25 july 06, page 1 company confidential results 2q06 and 1h06 martin de prycker 25 july, 2006

TRANSCRIPT

25 July 06, page 1Company Confidential

Results 2Q06 and 1H06Results 2Q06 and 1H06

Martin De PryckerMartin De Prycker

25 July, 2006

25 July 06, page 2Company Confidential

Operational results 2Q06 and 1H06Operational results 2Q06 and 1H06

In € million 2Q05 2Q06 Growth 2Q06/2Q05

1H05 1H06 Growth 1H06/1

H05

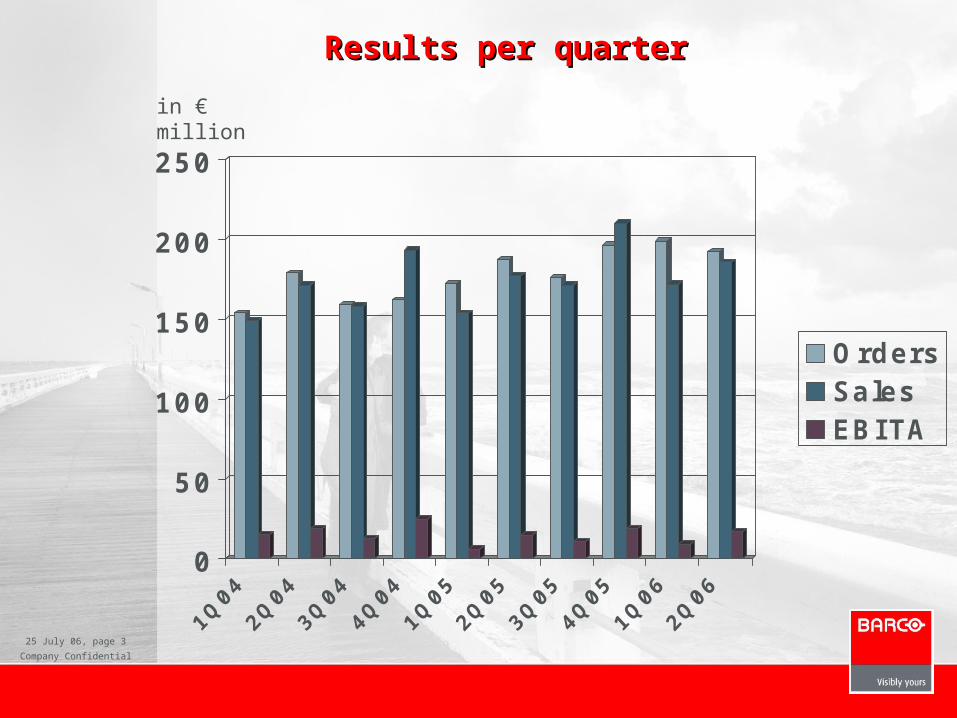

Orders 185.6 192.0 3.4% 358.0 391.6 9.4%

Sales 176.9 186.0 5.1% 330.5 358.1 8.3%

EBITA 15.5 16.1 4.1% 21.9 25.4 16.0%

EBITA % 8.7 8.7 - 6.6 7.1 -

Book-to-bill 1.05 1.03 - 1.08 1.09 -

25 July 06, page 3Company Confidential

Results per quarterResults per quarter

0

50

100

150

200

250

OrdersSalesEBI TA

in € million

25 July 06, page 4Company Confidential

Overall comments 2Q06Overall comments 2Q06

• Order and sales growth continued in the second quarter, with a positive book-to-bill ratio of 1.03

– Strong growth in Medical, Events and DC markets– Order intake at € 192.0 million, remaining at a high

level, even though some large orders shifted to 3Q06

• Operational improvement actions, resulting in– Gross profit margin at 42.6%, improved vs 2Q05 at

42.3% – EBITA at 8.7%, the same as last year. However,

EBITA of 2Q05 was positively impacted by other operating income, 2Q06 negatively impacted by other operating results

