2.3 lessons learned project and partnership dispo final · •read lura closely – what ami levels...

TRANSCRIPT

June 12, 2018 www.novoco.com

Lessons Learned:

Project and Partnership Dispositions and Buy Outsfor the 2018 NH&RA Asset Management Conference

H. Blair KincerPartner, Bethesda

[email protected] & Company LLP

240.235.1704

Value of LIHTC Property at (or near) Year 15

Purpose of Valuation -Review Partnership

Agreement

Dissolution of Partnership

Buyout of Interest (GP, LP)

Partnership Agreement Valuation Stipulations – Who,

What, How

June 12, 2018 www.novoco.com

Value of LIHTC Property at (or near) Year 15

Internal Property Valuation

Problems – GP & LP value may be

substantially different

Many partnership agreements require an independent appraisal

Market Value – Underlying Real Estate Asset first

More supportable for legal proceedings

Unbiased third party opinion of value, subject

to the scope of work

June 12, 2018 www.novoco.com

Value of LIHTC Property at (or near) Year 15

How do you Value at Year 15?

Market Value –assuming continued

affordability restrictions

Market Value –assuming Market Rate

(hypothetical)

Market Value – assuming 3 year conversion from

affordable to market rate (Qualified Contract –

voids LURA)

June 12, 2018 www.novoco.com

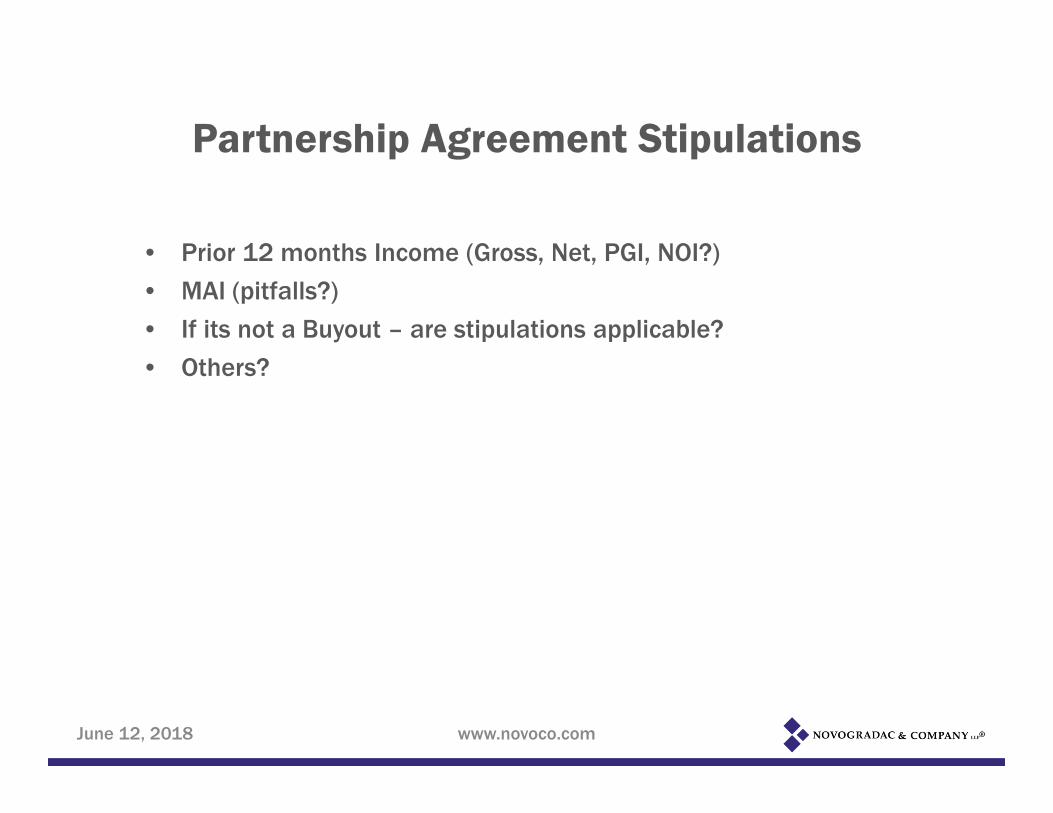

Partnership Agreement Stipulations

• Prior 12 months Income (Gross, Net, PGI, NOI?)

• MAI (pitfalls?)

• If its not a Buyout – are stipulations applicable?

• Others?

June 12, 2018 www.novoco.com

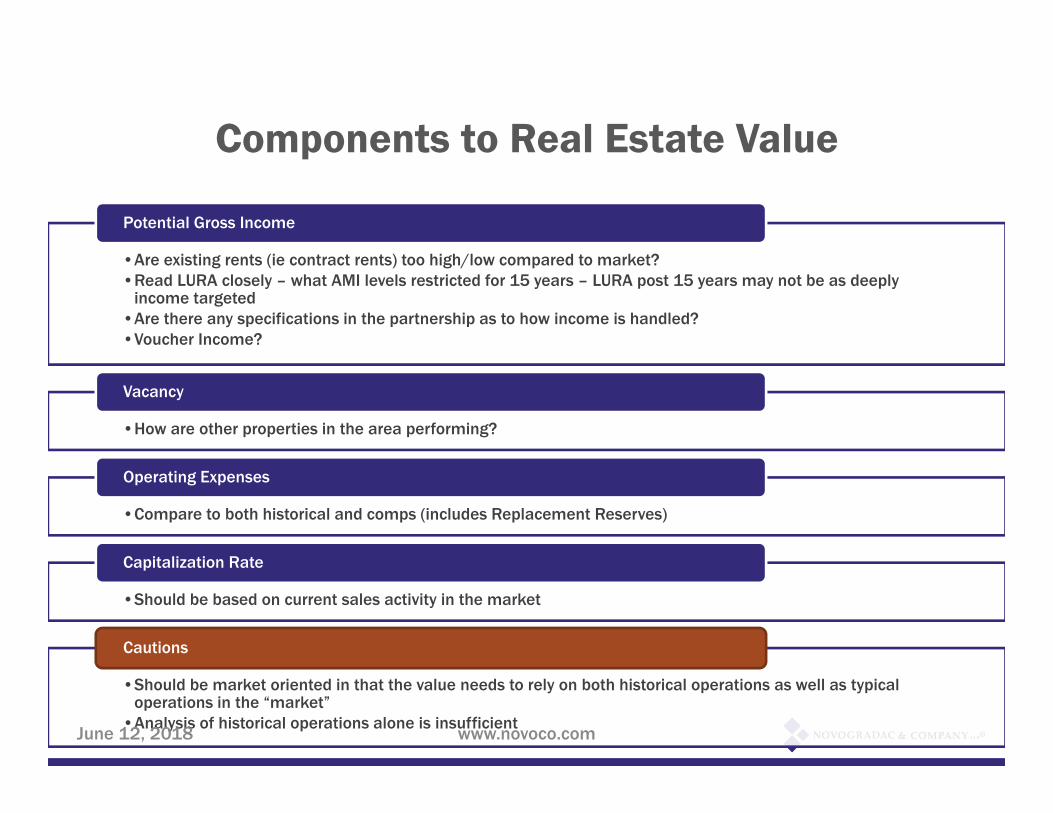

Components to Real Estate Value

•Are existing rents (ie contract rents) too high/low compared to market? •Read LURA closely – what AMI levels restricted for 15 years – LURA post 15 years may not be as deeply

income targeted•Are there any specifications in the partnership as to how income is handled?•Voucher Income?

Potential Gross Income

•How are other properties in the area performing?

Vacancy

•Compare to both historical and comps (includes Replacement Reserves)

Operating Expenses

•Should be based on current sales activity in the market

Capitalization Rate

•Should be market oriented in that the value needs to rely on both historical operations as well as typical operations in the “market”

•Analysis of historical operations alone is insufficient

Cautions

June 12, 2018 www.novoco.com

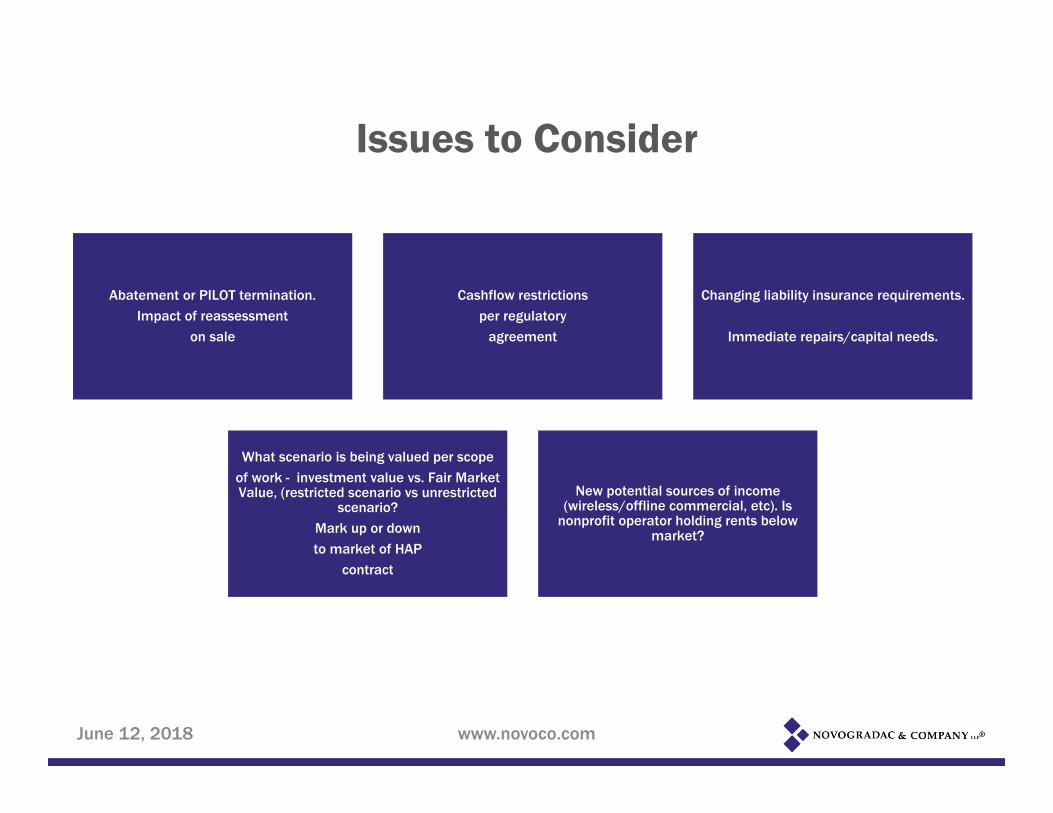

Issues to Consider

Abatement or PILOT termination. Impact of reassessment

on sale

Cashflow restrictions per regulatory

agreement

Changing liability insurance requirements.

