25th tax executive workshop - tax legislative and irs update€¦ · herein is prohibited and is in...

TRANSCRIPT

Tax legislative and IRS update

Michael Mundaca

Heather Maloy

Ray Beeman

Page 1

Disclaimer

► EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global

Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young

Global Limited operating in the US.

► This presentation is © 2018 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced,

transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying,

facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written

permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material

herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability

in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are those of the speakers and do not necessarily represent the views of

Ernst & Young LLP.

► This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax

advice to any taxpayer because it does not take into account any specific taxpayer’s facts and circumstances.

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting

advice.

Page 2

Tax legislative and policy update

Page 3

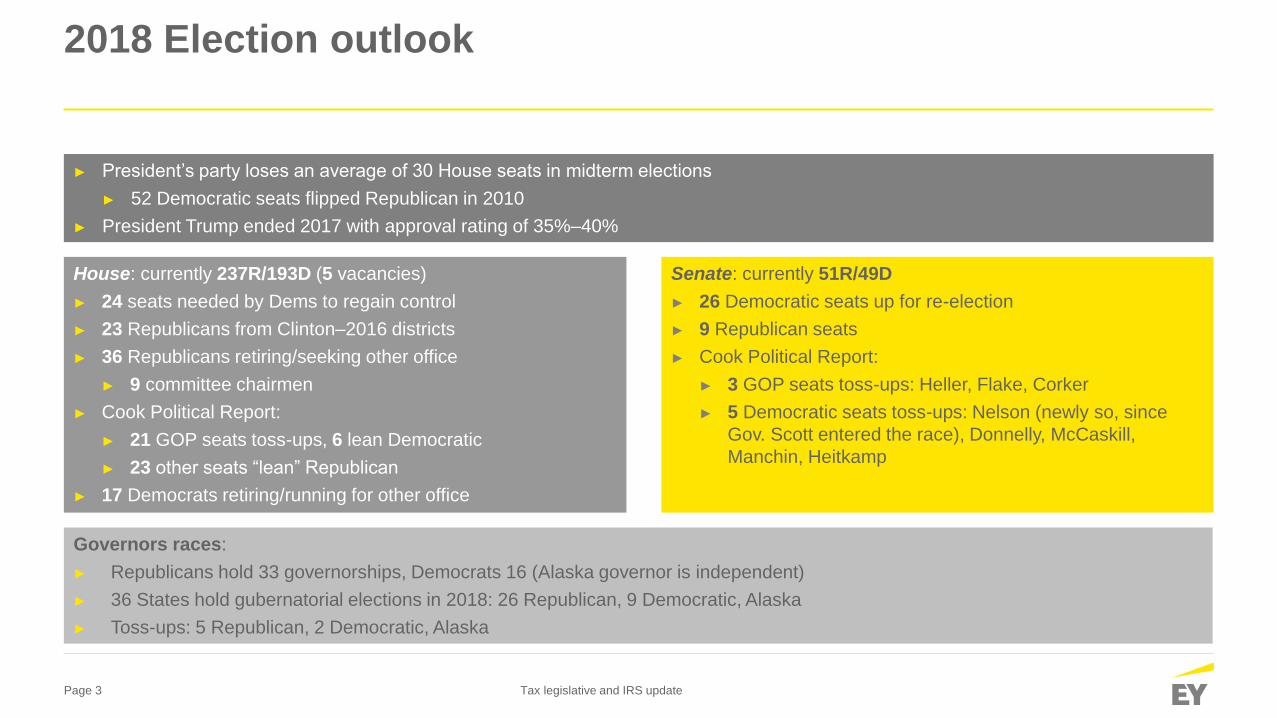

2018 Election outlook

► President’s party loses an average of 30 House seats in midterm elections

► 52 Democratic seats flipped Republican in 2010

► President Trump ended 2017 with approval rating of 35%–40%

House: currently 237R/193D (5 vacancies)

► 24 seats needed by Dems to regain control

► 23 Republicans from Clinton–2016 districts

► 36 Republicans retiring/seeking other office

► 9 committee chairmen

► Cook Political Report:

► 21 GOP seats toss-ups, 6 lean Democratic

► 23 other seats “lean” Republican

► 17 Democrats retiring/running for other office

Senate: currently 51R/49D

► 26 Democratic seats up for re-election

► 9 Republican seats

► Cook Political Report:

► 3 GOP seats toss-ups: Heller, Flake, Corker

► 5 Democratic seats toss-ups: Nelson (newly so, since

Gov. Scott entered the race), Donnelly, McCaskill,

Manchin, Heitkamp

Governors races:

► Republicans hold 33 governorships, Democrats 16 (Alaska governor is independent)

► 36 States hold gubernatorial elections in 2018: 26 Republican, 9 Democratic, Alaska

► Toss-ups: 5 Republican, 2 Democratic, Alaska

Tax legislative and IRS update

Page 4

Members not running for re-election in 2018

Senators Orrin Hatch (R-UT), Bob Corker (R-TN), Jeff Flake (R-AZ)

House

members

retiring

Republicans:

Committee Chairmen

► Rodney Frelinghuysen (R-NJ), Appropriations

► Bob Goodlatte (R-VA), Judiciary

► Trey Gowdy (R-SC), Oversight

► Gregg Harper (R-MS), Administration

► Jeb Hensarling (R-TX), Financial Services

► Ed Royce (R-CA), Foreign Affairs

► Bill Shuster (R-PA) Transportation & Infrastructure

► Lamar Smith (R-TX), Science, Space & Tech

► Joe Barton (R-TX)

► Ryan Costello (R-PA)

► Charlie Dent (R-PA)

► John Duncan (R-TN)

► Darrell Issa (R-CA)

► Lynn Jenkins (R-KS)

► Sam Johnson (R-TX)

► Frank LoBiondo (R-NJ)

► Patrick Meehan (R-PA)

► Tim Murphy (R-PA)

► Ted Poe (R-TX)

► Dave Reichert (R-WA)

► Tom Rooney (R-FL)

► Ileana Ros-Lehtinen (R-FL)

► Dave Trott (R-MI)

Democrats:

► Bob Brady (D-PA)

► Elizabeth Esty (D-CT)

► Gene Green (D-TX)

► Luis Gutiérrez (D-IL)

► Ruben Kihuen (D-NV)

► Sander Levin (D-MI)

► Rick Nolan (D-MN)

► Carol Shea-Porter (D-NH)

► Niki Tsongas (D-MA)

House

members

running for

other office

Republicans:

