23 march 2018 -...

TRANSCRIPT

1

23 March 2018

The next Economics Weekly will be published on Friday 6 April.

AUSTRALIAN ECONOMIC DEVELOPMENTS

In the international economy this week, the US Federal Reserve raised the Fed funds rate by

0.25% to a target range of 1.50 to 1.75%. This is the first time in 17 years that US rates have

been higher than Australia’s. It further confirms that the two countries are at different stages in

their economic cycle. In particular, the US labour market is much tighter than Australia’s. After

peaking at 10% in 2009, the US unemployment rate has been trending down for some years. At

4.1% in February, US unemployment is now indicating little or no spare capacity, which is

beginning to put upward pressure on wages and prices.

In contrast, Australia’s GDP growth has remained modest and the national unemployment rate

has been stable at around 5.5% for some time, despite solid employment growth over the past

year. The latest Australian jobs data (released this week by the ABS) suggest there is still

significant spare capacity in the local labour market. The unemployment rate ticked up to 5.6%,

despite total employment increasing by 17,500 in February (seasonally adjusted). The rise in the

unemployment rate in February was because the number of people who started looking for work

was greater than the number of people who found work. Female workforce participation is rising

especially strongly at present, with the female participation rate hitting a new record high of 60.6%

in February. Job ads data for February suggest employment growth will continue in the coming

months, with new jobs ads on SEEK up 16.2% compared to February last year. Engineering;

trades & services; IT; and mining, resources & energy jobs ads all increased by at least 25% p.a.

in February.

Other data released this week indicate that Australia’s population increased by almost 400,000

to 24.7 million people (+1.6% p.a.) over the year to September 2017. Net overseas migration

(permanent and long-term arrivals less departures) accounted for 63.2% of the rise, (250,200

more people), with natural population growth (births less deaths) accounting for the remainder.

Jobs growth moderates but more people seek work in February 2018

The ABS estimates that Australia’s unemployment rate ticked up to 5.6%, despite total

employment increasing by 17,500 in February (seasonally adjusted). The unemployment rate

rose in February despite this rise in employment because more people were actively searching

for work; 26,400 additional people entered the labour force in February to work or search for work.

2

Employment growth in February included an increase of 64,900 in full-time employment, offset

by a fall of 47,400 in part-time employment (seasonally adjusted). This represented a reversal

from January, when part-time employment increased and full-time employment decreased in the

month. This is partly because seasonal effects are particularly large in January and February due

to higher levels of temporary and seasonal work in summer.

The trend estimates help to provide a clearer guide to the underlying patterns emerging in the

labour market1. In trend terms, employment growth actually moderated in February - 19,300 jobs

were added in the month, below the 12-month average of 33,100 jobs per month. Although

full-time employment increased for a 16th straight month, it has been slowing since May 2017,

while part-time employment growth has held relatively stable. Part-time employment (defined by

the ABS as 35 hours or less per week) accounted for 31.7% of the total workforce in February

2018, below the high of 32.0% of the total workforce in November 2016 (see Chart 1 and table 1).

On an annual growth basis, employment continues to strengthen, increasing by 0.2% m/m and

3.3% p.a. in February and adding a total of 399,500 jobs over the year. Full-time employment

accounted for 73.4% employment growth over the year to February, adding 293,100 jobs.

Chart 1: Full-time and part-time employment growth (trend)

Source: ABS, Labour force Australia February 2018

1 The ABS recommend that “Trend estimates are considered the best indicators of the underlying behaviour in the labour market.” ABS 6202.0, Labour Force, Australia, Media Release. 14 Sep 2017. The data below are all trend.

3

Table 1: Key labour market numbers, February 2018 (trend)

Number Change per month Change per year

trend ‘000 ‘000 m/m % m/m ‘000 p.a. % p.a. Employment 12,480 19.3 0.2 399.5 3.3

Full-time 8,519 7.7 0.1 293.1 3.6 Part-time 3,961 11.6 0.3 106.5 2.8

Aggregate hours worked 1,730,293 -1,362 -0.1 46,772 2.7 Labour force 13,210 23.7 0.2 389.5 3.0 Adult civilian population 20,128 32.9 0.2 328.5 1.7

Number Rate Change from one year ago

‘000 % of labour force Percentage point change p.a. Unemployment (trend) 729.5 5.5 -0.2 Underemployment (orig) 1,102.3 8.3 -0.5 Underutilization (orig) 14.3 -0.8

trend % of adult population Percentage point change p.a.

Participation rate 65.7 0.9 Employment to population ratio 62.1 1.0

Source: ABS, Labour force Australia, February 2018

On the supply side, the labour force (all people working or looking for work) grew by 3.0% p.a. in

February, taking the participation rate to 65.7% of the adult population. Labour force participation

is rising especially strongly among women and older workers. The female participation rate

reached an historic high of 60.6% in February and has risen every month for the past 10 months.

