2018 governmental gaap update€“if an aro is not recognized because it is not yet reasonably...

TRANSCRIPT

2018 Governmental GAAP Update

February 6, 2018

Webinar

Presented in association with

Presented by:

Stephen W. Blann, CPA, CGFM, CGMA

Director of Governmental Audit QualityRehmann

Session Outline

• Newly effective standards

• Newly issued standards

• Upcoming standards

• Exposure drafts and preliminary views

Newly Issued Standards

• GASB Pronouncements effective in 2017:No. Title Effective

80 Blending Requirements for Certain Component Units

06/15/2017

81 Irrevocable Split-Interest Agreements 12/15/2017

82 Pension Issues 06/15/2017

Newly Issued Standards

• GASB Pronouncements effective soon:No. Title Effective

83 Certain Asset Retirement Obligations 06/15/2019

Newly Issued Standards

• GASB Pronouncements issued in 2017:No. Title Effective

84 Fiduciary Activities 12/15/2019

85 Omnibus 2017 06/15/2018

86 Certain Debt Extinguishment Issues 06/15/2018

87 Leases 12/15/2020

Newly Issued Standards

• GASB Implementation Guides issued in 2017:No. Title Effective

2017-1 Implementation Guidance Update—2017 06/15/2018

2017-2 Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans

12/15/201706/15/2018

2017-3 Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions (and Certain Issues Related to OPEB Plan Reporting)

12/15/201706/15/201806/15/2019

GASB Statement 80

Blending Requirements for Certain CUs

• Effective 06/15/2017

• Adds a criteria for blending component units:

– Not-for-profit corporation

– Primary government is identified in the articles of incorporation or bylaws as the sole corporate member

– Does not apply to CUs included as supporting organizations under GASB 39

GASB Statement 81

Irrevocable Split-Interest Agreements

• Effective 12/31/2017

• Applies to irrevocable split-interest agreements:

– Held by the government

– Held by others for the benefit of the government

GASB Statement 81

Irrevocable Split-Interest Agreements

• Effective 12/31/2017

• Addresses accounting for donations (largely to foundations) of charitable remainder trusts, annuity gifts, and life interests in real estate

• Applies to split-interest agreements:

– Held by the government

– Held by others for the government’s benefit

GASB Statement 81

Irrevocable Split-Interest Agreements

• Split-interest agreement

– An agreement in which the donor enters into a trust or other legally enforceable agreement under which the donor transfers resources to an intermediary to administer for the benefit of at least two beneficiaries, one of which could be a government.

GASB Statement 81

Irrevocable Split-Interest Agreements

• Intermediary

– The trustee, fiscal agent, government, or any other legal or natural person that is holding and administering donated resources pursuant to a split-interest agreement. An intermediary is not required to be a third party.

GASB Statement 81

Irrevocable Split-Interest Agreements

• Lead interest

– A type of beneficial interest that confers the right to receive all or a portion of the benefits of resources during the term of a split-interest agreement

• Remainder interest

– A type of beneficial interest that confers the right to receive all or a portion of the resources remaining at the end of a split-interest agreement’s term

GASB Statement 81

Irrevocable Split-Interest Agreements

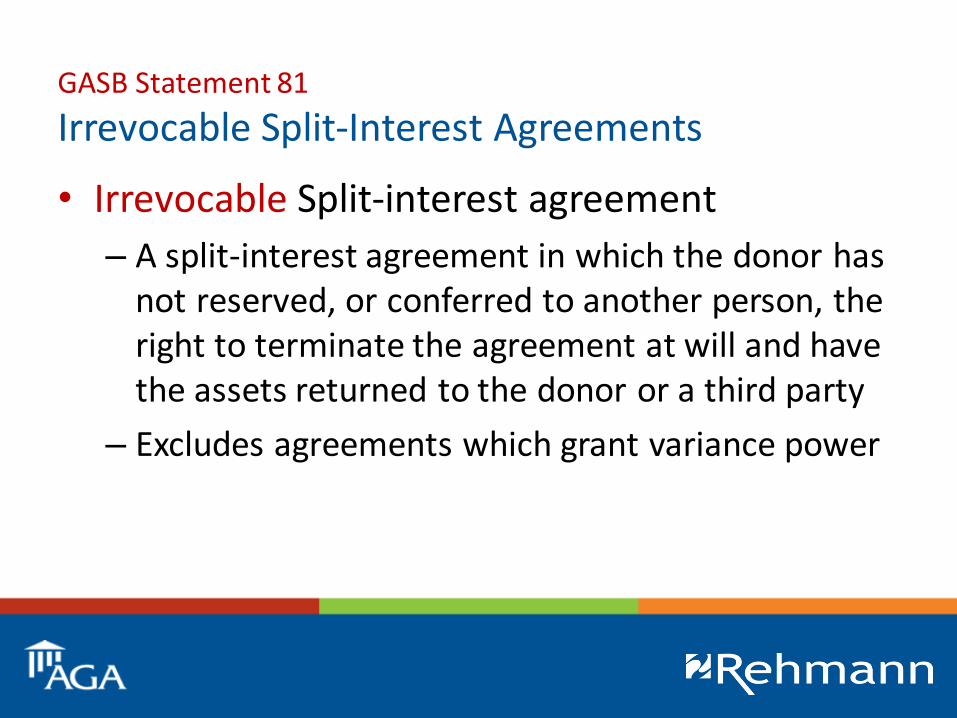

• Irrevocable Split-interest agreement

– A split-interest agreement in which the donor has not reserved, or conferred to another person, the right to terminate the agreement at will and have the assets returned to the donor or a third party