► Diane Black (R-TN), governor – former Budget

Chairman

► Ron Desantis (R-FL), governor

► Raul Labrador (R-ID), governor

► Kristi Noem (R-SD), governor

► Steve Pearce (R-NM), governor

► Jim Bridenstine (R-OK), nominated for NASA

administrator

► Lou Barletta (R-PA), Senate

► Marsha Blackburn (R-TN), Senate

► Evan Jenkins (R-WV), Senate

► Martha McSally (R-AZ), Senate

► Luke Messer (R-IN), Senate

► Jim Renacci (R-OH), Senate

► Todd Rokita (R-IN), Senate

Democrats:

► Colleen Hanabusa (D-HI), governor

► M. Lujan Grisham (D-NM), governor

► Beto O’Rourke (D-TX), Senate

► Jared Polis (D-CO), governor

► Tim Walz (D-MN), governor

► Jacky Rosen (D-NV), Senate

► Kyrsten Sinema (D-AZ), Senate

► John Delaney (D-MD), president

Tax legislative and IRS update

Page 5

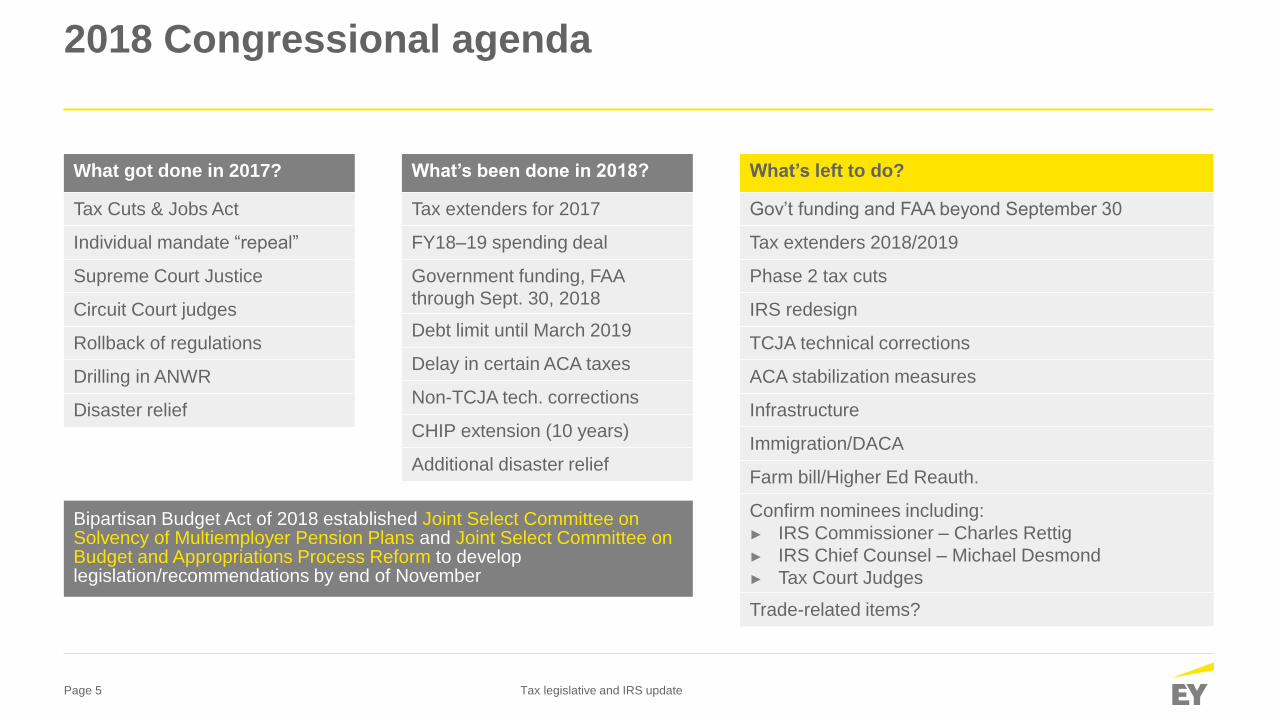

2018 Congressional agenda

What got done in 2017?

Tax Cuts & Jobs Act

Individual mandate “repeal”

Supreme Court Justice

Circuit Court judges

Rollback of regulations

Drilling in ANWR

Disaster relief

What’s been done in 2018?

Tax extenders for 2017

FY18–19 spending deal

Government funding, FAA

through Sept. 30, 2018

Debt limit until March 2019

Delay in certain ACA taxes

Non-TCJA tech. corrections

CHIP extension (10 years)

Additional disaster relief

What’s left to do?

Gov’t funding and FAA beyond September 30

Tax extenders 2018/2019

Phase 2 tax cuts

IRS redesign

TCJA technical corrections

ACA stabilization measures

Infrastructure

Immigration/DACA

Farm bill/Higher Ed Reauth.

Confirm nominees including:

► IRS Commissioner – Charles Rettig

► IRS Chief Counsel – Michael Desmond

► Tax Court Judges

Trade-related items?

Bipartisan Budget Act of 2018 established Joint Select Committee on Solvency of Multiemployer Pension Plans and Joint Select Committee on Budget and Appropriations Process Reform to develop legislation/recommendations by end of November

Tax legislative and IRS update

Page 6

‘Tax Cuts and Jobs Act’ – overview of top provisions

► Seven brackets; 10%, 15%, 22%, 25%, 32%, 35%, 37%

► Standard deduction set at $24k for joint returns, $12k for single filers;

personal exemptions repealed

► Net capital gains and qualified dividends retain current law; subject to 3.8%

net investment income tax

► Individual AMT retained; exemption amount increased; phase out of

exemption increased

► Estate tax exclusion increased to $10m

► Child tax credit increased to $2k, $1,400 refundable; phase out increased

to $200k (single) and $400k (married filing jointly)

► Principal cap on deductible home mortgage interest for new mortgages

(after 12/15/17) reduced from $1m to $750k; deduction retained for second

homes, but no longer available for home equity lines

► Itemized deductions subject to 2% floor repealed

► Medical expense deduction would apply to expenses that exceed 7.5% of

AGI in 2017 and 2018 and expenses that exceed 10% of AGI thereafter

► 50% AGI limitation for charitable contributions increased to 60% for gifts of

cash to specified organizations

► State and local deduction available for $10k of property and income (or

sales) taxes

► ACA “shared responsibility payment” reduced to $0

Top individual provisions

► 21% corporate rate, beginning 2018; AMT repealed

► 20% deduction for domestic “qualified business income” from a

partnership, S corporation, or a sole proprietorship

► Limits interest deduction to 30% of earnings before interest, tax,

depreciation and amortization (EBITDA) for four years, thereafter 30% of

earning before interest and tax (EBIT); worldwide debt limit removed

► Bonus depreciation increased from 50% to 100% for “qualified property”

placed in service after 9/27/17; starting in 2023 phase-down of 20% for five

years

► Expands definition of covered employee for purpose of compensation

deduction limits (§162(m))