Over the past year, labour force participation has increased most strongly for women aged

between 25 and 44 years and for older men. The RBA noted recently that these groups tend to

be attracted back into the labour market when conditions are strong, but also that structural forces

could be encouraging greater participation, including trends towards less physically demanding

work (e.g. in services industries) and improvements in health outcomes.

Australia’s unemployment rate has been steady at 5.5% since July 2017 (trend). This indicates

that despite strong employment growth (and the emergence of skill shortages in certain specialist

areas), some slack remains. At the same time, the underemployment rate (that is, the proportion

of the labour force who are working but are willing and able to work more hours) decreased

marginally (-0.1% q/q) to 8.3% (trend) over the quarter to February - its lowest point in since

August 2015. This small improvement probably reflects the drop in part-time employment as a

share of total employment. Nevertheless, underemployment remains well above historical

average levels and is a further indication that a significant amount of spare capacity still exists

(Chart 2).

4

Chart 2: Unemployment, underemployment and underutilisation rates

(trend)

Source: ABS, Labour force Australia, February 2018

Across the states, employment growth over the 12 months to February 2018 was strongest in

Queensland (4.6%), followed by New South Wales (3.9%) and Victoria (2.6%). In the first two

months of 2018, monthly employment growth has been slower compared to 2017 in all states

except South Australia (see Chart 3).

The unemployment rate rose in February in NSW, SA and the ACT, held steady in Victoria,

Queensland, WA and Tasmania and fell (to 4.4%) in the NT. The unemployment rate remains

lowest in the territories (as it is in most months) and in NSW. Unemployment rates were highest

in Queensland, WA and SA, with all three above 6.0% in February.

Table 2: Employment, unemployment and participation by state, Feb 2018

Employment growth Part time workers Unemployment

Under-employment Participation

Trend '000 m/m '000 y/y % p.a. % rate % rate % (orig) rate %

NSW 7.3 147.4 3.9 30.5 4.9 8.0 64.6

VIC 0.3 77.7 2.5 32.6 5.7 7.9 65.8

Qld 4.2 110.0 4.6 31.1 6.1 8.6 66.2

SA 2.7 19.0 2.3 34.9 6.2 9.9 62.9

WA 0.2 30.6 2.3 32.8 6.0 8.8 68.2

Tas -0.0 5.7 2.4 37.9 5.8 9.8 60.9

NT 0.2 -5.0 -3.5 22.0 4.4 4.9 76.1

ACT 0.2 10.4 4.7 26.6 4.1 5.6 72.8

Australia 19.3 399.5 3.3 31.7 5.5 8.3 65.7

Source: ABS, Labour force Australia February 2018.

5

Chart 3: Monthly employment growth by state, Feb 2018

Source: ABS, Labour force Australia February 2018

Australia’s population continues to rise in year to September 2017

Australia’s estimated resident population (ERP) increased by 395,600 (1.6% p.a.) to 24.7 million

people over the year to September 2017, which is the largest annual increase since 2013. In

absolute terms, population growth is slightly higher than the average increase since 2005 of

360,000 per year. However, the current population growth rate is in line with the 2005 to 2017

average of 1.6% p.a. (see Chart 4). Net overseas migration (permanent and long-term arrivals

less departures) accounted for 63.2% of the population rise, increasing by 250,200. The

remainder came from a natural increase (births less deaths) of 145,400 people.

Chart 4: Australian estimated resident population (ERP) growth

Source: ABS, Australian Demographic Statistics September 2017

6

Australia’s population growth has accelerated since 2005 (Chart 4) largely due to a rise in net

migration. This acceleration has contributed to economic growth over this period but at the same

time, it is a response to it. As can be seen in Chart 5, annual net migration2 tends to lag

movements in the unemployment rate, as more people are attracted to growing labour demand

and fewer people choose to leave. During Australia’s last recession in 1990-91 for example,

unemployment rose above 11% in Q4 of 1992, followed by a fall in net migration as a proportion

of the population to an historical low of 0.2% in Q2 of 1993. Conversely, when unemployment

reached its most recent low of 4.2% in Q1 of 2008, annual net migration as a proportion of the

population rose to a high of 1.5% in Q4 of 2008. Most recently, stronger labour demand since

2015 has again coincided with accelerating population growth. But even with this latest

acceleration, net migration in the year to September 2017 remains well below previous peaks in

2012 and 2008 (both of which were related to temporary workers arriving for large-scale mining

construction projects that were under way at that time).