– Excludes agreements which grant variance power

GASB Statement 81

Irrevocable Split-Interest Agreements

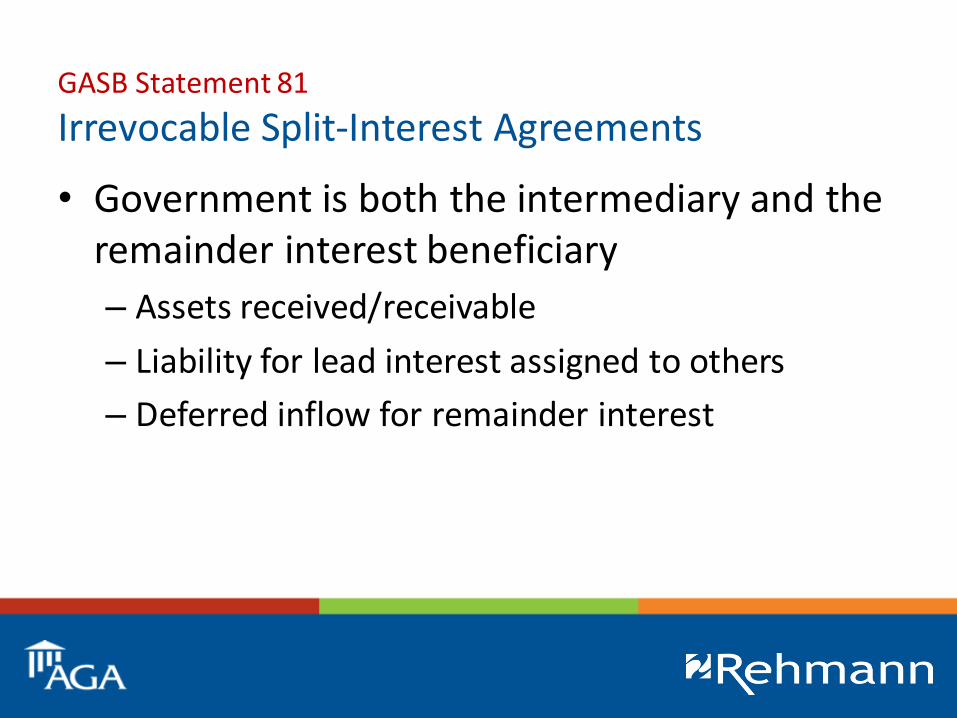

• Government is both the intermediary and the remainder interest beneficiary

– Assets received/receivable

– Liability for lead interest assigned to others

– Deferred inflow for remainder interest

GASB Statement 81

Irrevocable Split-Interest Agreements

• Government is both the intermediary and the lead interest beneficiary

– Assets received/receivable

– Deferred inflow for lead interest

– Liability for remainder interest assigned to others

GASB Statement 81

Irrevocable Split-Interest Agreements

• Life interest in real estate

– Donor provides asset (e.g., residence) but retains the right to use it until death

– Record an investment or capital assets based on intended future use

– Record liability for any obligations to sacrifice future resources (maintenance, etc.)

– Deferred inflow for the residual balance

GASB Statement 81

Irrevocable Split-Interest Agreements

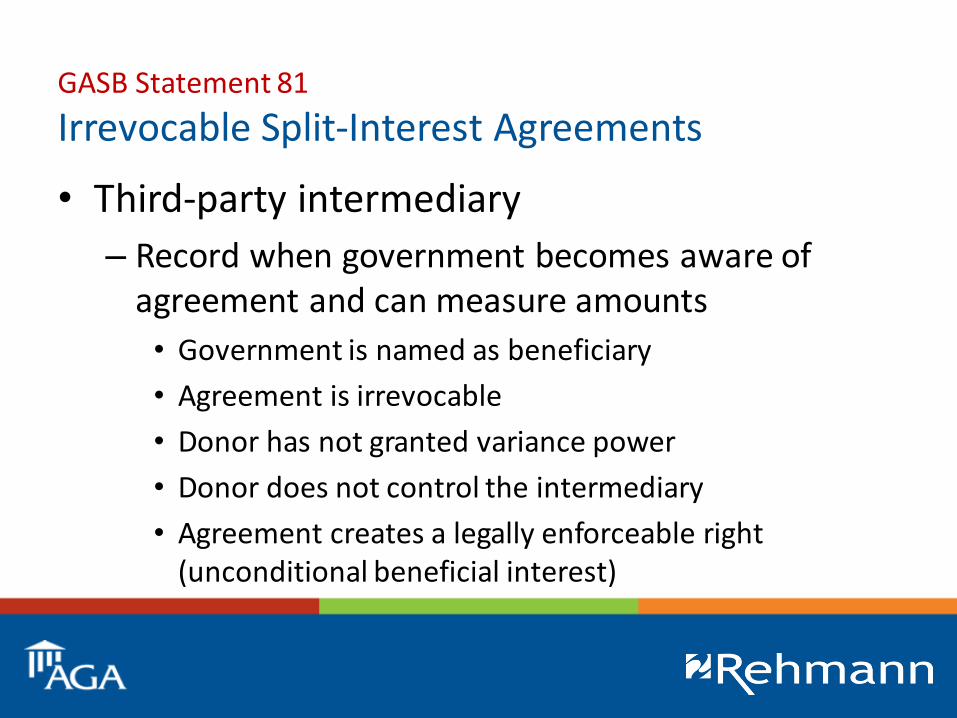

• Third-party intermediary

– Record when government becomes aware of agreement and can measure amounts

• Government is named as beneficiary

• Agreement is irrevocable

• Donor has not granted variance power

• Donor does not control the intermediary

• Agreement creates a legally enforceable right (unconditional beneficial interest)