► Establishes exemption for dividends received by US corporations from

10%-owned foreign corporations

► Transition tax on deferred foreign earnings: 15.5% (cash)/8% (non-cash)

► New broad-based anti-deferral provision taxes global intangible low-taxed

income (GILTI) on a current basis at 10.5% effective tax rate (some FTCs

available)

► New deduction for “foreign-derived intangible income”

► Minimum tax of 10% (5% transition rate in 2018) applied on income

determined after adding back deductible payments made to related foreign

persons

Top business provisions

Tax legislative and IRS update

Page 7

Expiration dates of various tax provisions

Provision 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Individual rate cuts

21% corporate rate

20% pass-through deduction

100% expensing – effective 9/27/17

Individual AMT exemption amount

Corporate AMT repeal

Interest deduction 30% of EBITDA

Amortization of R&D expense

Estate tax doubled exemption

$10,000 State & local deduction

Alcohol tax modernization

Medical deduction 7.5%/AGI floor

More than two dozen extenders

Other extenders: CFC look-through, NMTC, WOTC

(EBIT after 2021)

10% after 2019

ACA taxes 2018 2019 2020 2021 2022

Cadillac tax

Device tax

HIT

Tax legislative and IRS update

Page 8

“Tax Cuts and Jobs Act” by the numbers: tax cuts vs. increases, total cost

0

500

1000

1500

2000

2500

3000

3500

4000

Business International Individual

Tax cuts Tax increases

$1.555t

$901b

Net total = -$654b Net total = $324b

$294b

$618b

Net total = -$1.121t

$3.648t

$2.527t

$b

Net total cost $1.456t

- Economic growth* $385b

= $1.017t

$1.456t

$385b

Conventional score

Macroeconomic effects

Total Cost

*JCX-69-17

Tax legislative and IRS update

Page 9

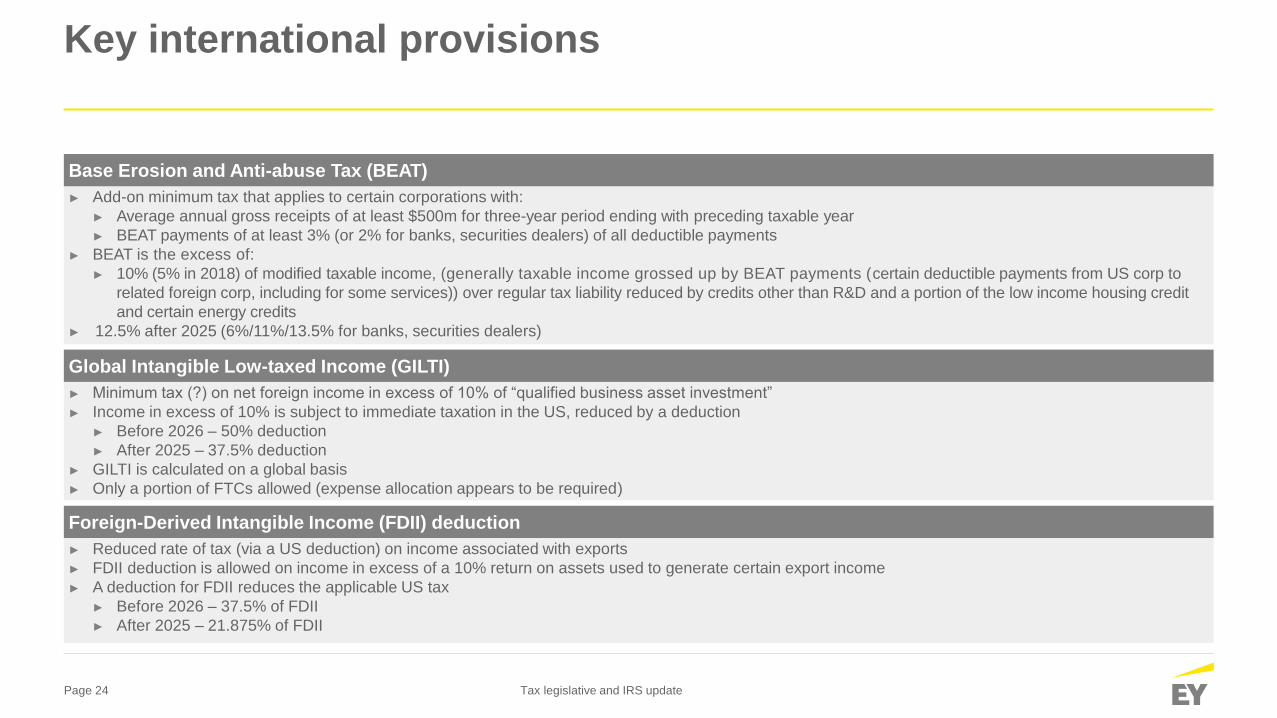

Key international provisions

► Add-on minimum tax that applies to certain corporations with:

► Average annual gross receipts of at least $500m for three-year period ending with preceding taxable year

► BEAT payments of at least 3% (or 2% for banks, securities dealers) of all deductible payments

► BEAT is the excess of:

► 10% (5% in 2018) of modified taxable income, (generally taxable income grossed up by BEAT payments (certain deductible payments from US corp to

related foreign corp, including for some services)) over regular tax liability reduced by credits other than R&D and a portion of the low income housing credit

and certain energy credits

► 12.5% after 2025 (6%/11%/13.5% for banks, securities dealers)

Base Erosion and Anti-abuse Tax (BEAT)

► Minimum tax (?) on net foreign income in excess of 10% of “qualified business asset investment”

► Income in excess of 10% is subject to immediate taxation in the US, reduced by a deduction

► Before 2026 – 50% deduction

► After 2025 – 37.5% deduction

► GILTI is calculated on a global basis

► Only a portion of FTCs allowed (expense allocation appears to be required)

Global Intangible Low-taxed Income (GILTI)

► Reduced rate of tax (via a US deduction) on income associated with exports

► FDII deduction is allowed on income in excess of a 10% return on assets used to generate certain export income

► A deduction for FDII reduces the applicable US tax

► Before 2026 – 37.5% of FDII

► After 2025 – 21.875% of FDII

Foreign-Derived Intangible Income (FDII) Deduction

Tax legislative and IRS update

Page 10

EU reaction to US tax reformSummary of EU concerns

► In summary, at this point the concerns of the EU focus on the BEAT and FDII provisions. The arguments raised are

basically the following:

► BEAT: “Base Erosion and Anti-abuse Tax could give rise to discrimination and incompatibility with WTO rules”:

► It would not allow a credit of foreign taxes paid.