25 July 06, page 5Company Confidential

Company divisional structureCompany divisional structure

BarcoView Barco Media & Entertainment

Barco Control Rooms

Barco Presentation & Simulation

BarcoVision

Barco Manufacturing Services

Defense & security

Traffic management

Medical imaging

Avionics

Events

Media

Digital cinema

Traffic & surveillance

Utilities & process

control

Broadcasting

Simulation

Presentation

Textiles

Plastics

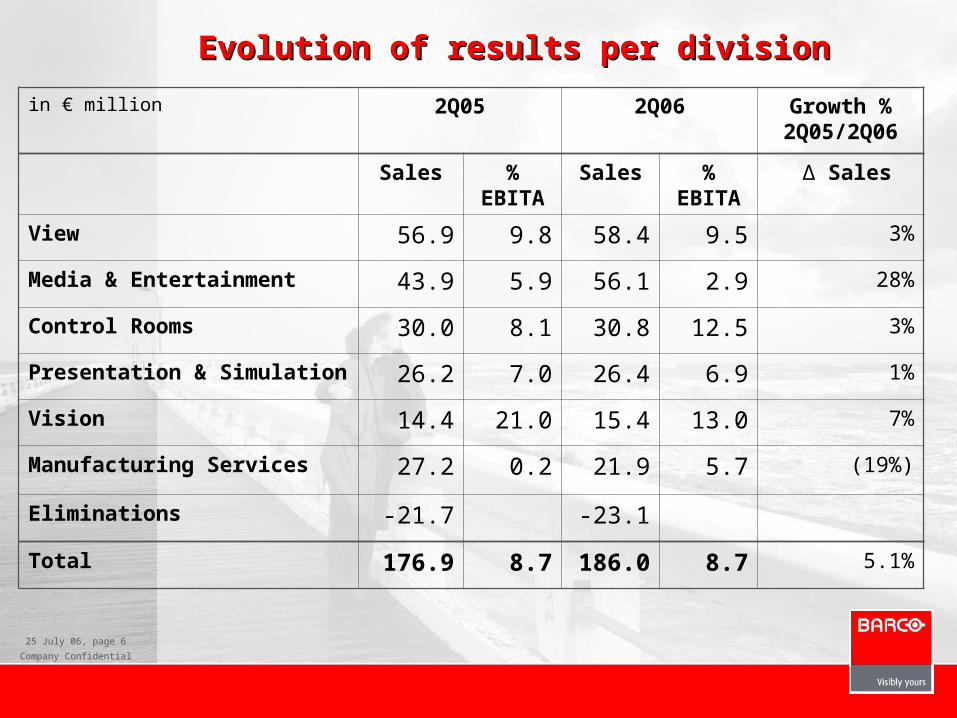

25 July 06, page 6Company Confidential

Evolution of results per divisionEvolution of results per division

in € million 2Q05 2Q06 Growth % 2Q05/2Q06

Sales % EBITA

Sales % EBITA

∆ Sales

View 56.9 9.8 58.4 9.5 3%

Media & Entertainment 43.9 5.9 56.1 2.9 28%

Control Rooms 30.0 8.1 30.8 12.5 3%

Presentation & Simulation 26.2 7.0 26.4 6.9 1%

Vision 14.4 21.0 15.4 13.0 7%

Manufacturing Services 27.2 0.2 21.9 5.7 (19%)

Eliminations -21.7 -23.1

Total 176.9 8.7 186.0 8.7 5.1%

25 July 06, page 7Company Confidential

BarcoView BarcoView (1)(1)

0

10

20

30

40

50

60

70

80

OrdersSalesEBI TA

in € million

25 July 06, page 8Company Confidential

BarcoView BarcoView (2)(2)

• Orders – Book-to-bill at 1.02– Orders in Medical increased strongly vs 2Q05– Orders in Defense & Security stabilizing at the level of last

year, also including some initial small orders, laying the foundation for new business

– Orders in Traffic Management lower than 2Q05 as projects are further delayed into 2007

– Orders in Avionics weaker than very high orders in 2Q05

• Sales– Strong sales growth in Medical confirms market leadership

and Frost & Sullivan award won for 3D software– Defense and Traffic Management sales lower than in 2Q05– Avionics sales strongly growing vs 2Q05

• Margins– Gross profit margin slightly lower than last year (45.4% vs

46.3%), mainly due to shift in product mix– EBITA margin of 9.5% stable vs 9.8% in 2Q05