GASB Statement 81

Irrevocable Split-Interest Agreements

• Third-party intermediary

– Record asset for beneficial interest

– Offset with a deferred inflow

– Recognize revenue:

• Lead interest = over term of agreement

• Remainder interest = at termination of agreement

CPE Prompt 1 of 4

• Governments that are the beneficiaries of charitable remainder gift annuities held be a third-party should record:

A. Receivables and revenue

B. Receivables and deferred inflows

C. Nothing

D. Either B or C depending on whether the third-party has variance power

GASB Statement 82

Pension Issues

• Effective 06/15/2017

• Q: What if the actuarial assumptions selected are reported as deviations by the actuary in accordance with Actuarial Standards of Practice?

– A: The valuation is not in conformance with GAAP

GASB Statement 82

Pension Issues

• Q: What is “covered payroll” for RSI?

– A: Pensionable wages (reported to the plan)

• Q: What if an employer “picks up” the required employee contribution?

– A: Treat it as an employee contribution

GASB Statement 83

Certain Asset Retirement Obligations

• Effective 06/15/2019

• Addresses legally enforceable liabilities associated with the retirement of a tangible capital asset

– Excludes landfills and pollution remediation

– Excludes routine costs of maintenance and sale

GASB Statement 83

Certain Asset Retirement Obligations

• Example AROs

– Decommissioning of nuclear reactors

– Removal and disposal of wind turbines in wind farms

– Dismantling and removal of sewage treatment plants

– Removal and disposal of x-ray machines

GASB Statement 83

Certain Asset Retirement Obligations

• Definition of an ARO

– Legally enforceable liability

– Associated with the retirement of a tangible capital asset

• Asset is permanently removed from service

• Includes sale, abandonment, recycling, or disposal

• Excludes temporary idle status

GASB Statement 83

Certain Asset Retirement Obligations

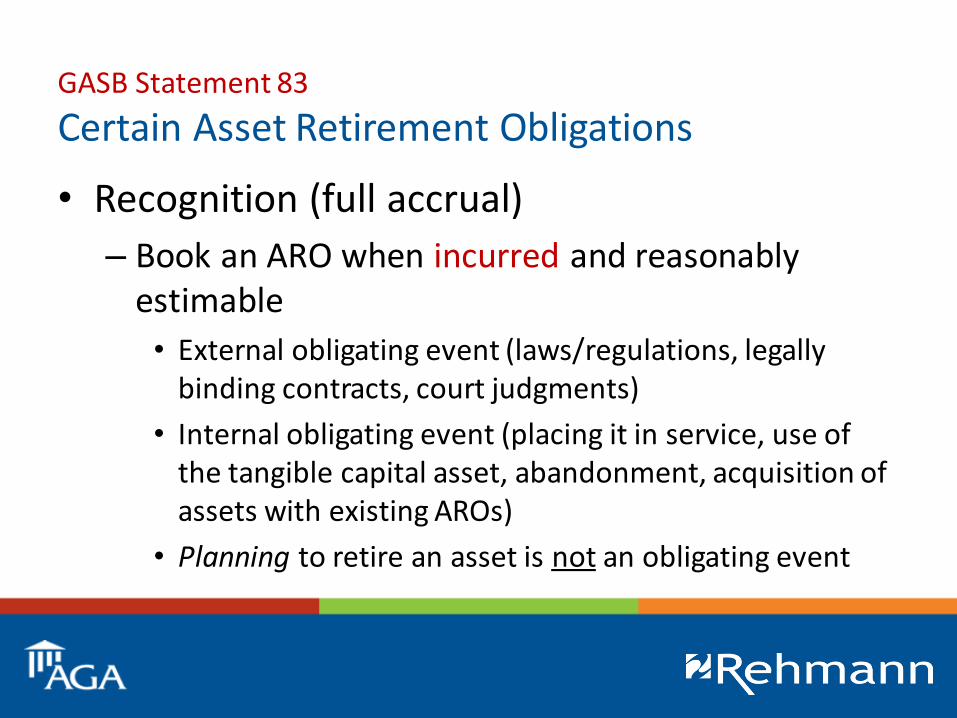

• Recognition (full accrual)

– Book an ARO when incurred and reasonably estimable

• External obligating event (laws/regulations, legally binding contracts, court judgments)

• Internal obligating event (placing it in service, use of the tangible capital asset, abandonment, acquisition of assets with existing AROs)

• Planning to retire an asset is not an obligating event

GASB Statement 83

Certain Asset Retirement Obligations

• Recognition (full accrual)

– Amount of liability = best estimate of the current value of outlays expected to be incurred

• Probability-weighted average of all potential outcomes

• Most likely outcome (if not cost effective to weight)

GASB Statement 83

Certain Asset Retirement Obligations

• Recognition (full accrual)

– Offset the ARO with a deferred outflow

– Amortize over asset’s useful life

– Exception: asset abandoned before being placed in service (expense all at once)

GASB Statement 83

Certain Asset Retirement Obligations

• Recognition (full accrual)

– Annually adjust estimates for inflation and other changes

• Assets still in service: adjust deferred outflows

• Retired assets: changes run through expense

GASB Statement 83

Certain Asset Retirement Obligations

• Recognition (modified accrual)

– Only record portion that is expected to be liquidated with expendable available financial resources (as they become due and payable)

GASB Statement 83

Certain Asset Retirement Obligations

• Disclosure

– General description of AROs and related assets

– Methods/assumptions used

– Remaining useful life

– Any restricted assets set aside for ARO

– If an ARO is not recognized because it is not yet reasonably estimable, still describe

CPE Prompt 2 of 4

• For which of the following might a government report an ARO?