► It could impact on genuine commercial arrangements and lead to double taxation of the same payments, notably in the finance

industry.

► Moreover, it could impact intra-group payments which are necessary for the financial sector to comply with financial stability

requirements (e.g., interest on TLAC debt in the banking industry).

► FDII: “Deduction for foreign derived intangible income would apply the preferential tax treatment to a broader range of

intellectual property than other internationally accepted regimes”.

► It appears that the preferential tax treatment would also be given to intellectual property that was initially created outside the US.

► Could be contrary to the OECD Base Erosion and Profit Shifting (BEPS) Action 5 report with its modified nexus approach.

► Seem to result in an export subsidy since income from exports of intellectual property rights and goods would appear to be taxed

less than income generated by domestic sales. The fact that the deduction would be contingent upon export performance could

potentially make this subsidy prohibited by the WTO Agreement on Subsidies and Countervailing Measures.

Tax legislative and IRS update

Page 11

CBO budget and economic outlook: 2018 to 2028 highlights

► FY 2018 deficit of $804b

► $242b larger than projected in June 2017

► $139b than FY 2017

► $1t+ annual deficits beginning in FY 2020

► Federal debt held by public near 100% within decade

► 96% in 2028

► Increase in deficits/debt mainly due to

► Tax Cuts and Jobs Act

► Bipartisan Budget Act of 2018 that increased discretionary caps

► Consolidated Appropriations Act, 2018 appropriations bill

► Due to those 3 bills, revenues lower by $1t and outlays higher by $500bthan forecast in June 2017

► IRS FY 2019 budget – $11.1b

► $320m for tax reform implementation

Tax legislative and IRS update

Page 12

CBO deficit projections before, after TCJA, Bipartisan Budget Agreement, Omnibus

56

3

68

9 77

5 87

9

10

27

10

57

10

83 1

22

5 13

52 14

63

80

4

98

1

10

08 11

23 1

27

6

12

73

12

44 13

52

13

20

13

16

0

200

400

600

800

1000

1200

1400

1600

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Projections before TCJA, BBA, Omnibus (June 2017)

Projections after TCJA, BBA, Omnibus (April 2018)

0

2

4

6

8

10

12

14

Cumulative deficit 2018–2027

$11.7t

$10.1t

$b $t

$1t

Annual deficits

Source: CBO “Budget and Economic Outlook: 2018 to 2028,” April 2018

Tax legislative and IRS update

Page 13

Federal debt as share of GDP near 100% within a decade: CBO

0

10

20

30

40

50

60

70

80

90

100

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

78% 79% 81% 83% 86% 88% 90% 92% 93% 95% 96%

Source: CBO “Budget and Economic Outlook: 2018 to 2028”

%/G

DP

Tax legislative and IRS update

Page 14

Sources and uses of federal revenues, FY2017

Individual income taxes,

48%Social

Security, 35%

Corporate income taxes,

9%

Excise taxes, 3%

Other, 5%

Total: $3.315t

Social Security,

24%

Medicare and health,

28%Defense,

15%

Income security,

13%

Nondefense discretionary,

6%

Other entitlements,

7%

Net interest, 7%

Total: $3.981t

Note: “Other” revenue includes Federal Reserve earnings, customs duties, estate and gift taxes, and other miscellaneous receipts. “Other entitlements” include commerce and housing credit,

education, training, employment, social services, and veterans benefits and services. “Nondefense discretionary” includes international affairs, general science, space and technology, energy,

natural resources and environment, agriculture, transportation, community and regional development, administration of justice, general government and undistributed offsetting receipts. Income

security includes items such as food stamps, public housing and non-veteran pensions.

Source: US Department of Treasury, Monthly Treasury Statement, September 2017.

Revenues Expenditures

Tax legislative and IRS update

Page 15

IRS and guidance update

Page 16

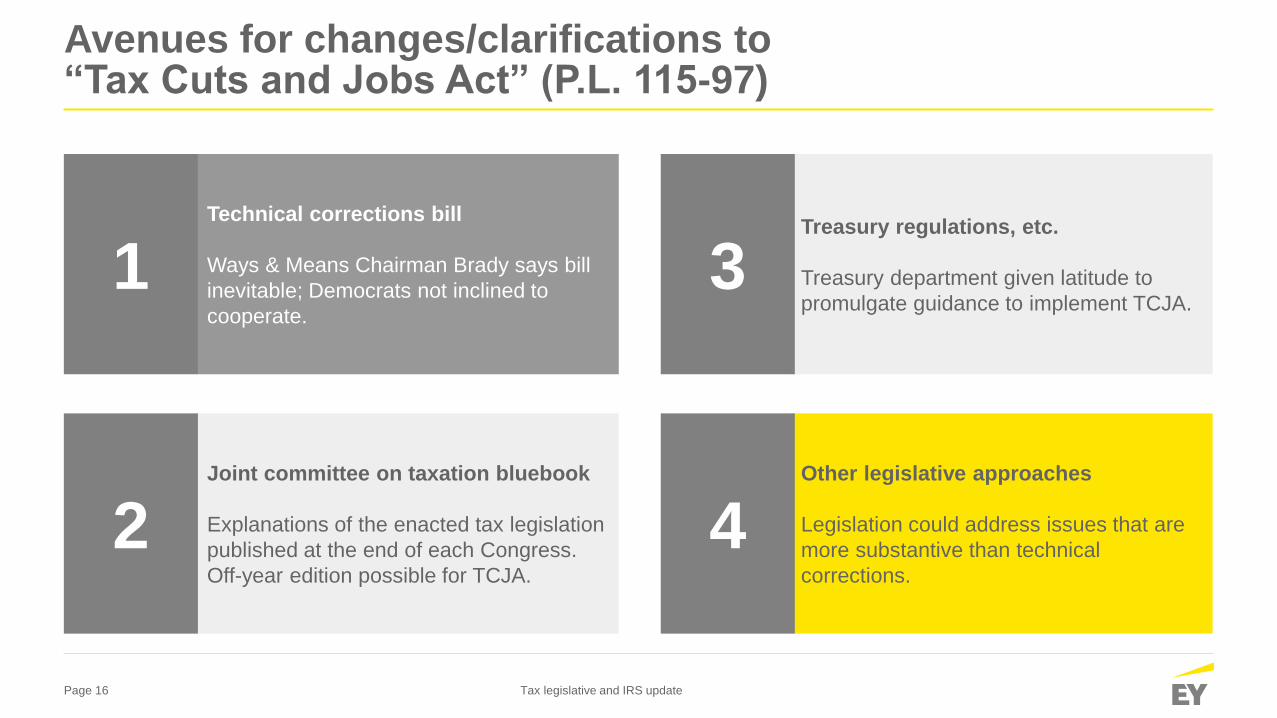

Joint committee on taxation bluebook

Explanations of the enacted tax legislation

published at the end of each Congress.