• Goodwill impairment– On the acquisition of Voxar an impairment of € million 1.6

was taken, because the market is not developing as fast as expected

25 July 06, page 9Company Confidential

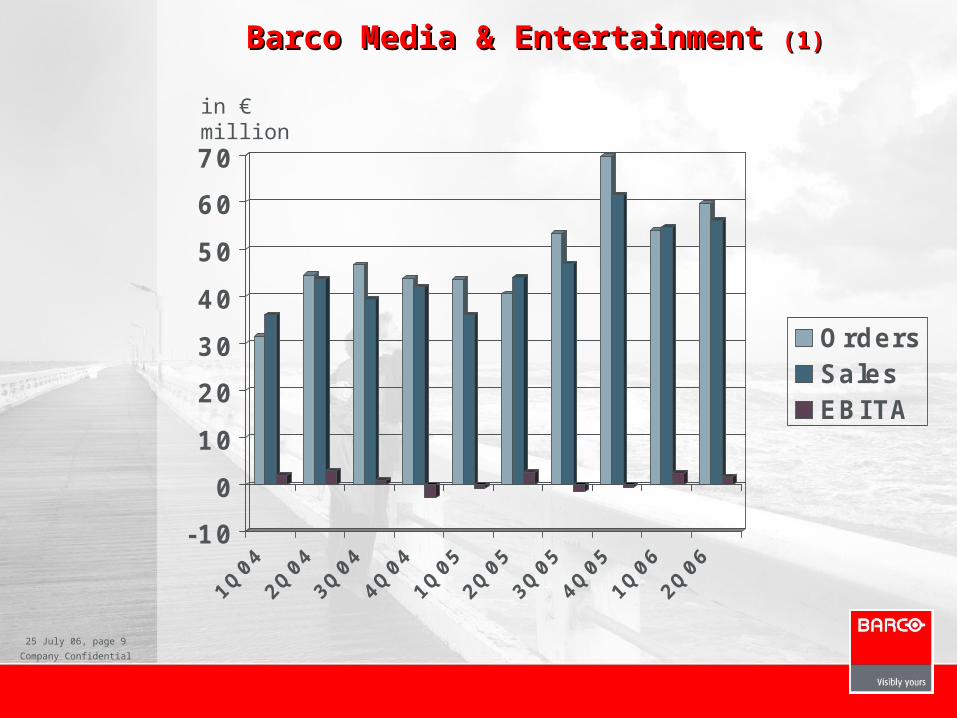

Barco Media & Entertainment Barco Media & Entertainment (1)(1)

-10

0

10

20

30

40

50

60

70

OrdersSalesEBI TA

in € million

25 July 06, page 10Company Confidential

Barco Media & Entertainment Barco Media & Entertainment (2)(2)

• Orders– Good book-to-bill ratio at 1.06– Orders in Media slightly higher, against background of

more selective market approach– Orders in Events strongly growing– Digital Cinema: very strong order growth confirms

that the market is definitively taking off

• Sales– Strong Events and DC sales– Media sales lower than last year

• Margins– Gross profit margin at 31.9%, lower than 2Q05, but

better than 1Q06 at 31.1%– EBITA margin at 2.9%, lower than last year, due to

higher non-recurrent cost of € 3 million (negative currency fluctuations and exceptionals)

25 July 06, page 11Company Confidential

Barco Control Rooms Barco Control Rooms (1)(1)

0

5

10

15

20

25

30

35

OrdersSalesEBI TA

in € million

25 July 06, page 12Company Confidential

Barco Control Rooms Barco Control Rooms (2)(2)

• Orders– Orders declined vs 2Q05 due to competitive pressure

in the broadcast market– Book-to-bill at 0.96

• Sales– Sales growing 3%, at a lower speed than last year,

but larger backlog (+ 12%) as compared to the end of 2Q05, for second half

• Margins– Gross profit margin to 43.8%, comparable to the one

in 2Q05– EBITA margin good at 12.5%, better than 8.1% in

2Q05

25 July 06, page 13Company Confidential

Barco Presentation & Simulation Barco Presentation & Simulation (1)(1)

0

5

10

15

20

25

30

35

OrdersSalesEBI TA

in € million

25 July 06, page 14Company Confidential

Barco PresentationPresentation & Simulation (2)

• Orders– Good book-to-bill ratio at 1.08– Order intake lower in Simulation and flat in