Chart 5: Australian unemployment and migration

Source: ABS, Australian Demographic Statistics September 2017;

ABS, Labour force Australia February 2018

All states experienced population increases in the year to September 2017, ranging from 0.6%

p.a. in South Australia to 2.4% p.a. in Victoria. Most new immigrants moved to either New South

Wales (98,800) or Victoria (88,500). Natural increases in the population occurred across all states,

with the highest numbers added in Victoria (42,000), followed by New South Wales (40,800) and

Queensland (30,600).

Queensland had the highest number of net interstate migrants in the year to September 2017 at

19,300, including a net flow of 12,000 people moving from New South Wales. The ABS projects

2 as a percentage of the population.

7

Queensland’s population to reach 5 million people in May 2018 after growing at 1.7% in the year

to September 2017. Net interstate migration also added to the population in Victoria and

Tasmania while New South Wales, South Australia and Western Australia all recorded net

interstate migration losses (see Chart 6).

Chart 6: Estimated resident population (ERP) growth rates, by state and type

Source: ABS, Australian Demographic Statistics September 2017

More information about Queensland’s economic outlook and emerging skill shortages is available

in our research note here.

8

This week’s data and events, 19 March – 23 March 2018

Day Date Data / event Data period Current release

Tue 20 Mar RBA Minutes Mar (M) Feb (M): N/A

Wed 21 Mar Department of Jobs and Small Business Skilled Vacancy Index

Feb (M) +10.5% p.a. (trend)

Thu 22 Mar ABS Labour Force Feb (M) Jan (M): emp. growth +3.3% p.a. Unemp. rate 5.5% (trend)

ABS Demographic Statistics Sep (Q) Jun (Q): population 24.7mn, +1.6% growth p.a.

Seek Job Ads Feb (M) +16.2 p.a.

M = monthly. Q = quarterly. H = half-yearly. A = annual. B= bi-annual. All data are seasonally adjusted unless otherwise noted.

Next week’s data and events, 26 March – 6 April 2018

Day Date Data/event Data period due for release

Previous release

Wed 28 Mar ABS Engineering Construction Activity Dec (Q) Sep (Q): value of work done 35.3bn, +68.9% p.a.

28 Mar ABS Household Use of Information Technology

2016-17 2014-15: 86% of households with internet access

Thu 29 Mar ABS Labour Force Detailed Quarterly Feb (Q) Nov (Q): -

29 Mar ABS Job Vacancies Feb (Q) Nov (Q): +16.8% p.a. (trend)

Tue 3 Apr Australian PMI® Mar (M) Feb (M): 57.5 points

3 Apr RBA cash rate decision Apr (M) Mar (M): 1.50%

3 Apr ABS Internet Activity Dec (H) Jun (H): 13.7 million internet

subscribers

Wed 4 Apr ABS Retail Trade Feb (M) Jan (M): turnover $26.2bn,

+0.1% m/m

4 Apr ABS Building Approvals Feb (M) Jan (M): no. of approvals

+12.0% p.a.

Thu 5 Apr Australian PSI® Mar (M) Feb (M): 54.0 points

ABS International Trade in Goods and

Services Feb (M)

Jan (M): imports $32.9bn, exports

$33.9bn

M = monthly. Q = quarterly. H = half-yearly. A = annual. All data are seasonally adjusted unless otherwise noted.