Off-year edition possible for TCJA.

Treasury regulations, etc.

Treasury department given latitude to

promulgate guidance to implement TCJA.

Technical corrections bill

Ways & Means Chairman Brady says bill

inevitable; Democrats not inclined to

cooperate.

Other legislative approaches

Legislation could address issues that are

more substantive than technical

corrections.

1

2

3

4

Avenues for changes/clarifications to “Tax Cuts and Jobs Act” (P.L. 115-97)

Tax legislative and IRS update

Page 17

February seven treasury/IRS priority guidance plan – initial implementation of Tax Cuts and Jobs Act

Treasury/IRS priority guidance plan – initial implementation of Tax Cuts and Jobs Act

1. Issues related to the business credit under §45S with

respect to wages paid to qualifying employees during

family and medical leave.

2. Sections 101 and 1016 and new Section 6050Y regarding

reportable policy sales of life insurance contracts.

3. Guidance under Section 162(m) regarding the application

of the effective date provisions to the elimination of the

exceptions for commissions and performance-based

compensation from the definition of compensation subject

to the deduction limit.

4. Guidance under Section 162(f) and new Section 6050X. 5. Computational, definitional, and other guidance under new

Section 163(j).

6. Guidance on new Section 168(k).

7. Computational, definitional, and anti-avoidance guidance

under new Section 199A.

8. Guidance adopting new small business accounting

method changes under Sections 263A, 448, 460, and 471.

9. Definitional and other guidance under new Sections

451(b) and (c).

10. Guidance on computation of unrelated business taxable

income for separate trades or businesses under new

Section 512(a)(6).

11. Guidance implementing changes to Section 529. 12. Guidance implementing new Section 965 and other

international sections of the TCJA.

13. Guidance implementing changes to Section 1361

regarding electing small business trusts.

14. Guidance regarding Opportunity Zones under Sections

1400Z–1 and 1400Z–2.

15. Guidance under new Sections 1446(f) for dispositions of

certain partnership interests.

16. Guidance on computation of estate and gift taxes to reflect

changes in the basic exclusion amount.

17. Guidance regarding withholding under Sections 3402 and

3405 and optional flat rate withholding.

18. Guidance on certain issues relating to the excise tax on

excess remuneration paid by “applicable tax-exempt

organizations” under Sections 4960.

Application of treasury/OMB OFFICE of Information and Regulatory Affairs (OIRA)

release of Memorandum of Agreement (MOA) on tax regulations?

Tax legislative and IRS update

Page 18

Tax reform impact on IRS

► IRS FY 2017 statistics update

► Number of employee 72,803 down from 94,346 in FY 2010

► Large corporate audits coverage – 7.9% down from 9.5% in FY 2016

► $ 1m > Individuals audits – 4.4% down from 5.8% in FY 2016

► IRS reform legislation

► Commissioner changed to administrator

► Changes to appeals

► Change to designated summons and third party summons rules

► Effect of tax reform on IRS examinations

► Years prior to tax reform

► Future years

► LB&I campaigns

Tax legislative and IRS update

Page 19

Appendix

Page 20

Tax reform timeline

January 2011 – Rep. Camp becomes Ways and Means Chairman

October 2011 – Camp releases international tax reform discussion draft

February 2012 – Obama Framework proposes 28% corp. rate (25%/manufacturing), minimum tax

January 2013 – Camp releases discussion draft on tax treatment of financial products

July 2013 – Obama proposes using repatriation revenue for highway funding

November 2013 – Senate Finance Chairman Baucus releases international draft with 2 options for minimum tax

February 2014 – Camp comprehensive draft details base broadening to reduce rates, move to territorial

February 2015 – Obama budget proposes 19% minimum tax, 14% tax on un-repatriated foreign earnings

September 2015 – Candidate Trump outlines initial tax plan with 15% corporate income tax rate

April 2016 – Obama releases 385 regulations, updates reform framework to denounce inversions

June 2016 – House GOP Blueprint proposes 20% corporate tax rate, territorial system, border adjustment tax

November 2016 – Trump elected President

April 2017 – Trump team outlines tax plan, states desire to work with Congress on details.

July 2017 – Big 6 group of WH officials and GOP leaders release joint statement declaring border adjustment tax dead

September 2017 – Administration and GOP leaders release’ “Unified Framework” template for tax-writing committees

2011

2012

2013

2014

2015

2016

2017

September 27:

Unified

Framework

released

November 2:

Ways & Means

releases bill

November 9:

Ways & Means

reports bill,

Senate Finance

releases its

version

November 16:

House approves

bill, Senate

Finance approves

bill

December 2:

Senate approves

bill

December 15:

Conference

agreement

released

December 20:

Conference

agreement

passed by House

& Senate

December 22:

President signed

bill

Tax legislative and IRS update

Page 21

► Doubles basic exclusion to $10m, indexed for inflation after 2011

Estate tax

Key individual provisions

► Capped at $750,000 of debt; $1m for debt incurred before

12/15/17. Reverts back to $1m 1/1/26, regardless of when debt

incurred. Available for second homes.

► Repeal deduction for interest on home equity debt

Mortgage interest deduction

► Capped at $10,000 for aggregate of state and local real property

and income taxes or state and local sales taxes

State and local tax deduction

► Lower rates to 10%, 12%, 22%, 24%, 32%, 35%, and 37%;

adjust rate bracket thresholds

► Roughly double standard deduction; repeal deduction for

personal exemptions; repeal overall limitation on itemized

deductions; repeal miscellaneous itemized deductions subject to

2% floor

Individual income tax rates

► Retain individual AMT

► Increases the exemption amounts ($70,300 single/$109,400

married filing jointly)

Alternative minimum tax (AMT)

Retains: 401(k)s and IRAs, current capital gains and dividends rates,

charitable contribution deduction, adoption credit, rules for the exclusion

of gain from the sale of a principal residence

► Child tax credit $2,000/child ($1,400 refundable)

► New $500 nonrefundable dependent credit

Child tax credit

► Applies to expenses that exceed 7.5%/10% of AGI (7.5% for 2017 &

2018, 10% thereafter)

Medical expense deduction

Tax legislative and IRS update

Page 22

Key business tax provisions

Corporate tax rate and corporate AMT

► 21% tax rate, effective 1/1/18

► Eliminate corporate AMT with refunds for AMT credits

Interest expense deduction

► Limit deduction to net interest expense that exceeds 30% of ATI

► ATI through 2021 = EBITDA; Beginning in 2022 = EBIT

Expensing

► 100% deduction for “qualified property” placed in service after 9/27/17 for five years; phase-down starting in 2023

Net operating losses (NOLs)

► Indefinite carryforward/repeal carryback (subject to certain exceptions)

► Offset limited to 80% of taxable income for NOLs arising after 2017

Like-kind exchanges

► Tax-free treatment limited to exchanges involving real property only

Domestic production deduction (current law Section 199)

► Repeal deduction for tax years after 2017

Tax legislative and IRS update

Page 23

► Dividend exemption

► 100% deduction for foreign-source portion of dividend received by domestic corporation from specified 10%-owned foreign corporations. Retain

current year taxation of passive income (via subpart F rules)

► Transition tax

► One-time mandatory transition tax on accumulated untaxed post-1986 earnings of 10% owned foreign subsidiaries. Payable in installments up

to 8 years

► 15.5% rate on cash and cash equivalents, and 8% rate on the remainder

► Administration Guidance issued in the form of Notices that provide taxpayers immediate guidance that will be formalized in future regulations

and Revenue Procedures.