Presentation vs 2Q05

• Sales– Sales at the same level as last year (+ 1%)– Presentation sales grew 4% vs 2Q05– Simulation sales declined vs 2Q05, due to ongoing

shift in technology for flight simulation

• Margins– Gross profit margin improved to 42.5% vs 41.7% in

2Q05– EBITA margin stable at 6.9% vs 7.0% in 2Q05

25 July 06, page 15Company Confidential

BarcoVision BarcoVision (1)(1)

0

2

4

6

8

10

12

14

16

18

OrdersSalesEBI TA

in € million

25 July 06, page 16Company Confidential

BarcoVision BarcoVision (2)(2)

• Sales & Orders– Book-to-bill ratio at 1.05 shows some recovery in

investment climate outside China, complemented by an important win in China for system business

• Margins– Gross profit margin at 47.8% vs 47.4% in 2Q05, – EBITA margin high at 13.0%. In 2Q05, the EBITA

margin was higher, but included the profit on the sale of 2 buildings

25 July 06, page 17Company Confidential

Barco Manufacturing Services Barco Manufacturing Services (1)(1)

-5

0

5

10

15

20

25

30

35

OrdersSalesEBI TA

in € million

25 July 06, page 18Company Confidential

Barco Manufacturing Services Barco Manufacturing Services (2)(2)

• Sales & Orders– High book-to-bill ratio of 1.14, preparing for large

internal demand for second half– Sales lower than last year, due to shift of production

to Asia

• Margins– EBITA margin at 5.7%, much better than 2Q05 as

manpower and cost have strongly declined vs last year, thanks to restructuring actions taken in 2005

25 July 06, page 19Company Confidential

Geographical breakdown of salesGeographical breakdown of sales

2Q05

30,3%

19,3%

50,4%EMEAAMERI CASASI APAC.

2Q06

31,7%

15,1%

53,2%

25 July 06, page 20Company Confidential

Key figures Income Statement 2Q06Key figures Income Statement 2Q06

in € million 2Q05 % 2Q06 % 1H05 % 1H06 %Sales 176,9 100,0 186,0 100,0 330,5 100,0 358,1 100Cost of goods sold -102,1 -57,7 -106,8 -57,4 -195,0 -59,0 -208,1 -58,1Gross Profit 74,8 42,3 79,2 42,6 135,6 41,0 150,0 41,9Research & Development -16,2 -9,2 -17,8 -9,6 -32,2 -9,7 -34,6 -9,6Sales & Marketing -29,6 -16,7 -30,6 -16,4 -58,0 -17,5 -60,4 -16,9General & Administration -14,1 -7,9 -13,6 -7,3 -27,0 -8,2 -27,8 -7,8Other operating result 0,6 0,3 -1,2 -0,6 3,5 1,1 -1,9 -0,5EBI TA 15,5 8,7 16,1 8,7 21,9 6,6 25,4 7,1Goodwill impairment 0,0 0,0 -1,6 -0,9 0,0 0,0 -1,6 0,4Operating Result 15,5 8,7 14,5 7,8 21,9 6,6 23,8 6,6Non-operating result -0,3 -0,2 -0,2 -0,1 -0,5 -0,1 -0,2 0,0I ncome Taxes -3,4 -1,9 -3,2 -1,7 -4,8 -1,5 -5,1 -1,4Net I ncome 11,7 6,6 11,2 6,1 16,5 5,0 18,8 5,2Current Cash Flow 25,8 14,6 27,1 14,6 44,0 13,4 48,9 13,7Current Earnings/ Share ( in €) 0,96 1,05 1,36 1,66Net Earnings/ Share ( in €) 0,95 0,93 1,35 1,55

25 July 06, page 21Company Confidential

Key figures Balance SheetKey figures Balance Sheet

in € million 30/06/05 31/12/05 30/06/06

Accounts Receivable

173.7 188.8 175.2

Inventory 167.8 141.4 167.0

Cash 87.4 106.3 83.4

Financial debt 104.3 84.3 81.3

• Dividend payment: € 26.1 million

• Share buyback 1H06: € 6.6 million

25 July 06, page 22Company Confidential

Expectations 3Q06Expectations 3Q06

• Sales between € 172 – € 182 million vs € 171.5 million in 3Q05

• EBITA of between € 10 and € 15 million vs € 11.1 million in 3Q05

25 July 06, page 23Company Confidential

Questions & Answers