Immediate repairs/capital needs.

What scenario is being valued per scope of work - investment value vs. Fair Market Value, (restricted scenario vs unrestricted

scenario? Mark up or down to market of HAP

contract

New potential sources of income (wireless/offline commercial, etc). Is

nonprofit operator holding rents below market?

June 12, 2018 www.novoco.com

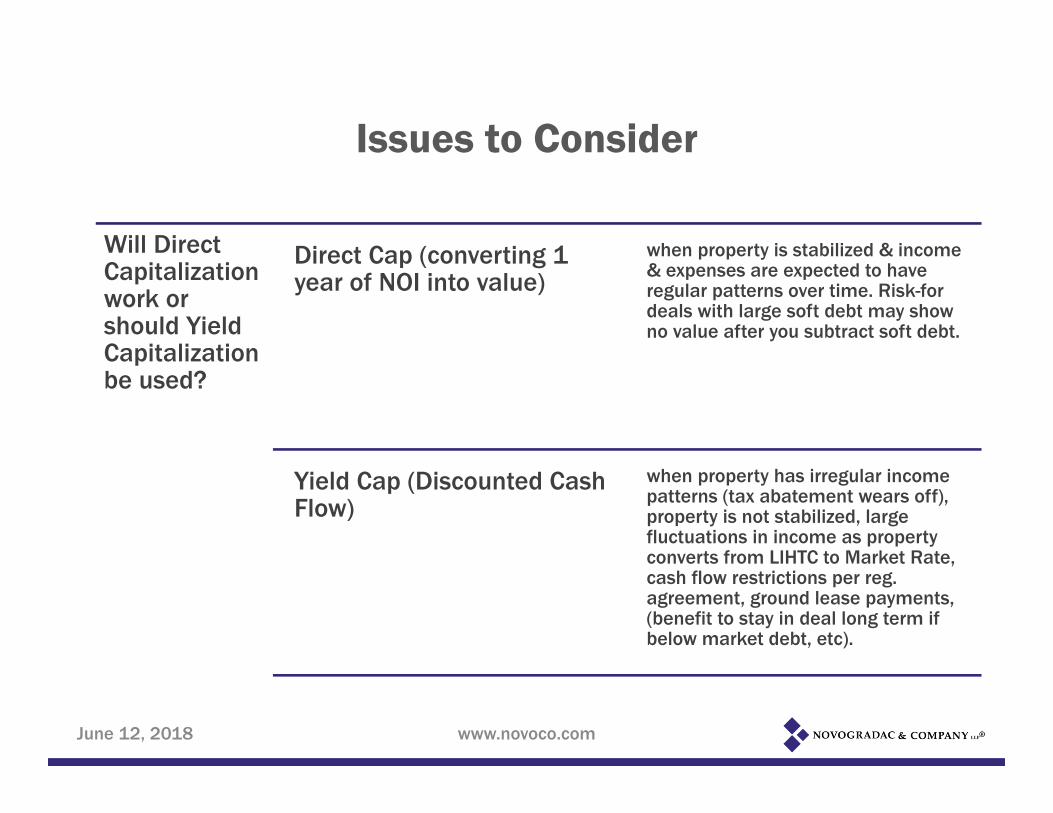

Issues to Consider

Will Direct Capitalization work or should Yield Capitalization be used?

Direct Cap (converting 1 year of NOI into value)

when property is stabilized & income & expenses are expected to have regular patterns over time. Risk-for deals with large soft debt may show no value after you subtract soft debt.

Yield Cap (Discounted Cash Flow)

when property has irregular income patterns (tax abatement wears off), property is not stabilized, large fluctuations in income as property converts from LIHTC to Market Rate, cash flow restrictions per reg. agreement, ground lease payments, (benefit to stay in deal long term if below market debt, etc).

June 12, 2018 www.novoco.com

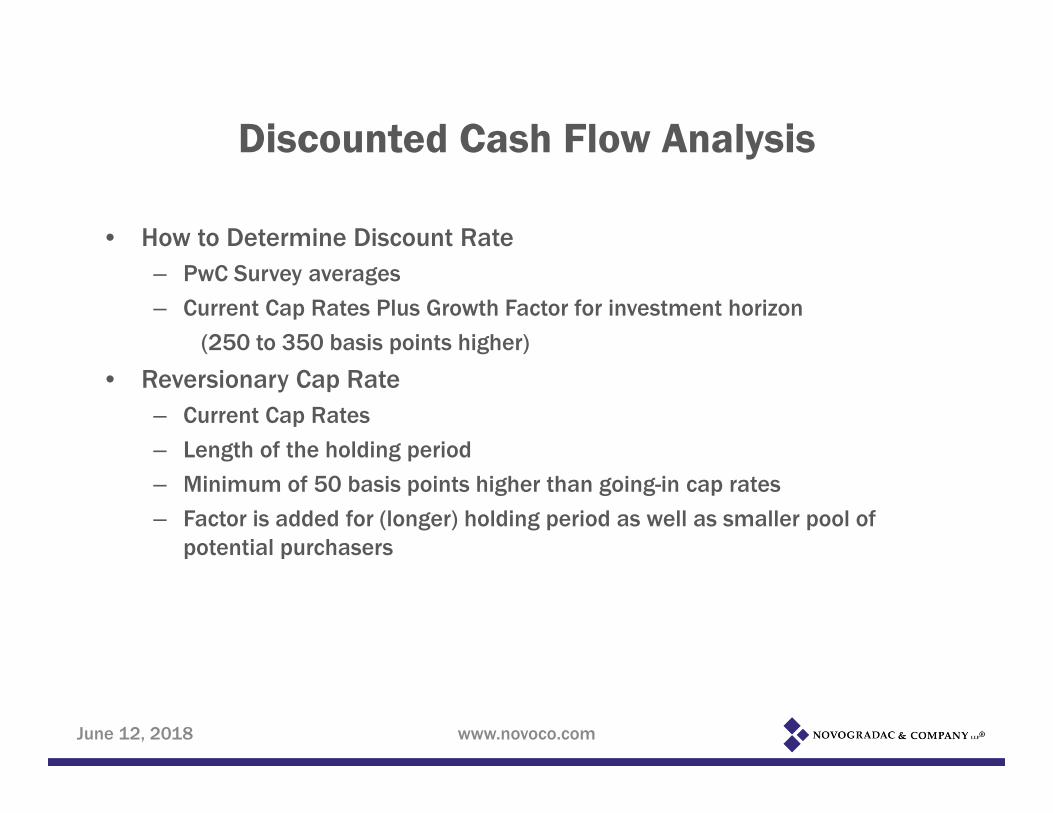

Discounted Cash Flow Analysis

• Appropriate discount rate?

• Appropriate reversionary cap rate?

• Typical holding period?

June 12, 2018 www.novoco.com

Discounted Cash Flow Analysis

• How to Determine Discount Rate– PwC Survey averages

– Current Cap Rates Plus Growth Factor for investment horizon

(250 to 350 basis points higher)

• Reversionary Cap Rate– Current Cap Rates

– Length of the holding period

– Minimum of 50 basis points higher than going-in cap rates

– Factor is added for (longer) holding period as well as smaller pool of potential purchasers

June 12, 2018 www.novoco.com

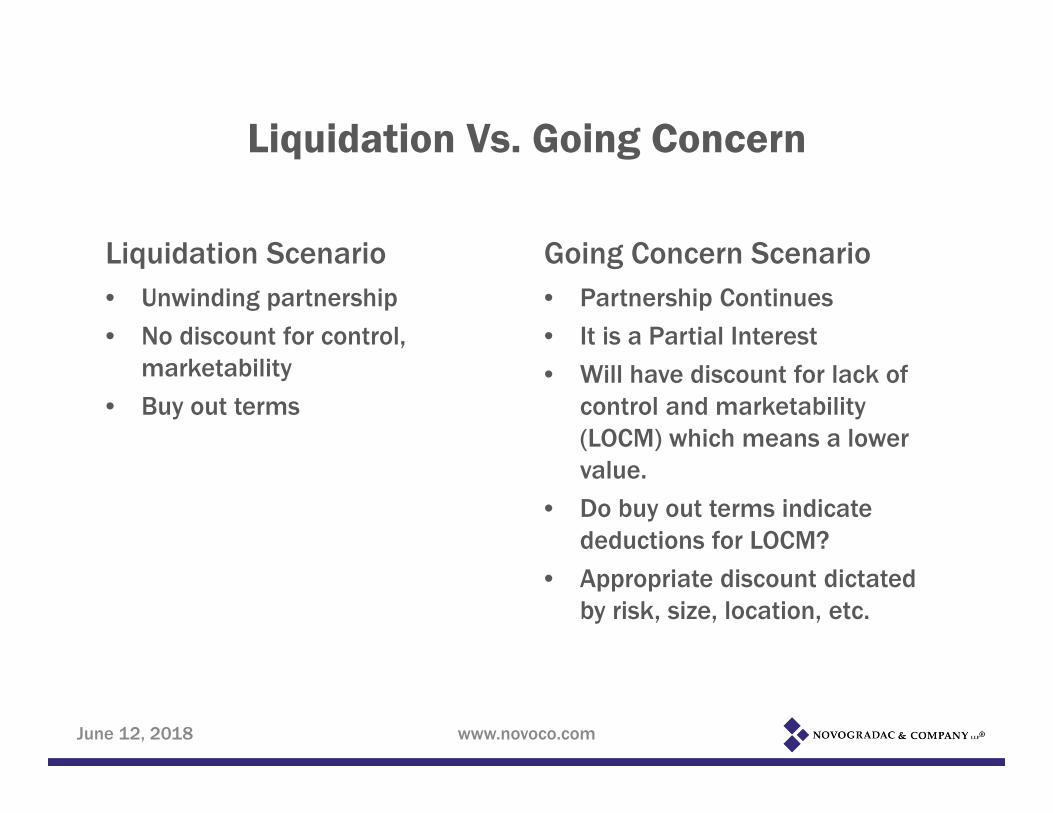

Liquidation Vs. Going Concern

Liquidation Scenario• Unwinding partnership

• No discount for control, marketability

• Buy out terms

Going Concern Scenario• Partnership Continues

• It is a Partial Interest

• Will have discount for lack of control and marketability (LOCM) which means a lower value.

