21 - 1 corporations and bonds payable chapter 21

TRANSCRIPT

21 - 1

Corporations and Bonds Payable

Chapter 21

21 - 2

Journalizing the recording of bondsas well as

interest payments.

Learning Objective 1

21 - 3

Learning Unit 21-1

Each bond certificate is usually issued in denominations of $1,000.

The face value is the amount to be repaid at maturity date.

The contract rate is the stated interest rate. A bond indenture is a written agreement. A trustee usually monitors bond activities.

21 - 4

Learning Unit 21-1

Bonds are stated at a percentage of face value. Bonds are 100% if the bond rate and market

interest rate are equal. A bond discount occurs when the bond rate is

lower than market rate. Bonds are sold at a premium when the bond

rate is higher than market rate.

21 - 5

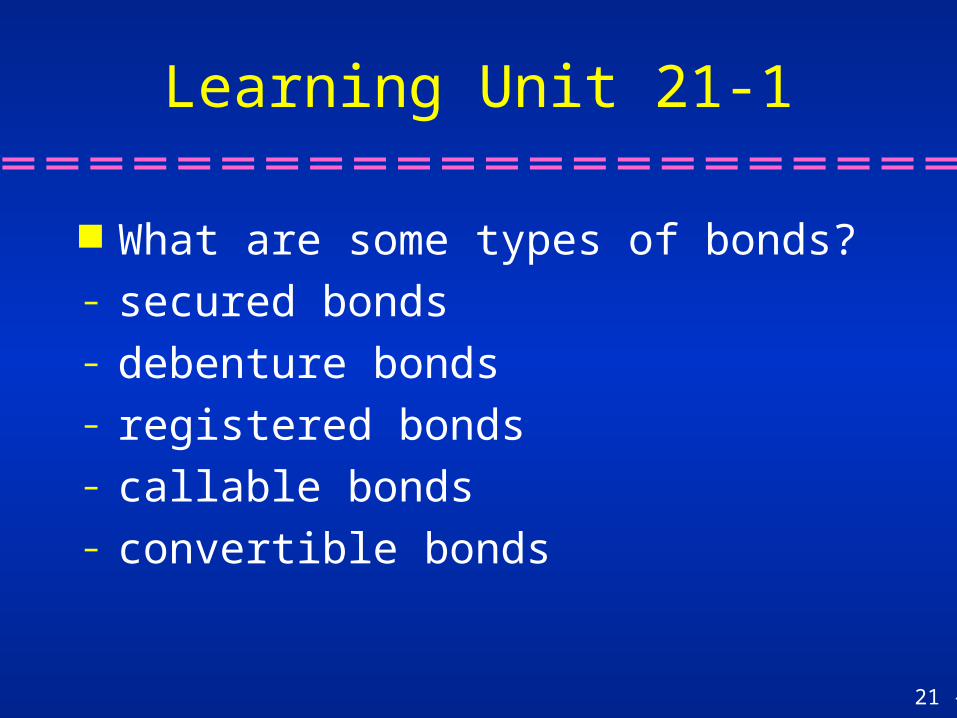

Learning Unit 21-1

What are some types of bonds?– secured bonds– debenture bonds– registered bonds– callable bonds– convertible bonds

21 - 6

Learning Unit 21-1

Bond issuance requires interest to be paid. Interest expense reduces net income,

thereby reducing income tax. Issuing bonds is borrowing while issuing

shares of stock means less ownership for existing shareholders (unless they buy the new shares).

21 - 7

Learning Unit 21-1

Interest on bonds must be paid each year. Dividend payments are optional. Bonds are a long-term liability. Interest is computed on a semi-annual basis.

21 - 8

Face value × Market rate at issuance date × 6/12= Amount to be debited to interest expense

every 6 months (effective method)

Face value × Market rate at issuance date × 6/12= Amount to be debited to interest expense

every 6 months (effective method)

Face value × Stated rate × 6/12 = Amount of interest to be paid in cash each 6 months.

Face value × Stated rate × 6/12 = Amount of interest to be paid in cash each 6 months.