A. Decommissioning a power plant

B. Landfill

C. Clean-up of an oil spill

D. All of the above

GASB Statement 84

Fiduciary Activities

• Summary

– Defines fiduciary activities and limits the use of fiduciary funds to accounting for them

– Redefines “control” in a fiduciary capacity

– Distinguishes between trust agreements and “custodial” funds (replaces “agency” funds)

GASB Statement 84

Fiduciary Activities

• Four paths to identifying fiduciary activities

1. Pension/OPEB plans that are component units

2. Other fiduciary component units

3. Other pension/OPEB plans (not CUs)

4. Other fiduciary activities

GASB Statement 84

Fiduciary Activities

• Pension/OPEB plans administered through trusts:

– Contributions are irrevocable

– Plan assets are dedicated to providing benefits

– Plan assets are legally protected from creditors

• Resources accumulated for pension/OPEB benefits for other governments not in a trust

1. Pension/OPEB plans that are component units

GASB Statement 84

Fiduciary Activities

• Component unit status will likely come down to board appointment

– Separate legal standing

– Financial burden (making contributions)

– Appointment of a voting majority of the pension/OPEB board

1. Pension/OPEB plans that are component units

GASB Statement 84

Fiduciary Activities

• Other component units are fiduciary activities if they have one of the following characteristics:

a. Assets are administered through a trust

– Government itself is not the beneficiary

– Assets are dedicated to providing benefits

– Assets are legally protected from creditors

2. Other fiduciary component units

GASB Statement 84

Fiduciary Activities

• Other component units are fiduciary activities if they have one of the following characteristics:

b. Assets are for the benefit of individuals

– Government does not have administrative or direct financial involvement with the assets

– Assets are not derived from the government’s provision of goods or services to those individuals

2. Other fiduciary component units

GASB Statement 84

Fiduciary Activities

• Other component units are fiduciary activities if they have one of the following characteristics:

c. Assets are for the benefit of organizations or other governments

– Beneficiary is not part of the reporting entity

– Assets are not derived from the government’s provision of goods or services to those organizations or other governments

2. Other fiduciary component units

GASB Statement 84

Fiduciary Activities

• If not a component unit, a pension/OPEB plan is a fiduciary activity if:

– Administered through a trust (or accumulated for pension/OPEB benefits of other governments); and

– The government controls the assets

• Holds the assets; or

• Has the ability to direct the use, exchange, or employment of the assets

3. Other pension/OPEB plans (not CUs)

GASB Statement 84

Fiduciary Activities

• All other activities are fiduciary activities if:

– The government controls the assets; and

– The assets are not derived from the government’s own-source revenues, government-mandated or voluntary non-exchange transactions; and

– The assets are either administered through a trust or held for individuals without any administrativeor direct financial involvement

4. Other fiduciary activities

GASB Statement 84

Fiduciary Activities

• Terms:

– Own-source revenues

• Generated by the government itself.

• Includes: charges for services, interest earnings, income taxes, property taxes, etc.

4. Other fiduciary activities

GASB Statement 84

Fiduciary Activities

• Terms:

– Administrative involvement

• Monitoring recipients for compliance

• Determining eligibility

• Exercising discretion in the allocation of funds

– Direct financial involvement

• Matching requirements

• Liable for disallowed costs

4. Other fiduciary activities

GASB Statement 84

Fiduciary Activities

• Reporting fiduciary activities in fiduciary funds

1. Pension (and other employee benefit) trust funds

2. Investment trust funds

3. Private-purpose trust funds

4. Custodial funds (replace agency)

GASB Statement 84

Fiduciary Activities

• Financial statements of fiduciary activities

– Statement of Fiduciary Net Position

– Statement of Changes in Fiduciary Net Position

GASB Statement 84

Fiduciary Activities

• Statement of Fiduciary Net Position

– Reports the assets, deferred outflows, liabilities, deferred inflows, and fiduciary net position of fiduciary funds

GASB Statement 84

Fiduciary Activities

• Statement of Fiduciary Net Position

– Pension (and other employee benefit) trust funds follow GASB 67/74

– All others, recognize liability to beneficiaries when an event has occurred that compels the government to disburse fiduciary resources

• A demand for the resources has been made; or

• No further action, approval, or condition is required to be taken or met by the beneficiary to release the assets

GASB Statement 84

Fiduciary Activities

• Statement of Changes in Fiduciary Net Position

– Reports additions to and deductions from fiduciary funds

– Disaggregate and present by source:

• Investment earnings

• Investment costs (fees)

• Net investment earnings

GASB Statement 84

Fiduciary Activities

• Statement of Changes in Fiduciary Net Position

– Custodial funds may report a single aggregated amount for additions and a single aggregated amount for deductions if typically held for three months or less