9

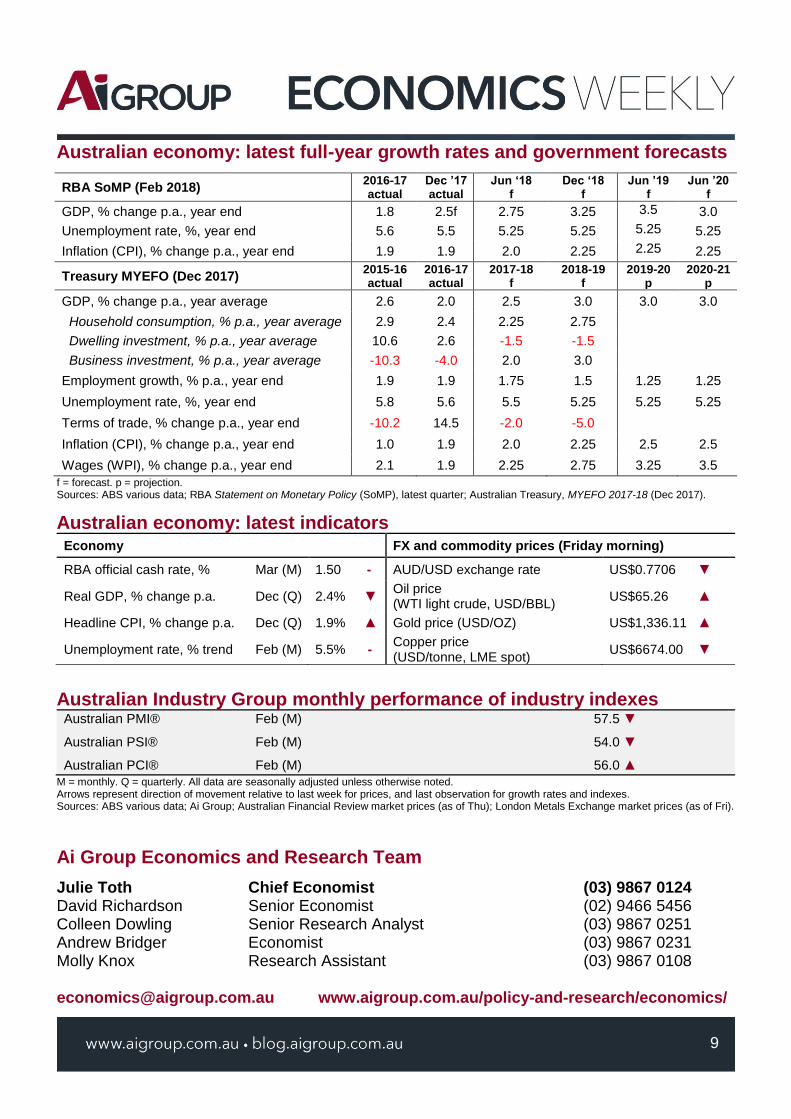

Australian economy: latest full-year growth rates and government forecasts

RBA SoMP (Feb 2018) 2016-17 actual

Dec ’17 actual

Jun ‘18 f

Dec ‘18 f

Jun ’19 f

Jun ’20 f

GDP, % change p.a., year end 1.8 2.5f 2.75 3.25 3.5 3.0

Unemployment rate, %, year end 5.6 5.5 5.25 5.25 5.25 5.25

Inflation (CPI), % change p.a., year end 1.9 1.9 2.0 2.25 2.25 2.25

Treasury MYEFO (Dec 2017) 2015-16 actual

2016-17 actual

2017-18 f

2018-19 f

2019-20 p

2020-21 p

GDP, % change p.a., year average 2.6 2.0 2.5 3.0 3.0 3.0

Household consumption, % p.a., year average 2.9 2.4 2.25 2.75

Dwelling investment, % p.a., year average 10.6 2.6 -1.5 -1.5

Business investment, % p.a., year average -10.3 -4.0 2.0 3.0

Employment growth, % p.a., year end 1.9 1.9 1.75 1.5 1.25 1.25

Unemployment rate, %, year end 5.8 5.6 5.5 5.25 5.25 5.25

Terms of trade, % change p.a., year end -10.2 14.5 -2.0 -5.0

Inflation (CPI), % change p.a., year end 1.0 1.9 2.0 2.25 2.5 2.5

Wages (WPI), % change p.a., year end 2.1 1.9 2.25 2.75 3.25 3.5

f = forecast. p = projection. Sources: ABS various data; RBA Statement on Monetary Policy (SoMP), latest quarter; Australian Treasury, MYEFO 2017-18 (Dec 2017).

Australian economy: latest indicators Economy FX and commodity prices (Friday morning)

RBA official cash rate, % Mar (M) 1.50 - AUD/USD exchange rate US$0.7706 ▼

Real GDP, % change p.a. Dec (Q) 2.4% ▼ Oil price (WTI light crude, USD/BBL)

US$65.26 ▲

Headline CPI, % change p.a. Dec (Q) 1.9% ▲ Gold price (USD/OZ) US$1,336.11 ▲

Unemployment rate, % trend Feb (M) 5.5% - Copper price (USD/tonne, LME spot)

US$6674.00 ▼

Australian Industry Group monthly performance of industry indexes Australian PMI® Feb (M) 57.5 ▼

Australian PSI® Feb (M) 54.0 ▼

Australian PCI® Feb (M) 56.0 ▲ M = monthly. Q = quarterly. All data are seasonally adjusted unless otherwise noted. Arrows represent direction of movement relative to last week for prices, and last observation for growth rates and indexes. Sources: ABS various data; Ai Group; Australian Financial Review market prices (as of Thu); London Metals Exchange market prices (as of Fri).

Ai Group Economics and Research Team

Julie Toth Chief Economist (03) 9867 0124 David Richardson Senior Economist (02) 9466 5456 Colleen Dowling Senior Research Analyst (03) 9867 0251 Andrew Bridger Economist (03) 9867 0231 Molly Knox Research Assistant (03) 9867 0108 [email protected] www.aigroup.com.au/policy-and-research/economics/