2q12 and 1h12 results conference call presentation

TRANSCRIPT

Strategic

Plan

Investor Relations

Villa Flora - Sumaré – São Paulo

Rossi is already in a process to close offices in many cities and to reduce the team in the headquarter. Savings are

expected to be concluded by 2013

The closing of offices will save R$26 million in 2013

Savings in the headquarter should be R$32 million in 2013

Rossi Vendas, in-house sales team, should be responsible for almost 90% of Rossi’s sales from 52%, currently

The new sales structure are expected to increase Rossi’s EBITDA margin;

As a result of the new strategy, by 2015, gross margin are expected to go up 4.5pp and margin EBITDA by 3.5pp (in

addition to fixed expenses dilution)

Focus in large cities and metropolitan regions:

In 3 years, home builder partners are expected to represent 10% of Rossi’s projects from 37% currently, while

developers should represent 5% Rossi’s projects from 55% currently

The reduction of home builder partners should increase gross margin by 2pp in a 3-year period and the reduction of

development partners should increase EBITDA margin by 0.5pp in the same period

Home builder and development partners

Geographic footprint

Rossi Vendas

G&A expenses

Summary

Rossi has two businesses under development: Rossi Commercial Properties and Rossi Urbanizadora

− Rossi Commercial Properties is focused on developing regional, neighborhood, convenience and strip mall

opportunities in Brazil (17 projects already in-house)

− Rossi Urbanizadora is focused in the development of unifamily and multifamily lots (the company has a landbank of

19,250,677 m2)

Each business should unlock R$ 500 million – R$ 700 million of value, in addition to increase Rossi’s profitability

New businesses

Rossi’s strategy

Participation of homer builder partners in Rossi’s launches per year Participation of development partners in Rossi’s launches per year

37.3%

7.4%7.4%5.7%

5.5%

4.8%

3.2%3.1%2.2%2.2%1.9%

16.0%

1.5%1.9%

Rossi

Eixo-M

Even

Capital

Tha Engenharia

Diagonal

Lindenberg

Scon

R. Yazbek

Costa Andrade

Larivoir

Cychorp

Norcon

Others

55.1%

7.4%

3.2%3.2%

3.0%2.8%2.2%2.2%1.9%1.9%

15.9%

1.5%

Rossi

Even

Diagonal

Lindencorp / PDG

Edinpe Quartier

GNO

Paulo Octavio

Costa Andrade

Larivoir

Capital / GRM

Cádiz

Others

Rossi’s partners in historical home building projects (cont’d)

Participation of home builders in Rossi’s current projects Participation of developers in Rossi’s current projects

36% 49%

74% 82%

64% 51%

26% 18%

2009 2010 2011 2012

Rossi Third parties

78% 70% 78% 68%

22% 30% 22% 32%

2009 2010 2011 2012

Rossi Developers

80% 90%

20% 10%

Current Future

Rossi Home builders

85% 95%

15% 5%

Current Future

Rossi Developers

Rossi’s partners in future projects

Home building partners: Current vs future scenario Developing partners: Current vs future scenario

In future projects partners are expected to represent just 10% of home building projects from 37% currently, while developers should

represent 5% Rossi’s projects from 55% currently

– Home builder partners: Thá, Capital, Norcon, Toctao, and GNO

– Development partners: Capital, Toctao, and Norcon

Strategy

In 3 years, home builder partners are expected to represent 10% and developers are expected represent 5% of VGV Timing

The reduction of home builder partners could increase gross margin by 2pp in a 3-year period and the reduction of development

partners could increase EBITDA margin by 0.5pp in the same period

Financial benefit

Rossi’s geographic footprint

Focus in large cities and metropolitan regions

Strategy

After the 2H12, Rossi should launch projects in the expected geographic footprint presented below. However, because the Company has

ongoing projects in the other cities/regions, only after 2014, 100% of Rossi’s projects should be located in the expected geographic

footprint

Timing

The projects located in the cities where Rossi does not plan to continue its activities had a gross margin of 18.5%, on average. Those

projects are expected to represent 30% of 2012 gross margin. The projects located in the expected geographic footprint have a gross

margin of 30%, on average. Therefore, in 2014, gross margin should increase by 2.5pp.