• Property taxes collected for other governments

• Property taxes distributed to other governments

GASB Statement 84

Fiduciary Activities

• GASB’s flowcharts

GASB Statement 84

Fiduciary Activities

• GASB’s flowcharts

– Many transactions previously reported in fiduciary funds may end up in governmental/proprietary funds

– They may still be liabilities… but they may not be fiduciary activities, and therefore both the assets and liabilities should appear on the government-wide financial statements

GASB Statement 84

Fiduciary Activities

• Practical implications (Michigan examples)

– Tax collection funds

– Deferred compensation plans

– Bail bonds

– Escrow funds

– Resources held for component units

– MERS Retiree Health Funding Vehicle

GASB Statement 84

Fiduciary Activities

• Next steps

– This standard is still very new

– There is still a lot of time between now and FYE 12/15/2019

– We will continue to analyze the standard and provide guidance

– Expect more training at future events!

CPE Prompt 3 of 4

• Under GASB 84, which of the following could not be accounted for in a custodial fund:

A. Taxes collected for other governments

B. A pass-through grant with no administrative involvement

C. Performance bonds assessed by the government

D. Assets of a pension or OPEB plan held on behalf of another government

GASB Statement 85

Omnibus 2017

• Summary

– Series of unrelated technical corrections

– Effective 06/15/2018, but may be early implemented individually

GASB Statement 85

Omnibus 2017

• Blending component units

– Business-type activities using a single column should still apply the blending criteria of GASB 14

• Goodwill

– Legacy goodwill (from pre-GASB 69) should be amortized over time

– Negative goodwill is not permitted

GASB Statement 85

Omnibus 2017

• Fair value measurement and application

– Each unit of account of real estate held by insurance entities should be classified as investments or capital assets following GASB 72

– Money market accounts and participating interest-earning investment contracts may (not must) be carried at amortized cost instead of fair value

GASB Statement 85

Omnibus 2017

• Pensions/OPEB

– Governmental funds should record liabilities as of the FYE, regardless of the measurement date

– Employer payments made on behalf of employees are still considered employer contributions

– OPEB RSI should be based on covered payroll (if used as the basis) or covered-employee payroll (if not used as the basis)

GASB 86

Certain Debt Extinguishments

• Summary

– Addresses how to handle the in-substance defeasance of debt using only existing resources (not issuing refunding bonds)

– Payments to escrow agent should be reported as debt service expenditures

– Effective 06/15/2018

GASB 87

Leases

• Summary

– Addresses contracts that convey a legal right to use a nonfinancial asset for a period of time in an exchange or exchange-like transaction

– Differs from FASB project

– Excludes leases of intangible assets (software)

– Effective 12/15/2020

GASB 87

Existing GAAP for Leases

• GASB Codification Section L20 - Leases

– NCGA Statement 5, Accounting and Financial Reporting Principles for Lease Agreements of State and Local Governments

– GASB Statement 13, Accounting for Operating Leases with Scheduled Rent Increases

– GASB Statement 62, Codification of Accounting and Financial Reporting Guidance Contained in Pre-November 30, 1989 FASB and AICPA Pronouncements

GASB 87

Existing GAAP for Leases

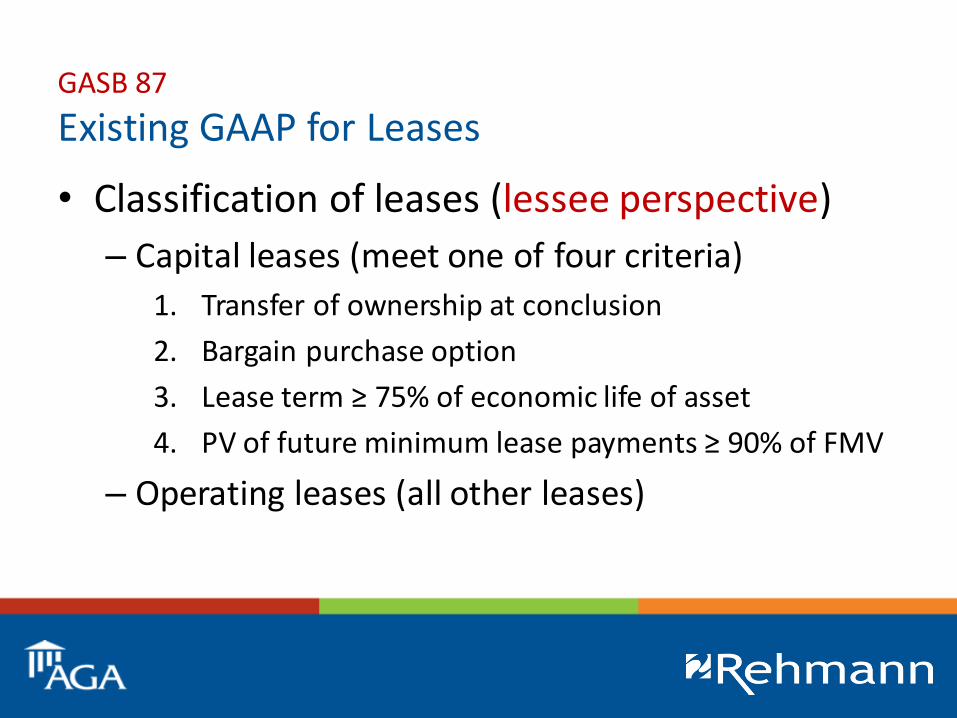

• Classification of leases (lessee perspective)