• Do buy out terms indicate deductions for LOCM?

• Appropriate discount dictated by risk, size, location, etc.

June 12, 2018 www.novoco.com

June 12, 2018 www.novoco.com

Lessons Learned:

Project and Partnership Dispositions and Buy Outsfor the 2018 NH&RA Asset Management Conference

H. Blair KincerPartner, Bethesda

[email protected] & Company LLP

240.235.1704

Lessons Learned:

Project and PartnershipDispostions and Buy Outs

Katherine AlitzBoston Capital

NH&RAJune 12, 2018

Lessons Learned

Boston Capital’s approach to Year 15 continues to evolve.

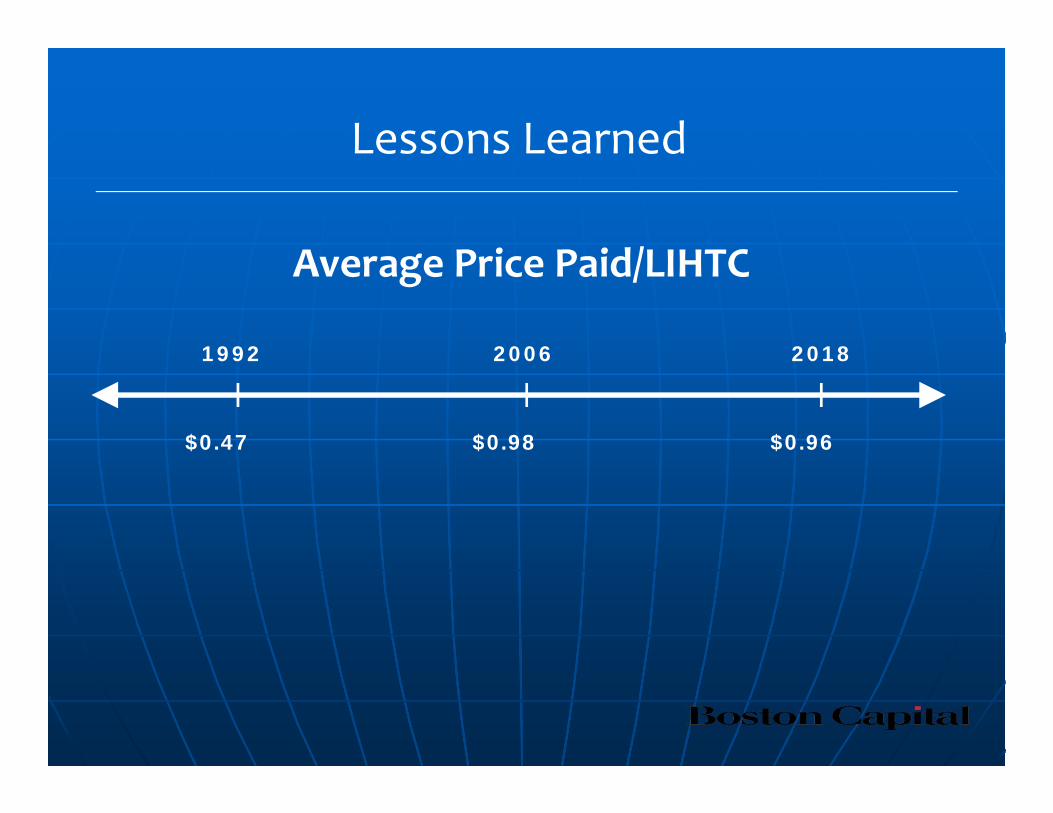

Average Price Paid/LIHTC

1992 20182006

$0.47 $0.96$0.98

Lessons Learned

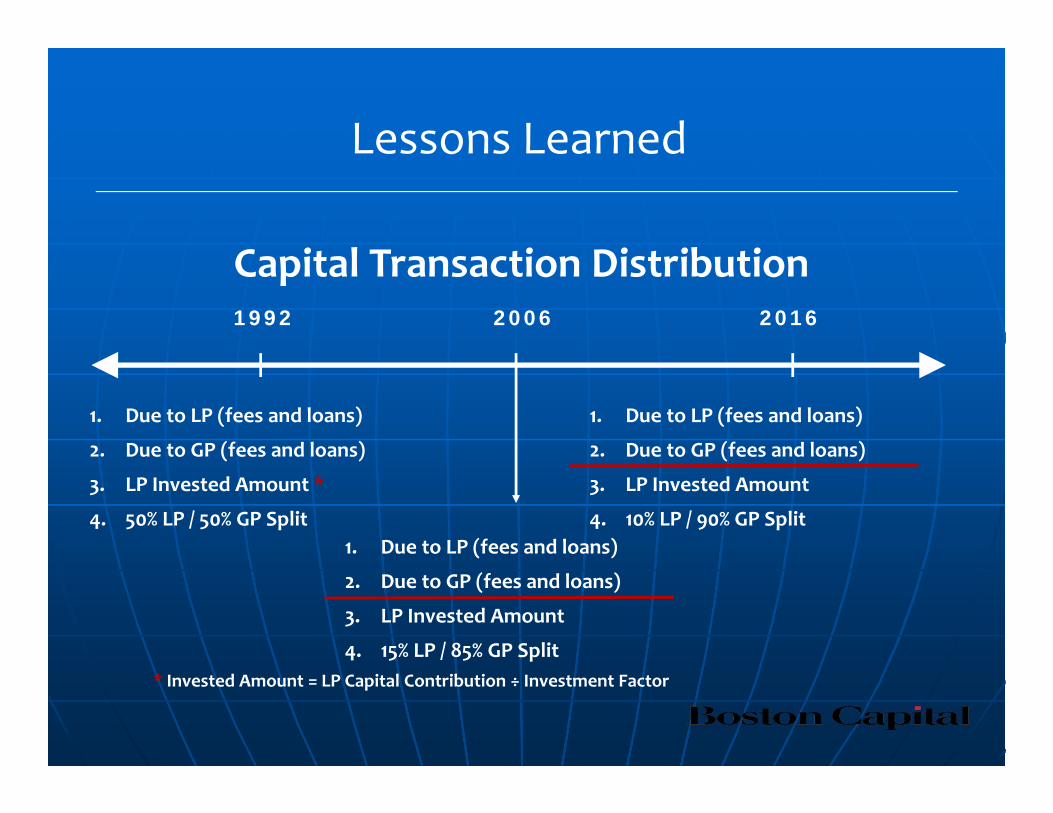

Capital Transaction Distribution1992 20162006

1. Due to LP (fees and loans)

2. Due to GP (fees and loans)

3. LP Invested Amount *

4. 50% LP / 50% GP Split

1. Due to LP (fees and loans)

2. Due to GP (fees and loans)

3. LP Invested Amount

4. 10% LP / 90% GP Split1. Due to LP (fees and loans)

2. Due to GP (fees and loans)

3. LP Invested Amount

4. 15% LP / 85% GP Split* Invested Amount = LP Capital Contribution ÷ Investment Factor

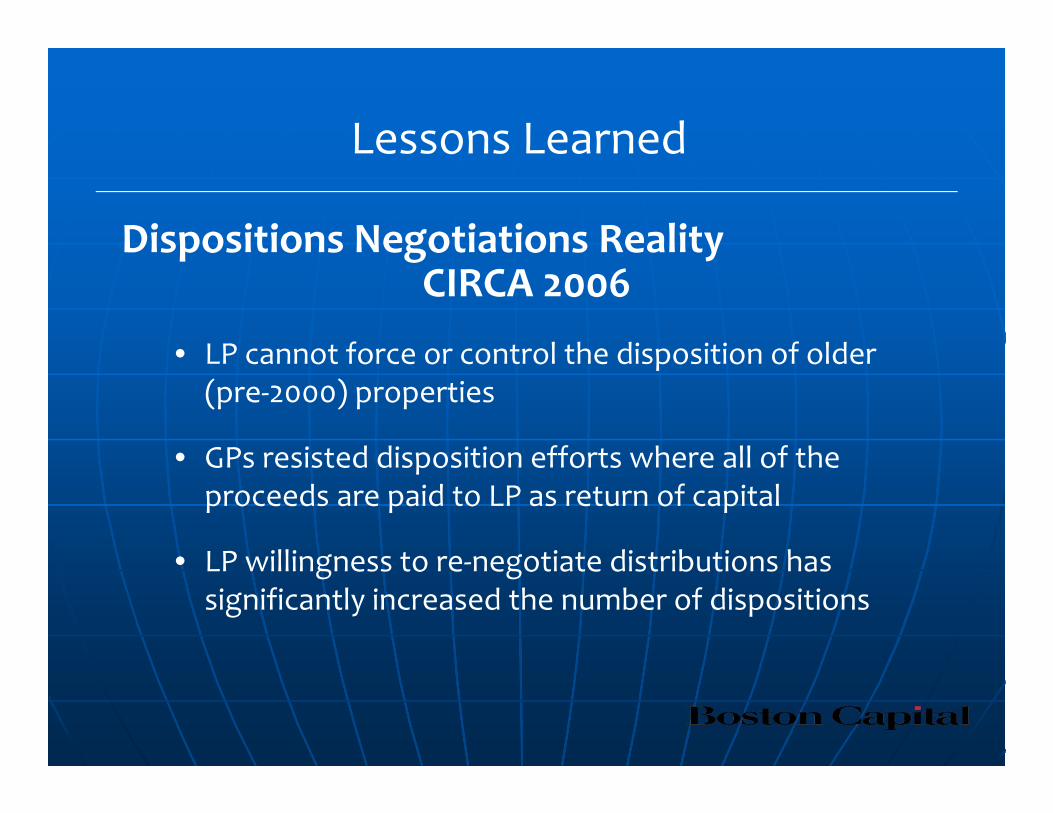

Lessons Learned

Dispositions Negotiations Reality CIRCA 2006

• LP cannot force or control the disposition of older (pre‐2000) properties

• GPs resisted disposition efforts where all of the proceeds are paid to LP as return of capital