Learning Unit 21-1

21 - 9

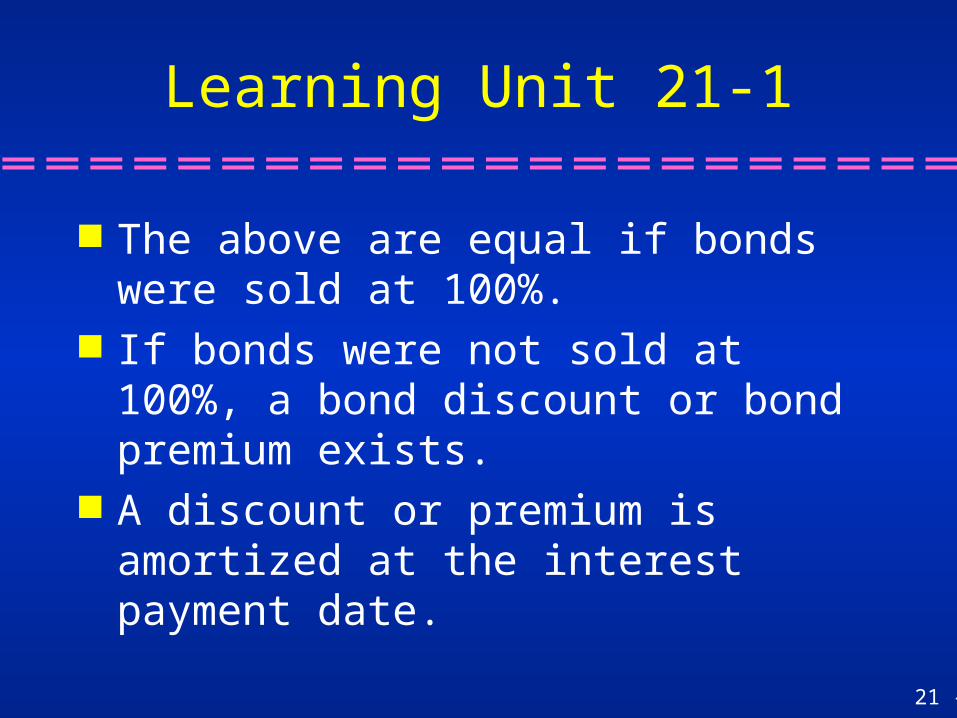

Learning Unit 21-1

The above are equal if bonds were sold at 100%.

If bonds were not sold at 100%, a bond discount or bond premium exists.

A discount or premium is amortized at the interest payment date.

21 - 10

Amortizing bond discountsand bond premiums by thestraight-line method and by

the interest method.Journalizing year-end

adjustingentries for bonds.

Learning Objectives 2 and 3

21 - 11

Straight-Line MethodStraight-Line Method

The discount (or premium) is divided by thenumber of interest periods for the bond issue

and provides the amount for amortization.

The discount (or premium) is divided by thenumber of interest periods for the bond issue

and provides the amount for amortization.

Learning Unit 21-2

21 - 12

Learning Unit 21-2

Amortization of a discount increases interest expense.

Amortization of a premium decreases interest expense.

21 - 13

Bonds with a face value of $200,000 are sold at 97%.The contract rate of interest is 12% (20 periods).The market rate is 12.4%.

Bonds with a face value of $200,000 are sold at 97%.The contract rate of interest is 12% (20 periods).The market rate is 12.4%.