– Capital leases (meet one of four criteria)

1. Transfer of ownership at conclusion

2. Bargain purchase option

3. Lease term ≥ 75% of economic life of asset

4. PV of future minimum lease payments ≥ 90% of FMV

– Operating leases (all other leases)

GASB 87

Existing GAAP for Leases

• Classification of leases (lessor perspective)

– Sales-type leases

– Direct financing leases

– Leveraged leases

– Operating leases

GASB 87

Existing GAAP for Leases

• Accounting for leases (lessee perspective)

– Capital leases

• Debit capital assets and credit long-term debt for PV

• Disclose future minimum payments

– Operating leases

• Expense payments as made *

• Disclose future minimum payments (if non-cancelable)

GASB 87

GASB’s Lease Project Overview

• 2011 – added to research agenda

• 2013 – added to current agenda

• 2014 – preliminary views issued

• 2015 – field test / public hearings

• 2016 – exposure draft issued / public hearing

• 2017 – final standard issued in June

GASB 87

Leases

• Key provisions

– Single model for lease accounting

– Foundational principle: leases are financings of the right to use an underlying asset

– Lessees recognize a lease liability and an intangible right-to-use lease asset

– Lessors recognize a lease receivable and a deferred inflow of resources

GASB 87

Leases

• Lease

– Includes contracts not explicitly defined as “leases” but that otherwise meet the definition

– Excludes contracts for services (except those contracts that contain both a lease component and a service component)

GASB 87

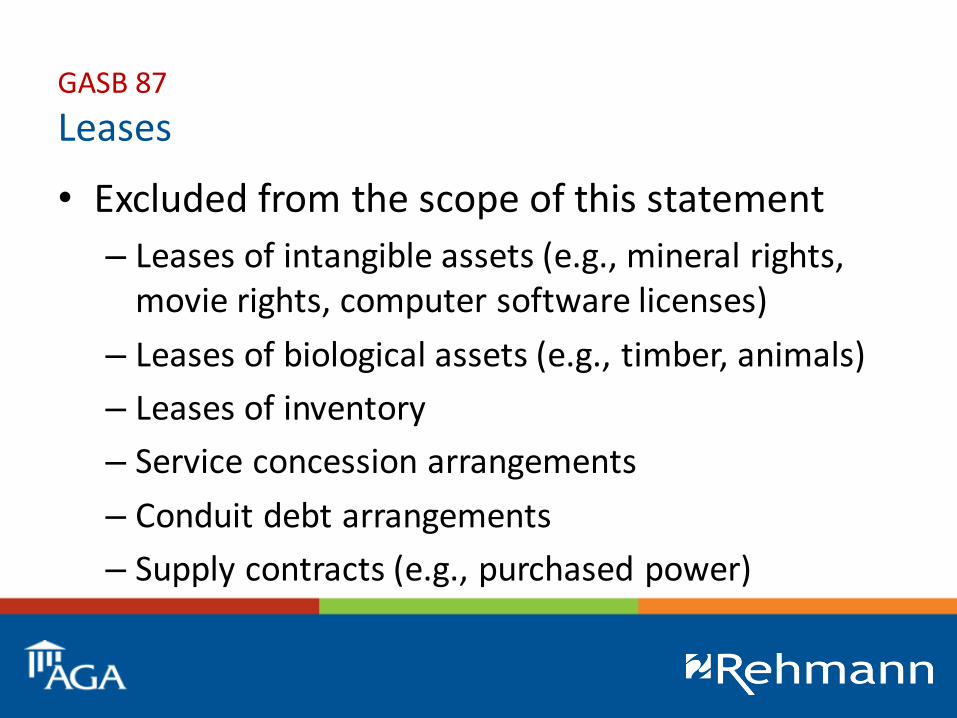

Leases

• Excluded from the scope of this statement

– Leases of intangible assets (e.g., mineral rights, movie rights, computer software licenses)

– Leases of biological assets (e.g., timber, animals)

– Leases of inventory

– Service concession arrangements

– Conduit debt arrangements

– Supply contracts (e.g., purchased power)