• LP willingness to re‐negotiate distributions has significantly increased the number of dispositions

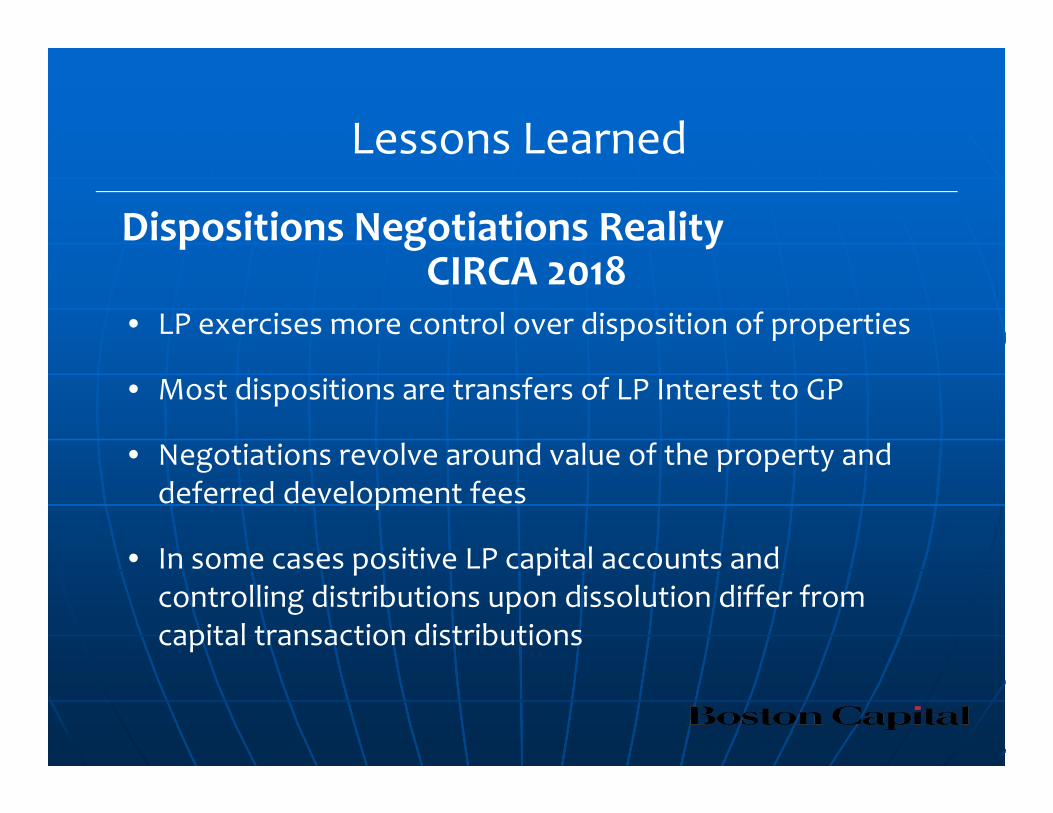

Lessons Learned

Dispositions Negotiations Reality CIRCA 2018

• LP exercises more control over disposition of properties

• Most dispositions are transfers of LP Interest to GP

• Negotiations revolve around value of the property and deferred development fees

• In some cases positive LP capital accounts and controlling distributions upon dissolution differ from capital transaction distributions