► Notice 2018-7 announced operational rules that include how to account for related-party transactions in computing E&P and cash.

► Notice 2018-13 announced rules clarifying definitions of foreign corporations, providing an alternative method for measuring 11/2 E&P, and

allowing netting of certain related party account receivables (notional cash pooling was not addressed)

► Notice 2018-13 also addresses source and reporting obligations resulting from the repeal of the stock attribution rules under section

958(b)(4)

► Rev. Proc. 2018-17 prevents changes to the annual accounting periods of certain foreign corporations in 2017 under the automatic change rules

or general procedures if such change could result in the avoidance, reduction, or delay of the transition tax.

► Additional Notices expected prior to April 1st

Key international provisions

Territorial system

Tax legislative and IRS update

Page 24

Key international provisions

► Add-on minimum tax that applies to certain corporations with:

► Average annual gross receipts of at least $500m for three-year period ending with preceding taxable year

► BEAT payments of at least 3% (or 2% for banks, securities dealers) of all deductible payments

► BEAT is the excess of:

► 10% (5% in 2018) of modified taxable income, (generally taxable income grossed up by BEAT payments (certain deductible payments from US corp to

related foreign corp, including for some services)) over regular tax liability reduced by credits other than R&D and a portion of the low income housing credit

and certain energy credits

► 12.5% after 2025 (6%/11%/13.5% for banks, securities dealers)

Base Erosion and Anti-abuse Tax (BEAT)

► Minimum tax (?) on net foreign income in excess of 10% of “qualified business asset investment”

► Income in excess of 10% is subject to immediate taxation in the US, reduced by a deduction

► Before 2026 – 50% deduction

► After 2025 – 37.5% deduction

► GILTI is calculated on a global basis

► Only a portion of FTCs allowed (expense allocation appears to be required)

Global Intangible Low-taxed Income (GILTI)

► Reduced rate of tax (via a US deduction) on income associated with exports

► FDII deduction is allowed on income in excess of a 10% return on assets used to generate certain export income

► A deduction for FDII reduces the applicable US tax

► Before 2026 – 37.5% of FDII

► After 2025 – 21.875% of FDII

Foreign-Derived Intangible Income (FDII) deduction

Tax legislative and IRS update

Page 25

Key pass-through provisions

► Allows individual taxpayers to deduct 20% of domestic “qualified business income” (QBI) from a partnership,

S corporation, or sole proprietorship (“qualified businesses”) subject to certain limitations and thresholds.

Trusts and estates may take the deduction. Effective for tax years beginning after 12/31/17 and before 1/1/26

► QBI for a tax year is the net amount of domestic qualified items of income, gain, deduction, and loss with

respect to a taxpayer’s qualified businesses. “Qualified businesses” does not include specified services

trades or businesses such as accounting, law, health, several other professions or service businesses related

to investing, but does include engineering and architecture trades

► Deduction is limited for taxpayers with income above $315,000 (married filing jointly) to the greater of 50% of

the W-2 wages, or the sum of 25% of the W-2 wages plus 2.5% of the unadjusted basis of all qualified

property. Limitation fully phased-in for taxpayers with income of $415,000 and above (married filing jointly).

For taxpayers with income from specified service businesses, deduction starts being phased out at $315,000

(married filing jointly) income amount and fully phases out over a $100,000 range (married filing jointly) at

$415,000 (married filing jointly) income amount

Tax legislative and IRS update

Page 26

► Expands the Section 162(m) $1m deduction limit that applies to compensation paid top executives of publicly held

companies for TY beginning after 12/31/17

► Covered employees would to include the CFO and all executives once identified

► Eliminates the performance-based compensation exceptions and extends deduction limitation to deferred compensation

paid to executives who previously held a covered employee position

► Expands applicability of the deduction limitation to certain foreign private issuers and private companies that have publicly

traded debt

► Provides a transition rule for compensation paid pursuant to a plan under a written binding contract that is in effect on

11/2/17 and is not materially modified thereafter

► Eliminates deduction for certain fringe benefit expenses

► Business entertainment activities and membership dues; transportation or commuting expenses are not excludable from

income or deductible by the employer

► Employee achievement awards may not be deducted or excluded from income if the award is paid in cash, gift cards,

meals, lodging, tickets, securities, or other similar items

► No longer exempts employer-provided eating facilities from 50% deduction limitation; in 2026, deductions are completely

disallowed for employer-provided eating facilities and meals provided for the convenience of the employer

► Adds a new income inclusion deferral election allowing deferral of tax for options and restricted stock units issued to

qualified employees of private companies; applies on or after 12/31/17

Provisions affecting compensation

Tax legislative and IRS update

Page 27

State and local TCJA considerations – overview

► 30% business interest limitation may conflict with state related-

party interest expense addback rules

► Certain states might seek to determine the limitation at the

individual entity level

► Immediately re-evaluate existing debt structures for state tax

purposes too?

Interest expense limitation

► The Internal Revenue Code (IRC) and resulting federal taxable

income (FTI) is typically the starting point to determine state

taxable income

► States differ on federal conformity, and IRC conformity dates are

key

► “Rolling” vs. “fixed” vs. “selective” conformity

Conformity to internal revenue code

Key state income tax issues to address…

► New anti-deferral “carrot” and “stick” provisions impact FTI, but will

conforming states statutorily treat “global intangible low-taxed

income” the same as current categories of subpart F income?

► New base erosion and anti-abuse tax on certain payments to

foreign affiliates is a new federal tax regime to which the states

may not conform

Anti-deferral/anti-base erosion

► Will states have their own “transition tax”?