Financial benefit

52.4%

11.1%

3.0%

6.4%

18.4%

1.8%0.7%

4.3%

1.2%0.8%

Rossi Vendas

Lopes

Decide

Brasil Brokers

Global Consult

Patrimóvel

Even

Beiramar

Eduardo Feitosa

Others

Rossi’s brokers

Rossi Vendas, in-house sales team, should be responsible for almost 90% of Rossi’s sales

Strategy

Due to current agreements with brokers, it should take 16 months for Rossi Vendas to be responsible for 90% of Rossi’s sales Timing

The new sales structure could increase Rossi’s EBITDA margin by 1pp Financial benefit

Broker partners in 1H12 Broker partners: Current vs future scenario

52.4%

90%

47.6%

10.0%

Current Future

Partners Rossi Vendas

(R$ million)

Reduction on G&A expenses

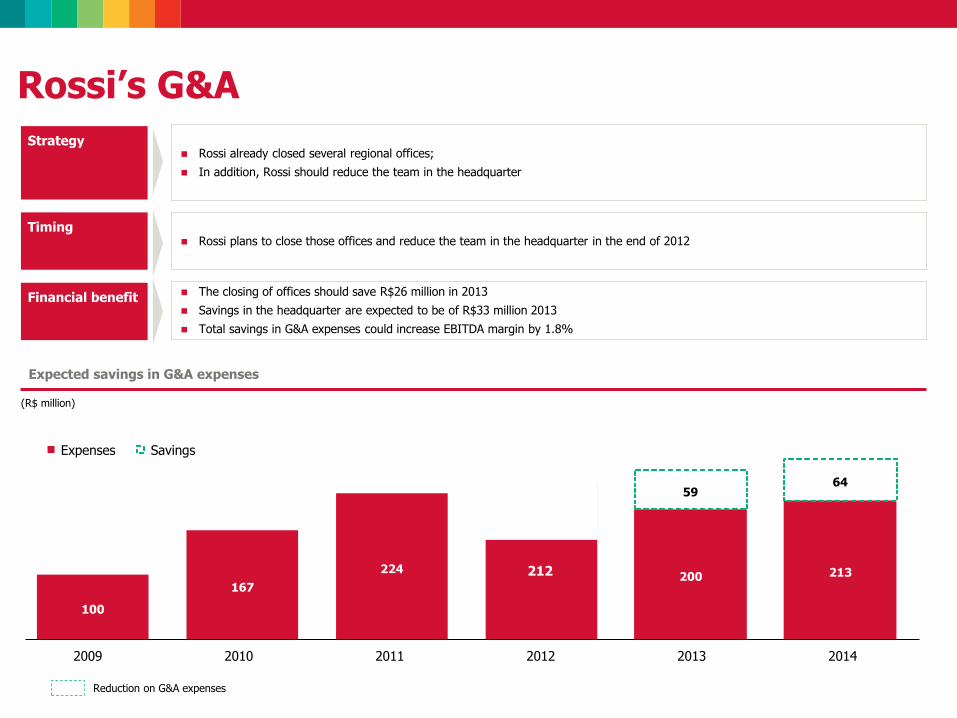

Rossi’s G&A

Rossi already closed several regional offices;

In addition, Rossi should reduce the team in the headquarter

Strategy

Rossi plans to close those offices and reduce the team in the headquarter in the end of 2012 Timing

The closing of offices should save R$26 million in 2013

Savings in the headquarter are expected to be of R$33 million 2013

Total savings in G&A expenses could increase EBITDA margin by 1.8%

Financial benefit

Expected savings in G&A expenses

2009 2010 2011 2012 2013 2014

Savings Expenses

100

167

224 241 200 213

59 64

212

RS

SC

PR

SP

MG

GO

MT

AC

AM

RR

RO BA

PI

MA PA

AP

TO

CE RN

PE

AL SE

MS

RJ

ES

DF

PB

17 Projects

169 mil m2 in GLA

9 States

RCP is focused on developing regional, neighborhood, convenience

and strip mall opportunities in Brazil

17 Projects “Already in-House” with total GLA of 169 mil m²

– Operates under 4 different formats:

– Focus on convenience consumption

– Neighbourhood Malls

– Shopping Canters

– Retail Mixed-Use Projects (combines residential and commercial

developments)

Access to Rossi nationwide landbank , with strong pipeline of projects

Proven track record in development and construction

Right of first refusal on Rossi landbank with retail potential

Financing facility already secured at attractive conditions

– R$750mm (US$480mm) already negotiated to leverage

80% of the projects Capex

4,150 2.5%

25,000 14.9%

20,184 12.1%

24,980 14.9%

63,058 37.7%

10,000 6.0%

2,000 1.2%

11,000 6.6%

7,068 4.2%

Rossi Commercial Properties Current Portfolio of Projects Overview

Canoas – RS

Ulbra

Goiânia – GO

Fazenda Oriente

Campinas – SP

3 Pontes do Atibaia | Garnero

Gleba A2 Haras Patente

Pau D’Alho USF

Região dos Lagos

Santana de Parnaíba – SP

Paio Velho

Cotia – SP

Cotolengo

Belo Horizonte – MG

Granja Werneck

Itaboraí – RJ

Villa Flora Itaboraí

Samambaia – DF

Bom Sucesso

Rossi Urbanizadora Current Portfolio of Projects Overview

Development of unifamily and multifamily lots

Nationwide structured portfolio

Landbank of 19,250,677 m2

Experienced and qualifed team

Rossi has proven track record of excelence:

Vila Flora Sumaré (Campinas – SP):

– Total landbank: 791,853 m2

– Area for lots: 475,112 m2

– # of units: 3,500

– Launch year: 1999

Vila Flora Votorantim (Campinas – SP):

– Total landbank: 465,610 m2

– Area for lots: 264,153 m2

– # of units: 1,322 houses and 470 apartments

Rossi Central Park (Porto Alegre – RS):

– Total landbank: 300,000 m2

– Launches: 246 commercial units, 742 apartments, 44 houses

10 10 10

Financial

Performance

Rossi Mais Reserva Especial | Belo Horizonte – BH

676

795

1.273

1.626

2T11 2T12 1S11 1S12

+18%

+28%

110

207188

374

2Q11 2Q12 1H11 1H12

+88%

+99%

28

51 53

114

2Q11 2Q12 1H11 1H12

+113%

+85%

188

233

350

488

2Q11 2Q12 1H11 1H12

+24%

+40%

Financial Highlights

11

Net Revenues (R$ million) Gross Income (R$ million) and Gross Margin (%)

EBITDA (R$ million) and EBITDA Margin (%) Net Income (R$ million) and Net Margin (%)

28%

29%

27%

30%

16%

26% 15%

23%

4%

6% 4%

7%

Construction

Financing

56%

Debentures

22%

Receivables

Securitization

12%

Working Capital

10%

Short Term38%

Long Term62%

12

Indebtness

Total Debt

Debt Breakdown Debt Profile

Strong cash position of R$ 1.3 billion (61% of Shareholders' Equity);

56% of debt is construction financing;

62% with long term maturity;

R$ million 2Q12 1Q12 Chg (%)

Short Term 1.650 1.508 9%

Construction Financing 628 588 7%

Working Capital 288 193 49%

Receivables Securitization 512 592 -14%

Debentures 221 135 64%

Long Term 2.691 2.525 7%

Construction Financing 1.804 1.640 10%

Working Capital 137 35 290%

Debentures 750 850 -12%

Total debt 4.341 4.033 8%

Cash and Cash Equivalents 1.259 1.300 -3%

Net Debt 3.082 2.733 13%

Net Debt / Shareholder´s Equity 148,5% 133,5% 15,0 p.p.

Net Debt Variation 349

(-) Dividends (83)

(-) Buyback Program (52)

Operating Cash Burn 214

675

1.1451.110

508

209

13

R$ 189.0 million Value R$ 440.1 million

Accounting nature

Reclassification Reclassification

Previously

Revenues used to be recognized through

the segregation between land and

development with different margins for

each item at different times

This practice usually led to a faster

recognition of its revenues

The sale of interests in certain subsidiaries

was initially booked at shareholders' equity

balance

Now

The Company had changed its policy so

that the revenue recognition revenue and

earnings per project now reflect the same

time of recognition and margin for land

and development of the same project

After detailed analysis of certain transactions

involving the sale of interests in certain

subsidiaries, the Company concluded that

the funds received had characteristics of

liabilities and not necessarily the sale of

equity investments, as originally formalized

Future impact

Management estimates that the negative

effect of this adjustment will be reversed

over the next 18 months, as the current

projects are concluded and their

respective revenues are recognized in

accordance with the new accounting

policy

The Administration estimates that the

negative effect of such adjustments will be

reverted over the next 24 months as such

projects are completed

Revenues Recognition Transaction with partner

R$ 105.1 million

Write-off

Initially, all Rossi’s projects were

considered as a collateral for the

issued debentures

The management of the Company

reviewed the allocation and

amortization practice for the

capitalized interest of the projects

that were financed with funds

obtained from third parties

Such adjustment shall not have any

future impact over the Company's

profit margins or cash equivalents

Interest Expenses

Accounting Adjustments

105

189

440

(19)

610

Interest Expenses Partner Revenues Good Will Accounting revision

14

Sum up of adjustments

(R$ million)

Value estimated of adjustements in Rossi’s financials

Write-off Accounting revision

Will be reverted back to the financial statements over the next 18 months as the projects under development are concluded

15

Equipe de RI

Thank You!

Equipe de RI Tel. (55 11) 4058-2502 [email protected] www.rossiresidencial.com.br/ri

16 16 16

Q&A