Lessons Learned

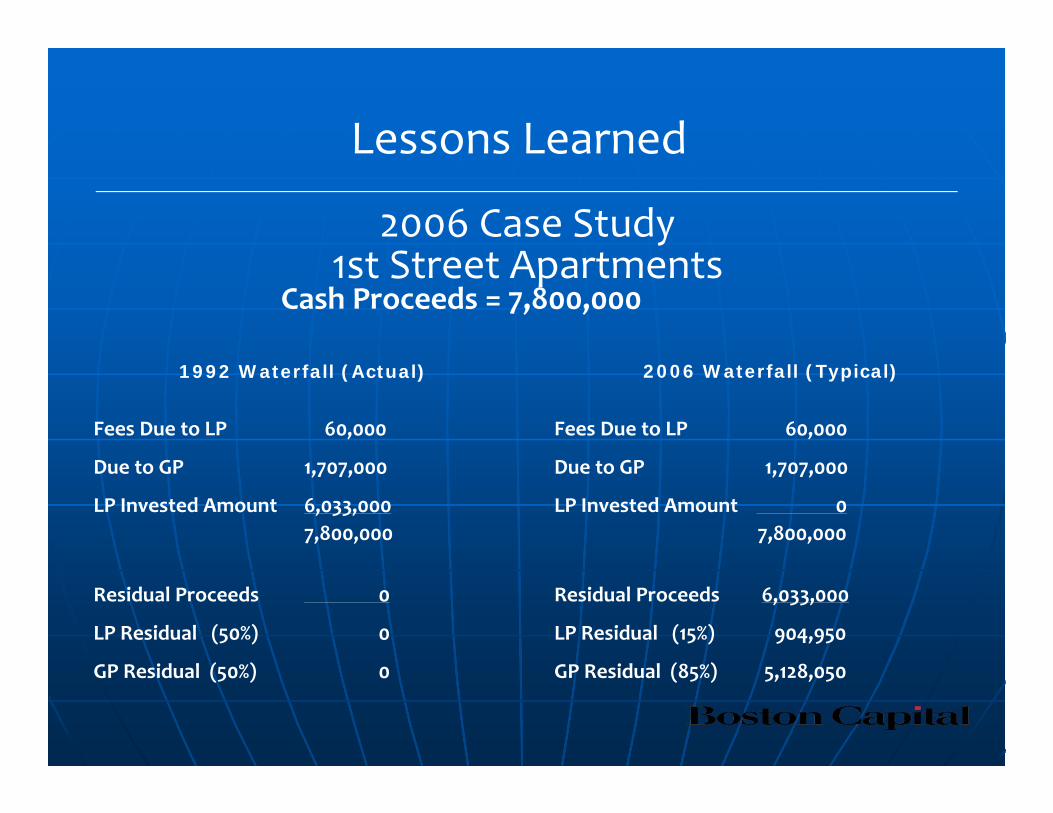

2006 Case Study1st Street Apartments

1992 Waterfall (Actual) 2006 Waterfall (Typical)

Fees Due to LP 60,000

Due to GP 1,707,000

LP Invested Amount 6,033,0007,800,000

Residual Proceeds 0

LP Residual (50%) 0

GP Residual (50%) 0

Cash Proceeds = 7,800,000

Fees Due to LP 60,000

Due to GP 1,707,000

LP Invested Amount 07,800,000

Residual Proceeds 6,033,000

LP Residual (15%) 904,950

GP Residual (85%) 5,128,050

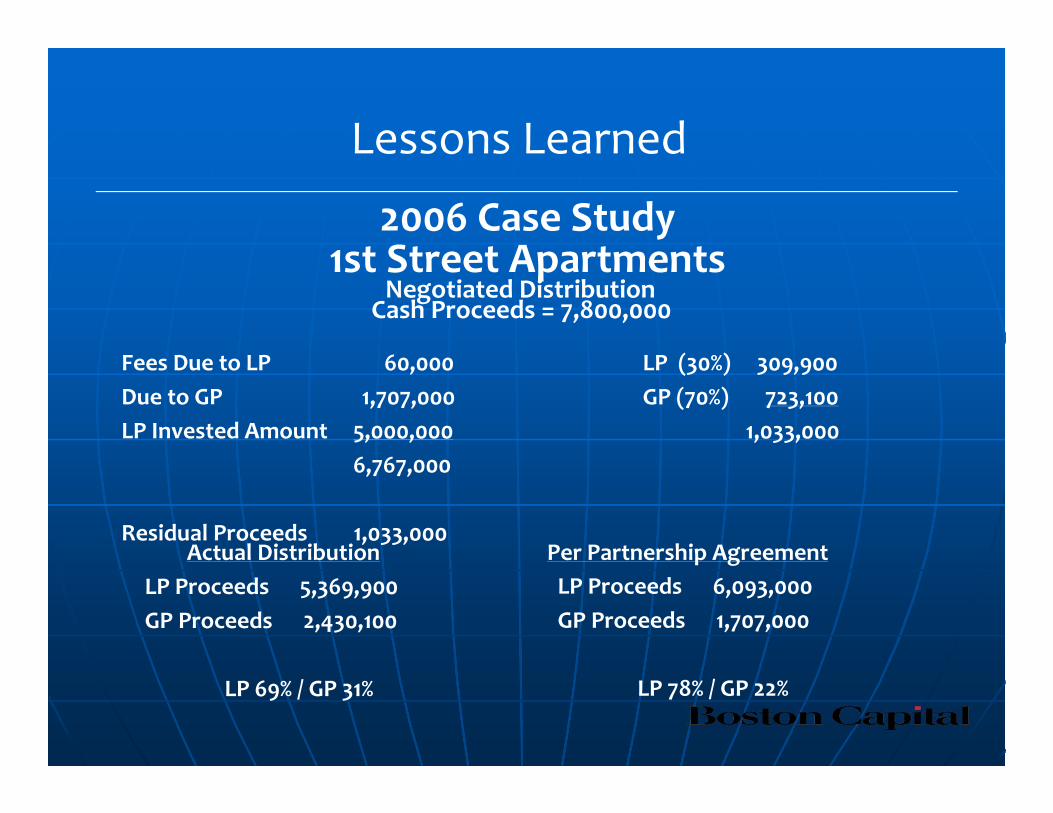

Lessons Learned

2006 Case Study1st Street Apartments

Fees Due to LP 60,000Due to GP 1,707,000LP Invested Amount 5,000,000

6,767,000

Residual Proceeds 1,033,000

Cash Proceeds = 7,800,000

LP Proceeds 5,369,900GP Proceeds 2,430,100

LP 69% / GP 31%

Negotiated Distribution

LP Proceeds 6,093,000GP Proceeds 1,707,000

LP 78% / GP 22%

Per Partnership AgreementActual Distribution

LP (30%) 309,900GP (70%) 723,100

1,033,000

Lessons Learned

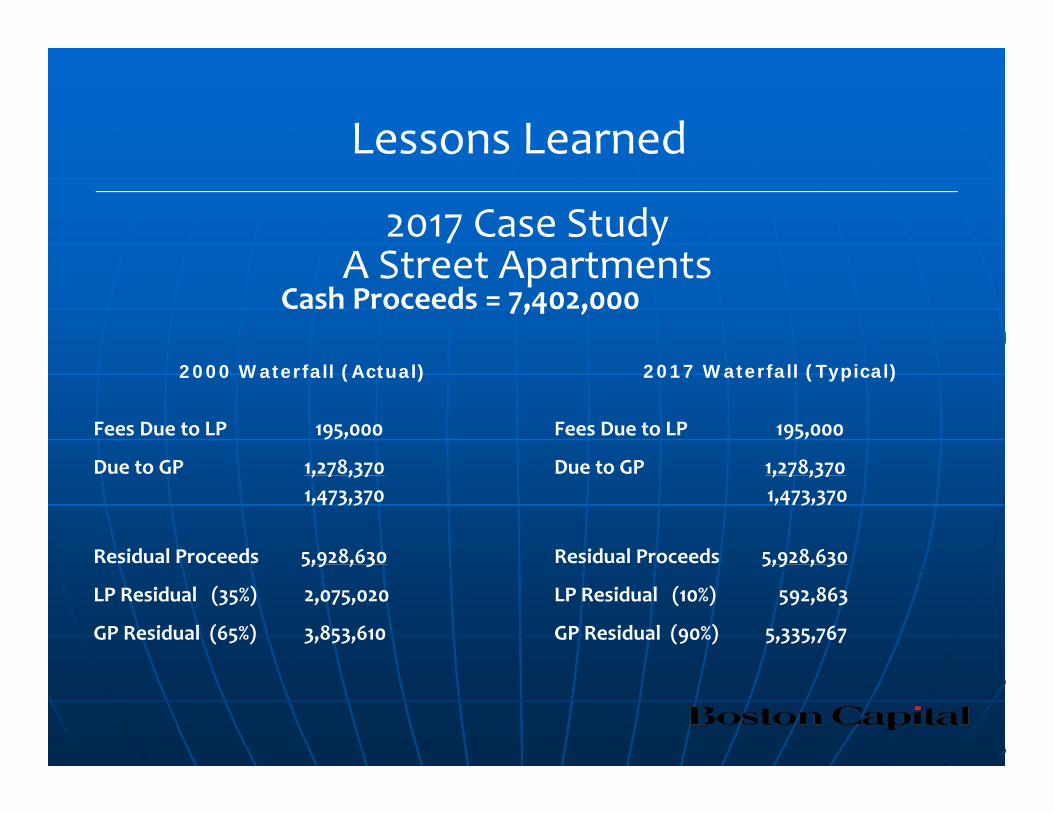

2017 Case StudyA Street Apartments

2000 Waterfall (Actual) 2017 Waterfall (Typical)

Fees Due to LP 195,000

Due to GP 1,278,3701,473,370

Residual Proceeds 5,928,630

LP Residual (35%) 2,075,020

GP Residual (65%) 3,853,610

Cash Proceeds = 7,402,000

Fees Due to LP 195,000

Due to GP 1,278,3701,473,370

Residual Proceeds 5,928,630

LP Residual (10%) 592,863

GP Residual (90%) 5,335,767

Lessons Learned

2017 Case StudyA Street Apartments

Due to LP 195,000Due to GP 1,278,370

1,473,370

Residual Proceeds 5,928,630

Cash Proceeds = 7,402,000

LP Proceeds 2,270,020GP Proceeds 5,131,980

LP 31% / GP 69%

Negotiated Distribution

Per Partnership AgreementActual Distribution

LP (35%) 2,075,020GP (65%) 3,853,610

LP Proceeds 2,270,020GP Proceeds 5,131,980

LP 31% / GP 69%

Lessons Learned

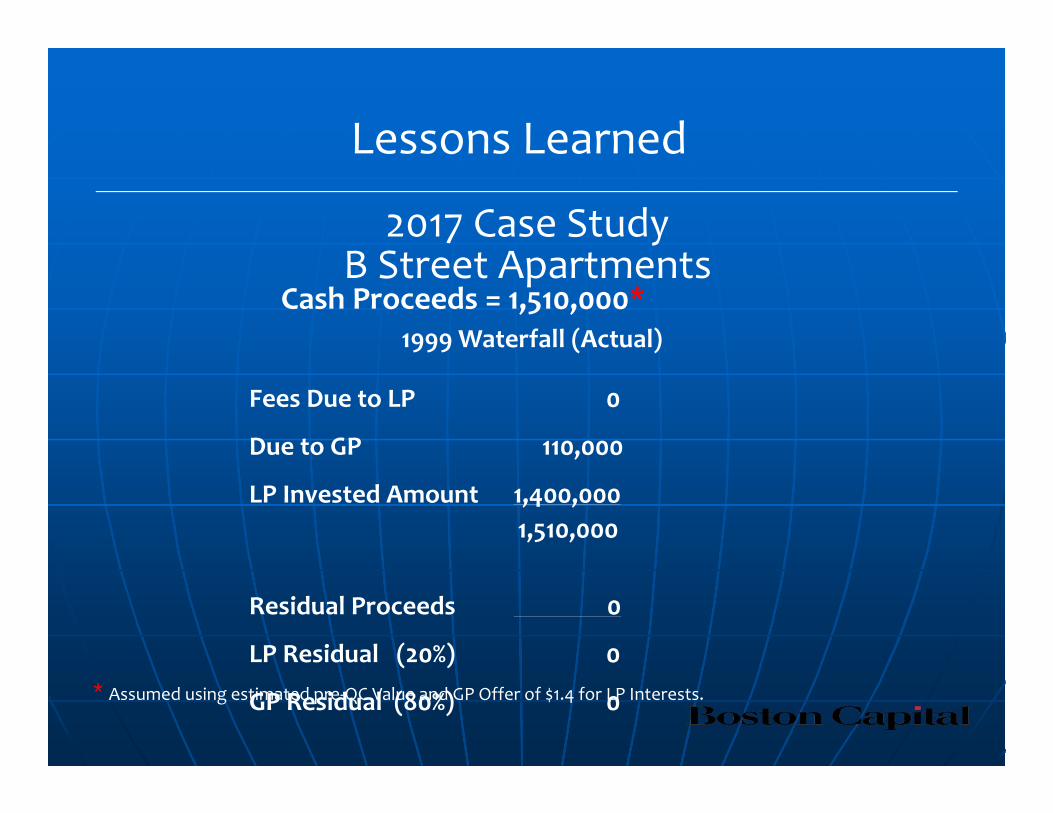

2017 Case StudyB Street Apartments

1999 Waterfall (Actual)

Fees Due to LP 0

Due to GP 110,000

LP Invested Amount 1,400,0001,510,000

Residual Proceeds 0

LP Residual (20%) 0

GP Residual (80%) 0

Cash Proceeds = 1,510,000*

*Assumed using estimated pre‐QC Value and GP Offer of $1.4 for LP Interests.

