVar

),(),(),(),(

),(

VYbdCovUYbcCovVXadCovUXacCov

dVcUbYaXCov

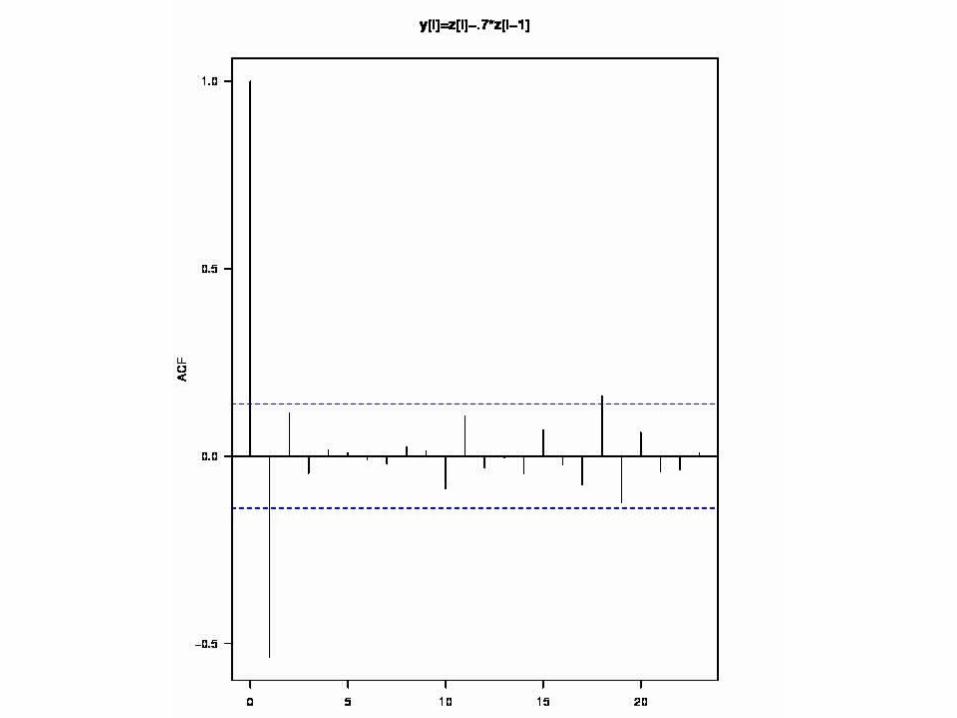

Moving average, MA(q)

qtqtttt ZZZX ...110

otherwise

k

kkMA

,0

1/ ),1/(

0 ,1)( ).1(2

11

From *

0)( ,0)( tt XEZEIf

stationary

)(

,...,1,0 ,

,0

)(

0

2

k

qk

qk

k

kq

ikiiZ

Backward shift operator

Linear process. )(MA

jtt

j XXB

0iitit ZX

Need convergence condition

q

q

t

q

q

tt

BBB

ZBB

ZBX

qMA

...)(

)...(

)(

)(

10

10

autoregressive process, AR(p)

first-order, AR(1) Markov

Linear process

For convergence/stationarity

1||

tt

tptptt

ZXB

ZXXX

)(

...11

ttt ZXX 1

...

)(

2

2

1

21

ttt

tttt

ZZZ

XZZX

*

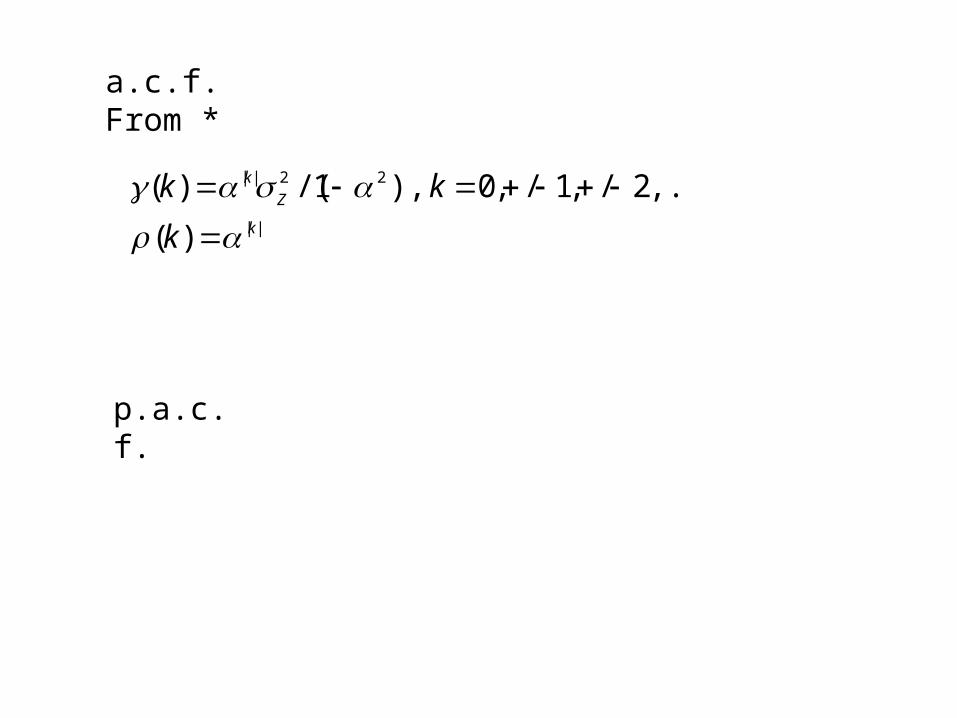

a.c.f. From *

||

22||

)(

,...2/,1/,0 ),1/()(k

Z

k

k

kk

p.a.c.f.

In general case,

Very useful for prediction

tptptt ZXXX ...11

tystationarifor 1||in 0(z) of roots need

)(

z

ZXB tt

ARMA(p,q)

)()( tt ZXB

qtqtttptptt ZZZXXX ...... 11011

ARIMA(p,d,q).

stationary is t

d X

0)ARIMA(0,1,

)1(

walkRandom

1

tt

ttt

ZX

XBXX

Yule-Walker equations for AR(p).

Correlate, with Xt-k , each side of

tptptt ZXXX ...11

0 ),(...)1()( 1 kpkkk p

For AR(1)

0 ),0()( kk k