► This 2017 tax year event will have state tax implications too

► State approaches to subpart F income vary widely (some might not

tax at it all), and state-specific expense disallowance rules for any

non-taxed subpart F income must be considered

► Future actual distributions that are not taxable for federal purposes

may still be taxable in certain states, particularly California

Transition tax/future distributions

Tax legislative and IRS update

Page 28

Treasury/IRS guidance issued

► Section 965 deemed repatriation rules

► Notice 2018-07 (December 29, 2017)

► Discusses regulations Treasury and IRS intend to issue include

► Notice 2018-13 (January 19, 2018)

► Says Treasury, IRS intend to issue rules addressing the calculation of earnings

► Provides taxpayers targeted relief from change to stock attribution rules

► Rev. Proc. 2018-17 (February 13, 2018)

► Prevents changes to the annual accounting periods of certain foreign corporations in 2017 under automatic or general procedures if it could result in the

avoidance, reduction, or delay of the transition tax

► FAQs (March 13, 2018)

► Outline how taxpayers subject to the Section 965 transition tax should report and pay the tax liability on their 2017 income tax returns

► Notice 2018-26 (April 2, 2018)

► Describes forthcoming rules intended to prevent avoidance of section 965, relating to certain special elections, and on the reporting and payment of the

transition tax

► Notice 2018-8 (Section 1446(f)) – Suspends application of Section 1446(f) in the case of disposition of certain publicly traded partnership interests

► Notice 2018-18 (Carried interest) – 3-year holding period can’t be avoided using S corps

► Notice 2018-23 (Fines and Penalties) – Transitional Guidance

► Notice 2018-28 (Section 163(j)) – Calculation of interest expense limitation

► Notice 2018-29 (Section 1446(f)) – Announces forthcoming regulations regarding withholding on a disposition by a foreign person of a partnership interest that

is not publicly traded

Tax legislative and IRS update

Page 29

Treasury/IRS guidance pending

► Other international tax provisions: the BEAT, the GILTI

► New rules applying to pass-through entities

► Individual tax changes

Tax legislative and IRS update

Page 30

EU reaction to US tax reformBackground

The EU has been looking into the impact of the US tax reform:

► On November 23, 2017 the Estonian Presidency invited an US representative at a High Level meeting to discuss US

tax reform plans (i.e., House and Senate Reform Bills). Given the significant differences between the two bills, it was

however still unclear what would be the final outcome of the US tax reform. Several delegations (DE/DK/FR/SE)

shared their concerns with US tax reform plans and stressed the need to have a debate and joint action at the EU

level on this issue.

► At the ECOFIN meeting of December 5, 2017, several ministers (FR/DE/AT/ES/IT/UK) and commissioner Moscovici

acknowledged that it is the sovereign right of the US to set its tax rates, but raised concerns of possible impacts on

existing double taxation treaties as well as WTO compatibility issues and possible negative economic impacts on EU

Member States.

► On December 11, 2017, G5 finance ministers (FR/DE/AT/ES/IT/UK) sent a joint letter to the Secretary of the US

Treasury (Steven Mnuchin), which recalled US international obligations, underlined concerns that "the inclusion of

certain less conventional international tax provisions could contravene the US’s double taxation treaties and may risk

having a major distortive impact on international trade“. They raised particular concerns in respect of the 20% excise

tax in the House bill, the BEAT in the Senate bill, and FDII in the Senate bill. The letter underlines that the OECD and

the BEPS Inclusive Framework are “the relevant forums for working on the evolution of international tax principles on

a multilateral basis”.

Tax legislative and IRS update

Page 31

EU reaction to US tax reformBackground

► On 12 December 2017, the European Commission (Vice-President Dombrovskis, Vice- President

Katainen, Commissioner Malmström and Commissioner Moscovici) sent another letter to the Secretary

of the US Treasury. The letter stressed that the draft US tax bill contained elements that "risk seriously

hampering trade and investment flows" and "would appear to be incompatible with WTO rules and other

international commitments taken by the US". The letter comments on the same elements of the US tax

bill as in the G5 letter. It also mentions risk of double taxation of the same payments in respect of the

BEAT and inconsistencies between the FDII and the OECD BEPS Action 5 report, before concluding that

the Commission looks forward to "continue [its] cooperation on ways to improve international taxation,

notably through the G20 and OECD work strands, as well as bilaterally".

► During January 2018 the EU held high level meetings where they again discussed the EU approach to

the US tax reform and raised questions to the delegations around:

► Economic and double tax treaties impact, in particular of BEAT and FDII

► Potential changes to the EU tax policy in reaction to the US tax reform and

► Need for a common EU reaction to these developments.

► It is expected that the EU Presidency will include this topic in the agenda of the upcoming monthly

ECOFIN meetings.

Tax legislative and IRS update

Page 32

EU reaction to US tax reformSummary of EU concerns

► In summary, at this point the concerns of the EU focus on the BEAT and FDII provisions. The arguments raised are

basically the following:

► BEAT: “Base Erosion and Anti-abuse Tax could give rise to discrimination and incompatibility with WTO rules”:

► It would not allow for the credit of foreign taxes paid.

► It could impact on genuine commercial arrangements and lead to double taxation of the same payments, notably in the finance

industry.

► Moreover, it could impact intra-group payments which are necessary for the financial sector to comply with financial stability

requirements (e.g., interest on TLAC debt in the banking industry).

► FDII: “Deduction for foreign derived intangible income would apply the preferential tax treatment to a broader range of

intellectual property than other internationally accepted regimes”.

► It appears that the preferential tax treatment would also be given to intellectual property that was initially created outside the US.

► Could be contrary to the OECD Base Erosion and Profit Shifting (BEPS) Action 5 report with its modified nexus approach.

► Seem to result in an export subsidy since income from exports of intellectual property rights and goods would appear to be taxed

less than income generated by domestic sales. The fact that the deduction would be contingent upon export performance could

potentially make this subsidy prohibited by the WTO Agreement on Subsidies and Countervailing Measures.

Tax legislative and IRS update

Page 33

EU reaction to US tax reformUS reaction

► The US response to these concerns could take into account the following arguments:

► US Tax reform is aligning the US International system with the territorial systems of it treaty partners.

► It is implementing the BEPS recommendations, in particular:

► Action 2 on hybrid mismatches

► Action 3 on CFC rules (through the GILTI provisions)

► Action 4 on Interest limitation rules (through the 30% EBITDA/EBIT limitation provisions).

► With respect to the BEAT, the potential US counter-arguments could be:

► BEAT is intended to tackle perceived weakness of Transfer Pricing rules to prevent BEPS as it would only apply

when there is high base erosion through deductible payments. Therefore, aligned with BEPS recommendations

and similar to what other countries are implementing (e.g., German rules restricting the tax deduction of royalties

and other payments).