Lessons Learned

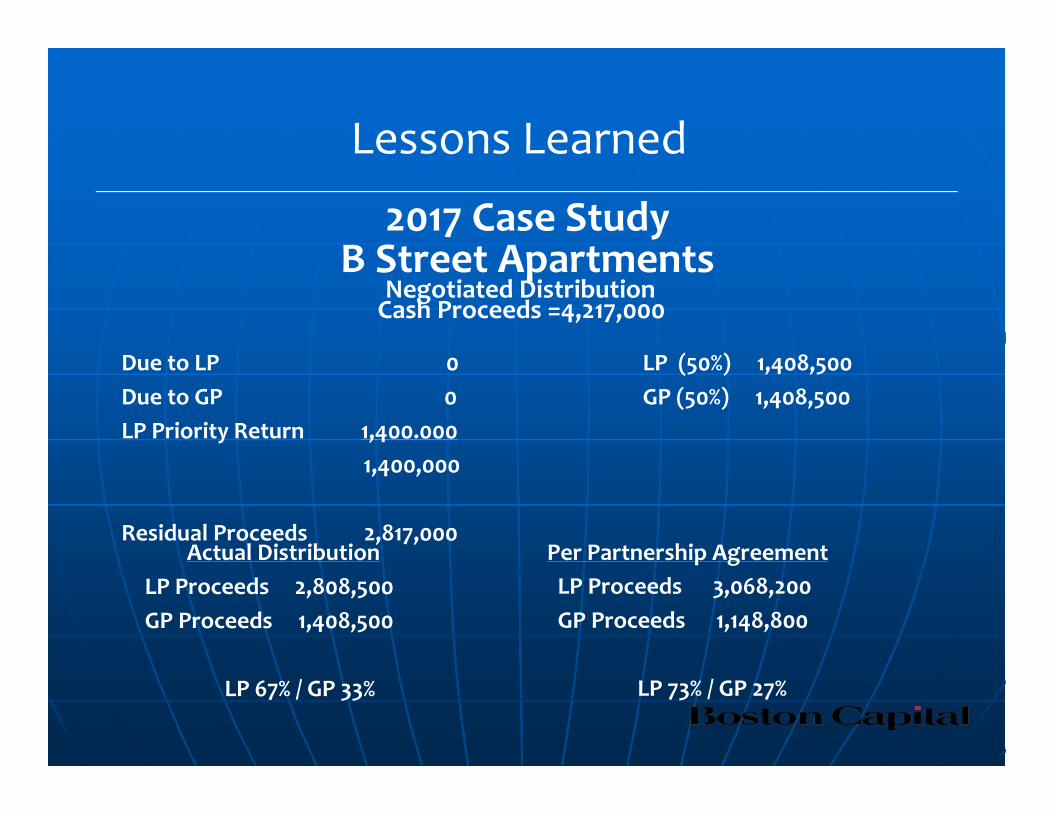

2017 Case StudyB Street Apartments

Due to LP 0Due to GP 0LP Priority Return 1,400.000

1,400,000

Residual Proceeds 2,817,000

Cash Proceeds =4,217,000

LP Proceeds 2,808,500 GP Proceeds 1,408,500

LP 67% / GP 33%

Negotiated Distribution

LP Proceeds 3,068,200GP Proceeds 1,148,800

LP 73% / GP 27%

Per Partnership AgreementActual Distribution

LP (50%) 1,408,500GP (50%) 1,408,500

Lessons Learned

2017 Case StudyC Street Apartments

Waterfall (Capital Transactions)

Waterfall (Dissolution)

Fees Due to LP 5,000

Due to GP 349,000

> LP Capital or LP Tax 0354,000

Residual Proceeds 4,898,000

LP Residual (10%) 490,000

GP Residual (90%) 4,408,000

Cash Proceeds = 5,252,000

Positive LP Capital 3,362,792

Residual Proceeds 1,889,208

LP Residual (10%) 188,918

GP Residual (90%) 1,700,265

Lessons Learned

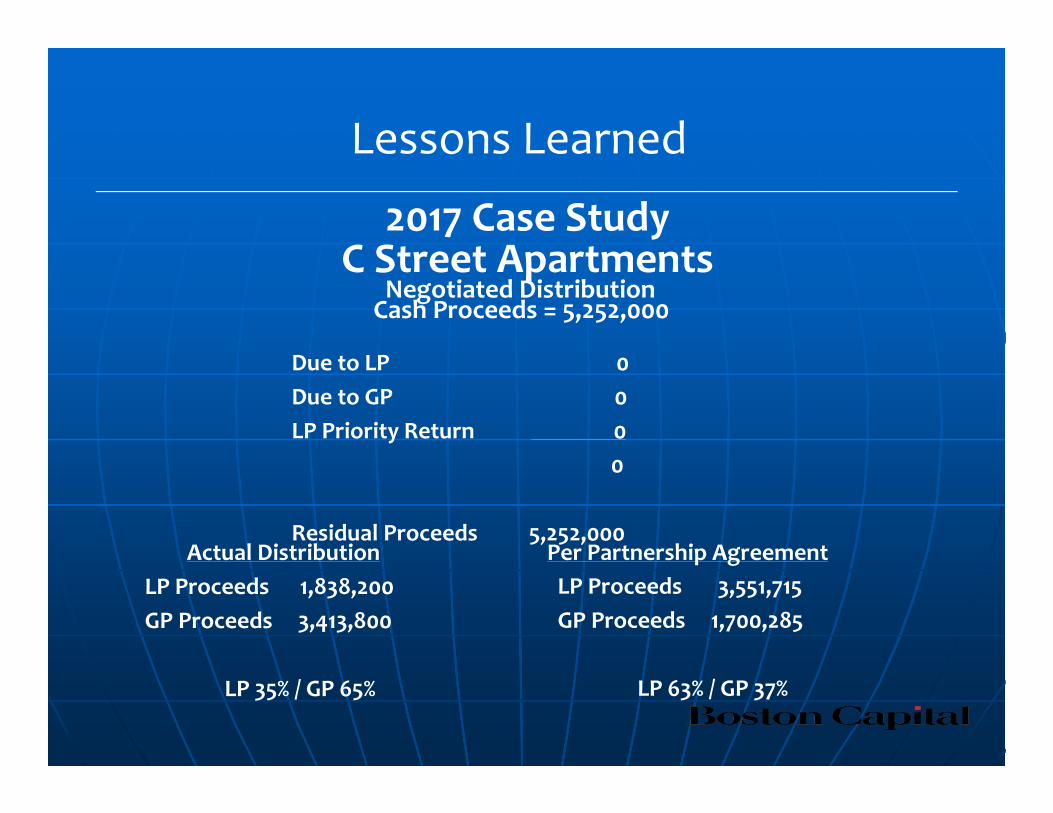

2017 Case StudyC Street Apartments

Due to LP 0Due to GP 0LP Priority Return 0

0

Residual Proceeds 5,252,000

Cash Proceeds = 5,252,000

LP Proceeds 1,838,200GP Proceeds 3,413,800

LP 35% / GP 65%

Negotiated Distribution

LP Proceeds 3,551,715GP Proceeds 1,700,285

LP 63% / GP 37%

Per Partnership AgreementActual Distribution

Lessons Learned

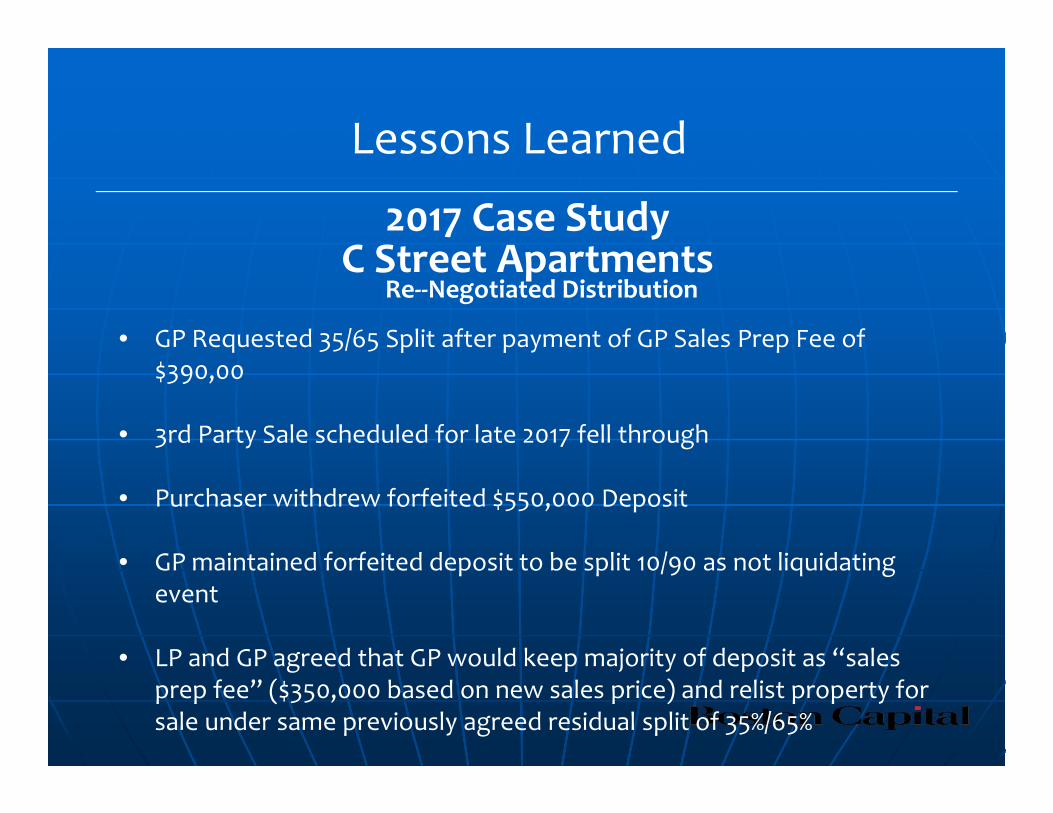

2017 Case StudyC Street Apartments

Re‐‐Negotiated Distribution

• GP Requested 35/65 Split after payment of GP Sales Prep Fee of $390,00

• 3rd Party Sale scheduled for late 2017 fell through

• Purchaser withdrew forfeited $550,000 Deposit

• GP maintained forfeited deposit to be split 10/90 as not liquidating event

• LP and GP agreed that GP would keep majority of deposit as “sales prep fee” ($350,000 based on new sales price) and relist property for sale under same previously agreed residual split of 35%/65%