Cash 194,000Discount onBonds Payable 6,000

Bonds Payable 200,000

Cash 194,000Discount onBonds Payable 6,000

Bonds Payable 200,000

Learning Unit 21-2

21 - 14

Learning Unit 21-2

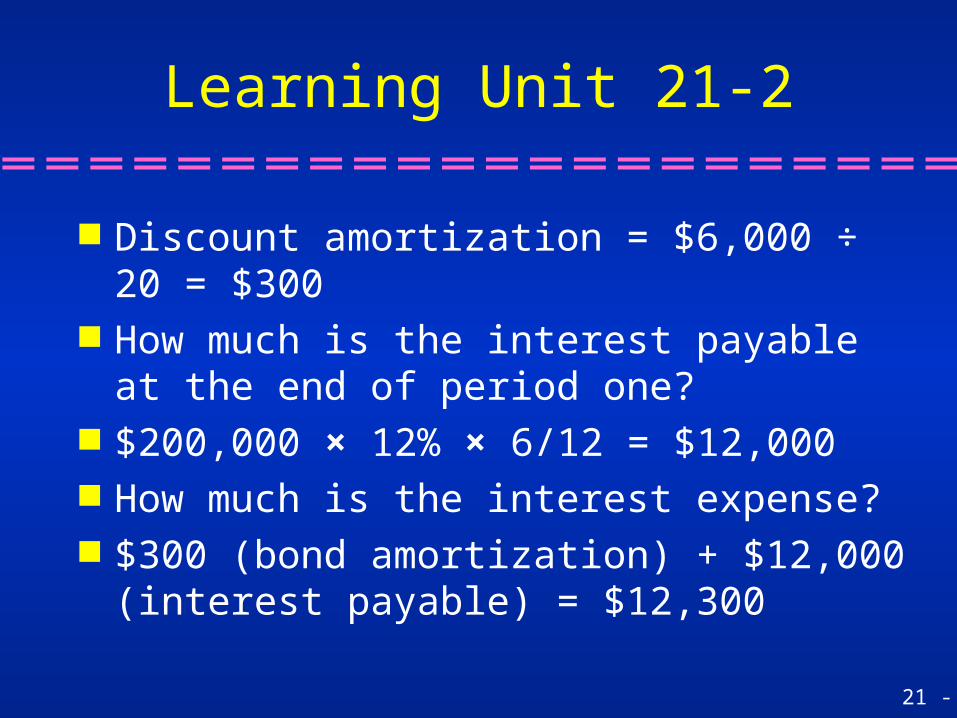

Discount amortization = $6,000 ÷ 20 = $300 How much is the interest payable at the end

of period one? $200,000 × 12% × 6/12 = $12,000 How much is the interest expense? $300 (bond amortization) + $12,000 (interest

payable) = $12,300

21 - 15

Bonds with a face value of $200,000are sold at 102%.The contract rate of interest is 12%.The market rate is 11.8%.

Bonds with a face value of $200,000are sold at 102%.The contract rate of interest is 12%.The market rate is 11.8%.

Cash 204,000Bonds Payable 200,000Premium on Bonds Payable 4,000

Cash 204,000Bonds Payable 200,000Premium on Bonds Payable 4,000

Learning Unit 21-2

21 - 16

Learning Unit 21-2

Cash payment is $12,000. 4,000/20 = 200 Premium amortization is $200. Interest expense is 12,000 – 200 = $11,800 What is the journal entry at the end of

period one?

21 - 17

Interest Expense 11,800Premium Bonds Payable(amortization) 200

Cash 12,000

Interest Expense 11,800Premium Bonds Payable(amortization) 200

Cash 12,000

Learning Unit 21-2

21 - 18

Interest MethodInterest Method

The interest method makes interest expense aconstant percentage of the bond carrying value.

The interest method makes interest expense aconstant percentage of the bond carrying value.

Learning Unit 21-3

21 - 19

Learning Unit 21-3

Face value × Stated rate × 6/12 = Amount of interest to be paid in cash each 6 months

Carrying value × Market rate at issuance date × 6/12 = Amount to be debited to Interest Expense every 6 months

The above are equal if bonds were sold at 100%.

21 - 20

Learning Unit 21-3

Assume that Yang Corporation is issuing $200,000 of 12%, ten-year bonds on April 1. Interest is to be paid on October 1 and April 1.

The selling price of the bonds is $178,808. The market rate is 14 %.

21 - 21

Learning Unit 21-3

What is the interest paid to bondholders at the end of period one?

$200,000 × 12% × 6/12 = $12,000

What is the interest expense? $178,808 × 14% × 6/12 = $12,517

What is the discount amortization? $517

21 - 22

Interest Expense 12,517Cash 12,000Discount on Bonds Payable(amortization) 517

Interest Expense 12,517Cash 12,000Discount on Bonds Payable(amortization) 517

Learning Unit 21-3

21 - 23

Interest Expense 6,276.50Discount on Bonds Payable 276.50

Bond interest payable 6,000.00

Interest Expense 6,276.50Discount on Bonds Payable 276.50

Bond interest payable 6,000.00

Learning Unit 21-3

Assume that on December 31, three months interest of $6,000 for the second period has accrued. What is the adjusting entry?

21 - 24

Journalizing entries related

to retirement of bonds and to sinking funds.

Learning Objective 4

21 - 25

Learning Unit 21-4

Bonds are a long-term liability. Liabilities are paid at maturity (or early). Amortization must be brought up to date and

interest paid to bondholders. Maturity value (face value of bonds) is paid. Some issues require a sinking fund in which

cash is set aside to repay the bonds at maturity date.

21 - 26

Learning Unit 21-4

Assume that on June 30, a corporation retired a $500,000, 10 % bond issue that had an unamortized premium of $19,000.

The bonds were called at 105. What is the journal entry?

21 - 27

Bonds Payable 500,000Premium on Bonds Payable 19,000Loss on Bond Retirement 6,000

Cash 525,000Retirement of bond

Bonds Payable 500,000Premium on Bonds Payable 19,000Loss on Bond Retirement 6,000

Cash 525,000Retirement of bond

Learning Unit 21-4

21 - 28

End of Chapter 21