► It should not raise treaty discrimination as it is designed as a minimum tax on US taxpayers and not so much as a

mere difference in the deductibility of certain payments between residents and non-residents.

► With respect to the FDII the potential US counter-arguments could be:

► FDII is not an intellectual property regime (not limited to intellectual property) and therefore not subject to the

BEPS recommendations on patent boxes.

► It needs to be analyzed in combination with the GILTI provisions as coordinated elements to tackle offshoring.

Tax legislative and IRS update

Page 34

EU effort on taxing digital technology

► European Commission March 21 unveiled 2 proposals

► Interim 3% Digital Sales Tax on revenues (not profits), collected where

the users involved are located, for companies with:

► Total annual worldwide revenues of €750m or more

► Annual EU revenues of €50m or more

► Proposal for virtual permanent establishment

► March 16 OECD interim report does not make recommendations for

interim measures

► No consensus on merits or need, and concerns about impact on

investment, potential for double taxation

► US leaders wary of global efforts to impose digital tax

► Similar to response to EU state aid investigations under Obama

► Mnuchin: US opposes singling out digital companies

► Hatch: To attempt to tax items with a so-called “digital presence” or

another questionable definition is counterproductive

Tax legislative and IRS update

Page 35

President Trump’s ‘Legislative Outline for Rebuilding Infrastructure in America’

► Asks Congress for $200b /10 years to spur $1.5t state/local, private

infrastructure investment

► Plan seeks $6b to create flexibility and broaden eligibility for private

activity bonds (PABs)

► Plan does not identify revenue source

► Administration: everything on the table

► Insufficient support in Congress for gas tax hike

► GOP leaders: time, revenue constraints make action this year

difficult, may do infrastructure in pieces

► Senate Dems: roll back $1t of tax law

► Increase the top rate from 37% to 39.6% ($139b/10 yrs)

► Increase corporate tax rate from 21% to 25% ($359b)

► 2017 parameters for AMT ($429b) and estate tax ($83b), and

► Close the “carried interest loophole” ($12b)

Tax legislative and IRS update

Page 36

Trade overview

► Congress concerned about retaliation from tariffs

► March 8 Sec 232 tariffs on steel, aluminum imports

► Exempt: Canada, Mexico, Korea, EU, Argentina, Australia, Brazil

► March 23 Sec 301 tariffs on China imports, ~$50b

► Trans-Pacific Partnership (TPP)

► President Trump pulled the US from the TPP in early 2017

► Remaining nations finalized deal March 8

► North American Free Trade Agreement (NAFTA)

► Negotiations continue, contentious issues include:

► Automobile rules-of-origin

► Investor-state dispute settlement (ISDS) corporate arbitration system, which

GOP lawmakers favor retaining

► Trump may propose “reciprocal tax”

► Other issues► Tariffs on imported washing machines, solar cells & modules

► Renegotiation of KORUS (US-Korea free trade agreement)

Tax legislative and IRS update

Page 37

Growth of real GDP and real potential GDP

Tax legislative and IRS update

Page 38

US federal budget deficits, 1968–2028 projected

Tax legislative and IRS update

Page 39

US federal debt held by the public, 1940–2028 projected

Tax legislative and IRS update

Page 40

Gross debt as a percent of GDP for OECD countries, 2015

Note: Includes all levels of government.

Source: OECD Statistics.

13 2

5 29 33 39 41 43

43 46 53

53

54

54

55 60 6

9 73 75 77

78

79 8

9 97

97 100

102

10

5

11

2

11

6

121

127 1

49

157

183

222

0

50

100

150

200

250E

sto

nia

Ch

ile

Lu

xe

mb

ou

rg

Tu

rke

y

No

rwa

y

La

tvia

Sw

itze

rla

nd

Au

str

alia

Ko

rea

Me

xic

o

Czech

Re

pu

blic

Sw

ed

en

De

nm

ark

Ne

w Z

ea

land

Slo

va

k R

ep

ub

lic

Po

land

Ice

lan

d

Fin

lan

d

Ne

the

rla

nd

s

Isra

el

Ge

rma

ny

Ire

lan

d

Hu

ng

ary

Canada

Au

str

ia

Slo

ve

nia

Un

ite

d S

tate

s

Un

ite

d K

ing

do

m

Spain

Fra

nce

Be

lgiu

m

Po

rtu

ga

l

Ita

ly

Gre

ece

Ja

pa

n

Pe

rce

nt o

f G

DP

(%

)

Tax legislative and IRS update

Page 41

Tax revenue as a percent of GDP for OECD countries, 2015

16

2123

25 25 26 28 28 29 31 31 32 32 32 33 33 33 34 34 3536 37 37 37 37 37 38 39

43 43 44 44 45 45 46

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Me

xic

o

Ch

ile

Ire

lan

d

Tu

rke

y

Ko

rea

United S

tate

s

Sw

itze

rla

nd

Au

str

alia

La

tvia

Ja

pa

n

Isra

el

Ca

na

da

Slo

va

k R

ep

ub

lic

Po

land

Un

ite

d K

ing

do

m

Ne

w Z

ea

land

Czech

Re

pu

blic

Sp

ain

Esto

nia

Po

rtu

ga

l

Gre

ece

Slo

ve

nia

Ice

lan

d

Lu

xe

mb

ou

rg

Ge

rma

ny

Ne

the

rla

nd

s

No

rwa

y

Hu

ng

ary

Italy

Sw

ed

en

Au

str

ia

Fin

lan

d

Be

lgiu

m

Fra

nce

De

nm

ark

Pe

rce

nt o

f G

DP

(%

)

Individual income tax Corporate income tax General goods & services taxes (including VAT) Other taxes

United States

Note: Includes all levels of government. “Other taxes” include payroll and social security taxes, property taxes, certain excise taxes, export and import taxes, and miscellaneous other taxes.

Source: OECD Statistics.

Tax legislative and IRS update

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and

advisory services. The insights and quality services we

deliver help build trust and confidence in the capital

markets and in economies the world over. We develop

outstanding leaders who team to deliver on our promises

to all of our stakeholders. In so doing, we play a critical

role in building a better working world for our people, for

our clients and for our communities.

EY refers to the global organization, and may

refer to one or more, of the member firms of

Ernst & Young Global Limited, each of which is a separate

legal entity. Ernst & Young Global Limited, a UK company

limited by guarantee, does not provide services to clients.

For more information about our organization, please visit

ey.com.

Ernst & Young LLP is a client-serving member firm of

Ernst & Young Global Limited operating in the US.

© 2018 Ernst & Young LLP.

All Rights Reserved.

1712-2535214

ED None

This material has been prepared for general informational

purposes only and is not intended to be relied upon as

accounting, tax or other professional advice. Please refer

to your advisors for specific advice.

ey.com