Lessons Learned

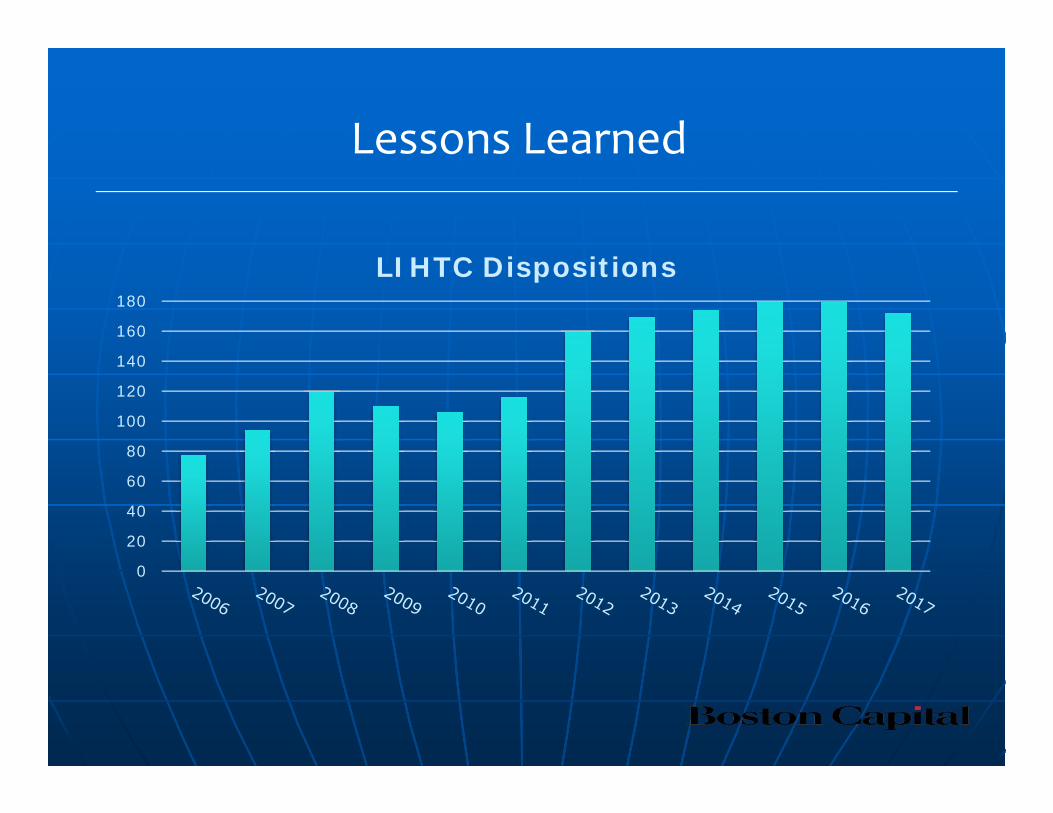

0

20

40

60

80

100

120

140

160

180

LIHTC Dispositions

Lessons Learned

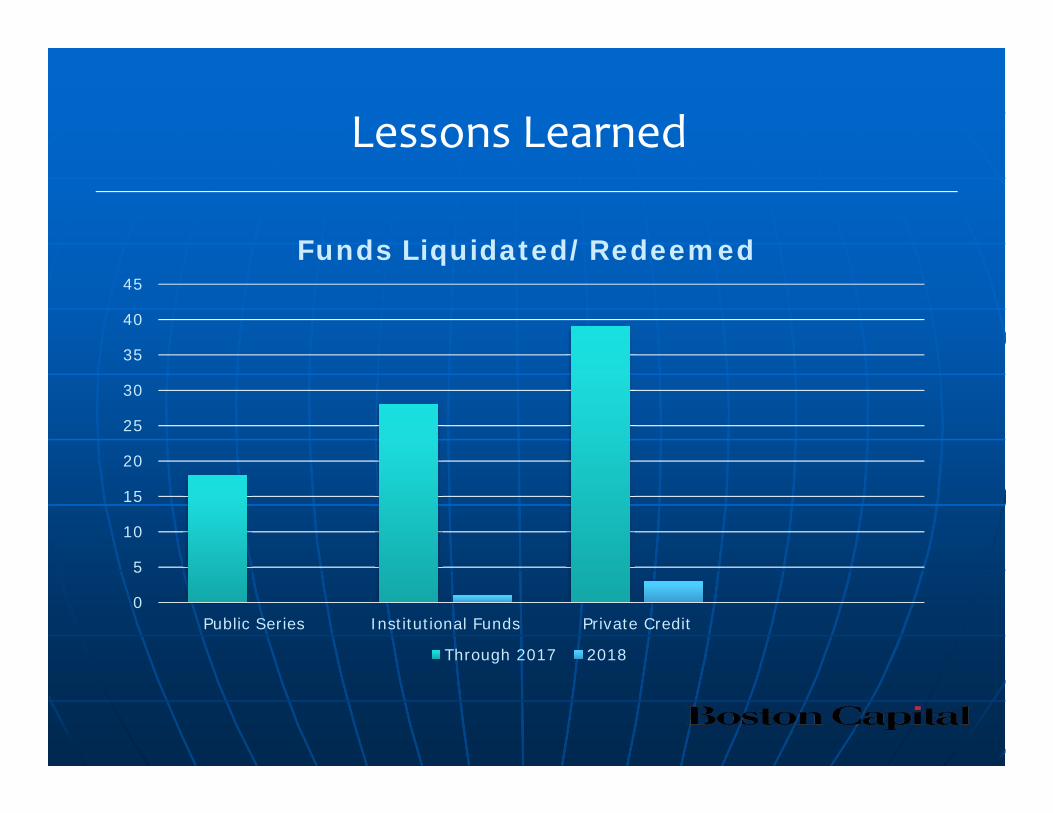

0

5

10

15

20

25

30

35

40

45

Public Series Institutional Funds Private Credit

Funds Liquidated/Redeemed

Through 2017 2018

Lessons Learned

Year 15 StrategiesLessons Learned

June 12, 2018 National Housing & Rehabilitation Association2018 Asset Management SymposiumBethesda, MDPresenter:Sean Barnes, Sr. Disposition Manager, Asset Management

31

EXIT STRATEGIES: POSSIBLE SCENARIOS

Right of First Refusal to purchase property

Buyout option to purchase partnership interest

Purchase within compliance period (“Early Exit”)

“Puts”: Obligation to Purchase Sale to 3rd party

32

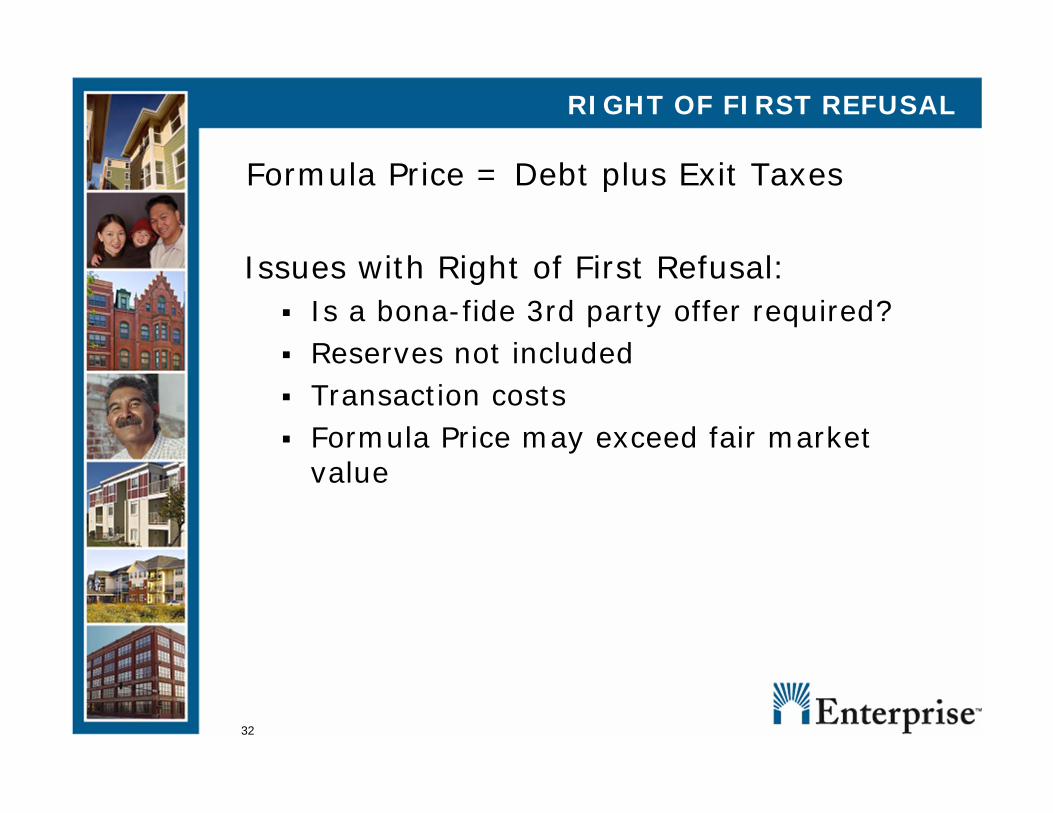

RIGHT OF FIRST REFUSAL

Formula Price = Debt plus Exit Taxes

Issues with Right of First Refusal: Is a bona-fide 3rd party offer required? Reserves not included Transaction costs Formula Price may exceed fair market

value

33

BUYOUT OPTION OF PARTNERSHIP INTEREST

Typically, option price is greater of:

Fair Market Value of Partnership Interest (defined as sale of property and liquidation of partnership)

Or Unpaid Benefits plus Exit Taxes

34

CASE STUDIES

Exit of Limited Partner:Alternative Strategies

1. Non Profit ROFR w/o Equity2. Non Profit ROFR w/ Equity

35

STUDY#1:Non-Profit ROFR with No Equity

PROJECT OVERVIEW

54 units

Located in suburbs of Baltimore, MD.

Serving seniors 62 and over

30%, 50% and 60% AMI

PIS 4/30/2002

LIHTC compliance period expired 2016

Extended Use Restrictions expire 2041

36

STUDY#1:Non-Profit ROFR with No Equity

NEGOTIATION POINTSGP holds the Right of First Refusal to purchase property for debt + exit taxes. LP potentially would receive $111,857.