GASB 87

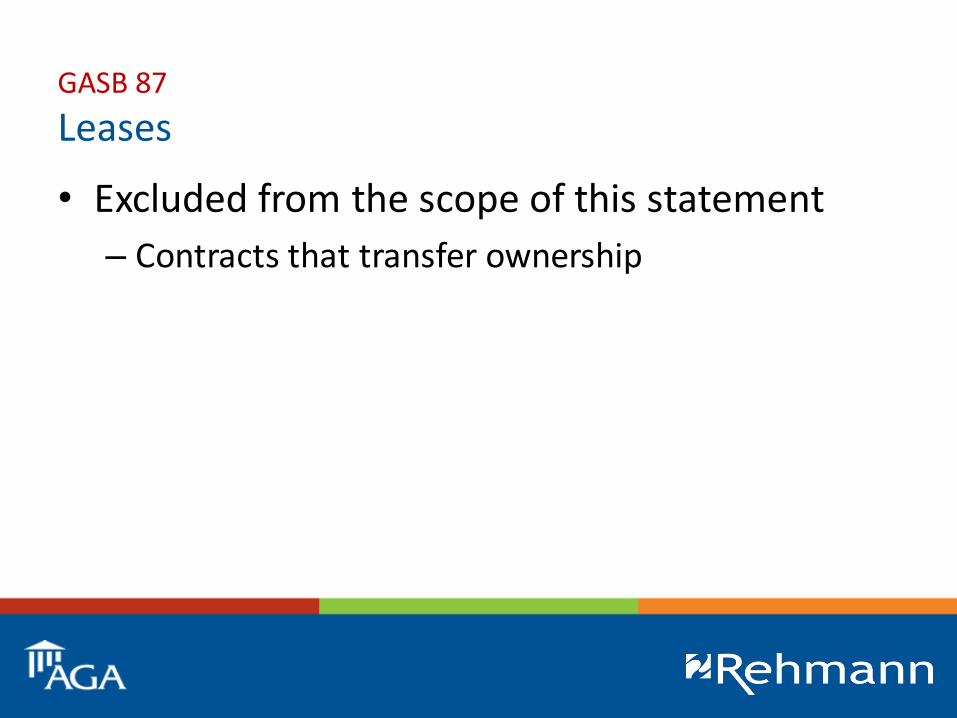

Leases

• Excluded from the scope of this statement

– Contracts that transfer ownership

GASB 87

Leases

• Lease term

– Noncancelable period + reasonably certain extension periods

• Lessees: Amortize (depreciate) lease asset

• Lessors: Recognize deferred inflow

– Rolling month-to-month leases generally considered short-term and excluded

GASB 87

Leases

• Bottom line:

– Largely balance sheet focused (asset = liability)

– Little budgetary impact (except former operating leases now = C/O and OFS when initiated)

– Apply materiality (capitalization threshold) to both asset and liability

GASB 87

Leases

• Contracts with multiple components

– Contracts may include:

• Both a lease and a non-lease component

• Multiple underlying assets

– Treat as separate contracts (use professional judgment to estimate amounts)

• If not practical to separate components, may treat as a single lease unit

GASB 87

Leases

• Lease terminations (lessee)

– Reduce carrying values of lease asset and lease liability (recognize gain/loss, if any)

– If terminated by purchasing the asset, transfer value of the lease asset to capital assets, and increase by reduction in lease liability

GASB 87

Leases

• Lease terminations (lessor)

– Reduce carrying values of lease receivable and deferred inflow (recognize gain/loss, if any)

– If terminated by selling the asset, derecognize the asset and include in the calculation of any gain/loss

GASB 87

Leases

• Subleases

– Treat initial lease and sublease as separate transactions

– Apply lessee and lessor guidance, as appropriate

GASB 87

Leases

• Sale-leaseback transactions

– Treat as two separate transactions

– Any difference between the carrying value of the sold asset and the proceeds from sale should be deferred and amortized over the lease term

– Disclose the terms/conditions

GASB 87

Leases

• Lease-leaseback transactions

– Treat as a net lease transaction

GASB 87

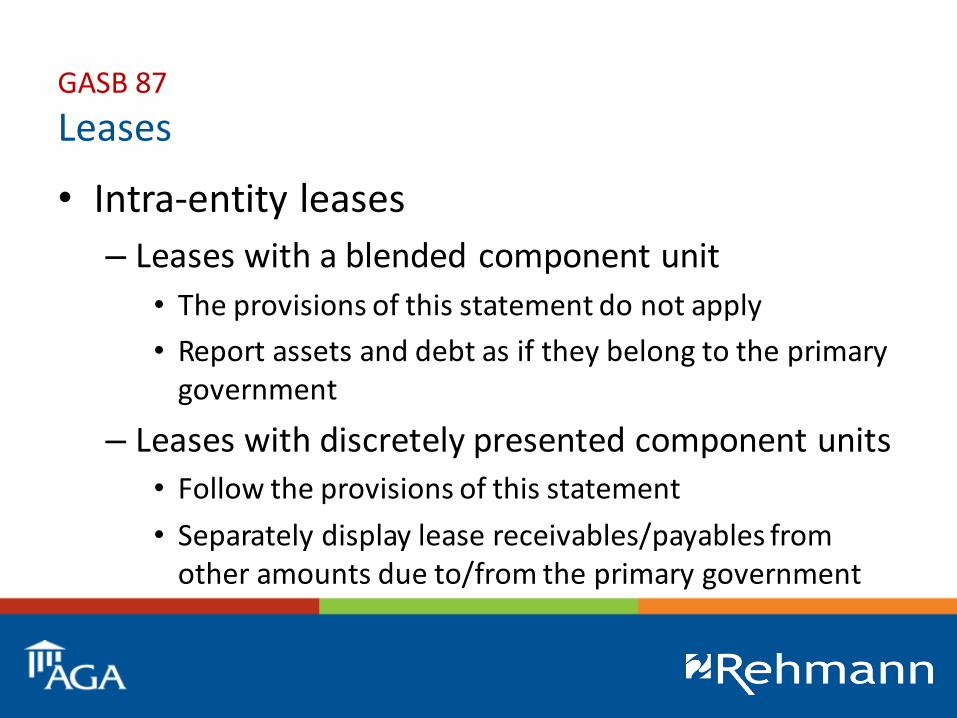

Leases

• Intra-entity leases

– Leases with a blended component unit

• The provisions of this statement do not apply

• Report assets and debt as if they belong to the primary government

– Leases with discretely presented component units

• Follow the provisions of this statement

• Separately display lease receivables/payables from other amounts due to/from the primary government

GASB 87

Example: Garbage Truck (Proprietary)