GP offers to assume limited partners interest citing limitation on value:

Large surplus cash loan

The project cannot be recapitalized – restrictions on re-syndication

Large prepayment penalty - the project cannot be refinanced.

Significant capital needs, > $700K.

37

STUDY#1:Non-Profit ROFR with No Equity

PARTNERSHIP ECONOMICSProperty NOI $144,731Cap Rate 6.8%Property Value $2,128,397Plus

Operating Reserves $77,037Replacement Reserves $109,554T&I Escrows $15,794Cash in Bank $59,777

$262,162Less

AP/Current Accruals $6,575Fees Payable $6,872Debt $2,956,748

$2,970,195

Net Assets $(579,636)

38

STUDY#1:Non-Profit ROFR with No Equity

PROJECT ECONOMICSProperty Value $2,128,397Projected Debt $2,956,748Other Liabilities $13,447Cash & Reserves $262,162

Capital Account Balances Residual Splits (LPA)GP $111,857.50 50% 80%LP $111,857.50 50% 20%Total $223,715 100% 100%

SCENARIO Property Value

Assets (sale proceeds + net assets)

LP Proceeds per Residual Split

LP Proceeds per Capital Accounts

Sale of Property/Dissolution 2,128,397$ (579,636)$ ‐ ‐$ Buyout Option 2,128,397$ (579,636)$ ‐ ‐$ ROFR Dissolution 2,956,748$ 223,715$ 111,857.50$

Negotiated Sale Amount Debt

FINANCIAL SUMMARY

VALUATION SUMMARY

39

STUDY#1:Non-Profit ROFR with No Equity

VIEW FROM THE FUND Business Purpose: includes long term

preservation after fund exit Investor benefits delivered Fund IRR exceeds target Partnership Agreement provides ROFR

disposition in Y16 Assign limited partner interest to GP

for debt GP assumes all assets and liabilities

40

STUDY#2:Non-Profit ROFR with Equity

PROJECT OVERVIEW

221 units

Serving seniors 60 and over or disabled

30%, 50% and 60% AMI

PIS 9/15/2003

LIHTC compliance period expired 2017

Extended Use Restrictions expire 2048

This is an active, current negotiation.

41

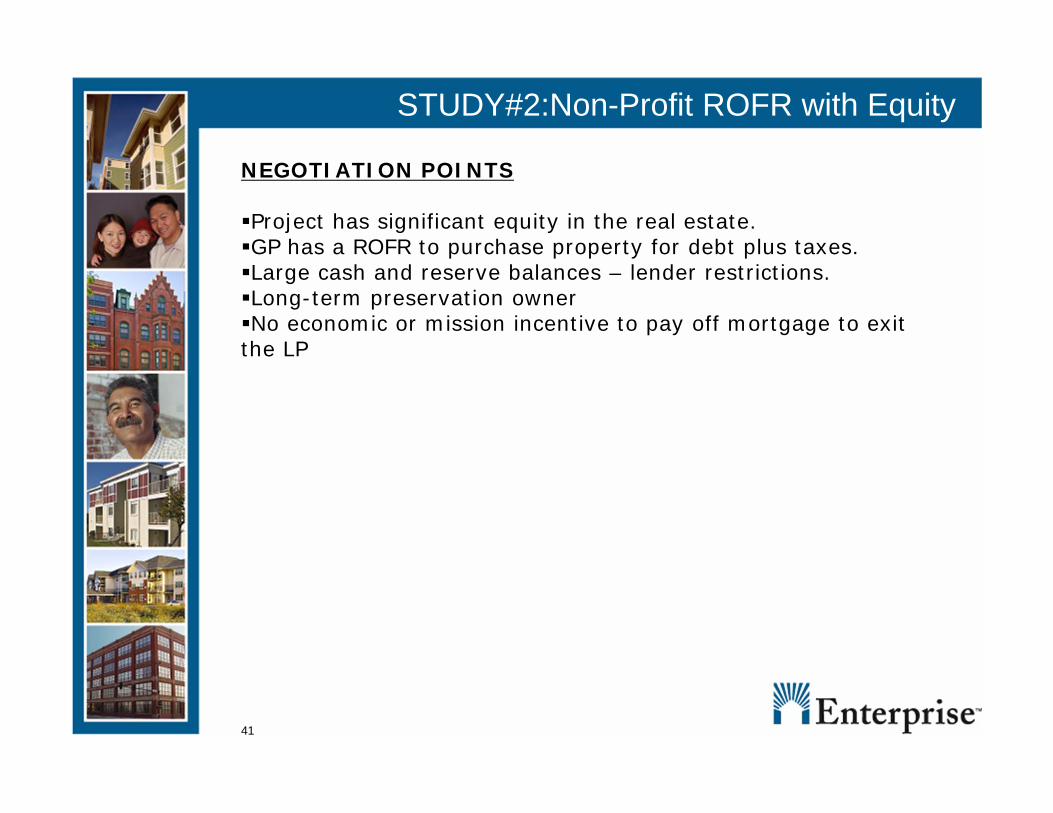

STUDY#2:Non-Profit ROFR with Equity

NEGOTIATION POINTS

Project has significant equity in the real estate.GP has a ROFR to purchase property for debt plus taxes.Large cash and reserve balances – lender restrictions.Long-term preservation ownerNo economic or mission incentive to pay off mortgage to exit the LP

42

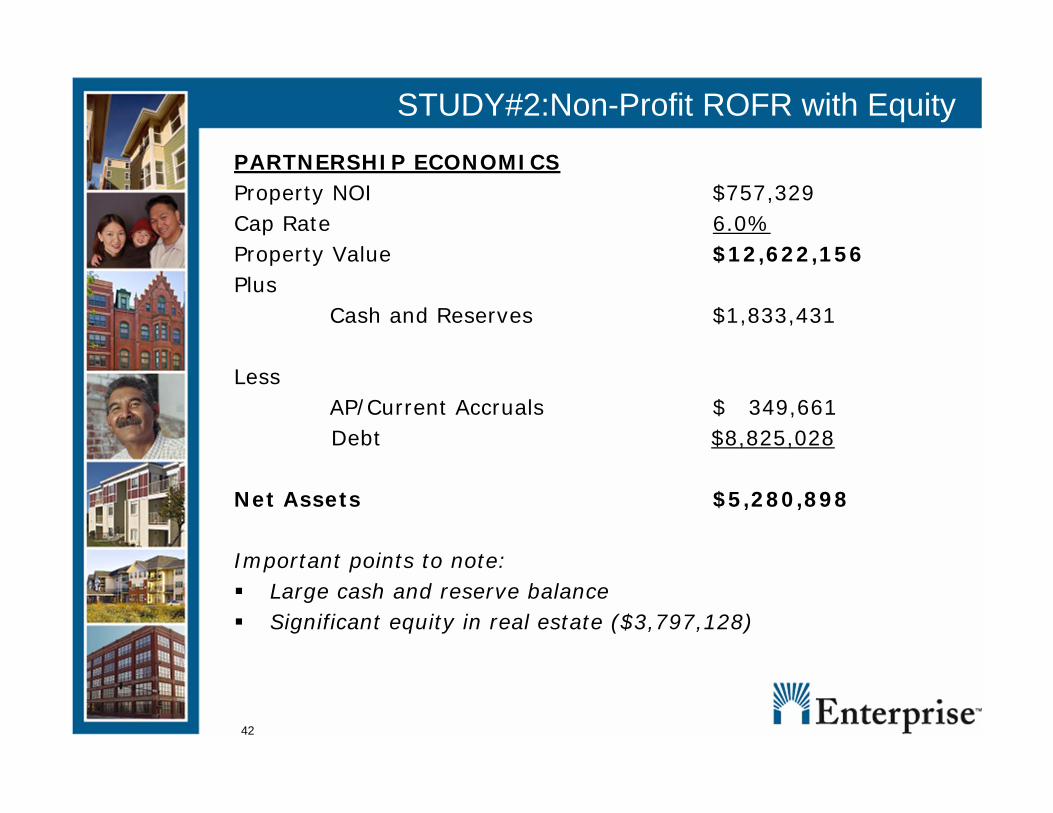

STUDY#2:Non-Profit ROFR with Equity

PARTNERSHIP ECONOMICSProperty NOI $757,329Cap Rate 6.0%Property Value $12,622,156Plus

Cash and Reserves $1,833,431

LessAP/Current Accruals $ 349,661Debt $8,825,028

Net Assets $5,280,898

Important points to note: Large cash and reserve balance Significant equity in real estate ($3,797,128)

43

STUDY#2:Non-Profit ROFR with Equity

ROFR CALCULATIONProperty Sale (debt + taxes) $8,825,028Less: Wind-up Costs 25,000Less: Debt 8,825,028Equals Sale Proceeds $(25,000)Plus Cash/Reserves 1,833,431Less: AP/Accruals/Fees 349,661

Total Proceeds*: $1,458,770

*Per liquidation provision, proceeds shall be distributed in accordance with capital accounts. In this case the GP has essentially a $0 capital account – entire amount would go to LP.

44

STUDY#2:Non-Profit ROFR with Equity

Impact of Lender Restrictions & Regulations on LP valuePublic purpose lender – mission to preserve affordable housing.

Partnership resources cannot be used to buyout a limited partner.

Favorable below-market financing (1%) - GP has no economic incentive to refinance.Extended land use agreement restricts rent through the year 2048 – partnership will need resources for capital needs.

45

STUDY#2:Non-Profit ROFR with Equity

ROFR CALCULATIONProperty Sale (debt + taxes) $8,825,028Less: Closing Costs 25,000Less: Debt 8,825,028Equals Sale Proceeds $(25,000)Plus Cash/Reserves 1,833,431Less: AP/Accruals/Fees 349,661

Total Proceeds $1,458,770Lender Restrictions (1,458,770)Distributable Proceeds: $0