• Determine total payment amount and lease term

– $300,000 over 5 years

• Calculate present value

– $275,000 principal, $25,000 interest

• Calculation at inception

Capital asset (leased equipment) 275,000

Long-term liability (lease payable) 275,000

GASB 87

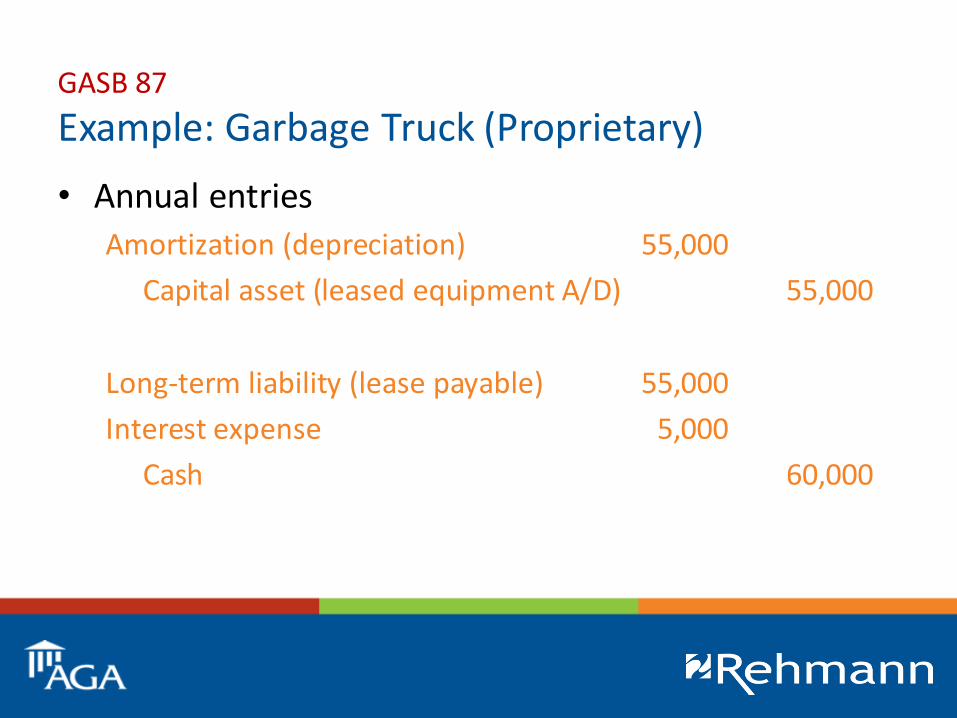

Example: Garbage Truck (Proprietary)

• Annual entries

Amortization (depreciation) 55,000

Capital asset (leased equipment A/D) 55,000

Long-term liability (lease payable) 55,000

Interest expense 5,000

Cash 60,000

GASB 87

Example: Fire Truck (Governmental)

• Determine total payment amount and lease term

– $350,000 over 5 years

• Calculate present value

– $325,000 principal, $25,000 interest

• Calculation at inception

Capital outlay 325,000

Other financing source 325,000

GASB 87

Example: Fire Truck (Governmental)

• Annual entry

Debt service - principal 65,000

Debt service - interest 5,000

Cash 70,000

GASB 87

Example: Copiers/Computer Equipment

• Review/update your capitalization threshold policy

• Determine if this is an area that you would normally capitalize

– If yes, follow previous examples

– If no, expense annually

GASB 87

Example: Land and Buildings

• Land

– No depreciation if purchase option is expected to be exercised; otherwise depreciate over lease term

• Buildings

– Asset capitalized should only reflect that portion of the building’s useful life that you will be leasing

– Depending on the length of the lease, the depreciable life may be significantly less than the true useful life of the underlying asset

CPE Prompt 4 of 4

• Under GASB 87, a lessee should record:

A. An intangible lease asset and a lease liability

B. An intangible lease asset and a lease expense

C. A deferred outflow and a lease liability

D. A deferred inflow and a lease liability

GASB Implementation Guide 2017-1

Implementation Guidance Update—2017

• Annual update of questions and answers

• Now Level B GAAP

– 41 new Q&A (mostly pension-related)

– 33 amended Q&A (technical clarifications)

GASB Implementation Guide 2017-2

Financial Reporting for OPEB Plans

• Initial Q&A guide for OPEB (plans)

– 160 “new” questions

– Largely patterned after the existing pension Q&A for plans

GASB Implementation Guide 2017-3

Accounting and Financial Reporting for OPEB

• Initial Q&A guide for OPEB (employers)

– 502 “new” questions

– Largely patterned after the existing pension Q&A for employers

Upcoming Standards

• GASB Pronouncements expected in 2018:

– Debt Disclosures, including Direct Borrowing (1Q18)

– Capitalization of Interest Cost (2Q18)

– Implementation Guidance – Update (2Q18)

– Equity Interest Ownership Issues (3Q18)

Looking Further Ahead

• Other GASB projects:

– Revenue and Expense Recognition (ITC 1Q18)

– Conduit Debt (ED 3Q18)

– Conceptual Framework: Recognition (PV 3Q18)

– Financial Reporting Model (PV 3Q18)

Looking Further Ahead

• Financial Reporting Model:– GASB 34 will be over 20 years old before this

project is complete (1Q22)

– Retaining government-wide and fund financial statements with minor changes

– Considering revisions to existing modified accrual:• Near-term resources

• Current resources

• Long-term resources

Questions?

For more information...

Stephen W. Blann, CPA, CGFM, CGMA

Director of Governmental Audit [email protected]/government